#Green and Bio Based Plastic Additive Market

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr has 411 employees.

Text

Rising Demand for Plasticizers and Solvents: A Deep Dive into the 2-Ethylhexanol Industry Landscape

Introduction

2-Ethylhexanol (2-EH) is a branched, eight-carbon fatty alcohol that is predominantly used as a chemical intermediate in the production of plasticizers such as dioctyl phthalate (DOP) and dioctyl adipate (DOA). Its low volatility and excellent solvent properties make it an essential component across various industries, including construction, automotive, paints and coatings, and chemicals.

The global 2-ethylhexanol market is projected to increase from USD 5.63 billion in 2022 to approximately USD 8.28 billion by 2030, registering a compound annual growth rate (CAGR) of 4.95% during the forecast period from 2022 to 2030. This growth is being driven by rising demand for plasticizers, increased use in coatings and adhesives, and growth in end-user industries such as automotive and construction.

Market Overview

Definition and Composition

2-Ethylhexanol is a colorless, combustible liquid with a characteristic odor. It is synthesized primarily by aldol condensation of n-butyraldehyde followed by hydrogenation. As a key intermediate, it plays a vital role in manufacturing a range of industrial chemicals.

Key Applications

Plasticizers (especially DEHP and DINP)

Acrylates and methacrylates

Lubricant additives

Solvents for coatings, adhesives, and inks

Emollients and cosmetics

Market Dynamics

Drivers

Booming Construction and Infrastructure Sector The growing global demand for PVC, especially in developing nations, is boosting the use of 2-EH-based plasticizers.

Automotive Industry Expansion 2-Ethylhexanol is used in automotive sealants and coatings. Increasing vehicle production is directly increasing demand for 2-EH.

Rising Use of Coatings and Adhesives The increase in residential and commercial construction is driving demand for paints and coatings, further fueling the 2-EH market.

Growing Demand for Acrylates With applications in adhesives, textiles, and superabsorbent polymers, acrylates contribute significantly to 2-EH consumption.

Restraints

Environmental and Regulatory Concerns Regulations on phthalate plasticizers due to environmental and health concerns may hinder market growth.

Volatility in Raw Material Prices Fluctuating prices of propylene and butyraldehyde can negatively impact production economics.

Opportunities

Shift Toward Non-Phthalate Plasticizers Growing environmental awareness has encouraged the development of eco-friendly alternatives, offering new avenues for innovation.

Bio-based 2-Ethylhexanol The emergence of bio-based production routes, including fermentation and renewable resources, offers a sustainable growth pathway.

Regional Analysis

Asia-Pacific

Largest and fastest-growing region

Driven by strong demand from China, India, and Southeast Asian nations.

Growing manufacturing base and urban infrastructure development are major contributors.

North America

Robust presence of end-user industries such as automotive and construction.

Environmental regulations promote innovation and green alternatives.

Europe

Established market for coatings, plastics, and chemical manufacturing.

Stringent environmental regulations are pushing the demand for safer plasticizers.

Latin America and Middle East & Africa

Gradual industrialization and infrastructure development.

Emerging markets for plasticizers and coatings with untapped growth potential.

Segmental Analysis

By Application

Plasticizers – Dominates the market with over 60% share.

Acrylates and Methacrylates

Solvents

Lubricant Additives

Others (e.g., cosmetics, pharmaceuticals)

By End-Use Industry

Construction

Automotive

Paints & Coatings

Chemicals

Others (e.g., personal care, packaging)

Request PDF Brochure: https://www.thebrainyinsights.com/enquiry/sample-request/13167

Key Players in the Market

BASF SE

Dow Chemical Company

Eastman Chemical Company

SABIC

LG Chem

INEOS Group

Evonik Industries

OXEA GmbH

Elekeiroz S.A.

China National Petroleum Corporation (CNPC)

These players focus on strategic collaborations, technological innovations, and capacity expansions to strengthen their market presence.

Key Trends

Integration of bio-based production technologies

Increased use of non-phthalate plasticizers

Expansion of manufacturing plants in Asia-Pacific

Collaborations between petrochemical and consumer goods companies

Focus on sustainability and circular economy initiatives

Conclusion

The 2-ethylhexanol market is poised for steady growth in the coming decade, fueled by increasing demand for plasticizers, coatings, and acrylates. As industries move toward sustainability, the shift to bio-based and environmentally safer alternatives offers lucrative opportunities. However, industry players must navigate regulatory hurdles and price volatility to maintain profitability and market share. Strategic investments, regional expansion, and R&D into green alternatives will define the future of this dynamic market.

For Further Information:

Market Introduction

Market Dynamics

Segment Analysis

Some of the Key Market Players

0 notes

Text

Chemical Additives Transforming Concrete Performance – Market Overview & Forecast 2025-2032

Global Chemical Construction Additive Market is experiencing robust growth, with its valuation reaching USD 12.7 billion in 2024. According to the latest industry analysis, the market is projected to grow at a CAGR of 5.7%, reaching approximately USD 19.2 billion by 2032. This expansion is driven by accelerating infrastructure development, urbanization trends, and increasing demand for high-performance construction materials across residential, commercial, and industrial sectors.

Chemical construction additives play a crucial role in enhancing concrete performance, durability, and workability while reducing water consumption and construction timelines. The shift toward sustainable construction practices and the implementation of stricter building codes are significantly boosting market adoption.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/293947/global-chemical-construction-additive-forecast-market-2025-2035-676

Market Overview & Regional Analysis

Asia-Pacific commands the largest market share, accounting for over 45% of global demand, with China and India being primary growth engines. This dominance stems from massive infrastructure projects, smart city initiatives, and rapid urbanization. Government investments in transportation networks and commercial real estate continue to drive consumption of plasticizers, waterproofing agents, and other specialized additives.

North America maintains steady growth through technological innovation and adoption of green building standards like LEED certification. Europe's market benefits from strict environmental regulations promoting sustainable construction materials. The Middle East shows promising growth with mega-projects in the UAE and Saudi Arabia, while Latin America gains momentum through urban renewal programs in Brazil and Mexico.

Key Market Drivers and Opportunities

The market is propelled by three primary factors: the global construction boom, technological advancements in additive formulations, and increasing focus on sustainable building practices. Plasticizers and superplasticizers dominate product demand due to their ability to improve concrete strength while reducing water content by up to 30%. Residential construction accounts for nearly 40% of consumption, followed by infrastructure (35%) and commercial projects (25%).

Emerging opportunities include the development of bio-based plasticizers, self-healing concrete additives, and smart additives with sensing capabilities. The growing skyscraper construction sector presents significant potential for high-performance additives that can withstand extreme loads and environmental conditions.

Challenges & Restraints

The market faces several headwinds including raw material price volatility, lengthy product approval processes, and inconsistent quality standards across regions. Developing countries often lack proper testing facilities, leading to quality concerns. The environmental impact assessment requirements for new additives can delay market entry, while the conservative nature of the construction industry slows adoption of innovative solutions.

Competition from alternative construction methods like prefabrication and modular construction also presents challenges, though these methods often still require specialized additives for optimal performance. The market must balance cost pressures with performance requirements as projects scale globally.

Market Segmentation by Type

Plasticizers

Air-entraining agents

Retarding agents

Waterproofing agents

Others (coloring agents, corrosion inhibitors, flame retardants, and fibers)

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/293947/global-chemical-construction-additive-forecast-market-2025-2035-676

Market Segmentation by Application

Residential

Commercial

Infrastructure

Market Segmentation and Key Players

BASF (Germany)

W.R. Grace (US)

RPM International (US)

Fosroc International (UK)

Dow (US)

Sika (Switzerland)

Mapei (Italy)

Fritz-Pak (US)

PAC Technologies (UAE)

Thermax Global (India)

ATPL (Canada)

Concrete Additives & Chemicals (India)

INNUA (US)

Berolan (Germany)

Hupan (China)

Report Scope

This comprehensive report provides in-depth analysis of the global Chemical Construction Additive Market from 2024 to 2032, offering detailed insights into market dynamics, trends, and growth prospects across all major regions and application segments.

