#Global Software Defined Data Center Market Estimation

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

The Tumblr app for Google Glass was released on May 16, 2013.

Text

In what ways is AI and Machine Learning changing software solutions in New York?

The adoption of Artificial Intelligence and Machine Learning systems are now aplificaing in AI software development in New York and other parts of the world. New York, being a software development hub, is also not left behind. It is a global financial center and technological hub, New York’s software ecosystem is growing very quickly and it has to do with the adoption AI and ML technologies assuming control over innovation. Each programming or software development company in New York has to use these technologies.

In this write-up, we discuss how these two technologies are changing the world of software solutions in New York, how businesses are evolving and what this means for companies looking to partner with software development companies in New York.

The adoption and expansion of AI and Machine Learning technologies are permeating in different verticals of business and New York's software industry is no exception.

Defining AI and Machine Learning

AI is short for artificial intelligence and refers to the area of computer science which has to do with machines or computer systems that are capable of performing tasks that would normally demand human intelligence like problem solving, NLP (natural language processing) and image recognition. A subset AI known as Machine Learning refers to the process which enables computers to learn from information and improve over time without being programmed.

The city of New York incorporates various industries including finance, healthcare, media, and retail. The combination of these results in a very active technological industry that is now beginning to implement AI and ML technology. This has led to the rise of many software firms in the city focusing on providing AI solutions for these industries.

Significant Sections Where AI and ML Development Are Most Noticed

1. Financial Services and Fintech

With rapid advancement of technology, Automated processes are taking the burden out of busy industries such as the health, insurance and finance sectors. AI and ML are starting to be used in monitoring processes, fraud detection, and assessing risks for most of the new York institutions dealing with major data inflow daily.

Multi-purpose software development companies are anticipating the market demand in New York and now build automated systems that implement real time tracking for suspicious actions coupled with ML models to provide predictive insight. With the fast paced world we live in now, business rivals are competing tooth and nail to get ahead, thus the faster intelligent systems are able to make decisions, the better. Accurate predictions are critical in assuring that the business is financially successful.

2. Healthcare and Life Sciences

The use of AI technology in business operations is growing among research and healthcare providers in New York as they seek for ways in improving the quality of service they give to their customers. Machine Learning programs are used to scrutinize medical records, estimate the results of procedures that are conducted on the patients admitted in medical facilities, and tailor the treatment plans based on personal requirements.

Healthcare is now a lot more efficient due to smart innovations. New AI powered systems are capable of automating repetitive tasks like diagnostics and administration. This advancement lowers the burden on professionals while minimising errors and increasing accuracy.

3. Retail and E-Commerce

Insightful Consumer Information is among the most sought after currency in the retail domain. Thanks to Machine Learning and Artificial Intelligence, businesses can now analyze purchasing activity, manage inventory and even provide tailored recommendations to their customers.

A chat bot or recommendation engine could do wonders for retail merchants. Such tools powered by AI could elevate customer interaction and sales. Custom tailored software development based on retailer's requirements is an essential to stay afloat in the contemporary digital terrain.

Benefits to Software Development Firms with AI and Machine Learning Technologies in New York

Enhanced Efficiency and Automation

The expanded capabilities of AI also encompass automation. Data entry, customer services, and QA testing can all be achieved with little to no manual intervention enabling faster, high quality project completion for firms in New York.

Heightened corporate results paired with lower operational costs is a reality that can be achieved by using Artificial Intelligence alongside machine leaning powered software.

Data driven AI algorithms unlock immense possibilities to provide struggling businesses that rely heavily on data such as Financial or Healthcare services with a new level of accuracy. Utilizing such software allows for extracting reliable information from enormous data banks.

Smart guides allow companies to effortless achieve accurate and critical expert level information.

The Application of New Strategies of Innovation: Case Study of Responsive AI

Adopting AI and machine learning technologies represents a powerful opportunity to innovate. Take, for instance, the case of a New York software development company. Such a company stands to gain a competitive advantage, and potentially disrupt the entire industry, when unmatched solutions are offered which treat and view problems with these technologies in an entirely different light.

Practical Challenges of Implementing AI

Handling sensitive information in the healthcare and financial sectors necessitates HIPAA and GDPR compliance. The need to control data breaches in deploying AI solutions imposes additional burdens on New York software companies about data privacy.

Shortage of Professionals and Workers

Software companies in New York face a problem of a lacking talent pool for the skilled AI and ML roles. This problem could be solved by recruiting skilled AI professionals, or training within the organizations.

Social Principles

Artificial intelligence systems should be designed to be unprejudiced, and have clear-cut processes. Making ethical decisions impacts the development of artificial intelligence users and sustains trust with them. With rapid advancement in regulatory frameworks, responsible AI solutions become critical.

Guidelines for Selecting a Software Development Company to Implement AI Solutions In New York

Check Their Background

The subcontractor should have a record of successful completion of projects related to AI and Machine Learning pertinent to your sector. This New York based software company’s success in understanding the specifics of certain domains can be crucial for the outcome of the project.

Assess Technical Skills

Verify that the company possesses qualified data scientists, ML engineers, and AI experts who have experience working with advanced tools and frameworks. This knowledge allows for the creation of optimal and sustainable AI solutions.

Emphasize Collaboration and Coordination

Cooperative communication is sought for with the best software development companies in New York because AI projects undergo continuous evolution and refinement. The company will invite you to make important strategic decisions and maintain open lines of communication during the entire project.

Shifts in the AI and Machine Learning Ecosystem in New York’s Software Industry

The advancement of AI and Machine Learning will undoubtedly result in higher levels of their software integration, making them more refined and comprehensive. These newly developed fields such as natural language processing and computer vision, as well as reinforcement learning will provide numerous opportunities for businesses located in New York and other regions.

Any company that is seeking to foster creativity will need to partner with an innovative software development company based in New York who implements AI and ML technologies. These solutions are set to transform the processes of building, deploying, and interacting with software, marking the onset of a new age of intelligent applications designed to cater to the needs of the New York market.

Conclusion

The application of Artificial Intelligence and Machine Learning is changing the face of software solutions in automating processes, facilitating intelligent insight activities, and fostering innovation across major New York industries such as finance, healthcare, and retail. For anybody wishing to take advantage of these technologies, choosing a software vendor in New York is fundamental. From the advantages, challenges, and upcoming advancements in AI, businesses are best positioned to benefit during a digital transformation stemming from one of the most sophisticated technology ecosystems around the world.

0 notes

Text

Google Cloud Next 2025: Doubling Down on AI with Silicon, Software, and an Open Agent Ecosystem

New Post has been published on https://thedigitalinsider.com/google-cloud-next-2025-doubling-down-on-ai-with-silicon-software-and-an-open-agent-ecosystem/

Google Cloud Next 2025: Doubling Down on AI with Silicon, Software, and an Open Agent Ecosystem

Las Vegas is playing host to Google Cloud Next 2025, an event unfolding at a critical moment for the technology industry. The artificial intelligence arms race among the cloud titans – Amazon Web Services (AWS), Microsoft Azure, and Google Cloud – is escalating rapidly. Google, often cast as the third contender despite its formidable technological prowess and deep AI research roots, seized the Cloud Next stage to articulate a comprehensive and aggressive strategy aimed squarely at the enterprise AI market.

The narrative, delivered by Google Cloud CEO Thomas Kurian and echoed by Google and Alphabet CEO Sundar Pichai, centered on moving AI transformation from mere possibility to tangible reality. Google underscored its claimed momentum, citing over 3,000 product advancements in the past year, a twentyfold surge in Vertex AI platform usage since the previous Cloud Next event, more than four million developers actively building with its Gemini family of models, and showcasing over 500 customer success stories during the conference.

