#Construction Chemicals Market Analysis

Text

#Construction Chemicals Market#Construction Chemicals Market size#Construction Chemicals Market share#Construction Chemicals Market trends#Construction Chemicals Market analysis#Construction Chemicals Market forecast#Construction Chemicals Market outlook#Construction Chemicals Market overview

0 notes

Text

SPECIALTY CHEMICALS MARKET - GLOBAL OUTLOOK AND FORECAST 2024-2029

The global specialty chemicals market size was valued at USD 800 billion in 2023 and is expected to reach USD 1.04 trillion by 2029, growing at a CAGR of 4.48% during the forecast period. The market is witnessing increased demand from cosmetics, automotive, packaging, and pharmaceutical industries. The demand for specialty chemicals for such markets has grown in countries such as China, Germany, Japan, and India, among others, due to the booming automotive, pharmaceutical, cosmetics, and candle industries. Specialty chemicals are essential to various manufacturing processes and are used as materials required for construction, oil and gas refining, and food preservation, among many others. Due to China’s improving manufacturing sector, Asia Pacific has been a dominant region as China and India are leading in manufacturing and exporting specialty chemicals. Though the U.S. still manufactures a significant amount to have a significant market share, European countries steadily increased their market share, which could indirectly affect the North American market.

MARKET TRENDS & DRIVERS

Increasing Demand for Green Chemistry

Sustainability and green chemistry are becoming among the most common practices in the global specialty chemicals market. This trend has led to innovation, efficiency, and responsibility in product development, manufacturing, and operations. Green chemistry has become significant due to the environmental challenges and to ensure a sustainable future. One of the aspects of green chemistry includes renewable feedstocks. The manufacturers of specialty chemicals are shifting towards renewable feedstocks derived from biomass, such as plant oils, agricultural residues, and algae, which are alternatives to fossil-based raw materials. For example, Solazyme, now known as TerraVia, developed a process to produce specialty oils and ingredients from microalgae, offering sustainable alternatives to traditional oils in cosmetics, personal care products, and nutrition supplements. Further, bio-based polymers are alternatives to petroleum-based plastics. For example, NatureWorks has developed bio-based polymers, such as Ingeo™ PLA (polylactic acid), which can be used in packaging, textiles, and personal care products. These polymers are biodegradable and compostable, reducing environmental impact at end-of-life.

SEGMENTATION INSIGHTS

INSIGHTS BY APPLICATION TYPEThe agrochemicals application type segment holds the most significant global specialty chemicals market share. Various specialty chemicals are used across the agricultural sector as these products help enhance the soil quality and control diseases, weeds, and other insects that might affect the growth and quality of the crop. Specialty chemicals in pesticides include insecticides used for controlling insects, herbicides for controlling weeds, fungicides used for controlling fungal diseases, and bactericides used for controlling bacterial diseases. With the demand for food increasing continuously across the globe, fertilizers and pesticides, which use many of these specialty chemicals, will have a higher market demand.

Furthermore, performance chemicals are specialty chemicals designed and formulated to meet specific performance requirements across various industrial and consumer applications. Performance chemicals are customized to enhance functionality, efficiency, and value for specific applications. They are used in various applications, such as detergents, personal care products, paints, and agrochemical formulations. Also, specialty chemicals in the construction industry are essential as they enhance building materials, construction processes, and overall infrastructure durability. Advancements in construction techniques and materials have enabled specialty chemicals to empower engineers and architects to design and build structures that meet stringent performance standards while minimizing environmental impact.

COMPETITIVE LANDSCAPE

The global specialty chemicals market is characterized by low market concentration, with high competition among the players. The present scenario drives vendors to alter and refine their unique value proposition to achieve a strong market presence. Currently, the specialty chemicals market is moderately fragmented and dominated by vendors. All these major vendors have a global presence in three major geographical regions: North America, APAC, and Europe. Further, there is intense competition in the market as players compete to gain market share. Due to the intensely competitive landscape, the specialty chemicals market will likely witness increased consolidation. These factors make it imperative for vendors to distinguish their products and service offerings through a clear and unique value proposition. Otherwise, they will not survive in a highly competitive environment. In addition, they must develop high functionalities and continue upgrading their products to keep pace with the latest technological developments, failing which they might lose relevance in the market.

#market#market research#market report#data center#industry insights#market research report#industry analysis#industry data#speciality chemicals#Agrochemicals#Performance Chemicals#Construction Chemicals#Home & Personal Care#Electronic Chemicals

0 notes

Text

The Flat Steel Market: Emerging Markets and Their Rising Influence

In the intricate web of the global steel industry, flat steel market stands out for its critical role in various sectors, including automotive, construction, and machinery. This versatility stems from its manufacturing process—steel is rolled into sheets or plates, producing products that are integral to our daily lives, from cars to skyscrapers.

As the world's economies evolve, the demand for flat steel is significantly influenced by emerging markets. These regions, through rapid urbanization, industrialization, and extensive infrastructure projects, are becoming pivotal in shaping the global flat steel landscape.

Download FREE Sample: https://www.nextmsc.com/flat-steel-market/request-sample

The Rising Tide of Emerging Markets

Emerging markets, with their dynamic economies, are at the forefront of boosting global flat steel demand. Countries such as China, India, Brazil, and Russia are not just large consumers of flat steel but also key players in its production. The demand in these economies is propelled by several factors, all of which interlink to create a robust appetite for flat steel.

Urbanization: A Catalyst for Change

Urbanization is a primary driver of flat steel demand in emerging markets. As populations migrate to cities in search of better opportunities, the need for urban infrastructure—from residential buildings to commercial spaces—witnesses a significant upswing. This urban expansion necessitates vast quantities of flat steel for construction purposes, not just for the buildings themselves but also for the infrastructure that supports urban life, including bridges, public transport networks, and utilities.

Industrialization: Fueling Demand

Parallel to urbanization, industrialization plays a crucial role in escalating the demand for flat steel. Emerging markets are rapidly transforming their economies, shifting from agriculture-based to industrial powerhouses. This transition involves the establishment and expansion of industries ranging from automotive to consumer goods, all of which rely heavily on flat steel. The automotive sector, in particular, is a significant consumer of flat steel, used in everything from chassis to body panels.

Infrastructure Development: The Backbone of Growth

Infrastructure development projects are pivotal in emerging markets, serving as the backbone for economic growth. These projects, which include transportation networks, energy plants, and water systems, require substantial amounts of flat steel. The Belt and Road Initiative by China is a prime example, aiming to enhance regional connectivity and embrace economic development on a trans-continental scale, thereby elevating the demand for flat steel to new heights.

Challenges and Opportunities

While the trajectory for flat steel demand in emerging markets appears promising, it is not without its challenges. Volatility in raw material prices, environmental concerns, and the need for sustainable production methods are pressing issues. Moreover, the global trade environment, influenced by tariffs and trade agreements, can impact the flow of flat steel between nations, affecting availability and prices.

However, these challenges also present opportunities for innovation and growth. The push towards sustainability is driving advancements in steel production technologies, making processes more efficient and environmentally friendly. Furthermore, recycling of steel, a key aspect of the industry, contributes to sustainable development goals, offering a pathway to a more circular economy.

Inquire before Purchase: https://www.nextmsc.com/flat-steel-market/inquire-before-buying

The Future of Flat Steel in Emerging Markets

Looking ahead, the demand for flat steel in emerging markets is set to continue its upward trajectory. Urbanization and industrialization trends show no signs of slowing down, underpinning the sustained need for flat steel. Moreover, as these economies grow, their capacity to innovate and adopt more sustainable practices will likely improve, ensuring that the demand for flat steel is met in more environmentally friendly ways.

