#North America Machine Control System Market

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Celebrities use Tumblr as well.

Text

Key Trends in North America Machine Control System Market: From Automation to Artificial Intelligence

The North American machine control systems market is poised for significant growth, with expanding industries like construction and mining driving demand for more advanced, efficient, and automated solutions. As technology continues to advance, machine control systems (MCS) are becoming a critical enabler in improving productivity, precision, and safety in heavy industries. These systems are widely used to optimize the operation of construction machinery, mining equipment, and other heavy machinery, providing real-time data and insights that streamline operations and reduce downtime.

0 notes

Text

Aquatic Robot Market to Eyewitness Huge Growth by 2030

Latest business intelligence report released on Global Aquatic Robot Market, covers different industry elements and growth inclinations that helps in predicting market forecast. The report allows complete assessment of current and future scenario scaling top to bottom investigation about the market size, % share of key and emerging segment, major development, and technological advancements. Also, the statistical survey elaborates detailed commentary on changing market dynamics that includes market growth drivers, roadblocks and challenges, future opportunities, and influencing trends to better understand Aquatic Robot market outlook. List of Key Players Profiled in the study includes market overview, business strategies, financials, Development activities, Market Share and SWOT analysis: Atlas Maridan ApS. (Germany), Deep Ocean Engineering Inc. (United States), Bluefin Robotics Corporation (United States), ECA SA (France), International Submarine Engineering Ltd. (Canada), Inuktun Services Ltd. (Canada), Oceaneering International, Inc. (United States), Saab Seaeye (Sweden), Schilling Robotics, LLC (United States), Soil Machine Dynamics Ltd. (United Kingdom) Download Free Sample PDF Brochure (Including Full TOC, Table & Figures) @ https://www.advancemarketanalytics.com/sample-report/177845-global-aquatic-robot-market Brief Overview on Aquatic Robot: Aquatic robots are those that can sail, submerge, or crawl through water. They can be controlled remotely or autonomously. These robots have been regularly utilized for seafloor exploration in recent years. This technology has shown to be advantageous because it gives enhanced data at a lower cost. Because underwater robots are meant to function in tough settings where divers' health and accessibility are jeopardized, continuous ocean surveillance is extended to them. Maritime safety, marine biology, and underwater archaeology all use aquatic robots. They also contribute significantly to the expansion of the offshore industry. Two important factors affecting the market growth are the increased usage of advanced robotics technology in the oil and gas industry, as well as increased spending in defense industries across various countries. Key Market Trends: Growth in AUV Segment Opportunities: Adoption of aquatic robots in military & defense

Increased investments in R&D activities Market Growth Drivers: Growth in adoption of automated technology in oil & gas industry

Rise in awareness of the availability of advanced imaging system Challenges: Required highly skilled professional for maintenance Segmentation of the Global Aquatic Robot Market: by Type (Remotely Operated Vehicle (ROV), Autonomous Underwater Vehicles (AUV)), Application (Defense & Security, Commercial Exploration, Scientific Research, Others) Purchase this Report now by availing up to 10% Discount on various License Type along with free consultation. Limited period offer. Share your budget and Get Exclusive Discount @: https://www.advancemarketanalytics.com/request-discount/177845-global-aquatic-robot-market Geographically, the following regions together with the listed national/local markets are fully investigated: • APAC (Japan, China, South Korea, Australia, India, and Rest of APAC; Rest of APAC is further segmented into Malaysia, Singapore, Indonesia, Thailand, New Zealand, Vietnam, and Sri Lanka) • Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe; Rest of Europe is further segmented into Belgium, Denmark, Austria, Norway, Sweden, The Netherlands, Poland, Czech Republic, Slovakia, Hungary, and Romania) • North America (U.S., Canada, and Mexico) • South America (Brazil, Chile, Argentina, Rest of South America) • MEA (Saudi Arabia, UAE, South Africa)Furthermore, the years considered for the study are as follows: Historical data – 2017-2022 The base year for estimation – 2022 Estimated Year – 2023 Forecast period** – 2023 to 2028 [** unless otherwise stated] Browse Full in-depth TOC @: https://www.advancemarketanalytics.com/reports/177845-global-aquatic-robot-market

Summarized Extracts from TOC of Global Aquatic Robot Market Study Chapter 1: Exclusive Summary of the Aquatic Robot market Chapter 2: Objective of Study and Research Scope the Aquatic Robot market Chapter 3: Porters Five Forces, Supply/Value Chain, PESTEL analysis, Market Entropy, Patent/Trademark Analysis Chapter 4: Market Segmentation by Type, End User and Region/Country 2016-2027 Chapter 5: Decision Framework Chapter 6: Market Dynamics- Drivers, Trends and Challenges Chapter 7: Competitive Landscape, Peer Group Analysis, BCG Matrix & Company Profile Chapter 8: Appendix, Methodology and Data Source Buy Full Copy Aquatic RobotMarket – 2021 Edition @ https://www.advancemarketanalytics.com/buy-now?format=1&report=177845 Contact US : Craig Francis (PR & Marketing Manager) AMA Research & Media LLP Unit No. 429, Parsonage Road Edison, NJ New Jersey USA – 08837 Phone: +1 201 565 3262, +44 161 818 8166 [email protected]

#Global Aquatic Robot Market#Aquatic Robot Market Demand#Aquatic Robot Market Trends#Aquatic Robot Market Analysis#Aquatic Robot Market Growth#Aquatic Robot Market Share#Aquatic Robot Market Forecast#Aquatic Robot Market Challenges

2 notes

·

View notes

Text

Residential Washing Machine Market to Witness Steady Growth Driven by Urbanization and Smart Home Trends

Residential Washing Machine Market size is forecast to grow from USD 76.53 billion to USD 143.66 billion between 2025 and 2034, marking a CAGR of more than 6.5%. The expected industry revenue in 2025 is USD 81.08 billion.

Growth Drivers & Challenge

The residential washing machine market is growing rapidly, driven by increasing urbanization and rising consumer demand for automated household appliances. One of the key growth drivers is the expansion of urban housing and the growing number of nuclear families, especially in developing economies. As more individuals and families migrate to urban areas, the demand for compact, efficient, and time-saving appliances such as washing machines has surged. These machines not only reduce the labor involved in manual washing but also save time, making them highly desirable in fast-paced urban lifestyles. With rising disposable incomes and the expansion of middle-class households, consumers are increasingly inclined to invest in technologically advanced appliances that offer convenience and efficiency.

Another significant driver is the continuous innovation and integration of smart technologies in washing machines. Features such as Wi-Fi connectivity, remote control via mobile apps, energy efficiency indicators, and AI-driven wash cycles are gaining popularity. These advancements enhance user experience by allowing greater control, customization, and operational efficiency. Manufacturers are also focusing on water and energy conservation, which resonates well with environmentally conscious consumers and contributes to long-term cost savings.

Request for a free sample report @ https://www.fundamentalbusinessinsights.com/request-sample/13395

Despite these positive trends, one of the main challenges faced by the residential washing machine market is the high upfront cost of advanced models. While smart and energy-efficient machines offer long-term savings, their initial purchase price can be a barrier for low-income households. Additionally, in some rural and underdeveloped regions, limited access to stable electricity and water supply further restricts market penetration. Manufacturers must find a balance between innovation, affordability, and sustainability to reach a broader consumer base.

Regional Analysis

North America

In North America, the residential washing machine market is well-established and driven by a high standard of living and widespread adoption of modern appliances. Consumers in the U.S. and Canada prefer energy-efficient models with large capacity and smart features that integrate with home automation systems. Front-load machines are particularly popular in this region due to their efficiency and better fabric care. Additionally, the growing trend of smart homes is pushing demand for Wi-Fi enabled washing machines that can be operated remotely. Environmental regulations and rebate programs promoting energy-saving appliances also contribute to market growth.

Europe

Europe has a mature washing machine market, characterized by strong environmental awareness and strict energy efficiency regulations. Consumers in countries like Germany, France, and the UK prioritize machines with low water and energy consumption, often opting for products with high Energy Star ratings. Built-in and integrated washing machines are widely used in smaller urban apartments where space is limited. Sustainability and durability are key purchasing factors in the European market, and brands that focus on long-lasting performance and recyclable components have a competitive edge. Moreover, the refurbishment and second-hand market is growing, supported by circular economy initiatives.

