#Integrated Passive Devices Market Development

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

The average Tumblr user visits about 67 pages every month.

Text

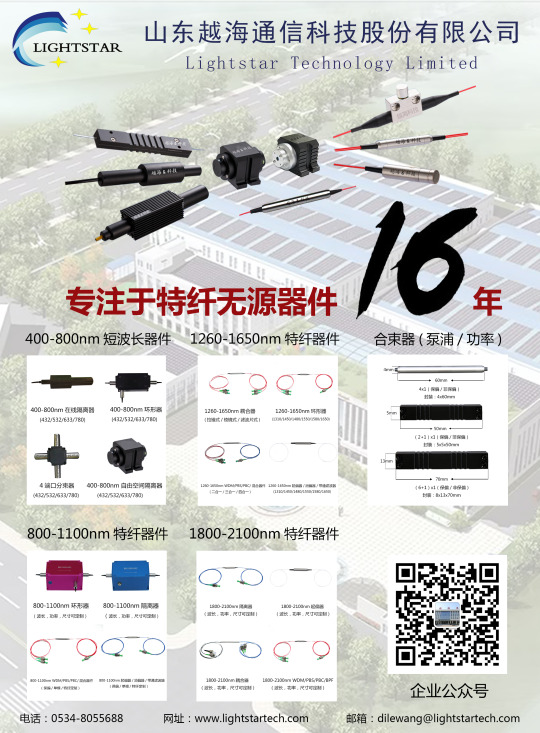

My name is Tina and from the Lightstar Compamy.

It's a pleasure to meet you and to introduce my company to you. Our company was founded in 2014, mainly engaged in the research and development, production and marketing of optical passive devices. The company has its own doctoral and master's research and development teams, focusing on the production of mini miniaturization, functional integration, high reliability and bias maintaining devices, with the design advantages of high-power products. Products are widely used in laser, sensing, lidar and autonomous driving fields.

Products include optical isolator, WDM, coupler, high power Circulator, polarizer, optical switch, bandpass filter and so on.

The product supports wavelength and power customization. For further information:

Please add my E-mail :[email protected] or log in to the company website :www.lightstartech.com.

2 notes

·

View notes

Text

Mastering Microlearning Games: An In-Depth Look at MaxLearn's DDE Framework

Maximize Impact: How MaxLearn's DDE Framework is Revolutionizing Microlearning Game Design for U.S. Industries

In today's fast-paced U.S. corporate landscape, traditional long-form training is increasingly ineffective. Businesses across vital sectors like Insurance, Finance, Retail, Banking, Mining, Healthcare, Oil & Gas, and Pharmaceuticals are grappling with declining engagement, knowledge retention, and the need for agile, scalable learning solutions. The answer? Microlearning, supercharged by strategic game design.

At MaxLearn, we're leading this transformation with our proprietary DDE Framework for Game Design in Microlearning. More than just gamification, DDE offers a structured, holistic approach to creating impactful, memorable, and measurable learning experiences.

Understanding the DDE Framework: Design, Dynamics, Experience (or Engage)

The DDE Framework stands on three foundational pillars, ensuring that every microlearning game we develop is not just fun, but profoundly effective:

Design: The Blueprint for Learning SuccessThis initial phase is about meticulous planning. We define clear learning objectives, identify key competencies, and map out the game's core mechanics, rules, and narrative. It’s here that the game's structure is aligned precisely with the desired learning outcomes. For instance, designing a scenario-based game for pharmaceutical sales training requires careful consideration of sales objections and product knowledge integration.

Dynamics: Driving Engagement and InteractionThe Dynamics phase focuses on the ongoing interactions within the game that keep learners motivated and invested. This includes implementing feedback loops, progression systems (like points, levels, and badges), social elements (leaderboards, team challenges), and adaptive difficulties that respond to learner performance. Think of how dynamic quizzes can enhance GMP training for the pharmaceutical industry by immediately correcting misconceptions.

Experience (or Engage): Ensuring Retention and Real-World ApplicationThe final, crucial element of DDE is the learner's overall experience and their sustained engagement. This phase ensures the learning journey is enjoyable, meaningful, and directly contributes to long-term knowledge retention and practical skill application. It's about creating intrinsic motivation, leveraging storytelling, and ensuring seamless accessibility across devices, whether for oil and gas certification online or online medical billing and coding training.

Why DDE for Microlearning Game Design in the U.S. Market?

The benefits of applying the DDE framework to microlearning game design are profound, particularly for U.S. businesses facing unique training challenges:

Enhanced Engagement & Retention: Gamified microlearning tackles shrinking attention spans head-on, turning passive learning into an active, enjoyable pursuit. This significantly boosts knowledge recall and application.

Agility & Scalability: Rapid content development and easy updates mean your training stays current with evolving industry standards, whether it's new regulations in healthcare administration training or updated safety protocols in mining safety certification.

Measurable ROI: The DDE framework allows for clear tracking of learner progress and performance, providing concrete data on the effectiveness of your training investments.

Accessibility: Microlearning games are designed for mobile-first consumption, enabling employees to learn anytime, anywhere – crucial for distributed workforces or those in the field, like pharma sales rep training or training for oil and gas.

MaxLearn's DDE in Action: Tailored Solutions for Key Industries

MaxLearn leverages the DDE framework to create bespoke microlearning game solutions that address the specific training needs of diverse U.S. industries:

Pharmaceuticals: From pharmaceutical sales training to ensuring compliance with GMP training for the pharmaceutical industry, our DDE-powered games make complex regulations and product knowledge digestible and memorable. This extends to comprehensive pharmaceutical training and rapid onboarding for pharma rep training.

Oil & Gas: Safety is paramount. Our DDE approach delivers crucial training for oil and gas employees, including modules for oil and gas certification and oil and gas classes. Online options like oil and gas certification online ensure broad accessibility for certifications in this demanding industry.

Healthcare: Navigating complex procedures and compliance is simplified. We develop engaging modules for online medical billing and coding training, essential home health aide training (including home health aide training online), and broader healthcare administration training and healthcare academy training.

Mining: Safety and operational efficiency are critical. MaxLearn's DDE framework creates impactful training for mining, covering topics like surface mining certification, mining safety certification, and coal mining certification. We specialize in MSHA certification, including MSHA Part 46, MSHA certification online, MSHA trainer certification, and MSHA mining certification.

Banking & Finance: Staying compliant and competitive requires continuous learning. Our solutions support American Bankers Association training and courses, investment banking prep courses, corporate banking courses, and specialized mortgage loan processing training. We also enhance foundational knowledge with online finance courses, financial modeling courses, financial analyst courses, financial management courses, financial accounting courses, and certified financial planner courses.

Retail: Empowering sales teams and improving customer service is key. MaxLearn offers dynamic training for retail, retail store training, retail management courses (including retail management courses online), retail sales training, retail management training, training for retail employees, retail staff training, and specialized content for retail store manager training and retail store staff training.

Insurance: Compliance, product knowledge, and sales skills are constantly evolving. Our DDE games provide effective insurance adjuster training, insurance agent training, insurance claims adjuster training, and even solutions for specialized needs like personal training insurance and liability insurance for personal trainers.

The MaxLearn Advantage

In the competitive U.S. market, MaxLearn stands out by not just offering microlearning, but by integrating a deeply researched DDE framework that transforms it into a powerful, game-based learning engine. We understand the specific nuances and regulatory landscapes of various U.S. industries, allowing us to create highly relevant and impactful training solutions that drive real business outcomes.

Ready to revolutionize your corporate training and achieve unparalleled learning success? Discover how MaxLearn's DDE Framework can empower your workforce in the USA.

Contact MaxLearn today for a personalized demonstration!

#ddeframework#ddegame#mdaframework#mdagamedesign#gamedesignmda#frameworkmda#dderival#mdaframeworkgamedesign#mdamodelgamedesign#gamedesignframework#mdagames#mdaingamedesign#mdagame#gamemda#mdaframeworkgamification#whoisdde#gamedesignframeworks#ddestandsfor#mechanicsdynamicsaesthetics#mdagaming#ddemeans#mdaframeworkexample#mdamodel#ddemeaning#mdastructure#ddestructure#diegeticsystem#mdadynamics#blueprintgamedesign#mdagamedesignframework

0 notes

Text

ETHRANSACTION Introduces Scalable Cloud Mining Model for Everyday Crypto Enthusiasts

LONDON, UK – As Bitcoin surpasses the $110,000 mark and the global cryptocurrency market reaches new milestones, ETHRANSACTION is making digital asset participation more inclusive with its fully automated, AI-driven cloud mining platform. Designed for ease, security, and global accessibility, ETHRANSACTION is changing the way people approach crypto income, without hardware, trading stress, or technical know-how.

