#IoT Edge Computing Software IoT Edge Computing Software Market IoT Edge Computing Software Market 2022 IoT Edge Computing Software Market An

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr has a 66 index score for customer satisfaction in the US.

Text

U.S. Internet of Things (IoT) Market Size to Hit USD 118.24 Bn by 2030

The U.S. Internet of Things (IoT) market share remains one of the most mature and dynamic ecosystems globally. Valued at USD 98.09 billion in 2022, the market is projected to grow from USD 118.24 billion in 2023 to USD 553.92 billion by 2030, registering a compound annual growth rate (CAGR) of 24.7% during the forecast period. The U.S. Internet of Things (IoT) market refers to the ecosystem of interconnected physical devices, sensors, software, and network infrastructure that enables the collection, exchange, and analysis of data across a wide range of industries. These devices are embedded with computing technology that allows them to monitor environments, automate processes, and communicate with other systems and users in real-time.

Key Market Highlights: • Market Size (2022): USD 98.09 billion • Projected Size (2030): USD 553.92 billion • CAGR (2023–2030): 24.7% • Growth Drivers: Technological maturity, innovation leadership, and extensive IoT adoption across industries.

Leading U.S. Companies in the IoT Space: • Cisco Systems, Inc. • Amazon Web Services (AWS) • Microsoft Corporation • Intel Corporation • Qualcomm Technologies, Inc. • Hewlett Packard Enterprise (HPE) • IBM Corporation • Google LLC • Oracle Corporation • PTC Inc.

Request For Sample PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/u-s-internet-of-things-iot-market-107392

Market Dynamics:

Strategic Market Drivers: • Expansion of smart city infrastructure supported by federal and state governments. • Increasing deployment of industrial IoT (IIoT) for manufacturing automation and predictive maintenance. • Growth in consumer IoT, including connected homes, wearables, and personal health tracking devices. • Advancements in 5G, AI, and edge computing fueling real-time, decentralized data processing.

Major Opportunities: • Healthcare IoT for remote patient monitoring, smart diagnostics, and hospital asset management. • Smart grid and energy optimization systems led by clean energy policies. • Transportation and mobility solutions such as connected vehicles and V2X communication. • Federal funding for infrastructure modernization and cybersecurity in IoT environments.

Market Applications: • Smart manufacturing • Connected healthcare and telemedicine • Smart homes and consumer IoT • Fleet and supply chain management • Environmental and agricultural monitoring • Retail automation and customer behavior tracking

Deployment Models & Connectivity: • Deployment Types: Cloud-based, on-premises, hybrid, and edge-enabled solutions • Connectivity: 5G, Wi-Fi 6, LPWAN (LoRa, NB-IoT), Bluetooth, Zigbee, and satellite IoT

Key Market Trends: • Surging interest in cybersecure IoT ecosystems and zero-trust architecture. • Integration of artificial intelligence (AI) with IoT for autonomous decision-making. • Proliferation of IoT-as-a-Service (IoTaaS) and managed IoT platforms. • Increased focus on sustainability and green IoT solutions for emissions tracking and resource efficiency.

Speak to Analyst: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/u-s-internet-of-things-iot-market-107392

Recent Industry Developments: May 2023 – Amazon Web Services (AWS) expanded its IoT TwinMaker platform, enabling faster digital twin deployment for industrial and logistics enterprises across the U.S.

August 2023 – Cisco launched its U.S.-focused IoT Operations Dashboard for real-time device tracking, configuration management, and anomaly detection at enterprise scale.

About Us: Fortune Business Insights delivers powerful data-driven insights to help businesses navigate disruption and capitalize on emerging trends. We specialize in delivering sector-specific intelligence, customized research, and strategic consulting across a wide range of industries. Our team empowers organizations with clarity, foresight, and a competitive edge in a fast-moving technological landscape.

Contact Us: US: +1 833 909 2966 UK: +44 808 502 0280 APAC: +91 744 740 1245 Email: [email protected]

#U.S. Internet of Things Market Share#U.S. Internet of Things Market Size#U.S. Internet of Things Market Industry#U.S. Internet of Things Market Driver#U.S. Internet of Things Market Growth#U.S. Internet of Things Market Analysis#U.S. Internet of Things Market Trends

0 notes

Text

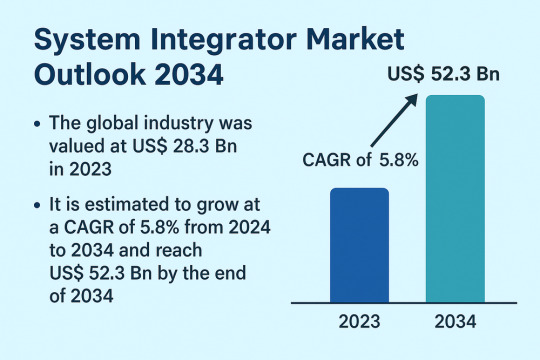

Automation and Integration Needs Power Robust Growth in System Integrator Market

The global System Integrator Market is poised for significant growth, projected to rise from US$ 28.3 Bn in 2023 to US$ 52.3 Bn by 2034, growing at a CAGR of 5.8% from 2024 to 2034. This growth is driven by the widespread adoption of industrial robots, technological advancements, and a pressing need among businesses to optimize operational efficiencies through connected systems.

System integrators play a pivotal role in designing, implementing, and maintaining integrated solutions that bring together hardware, software, and consulting services. These services support organizations in unifying internal and external systems, such as SCADA, HMI, MES, PLC, and IIoT, to enable seamless data flow and system interoperability.

Market Drivers & Trends: One of the primary market drivers is the rise in adoption of industrial robots. As industries accelerate automation, robotic system integrators have become vital in delivering customized, scalable, and high-performing solutions tailored to complex manufacturing needs.

Another major catalyst is the surge in technological advancements. Integrators are deploying cloud-based tools and platforms that provide real-time data insights, improve developer productivity, and support hybrid architectures. The increasing use of Artificial Intelligence (AI), Machine Learning (ML), and Internet of Things (IoT) in integration solutions is fostering innovation and growth.

Latest Market Trends

Several emerging trends are shaping the system integrator landscape:

Cloud modernization platforms such as IBM’s Z and Cloud Modernization Center are enabling businesses to accelerate the transition to hybrid cloud environments.

Modular automation platforms are gaining popularity, allowing companies to rapidly deploy and scale integration solutions across multiple industry verticals.

Edge computing and cybersecurity solutions are increasingly being integrated to support secure, real-time decision-making on the production floor.

Digital hubs and scalable workflow engines are being adopted by integrators to support multi-specialty applications with high adaptability.

Key Players and Industry Leaders

The system integrator market is characterized by a strong mix of global leaders and regional specialists. Key players include:

ATS Corporation

Avanceon

Avid Solutions

Brock Solutions

JR Automation

MAVERICK Technologies, LLC

Burrow Global, LLC

BW Design Group

John Wood Group PLC

TESCO CONTROLS

These companies are actively investing in next-generation technologies, enhancing their product portfolios, and pursuing strategic acquisitions to strengthen market presence. For instance, in July 2023, ATS Corporation acquired Yazzoom BV, a Belgian AI and ML solutions provider, expanding their capabilities in smart manufacturing.

Recent Developments

Olympus Corporation launched the EASYSUITE ES-IP system in July 2023 in the U.S., offering advanced visualization and integration solutions for procedure rooms.

IBM introduced key updates in 2021 and 2022 to streamline mission-critical application modernization using cloud services and hybrid IT strategies.

Asia-Pacific companies have led the charge in deploying advanced integrated systems, reflecting the rapid industrial digitization in countries such as China, Japan, and South Korea.

Market Opportunities

Opportunities abound in both mature and emerging markets:

Smart factories and Industry 4.0 transformation offer immense potential for integrators to offer comprehensive solutions tailored to real-time analytics, predictive maintenance, and remote monitoring.

