#Automotive Fuel Tank Market size

Text

Fueling the Future: Key Trends in the Automotive Fuel Tank Market

The automotive fuel tank market is evolving rapidly, driven by innovations in materials, design, and environmental regulations. According to Mordor Intelligence, The Automotive Fuel Tank Market is projected to be valued at USD 19.23 billion in 2024 and is expected to grow to USD 24.31 billion by 2029, with a compound annual growth rate (CAGR) of 4.80% during the forecast period (2024-2029). The demand for more efficient, lightweight, and eco-friendly fuel tank solutions is pushing manufacturers to explore new technologies and materials, transforming the industry.

Key Trends Shaping the Automotive Fuel Tank Market

Shift Toward Lightweight Materials One of the most significant trends in the automotive fuel tank market is the increasing use of lightweight materials such as plastic and composite materials. Traditional steel fuel tanks are gradually being replaced by plastic variants, which offer reduced weight, improved fuel efficiency, and better corrosion resistance. The use of high-density polyethylene (HDPE) in fuel tank production is particularly notable, as it offers flexibility, durability, and cost-effectiveness, helping automakers meet stringent fuel efficiency and emission standards.

Focus on Emission Regulations and Fuel Efficiency The automotive industry is under increasing pressure to comply with global emissions regulations, such as the Corporate Average Fuel Economy (CAFE) standards and Euro 6 emission norms. These regulations aim to reduce greenhouse gas emissions and improve fuel efficiency. As a result, manufacturers are developing fuel tanks that can withstand higher pressures, store alternative fuels, and incorporate features that minimize fuel evaporation. Evaporative emission control systems (EVAP) are becoming more common, helping to curb emissions and meet regulatory requirements.

Rising Demand for Alternative Fuels The push for alternative fuels such as compressed natural gas (CNG), liquefied petroleum gas (LPG), and hydrogen is reshaping the fuel tank industry. Specially designed fuel tanks are required to safely store and transport these fuels, leading to the development of reinforced composite tanks and multi-layer plastic tanks. As governments and consumers increasingly adopt cleaner fuels, the demand for alternative fuel tanks is expected to rise, presenting new opportunities for market growth.

Growth of Hybrid and Electric Vehicles The rise of hybrid and electric vehicles (EVs) is impacting the automotive fuel tank market. While EVs do not require traditional fuel tanks, hybrid vehicles still rely on fuel storage systems. However, the size and capacity of fuel tanks in hybrid vehicles are often smaller due to the presence of electric powertrains. This has led to a shift in the design and production of fuel tanks, focusing on compact, lightweight solutions that can fit into the limited space available in hybrid vehicles. Although the increasing penetration of EVs may slow the overall growth of the fuel tank market, hybrid vehicles will continue to drive demand for fuel storage systems.

Technological Advancements in Fuel Tank Design Innovations in fuel tank design are also shaping the market. Modern fuel tanks are being designed with advanced features such as modular fuel tank systems, which allow for easier installation and maintenance. Additionally, the integration of fuel level sensors, pressure management systems, and anti-leakage technologies is improving the overall performance and safety of fuel tanks. Manufacturers are investing in research and development to create more efficient and reliable fuel storage solutions that meet the needs of modern vehicles.

Regional Growth and Emerging Markets The Asia-Pacific region, particularly China, India, and Japan, is expected to experience significant growth in the automotive fuel tank market due to the rising demand for vehicles and increasing fuel efficiency regulations. North America and Europe are also witnessing growth, driven by the shift toward lightweight materials and alternative fuel adoption. Emerging markets in Latin America and Africa are presenting opportunities for manufacturers to expand their presence as vehicle ownership rises in these regions.

Conclusion

The automotive fuel tank market is set for steady growth in the coming years, driven by advancements in materials, environmental regulations, and the rising demand for alternative fuels. As the industry focuses on improving fuel efficiency, reducing emissions, and integrating new technologies, manufacturers must adapt to meet the evolving needs of the automotive sector. Lightweight, durable, and eco-friendly fuel tank solutions will be key to sustaining market growth, while innovations in design and technology will continue to shape the future of the industry.

With increasing investments in research and development and the global push for cleaner, more efficient transportation solutions, the automotive fuel tank market holds significant opportunities for growth and innovation. https://www.mordorintelligence.com/industry-reports/automotive-fuel-tank-market

#automotive fuel tank market#automotive fuel tank market size#automotive fuel tank market share#automotive fuel tank market forecast#automotive fuel tank market analysis

0 notes

Text

Automotive Fuel Tank Market is anticipated to reach $27.4 billion by 2027 at a CAGR of 4.2% during the forecast period 2022-2027. A fuel tank including reserve tanks, racing fuel cell, polymeric fuel tanks and others is a portion of an engine system where fuel is stored and then either pushed (fuel pump) or discharged (pressurized gas) into the engine.

👉 𝗗𝗼𝘄𝗻𝗹𝗼𝗮𝗱 𝐒𝐚𝐦𝐩𝐥𝐞 𝐑𝐞𝐩𝐨𝐫𝐭 @ https://tinyurl.com/2sfnxvxu

Automotive Fuel Tank Market Report Coverage

The report: “Automotive Fuel Tank Market – Forecast (2022-2027)”, by IndustryARC covers an in-depth analysis of the following segments of the Automotive Fuel Tank Market.

By Capacity: <45L, 45L-70L, >70L.

By Material: Aluminum, Plastic, Steel, Others.

By CNG Tank Type: Type 1, Type 2, Type 3, Type 4.

By Propulsion: Hybrid, Hydrogen, ICE, NGV.

By Application: Passenger vehicle, Light Commercial vehicle, Heavy commercial vehicle.

By Geography: North America (U.S, Canada, Mexico), Europe(Germany, UK, France, Italy, Spain, and Others), APAC(China, Japan India, SK, Aus and Others), South America(Brazil, Argentina and others) and RoW (Middle east and Africa)

#Automotive Fuel Tank Market Share#Automotive Fuel Tank Market Size#Automotive Fuel Tank Market Forecast#Automotive Fuel Tank Market Research#Automotive Fuel Tank Market Treads#Automotive Fuel Tank Market Application#Automotive Fuel Tank Market Growth#Automotive Fuel Tank Market Price

0 notes

Text

Automotive Fuel Tank Market Analysis, Size, Share, Growth, Trends, and Forecast, 2024-2034

The Automotive Fuel Tank market report offered by Reports Intellect is meant to serve as a helpful means to evaluate the market together with an exhaustive scrutiny and crystal-clear statistics linked to this market. The report consists of the drivers and restraints of the Automotive Fuel Tank Market accompanied by their impact on the demand over the forecast period. Additionally, the report includes the study of prospects available in the market on a global level. With tables and figures helping evaluate the Global Automotive Fuel Tank market, this research offers key statistics on the state of the industry and is a beneficial source of guidance and direction for companies and entities interested in the market. This report comes along with an additional Excel data-sheet suite taking quantitative data from all numeric forecasts offered in the study.

Get Sample PDF Brochure @ https://www.reportsintellect.com/sample-request/2911192

Key players offered in the market:

Inergy

Kautex

TI Automotive

Yachiyo

Hwashin

Magna Steyr

FTS

Futaba

SKH Metal

Sakamoto

Donghee

Tokyo Radiator

Additionally, it takes account of the prominent players of the Automotive Fuel Tank market with insights including market share, product specifications, key strategies, contact details, and company profiles. Similarly, the report involves the market computed CAGR of the market created on previous records regarding the market and existing market trends accompanied by future developments. It also divulges the future impact of enforcing regulations and policies on the expansion of the Automotive Fuel Tank Market.

Scope and Segmentation of the Automotive Fuel Tank Market

The estimates for all segments including type and application/end-user have been provided on a regional basis for the forecast period from 2024 to 2034. We have applied a mix of bottom-up and top-down methods for market estimation, analyzing the crucial regional markets, dynamics, and trends for numerous applications. Moreover, the fastest & slowest growing market segments are pointed out in the study to give out significant insights into each core element of the market.

