#Bank Account Freeze Court Recovery Order

Text

Understanding the Role of a Law Firm in Debt Collection

Ensuring the smooth flow of capital and maintaining the economic health of businesses and individuals. Law firms play a significant role in this process, providing legal expertise and strategic approaches to debt recovery.

The Role of a Law Firm in Debt Collection

The role of a law firm in debt collection is multifaceted and crucial. Acting as intermediaries, they work to recover outstanding debts for their clients using various strategies. They bring legal expertise, negotiating skills, and litigation capabilities. Law firms start with negotiation and mediation, proposing feasible debtor repayment plans. If these methods fail, they can resort to litigation, filing and seeking court orders. They also have the resources to trace and recover assets and can assist with debt restructuring. By ensuring debts are repaid, protecting the rights of all parties, and providing an efficient recovery process, law firms are invaluable in maintaining the financial health of businesses.

Legal Expertise and Advice

Legal expertise and advice are key offerings of law firms in debt collection. Law firms advise clients on their rights and obligations, ensuring they are well-informed throughout the debt recovery process. By operating within the confines of the law, they protect clients from potential legal issues. Their legal expertise also allows them to leverage specific laws to their client's advantage, making them a valuable asset in debt collection. Law firms' ability to interpret and apply laws accurately ensures a fair, legal, and efficient debt recovery process.

Negotiation and Mediation

Negotiation and mediation are initial strategies law firms employ in debt collection before pursuing legal action. Law firms communicate with debtors to discuss repayment options, often proposing feasible plans that accommodate both the debtor's financial situation and the creditor's expectations. This approach can lead to a win-win solution, avoiding lengthy and costly legal proceedings. Mediation can preserve business relationships and maintain the dignity of all parties involved. Law firms prioritizing negotiation and mediation demonstrate their commitment to finding amicable solutions while ensuring efficient and successful debt recovery.

Litigation

Litigation is a powerful tool that law firms employ when negotiation and mediation efforts prove unsuccessful. In such cases, law firms file lawsuits on behalf of their clients, taking the debt recovery process to court. They provide legal representation, ensuring their clients' interests are protected throughout the court proceedings. Law firms seek court orders to compel debtors to repay their debts, employing various enforcement methods. These may include wage garnishment, where a portion of the debtor's earnings are directed towards debt repayment, freezing bank accounts to prevent further transactions until the debt is settled, or placing liens on properties, effectively securing the debt with the debtor's assets. By resorting to litigation, law firms demonstrate their determination to recover debts, utilizing the full extent of legal measures available.

Asset Tracing and Recovery

Asset tracing and recovery are other crucial services that law firms provide in debt collection. They possess the resources and expertise to delve into a debtor's financial situation, uncovering valuable information to aid in debt recovery. Law firms can locate hidden assets that debtors may have concealed to evade their obligations. By employing legal methods, law firms can recover these assets, ensuring that creditors receive the repayment they are entitled to. This meticulous approach demonstrates law firms' commitment to exhausting all possible avenues for debt recovery, ultimately maximizing their clients' chances of successful repayment. Asset tracing and recovery is a testament to the comprehensive and strategic methods law firms employ in debt collection.

Debt Restructuring

Debt restructuring is a valuable service law firms offer when debtors face significant financial difficulties and cannot repay their debts in full. Law firms step in to negotiate with creditors on the debtor's behalf, aiming to reach a more manageable repayment plan. This could involve reducing the total amount owed or extending the repayment period, providing much-needed relief for the debtor. Debt restructuring benefits both parties by allowing debtors to avoid bankruptcy while enabling creditors to recover at least a portion of the money owed. By offering this service, law firms demonstrate their flexibility and commitment to finding the best possible solutions for all parties involved in the debt collection process. Debt restructuring highlights law firms' adaptability and problem-solving nature, making them indispensable in debt recovery.

The Importance of Law Firms in Debt Collection

The importance of law firms in debt collection cannot be overstated. They play a vital role in preserving the financial well-being of businesses by diligently working to recover outstanding debts. Law firms help businesses maintain a stable cash flow by securing repayment, ensuring their continued growth and success. Furthermore, law firms safeguard the rights of both creditors and debtors throughout the debt collection process. They operate within the confines of the law, guaranteeing fair treatment for all parties involved. This commitment to legality and ethics upholds the integrity of the debt collection industry. Additionally, law firms offer a structured and streamlined approach to debt recovery. In summary, the multifaceted role of law firms in debt collection is essential for maintaining financial stability, upholding legal standards, and providing efficient solutions in the debt recovery process.

" In conclusion, law firms are indispensable partners in the debt collection process, providing services that significantly enhance the recovery of outstanding debts. Their comprehensive legal knowledge, adept negotiation skills, and ability to pursue litigation when required set them apart as highly effective allies for businesses aiming to recoup unpaid amounts. Law firms' proficiency in navigating complex legal landscapes ensures that debt collection activities are conducted fairly, legally, and efficiently.

Moreover, law firms' commitment to exploring various strategies, such as negotiation, mediation, and debt restructuring, demonstrates their adaptability and dedication to achieving the best possible outcomes for their clients. Prioritizing these approaches often prevents the need for lengthy and costly legal proceedings, ultimately saving businesses time and resources.

Understanding the multifaceted role of a law firm in debt collection empowers businesses to make well-informed decisions regarding debt management. This knowledge enables companies to maintain financial health, protect their rights, and preserve valuable business relationships. In an ever-evolving economic landscape, the expertise and support of law firms in debt collection remain an essential component of a business's success and stability. "

1 note

·

View note

Text

Secured vs. Unsecured Debts: Creditors' Rights Explained

If you're a creditor, knowing the difference between secured and unsecured debts is crucial for effective debt recovery. Each type comes with its own set of challenges and legal approaches. This article will help you navigate these waters, improving your success rates and ensuring you are legally protected.

Understanding Secured Debts

Secured debts are those backed by collateral. Common examples include mortgages and auto loans. If a debtor fails to make payments, creditors have the right to repossess the collateral used to secure the loan.

The following is a DRAMATIZATION AND IS NOT AN ACTUAL EVENT: John's auto loan company successfully repossessed the car after several missed payments, quickly recovering a significant portion of the owed sum.

Knowing your rights to repossess can lead to faster recovery of funds, providing a higher level of security for your investments.

Understanding Unsecured Debts

Unsecured debts, like credit card debts and medical bills, do not have collateral. Recovery of these debts relies on legal actions such as lawsuits or wage garnishment.

The following is a DRAMATIZATION AND IS NOT AN ACTUAL EVENT: Lisa, a credit card company representative, facilitated a court order to garnish wages from a delinquent account holder, effectively recovering the outstanding balance.

Mastering the legal process for unsecured debts can enhance your ability to collect, even without collateral.

Legal Tools and Strategies

Secured Debt Recovery

Repossessing property or foreclosing on homes requires adherence to specific legal procedures. Additionally, negotiating payment plans can be a viable strategy to avoid the need for more drastic measures.

Utilizing these legal tools effectively ensures you recover maximum value, reducing potential losses and maintaining good customer relations.

Using a debt collection attorney, well-versed in the Fair Debt Collection Practices Act (FDCPA), ensures compliance with its guidelines while pursuing debt recovery, safeguarding the creditors' rights.

Unsecured Debt Recovery

Unlike secured debts, unsecured debts do not have collateral backing. This category includes debts like credit card balances, medical bills, personal loans, and certain types of retail financing. Since there is no physical asset to reclaim, creditors must rely on legal avenues to recover these funds.

Recovery typically begins with more benign attempts such as sending collection letters, making phone calls, and setting up payment plans. If these initial efforts fail, creditors may escalate to legal actions, which can include:

- Filing a lawsuit: Creditors may take legal action against the debtor. If successful, this can result in a judgment in favor of the creditor.

- Wage garnishment: Upon obtaining a court judgment, creditors might seek to garnish wages, meaning a portion of the debtor's paycheck is directed to the creditor until the debt is paid off.

- Bank levies: Another option following a judgment is to freeze and seize funds from the debtor's bank account.