Government-led infrastructure modernization projects, particularly in Asia and the Middle East, are increasing demand for integrated control systems and plant asset management solutions.

The energy transition movement, including renewables and electrification of industrial processes, requires new types of integration across decentralized assets.

Future Outlook

As industries pursue digital transformation, the role of system integrators will evolve from traditional project implementers to long-term strategic partners. The future will see increasing demand for intelligent automation, cross-domain expertise, and real-time adaptive solutions. Vendors who can provide holistic, secure, and scalable services will dominate the landscape.

With continued advancements in AI, IoT, and robotics, the system integrator market will continue to thrive, transforming operations across diverse sectors, from automotive and food & beverages to oil & gas and pharmaceuticals.

Review critical insights and findings from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=82550

Market Segmentation

The market is segmented based on offering, technology, and end-use industry.

By Offering:

Hardware

Software

Service (Consulting, Design, Installation)

By Technology:

Human-Machine Interface (HMI)

Supervisory Control and Data Acquisition (SCADA)

Manufacturing Execution System (MES)

Functional Safety System

Machine Vision

Industrial Robotics

Industrial PC

Industrial Internet of Things (IIoT)

Machine Condition Monitoring

Plant Asset Management

Distributed Control System (DCS)

Programmable Logic Controller (PLC)

By End-use Industry:

Oil & Gas

Chemical & Petrochemical

Food & Beverages

Automotive

Energy & Power

Pharmaceutical

Pulp & Paper

Aerospace

Electronics

Metals & Mining

Others

Regional Insights

Asia Pacific leads the global system integrator market, holding the largest market share in 2023. This leadership is attributed to:

Rapid industrialization and digital transformation in China, Japan, and India.

Strong investments in smart manufacturing and Industry 4.0 initiatives.

Government support for infrastructure modernization, especially through Smart City programs and cybersecure IT frameworks.

North America and Europe also show strong demand, driven by the presence of established manufacturing facilities and a robust focus on sustainable operations and green automation.

Why Buy This Report?

Comprehensive Market Analysis: Deep insights into market size, share, and growth across all major segments and geographies.

Detailed Competitive Landscape: Profiles of leading companies with analysis of their strategy, product offerings, and key financials.

Actionable Intelligence: Understand technological trends, regulatory developments, and investment opportunities.

Forecast-Based Strategy: Develop long-term strategic plans using data-driven forecasts up to 2034.

Frequently Asked Questions (FAQs)

1. What is the projected value of the system integrator market by 2034? The global system integrator market is projected to reach US$ 52.3 Bn by 2034.

2. What is the current CAGR for the forecast period 2024–2034? The market is anticipated to grow at a CAGR of 5.8% during the forecast period.

3. Which region holds the largest market share? Asia Pacific dominated the global market in 2023 and is expected to continue leading due to rapid industrialization and technology adoption.

4. What are the key growth drivers? Key drivers include the rise in adoption of industrial robots and continuous advancements in integration technologies like IIoT, AI, and cloud platforms.

5. Who are the major players in the system integrator market? Prominent players include ATS Corporation, JR Automation, Brock Solutions, MAVERICK Technologies, and Control Associates, Inc.

6. Which industries are adopting system integrator services the most? High adoption is seen in industries such as automotive, oil & gas, food & beverages, pharmaceuticals, and electronics.

Explore Latest Research Reports by Transparency Market Research:

Multi-Mode Chipset Market: https://www.transparencymarketresearch.com/multi-mode-chipset-market.html

Accelerometer Market: https://www.transparencymarketresearch.com/accelerometer-market.html

Luminaire and Lighting Control Market: https://www.transparencymarketresearch.com/luminaire-lighting-control-market.html

Advanced Marine Power Supply Market: https://www.transparencymarketresearch.com/advanced-marine-power-supply-market.html

About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

The Rise of the Prosumer IoT: Blurring the Lines Between Home and Business

Consumer IoT Industry Overview

The global Consumer IoT Market, valued at USD 220.50 billion in 2022, is projected to expand at a robust compound annual growth rate (CAGR) of 12.7% from 2023 to 2030. This significant growth can be attributed to the increasing popularity of technologically advanced devices and home appliances. Consumer internet of things (IoT) devices, integrating multiple microcontrollers and wireless technologies, streamline data sharing without direct user or computer interaction. Consumer IoT encompasses an interconnected ecosystem of digital and physical objects like smartphones, smart wearables, and smart home devices, specifically designed for consumer markets.

Detailed Segmentation:

Component Insights

On the basis of components, the global industry has been further categorized into hardware, services, and software. The hardware component segment accounted for the maximum revenue share of more than 38.85% in 2022 owing to the increasing demand for IoT devices. These devices comprise actuators, sensors, gadgets, machines, and appliances that are programmed for specific applications and can transmit data over networks.

Connectivity Technology Insights

The wireless connectivity technology segment is expected to record the fastest growth rate of more than 13.60% from 2023 to 2030, owing to the greater scalability offered by these networks. They do not require hardware installations and can be extended with ease without considering the obstructions in the facility. Most wireless sensors comprise nodes that can be extended by adding extra nodes whenever required. In addition, they are more cost-effective as their prices have reduced due to the ongoing advancements in wireless technology and an increasing number of manufacturers.

Application Insights

The wearable segment is estimated to register the fastest CAGR from 2023 to 2030 owing to the increasing internet penetration, rising disposable incomes, and lower average selling prices of these devices. In addition, wearable devices provide several benefits for healthcare providers as well as patients as they help in glucose monitoring, hand hygiene monitoring, heart-rate monitoring, Parkinson’s disease monitoring, depression monitoring, etc. Thus, the rising adoption of wearable consumer IoT devices for health monitoring is expected to create lucrative growth opportunities for the market.

Regional Insights

North America accounted for the largest share of more than 23.35% of the overall revenue in 2022 and is expected to grow significantly during the forecast period. This can be credited to the increased product demand, especially fitness tracking devices, in the region. According to a 2022 survey conducted by ValuePenguin on over 1,500 consumers, while 45% of Americans are already using smartwatches such as Fitbits and Apple Watches, 69% of respondents are willing to use a fitness tracker to get discounts on health insurance. Asia Pacific is expected to record a substantial CAGR from 2023 to 2030 with the growing popularity of smart home solutions in the region.

Gather more insights about the market drivers, restraints, and growth of the Consumer IoT Market

Key Companies & Market Share Insights

The key companies are focusing on introducing innovative offerings and enhancing their existing product portfolio to gain a competitive edge. In June 2022, SAMSUNG launched SmartThings Home Life, offering consumers a more holistic smart home experience. The new offering is an addition to the SmartThings app that provides users with integrated and centralized control over the company’s appliances through their smartphones. It combines the convenience of six SmartThings services - SmartThings Cooking, Clothing Care, Energy, Home Care, Pet Care, and Air Care. Some of the prominent players in the global consumer IoT market are:

Alphabet Inc.

Amazon.com, Inc.

Apple Inc.

AT&T

Cisco Systems, Inc.

Honeywell International Inc.

IBM Corp.

Intel Corp.

LG Corp.

Microsoft

Samsung

Schneider Electric

Sony Corp.

Texas Instruments

TE Connectivity

Order a free sample PDF of the Market Intelligence Study, published by Grand View Research.

0 notes

Text

Data-Driven Decisions: The Growing Importance of Enterprise Data Management in 2025

The global enterprise data management market size was estimated at USD 110.53 billion in 2024 and is anticipated to grow at a CAGR of 12.4% from 2025 to 2030. Several key factors drive the Enterprise Data Management (EDM) market. The exponential growth of data generated by businesses necessitates efficient data management solutions to harness this information for decision-making and competitive advantage. Increasing regulatory requirements for data privacy and security compels organizations to adopt robust EDM practices to ensure compliance. The rise of cloud computing and advancements in data analytics technologies also propel the market, enabling more scalable and sophisticated data management capabilities.