The analysis includes:

Market size and growth projections by value and volume

Detailed segmentation by additive type and end-use application

Manufacturing capacity and utilization rates analysis

Regional demand patterns and growth hotspots

The report also features extensive company profiles covering:

Product portfolios and specifications

Production capabilities and expansion plans

Pricing strategies and gross margin analysis

Market share and competitive positioning

Recent technological developments and innovation pipelines

Our research methodology incorporates primary interviews with industry executives, detailed plant-level analysis, and statistical modeling to ensure the highest data accuracy. The report identifies key success factors, potential risks, and strategic recommendations for stakeholders.

Get Full Report Here: https://www.24chemicalresearch.com/reports/293947/global-chemical-construction-additive-forecast-market-2025-2035-676

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

Plant-level capacity tracking

Real-time price monitoring

Techno-economic feasibility studies

With a dedicated team of researchers possessing over a decade of experience, we focus on delivering actionable, timely, and high-quality reports to help clients achieve their strategic goals. Our mission is to be the most trusted resource for market insights in the chemical and materials industries.

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Follow us on LinkedIn: https://www.linkedin.com/company/24chemicalresearch

Other Related Reports:

0 notes

Text

Bio-based Solketal Market Report: Trends, Opportunities, and Forecast 2025-2031

Bio-based Solketal Market, Global Outlook and Forecast 2025-2032

The global Bio-based Solketal Market is gaining significant traction as industries increasingly shift toward sustainable chemical solutions. Valued at USD 31.60 million in 2023, the market is projected to grow at a CAGR of 4.30%, reaching approximately USD 42.43 million by 2030. This growth trajectory is fueled by rising environmental awareness, stringent regulations supporting bio-based chemicals, and the material's versatility across pharmaceutical, solvent, and industrial applications.

Bio-based solketal, derived from glycerol and acetone, is emerging as a sustainable alternative to petroleum-based solvents. Its excellent solubility and eco-friendly properties make it a preferred choice in pharmaceuticals, cosmetics, and specialty chemical production. As regulatory bodies worldwide push for greener alternatives, manufacturers are investing heavily in bio-based chemical innovations, positioning solketal as a cornerstone of this transition.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/285802/global-biobased-solketal-forecast-market-2025-2032-62

Market Overview & Regional Analysis

Europe currently leads the bio-based solketal market, accounting for 38% of global demand in 2023, driven by the EU's circular economy action plan and REACH regulations. Germany and France are spearheading adoption through tax incentives for bio-based chemical production. Meanwhile, North America's market, valued at USD 8.23 million, benefits from robust pharmaceutical R&D and EPA initiatives promoting sustainable chemistry.

The Asia-Pacific region is poised for the fastest growth (5.1% CAGR) through 2030, with China and India investing heavily in glycerol refining infrastructure to support domestic solketal production. While Latin America and Africa show moderate adoption, their growing chemical industries and improving regulatory frameworks present long-term opportunities.

Key Market Drivers and Opportunities

The market's expansion is primarily driven by three factors: pharmaceutical industry demand (42% of current applications), increasing solvent regulations, and advancements in production technology. The pharmaceutical sector particularly values solketal's purity levels (>99%) for drug formulation, while manufacturers appreciate its compatibility with existing production processes.

Emerging opportunities include applications in biodegradable plastics and green cleaning products, where solketal's low toxicity makes it ideal. The compound's potential as a fuel additive is also being explored, with pilot projects underway in Scandinavia to improve biodiesel performance. Additionally, the growing bioplastics market, projected to reach 3 million tons by 2025, could significantly boost demand.

Challenges & Restraints

Despite positive growth indicators, the market faces hurdles including price volatility in glycerol feedstocks and higher production costs compared to conventional solvents. The industry must also navigate complex certification processes for bio-based products, which can delay market entry. In developing regions, limited awareness about solketal's benefits and established petrochemical supply chains create additional adoption barriers.

Supply chain disruptions remain a concern, as evidenced by the 15% price increase during the 2021-2023 period due to glycerol shortages. Market players are addressing this through vertical integration strategies and long-term supplier contracts.

Market Segmentation by Type

Purity: >98%

Purity: 98%-99%

Purity: ≥99%

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/285802/global-biobased-solketal-forecast-market-2025-2032-62

Market Segmentation by Application

Pharmaceutical Intermediates

Solvent

Others

Competitive Landscape

The market features a mix of chemical conglomerates and specialized producers:

Solvay (Belgium) - Leading production capacity with patented processes

Loba Feinchemie (Germany) - Specializing in pharmaceutical-grade solketal

Zhejiang Boju New Material (China) - Dominating APAC supply

CM Fine Chemicals (Switzerland) - Focus on high-purity formulations

Bioinspir (France) - Innovating sustainable production methods

Report Scope

This comprehensive analysis covers:

Market size and growth projections through 2030

In-depth regional breakdowns (NA, EU, APAC, LATAM, MEA)

Application-specific demand forecasts

Competitive analysis of 15+ key players

Production capacity and technological trends

Regulatory impact assessment

Supply chain and raw material analysis

The report combines primary interviews with industry leaders, proprietary data models, and statistical analysis to provide actionable insights for investors, manufacturers, and end-users navigating this evolving market.

Get Full Report Here: https://www.24chemicalresearch.com/reports/285802/global-biobased-solketal-forecast-market-2025-2032-62

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. Our data-driven insights leverage rigorous methodologies to address key industry factors:

Plant-level production tracking

Real-time price analysis

Techno-economic feasibility studies

With a team of experienced analysts, we deliver actionable market intelligence to support strategic decision-making across the chemical value chain.

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Follow us on LinkedIn: https://www.linkedin.com/company/24chemicalresearch

0 notes

Text

ESBO Plasticizer Market Size, Trends, Forecast, and Competitive Analysis 2025–2032

Definition

Epoxidized Soybean Oil (ESBO) is a bio-based plasticizer derived from soybean oil through the process of epoxidation. It is widely used in PVC products to enhance flexibility, thermal stability, and environmental compatibility. As a renewable, non-toxic alternative to phthalate-based plasticizers, ESBO is increasingly favored in the production of food packaging, medical devices, flooring materials, and toys.

Its applications extend across several industries due to its excellent heat and light stability, compatibility with polymers, and ability to act as a secondary heat stabilizer. ESBO is also approved for use in food contact materials by regulatory agencies like the FDA and EFSA, further supporting its global adoption.

Market Size

📥 Download Sample Report PDF https://www.24chemicalresearch.com/download-sample/290159/global-esbo-plasticizer-forecast-market-2025-2032-38

As of 2023, the global ESBO plasticizer market was valued at USD 298.6 million and is projected to reach USD 422.4 million by 2032, growing at a CAGR of 4.1% over the forecast period. The rising demand for eco-friendly plasticizers and stringent regulations banning hazardous phthalates are driving this growth.

Growth Projections and Trends

The ESBO market has seen robust growth due to rising awareness about environmental sustainability, especially in developed regions. Increasing regulations against phthalates in Europe and North America have significantly shifted industry preferences toward bio-based plasticizers.

Recent trends show a surge in ESBO use within the food packaging and healthcare sectors due to its non-toxic profile. Additionally, innovations in manufacturing processes have reduced costs, making ESBO more accessible to mid-tier manufacturers.

Market Dynamics

Drivers

Stringent Regulatory Frameworks: Ban on DEHP and other phthalates in many countries boosts ESBO adoption.

Rise in Bio-Based Products: Increased focus on renewable resources in manufacturing industries.

Growth in PVC Demand: Rapid urbanization and industrial growth raise the demand for flexible PVC applications, benefitting ESBO.

