#IoT-Asset Tracking Monitoring Market Share

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

There are dozens of funny blogs to kill time on Tumblr.

Text

IoT-based Asset Tracking and Monitoring Market Size in the Asia Pacific Region

In recent years, the Asia Pacific region has emerged as a key player in the global landscape of IoT-based asset tracking and monitoring solutions. With rapid urbanization, industrialization, and the proliferation of smart technologies, businesses and organizations across the region are increasingly turning to IoT solutions to optimize asset management, enhance operational efficiency, and improve productivity. As a result, the market for IoT-based asset tracking and monitoring in the Asia Pacific region is witnessing significant growth and evolution.

Download PDF Brochure:

Market Size and Growth: The Asia Pacific region is experiencing robust growth in the IoT-based asset tracking and monitoring market, driven by factors such as the expanding industrial and logistics sectors, increasing adoption of IoT technologies, and government initiatives promoting digitalization and smart infrastructure. According to market research reports, the IoT-based asset tracking and monitoring market in the Asia Pacific region is projected to reach a valuation of USD 9.2 billion by 2029 by 2029, growing at a 12.8% CAGR during the forecast period.

Key Drivers: Several factors contribute to the growth of the IoT-based asset tracking and monitoring market size in the Asia Pacific region. These include:

Rising Demand for Supply Chain Optimization: With the Asia Pacific region serving as a global hub for manufacturing and trade, there is a growing need for efficient supply chain management solutions. IoT-based asset tracking and monitoring technologies enable real-time visibility into the movement and status of assets, helping businesses streamline logistics operations, minimize delays, and reduce costs.

Focus on Fleet Management: The Asia Pacific region is home to a vast network of transportation and logistics companies, which rely heavily on fleet management solutions to ensure the timely and secure delivery of goods. IoT-based asset tracking and monitoring systems empower fleet operators to track vehicles, monitor driver behavior, optimize routes, and improve overall fleet efficiency.

Expansion of Smart Cities Initiatives: Many countries in the Asia Pacific region are investing in smart cities initiatives aimed at enhancing urban infrastructure, transportation systems, and public services. IoT-based asset tracking and monitoring solutions play a crucial role in these initiatives by enabling efficient management of city assets such as streetlights, waste bins, public transportation, and utilities.

Advancements in IoT Technology: Technological advancements in IoT sensors, connectivity, and data analytics are driving innovation in the field of asset tracking and monitoring. With the advent of low-power wide-area networks (LPWANs) and advancements in RFID and GPS technologies, IoT-based asset tracking solutions have become more affordable, scalable, and reliable, fueling market growth.

Market Dynamics: The IoT-based asset tracking and monitoring market in the Asia Pacific region is characterized by intense competition, rapid technological innovation, and evolving customer demands. Key market players are focusing on product innovation, strategic partnerships, and geographic expansion to gain a competitive edge in the market. Additionally, regulatory initiatives and industry standards are shaping the market landscape and influencing the adoption of IoT solutions across different sectors.

Future Outlook: Looking ahead, the future of the IoT-based asset tracking and monitoring market in the Asia Pacific region appears promising. As businesses and governments continue to prioritize digitalization and invest in IoT infrastructure, the demand for asset tracking and monitoring solutions is expected to grow. Moreover, the integration of IoT with emerging technologies such as artificial intelligence (AI), blockchain, and edge computing is likely to unlock new opportunities and use cases, further driving market expansion.

0 notes

Text

Luxembourg-based satellite telecom operator OQ Technology is testing investor appetite for space-based Internet of Things (IoT) technology, seeking EUR 30 million in fresh funding as competition intensifies in the nascent market for satellite-enabled device connectivity.

The company, which has deployed 10 satellites since 2019, plans to launch 20 more as larger telecommunications companies and satellite operators begin developing similar IoT services. The Series B funding round follows a EUR 13 million raise in 2022 and aims to strengthen its global 5G IoT network coverage.

OQ Technology has secured initial backing through a convertible loan from the Luxembourg Space Sector Development Fund, a joint initiative between SES S.A. and the Luxembourg government. Previous investors, including Aramco's venture capital arm Wa'ed Ventures and Greece's Phaistos Investment Fund, are participating in the new round.

The startup differentiates itself by focusing on standardized cellular technology for narrowband-IoT, contributing to 3GPP protocols that allow existing cellular chips to connect with satellites. This approach contrasts with proprietary systems offered by competitors, replacing traditional bulky satellite systems with compact, cost-efficient IoT modems that offer plug-and-play functionality.

"The satellite IoT sector is still largely in the proof-of-concept phase," says the company representative. "While there's significant potential, companies face challenges in standardization and convincing industries to adopt these new technologies at scale."

In an effort to secure its supply chain, the company is exploring partnerships in Taiwan's semiconductor industry. It has begun collaborating with the Industrial Technology Research Institute (ITRI), though these relationships are still in the early stages. The company has shipped initial terminals to prospective Taiwanese clients, marking its first steps in the Asian market.

The global reach for semiconductor partnerships comes as the company expands its geographical footprint, having established subsidiaries in Greece, Saudi Arabia, and Rwanda. Plans for US market entry are underway, though regulatory approvals and spectrum access remain hurdles in some markets.

Current clients include Aramco, Telefonica, and Deutsche Telekom, primarily using the technology for asset tracking and remote monitoring in industries such as energy, logistics, and agriculture. While the company estimates a potential market of 1.5 billion devices that could use satellite IoT connectivity, actual adoption rates remain modest.

"The challenge isn't just technical capability," notes the company representative. "It's about proving the economic case for satellite IoT in specific use cases where terrestrial networks aren't viable but the application can support satellite connectivity costs."

Market dynamics are also shifting. Recent announcements from major tech companies about satellite-to-phone services have sparked interest in space-based connectivity, but may also increase competition for spectrum and market share. Several companies are pursuing similar standards-based approaches, potentially commoditizing the technology.

For OQ Technology, the ability to deploy its planned satellites and convert pilot projects into paying customers will be crucial. While the company's focus on standardized technology may reduce technical risks, successfully scaling the business will require navigating complex regulatory environments and proving the technology's reliability across different use cases.

4 notes

·

View notes

Text

Transforming Industries: IoT Device Management Market Growth and Forecast to 2025

Introduction

The Internet of Things (IoT) has transformed industries by enabling seamless connectivity between devices, networks, and applications. As organizations integrate IoT technology, the demand for efficient IoT device management solutions has surged. The IoT Device Management Market is poised for rapid growth, driven by the increasing need for secure, scalable, and cost-effective device administration.

IoT Device Management Market Overview:

IoT Device Management Market Size and Growth Projections

The global IoT device management market is expected to grow at an impressive compound annual growth rate (CAGR) of 35% from 2023 to 2030. This growth is fueled by the rising adoption of IoT across various industry verticals, increased focus on device security, and the need for centralized management solutions.

Request Sample Report PDF (including TOC, Graphs & Tables): www.statsandresearch.com/check-discount/40226-global-iot-device-management-market

Key IoT Device Management Market Drivers

Expanding IoT Ecosystem: The proliferation of connected devices across industries necessitates advanced management solutions.

Security Concerns: Cybersecurity threats drive the adoption of secure IoT device management platforms.

Regulatory Compliance: Organizations must adhere to evolving data protection and security regulations.

Remote Device Management: Increasing demand for remote monitoring and troubleshooting solutions boosts market growth.

Cloud-Based IoT Solutions: The adoption of cloud-driven IoT platforms enhances scalability and efficiency.

Get up to 30% Discount: www.statsandresearch.com/check-discount/40226-global-iot-device-management-market

IoT Device Management Market Segmentation Analysis

By Solution Type

1. IoT Device Management Solutions

Device Registration & Provisioning: Automating device enrollment for seamless integration.

Configuration & Control: Enabling real-time adjustments and remote management.

Monitoring & Diagnostics: Enhancing predictive maintenance and troubleshooting.

Security Management: Ensuring data protection through encryption and authentication.

2. IoT Device Management Services

Consulting Services: Helping businesses strategize IoT adoption.

