#Industry 4.0 market in Key Countries

Text

#Industry 4.0 Market COVID-19 Analysis Report#Industry 4.0 Market Demand Outlook#Industry 4.0 Market Primary Research#Industry 4.0 Market Size and Growth#Industry 4.0 Market Trends#Industry 4.0 Market#global Industry 4.0 market by Application#global Industry 4.0 Market by rising trends#Industry 4.0 Market Development#Industry 4.0 market Future#Industry 4.0 Market Growth#Industry 4.0 market in Key Countries#Industry 4.0 Market Latest Report#Industry 4.0 market SWOT analysis#Industry 4.0 market Top Manufacturers#Industry 4.0 Sales market#Industry 4.0 Market COVID-19 Impact Analysis Report#Industry 4.0 Market Primary and Secondary Research#Industry 4.0 Market Size#Industry 4.0 Market Share#Industry 4.0 Market Research Analysis#Industry 4.0 Market Trends and Outlook#Industry 4.0 Industry Analysis

0 notes

Text

Looking forward to China’s industrial development prospects in the next 10 years

Looking forward to China's industrial development in the next 10 years, analysis and predictions can be made based on existing development trends, policy orientations and the global economic environment:

Industrial upgrading and structural optimization:

China will continue to promote the upgrading of its industrial structure from labor-intensive to technology- and capital-intensive. Mid- to high-end manufacturing will be the key development direction, including aerospace, high-end equipment, new energy vehicles, new materials and other fields.

With the deepening implementation of the "Made in China 2025" strategy and subsequent planning, China will accelerate the in-depth integration of industrialization and informatization, and promote the development of emerging industries such as intelligent manufacturing and the industrial Internet.

Innovation drive and technological progress:

Against the background of intensified global technological competition, China will further increase investment in technological innovation, especially in fields such as 5G, artificial intelligence, Internet of Things (IoT), quantum information, and biotechnology, to enhance the core competitiveness of the industry.

Industry 4.0 related technologies and digital transformation will become mainstream. Enterprises will improve production efficiency and product quality through automation and intelligent transformation, and achieve personalized customization and flexible production.

Green and sustainable development:

Environmental protection policies are becoming stricter, and low-carbon economy and circular economy will have a profound impact on the path of industrial development. China's industry will be committed to energy conservation and emission reduction, clean production, and the development of green manufacturing systems, such as new energy, energy-saving and environmental protection equipment and services.

Globalization and industrial chain reconstruction:

Taking into account the rise of trade protectionism and the adjustment trend of global supply chains, Chinese industry will actively build independent and controllable industrial and supply chains, seek a higher position in the global value chain, and enhance international competitiveness.

While low-end industries are being transferred, China will strengthen international cooperation in some areas, actively participate in the global industrial division of labor, and build international brands and multinational companies.

Talent training and system reform:

Facing the challenge of aging, China will pay more attention to the cultivation and introduction of talents, improve the quality of the labor force, especially the construction of highly skilled talent teams, to support the development needs of high-end industries.

Deepen institutional reform, create a better business environment, encourage innovation and entrepreneurship, promote the development of small, medium and micro enterprises, and stimulate market vitality.

To sum up, in the next ten years, China's industry will focus on high-quality development, focus on technological innovation, industrial chain upgrading, green development and improvement of global competitiveness, and strive to achieve the leap from a manufacturing country to a manufacturing power. At the same time, we will also respond to the challenges brought about by changes in the internal and external environments, continue to deepen reforms, and ensure the stable and healthy development of the industrial economy.

2 notes

·

View notes

Text

5G Systems Integration Market Driven By Increase Investments In U.S., China, And Japan

The global 5G systems integration market size is estimated to reach USD 62.69 billion by 2030, registering a CAGR of 27.3% from 2022 to 2030, according to a new study by Grand View Research, Inc. Robust increase in the investments to deploy 5G network infrastructures across key countries, such as U.S., China, and Japan, has created the demand for integrating entire fifth generation infrastructure and applications across enterprises. This process will help enterprises to work as a centralized platform that will assist in reducing overall complexity. Thus, robust investments in building fifth-generation infrastructure, coupled with the growing need to set up a 5G-enabled ecosystem, are estimated to propel market growth.

Rapidly building smart cities have surged the adoption of numerous Internet of Things (IoT) devices across the globe. IoT devices require enhanced bandwidth to function appropriately. Thus, in order to provide high-speed broadband by supporting fifth-generation New Radio (NR), such as sub-6GHz and mmWave frequency bands, the entire infrastructure across these smart cities need to be upgraded in line with supporting fifth-generation radio network. Therefore, it is further estimated to boost the market growth from 2022 to 2030.

Gain deeper insights on the market and receive your free copy with TOC now @: 5G Systems Integration Market Report

Moreover, with the evolution of industry 4.0, the adoption of industrial sensors and collaborative robots is gaining popularity in the manufacturing sector across the globe. Therefore, to deliver seamless network connectivity to these above-mentioned devices, it is anticipated to raise the demand for 5G system integration services to make entire manufacturing facilities compatible with supporting next-generation 5G NR.

Rapidly rising digital transformation has disrupted the entire operation of the manufacturing industry. This has increased the trend of the machine-to-machine (M2M) communications to increase overall productivity as well as streamline the whole process. As a result, this has further expanded the need for high broadband to deliver uninterrupted connectivity to industrial sensors and robots. Therefore, the growing need for high broadband connectivity to establish seamless communication between machines is expected to elevate the demand for 5G system integration services in the next few years.

Furthermore, with the emergence of new technologies, such as network slicing and software-defined networking (SDN), the adoption of 5G system integration will witness a rapid surge to reduce overall enterprise infrastructure costs. Moreover, highly trained professionals must implement and manage the fifth-generation system integration services. This is anticipated to hinder market growth over the forecast period.

#5G System Integration Market Size & Share#Global 5G System Integration Market#5G System Integration Market Latest Trends#5G System Integration Market Growth Forecast#COVID-19 Impacts On 5G System Integration Market#5G System Integration Market Revenue Value

2 notes

·

View notes

Text

Induction Motor Market - Forecast(2022 - 2027)

Induction Motor Market Size is forecast to reach $54.2 billion by 2026, at a CAGR of 6.5% during 2021-2026. An induction motor is an AC electric motor in which torque is produced by the reaction between a varying magnetic field generated in the stator and the current induced in the coils of the rotor. It is used in a majority of machinery, as it is more powerful and eco-friendly compared to the conventional motors in the market. North America has significant share in global induction motor market due to a developed usage of an induction motor in the significant industrial manufacturing, aerospace & defense, and automotive companies. In addition to the growing preference for electric vehicles in the U.S. is also stimulating the growth in North America.

Report Coverage

The report: “Induction Motor Market Report– Forecast (2021-2026)”, by IndustryARC covers an in-depth analysis of the following segments of the Induction Motor market

By Rotor Type: Inner Rotor, Outer Rotor

By Type: Single Phase, Three Phase

By Efficiency Class: IE1, IE2, IE3, IE4

By Voltage: Upto 1KV, 1-6.6 KV, Above 6.6KV

By Vertical: Industrial, Commercial, Residential, Agriculture, Automotive and Others

By Geography: North America (U.S, Canada, Mexico), South America(Brazil, Argentina and others), Europe(Germany, UK, France, Italy, Spain, Russia and Others), APAC(China, Japan India, SK, Aus and Others), and RoW (Middle East and Africa)

Request Sample

Key Takeaways

The rising demand for efficient energy usage over concerns of environmental impact of energy generation from conventional sources such as coal and natural gas, is expected to help grow the Induction Motor market in APAC.

The inner rotor segment is growing at a significant CAGR rate of 7.1% in the forecast period. In inner rotor type motors, rotors are positioned at the centre and surrounded by stator winding.

Automotive sector is expected to witness a highest CAGR of 8.9% the forecast period, owing to various factors such as increase in sales of electric vehicles due to rising concerns over greenhouse gases emissions, and favourable government policies in countries such as India, China and so on.

