#Electronic Design Automation Software Market forecast

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

1,644 Tumblr posts in 1 second.

Text

AI in Action: Intelligent Solutions for the Document Management System Market

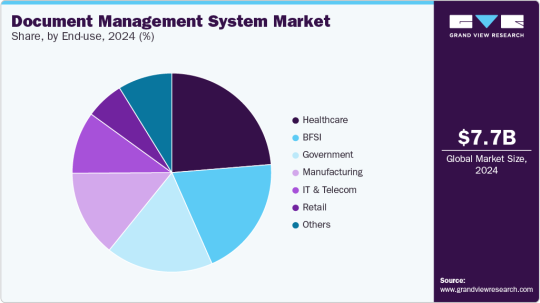

The global document management system market was valued at USD 7.68 billion in 2024 and is projected to reach USD 18.17 billion by 2030, demonstrating a robust Compound Annual Growth Rate (CAGR) of 15.9% from 2025 to 2030. This expansion is primarily fueled by organizations' increasing need to securely manage and store vast volumes of digital information.

As businesses worldwide embrace digital transformation and move towards paperless operations, the demand for effective solutions for document storage, retrieval, and management has escalated. The accelerated adoption of cloud-based DMS solutions has further spurred this trend, offering businesses scalable, cost-effective, and readily accessible options. Moreover, the heightened focus on compliance and regulatory mandates is significantly contributing to the growth of the DMS industry. Enterprises operating in heavily regulated sectors like healthcare, finance, and legal are increasingly implementing DMS to ensure strict adherence to data security, privacy, and record-keeping regulations. These systems facilitate streamlined audits, maintain secure document trails, and mitigate the risk of non-compliance penalties.

Key Market Trends & Insights:

Regional Leadership: The North American document management system market commanded a substantial revenue share of almost 40.0% in 2024, driven by the escalating demand for digital transformation across various industries.

Component Dominance: The software segment held the largest market share, exceeding 67.0% of the revenue in 2024. This dominance is attributed to the growing demand for cloud-based, AI-driven, and compliance-ready solutions.

Deployment Preference: The cloud segment led the market with a revenue share of over 67.0% in 2024. This is propelled by the integration of advanced technologies such as Artificial Intelligence (AI), Machine Learning (ML), and Robotic Process Automation (RPA) into cloud DMS platforms.

Enterprise Size Leadership: Large enterprises accounted for nearly 67.0% of the market's revenue share in 2024. This is due to the immense volume of enterprise-grade documents they manage and their critical need for scalable, secure, and intelligent document workflows.

End-Use Sector Dominance: The healthcare segment generated over 23.0% of the market's revenue share in 2024. A significant driver here is the accelerating shift towards Electronic Health Records (EHRs) and paperless systems within the healthcare industry.

Order a free sample PDF of the Document Management System Market Intelligence Study, published by Grand View Research.

Market Size & Forecast

2024 Market Size: USD 7.68 billion

2030 Projected Market Size: USD 18.17 billion

CAGR (2025-2030): 15.9%

North America: Largest market in 2024

Asia Pacific: Fastest growing market

Key Companies & Market Share Insights

Leading companies in the document management system (DMS) industry, including Microsoft, IBM Corporation, Oracle Corporation, Open Text Corporation, and Hyland Software, Inc., are actively engaged in strategic initiatives to enhance their competitive edge. These strategies largely involve new product development, forging partnerships and collaborations, and entering into agreements.

Illustrative of these efforts, in April 2025, Hyland Software, Inc. significantly expanded its product offerings by integrating advanced AI capabilities. Through substantial updates to Hyland Automate, Hyland Knowledge Discovery, and key improvements to Hyland OnBase and Hyland Alfresco, the company aims to provide organizations with sophisticated tools for optimizing content, processes, and application intelligence. Their Hyland Content Intelligence product line is designed to empower businesses with actionable insights derived from simple natural language queries, thereby streamlining complex searches and delivering precise information from vast enterprise content.

Similarly, in March 2025, IBM Corporation launched IBM Storage Ceph as a Service, broadening its suite of flexible on-premises infrastructure solutions. This new service complements IBM Power delivered as a service, offering a distributed compute platform with diverse form factors and adaptable consumption models. The IBM Storage Ceph service facilitates the integration of cloud-based solutions with on-premises environments, providing a unified software-defined storage solution that encompasses block, file, and object data. Its goal is to help organizations eliminate data silos and modernize their data lakes and virtual machine storage, delivering a seamless cloud storage experience within their own data centers.

Further demonstrating industry innovation, in December 2024, OpenText introduced Core Digital Asset Management (Core DAM). This solution is engineered to optimize the digital content supply chain by incorporating powerful features that yield tangible results. Core DAM leverages practical AI to automate tasks such as image tagging, video transcript generation, and the creation of design inspiration images using OpenText Experience Aviator, significantly boosting the efficiency and accuracy of creative workflows. It also provides global content access, enabling users to generate instant links for high-performance display worldwide.

Key Players

Agiloft, Inc.

Alfresco Software Inc.

Cflowapps

DocLogix

Hyland Software, Inc.

IBM Corporation

Integrify

Browse Horizon Databook for Global Document Management System Market Size & Outlook

Conclusion

The document management system (DMS) market is rapidly growing, driven by the need for secure digital information management and paperless transitions. Cloud-based solutions and regulatory compliance are key growth factors. North America leads the market, with software and cloud deployments dominating. Large enterprises and the healthcare sector are major adopters. Leading companies are innovating with AI and strategic collaborations to enhance their offerings.

0 notes

Text

0 notes

Text

0 notes

Text

Transforming Operations with SAP Supply Chain Management

In today's fast-paced and globally connected market, businesses must have agile, responsive, and data-driven supply chains to remain competitive. One of the most powerful tools helping organizations achieve this is SAP Supply Chain Management (SAP SCM). SAP SCM is an advanced solution designed to optimize and integrate every component of the supply chain, enabling businesses to deliver products efficiently, minimize costs, and enhance customer satisfaction.

What is SAP Supply Chain Management?

SAP SCM is part of SAP’s broader suite of enterprise resource planning (ERP) tools. It offers end-to-end visibility and coordination acrosTransforming Operations with SAP Supply Chain Managements all aspects of the supply chain — from planning and sourcing to manufacturing and delivery. By integrating real-time data, predictive analytics, and intelligent automation, SAP SCM allows companies to better forecast demand, manage inventory, streamline logistics, and respond proactively to market changes.

Key Features of SAP SCM

Supply Chain Planning: SAP SCM provides robust tools for demand forecasting, production planning, and capacity management. Its predictive capabilities allow companies to plan resources effectively and reduce overproduction or stockouts.

Supply Chain Execution: This includes modules for warehouse and transportation management, enabling real-time tracking and coordination of goods movement. It helps reduce delivery delays and improves efficiency.

Collaboration: SAP SCM supports seamless collaboration between suppliers, manufacturers, and customers through shared data and integrated workflows. This helps enhance responsiveness and agility.

Analytics and Insights: SAP’s built-in analytics tools help monitor performance, identify bottlenecks, and uncover opportunities for cost savings or service improvements.

Automation and AI Integration: SAP SCM integrates artificial intelligence (AI) and machine learning (ML) to automate routine tasks and offer smart decision-making support.

Benefits of SAP SCM

Implementing SAP Supply Chain Management offers several strategic advantages:

Enhanced Visibility: Real-time data helps businesses make faster, more informed decisions.

Cost Efficiency: By optimizing inventory levels and reducing waste, SAP SCM significantly cuts down operational costs.

Risk Mitigation: With scenario planning and risk analysis features, companies can better prepare for disruptions.

Scalability: SAP SCM can be tailored to fit businesses of all sizes and is scalable as companies grow.