Implementation & Deployment: Streamlining device onboarding processes.

Support & Maintenance: Ensuring uninterrupted operation of IoT networks.

By Organization Size

1. Large Enterprises

Large enterprises account for over 61% of total IoT device management market revenue. These organizations leverage IoT solutions for data-driven decision-making, operational efficiency, and centralized control.

2. Small & Medium Enterprises (SMEs)

SMEs are witnessing a surge in IoT adoption, particularly in emerging economies like India, China, and Singapore. Government initiatives promoting digital transformation and cloud-based IoT platforms are fueling growth in this segment.

By Industry Vertical

1. Manufacturing (36% Market Share in 2022)

Manufacturers use IoT to optimize industrial operations, increase productivity, and reduce downtime. Smart factories rely on IoT device management solutions for automation and predictive maintenance.

2. Healthcare (Fastest-Growing Segment)

The healthcare sector is rapidly integrating IoT for remote patient monitoring, smart medical devices, and real-time diagnostics. IoT security and compliance play a crucial role in this industry's growth.

3. Retail

Retailers leverage IoT for smart inventory management, real-time tracking, and automated checkouts. Connected IoT solutions enhance the customer experience while optimizing supply chain operations.

4. Transportation & Logistics

IoT-enabled fleet management, asset tracking, and predictive maintenance solutions contribute to improved efficiency in transportation and logistics industries.

5. Utilities & Smart Cities

Energy and utility companies implement IoT for smart grids, automated meter reading, and real-time monitoring. Smart city initiatives further propel IoT deployment for traffic control, waste management, and energy conservation.

Regional IoT Device Management Market Analysis

1. North America (30.5% Market Share in 2022)

North America dominates the IoT device management market, driven by advanced ICT infrastructure, high IoT adoption rates, and strong regulatory frameworks. Key players continuously innovate to maintain their competitive edge.

2. Asia-Pacific (Fastest-Growing Region)

Asia-Pacific is expected to witness significant growth due to rising industrial IoT adoption, government initiatives, and increasing investments in smart technologies. Countries like China, India, and Japan are at the forefront of IoT implementation.

3. Europe

The European market is characterized by strict data privacy laws (GDPR) and rapid digital transformation. The region’s focus on cybersecurity and sustainable IoT solutions further fuels growth.

4. Middle East & Africa

Smart city projects and industrial IoT adoption are driving market expansion in the Middle East and Africa. Government investments in 5G and smart infrastructure create opportunities for IoT management platforms.

5. South America

South America’s IoT market is evolving with investments in smart agriculture, energy management, and connected devices. Brazil and Argentina are leading regional adoption.

Competitive Landscape

Key IoT Device Management Market Players

Bosch Software Innovations GmbH

Smith Micro Software, Inc.

Advantech Co., Ltd.

International Business Machines Corp. (IBM)

Aeris Communications, Inc.

Microsoft Corporation

Oracle Corporation

PTC Inc.

These companies focus on product innovation, strategic partnerships, and mergers & acquisitions to strengthen their market presence. Open standards and interoperability initiatives like the Open Mobile Alliance (OMA) further drive market expansion.

Future Trends and Opportunities

1. AI-Driven IoT Management

The integration of artificial intelligence (AI) and machine learning (ML) algorithms enables predictive analytics, automated troubleshooting, and enhanced security measures.

2. Edge Computing

Edge computing reduces latency and enhances real-time processing capabilities, making it a critical component of IoT device management.

3. Blockchain for IoT Security

Decentralized blockchain solutions offer enhanced data security, authentication, and fraud prevention in IoT ecosystems.

4. 5G and IoT Expansion

The widespread rollout of 5G networks accelerates IoT adoption, improving data transfer speeds and connectivity for large-scale IoT deployments.

5. Sustainable IoT Solutions

As organizations prioritize environmental sustainability, IoT solutions with low energy consumption and eco-friendly materials gain traction.

Conclusion

The IoT Device Management Market is experiencing unprecedented growth, driven by technological advancements, increasing connectivity, and a rising focus on security and efficiency. With North America leading in market share and Asia-Pacific emerging as the fastest-growing region, businesses must stay ahead by adopting cutting-edge IoT management solutions. The integration of AI, edge computing, and blockchain will further revolutionize the industry, creating new opportunities for innovation and market expansion.

By leveraging AI-driven analytics, cloud-based solutions, and enhanced security protocols, enterprises can maximize operational efficiency and secure their IoT ecosystems. The next decade will witness transformational shifts, making IoT device management a crucial element in digital transformation strategies.

Purchase Exclusive Report: www.statsandresearch.com/enquire-before/40226-global-iot-device-management-market

Contact Us

Stats and Research

Email: [email protected]

Phone: +91 8530698844

Website: https://www.statsandresearch.com

1 note

·

View note

Text

Smart Shelves Market to be Worth $10.62 Billion by 2032

Meticulous Research®—a leading global market research company, published a research report titled, 'Smart Shelves Market by Offering (Hardware, Software, Services), Application (Inventory Management, Remote Monitoring, Demand Forecasting, Pricing Management, Others), End User (Hypermarkets, Supermarket, Others), & Geography - Global Forecast to 2032.’

According to this latest publication from Meticulous Research®, the smart shelves market is projected to reach $10.62 billion by 2032, at a CAGR of 22.8% from 2025 to 2032. The growth of this market is driven by the growing concern of retail business to keep inventory at an optimum level, increasing use of electronic shelve labels for pricing management, and growing customer demand for better in-store experiences. In addition, the rising use of advanced technologies in retail and the growing number of smart stores are expected to offer significant growth opportunities for the stakeholders in the smart shelves market.

However, the lack of technology adoption in the unorganized retail sector may restrain the market's growth. Furthermore, the rising shift towards E-commerce and data security & privacy issues are expected to challenge the growth of the smart shelves market.

Based on offering, the global smart shelves market is segmented into hardware, software, and services. In 2025, the hardware segment is expected to account for the largest share of the global smart shelves market. The large market share of this segment is attributed to factors such as the rising number of smart stores, growing adoption of electronic shelf labels for automated pricing, order picking, monitoring products, and asset information.

In addition, the rising focus of key players on product development and enhancement is also expected to drive market growth. For instance, in February 2025 , Qualcomm Technologies, Inc. (U.S.) collaborated with SES-imagotag (France), the global leader in smart electronic price tags and retail IoT solutions, to develop technology that enables new electronic shelf labels (ESLs) based on wireless standards from the Bluetooth Special Interest Group (SIG) to enable retailers to improve operational efficiencies, empower employees, and enhance their customers’ experiences.

However, the software segment is projected to register the highest CAGR during the forecast period. Growing need for smart shelve software among retailers to update the pricing of goods, real-time tracking of virtually all on-shelf inventory, and a growing need to analyze the data collected from the shelves to produce business insights. Several players operating in the market provide smart shelf management software. For instance, Scandit AG (Switzerland) offers ShelfView, a shelf management software that empowers more intelligent and efficient store operations for inventory localization and execution of prices and promotions.

Based on application, the global smart shelves market is broadly segmented into inventory management, remote monitoring, demand forecasting, pricing management, and other applications. In 2025, the inventory management segment is expected to account for the largest share of the global smart shelves market. The large market share of this segment is attributed to growing competition between retailers, the crucial need to optimize shelf stock, and the rising use of electronic shelf labels by retailers to accurately track inventory levels in real time, ensuring faster replenishment and better control of pricing, and inventory availability for customers.

However, the demand forecasting segment is projected to register the highest CAGR during the forecast period. The growth of this segment is driven by factors such as the rising need to optimize inventory levels, reduce stockouts and overstocks, improve customer satisfaction, and enhance supply chain efficiency are expected to drive the segment growth.

Based on end user, the global smart shelves market is broadly segmented into hypermarkets, supermarkets, department stores, specialty stores, warehouses, and other end users. In 2025, the hypermarkets segment is expected to account for the largest share of the global smart shelves market. The large market share of this segment is attributed to the increasing adoption of advanced technologies, the growing use of digitalized price labels for dynamic pricing, increased competition between e-commerce and physical stores, and the growing use of automated checkout systems.