Founded with the mission of making mining accessible to all users, ETHRANSACTION operates as a cloud-based AI mining pool and data center. With over 63% of the crypto market dominated by Bitcoin alone, ETHRANSACTION enables everyday users to participate in mining leading assets like BTC, LTC, and DOGE—all with just a few clicks from a smartphone or browser.

Why ETHRANSACTION Resonates with Global Users

What makes ETHRANSACTION stand out in a crowded field is its combination of simplicity, automation, and transparency:

No Hardware Required: Users do not need to purchase or manage any mining equipment.

One-Click Setup: Easy onboarding from any device—ideal for users of all skill levels.

Round-the-Clock Mining: AI optimises performance and selects the most efficient cryptocurrencies to mine in real time.

Real-Time Monitoring: Users can track mining output and platform performance via intuitive dashboards.

Global Reach: Open to users across all regions, designed to scale with increasing adoption.

“We believe crypto mining should be inclusive, effortless, and sustainable,” said a company spokesperson. “Our AI-backed infrastructure and clean user experience are built to support both beginners and experienced crypto users looking for a steady, low-friction alternative to trading.”

Commitment to Security and Reliability

ETHRANSACTION emphasises safety as a core part of its user experience. All user data is secured with SSL encryption, and the platform maintains a long-standing partnership with Legal & General Insurance Company to provide additional reliability through insurance-backed support.

The platform also allows users to monitor plan performance and data integrity in real time, supporting full transparency in all operations.

Built for Flexibility and Everyday Use

Unlike traditional mining operations or speculative trading platforms, ETHRANSACTION is built to fit into everyday life. Its cloud-first, mobile-compatible approach allows users to activate cloud mining and track progress in just minutes—no complex installations or energy bills involved.

ETHRANSACTION continues to develop user-centric features, including

Seamless mobile integration

Scalable participation models

Multilingual support for global accessibility Enhanced educational tools for new users

About ETHRANSACTION

ETHRANSACTION is a global cloud mining platform combining artificial intelligence, automation, and accessibility to provide a secure and intuitive way to mine popular cryptocurrencies. Based on a commitment to transparency and scalability, ETHRANSACTION aims to empower users with low-barrier entry to passive crypto participation, without the volatility or complexities of traditional crypto investments.

To learn more, visit: https://ethransaction.vip

Media ContactName: Georgina Godfrey Email: [email protected] Website: https://ethransaction.vip Location: London, United Kingdom

More info: https://chainwirenow.com/ethransaction-introduces-scalable-cloud-mining-model-for-everyday-crypto-enthusiasts/

0 notes

Text

[IOTE2025 Shenzhen Exhibitor] Exhibitor Introduction Collection

With the rapid development of artificial intelligence (AI) and Internet of Things (IoT) technologies, their integration is becoming increasingly close and is profoundly influencing technological innovation across various industries. AGIC + IOTE 2025, the 24th International Internet of Things Exhibition — Shenzhen Station, will take place from August 27 to 29, 2025, at the Shenzhen World Exhibition & Convention Center. IOTE 2025 is set to be an unprecedented professional exhibition event in the field of AI and IoT. The exhibition scale will expand to 80,000 square meters, focusing on the cutting-edge progress and practical applications of “AI + IoT” technology. It will also feature in-depth discussions on how these technologies will reshape our future world. It is expected that over 1,000 industry pioneers will participate to showcase their innovative achievements in areas such as smart city construction, Industry 4.0, smart home life, smart logistics systems, smart devices, and digital ecosystem solutions.

Many high-quality companies will appear in this exhibition as exhibitors. We welcome all industry friends to visit, learn and communicate, and participate in the industry event.

This article will introduce the following exhibitors:

1.Shenzhen Xinda Meng Technology Co.,Ltd

2.AXGOOD

3.GUANGZHOU CHI LI AUTOMATION EQUIPMENT CO., LTD.

4.SHENZHEN GARZOON ELECTRONICS CO.,LTD

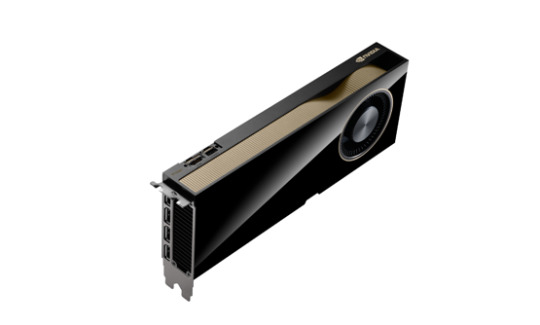

Shenzhen Xinda Meng Technology Co.,Ltd

Booth number: 12D29

August 27–29, 2025

Shenzhen World Convention and Exhibition Center (Bao’an New Hall)

Company Profile

Shenzhen Xinda Meng Technology Co., Ltd. takes “extreme performance, excellent service” as its business philosophy, is committed to the introduction and application of high-end graphics card products and technologies, and focuses on professional fields such as industrial design, image processing, GPU high-performance computing, virtualization technology, deep learning and overall solutions.

As an elite partner of NVIDIA professional visualization GPU products, we continue to enrich and expand our product line to meet the diverse needs of different consumers. With rich experience accumulated in the graphics card industry, Xinda Meng Technology provides users with high-quality products and solutions to help customers achieve comprehensive performance improvements in various fields.

Product Recommendation

AXGOOD

Booth number: 9D6

August 27–29, 2025

Shenzhen World Convention and Exhibition Center (Bao’an New Hall)

Company Profile

AXGOOD is committed to the research and development and production of smart IoT products. After years of development, it has accumulated a variety of IoT solutions and has occupied a place in the industry. The company’s technical R&D team includes software, hardware, and structural design, which can provide customers with one-to-one team services, tailor-made, and maximize the characteristics of the enterprise to meet the needs of enterprise development and publicity. Since the establishment of the company, the customer industry has covered multiple fields such as communications, towers, railways, electricity, and transportation. We adhere to the service core of professionalism, integrity, and aggressiveness, aiming to connect all business opportunities for enterprises through our unremitting efforts, help customers maintain their advantages in the Internet era and environment, and go with customers through thick and thin, grow together, share joy, and be the leader in technology marketing.

The company’s products include: NB-IOT smart manhole cover | NB-IOT padlock | optical exchange box smart lock | passive electronic lock | tower base station access control electric lock | integrated cabinet lock | IC card swipe electric lock | NFC smart lock and other products.

The Bluetooth key management box is a key management terminal product that supports USB/BLE4.0 Bluetooth communication and authorization.

The main body of the product is made of cold-rolled steel plate sprayed with plastic, and the window is made of tempered glass. The overall silver-gray tone is calm and generous. It contains Bluetooth communication and USB line communication. After connection, it can automatically upload the key internal records, authorize the latest permissions, and internal clock and other functions.

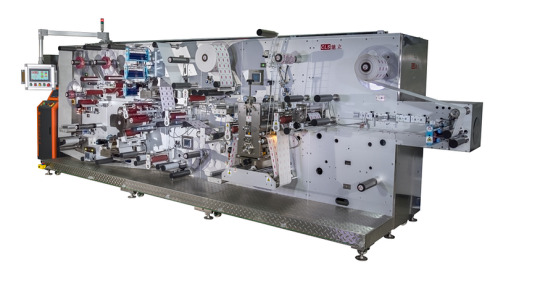

GUANGZHOU CHI LI AUTOMATION EQUIPMENT CO., LTD.

Booth number: 9D40

August 27–29, 2025

Shenzhen World Convention and Exhibition Center (Bao’an New Hall)

Company Profile

GUANGZHOU CHI LI AUTOMATION EQUIPMENT CO., LTD. is a high-tech enterprise located in Guangzhou Huangpu Technology Headquarters Port, focusing on the development and production of industrial RFID label automatic compounding equipment, RFID label high-speed UV printing, coding, testing equipment and automatic labeling equipment;

Chi Li’s equipment is widely used in many large, medium and small professional RFID label production companies, with a high market share and has won unanimous praise from customers.

Chi Li’s core team and technical force are the elites and pioneers in the domestic automation production equipment industry, and have been committed to the research and development, production and innovation of RFID label production equipment.