Induction Motor companies are strengthening their position through mergers & acquisitions and continuously investing in research and development (R&D) activities to come up with solutions to cater to the changing requirements of customers.

Induction Motor Market Segment Analysis - By Rotor Type

Three Phase segment is growing at a significant CAGR of 11.1%

in the forecast period. A three phase induction motor is a type of AC induction motors which operates on three phase supply. These three phase induction motors are widely used AC motor to produce mechanical power in industrial applications. Almost 70% of the machinery in industrial applications uses three-phase induction motors, as they are cost-effective, robust, maintenance-free, and can operate in any environmental condition. Moreover, induction motors are the most used in industry since they are rugged, inexpensive, and are maintenance free. In addition they are widely used in the mining metals and cement, automotive, oil and gas, healthcare, manufacturing industries and so on. Increase awareness of environmental protection across industries also contributes to the growth of three phase induction motors, as they have a low emission rate. Moreover, the shift towards industrial automation, coupled with the rising consumer confidence & promising investment plans triggers demand for the three phase induction motor in industrial application. Furthermore, the advent of Industry 4.0 and technological advancements enables a wide adoption base for the three phase induction motors. In 2019, Oriental Motor USA introduced their latest high efficiency three-phase AC induction motors equipped with a terminal box and a high strength right-angle hypoid gearhead, these new three-phase motors have the capacity of two new wattages of 30W and 40W and expands the KIIS Series Standard AC motors product line-up.

Inquiry Before Buying

Induction Motor Market Segment Analysis - By Vertical

Automotive sector is expected to witness a highest CAGR of 8.9% in the forecast period, owing to various factors such as increase in sales of electric vehicles due to rising concerns over greenhouse gases emissions, and favorable government policies in countries such as India, China and so on. In addition, the shift towards industrial automation, coupled with the rising consumer confidence & promising investment plans triggers demand for the induction motor in industrial application. Furthermore, the advent of Industry 4.0 enables a wide adoption base for the induction motors. Moreover, growing number of product launches by major manufacturers will drive the market growth in the forecast period. In September 2019, Motor and drive manufacturer WEG released the M Mining series of slip-ring induction motors which are designed especially for use in the dusty environments of iron ore operations and the cement sector. In July 2019, Ward Leonard launched 2000 HP induction motor WL29BC200 which is designed tote into a package of 15000 HP for the oil and gas industry. In September 2019, Tata Motors launched Tigor EV for private buyers as well as cab aggregators and EESL staff. he Tata Tigor electric uses a 72 V, 3-Phase Induction motor

Induction Motor Market Segment Analysis - By Geography

Induction Motor market in Asia-Pacific region held significant market share of 38.5% in 2020. Increasing compliance for energy efficient motors and rising adoption of motor-driven electric vehicles are the key factors driving market growth. The rising demand for efficient energy usage over concerns of environmental impact of energy generation from conventional sources such as coal and natural gas, is expected to help grow the Induction Motor market. In addition advancements in the agriculture sector and enormous investments in industrialization in countries such as China, India, South Korea, and Australia is driving the market growth. Further, the increasing production and sales of electric vehicles in countries including China and Japan is also analyzed to drive the market growth.

Schedule a Call

Induction Motor Market Drivers

Robust Structure of Motor

The rough physical structure of the motor is predicted to be a major driving factor for the growth of the induction motor market. Induction motor are robust in nature and can be operated in any climatic conditions. Moreover, the absence of slip rings and brushes in the motor induction eliminates the chances of sparks, which makes the operation safe even in the most explosive working conditions. In addition, induction motor is cost effective, highly reliable and the maintenance is very less, which is expected to propel the growth of the induction motor market in the forecast period 2021-2026.

Rise in Production of Electric Vehicles

The electric car market has witnessed rapid evolution with the ongoing developments in automotive sector and favourable government policies and support in terms of subsidies and grants, tax rebates. As induction motors especially three phase are widely used in electric vehicles because of high efficiency, good speed regulation and absence of commutators is analysed to drive the market growth. In addition these motor also serves as an alternative of a permanent magnet in the electric vehicles. Hence rise in production of electric vehicles is analysed to drive the market. In 2019, Ford has invested $1.45 billion in Detroit plants in U.S., to make electric, autonomous and sports utility vehicles, which is mainly aimed to increase the production of the vehicles thereby impacting on the high procurement of the induction motors. In 2019, Toyota announced plans to invest $749M in expanding the U.S. manufacturing facilities to increase the production of the electric and hybrid vehicles. In 2020, General Motors had committed boost its electric vehicle production by investing more than $7 billion. Moreover governments of several countries have been investing heavily for the development of electric vehicles. In 2019 German government has committed to invest more than $3 billion to expand electric car market growth in the region. Hence these investments and developments are analysed to be the key drivers for the growth of the electric vehicle market and thereby the growth of induction motor market during the forecast period 2021-2026.

Buy Now

Induction Motor Market Challenges

Easy availability of low-quality Induction Motors

The market for Induction Motors is highly fragmented, with a significant number of domestic and international manufacturers. Product quality is a primary parameter for differentiation in this market. The organized sector in the market mainly targets industrial buyers and maintains excellent product quality, while the unorganized sector offers low-cost alternatives to tap local markets. Local manufacturers of Induction Motors in most countries target the unorganized sector and compete strongly with the global suppliers in the respective markets. Leading market players are currently exposed to intense competition from such unorganized players supplying inexpensive and low-quality Induction Motors. This acts as a key challenge for the growth of the market.

Induction Motor Market Landscape

Product launches, acquisitions, Partnerships and R&D activities are key strategies adopted by players in the Induction Motor market. Induction Motor top 10 companies include ABB Ltd. AMETEK, Inc., Johnson Electric Holdings Limited, Siemens AG, Rockwell Automation, Toshiba Corp., Hitachi Ltd., Nidec Corporation, ARC Systems Inc., among others.

Acquisitions/Product Launches

In 2021 BorgWarner launched HVH 320 Induction Motors in four variants. They are offered to light-duty passenger cars and heavy-duty commercial vehicles.

In 2020, ABB has launched new range of low voltage IEC induction motors, which are compactly designed and reduces the overall size of the equipment by minimizing space and total cost of ownership.

For more Electronics related reports, please click here

#induction motor Market#induction motor Market Size#electric motor#induction motor Market Share#induction motor Market Analysis#electromagnetic induction#induction motor Market Revenue#asynchronous motor#induction motor Market Trends#induction motor Market Growth#induction motor Market Research#induction motor Market Outlook#induction motor Market Forecast#induction motor Market Price

3 notes

·

View notes

Text

Trunnion Clamps Market Trends and Evolution Analysis 2024 - 2031

The trunnion clamps market was valued at approximately $4.12 billion in 2023. It is projected to grow to $4.3 billion in 2024 and reach $6.12 billion by 2032. This growth corresponds to a compound annual growth rate (CAGR) of around 4.51% during the forecast period from 2024 to 2032. With increasing applications in various industries, the trunnion clamps market is set for steady expansion in the coming years.

The trunnion clamps market plays a crucial role in various industries, including oil and gas, construction, and manufacturing. These components ensure stability and support in a range of applications, making them essential for equipment performance and safety. This article explores the trunnion clamps market, examining its growth factors, key players, trends, and future outlook.

Introduction to Trunnion Clamps

What Are Trunnion Clamps?

Trunnion clamps are mechanical devices used to secure and stabilize equipment, particularly in heavy machinery and piping systems. They allow for easy adjustment and maintenance while providing robust support to prevent movement during operation.

Applications of Trunnion Clamps

Trunnion clamps are widely used in various sectors:

Oil and Gas: For securing pipelines and drilling equipment.

Construction: To stabilize heavy machinery and scaffolding.

Manufacturing: In assembly lines to hold components in place during production.

Market Overview

Market Size and Growth

The trunnion clamps market has been experiencing steady growth. According to industry reports, the market is projected to grow at a CAGR of approximately 5% over the next five years. Factors contributing to this growth include:

Increasing investments in infrastructure development.