Automotive Fuel Tank Market Type Coverage: -

Metal Fuel Tank

Plastic Fuel Tank

Automotive Fuel Tank Market Application Coverage: -

Commercial Vehicles

Passenger Vehicles

Regional Analysis:

North America Country (United States, Canada)

South America Asia Country (China, Japan, India, Korea)

Europe Country (Germany, UK, France, Italy)

Other Countries (Middle East, Africa, GCC)

Also, Get an updated forecast from 2024 to 2034.

Discount PDF Brochure @ https://www.reportsintellect.com/discount-request/2911192

The comprehensive report provides:

Reasons to Purchase Automotive Fuel Tank Market Research Report

Covid-19 Impact Analysis: Our research analysts are highly focused on the Automotive Fuel Tank Market covid-19 impact analysis. A whole chapter is dedicated to the covid-19 outbreak so that our clients get whole and sole details about the market ups & downs. With the help of our report the clients will get vast statistics as to when and where should they invest in the industry.

About Us:

Reports Intellect is your one-stop solution for everything related to market research and market intelligence. We understand the importance of market intelligence and its need in today's competitive world.

Our professional team works hard to fetch the most authentic research reports backed with impeccable data figures which guarantee outstanding results every time for you.

Contact Us:

[email protected]

Phone No: + 1-706-996-2486

US Address:

225 Peachtree Street NE,

Suite 400,

Atlanta, GA 30303

#Automotive Fuel Tank Market#Automotive Fuel Tank Market trends#Automotive Fuel Tank Market future#Automotive Fuel Tank Market size#Automotive Fuel Tank Market growth#Automotive Fuel Tank Market forecast#Automotive Fuel Tank Market analysis

0 notes

Text

Stainless Steel Market Size To Reach USD 197.29 Billion By 2030

Stainless Steel Market Growth & Trends

The global stainless steel market size is expected to reach USD 197.29 billion by 2030, registering a CAGR of 6.7% from 2024 to 2030, according to a new report by Grand View Research, Inc. Higher penetration of the product and its vital importance in numerous applications is expected to support the market growth, during the forecast period.

Stainless steel has extensive utilization in the automotive sector because of its visual appeal and corrosion resistance properties. Corrosion resistance helps its use in catalytic converters and exhaust silencers. These parts face exhaust gas attacks from the inner side and road dirt, salt, and water from the external side. In such cases, stainless steel is the best suitable material. Automotive applications of the product include fuel tanks, trim, gaskets, suspension systems, and bodies of the buses.

Characteristics of diverse stainless steel materials depending upon the application make them advantageous and preferable when compared to other materials. This is a major reason for their growing demand. For example, if we compare steel and aluminum since they are often considered alternatives in many applications, steel is preferable over aluminum because of its low cost, strength, and less likely to damp, bent, or warp.

Numerous applications have propelled the demand for stainless steel during these years and by enlargement in the end-use industries, the need for these materials is expected to increase further at a rapid rate. As a result, the production of the commodity is carried out on a large scale where iron ore is the key raw material. This ore is mined from the earth’s crust.

The increasing demand together with certain disadvantages, associated with conventional production processes such as the negative environmental effect of iron ore mining, has compelled vendors to opt for an alternative step, which is recycling. The phenomenal property of stainless steel can be recycled frequently without having any impact on the quality eventually promoting the stainless steel scrap industry.

Stainless steel scrap recycling has various benefits economically and environmental. Every ton of recycled steel saves 1.5 tons of iron ore, and 0.5 tons of coal, and reduces water consumption by 40.0%. In addition, carbon dioxide emissions are reduced by 50-60%. As a result, the advantages of metal recycling along with increasing demand for stainless steel in end-use applications are propelling the growth of the stainless steel market.

Request a free sample copy or view report summary: https://www.grandviewresearch.com/industry-analysis/stainless-steel-market

Stainless Steel Market Report Highlights

In terms of revenue, the Asia Pacific was the largest region in 2023 and is projected to remain the fastest-growing market during the forecast period. The region accounted for more than 68.0% of the total revenue in 2023 on account of industrial production for automotive, marine, construction, and consumer goods in the countries such as China, India, and Japan

The 300 series segment held the largest share of over 59.0% in 2023. The market is likely to be driven by the aerospace and marine industries on account of its properties such as thermal resistance and corrosion resistance

Flat products accounted for a revenue share of more than 73% in 2023 and is likely to dominate the market over the forecast period. The segment is projected to grow on account of the demand in consumer goods along with machinery & equipment industries, which is supported by the properties of stainless steel such as concentricity, straightness, and tolerance

Building & construction application segment is likely to observe a lucrative growth of 7.6% during the forecast period on account of massive investment in infrastructure and housing sectors by the countries such as the U.S., China, and India

The competitive rivalry within the industry is projected to increase with rising mergers & acquisitions, capacity expansion, in addition to network distribution

Stainless Steel Market Segmentation

Grand View Research has segmented the global stainless steel market on the basis of on grade, product, application, and region:

Stainless Steel Grade Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

200 Series

300 Series

400 Series

Duplex Series

Others

Stainless Steel Product Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

Flat

Long

Stainless Steel Application Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2030)

Building & Construction

Automotive & Transportation

Consumer Goods

Mechanical Engineering & Heavy Industries

Electronic Appliances

Food Manufacturing

Others

Stainless Steel Regional Outlook (Volume, Kilotons; Revenue, USD Billion, 2018 - 2030)

North America

Europe

Asia Pacific

Central & South America

Middle East & Africa

List of Key Players in the Stainless Steel Market

Acerinox S.A.

Aperam Stainless

ArcelorMittal

Baosteel Group

Jindal Stainless

Nippon Steel Corporation

Outokumpu

POSCO

ThyssenKrupp Stainless GmbH

Yieh United Steel Corp.

Browse Full Report: https://www.grandviewresearch.com/industry-analysis/stainless-steel-market

#Stainless Steel Market#Stainless Steel Market Size#Stainless Steel Market Share#Stainless Steel Market Trends

0 notes

Text

The Fuel Storage Tank market is projected to grow from USD 15295 million in 2024 to an estimated USD 21918.1 million by 2032, with a compound annual growth rate (CAGR) of 4.6% from 2024 to 2032.The fuel storage tank market is a critical segment of the energy infrastructure, providing essential storage solutions for various types of fuel, including crude oil, gasoline, diesel, and other petroleum products. These tanks play a vital role in ensuring a steady supply of fuel, managing demand fluctuations, and maintaining energy security. With the increasing global energy demand and the growing focus on energy infrastructure development, the fuel storage tank market has witnessed significant growth in recent years. This article explores the key trends, drivers, challenges, and future prospects of the fuel storage tank market.

Browse the full report at https://www.credenceresearch.com/report/fuel-storage-tank-market

Market Overview

Fuel storage tanks are containers designed to store fuel safely. These tanks come in various sizes and configurations, including underground, aboveground, and portable tanks. They are widely used across multiple industries, including oil and gas, chemical, automotive, and aviation, as well as by governments for strategic petroleum reserves. The market for fuel storage tanks is highly diversified, with applications ranging from small-scale storage solutions for individual consumers to large-scale storage facilities for industrial and commercial purposes.

Key Market Drivers

1. Rising Energy Demand: One of the primary drivers of the fuel storage tank market is the increasing global energy demand. As the world continues to industrialize and urbanize, the need for energy resources has surged. This has led to a growing demand for fuel storage solutions to ensure a continuous supply of energy.

2. Strategic Petroleum Reserves: Many countries maintain strategic petroleum reserves (SPR) to safeguard against supply disruptions. Governments around the world are investing in expanding their SPRs, driving the demand for large-scale fuel storage tanks. For example, the U.S., China, and India have been expanding their reserves in recent years, which has positively impacted the market.

3. Expansion of Refining Capacity: The expansion of refining capacities in emerging economies has created a significant demand for fuel storage tanks. As new refineries are built and existing ones are upgraded, the need for storage solutions to accommodate increased production volumes has grown.

4. Environmental Regulations: Stringent environmental regulations aimed at reducing emissions and preventing leaks are also driving the market. Compliance with these regulations often requires the installation of advanced storage tanks with leak detection and prevention systems.