Chi Li’s products are based on the domestic market, and are also exported to American countries such as the United States and Mexico; European and American countries such as Spain, Portugal, the United Kingdom, Germany, Turkey, Morocco, and Southeast Asian countries such as Vietnam, Bangladesh, India, Indonesia, Cambodia, and Myanmar.

Product: Label automatic laminating machine

Product: High-speed roll-to-roll label UV printing, coding, and testing equipment

Product: High-speed hang tag UV printing, coding, and testing equipment

Model: CL-526IE

SHENZHEN GARZOON ELECTRONICS CO.,LTD

Booth number: 11A51–2

August 27–29, 2025

Shenzhen World Convention and Exhibition Center (Bao’an New Hall)

Company Profile

SHENZHEN GARZOON ELECTRONICS CO.,LTD, founded in 2012, is a national high-tech enterprise integrating R&D, design, production and sales, and is also a leading supplier of touch display products and application solutions in China. The company focuses on the differentiated and personalized customized development of customer products, covering the R&D, design and production supply of touch screens and LCD screens. The products are mainly used in intelligent hardware products such as security industrial control, smart medical care, smart home, smart Internet of Things and human-computer interaction. As a leading manufacturer of touch technology, Garzoon can provide customers with a full range of touch technology application solutions, including product design, R&D to mass production.

LCD display products are mainly small and medium-sized products, targeting attendance access control, robots, smart hardware, smart small appliances and other product applications. At the same time, there are multiple options for special product applications such as high brightness, wide temperature and high resolution. In the field of touch display products, the company can produce and ship in a variety of combinations in line with the actual needs of customers, such as: cover plate + LCD screen + full lamination, touch screen + LCD screen + full lamination, cover plate + incell screen + full lamination, or single touch screen or single LCD screen production and shipment.

At present, industry trends are changing rapidly, and it is crucial to seize opportunities and seek cooperation. Here, we sincerely invite you to participate in the IOTE 2025, the 24th International Internet of Things Exhibition, Shenzhen Station, held at the Shenzhen World Convention and Exhibition Center (Bao’an New Hall) from August 27 to 29, 2025. At that time, you are welcome to discuss the cutting-edge trends and development directions of the industry with us, explore cooperation opportunities, and look forward to your visit!

0 notes

Text

Fibre Optic Combiner Market: Market Segmentation and Regional Insights 2025–2032

Fibre Optic Combiner Market, Trends, Business Strategies 2025-2032

Fibre Optic Combiner Market was valued at 1730 million in 2024 and is projected to reach US$ 3189 million by 2032, at a CAGR of 9.4% during the forecast period.

Our comprehensive Market report is ready with the latest trends, growth opportunities, and strategic analysis https://semiconductorinsight.com/download-sample-report/?product_id=103478

MARKET INSIGHTS

The global Fibre Optic Combiner Market was valued at 1730 million in 2024 and is projected to reach US$ 3189 million by 2032, at a CAGR of 9.4% during the forecast period.

Fibre optic combiners are specialized passive devices that merge multiple optical signals into a single output fibre while minimizing insertion loss. These components leverage fused biconical taper (FBT) technology or micro-optics to achieve efficient signal combination. Key product types include power combiners for high-power laser applications and pump combiners essential for optical amplifier systems.

The market growth is driven by increasing bandwidth demands in telecom networks and rapid adoption in data center interconnects. Furthermore, advancements in wavelength division multiplexing (WDM) technologies and growing investments in 5G infrastructure are accelerating deployment. Key players like Thorlabs and Newport Corporation are expanding their portfolios through strategic partnerships, with the Asia-Pacific region emerging as the fastest-growing market due to intensive fibre network rollouts.

List of Key Fibre Optic Combiner Companies Profiled

Newport Corporation (U.S.)

Thorlabs, Inc. (U.S.)

IDIL Fibres Optiques (France)

MilesTek Corporation (U.S.)

Electro Optical Components, Inc. (U.S.)

Advantech (Taiwan)

L-com, Inc. (U.S.)

S.I. Tech, Inc. (U.S.)

Corning Optical Communications (U.S.)

M2 Optics, Inc. (U.S.)

OFS (U.S.)

Segment Analysis:

By Type

Power Combiners Lead the Market Due to Growing Demand in High-Power Fiber Laser Systems

The global fibre optic combiner market is segmented based on type into:

Power Combiners

Subtypes: (2+1)x1, (6+1)x1, and others

Pump Combiners

Wavelength Division Multiplexers (WDM)

Polarization Maintaining Combiners

Others

By Application

Telecommunications Segment Dominates with Increasing Fiber Optic Network Deployments

The market is segmented based on application into:

Telecommunications

Data Centers

Medical Equipment

Military & Aerospace

Industrial Applications

By End-User Industry

IT & Telecom Sector Accounts for Major Share Due to 5G Infrastructure Development

The market is segmented based on end-user industry into:

IT & Telecommunications

Healthcare

Defense & Aerospace

Energy & Utilities

Others

Regional Analysis: Fibre Optic Combiner Market

North America The North American fibre optic combiner market is driven by rapid advancements in 5G infrastructure and robust investments in telecommunications upgrades. The U.S. leads the region with initiatives such as the $42.5 billion Broadband Equity, Access, and Deployment (BEAD) Program, accelerating demand for high-efficiency optical combiners in data centers and WDM systems. Canada follows closely, focusing on rural broadband expansion, while Mexico shows steady growth due to increasing private-sector telecom investments. Strict regulatory standards for network reliability and performance further push innovation in combiner technology, particularly in minimizing insertion loss and improving signal integrity.

Europe Europe’s market thrives on stringent data privacy laws and the region’s push for fiber-to-the-home (FTTH) deployment, with the EU targeting 100% high-speed broadband coverage by 2030. Germany and France dominate, leveraging their industrial automation sectors to adopt fibre optic combiners for precision applications like medical lasers and aerospace testing. The UK’s emphasis on smart cities and Italy’s growing data center footprint contribute to demand. However, high costs of raw materials and labor pose challenges, nudging manufacturers toward localized production to mitigate supply chain risks.

Asia-Pacific Asia-Pacific, accounting for over 40% of global fibre optic combiner demand, benefits from China’s “Digital Silk Road” initiative and India’s BharatNet project, which aim to connect millions via optical networks. Japan and South Korea lead in R&D for compact, high-power combiners used in semiconductor manufacturing and autonomous vehicles. Southeast Asian nations like Vietnam and Indonesia are emerging hotspots due to expanding submarine cable projects. The region’s cost-competitive manufacturing ecosystem, however, faces pressures from fluctuating silica prices and trade tensions impacting component supplies.

South America South America’s market grows moderately, driven by Brazil’s oil & gas sector deploying combiners for offshore pipeline monitoring and Argentina’s renewable energy projects requiring precise optical sensing. Economic instability and currency volatility hinder large-scale infrastructure spending, though Chile’s data localization laws are spurring localized data center builds. The lack of domestic combiner production forces reliance on imports, creating opportunities for suppliers offering financing solutions to cash-strapped telecom operators.

Middle East & Africa The Middle East’s fibre optic combiner market expands with smart city projects like Saudi Arabia’s NEOM and UAE’s 5G rollouts, prioritizing low-latency network components. Africa’s growth is uneven—South Africa and Nigeria lead in backbone network deployments, while East African nations adopt combiners for mobile money infrastructure. Geopolitical risks and underdeveloped last-mile connectivity slow adoption, but undersea cable investments (e.g., 2Africa Cable) signal long-term potential for optical component demand.

MARKET DYNAMICS

The market faces significant technical hurdles in developing combiners capable of handling high-power laser inputs common in industrial and defense applications. Thermal management becomes problematic as power levels exceed 100W, with potential for nonlinear optical effects that degrade signal quality. This limitation restricts the use of conventional combiners in critical applications such as laser material processing and directed energy systems, where power handling capabilities above 500W are increasingly required.

Material science limitations further complicate product development, as standard fused fiber technologies struggle to maintain beam quality at extreme power densities. While emerging solutions using specialty fibers show promise, their commercial viability remains constrained by prohibitively high production costs and limited manufacturing scalability.

These technical barriers are particularly significant given the growing demand for high-power fiber combiners in emerging sectors such as laser weapon systems and advanced manufacturing, where performance reliability cannot be compromised.

The development of space division multiplexing (SDM) technologies presents significant opportunities for advanced fibre optic combiner systems. As traditional WDM approaches approach theoretical capacity limits, network operators are increasingly exploring multi-core and few-mode fiber solutions that could multiply capacity by an order of magnitude. This technological shift requires innovative combiner architectures capable of managing multiple spatial channels while maintaining low crosstalk and insertion loss.