The influence of emerging markets on the global flat steel industry is profound and multifaceted. As these regions continue to develop, their impact on the demand, production, and innovation in the flat steel sector will undoubtedly grow stronger. Stakeholders across the value chain, from producers to end-users, need to closely monitor these trends and adapt to the evolving landscape. The future of flat steel is not just about meeting demand but doing so in a way that is sustainable, efficient, and aligned with global economic and environmental goals.

In conclusion, the flat steel market is at a critical juncture, with emerging markets playing a pivotal role in shaping its future. The interplay of urbanization, industrialization, and infrastructure development in these regions creates a robust demand for flat steel, offering both challenges and opportunities. As the industry navigates this landscape, the focus will increasingly be on not just how much flat steel we produce, but how we produce it, ensuring that the growth in demand is matched with advancements in sustainability and efficiency. The journey ahead for the flat steel market is as promising as it is challenging, with emerging markets at its heart, steering the course towards a more integrated and sustainable future.

#flat steel market#construction#materials and chemicals#chemical innovations#industry insights#steel#global market#market trends#analysis

0 notes

Text

#Vietnam Construction Chemicals Market#Market Size#Market Share#Market Trends#Market Analysis#Industry Survey#Market Demand#Top Major Key Player#Market Estimate#Market Segments#Industry Data

0 notes

Text

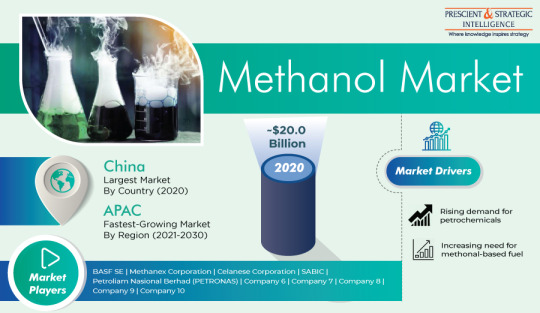

Global Methanol Market: Industry Analysis, Trends, and Growth Forecast

Methanol is a compound that is used as an alternative fuel. It is also known as wood alcohol. The properties of methanol are similar to the chemical and physical properties of ethanol. Methanol is produced by steam-reforming natural gas for producing synthesis gas. The addition of this gas into a reactor in the presence of a catalyst causes water vapor and methanol. Natural gas is preferred over…

View On WordPress

#applications#Automotive#chemical synthesis#chemicals#Competitive Landscape#Construction#emerging opportunities#fuel blending#growth forecast#industry analysis#industry collaborations#Key players#Market dynamics#market size#market trends#Methanol market#regional analysis#solvent#technological advancements#trends

0 notes

Text

Construction Chemicals Market 2022: Top Manufacturers, Production Analysis and Growth Rate Through 2030

Construction Chemicals Market is projected to be worth USD 37.55 billion by 2030, registering a CAGR of 8.60% during the forecast period 2021 - 2030

The growth of the global demand for building chemicals is powered mainly by growing investment in infrastructure development and residential construction activities worldwide. These chemicals are rapidly being used to enhance concrete performance, along with growing industry knowledge of the consistency of concrete, cement, asphalt, and other building materials. Growing urbanization and rapid population development worldwide push the development of residential projects and houses, and construction activity in both new construction and renovation and refurbishment is projected to increase over the forecast period. This, in fact, is expected to raise demand for building chemicals over the projected period.

Development is also driven by expanded spending in the Sector of Infrastructure. In addition, the government is spending heavily in infrastructure construction across the developed world to accelerate economic growth. The growing adoption of ready-mix concrete is expected to further propel the demand for construction chemicals, especially in the commercial and infrastructure sectors.

The absence of customer knowledge of chemical and building aids and lower profit margins are the factors that are projected to hinder the development of the global chemical construction market.

Market Segmentation

The global construction chemicals market, by product type, has been segmented into concrete admixtures, waterproof chemicals, flooring compounds, adhesives and sealants, and others.

By end-use, the global demand for building chemicals was segmented into domestic, commercial, manufacturing, and utilities. Owing to the growing population and urbanization, infrastructure will be the first choice for potential applicants, which would fuel the need for sustainable infrastructure and environmentally friendly goods. The residential sector is the second most lucrative category for new entrants in the demand for construction chemicals. In 2021, this sector was the biggest sales producer, representing almost half of the global industry. Leading to the rising in demand for houses and residences in urban areas, construction chemicals are commonly used in residential infrastructure.

Regional Overview

Asia-Pacific is projected to be the region's biggest and most profitable building chemicals market. Growing developments in urban construction accelerated industrialization and the rising amount of new residential building ventures are due to the fast growth of the regional sector. China is projected to be Asia-Pacific's largest market while India, led by ASEAN countries, is projected to be the fastest-growing market over the forecast period. To satisfy the rising demand for building chemicals in the country, the leading players are investing in rising their production capacity in the country.

Another prominent market for construction chemicals is expected to be in North America. Growth in the region is supported by the rebuilding of the US construction industry. As rapidly increasing urbanization needs the development of residential towers, North America has an enormous capacity for construction products, and buildings are in high demand in response to perennial urbanization worldwide. In order to offer increased structural stability and durability, building companies undertake relatively greater numbers of residential developments using high-grade construction materials.

During the review period, the European market is expected to see steady expansion. Due to economic growth and increased spending in infrastructure production, Latin America and the Near East & Africa are projected to have substantial demand for construction chemicals during the forecast period.

Access Full Report: https://www.marketresearchfuture.com/reports/construction-chemicals-market-1960

Competitive Dashboard

Some of the eminent players operating in the global construction chemicals market are LATICRETE International, Inc (US), BASF SE (Germany), Pidilite Industries Ltd (India), Tata Chemicals (India), Sika AG (Switzerland), Fosroc, Inc. (India), Henkel AG (Germany), Apple Chemie India Pvt. Ltd (India), Croda International Plc (UK), W. R. Grace & Company (US), RPM International, Inc (US), Evonik Industries AG (Germany), Huntsman International LLC (US), Dow (US), and Chemax Chemical (India).

Contact:

Market Research Future®

99 Hudson Street,5Th Floor

New York, New York 10013

United States of America

Phone:

+1 628 258 0071(US)

+44 2035 002 764(UK)

Email: [email protected]

Website: https://www.marketresearchfuture.com

#Construction Chemical Industry research#Construction Chemical Market Size#Construction Chemical Market Share#Construction Chemical Market Regional Analysis

0 notes

Text

Firefighting Foam Market is Estimated To Witness High Growth Owing To Stringent Safety Regulations

The global Firefighting Foam Market is estimated to be valued at US$ 7.31 billion in 2023 and is expected to exhibit a CAGR of 5.9% over the forecast period 2023-2030, as highlighted in a new report published by Coherent Market Insights. Market Overview: Firefighting foam is a specialized product used for extinguishing flammable liquid fires. It is highly effective in suppressing fires by forming a thick blanket over the fire, thus preventing oxygen from reaching the fuel and cooling the flames. Firefighting foam offers several advantages such as quick extinguishing capabilities, improved fire retardation, and reduced re-ignition. The increasing need for effective and efficient fire control methods, along with the stringent safety regulations imposed by various government agencies, are driving the demand for firefighting foam in the market. Market Key Trends: One key trend in the firefighting foam market is the growing adoption of environmentally friendly foam solutions. With increasing concerns regarding the environmental impact of firefighting foam, manufacturers are focusing on developing environmentally sustainable foam solutions.

These environmentally friendly foams are biodegradable and possess low toxicity, reducing the potential harm caused to the environment during firefighting activities. This trend is driven by the rising awareness among end-users and government regulations promoting the use of eco-friendly firefighting products. Overall, the global firefighting foam market is expected to witness significant growth due to the increased emphasis on fire safety and the growing demand for environmentally friendly foam solutions. PEST Analysis: Political: The political factors impacting the firefighting foam market include regulations and policies related to fire safety and environmental protection. Governments around the world are increasingly implementing stringent regulations to restrict the use of firefighting foams containing harmful chemicals like PFAS. This has led to the development and adoption of eco-friendly and more sustainable alternatives. Economic: The economic factors affecting the market include the overall economic growth and investments in infrastructure development.