Market Challenges

1. High Installation and Maintenance Costs: The installation and maintenance of fuel storage tanks can be expensive, particularly for large-scale facilities. The costs associated with construction, land acquisition, and regulatory compliance can be prohibitive for some market players, particularly in developing regions.

2. Environmental Concerns: Despite the critical role of fuel storage tanks, they pose significant environmental risks. Leaks and spills from storage tanks can lead to soil and water contamination, resulting in severe environmental damage and hefty fines for companies. This has led to increased scrutiny and regulatory pressure on tank operators.

3. Technological Advancements: The rapid pace of technological advancements in fuel storage solutions can be both an opportunity and a challenge. While new technologies offer improved safety and efficiency, they also require significant investment in research and development, which can be a barrier for smaller players in the market.

Future Outlook

The fuel storage tank market is poised for continued growth, driven by rising energy demand, strategic petroleum reserves, and the expansion of refining capacities. However, the market will also face challenges, including high costs, environmental concerns, and the need to keep pace with technological advancements. To stay competitive, market players will need to invest in innovation, comply with evolving regulations, and focus on sustainable practices.

Key Player Analysis:

Air Liquide

Belco

C&E Plastics Inc.

Cryolor

CST Industries

Enduraplas

Fuel Total Systems

GEI Works

Granby Industries

Haase Tank GmbH

Meridian Manufacturing Inc.

Sabre Manufacturing

Sintex

Textron

Western Global

Segmentation:

By Tank Type

Above-ground tanks

Underground tanks.

By Material Type

Steel,

Fiberglass,

Other materials.

By Tank Capacity

Small,

Medium,

Large tanks.

By End Use

Industrial,

Commercial,

Residential applications.

Based on the Region:

North America

US

Canada

Mexico

Europe

Germany

France

UK

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/fuel-storage-tank-market

About Us:

Credence Research is committed to employee well-being and productivity. Following the COVID-19 pandemic, we have implemented a permanent work-from-home policy for all employees.

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

0 notes

Link

0 notes

Text

Hydrogen Storage Market worth $6.3 billion by 2030

The report "Hydrogen Storage Market by Storage Form (Physical, Material-Based), Storage Type (Cylinder, Merchant, On-Site, On-board), Application (Chemicals, Oil Refineries, Industrial, Automotive & Transportation, Metalworking), Region - Forecast to 2030", size is projected to grow from USD 1.5 billion in 2023 to USD 6.3 billion by 2030, at a CAGR of 21.5% during the forecast period. The hydrogen storage market is growing due to the rise in the demand for fuel cell across various industries, and stringent government regulations globally.

Download pdf- https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=15698551

Gas form accounts the highest market share in terms of value and volume in 2022.

The gas form dominated the market in 2022 and is expected to hold its position during the forecast period. In the gas form, hydrogen is compressed into large tanks without liquefying it. This is generally preferred if gaseous supply is more economical. This technology enables the automakers to store enough hydrogen to allow a car that runs on a fuel cell battery to cover 500–600 km between fill-ups.

Merchant/Bulk accounts for the second-highest market share of the physical hydrogen storage market in 2022.

Bulk physical hydrogen storage tanks have applications in oil refineries, steel industries and more. Asia Pacific and North America have dominated the bulk physical hydrogen cylinder markets. The governments in some Asia Pacific countries are focusing on reducing greenhouse gases and adopting hydrogen as a fuel. For Instance, Japan aims to become a hydrogen society by 2050, whereas South Korea plans to build 310 hydrogen refueling stations by 2025. North America has manufacturing facilities like electronics manufacturing, transportation, and steel manufacturing; therefore, the demand for bulk physical hydrogen storage system is growing to support these industries. The demand for merchant physical hydrogen storage is expected to grow significantly due to the insufficiency of captive hydrogen in the existing oil refineries.

Oil refineries segment to be the second-largest application in the global physical hydrogen storage market in terms of value and volume in 2022.

Hydrogen gas is used for desulfurizing transportation fuels such as gasoline and diesel and reforming fuels derived from heavier distillates of crude oil refining. Furthermore, it is used in oil sand processing, gas-to-liquid, and coal gasification projects. The governments of developed and some developing countries have fixed regulations regarding using cleaner fuels to curb CO2 emissions, requiring hydrogen for desulfurization, which is expected to fuel the market growth.

Sample Request- https://www.marketsandmarkets.com/requestsampleNew.asp?id=15698551

Europe is witnessing exceptional growth during the forecast period in the physical hydrogen storage market.

In 2022, Europe held a share of 13.2% in the global physical hydrogen storage market. The primary drivers of physical hydrogen storage market in this region are the goal of reducing EU2 carbon emissions by 55% by 2030 compared to 1990 levels, rapid adoption of fuel cells due to an increasing number of fuel cell projects and government initiatives for their implementation. Further, the presence of prominent hydrogen storage tank manufacturers in the region are NPROXX, Plastic Omnium, Worthington Industries, and Air Liquide driving the hydrogen storage market.

The major players in hydrogen storage market are Air Liquide (France), Worthington Industries, Inc. (US), Luxfer Holdings PLC (UK), Linde plc (Germany), Chart Industries (US), HBank Technologies Inc. (Taiwan), Pragma Industries (France), Croyolor (France), INOXCVA (India), Hexagon Composites ASA (Norway), and others.

#HydrogenStorage#CleanEnergy#SustainableTech#RenewableEnergy#GreenHydrogen#EnergyTransition#HydrogenEconomy#FutureEnergy#HydrogenTechnology#EnergyStorage#CleanTech#Decarbonization#EnergyInnovation#HydrogenFuel#RenewableStorage

0 notes

Text

Global Coil Coatings Market Assessment, Opportunities, and Forecast, 2016-2030F

Global Coil Coatings Market size was valued at USD 3.82 billion in 2022, which is expected to grow to USD 5.56 billion in 2030 with a CAGR of 4.8% during the forecast period between 2023 and 2030. The coil coating market is primarily driven by the robust growth of the construction and infrastructure sectors, particularly in emerging economies such as India, China, and Brazil. Strong construction sector development fuels the demand for coil coatings, providing protective, aesthetic, and functional benefits to metal surfaces used in buildings and constructions. Additionally, the increasing emphasis on energy efficiency and sustainability drives the adoption of coil coatings, especially those that contribute to cool roofing and energy conservation in roofing systems. Regulatory compliance and the need for corrosion protection in the construction and automotive industries further spur the demand for high-quality coil coatings.

Coil coatings are extensively used for vehicle exteriors and components to enhance aesthetics, durability, and corrosion resistance. As the automotive sector grows with increasing production and sales, the demand for high-quality coil coatings is expected to rise accordingly. Moreover, the industrial and manufacturing sectors utilize coil coatings for various purposes such as durability in machinery, equipment, storage tanks, and more. Rising demand for electrical appliance contribute to the increased need for protective and functional coatings, further raising coil coating demand.

Sample report- https://www.marketsandata.com/industry-reports/coil-coatings-market

Huge Construction Projects to Drive the Demand for Coil Coating

Coil coatings protect and enhance metal surfaces used in residential, commercial, and industrial buildings. Coil Coatings provide essential features like corrosion resistance, durability, and aesthetic appeal. Modern architectural trends often integrate metal-coated surfaces, further driving the need for coil coatings to meet sustainability and durability requirements. Compliance with sustainability norms, and energy efficiency mandates are additional factors contributing to the growing demand for coil coatings in the construction industry.

For instance, the Magnolia Mixed-Use Complex in Texas is a project with an estimated value of USD 1,000 million and is anticipated to reach completion in the first quarter of 2025. Saudi Arabia has been actively undertaking numerous significant infrastructure endeavors. These encompass major initiatives such as NEOM, the Red Sea Project, Qiddiya, King Salman Energy Park, Jeddah Tower, and Riyadh Metro. Additionally, the Minamikoiwa 6-Chome District Type One Urban Redevelopment project in Tokyo, Japan, is on track for completion in 2026. These Large-scale construction projects around the globe will drive the demand for Coil Coating due to the increased requirement for efficient roofing and protection for metal surface.