Early SDM prototypes have demonstrated the potential to increase fiber capacity by 10-100 times, creating substantial demand for next-generation combining solutions. Manufacturers investing in SDM-compatible combiner technologies now stand to gain first-mover advantages in what could become a multi-billion dollar market segment within the next decade. The transition to SDM is particularly relevant for submarine cable systems and metropolitan area networks where fiber real estate is constrained.

Additionally, the growing adoption of fiber lasers in industrial and medical applications is driving demand for specialized pump combiners with enhanced power handling capabilities, opening new revenue streams for manufacturers able to address these niche requirements.

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies https://semiconductorinsight.com/download-sample-report/?product_id=103478

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Fibre Optic Combiner Market?

Which key companies operate in Global Fibre Optic Combiner Market?

What are the key growth drivers?

Which region dominates the market?

What are the emerging trends?

Related Reports:

https://semiconductorblogs21.blogspot.com/2025/07/global-market-for-gas-scrubbers-for_9.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/through-hole-slip-rings-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/semiconductor-test-consumables-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/antibacterial-medical-grade-computer.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/wireless-power-controller-ics-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/multi-purpose-diodes-for-esd-protection.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/ceramic-heating-components-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/dc-linear-voltage-regulators-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/led-dimming-interface-ics-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/enhancement-mode-gan-transistor-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/automatic-lighting-control-sensors.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/single-sided-copper-clad-laminate.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/glucose-ketone-meter-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/programmable-timers-and-oscillators.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/smart-plug-for-personal-use-market-size.htmlhttps://semiconductorblogs21.blogspot.com/2025/07/battery-reliability-test-system-market.html

CONTACT US: City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014 [+91 8087992013] [email protected]

0 notes

Text

North America Aromatherapy Diffuser Market to Reach USD 964.72 Million by 2030, Driven by Wellness and Smart Home Trends

The North America aromatherapy diffuser market Size is set to grow from USD 745.89 million in 2025 to USD 964.72 million by 2030, reflecting a CAGR of 5.28%. Growth is fueled by technological advancements, rising health awareness, and evolving consumer preferences for home wellness solutions that blend function with aesthetics.

Get More Insights: https://www.mordorintelligence.com/industry-reports/north-america-aromatherapy-diffuser-market

Key North America Aromatherapy Diffuser Market Trends

Smart Technology Drives Market Evolution

Manufacturers are integrating smart home and IoT capabilities into aromatherapy diffusers, enabling features such as remote control, scheduling, and intensity adjustments via smartphone applications. Recent product launches such as Air Wick’s Essential Mist Smart Diffuser and Organic Aromas’ Mobile-Mini Wireless Nebulizing Diffuser demonstrate the market's shift toward connected living. Consumers are increasingly seeking devices that align with broader home automation systems, reflecting growing demand for convenience and personalized wellness experiences.

Premium Segment Expands with Multifunctional Designs

The market is witnessing a move towards premium, multifunctional diffusers that cater to sophisticated consumer tastes. Companies like Airzai have introduced luxury fragrance diffusers combining European perfumes with intelligent diffusion technology. This trend aligns with the rising popularity of wellness as a lifestyle choice, supported by the USD 18.1 billion US spa industry revenue in 2021 reported by ISPA. Manufacturers are developing products with enhanced features such as humidity control, ambient lighting, and multiple diffusion modes to meet consumer expectations for premium wellness experiences at home and in commercial spaces.

Portable and Compact Diffusers Gain Traction

With 80% of U.S. workers reporting job-related stress��(American Institute of Stress), consumers are seeking wellness solutions for diverse environments. Manufacturers have responded with portable, USB-powered, and car diffusers such as AERON Lifestyle Technology’s FlashScent USB aromatherapy diffuser, catering to office, travel, and vehicle use. This reflects a broader trend of integrating aromatherapy into daily routines for stress management and mental wellness.

Sustainability and Aesthetics Influence Purchase Decisions

Consumers are increasingly opting for diffusers that combine eco-friendly materials with aesthetic appeal to complement modern interior décor. Products like Twystr Technologies’ TORNADO diffuser exemplify this trend, blending artistic design with functionality. This reflects rising environmental awareness and consumer preference for sustainable, stylish wellness products that also serve as home décor accents.

North America Aromatherapy Diffuser Market Segmentation

By Product Type

Ultrasonic Diffusers Lead the Marke: Ultrasonic diffusers accounted for approximately 79% of market share in 2024, driven by their cost-effectiveness, low power consumption, and ease of maintenance. They remain popular among consumers for daily home use due to their silent operation and ability to humidify indoor air while diffusing essential oils effectively.

Nebulizing Diffusers Show Strong Growth: The nebulizer segment is projected to grow at 9% CAGR from 2024 to 2029. Nebulizing diffusers are favored for maintaining the therapeutic integrity of essential oils without using heat or water. Their superior diffusion capabilities make them ideal for large spaces, spas, wellness centers, and professional therapeutic environments.

Other Types Cater to Niche Preferences: Ceramic, reed, electric, and candle diffusers maintain relevance for consumers preferring cordless or passive diffusion options. These products serve decorative and supplemental roles, appealing to consumers seeking aesthetic simplicity or traditional aromatherapy experiences.

By Distribution Channel

Specialty Stores Remain Dominant: Specialty stores held 42% of market share in 2024, driven by consumers’ preference for physical product evaluation and expert guidance. These stores provide personalized consultations and reliable authenticity, especially for premium and therapeutic-grade diffusers.

Online Retail Expanding Rapidly: Online retail is projected to grow at 11% CAGR from 2024 to 2029. E-commerce platforms offer 24/7 access, competitive pricing, and detailed product information, appealing to tech-savvy consumers seeking convenience. Brands are enhancing their digital presence through virtual demos, augmented reality features, and influencer marketing to boost engagement and sales.

Other Channels Maintain Market Presence: Supermarkets, hypermarkets, and convenience stores continue to serve essential roles, providing immediate product availability and attractive promotions. Direct selling and warehouse clubs cater to consumers seeking specialized or bulk purchases, enhancing overall market accessibility.

North America Aromatherapy Diffuser Market Regional Outlook

United States Dominates Regional Market

The United States commands approximately 74% of North America’s aromatherapy diffuser market share. Growing awareness about the therapeutic benefits of essential oils has fueled demand for ultrasonic and nebulizing diffusers, particularly among wellness practitioners and home users. The market is characterized by strong retail networks, advanced product offerings, and consumer education initiatives that integrate diffusers into daily health routines.

Mexico Emerges as a High-Growth Market

Mexico is projected to grow at 9% CAGR from 2024 to 2029, driven by rising stress-related health concerns and increasing consumer appreciation for native aromatic plants like lemongrass and sandalwood. Diffusers with unique designs and handcrafted aesthetics are particularly popular as gift items. Local brands are focusing on competitive pricing and expanding distribution networks to improve market penetration.

Canada Shows Steady Demand Growth

Canada’s market growth is supported by consumer interest in meditation, massage therapy, and holistic health. Heat-free ultrasonic diffusers are favored for safety and ease of use. E-commerce is expanding rapidly in Canada, driven by high internet penetration and the growing preference for convenient, contactless purchasing options.

Other North American Countries Experience Rising Awareness

Markets in countries such as Costa Rica, Panama, and the Dominican Republic are witnessing increasing demand for aromatherapy diffusers as consumers prioritize stress relief, better sleep, and mental wellness. The rising middle class and expanding retail networks support further market growth across these regions.

Get More Insights: https://www.mordorintelligence.com/ja/industry-reports/north-america-aromatherapy-diffuser-market

North America Aromatherapy Diffuser Market Competitive Landscape

The North America aromatherapy diffuser market is highly fragmented, featuring global brands and specialized local players. Key market leaders include:

doTERRA

Organic Aromas

Newell Brands

Edens Garden

Young Living Essential Oils

These companies focus on product innovation, smart technology integration, and premium designs to maintain market leadership. Strategies include expanding direct-to-consumer channels, launching IoT-enabled diffusers, and enhancing online retail partnerships. Mergers and acquisitions are common as larger players acquire niche brands to broaden portfolios and strengthen technological capabilities.

North America Aromatherapy Diffuser Market Conclusion

The North America aromatherapy diffuser market is poised for continued growth, driven by smart technology adoption, premium wellness trends, and consumer lifestyle shifts toward holistic health and sustainability. Companies that prioritize innovation, aesthetic design, and eco-friendly practices will be best positioned to capture emerging opportunities in this evolving market landscape.