Restraints

High Production Costs: ESBO is costlier than conventional plasticizers, which may deter price-sensitive markets.

Limited Compatibility: ESBO may not fully replace phthalates in all high-performance applications.

Opportunities

Green Packaging Innovations: Rising demand for sustainable packaging materials provides significant growth potential.

Medical Sector Expansion: Growing usage in IV bags, tubing, and blood storage systems.

Challenges

Raw Material Volatility: Soybean oil prices are influenced by climatic and geopolitical factors.

Performance Constraints: In certain applications, ESBO may require blending with other stabilizers for optimal performance.

Regional Insights

North America: A mature market with strong growth in medical and food-grade PVC applications. The U.S. leads due to FDA approvals.

Europe: High adoption rate driven by REACH and phthalate bans. Germany, France, and the UK are key markets.

Asia-Pacific: Fastest-growing region due to industrial growth in China and India and increasing environmental awareness.

Latin America & MEA: Nascent markets with rising industrialization and regulation compliance shaping future demand.

Competitive Analysis

Key Players

Arkema S.A. – A global leader offering bio-based plasticizer solutions including ESBO for diverse industries.

Galata Chemicals – Known for high-performance plasticizers and polymer additives.

The Chemical Company – Supplies ESBO primarily for food-grade and medical uses.

Emery Oleochemicals – Offers sustainable plasticizers with a focus on green chemistry.

Shandong Longkou Longda Chemical – Major ESBO manufacturer in Asia with a strong export portfolio.

These companies focus on sustainable product lines, global expansion, and R&D in high-performance applications to maintain competitive advantage.

Market Segmentation

By Application

Food Packaging

Medical Devices

Consumer Goods (toys, footwear, flooring)

Automotive Components

Others

By Type

Food Grade ESBO

Industrial Grade ESBO

📘 Get the Complete Report & TOC https://www.24chemicalresearch.com/reports/290159/global-esbo-plasticizer-forecast-market-2025-2032-38

Frequently Asked Questions (FAQs)

1. What is the current market size of the ESBO Plasticizer Market? As of 2023, the global ESBO market stands at USD 298.6 million and is forecasted to reach USD 422.4 million by 2032.

2. What is driving the demand for ESBO? Stringent global regulations against phthalates, growing sustainability trends, and rising demand in the food and medical sectors are key drivers.

3. Which regions are dominating the ESBO market? Europe and North America are leading due to advanced regulatory frameworks and high usage in food and healthcare packaging.

4. Who are the major players in the ESBO market? Key companies include Arkema S.A., Galata Chemicals, The Chemical Company, Emery Oleochemicals, and Shandong Longkou Longda Chemical.

5. What are the key trends to watch in this market? Adoption in green packaging, expansion in medical-grade PVC, and innovations in cost-effective production methods are major trends.

📍 Contact Us 203A, City Vista, Fountain Road, Kharadi, Pune, India - 411014 International: +1(332) 2424 294 Asia: +91 9169162030

🔗 Follow Us on LinkedIn https://www.linkedin.com/company/24chemicalresearch/

About 24Chemical Research

Established in 2015, 24chemicalresearch is a leading provider of high-quality market intelligence in the global chemical industry. Trusted by Fortune 500 clients, our reports deliver accurate data, detailed segmentation, and strategic insights.

0 notes

Text

Emerging Trends and Future Growth Opportunities in the Global Benzaldehyde Market

Benzaldehyde, a colorless liquid with a characteristic almond-like odor, is one of the most significant aromatic aldehydes in the chemical industry. It is commonly used in the production of perfumes, flavors, pharmaceuticals, and plastics, making it an essential raw material for numerous industrial applications. As industries like food and beverage, automotive, and personal care continue to grow, the demand for benzaldehyde has shown a steady rise. However, the benzaldehyde market is also influenced by various factors such as economic shifts, environmental concerns, and technological advancements. This article explores the key dynamics shaping the benzaldehyde market, focusing on trends, challenges, and future opportunities.

Key Drivers of Benzaldehyde Market Growth

Increasing Demand in the Fragrance Industry The fragrance industry is one of the primary consumers of benzaldehyde. It is used in a variety of perfumes, colognes, and air fresheners to add floral, almond, and cherry-like scents. As the global demand for personal care and cosmetics products continues to rise, especially in emerging markets, the demand for benzaldehyde is expected to increase. In addition, the growing trend towards premium and luxury perfumes has provided a boost to benzaldehyde consumption.

Expansion of the Pharmaceutical Sector Benzaldehyde plays a pivotal role in the synthesis of various pharmaceutical compounds. It is used in the production of benzodiazepines, which are commonly prescribed for anxiety and insomnia. The growing global healthcare industry and increasing awareness of mental health issues have resulted in a steady demand for pharmaceutical products containing benzaldehyde. This is particularly significant in regions with aging populations, such as Europe and North America.

Use in Agrochemicals and Plastics Benzaldehyde is also used in the manufacturing of agrochemicals, including pesticides and herbicides. With the global agricultural industry striving to increase food production to meet the demands of a growing population, the need for effective agrochemicals is increasing. Furthermore, benzaldehyde is used in the production of various plastics and resins, contributing to its demand in the packaging and automotive industries.

Rise of Bio-Based and Green Chemicals The increasing preference for sustainable, bio-based products has led to a growing focus on developing benzaldehyde through greener processes. The shift towards renewable feedstocks and more energy-efficient production methods is likely to impact the market. Companies that adopt eco-friendly technologies may have a competitive edge, which could spur further growth in the market.

Challenges in the Benzaldehyde Market

Environmental Regulations and Sustainability Concerns As the benzaldehyde market grows, so do the environmental and regulatory challenges. The production of benzaldehyde, particularly from non-renewable sources, can result in high carbon emissions and other environmental pollutants. In response to these concerns, governments around the world are tightening environmental regulations, pushing manufacturers to invest in cleaner technologies. Companies will have to balance economic efficiency with environmental responsibility, which may increase production costs in the short term.

Fluctuations in Raw Material Prices Benzaldehyde is primarily produced from toluene and other petroleum derivatives. The volatility in oil and gas prices can directly affect the cost of benzaldehyde production. Fluctuating raw material costs can lead to price instability, which may impact the profitability of manufacturers and disrupt the supply chain. This makes it essential for companies to adopt cost-effective and flexible sourcing strategies.

Supply Chain Disruptions Like many industries, the benzaldehyde market has also been susceptible to disruptions in global supply chains, especially in the aftermath of the COVID-19 pandemic. Raw material shortages, logistical bottlenecks, and labor shortages have made it difficult for manufacturers to maintain consistent production. This challenge may continue to affect the global market, especially in regions where raw material procurement and manufacturing processes are heavily reliant on imports.

Opportunities in the Benzaldehyde Market

Growing Demand for Specialty Chemicals The demand for specialty chemicals is one of the key opportunities for the benzaldehyde market. In addition to its use in fragrances and pharmaceuticals, benzaldehyde is also used as a precursor in the production of specialty chemicals, such as dyes and coatings. As industries such as automotive, construction, and textiles continue to expand, the need for specialty chemicals is expected to rise, opening new opportunities for benzaldehyde producers.

Technological Advancements in Production Innovations in the production of benzaldehyde, such as the development of catalytic processes and the use of renewable feedstocks, offer promising growth prospects. Companies that invest in advanced manufacturing technologies can lower production costs, improve product quality, and minimize environmental impact. Furthermore, adopting greener production methods can help businesses comply with stricter regulations and meet the growing consumer demand for sustainable products.

Growth of Emerging Markets Emerging markets, especially in Asia-Pacific and Latin America, present substantial growth potential for the benzaldehyde market. Rapid industrialization, increasing disposable incomes, and a growing middle class in countries like China, India, and Brazil are driving demand for personal care products, pharmaceuticals, and agrochemicals. This trend is expected to continue, providing manufacturers with a large and expanding market.

