#Policyholder contract

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr Inc. has $15.1M in annual revenue.

Text

What is an insurance policy? Explanation of items to be included, necessary situations, and precautions for handling

What is an insurance policy? Explanation of items to be included, necessary situations, and precautions for handling What is an insurance policy? An insurance policy is a legally binding contract between an individual (or entity) and an insurance company. It outlines the terms and conditions of the insurance coverage provided by the company in exchange for the payment of premiums. Key elements…

View On WordPress

#best home insurance#cheapest homeowners insurance#Claim process#Coverage terms#insurance jobmode#Insurance policy#Insurance policy definition#Policy benefits#Policyholder contract#Premium payments#property insurance#Types of Mortgages

0 notes

Text

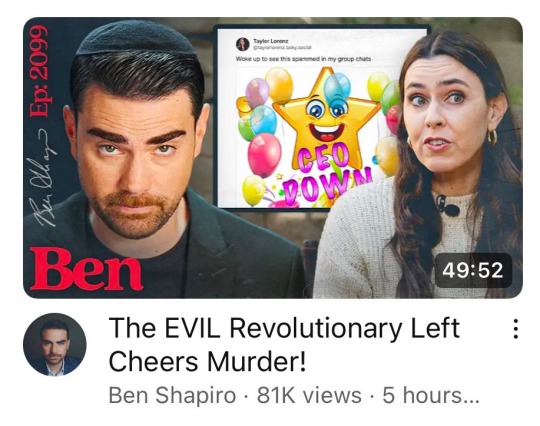

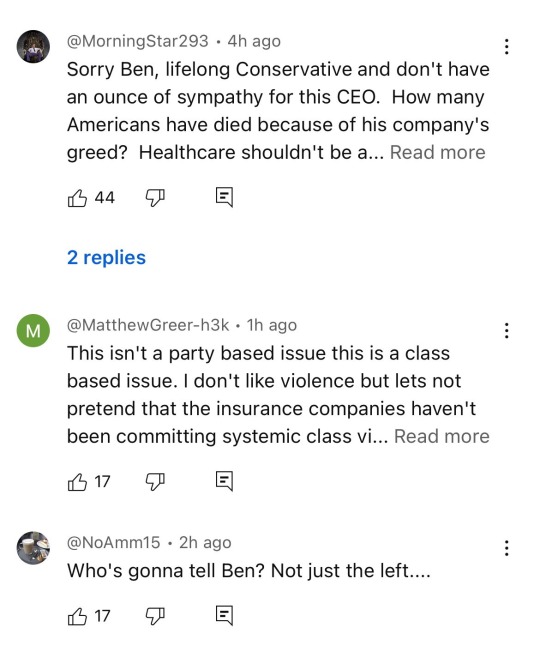

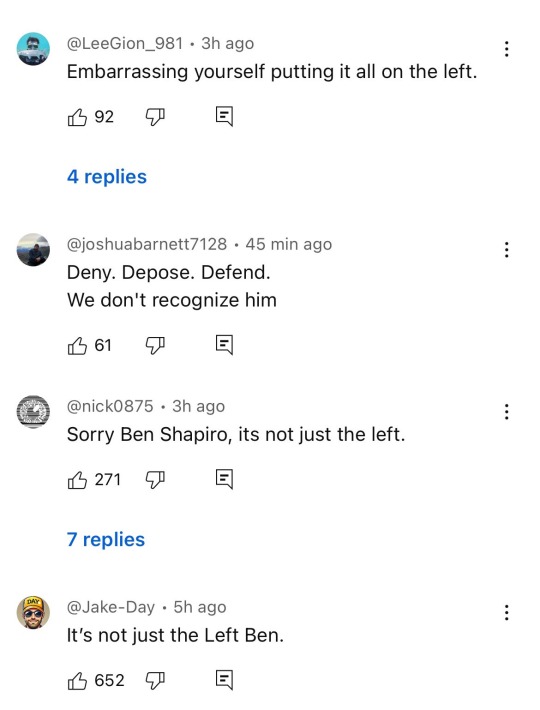

What He Did Was Good

On December 4, 2024, Luigi Mangione allegedly shot and killed Brian Thompson, CEO of UnitedHealthcare, a subsidiary of UnitedHealth Group, a massive financial entity with a market capitalization just under $500 billion. UnitedHealthcare is quite infamously known as one of the worst private health insurance companies in America, which in and itself is an achievement worthy of comment. As Mangione notes in his manifesto, a company such as UHC, which routinely declines to pay for life-saving treatments for its patients, is the definition of a parasite on the American working class. It sucks the blood out of hurt and dying people all over this country in the pursuit of financial gain for its shareholders. This is undeniable. As UHG notes in their Q3 2024 financial report, "The company returned over $9.6 billion to shareholders through the first nine months of 2024 through dividends and share repurchases. Return on equity of 26.3% in the quarter reflected the company’s consistent, broad-based earnings and efficient capital structure." This is an anodyne statement, and I include it to underline the dispassionate point I'm leading towards: UnitedHealthcare, as shepherded by holding company UnitedHealth Group is designed and operated in line with capitalist principles with the ultimate goal of financial efficiency and optimizing profits to ensure maximized returns to shareholders.

If you're reading this, you're likely thinking, ok? Seems pretty straightforward. And you would be exactly right. And that's the problem. The ideology expressed in the quoted statement is fundamentally at odds with the purported goal of serving "health care participants", a verbal choice in the report made by Parasite in Chief and Thompson's superior, Andrew Witty, that highlights the perverse inhumanity of executive officers. Ask yourself how they are achieving these financial successes while patients continue to be denied service (acquisition to drive vertical integration and artificial growth within their HC). Pretty simple - keep costs down through denials for "unnecessary services" and turn your hulking, aging healthcare engine's expenses into another of your company's revenues (seems totally legit!). It is a clear sign of American society's rot that these principles and ideas are considered "just the way things are". Capitalism and its adherents display their immorality proudly. The apotheosis of moral turpitude is responding to the uncovering and naming of these tactics with a resigned sigh and internal reconciliation.

The basic structure of health insurance services as a form of risk management, whereby a larger segment of the participating policyholders with smaller usage offsets the costs of a smaller segment with larger usage, has always been fragile, and the active speculation and investment by insurance companies in order to drive further growth is a breach of the social contract behind the entire concept. What is the consequence of insolvency or financial failure? The exact same consequences as financial success: denied claims and unpaid services. Once further risk has been introduced, often married with the rationale of battling increasing costs, which is likely true, but why is the result further risky investment? Are you starting to see the house of cards? They will never achieve full coverage because that would conflict with their number one goal. The contradictions are not sharpening, they are are as sharp as they can be. The question is what do you do about it?

All of us "health care participants" are marching on a treadmill as voices ring out constantly telling us to keep our eyes forward while "participants" around us are regularly and consistently shunted off into the abyss. Keep marching forward, keep paying your premiums, keep calling the support line and waiting for hours upon hours, keep pleading with a support specialist for help (knowing full well in your heart they are marching alongside you and equally at risk of being shunted off), keep on holding on while your body slowly loses the ability to maintain itself and you feel the abyss nearing.

