Don't wanna be here? Send us removal request.

Statistics

We looked inside some of the posts by novopaybanking and here's what we found interesting.

Average Info

Notes Per Post

1

Likes Per Post

1

Reblog Per Post

0

Reply Per Post

0

Time Between Posts

10 days

Number of Posts By Type

Text

6

Last Seen Tumblr Blogs

Fun Fact

In 2020, Tumblr had 29.4 million users in the US.

Text

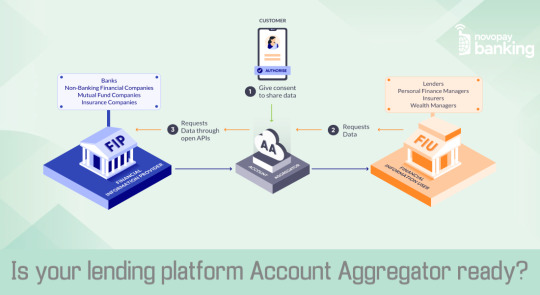

Is your lending platform Account Aggregator ready?

Account Aggregators are here to transform the digital lending sector as they bring absolute control for borrowers along with great convenience for lenders making it a win-win for both. Regulated and mandated by RBI, the Account Aggregation framework can be best defined as a platform collecting user’s personal financial data from Financial Information Providers (FIP) with consent and sharing it with the Financial Information Users (FIU) such as lenders making the process much faster while ensuring data is secured.

What does this mean for a User?

User-Controlled Data Sharing:

AA framework gives the users control of their data like nothing ever has. Known as an interoperable data-blind consent manager, this platform cannot read, use or sell consumer data which is encrypted by the user with digital signatures. The AA simply collects data and transfers it to FIUs who can decrypt and use the data as consented for. It equips the user to share data selectively, for a stipulated duration of time, and even withdraw the data once shared; giving the user complete visibility of when and where the data is being shared.

Simplifying Wealth Management:

Calling the AA system as your one-stop solution for managing multifarious financial assets and transactions wouldn’t be wrong. The user may consolidate all financial data across various applications to create a single touch-point through an account aggregator empowering the user in more ways than one. Along with the ease of sharing data with the service provider, the user gets a wholesome look at the portfolio and is able to closely monitor expenditure thus making wealth management simpler, faster and more secure. Consolidated data showing cash inflows through various sources can also help enhance a user’s credit scoring and underwriting.

Accelerating Lending Operations:

A consolidated system will eventually improve the efficiency of every financial operation. Registering on an AA platform via a financial entity eliminates a lot of time-consuming processes like queuing outside the bank, KYC, stamping documents et al. The lending agency can now quickly pull out borrowers’ accurate financial history, follow due diligence digitally and expedite the lending process.

Data on Fingertips:

The best part about getting on the AA framework? Consent, data-tracking, or connecting to the agency of your choice can now be managed through a simple app on the phone! Finally, feel in control? Yes, you are.

Read More: https://www.novopaybanking.com/blog/is-your-lending-platform-account-aggregator-ready

#digital lending#dasta sharing#data security#account aggregator#digital distribution solution#kyc for banking#retailers provide banking solutions#saas solutions#aeps

0 notes

Text

Most Useful Digitalizing Your SME Loan Process

Covid19 has contributed to the digitalization of the SME loan process as people have often started using their smartphones. Apart from SME lending, other lendings and financial transactions have increased worldwide as digital technologies have made the lending process more fun and simplified. Hence, banking and finance firms are looking for various solutions to digitalize their operations.

Banking and non-banking finance companies require digital assistance to overcome competition and defend their position in the market. The market of digital lending platforms in India will be $732 million in 2022. It indicates a notable growth in demand for digital lending services and associated businesses.

What is SME Loan Digitalization?

Small and medium enterprises (SMEs) need a little investment before starting their business. So, they approach various online/digital lending services these days. SME loanis also a part of such services. Banks or finance companies can cater to their customers by digitalizing these loans more effectively. It saves a lot of time processing loan applications for multiple customers through digital platforms like Novopay, Lendingkart, Navi, KreditBee, etc.

People can get easy loans through their mobile phones nowadays. They don't need to visit a financial institution or bank as such. Earlier, the processing time of SME Lending usually took 4 to 5 weeks. Digital platforms let it complete within a few minutes.

Digital Lending platforms are also helping renowned banking and financial firms reach out to their customers and do regular transactions effectively. Let's recall the leading advantages of the digitalization of SME loans!