Conclusion

The benzaldehyde market is poised for steady growth in the coming years, driven by rising demand from the fragrance, pharmaceutical, and agrochemical industries. However, the market is not without its challenges, including environmental regulations, raw material price fluctuations, and supply chain disruptions. Despite these hurdles, opportunities abound, particularly through technological advancements and the growth of emerging markets. As the industry adapts to changing consumer preferences and regulatory frameworks, the benzaldehyde market is likely to witness innovation and continued expansion. Manufacturers that embrace sustainability and invest in new technologies will be well-positioned to capitalize on these opportunities and maintain a competitive edge in the market.

0 notes

Text

Cellulose Acetate Market Expands with Biodegradable Alternatives in Textiles and Cigarette Filters

The cellulose acetate market is experiencing steady growth, driven by rising environmental concerns, increasing demand for biodegradable materials, and a shift away from petroleum-based plastics. Derived from natural cellulose, primarily wood pulp and cotton, cellulose acetate is a thermoplastic polymer known for its strength, transparency, and biodegradability. Its wide range of applications includes textiles, cigarette filters, eyeglass frames, films, and biodegradable packaging.

Market Dynamics

The key driver of the cellulose acetate market is the global push toward sustainable materials. With mounting regulatory pressure to reduce plastic pollution, industries are increasingly adopting bio-based alternatives. Cellulose acetate stands out as an eco-friendly substitute for synthetic polymers, particularly in single-use products. Furthermore, rising awareness among consumers regarding environmental impact has increased demand for biodegradable packaging and personal care products.

In the tobacco industry, cellulose acetate is widely used in cigarette filters. Despite a gradual decline in smoking rates in some regions, demand in developing economies continues to support this segment. Moreover, innovation in filter design—such as reduced environmental impact and increased biodegradability—is pushing manufacturers to explore modified cellulose acetate products.

Key Applications and Industry Segmentation

The cellulose acetate market is segmented by product type, application, and geography. Product types include fiber-grade and plastic-grade cellulose acetate. Fiber-grade cellulose acetate is primarily used in textiles, offering benefits such as breathability, silk-like feel, and easy dyeing. Plastic-grade cellulose acetate is utilized in the manufacture of films, coatings, and injection-molded items.

By application, the market spans cigarette filters, textiles and apparel, photographic films, optical frames, and packaging. Among these, cigarette filters hold the largest share, but the textiles and packaging segments are witnessing notable growth due to fashion sustainability and food safety trends.

Geographically, Asia-Pacific dominates the market, largely due to the presence of key manufacturing hubs in China, India, and Japan. North America and Europe are also significant markets, driven by regulatory support for eco-friendly materials and advanced research and development capabilities.

Technological Advancements and R&D

Research and development efforts are focused on enhancing the biodegradability and performance of cellulose acetate. For instance, companies are developing new blends and additives to improve its mechanical strength, thermal resistance, and water solubility. Nanotechnology and advanced fabrication techniques are also being explored to broaden its usage in medical and filtration applications.

Furthermore, manufacturers are investing in closed-loop production systems and cleaner extraction methods to reduce environmental impact and ensure compliance with green chemistry standards. These efforts are aligning cellulose acetate production with circular economy goals.

Challenges in the Market

Despite its advantages, the cellulose acetate market faces several challenges. The cost of production remains relatively high compared to conventional plastics. Raw material availability can also be a constraint, particularly with fluctuations in wood pulp and cotton prices. Additionally, public perception about cigarette filters, which are often considered single-use pollutants, could negatively impact the image of cellulose acetate in some sectors.

Furthermore, the competition from other biodegradable materials such as polylactic acid (PLA), polyhydroxyalkanoates (PHA), and starch-based plastics is intensifying. These materials also offer sustainable advantages and are gaining traction in similar applications.

Future Outlook

The cellulose acetate market is poised for significant transformation over the next decade. With regulatory frameworks becoming stricter on plastic waste, and consumers increasingly opting for green alternatives, cellulose acetate is likely to witness a broader adoption across industries. Growth is expected to be driven by increased investment in sustainable packaging, textile innovation, and product diversification beyond cigarette filters.

0 notes

Text

Biodegradable Alternatives in Construction for Eco-Conscious Builders

As the construction industry grapples with increasing pressure to reduce its environmental footprint, biodegradable alternatives in construction have emerged as a viable path toward sustainability. These materials offer an opportunity to replace conventional, non-renewable resources with options that decompose naturally without leaving behind harmful residues. Beyond their eco-conscious appeal, these alternatives signal a shift toward a more regenerative building philosophy, focusing on both ecological preservation and resource efficiency.

Introduction to Biodegradable Construction Materials Biodegradable construction materials are derived from natural sources such as agricultural waste, fungi, plant fibers, and recycled biomass. Unlike traditional materials that linger in landfills for decades, these alternatives break down organically when disposed of properly. The construction sector, which contributes significantly to global waste and carbon emissions, is seeing growing interest in these materials due to increasing awareness of climate change and circular economy principles. Common biodegradable options include mycelium-based composites, hempcrete, cork insulation, straw bales, and bio-based plastics. These materials offer comparable durability for various applications while supporting sustainable building practices.

Environmental Benefits of Biodegradable Alternatives One of the primary advantages of biodegradable alternatives in construction is their minimal environmental impact. From manufacturing to disposal, these materials typically require less energy and produce fewer emissions compared to concrete, steel, or plastic-based options. In addition, many biodegradable materials are renewable, meaning they can be replenished over short periods without depleting natural resources. By reducing construction waste, improving indoor air quality, and enhancing thermal performance, these alternatives contribute to greener building certifications and healthier living environments.

Challenges in Adoption and Implementation Despite their promise, biodegradable construction materials face several hurdles. Performance consistency, especially under varied weather conditions, remains a concern for architects and engineers. Many biodegradable materials still lack widespread regulatory standards and industry certifications, making them less appealing for commercial projects. There are also challenges related to supply chain reliability, scalability of production, and cost competitiveness when compared with conventional materials. In urban areas, integration with existing infrastructure can also be complex, requiring retrofitting or hybrid construction models.

Innovative Developments and Market Trends The future of biodegradable alternatives in construction is being shaped by innovation and research. Scientists are developing new composites using algae, seaweed, and agricultural residues to produce materials with superior strength and flexibility. Startups and green tech companies are introducing prefab modules made from biodegradable substances to speed up construction and reduce labor costs. Governments and private investors are also showing interest through green building incentives and eco-certifications. As digital tools like BIM and AI enter the design and planning phases, they are helping architects identify suitable biodegradable materials early in the construction lifecycle, increasing the likelihood of adoption.

For more info https://bi-journal.com/biodegradable-alternatives-in-construction/

Conclusion Biodegradable alternatives in construction present a compelling solution to the environmental issues plaguing the building industry. While challenges in performance and scalability remain, ongoing innovation and supportive policies are steadily breaking down these barriers. As the demand for sustainable living spaces grows, these alternatives are not just a trend—they represent a long-term shift toward eco-integrated architecture. Embracing these materials today sets the stage for a future where construction is in harmony with nature.

#BiodegradableConstruction#SustainableBuilding#GreenArchitecture#bi-journal news#bi-journal services#business insight journal

0 notes

Text

Trash Bags Market Report: Size, Share, and Strategic Insights

Plastics can take up to 1000 years to decompose; that’s a well-known fact. We have facts that are even scarier. Half of all plastic produced is designed to be used only once and then thrown away ! Even after they decompose, plastics don’t disappear. They just break down into smaller pieces, yet bigger problems, called microplastics. Doesn’t it force us to find a solution? Countries are banning single-use plastic, but they need an alternative.

Environmental consciousness has prompted a shift toward sustainable alternatives in many industries. The trash bag market, once dominated by single-use plastics, is also witnessing a transformative change. The introduction of biodegradable trash bags aims to reduce plastic waste and its detrimental impact on the environment.