Rising demand from the oil and gas sector.

Growth in the manufacturing industry.

Key Trends Driving Market Growth

Technological Advancements: Innovations in material science and design are leading to more efficient and durable trunnion clamps.

Sustainability Focus: There is a growing emphasis on eco-friendly materials and manufacturing processes, pushing companies to innovate.

Automation and Industry 4.0: The integration of smart technologies in manufacturing processes is enhancing the efficiency of trunnion clamp usage.

Competitive Landscape

Key Players in the Trunnion Clamps Market

The trunnion clamps market features several prominent players, including:

Cameron: A leader in oil and gas equipment, known for its high-quality trunnion clamps.

Parker Hannifin: Offers a wide range of industrial clamps and fastening solutions.

Hilti: Specializes in construction tools and fasteners, including trunnion clamps.

Market Share Analysis

These key players hold significant market share, driven by their strong distribution networks and continuous innovation. Collaborations and partnerships are common strategies to enhance market presence.

Challenges Facing the Market

Regulatory Compliance

The trunnion clamps market is subject to various regulations, especially in industries like oil and gas. Compliance with safety and environmental standards can be challenging for manufacturers.

Price Fluctuations of Raw Materials

The costs of raw materials used in manufacturing trunnion clamps can fluctuate significantly, affecting overall production costs and pricing strategies.

Future Outlook

Opportunities for Growth

The future of the trunnion clamps market appears promising, with several opportunities on the horizon:

Emerging Markets: Growth in developing countries presents new opportunities for market expansion.

Innovation in Design: There is a constant need for improved designs to meet specific industry requirements.

Conclusion

The trunnion clamps market is poised for growth as industries continue to expand and innovate. Key players will need to navigate challenges such as regulatory compliance and raw material costs while seizing opportunities in emerging markets and technological advancements. As the demand for robust and reliable clamps increases, the market is likely to evolve, offering new solutions to meet the needs of various sectors.

0 notes

Text

The global industrial automation software market is projected to grow at a CAGR of 7.4%, reaching $59.5 billion by 2029, driven by increasing demand for reliable manufacturing, mass production, and the emergence of Industry 4.0 technologies. Key growth opportunities exist in developing countries with automation-driven industries. The market is segmented by product, deployment type, end user, and geography, with supervisory control and data acquisition (SCADA) expected to dominate in 2022. However, the human machine interface (HMI) segment is anticipated to experience the highest growth during the forecast period.

0 notes

Text

Kaolin Market Intelligence Report Offers Growth Prospects

Kaolin Industry Overview

The global kaolin market size was valued at USD 3.98 billion in 2023 and is expected to grow at a compound annual growth rate (CAGR) of 4.0% from 2024 to 2030.Increasing investment in construction and infrastructure industry is propelling demand for paints & coatings, ceramic-based products, and cement, which is driving market growth.

Global construction industry is expected to witness lucrative growth over shifting inclination towards green construction, which in turn is expected to provide a significant growth opportunity for kaolin market. For instance, according to the World Bank’s new IFC report, green construction is anticipated to make investment opportunities worth USD 1.5 trillion for emerging markets.

Gather more insights about the market drivers, restrains and growth of theKaolin Market

Investments in construction, infrastructure development, and automotive production are expected to contribute to market growth over the forecast period. Growth of construction industry in the U.S. is a key factor contributing to demand for kaolin in the country. According to U.S. Census Bureau, total construction spending (residential and non-residential) grew by 3.5% in June 2023 on a y-o-y basis. The spending on single-family housing increased by 2.1% and multi-family housing by 1.5%.

Growing demand for painting due to rising investments in construction is leading companies to engage in strategic measures such as mergers & acquisitions, which are expected to influence the market demand positively. For instance, in November 2021, GDB International, Inc., a producer of paints & coatings, acquired a paint manufacturing plant in Illinois, U.S. This plant has a production capacity of 5 million gallons per year and can produce both water and solvent-based paints.

Further investments in medical industry are another driving factor for the market. For instance, in December 2021, Pfizer announced that it would acquire Arena Pharmaceuticals for about USD 6.70 billion. This deal was completed in March 2022 and is expected to help advance its presence in treatment of several immuno-deficiency diseases. Such developments indicate healthy growth for country’s pharmaceutical and medical industries. This is anticipated to have a positive impact on demand for kaolin in pharmaceuticals and medical application segment.

Browse through Grand View Research's Advanced Interior Materials Industry Research Reports.

The India kaolin market size was estimated at USD 349.6 million in 2023 and is expected to grow at a CAGR of 5.2% from 2024 to 2030. The increasing construction and infrastructural developments, paper manufacturing, and growing paints and coating industries are driving growth for kaolin.

The global HDPE and LLDPE geomembrane market size was estimated at USD 1.36 billion in 2023 and is expected to grow at a CAGR of 5.6% from 2024 to 2030.

Key Companies profiled:

BASF SE

EICL Ltd.

Imerys S.A.

I-Minerals Inc.

KaMin LLC

LB Minerals Ltd.

Maoming Xingli Kaolin Co. Ltd.

Quazwerke GmbH

Sibelco

Thiele Kaolin Company

Key Kaolin Company Insights

Some of the key players operating in the market include KaMin LLC, Imerys S.A. and Sibelco.

KaMin LLC acquired the kaolin business from BASF SE in September 2022. The divestiture consists of the production hub with sites Toddvile, Edgar, Deweyville, and Gordon mines, mills, and reserves in the U.S.

Imerys S.A. specializes in the production & processing of minerals. It sells its products through three business segments: Performance Minerals Americas, Performance Minerals Asia Pacific, and Performance Minerals Europe, Middle East, and Africa.

Sibelco’s product portfolio includes dry sand, wet sands, kaolin, silica flour, frac sand, ball clay, cristobalite, feldspar, filtration sand, olivine sand, spherical silica, high-purity quartz, quicklime, coated sands, red clay, prepared bodies, hydrated lime, diatomite, nepheline Semite, olivine flour, and lithium minerals. The company manufactures kaolin for producing fine ceramics. The company’s kaolin reserves are in UK, Czech Republic, France, Germany, Spain, Portugal, and Ukraine.

WA Kaolin Limited and Maoming Xingli Kaolin Co., Ltd. are some of the emerging market participants.

WA kaolin is a mineral exploration, mining, and processing company. In November 2020, the company completed its definitive feasibility study of Wickepin Kaolin Project and in 2022 the company commissioned stage 1 of the Wickepin Processing plant

Maoming Xingli Kaolin Co., Ltd. has a high-quality mine named acicular kaolin mine that spreads across 800 acres. The company offers several products such as bone china clay, clay for porcelain, kaolin clay, porcelain clay, and others. Its key focus is on washed kaolin (without acid), 90-degree ball clay, and 90- degree kaolin.

Recent Developments

In November 2023, KaMin LLC and CADAM announced a price increase of their kaolin products by up to 9% starting from January 2024. This is to offset cost increase due to inflation, increase in mining cost, stringent environmental and regulatory requirements, and increase in electricity rates in the U.S. and Brazil, and labor cost.

In January 2024, the Federal Government of Nigeria announced that it has started to explore the possibility of production of salt and kaolin in Abuja. This is expected to increase global supply, hence providing price favorability to end users at a regional level.

Order a free sample PDF of the Kaolin Market Intelligence Study, published by Grand View Research.

0 notes

Text

Chemical Injection Skid Market Analysis: Projected to Reach $2.8 Bn by 2034

The Chemical Injection Skid Market is a crucial segment within the global oil & gas, water treatment, petrochemical, and chemical industries. A chemical injection skid is a specialized system used for the precise dosing of chemicals to control and optimize processes in various industries. These skids are vital for corrosion control, pH regulation, scale inhibition, and other treatments, ensuring smooth operations and protecting equipment. The market for chemical injection skids is driven by the increasing need for automation in industrial processes, rising demand for enhanced safety protocols, and the growing emphasis on efficiency and environmental sustainability.