Browse complete report summary @ https://www.fundamentalbusinessinsights.com/industry-report/residential-washing-machine-market-13395

Asia Pacific

Asia Pacific represents the fastest-growing region in the residential washing machine market, driven by rapid urbanization, population growth, and improving living standards. Countries such as China, India, and Southeast Asian nations are witnessing a surge in demand for washing machines as more consumers shift from manual washing to automatic solutions. The entry of affordable domestic brands and increasing internet penetration has made washing machines accessible to a broader demographic. Semi-automatic machines remain popular in rural areas due to lower prices and less dependency on continuous water supply, while fully automatic and smart machines are gaining traction in urban centers.

Segmentation Analysis

Segments Analysis by Product

The residential washing machine market is segmented by product into fully automatic, semi-automatic, and dryers. Fully automatic machines dominate the market due to their convenience and advanced features. These are further divided into top-load and front-load machines, with front-load models preferred in regions with higher awareness about energy and water savings. Semi-automatic machines are more prevalent in price-sensitive markets due to their affordability and flexibility. Though still a niche segment, dryers are increasingly being adopted in cold and humid climates where outdoor drying is impractical.

Segments Analysis by Capacity

Washing machines are available in various capacities, typically ranging from below 6 kg to above 10 kg. Machines with a capacity of 6 to 8 kg are the most common, suitable for small to medium households. Larger capacity machines above 8 kg are gaining popularity among joint families and consumers with frequent and heavy laundry needs. Manufacturers are also offering compact and portable options for smaller homes or single-person households. Capacity preferences vary significantly by region and household size, influencing product development and inventory strategies for manufacturers.

Segments Analysis by Technology

Technological advancements in washing machines include inverter technology, direct drive motors, steam cleaning, and smart sensors. Inverter technology improves energy efficiency and reduces noise, while steam technology is used for better stain removal and fabric care. Smart sensors enable automatic detection of load and fabric type to optimize water and detergent usage. The adoption of AI and IoT-based features is creating a new segment of intelligent washing machines that offer predictive maintenance, usage insights, and compatibility with voice assistants. These innovations are reshaping consumer expectations and driving premium product adoption.

Segments Analysis by Distribution Channel

Distribution channels for residential washing machines include offline retail, online platforms, and direct sales. Offline retail, comprising appliance stores and electronics showrooms, remains dominant due to the preference for hands-on product evaluation. However, the online segment is growing rapidly, driven by convenience, attractive discounts, and broader product variety. E-commerce platforms offer detailed specifications, user reviews, and doorstep delivery, making them increasingly popular among tech-savvy consumers. Direct-to-consumer sales through brand websites and exclusive outlets are also gaining traction, especially for premium and smart models.

Browse related reports @

About Fundamental Business Insights:

Fundamental Business Insights is global market research and consulting company which is engaged in providing in depth market reports to its various types of clients like industrial sectors, financial sectors, universities, non-profit, and corporations. Our goal is to offer the correct information to the right stakeholder at the right time, in a format that enables logical and informed decision making. We have a team of consultants who have experience in offering executive level blueprints of markets and solutions. Our services include syndicated market studies, customized research reports, and consultation.

Contact us:

Robbin Fernandez

Head of Business Development

Fundamental Business Insights and Consulting

USA: +1–415–800–3393

Email: [email protected]

0 notes

Text

Growth Dynamics and Future Roadmap of the Continuous Bioprocessing Industry

Continuous Bioprocessing Market

The global continuous bioprocessing market was valued at USD 349.3 million in 2024 and is projected to reach USD 911.4 million by 2030, expanding at a compound annual growth rate (CAGR) of 18.63% from 2025 to 2030. This rapid growth trajectory is primarily fueled by the increasing demand for cost-effective, scalable, and efficient biopharmaceutical manufacturing solutions, especially in the production of monoclonal antibodies, vaccines, and cell & gene therapies. The adoption of process intensification strategies, underpinned by automation, real-time monitoring technologies, and single-use systems, is significantly improving overall productivity while simultaneously reducing operational expenses.

Furthermore, global regulatory authorities, including the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA), are actively promoting the implementation of continuous manufacturing methods. These regulatory bodies highlight the approach’s advantages in achieving superior process control, enhanced product consistency, and reduced production variability, making it a favorable alternative to traditional batch manufacturing.

The industry outlook remains highly optimistic, with market expansion being propelled by a combination of factors such as the accelerated adoption of cutting-edge biomanufacturing technologies, a rising global demand for biologic therapies, and ongoing investments in automation and process optimization across the biopharmaceutical sector. Continuous bioprocessing is rapidly becoming a preferred strategy among pharmaceutical and biotech companies due to its ability to deliver higher yields, minimize costs, and improve quality consistency. Moreover, the increasing global burden of chronic and complex diseases, including cancer, autoimmune disorders, and infectious diseases, is driving the need for faster, more cost-efficient production of biologic drugs—further amplifying the market’s momentum.

A pivotal growth driver lies in the technological advancements shaping bioprocessing equipment and systems. Innovations in real-time process analytics, single-use bioreactors, perfusion technologies, and predictive analytics have dramatically enhanced the practicality and reliability of continuous bioprocessing. Many biopharma firms are now investing heavily in digital biomanufacturing platforms, leveraging artificial intelligence (AI) and machine learning (ML) to fine-tune operations, elevate production yields, and uphold stringent quality standards. Regulatory support from agencies like the FDA and EMA—through published guidelines and streamlined approval pathways—is also easing the transition for companies moving from traditional batch methods to continuous operations.

The market is further propelled by the global shift toward cost-efficient and environmentally sustainable manufacturing. Traditional batch processing methods often involve large-scale facilities, higher capital investment, and excessive material waste. In contrast, continuous bioprocessing reduces energy and resource consumption, minimizes waste generation, and increases operational efficiency, making it an attractive solution for companies pursuing sustainable and agile manufacturing practices. The increasing trend of decentralized production and the need for flexible manufacturing infrastructure, especially in response to evolving global healthcare needs and pandemic preparedness initiatives, are accelerating the adoption of continuous bioprocessing technologies worldwide.

Key Market Trends & Insights

Regional Insights: In 2024, North America emerged as the leading revenue-generating region in the global market. This dominance is attributed to substantial investments in biopharmaceutical R&D, the presence of highly advanced manufacturing facilities, and favorable regulatory frameworks. Prominent industry leaders such as Thermo Fisher Scientific, Cytiva (a Danaher company), and Sartorius are channeling significant investments into next-generation bioprocessing technologies to support the production of biologics, biosimilars, and cell & gene therapies.

Country-Specific Insight: India is projected to register the highest CAGR in the market from 2025 to 2030, driven by its expanding biopharmaceutical sector, growing clinical research activity, and supportive government initiatives.

Segment Insights – Product Type: The consumables and reagents segment accounted for USD 214.6 million in revenue in 2024, fueled by the growing adoption of single-use technologies (SUTs), innovations in cell culture media, and the rising need for high-purity reagents to support uninterrupted and contamination-free bioproduction processes.

Segment Insights – Application: Monoclonal antibodies (mAbs) held the largest market share, contributing 98% of total revenue in 2024. The segment's dominance is linked to the surging global demand for biologic therapies, particularly those used in treating oncological, autoimmune, and infectious diseases.

Segment Insights – End-use: The pharmaceutical and biotechnology companies segment represented the largest end-user category, capturing a 43% revenue share in 2024. This is due to the increasing pressure on biopharma firms to produce high-yield, cost-effective, and scalable biologics, especially monoclonal antibodies, biosimilars, cell & gene therapies, and next-gen vaccines. As a result, many companies are transitioning from traditional batch processing models to continuous manufacturing platforms to improve efficiency, scalability, and product throughput.

Order a free sample PDF of the Continuous Bioprocessing Market Intelligence Study, published by Grand View Research.

Market Size & Forecast

2024 Market Size: USD 349.3 Million

2030 Projected Market Size: USD 911.4 Million

CAGR (2025-2030): 18.63%

North America: Largest market in 2024

Key Players

Danaher

Sartorius AG

Thermo Fisher Scientific Inc.

WuXi Biologics

Ginkgo Bioworks

Merck KGaA

GE Healthcare

Repligen Corporation

Asahi Kasei Bioprocess America, Inc.