Sustainability: Improved resource management and optimized logistics contribute to more sustainable operations.

Real-World Applications

From manufacturing to retail and logistics, businesses in various sectors use SAP SCM to streamline operations. For instance, a global electronics manufacturer might use it to balance supply and demand across multiple continents, while a retailer can ensure timely restocking and accurate demand forecasting during peak seasons.

Conclusion

SAP Supply Chain Management is more than just a software solution—it's a strategic tool that transforms how companies operate in a dynamic global environment. By integrating key supply chain functions and enabling smarter decisions through data, SAP SCM empowers organizations to build more resilient, efficient, and customer-centric operations.

Whether you're looking to reduce costs, enhance agility, or drive growth, SAP SCM provides the tools and insights needed to make your supply chain a competitive advantage.

0 notes

Text

Consumer Electronics and Auto Industries Boost ETS Market Momentum

The global Electronic Testing Services (ETS) Market was valued at US$ 88.2 billion in 2024 and is forecast to reach US$ 153.6 billion by 2035, expanding at a CAGR of 4.9%. The market is witnessing sustained momentum due to rapid advancements in electronics, increased adoption of connected devices, and the growing importance of robust quality assurance across industries including automotive, telecommunications, healthcare, and consumer electronics.

ETS providers play a critical role in testing electronic products for functionality, durability, compliance, and cybersecurity. With increasing device complexity and end-user demand for high reliability, the ETS landscape is evolving rapidly to accommodate advanced services such as In-Circuit Testing (ICT), Functional Testing, Automated Optical Inspection (AOI), and cybersecurity audits.

Market Drivers & Trends

Rising Complexity of Electronic Devices The demand for end-to-end testing solutions is growing as products become more intricate, incorporating multiple components and advanced functionalities. Complex devices—ranging from smartphones and industrial machines to connected vehicles—require multilayered testing to meet safety, performance, and regulatory standards.

Proliferation of IoT and Connected Devices The surge in Internet of Things (IoT) applications across healthcare, smart homes, industry automation, and transportation is driving the need for robust testing protocols. These devices must be tested for seamless interoperability, network connectivity, and security—challenges that ETS vendors are addressing through more intelligent and automated testing tools.

Cybersecurity and Compliance Requirements With increasing data breaches and system vulnerabilities, manufacturers are relying on ETS providers for comprehensive cybersecurity assessments. This includes penetration testing, vulnerability scanning, and compliance certification for data protection regulations.

Latest Market Trends

Integration of AI in Testing: Artificial intelligence is being embedded into testing systems to predict failures, automate test cases, and improve accuracy in fault detection.

Remote Testing Capabilities: With global supply chains, vendors are developing remote and cloud-based testing solutions to support distributed design and manufacturing operations.

5G and Advanced Communication Modules Testing: As 5G and other advanced communication technologies are deployed, ETS providers are seeing increased demand for specialized testing services for RF modules, antennas, and baseband processors.

Key Players and Industry Leaders

The competitive landscape of the electronic testing services market includes established players that are focusing on innovation, partnerships, and global expansion:

Benchmark Electronics, Inc.

Celestica Inc.

Fabrinet

FLEX LTD.

Global ETS (GETS)

Integrated Micro-Electronics, Inc. (IMI)

Jabil Inc.

Kimball Electronics

PEGATRON Corporation

Plexus Corp.

Sanmina Corporation

SGS SA

Venture Corporation Limited

Zollner Elektronik AG

These companies are investing in automation, software-driven testing tools, and expanding their geographical footprint to cater to increasing demand from end-user industries.

Download Sample PDF Copy: https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=86485

Recent Developments

SGS SA opened an advanced testing facility in Pune, India, in October 2022, focusing on consumer electronics and automotive sectors. The lab supports metallurgy, polymer, environmental, and EMC/EMI testing.

AIM Photonics, in May 2023, launched advanced Opto-electronic Testing Services offering high-precision testing for both photonic and electronic integrated circuits.

Market Opportunities

EV and Autonomous Vehicle Testing: The rise of electric and autonomous vehicles presents a major opportunity for ETS providers to develop specialized test solutions for automotive electronics, battery systems, and LiDAR sensors.

Medical Device Testing: The increasing use of connected and wearable medical devices calls for highly accurate and compliant testing services, especially for patient monitoring and diagnostic applications.

Smart City Infrastructure: With urban digitalization, demand for ETS services for smart grids, surveillance systems, and public transit automation is rising.

Future Outlook

The electronic testing services market is poised for long-term growth, driven by continuous innovation and an expanding range of applications. Players that integrate AI, automation, and cloud technologies into their testing systems will have a competitive edge. Partnerships, M&A activity, and regional expansions will remain key strategies.

Emerging areas like quantum computing, edge AI, and 6G communication protocols may further revolutionize the testing landscape, requiring ETS providers to continually invest in skills and infrastructure.

Market Segmentation

By Service Type:

In-Circuit Testing (ICT)

Functional Testing

Burn-In Testing

Automated Optical Inspection (AOI)

Environmental Testing

Others

By Product Type:

Printed Circuit Boards (PCBs)

Electronic Modules

Displays & Touchscreens

Connectivity Devices

Power Supplies

Sensors & Actuators

Assemblies & Enclosures

By Application:

Automotive (ICE & EVs)

Aerospace & Defense

Consumer Electronics

Industrial Automation

Medical Devices

Telecommunications

Retail Systems

Regional Insights

East Asia dominates the market with a 60.0% share in 2024 and continues to be a growth leader through 2035. The region’s strong manufacturing ecosystem, technological progress, and government support for innovation make it the central hub for ETS.

North America and Western Europe are also significant markets, driven by investments in automotive tech, medical electronics, and advanced communication systems.

South Asia and Southeast Asia are emerging as important markets due to cost-effective manufacturing bases and growing electronics exports.

Why Buy This Report?

In-depth analysis of global and regional market trends

Market size data from 2020 to 2035 with segment-wise breakdowns

Strategic insights on competitive landscape and key player profiles

Technological and regulatory trend evaluation

Identification of growth drivers, opportunities, and barriers

Forecasts on emerging technologies and future testing needs

This report serves as a valuable tool for manufacturers, investors, technology developers, and policy-makers to understand the evolving dynamics of the electronic testing services landscape.

About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

Wireless Power Transmission Market 2032: Is a Global Energy Transformation Underway

TheWireless Power Transmission Market Size was valued at USD 14.14 Billion in 2023 and is expected to reach USD 39.54 Billion by 2032 and grow at a CAGR of 12.1% over the forecast period 2024-2032.

Wireless Power Transmission Market is gaining widespread traction as the demand for cable-free energy transfer grows across industries including consumer electronics, automotive, healthcare, and industrial automation. The shift toward cordless environments is being driven by advancements in resonant inductive coupling, RF technologies, and laser-based systems.

U.S. leading innovations in automotive and consumer electronics sectors are fueling rapid adoption of wireless power solutions

Wireless Power Transmission Market continues to expand as manufacturers prioritize convenience, mobility, and sustainability. As the global push for efficient energy transfer gains ground, companies are investing in scalable and high-efficiency wireless charging solutions designed to enhance user experience and reduce dependency on physical connectors.