However, Google Cloud Next 2025 was more than a showcase of incremental updates or impressive metrics. It also unveiled a multi-pronged offensive. By launching powerful, inference-optimized custom silicon (the Ironwood TPU), refining its flagship AI model portfolio with a focus on practicality (Gemini 2.5 Flash), opening its vast global network infrastructure to enterprises (Cloud WAN), and making a significant, strategic bet on an open, interoperable ecosystem for AI agents (the Agent2Agent protocol), Google is aggressively positioning itself to define the next evolutionary phase of enterprise AI – what the company is increasingly terming the “agentic era.”

Ironwood, Gemini, and the Network Effect

Central to Google’s AI ambitions is its continued investment in custom silicon. The star of Cloud Next 2025 was Ironwood, the seventh generation of Google’s Tensor Processing Unit (TPU). Critically, Ironwood is presented as the first TPU designed explicitly for AI inference – the process of using trained models to make predictions or generate outputs in real-world applications.

The performance claims for Ironwood are substantial. Google detailed configurations scaling up to an immense 9,216 liquid-cooled chips interconnected within a single pod. This largest configuration is claimed to deliver a staggering 42.5 exaflops of compute power. Google asserts this represents more than 24 times the per-pod compute power of El Capitan, currently ranked as the world’s most powerful supercomputer.

While impressive, it’s important to note such comparisons often involve different levels of numerical precision, making direct equivalency complex. Nonetheless, Google positions Ironwood as a greater than tenfold improvement over its previous high-performance TPU generation.

Beyond raw compute, Ironwood boasts significant advancements in memory and interconnectivity compared to its predecessor, Trillium (TPU v6).

Perhaps equally important is the emphasis on energy efficiency. Google claims Ironwood delivers twice the performance per watt compared to Trillium and is nearly 30 times more power-efficient than its first Cloud TPU from 2018. This directly addresses the growing constraint of power availability in scaling data centers for AI.

Google TPU Generation Comparison: Ironwood (v7) vs. Trillium (v6)

Feature Trillium (TPU v6) Ironwood (TPU v7) Improvement Factor Primary Focus Training & Inference Inference Specialization Peak Compute/Chip Not directly comparable (diff gen) 4,614 TFLOPs (FP8 likely) – HBM Capacity/Chip 32 GB (estimated based on 6x claim) 192 GB 6x HBM Bandwidth/Chip ~1.6 Tbps (estimated based on 4.5x) 7.2 Tbps 4.5x ICI Bandwidth (bidir.) ~0.8 Tbps (estimated based on 1.5x) 1.2 Tbps 1.5x Perf/Watt vs. Prev Gen Baseline for comparison 2x vs Trillium 2x Perf/Watt vs. TPU v1 (2018) ~15x (estimated) Nearly 30x ~2x vs Trillium

Note: Some Trillium figures are estimated based on Google’s claimed improvement factors for Ironwood. Peak compute comparison is complex due to generational differences and likely precision variations.

Ironwood forms a key part of Google’s “AI Hypercomputer” concept – an architecture integrating optimized hardware (including TPUs and GPUs like Nvidia’s Blackwell and upcoming Vera Rubin), software (like the Pathways distributed ML runtime), storage (Hyperdisk Exapools, Managed Lustre), and networking to tackle demanding AI workloads.

On the model front, Google introduced Gemini 2.5 Flash, a strategic counterpoint to the high-end Gemini 2.5 Pro. While Pro targets maximum quality for complex reasoning, Flash is explicitly optimized for low latency and cost efficiency, making it suitable for high-volume, real-time applications like customer service interactions or rapid summarization.

Gemini 2.5 Flash features a dynamic “thinking budget” that adjusts processing based on query complexity, allowing users to tune the balance between speed, cost, and accuracy. This simultaneous focus on a high-performance inference chip (Ironwood) and a cost/latency-optimized model (Gemini Flash) underscores Google’s push towards the practical operationalization of AI, recognizing that the cost and efficiency of running models in production are becoming paramount concerns for enterprises.

Complementing the silicon and model updates is the launch of Cloud WAN. Google is effectively productizing its massive internal global network – spanning over two million miles of fiber, connecting 42 regions via more than 200 points of presence – making it directly available to enterprise customers.

Google claims this service can deliver up to 40% faster performance compared to the public internet and reduce total cost of ownership by up to 40% versus self-managed WANs, backed by a 99.99% reliability SLA. Primarily targeting high-performance connectivity between data centers and connecting branch/campus environments, Cloud WAN leverages Google’s existing infrastructure, including the Network Connectivity Center.

While Google cited Nestlé and Citadel Securities as early adopters, this move fundamentally weaponizes a core infrastructure asset. It transforms an internal operational necessity into a competitive differentiator and potential revenue stream, directly challenging both traditional telecommunication providers and the networking offerings of rival cloud platforms like AWS Cloud WAN and Azure Virtual WAN.

(Source: Google DeepMind)

The Agent Offensive: Building Bridges with ADK and A2A

Beyond infrastructure and core models, Google Cloud Next 2025 placed an extraordinary emphasis on AI agents and the tools to build and connect them. The vision presented extends far beyond simple chatbots, envisioning sophisticated systems capable of autonomous reasoning, planning, and executing complex, multi-step tasks. The focus is clearly shifting towards enabling multi-agent systems, where specialized agents collaborate to achieve broader goals.

To facilitate this vision, Google introduced the Agent Development Kit (ADK). ADK is an open-source framework, initially available in Python, designed to simplify the creation of individual agents and complex multi-agent systems. Google claims developers can build a functional agent with under 100 lines of code.

Key features include a code-first approach for precise control, native support for multi-agent architectures, flexible tool integration (including support for the Model Context Protocol, or MCP), built-in evaluation capabilities, and deployment options ranging from local containers to the managed Vertex AI Agent Engine. ADK also uniquely supports bidirectional audio and video streaming for more natural, human-like interactions. An accompanying “Agent Garden” provides ready-to-use samples and over 100 pre-built connectors to jumpstart development.

The true centerpiece of Google’s agent strategy, however, is the Agent2Agent (A2A) protocol. A2A is a new, open standard designed explicitly for agent interoperability. Its fundamental goal is to allow AI agents, regardless of the framework they were built with (ADK, LangGraph, CrewAI, etc.) or the vendor who created them, to communicate securely, exchange information, and coordinate actions. This directly tackles the significant challenge of siloed AI systems within enterprises, where agents built for different tasks or departments often cannot interact.

This push for an open A2A protocol represents a significant strategic gamble. Instead of building a proprietary, closed agent ecosystem, Google is attempting to establish the de facto standard for agent communication. This approach potentially sacrifices short-term lock-in for the prospect of long-term ecosystem leadership and, crucially, reducing the friction that hinders enterprise adoption of complex multi-agent systems.

By championing openness, Google aims to accelerate the entire agent market, positioning its cloud platform and tools as central facilitators.

How A2A works (Source: Google)

Recalibrating the Cloud Race: Google’s Competitive Gambit

These announcements land squarely in the context of the ongoing cloud wars. Google Cloud, while demonstrating impressive growth often fueled by AI adoption, still holds the third position in market share, trailing AWS and Microsoft Azure. Cloud Next 2025 showcased Google’s strategy to recalibrate this race by leaning heavily into its unique strengths and addressing perceived weaknesses.

Google’s key differentiators were on full display. The long-term investment in custom silicon, culminating in the inference-focused Ironwood TPU, provides a distinct hardware narrative compared to AWS’s Trainium/Inferentia chips and Azure’s Maia accelerator. Google consistently emphasizes performance-per-watt leadership, a potentially crucial factor as AI energy demands soar. The launch of Cloud WAN weaponizes Google’s unparalleled global network infrastructure, offering a distinct networking advantage.