The following is a DRAMATIZATION AND IS NOT AN ACTUAL EVENT: After repeated failed attempts to collect an outstanding credit card debt, a creditor successfully pursued a court judgment against the debtor, leading to wage garnishment that systematically reduced the balance over several months.

Understanding and effectively utilizing legal tools to enforce unsecured debt collection can significantly improve recovery rates. It is essential for creditors to be familiar with the legal procedures to ensure that they act within the law and optimize their chances of debt recovery.

For unsecured debts, initiating legal proceedings can be necessary. Employing a debt collection agency can also be an effective strategy. Understanding these strategies can lead to more successful debt recovery and reduce the time and resources spent on chasing payments.

Comparing Recovery Rates and Challenges

Recovery rates for secured debts are typically higher than for unsecured debts due to the presence of collateral. However, both types face unique challenges that require tailored strategies. Knowing which type of debt offers better recovery prospects allows you to allocate resources more efficiently and develop more effective recovery strategies.

Conclusion

Understanding the differences between secured and unsecured debts and using the right legal tools can significantly enhance your debt recovery processes. By focusing on effective communication, legal compliance, and strategic planning, you can improve your success rates and minimize legal risks.

Remember, you don't have to navigate these complex issues alone. Our team of experienced creditor's rights attorneys is ready to guide you through every step of the process. Contact us today to learn how we can help you maximize your debt recovery efforts and protect your rights as a creditor.

FAQs

1. What is the main difference between secured and unsecured debts?

Secured debts are backed by collateral, giving creditors the right to repossess the asset if debts are unpaid. Unsecured debts are not backed by collateral, and recovery relies on legal actions such as lawsuits, wage garnishment, or bank levies.

2. How can creditors improve their recovery rates for unsecured debts?

Creditors can improve recovery rates for unsecured debts by employing thorough record-keeping, understanding legal processes, using a debt collection attorney.

3. What legal tools are available for secured debt recovery?

For secured debts, creditors may use repossession and foreclosure as tools for debt recovery. These methods allow creditors to take back the collateral associated with the debt, such as real estate or automobiles.

4. What are effective strategies for creditors to recover owed funds?

To enhance the recovery of owed funds, creditors should employ a combination of effective strategies tailored to the nature of the debt and the debtor's circumstances. Here are some proven methods:

- Early Intervention: Act quickly when payments are missed. Early contact can prevent small issues from becoming bigger problems.

- Diverse Collection Methods: Use a mix of methods tailored to the situation, such as payment reminders, phone calls, restructuring debt, or offering settlement options for quicker resolution.

- Legal Enforcement: If amicable collection efforts fail, consider legal actions such as filing for a lien, pursuing wage garnishment, or obtaining a court judgment to enforce debt repayment.

- Debt Collection Attorney: Engage reputable debt collection attorney when internal efforts are insufficient. They specialize in debt recovery and can navigate the legal landscape effectively.

Implementing these strategies can significantly improve the likelihood of recovering the full amount owed, while also maintaining a professional approach to debt recovery.

By focusing on these strategies, creditors can enhance their chances of successful recoveries while maintaining a positive relationship with debtors, which can lead to more effective long-term debt management and fewer disputes.

Ready to optimize your debt recovery strategy? Dive into our comprehensive guide on navigating secured and unsecured debts to maximize your success rates.

Contact Marcadis Singer PA today at (813) 288-1881 to ensure your creditor rights are protected every step of the way.

Read the full article

0 notes

Text

Unveiling the Scam: Tales of Pig Butchering Fraud Recovery Cases

In recent years, the rise of online scams has affected various industries, and the agricultural sector is no exception. One particularly prevalent scam involves pig butchering, where unsuspecting victims are promised high returns on investment in the pig farming business. However, they ultimately fall victim to fraudulent schemes, losing their hard-earned money. Fortunately, there have been instances where victims have fought back and successfully recovered their losses. In this article, we will explore some inspiring stories of pig butchering scam recovery cases and shed light on the steps taken to seek justice.

The Mastermind Unmasked

In a significant scam recovery case, a dedicated team of investigators was able to unveil the mastermind behind the pig butchering fraud. The victims, who had invested substantial amounts of money into the fraudulent business, collaborated with law enforcement agencies and private investigators to gather evidence. Through extensive research and surveillance, the team successfully identified the scammer, who was operating under multiple aliases. This breakthrough allowed the victims to pursue legal action and work towards recovering their lost funds.

Legal Actions and Asset Seizures

Upon identifying the culprits, the victims initiated legal proceedings to hold them accountable. With the help of experienced lawyers specializing in fraud cases, the victims filed lawsuits and obtained court orders for asset seizures. This crucial step allowed them to freeze the scammers' bank accounts and seize their ill-gotten assets, including luxury vehicles, properties, and expensive equipment. The victims' determination and swift legal action played a vital role in ensuring that the scammers faced the consequences of their fraudulent activities.

Collaborative Efforts

In several pig butchering scam recovery cases, the victims came together and formed support groups to share information and resources. These collaborative efforts helped them gather evidence, identify additional victims, and exchange tips on navigating the legal system. By joining forces, the victims increased their collective strength and bolstered their chances of recovering their losses. Support groups also provided emotional support and a sense of solidarity during a challenging and distressing time.

Public Awareness Campaigns

To prevent others from falling prey to pig butchering scams, recovered victims launched public awareness campaigns to educate individuals about the modus operandi of scammers. Through social media platforms, public forums, and local community engagements, they shared their experiences, warning signs, and red flags to watch out for when considering investments in the agricultural sector. These campaigns helped raise awareness and empowered potential investors to exercise caution and conduct thorough due diligence before investing their money.

Assisting Law Enforcement Agencies

Recovered victims actively collaborated with law enforcement agencies to provide evidence, share insights, and assist in ongoing investigations. By maintaining open lines of communication and providing valuable information, they played a crucial role in helping law enforcement agencies build strong cases against the scammers. This cooperation between the victims and law enforcement agencies not only aided in individual recovery efforts but also contributed to dismantling the criminal networks behind the scams.

Rebuilding Lives and Learning from Experiences

Recovering from the financial and emotional impact of a pig butchering scam is a challenging process. However, many victims showcased resilience and determination to rebuild their lives. Some utilized their recovered funds to invest in legitimate agricultural ventures, while others started small businesses or pursued new career paths. They also emphasized the importance of sharing their experiences to educate others about the risks associated with fraudulent investment schemes. These recovered victims emerged stronger, more informed, and committed to preventing others from falling victim to similar scams.

For More Info:-

Digital currency investigation

Investment scam recovery specialists

Top-rated investment scam recovery firms

Successful pig butchering scam recovery cases

1 note

·

View note

Text

[ad_1]

Economy

How Nigerian techies wired Sh276bn without CBK nod

Friday February 03 2023

Olugbenga Agboola, co-founder and CEO of Flutterwave. FILE PHOTO | POOL

As the world toasted Nigeria’s Olugbenga Agboola as Africa’s freshly minted tech billionaire, Kenyan authorities were investigating his firm for possible money laundering links.It was February last year when a firm he co-founded — Flutterwave — was valued at $3 billion, making it the most valuable start-up in Africa as international investors bet on the continent’s fintech scene.While this made the 37-year-old Agboola one of Africa’s most well-known entrepreneurs, investigators and regulators in Kenya suspected his Nigerian payments company was riding on proceeds of crime, in particular card fraud.In the end, the High Court froze its Sh6.2 billion spread in 62 bank accounts on money laundering fears and the Central Bank of Kenya (CBK) ordered Kenyan banks to immediately cut links with Flutterwave.Flutterwave was one of the three Nigerian fintech that were at the centre of a complex money laundering probe in Kenya, with court records indicating that they wired over Sh276 billion in multiple currencies over four years without the knowledge and license from the CBK.The three, including RemX and Kandon Technologies, were investigated by the Assets Recovery Agency (ARA) on fears of card fraud and money laundering.