The increasing need for robust risk management strategies is driving the adoption of EDM software. As organizations collect and store vast amounts of data, the potential for security breaches, regulatory non-compliance, and compromised data integrity becomes a significant concern. The rising volumes of data, fueled by digital transformation initiatives and the subsequent adoption of emerging technologies, such as Internet of Things (IoT), creates a complex and dynamic data landscape and necessitates effective data management practices to mitigate the financial and reputational risks associated with data breaches, inaccurate insights, and regulatory non-compliance.

Data breaches can have severe financial implications stemming from undesired downtimes, data recovery costs, and potential lawsuits. Compromised data can also tarnish an organization's reputation, eroding customer trust and loyalty. To address these risks, enterprises are implementing robust data management strategies, such as data encryption, access controls, and Data Loss Prevention (DLP) measures. By adopting comprehensive data management practices, organizations can safeguard their data assets, ensure regulatory compliance, and gain a competitive edge. As the volume and complexity of data continue to grow, the need for effective risk management will only become more pressing.

Enterprises are facing an increasing risk of data breaches and privacy concerns due to the exponential growth in data volumes. According to IBM's 2022 Cost of a Data Breach Report, the average cost of a data breach reached a record high of USD 4.35 million globally. Effective data governance and risk management strategies are critical to mitigate these risks and protect an organization's brand reputation. A survey in November 2021, by Gartner found that 88% of the board of directors considered cybersecurity a business risk rather than solely an IT issue.

Regulatory compliance has become a critical driver in the EDM market, compelling organizations to rigorously manage and govern their data. Enterprises are confronted with a complex web of regulatory requirements varying for different industries, including finance, healthcare, and technology. These regulations mandate stringent data handling, storage, and security practices, making compliance essential for maintaining organizational reputation, avoiding hefty fines, and ensuring customer trust. Consequently, businesses are investing in sophisticated EDM solutions that provide robust data governance frameworks, audit trails, and compliance reporting features.

Global Enterprise Data Management Market Report Segmentation

Grand View Research has segmented the enterprise data management market report based on software, services, deployment, enterprise size, industry vertical, and region:

Software Outlook (Revenue, USD Billion; 2018 - 2030)

Data Security

Master Data Management

Data Integration

Data Migration

Data Warehousing

Data Governance

Data Quality

Metadata Management

Reference Data Management (RDM)

others

Services Outlook (Revenue, USD Billion; 2018 - 2030)

Managed Services

Professional Services

Deployment Outlook (Revenue, USD Billion; 2018 - 2030)

Cloud

On-premise

Enterprise Size Outlook (Revenue, USD Billion; 2018 - 2030)

Small & Medium Enterprise

Large Enterprise

Industry Vertical Outlook (Revenue, USD Billion; 2018 - 2030)

IT & Telecom

BFSI

Retail & Consumer Goods

Healthcare

Manufacturing

Others

Regional Outlook (Revenue, USD Billion, 2018 - 2030)

North America

US

Canada

Mexico

Europe

Germany

UK

France

Asia Pacific

China

India

Japan

South Korea

Australia

Latin America

Brazil

Middle East & Africa

A.E

Saudi Arabia

South Africa

Curious about the Enterprise Data Management Market? Get a FREE sample copy of the full report and gain valuable insights.

Key Enterprise Data Management Company Insights

Key players operating in the market include Amazon.com, Inc. (Amazon Web Services, Inc.), Broadcom, Cloudera, Inc., Informatica Inc., International Business Machines Corporation, LTIMindtree Limited, Open Text, Oracle, SAP SE, and Teradata. Companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

In June 2024, International Business Machines Corporation and Telefónica Tech, a digital transformation company, announced a new collaboration agreement to advance the deployment of analytics, AI, and data governance solutions, addressing the constantly evolving needs of enterprises. Initially focused on Spain, the agreement would establish a collaborative framework between the two companies, aimed at assisting customers in managing the complexities of new technologies in a diverse and dynamic environment and maximizing the value of these technologies in their business processes.

In March 2024, Cloudera, Inc. unveiled enhancements to its open data lakehouse on the private cloud, aimed at transforming on-premises data capabilities for scalable analytics and AI with enhanced trust. The latest updates would make Cloudera, Inc. the sole provider of an open data lakehouse featuring Apache Iceberg for both private and public cloud environments. The enhancements would enable customers to harness the full AI potential of their enterprise data.

Key Enterprise Data Management Companies:

The following are the leading companies in the enterprise data management market. These companies collectively hold the largest market share and dictate industry trends.

Amazon.com, Inc. (Amazon Web Services, Inc.)

Broadcom

Cloudera, Inc.

Informatica Inc.

International Business Machines Corporation

LTIMindtree Limited

Open Text

Oracle

SAP SE

Teradata

Order a free sample PDF of the Market Intelligence Study, published by Grand View Research.

0 notes

Text

Internet of Things Market (2025 – 2030)

Internet of Things Market (2025 – 2030)

The Internet of Things (IoT) Market was valued at USD 308.97 billion in 2024 and is projected to reach a market size of USD 996.90 billion by 2030. Over the forecast period of 2025-2030, the market is expected to grow at a CAGR of 26.4%.

Market Size and Overview:

The Internet of Things (IoT) refers to a network of physical objects—"things"—embedded with sensors, software, and other technologies that connect to and exchange data with other devices and systems over the Internet or other communications networks. These connected devices collect and transmit data, which can then be analysed to optimize processes, predict maintenance needs, enhance user experiences, or provide valuable insights. The true power of IoT comes from the combination of these interconnected devices, their data collection capabilities, and the analytics that transform raw data into actionable information. The Global Internet of Things (IoT) Market is experiencing exponential growth due to increasing connectivity, cloud computing advancements, and widespread sensor adoption. As per industry reports, the number of IoT-connected devices is expected to exceed 30 billion by 2030. The industrial IoT segment accounts for a significant market share, driven by smart manufacturing and automation solutions. Governments worldwide are also pushing smart city projects, further accelerating IoT adoption. Additionally, edge computing is transforming data processing by reducing latency and enhancing security.

👉 Request Free Sample : https://tinyurl.com/2s36vsdr

Key Market Insights:

The number of IoT-connected devices worldwide is projected to surpass 30 billion by 2030, driven by smart home adoption, industrial automation, and healthcare IoT. Businesses leveraging IoT-enabled predictive maintenance report a 25% reduction in operational costs. 5G and IoT integration are set to revolutionize industries, with 80% of global telecom operators investing in 5 G-powered IoT solutions. By 2026, 90% of new vehicles will be IoT-connected, enhancing safety and autonomous driving.

The Industrial IoT (IIoT) segment is expanding rapidly, with a CAGR of 16%, particularly in manufacturing, energy, and logistics. Smart factories implementing AI-powered IoT report up to 50% reduction in downtime and 30% higher productivity. According to Gartner, 75% of enterprises will adopt IoT-enabled technology, revolutionizing sectors such as healthcare, automotive, and retail.

The global smart home device shipments crossed 1.6 billion units in 2022, led by smart security systems, smart speakers, and connected appliances. The consumer IoT market is expected to grow by 15% annually, as home automation becomes mainstream.

Internet of Things Market Drivers:

An incredible rise in the use of digital and smart devices has placed IOT at the centre of things, There have been various industrial uses for it also which has meant that the demand has increased for devices integrated with this tech.

The explosion of smart devices and the rise in cloud computing are key factors driving IoT expansion. Businesses are leveraging IoT to enhance real-time analytics, automate workflows, and improve customer experiences. Companies like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud are aggressively investing in IoT ecosystems, offering AI-driven analytics and scalable solutions. The shift toward Industry 4.0 has also fuelled demand for sensor-enabled automation and predictive maintenance in sectors such as oil & gas, automotive, and logistics. Additionally, the healthcare industry is embracing IoT-powered wearable devices for real-time patient monitoring, while smart cities are integrating IoT to optimize traffic management, waste collection, and energy usage. With over $150 billion allocated globally for smart infrastructure projects, IoT remains at the core of digital transformation. IoT is also redefining supply chain efficiency. Connected logistics solutions enable real-time tracking, inventory management, and automated restocking. Companies using IoT in supply chain operations report a 20-25% increase in efficiency, reducing waste and optimizing fleet management.