Get Sample Copy of This Report: https://www.snsinsider.com/sample-request/6610

Market Keyplayers:

WiTricity Corporation (WiTricity Halo, WiCAD Simulation Software)

Qualcomm (Qualcomm Halo, Qualcomm WiPower)

Leggett and Platt (Qi-compatible wireless Charging Pads, Helios Wireless Power System)

Energizer (Energizer Wireless Charging Pad, Energizer Qi Charger Stand)

Plugless Power Inc. (Plugless L2 EV Charger, Plugless Power Wireless Charging System)

Texas Instruments (bq500212A Wireless Power Transmitter, bq51013B Wireless Power Receiver)

Murata Manufacturing Co., Ltd. (Wireless Power Supply Module LXWS Series, Power Transmitter Unit LXTX Series)

Unabiz Technology (UnaConnect Wireless Power IoT Module, UnaSensors with Energy Harvesting)

Energous Corporation (WattUp Mid Field Transmitter, WattUp PowerBridge)

Ossia Inc. (Cota Real Wireless Power System, Cota Power Receiver)

VoltServer Inc. (Digital Electricity Line Cards, Digital Electricity Gateway Modules)

Market Analysis

The Wireless Power Transmission Market is evolving rapidly due to growing demand for portable devices, electric vehicles (EVs), and smart medical implants. Businesses are shifting to wireless energy systems to enhance safety, minimize wear-and-tear from physical connections, and support design flexibility. The U.S. market leads with robust R&D funding and tech adoption, while Europe accelerates development through green energy policies and industrial automation strategies.

Market Trends

Surge in EV wireless charging systems

Integration of wireless power in smart homes and offices

Growth in medical devices with wireless energy needs

Development of long-range power delivery technologies

Adoption of magnetic resonance and microwave transmission

Partnerships between OEMs and tech startups

Focus on energy efficiency and eco-friendly design

Market Scope

The market holds vast potential as wireless energy transfer extends across industries, enhancing convenience, design freedom, and system longevity. Key scope areas include:

Wireless charging pads for consumer devices

Dynamic EV charging infrastructure

Remote energy supply for IoT and industrial sensors

Implantable medical devices with continuous power

Military and aerospace applications requiring contactless power

Integration with AI-based energy management systems

Forecast Outlook

Wireless power transmission is entering a new era of innovation, positioning itself as a key enabler of next-gen technologies. With continued investment in R&D, increasing consumer demand for clutter-free environments, and government incentives promoting green tech, the market is expected to evolve rapidly. As major players scale their offerings and infrastructure adapts to support advanced transmission methods, global adoption is set to surge—particularly in North America and Europe where digital ecosystems and sustainability goals align with wireless tech growth.

Access Complete Report: https://www.snsinsider.com/reports/wireless-power-transmission-market-6610

Conclusion

The Wireless Power Transmission Market is reshaping how industries deliver energy—silently, efficiently, and without cords. From powering smart devices in New York to enabling dynamic EV charging in Berlin, wireless technology is no longer futuristic—it's here and expanding fast. Forward-thinking businesses that embrace these innovations will lead the charge toward a more agile, untethered, and energy-smart future.

About Us:

SNS Insider is one of the leading market research and consulting agencies that dominates the market research industry globally. Our company's aim is to give clients the knowledge they require in order to function in changing circumstances. In order to give you current, accurate market data, consumer insights, and opinions so that you can make decisions with confidence, we employ a variety of techniques, including surveys, video talks, and focus groups around the world.

Related Reports:

U.S.A. experiences growing demand for real-time energy monitoring in the Distribution Automation Market

U.S.A drives innovation in wireless gas detection with advanced safety technologies

Contact Us:

Jagney Dave - Vice President of Client Engagement

Phone: +1-315 636 4242 (US) | +44- 20 3290 5010 (UK)

Mail us: [email protected]

#Wireless Power Transmission Market#Wireless Power Transmission Market Scope#Wireless Power Transmission Market Trends

0 notes

Text

Global Nursing Resource Allocation Market is driven by Patient Care Demand

The Global Nursing Resource Allocation Market encompasses solutions designed to streamline the distribution and scheduling of nursing staff across healthcare facilities, including hospitals, clinics, and long-term care centers. These platforms integrate real-time data analytics, shift-management modules, and workload forecasting tools to ensure optimal nurse-to-patient ratios, reduce overtime costs, and enhance patient outcomes. By leveraging cloud-based software and artificial intelligence algorithms, healthcare administrators gain market insights into staffing patterns and can dynamically adjust resources to meet seasonal fluctuations and emergency needs.

Advantages of these resource allocation systems include improved operational efficiency, reduced burnout among nursing staff, and significant cost savings by minimizing unnecessary labor expenses. As patient acuity levels and care complexity rise globally, the need for advanced Global Nursing Resource Allocation Market solutions becomes paramount. Hospitals seek robust market research-backed tools to maintain compliance with regulatory staffing mandates and to support business growth through higher patient satisfaction scores. Enhanced interoperability with electronic health record (EHR) systems further bolsters data-driven decision-making and promotes seamless workforce collaboration.

The nursing resource allocation market size is expected to reach US$ 4.71 Bn by 2032, from US$ 2.40 billion in 2025, at a CAGR of 10.1% during the forecast period. Key Takeaways Key players operating in the Global Nursing Resource Allocation Market are:

-Cerner Corporation

-Allscripts

-McKesson Corporation

-Optum, Inc.

-IBM

These market players continually invest in research and development to expand their service portfolios, leveraging advanced analytics and AI-driven modules to enhance market share and market growth. Cerner Corporation’s solutions emphasize real-time workload balancing, whereas Allscripts focuses on predictive scheduling to address peak demand periods. McKesson Corporation has integrated resource allocation with its supply chain services, creating a holistic ecosystem for healthcare providers. Optum, Inc. leverages big-data capabilities to offer comprehensive workforce optimization strategies, while IBM incorporates cognitive computing to forecast staffing needs based on historical patient volume and acuity. Collectively, these companies maintain a strong market position by pursuing strategic partnerships, mergers, and acquisitions, facilitating global expansion and solidifying their presence in key regions. Growing demand for automated nursing resource allocation solutions is fueled by increasing labor costs, nurse shortages, and stringent regulatory requirements. Healthcare facilities face market challenges related to managing complex shift rotations, minimizing overtime, and preventing clinician burnout. The adoption of cloud-enabled platforms offers scalable market opportunities, allowing institutions of all sizes to implement sophisticated scheduling and staffing models. As industry trends shift toward value-based care, providers are under pressure to optimize resource utilization while maintaining high-quality patient outcomes. This drives demand for end-to-end solutions that seamlessly integrate with existing EHR systems and payroll infrastructure. Moreover, evolving market dynamics, such as rising chronic disease prevalence and an aging population, underscore the critical need for flexible workforce management tools to support fluctuating patient loads and seasonal care demands.

‣ Get More Insights On: Global Nursing Resource Allocation Market

‣ Get this Report in Japanese Language: 世界の看護資源配分市場

‣ Get this Report in Korean Language: 글로벌간호자원할당시장

‣ Resources- Global Nursing Resource Allocation: An Analysis

0 notes

Text

North America Edge Computing Market Demand, Supply, Growth Factors, Latest Rising Trends and Forecast (2022-2028)

The North America edge computing market is expected to grow from US$ 16,212.71 million in 2022 to US$ 52,976.45 million by 2028. It is estimated to grow at a CAGR of 21.8% from 2022 to 2028.

North America Edge Computing Market

Edge computing operates through a highly distributed network, a design specifically crafted to eliminate the time-consuming round trip to the cloud. This core principle leads to reduced latency and real-time responsiveness, which are essential for enhancing user experience and supporting customer satisfaction in numerous applications. The acceleration of data transmission has become a critical business objective. From online meetings to mission-critical cloud-hosted computation applications, low latency ensures smooth and fast operation. Cumulative small improvements in latency across applications in sectors like healthcare, air traffic control, and combat situations can yield significant network performance improvements.

Low latency underpins a reliable and robust connection, effectively reducing connection loss, delays, lags, and buffers. This capability is vital for many businesses and industries that depend on real-time applications or live streaming, such as banking, diagnostic imaging, navigation, stock trading, weather forecasting, collaboration, research, ticket sales, video broadcasting, and online gaming. Thus, low latency enhances the operational speed at the edge, boosting the demand for edge computing. While all networks have limited bandwidth, particularly wireless communication, edge computing distributes data computation through on-premise smart devices, helping to alleviate these constraints.