ARA reckons that the three firms wired Sh276 billion in foreign currencies in over 100 accounts at Guaranty Trust Bank, Equity, EcoBank, Access Bank and UBA between January 2019 and June last year.By the time local investigators received court orders to freeze the accounts, an estimated Sh262.4 billion had been wired to offshore bank accounts in Dubai, Nigeria and Zambia.Bank statements attached to court documents revealed a cross-continental operation that moved huge sums of dollars to Kenyan banks and wired them to multiple companies registered locally with shared ownership and suspect addresses.So far, Kenyan authorities have withdrawn money laundering suits against Kandon and RemX, which is owned by Nehikhare Eghosasere and Demuren Olufemi.This saw the High Court lift orders to unfreeze Sh5.6 billion belonging to RemX and Sh16 million under Kandon.Read: Kenya freezes Sh6.2bn linked to Nigerian start-up FlutterwaveBut the CBK said the firms were not licensed to operate in Kenya and ordered local banks to block the three Nigerian fintech from their networks amid their strong linkages.Mr Olufemi is co-founder of Venture Garden Group, a venture capital firm operating from Lagos.Venture Garden Group was the first fund to invest in Flutterwave in 2018, underlining the links between the three firms that also exchanged billions of shillings among each other.The cash movements involved the same companies and entities registered in nearly identical names and in some cases owned by the same individuals across different countries, including Kenya, the US, UAE, Nigeria and Ghana.Lagos-based Kandon — which also has a hub on 400-77 King Street West Toronto, Canada —moved an estimated Sh6.7 billion between March 2021 and May last year in UBA Bank. About Sh6.4 billion and Sh28.2 million were held in euros and pounds respectively.RemX received Sh84 billion and wired out Sh78 billion, part of which was used to buy bitcoins at the US crypto exchange Binance and local exchange BitPesa.Kandon told the court last year that the billions were used to settle payments for importers and exporters moving cash across borders.“The company has been established locally to provide bridge financing services intended to address the numerous challenges faced in the SME in terms of mid- to short-term financing; this is in line with the overall ethos across the group of companies in the other jurisdictions where it has a presence,” Pauline Uzoamaka, a Kandon director, said in an affidavit.ARA believed there was a connection between RemX and Flutterwave, citing outsized amounts of money the startups transacted among each other.

Flutterwave sent Sh12.4 billion to RemX between 2020 and 2022.The funds were mostly wired from Flutterwave’s foreign accounts to a RemX fixed account at Equity Bank.

“No supporting documents were provided to justify the transactions, creating suspicions that the accounts were used as conduits for money laundering,” ARA told the court.Preserved fundsKandon received around Sh2.8 billion ($22.5 million) from RemX between February 1 and March 8, 2022 in the period that coincided with ARA investigations, which were later converted to bitcoins.“The source of the preserved funds are from several clients and suppliers serviced by the applicant whose funds are now caught up in baseless application filed by the 1st Respondent,” Ms Uzoamaka said in court papers defending the outsized transaction the startup facilitated.The firm was founded in 2019 by Ayowole Ayodele and Ms Uzoamaka.Between March to May last year, Flutterwave wired to Kandon a total of Sh21 million in tranches of between Sh1.5 million and Sh4 million, all in dollars.In a warning to Flutterwave in July last year, the CBK cautioned the company against engaging in remittance and payment services without a licence.The firm alleged in court documents that it applied for a licence in 2019.“CBK has received information that Flutterwave has been engaging in payment and money remittance services without the requisite authorisation/licence by CBK in contravention of the law,” CBK deputy director Matu Mugo said in a letter to Flutterwave.The three are not listed on the regulator’s website among licensed remittance and payment service providers.Flutterwave, which moved the biggest chunk of the funds at Sh184.9 billion in 62 bank accounts spread across five banks, told the court that they entered into agreements with local lenders and service providers to facilitate the transactions.Read: Payments firm Flutterwave raises Sh28bn for acquisitionsTransactions in dollars hit Sh111 billion ($892.1 million) while it also wired funds in local currency amounting to Sh67.4 billion, euros (Sh5.8 billion) and pounds (Sh681.4 million).“In the interim, while waiting for the issuance of appropriate licenses, the 1st Respondent (Flutterwave) partnered with licensed entities such as Safaricom PLC and commercial banks operating to remit payments on its behalf and receive Visa and Mastercard payments through their electronic payments gateways,” said Flutterwave legal vice-president David Oluranti.A Kenyan financial regulator, who sought anonymity, said the firms breached local laws by operating for years without the CBK nod.“When opening an account with a local bank, as part of the know your customer (KYC), the payment service providers must present a certificate of incorporation, CBK licences and now we have included the list of beneficial owners among other documents. That’s the law,” the regulator said.This is an indictment on the Kenyan banks that did business with the three Nigerian firms.The regulator said the Financial Reporting Centre—the agency that tracks illicit money—and the CBK were not aware of the flow of billions linked to the three Nigerian firms.Flutterwave, founded in 2016, is now the biggest payments start-up on the continent.The Lagos-based company has processed 200 million transactions worth more than $16 billion in 34 African countries.It maintains that claims of financial impropriety in Kenya were “entirely false”.→ [email protected]

[ad_2]

Source link

0 notes

Text

Debt collectors trying to scare you? Get help from the right lawyers

The typical American has $90,460 in debt, according to a research from 2021. According to a recent poll, 47% of Americans have a credit card amount due each month. 70% of them claim they will not be able to pay it off this year.

Despite the fact that debt is so widespread, those who owe money are stigmatised in our culture. People who are in debt sometimes feel too guilty to ask for the assistance they need. People who experience this kind of isolation are more likely to be taken advantage of.

In order to better prepare you for debt collectors' manipulations, we'd like to let you know about some of the most common scare techniques. We'll also let you know what you can do to change it.

Respect Your Rights

The Fair Debt Collection Privacy Act (FDCPA), which protects you against third-party debt collectors that use harassment and other unfair tactics to attempt and collect a debt, has been mentioned several times on this site. Debt buyers or third-party debt collectors are individuals who pursue the debt on behalf of the original creditor. You should be well-informed on what a debt collector is and is not permitted to do before interacting with them.

You can sue a debt collector for damages and attorney costs if they violate your FDCPA rights. An excellent, seasoned debt recovery collection defence lawyer can provide you with information, and many, including Attorney Debt Fighters, charge a fee for the initial session.

Avoid Being Manipulated or Intimidated by Debt Collector Scare Techniques

Even when debt collectors adhere to the law, dealing with them is unpleasant. The more prepared you are, the less likely it is that a meeting with a debt collector would frighten you and cause you to cave in to their demands when you really don't need to.

Threatening Quick Collection Actions That They Cannot Take

Debt collectors frequently use threats of urgent collection action to pressure you into making an immediate payment. For instance, they could insinuate or explicitly say that they can start garnishing your salary right now.

You are not subject to collection proceedings like bank account seizures or wage garnishments until a debt collector takes you to court and wins a judgement against you. Even after receiving a judgement, they must still apply for court permission before beginning any collection efforts.

This entire process takes time. You have some time to reflect and seek assistance from an experienced debt collection defence lawyer.

Getting in your face nonstop

Many folks are already irritated and even terrified when debt collectors call. Since they are aware of this, debt collectors profit from it. The worst debt collectors may contact you throughout the night in an effort to frighten you. Some could even come knocking on your door.

These two strategies constitute unlawful harassment. Federal law only permits debt collectors to contact you between 8 am and 9 pm, which can be a burden in and of itself. A debt collector is only permitted to phone your number a maximum of seven times each week. They might not contact them again for another week after they've really spoken to you on the phone.

Conclusion

You can be informed by a debt collector that you must make a payment by a certain date or the debt will significantly grow owing to additional costs. That is not the situation. Be aware, though, that if you continue to ignore a debt collector for a long enough period of time, the creditor will eventually likely take legal action against you, which could result in additional costs as well as a court ruling giving them the right to pursue actions such as wage garnishment or account freezing.

1 note

·

View note

Text

Meet Merc De Mesel The Man Who Wired Over Sh. 210 Million Nairobi ‘Girlfriends’

Meet Merc De Mesel The Man Who Wired Over Sh. 210 Million Nairobi ‘Girlfriends’

The Assets and Recovery Agency is after Felesta Nyamathira Njoroge. Felesta is a 21-year-old university student with Sh. 102 million in her bank account which she received from a man who alleges to be her boyfriend Merc De Mesel.