As economies grow, there is an increased demand for fire safety measures and firefighting equipment, including foams. Investments in industries such as oil and gas, aerospace, and construction also contribute to the demand for firefighting foams. Social: The social factors influencing the market include the awareness and concern for fire safety among individuals and organizations. With the increasing number of fire incidents and the potential risks associated with them, there is a greater emphasis on implementing effective firefighting measures. The demand for firefighting foams is driven by the need to protect lives and minimize property damage. Technological: The technological factors impacting the market include advancements in foam formulation and delivery systems. Manufacturers are constantly developing innovative products that are more efficient in suppressing fires. These advancements include the development of fluorine-free foams, improved foam stability, and better compatibility with various fire hazards.

Key Takeaways: The global Firefighting Foam Market Share is expected to witness high growth, exhibiting a CAGR of 5.9% over the forecast period (2023-2030). This growth is driven by several factors, including increasing regulations and policies focused on fire safety and the environment. The shift towards eco-friendly foams is expected to boost market demand. In terms of regional analysis, North America is expected to be the fastest-growing and dominating region in the firefighting foam market. This can be attributed to the stringent regulations in the region, the presence of major key players, and increased awareness and investment in fire safety measures. Key players operating.

1 note

·

View note

Text

Aluminum Market: Products, Applications & Beyond

Aluminum is a versatile element with several beneficial properties, such as a high strength-to-weight ratio, corrosion resistance, recyclability, electrical & thermal conductivity, longer lifecycle, and non-toxic nature. As a result, it witnesses high demand from industries like automotive & transportation, electronics, building & construction, foil & packaging, and others. The high applicability of the metal is expected to drive the global aluminum market at a CAGR of 5.24% in the forecast period from 2023 to 2030.

Aluminum – Mining Into Key Products:

Triton Market Research’s report covers bauxite, alumina, primary aluminum, and other products as part of its segment analysis.

Bauxite is anticipated to grow with a CAGR of 5.67% in the product segment over the forecast years.

Bauxite is the primary ore of aluminum. It is a sedimentary rock composed of aluminum-bearing minerals, and is usually mined by surface mining techniques. It is found in several locations across the world, including India, Brazil, Australia, Russia, and China, among others. Australia is the world’s largest bauxite-producing nation, with a production value of over 100 million metric tons in 2022.

Moreover, leading market players Rio Tinto and Alcoa Corporation operate their bauxite mines in the country. These factors are expected to propel Australia’s growth in the Asia-Pacific aluminum market, with an anticipated CAGR of 4.38% over the projected period.

Alumina is expected to grow with a CAGR of 5.42% in the product segment during 2023-2030.

Alumina or aluminum oxide is obtained by chemically processing the bauxite ore using the Bayer process. It possesses excellent dielectric properties, high stiffness & strength, thermal conductivity, wear resistance, and other such favorable characteristics, making it a preferable material for a range of applications.

Hydrolysis of aluminum oxide results in the production of high-purity alumina, a uniform fine powder characterized by a minimum purity level of 99.99%. Its chemical stability, low-temperature sensitivity, and high electrical insulation make HPA an ideal choice for manufacturing LED lights and electric vehicles. The growth of these industries is expected to contribute to the progress of the global HPA market.

EVs Spike Sustainability Trend

As per the estimates from the International Energy Agency, nearly 2 million electric vehicles were sold globally in the first quarter of 2022, with a whopping 75% increase from the preceding year. Aluminum has emerged as the preferred choice for auto manufacturers in this new era of electromobility. Automotive & transportation leads the industry vertical segment in the studied market, garnering $40792.89 million in 2022.

In May 2021, RusAl collaborated with leading rolled aluminum products manufacturer Gränges AB to develop alloys for automotive applications. Automakers are increasingly substituting stainless steel with aluminum in their products owing to the latter’s low weight, higher impact absorption capacity, and better driving range.

Also, electric vehicles have a considerably lower carbon footprint compared to their traditional counterparts. With the growing need for lowering emissions and raising awareness of energy conservation, governments worldwide are encouraging the use of EVs, which is expected to propel the demand for aluminum over the forecast period.

The Netherlands is one of the leading countries in Europe in terms of EV adoption. The Dutch government has set an ambitious goal that only zero-emission passenger cars (such as battery-operated EVs, hydrogen FCEVs, and plug-in hybrid EVs) will be sold in the nation by 2030. Further, according to the Canadian government, the country’s aluminum producers have some of the lowest CO2 footprints in the world.

Alcoa Corporation and Rio Tinto partnered to form ELYSIS, headquartered in Montréal, Canada. In 2021, it successfully produced carbon-free aluminum at its Industrial Research and Development Center in Saguenay. The company is heralding the beginning of a new era for the global aluminum market with its ELYSIS™ technology, which eliminates all direct GHG emissions from the smelting process, and is the first technology ever to emit oxygen as a byproduct.

Wrapping Up

Aluminum is among the most widely used metals in the world today, and is anticipated to underpin the global transition to a low-carbon economy. Moreover, it is 100% recyclable and can retain its properties & quality post the recycling process.

Reprocessing the metal is a more energy-efficient option compared to extracting the element from an ore, causing less environmental damage. As a result, the demand for aluminum in the sustainable energy sector has thus increased. The efforts to combat climate change are thus expected to bolster the aluminum market’s growth over the forecast period.

#Aluminum Market#aluminum#chemicals and materials#specialty chemicals#market research#market research reports#triton market research

4 notes

·

View notes

Text

Bioplastics Market Share, Size, Global Driving Factors by Manufacturers, Growth Opportunities

The global bioplastics market size was USD 10.64 Billion in 2021 and is expected to register a revenue CAGR of 16.8% over the forecast period, according to the latest analysis by Emergen Research. Increase in demand for bioplastics from the automotive industry and demand for compostable plastics to improve soil quality are factors expected to support revenue growth of the market between 2022 and 2030. The automotive industry's primary objective and challenge is to reduce fuel consumption and pollutants by reducing vehicle weight. Bioplastics are effective materials for achieving this purpose. These smart plastics, such as bio-PA and bio-PP, have been embraced by major vehicle manufacturers to reduce environmental impact and provide additional strength to automobile components. Thus, demand for these plastics in the automotive industry owing to their excellent properties is anticipated to create lucrative growth prospects for companies in the market.

Get a sample of the Bioplastics Market report @ https://www.emergenresearch.com/request-sample/169

The global Bioplastics market report covers the analysis of drivers, trends, limitations, restraints, and challenges arising in the Bioplastics market. The report also discusses the impact of various other market factors affecting the growth of the market across various segments and regions. The report segments the market on the basis of types, applications, and regions to impart a better understanding of the Bioplastics market.

Emergen Research has segmented the global Bioplastics market on the basis of type, platform, application, and region:

Type Outlook (Revenue, USD Billion; 2017-2027)

Biodegradable

Polybutylene Adipate Terephthalate (PBAT)

Polybutylene Succinate (PBS)

Polylactic Acid (PLA)

Polyhydroxyalkanoate (PHA)

Starch Blends

Others

Distribution Channel Outlook (Revenue, USD Billion; 2017-2027)

Online

Offline

Application Outlook (Revenue, USD Billion; 2017-2027)

Packaging

Textile

Automotive & Transportation

Consumer Goods

Agriculture

Building & Construction

Others

Request a discount on the Bioplastics Market report @ https://www.emergenresearch.com/request-discount/169

Based on the competitive landscape, the market report analyzes the key companies operating in the industry:

BASF SE, NatureWorks, Biome Plastics, Braskem, Biotec, Total Corbion, Plantic Technologies, Mitsubishi Chemical Holdings Corporation, Novamont SPA, and Toray Industries

Additionally, the report covers the analysis of the key players in the industry with a special focus on their global position, financial status, and their recent developments. Porter’s Five Forces Analysis and SWOT analysis have been covered by the report to provide relevant data on the competitive landscape.