Market Size and Growth

The global Chemical Injection Skid industry, valued at US$ 1.8 billion in 2023, is projected to grow at a compound annual growth rate (CAGR) of 4.0% from 2024 to 2034, reaching US$ 2.8 billion by 2034, especially in regions like North America, Asia-Pacific, and the Middle East. Factors such as the increasing demand for natural gas, water treatment, and chemical production are key growth drivers. In addition, the surge in offshore oil & gas exploration and production activities is contributing to the demand for chemical injection systems to ensure optimal process efficiency and compliance with environmental regulations.

For More Details, Request for a Sample of this Research Report: https://www.transparencymarketresearch.com/chemical-injection-skids-market.html

Market Segmentation

The Chemical Injection Skid Market can be segmented as follows:

By Service Type:

Design and Engineering

Installation and Commissioning

Maintenance and Support

By Sourcing Type:

In-house Manufacturing

Outsourced Manufacturing

By Application:

Oil & Gas

Water Treatment

Chemical Processing

Pharmaceuticals

Others (Mining, Power Generation)

By Industry Vertical:

Oil & Gas

Water and Wastewater Treatment

Chemicals and Petrochemicals

Energy and Power

Pharmaceuticals

By Region:

North America

Europe

Asia-Pacific

Middle East & Africa

Latin America

Regional Analysis

North America: Dominates the chemical injection skid market due to advanced industrial infrastructure and the significant presence of the oil & gas industry. The U.S. and Canada contribute largely to market demand, driven by shale gas exploration and the rising need for water treatment facilities.

Europe: The market in Europe is driven by stringent environmental regulations and the need for chemical treatment systems across sectors such as oil refining and wastewater treatment. Countries like Germany, Norway, and the UK are key contributors.

Asia-Pacific: Rapid industrialization in countries such as China, India, and Southeast Asia is fueling demand for chemical injection skids. The growing demand for energy and chemicals, coupled with infrastructure development, is a significant factor driving market growth in this region.

Middle East & Africa: Known for its large-scale oil production, the Middle East is a critical region for the market. The growing focus on enhanced oil recovery (EOR) and offshore exploration is expected to propel the demand for chemical injection systems in the coming years.

Latin America: Latin America, led by Brazil and Mexico, holds potential for market growth due to increasing investments in oil & gas exploration and the need for water treatment systems.

Market Drivers and Challenges

Drivers:

Rising Oil & Gas Exploration: Growing global energy demand and investments in upstream oil & gas exploration, particularly in offshore regions, is driving the need for chemical injection systems to maintain operational efficiency.

Environmental Regulations: Increasing regulatory pressure to reduce emissions and treat industrial waste is boosting the demand for advanced chemical treatment systems across sectors such as water treatment and chemicals.

Technological Advancements: Automation, remote monitoring, and intelligent systems for precise chemical dosing are further enhancing the adoption of chemical injection skids across industries.

Challenges:

High Initial Costs: The initial cost of installation and commissioning of chemical injection systems is high, which can deter smaller companies from adopting these systems.

Fluctuations in Raw Material Prices: The volatile nature of raw material prices, particularly metals and chemicals used in manufacturing, poses a challenge to market growth.

Complexity in System Design: Ensuring precise and customized system designs for various industry-specific applications can be a challenge for manufacturers.

Market Trends

Automation and Smart Skids: The integration of advanced sensors, automation, and real-time monitoring systems is a growing trend in the market. These smart skids allow operators to remotely monitor and control chemical dosing, enhancing safety and efficiency.

Sustainable Chemical Injection Systems: Increasing focus on environmentally friendly and sustainable processes is leading to the development of systems that optimize chemical usage, reduce waste, and improve the sustainability of industrial operations.

Growth in Water Treatment: The rising need for clean water and wastewater treatment across the globe is expected to drive demand for chemical injection systems that can precisely control chemical dosing in treatment facilities.

Future Outlook

The Chemical Injection Skid Market is poised for steady growth over the next decade, with increasing adoption across various industries such as oil & gas, chemicals, and water treatment. Technological advancements, coupled with rising environmental concerns, are expected to shape the future of the market. The ongoing shift towards automation, smart systems, and sustainable practices will further drive demand for innovative chemical injection solutions.

Key Market Study Points

Increasing demand for chemical injection systems in oil & gas, water treatment, and chemical processing.

The growing emphasis on automation and sustainability in industrial operations.

Regional market dynamics, particularly in North America, Asia-Pacific, and the Middle East, will play a crucial role in driving global market growth.

Advancements in remote monitoring and control technologies for chemical injection systems.

Buy this Premium Research Report: https://www.transparencymarketresearch.com/checkout.php?rep_id=66185<ype=S

Competitive Landscape

The competitive landscape of the Chemical Injection Skid Market is characterized by the presence of key players such as Frames Group, Parker Hannifin Corp., Lewa GmbH, SPX Flow, Milton Roy, and Petronash. These companies are focusing on innovation, product customization, and strategic collaborations to expand their market presence. Mergers and acquisitions, along with investments in R&D, are key strategies adopted by leading players to maintain competitiveness in the market.

Recent Developments

Frames Group has launched a new range of modular chemical injection skids with enhanced automation and real-time monitoring capabilities.

Parker Hannifin introduced a sustainable chemical dosing skid aimed at reducing chemical wastage and improving energy efficiency.

SPX Flow announced the expansion of its chemical injection skid product line, with a focus on systems designed for water and wastewater treatment.

About Transparency Market Research

Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information.

Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports.

Contact:

Transparency Market Research Inc.

CORPORATE HEADQUARTER DOWNTOWN,

1000 N. West Street,

Suite 1200, Wilmington, Delaware 19801 USA

Tel: +1-518-618-1030

USA – Canada Toll Free: 866-552-3453

Website: https://www.transparencymarketresearch.com

0 notes

Text

Asia Pacific USB Cable Market Demand, Industry Market, Growth, Size, Report by 2024 to 2032

The Reports and Insights, a leading market research company, has recently releases report titled “Asia Pacific USB Cable Market: Industry Trends, Share, Size, Growth, Opportunity and Forecast 2024-2032.” The study provides a detailed analysis of the industry, including the Asia Pacific USB Cable Market share, size, trends, and growth forecasts. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

Report Highlights:

How big is the Asia Pacific USB Cable Market?

The Asia Pacific USB cable market was valued at US$ 5.7 Billion in 2023 and is expected to register a CAGR of 15.6% over the forecast period and reach US$ 21.01 Bn in 2032.

What are Asia Pacific USB Cable?

A USB cable is a common interface used for both data transfer and power delivery between devices like computers, smartphones, and peripherals such as printers or external drives. It provides a universal solution for connecting different types of devices, eliminating the need for multiple ports and connectors. USB cables are available in various types, including USB-A, USB-B, and the increasingly popular USB-C, which offers faster data transfer and improved charging efficiency. USB-C, in particular, has become the standard for many modern devices due to its enhanced performance and versatility.

Request for a sample copy with detail analysis: https://www.reportsandinsights.com/sample-request/2435

What are the growth prospects and trends in the Asia Pacific USB Cable industry?

The Asia Pacific USB cable market growth is driven by various factors and trends. The USB cable market in the Asia Pacific region is witnessing significant growth, fueled by the rising demand for electronics such as smartphones, laptops, and tablets. The increasing use of USB Type-C cables, known for their high-speed data transfer and fast charging capabilities, is accelerating this trend. The expanding digital landscape and the surge in IoT devices have heightened the need for dependable connectivity solutions. Additionally, the region's strong manufacturing base and technological advancements are supporting the development of more efficient USB cables, with countries like China, Japan, and India playing pivotal roles in the market's growth. Hence, all these factors contribute to Asia Pacific USB cable market growth.

What is included in market segmentation?

The report has segmented the market into the following categories:

By Type

USB-A

USB-B

USB-C

Mini-USB

Micro-USB

By USB Version

USB 1.0

USB 2.0

USB 3.0/3.1/3.2

USB 4.0

By Length

Up to 1M

1-3M

3-5M

By Application

Consumer Electronics

Industrial Equipment

Medical Devices

Others

By End-User

Individual Consumers

Business and Enterprises

Original Equipment Manufacturers

Who are the key players operating in the industry?