The agency says that the money in Nyamathira’s account is proceeds of crime and money laundering.

The agency has moved to court seeking orders to freeze the account of…

View On WordPress

0 notes

Text

Court Freezes Bank Account of 21yr-old student Felesta Nyamathira, worth Sh102m for 3 months to allow investigation

Court Freezes Bank Account of 21yr-old student Felesta Nyamathira, worth Sh102m for 3 months to allow investigation

NAIROBI: A Court has ordered the freezing of Felesta Nyamathira Njoroge, a 21yr-old College Student’s bank account for 90 days to allow the Asset Recovery Agency (ARA) to establish the source of Sh102.5 million in it.

The Anti-Corruption Court judge, Esther Maina ordered that the money, which was banked at Co-operative Bank, be frozen for 90 days to allow Asset Recovery Agency (ARA) establish the…

View On WordPress

0 notes

Text

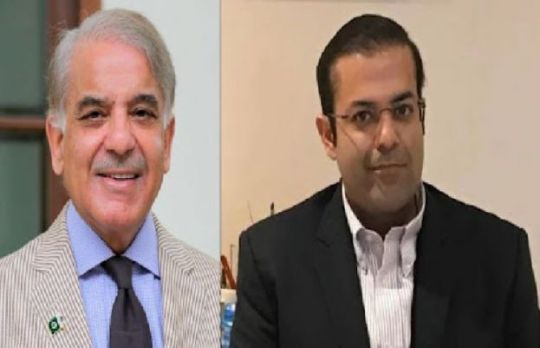

Shahbaz Sharif NCA probe: Govt embarrassing itself, says Shahid Khaqan Abbasi

Former prime minister Shahid Khaqan Abbasi on Tuesday lashed out at the government, saying that it had embarrassed itself in front of the world with the British National Crime Agency (NCA)'s probe against PML-N President Shahbaz Sharif.

In a hard-hitting press conference, flanked by Rana Sanaullah and Ahsan Iqbal, Abbasi said the government's claims that it was not involved or pursuing money laundering cases against Shahbaz had been exposed.

He said that the Assets Recovery Unit (ARU) and, as per the PML-N's sources, even Federal Investigation Agency (FIA) officials, used to go to London to meet NCA officials.

"The standard set by this government, when it comes to lying, is totally unique," he said. "The prime minister of this country, in his own office, creates an Asset Recovery Unit that has no legal basis. And what has that ARU done?" he questioned.

He referred to the papers in his hand, saying that they were official documents submitted by the NCA at the UK court.

Referring to the NCA probe against the PML-N president and his son Suleman, Abbasi said that normally in money laundering cases, financial transactions only six years back were traced.

"In this case, however, the probe stretched to cover financial transactions covering a period of over 20 years," he noted. "This inquiry was also not limited to just one country; it took place in Pakistan, the UK and the UAE."

The former prime minister said that money sent by Shahbaz from Pakistan to his UK bank account was legal money.

He said Shahbaz and Suleman had both given their consent to the NCA to probe their accounts. "Time and again, the NCA told the court that it has the complete support and cooperation of the Pakistani government and its agencies," he said.

Abbasi alleged that DG NAB Lahore, the ARU, FIA and other agencies were involved in framing allegations against the PML-N president. "And now, the prime minister of this country says his government had nothing to do with the probe," he said.

PML-N leader Ahsan Iqbal said that the government could not, till this day, find evidence of former prime ministers Nawaz Sharif and Shahid Khaqan Abbasi's involvement in corruption.

"Each case has slammed shut on their faces," he said, referring to the government. "You could not even prove corruption worth Rs32 in a Rs3,200bn project," he added.

Iqbal said that the government is failing the masses as it is busy registering fake cases against the Opposition. "However, your failure is becoming a matter of life and death for the public," he said.

Iqbal said the government itself was inviting trouble from the Financial Action Task Force (FATF) as the prime minister was repeatedly saying at international forums that political leaders in the country are involved in money laundering.

"This he does only to promote his politics of hatred and revenge," he said.

Shahbaz, Suleman's accounts ordered unfrozen

After 21 months of investigation and review of 20 years of financial affairs, a British court has ordered the unfreezing of the Opposition leader's bank accounts and those belonging to his son, Suleman Sharif.

The decision was taken by the court after UK's top anti-corruption body NCA concluded there was no evidence of money laundering, fraud and criminal conduct against the two, according to evidence seen by The News exclusively.

The Westminster Magistrates Court’s Judge Nicholas Rimmer set aside the two accounts freezing orders (AFO) against Shahbaz Sharif and his son related to a December 2019 case filed by the NCA at the Pakistani government's request.

The bank accounts of Shahbaz Sharif and Suleiman Shahbaz were freezed in December 2019 on court's order. The National Accountability Bureau East Recovery Unit shared the evidence with the British agency.

During the investigation, the accounts of the Shahbaz Sharif and Sharif family in the UK and UAE were investigated.

https://ift.tt/2XVQw0g

0 notes

Text

Secured vs. Unsecured Debts: Creditors' Rights Explained

If you're a creditor, knowing the difference between secured and unsecured debts is crucial for effective debt recovery. Each type comes with its own set of challenges and legal approaches. This article will help you navigate these waters, improving your success rates and ensuring you are legally protected.

Understanding Secured Debts

Secured debts are those backed by collateral. Common examples include mortgages and auto loans. If a debtor fails to make payments, creditors have the right to repossess the collateral used to secure the loan.

The following is a DRAMATIZATION AND IS NOT AN ACTUAL EVENT: John's auto loan company successfully repossessed the car after several missed payments, quickly recovering a significant portion of the owed sum.

Knowing your rights to repossess can lead to faster recovery of funds, providing a higher level of security for your investments.

Understanding Unsecured Debts

Unsecured debts, like credit card debts and medical bills, do not have collateral. Recovery of these debts relies on legal actions such as lawsuits or wage garnishment.

The following is a DRAMATIZATION AND IS NOT AN ACTUAL EVENT: Lisa, a credit card company representative, facilitated a court order to garnish wages from a delinquent account holder, effectively recovering the outstanding balance.

Mastering the legal process for unsecured debts can enhance your ability to collect, even without collateral.

Legal Tools and Strategies

Secured Debt Recovery

Repossessing property or foreclosing on homes requires adherence to specific legal procedures. Additionally, negotiating payment plans can be a viable strategy to avoid the need for more drastic measures.

Utilizing these legal tools effectively ensures you recover maximum value, reducing potential losses and maintaining good customer relations.

Using a debt collection attorney, well-versed in the Fair Debt Collection Practices Act (FDCPA), ensures compliance with its guidelines while pursuing debt recovery, safeguarding the creditors' rights.

Unsecured Debt Recovery

Unlike secured debts, unsecured debts do not have collateral backing. This category includes debts like credit card balances, medical bills, personal loans, and certain types of retail financing. Since there is no physical asset to reclaim, creditors must rely on legal avenues to recover these funds.

Recovery typically begins with more benign attempts such as sending collection letters, making phone calls, and setting up payment plans. If these initial efforts fail, creditors may escalate to legal actions, which can include:

- Filing a lawsuit: Creditors may take legal action against the debtor. If successful, this can result in a judgment in favor of the creditor.

- Wage garnishment: Upon obtaining a court judgment, creditors might seek to garnish wages, meaning a portion of the debtor's paycheck is directed to the creditor until the debt is paid off.

- Bank levies: Another option following a judgment is to freeze and seize funds from the debtor's bank account.

The following is a DRAMATIZATION AND IS NOT AN ACTUAL EVENT: After repeated failed attempts to collect an outstanding credit card debt, a creditor successfully pursued a court judgment against the debtor, leading to wage garnishment that systematically reduced the balance over several months.

Understanding and effectively utilizing legal tools to enforce unsecured debt collection can significantly improve recovery rates. It is essential for creditors to be familiar with the legal procedures to ensure that they act within the law and optimize their chances of debt recovery.

For unsecured debts, initiating legal proceedings can be necessary. Employing a debt collection agency can also be an effective strategy. Understanding these strategies can lead to more successful debt recovery and reduce the time and resources spent on chasing payments.