When legacy news media and politicians stick to platitudes and fail to engage with the reasoning behind the death, they are telling us we do not matter. That our deaths do not matter when we do not receive treatment. Thompson's death has become an emotional outlet for us at a time when infrastructure is quickly declining. Our world is rapidly warming, fascists are ascendant across the globe, the costs of goods remains high and wages stagnate, and tens of millions of people were stupid enough to vote for a white supremacist president who will destroy organized labor, deport and kill millions of immigrants, and orient the state to harm all minorities. We are out of time; it is the height of absurdity to attempt to anonymize the rationale into a cloud of "political violence" and not engage any further. Any random murder is worse than a person killing someone responsible for millions of deaths and untold carnage against “health care participants”. It's that simple. The killing was targeted, methodical, and had little collateral damage. We do not even need to condone the murder in order to keep the focus centered on making the ruling class afraid to further harm us.

I'm angry; I'm angry just writing this all out. I was lucky enough to survive a long period of chronic, life-altering pain, and see the other side. But I am informed and changed by it. I will forever be a new person due to what I experienced, and the psychological depths I reached. I know all too well what it's like to deal with denials for service, rapid accumulation of medical debt without end in sight, and the fear of my health never improving. I know all too well what it means to turn and face the idea of death, and reconcile to it. Where Luigi may have turned his pain outwards, my psychology was turned inwards. Even then I still externalized quite a bit - it's natural when faced with the imposing, unknowable face of a corporation that is engaged to deny you what you need to survive. Opinions like, "I have back pain and I haven't tried to kill anyone" are the sloppy drivel of mental infants and should be discarded outright.

Perhaps you think this will lead to further violence and reprisals from the state and right-wing paramilitaries. Perhaps you're right, but you miss the point - Thompson's death did not happen in a vacuum. It is not the start of this thread. What do we teach the next generations when we allow these companies to continue to hurt and kill us year in and year out? The state and right-wing paramilitaries have been conducting a cold war against the left for at least the past 10 years, if not more. There have been numerous instances of outright violence and murder against left-wing activists, while the media and politicians decry "violence on both sides". If the procedural avenues are riddled with obstacles, and media attention is fleeting, it is the right of the people to use violence to effect change to save ourselves and prevent further harm. That is a distinct and moral outcome.

Time will tell if Thompson's death is a structural piercing of the ruling class's armor and leads to a true movement of the people. It has galvanized wide swaths of working Americans, including the nurses and doctors that have to deal with health insurance services. The enemy is clear and obvious, and that is an unequivocal good. We are united across many class and cultural lines against the executives that treat us as rounding errors. Health insurance is just one tentacle in the American capitalist system, but it is the right node for this awakening. The campaign against mistreatment must expand to all areas that threaten our lives and health.

Executives like Thompson deserve to feel afraid to go outside. The commons belong to us.

3 notes

·

View notes

Text

VB ABUNDANCE - Financial Advisory Services

Life insurance is a contract between an individual (the policyholder) and an insurance company. In exchange for regular premium payments, the insurance company agrees to provide a lump sum payment, known as a death benefit, to the designated beneficiaries upon the death of the insured person.

Life insurance offers financial protection and peace of mind by helping to secure the financial future of loved ones in the event of the policyholder's death.

vb abundance - financial advisor - https://www.wealthy.in/p/vivek8292

If you want more details click here, https://vbabundance.com/ or call us +91 99430 18682.

Address : Ganapathy Complex, No. 104 - 1st Floor, AK Nagar, Saibaba Colony, Coimbatore - 11.

Map Location : https://goo.gl/maps/d89bNnFmL8UPCtMCA

life insurance

2 notes

·

View notes

Text

Assignment of Proceeds: Meaning, Pros and Cons, Example

What Is an Assignment of Proceeds?

An Assignment of Proceeds is a legal arrangement in which a party (the assignor) transfers their right to receive payments or proceeds from a specific financial transaction to another party (the assignee). This assignment typically occurs through a formal contract or agreement and is often used in various financial and business contexts. The key components of an assignment of proceeds are:

Assignor: The assignor is the party who currently holds the right to receive the proceeds. This could be the original beneficiary of a financial transaction, such as a seller, creditor, or policyholder.

Assignee: The assignee is the party to whom the right to receive the proceeds is transferred. The assignee becomes entitled to receive the payments or benefits specified in the assignment agreement.

Transaction or Proceeds: The assignment of proceeds pertains to a specific financial transaction or a source of funds. This could include sales of goods, insurance claims, letters of credit, accounts receivable, or other contractual obligations.

Assignment Agreement: The assignment is formalized through a legal contract or agreement between the assignor and assignee. This agreement outlines the terms and conditions of the assignment, including the rights and responsibilities of both parties.

Payment Mechanism: The agreement specifies how and when the assignee will receive the proceeds. It may involve direct payment by the debtor or the third party responsible for making the payment to the assignee instead of the assignor.

Assignment of proceeds can serve various purposes, such as risk mitigation, access to immediate funds, debt settlement, or simplifying complex financial transactions. It is commonly used in international trade, finance, insurance, and lending scenarios to ensure the secure and efficient flow of funds between parties.

For example, in international trade, a seller may assign the right to receive payment from a letter of credit to a bank, reducing the risk of non-payment due to issues with the buyer's creditworthiness. In another scenario, an individual facing financial difficulties might assign their life insurance policy's death benefit to a creditor as collateral for a loan or to settle a debt. In both cases, the assignment of proceeds facilitates the efficient transfer of financial benefits from one party to another.

Understanding an Assignment of Proceeds

Understanding an assignment of proceeds involves grasping the key elements and implications of this financial arrangement. Here are the fundamental aspects to consider:

Parties Involved:

Assignor: This is the party who currently holds the right to receive payments or proceeds from a specific financial transaction. The assignor is essentially transferring their claim to these proceeds to another party.

Assignee: The assignee is the recipient of the rights to the proceeds. They assume the assignor's position and become entitled to receive the payments or benefits specified in the assignment agreement.

Financial Transaction or Proceeds:

An assignment of proceeds relates to a particular financial transaction or source of funds. This could be a sale of goods, an insurance policy payout, a letter of credit, an accounts receivable balance, or any other contractual obligation that involves payment or benefits.

Assignment Agreement:

The assignment of proceeds is formalized through a legal contract or agreement between the assignor and assignee. This document outlines the terms and conditions of the assignment, including:

The specific proceeds being assigned.

The rights and obligations of the assignor and assignee.

The payment mechanism and schedule.

Any conditions or limitations on the assignment.

Governing law and dispute resolution procedures.

Signatures and date of execution.

Purpose and Benefits:

The reasons for executing an assignment of proceeds can vary widely, but some common purposes include:

Risk mitigation: Reducing the risk of non-payment or default, especially in international trade or lending scenarios.

Access to immediate funds: Gaining quick access to cash flow, such as through factoring of accounts receivable.

Debt settlement: Using assigned assets, like life insurance policies, as collateral to settle debts.

Simplifying transactions: Streamlining complex financial dealings by designating a single party to receive payments on behalf of others.

Payment Mechanism:

The assignment agreement specifies how and when the assignee will receive the proceeds. This often involves a redirection of payments, meaning that the debtor or the third party responsible for making payments will send them directly to the assignee instead of the assignor.

Considerations and Risks:

Assigning proceeds can have implications for both the assignor and assignee. Considerations include the loss of control over the proceeds, potential costs and fees associated with the assignment, credit implications, and legal complexities. It's essential to weigh the benefits against the drawbacks when entering into such an arrangement.