For instance, in April 2025, SES-Imagotag (France), the global leader in digital solutions for physical retail, entered into an agreement with Walmart Inc. (U.S.), an American multinational retail corporation, to initiate the deployment of the latest-generation VUSION platform within several hundred Walmart U.S. stores.

However, the department stores segment is projected to register the highest CAGR during the forecast period. The growth of this segment is driven by the rising focus of department stores on providing a high level of services, greater convenience to customers by offering a variety of products under one roof, increased use of smart shelves with digital displays for personalized advertisements, the need for automated processes in stores, and crucial need of continuous tracking and managing stocks in department stores.

Based on geography, the global smart shelves market is segmented into North America, Asia-Pacific, Europe, Latin America, and the Middle East & Africa. In 2025, Asia-Pacific is expected to account for the largest share of the global smart shelves market. The large market share of the region is attributed to the presence of rapidly developing economies, the growing technology investment in the retail sector to address changed consumer expectations on the shopping experience, and the increased use of electronic shelf labels at retail for providing an enhanced customer experience.

Moreover, the Asia-Pacific region is also projected to register the highest CAGR during the forecast period. The growth of this region is driven by factors such as the indispensable requirement of retailers to digitalize their traditional business operations, the recent development of the Bluetooth electronic shelf label standard and the rapidly increasing e-commerce, and the rising focus of key players on the development of low power electronic shelf label are creating demand for warehouse management.

For instance, in January 2025, Atmosic Technologies (U.S.), an innovator in energy harvesting wireless platforms for the Internet of Things (IoT), partnered with Etag Technology Corporation (China), a professional manufacturer of electronic shelf label systems, to bring Atmosic’s ultra-low power wireless solutions to ETAG Tech’s electronic shelf label (ESL) portfolio.

Key Players:

Some of the key players operating in the global smart shelves market are Intel Corporation (U.S.), AWM (U.S.), Panasonic Connect Oceania (Australia), Pricer AB (Sweden), Trax Technology Solutions Pte Ltd. (Singapore), SOLUM (South Korea), SES-imagotag (France), HCL Technologies Limited (India), E Ink Holdings Inc. (Taiwan), Huawei Technologies Co., Ltd. (China), Focal Systems Inc. (U.S.), MAGO SA (Poland), Minewtag (China), troniTAG GmbH (Germany), Samsung Electronics Co. Ltd (South Korea), Honeywell International Inc. (U.S.), Lenovo PCCW Solutions Limited (China), NXP Semiconductors N.V (Netherlands), and Avery Dennison Corporation (U.S.).

Download Sample Report Here @ https://www.meticulousresearch.com/download-sample-report/cp_id=5705

Key questions answered in the report:

Which are the high-growth market segments in terms of offering, application, and end user?

What is the historical market size for smart shelves across the globe?

What are the market forecasts and estimates for 2025–2032?

What are the major drivers, restraints, opportunities, and challenges in the global smart shelves market?

Who are the major players in the global smart shelves market, and what are their market shares?

How is the competitive landscape?

What are the recent developments in the global smart shelves market?

What are the different strategies adopted by the major players in the market?

What are the geographic trends and high-growth countries?

Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

#Smart Shelves Market#Smart Shelves#Smart Shelf Technology#Smart Shelving System#Shelf Sensors#Shelf Smart

1 note

·

View note

Text

Utility Asset Management Market Expands Through Predictive Maintenance and Real-Time Monitoring Trends

The Utility Asset Management Market is undergoing a transformative shift as utility providers across the globe strive to modernize aging infrastructure, enhance grid reliability, and ensure regulatory compliance. With increasing pressures from rising energy demand, decentralization of power generation, and climate change, effective asset management has become essential for sustaining utility operations. This market is expanding rapidly, integrating cutting-edge technologies like AI, IoT, predictive analytics, and GIS (Geographic Information Systems) to support smarter, more agile decision-making processes.

Market Overview

Utility asset management involves the systematic tracking, assessment, and optimization of physical infrastructure assets such as transformers, substations, pipelines, meters, and cables. Traditionally, utilities relied on manual processes and reactive maintenance, which often led to high costs, inefficiencies, and frequent outages. However, with the evolution of digital tools and advanced data analytics, companies now have the ability to monitor asset conditions in real-time, forecast failures, and plan maintenance proactively.

The global utility asset management market is segmented by component (hardware, software, and services), application (electrical, gas, water), and deployment (on-premises and cloud-based). Electric utilities form the largest share due to the criticality of grid reliability and increasing investments in smart grids and renewable integration.

Key Market Drivers

Aging Infrastructure: Many utility assets, especially in developed economies, are decades old. Replacing or upgrading these systems requires robust asset management planning to minimize downtime and allocate capital efficiently.

Smart Grid Development: The transition to smart grids has accelerated the adoption of asset management solutions, as real-time monitoring and predictive analytics help utilities optimize performance and improve service delivery.

Regulatory Compliance and Risk Management: Governments and regulatory bodies impose stringent standards related to safety, emissions, and reliability. Utility asset management helps organizations maintain compliance while mitigating risks of failure or accidents.

Decentralized Energy and Renewables: The integration of distributed energy resources (DERs), such as solar and wind, adds complexity to grid operations. Asset management ensures smoother coordination between traditional and renewable sources.

Digital Transformation: Adoption of technologies like cloud computing, machine learning, and digital twins has opened new opportunities for predictive maintenance and remote monitoring, reducing operational costs and improving asset lifecycle management.

Regional Insights

North America dominates the utility asset management market due to significant investments in smart grid technology, energy infrastructure modernization, and stringent regulatory frameworks.

Europe follows closely, driven by sustainability initiatives, decarbonization goals, and infrastructure upgrades across the energy and water sectors.

Asia-Pacific is experiencing rapid growth due to urbanization, rising electricity demand, and large-scale renewable energy projects, especially in China, India, and Southeast Asia.

Competitive Landscape

The market is moderately fragmented with the presence of global and regional players. Key players include ABB Ltd., IBM Corporation, Siemens AG, GE Digital, Schneider Electric, Hitachi Energy, and Bentley Systems, among others. These companies offer comprehensive utility asset management platforms combining field service management, real-time analytics, GIS, and condition-based monitoring.

Partnerships, mergers, and acquisitions are common strategies employed by major players to expand their service offerings and strengthen their regional presence. For example, collaborations between utility providers and tech firms are becoming more prevalent as utilities seek integrated solutions tailored to specific challenges.

Challenges in the Market

Despite its growth, the utility asset management market faces several challenges:

High Initial Investment: Implementing advanced asset management systems can be capital-intensive, particularly for small utilities.

Data Integration Issues: Integrating legacy systems with new digital tools can be complex and time-consuming.

Cybersecurity Risks: With increasing digitalization, utilities are more vulnerable to cyberattacks, making data protection and cybersecurity critical.

Future Outlook

The utility asset management market is poised for continued growth, fueled by the need for operational efficiency, resiliency, and sustainable energy practices. Emerging trends such as the use of drones for asset inspections, AI-driven fault detection, and blockchain for secure data sharing are set to reshape the market landscape. As utilities embrace digital innovation, the focus will shift from reactive asset management to proactive and strategic lifecycle planning.

In conclusion, utility asset management is not just a technical necessity—it’s a strategic imperative that will define the future of energy, water, and gas services worldwide.

0 notes

Text

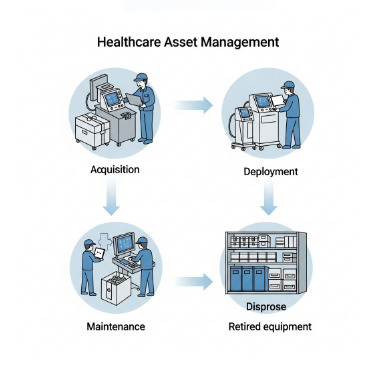

Healthcare Asset Management Market Key Players and Strategic Developments 2032

The global healthcare asset management market was valued at USD 11,002.5 million in 2019 and is expected to reach USD 215,133.5 million by 2032, growing at a compound annual growth rate (CAGR) of 25.3% during the forecast period. In 2019, North America led the market, accounting for 49.94% of the total market share.