The growth of AI is coinciding with the integration of IOT and the automation materials and technology across industry is seeking to profit majorly from the AI and IOT integration.

The integration of Artificial Intelligence (AI) with IoT is enhancing automation across industries. AI-powered IoT solutions can predict machine failures, optimize energy usage, and improve safety monitoring in high-risk environments. For example, AI-driven IoT sensors in industrial plants can reduce downtime by up to 50% by providing real-time diagnostics. Furthermore, consumer IoT applications continue to expand, with smart home devices becoming mainstream. The popularity of smart assistants like Amazon Alexa, Google Assistant, and Apple Siri has skyrocketed, with over 500 million active users globally. The rapid growth of Artificial Intelligence (AI) is fuelling the expansion of the Internet of Things (IoT) as industries increasingly integrate these technologies to drive automation, efficiency, and cost reduction. AI-powered IoT systems enable real-time data analysis, predictive maintenance, and autonomous decision-making, significantly improving operational workflows across multiple sectors. Smart factories, for instance, are leveraging AI-driven Industrial IoT (IIoT) to optimize production lines, reduce downtime, and enhance safety.

Internet of Things Market Restraints and Challenges:

Safety concerns and cybersecurity threats are the biggest challenges related to IOT.

Security concerns remain a major challenge in IoT adoption. Cybersecurity threats, data breaches, and unauthorized access to IoT networks have raised concerns, leading to stricter compliance regulations such as GDPR and CCPA. According to industry reports, over 60% of IoT devices remain vulnerable to cyberattacks due to outdated security protocols. Interoperability is another hurdle, as IoT ecosystems often use different communication protocols, making integration complex and costly. Additionally, the high initial investment for enterprise-scale IoT implementation deters small and medium-sized businesses from adopting IoT solutions. . These challenges, combined with persistent connectivity issues in rural and developing regions where internet infrastructure remains limited, create significant barriers to achieving the full potential of IoT technologies across global markets.

Internet of Things Market Opportunities:

The IoT market presents substantial growth opportunities, particularly in emerging application areas and previously underserved sectors. Healthcare IoT solutions show remarkable potential, with the remote patient monitoring segment projected to grow at a CAGR of 31.3% through 2030, driven by aging populations and healthcare cost pressures. Smart city initiatives represent another high-growth opportunity, with global investment expected to reach USD 189.5 billion by 2025. These projects encompass traffic management, waste management, and energy conservation solutions that leverage IoT capabilities to enhance urban living quality. Agricultural IoT applications are gaining significant traction, with precision farming technologies demonstrating yield improvements of up to 15% while reducing water usage by 30%. The emergence of IoT-as-a-Service business models has lowered barriers to entry, allowing smaller enterprises to implement solutions without substantial capital expenditure, thus expanding the total addressable market. Strategic partnerships between hardware manufacturers, software developers, and cloud service providers are creating integrated solutions that address complex industry-specific challenges, opening new revenue streams across the IoT ecosystem.

IoT Market Segmentation:

Market Segmentation: By Component:

• Hardware • Software

Hardware components currently dominate the IoT market landscape, accounting for approximately 42.3% of market share in 2022. This segment encompasses sensors, processors, connectivity modules, and other physical elements essential to IoT functionality. The decreasing cost of these components, with sensor prices declining at an average rate of 8-10% annually, has been instrumental in driving widespread adoption across various applications from consumer electronics to industrial equipment. The software and services segment, while representing a smaller share at 38.7% of the market in 2022, is projected to grow at the fastest CAGR of 29.6% through 2030. This growth is fueled by increasing demand for analytics platforms, security solutions, and management systems that enhance the value derived from IoT hardware deployments. Cloud-based IoT platforms alone generated approximately USD 16.9 billion in revenue during 2024, highlighting the critical role of software infrastructure in the IoT ecosystem.

Market Segmentation: By Application:

• Industrial IOT • Commercial/Industrial IOT

The industrial IoT segment accounted for the largest market share at 31.5% in 2022, with manufacturing, energy, and utilities being primary adopters. Smart factories implementing IoT solutions have reported productivity improvements of 20-30% and maintenance cost reductions of up to 25%. The industrial segment's dominance stems from clear ROI metrics, with companies typically recovering implementation costs within 12-18 months through operational efficiencies and reduced downtime. The consumer IoT segment, encompassing smart home devices, wearables, and connected vehicles, represented 28.4% of the market in 2022 but is expected to grow at a CAGR of 28.3% through 2030. This growth is driven by increasing consumer awareness, declining device prices, and improved user interfaces that simplify adoption. Smart home penetration is particularly notable, with approximately 258 million homes worldwide featuring at least one connected device in 2022, a figure projected to exceed 478 million by 2025.

0 notes

Text

Edge Computing Market Resilience and Risk Factors Impacting Growth to 2033

Introduction

Edge computing is rapidly transforming the digital landscape by bringing data processing closer to the source of data generation. Unlike traditional cloud computing, which relies on centralized data centers, edge computing enables real-time data analysis and reduced latency by processing data at the network's edge. This technology is becoming increasingly critical with the rise of Internet of Things (IoT) devices, autonomous vehicles, and real-time analytics. The edge computing market is poised for substantial growth, driven by advancements in 5G technology, increased demand for low-latency applications, and the growing adoption of IoT devices.

Market Overview

The global edge computing market is experiencing robust growth. According to industry reports, the market size was valued at approximately USD 10 billion in 2022 and is expected to reach over USD 60 billion by 2032, growing at a compound annual growth rate (CAGR) of around 20%. The market encompasses hardware, software, and services that facilitate edge data processing and analytics. Key industry players include tech giants such as Amazon Web Services (AWS), Microsoft Azure, Google Cloud, and edge-specific firms like EdgeConneX and Vapor IO.

𝗗𝗼𝘄𝗻𝗹𝗼𝗮𝗱 𝗮 𝗙𝗿𝗲𝗲 𝗦𝗮𝗺𝗽𝗹𝗲 𝗥𝗲𝗽𝗼𝗿𝘁👉https://tinyurl.com/4u5uvp8e

Key Market Drivers

Proliferation of IoT Devices: With billions of connected devices generating vast amounts of data, edge computing offers a solution to handle data locally, reducing bandwidth usage and enhancing response times.

Need for Low Latency: Industries such as autonomous vehicles, healthcare, and gaming require real-time data processing, which edge computing can efficiently provide.

Advancements in 5G Technology: The rollout of 5G networks is a significant enabler for edge computing, offering faster and more reliable connectivity.

Data Privacy and Security: By processing data closer to its source, edge computing enhances data security and compliance, particularly for industries dealing with sensitive information.

Increasing Demand for Smart Applications: The growing use of smart applications in smart cities, industrial automation, and augmented reality (AR) drives the adoption of edge computing.

Industry Trends

1. Hybrid Edge-Cloud Models

Many enterprises are adopting hybrid models that combine edge computing with cloud computing to leverage the best of both technologies. This approach allows critical data to be processed at the edge while less time-sensitive data is sent to the cloud for further analysis.

2. Edge AI (Artificial Intelligence)

Integrating AI at the edge enables devices to make autonomous decisions without the need for cloud-based processing. This trend is particularly beneficial in areas like predictive maintenance and personalized customer experiences.

3. Enhanced Edge Security Solutions

As edge devices are often more vulnerable to cyberattacks, there is a rising demand for robust security solutions. Companies are increasingly investing in edge-specific cybersecurity measures, including encryption, threat detection, and secure access controls.

4. Micro Data Centers

The deployment of micro data centers at the edge is gaining momentum. These small-scale data centers provide localized processing and storage, contributing to faster data processing and improved reliability.