Read More: https://www.novopaybanking.com/blog/advantages-of-digitalizing-sme-loan-process

#SME Loan#SME Lending#Digital Lending#small and medium enterprises#digital distribution solution#kyc for banking#saas solutions#retailers provide banking solutions

0 notes

Text

Improving productivity using Field Service Management

For many organizations, managing a team of sales/service professionals effectively is one of the most complex tasks. Because this involves the activities to be logged, monitored, and controlled by human labor which takes a considerable amount of time and precision to keep track of all the activities. Miscommunications, delays, and incorrect/incomplete information inevitably has plagued many companies in these situations.

As the technology has advanced with systems beginning to communicate easily, the next step was to devise a solution to solve the problem and thus gave way for Field Service Management System.

What is FSM – Field Service Management

FSM or Field Service Management is a technology that automates the field operations of a team of sales or service professionals through mobile systems. As customer demands and the logistics of managing field teams continue to increase in complexity, it is clear that business leaders — as well as employees, shareholders, and customers — are discovering the enormous efficiency gains and value that FSM software can bring to their organization as a whole.

FSM Systems: The Next Step of Ubiquitous Connectivity

At its core, FSM is simply any system that is designed to keep track of the various components of field operations. These components typically include employee/vehicle tracking, task scheduling, setting field force targets, performance measurement, incentive management and more. A typical FSM is a software-as-a-service sector (SaaS) offering, with management of these components controlled through a cloud-based WebApp which can be accessed from mobile devices while field technicians are on the job. Everything from tracking a customer acquisition, KYC or support call to empowering customers can be managed and tracked using a sophisticated FSM solution.

Voyager – Novopay’s FSM tool

Novopay’s Field Service Management tool Voyager helps monitor, analyse and improve the overall performance of the entire field force of a company. Often, companies have a large field force engaged in customer acquisition, sales or support. However, companies are unable to accurately measure the effectiveness or productivity of their workforce in the field. This is where Voyager comes in.

Voyager’s mobile app deployed on field force’s smartphones, uses various sensors and client-generated events to track the progress of the field force and informs the Voyager server of their various activities. Voyager dashboard displays the status of active tasks, attendance monitoring, real-time Tasks monitoring, geo-tracking of field force, business expenses management including reimbursements and incentive management and distribution.

#KYC for Banking#Saas solutions#Digital Distribution solution#Retailers provide Banking solutions#DMT#AePS#MicroATMs#CMS

0 notes

Text

How Technology is Revolutionizing Payments Processing

Money makes the world go round they say – but none of that would matter if the money itself couldn’t get around. That is usually the biggest issue with handling payments in the past: restrictions to how money can be paid, and where it can get to in the world.

Then, technology made an appearance.

Today, online payment processing services are as breezy as things could get. Constant technological evolution is making it such as there is now special attention to making instant payments to anywhere in the world as opposed to the existing traditional models.

Here, we examine the transformation of payments systems through technology.

4 Ways Technology is Revolutionizing Payments System

It is no news that technology is transforming the way nearly everything is done. Today, financial transactions have also undergone a fundamental change.

The opportunities offered by the advent of digital innovations to the traditional financial scene have helped institutions to project more comprehensive payments capabilities for better customer experiences.

So, we go through some of the ways technology is advancing the payments scene:

1. Leveraging Big Data for Improved Customer Engagement

Data management can make payments systems more efficient and tailored to meet up with customers’ needs by giving insights into trends and customers’ behavior.

The vital intervention of ‘big data’ in the financial scene has given payment systems the leverage to provide value-added services through optimized data-based understanding.

By providing means for effective interpretation and analysis of complex volumes of data, companies are able to optimize their decision-making process to empower improved customer engagement.

Today, AI and ML-enabled payments systems are able to provide highly scalable models of operations for better customer satisfaction. For instance, merchants might need a guide on payment gateways for the choice of a system to accommodate the needs of cross-border clients.

Thus, by analysis of clients’ data such as geo-locations and languages, merchants are able to provide means of faster and secured online transactions processing and better consumer relations. If you are interested in exploring options, you can check out a payment processors list.

2. The Advent of Digital Currencies for Globalization

Insights from the Global Findex Database provided by the World Bank on the reach of financial services explains that while more than two-thirds of the world’s total adult population has access to banking accounts, about 1.7 billion remain unbanked.