Strong Performance from automotive sector to raise the Usage of Coil Coating

The automotive industry stands as a substantial consumer of coil coatings as it is utilized for diverse applications encompassing vehicle exteriors, parts, and accessories. With the steady rise in global automobile production and sales, the demand for high quality coatings has surged correspondingly. Coil coatings play a pivotal role in enhancing the aesthetic appeal of vehicles, ensuring durability, corrosion resistance, and longevity of automotive components. As automakers prioritize the use of high-quality coatings to meet consumer expectations for visually appealing and durable vehicles, the demand for advanced coil coatings is anticipated to further escalate in the automotive sector.

For instance, the Society of Indian Automobile Manufacturers reported notable growth in various segments. Specifically, sales of passenger cars increased from 1,467,039 to 1,747,376 units, utility vehicles saw a surge from 1,489,219 to 2,003,718 units, and van sales rose from 113,265 to 139,020 units in comparison to the fiscal year of 2022.

Stringent Environmental Regulations and Sustainability Initiatives to Increase Coil Coating Demand

Coil coated metals compared to post-painted metals have demonstrated a notable reduction in environmental impact through reduced water consumption and recycling. One of the key areas where coil coated metals exhibit a positive environmental footprint is in the reduced water consumption compared to post coating metals. The process of pre-painting typically has low energy and labour cost, reduced environmental impact and decreased water usage compared to the traditional post-painting methods.

For instance, According to European Coil Coating Association, the impact of coil coated aluminum and steel on human are just 24% and 25% of the impact of post painted metals. Since coil coating offers sustainability and abets safety standards compared to post painted metals, the consumer sentiments towards coil coating improved.

Impact of COVID-19

The COVID-19 pandemic significantly disrupted global supply chains, impacting the production and distribution of coil coatings and their raw materials. Delays and shortages were witnessed in the supply chain for coil coating and substrates such as steel and aluminium primarily due to factory closures and transportation restrictions. The pandemic-induced lockdowns and economic slowdowns led to a notable decrease in demand across various sectors such as construction and automotive, which weakened the demand for coil coatings during the pandemic. Finally, the coil coating market faced price fluctuations during the pandemic, driven by supply and demand dynamics disruptions.

Impact of Russia-Ukraine War

The Russia-Ukraine conflict had a notable impact on the coil coating market, particularly because Russia is a major supplier of aluminium substrate to various countries, especially in Europe. The conflict prompted several European nations to enforce import bans on Russian products, including aluminium. This restriction significantly tightened the supply of coil coated metals in these markets. Consequently, production costs for coil coating increased in these countries, reducing procurement activities. The war reduced construction and automotive activities in the affected region further weakening the demand for coil coatings.

Global Coil Coatings Market: Report Scope

“Coil Coatings Market Assessment, Opportunities and Forecast, 2016-2030F”, is a comprehensive report by Markets and Data, providing in-depth analysis and qualitative & quantitative assessment of the current state of Coil Coatings Market globally, industry dynamics and challenges. The report includes market size, segmental shares, growth trends, COVID-19 and Russia-Ukraine war impact, opportunities and forecast between 2023 and 2030. Additionally, the report profiles the leading players in the industry mentioning their respective market share, business model, competitive intelligence, etc.

Click here for full report- https://www.marketsandata.com/industry-reports/coil-coatings-market

Contact

Mr. Vivek Gupta

5741 Cleveland street,

Suite 120, VA beach, VA, USA 23462

Tel: +1 (757) 343–3258

Email: [email protected]

Website: https://www.marketsandata.com

0 notes

Text

Best manufacturer of LLDPE Powder Manufacturer and Supplier in India

LLDPE Rotomoulding Powder is the core products of roto process. These can be utilized in different applications too. These Products have a lot of interest on the lookout. Rotomolding Powder has penetrated most ancient markets for polyethylene

It’s used for plastic bags and sheets, wrapping, stretch wrap, pouches, toys, covers, lids, pipes, buckets and containers, covering of cables, and mainly flexible tubing.

Applications of LLDPE Rotomoulding Powder

Water Tanks and Containers:

80% to 90% of the LLDPE Powders are used to Manufacturing Plastic Water Storage Tanks, Containers and plastic barrels. Due to its flexibility and chemical resistance properties it is ideal material for storing various liquids like water, chemical & industrial fluids.

Toys and Play Equipments

Playground equipment being manufactured by such types of powders. Due to its impact resistance and durability, it is a best choice for producing toys, playground equipment, and recreational products. Our Powders helps products to withstand rough play and environmental conditions that requires products longevity and safety.

Automotive Components:

These LLDPE powders are used to manufacture automotive components like fenders, interior trim parts and, fuel tanks these powders have great resistance to chemicals and impact strength makes it best choice for components exposed to oils, fuels, oils, and having various temperatures.

Agricultural Products

These LLDPE Powders has great chemical resistance which is suitable for storing fertilizers, pesticides and other agrochemicals. Applications involve agricultural tanks, containers, and bins.

Custom Containers and Pallets

These LLDPE powders also help in making custom size containers, pallets and storage solutions. Rotomoulding process is best when it comes to creative design flexibility, unique shapes and various sizes. These powders are best choice for such applications.

PRODUCT

LLDPE FOAM MATERIAL

STONE EFFECT MARBLE COLOUR

LLDPE AGGLOMERATES

LLDPE POWDER

ROTOMOLDING POWDER

LLDPE PLASTIC RAW MATERIAL

For more Details

Click here : https://www.lldpefoam.com/

0 notes

Text

Railcar Leasing Market - Forecast(2024 - 2030)

Railcar Leasing Market size is estimated to reach US$17 billion by 2030, growing at a CAGR of 6.2%% during the forecast period 2024-2030. The increased industrialization, expansion of global trade, and the need for efficient transportation solutions are driving the demand for Railcar Leasing from the end users. This market growth is significantly driven by the flexibility and cost-effectiveness that leasing provides to companies, enabling them to adapt to varying transportation demands without substantial investments in ownership. These trends are expected to boost the growth of the Railcar Leasing Market during the forecast period.

The continual modernization of rail networks and the shift towards more sustainable transportation options are expected to propel the Railcar Leasing industry outlook during the forecast period.

Market Snapshot:

Railcar Leasing Market - Report Coverage:

The “Railcar Leasing Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Railcar Leasing Market.

Attribute

Segment

By Railcar Type

Tank Cars

Box Cars

Hopper Cars

Flat Cars

Gondola Cars

Others

By Leasing Type

Full-Service Leasing

Net Leasing

Others

By End Use Industry

Chemical

Automotive

Agriculture

Food & Beverage

Construction

Others

By Geography

North America (U.S., Canada and Mexico)

Europe (Germany, France, UK, Italy, Spain, Netherlands, Denmark and Rest of Europe),

Asia-Pacific (China, Japan, South Korea, India, Australia and Rest of Asia-Pacific),

South America (Brazil, Argentina, Chile, Colombia and Rest of South America)

Rest of the World (Middle East and Africa).

COVID-19 / Ukraine Crisis - Impact Analysis:

● The railcar leasing sector faced significant challenges due to the COVID-19 pandemic, which led to disruptions in manufacturing, supply chain constraints, and reduced economic activities. The lockdown measures and restrictions imposed to curb the spread of the virus resulted in a temporary decline in demand for railcar leasing services, particularly in sectors like manufacturing, energy, and transportation.

● The Russia-Ukraine war could indirectly impact the railcar leasing market. Escalating inflation and disruptions in the supply chain might lead to increased production costs. This ripple effect could affect multiple sectors, including transportation and operational expenses for railcar leasing.

Key Takeaways:

● Dominance of APAC : Geographically, in the Railcar Leasing market share, APAC is analyzed to hold the highest market share in 2023. This trend is fueled by the region's burgeoning industrial landscape and the expanding need for efficient transportation solutions. The demand for railcar leasing is notably accelerated by economic growth in countries like China and India, where rapid industrialization, burgeoning trade activities, and infrastructural developments are propelling the need for reliable and cost-effective transportation options. The increased focus on trade expansion and infrastructure development solidifies Asia Pacific's position as a key driver and dominant force in the global railcar leasing market.