Market Segmentation

1. By Component

Hardware

Software

Services

2. By Application

Industrial IoT

Smart Cities

Healthcare

Retail

Autonomous Vehicles

Gaming

3. By Industry Vertical

Manufacturing

Transportation

Healthcare

Energy & Utilities

Telecommunications

Regional Analysis

The North American region holds the largest share of the edge computing market due to early technology adoption, strong infrastructure, and the presence of key industry players. Europe follows closely, with increasing investments in smart cities and industrial automation. The Asia-Pacific region is expected to exhibit the highest growth rate, driven by advancements in telecommunications and increasing adoption of IoT devices.

Challenges and Opportunities

Challenges:

High initial setup costs

Limited scalability compared to cloud computing

Management complexities of distributed networks

Opportunities:

Expansion of 5G networks

Growth of edge-enabled AI applications

Increasing demand for real-time analytics

Future Outlook

The future of the edge computing market looks promising, with significant potential in sectors such as healthcare, automotive, and industrial IoT. As edge computing technology matures, it is expected to play a critical role in emerging technologies such as the metaverse and Industry 4.0.

Conclusion

Edge computing is reshaping how data is processed and analyzed, offering significant advantages in terms of speed, efficiency, and security. With its rapid adoption across various industries, the edge computing market is set to witness remarkable growth in the coming decade. As businesses and technology providers continue to innovate, edge computing will remain at the forefront of digital transformation strategies, driving advancements in smart applications, real-time analytics, and data-driven decision-making.

Read Full Report:-https://www.uniprismmarketresearch.com/verticals/information-communication-technology/edge-computing

0 notes

Text

North America Edge Computing Market Trends, Competitive Landscape, Size 2028

The North America Edge Computing Market is expected to grow from US$ 16,212.71 million in 2022 to US$ 52,976.45 million by 2028. It is estimated to grow at a CAGR of 21.8% from 2022 to 2028.

North America Edge Computing Market Segmentation

The North America edge computing market is segmented into component, applications, enterprise size, verticals, and country.

Based on component, the North America edge computing market is segmented into hardware, software, and services. The hardware segment registered the largest market share in 2022.

Based on organization Size, the North America edge computing market is segmented into SMEs and large enterprises. The large enterprises segment held a larger market share in 2022.

Based on application, the North America edge computing market is segmented into smart cities, industrial internet of things (IIOT), remote monitoring, content delivery, augmented reality and virtual reality, and others. The smart cities segment held the largest market share in 2022.

Based on verticals, the North America edge computing market is segmented into manufacturing, energy and utilities, government, IT and telecom, retail and consumer goods, transportation and logistics, healthcare, and others. The IT and telecom segment held the largest North America edge computing market share in 2022.

Based on country, the North America edge computing market has been categorized into the US, Canada, and Mexico. The US dominated the North America edge computing market in 2022.

Get Sample PDF of this Report @

https://www.businessmarketinsights.com/sample/BMIRE00028905

Market Overview

The U.S., Canada, and Mexico are the major economies driving the market. The region's growth is fueled by several key factors, including the availability of high-speed connectivity, increased adoption of cloud technologies, a surge in connected devices propelling the Internet of Things (IoT), and the rapid emergence of 5G technology. The impact of deploying sensors and leveraging data for actionable insights varies depending on specific use cases. According to the IoT—Spring 2022 report released in May 2022, the IoT market is expected to grow by 18%, reaching 14.4 million active connections. Furthermore, the number of connected IoT devices is projected to reach 27 million by 2025. As the number of IoT devices continues to rise, the adoption of edge computing solutions is anticipated to grow significantly across North America in the coming years, positioning the region for continued expansion in this dynamic market.

North America Edge Computing Report Scope

Report Attribute Details

Market size in 2022 US$ 16,212.71 Million

Market Size by 2028 US$ 52,976.45 Million

Global CAGR (2022 - 2028) 21.8%

Historical Data 2020-2021

Forecast period 2023-2028

Segments Covered

By Component

Hardware

Software

Services

By Application

Smart Cities

Industrial Internet of Things

Remote Monitoring

Content Delivery

Augmented Reality and Virtual Reality

By Enterprise Size

SMEs and Large Enterprises

By Verticals

Manufacturing

Energy and Utilities

Government

IT and Telecom

Retail and Consumer Goods

Transportation and Logistics

Healthcare

About Us:

Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications

#North America Edge Computing Market#North America Edge Computing Market size#North America Edge Computing Market Trend

0 notes

Text

Exploring the Growth of Artificial Intelligence Market: What You Need to Know

The global artificial intelligence (AI) market is projected to reach USD 1,811.75 billion by 2030, according to a recent report by Grand View Research, Inc. The market is expected to grow at a compound annual growth rate (CAGR) of 36.6% from 2024 to 2030. AI refers to the development of computing systems capable of performing tasks that typically require human involvement, such as decision-making, speech recognition, visual perception, and language translation. AI relies on algorithms to interpret human speech, recognize visual objects, and process information, with these algorithms playing key roles in data processing, calculations, and automated reasoning. Since traditional algorithms often have limitations in terms of accuracy and efficiency, AI researchers continually work to enhance these algorithms across various domains.

This ongoing advancement has led manufacturers and technology developers to concentrate on creating more standardized AI algorithms. In fact, there have been notable innovations in AI algorithms recently. For example, in May 2020, International Business Machines Corporation (IBM) launched a range of AI-powered services, including IBM Watson AIOps, which are designed to assist with automating IT infrastructures, making them more resilient and cost-effective.

Numerous companies are adopting AI-driven solutions like Robotic Process Automation (RPA) to streamline their workflows and automate repetitive tasks. Additionally, AI is being integrated with the Internet of Things (IoT) to enhance the outcomes of various business processes. A notable instance is Microsoft's investment of USD 1 billion in OpenAI, a San Francisco-based company, with the aim of developing AI supercomputing technology on Microsoft's Azure cloud platform.

Gather more insights about the market drivers, restrains and growth of the Artificial Intelligence Market

Key Highlights from the Artificial Intelligence Market Report:

• The rapid rise of big data is expected to contribute significantly to the growth of the AI market, as there is an increasing need to capture, store, and analyze large volumes of data.

• Growing demand for image processing and identification is anticipated to accelerate industry expansion.

• AI's ability to analyze vast amounts of data and detect patterns or anomalies makes it an effective tool for identifying potential cyberattacks, enabling quicker and more accurate threat detection, which in turn promotes AI adoption in cybersecurity applications.

• The use of AI in predictive maintenance, process automation, and supply chain optimization is helping businesses streamline operations, reduce costs, and ensure the efficient delivery of their products and services.

• North America led the market in 2022, accounting for over 36.8% of global revenue.

• However, a key challenge hindering industry growth is the need for vast amounts of data to train AI systems, particularly for tasks like character and image recognition.

Browse through Grand View Research's Next Generation Technologies Industry Research Reports.

• Edge AI Market: The global edge AI market size was estimated at USD 20.78 billion in 2024 and is anticipated to grow at a CAGR of 21.7% from 2025 to 2030.

• IoT Devices Market: The global IoT devices market size was estimated at USD 70.28 billion in 2024 and is expected to grow at a CAGR of 16.8% from 2025 to 2030.