0 notes

Text

Heat Sinks Market Trends, Forecast, and Growth Outlook | EMR

According to Expert Market Research, the global heat sinks market reached a value of USD 7.37 billion in 2024. With increasing demand for electronic components and growing concerns about heat dissipation in high-performance systems, the market is expected to experience significant growth. It is projected to grow at a CAGR of 6.50% from 2025 to 2034, reaching a market value of USD 13.83 billion by 2034.

Overview of the Heat Sinks Market

Heat sinks play a critical role in the thermal management of electronic devices, helping to prevent overheating and prolong device lifespan. As technology advances and electronics become more compact and powerful, the need for efficient cooling systems like heat sinks has grown rapidly. These components are extensively used in consumer electronics, automotive electronics, industrial machinery, LEDs, and telecommunications equipment.

The rising adoption of smart devices, AI systems, and electric vehicles (EVs) is fueling the demand for high-performance heat sinks across sectors.

Key Drivers of Market Growth

1. Rise in Consumer Electronics and IoT Devices

The surge in global demand for smartphones, tablets, laptops, and wearables has significantly increased the need for thermal management solutions. Miniaturization of electronic devices means that internal components generate more heat within smaller spaces, necessitating advanced heat sink technologies.

2. Growth in Automotive and EV Industry

With electric and hybrid vehicles gaining traction worldwide, the heat sinks market is expanding in the automotive sector. These vehicles require efficient cooling systems to manage battery temperature, electric motors, and inverters. Additionally, autonomous and connected vehicles also use numerous processors and sensors, further increasing the demand.

3. Expansion of Data Centers and Cloud Computing

The booming cloud computing industry and massive data centers require large-scale thermal management to ensure servers operate efficiently without performance drops due to overheating. As a result, high-performance heat sinks are integral to data center infrastructure.

4. LED Lighting Applications

The transition from traditional lighting to energy-efficient LED solutions has created another growth channel for the heat sinks industry. LEDs require heat sinks to maintain luminous efficiency and long operational life.

Regional Insights

North America

North America is a leading market due to the strong presence of electronics and semiconductor manufacturers. The region’s fast adoption of AI, EVs, and 5G also contributes to the demand for heat sink solutions.

Asia-Pacific

Asia-Pacific is expected to register the fastest growth, driven by manufacturing hubs in China, Japan, South Korea, and India. Increasing production of consumer electronics, coupled with government support for EV infrastructure and industrial automation, is accelerating market growth.

Europe

Europe's market is supported by its robust automotive industry and focus on energy-efficient technologies. Sustainability initiatives and electric mobility policies in countries like Germany, France, and the Netherlands further boost demand.

Market Segmentation

The global heat sinks market can be segmented based on:

Type: Active Heat Sinks, Passive Heat Sinks, Hybrid Heat Sinks

Material: Aluminum, Copper, Others

End-Use Industry: Consumer Electronics, Automotive, Industrial, Telecommunication, Others

Passive heat sinks dominate the market due to their simplicity, reliability, and cost-effectiveness. However, active and hybrid variants are witnessing increased adoption in high-performance applications.

Competitive Landscape

Major players operating in the heat sinks market include:

Advanced Thermal Solutions Inc.

Aavid Thermalloy LLC

Sunonwealth Electric Machine Industry Co. Ltd.

Delta Electronics Inc.

CUI Devices

Molex LLC

TE Connectivity Ltd.

These companies are investing heavily in R&D to develop innovative and efficient heat sink technologies. Strategic collaborations, product launches, and geographic expansions are also part of their growth strategies.

Future Outlook

With the continuous innovation in electronic devices, rise in EV adoption, and need for thermal efficiency, the heat sinks market is poised for sustained growth. Companies focusing on lightweight, compact, and high-conductivity materials will have a competitive edge in the coming years.

As per Expert Market Research, players should focus on environmentally sustainable materials and customizable solutions to align with industry-specific thermal needs.

Request a Sample Report

To receive the full market report, please enter your Business email address in the link below and one of our analysts will contact you - Request a Sample

Contact Us

Expert Market Research (EMR) 30 North Gould Street, Sheridan, WY 82801 Phone: +1-415-325-5166

Please feel free to contact us with any questions or for more information about our reports and market research services. Our team is at your disposal.

0 notes

Text

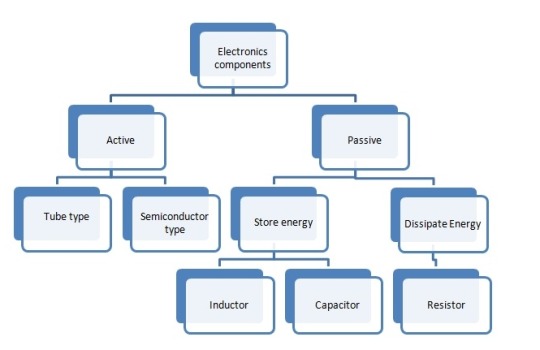

Understanding the Classification of Electronic Components

In simple terms, the basic parts used to manufacture or assemble electronic devices can be referred to as electronic components. Electronic components are independent entities within electronic circuits.

Technologically, the development of the electronics industry has led to two major branches of electronic circuits: integrated circuits and discrete component circuits.

Active Components and Passive Components

To align with the international distinction between active and passive components, mainland China typically refers to them as active devices and passive devices.

Active Devices

Active devices correspond to active components.

Electronic components such as transistors, thyristors, and integrated circuits require an excitation power source in addition to an input signal to function normally, hence the term “active devices.”

Active components also consume electrical energy, and high-power active components typically require heat sinks.

Passive components

Passive components, which encompass both passive electronic components and passive circuit components, are inherently defined by their functional characteristics in electrical systems. Resistors, capacitors, and inductors, as classic examples of these elements, can perform their specified functions in a circuit with the passage of a signal without relying on an external power source—this independence from auxiliary energy is precisely what categorizes them under the umbrella of passive components. Whether viewed as foundational passive electronic components that form the building blocks of device design or as critical passive circuit components that dictate circuit behavior, these elements exhibit a unique energy profile: they consume minimal electrical energy or efficiently convert it into other forms such as heat, light, or magnetic energy, thereby shaping the fundamental operation of electronic systems without active energy amplification.

Unikeyic is a global authorized distributor and stockist of high-quality electronic components. We offer a diverse product portfolio, including active components, passive components, discrete components, connectors, and more. Our website, https://www.unikeyic.com, showcases over 200,000 in-stock components, ensuring you can find the right parts for your electronic projects. We are committed to providing our customers with more than just components—we offer comprehensive solutions to help them optimize their designs and reduce time-to-market. Our technical team is well-equipped to provide design guidance, component selection recommendations, and troubleshooting support. We also have a robust quality management system in place to ensure that every component we distribute meets the highest industry standards. With Unikeyic, you can trust that you will receive the best components supported by reliable service and expert support.

0 notes

Text

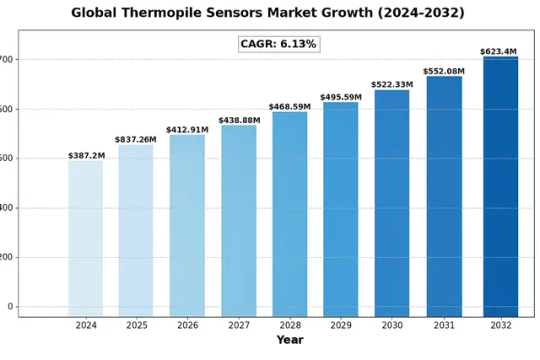

Global Thermopile Sensors Market, Emerging Trends, and Forecast to 2032

Global Thermopile Sensors Market was valued at US$ 387.2 million in 2024 and is projected to reach US$ 623.4 million by 2032, at a CAGR of 6.13% during the forecast period 2025-2032.

Thermopile sensors are infrared detection devices that convert thermal energy into electrical signals through series-connected thermocouples. These passive components measure temperature differences without direct contact, making them ideal for applications requiring non-invasive thermal monitoring. The technology is widely used in medical thermometers, industrial process control, automotive climate systems, and smart home devices.

The market growth is driven by increasing adoption in automotive HVAC systems, where demand rose 12% year-over-year in 2023. The healthcare sector accounts for 28% of total market share, propelled by contactless temperature measurement needs post-pandemic. Recent developments include Murata’s 2024 launch of ultra-thin thermopile arrays for wearable medical devices, while Texas Instruments expanded production capacity by 15% to meet growing IoT demand. Key players like Excelitas Technologies and FLIR Systems dominate the competitive landscape with advanced MEMS-based solutions.