The report covers the major market players including:

Promate

Infineon Technologies AG

Anker

ERD Technologies Private Limited

Ambrane

C.I. Cables

Bluesmart technologies

BMA technologies Ltd

View Full Report: https://www.reportsandinsights.com/report/Asia Pacific USB Cable-market

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

Reports and Insights consistently mееt international benchmarks in the market research industry and maintain a kееn focus on providing only the highest quality of reports and analysis outlooks across markets, industries, domains, sectors, and verticals. We have bееn catering to varying market nееds and do not compromise on quality and research efforts in our objective to deliver only the very best to our clients.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

Contact Us:

Reports and Insights Business Research Pvt. Ltd.

1820 Avenue M, Brooklyn, NY, 11230, United States

Contact No: +1-(347)-748-1518

Email: [email protected]

Website: https://www.reportsandinsights.com/

Follow us on LinkedIn: https://www.linkedin.com/company/report-and-insights/

Follow us on twitter: https://twitter.com/ReportsandInsi1

#Asia Pacific USB Cable Market share#Asia Pacific USB Cable Market size#Asia Pacific USB Cable Market trends

0 notes

Text

Rock Drilling Jumbo Market Size, Analyzing Forecasted Outlook and Growth for 2024-2030

Global Info Research announces the release of the report “Global Rock Drilling Jumbo Market 2024 by Manufacturers, Regions, Type and Application, Forecast to 2030” . This report provides a detailed overview of the market scenario, including a thorough analysis of the market size, sales quantity, average price, revenue, gross margin and market share.The report provides an in-depth analysis of the competitive landscape, manufacturer’s profiles,regional and national market dynamics, and the opportunities and challenge that the market may be exposed to in the near future. Global Rock Drilling Jumbo market research report is a comprehensive analysis of the current market trends, future prospects, and other pivotal factors that drive the market.

Rock Drilling Jumbo is mainly composed of rock drill, drill arm (the support, positioning and propelling mechanism), frame, travel system, and other necessary attachments. The product features self-propelling and that multiple rock drills can work simultaneously. And it is mainly used in the tunneling operation by drilling and blasting method and mining exploration.

According to our (Global Info Research) latest study, the global Rock Drilling Jumbo market size was valued at US$ 428 million in 2023 and is forecast to a readjusted size of USD 560 million by 2030 with a CAGR of 4.0% during review period.

The global rock drill jumbo market size reached US$415.71 million in 2023, and is expected to reach US$546.91 million in 2030, with a compound annual growth rate (CAGR) of 4.05%. The market is mainly driven by the downstream mining and infrastructure industries.

Global Rock Drilling Jumbo key players include Epiroc, Sandvik Construction, Furukawa, Komatsu Mining Corp., Sitoncn, etc. Global top five manufacturers hold a share about 56%.

Growth in mining activities and construction projects, particularly in developing economies, has driven demand for rock drill jumbos. Infrastructure development, urbanization, and the need for resource extraction are major contributors.Advances in drilling technology, including automation and smart drilling systems, are enhancing the efficiency and safety of rock drill jumbos. Features such as GPS navigation, remote operation, and real-time data analytics are becoming more common.There is a trend towards electric and hybrid rock drill jumbos as industries seek to reduce emissions and operating costs. These models are seen as more sustainable and cost-effective in the long run.

This report is a detailed and comprehensive analysis for global Rock Drilling Jumbo market. Both quantitative and qualitative analyses are presented by manufacturers, by region & country, by Type and by Application. As the market is constantly changing, this report explores the competition, supply and demand trends, as well as key factors that contribute to its changing demands across many markets. Company profiles and product examples of selected competitors, along with market share estimates of some of the selected leaders for the year 2024, are provided.

Market Segmentation

Rock Drilling Jumbo market is split by Type and by Application. For the period 2019-2029, the growth among segments provides accurate calculations and forecasts for consumption value by Type, and by Application in terms of volume and value.

Market segment by Type: Single Arm Rock Drilling Jumbo、Double Arm Rock Drilling Jumbo、Multi Arm Rock Drilling Jumbo

Market segment by Application:Mining、Railway and Highway Construction、Other

Major players covered: Epiroc、Sandvik Construction、Furukawa、Komatsu Mining Corp.、J.H. Fletcher、Sitoncn、Mine Master、Hebei Hong Yuan Hydraulic Machinery and Technology Co.、HAZEMAG、Lake Shore Systems、XCMG、China Railway Engineering Equipment Group Co., Ltd.、Zhangjiakou Xuanhua Huatai Mining&Metallurgical Machinery Co., Ltd.、Shandong China Coal Industrial&Mining Supplies Group Co.,Ltd、Cocental - CMM、Sichuan Zuanshen Intelligent Machinery Manufacturing Co., Ltd.

The content of the study subjects, includes a total of 15 chapters:

Chapter 1, to describe Rock Drilling Jumbo product scope, market overview, market estimation caveats and base year.

Chapter 2, to profile the top manufacturers of Rock Drilling Jumbo, with price, sales, revenue and global market share of Rock Drilling Jumbo from 2019 to 2024.

Chapter 3, the Rock Drilling Jumbo competitive situation, sales quantity, revenue and global market share of top manufacturers are analyzed emphatically by landscape contrast.

Chapter 4, the Rock Drilling Jumbo breakdown data are shown at the regional level, to show the sales quantity, consumption value and growth by regions, from 2019 to 2030.

Chapter 5 and 6, to segment the sales by Type and application, with sales market share and growth rate by type, application, from 2019 to 2030.

Chapter 7, 8, 9, 10 and 11, to break the sales data at the country level, with sales quantity, consumption value and market share for key countries in the world, from 2017 to 2023.and Rock Drilling Jumbo market forecast, by regions, type and application, with sales and revenue, from 2025 to 2030.

Chapter 12, market dynamics, drivers, restraints, trends and Porters Five Forces analysis.

Chapter 13, the key raw materials and key suppliers, and industry chain of Rock Drilling Jumbo.

Chapter 14 and 15, to describe Rock Drilling Jumbo sales channel, distributors, customers, research findings and conclusion.

Our Market Research Advantages:

Global Perspective: Our research team has a strong understanding of the company in the global Rock Drilling Jumbo market.Which offers pragmatic data to the company.

Aim And Strategy: Accelerate your business integration, provide professional market strategic plans, and promote the rapid development of enterprises.

Innovative Analytics: We have the most comprehensive database of resources , provide the largest market segments and business information.

About Us:

Global Info Research is a company that digs deep into global industry information to support enterprises with market strategies and in-depth market development analysis reports. We provide market information consulting services in the global region to support enterprise strategic planning and official information reporting, and focuses on customized research, management consulting, IPO consulting, industry chain research, database and top industry services. At the same time, Global Info Research is also a report publisher, a customer and an interest-based suppliers, and is trusted by more than 30,000 companies around the world. We will always carry out all aspects of our business with excellent expertise and experience.

0 notes

Text

Global Sensors in Oil and Gas Market Analytical Overview and Growth Opportunities by 2034

Global Sensors in Oil and Gas Market: Key Trends and Insights for 2024

Introduction

In the evolving landscape of the oil and gas industry, sensors have become indispensable tools for enhancing operational efficiency and safety. The Global Sensors in Oil and Gas Market is witnessing remarkable growth, driven by advancements in technology and an increasing focus on optimizing resource management. As we approach 2024, understanding the current trends and future outlook of this market is crucial for industry stakeholders. This blog provides an overview of the key developments and insights shaping the sensors market in the oil and gas sector.

Grab Sample PDF Copy:https://wemarketresearch.com/reports/request-free-sample-pdf/global-sensors-in-oil-and-gas-market/1522

The Role of Global Sensors in Oil and Gas Market

Sensors play a critical role in the oil and gas industry by providing real-time data and insights that help in monitoring, controlling, and optimizing various processes. These devices are used across a range of applications, including exploration, drilling, production, and refining. Common types of sensors used in the industry include pressure sensors, temperature sensors, flow sensors, and level sensors. By delivering accurate and timely data, sensors enable better decision-making, enhance safety, and reduce operational costs.