● Tank Car to Register the Fastest Growth : In the Railcar Leasing Market analysis, the tank car segment is estimated to grow the fastest CAGR of 5.8% during the forecast period 2024-2030. This is attributed to the escalating demand for the transportation of bulk liquids and gases, including petroleum, chemicals, and liquefied gases. Tank cars serve as crucial assets in the energy and chemical industries, providing a secure means for transporting hazardous materials. According to the Association of American Railroads (AAR), railways is the preferred mode of ethanol transportation and 60 to 70% of ethanol transportation is done by rail. The expansion of industries reliant on these materials and the increasing need for efficient, safe transportation solutions drive the market growth in the tank car segment. This growth trajectory is reinforced by stringent safety standards and regulations, further emphasizing the importance and demand for specialized tank cars in the transportation of various liquid and gaseous commodities.

● Chemical is the Largest Segment in the Market : According to the Railcar Leasing Market forecast, the chemical segment is estimated to register the largest market share during the forecast period. According to the American Chemistry Council, the U.S. chemical manufacturing industry is one of the largest users of freight rail, shipping more than 33,000 carloads per week. This can be attributed to the ongoing growth and diversification of the chemical sector, which relies heavily on the efficient transportation of various chemical products. The chemical industry encompasses a wide range of products, from petrochemicals to specialty chemicals, used in manufacturing, agriculture, pharmaceuticals, and other sectors. As this industry continues to evolve and expand, the demand for specialized railcar leasing solutions for safe and efficient chemical transportation is set to surge. Moreover, stringent safety and environmental regulations further underscore the importance of dedicated railcar services, making the chemical industry a significant driver of growth in the railcar leasing market.

● Need for Efficient Transportation Solutions : The pressing need for efficient transportation solutions stands as a pivotal driver in the railcar leasing industry. As industries expand globally and supply chains become increasingly complex, the demand for reliable, cost-effective, and flexible transportation options intensifies. Railcar leasing offers a strategic solution, enabling businesses to adapt swiftly to fluctuating transportation demands without massive capital investments in ownership. The efficiency of rail transport in moving bulk goods, coupled with its relatively lower environmental impact, makes it an attractive option. Moreover, railcar leasing fulfills the necessity for specialized transport of various commodities, promoting a safer and more sustainable mode of freight movement within the ever-evolving logistics landscape. For example, the Norwegian government decided to invest $14.4 billion in rail infrastructure & digitization projects under the National Transportation Plan, in March 2021. It will cover new railway projects and digitalization investments and the existing infrastructure to meet the growing population's requirements, thus reducing emissions and road congestion. Thus, the need for efficient transport solutions acts as a driver for the growth of the Railcar Leasing Market during the forecast period.

● Flexibility and Cost-Effectiveness of Leasing : Offering a dynamic alternative to outright ownership, leasing allows companies to swiftly adapt to changing market demands without substantial upfront capital investments. This financial flexibility is crucial in industries where demand fluctuates, enabling businesses to adjust their fleet size according to immediate needs without the burden of maintaining excess railcars during downturns. Additionally, leasing reduces operational costs by outsourcing maintenance, repair, and regulatory compliance, providing a predictable cost structure. This flexibility and financial prudence make railcar leasing an appealing, adaptive, and economically viable solution for various industries reliant on efficient transportation of goods. Thus, the flexibility and cost-effectiveness drive the Railcar Leasing Market.

● Regulatory Compliance and Safety Standards to Impede to Market growth : Stricter regulations imposed by governmental bodies require railcar lessors to consistently meet evolving safety protocols, environmental standards, and industry-specific regulations. Compliance demands vigilant monitoring and investment in retrofitting, maintenance, and upgrades to ensure the fleet aligns with the latest safety measures. The intricacies of meeting these stringent standards entail significant costs and procedural complexities. Such challenges can hinder the growth of the Railcar Leasing Market.

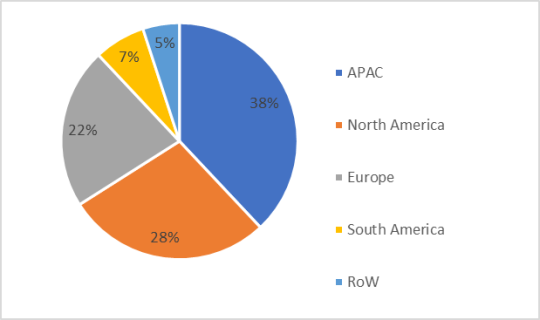

Railcar Leasing Market Share (%) By Region, 2023

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the Railcar Leasing Market. The top 10 companies in this industry are listed below:

American Railcar Industries Inc.

Brunswick Rail Management Ltd.

CIT Group Inc.

GATX Corporation

Mitsui Rail Capital

The Greenbrier Companies

Trinity Industries Inc.

SMBC GROUP

Touax Group

Chicago Freight Car Leasing

Scope of Report:

Report Metric

Details

Base Year Considered

2023

Forecast Period

2024–2030

CAGR

6.2%

Market Size in 2030

$17 billion

Segments Covered

Rail Car Type, Leasing Type, End Use Industry and Region

Geographies Covered

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Netherlands, Denmark and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa).

Key Market Players

American Railcar Industries Inc.

Brunswick Rail Management Ltd.

CIT Group Inc.

GATX Corporation

Mitsui Rail Capital

The Greenbrier Companies

Trinity Industries Inc.

SMBC GROUP

Touax Group

Chicago Freight Car Leasing

For more Automotive Market reports - Please click here

0 notes

Text

Heating Oil Additives Market: Global Demand Analysis & Opportunity Outlook 2035

Research Nester’s recent market research analysis on “Heating Oil Additives Market: Global Demand Analysis & Opportunity Outlook 2035” delivers a detailed competitor’s analysis and a detailed overview of the global heating oil additives market in terms of market segmentation by type, fuel type, end-user, and by region.

Growing Incidents of Engine Failures to Drive Growth of the Global Heating Oil Additives Market

The global heating oil additives market is estimated to grow majorly on account of the growing demand for heating oil additives to reduce the number of incidents associated with the failure of engines across the globe. Most engine failure incidents occur owing to clogged tanks where fuel can flow properly. Engine failures are expected to cause multiple unpleasant events and this issue is anticipated to hike the market growth over the forecast period. For instance, the annual rate of engine failure across the globe was estimated to be around 200. If the engine failure is associated with the aviation sector, it was projected to deduct around 300,000 scheduled flight hours. Furthermore, the surge in the prices of fuel worldwide and rising government initiatives towards fuel efficiency are further expected to expand the market size during the forecast period. For instance, it was anticipated that the average price reached around USD 1.35 per liter worldwide in 2022.

Request Report Sample@ https://www.researchnester.com/sample-request-4080

Furthermore, the global heating oil additives market is also anticipated to grow on the back of the growing production of diesel and its growing demand in the automotive industry over the forecast period. Heating oil additives are mixed in the diesel to increase its efficiency and it is also a highly preferable fuel by the consumer owing to its enhanced properties. For instance, more than 45 billion gallons of diesel were noticed to be consumed in the USA in 2021 while around 1 billion barrels of diesel were produced in a similar year in the United States. Additionally, the surge in the production of automobiles with combustion engines worldwide is further anticipated to hike the market growth over the forecast period. As of 2021, nearly 75 million motor vehicles were anticipated to be produced across the globe. Hence, all these factors are projected to influence the growth of the market positively during the forecast period.

Some of the major growth factors and challenges that are associated with the growth of the global heating oil additives market are:

Growth Drivers:

Surge in Production of Motor Vehicle

Rising Concern of Cod Emission from Vehicles

Challenges:

The presence of substitute products and the requirement for a Large Amount of Money as an Initial Investment are some of the major factors anticipated to hamper the growth of the global heating oil additives market during the forecast period. Furthermore, increasing production of electric vehicles is projected to hamper the market growth as well in every aspect. Electric vehicles are produced with the notion of eliminating the utilization of fuel completely. The higher production of electric vehicles has been observed in recent decades. For instance, there will be more than 120 million electric vehicles on the road by 2030.