Artificial Intelligence Market Segmentation

Grand View Research has segmented the global artificial intelligence market based on solution, technology, function, end-use, and region:

Artificial Intelligence Solution Outlook (Revenue, USD Billion, 2017 - 2030)

• Hardware

o Accelerators

o Processors

o Memory

o Network

• Software

• Services

o Professional

o Managed

Artificial Intelligence Technology Outlook (Revenue, USD Billion, 2017 - 2030)

• Deep Learning

• Machine Learning

• Natural Language Processing (NLP)

• Machine Vision

• Generative AI

Artificial Intelligence Function Outlook (Revenue, USD Billion, 2017 - 2030)

• Cybersecurity

• Finance and Accounting

• Human Resource Management

• Legal and Compliance

• Operations

• Sales and Marketing

• Supply Chain Management

Artificial Intelligence End-use Outlook (Revenue, USD Billion, 2017 - 2030)

• Healthcare

o Robot Assisted Surgery

o Virtual Nursing Assistants

o Hospital Workflow Management

o Dosage Error Reduction

o Clinical Trial Participant Identifier

o Preliminary Diagnosis

o Automated Image Diagnosis

• BFSI

o Risk Assessment

o Financial Analysis/Research

o Investment/Portfolio Management

o Others

• Law

• Retail

• Advertising & Media

• Automotive & Transportation

• Agriculture

• Manufacturing

• Others

Artificial Intelligence Regional Outlook (Revenue, USD Billion, 2017 - 2030)

• North America

o U.S.

o Canada

• Europe

o U.K.

o Germany

o France

• Asia Pacific

o China

o Japan

o India

o South Korea

o Australia

• Latin America

o Brazil

o Mexico

• Middle East and Africa (MEA)

o KSA

o UAE

o South Africa

List of Key Players in the Artificial Intelligence Market

• Advanced Micro Devices

• AiCure

• Arm Limited

• Atomwise, Inc.

• Ayasdi AI LLC

• Baidu, Inc.

• Clarifai, Inc.

• Cyrcadia Health

• Enlitic, Inc.

• Google LLC

• H2O.ai.

• HyperVerge, Inc.

• International Business Machines Corporation

• IBM Watson Health

• Intel Corporation

• Iris.ai AS.

• Lifegraph

• Microsoft

• NVIDIA Corporation

• Sensely, Inc.

• Zebra Medical Vision, Inc.

Order a free sample PDF of the Artificial Intelligence Market Intelligence Study, published by Grand View Research.

#Artificial Intelligence Market#Artificial Intelligence Market Analysis#Artificial Intelligence Market Report#Artificial Intelligence Market Size#Artificial Intelligence Market Share

0 notes

Text

Streaming Analytics Market: Unprecedented Growth Projected, Aiming for USD 107,548.7 Million by 2033

The global market for streaming analytics market is anticipated to increase at a CAGR of 21.1% from US$ 15,811.3 million in 2023 to US$ 107,548.7 Million by 2033. Nearly 40% of the worldwide data analytics industry was accounted for by the market for streaming analytics.

Massive amounts of data are being generated as a result of the widespread use of industrial 4.0 techniques, which is also expected to raise the potential for real-time analytics adoption throughout the projected period.

Streaming analytics technology is being used by businesses to develop new business channels and boost customer engagement. As a result, stream analytics are growing in popularity in sectors like BFSI, supply chain management, and advertising & marketing. This will likely have a positive impact on the market for streaming analytics.

Businesses are beginning to focus more intently on gathering data on streaming events. Rapid response to events encourages operational responsiveness and organizational effectiveness. Businesses that use streaming analytics software can apply important context to events as they happen.

Implementing streaming analytics will improve operational effectiveness, reduce infrastructure costs, and speed up the delivery of information and results. Organizations of all sizes can access data streaming through apps, social media, sensors, gadgets, websites, and other sources. Real-time analysis can provide essential, useful insights in a range of operational and functional domains, as opposed to storing and analyzing data later.

Key Takeaways from the Streaming Analytics Market Report:

The Streaming Analytics Market Report highlights several significant trends. The streaming analytics platform emerges as a key solution, projected to lead in global demand with a robust 22.5% CAGR. Cloud-based platforms dominate, commanding a substantial 53.4% market share in 2022, followed closely by hybrid solutions. Managed services are poised for substantial growth, expected to expand by 2.9X by the end of the forecast period, while advertising & marketing initially hold the highest market share, supply chain management is forecasted to experience the highest CAGR. Among industries, IT & telecom lead with a remarkable 25.8% CAGR, closely followed by retail & e-commerce. North America spearheads the market, trailed by Europe, while South Asia & Pacific emerge as the fastest-growing region. Notably, East Asia presents a significant absolute opportunity of US $12,612.7 Million in the forecast period, indicative of the market’s global dynamism and potential for growth.

Leading Key Players:

In the competitive landscape of the streaming analytics market, prominent players such as Oracle Corporation, IBM Corporation, Google, Microsoft Corporation, SAS, SAP, Amazon Web Services, TIBCO, Software AG, Cloudera, Apache Software Foundation, Guavas, Adobe, Altair, Quix, Striim Inc., and Confluent lead the industry with their innovative solutions and robust platforms, driving advancements in real-time data processing and insights generation.

Key Trends:

The Streaming Analytics Market is witnessing a seismic shift driven by several key trends. Firstly, there’s a growing demand for instant insights fueled by the explosion of data from diverse sources such as IoT devices, social media, and sensors. Businesses are increasingly recognizing the need to swiftly analyze this torrent of data to make timely decisions. Moreover, advancements in technologies like artificial intelligence and machine learning are empowering streaming analytics platforms to deliver more accurate and actionable insights in real-time. Additionally, the rise of edge computing is enabling organizations to analyze data closer to its source, reducing latency and enhancing operational efficiency.

Regional Analysis:

The adoption of streaming analytics solutions varies across different regions, influenced by factors such as technological infrastructure, regulatory environment, and market maturity. North America leads the global Streaming Analytics Market, driven by the presence of tech giants, robust IT infrastructure, and a strong culture of innovation. Meanwhile, Asia Pacific is emerging as a hotbed for streaming analytics adoption, propelled by rapid digital transformation and the proliferation of mobile devices. Europe follows suit, with industries like manufacturing, finance, and healthcare increasingly leveraging streaming analytics to gain a competitive edge.

Key Players in the Global Streaming Analytics Market

Oracle Corporation

IBM Corporation

Google

Microsoft Corporation

SAS

SAP

Amazon Web Services

TIBCO

Software AG

Cloudera

Apache Software Foundation

Guavas

Adobe

Altair

Quix

Striim, Inc.

Confluent

Streaming Analytics Market Segmentation

By Solution:

Platform

Cloud-based

On-premises

Hybrid

Services

Managed Services

Professional Services

Consulting Services

Integration & Implementation

Support & Maintenance

By Application:

Advertising & Marketing

Financial Analytics

Supply Chain Management

Demographic Location Intelligence

Fraud Intelligence

Customer Experience Monitoring

Others

By Enterprise Size:

Large Enterprises

Small & Medium Enterprises (SMEs)

By Industry:

IT & Telecom

Media and Entertainment

Retail & E-commerce

Manufacturing

Banking, Financial Services, and Insurance (BFSI)

Healthcare

Government

Education

Others

By Region:

North America

Latin America

Europe

East Asia

South Asia & Pacific

Middle East & Africa (MEA)

0 notes

Text

The Middle East & Africa IOT Market Size, Share | CAGR 27.5% During 2025-2032

The Middle East & Africa (MEA) stands as the second largest region in the global Internet of Things (IoT) market industry. With increasing investments in smart infrastructure, digital transformation, and connectivity initiatives, the region is poised for strong growth. The global IoT market size is projected to expand from USD 544.38 billion in 2022 to USD 3,352.97 billion by 2030, at a CAGR of 27.5% during the forecast period.

Market Highlights: • CAGR: 27.5% (2023–2030) • Market Size (Global): USD 544.38 billion (2022) → USD 3,352.97 billion (2030) • Regional Focus: Infrastructure modernization, industrial IoT, and smart city deployments across the Gulf Cooperation Council (GCC), South Africa, and North Africa.

Major Companies Active in the Region: • Etisalat Group • MTN Group • SAP MENA • Cisco Systems, Inc. • Huawei Technologies Co., Ltd. • Ericsson • IBM Corporation • GE Digital • Siemens AG • Microsoft Corporation

Request for Free Sample Reports: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/middle-east-africa-internet-of-things-iot-market-107394

Market Trends:• Adoption of IoT in oil & gas for real-time pipeline monitoring and predictive maintenance. • Smart city investments driven by UAE, Saudi Arabia, and South Africa. • Increased government funding for digital infrastructure and AI+IoT integration. • Growing emphasis on cybersecurity for connected systems.