In healthcare settings, asset management is a highly systematic and cost-effective approach to planning, acquiring, deploying, operating, maintaining, and disposing of physical assets within a medical facility. By providing a comprehensive asset registry, healthcare asset management solutions enable hospitals and clinics to efficiently track and manage inventory. This, in turn, enhances patient care, reduces operational costs, and improves overall efficiency. A healthcare asset management system encompasses various aspects, including ward management, facility layout, intensive care, operational care, and broader facility management. The optimal utilization of physical assets plays a crucial role in enhancing the quality of patient care, making well-structured asset management an essential component of hospital operations. The growing emphasis on effectively managing existing assets and workforce has led healthcare facilities worldwide to adopt advanced asset management solutions, significantly driving the expansion of the healthcare asset management market.

Continue reading for more details: https://www.fortunebusinessinsights.com/industry-reports/hospital-asset-management-systems-market-100625

Market Segmentation:

Component: The healthcare asset management market is segmented into hardware, software, and services. Hardware (including tags and readers) holds the largest share due to widespread use in tracking physical assets.

Product Type: Includes RFID-based asset management, RTLS-based asset management, and others. RFID is widely adopted for inventory and equipment tracking.

Application: Key applications include hospital asset tracking, pharmaceutical tracking, patient tracking, and staff management. Hospital asset tracking dominates the healthcare asset management market.

End User: Segments include hospitals, laboratories, pharmaceutical companies, and clinics. Hospitals are the major end users due to the need to manage high volumes of assets efficiently.

List Of Key Companies Profiled In Healthcare Asset Management Market:

IBM Corporation

Stanley Healthcare

CenTrak, Inc.

AiRISTA Flow

Versus Technology, Inc.

Zebra Technologies,

GE Healthcare

Sonitor

AeroScout Inc.

Others

Market Growth

The healthcare asset management market is growing rapidly due to increasing demand for efficient asset tracking and resource optimization in hospitals and healthcare facilities.

Rising concerns about the loss, misplacement, and underutilization of medical equipment are driving adoption of asset management solutions.

Integration of advanced technologies such as RFID, IoT, and real-time location systems (RTLS) is fueling innovation in the healthcare asset management market.

Growing need to reduce operational costs, enhance workflow efficiency, and improve patient safety is contributing to market expansion.

The shift toward digital transformation and automation in the healthcare sector is creating new opportunities for the healthcare asset management market.

Restraining Factors

High initial costs for deployment and integration of asset management systems may hinder adoption, especially in smaller healthcare facilities.

Complexity in system implementation and lack of interoperability with existing healthcare IT infrastructure can limit scalability in the healthcare asset management market.

Data privacy and cybersecurity concerns regarding real-time tracking and monitoring systems present challenges for stakeholders.

Limited awareness and technical expertise in developing regions can slow market penetration of the healthcare asset management market.

Regional Analysis

North America dominates the healthcare asset management market due to strong healthcare infrastructure, high adoption of advanced technologies, and regulatory emphasis on operational efficiency.

Europe follows, driven by increasing focus on patient safety, regulatory compliance, and hospital modernization initiatives.

Asia-Pacific is emerging as a high-growth region, with expanding healthcare facilities, growing investment in hospital IT infrastructure, and increasing awareness of asset management benefits.

Latin America and Middle East & Africa offer potential growth opportunities but are currently limited by budget constraints and lack of infrastructure in the healthcare asset management market.

Contact Us:

Fortune Business Insights™ Pvt. Ltd.

9th Floor, Icon Tower,

Baner - Mahalunge Road,

Baner, Pune-411045,

Maharashtra, India.

Phone:

U.S.: +1 424 253 0390

U.K.: +44 2071 939123

APAC: +91 744 740 1245

Email:[email protected]

0 notes

Text

IoT Insurance Market Booms Amid Rising Adoption of Smart Home Technologies

TheIoT Insurance Market Size was valued at USD 15.09 Billion in 2023 and is expected to reach USD 152.76 Billion by 2032 and grow at a CAGR of 29.4% over the forecast period 2024-2032.

IoT Insurance Market is revolutionizing traditional insurance operations by integrating connected devices and real-time data analytics into policy development and risk management. This digital shift is empowering insurers to offer dynamic, personalized coverage, leading to improved customer satisfaction and operational efficiency across various segments such as auto, home, and health insurance.

U.S. Accelerates IoT Insurance Adoption with Advanced Telematics and Smart Home Integration

IoT Insurance Market continues to grow as insurers adopt smart technologies to minimize claims, reduce fraud, and monitor insured assets in real time. With enhanced transparency and improved underwriting accuracy, the insurance landscape is experiencing a data-driven transformation that aligns with modern customer demands.

Get Sample Copy of This Report: https://www.snsinsider.com/sample-request/6558

Market Keyplayers:

Oracle Corporation (Oracle Insurance Policy Administration, Oracle IoT Cloud)

SAP SE (SAP Leonardo IoT, SAP S/4HANA for Insurance)

IBM Corporation (IBM Watson IoT Platform, IBM Cloud for Insurance)

Microsoft Corporation (Azure IoT Hub, Microsoft Cloud for Financial Services)

Intel Corporation (Intel IoT Platform, Intel SDO (Secure Device Onboard))

Telit Communications PLC (Telit IoT Platform, Telit deviceWISE for Insurance Telematics)

Capgemini SE (Capgemini Insurance Connect, Capgemini IoT Solutions for Insurers)

Cognizant (Cognizant Intelligent Insurance Operations, Cognizant IoT Assurance Platform)

Cisco Systems Inc. (Cisco Kinetic for Insurance IoT, Cisco IoT Threat Defense)

Accenture PLC (Accenture Connected Insurance Platform, Accenture IoT Insights)

Verisk Analytics Inc. (AIR Worldwide [catastrophe risk modeling], Verisk Telematics for Usage-Based Insurance)

Wipro Limited (Wipro HOLMES IoT, Wipro Insurance Analytics Suite)

Google LLC (Google Cloud IoT Core, Google Cloud for Insurance)

Synechron, Inc. (Synechron InsurTech Accelerator, Synechron IoT-Driven Insurance Solutions)

Market Analysis

The IoT Insurance Market is evolving rapidly, fueled by increasing adoption of connected devices and growing consumer demand for usage-based policies. In the U.S., automotive telematics and smart home sensors are driving real-time risk insights, while in Europe, regulatory frameworks are encouraging data security and innovation. Insurance providers are leveraging IoT to enable proactive services, making coverage more responsive and personalized than ever.

Market Trends

Increased deployment of telematics in vehicle insurance for driving behavior tracking

Adoption of smart home sensors to prevent and monitor property damage

Growing integration of wearables for health and wellness-based insurance plans

Rise of AI and machine learning for risk scoring and predictive claims management

Expansion of blockchain for secure data sharing and automation

Surge in demand for real-time customer alerts and notifications

Cross-industry collaborations enhancing service offerings and IoT device connectivity

Market Scope

IoT is redefining how insurers interact with data, customers, and risk. The scope of the market is broadening as connected ecosystems become more accessible and insurers focus on proactive engagement.

Real-time monitoring for instant risk detection

Customized premiums based on user behavior and conditions

Smart claim automation improving accuracy and response speed

IoT-enabled health tracking for preventive care programs

Enhanced fraud detection through device-driven data verification

This expanding ecosystem enables insurers to provide tailored policies while improving claims efficiency and reducing operational costs.

Forecast Outlook

The future of the IoT Insurance Market is marked by intelligent automation, expanded device adoption, and customer-centric innovations. As insurers move beyond traditional actuarial models, real-time behavioral data and predictive analytics will redefine the foundation of underwriting. The market is set to witness substantial growth, particularly in regions with high IoT penetration and regulatory support, such as the U.S. and Europe. Expect deeper integration with home security, automotive OEMs, and health-tech platforms, driving a seamless insurance experience.