Download our Sample PDF Report

@ https://www.businessmarketinsights.com/sample/BMIRE00028905

North America Edge Computing Strategic Insights

Strategic insights for the North America Edge Computing market deliver a data-driven analysis of the industry landscape. This includes an examination of current trends, identification of key players, and an understanding of specific regional nuances. These insights offer actionable recommendations, enabling readers to differentiate themselves from competitors by pinpointing untapped segments or developing unique value propositions. By leveraging data analytics, these insights help industry players anticipate market shifts, benefiting investors, manufacturers, and other stakeholders alike. A future-oriented perspective is indispensable for stakeholders to foresee market changes and position themselves for long-term success in this dynamic region. Ultimately, effective strategic insights empower readers to make informed decisions that drive profitability and achieve their business objectives within the market.

North America Edge Computing Market By Component

Hardware

Software

Services

North America Edge Computing Market By Application

Smart Cities

Industrial Internet of Things

Remote Monitoring

Content Delivery

Augmented Reality and Virtual Reality

North America Edge Computing Market By Enterprise Size

SMEs and Large Enterprises

North America Edge Computing Market By Verticals

Manufacturing

Energy and Utilities

Government

IT and Telecom

Retail and Consumer Goods

Transportation and Logistics

Healthcare

North America Edge Computing Market Regions and Countries Covered

North America

US

Canada

Mexico

North America Edge Computing Market leaders and key company profiles

ADLINK Technology Inc

Amazon Web Services

Dell Technologies

EdgeConnex Inc.

FogHorn Systems

Hewlett Packard Enterprise Development LP (HPE)

IBM Corporation

Litmus Automation, Inc

Microsoft Corporation

Vapor IO, Inc.

About Us:

Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications

0 notes

Text

Plastic Surgery Software Market to Grow on Efficient Patient Management Demand

The Global Plastic Surgery Software Market is estimated to be valued at US$ 1.31 Bn in 2025 and is expected to exhibit a CAGR of 9.01% over the forecast period 2025 to 2032.

Plastic surgery software encompasses specialized platforms designed to streamline clinical workflows, patient management, imaging, and billing processes for aesthetic and reconstructive surgeons. These solutions typically offer electronic medical record (EMR) capabilities tailored to pre- and post-operative tracking, integrated 3D imaging for treatment simulation, appointment scheduling, secure patient communication, and automated revenue cycle management. Plastic Surgery Software Market Insights by adopting these systems, clinics benefit from reduced administrative overhead, enhanced data accuracy, faster patient turnarounds, and improved compliance with healthcare regulations. As demand for minimally invasive procedures rises and competition intensifies, robust software aids in differentiating services, optimizing resource allocation, and ensuring consistent quality of care. The ability to integrate with existing electronic health records and telemedicine solutions further expands the market scope, positioning plastic surgery software as a critical enabler of both operational efficiency and patient satisfaction. Get more insights on,Plastic Surgery Software Market

#Coherent Market Insights#Plastic Surgery Software#Plastic Surgery Software Market#Plastic Surgery Software Market Insights#Aesthetic Surgery Management#Reconstructive Surgery Coordination

0 notes

Text

Collaborative Robots Market Overview: Growth Drivers and Future Prospects

Introduction

The global collaborative robots market, commonly referred to as the cobots market, is witnessing unprecedented growth as industries shift toward more efficient, flexible, and human-friendly automation solutions. Unlike traditional industrial robots, collaborative robots are designed to work safely alongside human operators, making them ideal for diverse industries ranging from manufacturing to healthcare. This article offers an overview of the market, highlighting the major growth drivers and projecting its future prospects.

1. Understanding Collaborative Robots

Collaborative robots are designed with sensors, safety mechanisms, and smart software that allow them to interact with humans without the need for protective barriers. They can be easily programmed and redeployed, making them particularly appealing for small and medium enterprises (SMEs). These robots typically assist with repetitive or ergonomically challenging tasks, improving workforce productivity and safety.

2. Key Market Drivers

a. Rising Demand for Automation

One of the major forces behind cobot adoption is the growing demand for automation. Companies are seeking to reduce labor costs, increase efficiency, and minimize human error. Collaborative robots provide a flexible, cost-effective solution that doesn't require the significant infrastructure changes associated with traditional robotics.

b. Labor Shortages and Workforce Augmentation

With an aging population in many industrialized nations and ongoing labor shortages in skilled trades, cobots offer a solution that augments human labor rather than replacing it outright. Their ability to take over repetitive, tedious tasks allows human workers to focus on more complex responsibilities.

c. Cost Efficiency and ROI

Compared to traditional industrial robots, cobots are often more affordable, with quicker return on investment (ROI). Their plug-and-play nature and ease of programming further reduce implementation costs and time, making them ideal for businesses without dedicated robotics teams.

d. Improved Safety Standards

Enhanced safety features in cobots, such as force limiting and real-time sensing, have made them increasingly viable in open production environments. Compliance with international safety standards (like ISO/TS 15066) has further boosted user confidence and market adoption.

3. Emerging Applications

Cobots are no longer limited to large manufacturing firms. Industries across the board are integrating collaborative robots into their operations:

Automotive: Assisting in assembly, painting, and quality inspection.

Electronics: Handling delicate components and performing precision tasks.

Healthcare: Supporting surgical procedures and laboratory automation.

Food & Beverage: Managing packaging and repetitive processes.

Logistics: Sorting, packing, and handling inventory in warehouses.

The growing scope of applications is rapidly expanding the collaborative robots market.

4. Technological Advancements Fueling Growth

New technological integrations are transforming cobots from simple task performers to intelligent collaborators. Key innovations include:

Artificial Intelligence (AI) for adaptive behavior and predictive maintenance.

Machine Vision Systems for complex inspection and quality assurance.

Natural Language Processing (NLP) for intuitive human-machine communication.

Cloud-Based Connectivity for centralized monitoring and updates.

These advancements are making cobots smarter, safer, and more versatile, boosting their value across diverse sectors.

5. Market Size and Growth Forecast

As of the mid-2020s, the global collaborative robots market is valued in the multi-billion-dollar range and is projected to expand at a compound annual growth rate (CAGR) exceeding 25% through 2030. Asia-Pacific is expected to dominate market share, driven by rapid industrialization and automation in countries like China, Japan, and South Korea. North America and Europe follow closely due to strong innovation ecosystems and high labor costs.

6. Opportunities and Future Outlook

The future of the collaborative robots market appears bright, with several growth avenues:

SME Adoption: As cobots become more affordable and easier to integrate, small businesses will increasingly deploy them to remain competitive.

Healthcare Sector: The use of cobots in surgery, diagnostics, and rehabilitation presents a significant opportunity.

Remote Operation and Telepresence: Cobots may evolve to support remote work scenarios and virtual human-machine collaboration.

Educational Integration: Universities and vocational institutes are beginning to use cobots to train the future workforce, boosting long-term market adoption.

As the technology matures, collaborative robots will become even more autonomous and integrated into smart factory ecosystems.

Conclusion

The collaborative robots market is at the forefront of the next wave of industrial automation. With benefits like cost savings, ease of use, and the ability to work alongside humans, cobots are well-positioned to revolutionize both manufacturing and non-manufacturing sectors. Continued innovation, combined with expanding awareness and regulatory support, will ensure that cobots play a central role in the future of work across the globe.

0 notes

Text

Intelligent Flexible Manufacturing System Market Growth Analysis, Market Dynamics, Key Players and Innovations, Outlook and Forecast 2025-2032

In 2024, the global Intelligent Flexible Manufacturing System market is valued at approximately US$ 1,380.20 million, and it is projected to reach US$ 1,844.77 million by 2031, growing at a CAGR of 3.97% over the forecast period 2025–2031.