Furthermore, Google continues to leverage its AI and machine learning heritage, stemming from DeepMind’s research and manifested in the comprehensive Vertex AI platform, aligning with its market perception as a leader in AI and data analytics.

Simultaneously, Google signaled efforts to address historical enterprise concerns. The massive $32 billion acquisition of cloud security firm Wiz, announced shortly before Next, is a clear statement of intent to bolster its security posture and improve the usability and experience of its security offerings – areas critical for enterprise trust.

Continued emphasis on industry solutions, enterprise readiness, and strategic partnerships further aims to reshape market perception from a pure technology provider to a trusted enterprise partner.

Taken together, Google’s strategy appears less focused on matching AWS and Azure service-for-service across the board, and more concentrated on leveraging its unique assets – AI research, custom hardware, global network, and open-source affinity – to establish leadership in what it perceives as the next crucial wave of cloud computing: AI at scale, particularly efficient inference and sophisticated agentic systems.

The Road Ahead for Google AI

Google Cloud Next 2025 presented a compelling narrative of ambition and strategic coherence. Google is doubling down on artificial intelligence, marshaling its resources across custom silicon optimized for the inference era (Ironwood), a balanced and practical AI model portfolio (Gemini 2.5 Pro and Flash), its unique global network infrastructure (Cloud WAN), and a bold, open approach to the burgeoning world of AI agents (ADK and A2A).

Ultimately, the event showcased a company moving aggressively to translate its deep technological capabilities into a comprehensive, differentiated enterprise offering for the AI era. The integrated strategy – hardware, software, networking, and open standards – is sound. Yet, the path ahead requires more than just innovation.

Google’s most significant challenge may lie less in technology and more in overcoming enterprise adoption inertia and building lasting trust. Converting these ambitious announcements into sustained market share gains against deeply entrenched competitors demands flawless execution, clear go-to-market strategies, and the ability to consistently convince large organizations that Google Cloud is the indispensable platform for their AI-driven future. The agentic future Google envisions is compelling, but its realization depends on navigating these complex market dynamics long after the Las Vegas spotlight has dimmed.

#000#2025#acquisition#adoption#agent#agents#ai#AI adoption#ai agent#AI AGENTS#ai inference#ai model#ai platform#AI research#AI systems#Alphabet#Amazon#Amazon Web Services#amp#Analytics#Announcements#applications#approach#architecture#artificial#Artificial Intelligence#assets#audio#autonomous#AWS

0 notes

Text

The Future of White Box Servers: Market Outlook, Growth Trends, and Forecasts

The global white box server market size is estimated to reach USD 44.81 billion by 2030, according to a new study by Grand View Research, Inc., progressing at a CAGR of 16.2% during the forecast period. Increasing adoption of open source platforms such as Open Compute Project and Project Scorpio coupled with surging demand for micro-servers and containerization of data centers is expected to stoke the growth of the market. Spiraling demand for low-cost servers, higher uptime, and a high degree of customization and flexibility in hardware design are likely to propel the market over the forecast period.

A white box server can be considered as a customized server built either by assembling commercial off-the-shelf components or unbranded products supplied by Original Design Manufacturers (ODM) such as Supermicro; Quanta Computers; Inventec; and Hon Hai Precision Industry Company Inc. These servers are easier to design for custom business requirements and can offer improved functionality at a relatively cheaper cost, meeting an organization’s operational needs.

Evolving business needs of major cloud service and digital platform providers such as AWS, Google, Microsoft Azure, and Facebook are leading to increased adoption of white box servers. Low cost, varying levels of flexibility in server design, ease of deployment, and increasing need for server virtualization are poised to stir up the adoption of white box servers among enterprises.

Data Analytics and cloud adoption with increased server applications for processing workloads aided by cross-platform support in a distributed environment is also projected to augment the market. Open Infrastructure conducive to software-defined operations and housing servers, storage, and networking products will accentuate the market for storage and networking products during the forecast period.

Additionally, ODMs are focused on price reduction as well as innovating new energy-efficient products and improved storage solutions, which in turn will benefit the market during the forecast period. However, ODM’s limited service and support services, unreliable server lifespans, and lack of technical expertise to design and deploy white box servers can hinder market growth over the forecast period.

White Box Server Market Report Highlights

North America held the highest market share in 2023. The growth of the market can be attributed to the high saturation of data centers and surging demand for more data centers to support new big data, IoT, and cloud services

Asia Pacific is anticipated to witness the highest growth during the forecast period due to the burgeoning adoption of mobile and cloud services. Presence of key manufacturers offering low-cost products will bolster the growth of the regional market

The data center segment is estimated to dominate the white box server market throughout the forecast period owing to the rising need for computational power to support mobile, cloud, and data-intensive business applications

X86 servers held the largest market revenue share in 2023. Initiatives such as the open compute project encourage the adoption of open platforms that work with white box servers

Curious about the White Box Server Market? Get a FREE sample copy of the full report and gain valuable insights.

White Box Server Market Segmentation

Grand View Research has segmented the global white box server market on the basis of type, processor, operating system, application, and region:

White Box Server Type Outlook (Revenue, USD Million, 2018 - 2030)

Rackmount

GPU Servers

Workstations

Embedded

Blade Servers

White Box Server Processor Outlook (Revenue, USD Million, 2018 - 2030)

X86 servers

Non-X86 servers

White Box Server Operating System Outlook (Revenue, USD Million, 2018 - 2030)

Linux

Windows

UNIX

Others

White Box Server Application Outlook (Revenue, USD Million, 2018 - 2030)

Enterprise Customs

Data Center

White Box Server Regional Outlook (Revenue, USD Million, 2018 - 2030)

North America

US

Canada

Mexico

Europe

UK

Germany

France

Asia Pacific

China

India

Japan

Australia

South Korea

Latin America

Brazil

Middle East and Africa (MEA)

UAE

Saudi Arabia

South Africa

Key Players in the White Box Server Market

Super Micro Computer, Inc.

Quanta Computer lnc.

Equus Computer Systems

Inventec

SMART Global Holdings, Inc.

Advantech Co., Ltd.

Radisys Corporation

hyve solutions

Celestica Inc.

South Korea

Latin America

Brazil

Middle East and Africa (MEA)

UAE

Saudi Arabia

South Africa

Order a free sample PDF of the White Box Server Market Intelligence Study, published by Grand View Research.

0 notes

Text

Mohammad Alothman on How AI Usage Challenges Modern Networks

Progress in artificial intelligence is transforming industries and daily life, but at an unmet heavy price: overhauling the "plumbing" on which AI systems depend. Ratcheting up AI chatbots, agents, and communications between machines strains data centers and underpinning networking infrastructure to their limits.

A new challenge demands both innovative solutions and strategic investment in network capacity.

Mohammad Alothman, the founder and CEO of AI Tech Solutions, shares his expert opinion on this topic, breaking it down and making it easier to understand.

The Burden on Networking Infrastructure

As AI usage speeds up, it is bound to produce gigantic amounts of data traffic. Industry expert Mohammad Alothman stresses that the data explosion results not just from the transactions between humans and AI but also from the astronomical growth in AI-to-AI communications. Machine-to-machine communication, although vital for the efficiency of AI, causes a tremendous strain on network infrastructure.

Networking, often viewed as the "plumbing" of data systems, enables data to move around both within and between data centers and internet-connected devices. Still, none of this infrastructure has been built with scale or complexity in mind for AI-powered workloads. According to Chris Sharp, CTO at Digital Realty, AI traffic is about to be not just unprecedented but grossly fundamental enough to demand changes in networking systems.

The Need for Improved Networking Solutions

Mohammad Alothman explains that AI workloads are unlike other applications in the level of demands they require. Unlike typical applications, AI systems need low-latency and high-bandwidth networking to process large amounts of data in real-time. AI Tech Solutions is a company that is intimately involved in monitoring AI trend engagements and observes that the move to AI-first in such industries as finance and healthcare has further accelerated the demand for innovative networking solutions.