Access Complete Report: https://www.snsinsider.com/reports/iot-insurance-market-6558

Conclusion

The IoT Insurance Market is paving the way for a smarter, data-powered insurance industry. By embracing real-time intelligence, insurers are not just reacting to risks—they are actively preventing them. As customers increasingly seek flexible and responsive coverage, the combination of connected devices and advanced analytics is reshaping expectations across the insurance lifecycle. Insurers that innovate with agility will lead the next era of trust, personalization, and efficiency in the global insurance landscape.

About Us:

SNS Insider is one of the leading market research and consulting agencies that dominates the market research industry globally. Our company's aim is to give clients the knowledge they require in order to function in changing circumstances. In order to give you current, accurate market data, consumer insights, and opinions so that you can make decisions with confidence, we employ a variety of techniques, including surveys, video talks, and focus groups around the world.

Contact Us:

Jagney Dave - Vice President of Client Engagement

Phone: +1-315 636 4242 (US) | +44- 20 3290 5010 (UK)

Mail us: [email protected]

0 notes

Text

How Will Technological Advancements Impact the Patient Monitoring Devices Market by 2032?

The global Patient Monitoring Devices Market was valued at USD 48.03 billion in 2023 and is projected to grow significantly, reaching USD 93.53 billion by 2032, expanding at a CAGR of 7.71% during the forecast period (2024–2032). This rapid growth is attributed to the increasing prevalence of chronic diseases, a rapidly aging global population, and continuous advancements in medical technologies that make remote and real-time patient monitoring more efficient and accessible. For a more detailed analysis, you can explore the comprehensive report on Patient Monitoring Devices Market Size.

https://www.snsinsider.com/assets/images/report/1731997958-709192537.png

Modern healthcare increasingly demands real-time and continuous patient insights, especially for managing critical and long-term conditions such as diabetes, cardiovascular diseases, and respiratory disorders. With this demand, wearable and wireless monitoring devices, AI-integrated platforms, and telehealth services are gaining traction globally.

Key Growth Drivers

Several factors are contributing to the robust expansion of the Patient Monitoring Devices Market:

Rising Chronic Disease Cases: Conditions such as heart disease, hypertension, and diabetes require continuous monitoring, driving demand for advanced monitoring tools.

Aging Population: As the global geriatric population grows, the need for at-home and hospital-based monitoring is increasing.

Technology Integration: The integration of AI, machine learning, and IoT has revolutionized how healthcare providers track patient health remotely.

Healthcare Infrastructure Development: Especially in emerging economies, improvements in healthcare systems are promoting the adoption of these devices.

Market Segmentation Insights

The market is segmented into various device categories such as:

Cardiac Monitoring Devices

Blood Glucose Monitors

Multi-parameter Monitors

Respiratory Monitoring Devices

Remote Patient Monitoring Devices

Among these, remote patient monitoring devices are expected to witness the fastest growth due to increased adoption of telehealth and home care settings post-pandemic.

Regional Outlook

North America holds the largest market share, owing to its advanced healthcare infrastructure, high healthcare expenditure, and early adoption of innovative technologies.

Asia-Pacific is projected to witness the highest CAGR due to rising healthcare awareness, increasing investment in medical technology, and growing elderly population in countries like Japan, China, and India.

Key Players in the Market

Prominent companies driving innovation and competition in this space include:

GE Healthcare

Medtronic

Philips Healthcare

Nihon Kohden

Masimo Corporation

Siemens Healthineers

Honeywell Life Sciences

These companies are focusing on R&D, product launches, strategic collaborations, and acquisitions to strengthen their market positions.

Challenges and Opportunities

While the market holds great promise, challenges such as data privacy concerns, high device costs, and lack of infrastructure in certain regions still exist. However, with government initiatives promoting digital health and increasing investment from both public and private sectors, these challenges are expected to be addressed over time.

The future of patient monitoring lies in seamless data integration, cross-device connectivity, and predictive analytics, which are increasingly becoming part of standard healthcare practices globally.

About Us:

SNS Insider is one of the leading market research and consulting agencies that dominates the market research industry globally. Our company's aim is to give clients the knowledge they require in order to function in changing circumstances. In order to give you current, accurate market data, consumer insights, and opinions so that you can make decisions with confidence, we employ a variety of techniques, including surveys, video talks, and focus groups around the world.

Contact Us:

Jagney Dave – Vice President of Client Engagement 📞 Phone: +1-315 636 4242 (US) | +44- 20 3290 5010 (UK) 📧 Email: [email protected]

#Patient Monitoring Devices Market#Healthcare Technology#Remote Patient Monitoring#Medical Devices Market#Digital Health Trends

0 notes

Text

Fluid Handling Services Market Size, Trends, Key Players & Market Path

Global Fluid Handling Services Market Overview The global fluid handling services market is estimated at approximately USD 64–65 billion in 2023, with forecasts projecting growth to between USD 85–90 billion by 2032–2033. This trajectory implies a compound annual growth rate (CAGR) in the range of 4.5–5.5%, driven by the industrial automation revolution, aging operational infrastructure, and escalating environmental compliance requirements. North America and Europe remain dominant in market share, while the Asia‑Pacific region—especially China and India—emerges as the fastest-growing market owing to rapid urbanisation, petrochemical expansion, and water/wastewater infrastructure development. Global Fluid Handling Services Market Dynamics Key Drivers: Demand for efficient pumping, filtration, valve, and instrumentation services in critical industries like oil & gas, chemical processing, power generation, and food & beverage. This growth is reinforced by regulatory imperatives and the surge in digital monitoring and predictive maintenance technologies. Market Restraints: Cost volatility for raw materials, intense pricing competition from third-party service providers, and the complexity of asset lifecycles and regulatory registries contribute to margin pressure. Strategic Opportunities: Expansion in water and wastewater treatment sectors, rising adoption of sustainable fluid management solutions, and an uptick in digital service platforms offering analytics and remote asset supervision. Technology & Compliance: IoT-enabled fluid monitoring platforms, AI-driven predictive diagnostics, and computerized maintenance management systems (CMMS) are increasingly being integrated. Regulatory frameworks around emissions, spill containment, and worker safety are catalysing investments in advanced service offerings. Download Full PDF Sample Copy of Global Fluid Handling Services Market Report @ https://www.verifiedmarketresearch.com/download-sample?rid=25928&utm_source=PR-News&utm_medium=387 Global Fluid Handling Services Market Trends and Innovations 1. Digital twin and remote monitoring: Real-time asset tracking through digital twin technology and condition-based monitoring is lowering downtime and optimising performance. 2. Predictive analytics and AI: AI‑augmented diagnostics process sensor data to forecast equipment failure and schedule proactive maintenance. 3. Advanced filtration and purification: Cutting-edge filtration services—including microfiltration and reverse osmosis maintenance—are gaining traction in pharmaceuticals, food & beverage, and water utilities. 4. Collaborative platforms: OEMs and service companies partnering to deliver bundled service and lifecycle management contracts, offering holistic support for pumps, valves, meters, and electronics. 5. Sustainability services: Fluid management audits, leak detection, and industrial water reuse programmes address resource efficiency and environmental footprint reduction. Global Fluid Handling Services Market Challenges and Solutions Challenge – Supply chain instability: Geopolitical tensions and logistical bottlenecks disrupt spare-parts availability. Solution: Maintain multi-sourcing strategies, localize inventories, and adopt digital procurement platforms. Challenge – Price competition and margin pressure: Low-cost service providers erode profitability. Solution: Differentiate on value-added services—digital dashboards, lifecycle contracts, and regulatory compliance advisory. Challenge – Regulatory and environmental complexity: Firms face region-specific compliance obligations. Solution: Invest in specialized compliance teams, standardize service bundles across jurisdictions, and develop green-certified offerings. Challenge – Talent and skills gap: Skilled technicians and data analysts are scarce. Solution: Launch training partnerships with technical institutes, implement augmented-reality guided maintenance, and broaden remote assistance via digital tools. Global Fluid Handling Services Market Future Outlook