Key Trends Shaping the Global Sensors in Oil and Gas Market

Technological Advancements

The sensors market in oil and gas is experiencing rapid technological advancements. Innovations such as wireless sensor networks, advanced data analytics, and the integration of IoT are transforming how sensors operate and communicate. Wireless sensors are particularly valuable for remote monitoring, eliminating the need for extensive cabling and reducing installation costs. Advanced data analytics enable predictive maintenance, helping companies anticipate and address potential issues before they become critical.

Increased Focus on Safety and Compliance

Safety and regulatory compliance are top priorities in the oil and gas industry. Sensors are instrumental in ensuring adherence to safety standards and environmental regulations. For instance, gas leak detectors and pressure sensors help prevent accidents and mitigate the risk of hazardous incidents. The increasing emphasis on environmental protection and safety regulations is driving the demand for advanced sensors that offer higher precision and reliability.

Rising Adoption of IoT and Smart Sensors

The integration of IoT technology with sensors is a significant trend in the oil and gas sector. Smart sensors equipped with IoT capabilities provide real-time data access, remote monitoring, and enhanced connectivity. This integration allows for more effective asset management, streamlined operations, and improved decision-making. IoT-enabled sensors also facilitate the implementation of Industry 4.0 principles, promoting automation and digital transformation within the industry.

Demand for Predictive Maintenance

Predictive maintenance is becoming a crucial aspect of operations in the oil and gas industry. By leveraging sensor data and advanced analytics, companies can predict equipment failures and perform maintenance activities proactively. This approach minimizes downtime, extends equipment lifespan, and reduces operational costs. As a result, there is a growing demand for sensors that can deliver precise and actionable data for predictive maintenance applications.

Expansion in Emerging Markets

Emerging markets are playing a significant role in the growth of the sensors market. Countries in Asia-Pacific, Latin America, and the Middle East are investing heavily in their oil and gas infrastructure, leading to increased demand for advanced sensor technologies. The expansion of exploration and production activities in these regions is driving the need for reliable and efficient sensors to support new projects and enhance existing operations.

Challenges Facing the Global Sensors in Oil and Gas Market

Despite the positive trends, the sensors market in oil and gas faces several challenges. Harsh operating environments, such as extreme temperatures and high pressure, can impact sensor performance and longevity. Additionally, the high cost of advanced sensor technologies may be a barrier for some companies, particularly smaller players in the industry. Addressing these challenges requires ongoing innovation and investment in sensor development.

Global Sensors in Oil and Gas Market Segmentation

The global sensors in oil and gas market can be segmented based on various factors, including:

Sensor type: Pressure sensors, temperature sensors, flow sensors, level sensors, gas sensors, and others.

Application: Upstream, midstream, and downstream sectors of the oil and gas industry.

Region: North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa.

Conclusion

The Global Sensors in Oil and Gas Market is poised for substantial growth in 2024, driven by technological advancements, a focus on safety and compliance, and the adoption of IoT and smart sensors. As the industry continues to evolve, the demand for reliable and innovative sensor solutions will increase. Companies that embrace these trends and invest in cutting-edge technologies will be well-positioned to enhance their operational efficiency and stay ahead in this competitive market.

0 notes

Text

Enhancing Supply Chain Efficiency with Carbon Steel Procurement Intelligence

The carbon steel category is expected to grow at a CAGR of 4.0% from 2023 to 2030. The APAC region accounts for the largest category share and is anticipated to be the fastest-growing region in the forecast period. Factors such as the rise in the need for carbon steel in infrastructure development, the automotive sector, construction sites, and machinery are driving the category growth. One of the key trends is the use of this product in the shipbuilding industry owing to the growing demand in China, and Southeast Asia. Availability of cheap labor and technological advancement are the reason companies are shifting their shipbuilding manufacturing to these countries.

High-temperature drawing (HTD), advanced metallurgy, and coatings are a few technological advancements that are generally used in this category to enhance the properties of carbon steel. HTD is used by manufacturers to reduce cost, production time, and the impact on environment during the production. Coatings and advanced metallurgy techniques are used by manufacturers to enhance durability and to give strengthening to the product thereby increasing protection from corrosion and less wear and tear resulting in an enhanced product life cycle. Companies are utilizing technologies to gain a competitive advantage over others. In 2020, U.S. Steel Corporation invested USD 1.2 billion in constructing a rolling and endless casting facility in Pennsylvania to reduce its environmental footprint and improve operational efficiency.

The category is consolidated with top players taking over and capturing a larger market share. They are constantly working on developing new and innovative products, solutions, and technologies to cater to the demand of larger industries and to have a competitive lead over others. Top players have strategically allied with other manufacturers to acquire the latest technology and outsource some of their operations to make the market competitive and extend barriers for new entrants. In 2021, Sumitomo Metal Corporation and Nippon Steel called a new business strategy – NSSMC Beyond 2022, to strengthen their market competitiveness and expand their business globally. Players are acquiring stakes to expand their business portfolios. In 2020, Tata Steel acquired the remaining 25.1% stake in the Tata Steel subsidiary company, Tata Steel BSL Limited. This acquisition helped in strengthening and expanding their product portfolio.

Order your copy of the Carbon Steel Procurement Intelligence Report, 2023 - 2030, published by Grand View Research, to get more details regarding day one, quick wins, portfolio analysis, key negotiation strategies of key suppliers, and low-cost/best-cost sourcing analysis

Coking coal and iron ore drives the steel price along with the effect of the supply-demand scenario of the category plays a major role in constituting the price. The prices of these raw materials are expected to remain volatile due to state-mandated measures to reduce carbon emissions and rising geopolitical tensions. Owing to strict lockdowns in Shanghai amid covid-19 pandemic and the Russia-Ukraine war have caused drastic effects in disrupting the supply chain. With easing curbs in restrictions and normalization in the supply chain have rallied the demand. In 2023, steel prices in China went up by 55.4% from USD 749 to USD 1,164 in April. With the U.S. and Europe back on inventory replenishment, demand for global supply increased resulting in an increase in prices of hot rolled carbon steel by USD 38.24 per tonne and hot rolled steel coils by USD 28.68.

Sourcing of the category involves procurement of raw materials and import of the final product from various countries. China, Russia, and Japan are the top exporters in this category. The wide availability of raw materials and large export of semi-finished and finished goods are helping them in leading the market. Best sourcing practices include reaching potential suppliers with the delivery of good quality raw materials, reduced lead time, competitive pricing, and meeting regulatory compliance. China dominates the category with the export of 66.2 million metric tons of its production. It exports majorly to the U.S., Vietnam, and India. It stands at the largest steel industry in the world and manufactures around half of all crude steel produced globally. Chinese producer, Baowu Group produces 120 million metric tons of crude steel, which is significantly higher than other producers around the world.

Browse through Grand View Research’s collection of procurement intelligence studies:

• Activated Carbon Procurement Intelligence Report, 2023 - 2030 (Revenue Forecast, Supplier Ranking & Matrix, Emerging Technologies, Pricing Models, Cost Structure, Engagement & Operating Model, Competitive Landscape)

• Glycol Ethers Procurement Intelligence Report, 2023 - 2030 (Revenue Forecast, Supplier Ranking & Matrix, Emerging Technologies, Pricing Models, Cost Structure, Engagement & Operating Model, Competitive Landscape)

Carbon Steel Procurement Intelligence Report Scope

• Carbon Steel Category Growth Rate: CAGR of 4.0% from 2023 to 2030

• Pricing growth Outlook: 20 - 25% (Annual)

• Pricing Models: Volume-based pricing model, and Market-based Pricing model

• Supplier Selection Scope: Cost and pricing, Past engagements, Productivity, Geographical presence

• Supplier Selection Criteria: By Steel Durability, End Use, Category Product Segment, Type of Grade, Fitting Type, Size, Number of Production Units, Technical Specifications, Operational Capabilities, Regulatory Standards, and Mandates, Category Innovations, and Others

• Report Coverage: Revenue forecast, supplier ranking, supplier matrix, emerging technology, pricing models, cost structure, competitive landscape, growth factors, trends, engagement, and operating model

Key companies profiled

• AK Steel Corporation

• Arcelor Mittal

• Baosteel Group

• Evraz plc

• HBIS Group

• JFE Steel Corporation

• Nippon Steel Corporation

• NLMK

• POSCO

• United States Steel

Brief about Pipeline by Grand View Research:

A smart and effective supply chain is essential for growth in any organization. Pipeline division at Grand View Research provides detailed insights on every aspect of supply chain, which helps in efficient procurement decisions.