Understanding an assignment of proceeds is crucial when entering into such agreements to ensure that both parties are clear about their roles, rights, and obligations. Additionally, seeking legal or financial advice may be advisable to navigate the complexities of these arrangements, especially in contexts with significant financial implications.

Advantages and Disadvantages of an Assignment of Proceeds

An assignment of proceeds can offer several advantages and disadvantages, depending on the specific context and the parties involved. Here's a breakdown of the pros and cons:

Advantages:

Risk Mitigation:

Pro: Assigning proceeds can help mitigate the risk of non-payment or default. By transferring the right to receive payments to a more creditworthy or reliable party, the assignor can ensure they receive the funds they are entitled to.

Improved Liquidity:

Pro: Assigning proceeds can provide immediate access to cash flow. This is particularly beneficial for businesses that need working capital to cover expenses, as they can receive funds upfront in exchange for their rights to future payments.

Debt Settlement:

Pro: Individuals facing financial difficulties can use an assignment of proceeds to settle debts or secure loans. For example, they might assign the death benefit of a life insurance policy as collateral for a loan.

Simplified Transactions:

Pro: In complex financial transactions involving multiple parties, an assignment of proceeds can streamline the process by designating a single party to receive payments on behalf of others, reducing administrative complexity.

Guaranteed Payment:

Pro: When an assignee with a strong financial standing is involved, the assignor can be more certain of receiving payments, which can improve financial planning and reduce uncertainty.

Disadvantages:

Loss of Control:

Con: Assigning proceeds often means giving up control over those funds. This may not be ideal if the assignor needs flexibility or has specific plans for the proceeds.

Costs and Fees:

Con: Assigning proceeds can come with fees and costs. For instance, factoring companies charge fees for advancing funds against accounts receivable, which can reduce the overall amount the assignor receives.

Credit Implications:

Con: Depending on the context, assigning proceeds can affect the assignor's creditworthiness. For example, using valuable assets like life insurance policies as collateral can impact credit.

Legal Complexities:

Con: The legal aspects of assignment can be complex and may require careful documentation and compliance with relevant laws and regulations. Errors or disputes can lead to legal complications.

Dependency on Assignee:

Con: The assignor becomes dependent on the assignee for receiving payments. If the assignee encounters financial difficulties or issues arise between the assignor and assignee, it can disrupt the payment process.

Limited Flexibility:

Con: Assigning proceeds can limit the assignor's ability to change payment arrangements or adapt to changing circumstances. It may be challenging to renegotiate terms once the assignment is in place.

In summary, the advantages of an assignment of proceeds include risk mitigation, improved liquidity, and simplified transactions, while the disadvantages include loss of control, costs and fees, potential credit implications, and legal complexities. Businesses and individuals should carefully evaluate their specific needs and circumstances before entering into an assignment of proceeds to determine if the benefits outweigh the drawbacks. Legal and financial advice may be essential in complex cases to ensure the arrangement is structured correctly and is in the best interest of all parties involved.

Example of an Assignment of Proceeds

Here's an example of an assignment of proceeds in the context of international trade:

Scenario: Company A, a manufacturer based in the United States, is exporting a large shipment of machinery to Company B, a buyer located in Germany. To secure payment for the machinery, Company B agrees to open a letter of credit (LC) with its bank in Germany. However, Company A is concerned about the creditworthiness of Company B's bank and wants to ensure they receive payment for the machinery.

Assignment of Proceeds Agreement:

Parties Involved:

Assignor: Company A (the exporter and beneficiary of the LC).

Assignee: XYZ Bank (a trusted U.S. bank).

Financial Transaction:

The financial transaction involves the export of machinery by Company A to Company B in Germany, with payment to be made through a letter of credit.

Assignment Agreement Terms:

Company A and XYZ Bank enter into an assignment of proceeds agreement.

Company A assigns the right to receive payment under the letter of credit to XYZ Bank.

The assignment agreement specifies that any payments made by Company B's bank in Germany under the letter of credit should be directly received by XYZ Bank in the United States.

The agreement outlines the payment mechanism, terms, and conditions of the assignment.

Purpose and Benefits:

The purpose of this assignment is to reduce the risk of non-payment for Company A. By assigning the proceeds to XYZ Bank, Company A ensures that even if Company B's bank in Germany faces financial difficulties or disputes arise, they will still receive payment for the machinery.

Payment Mechanism:

The assignment agreement instructs Company B's bank to remit the payment for the machinery directly to XYZ Bank in the United States, bypassing Company A as the beneficiary.

Considerations:

Company A benefits from reduced risk and more secure payment, while XYZ Bank earns a fee or commission for facilitating the assignment. Company B's bank may charge additional fees for processing payments to XYZ Bank.

In this example, the assignment of proceeds provides a level of security and risk mitigation for Company A. They can proceed with the export transaction with confidence, knowing that even if there are issues with Company B's bank in Germany, XYZ Bank in the United States will receive the payment on their behalf. This type of arrangement is common in international trade to protect the interests of exporters and ensure the smooth flow of funds across borders.

Read more: https://computertricks.net/assignment-of-proceeds-meaning-pros-and-cons-example/

2 notes

·

View notes

Text

Caring about other people's lives is a social contract. When a wealthy person with undue power over other people egregiously violates that social contract, they absolve the rest of society from the moral obligation to pity their death.

When policyholders suffer because United Healthcare delayed, denied, and defended, the corporate shareholders celebrate the money they save. If the people in power at UHC are going to celebrate everyone else's suffering, why should everyone else not celebrate theirs?

something interesting is happening

96K notes

·

View notes

Text

Fixed Deposit vs Life Insurance: Which is the Right Choice for You?

When it comes to securing your financial future, two traditional options often top the list: Fixed Deposit (FD) and Life Insurance. While both are low-risk financial instruments, they serve entirely different purposes. This article compares Fixed Deposit vs Life Insurance in terms of returns, purpose, tax benefits, risk, and flexibility to help you make the best decision. What is a Fixed Deposit?

A Fixed Deposit (FD) is a popular investment product offered by banks and NBFCs where you deposit a lump sum amount for a fixed tenure and earn a guaranteed interest rate. FDs are ideal for risk-averse individuals seeking stable and predictable returns.

✅ Features of Fixed Deposits:

Guaranteed returns (typically 5% to 7.5%)

Flexible tenure (7 days to 10 years)

Premature withdrawal allowed (with penalty)

Safe and low-risk investment

Option for cumulative or non-cumulative payouts

What is Life Insurance?

Life Insurance is a financial contract where an insurance company provides a sum assured to the nominee in case of the policyholder’s death. Some policies also provide maturity benefits (endowment or ULIPs) if the policyholder survives the term.

✅ Features of Life Insurance:

Financial protection for your dependents

Long-term wealth accumulation in some plans

Tax-free maturity under Section 10(10D)

Various types: Term, Whole Life, ULIP, Endowment

Premiums qualify for tax deductions

Fixed Deposit vs Life Insurance: A Head-to-Head Comparison

Feature

Fixed Deposit

Life Insurance

Purpose

Safe savings & short-term investment

Financial protection & long-term planning

Returns

Fixed (5%–7.5%)

Varies: Term – none; ULIP – 8–12%; Endowment – 4–6%

Risk Level

Very low

Low to moderate (based on policy type)

Liquidity

High (with penalty on early exit)

Low (lock-in of 5+ years)

Lock-in Period

Optional (except tax-saving FDs)

Yes (depends on policy type)

Tax Benefits

₹1.5L under 80C (5-year FD only)

₹1.5L under 80C + 10(10D) exemption on returns

Goal Suitability

Ideal for short-medium goals

Ideal for long-term protection and wealth When to Choose Fixed Deposit?