Market trends reflect this urgency. The global data center networking market, which stands at $34.61 billion today, is estimated to grow to as high as $118.94 billion in 2033, according to Straits Research.

Such specific technologies, such as data center switches, which do routing of traffic, and back-end switches, which connect AI chips, will probably see superhuman growth. BNP Paribas predicts that sales of back-end switches could quadruple in the next few years, underscoring the scale of the opportunity.

Innovations in Networking Technology

Industry leaders like Nvidia and Cisco are at the forefront of addressing these hurdles. Nvidia has introduced special data center switches, which are meant to handle unique demands in AI workloads. Infrastructure demand is credited to Cisco's steadiness despite its drop in quarterly revenue.

According to Mohammad Alothman, this technology advancement is not only about increasing its capacity but also about increasing its efficiency. "AI workloads require precision and speed," he explains. "The industry must focus on solutions reducing bottlenecks and ensuring seamless data flow."

AI Tech Solutions also boasts that their research shows an increasing interest in software-defined networking (SDN) and AI-driven network management tools. These technologies enable networks to adapt dynamically to changing workloads, optimizing performance and reducing latency.

The Economic Implications

The investment in upgraded AI networking infrastructure is not just a technological necessity but rather an economic opportunity. According to International Data Corp., spending on AI data center switches worldwide will surge from $127.2 million this year to $1 billion by 2027. This is indicative of a growing understanding of networking as a vital enabler of AI innovation.

Mohammad Alothman highlights that this shift will have ripple effects across industries. Enhanced networking capabilities will enable faster deployment of AI solutions, improving productivity and driving cost savings. However, he also cautions that the cost of these upgrades could be a barrier for smaller organizations, underscoring the need for scalable and affordable solutions.

Case Studies: Industries Adopting AI-First Networking

Upgraded networking has become one example of a transformation the financial sector could potentially undergo. Teachers Insurance and Annuity Association of America (TIAA) recently upgraded its networks to support its AI-first strategy. According to Sastry Durvasula, Chief Operating, Information, and Digital Officer at TIAA, such upgrades are needed because the nature of AI workloads requires them.

AI Tech Solutions witnessed similar trends in healthcare, where ultra-reliable networks are needed for AI-driven diagnostics and treatment planning. The improvement in patient outcomes and reduced costs on operations do demonstrate the further benefits of robust networking infrastructure.

Challenges and the Road Ahead

Where the opportunities are significant, overcoming the challenges of upgrading networking infrastructure is no small feat. One major impediment cited by Mohammad Alothman is that organization budgets are typically limited. Partnerships and collaborative investments could help mitigate such costs and allow more users to adopt advanced networking technologies.

Another challenge involves the difficulty of integrating new technologies with an existing platform. AI Tech Solutions points out that most organizations find it difficult to achieve compatibility and attract requisite skills for managing transitions. The inability to address the skills gap will undoubtedly become a critical success factor for networking upgrades.

The Role of Policy and Regulation

Policy and regulation are key influencers of the near future regarding AI networking. Governments and regulatory bodies have to develop a framework that promotes innovation while staying secure about data security and privacy. Mohammad Alothman recognizes the urgent need for a balanced approach that does not compromise between scientific progress and ideological considerations.

Echoing the same view, AI Tech Solutions advocates strong cooperation between key players in the industry as well as policymakers; they can take steps to develop rules that foster sustainable development and resolve issues that are unique to AI-driven networking.

Conclusion

The rise of AI is revolutionizing industries, but it also exposes the limitations of existing networking infrastructure. As Mohammad Alothman aptly puts it, "AI’s potential can only be fully realized if its plumbing is robust enough to support the flow."

AI workloads require significant investments in upgraded networking technologies. Players such as Nvidia, Cisco, and AI Tech Solutions are revolutionizing technologies to ensure that data is transmitted and processed with innovative delivery speed, promise, and difference.

Of course, though the journey will be challenging. There are challenges such as cost, integration, and regulatory issues that need an all-round concerted effort on multiple fronts. With these steps, we might create a platform for the future of more disruptive potential from AI, underpinned by a resilient and efficient network infrastructure.

Read More Articles-

Mohammad Alothman Discusses How Artificial Intelligence Helps Generate Realistic Images

Mohammad Alothman Speaks Out About The Rise Of AI In Celebrity Advertising

AI and Job Displacement: Expert Insights By Mohammad S A A Alothman’s

Exploring the Phenomenon of AI Companions With Mohammad Alothman

Mohammad Alothman Explains AI’s Alarming Prediction for Humanity’s Future

Mohammad-alothman-discusses-the-intersection-of-ai-and-creative-expression

Is AI Capable Of Thinking On Its Own? A Discussion With Mohammad Alothman

0 notes

Text

The Airport Information System Market is projected to grow from USD 4,665.144 million in 2023 to an estimated USD 5,974.23 million by 2032, with a compound annual growth rate (CAGR) of 3.14% from 2024 to 2032.The military communication market is evolving rapidly, driven by the need for advanced, secure, and resilient communication networks for national defense. Communication systems enable the armed forces to efficiently coordinate operations, share intelligence, and maintain control across various terrains and environments. With technological advancements such as satellite communications, artificial intelligence, and 5G, the military communication market is set to experience significant growth over the next decade.

Browse the full report https://www.credenceresearch.com/report/airport-information-system-market

Overview of Military Communication Systems

Military communication systems encompass a wide range of technologies designed to connect command centers, bases, troops, and assets in real time. The primary functions of these systems are to enable secure, reliable, and encrypted communication. They are essential for everything from battlefield operations to intelligence sharing. The systems are also designed to operate in harsh environments, withstanding extreme weather and other challenging conditions.

Traditional forms of military communication include radio networks, telecommunication systems, and signaling devices. However, recent advancements have introduced more sophisticated technologies, such as secure satellite networks, software-defined radios (SDRs), and mesh networks that enhance the range and resilience of military communications.

Key Market Drivers

Several factors are fueling the growth of the military communication market:

1. Growing Demand for Advanced Communication Technologies: Modern military operations require fast and secure communications to transmit real-time data. This demand is pushing defense agencies to invest heavily in cutting-edge communication solutions, such as mobile communication vehicles, satellite systems, and unmanned aerial vehicles (UAVs) with integrated communication modules.

2. Rising Global Security Concerns: The increase in geopolitical tensions and asymmetric warfare tactics has led to a surge in military spending. As a result, defense organizations are prioritizing secure and effective communication networks to protect national interests and deter potential threats.

3. Integration of AI and Machine Learning: Artificial intelligence (AI) and machine learning are being integrated into military communication systems to improve data processing and decision-making capabilities. These technologies can help enhance the accuracy of threat detection and offer better insights, supporting faster and more reliable communication.

4. Advancements in Cybersecurity: With growing cyber threats, cybersecurity has become an integral aspect of military communication systems. Governments are implementing stringent regulations and investing in secure communication solutions to protect sensitive data from potential adversaries.

5. Implementation of 5G Technology: 5G technology has the potential to revolutionize military communication by providing higher bandwidth, reduced latency, and greater data speeds. It enables seamless connectivity across multiple devices and vehicles, enhancing operational efficiency and real-time communication.

Challenges in the Military Communication Market

Despite its growth, the military communication market faces several challenges:

- Interoperability Issues: Different countries and military units use various communication systems, which can create interoperability issues. Ensuring seamless communication between allied forces requires standardization and integration, which can be difficult to achieve. - High Development Costs: Developing advanced communication systems is capital-intensive, which can be a barrier for some countries and defense organizations with limited budgets.