How will this Report Benefit you?

An Emergen Research report of 250 pages contains 194 tables, 189 charts and graphics, and anyone who needs a comprehensive analysis of the global Bioplastics market, as well as commercial, in-depth analyses of the individual segments, will find the study useful. Our recent study allows you to assess the entire regional and global market for Bioplastics. In order to increase market share, obtain financial analysis of each segment and the whole market. Look at how you can utilize the current and potential revenue-generating opportunities available in this sector. We believe that there are significant prospects for energy storage technology in this industry due to the rapid expansion of the technology. In addition to helping you build growth strategies, improve competitor analysis, and increase business productivity, the research will also assist you in making better strategic decisions.

Detailed Regional Analysis covers:

North America (U.S., Canada)

Europe (U.K., Italy, Germany, France, Rest of EU)

Asia-Pacific (India, Japan, China, South Korea, Australia, Rest of APAC)

Latin America (Chile, Brazil, Argentina, Rest of Latin America)

Middle East & Africa (Saudi Arabia, U.A.E., South Africa, Rest of MEA)

To Study Full Bioplastics Market Report, click here @ https://www.emergenresearch.com/industry-report/bioplastics-market

What Questions Should You Ask before Buying a Market Research Report?

How is the Bioplastics market evolving?

What is driving and restraining the Bioplastics market?

How will each Bioplastics submarket segment grow over the forecast period and how much revenue will these submarkets account for in 2027?

How will the market shares for each Bioplastics submarket develop from 2020 to 2027?

What will be the main driver for the overall market from 2020 to 2027?

Will leading Bioplastics markets broadly follow the macroeconomic dynamics, or will individual national markets outperform others?

How will the market shares of the national markets change by 2027 and which geographical region will lead the market in 2027?

Who are the leading players and what are their prospects over the forecast period?

What are the Bioplastics projects for these leading companies?

How will the industry evolve during the period between 2020 and 2027? What are the implications of Bioplastics projects taking place now and over the next 10 years?

Is there a greater need for product commercialisation to further scale the Bioplastics market?

Where is the Bioplastics market heading and how can you ensure you are at the forefront of the market?

What are the best investment options for new product and service lines?

What are the key prospects for moving companies into a new growth path and C-suite?

Request customization on the report @ https://www.emergenresearch.com/request-for-customization/169

Thank you for reading our report. To know more about the customization of the report, please get in touch with us, and our team will ensure the report is suited to your requirements.

About Us:

Emergen Research is a market research and consulting company that provides syndicated research reports, customized research reports, and consulting services. Our solutions purely focus on your purpose to locate, target, and analyse consumer behavior shifts across demographics, across industries, and help clients make smarter business decisions. We offer market intelligence studies ensuring relevant and fact-based research across multiple industries, including Healthcare, Touch Points, Chemicals, Types, and Energy. We consistently update our research offerings to ensure our clients are aware of the latest trends existent in the market. Emergen Research has a strong base of experienced analysts from varied areas of expertise. Our industry experience and ability to develop a concrete solution to any research problems provides our clients with the ability to secure an edge over their respective competitors.

For More Related Reports by Emergen Research

gambling software market: https://www.emergenresearch.com/industry-report/gambling-software-market

functional ingredients market: https://www.emergenresearch.com/industry-report/functional-ingredients-market

space mining market: https://www.emergenresearch.com/industry-report/space-mining-market

acrylic resins market: https://www.emergenresearch.com/industry-report/acrylic-resins-market

drone logistics and transportation market: https://www.emergenresearch.com/industry-report/drone-logistics-and-transportation-market

targeted therapeutics market: https://www.emergenresearch.com/industry-report/targeted-therapeutics-market

airborne intelligence surveillance and reconnaissance market: https://www.emergenresearch.com/industry-report/airborne-intelligence-surveillance-and-reconnaissance-market

small caliber ammunition market: https://www.emergenresearch.com/industry-report/small-caliber-ammunition-market

1 note

·

View note

Text

Carbon Capture & Storage (CCS) Market - Forecast(2024–2030)

Carbon Capture and Storage (CCS) market size is forecast to reach US$25.3 billion by 2026, after growing at a CAGR of 29.1% during 2021–2026. The emerging demand for carbon dioxide injection technologies for Enhanced Oil Recovery (EOR) and stringent government standards for greenhouse gas emissions are the key factors driving the market growth. Carbon Capture and Storage or Carbon Capture and Sequestration (CCS) is a technology to combat climate change in which Carbon dioxide (CO2) is captured and then transported where it is stored permanently across depleted hydrocarbon fields and deep saline aquifer formations. The goal of carbon capture and storage is to keep CO2 emissions out of the atmosphere as increased levels of CO2 is the main culprit behind the Greenhouse effect and global warming which has a detrimental effect not only on the environment and also on the economy as a whole. Carbon capture and storage aims at reducing the human carbon footprint. CO2 is mainly produced by the combustion of fossil fuels and is also a major by-product of many industries. Hence, it is vital to get rid of it in a responsible manner as it is a greenhouse gas. According to a report by the International Energy Agency (IEA), CCS could contribute to a 19% reduction in global CO2 emissions by 2050. In the Paris Climate Agreement, world governments agreed to keep emissions well below 2?C and to pursue efforts to keep it below 1.5?C. The Intergovernmental Panel on Climate Change (IPCC) concluded that global emissions need to reach net zero by 2050 to limit warming to 1.5?C. To achieve the Paris Agreement objective countries are trying to reach net zero. This goal to reach net zero greenhouse gas emissions is one of the major contributing factors to the growth of the Carbon Capture and Storage market. Clean technologies and increasing power consumption also play a significant role in driving the carbon capture and storage industry during the forecast period.

Sample Report:

COVID-19 Impact

Carbon Capture and Storage (CCS) Market Report Coverage

The report: “Carbon Capture and Storage (CCS) Market — Forecast (2021–2026)”, by IndustryARC, covers an in-depth analysis of the following segments of the Carbon Capture and Storage Market.

Inquiry Before:

By Capture Technology: Post Combustion Capture, Pre-Combustion Capture, Oxyfuel Combustion and Industrial Separation

By Storage Technology: Geological Storage, Deep Ocean Storage, and Enhanced Oil Recovery (EOR)

By End-Use Industry: Power Generation, Iron and Steel, Oil and Gas, Chemicals, Cement and Concrete, Biofuels, Fertilizers, Textiles, Food and Beverages, Paper and Pulp, and Others

By Geography: North America (USA, Canada, and Mexico), Europe (UK, Germany, France, Italy, Netherlands, Spain, Russia, Belgium, and Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Australia and New Zealand, Indonesia, Taiwan, Malaysia, and Rest of APAC), South America (Brazil, Argentina, Colombia, Chile, and Rest of South America), Rest of the World (Middle East and Africa)

Key Takeaways

North America dominates the CCS market, with USA having the lion’s share of operational or under construction schemes of CCS plants.

The International Energy Agency (IEA) estimates that we need a carbon capture and storage industry capable of capturing 7,000 million tons of carbon dioxide per year and storing it underground by 2050. So, the future of the global CCS industry looks promising.

There has been an increase in Global warming and CO2 emissions post lockdowns. This is leading to an increase in demand to curb emissions, which is increasing the demand for carbon capture and consecutively driving the market growth.

The major opportunity for this market is growing climate change awareness and development of clean and green mitigation technologies. Furthermore, it is also an opportunity for this market to develop advanced technology for safe and long-term storage of CO2.