The Intelligent Flexible Manufacturing System (IFMS) is an advanced manufacturing approach that integrates smart automation technologies with flexible production processes to enable real-time adaptability in manufacturing operations. It combines robotics, machine learning, industrial IoT (IIoT), and digital twins to manage manufacturing tasks with high efficiency, agility, and precision. IFMS is designed to handle varying product types and volumes without extensive manual reconfiguration, thereby supporting mass customization, improving resource utilization, and minimizing production downtime.As the manufacturing industry has been embracing the era of Industry 4.0, the demand for intelligent and adaptive production systems has been growing. Intelligent Flexible Manufacturing System (IFMS) has been in the forefront of this transformation acting as an next-generation solution that combines automation, real-time data analytics, machine learning, and interconnected machinery to optimize production efficiency, adaptability, and decision-making. IFMS is redefining traditional manufacturing by enabling rapid shifts in production lines, customized output, and minimal downtime, addressing the growing need for agile and resilient operations in a volatile global market.

The global IFMS market is witnessing robust growth, driven by increased investment in smart factories, rising labor costs, technological advancements in AI and IoT, and the urgent need to enhance operational efficiency.

Key components typically include automated material handling systems, CNC machines, supervisory control software, and data analytics tools. This makes IFMS an essential part of Industry 4.0, playing a critical role in transforming traditional factories into smart factories.

Market Size

Regional Market Size (2024–2031)

North America: $390.33 million (2024) to $494.41 million (2031); CAGR of 3.09%.

Asia-Pacific: $607.02 million (2024) to $839.88 million (2031); CAGR of 4.76%.

This growth is primarily driven by increased adoption of Industry 4.0, rising demand for agile manufacturing, and strong governmental support in developing smart manufacturing hubs.

Market Dynamics (Drivers, Restraints, Opportunities, and Challenges)

Drivers

Rise of Industry 4.0 and Smart Factory Adoption

Industry 4.0 adoption and smart factory initiatives are driving the global market for Intelligent Flexible Manufacturing Systems (IFMS). Businesses are creating highly adaptable, networked production environments by combining technologies like robotics, AI, and the Internet of Things. For instance, the Siemens Amberg Electronics Plant in Germany produces over 1,000 product variants with 99.99% quality consistency using real-time analytics and a digital twin. Similar to this,GE's Brilliant Factories increase throughput and decrease unscheduled downtime by leveraging machine learning and predictive analytics. To handle custom orders, react to changing demand, and switch between product types with ease, these smart factories depend on IFMS. Additionally, the systems facilitate real-time production monitoring, energy optimization, and predictive maintenance, converting conventional plants into resilient, agile, and efficient operations. Investing in IFMS is becoming crucial for manufacturers to remain competitive in a global market that is changing quickly as they strive for efficiency, personalization, and shorter lead times.

Restraints

High Initial Investment and Integration Complexity

The high initial implementation costs and intricate system integration are two of the main obstacles to the Intelligent Flexible Manufacturing System (IFMS) market's promising growth. Advanced robotics, AI-powered software, IoT infrastructure, and qualified staff are all necessary for the deployment of IFMS. These expenses may be unaffordable for small and medium-sized businesses (SMEs), which would prevent widespread adoption.Additionally, integrating IFMS into existing manufacturing environments often involves overhauling legacy systems, which can disrupt operations and require extensive customization. For example, businesses switching from conventional production lines to intelligent systems might experience problems with data migration, compatibility, and extended training times. Older automotive plants serve as an example, where switching to flexible manufacturing systems necessitates reconfiguring both hardware and control software, which is costly and time-consuming.

Opportunities

Growing Demand for Mass Customization and Agile Manufacturing

As consumer preferences shift toward personalized products from made-to-order sneakers to custom smartphones, manufacturers are looking for systems that can quickly adapt to varying designs, batch sizes, and delivery schedules without sacrificing efficiency. IFMS enables production lines to switch between different product types with minimal downtime. For example, Nike's advanced manufacturing centers use flexible systems to produce customized footwear at scale, reducing lead times while enhancing customer satisfaction. Similarly, Tesla's Gigafactories employ adaptive manufacturing setups to quickly switch between different EV models and battery components in response to market demand. These factors represent a significant opportunity for the Intelligent Flexible Manufacturing System (IFMS) market.

Challenges

Skill Gaps and Workforce Readiness

The absence of a trained workforce capable of overseeing and maintaining sophisticated, intelligent production systems is one of the major issues confronting the Intelligent Flexible Manufacturing System (IFMS) market. The need for technicians, engineers, and operators skilled in digital tools has increased as manufacturing becomes more reliant on technologies like AI, machine learning, and IoT. However, many businesses have trouble finding talent with the requisite knowledge of data analytics, system programming, and robotics integration, particularly in traditional manufacturing hubs.For instance, according to a Manufacturing Institute survey, skill shortages may result in the loss of over 2 million manufacturing jobs in the United States by 2030. This lack of talent lowers the effectiveness of IFMS systems, delays implementation, and raises training expenses. Manufacturers may encounter major obstacles in utilizing the full potential of intelligent flexible manufacturing if they do not make strategic investments in workforce development and upskilling initiatives.

Regional Analysis

The Intelligent Flexible Manufacturing System (IFMS) market is experiencing strong regional momentum, led by Asia-Pacific, North America, and Europe each driven by distinct industrial strengths and strategic initiatives. Due to the enormous manufacturing bases in China, Japan, and South Korea as well as government initiatives like "Made in China 2025" and Japan's Society 5.0, which support intelligent and adaptable production systems, Asia-Pacific has a dominant market share. For example, Huawei's Smart Factory in Dongguan uses IoT and AI to instantly adjust to changing production demands.The use of Industry 4.0 technologies in industries like aerospace and automotive is driving North America's rapid growth. To effectively manage model variations and production scale-ups, businesses such as Tesla and Boeing are investing in flexible automation.High-end, precision-driven smart manufacturing is the focus of Europe, with Germany at the forefront. Companies like Siemens and Bosch are leading the way in advanced IFMS with integrated digital twins and cyber-physical systems thanks to initiatives like Industrie 4.0.

Competitor Analysis (in brief)

Competitor Analysis

In order to obtain a competitive advantage, major players in the fiercely competitive global market for intelligent flexible manufacturing systems (IFMS) are concentrating on technological innovation, strategic partnerships, and industry-specific customization. Leading firms at the forefront of creating integrated, AI-powered, and modular manufacturing solutions include Siemens AG,Fanuc Corporation, ABB Ltd, Rockwell Automation, and Mitsubishi Electric. For instance, with its Digital Enterprise Suite, Siemens has extended its digital manufacturing ecosystem, allowing for flexibility and end-to-end automation across production lines. Renowned for its proficiency in robotics, Fanuc provides intelligent manufacturing cells that can adjust to shifting production requirements with little assistance from humans. PTC and Rockwell Automation have teamed up to provide smart manufacturing platforms that combine augmented reality, real-time analytics, and industrial control systems.

January 18, 2023 Schneider Electric successfully acquired AVEVA, a top supplier of industrial software. The goal of this merger is to improve Schneider's digital transformation and industrial automation skills. October 02, 2023, Rockwell Automation strengthened its position in industrial automation and smart manufacturing by acquiring Clearpath Robotics and its subsidiary OTTO Motors, which specializes in autonomous mobile robots.

Global Intelligent Flexible Manufacturing System: Market Segmentation Analysis

This report provides a deep insight into the global Intelligent Flexible Manufacturing System, covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size, competitive landscape, development trend, niche market, key market drivers and challenges, SWOT analysis, value chain analysis, etc.