Over the next 5–10 years, the fluid handling services industry is expected to sustain mid‑single digit CAGR momentum, reaching close to USD 90 billion by 2032–2033. Growth will be anchored in the convergence of digital transformation, sustainability mandates, and precision process control. Key sectors such as petrochemicals, power, pharmaceuticals, and water utilities will drive service adoption. Looking ahead, future development hinges on three primary pillars: Digital evolution: Expansion of cloud‑based CMMS, edge computing, IoT sensor fusion, and automated diagnostics will underpin service differentiation. Sustainable fluid management: Circular economy principles—water reuse, hydrocarbon recovery, emissions capture—will shape service innovation and product–service hybrid models. Service-driven business models: Expect to see increased adoption of subscription‑based lifecycle services, equipment-as-a-service (EaaS), and performance-based contracting, aligning provider revenue with uptime and efficiency metrics. In summary, the global fluid handling services market is poised for transformation from traditional break-fix models to integrated, analytics‑driven, sustainability-focused service platforms, underpinned by digital innovation and regulatory evolution. Key Players in the Global Fluid Handling Services Market Global Fluid Handling Services Market are renowned for their innovative approach, blending advanced technology with traditional expertise. Major players focus on high-quality production standards, often emphasizing sustainability and energy efficiency. These companies dominate both domestic and international markets through continuous product development, strategic partnerships, and cutting-edge research. Leading manufacturers prioritize consumer demands and evolving trends, ensuring compliance with regulatory standards. Their competitive edge is often maintained through robust R&D investments and a strong focus on exporting premium products globally. HYDAC RelaDyne INOXPA Group (Interpump Group SpA) Hudson Pump Astro Pak Corporation Gaubert Oil Company and Global Industrial Solutions. Get Discount On The Purchase Of This Report @ https://www.verifiedmarketresearch.com/ask-for-discount?rid=25928&utm_source=PR-News&utm_medium=387 Global Fluid Handling Services Market Segments Analysis and Regional Economic Significance The Global Fluid Handling Services Market is segmented based on key parameters such as product type, application, end-user, and geography. Product segmentation highlights diverse offerings catering to specific industry needs, while application-based segmentation emphasizes varied usage across sectors. End-user segmentation identifies target industries driving demand, including healthcare, manufacturing, and consumer goods. These segments collectively offer valuable insights into market dynamics, enabling businesses to tailor strategies, enhance market positioning, and capitalize on emerging opportunities. The Global Fluid Handling Services Market showcases significant regional diversity, with key markets spread across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Each region contributes uniquely, driven by factors such as technological advancements, resource availability, regulatory frameworks, and consumer demand. Fluid Handling Services Market, By Type • Flushing• Filtration• Varnish Removal• Others Fluid Handling Services Market, By Industry • Oil & Gas• Chemicals• Food & Beverage• Paper & Pulp• Energy & Power• Others Fluid Handling Services Market By Geography • North America• Europe• Asia Pacific• Latin America• Middle East and Africa For More Information or Query, Visit @ https://www.verifiedmarketresearch.com/product/fluid-handling-services-market/ About Us: Verified Market Research Verified Market Research is a leading Global Research and Consulting firm servicing over 5000+ global clients. We provide advanced analytical research solutions while offering information-enriched research studies.

We also offer insights into strategic and growth analyses and data necessary to achieve corporate goals and critical revenue decisions. Our 250 Analysts and SMEs offer a high level of expertise in data collection and governance using industrial techniques to collect and analyze data on more than 25,000 high-impact and niche markets. Our analysts are trained to combine modern data collection techniques, superior research methodology, expertise, and years of collective experience to produce informative and accurate research. Contact us: Mr. Edwyne Fernandes US: +1 (650)-781-4080 US Toll-Free: +1 (800)-782-1768 Website: https://www.verifiedmarketresearch.com/ Top Trending Reports https://www.verifiedmarketresearch.com/ko/product/personal-safety-tracking-devices-market/ https://www.verifiedmarketresearch.com/ko/product/food-grade-citral-market/ https://www.verifiedmarketresearch.com/ko/product/mmwave-5g-market/ https://www.verifiedmarketresearch.com/ko/product/gasket-market/ https://www.verifiedmarketresearch.com/ko/product/offshore-decommissioning-market/

0 notes

Text

U.S. Internet of Things (IoT) Market Size to Hit USD 118.24 Bn by 2030

The U.S. Internet of Things (IoT) market share remains one of the most mature and dynamic ecosystems globally. Valued at USD 98.09 billion in 2022, the market is projected to grow from USD 118.24 billion in 2023 to USD 553.92 billion by 2030, registering a compound annual growth rate (CAGR) of 24.7% during the forecast period. The U.S. Internet of Things (IoT) market refers to the ecosystem of interconnected physical devices, sensors, software, and network infrastructure that enables the collection, exchange, and analysis of data across a wide range of industries. These devices are embedded with computing technology that allows them to monitor environments, automate processes, and communicate with other systems and users in real-time.

Key Market Highlights: • Market Size (2022): USD 98.09 billion • Projected Size (2030): USD 553.92 billion • CAGR (2023–2030): 24.7% • Growth Drivers: Technological maturity, innovation leadership, and extensive IoT adoption across industries.

Leading U.S. Companies in the IoT Space: • Cisco Systems, Inc. • Amazon Web Services (AWS) • Microsoft Corporation • Intel Corporation • Qualcomm Technologies, Inc. • Hewlett Packard Enterprise (HPE) • IBM Corporation • Google LLC • Oracle Corporation • PTC Inc.

Request For Sample PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/u-s-internet-of-things-iot-market-107392

Market Dynamics:

Strategic Market Drivers: • Expansion of smart city infrastructure supported by federal and state governments. • Increasing deployment of industrial IoT (IIoT) for manufacturing automation and predictive maintenance. • Growth in consumer IoT, including connected homes, wearables, and personal health tracking devices. • Advancements in 5G, AI, and edge computing fueling real-time, decentralized data processing.

Major Opportunities: • Healthcare IoT for remote patient monitoring, smart diagnostics, and hospital asset management. • Smart grid and energy optimization systems led by clean energy policies. • Transportation and mobility solutions such as connected vehicles and V2X communication. • Federal funding for infrastructure modernization and cybersecurity in IoT environments.

Market Applications: • Smart manufacturing • Connected healthcare and telemedicine • Smart homes and consumer IoT • Fleet and supply chain management • Environmental and agricultural monitoring • Retail automation and customer behavior tracking

Deployment Models & Connectivity: • Deployment Types: Cloud-based, on-premises, hybrid, and edge-enabled solutions • Connectivity: 5G, Wi-Fi 6, LPWAN (LoRa, NB-IoT), Bluetooth, Zigbee, and satellite IoT

Key Market Trends: • Surging interest in cybersecure IoT ecosystems and zero-trust architecture. • Integration of artificial intelligence (AI) with IoT for autonomous decision-making. • Proliferation of IoT-as-a-Service (IoTaaS) and managed IoT platforms. • Increased focus on sustainability and green IoT solutions for emissions tracking and resource efficiency.

Speak to Analyst: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/u-s-internet-of-things-iot-market-107392

Recent Industry Developments: May 2023 – Amazon Web Services (AWS) expanded its IoT TwinMaker platform, enabling faster digital twin deployment for industrial and logistics enterprises across the U.S.

August 2023 – Cisco launched its U.S.-focused IoT Operations Dashboard for real-time device tracking, configuration management, and anomaly detection at enterprise scale.

About Us: Fortune Business Insights delivers powerful data-driven insights to help businesses navigate disruption and capitalize on emerging trends. We specialize in delivering sector-specific intelligence, customized research, and strategic consulting across a wide range of industries. Our team empowers organizations with clarity, foresight, and a competitive edge in a fast-moving technological landscape.