Comparing Recovery Rates and Challenges

Recovery rates for secured debts are typically higher than for unsecured debts due to the presence of collateral. However, both types face unique challenges that require tailored strategies. Knowing which type of debt offers better recovery prospects allows you to allocate resources more efficiently and develop more effective recovery strategies.

Conclusion

Understanding the differences between secured and unsecured debts and using the right legal tools can significantly enhance your debt recovery processes. By focusing on effective communication, legal compliance, and strategic planning, you can improve your success rates and minimize legal risks.

Remember, you don't have to navigate these complex issues alone. Our team of experienced creditor's rights attorneys is ready to guide you through every step of the process. Contact us today to learn how we can help you maximize your debt recovery efforts and protect your rights as a creditor.

FAQs

1. What is the main difference between secured and unsecured debts?

Secured debts are backed by collateral, giving creditors the right to repossess the asset if debts are unpaid. Unsecured debts are not backed by collateral, and recovery relies on legal actions such as lawsuits, wage garnishment, or bank levies.

2. How can creditors improve their recovery rates for unsecured debts?

Creditors can improve recovery rates for unsecured debts by employing thorough record-keeping, understanding legal processes, using a debt collection attorney.

3. What legal tools are available for secured debt recovery?

For secured debts, creditors may use repossession and foreclosure as tools for debt recovery. These methods allow creditors to take back the collateral associated with the debt, such as real estate or automobiles.

4. What are effective strategies for creditors to recover owed funds?

To enhance the recovery of owed funds, creditors should employ a combination of effective strategies tailored to the nature of the debt and the debtor's circumstances. Here are some proven methods:

- Early Intervention: Act quickly when payments are missed. Early contact can prevent small issues from becoming bigger problems.

- Diverse Collection Methods: Use a mix of methods tailored to the situation, such as payment reminders, phone calls, restructuring debt, or offering settlement options for quicker resolution.

- Legal Enforcement: If amicable collection efforts fail, consider legal actions such as filing for a lien, pursuing wage garnishment, or obtaining a court judgment to enforce debt repayment.

- Debt Collection Attorney: Engage reputable debt collection attorney when internal efforts are insufficient. They specialize in debt recovery and can navigate the legal landscape effectively.

Implementing these strategies can significantly improve the likelihood of recovering the full amount owed, while also maintaining a professional approach to debt recovery.

By focusing on these strategies, creditors can enhance their chances of successful recoveries while maintaining a positive relationship with debtors, which can lead to more effective long-term debt management and fewer disputes.

Ready to optimize your debt recovery strategy? Dive into our comprehensive guide on navigating secured and unsecured debts to maximize your success rates.

Contact Marcadis Singer PA today at (813) 288-1881 to ensure your creditor rights are protected every step of the way.

Read the full article

0 notes

Text

BREAKING:Court freezes bank accounts, shares of Rainoil, 13 Others over N1.6Bn debt

New Post has been published on https://thebiafrastar.com/breakingcourt-freezes-bank-accounts-shares-of-rainoil-13-others-over-n1-6bn-debt/

BREAKING:Court freezes bank accounts, shares of Rainoil, 13 Others over N1.6Bn debt

A Federal High Court in Lagos has requested the freezing of the financial balances and offers having a place with downstream oil and gas organization, Rainoil Limited, and 13 others over a N1.6bn obligation.

(adsbygoogle = window.adsbygoogle || []).push();

The 13 others influenced incorporate David Ogwu, Anthony Ezeh, Clara Rotzler, Vincent Otiono, Vincent Sankey, Victoria Alo, Preye Ogriki, Treasure Afolanyan, Chief Nwagwu, Peter Ololo, Gordons Ejikeme, Joe Idudu and Falcon Securities Ltd.

The Asset Management Company of Nigeria said this in an assertion named, ‘AMCON Seize Assets of Deap Capital Directors over N1.6bn Debt’ on Wednesday, adding that the request to hold onto the resources was given by Justice C.J. Aneke.

AMCON said following the request, it took viable ownership of the seven properties as recorded by the court through its Debt Recovery Agent – Etonye and Etonye.

(adsbygoogle = window.adsbygoogle || []).push();

A portion of the properties incorporate Plots 14, 15, 16 and 17 in Block 1B, Isolo-Ishaga Area, Mushin, Lagos State; Mile 3 Old Isheri Road, Ikeja, Lagos State; Plot 13, Block 65 Magodo Residential Scheme, Lagos State; No. 73, Femi Kila Street, Okota, Isolo, Lagos State; Plot 22, Block 91, Lekki Peninsula Residential Scheme, Lekki Area, Lagos; and Government Land Allocation, Lekki Peninsula Scheme II.

The assertion read, “The court likewise requested the freezing of the Bank Accounts and portions of the organization’s chiefs in particular: David Ogwu, Anthony Ezeh, Clara Rotzler, Vincent Otiono, Vincent Sankey, Victoria Alo, Hon. Preye Ogriki, Treasure Afolanyan, Chief Nwagwu, Peter Ololo, Gordons Ejikeme, Joe Idudu, Falcon Securities Ltd and Rainoil Limited.”

(adsbygoogle = window.adsbygoogle || []).push();

AMCON representative, Jude Nwauzor affirmed that all the property as recorded by the court request had been taken over by AMCON with the help of court bailiffs among different authorities of the law.

On why AMCON needed to sit tight for longer than a month to do the request, Nwauzor said, “It produces a cycle to results these orders. We are an administration organization that is guided by peace, and we should meet all the lawful conditions before any implementation is made. Along these lines, the length of deferral isn’t the issue. The significant thing is to do the request as guided by the law.”

(adsbygoogle = window.adsbygoogle || []).push();

AMCON, which is an obligation recuperation office of the Federal Government, had in July 2020, implemented on properties having a place with the Chief Promoter of the organization, Mr Emmanuel Ugboh, in the wake of offering him concessions and investigating all roads to determine the obligation amicably without much of any result.

(adsbygoogle = window.adsbygoogle || []).push();

In any case, because of the absence of satisfactory security, AMCON needed to start resource following on the Company’s Directors, an activity, which uncovered the seven properties the Corporation has now authorized upon. AMCON’s activity is in accordance with Section 61 of the AMCON Act, 2010 and Section 49 (1) and (2) of the AMCON Act 2019 (as revised).

AMCON bought the Non-Performing Loan of Deap Capital Management and Trust Plc. during the primary period of Eligible Bank Assets buys from Zenith Bank and FCMB in 2011.

0 notes

Photo

AMCON TAKES OVER JIMOH IBRAHIM'S ASSETS OVER N69.4BN DEBT The Asset Management Corporation of Nigeria has taken over 12 assets belonging to the Chairman of Global Fleet Group, Jimoh Ibrahim, and frozen all his accounts over his debt which amounts to N69.4bn. The seizure of the assets is pursuant to an order by Justice R.M. Aikawa of a Federal High Court, in Lagos. AMCON on Wednesday took effective possession of all 12 properties through its Debt Recovery Agent – Pinheiro Legal Partners, which include the following: the building of NICON Investment Limited at Plot 242, Muhammadu Buhari Way, Central Business District, Abuja; NICON Hotels Limited building at Plot 557, Port-Harcourt Crescent, off Gimbiya Street, Abuja and the building of NICON Lekki Limited also at No. 5, Customs Street, Lagos. Other properties include The building of Abuja International Hotels Limited located at No. 3, Hospital Road, Lagos; another Property at Plot 242, Muhammadu Buhari Way, Abuja; the former Allied Bank Building on Mile 2, Oshodi Express Way, Apapa Road, Lagos; Energy House located on No. 94, Awolowo Road, Ikoyi, Lagos; NICON Building at No. 40, Madeira Street, Maitama, Abuja; a Residential Apartment at Road 2, House A14, Victoria Garden City, Lagos; NICON Hotels Building at Plot 3, Road 3, Victoria Garden City, Lagos as well as the NICON Luxury Hotel’s Building, Garki I, FCT, Abuja. In addition to the takeover of the listed properties, the court also ordered the freezing of all accounts belonging to Ibrahim and his companies including Global Fleet Oil & Gas Limited and NICON Investment Limited all of who are defendants in suit No. FHL/L/CL/776/2016 presided over by Justice Aikawa on Wednesday, November 4, 2020. The court also granted AMCON possession overall shares belonging to the embattled Ibrahim and his two companies that are domiciled in Nigerian Re-Insurance Company Plc, NICON Insurance Company Plc, Nigeria Stockbrokers Limited, and NICON Trustees Limited. AMCON’s Spokesman, Jude Nwauzor, said all the assets that are listed by the court and scattered around Abuja and Lagos had been successfully taken over by AMCON with the help of court bailiffs and officers and men https://www.instagram.com/p/CHx4YamA_Ex/?igshid=1k9ueisjh5978

0 notes

Text

BREAKING....CBN WANTS TO BE ABLE TO FREEZE BANK ACCOUNTS LINKED TO SUSPECTED CRIMINALS

The bill will give the CBN new sweeping powers to curb financial fraud and manage distressed banks.