Schedule a Call:

Figure: Carbon Capture and Storage (CCS) Market Revenue Share, By Capture Technology, 2020 (%)

For More Details on This Report — Request for Sample

Carbon Capture and Storage (CCS) Market Segment Analysis — By Capture Technology

Pre-combustion, post-combustion, oxy-fuel combustion, and industrial separation are some of the widely used capture technologies. The post-combustion capture segment held the largest share of 55.6% in the CCS market in 2020. In post combustion capture CO2 is removed after combustion of fossil fuels in power plants. CO2 is captured from flue gases at power stations or other point sources. The technology is currently used in other industrial applications as well. Post combustion capture is most popular in research because PCC can be typically built into existing industrial plants and power stations (retro-fitting) without significant modifications to the original plant. Post Combustion Capture offers high operational flexibility (partial retrofit, zero to full capture operation) and it can match market conditions for both existing and new power stations. Renewable technologies can be integrated in this process, in particular, Post Combustion Capture allows the use of low-cost solar thermal collectors to provide the necessary heat to separate CO2 from sorbents, effectively reducing the loss of electrical output caused by capture.

Oxy-fuel combustion is the fastest growing capture technology in the Carbon Capture and Storage market in 2020 and is growing at a CAGR of 41.0% during 2021–2026. Oxy-fuel combustion is the process of combusting hydrocarbon fuel in the presence of high purity oxygen. Generally, oxy-fuel combustion recycles flue gas to achieve a lower flame temperature, which makes it a highly efficient energy-saving combustion technology. Due to the large quantity of high purity oxygen required for this process, cryogenic air separation is currently the technology of choice for oxygen production. As demand for highly efficient and effective capture technologies increases, Post-combustion Capture and Oxy-fuel Combustion are expected to dominate the market during the forecast period.

Carbon Capture and Storage (CCS) Market Segment Analysis — By Storage Technology

The last and the most critical step in CCS is permanent storage of CO2. Geological Storage, Deep Ocean Storage and Enhanced Oil Recovery (EOR) are some of the storage technologies used. The EOR segment held the largest share of 70.0% in the CCS market in 2020. Enhanced Oil Recovery (EOR) is a process of extraction of crude oil from an oil field that otherwise cannot be recovered. Due to the physics of fluid flow, about two-thirds of conventional crude oil discovered in oil fields remains unproduced — primary oil recovery produces only about 10% of the reservoir’s original oil in place, with secondary recovery techniques increasing original oil in place production to approximately 20 to 40%. Tertiary (EOR) techniques prolong the life of producing fields, ultimately leading to recovery of 30 to 60% of the original oil in place. The United States Department of Energy (DOE) has estimated that full use of next generation CO2-EOR in the country could generate an additional 240 billion barrels of recoverable oil resources. Developing this potential would depend on the availability of commercial CO2 in large volumes, which could be made possible by widespread use of carbon capture and storage. Geological storage is the fastest growing storage technology segment in the Carbon Capture and Storage market in 2020 and is growing at a CAGR of 33.1% during 2021–2026. Geological Storage involves injecting CO2 as a supercritical fluid and injecting it into geological formations like saline aquifers or deep unminable coal beds 800 meters or more below the Earth’s crust. According to the Global CCS institute, as of June 2021, 26 commercial CCS facilities with a total capacity of 40 million tons per annum (Mtpa) are operating, 3 more are in construction, 13 are in advanced development and approximately 21 are in early development. Each of these facilities is or will permanently store hundreds of thousands of tons of CO2 per year, and several store more than one million tons of CO2 each year. Five of the 21 operating facilities use dedicated geological storage.

Buy Now:

Carbon Capture and Storage (CCS) Market Segment Analysis — By End Use Industry

Industries produce about 8 billion tons of CO2 emissions annually. Chemical, Iron and steel and cement industries are responsible for 70% of these emissions due to the nature of their processes and high temperature heat requirements. The only feasible option for mitigation is to remove CO2 after production using CCS. The Oil and gas segment held the largest share of 62.8% in the Carbon Capture and Storage market in 2020. The rising demand for crude oil and natural gas across various industries has driven the growth of the oil and gas industry. The rising investments in the oil industry to meet growing energy requirements with the focus on lowering greenhouse gas emissions will significantly stimulate the implementation of carbon capture and storage projects. The fastest growing end use industry segment in the Carbon Capture and Storage market in 2020 is biofuels which is growing at a CAGR of 43.2% during 2021–2026. This segment is growing fast owing to its popularity as a negative emission technology- Bioenergy with Carbon Capture and Storage (BECCS). BECCS is the process of extracting bioenergy from biomass and capturing and storing the CO2 thereby removing the atmospheric CO2. Biogenic CO2 is typically counted as a net-zero emission in most Greenhouse gas accounting schemes. This makes it a very low-cost CO2 source for capture. Thus, favoring the CCS market.

Carbon Capture and Storage (CCS) Market Segment Analysis — By Geography

North America held the largest share in the CCS market in 2020 up to 54.0%. The US already had the highest number of operational CCS facilities and continued its lead in the global CCS projects with 12 of the 17 new commercial facilities added to the list projects in 2020. According to industry insights, North America will witness substantial growth on account of the increasing energy demands. For instance, the primary energy produced from fossil fuels in the US accounted for 79% of the total primary energy production in 2020 according to the IEA. Hence, there is a need to upgrade the conventional systems with effective emission control technologies like CCS to achieve the minimum emission rate. This contributes to the regional market growth. Projects were announced in the following end use industries — cement manufacturing, coal and gas-fired power plants, waste-to-energy plants, ethanol facilities and chemical production. These new projects are mainly due to incentives from the government as well as the DOE. Stringent regulatory standards by the government to decrease the greenhouse gas emissions will further boost the demand for carbon capture and storage technology in the region.

The APAC region is the fastest growing region and is growing at a CAGR of 44.3% during 2021–2026. In the Asia Pacific region commitments to reach net-zero emissions saw significant support over the last year from both, governments and businesses, which is spearheading CCS investment and driving the growth of the market. Increasing industrialization rate coupled with the growing investment toward expansion of manufacturing facilities has raised the deployment of CCS projects. Rapid deployment of gas and coal power plants in to cater to the growing demand for energy will accelerate the Asia Pacific market growth. For instance, in June 2021 Japan proposed $10 billion in government funding for low carbon projects overseas, particularly in Asia with the aim of offsetting the environmental impacts as it stays dependent on oil and gas imports to maintain energy security. Rising awareness regarding emission control along with ongoing industrial and commercial expansion will boost the market.

Carbon Capture and Storage (CCS) Market Drivers

Global Aim for Net Zero

There has been a tremendous growth in the renewable energy sources sectors but climate experts and scientists believe that this alone will not result in zero carbon emissions. CCS plays a vital role in ridding the existing energy sources of greenhouse gas emissions and one step closes to net zero. The CCS technologies available today can absorb more than 90% of CO2 generated by fossil fuel power stations and industrial plants. According a report, the International Energy Agency declares that without CCS it will be impossible to achieve the ambition of the Paris Agreement. Many countries have begun adopting CCS to put them on the right track to net zero. A Norwegian Company, Equinor’s “Hydrogen to Humber (H2H) Saltend” project will provide blue (zero emission) hydrogen from natural gas with carbon capture and storage technology for the Humber region in UK. The project is one of many steps toward realizing the 2019 UK law committing to net-zero greenhouse gas emissions by 2050. Such projects act as drivers for the CCS market during the forecast period.