The global trash bags industry was valued at $12.64 billion in 2024, and biodegradable polyethylene is expected to be its fastest-growing material segment, according to Grand View Research. Biodegradable trash bags are designed to decompose more rapidly than conventional plastic bags. Unlike traditional polyethylene bags, biodegradable versions incorporate additives that promote oxidation, allowing them to degrade more swiftly under environmental conditions. This innovation addresses the growing concerns over plastic pollution, particularly in landfills and oceans.

Benefits of Biodegradable Trash Bags:

Reduced Plastic Pollution: These bags break down more quickly than conventional plastics, helping reduce long-term waste in landfills and oceans.

Lower Carbon Footprint: Biodegradable bags are generally made with plant-based materials or recycled content, resulting in lower greenhouse gas emissions during production.

Less Harm to Wildlife: Since they degrade faster, there's a reduced risk of animals ingesting or becoming entangled in plastic waste.

Improved Soil Quality: Some biodegradable bags are also compostable, meaning they break down into non-toxic components that enrich the soil. Green Earth, Bag to Nature, If You Care, and UNNI compostable bags are some prime examples.

Applications and Examples

Several companies are leading the way in producing and distributing biodegradable trash bags.

Polymateria, a London-based company, has developed a technology that involves adding a masterbatch to plastics during production to help their decomposition. This technology is applicable to polyolefins, including polyethylene and polypropylene, and allows them to decompose into a waxy substance in less than a year when exposed to environmental conditions.

HoldOn Bags offers plant-based trash bags made from Polybutylene Adipate Terephthalate (PBAT), Polylactide (PLA), and cornstarch. The company uses 100% compostable and FSC-certified materials.

In April 2024, the Arkansas-based company Revolution introduced the DailyGood Bags. These heavy-duty trash bags are made with up to 97% post-consumer recycled plastic, emphasizing environmental sustainability while meeting everyday household needs.

Simply Bio provides a practical solution for households seeking biodegradable options without compromising on durability. The company offers 13-gallon home-compostable bags with drawstring closures that transform into humus within 180 days.

Some Recent Developments in the Industry

In April 2023, Microban International and Berry Global announced a collaboration to deliver a range of Color Scents flavored garbage bags featuring antimicrobial technology. These bags combine subtle fragrances with antimicrobial properties to combat odor-causing bacteria.

In September 2022, Novolex invested $10 million to expand its capacity to recycle plastic bags and polyethylene film at its recycling facility in North Vernon, Indiana. This move aims to advance sustainability and innovation within the packaging industry.

In Bangladesh, the development of the Sonali Bag has emerged as a sustainable alternative to traditional plastic bags. It is a biodegradable polymer bag made from jute. The initiative highlights the potential of natural fibers in creating eco-friendly packaging solutions.

Upshot

Apart from the above-mentioned benefits, modern biodegradable trash bags provide the strength and durability of traditional plastic bags, making them a viable everyday alternative. Many are designed to decompose in home composting systems or under industrial composting conditions, aligning with household waste routines. Some products also incorporate antimicrobial or odor-blocking technologies, enhancing user experience without compromising on sustainability.

0 notes

Text

Strategic Insights and Leading Players in the Biodegradable Plastic Additives Market

Biodegradable plastic additives are specialized chemical compounds blended into traditional plastic formulations to enhance their ability to break down naturally in the environment. These additives accelerate the degradation process by enabling microbes to digest the plastic once it's exposed to specific conditions like heat, moisture, and oxygen. Unlike standard plastics that can persist for hundreds of years, plastics enhanced with biodegradable additives can decompose more quickly into harmless byproducts such as water, carbon dioxide, and biomass—helping reduce long-term plastic pollution and supporting sustainable waste management practices across industries.

The global biodegradable plastic additives market size was valued at USD 1.49 billion in 2024 and is projected to reach USD 2.20 billion by 2029, growing at 8.1% cagr from 2024 to 2029.

This growth is fueled by the integration of biodegradable additives with bioplastics, the implementation of biodegradability standards for single-use plastics, and an increased focus on food safety and non-toxicity .

Leading Biodegradable Plastic Additives Companies

Several companies are at the forefront of this market, offering innovative solutions:

BioSphere Plastic: Specializes in biodegradable additives that enhance the biodegradation of synthetic polymers. The company has a global presence with offices in the USA, Chile, and Thailand .

Green Dot Bioplastics: Utilizes commercially available bioplastics such as PBAT, PBS, PLA, and patented thermoplastic starch technology to create blends that improve physical properties and compostability rates .

Bio-Tec Environmental: Offers EcoPure®, an organic plastic additive that significantly increases the biodegradation rate of plastics and plastic products .

ENSO Plastics: Provides organic additives that render almost any plastic polymer biodegradable in various environments, including landfills and marine settings

Polymateria: A UK-based company developing biodegradable plastic alternatives through its Biotransformation technology, which allows plastics to decompose into a waxy substance digestible by microbes without leaving microplastics .

Strategic Considerations for Industry Leaders

For executives and decision-makers, the following strategic considerations are paramount:

Innovation Investment: Investing in R&D to develop advanced biodegradable additives that meet regulatory standards and consumer expectations.

Regulatory Compliance: Staying ahead of evolving regulations by adopting additives that facilitate compliance with biodegradability standards.

Sustainability Goals: Aligning product development with corporate sustainability objectives to meet environmental targets and enhance brand reputation.

Market Expansion: Exploring emerging markets with growing demand for biodegradable plastics, particularly in regions with stringent environmental regulations.

Access in-depth market analysis, download the PDF brochure today !

The biodegradable plastic additives market presents significant opportunities for companies committed to sustainability and innovation. By understanding market dynamics and investing in advanced technologies, industry leaders can position themselves at the forefront of this transformative sector.

#DecorativeConcrete#ConcreteDesign#ConstructionInnovation#SustainableArchitecture#ConcreteFinishing#DecorativeFlooring#ArchitecturalConcrete

0 notes

Text

Future of Polymer Additive Manufacturing: Market Size, Trends, and Growth Forecast to 2031

Polymer Additive Manufacturing Size & Forecast

The growth of the polymer additive manufacturing market is being driven by a combination of key advantages it offers, including cost efficiency, reduction in material waste, customization and design flexibility, shorter lead times, lower labor costs, and environmental sustainability. Furthermore, the increasing interest in customization and personalization, the need for more resilient supply chains and on-demand production capabilities, and the progress in bioprinting and healthcare applications are contributing significantly to market expansion. Industry collaborations and partnerships are also opening new opportunities for innovation and commercial growth.

Get Sample Copy @ https://www.meticulousresearch.com/download-sample-report/cp_id=6128?utm_source=Blog&utm_medium=Product&utm_campaign=SB&utm_content=18-04-2025

Key Findings

By Offering: In 2024, the services segment dominated the polymer additive manufacturing market.

By Technology: In 2024, the Fused Deposition Modeling (FDM) segment accounted for the largest share of the market.

By End User: In 2024, the consumer products segment held the largest share of the polymer additive manufacturing market.

By Geography: North America led the global polymer additive manufacturing market in 2024.

Polymer Additive Manufacturing Market Drivers

Cost Efficiency and Reduction in Material Waste

One of the strongest drivers for the polymer additive manufacturing (AM) market is the significant reduction in manufacturing costs and material waste. Traditional manufacturing methods like subtractive manufacturing involve cutting away material from larger blocks, which results in substantial material waste. In contrast, additive manufacturing uses a layer-by-layer approach based on digital files, consuming only the necessary material for each object. This not only cuts down on waste but also makes low-volume production more cost-effective, especially for industries producing highly customized parts.

The savings are particularly evident in the production of complex parts. 3D printing allows for intricate geometries without the need for costly molds, tooling, or lengthy assembly processes. Even smaller manufacturers can now create parts that were once only viable for large-scale operations, thereby reducing entry barriers across industries.