Browse Horizon Databook on Global Continuous Bioprocessing Market Size & Outlook

Conclusion

The global continuous bioprocessing market is undergoing a significant transformation, driven by the urgent need for more efficient, scalable, and cost-effective biomanufacturing solutions. With a robust CAGR of 18.63% forecasted between 2025 and 2030, the market is poised for remarkable growth, reflecting a broader industry shift toward innovation, automation, and sustainability. Continuous bioprocessing offers substantial advantages over traditional batch methods—including enhanced product consistency, reduced operational costs, and improved process efficiency—making it increasingly attractive to pharmaceutical and biotechnology companies worldwide.

As chronic diseases and demand for biologics continue to rise, coupled with advancements in single-use technologies, real-time analytics, and AI-driven process control, continuous manufacturing is set to become the new standard in biologic drug production. Supportive regulatory frameworks from agencies such as the FDA and EMA further facilitate this transition, encouraging adoption through guidance and faster approvals.

Looking ahead, regions like North America will continue to lead the market due to their advanced infrastructure and high investment levels, while emerging markets such as India will offer strong growth opportunities. Key segments like monoclonal antibodies and consumables & reagents will remain central to revenue generation. In an era that demands flexible, rapid-response manufacturing—especially in light of global health emergencies—continuous bioprocessing stands out as a pivotal solution shaping the future of biologics production.

0 notes

Text

Trends and Forecasts in the Second Life Industrial Robot Market

The Second Life Industrial Robot MarketSecond Life Industrial Robot Market is rapidly expanding as businesses increasingly seek cost-effective automation solutions across manufacturing, logistics, and automotive sectors. These pre-owned, refurbished robots offer a budget-friendly alternative to new systems while delivering reliable performance and extended lifecycles. Growing trends include advanced refurbishing services, AI integration, and alignment with Industry 4.0 technologies, enhancing robot adaptability and efficiency. Despite challenges like standardization gaps, compatibility issues, and skilled labor shortages, the market benefits from rising demand driven by cost optimization and sustainability efforts. With ongoing innovations and a focus on circular economy practices, the second-life robot market is poised for significant growth and greater adoption worldwide.

Market Segmentation:

1. By End Use:

Industrial

Waste Recycling

Others

2. By Type of Refurbishment:

New Controller Technology

Others

3. By Region:

North America

Europe

Asia-Pacific

Rest of the World

Key Market Players

ABB

FANUC

IRS Robotics

Key Demand Drivers

Inexpensive Automation for Small and Medium Businesses: Because second-life robots drastically lower startup costs, automation is now affordable for manufacturers on a budget as well as small and mid-sized businesses (SMEs). This affordability is especially alluring in budget-conscious competitive industries and growing markets.

Goals for the Circular Economy and Sustainability: Businesses are adopting sustainable practices as a result of increased environmental awareness and more stringent e-waste rules. In line with circular economy concepts, refurbished robots prolong the useful life of current gear while lowering the load on landfills and conserving vital resources.

Improvements in Technology: Refurbished robots are becoming more versatile thanks to improved controller systems, AI integration, and machine learning applications. These improvements make older models more useful in high-precision settings and smart factories by enabling them to function on par with machines of the latest generation.

Market Challenges

Absence of Standardized Procedures for Renovation: Variations in robot safety, dependability, and quality caused by inconsistent refurbishing procedures among vendors may worry end users and restrict further adoption.

Integration Difficulties: Connecting legacy systems to automation platforms, Industry 4.0 frameworks, or contemporary software environments may necessitate extensive adaptation. Potential customers may be turned off by these integration fees, which can cancel out any initial savings.

Lack of Skilled Workers: Industrial robot maintenance and repair require specialized technical knowledge. The consistency of refurbished equipment quality and the scalability of services can be affected by a shortage of qualified personnel.

Get your hands on this Sample Report to stay up-to-date on the latest developments in the Second Life Industrial Robot Market.

Gain deep information on Robotics and Automation Market. Click Here!

Future Outlook

Through 2030, the market for used industrial robots is anticipated to develop significantly due to the combined demands of sustainability and economic efficiency. The performance of reconditioned robots will continue to improve with the development of AI-enabled control systems and modular modifications, making them more and more feasible for high-end industrial applications. With the help of favorable government policies, growing SME automation, and fast industrialization, the Asia-Pacific area is expected to grow at the fastest rate. Because of its well-established robotics infrastructure and advanced refurbishing skills, North America is expected to continue to hold its dominant position.

Conclusion

With its perfect blend of cost, sustainability, and performance, the second life industrial robot market is becoming a vital part of the worldwide automation scene. Refurbished robots are turning out to be a valuable asset for contemporary industry as the need for intelligent, environmentally friendly, and scalable automation solutions increases. Even if there are still issues with standardization and integration today, industry cooperation, technical advancement, and training programs should help to lessen them over time. The market for second-life robots is positioned for long-term growth and change because to strong regional demand and growing environmental concern.

#Second Life Industrial Robot Market#Second Life Industrial Robot Industry#Second Life Industrial Robot Report#robotics#automation

0 notes

Text

From Rolls to Retail: The Journey of Paper Bag Manufacturing

In an era increasingly defined by sustainability and eco-conscious choices, the humble paper bag has emerged as a symbol of responsible consumption. Behind this everyday product lies a marvel of modern manufacturing—the paper bag machine. Combining mechanical precision with environmental awareness, paper bag machines have become a critical tool in both industrial packaging and the global effort to reduce plastic waste.Get more news about paper bag machine,you can vist our website! Paper bag machines are highly automated systems designed to transform rolls of kraft paper or recycled paper into finished bags of various shapes and sizes. These machines can produce flat or square-bottom bags, with or without handles, depending on the configuration. As businesses and consumers alike shift toward greener packaging alternatives, demand for paper bags—and by extension, paper bag machinery—has soared across the globe. The process begins with feeding large rolls of paper into the machine’s unwinding system, which precisely aligns the material before it moves into the folding section. Here, the paper is shaped into the desired bag profile using a combination of rollers, creasing devices, and glue applicators. Advanced machines incorporate servo motors and programmable logic controllers (PLC) to ensure real-time adjustments and tight quality control. This high-speed automation enables manufacturers to produce thousands of bags per hour with minimal labor input and consistent output quality. One of the defining features of modern paper bag machines is their adaptability. Manufacturers can quickly switch between different bag sizes, thicknesses, and handle designs to meet custom client requirements. Integration with printing modules allows for brand logos, product information, or decorative patterns to be applied directly onto the bags during production—an especially valuable feature for the retail and food-service industries. The environmental benefits of paper bag machines are equally significant. With increasing bans on single-use plastics in many countries, paper bags have stepped in as a recyclable, biodegradable alternative. Machine producers have responded by offering systems that work efficiently with recycled paper and water-based adhesives, reducing energy consumption and minimizing environmental impact during the manufacturing process. Globally, regions like Asia, Europe, and North America have witnessed rapid growth in the paper bag machine market. In China and India, rising consumer awareness and government-led plastic reduction initiatives have spurred significant investment in domestic manufacturing. Meanwhile, European companies have focused on upgrading machine precision and efficiency, contributing to a competitive, innovation-driven industry. Despite their advantages, paper bag machines are not without challenges. The cost of raw paper, machine maintenance, and the need for skilled operators can impact profitability. Nevertheless, ongoing technological improvements—such as smart diagnostics, real-time monitoring, and modular machine design—are steadily addressing these issues and pushing the boundaries of what's possible. In conclusion, paper bag machines are more than just production equipment—they are enablers of a global movement toward sustainable packaging. By marrying mechanical engineering with environmental innovation, these machines stand at the crossroads of commerce and conscience, quietly supporting a greener tomorrow with every fold and seal.

0 notes

Text

Basecoater Market Expands with Advancements in Sustainable Coating Technologies

The global basecoater market, valued at US$ 352.3 million in 2024, is projected to grow at a compound annual growth rate (CAGR) of 4.2%, reaching US$ 532.1 million by 2034, according to a recent report by FactMR. This growth reflects the increasing demand for precision coating solutions in industries such as automotive, packaging, and electronics, driven by technological advancements and the need for durable, high-quality finishes.