Role of Power Generation Industry

The expeditious decarbonization of power generation industry is of utmost importance in achieving net-zero emissions as electricity generation is one of the largest sources of CO2 emissions globally. The demand for electricity is forecast to increase significantly. CCS equipped power plants will help ensure that the low carbon grid of the future is resilient and reliable. CCS is also essential for reducing emissions from the existent world-wide fossil fuel power plants. Globally, there is approximately 2,000 Giga Watts (GW) of operating coal-fired capacity, with over 500 GW of new capacity expected by 2030. Over 200 Gigatons of new capacity is already under construction. Without CCS retrofit or early retirement, coal and gas-fired power stations, both current as well as under construction, will continue emitting CO2 at rates that will consume 95% of the IEA’s Sustainable Development Scenario carbon budget by 2050. Retrofitting fossil fuel power generation plants with CCS can be a cost-effective option which means economies that are heavily dependent on coal such as China, India, and Southeast Asian countries can continue using it while moving toward a low-carbon economy, thereby transitioning towards zero emission. Thus, the growth in power generation also fuels the growth of CCS market.

Carbon Capture and Storage (CCS) Market Challenges

High Cost of Carbon Capture and Storage

Incorporating CCS technologies increases costs including capital investment in equipment technology, operating costs and transportation costs without providing additional revenue. The high cost of carbon capture and storage has kept the technology from entering mainstream use. Climate policies like carbon pricing are still not strong enough to make CCS economically attractive. For Carbon capture alone the cost varies from $15–120 per ton of CO2. Some CO2 capture technologies are commercially available now, while others are still in development, and this further contributes to the large range in costs. This challenge can be offset by government economic packages and incentives.

Environmental Considerations

The main critique towards CCS is that it may strengthen dependency on non-renewable fossil fuels and coal mining instead of adopting renewable energy solutions. Another concern is regarding the possible leaks in storage. Other concerns are explosions, earthquakes or any ecosystem side-effects. Such factors have become the major challenge of CCS which constrains the growth of the market.

Carbon Capture and Storage (CCS) Market Landscape

Technological advancements, partnerships, and R&D activities are key strategies adopted by players in the Carbon Capture and Storage market. Carbon Capture and Storage market top companies are General Electric Company, Royal Dutch Shell PLC, Aker Solutions ASA, Fluor Corporation, Mitsubishi Heavy Industries, Ltd, Halliburton Company, Siemens AG, Total S.A., Equinor ASA, ADA-ES, Inc, Exxon Mobil Corporation and Schlumberger Limited among others.

Acquisitions/Technology Launches

In June 2021, Northern Lights, Total Energies, Oxy Low Carbon Ventures, South Pole, Perspectives and Carbon Finance Labs announced the launch of the CCS+ Initiative which focus on advancing carbon accounting for a range of carbon capture, utilization, storage, and removal technologies that are underpinned by robust cradle-to-grave life cycle assessments (LCA) and rigorous verification standards to ensure environmental integrity.

In February 2020 Chevron Technology Ventures partnered with WAVE Equity Partners, and Marubeni Corporation by investing $16 million in Carbon Clean Solutions. Carbon Clean Solutions Limited is developing a carbon capture system that can be shipped to remote sites, where it will remove carbon dioxide at a price of $30 per ton.

For more Chemicals and Materials Market reports, please click here

0 notes

Text

Epoxy Resins Market Growth Forecast: From $10.5 Billion in 2020 to $21.87 Billion by 2031

Epoxy resins are versatile thermosetting polymers with a wide range of applications due to their excellent mechanical properties, chemical resistance, and adhesion. These resins play a crucial role in various industries, including construction, automotive, aerospace, and electronics. The epoxy resins market has seen substantial growth over the years, driven by advancements in technology and increasing demand across diverse sectors.

The global epoxy resins market is estimated to flourish at a CAGR of 6.9% from 2021 to 2031. Transparency Market Research projects that the overall sales revenue for epoxy resins is estimated to reach US$ 21.87 billion by the end of 2031. The growing use of epoxy resins in medical devices, dental materials, and pharmaceutical packaging emerges as an unseen driver. Epoxy's biocompatibility and resistance make it a valuable material in healthcare applications.

The rising emphasis on renewable energy sources drives demand for epoxy resins in wind turbine blades and solar panel components. Epoxy's strength and durability contribute to the reliability of these critical components. Epoxy resins gain popularity in artistic and craft sectors, with resin-based art projects and DIY applications on the rise.

For More Details, Request for a Sample of this Research Report: https://www.transparencymarketresearch.com/epoxy-resins-market.html

Market Segmentation

By Service Type

Formulation Services: Involves the customization of epoxy resin formulations to meet specific industry requirements.

Application Services: Encompasses the application of epoxy resins in various sectors such as construction and manufacturing.

By Sourcing Type

Primary Production: Direct production of epoxy resins from raw materials.

Recycled Resins: Reuse of epoxy resin products to create new formulations.

By Application

Construction: Used in adhesives, coatings, and flooring.

Automotive: Employed in parts and components for improved durability and strength.

Aerospace: Utilized in composites for lightweight and high-strength materials.

Electronics: Found in circuit boards and encapsulation.

Marine: Applied in boat building and maintenance due to its water-resistant properties.

By Industry Vertical

Construction & Infrastructure

Automotive

Aerospace & Defense

Electronics

Marine

Others (e.g., industrial coatings, sports equipment)

By Region

North America: Dominates the market due to advanced industrial sectors and high demand in aerospace and automotive industries.

Europe: Significant growth driven by the construction and automotive sectors.

Asia-Pacific: Fastest-growing region, with increasing industrial activities and rising infrastructure development.

Latin America: Emerging market with growing investments in construction and automotive industries.

Middle East & Africa: Gradual growth due to expanding industrial applications and infrastructure projects.

Regional Analysis

North America: The market is characterized by high demand for epoxy resins in aerospace, automotive, and construction sectors. The U.S. is a major contributor to this region’s growth due to its robust industrial base.

Europe: The European market benefits from technological advancements and stringent regulations promoting the use of high-performance materials. Countries like Germany and France are key players.

Asia-Pacific: The region is expected to witness the highest growth due to rapid industrialization, urbanization, and infrastructure development. China and India are major contributors to this growth.

Latin America: The market is expanding with increased investments in construction and automotive sectors, especially in countries like Brazil and Mexico.

Middle East & Africa: The growth is driven by infrastructure projects and increasing adoption of epoxy resins in industrial applications.

Market Drivers and Challenges

Drivers:

Technological Advancements: Innovations in resin formulations and processing techniques enhance performance and broaden applications.

Growing Construction and Infrastructure Activities: Rising urbanization and infrastructure development increase demand for epoxy-based products.

Expansion in Automotive and Aerospace Industries: High-performance requirements drive the use of epoxy resins in these sectors.

Challenges:

Volatility in Raw Material Prices: Fluctuations in the cost of key raw materials impact production costs and market stability.

Environmental Concerns: Increasing scrutiny on the environmental impact of epoxy resins and regulatory pressures for sustainable practices pose challenges.

Market Trends

Shift Towards Eco-friendly Resins: Growing emphasis on sustainable and bio-based epoxy resins to reduce environmental impact.

Advancements in Epoxy Resin Technology: Development of high-performance, lightweight, and durable resins for specialized applications.

Increased Adoption in Emerging Markets: Expanding industrial activities in developing regions drive demand for epoxy resins.

Future Outlook

The epoxy resins market is expected to continue its upward trajectory, supported by ongoing technological innovations and increasing demand across various sectors. The emphasis on sustainability and eco-friendly products will likely shape future developments in the industry. Companies are anticipated to focus on enhancing the performance characteristics of epoxy resins and expanding their applications in emerging sectors.

Key Market Study Points

Analysis of market trends and growth drivers.

Evaluation of regional market dynamics and key players.

Assessment of technological advancements and their impact on the industry.

Buy this Premium Research Report: https://www.transparencymarketresearch.com/checkout.php?rep_id=583<ype=S

Competitive Landscape

The epoxy resins market is competitive, with key players including:

BASF SE

Hexion Inc.

Dow Chemical Company

SABIC

Huntsman Corporation

These companies are engaged in strategic initiatives such as mergers and acquisitions, partnerships, and technological innovations to strengthen their market position and address evolving customer needs.