You need capital preservation with fixed returns

You’re investing for short-term goals like travel or emergency fund

You prefer liquid and safe options

You’re a conservative investor

When to Choose Life Insurance?

You want to secure your family’s future

You’re planning for long-term goals like retirement or children’s education

You want tax-efficient estate planning

You seek a combination of insurance + savings

Taxation: Fixed Deposit vs Life Insurance

🔹 Fixed Deposit:

Interest is fully taxable under "Income from Other Sources"

5-Year Tax-saving FD qualifies under Section 80C

TDS applicable if interest exceeds ₹40,000 (₹50,000 for senior citizens)

🔹 Life Insurance:

Premiums up to ₹1.5 lakh are deductible under 80C

Maturity benefits are tax-free under Section 10(10D) (subject to conditions)

Final Verdict: FD or Life Insurance?

Objective

Best Option

Capital safety + stable returns

Fixed Deposit

Long-term protection + legacy

Life Insurance

Short-term financial goals

Fixed Deposit

Tax-efficient wealth transfer

Life Insurance

Both Fixed Deposits and Life Insurance can be part of a well-diversified financial plan. FDs give you the safety and liquidity, while life insurance offers protection and planning for uncertainties.

0 notes

Text

What is the Most Important Thing in Insurance?

Navigating the world of insurance can feel overwhelming at times. As you explore various types of insurance, from travel to health and auto coverage, you may wonder what truly matters when protecting your assets and ensuring your peace of mind. Whether you’re a seasoned policyholder or looking to buy your first insurance plan, understanding the key factors in insurance can help you make informed decisions.

Let’s examine one vital aspect: the role of a car accident attorney in Tucson, Arizona in auto insurance and the protection it provides.

Understanding the Basics of Insurance

Insurance is a financial safety net, helping people recover after unforeseen events such as accidents, theft, or illness. You enter into a legal contract with your insurance provider when you purchase an insurance policy. This contract outlines what is covered, how claims are handled, and the financial support you’re entitled to in case of a loss.

The Importance of Coverage Limits

The coverage limit is one of the most important elements of any insurance plan. This is the maximum amount your insurer will pay for a covered loss. Understanding your coverage limits is essential because they dictate how much financial support you will receive in times of need. For example, in auto insurance, having sufficient liability coverage is crucial to protect your assets in the event of a car accident.

How to Choose the Right Insurance Policy

When selecting an insurance policy, it's crucial to consider your unique needs and circumstances. People often overlook factors such as:

Deductibles: You must pay out of pocket before your insurance kicks in. A higher deductible typically results in lower premiums, but it can lead to larger out-of-pocket expenses during a claim.

Exclusions: These are specific situations or conditions that your policy won’t cover. Understanding these can prevent unpleasant surprises later on.

Customer Service: Your insurance company's reputation and customer service availability can significantly impact your experience, especially during stressful situations.

The Role of a Car Accident Attorney

Having a Car Accident Attorney by your side can be invaluable if you are involved in a car accident. Here’s why:

Expert Guidance: A Car Accident Attorney understands the complexities of insurance claims and can help you navigate the process. They can also help you determine whether you receive fair compensation for damages and injuries.

Negotiation Skills: Insurance companies may not always offer the full amount you deserve. An attorney can negotiate on your behalf, ensuring your interests are represented.

Understanding the Law: Laws regarding car accidents can vary significantly by state. A knowledgeable attorney will know local regulations and how they affect your case.

What to Do After a Car Accident

If you’re involved in a car accident, there are several steps you should take:

Ensure Safety: First, call emergency services and check if anyone is injured.

Document the Scene: Take pictures and gather information from all parties involved, including contact information and insurance details.

Notify Your Insurance Company: Report the accident to your insurer immediately.

Consult a Car Accident Attorney: If you are involved in a car accident and have sustained injuries or significant damages, seeking legal guidance can help protect your rights.

The Financial Aspect of Insurance

Insurance is a financial tool designed to mitigate risks. Understanding how premiums, deductibles, and coverage limits work together is essential for making the right choices.

Premiums are the amount you pay for your insurance policy. Factors such as your driving history, age, and vehicle type can influence your premium costs.

Claims Process: Knowing how to file a claim and what to expect can alleviate stress during a challenging time. Your Car Accident Attorney can guide you through this process.

The Importance of Regularly Reviewing Your Insurance

Insurance needs can change over time due to life events such as marriage, moving, or purchasing a new vehicle. Regularly reviewing your policies ensures that you have adequate coverage for your current situation.

Adjusting Your Coverage: Consider increasing your liability limits as you accumulate assets. This adjustment can provide better protection in case of unexpected incidents.

Comparing Insurance Options: Periodically reassessing your insurance options can help you find better rates or coverage that suits your evolving needs.

Take Charge of Your Insurance Needs

Understanding your options and knowing what to prioritize can significantly improve your protection of yourself and your loved ones. The most important thing in insurance is ensuring you have the right coverage to fit your needs, particularly in auto insurance and the potential involvement of a Car Accident Attorney.

If you have questions about your current insurance policies or need assistance navigating the aftermath of a car accident, don't hesitate to seek professional guidance.

Secure Your Justice with Abboud Law Firm Today

For personalized assistance and legal guidance, contact the Abboud Law Firm today. Our experienced Car Accident Attorneys are here to help you navigate the complexities of your situation and ensure you receive the compensation you deserve. Don’t leave your future to chance—reach out to us now!

0 notes

Text

Insurtech Market transforming claims management efficiency by 2032

Insurtech Market was worth USD 8.24 billion in 2023 and is predicted to be worth USD 378.08 billion by 2032, growing at a CAGR of 53.03 % between 2024 and 2032.

Insurtech Market is rapidly redefining the global insurance sector through the integration of advanced technologies such as artificial intelligence, machine learning, big data, IoT, and blockchain. These innovations are enabling insurers to streamline operations, personalize services, and reduce costs, creating a more agile and customer-centric ecosystem.

U.S. sees rapid insurtech adoption led by AI-driven policy customization and digital-first platforms.

Insurtech Market is attracting significant investment and partnership activity as both startups and traditional insurers look to digitalize their value chains. With growing demand for on-demand insurance, automated claims processing, and embedded insurance solutions, the market is experiencing a fundamental shift in how insurance is accessed, delivered, and consumed.

Get Sample Copy of This Report: https://www.snsinsider.com/sample-request/2800

Market Keyplayers:

Damco Group

DXC Technology Company

Insurance Technology Services

Majesco

Oscar Insurance

Quantemplate

Shift Technology

Policy Bazaar

Wipro Limited

Clover Health Insurance

ZhongAn Insurance

Acko General Insurance Limited

Market Analysis

The global Insurtech landscape is being shaped by consumer expectations for speed, convenience, and personalization. Traditional insurers are increasingly collaborating with tech firms to enhance digital infrastructure, while startups continue to disrupt with innovative offerings. The United States remains a hub for insurtech innovation, while Europe is gaining momentum through regulatory flexibility and strong digital adoption across key markets.