The analysis helps the reader to shape the competition within the industries and strategies for the competitive environment to enhance the potential profit. Furthermore, it provides a simple framework for evaluating and assessing the position of the business organization. The report structure also focuses on the competitive landscape of the Global Intelligent Flexible Manufacturing System. This report introduces in detail the market share, market performance, product situation, operation situation, etc., of the main players, which helps the readers in the industry to identify the main competitors and deeply understand the competition pattern of the market.

In a word, this report is a must-read for industry players, investors, researchers, consultants, business strategists, and all those who have any kind of stake or are planning to foray into the Intelligent Flexible Manufacturing System in any manner.

Market Segmentation (by Component)

Hardware

Robots

CNC Machines

Automated Storage and Retrieval Systems (ASRS)

Others

Software

Manufacturing Execution Systems (MES)

Enterprise Resource Planning (ERP)

Product Lifecycle Management (PLM)

Others

Market Segmentation (by Technology)

Industrial Internet of Things (IIoT)

Artificial Intelligence (AI) and Machine Learning

Additive Manufacturing

Digital Twin & Simulation

Others

Market Segmentation (byApplication)

Automated Assembly Lines

Precision Machining

Quality Inspection & Testing

Material Handling & Logistics

Others

Market Segmentation (by End Use Industry)

Automotive

Aerospace & Defense

Electronics & Semiconductors

Healthcare & Medical Devices

Consumer Goods

Industrial Machinery

Others

Key Company

United Faith Auto-Engineering

Guangzhou Risong Technology

TianJin ASSET Industrial

Dalian Auto-Tech

CBWEE

Demc

AUTOMATE

Sinylon

AUTOBOX

Intelitek

Mazak

Hitachi Seiki

Toyoda

OKUMA

Fanuc

Edibon

Yawei

Beijing Jingdiao Group

Dongguan GKG

Nanjing Gongda CNC Technology

DOLANG Technology

Jingyan Seiko Machinery

Omron

Fastems

Leidos

DKSH

Rile Group

Fujian Mingxin

Geographic Segmentation

North America: US, Canada, Mexico

Europe: Germany, France, U.K., Italy, Russia, Nordic Countries, Benelux, Rest of Europe

Asia: China, Japan, South Korea, Southeast Asia, India, Rest of Asia

South America: Brazil, Argentina, Rest of South America

Middle East & Africa: Turkey, Israel, Saudi Arabia, UAE, Rest of Middle East & Africa

FAQ

▶ What is the current market size of Intelligent Flexible Manufacturing System?

As of 2024, the market size is valued at US$ 1,380.20 million and is projected to reach US$ 1,844.77 million by 2031.

▶ Which are the key companies operating in the Intelligent Flexible Manufacturing System market?

Major players include Mazak, Fastems, Okuma, United Faith Auto-Engineering, Guangzhou Risong Technology, and JTEKT Machinery, among others.

▶ What are the key growth drivers in the Intelligent Flexible Manufacturing System market?

Key growth drivers include the adoption of Industry 4.0, demand for mass customization, automation for cost reduction, and advances in AI and IoT.

▶ Which regions dominate the Intelligent Flexible Manufacturing System market?

Asia-Pacific dominates in terms of growth rate, while North America and Europe maintain strong market shares due to technological leadership.

▶ What are the emerging trends in the Intelligent Flexible Manufacturing System market?

Trends include AI-driven predictive maintenance, cloud-based control systems, modular automation, and increasing focus on cybersecurity in manufacturing environments.

Get free sample of this report at : https://www.intelmarketresearch.com/machines/880/Intelligent-Flexible-Manufacturing-System-Market

0 notes

Text

How Manufacturing ERP Systems Streamline Production Planning

1. Centralized Data for Real-Time Decision Making

Manufacturing ERP systems consolidate data from all departments — production, procurement, inventory, sales, and finance — into a single, unified platform. This centralization provides real-time visibility into:

Raw material availability

Machine and labor capacity

Order pipeline and delivery timelines

This helps production planners make informed decisions quickly, reducing planning errors and improving coordination.

2. Accurate Demand Forecasting

Using historical data and market trends, ERP systems generate highly accurate demand forecasts. This empowers Indian manufacturers to plan production more effectively, minimizing:

Overproduction

Inventory holding costs

Supply chain disruptions

Such forecasting is especially useful in sectors like textiles, pharmaceuticals, and FMCG, where consumer demand fluctuates.

3. Automated Material Requirement Planning (MRP)

An ERP-integrated MRP module automatically calculates material needs based on production schedules and demand forecasts. It initiates procurement at the right time, ensuring:

Raw materials arrive just when needed

Inventory levels remain optimized

Production never halts due to shortages

This is particularly beneficial for just-in-time (JIT) manufacturing models.

4. Dynamic and Real-Time Production Scheduling

Modern ERP systems include AI-enabled or rules-based scheduling tools that adapt in real time to changes in:

Machine availability

Labor shifts and skill sets

Order priorities and delivery deadlines

For Indian industries operating in multi-location plants or dealing with custom manufacturing orders, this level of flexibility is a game-changer.

Key Benefits of ERP in Production Scheduling for Indian Industries

Reduced Downtime: ERP systems support predictive maintenance, allowing machines to be serviced without disrupting production cycles.

Optimized Resource Utilization: Smart scheduling maximizes the use of labor, materials, and equipment, leading to higher throughput.

Faster Time-to-Market: Streamlined operations enable quicker production and delivery, giving manufacturers a competitive edge.

Lower Operating Costs: By reducing manual errors, overtime, and material wastage, ERP systems contribute directly to cost savings.

Regulatory Compliance: ERP solutions come with in-built support for compliance with Indian standards such as GST, ISO, GMP, and FDA, reducing the risk of legal penalties.

To achieve these advantages, many manufacturers are turning to the Best ERP Solutions in India that are tailored to their specific industry requirements and local compliance needs.

Why Indian Industries Are Rapidly Adopting Manufacturing ERP

Government programs like “Make in India”, along with the growth of sectors like automotive, pharmaceuticals, electronics, and defense, are pushing manufacturers to modernize. Manufacturing ERP solutions tailored for Indian conditions offer features such as:

GST compliance and e-invoicing

Multi-currency and multi-location operations

Support for vernacular languages and localized workflows

Mobile access for on-the-go factory management

These systems are no longer a luxury — they are a necessity for digital transformation and global competitiveness.

To support this shift, the Best ERP Software Company India offers solutions designed to streamline every aspect of manufacturing — backed by strong implementation support, training, and local expertise.

Choosing the Right Manufacturing ERP for Your Business

Indian manufacturers should evaluate ERP solutions based on:

Industry-Specific Capabilities: Ensure the ERP has modules tailored for your sector — be it textiles, food processing, or electronics.

Scalability: Choose a system that can grow with your business, whether you’re a small manufacturer or a large enterprise.

Integration Capabilities: Look for seamless integration with existing tools like accounting software, IoT devices, or CRM systems.

User-Friendly Interface: A well-designed UI improves adoption across departments, reducing training time.

Vendor Support: Reliable onboarding, customization, and technical support are crucial for smooth implementation.

Conclusion

Manufacturing ERP systems are revolutionizing how Indian industries plan and execute production. By automating workflows, enabling real-time decision-making, and optimizing resources, ERP solutions empower manufacturers to meet today’s market demands swiftly and cost-effectively.

In a competitive manufacturing environment, investing in the right ERP system is not just an upgrade — it’s a strategic move toward sustainable growth, regulatory compliance, and global success.

0 notes

Text

Programmable Logic Controller Market Set to Hit US$ 17.2 Bn with Strong Demand from Smart Industries

The global programmable logic controller (PLC) market, valued at US$ 11.6 Bn in 2022, is forecast to grow at a CAGR of 4.7% between 2023 and 2031, reaching a market value of US$ 17.2 Bn by the end of 2031, according to the latest industry insights. This growth is propelled by a surge in demand for industrial automation, smart manufacturing, and increased integration of the Industrial Internet of Things (IIoT).