Recent Developments

Product Innovations: Introduction of advanced epoxy resins with improved properties for specialized applications.

Sustainability Initiatives: Increased focus on developing eco-friendly and recyclable epoxy resins to meet environmental regulations.

Expansion Strategies: Companies expanding their production capacities and geographic presence to cater to growing market demands.

About Transparency Market Research

Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information.

Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports.

Contact:

Transparency Market Research Inc.

CORPORATE HEADQUARTER DOWNTOWN,

1000 N. West Street,

Suite 1200, Wilmington, Delaware 19801 USA

Tel: +1-518-618-1030

USA – Canada Toll Free: 866-552-3453

Website: https://www.transparencymarketresearch.com

0 notes

Text

Understanding the Global Soda Ash Import Market

Soda ash, also known as sodium carbonate, is a vital chemical with a rich history spanning over a thousand years. It ranks as the tenth most consumed inorganic chemical globally, playing a crucial role in various industries, including detergent manufacturing, glass production, and water treatment. With a growing market anticipated to reach $38.2 billion by 2032, it’s essential to explore the dynamics of the soda ash import market, particularly in key regions such as South America and Southeast Asia.

Key Players in the Soda Ash Market

Among the leading suppliers of dense soda ash are GHCL Limited, Ciner Resources Corporation, and Shreenathji Chemicals. In India, the primary importers of soda ash include Drita Technologies Pvt. Ltd., Mahalaxmi Dyes & Chemicals Ltd., and Delta Chemicals. These companies play a pivotal role in meeting the demand for soda ash in various applications, from manufacturing lithium batteries to controlling pH levels in water treatment processes.

Soda Ash Import Data Insights

In 2023, India emerged as the world's top soda ash importer, with 18,747 shipments recorded. This substantial import volume underscores the country's growing industrial sectors, especially in construction and chemicals. The majority of these imports come from China, Romania, and Kenya, with Vietnam and Bangladesh following closely in terms of import volume.

The import landscape is characterized by a network of 634 buyers sourcing from 730 suppliers of dense soda ash in India. The corresponding HS codes for soda ash include 28362020 for light disodium carbonate and 28362010 for dense disodium carbonate, among others.

Growth Projections and Market Drivers

The global soda ash market is projected to grow at a compound annual growth rate (CAGR) of 4.1% from 2024 to 2031, reaching a valuation of USD 26.64 billion by 2031. Factors driving this growth include:

Increasing Construction Activity: With urbanization and infrastructure development on the rise, the demand for soda ash in construction-related applications is set to grow.

Expanding Chemical and Detergent Production: The surge in the production of glass and chemicals, particularly in emerging markets like Southeast Asia and Latin America, is significantly contributing to the demand for soda ash.

Sustainability Initiatives: As industries pivot toward sustainable practices, advancements in production methods are making soda ash manufacturing more environmentally friendly, further boosting its market appeal.

Leading Suppliers and Importers

When considering suppliers of dense soda ash, notable names include:

Shreenathji Chemicals

Ciner Resources Corporation

GHCL Limited

Novella Corporation

Akshar Chemicals

These suppliers are integral to ensuring the reliability and quality of soda ash for various industrial applications.

In India, key importers also encompass companies like Aimchem Ingredients Pvt. Ltd., Belami Fine Chemicals Pvt. Ltd., and Sumitomo Chemical India Pvt. Ltd. This diverse network highlights the competitive landscape in the Indian soda ash import market.

Conclusion

The soda ash market is experiencing robust growth driven by rising local demand, especially in India. However, importers must navigate challenges such as price competition and potential market surpluses. A strategic approach, involving careful supplier selection and market trend analysis, will be crucial for success in this dynamic landscape.

For those looking for detailed insights on soda ash imports, the platform Exportimportdata.in offers comprehensive data-driven resources, including information on suppliers, importers, and market trends. As the soda ash industry continues to evolve, staying informed will be vital for stakeholders looking to capitalize on this essential chemical’s growing market.

If you have any questions or need further insights into soda ash suppliers or import data, feel free to reach out for expert guidance and a free live demo!

#SodaAsh#SodiumCarbonate#ChemicalIndustry#ImportMarket#SodaAshSuppliers#SodaAshImporters#GlobalTrade#IndustrialChemicals#DetergentManufacturing#GlassProduction#WaterTreatment#SustainablePractices#MarketGrowth#ChemicalExports#IndiaImports#APACMarket#TradeData#ExportImport#SupplyChain#MarketInsights

0 notes

Text

#Japan Construction Chemicals Market#Market Size#Market Share#Market Trends#Market Analysis#Industry Survey#Market Demand#Top Major Key Player#Market Estimate#Market Segments#Industry Data

0 notes

Text

Cryogenic Valves Market Size, Trends, Research Report - 2032 | Reports and Insights

The Reports and Insights, a leading market research company, has recently releases report titled “Cryogenic Valves Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2024-2032.” The study provides a detailed analysis of the industry, including the global Cryogenic Valves Market share, size, trends, and growth forecasts. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

Report Highlights:

How big is the Cryogenic Valves Market?

The global cryogenic valves market size reached US$ 3.8 billion in 2023. Looking forward, Reports and Insights expects the market to reach US$ 6.5 billion in 2032, exhibiting a growth rate (CAGR) of 6.2% during 2024-2032.

What are Cryogenic Valves?

Cryogenic valves are specifically designed to control the flow of extremely cold gases and liquids, typically at temperatures below -150°C (-238°F). They are crucial for managing cryogenic substances such as liquid nitrogen, helium, oxygen, and natural gas in industries like aerospace, energy, medical, and chemical processing. Built to maintain secure seals and provide effective insulation, these valves prevent leaks and reduce thermal loss even under extreme cold conditions. Their construction materials and design enable them to endure the expansion and contraction caused by low temperatures, ensuring safe and reliable performance in demanding applications.

Request for a sample copy with detail analysis: https://www.reportsandinsights.com/sample-request/1931

What are the growth prospects and trends in the Cryogenic Valves industry?

The cryogenic valves market growth is driven by various factors and trends. Cryogenic valves are designed to manage the flow of extremely cold liquids and gases, typically at temperatures below -150°C (-238°F), such as liquid nitrogen, helium, and oxygen. Essential for sectors like aerospace, energy, medical, and chemical processing, these valves ensure precise control and safe handling of cryogenic fluids. Built to endure the harsh conditions of low temperatures, cryogenic valves are constructed with materials and insulation methods that prevent leakage and reduce thermal loss. Their design accommodates the expansion and contraction of materials due to temperature changes, providing reliable and efficient performance in demanding environments. Hence, all these factors contribute to cryogenic valves market growth.

What is included in market segmentation?

The report has segmented the market into the following categories:

By Paper Type:

Matte Paper

Glossy Paper

Semi-gloss Paper

By Application:

Universal Files Copy Application

Advertisement Making Application

Graphic Design Application

Market Segmentation By Region:

North America:

United States

Canada

Europe:

Germany

United Kingdom

France

Italy

Spain

Russia

Poland

BENELUX

NORDIC

Rest of Europe

Asia Pacific:

China

Japan

India

South Korea

ASEAN

Australia & New Zealand

Rest of Asia Pacific

Latin America:

Brazil

Mexico

Argentina

Rest of Latin America

Middle East & Africa:

Saudi Arabia

South Africa

United Arab Emirates

Israel

Rest of MEA

Who are the key players operating in the industry?

The report covers the major market players including:

Emerson Electric Co.

Flowserve Corporation

Schlumberger Limited

Parker Hannifin Corporation

Velan Inc.

Herose GmbH

Chart Industries, Inc.

Cryogenic Limited

L&T Valves Limited

Bray International, Inc.