Contact Us: US: +1 833 909 2966 UK: +44 808 502 0280 APAC: +91 744 740 1245 Email: [email protected]

#U.S. Internet of Things Market Share#U.S. Internet of Things Market Size#U.S. Internet of Things Market Industry#U.S. Internet of Things Market Driver#U.S. Internet of Things Market Growth#U.S. Internet of Things Market Analysis#U.S. Internet of Things Market Trends

0 notes

Text

Government and Defense Fuel Global Supply Chain Protection Efforts

The Supply Chain Security Market market is on a strong growth trajectory, forecast to expand from USD 2.1 billion in 2023 to USD 4.9 billion by 2030. This represents a compound annual growth rate (CAGR) of approximately 11% over the forecast period. Increased cargo theft, cyber threats, and the need for regulatory compliance are prompting businesses worldwide to invest in advanced supply chain security solutions.

Industries such as retail, pharmaceuticals, automotive, and logistics are experiencing growing pressure to adopt proactive measures to mitigate physical and digital threats throughout their supply chains. Technologies like blockchain, IoT sensors, artificial intelligence, and cloud-based platforms are playing an integral role in shaping the market landscape.

To Get Free Sample Report: https://www.datamintelligence.com/download-sample/supply-chain-security-market

Key Market Drivers

Rising Cargo Theft and Physical Threats Supply chain theft and fraud continue to grow in sophistication, with incidents of fake shipping documentation and identity-based theft. These risks are prompting businesses to adopt real-time monitoring, tracking systems, and secure transportation protocols.

Cybersecurity Challenges Supply chains are increasingly vulnerable to cyberattacks, particularly ransomware and data breaches affecting logistics software, warehouse systems, and supplier communication networks. This has spurred a significant rise in cybersecurity integration across supply chain infrastructures.

Stringent Regulatory Compliance Governments and international agencies have implemented regulatory standards such as ISO 28000, C-TPAT (Customs-Trade Partnership Against Terrorism), and the European Union’s supply chain visibility directives. Compliance is no longer optional it is central to operations and partnerships.

Demand for End-to-End Visibility Enterprises require uninterrupted visibility into their supply networks to mitigate disruption risks, enhance inventory management, and preemptively address vulnerabilities. IoT devices, GPS trackers, and RFID chips are becoming integral tools for real-time logistics management.

Adoption of Advanced Technologies Technologies like AI-driven analytics, machine learning, blockchain, and digital twins are transforming how businesses monitor, secure, and optimize supply chain operations.

Regional Insights

North America North America holds the largest market share, fueled by advanced technological infrastructure, strong cyber regulations, and high demand from logistics, defense, and healthcare sectors. The U.S. is the dominant market, supported by substantial government and private sector investments.

Europe Europe accounts for a significant portion of global market revenue, supported by strict data protection laws (GDPR), regulatory enforcement on product traceability, and a focus on supply chain transparency in cross-border trade.

Asia-Pacific Asia-Pacific is the fastest-growing regional market, forecast to expand at a CAGR of around 16%. Rapid industrialization, the expansion of e-commerce, increasing cases of cargo fraud, and growing awareness around cybersecurity are key factors propelling growth in countries like China, India, and Japan.

Latin America and Middle East & Africa (MEA) These emerging markets are witnessing rising investments in logistics, port security, and smart infrastructure, especially in industries like oil & gas, pharmaceuticals, and food logistics.

Market Segmentation

By Component

Hardware: Includes GPS trackers, RFID tags, and IoT sensors, essential for physical asset tracking.

Software: Encompasses risk analytics platforms, monitoring dashboards, and AI-based threat detection systems.

Services: Consulting, deployment, compliance audits, and managed monitoring services are growing in demand.

By Application

Data Security and Integrity

Real-Time Monitoring and Alerts

Access Control and Authentication

Risk Assessment and Compliance Management

By Industry

Retail & E-Commerce: High theft vulnerability, especially in last-mile delivery and warehouse operations.

Healthcare & Pharmaceuticals: Demand for secure handling of biologics and anti-counterfeiting systems.

Manufacturing and Automotive: Focus on supplier verification and just-in-time delivery security.

Defense & Aerospace: National security-related logistics demand top-tier surveillance and risk minimization.

Transportation & Logistics: Adoption of end-to-end digital security systems and cold-chain monitoring.

Market Challenges

High Implementation Costs The cost of integrating AI, IoT, and blockchain into supply networks can be substantial, particularly for small-to-medium enterprises.

Lack of Standardization Global supply chains span diverse regulatory environments, making standardization difficult across industries and countries.

Evolving Threat Landscape Cyber threats evolve rapidly, requiring continuous investment in security upgrades, staff training, and threat intelligence.

Subscribe for Insights: https://www.datamintelligence.com/reports-subscription

Future Market Opportunities

Blockchain for Tamper-Proof Verification Blockchain’s ability to provide immutable transaction records is enabling secure verification of product movement, improving transparency and trust across stakeholders.

AI and Predictive Analytics AI models can now identify patterns of potential fraud, shipment delays, and operational anomalies before they escalate into major disruptions.

Cloud-Based Platforms The shift to SaaS-based supply chain security platforms is growing, especially among multinational organizations seeking centralized control and scalability.

Government and Defense Support Public sector programs promoting secure trade and protected infrastructure (such as defense-grade cybersecurity for transport systems) are expected to drive substantial growth.

Key Market Players

Leading vendors include IBM Corporation, Cisco Systems, Oracle Corporation, Honeywell International, Siemens AG, Sensitech, Huawei Technologies, Check Point Software Technologies, Johnson Controls, Securitas AB, and Intel Corporation. These players focus on integrated platforms offering visibility, risk analysis, and automated threat detection.

Conclusion

The global supply chain security market is evolving rapidly in response to rising physical and cyber threats. As businesses strive to protect assets, ensure regulatory compliance, and optimize global operations, the need for integrated, intelligent security solutions continues to grow. With strong growth expected through 2030, organizations that prioritize transparency, tech-enabled risk management, and regulatory readiness will be best positioned to thrive in this complex and competitive environment.

0 notes

Text

Global Geospatial Analytics Market – $33B (2024) to $56B by 2029, 11.1% CAGR

Segmentation Overview The geospatial analytics market is segmented by:

Type: Surface & field analytics; Geovisualization; Network analysis; Artificial neural networks; Others

Technology: Remote sensing; GPS; GIS; Others

Solutions: Geocoding & reverse geocoding; Reporting & visualization; Thematic mapping & spatial analysis; Data integration & ETL; Others

Applications: Surveying; Disaster risk reduction & management; Medicine & public safety; Climate change adaptation; Predictive asset management; Others

End-Users: Agriculture; Defense & intelligence; Utilities & communication; Automotive; Government; Travel & logistics; Others

Regions: North America; Latin America; Europe; Asia-Pacific; Middle East & Africa To buy the report, click on https://www.datamintelligence.com/buy-now-page?report=geospatial-analytics-market

Market Size & Forecast

The global geospatial analytics market is projected to expand at a CAGR of 12.8% between 2024 and 2031.

Other projections estimate market growth from USD 32.97 billion in 2024 to USD 55.75 billion by 2029.

A broader estimate values the market at USD 114.3 billion in 2024, expected to reach over USD 226.5 billion by 2030.

Introduction & Definition

Geospatial analytics is the process of gathering, interpreting, and visualizing location-based data—drawn from satellites, GPS, mobile devices, sensors, and social media—using GIS, AI, and computer vision. This powerful fusion helps governments and businesses gain real-time insights into transportation, urban planning, agriculture, disaster response, defense, utilities, and logistics.

Market Drivers & Restraints

Key Drivers:

Smart City Expansion: The proliferation of IoT sensors and connected devices in urban infrastructure drives demand for spatial analytics to manage traffic, utilities, public safety, and emergency planning.

Technological Integration: Advances in AI, 5G, satellite imaging, and edge computing enable high-resolution, real-time spatial decision-making.

Enterprise Adoption: Widespread demand for location intelligence across sectors—such as agriculture, defense, utilities, transportation, and retail—boosts comprehensive geospatial integration.

Restraints:

Privacy & Security: Handling sensitive spatial data raises concerns over surveillance, data protection, and regulatory compliance.

Data Complexity: Integrating varied data sources—maps, sensors, satellite imagery—remains a challenge due to formatting and standardization issues.