Market Dynamics and Key Drivers

Basecoaters, specialized machines used to apply uniform base coatings to substrates, are critical in industries requiring precision and durability. These machines ensure consistent application of coatings, enhancing product aesthetics and functionality. The report highlights that the rising demand for eco-friendly and high-performance coatings, particularly in automotive and packaging, is a primary driver. The shift toward sustainable materials and processes is pushing manufacturers to adopt advanced basecoating technologies that minimize waste and environmental impact.

The packaging industry, in particular, is a significant contributor, with basecoaters used to apply protective and decorative coatings to materials like paperboard and flexible packaging. The report notes that the automotive sector’s focus on lightweight, corrosion-resistant coatings is also driving demand, as basecoaters enable precise application of primers and base layers that enhance vehicle durability and aesthetics.

Analytical Perspective: The Precision Coating Ecosystem

To analyze the basecoater market, we propose the Precision Coating Ecosystem, which views the market as an interconnected system of technological innovation, industrial applications, and regulatory influences. This framework highlights how basecoaters enable precision, sustainability, and efficiency in coating processes.

1. Technological Innovation: Advancing Coating Precision

Basecoaters are evolving with advancements in automation and digital controls, enabling precise application and reduced material waste. The report emphasizes that innovations like robotic arms and IoT-enabled basecoaters are improving efficiency and consistency, particularly in high-volume industries like automotive and electronics. These technologies allow for real-time monitoring and adjustments, ensuring optimal coating thickness and quality.

2. Industrial Applications: Diverse and Expanding

The versatility of basecoaters extends across industries, from automotive primers to food-grade packaging coatings. The report projects that the packaging segment will lead due to the rising demand for sustainable, recyclable packaging. In electronics, basecoaters are used to apply protective coatings to circuit boards, enhancing durability. This ecosystem thrives on the ability of basecoaters to adapt to diverse substrates and coating types, driving market growth.

3. Regulatory Influences: Sustainability and Compliance

Stringent environmental regulations are pushing industries to adopt eco-friendly coatings and processes. Basecoaters that support water-based and low-VOC (volatile organic compound) coatings are gaining traction, aligning with global sustainability goals. The report notes that regulatory compliance is a key driver, particularly in Europe and North America, where environmental standards are rigorous.

Regional Insights and Market Opportunities

North America and Europe dominate the basecoater market due to their advanced manufacturing sectors and strict environmental regulations. The Asia-Pacific region, led by China and India, is expected to witness the fastest growth, driven by rapid industrialization and increasing demand for automotive and consumer electronics. The report highlights that emerging markets in Latin America and the Middle East offer growth potential as infrastructure development accelerates.

Challenges and Competitive Landscape

The high cost of advanced basecoating equipment is a significant challenge, particularly for small and medium-sized enterprises. The report notes that the complexity of integrating basecoaters into existing production lines can also hinder adoption. However, manufacturers are addressing these challenges by offering modular and cost-effective solutions.

Key players, such as Dürr AG and Nordson Corporation, are investing in R&D to develop energy-efficient and automated basecoaters. Strategic partnerships with coating material suppliers are enhancing product compatibility, ensuring seamless integration into industrial processes. The report highlights that innovation in eco-friendly technologies is a key competitive strategy.

Future Outlook: A Pillar of Sustainable Manufacturing

The basecoater market is set to play a critical role in the shift toward sustainable and precise manufacturing. The Precision Coating Ecosystem underscores the market’s potential to drive efficiency and environmental responsibility. Emerging trends, such as the adoption of AI-driven coating systems and bio-based coatings, will further enhance market growth. As industries prioritize sustainability, basecoaters will remain essential for delivering high-quality, eco-friendly finishes.

0 notes

Text

Innovations in Oscillatory Therapy Boost Airway Clearance Segment

Global Mucus Clearance Devices Market to Surpass USD 847 Million by 2028, Driven by Rising Respiratory Health Challenges and Homecare Adoption

The Global Mucus Clearance Devices Market is projected to exceed USD 847 million by 2028, expanding at a compound annual growth rate (CAGR) of approximately 6.1%. This growth is attributed to the rising prevalence of respiratory illnesses such as chronic obstructive pulmonary disease (COPD), cystic fibrosis, bronchiectasis, and asthma, especially in aging populations and regions with high exposure to air pollution and smoking.

These devices are vital in managing mucus accumulation in the lungs, reducing infection risk, improving oxygen exchange, and preventing complications. Technologies such as positive expiratory pressure (PEP) devices, oscillatory PEP systems, high-frequency chest wall oscillation (HFCWO) vests, cough assist machines, and intrapulmonary percussive ventilation (IPV) are increasingly utilized across hospitals, homes, and clinics.

To Get Free Sample Report : https://www.datamintelligence.com/download-sample/mucus-clearance-devices-market

Key Market Drivers

1. Rising Incidence of Chronic Respiratory Diseases Chronic conditions like COPD and cystic fibrosis affect millions globally. For instance, over 16 million people in the U.S. have been diagnosed with COPD. Effective mucus clearance is essential to reducing flare-ups, hospitalizations, and mortality in these patients.

2. Global Aging Population Older adults are more prone to impaired mucociliary clearance, making them more dependent on mechanical airway clearance therapies. This demographic shift supports long-term market expansion.

3. Growing Adoption of Homecare and Self-Management Solutions The rise in remote patient care and non-hospital interventions has led to increased demand for user-friendly, portable devices. Home-based treatments reduce costs and support chronic disease management.

4. Technological Innovations The development of wearable HFCWO vests, app-enabled tracking, automated therapy control, and personalized treatment settings has made airway clearance devices more effective and accessible.

5. Rise in Post-COVID-19 Respiratory Support Needs Long-COVID has highlighted the need for airway support in recovering patients. Mucus clearance devices are increasingly used in post-infection rehabilitation programs.

Regional Market Insights

North America North America remains the dominant market, contributing over 40% of total revenue. This is driven by high diagnosis rates of chronic respiratory illnesses, greater awareness, well-established healthcare infrastructure, and significant homecare utilization.

Europe Europe is a mature market supported by public health reimbursement policies, aging populations, and national respiratory disease prevention programs. Germany, the UK, and France lead regional demand.

Asia-Pacific This region is expected to register the fastest growth through 2028, due to expanding healthcare infrastructure, rising urban pollution, and growing elderly populations. Countries like India, China, and Japan are investing in pulmonary care innovation and access.

Latin America & Middle East/Africa These markets are evolving as awareness increases and investments in healthcare modernization improve access to respiratory therapies.

Application Areas and End Users

Hospitals and Clinics These facilities represent the largest segment due to the need for clinical monitoring and advanced device capabilities in critical care and pulmonary rehabilitation.

Homecare Settings With the rise of outpatient and chronic disease management, homecare solutions are gaining momentum. Devices that are compact, battery-powered, and easy to use are leading in this segment.

Ambulatory Surgical Centers (ASCs) ASCs utilize mucus clearance devices for pre- and post-operative respiratory support, especially in patients with underlying pulmonary conditions.

Rehabilitation Centers Specialty respiratory rehab centers are adopting airway clearance devices for long-term disease management and post-surgical recovery.

Get the Demo Full Report : https://www.datamintelligence.com/enquiry/mucus-clearance-devices-market

Market Challenges

Cost and Reimbursement Barriers In developing markets, affordability and lack of insurance reimbursement for mucus clearance devices limit adoption.

Training and Compliance Issues Proper usage often requires patient education and periodic therapist supervision, which can be challenging in homecare settings.

Limited Awareness in Emerging Economies Despite growing respiratory disease prevalence, knowledge about airway clearance techniques remains low in many regions.

Industry Trends and Innovations

Smart Vest Systems High-frequency chest wall oscillation vests with Bluetooth-enabled control and real-time performance tracking are gaining favor in both hospitals and homes.

Telehealth Integration Airway clearance devices that transmit usage data to healthcare providers are supporting remote care models and improving therapy adherence.

Clinical Trials and Regulatory Approvals Several companies are conducting studies to demonstrate improved outcomes and secure approvals for broader indications.

Strategic Partnerships Mergers, acquisitions, and distribution collaborations are shaping market competition. Leading players are focusing on expanding product portfolios and regional penetration.