Powell Valves

Habonim Industrial Valves & Actuators

Valco Group

Samson AG

Valvesco AG

View Full Report: https://www.reportsandinsights.com/report/Cryogenic Valves-market

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

Reports and Insights consistently mееt international benchmarks in the market research industry and maintain a kееn focus on providing only the highest quality of reports and analysis outlooks across markets, industries, domains, sectors, and verticals. We have bееn catering to varying market nееds and do not compromise on quality and research efforts in our objective to deliver only the very best to our clients globally.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

Contact Us:

Reports and Insights Business Research Pvt. Ltd.

1820 Avenue M, Brooklyn, NY, 11230, United States

Contact No: +1-(347)-748-1518

Email: [email protected]

Website: https://www.reportsandinsights.com/

Follow us on LinkedIn: https://www.linkedin.com/company/report-and-insights/

Follow us on twitter: https://twitter.com/ReportsandInsi1

0 notes

Text

Zinc Nitrite Manufacturing Plant Project Report 2024: Industry trends and Plant Setup

Introduction

Zinc nitrite is an inorganic compound used in various applications, including the production of other zinc compounds, corrosion inhibitors, and as a nitrifying agent in the chemical industry. Its unique properties make it valuable across several sectors, including construction, automotive, and agriculture. With the increasing demand for zinc compounds in industrial applications, establishing a zinc nitrite manufacturing plant presents a significant business opportunity. This Zinc Nitrite Manufacturing Plant Project Report outlines the essential components necessary for setting up a successful manufacturing facility, including market analysis, production processes, equipment requirements, and financial projections.

Market Analysis

Industry Overview

The global market for zinc nitrite is expanding due to its widespread applications in various industries. The demand for corrosion-resistant materials, particularly in the automotive and construction sectors, is driving growth. Additionally, as environmental regulations become stricter, the need for effective corrosion inhibitors and sustainable chemical solutions is rising.

Target Market

The primary target market for zinc nitrite production includes:

Chemical Manufacturers: Companies that utilize zinc nitrite in the synthesis of other zinc compounds.

Construction Industry: Manufacturers of paints, coatings, and adhesives that require corrosion inhibitors.

Automotive Sector: Producers of vehicle components that need protective coatings to enhance durability.

Agriculture: Fertilizer manufacturers looking for effective nitrifying agents.

Get a Free Sample Report with Table of Contents @

https://www.expertmarketresearch.com/prefeasibility-reports/zinc-nitrite-manufacturing-plant-project-report/requestsample

Production Process

Raw Materials

The primary raw materials required for zinc nitrite production include:

Zinc Oxide: The main source of zinc for the synthesis of zinc nitrite.

Nitric Acid: A key reactant that provides the nitrite ion necessary for the formation of zinc nitrite.

Water: Used for the reaction and purification processes.

Manufacturing Steps

Preparation of Reactants: High-quality zinc oxide and nitric acid are sourced to ensure optimal reaction conditions.

Chemical Reaction: The production of zinc nitrite involves the reaction of zinc oxide with nitric acid. The reaction typically occurs in a controlled environment to prevent excessive heat and ensure complete conversion.ZnO+2HNO3→Zn(NO2)2+H2O\text{ZnO} + 2\text{HNO}_3 \rightarrow \text{Zn(NO}_2)_2 + \text{H}_2\text{O}ZnO+2HNO3→Zn(NO2)2+H2O

Neutralization: The resulting zinc nitrite solution may be neutralized if necessary to adjust the pH for further processing.

Crystallization: The zinc nitrite is then crystallized from the solution. This involves cooling the solution to promote the formation of solid zinc nitrite crystals.

Separation and Drying: The crystals are separated from the remaining solution through filtration or centrifugation. The separated zinc nitrite is then dried to obtain the final product in powder form.

Quality Control: Rigorous quality control measures are implemented throughout the production process to ensure that the final product meets industry standards and regulatory requirements.

Equipment Requirements

Establishing a zinc nitrite manufacturing plant requires specialized equipment, including:

Reactor Vessels: For conducting the chemical reactions between zinc oxide and nitric acid.

Filtration Units: For separating zinc nitrite crystals from the solution.

Centrifuges: To enhance the separation process.

Crystallizers: For promoting the crystallization of zinc nitrite.

Dryers: To remove moisture from the final product.

Quality Control Laboratory Equipment: For testing the purity and quality of the final product.

Facility Requirements

Location

Choosing an appropriate location for the manufacturing plant is critical. Proximity to raw material suppliers and access to transportation networks can help minimize operational costs and streamline distribution.

Space

The facility should have designated areas for:

Raw material storage

Production area

Crystallization and drying sections

Quality control laboratory

Finished product storage

Administrative offices

Utilities

Ensure the facility has access to essential utilities such as water, electricity, and waste management systems. Compliance with environmental regulations is vital for sustainable operations.

Financial Projections

Initial Investment

The initial investment required for establishing a zinc nitrite manufacturing plant can vary widely based on factors such as location, scale, and technology. Major cost components include:

Land and facility construction

Equipment procurement

Raw material costs

Labor and operational expenses

Regulatory compliance and marketing costs

Revenue Projections

With effective management, a zinc nitrite manufacturing plant can expect to break even within the first 3-5 years. Revenue can be generated through direct sales to chemical manufacturers, construction companies, and other industries requiring zinc nitrite.

Profitability

Profit margins in the chemical manufacturing sector can vary but typically range from 15-25%, depending on market demand and operational efficiency.

Marketing Strategy

To effectively market zinc nitrite, consider the following strategies:

Brand Development: Establish a strong brand identity that emphasizes the quality and effectiveness of the product.

Industry Networking: Attend trade shows and conferences to build relationships with potential clients in the chemical and construction sectors.

Digital Marketing: Utilize online platforms to promote products and reach a broader audience.

Educational Campaigns: Conduct campaigns to inform industries about the benefits and applications of zinc nitrite.

FAQ

1. What is zinc nitrite used for?

Zinc nitrite is primarily used as a corrosion inhibitor, a nitrifying agent in fertilizers, and in the production of other zinc compounds.

2. How is zinc nitrite produced?

Zinc nitrite is produced by reacting zinc oxide with nitric acid, followed by crystallization and drying processes.

3. What safety concerns are associated with zinc nitrite manufacturing?

Safety concerns include handling hazardous chemicals and managing emissions. Strict safety protocols and proper equipment are essential to mitigate risks.

4. What are the startup costs for a zinc nitrite manufacturing plant?

Startup costs can vary significantly based on location and scale, typically including land, equipment, raw materials, and labor. A detailed business plan will help estimate these costs accurately.

5. Can zinc nitrite be sold internationally?

Yes, zinc nitrite can be sold internationally, but compliance with various regulatory standards in different countries is essential for successful export and market entry.

Related Reports

https://www.expertmarketresearch.com/reports/gas-treatment-market

https://www.expertmarketresearch.com/reports/incident-and-emergency-management-market

https://www.expertmarketresearch.com/articles/top-digital-marketing-companies

Media Contact:

Company Name: Claight Corporation

Contact Person: Lewis Fernandas, Corporate Sales Specialist — U.S.A.

Email: [email protected]

Toll Free Number: +1–415–325–5166 | +44–702–402–5790

Address: 30 North Gould Street, Sheridan, WY 82801, USA

Website: www.expertmarketresearch.com

Aus Site: https://www.expertmarketresearch.com.au

0 notes

Text

Engineering Plastic Market Trends, Key Players, DROT, Analysis & Forecast Till 2030

Engineering plastics are a group of plastic materials such as polystyrene, PVC, polypropylene and polyethylene, and others. These materials have superior properties such as higher impact strength, high abrasion, wear, and fatigue resistance. It has better mechanical and thermal properties. Engineering Plastics are expensive and are manufactured for special purpose applications only. These are usually thermoplastic materials. Hence these materials can be easily processed with conventional plastic processing machinery.