The Central Bank of Nigeria (CBN), yesterday, demanded statutory powers from the Nigerian Senate that will enable it to freeze bank accounts that are linked to criminal suspects.

The apex bank’s director in charge of legal services, Mr. Kofo Salam-Alade, argued this point while appearing before a Senate Committee Hearing for a new Act seeking to replace the Banks and Other Financial Institutions Act (BOFIA) of 2004. The lawmakers have commenced the process of repealing/replacing BOFIA 2004 with the re-enactment of BOFIA 2020. However, a particular omission in the new bill has the CBN worried.

UBA ADS

The details: In his presentation to the lawmakers, Mr. Salam-Alada pointed out that the new BOFIA bill has ‘inadvertently’ omitted a clause that should normally grant the CBN Governor the power to freeze any bank accounts linked to criminals, using of a court order. Note that BOFIA 2004 contained this clause. However, the new bill seeking to re-enact BOFIA does not have it. Interestingly, this new bill has passed its second reading at the senate, meaning that it could soon become law.

Speaking further, Mr. Salam-Alade argued that the clause should be re-introduced into the new BOFIA bill in order not to frustrate the apex bank’s fight against fraud and other financial crimes.

“This omission erodes the powers of the CBN and creates a huge gap in the regulatory and resolution framework. Therefore, we propose that the extant provisions should be reinstated,” Mr. Salam-Alada noted.

GTBank 728 x 90

Creation of Credit Tribunal: The CBN director later called on the lawmakers to consider the creation of a credit tribunal that will have the responsibility of addressing the persistent issue of non-performing loans in the banking sector. Such a tribunal is expected to fast-track the recovery of bank loans and other financial institutions through the enforcement of rights over collaterals. Salam-Alade said:

“As part of measures to address the role of nonperforming loans, we propose the creation of a credit tribunal. The overarching objective is to create an efficient regime for the recovery of eligible loans of banks and other financial institutions and enforcement of rights over collateral securities.

“Several new types of licensed institutions have entered the Nigerian financial services sector since the enactment of the 1991 Act. These include the non-interest banks, credit bureaux, payment system service providers, among others. There is a compelling need to introduce new provisions in the bill to address the unique peculiarities of these institutions.”

Another important point Salam-Alade raised during the hearing was the fact that the CBN’s power to intervene and rescue a failing bank was ‘inadvertently omitted in the new BOFIA bill.

Further Reading attempting to explain this proposed bill.

0 notes

Link

CBN Seeks Power To Freeze Crime Suspects Accounts

The Nigerian Central Bank (CBN) has reached out to the Senate to grant it powers to freeze linked accounts for crime suspects.

The CBN made the appeal Wednesday at a public hearing of the Senate Committee on its bill for a law to repeal the Banks and Other Financial Institutions Act (BOFIA) of 2004 and re-enact the Banks and Other Financial Institutions Act. 2020.

The CBN represented at the hearing by the Director of Legal Services, Mr. Kofo Salam-Alada, proposed to the Senate to restore the powers of the Governor of the CBN "to ask the court for orders to freeze accounts considered to be linked to crimes and other civil offenses " He regretted that this power was omitted from the bill.

The main bank also wants legislation for the Credit Creation Court to address the issue of delinquent loans.

Salam-Alada said: “As part of the measures to address the role of delinquent loans, we propose the creation of a Credit Court. The goal is to create an efficient regime for the recovery of eligible loans from banks and other financial institutions (OFls) and the application of collateral rights. "

The provisions, Salam-Alada said, "must address requirements such as criteria for determining latency, processes for managing funds in inactive accounts, and the procedure for claiming funds from beneficiaries."

current market conditions).

Also addressing the Senate Committee, the Managing Director of the Nigerian Deposit Insurance Corporation (NDIC), Alhaji Ibrahim Umar, said that the bill for a repeal of the BOFI Act and its new enactment by the banking committee, Insurance and other financial institutions was an appropriate step to meet the current challenge facing the economy.

“Since 2004, a lot has happened to the banking sector. Many things have been implemented to make it efficient, many things have been done by introducing new products, agent banking; mobile banking. All this speaks of the need to take a closer look at BOFIA, ”he said.

Going forward, NDIC and CBN, he said, are partners working for an efficient and healthy banking system. "We agree to disagree with CBN on certain issues. The two institutions have come a long way in shared responsibilities, "he said.

In her presentation, the director of the NDIC legal department, Mr. Bellema Taribo, sought the support of the Senate to recognize NDIC along with CBN as co-regulators, since NDIC is already a co-supervisor of banks with CBN.

She asked the Senate for legislation to deal with insider trading in banks. She dismissed the clamor for the appointment of another liquidator for the banks, insisting that the NDIC is the only liquidator of the banks.

She said that the powers of the CBN to intervene in the process of managing a bankrupt bank and the reintegration of a bank in a serious situation and return it to good financial health were omitted in the bill.

This omission that he told the Senate “erodes the powers of the CBN and creates a great breach in the regulatory and resolution framework. Therefore, we propose that the existing provisions be reinstated. "

On the administration of inactive accounts in deposit banks (DMB), the CBN is calling for the "inclusion of provisions to improve the administration of inactive accounts in the Nigerian banking sector".

According to him, “NDIC is the only liquidator of banks. The question of naming another liquidator should never arise. We have to see that in the BOFI Law enacted. ”

Earlier in his opening remarks, Senate President Ahmed Lawan, who was represented by Deputy Senate Leader Robert Ajayi Boroffice, assured stakeholders at the hearing that their contributions will not only be absorbed but will form the main ingredients which will be used to produce the new laws.

For his part, the chairman of the Senate Committee on Banking, Insurance and other financial institutions, Uba Sani, said the bills were critical to the economic stabilization of the economy. He said the BOFIA review had been long overdue, adding that it will avoid future banking problems and address severe practices.

Also speaking, BOFIA cosponsor Betty Apiafi said the value of financial technology will be reflected in the bill as it will help reduce NPLs. "It will also help the watch list of chronic defaulters who are responsible for the NPLs. It is a big problem for financial institutions, "she said.

0 notes

Text

Court Freezes Bank Account of 21yr-old student Felesta Nyamathira, worth Sh102m for 3 months to allow investigation

Court Freezes Bank Account of 21yr-old student Felesta Nyamathira, worth Sh102m for 3 months to allow investigation

NAIROBI: A Court has ordered the freezing of Felesta Nyamathira Njoroge, a 21yr-old College Student’s bank account for 90 days to allow the Asset Recovery Agency (ARA) to establish the source of Sh102.5 million in it.

The Anti-Corruption Court judge, Esther Maina ordered that the money, which was banked at Co-operative Bank, be frozen for 90 days to allow Asset Recovery Agency (ARA) establish the…

View On WordPress

0 notes

Text

British court issues orders to unfreeze Shahbaz Sharif, son's bank accounts

In a major relief for PML-N President Shahbaz Sharif, a British court has ordered the unfreezing of the Opposition leader's bank accounts and those belonging to his son, Suleman Sharif Monday.

The decision was taken by the court after the UK's top anti-corruption body, the National Crime Agency (NCA) concluded there was no evidence of money laundering, fraud and criminal conduct against the two, according to evidence seen by The News exclusively.