Key Players

Major companies in the mucus clearance devices market include:

Hill-Rom (now part of Baxter) – known for SmartVest

Philips Respironics

Electromed

Monaghan Medical Corporation

Smiths Medical

PARI GmbH

These players are actively investing in R&D, digital health integration, and global distribution to maintain competitive advantage.

Conclusion

The global mucus clearance devices market is entering a transformative phase, driven by rising chronic respiratory conditions, aging demographics, and increasing preference for home-based healthcare. With significant technological progress and wider clinical acceptance, the market is poised to exceed USD 847 million by 2028. North America remains dominant, while Asia-Pacific is set for rapid expansion. From smart vests to portable oscillatory devices, the future of mucus clearance will be shaped by innovation, accessibility, and patient-centric care models.

#Mucus Clearance Devices Market#Mucus Clearance Devices Market share#Mucus Clearance Devices Market size

0 notes

Text

Automated Endoscope Reprocessing Market Overview: Global Industry Snapshot

The Automated Endoscope Reprocessing Market has emerged as a pivotal segment within the broader landscape of medical device disinfection and sterilization. As minimally invasive surgeries (MIS) continue to gain traction, the demand for high-level disinfection of endoscopic instruments has become increasingly critical. Automated endoscope reprocessors (AERs) have thus transformed from optional support systems into indispensable components of modern healthcare infrastructure.

What is Automated Endoscope Reprocessing?

Automated Endoscope Reprocessing refers to the use of specialized machines to clean, disinfect, and dry endoscopes after clinical use. The process ensures a standardized, consistent, and safe method of preparing endoscopes for reuse. AERs reduce the risks associated with human error in manual cleaning and provide traceable documentation to meet stringent regulatory compliance standards.

Market Size and Dynamics

The global Automated Endoscope Reprocessing Market has experienced consistent growth over the past decade. This growth is driven by a combination of rising surgical procedures, hospital-acquired infection (HAI) prevention protocols, and global health initiatives pushing for sterilization automation in medical settings. The market is projected to continue expanding from 2025 to 2032 due to:

Increasing geriatric population and chronic illnesses requiring endoscopy

Surge in demand for MIS procedures

Regulatory enforcement for infection control

Rising investment in hospital infrastructure

As of 2024, the market valuation is estimated to be in the range of USD 1.5 to 2 billion, with robust CAGR expectations of around 8–10% through the forecast period.

Key Market Segments

The Automated Endoscope Reprocessing Market can be segmented based on product types, end users, and regions:

Product Types: Single basin, double basin, and advanced multi-cycle units

End Users: Hospitals, ambulatory surgical centers (ASCs), specialty clinics

Geography: North America leads due to strict regulations and advanced hospital facilities, followed by Europe and Asia-Pacific, where rapid infrastructure growth is boosting demand.

Drivers of Market Growth

Several factors fuel the adoption of automated endoscope reprocessors:

Stringent Regulatory Requirements: Regulatory bodies like the U.S. FDA, CDC, and European CE authorities mandate validated cleaning protocols.

HAI Prevention and Patient Safety: AERs reduce the risk of cross-contamination and infection outbreaks.

Growing Demand for Reusable Endoscopes: Single-use scopes are costlier in the long term; thus, proper reprocessing becomes essential.

Operational Efficiency: Automated systems reduce manpower needs and provide traceable reports for compliance audits.

Challenges in the Market

Despite its rapid growth, the Automated Endoscope Reprocessing Market faces several obstacles:

High Initial Investment: The cost of acquiring and maintaining AER systems may be prohibitive for small healthcare providers.

Complexity in Operation and Maintenance: Technical training and ongoing support are critical to ensure safe and correct use.

Infrastructure Gaps in Low-Income Regions: Limited access to utilities and space can hinder adoption in rural or underdeveloped areas.

Competitive Landscape

Major players in the Automated Endoscope Reprocessing Market include:

Olympus Corporation

Getinge AB

Cantel Medical (Steris)

Ecolab Inc.

Advanced Sterilization Products (ASP)

These companies are investing in technological innovation, AI integration, and ergonomically designed units to offer better cleaning efficiency, traceability, and operator convenience.

Global Trends and Future Outlook

Global trends in the Automated Endoscope Reprocessing Market include the adoption of smart reprocessors with integrated software systems for performance monitoring, IoT-based devices for maintenance alerts, and energy-efficient designs to align with green hospital initiatives.

Moreover, the COVID-19 pandemic has led to heightened awareness of sterilization and disinfection in healthcare settings. The resulting surge in sterilization compliance continues to positively influence market growth even in the post-pandemic era.

Conclusion

The Automated Endoscope Reprocessing Market represents a critical aspect of infection control within the healthcare system. With rising emphasis on patient safety, regulatory compliance, and healthcare automation, the market is poised for significant expansion in the coming years. As technology evolves and cost-effectiveness improves, adoption is expected to widen globally—particularly in emerging healthcare markets seeking to enhance their clinical hygiene standards.

0 notes

Text

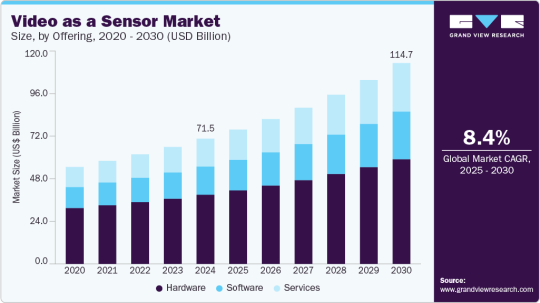

The Future of Analytics: How Video As A Sensor is Redefining Data Capture

The global Video As A Sensor Market, estimated at USD 71.50 billion in 2024, is forecast to reach USD 114,664.7 million by 2030, exhibiting a Compound Annual Growth Rate (CAGR) of 8.4% from 2025 to 2030. This growth is propelled by rapid technological advancements that have transformed conventional video systems and recording tools into sophisticated, intelligent decision-making instruments.

A significant catalyst for VaaS adoption is the technology's capacity to deliver real-time insights, including capabilities like facial recognition, anomaly detection, and behavior prediction. These features render VaaS highly suitable for contemporary security and surveillance systems, where prompt threat identification is crucial. Beyond security applications, the versatility of video sensors is increasingly evident across various sectors. In smart city initiatives, they play a vital role in enhancing urban infrastructure, contributing to public safety, optimizing energy consumption, and improving waste management efforts.

Key Market Trends & Insights:

North American Dominance: North America led the market with a 35.5% share in 2024. This leadership is driven by substantial investments in advanced surveillance systems and the early adoption of cutting-edge technologies such as Artificial Intelligence (AI) and machine learning.

U.S. Market Expansion: The video as a sensor market in the U.S. is experiencing notable growth, corresponding with increasing regional demand. The accelerating pace of industrialization and the integration of advanced technologies are key factors driving this market's expansion.

Video Surveillance Product Leadership: By product type, video surveillance accounted for the largest market revenue share in 2024. This segment's dominance is primarily due to escalating security concerns across residential, commercial, and public domains, coupled with rapid advancements in technologies like AI-driven analytics, cloud computing, and high-resolution imaging.

Security & Surveillance Application Dominance: In terms of application, the security and surveillance segment held the largest market revenue share in 2024. This is attributed to VaaS's ability to automate real-time threat detection, significantly reduce false alarms, and efficiently manage large volumes of video footage, thereby lessening the workload on security personnel.

Commercial End-Use Sector Growth: The commercial segment accounted for the largest market revenue share in 2024. This is driven by the growing need for enhanced security and surveillance solutions in commercial environments, including office buildings and retail establishments, to protect assets and ensure safety.

Order a free sample PDF of the Video As A Sensor Market Intelligence Study, published by Grand View Research.

Market Size & Forecast

2024 Market Size: USD 71.50 Billion

2030 Projected Market Size: USD 114,664.7 Million

CAGR (2025-2030): 8.4%

North America: Largest market in 2024

Asia Pacific: Fastest growing market

Key Companies & Market Share Insights

Leading firms in the Video As A Sensor (VaaS) market are employing a range of strategic initiatives to expand their market presence. These primarily include product launches and developments, alongside expansions, mergers and acquisitions, contracts, agreements, partnerships, and collaborations. Companies are leveraging diverse techniques to enhance market penetration and strengthen their competitive standing.