Key Developments: August 2022 – Etisalat partnered with regional governments to expand its Smart City IoT offerings across the UAE, introducing connected street lighting and waste management systems.

November 2022 – MTN Group rolled out its pan-African IoT platform aimed at unifying connectivity and services for smart logistics and manufacturing in Sub-Saharan Africa.

Core Segments: • Components: Sensors and devices, connectivity modules, IoT platforms, and analytics software. • Connectivity: NB-IoT, LTE-M, 5G, Zigbee, LoRa, and satellite. • Deployment Types: Cloud-native, edge computing, and on-premises models. • Applications: Smart cities, oil & gas monitoring, connected healthcare, fleet management, agriculture, and utilities. • Key Stakeholders: Government agencies, telecom operators, energy firms, logistics providers, and enterprise IT leaders

Speak to Analyst: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/middle-east-africa-internet-of-things-iot-market-107394

About Us: At Fortune Business Insights, we empower businesses to thrive in rapidly evolving markets. Our comprehensive research solutions, customized services, and forward-thinking insights support organizations in overcoming disruption and unlocking transformational growth. With deep industry focus, robust methodologies, and extensive global coverage, we deliver actionable market intelligence that drives strategic decision-making. Whether through syndicated reports, bespoke research, or hands-on consulting, our result-oriented team partners with clients to uncover opportunities and build the businesses of tomorrow. We go beyond data offering clarity, confidence, and competitive edge in a complex world.

Contact Us: US: +1 833 909 2966 UK: +44 808 502 0280 APAC: +91 744 740 1245 Email: [email protected]

#Middle East & Africa Internet of Things Market Share#Middle East & Africa Internet of Things Market Size#Middle East & Africa Internet of Things Market Industry#Middle East & Africa Internet of Things Market Driver#Middle East & Africa Internet of Things Market Growth#Middle East & Africa Internet of Things Market Analysis#Middle East & Africa Internet of Things Market Trends

0 notes

Text

Beyond Connectivity: Emerging Applications of Multi-Mode Chipsets

The global multi-mode chipset market, valued at USD 5.8 billion in 2022, is projected to surge to USD 17.2 billion by the end of 2031, advancing at a robust compound annual growth rate (CAGR) of 13.0% from 2023 through 2031. This comprehensive report examines market drivers, technological trends, leading players, and regional dynamics shaping the future of multi-mode chipsets, which integrate multiple wireless communication standards Wi-Fi, Bluetooth, 3G, 4G, and 5G into a single silicon solution.

Market Overview

Multi-mode chipsets serve as the backbone of modern connected devices, enabling seamless handoffs between various wireless networks to maintain uninterrupted high-speed data delivery. In 2022, increasing smartphone penetration and the rollout of early 5G networks propelled market value to US$ 5.8 billion. With network operators worldwide accelerating 5G deployments, chipset vendors are responding with advanced solutions optimized for power efficiency, spectral flexibility, and backward compatibility with legacy 2G–4G standards.

Market Drivers & Trends

Adoption of 5G Devices • The global uptake of 5G-capable devices is a primary growth engine. Consumers and enterprises demand faster download/upload speeds, ultra-low latency, and greater network capacity. Multi-mode chipsets that support both 5G and previous generations ensure broad device interoperability and extend product lifecycles.

R&D of New Products • Continuous investment in chipset innovation—across baseband units, RF front-ends, and integrated SoCs—fuels incremental improvements in throughput and energy consumption. Initiatives such as Samsung’s third-gen mmWave RFICs and second-gen 5G modems exemplify the push toward higher integration and performance.

Edge Computing & IoT Integration • The emergence of edge-computing architectures and proliferation of IoT endpoints (smart homes, industrial sensors, autonomous vehicles) require versatile connectivity modules. Multi-mode chipsets are becoming integral to IoT gateways and edge nodes, balancing cost, performance, and simultaneous multi-network access.

Regulatory & Spectrum Allocations • Governments in regions like North America and Europe are reopening legacy spectrum bands for private LTE and 5G deployments. This regulatory momentum encourages chipset suppliers to develop solutions tailored for industrial and enterprise private networks.

Latest Market Trends

Dual-Connectivity Solutions: Chipset architectures now natively support 5G NSA (Non-Standalone) and SA (Standalone) modes alongside LTE, enabling smoother network migrations.

Power-Optimized Designs: Low-power operation is critical for battery-constrained wearables and industrial sensors; advanced power-gating and dynamic clocking techniques are being integrated into new models.

Software-Defined Radio (SDR) Features: Some multi-mode chipsets incorporate programmable blocks, allowing firmware updates to support new spectrum bands and protocols without hardware revisions.

Miniaturization: More compact chip packages facilitate integration into ultra-small form factors, from wireless earbuds to drones.

Gain a preview of important insights from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=46704

Key Players and Industry Leaders

The competitive landscape is dominated by a handful of semiconductor giants and specialized communication chipset firms:

HiSilicon Technologies

Intel Corporation

Qualcomm Technologies Inc.

Samsung Group

MediaTek

Spreadtrum Communications

Marvell Technology Group

Altair Semiconductor, Inc.

Broadcom Corporation

GCT Semiconductor Inc.

Recent Developments

VeriSilicon & Innobase Partnership (Feb 2024): Launched a 5G RedCap/4G LTE dual-mode modem targeting cost-sensitive IoT segments.

Qualcomm Snapdragon Summit (Oct 2023): Announced two AI-enabled chips designed to offload generative AI workloads on mobile and PC platforms.

BSNL & Echelon Edge Collaboration (Jan 2023): Deployed private LTE/5G networks for enterprise customers in India, demonstrating growing demand for bespoke private networks.

Samsung 5G SoC Launch (June 2021): Introduced a line of baseband units, compact macro units, and massive MIMO with integrated third-gen mmWave RFIC.

Market Opportunities

Private Network Solutions – Enterprises across manufacturing, logistics, and mining seek private 5G/LTE networks for secure, low-latency connectivity, creating demand for specialized multi-mode modems.

Automotive & Transportation – Vehicle-to-everything (V2X) communication systems require multi-mode support for both cellular and dedicated short-range communication (DSRC).

Healthcare & Wearables – The telemedicine boom drives the need for wearable devices that seamlessly switch between Wi-Fi, Bluetooth, and cellular networks.

Rural Connectivity – Cost-effective 4G/5G solutions can bridge digital divides in emerging markets, where legacy networks remain prevalent.

Future Outlook

By 2031, the global multi-mode chipset market is forecast to reach US$ 17.2 billion. Key growth catalysts include the maturation of 5G SA networks, expansion of AI-driven edge-computing applications, and continued convergence of wireless standards. Chipset vendors that invest in highly integrated, software-upgradable designs will capture the largest share, while niche players focused on IoT and private network solutions will benefit from specialized verticals.

Market Segmentation

The report segments the global market by:

Application: Smartphones; Tablets; Wearable Devices; Others (automotive, industrial, healthcare)

End-User Vertical: Consumer Electronics; Automotive & Transportation; Industrial; Healthcare; Others

Component: Baseband Processors; RF Front-Ends; Antenna Switches; Others

Regional Insights

North America: Holds the largest market share (2022) driven by rapid urbanization, strong 5G rollout (e.g., U.S. National Telecommunications and Information Administration’s 5G strategy in 2020), and home to key chipset developers.

Asia Pacific: Fastest growing owing to high smartphone adoption in China and India, aggressive 5G infrastructure investments in South Korea and Japan, and burgeoning IoT deployments.

Europe: Steady growth supported by private 5G initiatives in Germany and U.K., and stringent automotive communication standards.

Rest of World: Latin America and Middle East & Africa present gradual uptake, with governments planning spectrum auctions and encouraging digital transformation.