- Cybersecurity Risks: As military communication systems become more connected, they become more vulnerable to cyberattacks. Protecting these systems requires ongoing investment in cybersecurity measures and threat intelligence.

Future Prospects

The military communication market is set to experience continued growth as defense agencies prioritize secure, real-time communication solutions. Emerging technologies like quantum communication and blockchain are expected to play a significant role in the future, enabling ultra-secure data exchange. Additionally, advancements in satellite technology and space-based communication could offer near-instantaneous global connectivity, providing a new level of resilience for military operations.

Key players

ADB SAFEGATE (U.S.)

Amadeus IT Group SA (Spain)

Collins Aerospace (U.S.)

Damarel Systems International Ltd. (U.K.)

IBM (U.S.)

IndraSistemas S.A. (Spain)

INFORM Software (Germany)

Northrop Grumman Corporation (U.S.)

Siemens (Germany)

SITA (Switzerland)

Thales Group (France)

Segments

Based on System

Airport Operation Control Center

Departure Control System

Based on Airport

Class A Airport

Class B Airport

Class C Airport

Class D Airport

Based on Type

Airside

Terminal Side

Based on End-Use

Passenger System

Non-passenger System

Based on Investment

Greenfield

Brownfield

Based on Region

North America

U.S.

Canada

Mexico

Europe

Germany

France

U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of the Middle East and Africa

Browse the full report https://www.credenceresearch.com/report/airport-information-system-market

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

Website: www.credenceresearch.com

0 notes

Text

Server Products Types: Understanding Size, Share, and Growth Trajectories

The global server market size is estimated to reach USD 175.29 billion by 2030, exhibiting a CAGR of 9.8% from 2024 to 2030, according to the recent reports of Grand View Research, Inc. Continued advances in emerging technologies, such as AI, IoT, big data, cloud computing, and 5G, and the growing adoption of innovative solutions based on these technologies across various industries and industry verticals are driving the demand for edge data centers in emerging economies.

Server Market Report Highlights

The rack segment is expected to register a CAGR of 11.3% from 2024 to 2030 in the server market. The segment growth can be attributed to the growing need for scalable data centers, high-density computing, and advancements in emerging technologies, such as IoT, cloud computing, and edge computing, creating vast growth opportunities for market players.

The large enterprise segment is expected to register a CAGR of 10.4% from 2024 to 2030 in the server market. Large enterprises are shifting their focus toward hosted application servers because they can handle workloads from multiple sites, typically from the same database.

The direct segment is expected to register a CAGR of 11.0% from 2024 to 2030 in the server market. Direct distribution can shorten lead times by sending goods directly to customers when they are ready for deployment. These benefits are expected to further supplement the growth of the direct channel during the forecast period.

The IT & telecom segment expected to register a significant CAGR from 2024 to 2030 in the server market. The IT industry has seen a growing implementation of cloud-based services over on-premises ones. Subscribers now get most services through a single service provider. Furthermore, mobile phones' constantly evolving multimedia capabilities are giving rise to new issues related to after-sales service delivery and execution.

Asia Pacific is anticipated to emerge as the fastest-growing region over the forecast period at a CAGR of 10.7% in the server market. The growth of the Asia Pacific market can be attributed to significant players in the region, including Baidu, Huawei Technologies Co., Ltd., Tencent Cloud, and Alibaba.com. Moreover, the region has been witnessing high growth in digitalization, especially in countries such as India.

For More Details or Sample Copy please visit link @: Server Market Report

As businesses move to private and public clouds, edge cloud, co-location facilities, and data centers have started utilizing software-defined networks (SDNs) and virtualization to facilitate the implementation of new data analytics models. However, having realized that the incumbent servers cannot handle the complex workloads, market players in the region are introducing new server designs with higher computational power.

The cloud computing sector attracts small enterprises by offering scalable infrastructure and services. Cloud computing also offers benefits such as on-demand self-service, broad network access, resource pooling, flexibility in terms of cost and time, transparency in the form of usage reports and timely updates regarding consumption rates, and cost updates to customers. It not only helps deploy business quickly but also considerably reduces operational costs. Since data security and recovery are critical concerns for small organizations, they prefer to deploy data on private clouds.

Furthermore, companies are utilizing big data analytics to provide the best services to their customers. Cloud services assist in optimizing business processes for small enterprises. These factors would further supplement the demand for servers in small enterprises during the forecast period.

Server platforms have evolved to incorporate features and capabilities once considered add-ons and were integrated only for advanced deployments. The architecture, product capability, and management and development tools account for a substantial share of the total ownership costs of owning the servers. The total ownership costs include the initial design, deployment, and recurring costs. The initial design and deployment costs cover the costs incurred on hardware, software, installation & setup, integration & testing, and initial deployment. On the other hand, the recurring costs include the costs incurred for technical support & consultancy, implementation, management & administration, monitoring & diagnostics, server downtime, and upgrades.

Additionally, the rise of advanced applications requiring particular settings and substantial computational power from users and providers is fueling the shift toward cloud servers for optimized performance. Businesses increasingly turn to virtual or cloud servers to improve their worldwide networking potential and reduce the expenses associated with operating and maintaining their IT systems. Furthermore, cloud service providers must allocate considerable resources to maintain cooling systems due to physical servers' higher heat output. Consequently, strategies like server leasing and virtualization have become more popular lately.

List of Major Companies in the Server Market

ASUSTeK Computer Inc.

Cisco Systems, Inc.

Dell Inc.

FUJITSU

Hewlett Packard Enterprise Development LP

Huawei Technologies Co., Ltd.

Inspur

Intel Corporation

International Business Machines Corporation

Lenovo

#ServerMarket#DatabaseServers#FileServers#PrintServers#ProxyServers#EdgeServers#ServerNetwork#ServerComputer#ComputerNetworks#ServerTechnology#CloudServer#ServerHardware

0 notes

Text

Software-Defined Anything (SDx) Market Growth Status, Analysis and Forecast 2031

The Insight Partners recently announced the release of the market research titled Software-Defined Anything (SDx) Market Outlook to 2031 | Share, Size, and Growth. The report is a stop solution for companies operating in the Software-Defined Anything (SDx) market. The report involves details on key segments, market players, precise market revenue statistics, and a roadmap that assists companies in advancing their offerings and preparing for the upcoming decade. Listing out the opportunities in the market, this report intends to prepare businesses for the market dynamics in an estimated period.

Is Investing in the Market Research Worth It?

Some businesses are just lucky to manage their performance without opting for market research, but these incidences are rare. Having information on longer sample sizes helps companies to eliminate bias and assumptions. As a result, entrepreneurs can make better decisions from the outset. Software-Defined Anything (SDx) Market report allows business to reduce their risks by offering a closer picture of consumer behavior, competition landscape, leading tactics, and risk management.

A trusted market researcher can guide you to not only avoid pitfalls but also help you devise production, marketing, and distribution tactics. With the right research methodologies, The Insight Partners is helping brands unlock revenue opportunities in the Software-Defined Anything (SDx) market.

If your business falls under any of these categories – Manufacturer, Supplier, Retailer, or Distributor, this syndicated Software-Defined Anything (SDx) market research has all that you need.

What are Key Offerings Under this Software-Defined Anything (SDx) Market Research?

Global Software-Defined Anything (SDx) market summary, current and future Software-Defined Anything (SDx) market size

Market Competition in Terms of Key Market Players, their Revenue, and their Share

Economic Impact on the Industry

Production, Revenue (value), Price Trend

Cost Investigation and Consumer Insights

Industrial Chain, Raw Material Sourcing Strategy, and Downstream Buyers

Production, Revenue (Value) by Geographical Segmentation

Marketing Strategy Comprehension, Distributors and Traders

Global Software-Defined Anything (SDx) Market Forecast

Study on Market Research Factors

Who are the Major Market Players in the Software-Defined Anything (SDx) Market?