Axis Communications, a prominent player, specializes in network video surveillance and intelligent security solutions. Their comprehensive offerings, including a wide array of cameras, video management software, analytics, and access control systems, enable businesses and smart cities to utilize video as a sensor for real-time insights, improved safety, and enhanced operational efficiency. Axis's commitment to innovation, sustainability, and fostering a robust partner ecosystem underpins their goal of contributing to a smarter and safer global environment.

Hikvision is a significant force in video-centric IoT solutions, with a strong focus on advanced video-as-a-sensor technologies for both security and intelligent monitoring. By integrating state-of-the-art AI, deep learning, and high-performance video analytics, Hikvision delivers real-time surveillance, environmental sensing, and actionable insights. Their solutions are deployed across various sectors globally, including smart cities, transportation systems, and commercial enterprises.

Key Players

Axis Communications AB

Hangzhou Hikvision Digital Technology Co., Ltd.

Bosch Sicherheits systeme GmbH

Dahua Technology Co., Ltd.

Sony Corporation

Honeywell International Inc.

Sportradar AG

i-PRO

Johnson Controls

OMNIVISION

Browse Horizon Databook for Global Video As A Sensor Market Size & Outlook

Conclusion

The global Video As A Sensor (VaaS) market is experiencing rapid growth, driven by technological advancements transforming video into intelligent decision-making tools. Its ability to provide real-time insights makes it crucial for security, surveillance, and smart city initiatives. North America leads the market, with video surveillance and security applications dominating across commercial sectors. Leading companies are strategically innovating and collaborating to further expand their market share in this dynamic industry.

0 notes

Text

Marck Industries: Trusted Manufacturer of Premium Elevator Spare Parts

Why Reliable Spare Parts Matter in Elevator Systems

Elevators are essential in modern buildings—transporting people and goods swiftly and safely. Downtime due to broken or worn-out parts isn’t just inconvenient—it can impact safety, building efficiency, and tenant satisfaction. That’s why having a dependable source of high-quality spare parts is vital.

What Sets Marck Industries Apart

1. Decades of Expertise

With years of experience in manufacturing elevator components, Marck Industries understands the stringent requirements of vertical transportation—ensuring every part is engineered for precision, durability, and compliance with international safety standards.

2. Comprehensive Product Portfolio

From mechanical to electrical systems, we supply a full range of elevator parts, including:

Controller boards & PCBs

Inverter and VFD units

Proximity switches & sensors

Door lock and safety gear

Brake assemblies & drums

Buffers, rollers, and pulleys

Cabin fixtures: buttons, display panels, handrails

3. Precision Manufacturing

Utilizing CNC machining, injection molding, and automated PCB assembly, each component is produced to exact tolerances—ensuring fit and function with OEM performance or better. Strict quality checks, including EN 81, ASME A17.1, and ISO audits, guarantee consistency.

4. Certified Quality & Safety

Marck operates with certifications to:

ISO 9001 Quality Management

CE marking and compliance

Adherence to EN (Europe) and ASME (North America) elevator safety codes

These credentials ensure safe, global-grade parts.

5. Custom Solutions & Adaptability

Recognizing that every elevator system is unique, Marck Industries excels in custom engineering—from tailored connectors and cables to complete PCB re-engineering—while maintaining cost and lead-time efficiency.

Benefits of Partnering with Marck Industries

Advantage

Impact

High Uptime & Quick Delivery

Minimize downtime with rapid part replacement and fast shipping

Competitive Pricing

Optimized production lowers costs without compromising quality

Global Support Infrastructure

Sales and technical teams available round-the-clock across regions

Extended Product Warranty

Confidence via long-term warranty and support packages

Serving Diverse Market Segments

Residential Buildings: Reliable replacements for passenger-lift maintenance.

Commercial Complexes: Durable components suited for high-traffic usage.

Industrial Facilities: Heavy-duty parts designed for freight and goods lifts.

OEM Collaborations: Contract manufacturing aligned with global elevator brands.

Quality Control & Testing Procedures

Each batch undergoes:

Incoming Material Inspection (IQC)

In-Process Monitoring (IPC)

Performance Testing: Load, endurance, vibration, and electrical tests

Final Audits & Certification

Partnering with Marck: How It Works

Initial Consultation Understand your system specs, OEM models, and usage patterns.

Quotation & Sample Approval We provide detailed proposals and offer test samples for validation.

Order & Production Ranging from small spare lots to mass production, with regular updates.

Technical & After-Sales Support Including troubleshooting, field assistance, and prompt RMA processes.

Ongoing Relationship We offer lifecycle support—even for legacy elevators requiring obsolete part replacements.

Elevate Your Operations with Marck Industries

Your elevator fleet deserves nothing less than reliable, certified parts that stand the test of time. Choose Marck Industries for precision, safety, and peace of mind—backed by technical excellence and global service reach.

Ready to discuss your parts needs? Contact our sales team or request a quote through the Marck Industries website today.

0 notes

Text

Global Capsule Fillers Market Growth Analysis 2025

Capsule fillers play a pivotal role in the pharmaceutical industry, enabling the efficient and precise encapsulation of various drug formulations. These specialized machines are designed to streamline the capsule-filling process, ensuring consistent dosage and quality control. As the demand for pharmaceuticals continues to rise globally, the capsule fillers market is poised for significant growth, driven by technological advancements and the need for enhanced production capabilities.

Get free sample of this report at : https://www.intelmarketresearch.com/download-free-sample/246/capsule-fillers

Market Overview:

Market Size and Projections:

In 2023, the global capsule fillers market was valued at US$ 223.8 million, reflecting the essential nature of these machines in pharmaceutical manufacturing.

The market is anticipated to reach US$ 321.1 million by 2030, witnessing a compound annual growth rate (CAGR) of 6.0% during the forecast period of 2024-2030.

Key Players and Market Concentration:

The global capsule fillers market is dominated by several major manufacturers, including Mettler Toledo, Syntegon, Sejong, Schaefer Technologies, IMA, ACG Worldwide, Lonza (Capsugel), Anchor Mark, and MG2.

In 2023, the world's top three vendors accounted for approximately 21% of the market's revenue, indicating a moderate level of market concentration.

This report aims to provide a comprehensive presentation of the global market for Capsule Fillers, with both quantitative and qualitative analysis, to help readers develop business/growth strategies, assess the market competitive situation, analyze their position in the current marketplace, and make informed business decisions regarding Capsule Fillers.

The Capsule Fillers market size, estimations, and forecasts are provided in terms of output/shipments (Units) and revenue ($ millions), considering 2023 as the base year, with history and forecast data for the period from 2019 to 2030. This report segments the global Capsule Fillers market comprehensively. Regional market sizes, concerning products by Type, by Application, and by players, are also provided.

For a more in-depth understanding of the market, the report provides profiles of the competitive landscape, key competitors, and their respective market ranks. The report also discusses technological trends and new product developments.

The report will help the Capsule Fillers manufacturers, new entrants, and industry chain related companies in this market with information on the revenues, production, and average price for the overall market and the sub-segments across the different segments, by company, by Type, by Application, and by regions.

Market Segmentation

By Company

Mettler Toledo

Syntegon

Sejong

Schaefer Technologies

IMA

ACG Worldwide

Lonza (Capsugel)

Anchor Mark

MG2

Qualicaps

Chin Yi Machinery

Feton

Fette Compacting

IRM Enterprises

Harro Hofliger

Hanlin Hangyu Industrial

Zhejiang Fuchang Machinery

Adinath International

by Type

Fully Automatic

Semi-automatic

Manual

by Application

Pharmaceutical Company

Nutraceutical Company

Biological Company

Other

Production by Region

North America

Europe

China

India

Consumption by Region

North America

U.S.

Canada

Asia-Pacific

China

Japan

South Korea

Southeast Asia

India

Europe

Germany

France

U.K.

Italy

Netherlands

Rest of Europe

South America

Mexico

Brazil

Rest of South America

Market Drivers:

Increasing Demand for Pharmaceuticals:

The growing global population, rising healthcare expenditure, and the prevalence of chronic diseases have fueled the demand for pharmaceuticals, driving the need for efficient and high-throughput capsule filling solutions.