Get Full Report with trend analysis, growth forecasts, and Future strategies : https://semiconductorinsight.com/report/global-thermopile-sensors-market/

Segment Analysis:

By Type

Thermopile Infrared Sensors Lead the Market with Rising Demand in Non-Contact Temperature Measurement

The market is segmented based on type into:

Thermopile Infrared Sensors

Thermopile Laser Sensors

Dual-band Thermopile Sensors

Matrix Thermopile Sensors

Others

By Application

Medical Science Segment Shows Strong Growth Potential Due to Increased Use of Thermopile Sensors in Diagnostic Equipment

The market is segmented based on application into:

Medical Science

Military and Defense

Automobile Industry

Intelligent Furnishing

Others

By Operating Wavelength

Long-Wave Infrared (LWIR) Sensors Dominate With Widespread Use in Thermal Imaging

The market is segmented based on operating wavelength into:

Short-Wave Infrared (SWIR)

Mid-Wave Infrared (MWIR)

Long-Wave Infrared (LWIR)

Others

By End User

Industrial Sector Accounts for Significant Market Share Due to Process Control Applications

The market is segmented based on end user into:

Industrial

Healthcare

Consumer Electronics

Automotive

Others

Regional Analysis: Global Thermopile Sensors Market

North America The North American thermopile sensors market is driven by strong demand from key industries such as defense, automotive, and medical technology. The region benefits from significant R&D investments in sensor technology, with the U.S. accounting for over 40% of global spending in infrared and thermal sensing applications. Regulatory requirements mandating safety and efficiency in automotive emissions monitoring and smart HVAC systems are accelerating adoption. Major players like Excelitas Technologies and Texas Instruments dominate the landscape, leveraging advanced manufacturing capabilities. However, high production costs and competition from cheaper Asian suppliers pose challenges. The growing shift toward Industry 4.0 and IoT integration in manufacturing presents long-term opportunities.

Europe Europe maintains steady growth in thermopile sensors, primarily due to stringent industrial safety standards and rapid advancements in automotive ADAS (Advanced Driver Assistance Systems). Germany, France, and the UK lead adoption in medical diagnostics and energy-efficient building automation. EU directives on CO2 monitoring and non-contact temperature measurement in public spaces post-pandemic have further boosted demand. European manufacturers like Heimann Sensor GmbH excel in precision thermopile solutions for aerospace and healthcare. However, supply chain disruptions caused by geopolitical tensions and reliance on external semiconductor suppliers create vulnerabilities. Sustainability-focused innovations, particularly in renewable energy applications, are key growth drivers.

Asia-Pacific As the fastest-growing regional market, Asia-Pacific benefits from mass production capabilities in China and Japan, with Shenzhen emerging as a major sensor manufacturing hub. Japan’s Nippon Ceramic and China’s Winsensor lead in cost-competitive thermopile modules for consumer electronics and automotive uses. India’s expanding medical device sector and Southeast Asia’s smart city initiatives drive incremental demand. Price sensitivity remains a challenge, with local manufacturers prioritizing affordability over high-end specifications. The region’s dominance in electronics manufacturing ensures sustained growth, though intellectual property protection issues occasionally disrupt market dynamics.

South America The South American market shows moderate growth, concentrated in Brazil’s industrial automation and Argentina’s agricultural monitoring sectors. Limited local manufacturing capabilities result in heavy reliance on imports from North America and Asia. Economic instability and fluctuating currency values hinder large-scale adoption, though mining and oil/gas applications provide stable demand pockets. Governments are increasingly investing in infrared-based security systems for public safety, creating opportunities. The lack of standardized regulations compared to Europe or North America slows market maturation, but Brazil’s automotive sector shows promising uptake for driver monitoring systems.

Middle East & Africa This emerging market is gaining traction through infrastructure modernization in Gulf Cooperation Council (GCC) countries, particularly for smart building technologies in UAE and Saudi Arabia. South Africa leads in mining safety applications, while North African nations are adopting medical thermopiles for pandemic preparedness. The market suffers from fragmented distribution networks and low awareness of advanced sensing solutions outside oil/gas sectors. However, megaprojects like NEOM in Saudi Arabia are expected to drive demand for environmental monitoring sensors. Price competition from Asian suppliers and delayed technology transfer remain barriers to widespread implementation.

MARKET OPPORTUNITIES

Medical Diagnostic Applications Present Significant Growth Potential

The healthcare sector offers substantial opportunities for thermopile sensor expansion, particularly in non-contact temperature measurement applications. The global medical infrared thermometer market alone is projected to grow at nearly 8% CAGR through 2030, driven by infection control protocols and telehealth adoption. Thermopile sensors enable precise, hygienic temperature monitoring without patient contact, making them ideal for hospitals, clinics, and home healthcare settings.

Advancements in AI-Enabled Predictive Maintenance Create New Use Cases

The integration of thermopile sensors with artificial intelligence and machine learning platforms is creating innovative industrial applications. By combining thermal imaging data with predictive analytics, these systems can identify equipment faults before they cause failures. Major industrial automation providers are increasingly incorporating thermopile-based condition monitoring into their service offerings, representing a high-value market segment growing at approximately 15% annually.

Furthermore, smart city initiatives leveraging thermopile sensors for building efficiency and traffic management present additional growth avenues. Municipalities worldwide are investing in intelligent infrastructure that utilizes thermal sensing for applications ranging from pedestrian flow analysis to building heat loss detection.

THERMOPILE SENSORS MARKET TRENDS

Expanding Applications in Automotive and Smart Home Devices Driving Market Growth

The global thermopile sensors market is experiencing robust growth, primarily fueled by increasing integration in automotive climate control systems and smart home devices. As vehicles evolve toward electrification and autonomous operation, demand for precise temperature monitoring in battery management and cabin comfort systems has surged. The smart home sector, valued at over $100 billion globally, relies heavily on thermopile sensors for HVAC optimization and presence detection in intelligent thermostats. Industry data suggests that shipments for consumer-grade infrared temperature sensors grew by approximately 18% year-over-year in 2023, with thermopiles representing nearly 40% of this segment.

Other Trends

Miniaturization and Energy Efficiency Innovations

Technological advancements are enabling the development of smaller, lower-power thermopile sensors without compromising accuracy. Recent innovations in MEMS (Micro-Electro-Mechanical Systems) technology have produced sensors with footprints under 3x3mm while achieving sub-0.1°C resolution. These improvements are critical for wearable medical devices and IoT applications where space and power constraints are paramount. Furthermore, the adoption of advanced materials like silicon-germanium alloys has enhanced thermal response times by up to 30% compared to conventional designs.

Growing Demand in Industrial Automation and Safety

Industrial sectors are increasingly deploying thermopile sensors for predictive maintenance and equipment monitoring. The ability to perform non-contact temperature measurements in hazardous environments makes them ideal for manufacturing plants and energy facilities. Market analysis indicates that the industrial segment accounted for over 25% of global thermopile sensor revenue in 2023, with particularly strong adoption in semiconductor fabrication and chemical processing. Moreover, stricter workplace safety regulations worldwide are accelerating the replacement of traditional thermocouples with more reliable thermopile-based solutions in high-risk applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Define Market Leadership in Thermopile Sensors

The global thermopile sensors market features a dynamic competitive landscape, characterized by the presence of established players and emerging innovators. Leading companies such as Excelitas Technologies and FLIR Systems dominate the market, leveraging their strong R&D capabilities and diverse product portfolios. Excelitas, for instance, holds a substantial market share due to its high-performance infrared thermopile sensors, widely used in automotive and industrial applications.

Meanwhile, Hamamatsu Photonic and Nippon Ceramic have strengthened their positions through continuous technological advancements. Hamamatsu’s expertise in photonics has enabled it to develop ultra-sensitive thermopile sensors, particularly for medical and scientific applications, contributing to its growing market influence.

The market also sees intense competition from mid-sized players like Heimann Sensor GmbH and TE Connectivity, which focus on niche applications such as smart home devices and consumer electronics. These companies are rapidly expanding their geographic footprint, particularly in Asia-Pacific, where demand for smart sensors is surging.

Recent strategic moves, such as Murata’s acquisition of smaller sensor manufacturers and Texas Instruments’ investment in MEMS-based thermopile technology, highlight the market’s evolution. Such initiatives not only enhance product offerings but also consolidate market positions, ensuring long-term competitiveness.

List of Key Thermopile Sensor Companies Profiled

Excelitas Technologies (U.S.)