However, two-thirds of the population were reported to have access to mobile devices – highlighting the importance of an electronic payment system in extending the circulation of payments options to populations all across the globe.

The advent of digital currencies brought by the largest payment processing companies sought to open the door of mobile and digital systems to various sections of the world including the unbanked sector while bringing about globalization in various sectors.

Despite the lack of a global consensus on the use of digital currencies, these currencies have been found to revolutionize the payments scene by providing a well-developed online payment system tailored to counter the barriers of locations, cultural nuances, and literacy amongst populations.

Digital currencies were developed to proffer solutions to scalability issues found in traditional payment systems and bring about transparency in transactions. Here, transactions are optimized to be validated and secured within hours instead of days.

3. Decentralization and Security in Transactions with Blockchain Technology

As technology rapidly evolves, traditional financial systems have had to combat the rise in cyber threats. These days, cyber risks are taking more sophisticated forms, highlighting the need for more advanced ways to provide consumers with security and transparency in their transactions.

Statistically, cybercrime costs accelerated globally by 27% with the financial services industry taking in the highest cost at over $18 million per surveyed company. Predictably, cybercrime-related damage cost will hit $6 trillion by 2021 which provides strong evidence of an increasing need for a system that handles volumes of sensitive information effectively.

In this regard, the advent of Blockchain technology to payment systems is revolutionizing existing models by providing transparency and a strong security framework through its immutable background.

Also, one of the key advantages of electronic payment systems backed up by Blockchain is the power of scalability. Payment gateway systems in this variation are now equipped to handle faster and cheaper cross-border payments and remittances through automation and transparency.

4. Mobile Wallets

Within the last couple of years, smartphones have a regular facet of consumer activities globally and they are now significantly transforming the payment processing industry. Today, mobile “one-click” apps like WeChat and Alipay are taking the place of traditional payments models.

Studies on mobile payments growth by Sharespost indicate a steady rise in mobile transactions at more than 52% and an estimated global transaction value of about $379 million.

Stuck with a fragmented tech-enabled framework, the digital revolution is helping to consolidate these solutions to help companies project cash-less and card-less solutions to consumers for advancements into adjacent markets.

As such, various companies and players in the global industrial sector are partnering with mobile wallet services to enable data-driven apps equipped with commerce capabilities for their consumers. In return, mobile transactions via an online payment gateway are on the rise and projected with an estimated global transaction value of about $865 million by 2021.

Technology is Reshaping Traditional Financial Systems

Over the next few years, technology is poised to bring more change into payments systems, countering boundaries to better investments and finance opportunities.

With the trend in the adoption of digital innovations, it is expected that future purchasing decisions will be powered by more advanced payments mechanisms. Thus, employing the power wielded by technology is set to give companies the leverage to compete and advance.

#KYC for Banking#Saas solutions#Digital Distribution solution#Retailers provide Banking solutions#DMT#AePS#MicroATMs#CMS

0 notes

Text

How Digital Lending can help you transform your organization

Digital lending is revolutionizing lending processes and offers too many competitive advantages for lenders to ignore. Innovation in digital lending is enabling lenders to offer better products to their customers faster, more cost-efficient and in an engaging way. In the Amazon era where customers expect service with fast turnaround and efficient services, traditional lenders have no choice but to adopt digital strategies to remain relevant and competitive.

Although integrating digital lending practices into the lending process is challenging, ignoring digital lending process is detrimental. If done correctly, it will help lenders evolve, scale and be competitive in the marketplace. Customer expectations are changing rapidly, shaped by use of smartphones, social media and ecommerce. Lenders develop their own digital lending capability or partner with other organizations or a combination thereof.

While the ‘correct’ mix of digitisation might vary, adopting a digital lending process offers several key advantages – lower operating costs, faster turnaround times, improved understanding of customer behaviour, lower delinquency rates, and enhanced customer engagement.

What is digital lending?

The lending process broadly refers to a sequence of activities to be performed to provide a loan. From acquiring customers, onboarding, assessing credit, disbursement of loan to receiving repayments and managing collections form core steps of a lending process. Digital lending refers to managing the entire lending process by using the right technology to enhance customer satisfaction.

Key Pillars of Digital lending

Digital lending can mean many different things to different lenders based on their perspective of their customers and market. However most digital lending processes incorporate the following 3 key pillars

Use of digital Channels: Efficient digital channel enables customers to engage with the lender easily, wherever and whenever they want. Digital lenders use digital channels to reach new and existing customers to enable them to apply for credit, receive loan disbursements, access information about their accounts and enable multi mode payments.