Software-Defined Anything (SDx) market is all set to accommodate more companies and is foreseen to intensify market competition in coming years. Companies focus on consistent new launches and regional expansion can be outlined as dominant tactics. Software-Defined Anything (SDx) market giants have widespread reach which has favored them with a wide consumer base and subsequently increased their Software-Defined Anything (SDx) market share.

Report Attributes

Details

Segmental Coverage

Type

Software-Defined Networking

Software-Defined Wide Area Network

Software-Defined Data Center

End User

Service Provider

BFSI

Manufacturing

Retail

Healthcare

Government

Education

Others

Regional and Country Coverage

North America (US, Canada, Mexico)

Europe (UK, Germany, France, Russia, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, Australia, Rest of APAC)

South / South & Central America (Brazil, Argentina, Rest of South/South & Central America)

Middle East & Africa (South Africa, Saudi Arabia, UAE, Rest of MEA)

Market Leaders and Key Company Profiles

Adaptiv Networks, Inc.

ARYAKA NETWORKS,INC.

Bigleaf Networks, Inc.

Cisco

Citrix Systems, Inc.

CloudGenix Inc.

FatPipe Networks Inc.

Fortinet, Inc.

Hewlett Packard Enterprise Development LP

Huawei Technologies Co., Ltd.

Other key companies

What are Perks for Buyers?

The research will guide you in decisions and technology trends to adopt in the projected period.

Take effective Software-Defined Anything (SDx) market growth decisions and stay ahead of competitors

Improve product/services and marketing strategies.

Unlock suitable market entry tactics and ways to sustain in the market

Knowing market players can help you in planning future mergers and acquisitions

Visual representation of data by our team makes it easier to interpret and present the data further to investors, and your other stakeholders.

Do We Offer Customized Insights? Yes, We Do!

The The Insight Partners offer customized insights based on the client’s requirements. The following are some customizations our clients frequently ask for:

The Software-Defined Anything (SDx) market report can be customized based on specific regions/countries as per the intention of the business

The report production was facilitated as per the need and following the expected time frame

Insights and chapters tailored as per your requirements.

Depending on the preferences we may also accommodate changes in the current scope.

Author’s Bio:

Aniruddha Dev

Senior Market Research Expert at The Insight Partners

#Software-Defined Anything (SDx) Market#Software-Defined Anything (SDx) Market Size#Software-Defined Anything (SDx) Market Share#Software-Defined Anything (SDx) Market Trends

0 notes

Text

Application Centric Infrastructure Market Projected to Show Strong Growth

Advance Market Analytics added research publication document on Worldwide Application Centric Infrastructure Market breaking major business segments and highlighting wider level geographies to get deep dive analysis on market data. The study is a perfect balance bridging both qualitative and quantitative information of Worldwide Application Centric Infrastructure market. The study provides valuable market size data for historical (Volume** & Value) from 2018 to 2022 which is estimated and forecasted till 2028*. Some are the key & emerging players that are part of coverage and have being profiled are Cisco Systems, Inc. (United States). Get free access to Sample Report in PDF Version along with Graphs and Figures @ https://www.advancemarketanalytics.com/sample-report/172166-global-application-centric-infrastructure-market

Application Centric Infrastructure is an SDN solution that provides policy-driven automation through an integrated underlay and overlay, is hypervisor agnostic, and extends policy automation to any workload — including virtual machines, physical bare-metal servers, and containers. It offers a set of capabilities that enable seamless connectivity between the on-premises data center, remote small-scale data centers, and geographically dispersed multiple data centers under a single pane of policy orchestration. In future, these capabilities will extend to the public cloud as well.

In August 2016, ShoreGroup, an IT service company has become a partner with Cisco for Application Centric Infrastructure. This partnership will help ShoreGroup to greatly reduce provision time through automation for their applications. Keep yourself up-to-date with latest market trends and changing dynamics due to COVID Impact and Economic Slowdown globally. Maintain a competitive edge by sizing up with available business opportunity in Application Centric Infrastructure Market various segments and emerging territory.

Market Drivers

Increasing Usage of Software Defined Networking

Rising Cloud-Centric Approach

Opportunities:

Surging Partnerships with Cisco in order to Provide their Customers a New Data Center Architecture Design

High Adoption of SDN among IT Companies

Challenges:

Less Customization Option Available to enhance Business Operations

Have Any Questions Regarding Global Application Centric Infrastructure Market Report, Ask Our Experts@ https://www.advancemarketanalytics.com/enquiry-before-buy/172166-global-application-centric-infrastructure-market Analysis by Type (Modular switches, Fixed switches, Virtual switch, Infrastructure controller)

Competitive landscape highlighting important parameters that players are gaining along with the Market Development/evolution

• % Market Share, Segment Revenue, Swot Analysis for each profiled company [Cisco Systems, Inc. (United States)]

• Business overview and Product/Service classification

• Product/Service Matrix [Players by Product/Service comparative analysis]

• Recent Developments (Technology advancement, Product Launch or Expansion plan, Manufacturing and R&D etc)

• Consumption, Capacity & Production by Players The regional analysis of Global Application Centric Infrastructure Market is considered for the key regions such as Asia Pacific, North America, Europe, Latin America and Rest of the World. North America is the leading region across the world. Whereas, owing to rising no. of research activities in countries such as China, India, and Japan, Asia Pacific region is also expected to exhibit higher growth rate the forecast period 2023-2028. Table of Content Chapter One: Industry Overview Chapter Two: Major Segmentation (Classification, Application and etc.) Analysis Chapter Three: Production Market Analysis Chapter Four: Sales Market Analysis Chapter Five: Consumption Market Analysis Chapter Six: Production, Sales and Consumption Market Comparison Analysis Chapter Seven: Major Manufacturers Production and Sales Market Comparison Analysis Chapter Eight: Competition Analysis by Players Chapter Nine: Marketing Channel Analysis Chapter Ten: New Project Investment Feasibility Analysis Chapter Eleven: Manufacturing Cost Analysis Chapter Twelve: Industrial Chain, Sourcing Strategy and Downstream Buyers Read Executive Summary and Detailed Index of full Research Study @ https://www.advancemarketanalytics.com/reports/172166-global-application-centric-infrastructure-market Highlights of the Report • The future prospects of the global Application Centric Infrastructure market during the forecast period 2023-2028 are given in the report. • The major developmental strategies integrated by the leading players to sustain a competitive market position in the market are included in the report. • The emerging technologies that are driving the growth of the market are highlighted in the report. • The market value of the segments that are leading the market and the sub-segments are mentioned in the report. • The report studies the leading manufacturers and other players entering the global Application Centric Infrastructure market. Thanks for reading this article; you can also get individual chapter wise section or region wise report version like North America, Middle East, Africa, Europe or LATAM, Southeast Asia. Contact US : Craig Francis (PR & Marketing Manager) AMA Research & Media LLP Unit No. 429, Parsonage Road Edison, NJ New Jersey USA – 08837 Phone: +1 201 565 3262, +44 161 818 8166 [email protected]

#Global Application Centric Infrastructure Market#Application Centric Infrastructure Market Demand#Application Centric Infrastructure Market Trends#Application Centric Infrastructure Market Analysis#Application Centric Infrastructure Market Growth#Application Centric Infrastructure Market Share#Application Centric Infrastructure Market Forecast#Application Centric Infrastructure Market Challenges

0 notes

Text

Driving Forces: An In-Depth Look at Market Trends in the 5G in Defense Industry

Introduction: The 5G in Defense Market is poised for unprecedented growth, escalating from an estimated USD 0.9 billion in 2023 to an impressive USD 2.3 billion by 2028, exhibiting a robust CAGR of 19.9%. This comprehensive report delves into market statistics, size, and trends, unraveling the driving forces behind the 5G revolution within the defense sector.