FLIR Systems (U.S.)

Hamamatsu Photonic (Japan)

Nippon Ceramic (Japan)

TE Connectivity (Switzerland)

Heimann Sensor GmbH (Germany)

Texas Instruments (U.S.)

Panasonic (Japan)

Fuji Ceramics Corporation (Japan)

Murata (Japan)

Learn more about Competitive Analysis, and Forecast of Global Thermopile Sensors Market : https://semiconductorinsight.com/download-sample-report/?product_id=44627

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Thermopile Sensors Market?

-> Thermopile Sensors Market was valued at US$ 387.2 million in 2024 and is projected to reach US$ 623.4 million by 2032, at a CAGR of 6.13% during the forecast period 2025-2032.

Which key companies operate in Global Thermopile Sensors Market?

-> Key players include Excelitas Technologies, Flir Systems, Texas Instruments, Hamamatsu Photonic, TE Connectivity, and Murata, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for non-contact temperature measurement, increasing adoption in automotive applications, and growing IoT deployments.

Which region dominates the market?

-> Asia-Pacific dominates the market with over 40% share, driven by manufacturing growth in China and Japan, while North America leads in technological advancements.

What are the emerging trends?

-> Emerging trends include miniaturization of sensors, integration

Browse Related Reports :

CONTACT US:

City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014 +91 8087992013 [email protected]

0 notes

Text

UHF RFID IC Market 2025-2032

MARKET INSIGHTS

The global UHF RFID IC Market size was valued at US$ 1,930 million in 2024 and is projected to reach US$ 3,460 million by 2032, at a CAGR of 8.6% during the forecast period 2025-2032. This growth aligns with the broader semiconductor market expansion, which was valued at USD 579 billion in 2022 and is expected to reach USD 790 billion by 2029.

UHF RFID ICs are semiconductor devices operating in the 860-960 MHz frequency range, enabling wireless identification and tracking of objects through radio waves. These integrated circuits power RFID tags and readers across industries by providing unique identification, data storage, and wireless communication capabilities. The market comprises two primary types: Active RFID ICs (with battery power for longer ranges) and Passive RFID ICs (harvesting energy from reader signals).

The market expansion is driven by increasing adoption in retail inventory management, supply chain logistics, and healthcare asset tracking. Notably, the retail sector accounted for over 35% of application share in 2024, followed by logistics at 28%. While analog IC segments grew by 20.76% in 2022, memory ICs faced a 12.64% decline, creating opportunities for RFID innovation. Key players like Impinj and NXP Semiconductors continue to enhance IC designs for better read ranges and data capacities, with recent advancements focusing on IoT integration and edge computing capabilities.

Access Your Free Sample Report Now-https://semiconductorinsight.com/download-sample-report/?product_id=97575

Key Industry Players

Technological Advancements and Strategic Alliances Drive Market Competition

The global UHF RFID IC market features a dynamic competitive landscape with a mix of established semiconductor giants and specialized RFID solution providers. Impinj stands out as the market leader, capturing approximately 25% market share in 2024 due to its pioneering RAIN RFID technology and expansive portfolio of high-performance UHF RFID ICs. The company’s strategic partnerships with retail and logistics enterprises have further solidified its dominant position.

NXP Semiconductors, with its strong foothold in the automotive and industrial sectors, holds the second-largest market share. The company’s UCODE series has become an industry standard, particularly in supply chain applications. Alien Technology follows closely, specializing in flexible tag ICs that cater to emerging applications in smart packaging and connected devices.

Market competition intensifies as companies pursue three key strategies: miniaturization of IC components, enhanced read ranges, and better power efficiency. Recent technological breakthroughs include EM Microelectronic’s development of sensor-enabled RFID ICs for cold chain logistics and STMicroelectronics’ introduction of automotive-grade UHF ICs.

Chinese manufacturers like Fudan Microelectronics Group and Shanghai Quanray Electronics are rapidly gaining traction through competitive pricing and government-supported R&D initiatives. These regional players accounted for 18% of the Asia-Pacific market in 2024, challenging established Western manufacturers.

List of Leading UHF RFID IC Manufacturers

Impinj, Inc. (U.S.)

NXP Semiconductors (Netherlands)

Alien Technology (U.S.)

EM Microelectronic (Switzerland)

STMicroelectronics (Switzerland)

Fudan Microelectronics Group (China)

Kiloway (China)

Invengo Information Technology (China)

Shanghai Quanray Electronics (China)

ZSM Electronics (China)

RICE GROUP (Japan)

Segment Analysis:

By Type

Passive RFID IC Segment Dominates Due to Cost-Effectiveness and Widespread Adoption in Retail and Logistics

The market is segmented based on type into:

Active RFID IC

Passive RFID IC

By Application

Retail Application Leads the Market Owing to Increased Adoption of Smart Inventory Management

The market is segmented based on application into:

Retail

Logistics

Medical

Clothing

Other

By Frequency Range

860-960 MHz Segment Holds Major Share Due to Global Standardization in UHF RFID

The market is segmented based on frequency range into:

860-960 MHz

Other frequency bands

By End User

Manufacturing Sector Accounts for Significant Adoption of UHF RFID ICs for Asset Tracking

The market is segmented based on end user into:

Manufacturing

Healthcare

Transportation

Government

Other

Download Your Complimentary Sample Report-https://semiconductorinsight.com/download-sample-report/?product_id=97575

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global UHF RFID IC Market?

-> The global UHF RFID IC market was valued at USD 780 million in 2024 and is expected to reach USD 1.2 billion by 2032.

Which key companies operate in Global UHF RFID IC Market?

-> Key players include Impinj, NXP, Alien Technology, EM Microelectronic, ST Microelectronics, and Fudan Microelectronics Group, among others.

What are the key growth drivers?

-> Key growth drivers include retail automation, supply chain digitization, IoT adoption, and increasing use in healthcare asset tracking.

Which region dominates the market?

-> Asia-Pacific dominates with 42% market share, while North America shows the highest growth potential at 6.2% CAGR.

What are the emerging trends?

-> Emerging trends include AI-powered RFID systems, sustainability-focused IC designs, and integration with blockchain for supply chain transparency.

About Semiconductor Insight

Established in 2016, Semiconductor Insight specializes in providing comprehensive semiconductor industry research and analysis to support businesses in making well-informed decisions within this dynamic and fast-paced sector. From the beginning, we have been committed to delivering in-depth semiconductor market research, identifying key trends, opportunities, and challenges shaping the global semiconductor industry.

CONTACT US:

City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

0 notes

Text

The Podcast Boom: Is Audio the New King of Media?

The Podcast Boom: Is Audio the New King of Media?

In a world saturated with visual content, a quieter yet powerful revolution has been unfolding—the podcast boom. Over the past decade, audio has surged ahead, not just as an alternative form of content, but as a dominant force transforming how people consume media. From the daily news to niche interests and branded storytelling, podcasts are becoming central to digital media strategies and audience engagement.

This article dives into the rise of podcasts, the shifting audio content trends, and why experts believe the podcast industry is now one of the fastest-growing sectors in entertainment and marketing.

The Rise of Podcasts: A Digital Disruption

Once a fringe medium for hobbyists, podcasts have gone mainstream. The rise of podcasts is undeniable—millions of episodes are streamed daily on platforms like Spotify, Apple Podcasts, and YouTube. According to recent statistics, over 460 million people globally now listen to podcasts, with that number expected to grow significantly by 2026.

This explosion is partly due to the accessibility of digital audio content. With smartphones, Bluetooth-enabled cars, and smart home devices, audio is now an anytime, anywhere format. Listeners can multitask—learning, laughing, or relaxing—while commuting, working out, or cooking dinner.

Podcast Boom: Redefining Media Engagement

The podcast boom is about more than numbers—it's about a change in consumer behavior. Audiences crave content that is authentic, convenient, and relevant. Podcasts provide a uniquely intimate experience; listeners feel like they’re part of a conversation, not just passive consumers.

Brands have taken notice. The growth of podcasting is also fueled by marketers who are integrating audio strategies into their content mix. From sponsorships and host-read ads to branded podcast series, the opportunities for podcast marketing are vast.

Major companies across industries now view podcasting as a serious content pillar. It’s a direct way to build trust, deliver value, and target niche demographics with precision.

Audio Content Trends Driving the Boom

Several audio content trends have emerged alongside the podcast boom:

Personalization: Platforms now offer personalized podcast recommendations, increasing listener retention and satisfaction.