By end-user, the global heating oil additives market is segmented into industrial, residential, and commercial. The commercial segment is expected to generate the most revenue by the end of 2035, with a significant CAGR over the forecast period. The growth of the commercial segment can be ascribed to the higher sales volume of fuel additives across the globe on the back of booming demand in the aerospace and automotive industry. Furthermore, the lower quality of the crude oil is furthermore anticipated to propel the segment growth over the forecast period. As of 2021, approximately 65 million automobiles were sold across the globe. Furthermore, by fuel type, the market is further bifurcated into bio-diesel, diesel, LPG, and petrol, out of which, the diesel segment is estimated to hold the largest share during the forecast period. The segment is estimated to grow on the back of higher demand for diesel in various industries such as automotive, aerospace, and others.

By region, the Asia Pacific heating oil additives market is to generate the highest revenue by the end of 2035. This growth is anticipated increasing sales of 2 and 3-wheelers in the region coupled with the escalated production of passenger cars in the region. Asia Pacific has an important role in the global automotive industry which is also one of the major growth factors of the market. For instance, approximately 30 million passenger cars were noticed to be produced in the Asia pacific in 2020. Furthermore, the surge in the manufacturing sector of the region which is being supported by the up-surged investment is also expected to hike the market growth owing to higher demand for heating oil additives over the forecast period. Furthermore, the market is also estimated to witness notable growth in the European region by obtaining the second-largest share during the forecast period. Europe is known to be the leading consumer of heating oil additives which is expected to flourish the market growth over the forecast period.

This report also provides the existing competitive scenario of some of the key players of the global heating oil additives market which includes company profiling of East Cork Oil Company Unlimited Company, Emissions-Reduzierungs-Concepte GmbH, Yorkshire Oils Ltd, Estuary Oils Depot, HomeFuels Direct Ltd, Bell Performance, Inc., Afton Chemical Corporation, BASF SE, Lubrizol Corporation, CPS Fuels Ltd, and others.

Access our detailed report at: https://www.researchnester.com/reports/heating-oil-additives-market/4080

Research Nester is a leading service provider for strategic market research and consulting. We aim to provide unbiased, unparalleled market insights and industry analysis to help industries, conglomerates, and executives to take wise decisions for their future marketing strategy, expansion, investment, etc. We believe every business can expand to its new horizon, provided the right guidance at a right time is available through strategic minds. Our out of box thinking helps our clients to take wise decisions in order to avoid future uncertainties.

Contact for more Info:

AJ Daniel

Email: [email protected]

U.S. Phone: +1 646 586 9123

U.K. Phone: +44 203 608 5919

0 notes

Text

The global demand for Adipic Acid market was valued at USD 7984.2 Million in 2023 and is expected to reach USD 12927.1 Million in 2032, growing at a CAGR of 5.50% between 2024 and 2032.Adipic acid, a white crystalline powder, is primarily used as a monomer in the production of nylon 6,6, a key component in the textile and automotive industries. With its wide-ranging applications in various sectors, the adipic acid market has experienced significant growth over the past few decades. This article delves into the current state of the adipic acid market, its growth drivers, challenges, and future prospects.

Browse the full report at https://www.credenceresearch.com/report/adipic-acid-market

Market Overview

The global adipic acid market was valued at approximately USD 5 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 4.5% from 2024 to 2030. This growth can be attributed to the increasing demand for nylon 6,6, the expansion of the automotive and textile industries, and the rising emphasis on sustainability.

Key Drivers

1. Automotive Industry Growth: Nylon 6,6, derived from adipic acid, is extensively used in the automotive industry for manufacturing various components such as air intake manifolds, engine covers, and radiator end tanks. The lightweight and durable nature of nylon 6,6 makes it a preferred material, driving the demand for adipic acid. The global shift towards electric vehicles (EVs) further fuels this demand, as EVs require lightweight materials to enhance energy efficiency.

2. Textile Industry Expansion: Nylon 6,6 is also a crucial material in the textile industry, used in the production of carpets, apparels, and industrial yarns. The increasing consumer demand for high-performance textiles and the growth of the fashion industry are significant factors propelling the adipic acid market.

3. Sustainability and Green Chemistry: There is a growing emphasis on sustainability and reducing carbon footprints across industries. The adipic acid market is witnessing innovations in bio-based production methods, which utilize renewable raw materials instead of traditional petrochemical sources. These environmentally friendly processes are gaining traction, aligning with global sustainability goals and attracting investments.

Challenges

Despite its promising growth, the adipic acid market faces several challenges:

1. Volatile Raw Material Prices: Adipic acid production relies heavily on petrochemical derivatives such as cyclohexane. Fluctuations in crude oil prices directly impact the cost of raw materials, affecting the overall production cost and market stability.

2. Environmental Concerns: Traditional adipic acid production methods involve the use of nitric acid, leading to the emission of nitrous oxide, a potent greenhouse gas. Stricter environmental regulations and the need to reduce greenhouse gas emissions pose significant challenges to conventional production processes. Companies are investing in research and development to discover more sustainable and eco-friendly production methods.

3. Competition from Alternatives: The development of alternative materials, such as bio-based polyamides and other synthetic fibers, poses a threat to the adipic acid market. These alternatives offer similar properties and, in some cases, better performance, leading to a potential shift in market dynamics.

Regional Insights

The Asia-Pacific region dominates the adipic acid market, accounting for the largest share in 2023. The region's rapid industrialization, expanding automotive and textile sectors, and growing population contribute to this dominance. China, in particular, is a major consumer and producer of adipic acid, driven by its robust manufacturing capabilities and increasing demand for high-performance materials.

North America and Europe also hold significant market shares, with well-established automotive and textile industries. The focus on sustainable production methods and stringent environmental regulations in these regions further drive innovation and market growth.

Future Prospects

The future of the adipic acid market looks promising, with several trends shaping its trajectory:

1. Bio-based Production Methods: Continued advancements in bio-based adipic acid production methods are expected to reduce the environmental impact and enhance sustainability. These methods leverage renewable resources and offer a greener alternative to traditional processes.

2. Technological Innovations: Ongoing research and development efforts are focused on improving production efficiency, reducing costs, and discovering novel applications for adipic acid. Innovations in catalyst technologies and process optimization are likely to drive future growth.

3. Rising Demand for High-Performance Materials: The increasing demand for lightweight, durable, and high-performance materials in various industries, including automotive, textiles, and electronics, will continue to propel the adipic acid market. The shift towards electric vehicles and sustainable practices will further augment this demand.

Key Players

Ascend Performance Materials

Asahi Kasei Corporation

BASF SE

INVISTA

LANXESS

Liaoyang Tianhua Chemical Co., Ltd

Radici Partecipazioni S.p.A.

Solvay

Sumitomo Chemical Co., Ltd.

DOMO Chemicals

Segmentation by Application

In 2023, the nylon production, six fiber application segment dominated the market, accounting for 53.1% of the total revenue. Its significant market share is driven by the expanding use of nylon 6, 6 as a metal alternative in automotive, electrical, and electronic devices, among other things. Nylon 6,6 fiber is also commonly used in technical components such as gears, nuts, bolts, bearings, powder tool casings, rivets and wheels, and rocker box covers. The properties of nylon 6,6 fiber, such as moisture and mildew resistance, high melting temperature, outstanding durability, and improved strength, are predicted to push its employment in a variety of applications in the coming years.

Polyurethane Production also has a consistent growth potential due to its use in a variety of end-use industries.

Segmentation by End-Use Industry

The automotive segment dominated the market over the projection period. The automotive industry mostly uses nylon 66, which is manufactured from adipic acid, due to its superior mechanical, temperature-resistant, and lightweight properties. Adipic acid is commonly used as a monomer in the production of polyamide 6.6 pellets and other polyamides or polymers for engineering plastics, as well as polyurethane for flexible and semi-rigid foam.

However, the food and beverage industry sector has gained significant market share.

Segmentation by Form

The powder form of Adipic Acid is in high demand in the market. Adipic acid powder is widely utilized in a variety of industries, including textiles, automobiles, and food. It is preferred for its portability, storage, and transportation. The powder form enables exact dosing, making it suited for a variety of applications. In addition, the powder form is more stable and has a longer shelf life than the liquid version.