Cost & Skills Gap: High initial investment and talent shortages for GIS and AI expertise hinder full-scale adoption.

Segmentation Analysis

By Type: Surface & field analytics lead due to applications in topography, hydrology, and asset monitoring. Geovisualization supports urban planning and stakeholder communication.

By Technology: GIS dominates software solutions; GPS and remote sensing—particularly LiDAR, radar, and GNSS—are key data capture technologies.

By Solutions: Thematic mapping and ETL tools are in high demand for data-driven decisions across utilities, logistics, and infrastructure.

By Applications: Surveying, disaster mitigation, climate adaptation, asset management, medicine, and public safety are major application fields.

By End-Users: Agriculture (precision farming), defense (geospatial intelligence), utilities, transportation, government services, and logistics are top verticals.To get a free sample report, click on https://www.datamintelligence.com/download-sample/geospatial-analytics-market

Geographical Insights

North America: Holds the largest market share (~34% in 2024), driven by government and defense investments, smart cities, and GIS adoption.

Europe: Adoption spans from transport and delivery logistics to environmental tracking; EU programs boost earth observation and AI integration.

Asia-Pacific: Fastest-growing region due to rapid urbanization and expansion in countries like China, India, and Japan.

Middle East & Africa: High growth supported by smart city initiatives and infrastructure investments.

Recent Trends or News

AI-Embedded Spatial Tools: Major GIS platforms are embedding AI and machine learning for predictive analysis.

Mobile Mapping & 3D Scanning: Use of LiDAR-equipped vehicles and drones is increasing rapidly in infrastructure and mapping applications.

Pandemic & Disaster Applications: The pandemic accelerated use of geospatial analytics for vaccine distribution, health mapping, and crisis response.

Competitive Landscape

Leading companies in the geospatial analytics market include:

Microsoft

Google

General Electric (GE)

SAP

Salesforce

Precisely

Oracle

RMSI

OmniSci

Maxar Technologies

Hexagon AB

TomTom

Trimble

Esri

CARTO

Orbital Insight

These companies lead through AI-powered tools, cloud-native GIS, satellite imagery, mobile solutions, and strategic acquisitions.

Impact Analysis

Economic Impact: Geospatial analytics streamlines operations—optimizing routes, reducing resource wastage, and enhancing project ROI.

Environmental Impact: Unlocks data for spatial monitoring—supporting climate modeling, land-use mapping, environmental compliance, and disaster mitigation.

Social Impact: Shapes public health response systems, emergency services, and urban planning, while challenging privacy norms.

Technological Impact: Drives growth in cloud GIS, AI-engineered mapping, real-time analytics, and sensor networks, enabling scalable spatial insights.

Key Developments

GeoAnalytics Engine by Esri: An AI-integrated GIS platform for advanced spatial querying and real-time analytics.

Hexagon Captura Launch: Optical sensor-based system enhancing spatial measurement precision.

CADLM Acquisition by Hexagon: Adds simulation and reliability modeling for enhanced engineering workflows.

Orbital Insight Growth: Enhances satellite-based analytics capabilities through new partnerships and investment.

Report Features & Coverage

This market report includes:

Global and regional market sizing (2018–2024) with forecasts to 2031

In-depth segmentation by type, technology, solution, application, industry, and region

Competitive landscape with company profiling

Key trends, opportunities, and growth challenges

SWOT analysis, Porter’s Five Forces, and market attractiveness index

Recent innovations and investment updates

About Us

We are a global market intelligence firm committed to delivering in-depth insights across emerging technologies. Our expertise in geospatial analytics helps clients unlock data-driven innovation, streamline operations, and improve strategic planning across industries. We provide accurate forecasting, custom reports, and actionable guidance tailored to enterprise and government needs.

Contact Us

Email: [email protected]

Phone: +1 877 441 4866

0 notes

Text

IoT Chips Market is Driven by Explosive Connectivity Demand

Internet of Things (IoT) chips are specialized microprocessors, system-on-chips (SoCs), and connectivity modules designed to enable seamless data exchange among sensors, devices, and cloud platforms. These chips incorporate ultra-low-power architectures, embedded security protocols, and advanced signal processing capabilities that support a broad spectrum of IoT applications—from smart homes and wearable gadgets to industrial automation and connected vehicles. Advantages include reduced latency through edge computing, optimized energy efficiency for battery-operated devices, and streamlined integration into existing network infrastructures.

As businesses pursue digital transformation, there is a growing need for reliable, scalable chipsets capable of handling massive device connectivity, real-time analytics, and robust encryption. Continuous innovation in semiconductor fabrication processes has driven down production costs and boosted performance metrics, enabling smaller startups and established market players alike to introduce competitive products. Meanwhile, evolving market trends such as 5G rollout, AI-enabled analytics, and smart city initiatives are creating new IoT Chips Market opportunities and shaping the industry landscape. Comprehensive market research highlights expanding market segments in healthcare monitoring, agricultural sensors, and asset tracking.

The IoT chips market is estimated to be valued at USD 620.36 Bn in 2025 and is expected to reach USD 1415.005 Bn by 2032, growing at a compound annual growth rate (CAGR) of 15.00% from 2025 to 2032. Key Takeaways

Key players operating in the IoT Chips Market are:

-Intel Corporation

-Samsung Electronics Co. Ltd

-Qualcomm Technologies Inc.

-Texas Instruments Incorporated

-NXP Semiconductors NV

These market companies have established strong footholds through diversified product portfolios that span microcontrollers, application processors, short-range wireless SoCs, and AI inference engines. Their strategic investments in R&D, partnerships with tier-one automotive and industrial firms, and capacity expansions in fabrication plants are instrumental in driving market share growth. Robust alliances and licensing agreements help these players accelerate time-to-market for next-generation solutions, while continuous performance enhancements maintain their competitive edge. As major players optimize supply chains and strengthen IP portfolios, they contribute significantly to the overall market dynamics and industry size. The growing demand for IoT chips is fueled by accelerated digitalization across verticals such as automotive, healthcare, consumer electronics, and manufacturing. Automotive OEMs are integrating IoT chips for connected car features—remote diagnostics, vehicle-to-everything (V2X) communication, and advanced driver-assistance systems (ADAS)—driving substantial market growth. In healthcare, remote patient monitoring and telemedicine solutions rely on miniaturized, power-efficient chips to ensure continuous data transmission and secure access. Additionally, smart agriculture applications leverage low-cost sensors and communication modules to optimize resource usage and crop yields. As enterprises embrace Industry 4.0, the deployment of IoT solutions for predictive maintenance and asset tracking has become a critical business growth strategy. These evolving market trends underscore the importance of high-performance, cost-effective IoT chips to sustain long-term expansion.

‣ Get More Insights On: IoT Chips Market

‣ Get this Report in Japanese Language: IoTチップ市場

‣ Get this Report in Korean Language: IoT칩시장

0 notes

Text

The Future of IoT Device Management Market: Emerging Technologies and Innovations

Introduction

The Internet of Things (IoT) has transformed industries by enabling seamless connectivity between devices, networks, and applications. As organizations integrate IoT technology, the demand for efficient IoT device management solutions has surged. The IoT Device Management Market is poised for rapid growth, driven by the increasing need for secure, scalable, and cost-effective device administration.

IoT Device Management Market Overview:

IoT Device Management Market Size and Growth Projections

The global IoT device management market is expected to grow at an impressive compound annual growth rate (CAGR) of 35% from 2023 to 2030. This growth is fueled by the rising adoption of IoT across various industry verticals, increased focus on device security, and the need for centralized management solutions.

Request Sample Report PDF (including TOC, Graphs & Tables): www.statsandresearch.com/check-discount/40226-global-iot-device-management-market

Key IoT Device Management Market Drivers

Expanding IoT Ecosystem: The proliferation of connected devices across industries necessitates advanced management solutions.

Security Concerns: Cybersecurity threats drive the adoption of secure IoT device management platforms.

Regulatory Compliance: Organizations must adhere to evolving data protection and security regulations.