Short-form content: Microcasts (5–10-minute episodes) are on the rise, catering to the TikTok-style preference for quick, digestible content.

Video-podcast hybrids: Many podcasters are now filming their episodes for YouTube or TikTok, enhancing discovery and expanding reach.

Localization: As podcasting grows globally, localized content in multiple languages is fueling new audience segments.

These trends reflect not only the growth of podcasting but also the adaptability of audio to fit seamlessly into modern life.

Podcast Boom and the Evolving Podcast Industry

The podcast industry has matured significantly. Once decentralized and grassroots, it is now structured, monetized, and professionalized. From podcast studios and production agencies to podcast-specific ad networks, the infrastructure around audio content has evolved rapidly.

Big players like Amazon, Spotify, and Apple are investing billions into exclusive deals, talent acquisition, and platform development. Meanwhile, independent creators continue to thrive, proving that podcasting remains one of the few media landscapes where small voices can still go viral.

The podcast market growth shows no signs of slowing. According to Insider Intelligence, U.S. podcast ad revenue is projected to surpass $4 billion by 2025, with global growth following closely behind.

The Role of Podcast Marketing in Business Strategy

As businesses adapt to changing content consumption habits, podcast marketing is becoming a strategic differentiator. Audio allows brands to reach consumers in contexts where visual media can't—like during a commute, run, or household chores.

Podcast listeners are also more engaged. Studies show they tend to be more loyal, more likely to make purchases, and more receptive to ads. In fact, 63% of listeners say they've bought something after hearing an ad on a podcast.

That’s why companies large and small are using branded podcasts to tell their stories, educate their audience, or support broader campaigns. In a time when trust in traditional advertising is low, the human voice still has persuasive power.

What’s Next for the Podcast Boom?

So, is audio the new king of media? While video and visual formats will always have their place, the podcast boom is proving that audio isn’t just an alternative—it’s a preferred channel for millions.

The future of the podcast industry lies in innovation, accessibility, and continued audience growth. As new tools make podcast creation easier and distribution more targeted, we’ll likely see an even greater democratization of content.

For investors, creators, and marketers alike, now is the time to tune in and turn up the volume on audio.

Want to explore how innovations like podcasting are reshaping the media world? Discover deep insights in IMPAAKT, the leading top business magazine for impact-driven trends.

0 notes

Text

The Symbiosis Between Microbial Inoculants and Fertilizer Production Line

Agricultural microbial agents, as functional additives, are organically integrated with fertilizer production lines, combining active microorganisms with fertilizer carriers through scientific formulation and special processes to form bio-fertilizers that improve soil and promote crop growth.

How Microbial Inoculants Enhance Fertilizer Efficiency

Agricultural microbial inoculants complement rather than replace chemical fertilizers through three key mechanisms:

Nutrient conversion: Nitrogen-fixing bacteria convert 40-200kg/ha atmospheric N annually, while P-solubilizing microbes increase phosphate availability by 30-50%[1]

Nutrient retention: Microbial metabolites form organo-mineral complexes that reduce leaching

Root enhancement: Rhizosphere microbes expand root absorption area by 50-70%, boosting fertilizer efficacy[2]

FAO data shows: Combined use of microbial inoculants with fertilizers can reduce chemical inputs by 25-40% while maintaining yields and lowering environmental risks[3].

Innovative Applications in Fertilizer Production

The modern fertilizer industry has developed various microbe-enhanced products:

Bio-coated fertilizers: Urea granules coated with nitrogen-fixing bacteria for dual slow-release and biological N fixation

Composite microbial fertilizers: Containing ≥20 million CFU/g viable bacteria plus N-P-K and micronutrients

Organic-inorganic-bio ternary fertilizers: Combining the advantages of organic matter, chemical nutrients and functional microbes

The global microbial fertilizer market reached $2.87 billion in 2023 with 12.4% CAGR, reflecting market acceptance[4].

Critical Roles in Fertilizer Processing

Microbial inoculants play central roles in organic fertilizer production:

Rapid composting: Thermophilic microbes reduce processing time from 60 to 20-30 days

Deodorization: Specialized microbes degrade NH₃, H₂S etc., reducing nitrogen loss

Heavy metal passivation: Microbial metabolites immobilize Cd, Pb etc., decreasing bioavailability by 30-60%[5]

Advanced organic fertilizer plants adopt "pretreatment+composite inoculants+smart control" systems to meet organic farming standards.

Agricultural microbial agents are closely related to fertilizer production lines. Microbial agents can be directly blended into organic or compound fertilizer production lines as functional additives, combining with fertilizer carriers through specific processes to form bio-organic fertilizers. Alternatively, they can be coated onto granular fertilizers using post-production coating technology. The production line requires specialized equipment such as precise dosing systems and low-temperature mixing devices to ensure microbial viability. The use of microbial agents enhances the functionality of traditional fertilizers, promotes soil improvement and crop nutrient uptake, creating a synergistic "fertilizer carrier + active microbial community" system.

References

[1] Chen et al. (2022). Nature Microbiology: Microbial Nutrient Cycling

[2] FAO. (2021). Soil Biofertilizers: Technical Guidelines

[3] UNEP. (2023). Global Fertilizer Reduction Roadmap

[4] MarketsandMarkets. (2023). Biofertilizers Market Report

[5] Wang & Smith. (2023). Journal of Cleaner Production, Vol. 412

0 notes

Text

Role of Colloidal Metal Nanoparticles in Drug Delivery Systems

The colloidal metal particles market, long associated with conventional applications in electronics, optics, and chemical catalysis, is undergoing a quiet but profound transformation. Comprising nanoscale dispersions of metals such as gold, silver, platinum, and palladium, colloidal particles possess unique optical, electronic, and catalytic properties. Traditionally, their use has centered around established industries, yet recent technological advancements are pushing these particles into uncharted and highly promising territories. Among the most compelling of these are biosensing and sustainable catalysis—sectors where their potential remains underexplored but undeniably powerful.

𝐄𝐦𝐞𝐫𝐠𝐢𝐧𝐠 𝐑𝐨𝐥𝐞 𝐢𝐧 𝐏𝐫𝐞𝐜𝐢𝐬𝐢𝐨𝐧 𝐁𝐢𝐨𝐬𝐞𝐧𝐬𝐢𝐧𝐠 𝐓𝐞𝐜𝐡𝐧𝐨𝐥𝐨𝐠𝐢𝐞𝐬

In recent years, colloidal metal particles—especially gold and silver nanoparticles���have emerged as critical components in the design of next-generation biosensors. Their high surface-area-to-volume ratio and tunable surface plasmon resonance properties make them ideal candidates for detecting biological markers with extreme sensitivity. In particular, gold colloids have been successfully integrated into lateral flow assays, enabling the rapid detection of viral infections such as COVID-19 and Zika virus. These tests, which rely on the optical properties of gold nanoparticles to signal the presence of antigens, have demonstrated that metal colloids are not just passive materials but active agents of change in the diagnostic landscape.

𝐌𝐚𝐤𝐞 𝐈𝐧𝐟𝐨𝐫𝐦𝐞𝐝 𝐃𝐞𝐜𝐢𝐬𝐢𝐨𝐧𝐬 – 𝐀𝐜𝐜𝐞𝐬𝐬 𝐘𝐨𝐮𝐫 𝐒𝐚𝐦𝐩𝐥𝐞 𝐑𝐞𝐩𝐨𝐫𝐭 𝐈𝐧𝐬𝐭𝐚𝐧𝐭𝐥𝐲! https://www.futuremarketinsights.com/reports/sample/rep-gb-9012

The biosensor application of metal colloids extends far beyond rapid test kits. A study published in ACS Nano showed that silver nanoparticles functionalized with specific DNA sequences could detect microRNA at concentrations as low as one femtomolar, suggesting enormous promise for early-stage cancer diagnostics. Likewise, palladium and platinum colloids are being researched for their role in electrochemical biosensors, where their catalytic behavior enhances the detection of glucose, lactate, and other biomarkers in real time. This innovation has far-reaching implications for the development of non-invasive, wearable biosensors that could eventually replace traditional blood-based testing protocols.

𝐂𝐚𝐭𝐚𝐥𝐲𝐭𝐢𝐜 𝐁𝐫𝐞𝐚𝐤𝐭𝐡𝐫𝐨𝐮𝐠𝐡𝐬 𝐢𝐧 𝐭𝐡𝐞 𝐇𝐲𝐝𝐫𝐨𝐠𝐞𝐧 𝐄𝐜𝐨𝐧𝐨𝐦𝐲