Segmentation by Purity

Food Grade is the fastest-growing section of the Adipic Acid Market. Adipic Acid is becoming increasingly popular in the food business due to its numerous possibilities as a food ingredient. In food and beverage items, adipic acid is used to regulate acidity and increase flavor.

Segmentation by Production Process

Cyclohexane held the largest market share in 2023. Almost all commercial adipic acid is made from cyclohexane. It is commonly utilized as an intermediate chemical in a variety of processes, with around 54% of its output used to produce adipic acid for nylon-66.

However, cyclohexanone is expected to increase at the fastest CAGR of 8.5% throughout the projection period.

Segmentation by Region

North America dominated the global industry in 2023, accounting for more than 32.9% of total revenue

Asia Pacific is predicted to be the fastest-growing regional market

The rest of the world, including Latin America, the Middle East, and Africa, supplies the remaining demand for Adipic Acid.

Browse the full report at https://www.credenceresearch.com/report/adipic-acid-market

About Us:

Credence Research is committed to employee well-being and productivity. Following the COVID-19 pandemic, we have implemented a permanent work-from-home policy for all employees.

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

Website: www.credenceresearch.com

0 notes

Text

Automotive Gas Cylinder Market Analysis: Forecasted Market Size, Top Segments, And Largest Region

The latest report by Fortune Business Insight Research Company Insights, titled Global Automotive Gas Cylinder Market - Size, Trends, Share, Growth, Dynamics, Competition, and Opportunity Forecast Period, provides a thorough analysis of the global Automotive Gas Cylinder Market. The report meticulously examines both macro and micro trends, offering insights into the dynamic factors influencing the market. It encompasses a detailed exploration of qualitative and quantitative aspects, delivering a precise depiction of market size, growth rates, annual progression, prevailing trends, key drivers, promising opportunities, and potential challenges. Additionally, the report highlights the impact of crucial events such as new product launches or approvals, as well as the influence of external factors such as technological advancements and consumer preferences on the automotive carbon wheels market landscape. This exhaustive examination equips businesses and stakeholders with invaluable intelligence for making informed decisions in the evolving automotive industry.

A parallel surge in industrial growth and heightened utilization of commercial vehicles is underway throughout the Asia Pacific.

Get Sample PDF Report: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/108312

Market Size And Growth Forecast:

The automotive Automotive Gas Cylinder Market size has grown strongly in recent years. in the historic period can be attributed to vehicle production growth, stringent automotive safety standards, consumer demand for noise reduction, increasing emphasis on vehicle aesthetics, and globalization of automotive supply chains.

The Automotive Gas Cylinder Market size is expected to see strong growth in the next few years. It will grow in the forecast period & can be attributed to rise in autonomous vehicle adoption, stringent environmental regulations, demand for enhanced weather resistance, focus on energy-efficient vehicles, and innovations in seal manufacturing processes. Major trends in the forecast period include advancements in sealing technologies, the development of self-healing seals, customization for luxury and premium vehicles, integration of advanced materials, and collaborations for innovation.

Major Automotive Gas Cylinder Market Manufacturers covered in the market report include:

3M, Clean NG, CNG Cylinders International, Cobham Plc, Faber Industries, Luxfer Gas Cylinders, Quantum Fuel Systems LLC, Beijing China Tank Industry Co. Ltd., Everest Kanto Cylinder Ltd, and MCH Technologies GmbH.

The demand for automotive gas cylinders is continuously fueled by the surge in automotive fleets, emerging commercial vehicle infrastructure, and advancements in manufacturing technology.

What is the anticipated market size in 2030, along with the major drivers, restraints, and opportunities?

The market is driven by factors such as the increasing demand for lightweight and high-performance automotive components to enhance fuel efficiency and reduce carbon emissions. Advancements in carbon fibre technology, coupled with growing consumer preference for premium and customized vehicles, are also significant drivers. However, challenges such as high manufacturing costs and limited adoption in mass-market vehicles may hinder market growth. Opportunities lie in collaborations between automotive manufacturers and carbon fibre suppliers to develop innovative and cost-effective solutions for various vehicle segments.

Scope of the Report:

► Executive Summary

► Demand and Supply-side Trends

► Market Drivers, Restraints, Opportunities, and Challenges

► Value Chain Analysis

► Porter's Five Forces Analysis

► Industry SWOT Analysis

► COVID-19 Impact Assessment

► PESTLE Analysis

► Global Market Size and Forecast

► Regional Market Size and Forecast (Cross-country Analysis)

► Competition Landscape

► Company Profiles

Market Segmentation by Geography includes:

∆ North America: U.S., Canada, and Mexico

∆ Europe: Germany, France, U.K., Italy, Spain, and Rest of Europe

∆ Asia Pacific: China, India, Japan, South Korea, Southeast Asia, and Rest of Asia Pacific

∆ South America: Brazil, Argentina, and Rest of Latin America

∆ Middle East & Africa: GCC Countries, South Africa, and the Rest of Middle East & Africa

Frequently Asked Questions (FAQs):

► What is the current market scenario?

► What was the historical demand scenario, and forecast outlook from 2024 to 2030?

► What are the key market dynamics influencing growth in the Global Automotive Gas Cylinder Market?

► Who are the prominent players in the Global Automotive Gas Cylinder Market?

► What is the consumer perspective in the Global Automotive Gas Cylinder Market?

► What are the key demand-side and supply-side trends in the Global Automotive Gas Cylinder Market?

► What are the largest and the fastest-growing geographies?

► Which segment dominated and which segment is expected to grow fastest?

► What was the COVID-19 impact on the Global Automotive Gas Cylinder Market?

Table Of Contents:

1 Market Overview

1.1 Automotive Gas Cylinder Market Introduction

1.2 Market Analysis by Type

1.3 Market Analysis by Applications

1.4 Market Analysis by Regions

1.4.1 North America (United States, Canada and Mexico)

1.4.1.1 United States Market States and Outlook

1.4.1.2 Canada Market States and Outlook

1.4.1.3 Mexico Market States and Outlook

1.4.2 Europe (Germany, France, UK, Russia and Italy)

1.4.2.1 Germany Market States and Outlook

1.4.2.2 France Market States and Outlook

1.4.2.3 UK Market States and Outlook

1.4.2.4 Russia Market States and Outlook

1.4.2.5 Italy Market States and Outlook

1.4.3 Asia-Pacific (China, Japan, Korea, India and Southeast Asia)

1.4.3.1 China Market States and Outlook

1.4.3.2 Japan Market States and Outlook

1.4.3.3 Korea Market States and Outlook

1.4.3.4 India Market States and Outlook

1.4.3.5 Southeast Asia Market States and Outlook

1.4.4 South America, Middle East and Africa

1.4.4.1 Brazil Market States and Outlook

1.4.4.2 Egypt Market States and Outlook

1.4.4.3 Saudi Arabia Market States and Outlook

1.4.4.4 South Africa Market States and Outlook

1.5 Market Dynamics

1.5.1 Market Opportunities

1.5.2 Market Risk

1.5.3 Market Driving Force

2 Manufacturers Profiles

Continued…

About Us:

Fortune Business Insights™ delivers accurate data and innovative corporate analysis, helping organizations of all sizes make appropriate decisions. We tailor novel solutions for our clients, assisting them to address various challenges distinct to their businesses. Our aim is to empower them with holistic market intelligence, providing a granular overview of the market they are operating in.

Contact Us:

Fortune Business Insights™ Pvt. Ltd.

308, Supreme Headquarters,

Survey No. 36, Baner,

Pune-Bangalore Highway,

Pune - 411045, Maharashtra, India.

Phone:

US:+1 424 253 0390

UK: +44 2071 939123

APAC: +91 744 740 1245

#Automotive Gas Cylinder Market#Automotive Gas Cylinder Market Share#Automotive Gas Cylinder Market Size#Automotive Gas Cylinder Market trends#Automotive Gas Cylinder Market Growth

0 notes

Text

Diving into the Polyethylene (PE) Market: Beyond the Numbers

The Plastic Odyssey Begins

In the grand scheme of plastics, polyethylene reigns supreme. From detergent bottles to car fuel tanks, this versatile material has its hands (or should we say molecules?) in everything. It’s practically the Beyoncé of plastics, used in transparent food wrapping, shopping bags, and even flexing its synthetic fiber muscles.