According to Deloitte’s 2020 report titled "3D Printing and the Future of Manufacturing," companies adopting additive manufacturing in place of traditional techniques have achieved up to 70% reductions in material costs in certain use cases. This is especially impactful in aerospace and automotive sectors where material optimization is key to both cost savings and performance.

Wohlers Associates also highlights that 3D printing has the potential to slash tooling costs by as much as 90%, since traditional molds and dies are no longer needed.

Polymer Additive Manufacturing Market Trends

Rise of Biodegradable and Sustainable Materials

Sustainability is becoming a vital concern in modern manufacturing, and polymer additive manufacturing is responding to this shift with the development and adoption of biodegradable and eco-friendly materials. These include materials made from renewable sources, recycled plastics, and biodegradable polymers. The trend is especially prominent in consumer goods, packaging, and healthcare industries that are increasingly seeking green solutions.

Bio-based polymers like PLA (Polylactic Acid), which is derived from sources such as corn starch and sugarcane, are paving the way for sustainable 3D printing. Recycled filaments made from discarded plastics are also gaining traction, reducing dependency on virgin materials and supporting circular economy principles.

The market for bio-based and biodegradable 3D printing materials is mainly driven by packaging, consumer goods, and healthcare demands. Companies like MakerBot and 3D Systems have broadened their portfolios to include sustainable filament options. Major players such as NatureWorks (a leading PLA producer) and Filabot (which specializes in recycled filament) are increasingly favored by industries that are prioritizing environmentally responsible practices.

Moreover, automotive and aerospace manufacturers are exploring the use of biocomposites and biopolymers to reduce the environmental footprint of their components.

Polymer Additive Manufacturing Market Opportunities

Customization and Personalization

The growing demand for personalized products and tailored manufacturing solutions is creating major opportunities in the polymer additive manufacturing market. Traditional processes like injection molding or CNC machining struggle with high variability and customization, but 3D printing provides a flexible, efficient alternative.

In healthcare, consumer goods, and fashion, polymer additive manufacturing makes it possible to produce custom medical devices, orthopedic implants, and wearable technologies designed with exact specifications. Medical applications include prosthetics, orthodontic devices, and surgical implants tailored to a patient’s anatomy, resulting in superior fit, comfort, and effectiveness.

Companies such as Stratasys and Materialise are leading in this domain. Stratasys, for instance, offers the J750 Digital Anatomy Printer, which allows for personalized surgical planning and creation of patient-specific medical devices. In consumer industries, Nike and Adidas have already embraced 3D printing for customized shoes and apparel, enabling customers to select unique designs, colors, and performance attributes.

Get Full Report @ https://www.meticulousresearch.com/product/polymer-additive-manufacturing-market-6128?utm_source=Blog&utm_medium=Product&utm_campaign=SB&utm_content=18-04-2025

Polymer Additive Manufacturing Market Analysis: Top Market Opportunity

By Offering: In 2024, the Services Segment Dominated the Polymer Additive Manufacturing Market

The polymer additive manufacturing market is divided into services, hardware, software, and materials. Among these, the services segment held the largest market share in 2024. This dominance is due to the increasing demand for specialized and custom products in industries like aerospace, healthcare, and automotive. Outsourcing manufacturing services also helps businesses avoid heavy upfront investments in 3D printing infrastructure.

This services segment is projected to record the highest CAGR during the forecast period (2024–2031). Growth is supported by the emergence of comprehensive service providers and expanding access to 3D printing technologies across the globe.

By End User: The Automotive Segment to Witness Rapid Growth During the Forecast Period

Although consumer products were the leading end-user segment in 2024, the automotive industry is expected to grow the fastest, with a forecasted CAGR of 17.6% between 2024 and 2031. Automotive manufacturers are increasingly leveraging polymer additive manufacturing for its ability to deliver lightweight, cost-effective, and customizable components.

Applications range from prototyping and tooling to the direct manufacturing of functional components, made possible by improvements in material performance and AM technologies. The focus on lightweighting—critical to improving fuel efficiency and meeting emissions regulations—is driving the adoption of materials like nylon, polycarbonate, and high-performance thermoplastics such as PEEK and PEKK.

Customization remains another key advantage. Polymer 3D printing supports intricate, vehicle-specific parts that enhance performance and aesthetic appeal, allowing brands to offer personalized products and gain competitive edge.

The growing market for electric vehicles (EVs) is also contributing to polymer AM adoption. Lightweight components are vital for maximizing battery range and efficiency. Additionally, the technology's suitability for small-scale, low-volume production makes it ideal for producing specialized EV components.

Geographical Analysis

North America Dominated the Polymer Additive Manufacturing Market in 2024

North America accounted for the largest share of the global polymer additive manufacturing market in 2024. This regional leadership is attributed to a mix of technological innovation, advanced infrastructure, significant R&D funding, and supportive government initiatives. High demand for customization, strong industrial bases, and cross-border collaborations also strengthen the region's position in the market. Sectors like aerospace and healthcare are particularly advanced in implementing polymer AM technologies.

On the other hand, Asia-Pacific is projected to record the highest CAGR during the forecast period. This surge is being driven by rapid industrialization, digital transformation, and rising interest in tailored and sustainable manufacturing practices. Government investments in advanced manufacturing technologies and the roll-out of Industry 4.0 initiatives are expected to play a crucial role in adoption, particularly in industries such as automotive, aerospace, electronics, and healthcare.

Key Companies

The market report profiles major players based on strategic developments undertaken between 2021 and 2024. The key companies in the global polymer additive manufacturing market include:

Stratasys, Ltd. (U.S.)

3D Systems Corporation (U.S.)

EOS GmbH (Germany)

Materialise NV (Belgium)

voxeljet AG (Germany)

Markforged Holding Corporation (U.S.)

Proto Labs, Inc. (U.S.)

Autodesk, Inc. (U.S.)

3Dceram (France)

Dassault Systemes SE (France)

Formlabs Inc. (U.S.)

Shapeways Holdings, Inc. (U.S.)

Polymer Additive Manufacturing Industry Overview: Latest Developments

November 2024: Stratasys announced upgrades to its GrabCAD Print and GrabCAD Print Pro software.

November 2024: EOS introduced EOS P3 NEXT, a new 3D printer aimed at improving productivity and efficiency in polymer printing.

June 2024: Stratasys entered a partnership with AM Craft (Latvia) to boost 3D part manufacturing in the aviation industry.

October 2023: 3D Systems unveiled the MJP 300W printer and VisiJet Wax Jewel Ruby, designed for high-productivity jewelry pattern production with customizable features.

June 2023: 3D Systems partnered with SWANY Co. Ltd (Japan) to promote large-format pellet extrusion 3D printing in Japan. SWANY’s demo center will house the country’s first EXT 1070 Titan Pellet printer.

Get Sample Copy @ https://www.meticulousresearch.com/download-sample-report/cp_id=6128?utm_source=Blog&utm_medium=Product&utm_campaign=SB&utm_content=18-04-2025

0 notes

Text

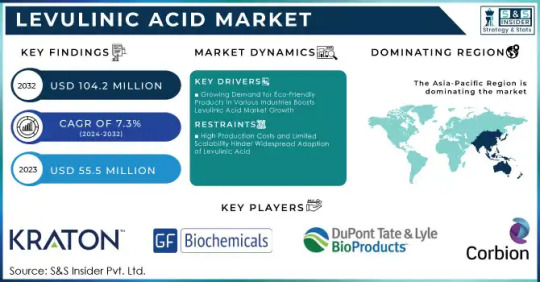

Bio-Based Chemicals Drive Growth in the Levulinic Acid Market

Growing Demand for Bio-Based Chemicals and Sustainable Industrial Solutions Drives Growth in the Levulinic Acid Market.