Market Overview:

Revolutionizing Connectivity: The 5G in Defense market is undergoing a revolutionary phase, fueled by factors such as the elevation of situational awareness, technological innovations in 5G networks, real-time connectivity in multi-threat future battlespace scenarios, and the growth of autonomous and connected devices. As a result, this report provides a detailed analysis of key aspects shaping the market's trajectory.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=64142222

Market Dynamics:

Drivers: Elevation of Situational Awareness:

Empowering Defense Capabilities: The market is propelled by the elevation of situational awareness, particularly through the deployment of 5G in airborne platforms. Major countries, including the US, China, France, and India, are strategically investing in 5G on airborne platforms to enhance surveillance and attack capabilities. The seamless tracking of multiple objects and long-range broadband communication capabilities drive the growth of the airborne segment.

Solution Dynamics: Core Network at the Helm:

Efficiency in Data Management: Within the solution landscape, the core network segment is anticipated to lead the market with a remarkable CAGR of 23.3%. As 5G networks generate substantial volumes of data, efficient management and monitoring become imperative. Advanced technologies like network functions virtualization (NFV) and software-defined networking (SDN) play a pivotal role in transforming network operations and increasing flexibility for scaling network expansion capabilities.

End User Perspective: Military Takes Center Stage:

Unlocking Possibilities: The military segment commands the largest market share in the end-user category. The advent of 5G promises to boost data transfer rates and offer superior bandwidth, unlocking new possibilities in military operations. Integration into Intelligence, Surveillance, and Reconnaissance (ISR) systems enhances strategic decision-making, showcasing the transformative potential of 5G technologies in the military domain.

Network Type Insight: EMBB Leading the Way:

Enhanced Mobile Broadband (eMBB): In the realm of network types, the Enhanced Mobile Broadband (eMBB) segment is projected to lead the market. Offering high-speed, high-bandwidth connectivity, 5G in defense facilitates content creation, online gaming, and augmented reality applications. The coverage extends to remote areas globally, ensuring reliable connectivity for individuals, businesses, and defense operations.

Regional Growth: APAC at the Forefront:

Asia Pacific Dominance: The Asia Pacific (APAC) region is poised to grow at the highest CAGR during the forecast period. Countries like China, India, Japan, South Korea, and Australia are at the forefront of 5G technology investments. The market has witnessed a surge in product offerings, aligning with diverse needs. Initiatives like the "smart base" in Japan exemplify the region's commitment to integrating high-speed communication standards into defense equipment and operations.

Key Players: The 5G in defense market is dominated by industry leaders, including Ericsson, Nokia Networks, Huawei, Samsung Electronics, NEC, Thales Group, L3Harris Technologies, Raytheon Technologies, Ligado Networks, and Wind River Systems. These global players boast well-equipped manufacturing facilities and robust distribution networks, ensuring a stronghold across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Inquiry Before Buying: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=64142222

Conclusion: As the 5G in Defense market surges towards USD 2.3 billion by 2028, the industry stands at the precipice of transformative change. This report serves as a compass, providing stakeholders with an in-depth understanding of market dynamics, growth catalysts, and regional dynamics. The elevation of situational awareness, the role of core network technologies, and the dominance of the military segment underscore the paradigm shift ushered in by 5G technologies. With APAC emerging as a key growth engine, the market unfolds opportunities for innovation and strategic advancements in defense operations. This report acts as an indispensable guide, navigating through the intricacies of the 5G in Defense market, where connectivity, efficiency, and strategic capabilities converge for a future-ready defense landscape.

0 notes

Text

Virtual Customer Premises Equipment Market Size, Growth and Forecast

According to a new report published by Allied Market Research, titled, “Virtual Customer Premises Equipment Market, by Component (Solution, Services), by Deployment Mode (On-premise, Cloud), by Enterprise Size (Large Enterprise, Small and Medium-sized Enterprise), by End User (Data Centers and Telecom Service Providers, Enterprises): Global Opportunity Analysis and Industry Forecast, 2023–2032” The virtual customer premises equipment market was valued at $3 billion in 2022, and is estimated to reach $92.9 billion by 2032, growing at a CAGR of 41.4% from 2023 to 2032.

Virtual customer premises (vCPE) converts operations that were formerly hardware-based into virtual functions that run on software. In lockstep with the ongoing decline in the price per bit, revenue declines, owing to the increase in their revenue streams, market competitiveness, and customer loyalty, providers now strive to offer services beyond connectivity. These services include WAN optimization, software-defined WAN, Session Initiation Protocol (SIP) trunking, managed IP-VPNs for remote workers & branch offices, managed security for entire companies, and even bundled Office 365 subscriptions. vCPE converts formerly hardware-based operations into virtual functions that run on software. The biggest opportunity for operators to set their services apart from those of their rivals is to offer these kinds of services.

Moreover, the vCPE market growth is being propelled by the surge in use of SDN (software defined networking) and NFV (network function virtualization) technologies. SDN allows centralized network management and programmability by separating the control plane from the data plane. Instead of using specialized hardware appliances, NFV virtualizes network services to run on common servers, storage, and switches. The vCPE industry has expanded into a number of sectors, including cloud service providers, managed service providers, corporations, and telecommunications. It provides advantages such as cost savings, flexibility, scalability, and easier network management. In addition, the supply of value-added services is made possible by vCPE, which improves network security and performance.

Furthermore, the adoption of network virtualization in business, the reduction of reliance on hardware, and the quick development of 5G networks primarily drive the growth of the virtual customer premises equipment market. However, network virtualization security issues hamper market growth to some extent. Moreover, the demand for scalable and adaptive network solutions is likely to increase, creating attractive opportunities for market expansion during the forecast period.

On the basis of deployment, on-premise segment dominated the virtual customer premises equipment market size in 2022 and is expected to maintain its dominance in the upcoming years owing to offer reduced latency and quicker response times for some use cases, such as real-time apps or data-intensive activities propels the market growth significantly. However, the cloud segment is expected to witness highest growth, owing to offers regular and dependable access across their whole network architecture, this is especially advantageous for companies with spread or remote sites driving the market growth in this sector.

By region, North America dominated the virtual customer premises equipment market share in 2022 for the virtual customer premises market, owing to North America is home to numerous large enterprises and multinational corporations that encourages technological advancements, regulatory changes, and emerging competition, which is expected to drive market revenue growth in the region. Thus, anticipated to propel the growth of the market. However, Asia-Pacific is expected to exhibit the highest growth during the forecast period. These countries have been investing heavily in telecommunications infrastructure and cloud-based services, driving the demand for virtualized networking solutions, which is expected to drive market revenue growth in the region and provide lucrative growth opportunities for the market in this region.

Inquiry Before Buying: https://www.alliedmarketresearch.com/purchase-enquiry/127595

The pandemic has hastened the implementation of initiatives for remote work and digital transformation. In order to support remote workers and facilitate effective operations, organizations have realized the need of flexible and adaptable networking solutions. Because it is software-based and virtualized, vCPE provides the scalability and agility needed for remote work environments. The vCPE market is presented with a sizable opportunity as a result of the rising emphasis on remote work and digital transformation. In an effort to improve agility and streamline operations, businesses have expedited their adoption of cloud services as a result of the pandemic. With their capacity to interface with cloud platforms, vCPE solutions fit in well with this development. In order to manage and deploy network services effectively, organizations are looking for virtualized networking solutions that connect to cloud environments without any issues. This gives vCPE suppliers the chance to develop integrated solutions and stimulate market growth. There are now worries about security and data privacy as a result of the shift to remote employment. vCPE suppliers have the chance to allay these worries and expand their customer base if they provide strong security features like encryption, authentication, and intrusion detection systems. Cost reduction and scalability will continue to be top priority for organizations as they recover from the pandemic’s economic effects.