Our services include (not limited to):

• Market Intelligence involving – market size and forecast, growth factors, and driving trends

• Price and Cost Intelligence – pricing models adopted for the category, total cost of ownerships

• Supplier Intelligence – rich insight on supplier landscape, and identifies suppliers who are dominating, emerging, lounging, and specializing

• Sourcing / Procurement Intelligence – best practices followed in the industry, identifying standard KPIs and SLAs, peer analysis, negotiation strategies to be utilized with the suppliers, and best suited countries for sourcing to minimize supply chain disruptions

#Carbon Steel Procurement Intelligence#Carbon Steel Procurement#Procurement Intelligence#Carbon Steel Market#Carbon Steel Industry

0 notes

Text

China Servo Drive Market Size, Share, Overview, Segments, Top Vendors, Regional Outlook and Forecast by 2031

The China Servo Drive Market has emerged as a significant player in the global industrial automation sector, demonstrating remarkable growth and resilience in recent years. Servo drives, essential components in motion control systems, play a crucial role in various industries, including manufacturing, automotive, electronics, and robotics. As China continues to advance technologically and invest heavily in industrial automation, the demand for servo drives has surged, driven by the need for precise and efficient control of machinery and equipment.

Get Free Sample Report @ https://www.metastatinsight.com/request-sample/2744

Top Companies

Ningbo Xingtai Technology Co., Ltd., Shenzhen Sinovo Electric Technologies Co., Ltd., Nanjing Oulu Electric Corp., Ltd., COTRUST Technologies Co., Ltd., Shenzhen Lensail Technology Co., Ltd., Wuhan Huazhong Numerical Control Co., Ltd., Ningbo Vicks Hydraulic Co., Ltd., ACS Motion Control Ltd., CoolDrive A8 (Tsino-Dynatron Electrical Technology).

The growth of the China Servo Drive market can be attributed to several factors, including the country's robust manufacturing sector, rapid industrialization, and increasing adoption of automation technologies. China's manufacturing prowess, fueled by its large labor force, infrastructure development, and government support, has made it a global manufacturing hub. As manufacturers strive to improve productivity, quality, and flexibility, they are increasingly turning to servo drives to optimize their production processes and achieve higher levels of efficiency.

Moreover, the automotive industry, a key driver of demand for servo drives, has witnessed significant growth in China. With the rise of electric vehicles (EVs) and the transition towards smart manufacturing, automotive manufacturers are increasingly relying on servo drives to power various components, such as robotics, conveyors, and assembly lines. The demand for servo drives in the automotive sector is expected to continue growing as China aims to become a leader in electric and autonomous vehicles.

Browse Complete Report @ https://www.metastatinsight.com/report/china-servo-drive-market

In addition to manufacturing and automotive, the electronics industry in China has also contributed to the growth of the servo drive market. With the proliferation of consumer electronics, smartphones, and other electronic devices, there is a growing demand for high-precision manufacturing processes that rely on servo drives for precise motion control. Furthermore, the emergence of Industry 4.0 and the Internet of Things (IoT) has accelerated the adoption of servo drives in smart factories and industrial automation applications, driving further growth in the market.

0 notes

Text

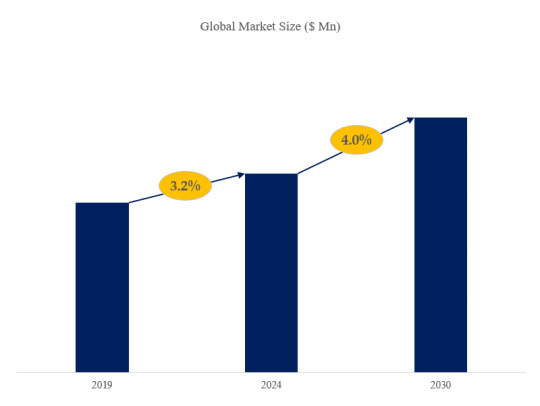

Cromado duro, previsión del tamaño del mercado mundial, clasificación y cuota de mercado de las 11 principales empresas

Según el nuevo informe de investigación de mercado “Informe del Mercado Global del Cromado duro 2024-2030”, publicado por QYResearch, se prevé que el tamaño del mercado mundial del Cromado duro alcance 2.46 mil millones de USD en 2030, con una tasa de crecimiento anual constante del 4.0% durante el período de previsión.

Figure 1. Tamaño del mercado de Cromado duro global (US$ Millión), 2019-2030

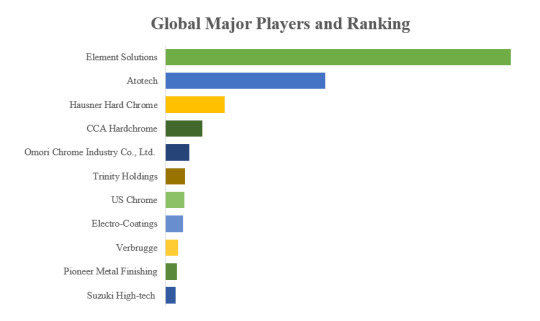

Según QYResearch, los principales fabricantes mundiales de Cromado duro incluyen Element Solutions, Atotech, Hausner Hard Chrome, CCA Hardchrome, Omori Chrome Industry Co., Ltd., Trinity Holdings, US Chrome, Electro-Coatings, Verbrugge, Pioneer Metal Finishing, etc. En 2022, las cinco principales entidades mundiales tenían una cuota de aproximadamente 11.0% en términos de ingresos.

Figure 2. Clasificación y cuota de mercado de las 11 principales entidades globales de Cromado duro (la clasificación se basa en los ingresos de 2022, actualizados continuamente)

The hard chrome plating industry, often associated with the manufacturing and surface finishing sectors, is influenced by several key drivers:

1. Industrial Growth and Manufacturing Sector: The demand for hard chrome plating is closely tied to the manufacturing industry. As industrial production and manufacturing activities expand, particularly in sectors such as automotive, aerospace, and machinery, the demand for hard chrome plating as a surface treatment for various components and parts increases.

2. Automotive and Transportation: The automotive and transportation industries are major consumers of hard chrome plating, using it for applications such as piston rings, cylinder bores, and various other critical components. As these industries grow, the demand for hard chrome plating rises.

3. Aerospace and Defense Applications: Hard chrome plating is widely used in aerospace and defense applications for its ability to provide corrosion resistance, wear resistance, and dimensional restoration. The expansion of aerospace and defense projects directly influences the demand for hard chrome plating.

4. Machinery and Equipment Manufacturing: Machinery and equipment industries utilize hard chrome plating for hydraulic components, cylinders, molds, and other critical parts. The growth and modernization of these sectors contribute to the demand for hard chrome plating.

5. Renewal and Maintenance: Ongoing maintenance, refurbishment, and renewal activities across various industries drive the demand for hard chrome plating, particularly for repairing and restoring worn-out or corroded parts, thus extending the operational life of components.

6. Corrosion Resistance Requirements: Various industries, including marine, chemical processing, and oil & gas, require components with high corrosion resistance. Hard chrome plating provides an effective solution, making it a critical choice for parts used in harsh environments.

7. Market Innovations in Plating Technologies: Evolving plating technologies, such as advancements in environmentally friendly processes and alternative materials, continually impact the hard chrome plating industry. Innovations that improve efficiency, reduce environmental impact, or offer superior performance can drive market growth.