Market Trends

Surge in usage-based insurance (UBI) and pay-as-you-go models

AI-powered chatbots and virtual assistants improving customer service

Increased adoption of blockchain for policy issuance and fraud prevention

Rise in microinsurance and embedded coverage in digital transactions

Expansion of API-based platforms for insurer-insurtech integrations

Greater focus on ESG-compliant insurtech products

Use of predictive analytics for underwriting and risk profiling

Market Scope

The Insurtech Market has broadened significantly, shifting beyond traditional offerings into highly specialized, digital-native solutions. Companies are increasingly leveraging real-time data and smart technologies to tailor policies and improve user experience.

On-demand and customizable policy platforms

Telematics integration in auto insurance

Real-time claims tracking via mobile apps

Smart contracts automating claim settlements

Health and wellness apps influencing premium adjustments

Risk management tools for small businesses and gig workers

Forecast Outlook

The Insurtech Market is expected to expand robustly as digital transformation accelerates across the insurance value chain. Key drivers include growing smartphone penetration, rising demand for seamless digital experiences, and evolving consumer behavior. Future market momentum will rely heavily on AI advancements, regulatory adaptability, and deeper insurer-tech collaborations. North America and Europe will continue to play leading roles due to their strong tech infrastructure and innovation-friendly ecosystems.

Access Complete Report: https://www.snsinsider.com/reports/insurtech-market-2800

Conclusion

The Insurtech Market is not just modernizing insurance—it’s reinventing it. With smarter technologies, personalized solutions, and faster service delivery, insurtech is creating new value for both providers and policyholders. From real-time risk assessment in Chicago to AI-driven claims in Berlin, the industry is shifting toward a future where digital-first is the default.

Related Reports:

U.S.A braces for soaring demand in Cybersecurity Insurance Market amid rising digital threats

U.S.A witnesses rising adoption of secure authentication in the booming Digital Signature Market

U.S.A witnesses soaring demand for AI-powered imaging in the Computer Vision Market

About Us:

SNS Insider is one of the leading market research and consulting agencies that dominates the market research industry globally. Our company's aim is to give clients the knowledge they require in order to function in changing circumstances. In order to give you current, accurate market data, consumer insights, and opinions so that you can make decisions with confidence, we employ a variety of techniques, including surveys, video talks, and focus groups around the world.

Contact Us:

Jagney Dave - Vice President of Client Engagement

Phone: +1-315 636 4242 (US) | +44- 20 3290 5010 (UK)

Mail us: [email protected]

0 notes

Text

Different Types of Insurance Policies In India

What are the Different Types of Insurance Policies? Insurance policies can safeguard you from unforeseen risks. You can insure your health, life, home, and many other things with a premium for a pre-decided cover. Let us understand the various types of insurance plans in India:

General Insurance General insurance, also known as non-life insurance, covers auto and homeowners’ policies. It provides payouts based on losses from specific financial events. Essentially, it includes any type of insurance that isn’t classified as life insurance.

Life Insurance Life insurance is a contract between an individual (the policyholder) and an insurance company. In exchange for regular premium payments, the insurance company promises to pay a lump sum amount, known as the death benefit, to the policyholder’s beneficiaries upon the policyholder’s death.

General Insurance General insurance is a contract between the policyholder and the insurance company, where the insurer agrees to compensate for any financial losses incurred due to specific events in exchange for a premium.

Health Insurance Health insurance may sound similar to life insurance, but this type of policy is bought to cover medical treatment and procedure costs. Policies are available for specific ailments, but health insurance can be bought. They cover the cost of treatment, medication, and hospitalization.

Individual Health Insurance Individual health insurance policies are designed to cover a single person. These policies cover hospitalization, surgeries, doctor consultations, and other medical expenses. The sum insured is specific to the individual, meaning only the policyholder can claim the benefits.

Family Floater Insurance Family floaters and health insurance policies cover the entire family under a single sum insured. Instead of having individual policies for each family member, a family floater plan provides a combined coverage amount that any family member can utilize. This type of insurance policy is cost-effective and convenient, as it simplifies management and often comes at a lower premium than separate individual policies for each member. Family floater plans typically cover the policyholder, spouse, children, and sometimes parents.

Critical Illness Cover Critical illness insurance provides a lump sum payout upon the diagnosis of specified critical illnesses such as cancer, heart attack, stroke, and kidney failure. This type of coverage is designed to help policyholders manage the high costs associated with treating severe health conditions.

Senior Citizen Health Insurance Senior citizen health insurance plans are tailored to meet the healthcare needs of individuals aged 60 and above. These policies typically offer higher coverage for age-related illnesses, pre-existing conditions, and critical illnesses.

0 notes

Text

0 notes

Text

Exploring the Pros and Cons of Payment Protection Insurance for Remote Workers

In today's evolving work environment, remote work has become a common lifestyle for millions worldwide. With flexibility, autonomy, and reduced commuting stress, remote work offers a range of benefits. However, it also brings uncertainties, particularly in financial stability during unforeseen circumstances. This is where payment protection insurance (PPI) is a potential safety net.

Payment protection insurance, often bundled with loans, mortgages, or credit cards, is designed to help policyholders meet their financial obligations when they cannot work due to illness, accident, or involuntary unemployment. For remote workers, who may not always have access to employer-sponsored safety nets, choosing the best payment protection insurance can make a significant difference.

This blog explores the pros and cons of payment protection insurance for remote workers, helping you understand whether it's a sensible choice based on your work style and financial needs.

Understanding Payment Protection Insurance for Remote Workers

Remote workers often manage multiple projects, work on freelance contracts, or operate as self-employed individuals. Unlike traditional employees, they may not receive paid sick leave, health insurance, or job security. Therefore, an income protection policy (سياسة حماية الدخل) becomes an attractive option for securing one's livelihood.

A payment protection plan usually covers loan or debt payments if you cannot work due to disability, redundancy, or illness. Some policies even extend coverage to temporary conditions, vital for remote professionals who cannot afford prolonged income breaks.

Pros of Payment Protection Insurance for Remote Workers

1. Financial Security During Illness or Injury

Financial continuity is one of the biggest advantages of having the best payment protection insurance. Remote workers, especially those self-employed, often do not have access to sick pay. If a sudden illness or accident prevents you from working, the insurance covers your financial obligations, such as loan repayments or credit bills. This provides you with peace of mind and lets you focus on recovery.

2. Protection Against Redundancy or Client Loss

While redundancy is more commonly associated with traditional employment, remote workers can suddenly lose income if a long-term client ends a contract. A robust سياسة حماية الدخل (income protection policy) can bridge the gap until you secure new work, ensuring that your financial health isn't compromised during such transitions.

3. Customisation for Freelancers and Gig Workers

Some insurance providers offer plans tailored to the needs of freelancers, consultants, and other remote professionals. These often include flexible payment options, wider eligibility criteria, and shorter waiting periods. When chosen wisely, the best payment protection insurance offers a valuable layer of financial defence.