The Levulinic Acid Market Size was valued at USD 55.5 Million in 2023 and is expected to reach USD 104.2 Million by 2032 and grow at a CAGR of 7.3% over the forecast period 2024-2032.

The Levulinic Acid Market is driven by increasing global interest in bio-based and renewable chemicals. Levulinic acid, derived from biomass such as cellulose and sugars, serves as a versatile platform chemical used in the production of resins, plasticizers, solvents, pharmaceuticals, and fuel additives. With growing environmental concerns and the shift away from fossil-based feedstocks, levulinic acid is emerging as a key ingredient in green chemistry solutions across various industries.

Key Players

Beijing Sino-High Technology

BioChem

Corbion

Dupont Tate & Lyle Bio Products

GFBiochemicals

Kraton Polymers

Nexant Inc.

Renewable Energy Group, Inc.

Segetis, Inc.

Shanxi Lihua Bio-Technology Co., Ltd.

Future Scope & Emerging Trends

The future of the levulinic acid market looks promising, bolstered by increasing R&D investment in bio-refineries and rising adoption of sustainable manufacturing practices. Key emerging trends include the use of levulinic acid in biodegradable plasticizers, agrochemicals, and green solvents, along with its growing role as a platform chemical in the synthesis of biofuels and specialty polymers. As regulatory bodies worldwide push for reduced environmental impact and carbon footprint, industries are transitioning to renewable alternatives—positioning levulinic acid as a vital contributor to the global green chemical economy. The Asia-Pacific region is expected to witness the fastest growth due to increasing demand from pharmaceuticals, agriculture, and cosmetics sectors.

Key Points

Derived from renewable biomass; key ingredient in green chemistry

Used in pharmaceuticals, agrochemicals, plasticizers, and fuel additives

Strong push from environmental regulations favoring bio-based chemicals

R&D driving innovation in levulinic acid-derived polymers and solvents

Asia-Pacific leading market growth due to industrial demand and sustainability goals

Conclusion

The Levulinic Acid Market is set for long-term expansion as industries and governments prioritize sustainability and the transition to a circular bioeconomy. With its wide application range and eco-friendly profile, levulinic acid is becoming a cornerstone in the development of next-generation bio-based products.

Read Full Report: https://www.snsinsider.com/reports/levulinic-acid-market-4917

Contact Us:

Jagney Dave — Vice President of Client Engagement

Phone: +1–315 636 4242 (US) | +44- 20 3290 5010 (UK)

#Levulinic Acid Market#Levulinic Acid Market Size#Levulinic Acid Market Share#Levulinic Acid Market Report#Levulinic Acid Market Forecast

0 notes

Text

Polybutylene Adipate Terephthalate Market: A Sustainable Alternative in the Plastics Industry - UnivDatos

According to a new report by UnivDatos, the Polybutylene Adipate Terephthalate Market was valued at USD 1382 Million in 2023 and growing at a CAGR of 8.7%. Polybutylene Terephthalate (PBT) is a high-performance engineering plastic material that is used in a variety of applications because of its high mechanical, chemical, and thermal performances. Polybutylene terephthalate known as PBT is a member of the polyester family, mainly used in automotive, electrical, and electronics, and some consumer durable applications. The PBT market is predicted to grow rapidly in the next few years due to new developments, key player activity, and the support for sustainable materials by authorities.

Get Access to Sample PDF Here- https://univdatos.com/reports/polybutylene-adipate-terephthalate-market?popup=report-enquiry

The dynamic changes in the PBT market are due to the advancement in technology introduction of new materials and the growing concern about green solutions. One of the most prominent trends has been the shift toward the use of bio-based PBT as companies seek to depend on fossil fuels. Bio-based PBT plastics also have mechanical properties similar to the non-bio-based PBT but are recyclable and have a lower carbon footprint since it is derived from bio-based carbon sources. In addition to PBT growth, the increases in the environmental friendliness of PBT are also beneficial; one of these is the enhancement of the recyclability of PBT. With industries and governments adopting circular economy concepts, the market for recycled material has witnessed a boost. Due to this, many corporations are seeking to buy technologies that enable recycling of PBT without a major degradation of the properties of this material. This is considerably significant in industries such as automotive and electronics where the minimization of wastes is highly valued.

Government Support and Regulations:

Government policies and environmental standards have been instrumental to the existing and potential market for PBT. Due to worrying trends of plastic pollution and environmental degradation, governments around the globe are enacting measures that foster the adoption of eco-friendly and reusable materials. For instance, in Europe and North America, the strict regulation on the use of plastics has prompted industries to use more of bio-based and recyclable PBT.

The EU has been particularly proactive in the promotion of sustainable materials as part of the research for future products. The EU intends to cut out plastic waste in the environment via measures that also include the European Green Deal and the circular economy action plan. Such policies are expected to boost the demand for bio-based PBT in the automotive and consumer goods industries among others.

In North America, sustainability policies of the government are trying to look for ways how to implement themselves. Biopolymers have been some of the green materials that the US government has been supporting to be developed through various projects. The rise in the Sustainability policies and the initiatives taken to reduce greenhouse gas emissions will in turn continue to fuel the growth of the bio-based PBT market in the forecast period in the region.

Sustainable material is also being supported by the governmental bodies in the Asia Pacific region, especially China and Japan. China remains the largest global producer of plastics hence, has enacted measures to reduce consumption of plastics, especially the single-use type. Japan has also been promoting bio-based and biodegradable plastics in the country to assist the country in attaining a brown economy more effectively. These government policies are expected to contribute towards the development of the PBT market in the next few years.

Future Outlook and Growth Opportunities:

Based on technological developments, industry requirements, and government support for sustainable materials, it is anticipated that the PBT market has a favorable outlook. The automotive industry is one of the attractive markets for PBT, specifically, the market of electric vehicles, or EVs. Consequently, with the growth in the adoption of EVs, there will be a corresponding growth in the necessity for lightweight yet high-performing materials like the PBT. Due to properties such as high heat resistance, durability, and electrical resistance, PBT can be effectively incorporated into EV parts, particularly the casings of batteries and connectors, as well as sensors.

Subsequently, the PBT market will remain fuelled by the trend in sustainability. From the increasing environmental consciousness of industries and consumers, there will be a gradual shift towards bio-based and recyclable PBT. Companies that could dedicate their resources to developing sustainable PBT solutions have a chance to fit this market niche. Moreover, the circular economy model that involves the reuse and recycling of the materials would open a wider market for the recyclable PBT. The Asia-Pacific is expected to emerge as the leading PBT market owing to the increasing industrialization, urbanization trends, and the growing demand for superior performance materials across the automotive, electronics, and consumer goods industries. The market of PBT is expected to grow at a fast pace and China in particular will be instrumental in the growth of the market due to the abundant manufacturing companies in China. Amid escalating concern for sustainable living and non-plastic waste management in the region, governments have undertaken several measures towards its reduction; thus, will offer great growth opportunities for PBT makers.

For More Detailed Analysis, Please Visit- https://univdatos.com/reports/polybutylene-adipate-terephthalate-market

Conclusion:

In Conclusion, the market size of PBT is expected to grow rapidly in the following years due to the growth of high-technology industries, demand from essential end-use sectors, and backing of the government for eco-friendly products. Businesses that aim at producing new and improved products, embracing more sustainable and eco-friendly practices, and increasing their production capacities are likely to thrive in this changing environment.

0 notes

Text

Global Sunglasses Market: Product Type Analysis, Market Size, Regional Trends, Company Share

Industry Outlook

The Sunglasses market accounted for USD 25.3 Billion in 2024 and is expected to reach USD 47.5 Billion by 2035, growing at a CAGR of around 5.9% between 2025 and 2035. This market for sunglasses relates to the worldwide industry that deals with designing, manufacturing, and marketing sunglasses. These are eyeglasses that protect the eyes against hazardous UV rays and provide sharp vision in bright conditions. The product line ranges from more affordable mass-market brands to very exclusive designer models. The market has gained tremendous pace because of eye health awareness, fashionable styles, and growing demand for luxury and sports-oriented eyewear. Moreover, the online penetration of retail, brand collaborations, and sustainability are also compelling the sunglasses market growth.