The Westminster Magistrates Court’s Judge Nicholas Rimmer set aside the two accounts freezing orders (AFO) against Shahbaz Sharif and his son related to a December 2019 case filed by the NCA at the Pakistani government's request.

The UK's top anti-corruption agency filed a unilateral application before Judge Rimmer to declare that its two-year high-profile investigation in the jurisdictions of Pakistan, UK and Dubai found no evidence of money laundering and criminal conduct on part of the two Sharifs who were investigated.

Documents obtained by The News reveal that the bank accounts of Suleman Sharif were frozen and Shahbaz Sharif’s accounts were probed through a December 17, 2019 court order and both were subjected to high-profile criminal forensic investigation under the Proceeds of Crime Act 2002 (POCA), conducted by the NCA’s Investigations Command at the International Corruption Unit.

Their accounts were frozen after the Pakistan government asked the UK to “assist in the recovery of criminal assets to the state of Pakistan”, triggering a wide-ranging investigation.

NCA probes Shahbaz. Suleman's accounts

After the Westminster Magistrates Court allowed the accounts to be freezed and issued a probe consent to the NCA on December 19, 2019, Suleman Sharif’s declared Barclays account, Shahbaz Sharif’s HBL UK and Barclays account were immediately probed, seized and monies frozen.

This correspondent has seen court evidence which shows that the NCA’s investigators sought consent from Shahbaz Sharif to have access to his closed Barclays account as well or else the account will be accessed through a production order. Shahbaz Sharif agreed to the consent on the advice of his lawyers.

Usually, anti-money laundering investigations go back only six years, but in this case, the NCA used its excessive powers and investigated Shahbaz Sharif and his son's transactions dating back to around 20 years. NCA's investigators started the probe from the first flat that Shahbaz Sharif bought in 2004 on Edgware Road when he was in exile and asked him to produce evidence of the clean origin of the money, including mortgage payments, sources of proceeds in his accounts, salaries and dividends, and full proceeds of the property purchase in the UK, bought during exile.

The NCA investigated Suleman Sharif’s Barclays account declared in Pakistan with the Federal Board of Revenue (FBR) and looked into all transfers which were made from Pakistan after the State Bank of Pakistan’s approval. The NCA went through each receipt of transfers from the official money exchangers.

The court documents obtained by this correspondent from credible sources show that the NCA received a letter from the ARU on December 11, 2019, in which it levelled allegations of criminal conduct against Shahbaz Sharif and Suleman Sharif.

The government of Pakistan had requested the UK government to seize all assets and funds of Shahbaz Sharif and his family, and asked them to return the same to Pakistan and extradite Suleman Shehbaz with his family.

The Home Office was in the loop and a separate letter was sent to the Home Office requesting Suleman's extradition, as well as asking Her Majesty’s Revenue and Customs (HMRC) ministry to probe Suleman.

Court papers show that two AFOs were issued by the Westminster Magistrates Court on December 17 for 12 months in case numbers 011902628734 and 011902628947.

A year later, on December 8, 2020, the NCA went to the court again, applying to extend both AFOs for six months, arguing that investigations were continuing in the UK, Dubai and Pakistan. According to court papers, Suleman Shehbaz agreed to the extension of the AFOs by the court on three applications filed by the NCA.

No evidence of money laundering or fraud

On September 10, 2021, the NCA submitted a unilateral application to the court informing that its investigations had been completed and the NCA crime investigators had found no evidence of money-laundering, fraud or wrongdoings in any of the transactions made either from Pakistan to the UK or from the UK to Pakistan in Suleman and Shahbaz Sharif's accounts.

District Judge Nicholas Rimmer signed the final order setting aside the AFOs, releasing and returning the accounts and monies to Suleman Shehbaz and his father.

According to a chronological order of the sensitive investigation - kept under tight wraps by the Sharifs, the NCA and the Pakistan government - a senior director of the NCA’s International Corruption Unit met Shehzad Saleem, Director General of NAB Lahore, in London on December 9, 2019 to discuss the formal investigation against Shahbaz and Suleman Sharif.

According to court papers, Shehzad Saleem explained to the NCA that Shehbaz Sharif’s wealth began to accumulate when he and his brother Nawaz Sharif gained prominence in the 1980s. The implication being that they were receiving bribes and other kickbacks because of their influential position.

The NAB Lahore official told the NCA official during their Central London meeting that Sharifs’ used the hawala system to transfer monies to make them clean and to legalise such transactions. He told the NCA that NAB’s investigation had identified a large number of remittances to bank accounts of the family, allegedly from Pakistanis living abroad.

It is therefore the NAB’s case, he told the NCA, and that the remittances are the laundering of illicit funds by, or on behalf of, Shahbaz Sharif and family, according to court papers.

The ARU's letter

This correspondent has reviewed the letter of December 11, 2019 from the ARU to the NCA explaining why Shahbaz and Suleman Sharif should be investigated and what action should be taken. The ARU told the NCA that Shehbaz was wanted in Pakistan, under investigation, on bail, and a person of interest for misuse of authority during his tenure as chief minister Punjab, namely in his involvement in the Ashiana Housing scheme case and Hamza Sugar Mills case.

The Assets Recovery Unit (ARU) said in the same letter that Suleman was the “principal accused and beneficiary of the fake international remittances and money laundering through front and paper companies”. The Pakistani government's letter to the UK’s anti-corruption agency alleged that its investigation revealed that Shahbaz Sharif and Suleman “patronised a local network of front companies in the name of their low paid employees to launder their proceeds of corruption to show as legitimate money” and that both had “used informal money transfers (hawala) to shift and conceal their money abroad”.

The Pakistan government further told the NCA that the Panamagate investigations had “already culminated in sentences to Nawaz Sharif, Maryam Nawaz Sharif and others from the accountability court and these cases are presently pending with the Islamabad High Court in the appellate's jurisdiction.

It mentioned that investigations by NAB are presently underway for “corruption and organised money laundering” in relation to various members of the Sharif family, including Nawaz Sharif, Maryam Nawaz, Hamza Sharif, Shahbaz Sharif, Ishaq Dar, Nusrat Shahbaz, Suleman Sharif and mainly family members of Shahbaz Sharif for “money laundering “through companies owned by Shahbaz’s family members.

This correspondent has seen the full file which the NCA placed before the Westminster Magistrates Court in order to get the freezing orders (AFOs) issued against Shahbaz Sharif and Suleman. The NCA bundle went into detail to describe Shahbaz and his son as being allegedly involved in criminal conduct through misuse of authority and associated money laundering.

t relied on several newspaper clippings which carried allegations of money laundering, quoting Pakistan government ministers and their press conferences.

Attached in the bundle was also an article by David Rose for the Daily Mail which had been published on July 13, 2019 in which the paper alleged that Shahbaz had stolen the UK government funds.

The article carried the same allegations of money laundering that the ARU later on submitted before the NCA, asking the UK to rely on the article for its investigations.

The NCA gained AFOs and probe consent order for violations contrary to sections 327, 328 and 329 of the Proceeds of Crime Act 2002, involving criminal offending contrary to conspiracy to commit misconduct in a public office and conspiracy to cheat the public revenue; concealing criminal property; acquisition of criminal property; use and possessions of criminal property; and fraud by false representation and fraud by abuse of position.

No case for 'recoverable property', says NCA

The NCA lawyers, requesting freezing orders for 12 months, added: "This will ultimately allow us to prove or disprove if these funds in whole or part, constitute recoverable property in that they are derived from criminal conduct or intended for use in unlawful conduct."

The NCA application, quoting the allegations made by the ARU, said that it needed 12 months because it will conduct enquiries internationally.

Credible legal sources here shared that the grounds of suspicion on which the NCA filed its application in the Westminster Magistrates Court to secure freezing orders were not proven as the investigations in multiple jurisdictions couldn’t establish evidence to prove money-laundering and criminal conduct.

That is the sole reason, according to sources, why the NCA gave it in writing to the Westminster Magistrates Court that its investigations had established that there was no case for the “recoverable property”, hence the unfreezing of assets and closure of the case file.