4. Supports Mental Well-being

Constant worry about finances can affect productivity and mental health. Financial stress can significantly affect remote workers who already deal with the pressures of working from home, often in isolation. Knowing that your income is protected under a comprehensive سياسة حماية الدخل (income protection policy) can alleviate this burden and promote emotional well-being.

5. Helps Maintain Credit Rating

Payment defaults due to income disruptions can negatively impact your credit score. The insurance ensures timely payments, helping maintain your creditworthiness and avoiding late fees or penalties.

Cons of Payment Protection Insurance for Remote Workers

While the benefits are compelling, there are also potential drawbacks before committing to a policy.

1. Coverage Limitations

Not all payment protection insurance policies cover all causes of income loss. For instance, self-employed workers might find that only some policies acknowledge their employment type. In some cases, pre-existing conditions, part-time contracts, or short-term illnesses may not be covered. Therefore, even the best payment protection insurance may come with exclusions that are critical to understand beforehand.

2. Delayed Payouts and Waiting Periods

Most policies include a waiting period before the benefits start. For remote workers who rely on consistent cash flow, even a 30- or 60-day waiting period can create financial strain. A سياسة حماية الدخل (income protection policy) must be evaluated carefully in terms of payout timelines to ensure that the support arrives when it is most needed.

3. Complex Terms and Conditions

Payment protection policies often contain complex language, and understanding what is included or omitted can be confusing. Misunderstanding these terms could lead to denied claims. Remote workers must read the fine print and consult a financial advisor to understand what the best payment protection insurance offers.

4. Not Always Cost-Effective

While we won't discuss actual costs, some remote workers might find that the premiums don't align with their risk level or monthly budget. Especially if your remote job provides consistent income and you're financially prepared for emergencies, a سياسة حماية الدخل (income protection policy) might not always offer the best value for money.

5. Possible Overlap with Other Coverage

Remote workers with comprehensive health insurance, life insurance, or an emergency fund might find that a payment protection policy overlaps with their existing safety nets. In such cases, evaluating whether an additional policy is necessary becomes essential.

How Remote Workers Can Make the Most of Payment Protection Insurance

To make an informed decision, remote professionals should consider the following steps:

Assess Your Risk Level: Are you self-employed with no fallback income? Or do you work for a remote-friendly employer who offers sick leave? Your need for a سياسة حماية الدخل (income protection policy) depends on your risk profile.

Compare Policies Carefully: Look for the best payment protection insurance that includes coverage for freelancers or gig workers. Evaluate how claims are processed and what the eligibility requirements are.

Understand Exclusions: Make sure to go through the exclusions thoroughly. Check whether the policy accommodates such factors if you have pre-existing conditions or irregular income.

Read Reviews and Ask Questions: Look for feedback from other remote workers and don't hesitate to ask for clarification on terms. The more you know, the better your decision will be.

Conclusion

The rise of remote work has brought both freedom and financial unpredictability. For individuals working without employer-backed benefits, having a سياسة حماية الدخل (income protection policy) can offer much-needed security. While it's not a one-size-fits-all solution, the best payment protection insurance policies provide valuable coverage tailored to modern work lifestyles.

However, the decision should not be made lightly. Carefully weighing the pros and cons, understanding policy details, and aligning them with your financial circumstances are key to determining whether such insurance is a good fit.

The goal is to protect your livelihood and gain peace of mind, whether working from a home office, a coffee shop, or halfway across the world.

0 notes

Text

Unlocking the Value: Understanding the Possibility of Cashing Out a Life Insurance Policy

Life insurance policies are often purchased with the intent to provide financial security for loved ones in the event of the policyholder’s death. However, certain types of life insurance, particularly whole life or other permanent policies, may also carry a cash value component that accumulates over time. This cash value can sometimes be accessed while the policyholder is still alive, leading many to ask, can I cash out a life insurance policy?

When considering this option, it’s essential to understand the type of policy you hold. Term life insurance, for instance, does not build cash value and therefore cannot be cashed out. In contrast, permanent life insurance policies such as whole life, universal life, or variable life often include a savings element. Over time, as you pay premiums, a portion of those payments goes into this cash value account. This account grows at a rate determined by the policy’s terms, and after a certain period, it may become substantial enough to withdraw or borrow against.

There are several ways to access the cash value in a life insurance policy. One method is through a policy loan, where you borrow money from the insurer using the cash value as collateral. Another approach is to make a withdrawal, although this may reduce the death benefit or result in tax consequences. A more final route is surrendering the policy altogether. This means canceling the policy and receiving the cash surrender value, which is the cash value minus any applicable fees or loans. However, surrendering a policy also means losing the life insurance coverage entirely.

Before making any decision, policyholders must weigh the advantages and consequences. Cashing out may provide quick access to funds in emergencies or for investment opportunities. Yet, it also potentially reduces future financial protection for beneficiaries and might trigger taxable events if the amount withdrawn exceeds the premiums paid.

In addition, policyholders should consider the timing of the cash out. Early withdrawals or surrenders can carry steep surrender charges, especially in the initial years of the policy. Furthermore, borrowing against the policy, while often not subject to immediate taxation, may accrue interest, and if unpaid, could erode the policy’s value or even cause it to lapse.

Financial advisors often recommend consulting a professional before making any moves. The intricacies of life insurance contracts and the potential impact on your overall financial plan make it critical to have a clear understanding of what you’re giving up versus what you’re gaining. Family needs, tax considerations, and long-term financial goals should all be part of the evaluation process.

Ultimately, the answer to the question, can i cash out my life insurance policy, lies in the type of policy you hold and your current financial situation. While it is possible under the right circumstances, it should never be a decision made lightly. Exploring all options and seeking guidance can ensure that your actions align with both your immediate needs and long-term goals.

0 notes

Text

Fixed Deposit vs Life Insurance: A Complete Financial Comparison Guide

When it comes to safe investments in India, two prominent options emerge — Fixed Deposits (FDs) and Life Insurance. Both serve different purposes, yet they are often compared due to their popularity among conservative investors. In this comprehensive guide, we analyze, contrast, and break down everything you need to know about Fixed Deposits vs Life Insurance, helping you make an informed decision based on your financial goals.

What is a Fixed Deposit?

Fixed Deposit (FD) is a financial instrument provided by banks and Non-Banking Financial Companies (NBFCs) that offers investors a higher rate of interest than a regular savings account, until the given maturity date. It is one of the most secure ways to grow your money without any market risk.

Key Features of Fixed Deposits

Guaranteed Returns: Pre-determined interest rate irrespective of market volatility.

Flexible Tenure: Ranges from 7 days to 10 years.

Loan Facility: Loans up to 90% of FD amount can be availed.

Premature Withdrawal: Allowed with penalty.

Tax Deduction: Section 80C deduction available for Tax Saver FDs.

What is Life Insurance?

Life Insurance is a contract between the policyholder and the insurer, where the insurer promises to pay a sum of money either on the death of the insured or after a set period. It serves dual purposes — financial protection and long-term investment.

Key Features of Life Insurance

Financial Security: Payout to nominee in case of death of the insured.

Investment Component: Endowment and ULIP plans build corpus over time.

Tax Benefits: Premiums qualify for deduction under Section 80C, and maturity/death benefits under Section 10(10D).

Policy Loans: Loans can be taken against the surrender value.

Investment Objective Comparison

Wealth Accumulation

FDs are ideal for parking lump sums for short-term goals like buying a car or building emergency funds. The compounding interest ensures stable growth.