Get free sample Research Report - https://www.metatechinsights.com/request-sample/1286

Market Dynamics

Sustainability and Fashion-Forward Trends Drive Demand for Sunglasses Among Gen Z and Millennials

The young generation is making a difference in the sunglasses market. Gen Z and Millennials are interested in fashionable, environmentally friendly glasses. Beyond trends, younger consumers expect the brand to be an embodiment of their sustainability and social responsibility ideals. A company should care about production ethics and employ the use of environment-friendly materials for its frames like recycled plastics, bamboo, or bio-based. This increasing desire for environment-friendly and green products is changing the creation, production, and sale of products by the brands.

As these consumers become an ever-larger share of global purchasing power, sunglasses brands respond by taking up more sustainable practices, from carbon-neutral manufacturing to biodegradable or recycled material packaging. This generation really has much social influence on other mediums such as Instagram, TikTok, and so forth since they make consumers post and promote their sustainable fashion choices, hence further pushing the trend towards environmentally friendly eyewear.

Technological Advancements in Lenses Drive Consumer Demand for Enhanced Sunglasses Features

New technologies that support lens design encourage growth in the market for sunglasses. Polarized lenses that cut glare and images improve clarity and are thus increasingly popular for outdoor pursuits and driving. The flexibility of photochromic lenses allows the lens to change according to the light situation; this gives added convenience for consumers who require both indoor and outdoor eyewear. Another growing area includes blue light-blocking lenses, particularly for consumers who spend much time on digital devices, which they would like to reduce eye strain resulting from frequent screen time.

Apart from the additional functionality alone, these new technological features also answer the growing demand of consumers wanting products that combine fashion with practical benefits. The technology also continues to evolve with smart sunglasses and the like, adding features that may include audio systems and fitness tracking, thereby opening up the market further.

Misleading UV Protection Claims Undermine Consumer Trust in the Sunglasses Market

The claims of UV protection of sunglasses are misleading, and consumers have a loss of confidence and confusion. Most sunglasses are showcased with 100% UV protection, but these cannot be certified and regulated properly, through which effectiveness cannot be confirmed sometimes. This problem is further intensified as regulations differ in different markets. Some have more stringent standards while others have far more flexible standards, which leaves ample amounts of room for false or exaggerated claims by brands. This is confusing, particularly for consumers who seek protection against damaging UV rays.

In the absence of clear and consistent regulations in the marketplace, sunglasses that do not support the claims made during advertisement may flood the markets to the detriment of consumer health and at the same time damage the eyewear industry's reputation. In this regard, consumers are likely to be misguided under the impression that all sunglasses have no protection at all and therefore resort to other eye protection methods, such as a hat or dousing oneself in sunscreen to protect the eyes from UV exposure.

Read Full Research Report https://www.metatechinsights.com/industry-insights/sunglasses-market-1286

Growing Demand for Sport-Specific Eyewear Creates Opportunities in Niche Markets

The sport-specific eyewear market is highly booming, and consumers are looking for sunglasses tailored to the demands of a certain activity, like cycling, skiing, or fishing. The U.S. Bureau of Labor Statistics reported that participation in sports has been on the rise and was led by millennials and Gen Z, who seem to be embracing active lifestyles. Additionally, NPD Group said that sales of sports-specific eyewear skyrocketed across its lines, including categories such as cycling and skiing that demanded lenses with high-performance attributes like polarization, anti-fog coatings, and UV protection.

Another kind of demand on the uptick is for specialty eyewear designed to enhance vision and comfort in specific environments; this is as consumers increasingly seek products that marry functionality with aesthetics. As more individuals engage in outdoor pursuits, a niche market for sport-specific sunglasses provides brands with opportunities to develop custom lenses and tough frames designed for specific needs such as water resistance when fishing, to protection from wind when cycling.

Collaborations with Fashion and Sports Brands Unlock New Consumer Segments for Eyewear

Collaborations between eyewear brands and popular fashion designers or sports brands are creating significant opportunities to target diverse consumer segments. Sportswear collaborations are on the boom, particularly through companies, such as Nike and Adidas collaborating with other companies like Luxottica or Essilor, which sell eyeglasses, to share sports-inclined fashion designs. Sports equipment/fashion-accessory spending experienced a steeply increasing trend where brand association takes precedence even when making spending decisions by Millennials as well as Gen Z.

These collaborations not only enhance the visibility of brands but also resonate with consumer demand for high-performance features combined with fashion-forward designs. As a related business, cross-industry collaborations are expected to increase continuously, making eyewear brands ideal for expanding reach while also appealing to sports enthusiasts and fashion-conscious buyers.

Buy Now https://www.metatechinsights.com/checkout/1286

Competitive Landscape

The competitive landscape is dominated by several major players including Luxottica Group, Safilo Group, Maui Jim, Marchon Eyewear, and Warby Parker, among others. These companies continue to grow market share through strategic partnerships, innovative product offerings, and brand diversification. Notably, Luxottica still finds itself on top in terms of market leadership through owning brands such as Ray-Ban and Oakley. The digital footprint was enhanced through virtual try-on capabilities, which add momentum to e-commerce sales. Polarized lenses through Maui Jim got recognition and continue to drive share in the premium space. Warby Parker surprised the market with its direct-to-consumer model, with a thrust on affordability and sustainability. In the future, these players will really respond to demands of changing consumer preference, such as the demand for using even more eco-friendly materials and personalized products, as the market continues to innovate-actually with products such as blue light-blocking and photochromic lenses.

0 notes

Text

𝐂𝐨𝐦𝐩𝐥𝐞𝐭𝐞 𝐆𝐮𝐢𝐝𝐞 𝐀𝐛𝐨𝐮𝐭 - 𝐁𝐢𝐨𝐩𝐥𝐚𝐬𝐭𝐢𝐜𝐬 [𝐞-𝐏𝐃𝐅]

Bio-plastics Market size is forecast to reach $21.7 billion by 2030, after growing at a CAGR of 17.2% during 2024-2030.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐒𝐚𝐦𝐩𝐥𝐞 @ https://lnkd.in/gmyaQXA7

#Bioplastics are #plastics #materials that are made up of renewable #biomass sources which include vegetable fats and oils, corn starch, straw, woodchips, sawdust, recycled food wastes, among others. Bioplastics are being increasingly used to reduce the problem of plastic waste that is suffocating the planet and contaminating the environment along with this the production of #bioplastic requires 65% less energy than conventional petroleum #plastic.

With a rise in the consumption of eco-friendly products and wide usage of bioplastics in various industries such as, #transportation, and food industries, the bio-#plastics market is witnessing an increase in its demand. Bio-plastics composites reduce landfill wastes, release much lower #carbon footprint, and decrease volatile organic compound emissions. In addition, government and #environmental governing bodies around the world have imposed various policies to encourage the use of bio-based products which fuels the growth of bio-plastics market.

📊 𝐆𝐞𝐭 𝐭𝐡𝐞 𝐅𝐮𝐥𝐥 𝐑𝐞𝐩𝐨𝐫𝐭 @ https://lnkd.in/gCnv22Y2

𝐓𝐨𝐩 𝐋𝐞𝐚𝐝𝐢𝐧𝐠 𝐊𝐞𝐲 𝐏𝐥𝐚𝐲𝐞𝐫𝐬 𝐚𝐫𝐞: DSM | Mitsubishi Corporation | Footprint | LG Chem | Coperion | Kaneka Green Planet® | Sterling Parfums Industries LLC | Cedo |Mitsubishi Corporation American Chemical Society |DEMGY | Napco National Packaging

0 notes