Consume diverse data: Digital lenders depend on diverse data sets to evaluate their customers. Bank payments, bill payment history, invoices, credit bureau etc to assess credit worthiness. Customer data is also leveraged to enhance engagement.

Focus on customer experience: One of the most deterrent process of traditional lending is onboarding. Filling the several forms consumes time, is expensive and many times might lead to customers losing interest. Use of digital onboarding, video KYC and India stack reduces onboarding time to minutes resulting in increase in consumer experience.

How to enable digital lending

Organizations need to go through an evolution to embrace digital lending fully. Early stage adopters start with transforming the customer acquisition process. Shifting from paper based onboarding to app based onboarding.

In the case of ‘touch and tech’ process, the loan agents are equipped with applications to enable digital onboarding. Use of digital KYC mechanisms such as video KYC and India Stack for KYC is a common practice. However many of the backend process are still managed in the traditional sense. Implementing a robust Loan Origination System ( LOS) is key at this stage. A fully-integrated LOS will offer lenders both offline and digital processes and streamline the lending process.

Organizations who push forward in their transformation journey will enhance their customer engagement by enabling their customers to manage the majority of the account functionality. Implementation of a robust digital-ready lending management system ( LMS) offers customers to completely digitize management of their loan book. An LMS enables a data driven approach to managing delinquencies, analytics and enhanced collection management. A robust collection management system enhances collection ratios. A digital-ready LMS enables a lender to keep real-time track of the entire lending book.

Ability to assess credit is the cornerstone for digital lending. Lenders need to transform from the current rule based credit engine to credit scorecard system. In order to move to digital credit assessment, lenders need to organise existing data about their customers and identify new data points to collect. Using the existing credit history, lenders need to develop an intermediate credit scorecard approach before moving to a fully automated / AI & ML based system.

How do you start?

Given the vast scope of digital lending, it can be difficult for lenders to know where to start and how do you start on this journey. Firstly lenders need to assess and build your readiness. Least risky mechanism is to first transform your onboarding process. Adopting digital form filling, KYC and India stack for simplifying customer onboarding journeys.

Next is to identify product and market segments that can be completely managed via digital lending. There is no need to incur capital expenditure for digital lending. There are SaaS based technology providers such as Novopay who offer you an entire digital lending suite on a pay-as-you-go model. More importantly, it is the organizational change that is required to embrace digital technology for the lending process.

A particular product / market segment is fully functional on a digital platform, it is important to define metrics for measurement of success factors. Based on the metrics you need to define success criterias for extending the digital lending ecosystem for all your products. Such a process carries lesser risk in terms of disruption of your existing business and significantly less capital expenditure for technology. Technology landscape is moving very fast. Identifying what is next for digital lending is a moot exercise. However on-the-ground implementation of digital lending is imperative for growth. Implementing a digital lending ecosystem is challenging. We have outlined some common pitfalls and simple but effective methods for lenders embarking on this journey. Novopay offers an end-to-end digital lending technology platform both as a SaaS and an enterprise solution. Contact us for a more detailed discussion to digitally enable your lending process.

#KYC for Banking#Saas solutions#Digital Distribution solution#Retailers provide Banking solutions#DMT#AePS#MicroATMs#CMS

0 notes

Text

4 Trends that Define the Future of Banking | Novopay Banking

The usually conservative banking industry is in the midst of transformational change. This change is led by 4 tectonic shifts in technology that have changed how we live, interact and deal with money.

Smartphones & Mobile Networks

Every smartphone user is carrying a computer a million times more powerful than all of NASA’s computing power in the early 70s. It is also embedded with 30+ sensors that can track our location, scan barcodes to capture our biometrics. This coupled with the current 4G network provides 60-100 Mbps speeds which can easily power the most engaging apps and content. The launch of low-cost internet data providers like Jio has doubled the data usage making India the 2nd largest internet-user in the world (see graph below).

This is the device for banking of the future be it deposit accounts, taking loans, buying insurance or buying mutual funds. You will do all your banking – anytime anywhere on the smartphone. The smartphone sensors can help make your banking personalized and location-specific. Connectivity ensures you can do all your payments and banking activities on the move at your convenience. Mobile alerts and notifications will help keep your money safe and secure.