Types of Polyethylene: It’s not a One-Size-Fits-All Extravaganza

HDPE — The Tough Guy: With its low manufacturing costs, high strength to density ratio, and resistance to various solvents, High Density Polyethylene (HDPE) takes the crown. It’s the superhero of the polyethylene world, saving the day in ballistic plates, bottle caps, and even boats.

LDPE — The Flexible Friend: Low Density Polyethylene (LDPE) takes a softer approach, finding its home in packaging, especially in the food business. Its chemical resistance, flexibility, and softness make it the go-to choice for lightweight packaging in electronics, healthcare, and food & beverage.

End-User Extravaganza

Packaging — Where Polyethylene Takes the Lead: The food & beverage industry is headlining the show, accounting for the largest market share in the packaging segment. With a demand for flexible packaging soaring, polyethylene is the rockstar keeping things sealed, protected, and looking good on the shelves.

Infrastructure & Construction — The Supporting Act: Coming in hot as the second most significant segment, polyethylene’s role in construction materials is on the rise. From films and sheets for windows to roofing materials, it’s helping build a world that’s sturdy and, dare we say, polyethene-fabulous.

Global Domination: Asia-Pacific Leads the Charge

Surprise, surprise! Asia Pacific steals the spotlight with the largest market share, thanks to major consumers like China and India. The demand for polyethylene in this region increased by 4%, fueled by the packaging and infrastructure & construction sectors.

What’s Driving the Polyethylene Party?

The Polyethylene Parade: The rise in demand for high-strength plastic is turning heads across various sectors, including automotive, electrical & electronics, and consumer goods. Manufacturers are on the polyethylene bandwagon, using it for everything from packaging electrical components to making vehicles lighter and more efficient.

Food & Beverage Frenzy: The food and beverage industry is all about that effective packaging life. Polyethylene’s ability to block moisture is the superhero cape that shields our favorite snacks and drinks from internal and external disturbances. No one likes a soggy chip, after all.

Speed Bumps on the Polyethylene Highway

The Imitation Game: Polyethylene has some rivals in the form of polypropylene and polyethylene terephthalate (PET). These copycats threaten to steal the polyethylene thunder with their similarity in properties. Fluctuating raw material prices also decide to join the party as potential party poopers.

Polyethylene Powerhouses: Who’s Who in the PE World

Meet the giants — Exxon Mobil Corporation, Dow Chemical Company, LyondellBasell Industries N.V., and more. These powerhouses are making sure polyethylene continues its world tour, reaching every nook and cranny.

Recent Highlights from the Polyethylene Chronicles

November 2021: Charter Next Generation and NOVA Chemicals Corporation join forces for environmentally friendly packaging films. Recycling plastic components? Bravo!

May 2021: LACTEL and INEOS team up for the world’s first HDPE milk bottles using circular polyethylene from post-consumer recycled materials. Talk about milking the eco-friendly trend!

For More Information: https://www.skyquestt.com/report/polyethylene-market

Key Trends: What’s Hot in the Polyethylene World?

Packaging Paradise: Thanks to its durability, ease of customization, and moisture resistance, polyethylene is the rockstar of packaging. The cheap and recyclable nature of polyethylene makes it the go-to choice for the food and beverage and consumer goods industries.

In Conclusion: Polyethylene — The Undisputed Champion

In a world drowning in plastics, polyethylene stands tall. With its varied applications, from saving our snacks from moisture to building the structures we live in, it’s the unsung hero of our daily lives.

So, next time you grab that bottle of water or open a bag of chips, remember — behind that convenience is a world of polyethylene magic, making our lives a little easier, one plastic molecule at a time.

About Us-

SkyQuest Technology Group is a Global Market Intelligence, Innovation Management & Commercialization organization that connects innovation to new markets, networks & collaborators for achieving Sustainable Development Goals.

Contact Us-

SkyQuest Technology Consulting Pvt. Ltd.

1 Apache Way,

Westford,

Massachusetts 01886

USA (+1) 617–230–0741

Email- [email protected]

Website: https://www.skyquestt.com

0 notes

Text

Diving into the Polyethylene (PE) Market: Beyond the Numbers

Peekaboo, plastics are everywhere! Well, not that it’s hiding, but the Global Polyethylene (PE) Market is definitely making waves. Let’s take a stroll through the world of polyethylene, where low cost meets water resistance, and manufacturing ease is the name of the game.

The Plastic Odyssey Begins

In the grand scheme of plastics, polyethylene reigns supreme. From detergent bottles to car fuel tanks, this versatile material has its hands (or should we say molecules?) in everything. It’s practically the Beyoncé of plastics, used in transparent food wrapping, shopping bags, and even flexing its synthetic fiber muscles.

Types of Polyethylene: It’s not a One-Size-Fits-All Extravaganza

HDPE — The Tough Guy: With its low manufacturing costs, high strength to density ratio, and resistance to various solvents, High Density Polyethylene (HDPE) takes the crown. It’s the superhero of the polyethylene world, saving the day in ballistic plates, bottle caps, and even boats.

LDPE — The Flexible Friend: Low Density Polyethylene (LDPE) takes a softer approach, finding its home in packaging, especially in the food business. Its chemical resistance, flexibility, and softness make it the go-to choice for lightweight packaging in electronics, healthcare, and food & beverage.

End-User Extravaganza

Packaging — Where Polyethylene Takes the Lead: The food & beverage industry is headlining the show, accounting for the largest market share in the packaging segment. With a demand for flexible packaging soaring, polyethylene is the rockstar keeping things sealed, protected, and looking good on the shelves.

Infrastructure & Construction — The Supporting Act: Coming in hot as the second most significant segment, polyethylene’s role in construction materials is on the rise. From films and sheets for windows to roofing materials, it’s helping build a world that’s sturdy and, dare we say, polyethene-fabulous.

Global Domination: Asia-Pacific Leads the Charge

Surprise, surprise! Asia Pacific steals the spotlight with the largest market share, thanks to major consumers like China and India. The demand for polyethylene in this region increased by 4%, fueled by the packaging and infrastructure & construction sectors.

What’s Driving the Polyethylene Party?

The Polyethylene Parade: The rise in demand for high-strength plastic is turning heads across various sectors, including automotive, electrical & electronics, and consumer goods. Manufacturers are on the polyethylene bandwagon, using it for everything from packaging electrical components to making vehicles lighter and more efficient.

Food & Beverage Frenzy: The food and beverage industry is all about that effective packaging life. Polyethylene’s ability to block moisture is the superhero cape that shields our favorite snacks and drinks from internal and external disturbances. No one likes a soggy chip, after all.

Speed Bumps on the Polyethylene Highway

The Imitation Game: Polyethylene has some rivals in the form of polypropylene and polyethylene terephthalate (PET). These copycats threaten to steal the polyethylene thunder with their similarity in properties. Fluctuating raw material prices also decide to join the party as potential party poopers.

Polyethylene Powerhouses: Who’s Who in the PE World

Meet the giants — Exxon Mobil Corporation, Dow Chemical Company, LyondellBasell Industries N.V., and more. These powerhouses are making sure polyethylene continues its world tour, reaching every nook and cranny.

Recent Highlights from the Polyethylene Chronicles

November 2021: Charter Next Generation and NOVA Chemicals Corporation join forces for environmentally friendly packaging films. Recycling plastic components? Bravo!

May 2021: LACTEL and INEOS team up for the world’s first HDPE milk bottles using circular polyethylene from post-consumer recycled materials. Talk about milking the eco-friendly trend!

For More Information: https://www.skyquestt.com/report/polyethylene-market

Key Trends: What’s Hot in the Polyethylene World?

Packaging Paradise: Thanks to its durability, ease of customization, and moisture resistance, polyethylene is the rockstar of packaging. The cheap and recyclable nature of polyethylene makes it the go-to choice for the food and beverage and consumer goods industries.

In Conclusion: Polyethylene — The Undisputed Champion