Reports of Shahbaz being acquirred incorrect, says Shahzad Akbar

Meanwhile, Adviser to the Prime Minister on Accountability Shahzad Akbar said that reports of Shahbaz Sharif being acquitted by the British court were incorrect, clarifying that neither had the ARU nor NAB requested the UK government to initiate a probe against the PML-N leader.

He said the inquiry had been initiated over a "suspicious transaction" that a bank had reported to the NCA, adding that these consisted of certain funds transferred by Suleman Shahbaz from Pakistan to the UK in 2019.

"[These transactions] were declared as a suspicious transaction by the UK authorities and the NCA secured an asset freezing order(AFO) from the court against these funds," he tweeted. "However, recently the NCA decided to stop investigating these funds and therefore agreed for the release of these funds through the court.

"It is clarified that such a release order is not an acknowledgement that funds are from a legitimate source," he added. The prime minister'a aide said that Shahbaz and Suleman have not been acquitted since they had not been tried to begin with.

"The funds were frozen by the NCA and the NCA has decided to not investigate these funds anymore," he added. "Suleman Shahbaz remains a fugitive in a money laundering case against him and his father before the AC Lahore," he added.

PMLN Secretary Information Marriyum Aurangzeb said the UK court decision has unequivocally exonerated Shehbaz Sharif and his family of all malicious and vexatious claims of corruption and money laundering.

Responding to Shahzad Akbar’s tweet, she said the NCA UK conducted a 21-month global investigation spanning 20 years whilst overcoming unprecedented jurisdictional challenges.

She said never in the history of Pakistan has a public office holder ever been subjected to global scrutiny and multi-jurisdictional probing as Shahbaz Sharif had been.

Marriyum said the government's false corruption narrative was exposed, adding that it was telling a hundred more lies to cover up thousands that it had already told.

She said the government will fall on the weight of its own deceit and lies.

https://ift.tt/3m4G2Ek

0 notes

Text

How banks fell victim to their own greed for handsome returns

How banks fell victim to their own greed for handsome returns

How banks fell victim to their own greed for handsome returns

By OTIATO GUGUYU

IN SUMMARY

A huge number of people who took out real estate loans have defaulted, with lenders forced to plead with them on how the money will be repaid.

Nothing describes frustration than the tale of a banker who has to plead with his customer to choose their own terms on how they will repay a loan they have already defaulted on.

The shoe is usually on the other foot, with an overbearing lender deciding on how long you will stay with their money, what rate you will pay and setting up painful repercussions for missing payments that should whip you into line.

The famous quote, “If you owe the bank $100, that's your problem. If you owe the bank $100 million, that’s the bank’s problem”, holds true until you are in Kenya in 2020.

Almost everyone who took out a real estate loan is defaulting, becoming the banks’ problem.

Bankers are unable to sell property on the auction market and have now been forced to renegotiate loans on their customers’ terms. A keen observer will have noticed that auctioneers are finding it hard to dispose of property, with the same assets appearing week after week in the papers.

“Customers discovered that banks cannot sell the properties and when banks approach them they tell them to go ahead and sell,” said Eric Oluoch, group CEO at debt management firm Quest.

“Banks realised they will find themselves holding a huge portfolio of property that cannot be disposed of and that is when they came up with this new plan. I think what we are going to have is that the terms of the mortgages are going to be longer,” he said.

Economist Robert Shaw says he does not pity banks for falling into this quagmire. He said lenders fuelled this unstainable system and are victims of their own practices.

“It is not just a question of customers, banks also made lending decisions without being aware of the circumstances of the market. Banks must bear in mind that the relationship with a customer is two way, they should look at themselves and see that maybe there is a different way,” he said.

Mr Oluoch, says this is a build-up from when bankers never used to lend to people without property until Barclays started offering unsecured loans.

This ushered in a period where loans could be issued on the strength of a payslip, a balance sheet or even a history of banking transactions, liberalising the market and causing a credit boom.

HOUSING BOOM

During this period of plenty, a housing boom was created in the market funded partly by a thin mortgage sector but mostly unexplained cash.

These houses were then used to take up more loans to build more for a seemingly insatiable market for office space and high-end properties in the Rundas and Kilimanis.

“At the time, a lot of people were putting up houses, which fuelled a situation of speculation in the real estate sector with superficial demand and crazy prices. You could go to an empty plot kilometres away from Nairobi and because a university had promised to build there or a road would be built there later, prices would go up,” Oluoch said.

“Banks were giving loans on properties with crazy values,” he said.

But when the rate cap was introduced, suddenly banks became defensive, stopped lending to risky businesses and concentrated on those with property, starving the rest of the economy of much needed cash to keep up the demand.

Then the economy took a dip with government delaying payments to suppliers and cutting down expenditure on large-scale infrastructure.

DOMINO EFFECT

The domino effect hit businesses denied loans by banks and starved of cashflows by government, leading to losses in wider sectors of the economy.

As a reaction, businesses themselves started firing workers to cut costs, sending home thousands of employees, and demand for houses vanished.

People stopped servicing their loans and banks started foreclosures, repossessing houses and selling them via auction.

“With no disposable income, it became a case of whether you will eat and pay school fees or service a loan, it was a no-brainer,” Oluoch said.

The problem was that those who sit at auctions are looking for a bargain and would not pay those crazy values the market boom had created.

But repricing was almost impossible given the consumer protection laws stopping banks from selling distressed properties for peanuts, requiring them to get as much value as possible.

Section 97 of the Land Act 2012 requires banks to exercise duty of care on reposed properties and empowers defaulters to sue if their assets are sold off cheaply.

It came up after several cases of collusion had seen properties sold off for a song then banks would audaciously demand more money from auctioned clients to top up the difference.

“The problem is that nobody is offering 75 per cent so we keep advertising, but we are not selling. So someone is sitting on money, but can’t buy because the price is up,” said NCBA Group Managing Director John Gachora.

How banks fell victim to their own greed for handsome returns

MAKES NO SENSE

Houses that were selling for Sh25 million in Kilimani two or three years ago are going for Sh13 million and that is by their owners not the banks.

Deepak Dave of Riverside Advisors said the costs and agitation involved with repossession only to then find you are still in loss makes no sense.

According to bankers who have talked to Smart Company, they are now forced to go back to the property owners to renegotiate terms.

“The customer shows you this are my Local Purchasing Orders, and he has not been paid, at that point what can you do, we just sit with them and say look, let us see what arrangement we can have rather than auctioning,” a local banker, who did not wish to be named, told Smart Company.

National Bank of Kenya CEO Paul Russo says the first option of dealing with defaulters is not to auction but rather try and sit with them to find an amicable solution.

“There are those willing to come to the table, those we are going after their security and those who we are pursuing over and above through courts. You can’t rule out that there are people who take loans with no intention of repaying,” Russo said.

Deepak said the strategy only makes sense if the restructuring is done with enough cost attached or a recovery-dependent cash sweep that means the developer is not getting a gift.

He said that he hoped the Central Bank of Kenya is keeping an eye on what is being signed off at the banks

“I think what is happening is the defaulting developers are likely getting a gift. If the market recovers, then their debt looks less expensive. If it stays weak, then the lender is carrying the cost of waiting, not the developer,” he said.

There is fear that we may have blown a real estate balloon like the 2008 financial crisis and the reason it has not burst is this accounting trick.

Deepak said that fake restructuring is not repricing housing, it is falsely padding bank capital. Sooner or later this freezes working capital and capex in the economy, hurting the wananchi most of all as demand falls.

“The 2008 crisis did not affect us so much because we were not credit intense but now we have fintechs lending, banks setting up fintechs to lend and people are credit driven. Unfortunately for us it is driven by consumption rather than creating cash-flow. The government needs to find a way to pump money into the economy so that money starts flowing and hopefully people can start paying,” said Oluoch.

STOPPED LENDING

To survive, banks have stopped lending to real estate projects a trend that has seen mortgage banks chase mobile loans and retail banking rather than touch real estate.

“The prolonged troubles in the real estate sector, and the economy at large, have weakened banking asset quality. Based on banks internal models and expectations of the economic environment, this potentially leads to increased provisioning levels and write offs. Cautious lending by banks, in turn, leads to economic constraints as PSCG is subdued,” said Patrick Mumu, a research analyst Genghis Capital Ltd.