Artificial Intelligence in Banking

The last decade has seen huge advances in Machine Learning(ML) algorithms that provide enormous power to transform banking as we know it. The ability of machine learning methods to ingest large amounts of existing data and hence behavior to learn and improve banking outcomes has remarkably improved.

According to a McKinsey report, more than half a dozen banks in Europe have already replaced the antiquated statistical-modeling approach with machine-learning techniques, which have resulted in a 10% increase in the sale of new products, 20% savings in capital expenditures and a 20% decline in churn.

Credit scoring attempts to predict human behavior when it comes to loan repayment. Traditional credit scoring methods looking at one variable at a time cannot unearth complex hidden relationships between parameters. Deep learning more closely mimicking the human brain is able to fit the data with more accurate non-linear models that will result in better loan decisions and hence small NPAs (non-performing assets).

Other Banking Applications There are several areas where AI has been used in Banking applications and the diagram below highlights the maturity of these applications.

API Banking

Despite Banks offering smartphone apps and web apps frontends to their customers, the future portends a more dynamic way in which the banking products will be consumed. Not all the customers of a Bank’s products will come from the Bank’s own Apps be it mobile or Web. Various aggregators, intermediaries, and partners could sell the bank’s your lending, insurance or investment products through their own apps hence bringing in new-to-bank customers dynamically. The weaving of new dynamic services and distribution channels for banking products is possible through APIs – Application Programmatic Interfaces. The new banking system architecture will need to support APIs that wrap key products to provide your partners with access to the banks offering in a simple yet secure system. These APIs need to be sufficiently granular so that the partner can deliver a differentiated and rich customer experience.

A Capgemini Financial Services Analysis study shows that there are several benefits that a Bank accrues when it supports APIs. See the diagram below for a quick summary of the analysis results.

Online Authentication and KYC

As smartphones grow and become the dominant mode of internet and online access they mobile device with its camera and other sensors allows for more convenient modes of verifying the mobile online customer – be it for authentication or performing KYC. The dominant smartphone platforms of Apple and Google Android have supported built-in biometric authentication using fingerprint or face, which have in turn been used to provide approval for payments be it for app purchase or for other online purchases – as in the case of Apple Pay or Google Pay.

These smartphone-based online verification mechanisms bring in enormous convenience literally at people’s fingertips while simultaneously increasing the level of assurance and security. These biometric modes can also be used in conjunction with OTP or pin/password making it a much stronger 2-factor authentication method.

The adoption of biometric-based authentication and KYC is increasing in banks the world over. A Deloitte study that highlights the growth of biometrics authentication by US consumers is shown in the diagram. Banks are increasingly performing transactions using an online device be it a smartphone, tablet or PC. Both dominant mobile platforms iOS and Android support built-in biometric sensors or attach biometric accessories through a USB cable or a Wi-Fi connection.

In India Aadhaar (biometric-based ID) has gained tremendous momentum in seamlessly verifying consumers using biometric and other methods over smartphones and PC platforms.

In the US and other western economies, the use of biometrics for payment authentication using mobile devices like smartphones has been gaining traction after the launch of Apple Pay on iPhones and other Apple devices, which uses a built-in fingerprint scanner or face-matching system to verify customers instantly. These methods of online authentication and KYC will reduce friction and improve not only the speed of acquiring customers but also for product purchase and registration.

In Conclusion

Smartphones and mobile networks will drive banking convenience and internet penetration making it the most important consumer platform for banking. Artificial Intelligence has made rapid strides and offers the ability to learn from large amounts of existing data in order to make more accurate credit-score predictions or accurate product recommendations. API Banking allows for the bank’s products to be unbundled and distributed using various partners and distribution channels in dynamic ways that the bank in itself would not have reached. Biometric and other online authentication and KYC methods provide for customer verification to happen on the customer’s own mobile device, delivering customer convenience but at the same time providing a high level of assurance on customer verification and KYC. The productivity gains of these innovations will also drive down the processing cost, allowing for smaller ticket size financial products and transactions – hence delivering on financial inclusion. These four megatrends fundamentally change the nature of banking services and bring a level of automation, convenience, customer focus & productivity that will transform and usher in a much more responsive and differentiated future bank.

#KYC for Banking#Saas solutions#Digital Distribution solution#Retailers provide Banking solutions#DMT#AePS#MicroATMs#CMS

1 note

·

View note