8. Global Economic Trends: The overall economic health of regions and countries has a direct bearing on the demand for hard chrome plating. Growth in industrial output and manufacturing, coupled with expansion in trade and commerce, impacts the market for hard chrome plating.

These drivers collectively impact the hard chrome plating market, shaping its growth, development, and technological advancement within various industrial sectors.

Sobre QYResearch

QYResearch se fundó en California (EE.UU.) en 2007 y es una empresa líder mundial en consultoría e investigación de mercados. Con más de 17 años de experiencia y un equipo de investigación profesional en varias ciudades del mundo, QY Research se centra en la consultoría de gestión, los servicios de bases de datos y seminarios, la consultoría de OPI, la investigación de la cadena industrial y la investigación personalizada para ayudar a nuestros clientes a proporcionar un modelo de ingresos no lineal y hacer que tengan éxito. Gozamos de reconocimiento mundial por nuestra amplia cartera de servicios, nuestra buena ciudadanía corporativa y nuestro firme compromiso con la sostenibilidad. Hasta ahora, hemos colaborado con más de 60.000 clientes en los cinco continentes. Trabajemos estrechamente con usted y construyamos un futuro audaz y mejor.

QYResearch es una empresa de consultoría a gran escala de renombre mundial. La industria cubre varios segmentos de mercado de la cadena de la industria de alta tecnología, que abarca la cadena de la industria de semiconductores (equipos y piezas de semiconductores, materiales semiconductores, circuitos integrados, fundición, embalaje y pruebas, dispositivos discretos, sensores, dispositivos optoelectrónicos), cadena de la industria fotovoltaica (equipos, células, módulos, soportes de materiales auxiliares, inversores, terminales de centrales eléctricas), nueva cadena de la industria del automóvil de energía (baterías y materiales, piezas de automóviles, baterías, motores, control electrónico, semiconductores de automoción, etc.. ), cadena de la industria de la comunicación (equipos de sistemas de comunicación, equipos terminales, componentes electrónicos, front-end de RF, módulos ópticos, 4G/5G/6G, banda ancha, IoT, economía digital, IA), cadena de la industria de materiales avanzados (materiales metálicos, materiales poliméricos, materiales cerámicos, nanomateriales, etc.), cadena de la industria de fabricación de maquinaria (máquinas herramienta CNC, maquinaria de construcción, maquinaria eléctrica, automatización 3C, robots industriales, láser, control industrial, drones), alimentación, bebidas y productos farmacéuticos, equipos médicos, agricultura, etc.

0 notes

Text

Sine Wave Filters Market Performance and Future Trends Review 2024 - 2031

The sine wave filters market was valued at approximately $2.59 billion in 2023. It is anticipated to grow to $2.76 billion in 2024 and reach $4.5 billion by 2032. This represents a compound annual growth rate (CAGR) of about 6.31% during the forecast period from 2024 to 2032. As demand for efficient power quality solutions increases, the sine wave filters market is expected to experience significant growth in the coming years.

The sine wave filters market has been gaining significant traction in recent years, driven by the increasing demand for cleaner power in various applications. This article provides a comprehensive overview of the sine wave filters market, exploring its definitions, trends, applications, and future outlook.

What Are Sine Wave Filters?

Sine wave filters are electronic devices designed to reduce the harmonic distortion in electrical systems, ensuring that the output waveform closely resembles a pure sine wave. They are essential in various applications, particularly where sensitive equipment is used, as they help improve power quality and efficiency.

Types of Sine Wave Filters

Passive Filters

Constructed using passive components like resistors, inductors, and capacitors.

Typically more cost-effective but may have limitations in performance under varying loads.

Active Filters

Utilize operational amplifiers and other active components to provide superior performance.

Offer better adaptability to load changes and can be more efficient in terms of energy consumption.

Hybrid Filters

Combine elements of both passive and active filters.

Aim to provide the benefits of both types, addressing specific application needs.

Market Dynamics

Drivers

Growing Demand for Renewable Energy Sources

As renewable energy sources like solar and wind become more prevalent, the need for sine wave filters to manage power quality increases.

Industrial Automation

The rise of Industry 4.0 and automation technologies necessitates high-quality power for efficient operation.

Electrification of Transportation

The shift toward electric vehicles (EVs) has created a surge in demand for power quality management solutions, including sine wave filters.

Restraints

High Initial Costs

The investment required for high-quality sine wave filters can be a barrier for some industries.

Technological Complexity

The design and implementation of advanced filtering systems can be complex, requiring specialized knowledge.

Opportunities

Emerging Markets

Developing economies are rapidly industrializing, leading to increased investments in power quality solutions.

Technological Advancements

Continuous innovation in filter technology can enhance efficiency and reduce costs, expanding market reach.

Key Applications of Sine Wave Filters

Industrial Applications

Sine wave filters are widely used in industrial settings, particularly in:

Motor Drives

Robotics

Manufacturing Equipment

Commercial Applications

In commercial environments, sine wave filters help ensure:

HVAC Systems

Lighting Solutions

IT Infrastructure

Residential Applications

As more households adopt smart technology and renewable energy solutions, sine wave filters are becoming crucial in:

Solar Power Systems

Home Automation

Geographic Overview

North America

The North American market is driven by the increasing adoption of advanced power quality solutions across various sectors. Strong regulatory frameworks also support the integration of renewable energy sources.

Europe

Europe has witnessed a significant push toward sustainable energy practices, creating a favorable environment for sine wave filter adoption. Countries like Germany and France lead the charge.

Asia-Pacific

The Asia-Pacific region is expected to experience the fastest growth due to rapid industrialization, urbanization, and an increase in electricity consumption. Countries like China and India are key players in this market.

Future Outlook

The sine wave filters market is poised for significant growth in the coming years. As industries continue to focus on improving energy efficiency and adopting cleaner technologies, the demand for high-quality power solutions will rise. Innovations in filter design and technology will further enhance market prospects.

Conclusion

In summary, the sine wave filters market is influenced by various factors, including the increasing need for power quality management in industrial, commercial, and residential applications. With ongoing technological advancements and growing awareness of the importance of clean energy, the market is expected to thrive in the foreseeable future. Businesses looking to invest in sine wave filters should consider the diverse applications and benefits they offer to enhance operational efficiency and sustainability.

0 notes

Text

29th August 2024

Discover how smart factories are revolutionizing manufacturing in Malaysia. Learn about the benefits, technologies, and challenges of Industry 4.0.

Malaysia has been actively embracing technological advancements to bolster its manufacturing sector. One of the most prominent trends is the emergence of smart factories, a key component of Industry 4.0. This revolution involves the integration of digital technologies to enhance efficiency, productivity, and competitiveness. In this article, we will delve into the concept of smart factories, their benefits, and the progress made in Malaysia.

Understanding Smart Factories

Smart factories are manufacturing facilities that leverage advanced technologies to optimize operations. They employ interconnected devices, sensors, and data analytics to create a highly automated and intelligent environment. Key technologies powering smart factories include:

Internet of Things (IoT): Connecting machines, devices, and systems to enable real-time data exchange and control.

Artificial Intelligence (AI): Utilizing AI algorithms for predictive maintenance, quality control, and decision-making.

Robotics: Deploying robots for tasks such as assembly, packaging, and material handling.

Big Data Analytics: Analyzing large datasets to identify trends, optimize processes, and improve efficiency.

Benefits of Smart Factories

The adoption of smart factories brings numerous advantages to Malaysian manufacturers:

Increased Efficiency: Automation and optimization lead to reduced downtime, improved productivity, and faster turnaround times.

Enhanced Quality: Real-time monitoring and data analysis enable better quality control and defect prevention.

Cost Reduction: Streamlined operations, energy efficiency, and reduced waste contribute to lower operating costs.

Flexibility: Smart factories can adapt to changing market demands and product variations more easily.

Innovation: The integration of new technologies fosters a culture of innovation and continuous improvement.

Progress of Smart Factories in Malaysia