Automation and Digitalization in Pharmaceutical Manufacturing:

The pharmaceutical industry's focus on automation, digitalization, and Industry 4.0 initiatives has driven the adoption of advanced capsule fillers with integrated control systems, data logging, and remote monitoring capabilities.

Regulatory Compliance and Quality Standards:

Stringent regulatory requirements and quality standards set by governing bodies, such as the Food and Drug Administration (FDA) and the European Medicines Agency (EMA), have prompted pharmaceutical companies to invest in precise and reliable capsule filling equipment.

Growing Demand for Specialized Dosage Forms:

The rise in demand for specialized dosage forms, such as delayed-release, enteric-coated, and sustained-release capsules, has necessitated the use of advanced capsule fillers capable of handling unique formulations and encapsulation processes.

Competitive Landscape:

The capsule fillers market is highly competitive, with established players and emerging companies vying for market share. Key strategies adopted by market participants include:

Technological Innovation: Companies are investing in research and development activities to introduce advanced capsule fillers with enhanced productivity, precision, and automation capabilities, catering to the evolving needs of the pharmaceutical industry.

Strategic Partnerships and Collaborations: Market players are forming partnerships and collaborations with pharmaceutical companies, research institutes, and regulatory bodies to gain insights into industry trends, regulatory requirements, and product development opportunities.

Expansion into Emerging Markets: With the increasing demand for pharmaceuticals in emerging markets, capsule filler manufacturers are expanding their global presence and exploring new market opportunities.

Mergers and Acquisitions: Strategic mergers and acquisitions are being pursued to consolidate market share, acquire complementary technologies, and expand product portfolios.

Focus on Customization and Flexibility: Companies are offering customized and flexible capsule filling solutions to cater to the specific needs of pharmaceutical manufacturers, accommodating various capsule sizes, formulations, and production volumes.

Get free sample of this report at : https://www.intelmarketresearch.com/download-free-sample/246/capsule-fillers

0 notes

Text

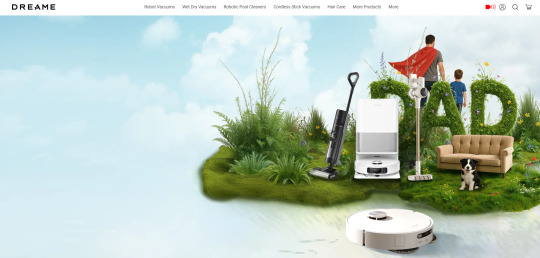

Top 10 Cleaning Robot Manufacturers in China

Cleaning Robots refer to autonomous devices specifically engineered to maintain floor surfaces through automated vacuuming and

mopping functions. These intelligent machines utilize cutting-edge technologies including LIDAR navigation, AI-powered path planning,

and smart suction systems to deliver thorough, hands-free cleaning. The core purpose of these robots is to provide a safer, more convenient,

and time-efficient solution for home and commercial cleaning, particularly in large spaces or hard-to-reach areas. China has emerged as

the global manufacturing center for robotic cleaning technology, housing numerous specialized manufacturers recognized for their innovative

designs, superior quality, and continuous technological advancements.

In this definitive industry guide, we will examine the top 10 floor cleaning robot manufacturers in China. You'll gain detailed insights into each

company's background, technological capabilities, product advantages, market positioning, and ideal use cases - all from the perspective of

an industry insider with over a decade of manufacturing experience. Whether you're a wholesaler, private label brand, or commercial buyer,

this guide will help you identify the perfect manufacturing partner for your specific business needs.

Brand

Strengths

Best For

1: LINCINCO

Premier OEM/ODM Specialist

OEM partners, tailored solutions

2: Ecovacs Robotics

Technology Leader

High-end residences and families of technology enthusiasts

3: Roborock

Premium Performance

Hard floor cleaning and quality-oriented users

4: Xiaomi Mijia

Value Leader

Entry-level market, young user group

5: Dreame Technology

Dreame Technology

Demand for technology-innovative products

6: ILIFE Robotics

Specialized Cleaning Solutions Expert

Special floor cleaning requirements

7: Kyvol

Smart Home Integration Leader

Smart home integration scenarios

8: Lefant

Compact Design Specialist

An apartment with low furniture

9: Proscenic

Commercial Cleaning Solutions

The field of commercial cleaning

10: Coredy

Balanced Value Provider

Basic cleaning of rental housing

1. LINCINCO - Premier OEM/ODM Specialist

Headquarters: Dongguan, Guangdong Established: 2018

Factory Area: 50,000㎡

Employee: 635 ( include 65 professionals)

135 sets of molding injection, molding machine 80-1400T.

Production lines: 11 finished product assembly lines, 4.5 finished product lines

Production Capacity:4 million units per year

Product Standard:

GB 4343.1-2009;GB 4706.1-2005;

GB 4706.7-2004;GB 17625.1-2012 Export Markets: 85% of production (North America, Europe, Asia)

Technical Specifications:

Navigation: LIDAR 4.0 + AI Visual (dual system)

Corner Cleaning:Mechanical arm extension,clean the corners

Suction Power: 5000Pa-10000Pa (adjustable)

Battery: 5200mAh lithium (120min runtime)

Noise Level: ≤65dB

Key Advantages:

Deep Customization: 15+ customizable points including:

Housing colors/materials

Voice prompt languages (supports 12 languages)

App interface branding

Cleaning mode presets

Rapid Prototyping: New samples ready in 7-10 days

Quality Assurance: 7 inspection points with <0.5% defect rate

Certifications: CE, FCC, RoHS, ERP, KC, PSE

Market Positioning:

SegmentPrice RangeMOQLead Time

Entry-level

$120-$180

500

25 days

Mid-range

$180-$280

300

30 days

Premium

$280-$400

200

35 days

Recent Development: Launched new AI-powered navigation system in Q1 2024, reducing cleaning time by 25% through optimized path algorithms.

Recommended For: Private label brands, wholesalers needing custom solutions, buyers targeting specific regional markets.

2. Ecovacs Robotics - Technology Leader

Headquarters: Suzhou, Jiangsu Annual Output: 3 million+ units R&D Investment: 8.7% of revenue

Flagship Model: DEEBOT X2 Omni

Navigation: AIVI 3.0 (AI Visual Interpretation)

Suction: 8000Pa (industry-leading)

Features: Auto-empty, auto-mop wash, voice control

Battery: 6400mAh (200min runtime)

Market Reach:

Sold in 60+ countries

1,200+ retail partners worldwide

37% market share in North America (2023)

Strengths: Best-in-class navigation technology, complete product ecosystem Weaknesses: Higher price point, limited customization options Recommended For: Tech-focused buyers, premium market segments

3. Roborock - Premium Performance

Production Base: Beijing Employees: 2,800+ (35% in R&D)

Technology Highlights:

ReactiveAI 2.0: Recognizes 42 object types

Sonic Mopping: 3,000 vibrations/minute

Dock Features: Hot water washing, 3-hour drying

2024 Models Comparison:

ModelSuctionBatteryPriceSpecial Feature

S8 Pro Ultra

5100Pa

5200mAh

$1,599

VibraRise 2.0

Q Revo

5500Pa

5000mAh

$899

Dual Spinning Mops

Dyad Pro

N/A

60min

$499

Wet/Dry Combo

Recent Achievement: Roborock S8 Pro Ultra won 2024 CES Innovation Award Recommended For: High-end residential market, tech enthusiasts

4. Xiaomi Mijia - Value Leader

Parent Company: Xiaomi Ecosystem Manufacturing Partners: 3 contract factories

Product Strategy:

Price Range: $200-$500

Refresh Cycle: 18 months

Smart Home Integration: Mi Home ecosystem

Market Performance:

#1 budget brand in Asia (32% market share)

15 million units sold globally (2023)

4.8/5 average customer rating

Recommended For: Price-sensitive markets, first-time buyers

5. Dreame Technology - Innovation Powerhouse

Owned By: Xiaomi (minority stake) Patents Held: 1,200+

Breakthrough Technologies:

Auto-Empty Station: 60-day capacity

Dual-Rotary Mopping: 180RPM

Cross-Brand Compatibility: Works with 3rd party apps

2024 Expansion:

New D10 series for European market

Partnership with Bosch for motor technology

$200 million R&D center under construction

Recommended For: Innovative retailers, smart home integrators

Comparison Table: Top 5 Manufacturers

ManufacturerStrengthPrice RangeMOQLead TimeBest For

LINCINCO

Customization

$120-$400

200

25-35d

OEM/Private Label

Ecovacs

Technology

$400-$1,500

1,000

45d

Premium Retail

Roborock

Performance

$500-$1,600

800

50d

High-End Market

Xiaomi

Value

$200-$500

5,000

20d

Mass Market

Dreame

Innovation

$300-$800

1,500

30d

Tech Retailers

6. ILIFE Robotics - Specialized Cleaning Solutions Expert

Headquarters: Shenzhen, Guangdong Established: 2007 Annual Production: 2.4 million units

Technical Specifications:

Navigation System: Gyroscopic navigation with anti-drop sensors

Suction Power: 1000-2000Pa (adjustable)

Specialized Models:

V3s Pro: Pet hair specialist with tangle-free rubber brush

A4s: Hard floor expert with triple cleaning system

W400: Wet/dry hybrid for complete floor care

Manufacturing Capabilities:

FacilityAreaProduction LinesDaily Output

Shenzhen

45,000㎡

8

8,000 units

Dongguan

30,000㎡

5

5,000 units

Market Performance:

85% export ratio (North America 60%, Europe 25%)

35% YOY growth in pet specialty models

4.3/5 average Amazon rating across products

Recommended For: Retailers targeting pet owners, hard surface cleaning specialists

7. Kyvol - Smart Home Integration Leader

Headquarters: Nanjing, Jiangsu R&D Team: 150+ engineers Patents Held: 87 (including 12 invention patents)

Smart Connectivity Features:

App Control: Kyvol Home App (iOS/Android)

Voice Control: Amazon Alexa, Google Assistant

Smart Scheduling: AI-powered cleaning planning

Matter Protocol: Full compatibility with smart home ecosystems

Product Line Overview:

SeriesKey FeaturePrice RangeTarget Market

E30

Basic Smart

$199-$249

Entry-level

E31

Matter Support

$279-$329

Smart Homes

P50

AI Camera

$399-$449

Premium

Quality Certifications:

CE, FCC, RoHS

ISO 9001:2015 certified

Google Home official partner

Recommended For: Smart home retailers, tech-focused distributors

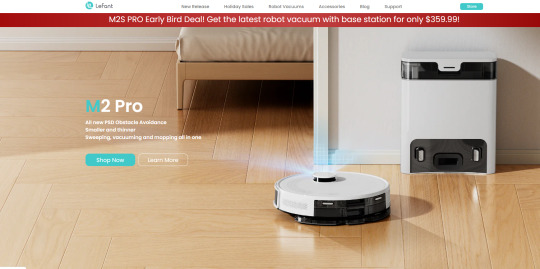

8. Lefant - Compact Design Specialist

Factory Location: Zhongshan, Guangdong Production Area: 28,000㎡ Workforce: 800+ employees

Design Innovations:

Ultra-Low Profile: 2.85" height (industry thinnest)

Modular Design: Quick-change components

Quiet Operation: As low as 52dB (library-quiet)

Product Comparison:

ModelHeightNoiseSuctionBattery

M210

2.85"

52dB

2000Pa

2600mAh

M280

3.15"

55dB

2500Pa

3000mAh

M350

3.50"

58dB

3000Pa

3200mAh

Market Position:

#1 in compact robots (32% market share)

90% customer satisfaction rate

18-month product lifecycle

Recommended For: Apartment dwellers, urban retailers, pet owners

9. Proscenic - Commercial Cleaning Solutions

Parent Company: Proscenic Technology Group Established: 1996 Global Offices: 5 countries

Commercial Product Line:

UV Sterilization Series:

Hospital-grade disinfection

99.9% germ elimination rate

50,000 sq.ft daily coverage

Large-Area Series:

6000mAh battery (8h runtime)

5000Pa suction

Fleet management software

Window Cleaning Series:

25kg suction force

IP65 waterproof

200m cable length

Certifications:

ISO 13485 (Medical Devices)

EN 60601-1 (Medical Electrical Equipment)

UL Commercial Grade

Recommended For: Hotel chains, hospital suppliers, facility managers

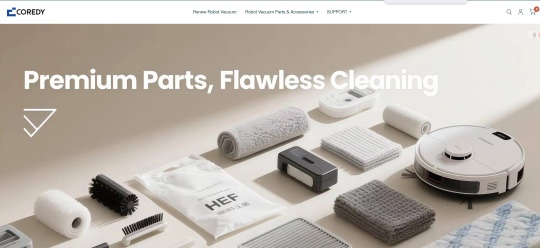

10. Coredy - Balanced Value Provider

Manufacturing Base: Ningbo, Zhejiang Export Experience: 12 years Main Markets: Europe (60%), North America (30%)

Value Proposition:

Price-Performance Ratio: 30% below major brands

Reliability: <2% return rate

Simplicity: One-button operation

Product Matrix:

SeriesSuctionBatteryNavigationPrice

R300

2000Pa

2600mAh

Random

$199

R500

2500Pa

3000mAh

Gyro

$249

R700

3000Pa

3200mAh

LDS

$299

Production Capacity:

3 fully automated production lines

40,000 units/month capacity

15-day standard lead time

Recommended For: Value-focused retailers, secondary product lines

Detailed Comparison: 6-10 Manufacturers

CriteriaILIFEKyvolLefantProscenicCoredy

Specialization

Pet/Hard Floors

Smart Home

Compact

Commercial

Value

Price Range

$199-$399

$199-$449

$179-$349

$499-$2,999

$199-$299

MOQ

500

300

400

100

500

Lead Time

30d

25d

28d

45d

20d

Customization

Limited

UI Only

Colors

Full OEM

None

Best For

Specialty Retail

Tech Stores

Urban

B2B

Mass Market

How to Choose Your Ideal Manufacturer?

Selection Matrix:

NeedBudgetRecommended Choice

Custom OEM/ODM

Medium

LINCINCO

Cutting-Edge Tech

High

Ecovacs

Premium Performance

High

Roborock

Mass Market Value

Low

Xiaomi

Innovative Features

Medium

Dreame

Pet Hair Solutions

Medium

ILIFE

Smart Home Focus

Medium

Kyvol

Compact Design

Low-Med

Lefant

Commercial Grade

High

Proscenic

Balanced Value

Medium

Coredy

Why LINCINCO Stands Out for Business Buyers?

While all these manufacturers have strengths, LINCINCO offers unique advantages for B2B buyers:

True Customization: Unlike brands focused on their own products, we adapt to your specifications

Flexible MOQs: Starting from 200 units vs. typical 1,000+ minimums

Faster Time-to-Market: 30-day average production cycle vs. industry-standard 45-60 days

Direct Factory Pricing: No brand premium markup

Quality Assurance: Our defect rate is 80% lower than industry average

Recent Client Success: Helped a European retailer launch their private label line with 15 customized models in just 4 months.

Conclusion

China's cleaning robot manufacturers offer unparalleled variety from budget to premium segments. For private label and customized

solutions, LINCINCO provides the ideal combination of quality, flexibility and value. Meanwhile, brands like Ecovacs and Roborock lead

in consumer-facing technology. Your optimal choice depends on target market, technical requirements and business model.

0 notes

Text

Machine Tending Robots Market Analysis and Forecast

Machine tending robots are specialized industrial systems designed to automate the loading, unloading, and overall management of machine operations within manufacturing environments. Equipped with advanced sensors and control systems, these robots execute repetitive tasks highly, enhancing productivity, improving workplace safety, and reducing labor costs. Their integration across various industrial sectors supports streamlined production processes and optimizes operational efficiency.

The machine tending robots industry was valued at $9,873.9 million in 2024 and is projected to reach $25,598.1 million by 2034, growing at a CAGR of 9.99% during the forecast period.

Industrial Impact

By automating monotonous, dangerous, or highly precise operations, machine tending robots have completely changed the production scene. Faster production cycles, less human error, and consistent product quality have resulted from their use. Furthermore, by reducing human exposure to potentially hazardous jobs, these devices have improved workplace safety.

Beyond automation, these robots promote innovation, assist company scalability, and reallocate workers to more strategic positions, all of which result in cost savings. They are positioned as important facilitators in the creation of smart industrial environments because to their alignment with the objectives of digital transformation.