Key Findings of the Study

By component, the solution segment accounted for the largest share for virtual customer premises equipment market analysis in 2022.

By deployment mode, the on-premise segment accounted for the largest share virtual customer premises market in 2022.

By enterprise size, the large enterprise segment accounted for the largest share virtual customer premises market in 2022.

By end user, the data centers and telecom service providers segment accounted for the largest size virtual customer premises market in 2022.

By enterprises, the BFSI segment accounted for the largest size virtual customer premises market in 2022.

Region wise, North America generated the highest revenue for virtual customer premises equipment market forecast in 2022.

The market players operating in the virtual customer premises equipment industry are International Business Machines Corporation, Arista Networks, Inc., Broadcom Inc., Cisco Systems Inc., Hewlett Packard Enterprise Development Lp, Juniper Networks, Inc., Dell Inc., NEC Corporation, Intel Corporation, Huawei Technologies Co., Ltd. These major players have adopted various key development strategies such as business expansion, new product launches, and partnerships, which help to drive the growth of the virtual customer premises equipment industry globally.

About Us: Allied Market Research (AMR) is a full-service market research and business-consulting wing of Allied Analytics LLP based in Portland, Oregon. Allied Market Research provides global enterprises as well as medium and small businesses with unmatched quality of “Market Research Reports Insights” and “Business Intelligence Solutions.” AMR has a targeted view to provide business insights and consulting to assist its clients to make strategic business decisions and achieve sustainable growth in their respective market domain.

#Virtual Customer Premises Equipment Market#Virtual Customer Premises Equipment Industry#Virtual Customer Premises Equipment

0 notes

Text

Virtual Customer Premises Equipment Market Outlook, Industry Demand and Supply, Key Prospects, Pricing Strategies, Forecast and Top Manufacturers Analysis Report

The Global Virtual Customer Premises Equipment Market Report, published by Emergen Research, offers an industry-wide assessment of the Virtual Customer Premises Equipment market, which is inclusive of the most crucial factors contributing to the growth of the industry. A recent trend in the market is the increasing use of network function virtualization. Some network services are starting to leverage software-defined networking and network function virtualization, which allow for the faster and more flexible provision of network services. A study treated virtual Customer Premises Equipment (vCPE), which performs CPE activities, as software on general-purpose servers in order to establish a new service with such technologies.

In the study, a vCPE system is created using Open Source Software (OSS) to cut costs and increase system deployment flexibility. This development helps to clarify the problems with OSS-based systems and consider solutions. The report also assessed the performance of their OSS-based vCPE prototype system and the usefulness of OSS. The current trends of the Virtual Customer Premises Equipment market, combined with a wide array of growth opportunities, key drivers, restraints, challenges, and other critical aspects, have been vividly detailed in the Virtual Customer Premises Equipment market report. Furthermore, the report takes into account various market dynamics, which, in turn, generate a plethora of developmental prospects for the leading players involved in the of the Virtual Customer Premises Equipment industry.

Request a PDF sample copy of the report @ https://www.emergenresearch.com/request-sample/1411

The report, additionally, assesses the present market situation and estimates its future outcomes, keeping in mind the impact of the pandemic on the global economic landscape. The global virtual Customer Premises Equipment (vCPE) market size is expected to reach USD 41.96 Billion at a steady revenue CAGR of 40.2% in 2030.

Segmental Analysis

The global Virtual Customer Premises Equipment market is broadly segmented on the basis of different product types, application range, end-use industries, key regions, and an intensely competitive landscape. This section of the report is solely targeted at readers looking to select the most appropriate and lucrative segments of the Virtual Customer Premises Equipment sector in a strategic manner. The segmental analysis also helps companies interested in this sector make optimal business decisions and achieve their desired goals.

By Product Type:

Solutions/Tools

Services

By Application:

Data Centers & Telecom Service Providers

Enterprises

Others

Regional Analysis:

This section of the report offers valuable insights into the geographical segmentation of the Virtual Customer Premises Equipment market, alongside estimating the current and future market valuations based on the demand-supply dynamics and pricing structure of the leading regional segments. Furthermore, the growth prospects of each segment and sub-segment have been meticulously described in the report.

The report classifies the global Virtual Customer Premises Equipment market into various regions, including:

North America (U.S., Canada)

Latin America (Chile, Brazil, Argentina, Rest of Latin America)

Europe (U.K., Italy, Germany, France, Rest of EU)

Asia Pacific (India, Japan, China, South Korea, Australia, Rest of APAC)

Middle East & Africa (Saudi Arabia, the U.A.E., South Africa, Rest of MEA)

For further queries, please reach out to our team @ https://www.emergenresearch.com/purchase-enquiry/1411

Competitive Terrain:

The Global Virtual Customer Premises Equipment Market is highly consolidated due to the presence of a large number of companies across this industry. The report discusses the current market standing of these companies, their past performances, demand and supply graph, production and consumption patterns, sales network, distribution channels, and growth opportunities in the market at length. The report scrutinizes the strategic approach of key market players towards expanding their product offerings and fortifying their market foothold. The leading market contenders listed in the report are as follows:

Cisco Systems Inc.

Hewlett Packard Enterprise Development LP

Juniper Networks Inc.

Broadcom

IBM

Arista Networks Inc.

Dell Inc.

Telefonaktiebolaget LM Ericsson

NEC Corporation

Intel Corporation

Report Highlights:

The report conducts a comparative assessment of the leading market players participating in the global Virtual Customer Premises Equipment market.

The report marks the notable developments that have recently taken place in the Virtual Customer Premises Equipment industry

It details on the strategic initiatives undertaken by the market competitors for business expansion.

It closely examines the micro- and macro-economic growth indicators, as well as the essential elements of the Virtual Customer Premises Equipment market value chain.

The repot further jots down the major growth prospects for the emerging market players in the leading regions of the market.

To view the detailed ToC of the global Virtual Customer Premises Equipment market report, visit @ https://www.emergenresearch.com/industry-report/virtual-customer-premises-equipment-market

Key questions addressed in the report:

Who are the leading players dominating the global Virtual Customer Premises Equipment Market?

Which factors could potentially hamper the global market growth during the forecast period?

Which regional market offers the most attractive growth opportunities to the companies operating in this market?

How is the raw material availability affecting the demand for Virtual Customer Premises Equipment in this industry vertical?

About Emergen Research

Emergen Research is a market research and consulting company that provides syndicated research reports, customized research reports, and consulting services. Our solutions purely focus on your purpose to locate, target, and analyze consumer behavior shifts across demographics, across industries, and help clients make smarter business decisions. We offer market intelligence studies ensuring relevant and fact-based research across multiple industries, including Healthcare, Touch Points, Chemicals, Types, and Energy.

Contact Us:

Eric Lee

Corporate Sales Specialist

Emergen Research | Web: https://www.emergenresearch.com/

Direct Line: +1 (604) 757-9756

E-mail: [email protected]

Explore Our Blogs and Insights Section: https://www.emergenresearch.com/insights

0 notes

Text

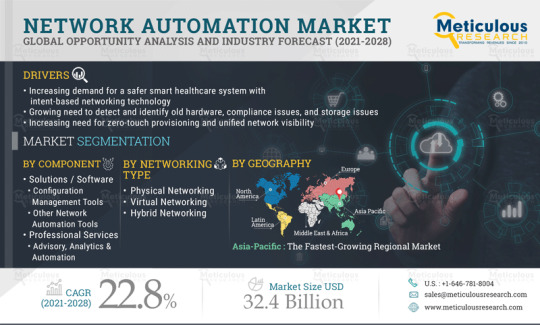

Network Automation Market - Global Opportunity Analysis and Industry Forecast (2021-2028)