Life Insurance, particularly ULIPs (Unit Linked Insurance Plans), offers long-term growth linked to market performance, making it suitable for retirement planning or child education.

Risk Management

Life insurance is essential for risk coverage. In case of the policyholder’s untimely demise, the nominee gets a lump sum amount — a crucial financial safety net.

FDs offer no risk cover and thus fail to protect dependents.

Tax Implications

Fixed Deposits

Interest earned is fully taxable under 'Income from Other Sources'.

Tax Saver FDs provide Section 80C benefit up to ₹1.5 lakh.

TDS @10% is deducted if interest exceeds ₹40,000/year (₹50,000 for senior citizens).

Life Insurance

Premiums qualify for Section 80C deduction.

Maturity proceeds are tax-free under Section 10(10D) if annual premium is below 10% of the sum assured.

Which One Should You Choose?

Choose Fixed Deposit If:

You need short-term guaranteed returns.

You are highly risk-averse.

You want easy access to funds when needed.

Choose Life Insurance If:

You have financial dependents.

You’re looking for long-term investment with tax benefits.

You want to combine savings with life cover.

When to Use Both Strategically?

Many financial advisors suggest using both tools in tandem:

Use FDs for your short-term goals and liquidity needs.

Use Life Insurance (preferably term + ULIP) for family security and long-term wealth creation.

Final Verdict

Fixed Deposits and Life Insurance serve fundamentally different purposes — one secures your capital, the other secures your family. While FD is excellent for parking surplus funds, life insurance is crucial for ensuring your loved ones' financial future. A balanced portfolio should ideally include both, tailored to your risk profile and life goals.

Frequently Asked Questions

1. Can I use FD returns to pay life insurance premiums?

Yes, especially for retirees. The predictable interest from FDs can fund recurring premium payments.

2. Which has better post-tax returns — FD or Life Insurance?

Life insurance has tax-exempt maturity proceeds, whereas FD interest is taxable. So life insurance generally provides better post-tax returns over the long term.

3. Is ULIP better than FD?

ULIPs have the potential to give higher returns but carry market risk. They are suitable only if you have a long-term horizon and moderate-to-high risk appetite.

4. Is a Term Insurance Plan better than an FD?

For pure protection, yes. Term insurance offers high cover at low premium, which FDs can’t match.

Conclusion

When comparing Fixed Deposit vs Life Insurance, the choice should align with your financial goals, risk appetite, and time horizon. While fixed deposits bring stability and liquidity, life insurance ensures financial protection and disciplined long-term savings. Use each where it fits best — not interchangeably, but complementarily.

For a truly secure future, don’t just invest. Plan.

0 notes

Text

What is Insurance's Best Answer?

Understanding insurance can often feel like navigating a maze. Whether you're a first-time buyer or looking to brush up on your knowledge, knowing the ins and outs of insurance is essential. You may find yourself asking, " Do I need insurance?” and “How does it work for my needs?” This article will break down what insurance is, the different types available, and why you may need a car accident attorney in Tucson, Arizona, to guide you through the complexities involved, especially in the event of an accident.

What is Insurance?

Insurance is a financial safety net designed to protect against unforeseen events. You enter into a legal contract with an insurance provider when you purchase insurance. In this agreement, you pay a premium, and in return, the insurance company promises to compensate you or a designated beneficiary should a specific loss occur. This could be from a fire, theft, car accident, or other events covered by your policy.

Insurance can alleviate the burden of financial loss. It helps people recover from incidents that would otherwise be financially devastating. For example, having the right insurance can mean the difference between manageable expenses and overwhelming debt if you are involved in a car accident.

Understanding Coverage Types

Insurance coverage can come in many forms. Understanding the common types can help you make informed decisions. This is particularly important when considering auto insurance, where having a knowledgeable Car Accident Attorney can make a difference.

Auto Insurance

Auto insurance is one of the most common types of insurance. It typically includes several components:

Liability Coverage: This protects you in case you are found legally responsible for causing an accident that injures someone or damages their property.

Collision Coverage: This coverage pays for damages to your car resulting from a collision, regardless of who is at fault.

Comprehensive Coverage: This covers damages to your car caused by events other than collisions, such as theft, vandalism, or natural disasters.

Uninsured/Underinsured Motorist Coverage: This protects you if you're involved in an accident with someone who doesn’t have insurance or does not have enough coverage.

In the event of a car accident, having a Car Accident Attorney can help navigate the complexities surrounding liability, claims, and insurance negotiations.

Health Insurance

Health insurance helps cover medical expenses incurred due to illness or injury. Plans can vary significantly based on the coverage provided, deductibles, and out-of-pocket limits. This type of insurance is critical for managing healthcare costs and ensuring access to necessary medical services.

Homeowners Insurance

Homeowners' insurance protects your property against fire, theft, and natural disasters. It typically covers both the physical structure of your home and your personal belongings. In the case of damage or loss, having this insurance can help you recover quickly without incurring major out-of-pocket expenses.

Life Insurance

Life insurance provides financial support to beneficiaries after the policyholder passes away. It can be a vital part of financial planning, ensuring that loved ones are financially secure in the event of an untimely death.

When Should You Buy Insurance?

Another common question is: When should you purchase insurance? The answer often depends on personal circumstances and needs. Here are some general guidelines:

Before Major Life Events: It’s wise to secure insurance before significant life changes, such as getting married, buying a home, or starting a family.

Before Traveling: Travel insurance can cover unexpected cancellations or emergencies if you plan a trip.

When You Buy a Vehicle: Auto insurance is a legal requirement in many areas and should be secured before you drive your new vehicle.

In all these cases, consulting with experts, such as a Car Accident Attorney, can provide insights into the necessary coverage based on your unique situation.

How to Buy Insurance: Seek Guidance from a Car Accident Attorney

Insurance can be bought directly through an insurance provider or through independent agents. Independent agents can offer you the best options from multiple companies, while direct insurers provide their products.

By working with experts, you can get the coverage you need without overpaying. If you're dealing with auto insurance specifically, a Car Accident Attorney can offer valuable advice on what coverage options best suit your driving habits and lifestyle.

The Role of a Car Accident Attorney

If you find yourself involved in a car accident, the expertise of a Car Accident Attorney can be invaluable. They can help you understand your rights, manage communication with insurance companies, and advocate for fair treatment.

Here’s how a Car Accident Attorney can assist you:

Navigating Claims: They help you file claims and can clarify your insurance policy's complicated terms and conditions.

Advocating for You: Should disputes arise, a Car Accident Attorney can represent your interests, ensuring you receive the compensation you're entitled to.

Understanding Coverage: They can explain the insurance coverage and ensure you have the right policies before accidents occur.

Take Control of Your Insurance Needs

Understanding insurance doesn’t have to be daunting. Knowing what insurance entails, the types available, and when to purchase them, you can make informed decisions about protecting your financial future. Whether dealing with auto, health, or homeowners insurance, having the right coverage is critical.

Don't hesitate to contact the Abboud Law Firm if you’re involved in a car accident or need guidance on your insurance options. Our experienced Car Accident Attorneys are here to provide the support and legal advice you need to navigate the complexities of insurance and ensure you are well-protected.