Market Overview: A programmable logic controller (PLC) is a digital computer used to automate electromechanical processes, particularly in manufacturing environments. These devices are integral to the efficient operation of assembly lines, robotic devices, and any activity requiring high-reliability control and ease of programming. With increasing adoption across automotive, food & beverage, chemical, energy & utility, and construction industries, the global PLC market continues to expand in scope and application.

Market Drivers & Trends

The rising trend of smart factories and Industry 4.0 is among the most significant growth drivers. Manufacturers are increasingly adopting automation to reduce operational costs, improve productivity, and enhance precision. PLCs play a critical role in this transformation by allowing control over complex industrial processes with minimal human intervention.

Additionally, the growing need for data-driven decision-making, along with advancements in machine learning and artificial intelligence, is leading to deeper integration of PLCs in industrial settings. As automation becomes central to production and operational strategies, the demand for PLCs is expected to surge further.

Latest Market Trends

One of the most notable trends is the shift toward modular PLCs, which accounted for over 68.2% of the market share in 2022. These PLCs are gaining popularity due to their scalability and suitability for large-scale, complex automation tasks. Modular systems offer higher flexibility, can handle thousands of inputs/outputs, and support multitasking environments—making them ideal for high-volume manufacturing operations.

Another trend is the miniaturization of PLCs, which supports their deployment in compact systems and small machinery, especially in consumer electronics and smaller automated units.

Key Players and Industry Leaders

The competitive landscape is fragmented yet dominated by global industrial automation giants. Leading companies in the PLC market include:

Siemens

Rockwell Automation

Mitsubishi Electric Corporation

Schneider Electric

OMRON Corporation

ABB

Panasonic Corporation

Bosch Rexroth Corporation

Delta Electronics, Inc.

Honeywell International Inc.

These companies continue to drive innovation through strategic partnerships, R&D investments, and product expansions to enhance their market share and global footprint.

Recent Developments

Crouzet, in December 2022, launched Millennium Slim, the slimmest PLC in the world, tailored for compact industrial applications.

In July 2022, OMRON Corporation introduced the CP2E Micro PLC, designed for smaller devices and capable of data collection and machine-to-machine communication. This supports low-cost automation solutions for small- and mid-sized enterprises.

Electronics Corporation of India Limited (ECIL) released its own PLC and SCADA software in May 2022, targeting industrial control applications in Indian manufacturing ecosystems.

These product introductions underline the market’s commitment to technological advancement and responsiveness to evolving industrial demands.

Market Opportunities

The expansion of material handling systems, especially in e-commerce logistics, warehousing, and food processing industries, presents substantial growth potential for PLC integration. In material handling, PLCs streamline storage, movement, and tracking—drastically improving throughput and inventory management.

Additionally, the increasing popularity of energy-efficient manufacturing and sustainability initiatives provides ample opportunity for advanced PLC systems that help monitor and reduce energy consumption across production lines.

Gain a preview of important insights from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=32672

Future Outlook

The future of the programmable logic controller market lies in enhanced interoperability, cloud integration, and edge computing. With greater reliance on smart infrastructure and connected devices, PLCs are expected to evolve into more intelligent, connected controllers.

The incorporation of AI-powered PLCs is expected to revolutionize industrial automation by enabling predictive maintenance, self-diagnosis, and adaptive process control. As PLCs continue to advance, their use will extend beyond industrial sectors into smart cities, transportation systems, and building automation.

Market Segmentation

By Offering:

Hardware: CPU, I/O Modules, Power Supply, Memory System

Software

Services

By Type:

Compact PLC

Modular PLC

Nano, Micro, Small, Medium, and Large PLCs

By Application:

Material Handling

Packaging & Labeling

Process Control

Safety Monitoring

Energy Management

Home & Building Automation

Industrial Equipment Control

By End-use Industry:

Automotive

Energy & Utilities

Food & Beverage

Pharmaceuticals

Construction

Oil & Gas

Semiconductors & Electronics

Regional Insights

Asia Pacific held the largest market share of 36.3% in 2022, led by strong industrial growth in China, Japan, South Korea, and India. The increasing demand for smart manufacturing systems and compact automation solutions in the region is expected to maintain its dominance through 2031.

North America, with a market share of 26.4% in 2022, continues to grow due to early adoption of factory automation and significant investment in smart infrastructure in the U.S. and Canada.

Europe remains a hub for automation technology innovation, with countries like Germany, the U.K., and France focusing on Industry 4.0 implementation across automotive and manufacturing sectors.

Why Buy This Report?

This comprehensive report offers:

Detailed market size, forecast, and growth rate

In-depth competitive landscape and company profiling

Analysis of key market drivers, trends, and opportunities

Region-wise breakdown for strategic decision-making

Porter’s Five Forces, value chain, and trend analysis

Insights into technological developments and their impact

Market segmentation for customized investment strategies

With expert analysis and forward-looking insights, this report serves as a valuable resource for stakeholders, investors, industrial engineers, and policymakers seeking to navigate and capitalize on the fast-evolving programmable logic controller market.

Explore Latest Research Reports by Transparency Market Research: 5G Smart Antenna Market: https://www.transparencymarketresearch.com/5g-smart-antenna-market.html

Solid State Transformer Market: https://www.transparencymarketresearch.com/solid-State-transformer.html

Interactive Display Market: https://www.transparencymarketresearch.com/interactive-display-market.html

GaN Epitaxial Wafers Market: https://www.transparencymarketresearch.com/gan-epitaxial-wafers-market.html

About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

How will changing consumer shopping habits shape the evolution of self-checkout solutions

The Self-Checkout Systems Market was valued at USD 4.62 Billion in 2023 and is expected to reach USD 15.49 Billion by 2032, growing at a CAGR of 14.42% over the forecast period 2024-2032.

Self-checkout Systems Market is rapidly transforming the global retail experience as businesses increasingly invest in automation to enhance efficiency and customer satisfaction. With major supermarkets, convenience stores, and pharmacies adopting these systems, retailers are reducing wait times and labor costs while offering faster and more personalized shopping experiences.

U.S. Market Surge: The U.S. leads global adoption, driven by labor shortages, rising operational costs, and growing consumer preference for self-service technology

Self-checkout Systems Market continues to expand as evolving consumer expectations drive demand for seamless, contactless transactions. The integration of AI, machine vision, and mobile wallet compatibility further strengthens the market, especially in tech-forward regions like North America and Europe.

Get Sample Copy of This Report: https://www.snsinsider.com/sample-request/2784

Market Keyplayers:

NCR Corporation (Self-Checkout Kiosks, POS Systems)

Diebold Nixdorf (Vynamic Software, Self-Service Kiosks)

Toshiba Global Commerce Solutions (Self-Checkout Solutions, POS Terminals)

Zebra Technologies (Self-Checkout Solutions, Mobile Point of Sale)

Panasonic Corporation (Self-Checkout Kiosks, POS Solutions)

Fujitsu Limited (Self-Checkout Systems, POS Terminals)

HP Inc. (Self-Checkout Kiosks, Retail Solutions)

TPI Software (Self-Checkout Software Solutions, Retail Management Software)

Kiosk Information Systems (Self-Checkout Kiosks, Interactive Kiosks)

SZZT Electronics (Self-Checkout Systems, Payment Terminals)

Wincor Nixdorf (Self-Checkout Systems, Cash Management Solutions)

Coinstar (Self-Service Coin Machines, Kiosk Solutions)

VivaKi (Self-Checkout Kiosks, Digital Signage Solutions)

Intuit (Self-Checkout Solutions, Point of Sale Software)

AURES Technologies (Self-Checkout Systems, POS Hardware)

Datalogic (Self-Checkout Scanners, Retail Automation Solutions)

SATO Holdings Corporation (Self-Checkout Solutions, Labeling Solutions)

NEXTEP SYSTEMS (Self-Service Kiosks, Digital Signage)

MHI (Self-Checkout Solutions, Retail Management Software)

PayRange (Mobile Payment Solutions, Self-Service Kiosks)

Market Analysis

Retailers are rethinking their in-store operations to accommodate increasing customer demand for speed and autonomy. Self-checkout systems have emerged as a critical retail technology—streamlining checkout processes and minimizing human error. The pandemic accelerated the shift toward contactless solutions, and that momentum has only intensified post-COVID. Large chains in the U.S. and Europe are deploying scalable self-checkout kiosks to meet rising demand while integrating advanced technologies for fraud detection and user assistance.