Frequently Asked Questions

What is a multi-mode chipset? A multi-mode chipset is an integrated circuit that supports multiple wireless communication standards such as Wi-Fi, Bluetooth, 3G, 4G, and 5G on a single chip, enabling devices to switch seamlessly between networks.

Why is the CAGR projected at 13.0%? Strong 5G network rollouts, increasing smartphone penetration, and growing demand for IoT and industrial applications drive sustained market growth at a 13.0% CAGR from 2023 to 2031.

Which region leads the market? North America dominated in 2022, owing to early 5G deployments, presence of leading semiconductor companies, and government support for spectrum reallocation.

Who are the major players? Qualcomm, Intel, MediaTek, Samsung, and Broadcom lead the landscape, with several regional specialists competing in niche IoT and private network segments.

How does this report help enterprises? It equips businesses with actionable insights into market trends, growth opportunities, competitor strategies, and technological roadmaps, supporting informed decision-making for product development and investments.

Explore Latest Research Reports by Transparency Market Research:

Photoionization Detection (PID) Gas Analyzer Market: https://www.transparencymarketresearch.com/photoionization-detection-gas-analyzer-market.html

Haptic Technology Market: https://www.transparencymarketresearch.com/haptic-technology-market.html

Silicon on Insulator (SOI) Market: https://www.transparencymarketresearch.com/silicon-insulator-market.html

Broadcast Equipment Market: https://www.transparencymarketresearch.com/broadcast-equipment-market.html

About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

Global Observability Tools and Platforms Market Analysis 2024: Size Forecast and Growth Prospects

The observability tools and platforms global market report 2024 from The Business Research Company provides comprehensive market statistics, including global market size, regional shares, competitor market share, detailed segments, trends, and opportunities. This report offers an in-depth analysis of current and future industry scenarios, delivering a complete perspective for thriving in the industrial automation software market.

Observability Tools and Platforms Market, 2024 report by The Business Research Company offers comprehensive insights into the current state of the market and highlights future growth opportunities.

Market Size - The observatory tools and platforms market size has grown rapidly in recent years. It will grow from $2.54 billion in 2023 to $2.85 billion in 2024 at a compound annual growth rate (CAGR) of 12.3%. The growth in the historic period can be attributed to regulatory compliance, aging infrastructure, increased complexity of operations, focus on operational efficiency, growing awareness of predictive maintenance.

The observatory tools and platforms market size is expected to see rapid growth in the next few years. It will grow to $4.43 billion in 2028 at a compound annual growth rate (CAGR) of 11.6%. The growth in the forecast period can be attributed to industry 4.0 integration, sustainability and environmental concerns, globalization of supply chains, rise of performance-based contracts, increased emphasis on data-driven decision-making. Major trends in the forecast period include edge computing integration, artificial intelligence and machine learning adoption, blockchain for asset management, augmented reality (AR) for maintenance support, subscription-based and cloud solutions.

Order your report now for swift delivery @ https://www.thebusinessresearchcompany.com/report/observability-tools-and-platforms-global-market-report

Scope Of Observability Tools and Platforms Market The Business Research Company's reports encompass a wide range of information, including:

1. Market Size (Historic and Forecast): Analysis of the market's historical performance and projections for future growth.

2. Drivers: Examination of the key factors propelling market growth.

3. Trends: Identification of emerging trends and patterns shaping the market landscape.

4. Key Segments: Breakdown of the market into its primary segments and their respective performance.

5. Focus Regions and Geographies: Insight into the most critical regions and geographical areas influencing the market.

6. Macro Economic Factors: Assessment of broader economic elements impacting the market.

Observability Tools and Platforms Market Overview

Market Drivers - The increasing adoption of IoT is expected to propel the growth of the observability tools and platforms market going forward. Internet of Things (IoT) encompasses a network of interlinked physical devices, vehicles, appliances, and other objects equipped with sensors, software, and connectivity, facilitating the gathering and sharing of data. and network connectivity, enabling them to collect and exchange data. The advancements in areas such as artificial intelligence (AI) and machine learning (ML) are enabling deeper analysis of IoT data and unlocking new applications. Observability tools and platforms enable the collection, analysis, and visualization of vast amounts of data generated by IoT devices, aiding operators and developers in understanding system performance, identifying anomalies, and optimizing operations. For instance, in November 2022, according to a report published by Ericsson, a Sweden-based telecommunication company, broadband IoT (4G/5G), the primary connectivity for most cellular IoT devices, achieved 1.3 billion connections in 2022 and nearly 60% of cellular IoT connections are projected to be broadband IoT connections by 2026, predominantly using 4G. Further, Northeast Asia currently leads in cellular IoT connections and is expected to exceed 2 billion connections in 2023. Therefore, the increasing adoption of IoT is driving the growth of the observability tools and platforms market

Market Trends - Major companies operating in the observability tools and platforms market are developing advanced technologies, such as artificial intelligence (AI)-powered observability assistants, to gain a competitive edge in the market. These solutions utilize artificial intelligence techniques to collect, analyze, and interpret telemetry data such as logs, metrics, and traces within a software system. For instance, in May 2023, New Relic, a US-based software development company, launched relic grok, an AI-powered observability assistant. It is uniquely designed by leveraging generative AI and openAI's language models, to simplify observability for engineers. The users can interact in natural language to set up instrumentation, troubleshoot issues, generate reports, and manage accounts. Grok performs AI-driven root cause analysis, assists with code-level issue resolution, and automates reporting to support multiple languages and handle administrative tasks.

The observability tools and platforms market covered in this report is segmented –

1) By Component: Solution, Services 2) By Deployment Type: Public Cloud, Private Cloud 3) By End User: Banking, Financial Services And Insurance, Healthcare And Life Sciences, Retail And E-commerce, Manufacturing, Telecom And Information Technology, Government And Public Sector, Media And Entertainment, Other End Users

Get an inside scoop of the observability tools and platforms market, Request now for Sample Report @ https://www.thebusinessresearchcompany.com/sample.aspx?id=13890&type=smp

Regional Insights - North America was the largest region in the observatory tools and platforms market in 2023. The regions covered in the observability tools and platforms market report are Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East, Africa.

Key Companies - Microsoft Corporation, International Business Machines Corporation (IBM), Broadcom Inc., Splunk Inc., Datadog Inc., ScienceLogic, Inc., Dynatrace Inc., Elastic N.V., New Relic Inc., SolarWinds Worldwide, LLC, Riverbed Technology LLC, Sumo Logic Inc., GitLab Inc., Nexthink S.A., Grafana Labs, AppDynamics LLC, LogicMonitor Inc., Auvik Networks Inc., Monte Carlo Data Inc., Honeycomb.io Inc., Graylog Inc., Sysdig Inc., Raygun Inc., Acceldata Inc., Lightstep Inc., StackState B.V., Instana Inc.

Table of Contents 1. Executive Summary 2. Observability Tools and Platforms Market Report Structure 3. Observability Tools and Platforms Market Trends And Strategies 4. Observability Tools and Platforms Market – Macro Economic Scenario 5. Observability Tools and Platforms Market Size And Growth ….. 27. Observability Tools and Platforms Market Competitor Landscape And Company Profiles 28. Key Mergers And Acquisitions 29. Future Outlook and Potential Analysis 30. Appendix

Contact Us: The Business Research Company Europe: +44 207 1930 708 Asia: +91 88972 63534 Americas: +1 315 623 0293 Email: [email protected]

Follow Us On: LinkedIn: https://in.linkedin.com/company/the-business-research-company Twitter: https://twitter.com/tbrc_info Facebook: https://www.facebook.com/TheBusinessResearchCompany YouTube: https://www.youtube.com/channel/UC24_fI0rV8cR5DxlCpgmyFQ Blog: https://blog.tbrc.info/ Healthcare Blog: https://healthcareresearchreports.com/ Global Market Model: https://www.thebusinessresearchcompany.com/global-market-model

0 notes

Text