Secure Your Peace of Mind

Are you ready to take control of your insurance needs, or need assistance after a car accident? Contact the Abboud Law Firm today for a free consultation with our skilled Car Accident Attorneys. We are here to help you understand your options and secure the coverage you need for peace of mind.

0 notes

Text

Insurance Policy Explained: Types, Features & How to Choose the Right One

Choosing the right insurance policy can feel overwhelming, especially with so many types, features, and fine print. Whether you're insuring your car, health, or even your life, it's essential to understand how insurance works, what to look for in a policy, and how to make informed decisions.

In this guide, we’ll break down what an insurance policy is, its types and features, and how to choose the best one for your needs. We’ll also cover essential elements like No Claim Bonus and E-Insure First, a modern digital solution that simplifies policy access.

What Is an Insurance Policy?

An insurance policy is a legal contract between you (the policyholder) and the insurance company. It outlines the terms under which the insurer will provide financial protection or reimbursement for specific types of loss, damage, illness, or death.

The main components of any insurance policy include:

Coverage: What risks or items are insured?

Premium: The cost you pay to keep the policy active.

Sum Insured / IDV: The maximum payout the insurer will offer.

Policy Term: The duration of coverage.

Exclusions: What is not covered under the policy?

Types of Insurance Policies

Different types of insurance policies are tailored to protect you from different risks:

1. Health Insurance

Provides coverage for medical expenses like hospitalization, surgery, and preventive care. Many policies now include wellness benefits and cumulative bonuses.

NCB in health insurance: If you don’t claim during a policy year, your sum insured often increases (typically 10% to 50% over time), providing more value without raising your premium. This is the power of policy with NCB in insurance.

2. Motor Insurance (Car/Bike)

Covers damage or theft of your vehicle and liability to third parties.

No Claim Bonus in Motor Insurance: If you don’t make a claim, you earn a discount on your premium, up to 50% after 5 claim-free years. It’s a major incentive for safe driving.

E-Insure First: Many insurers now allow you to buy, renew, or manage your vehicle policy digitally through platforms like E-Insure First, ensuring faster access to documents and better transparency.

3. Life Insurance

Pays a lump sum to your beneficiaries in the event of your death. It can be term-based (for a fixed period) or whole life (for life coverage).

4. Travel Insurance

Covers risks like trip cancellations, medical emergencies abroad, lost luggage, etc.

5. Home Insurance

Covers damage or loss due to fire, theft, or natural disasters.

Key Features to Look For in an Insurance Policy

Here are the critical features you should review before purchasing any policy:

Coverage Scope - Does it include all common and relevant risks for your needs?

Sum Insured / IDV - For health/motor – is it adequate to cover real-world loss or medical bills?

Premium Affordability - Are you paying a fair price for the level of coverage offered?

Add-on Covers - E.g., NCB Protection, Zero Depreciation, Critical Illness Rider, etc.

Claim Process - Is it digital, fast, and hassle-free?

No Claim Bonus (NCB) - How much does your premium reduce or your sum insured increase if unused?

Digital Access - Can you manage the policy via apps or portals like E-Insure First?

How to Choose the Right Insurance Policy?

Here’s a step-by-step approach to selecting the ideal policy:

1. Assess Your Needs

For health: Consider your age, lifestyle, and family medical history.

For vehicles: Factor in usage frequency, age of vehicle, and location.

For life: Look at financial dependents and long-term goals.

2. Compare Policies

Use comparison tools or platforms like E-Insure First to check:

Premiums

Inclusions & exclusions

Network hospitals (health) or garages (motor)

Add-on covers and benefits like NCB

3. Read the Fine Print

Always review:

Waiting periods (for health)

Deductibles or co-pays

The claim settlement ratio of the insurer

4. Check Digital Access

A modern insurer offers digital ease:

Download e-policy instantly

File claims online

Use e-wallets or apps (E-Insure First is a good example)

5. Look for NCB Opportunities

Choose policies that reward claim-free behavior through No Claim Bonus.

In motor insurance, consider NCB Protector add-ons to retain your discount even after small claims.

What Is E-Insure First?

E-Insure First is a digital insurance management platform that helps users:

Buy or renew policies online

Compare premiums

Access policy documents instantly

Track claims and NCB status

Set renewal reminders

It’s a powerful tool for modern policyholders who want control and transparency over their insurance portfolio.

Conclusion

Insurance isn’t just about protecting against loss — it’s also about gaining value. By understanding your needs, comparing options, and leveraging tools like E-Insure First, you can make smart choices.

Don’t forget the power of the No Claim Bonus — a reward that saves you money and reflects responsible behavior.

Whether you're new to insurance or reviewing existing plans, always revisit your coverage every year to ensure you're fully protected — and not overpaying.

0 notes

Text

Navigating Property Damage Claims in Miami: Your Guide to Legal Representation

Dealing with insurance companies after significant property damage can feel like an uphill battle. Their adjusters may offer lowball settlements, delay processing your claim, or even deny it outright. Understanding your rights and the intricacies of your insurance policy is crucial, and a seasoned legal professional can provide the guidance and advocacy you need to secure a fair and just settlement.

A skilled residential property damage lawyer Miami is well-versed in the specific challenges faced by homeowners in the area. They understand the common types of damage, the local building codes, and the tactics insurance companies often employ. Whether your home has suffered wind damage, water intrusion, mold growth, or structural issues, a lawyer can help you accurately assess the damage, gather necessary evidence, and negotiate with your insurer. They can also assist with claims related to theft, vandalism, and other covered perils.

Similarly, commercial property damage attorney Miami specializes in representing businesses that have experienced losses due to property damage. The financial implications of business interruption and property repairs can be significant, and a lawyer can help navigate the complexities of commercial insurance policies, which often include provisions for business income loss and extra expenses. They work to ensure that your business can recover and resume operations as quickly as possible.

One of the most challenging situations property owners can face is when their insurance company acts in "bad faith." This occurs when an insurer fails to uphold their end of the contract by unreasonably delaying, denying, or underpaying a legitimate claim. In such cases, a bad faith insurance attorney Miami is essential. These attorneys are experts in identifying and proving bad faith practices, which can include:

Unreasonable delays in investigating or paying a claim.

Denying a claim without a proper investigation.

Offering a settlement amount significantly lower than the actual value of the claim.

Misrepresenting policy terms or coverage.

Using intimidation or aggressive tactics to discourage policyholders from pursuing their claims.

If you suspect your insurance company is acting in bad faith, it is crucial to seek legal counsel immediately. A bad faith insurance attorney can help you file a lawsuit against the insurer to recover not only the full value of your property damage claim but potentially also punitive damages and attorney's fees.

When choosing a property insurance claim lawyer Miami, look for a firm with a proven track record of success in handling property damage cases. Experience in negotiating with insurance companies, litigating claims when necessary, and understanding the nuances of Florida insurance law are all critical factors. A good lawyer will be transparent about the process, communicate effectively, and prioritize your best interests. They will work diligently to ensure you receive the compensation you deserve to repair or rebuild your property and recover from your losses.

Navigating the aftermath of property damage can be overwhelming, but you don't have to face it alone. With the right legal representation, you can level the playing field with your insurance company and fight for a fair outcome.

For expert legal assistance with your property damage claim in Miami, we encourage you to visit [Your Website Address Here]. Our team of experienced property damage attorneys is ready to help you understand your rights and guide you through the claims process.

0 notes