Market Trends

Surge in AI-powered checkout systems with item recognition

Growth in mobile and app-based self-scanning solutions

Implementation of biometric authentication and facial recognition

Expansion of hybrid checkout systems (manned + self-checkout)

Focus on theft reduction via weight sensors and computer vision

Integration with loyalty programs and digital coupons

Demand for multilingual interfaces and accessibility features

Market Scope

The market is expanding rapidly beyond grocery stores into sectors like apparel, hardware, and hospitality. Self-checkout systems are no longer limited to big-box retailers; even small businesses are investing in compact and affordable solutions.

Wide adoption in retail, QSR, and airport kiosks

Enhanced data analytics for inventory and footfall tracking

Real-time support via AI chatbots and remote monitoring

Customizable UI to match brand identity and customer demographics

Strong investment in modular, space-saving designs

Forecast Outlook

The future of the Self-checkout Systems Market is highly promising, shaped by innovations in AI, edge computing, and IoT integration. Retailers across the U.S. and Europe are expected to continue prioritizing self-service technologies as a strategic investment. As customer satisfaction, operational agility, and profitability converge, self-checkout will become a core component of retail modernization. Enhanced fraud prevention and real-time data feedback will further solidify its role in retail strategy.

Access Complete Report: https://www.snsinsider.com/reports/self-checkout-systems-market-2784

Conclusion

Self-checkout technology is no longer a novelty—it's a necessity. Retailers seeking to remain competitive must embrace intelligent, user-friendly systems that align with modern consumer expectations. With the U.S. and European markets setting the pace, the self-checkout industry is poised to redefine in-store experiences. The future belongs to fast, frictionless, and flexible retail, and self-checkout systems are leading the way.

Related Reports:

U.S.A Media Asset Management Market Set to Witness Dynamic Growth Across Digital Platforms

U.S.A Intelligent Transportation System Market Poised for Technological Disruption and Growth

U.S.A Conversational Systems Market Witnesses Rising Adoption of AI-Powered Interfaces

About Us:

SNS Insider is one of the leading market research and consulting agencies that dominates the market research industry globally. Our company's aim is to give clients the knowledge they require in order to function in changing circumstances. In order to give you current, accurate market data, consumer insights, and opinions so that you can make decisions with confidence, we employ a variety of techniques, including surveys, video talks, and focus groups around the world.

Contact Us:

Jagney Dave - Vice President of Client Engagement

Phone: +1-315 636 4242 (US) | +44- 20 3290 5010 (UK)

Mail us: [email protected]

0 notes

Text

Global Trends Watch: The Emerging Landscape of eClinical Solutions Market

Introduction

The eClinical Solutions market has emerged as one of the most dynamic and rapidly evolving segments in the global healthcare and pharmaceutical industries. As clinical trials grow in complexity, the demand for sophisticated digital solutions to streamline data collection, management, and analysis has skyrocketed. eClinical solutions — which include systems like Electronic Data Capture (EDC), Clinical Data Management Systems (CDMS), Randomization and Trial Supply Management (RTSM), Clinical Trial Management Systems (CTMS), and electronic patient-reported outcomes (ePRO) — are playing a pivotal role in enhancing the speed, efficiency, and accuracy of clinical trials.

As of 2024, the global eClinical Solutions market is experiencing strong growth, and this trend is expected to accelerate over the coming years, with forecasts suggesting a robust compound annual growth rate (CAGR) through 2032. Let’s take a deep dive into what’s shaping this market, the opportunities it holds, and the challenges it faces.

Market Overview

eClinical solutions represent a suite of digital tools designed to automate and manage clinical trial processes. The increased adoption of these systems is being driven by:

Rising demand for drug and therapy development

Growing complexity of clinical trials

Regulatory emphasis on data accuracy and integrity

The global push for decentralized and virtual trials

With global clinical research spending projected to rise and the competitive need to bring therapies to market faster than ever, eClinical platforms are becoming indispensable for pharmaceutical and biotechnology companies.

Download a Free Sample Report:-https://tinyurl.com/3rhnwvbv

Market Drivers

1. Growing Complexity of Clinical Trials

Clinical trials are becoming increasingly intricate due to the rise of biologics, personalized medicine, and precision therapies. This complexity requires advanced software platforms to manage large datasets, patient recruitment, regulatory compliance, and adaptive trial designs.

eClinical solutions automate many of these tasks, reducing human error, saving time, and providing real-time visibility into trial performance.

2. Increasing Adoption of Decentralized Trials (DCTs)

The COVID-19 pandemic accelerated the adoption of decentralized clinical trials, and that shift is here to stay. These trials rely heavily on digital technologies for remote data collection and monitoring, making eClinical solutions a central part of the modern trial toolkit.

ePRO tools, wearable devices, and remote monitoring platforms — all underpinned by eClinical systems — enable researchers to collect real-time data directly from patients, significantly improving trial efficiency.

3. Regulatory Push for Data Integrity

Global regulatory bodies like the U.S. FDA, EMA, and MHRA are increasingly stringent about data traceability, audit trails, and transparency. eClinical solutions are designed to enforce compliance by providing electronic signatures, validation rules, and automated quality checks, making them essential tools for clinical research teams navigating complex regulatory landscapes.

Market Segmentation

By Product:

Electronic Data Capture (EDC) and Clinical Data Management Systems (CDMS)

Clinical Trial Management Systems (CTMS)

Randomization and Trial Supply Management (RTSM)

Electronic Patient-Reported Outcomes (ePRO)

eCOA (Clinical Outcome Assessment) Solutions

Pharmacovigilance Software

Others

Among these, EDC and CDMS hold the largest market share, but ePRO and decentralized monitoring tools are expected to experience the fastest growth through 2032.

By Delivery Mode:

Web-hosted (On-Demand)

Licensed Enterprise (On-Premise)

Cloud-based (SaaS)

Cloud-based solutions are anticipated to witness significant adoption, thanks to their scalability, lower upfront costs, and enhanced remote collaboration capabilities.

By End User:

Pharmaceutical and Biopharmaceutical Companies

Contract Research Organizations (CROs)

Medical Device Manufacturers

Academic & Research Institutions

Hospitals and Clinics

Pharmaceutical companies remain the dominant consumers of eClinical solutions, while CROs are expected to become increasingly influential as outsourcing trends in clinical research continue.

Regional Insights

North America

North America, particularly the U.S., holds the lion’s share of the eClinical Solutions market. A mature clinical trial ecosystem, high healthcare IT spending, and stringent regulations drive strong adoption in this region.

Europe

Europe is another significant contributor, especially with countries like Germany, the UK, and France focusing on pharmaceutical R&D and large-scale data management frameworks.

Asia Pacific

The Asia Pacific region is poised for the highest growth rate, driven by increased clinical trial outsourcing, an expanding pharmaceutical market, and the digital transformation of healthcare in countries like China, India, South Korea, and Japan.

Industry Trends

AI and Machine Learning Integration