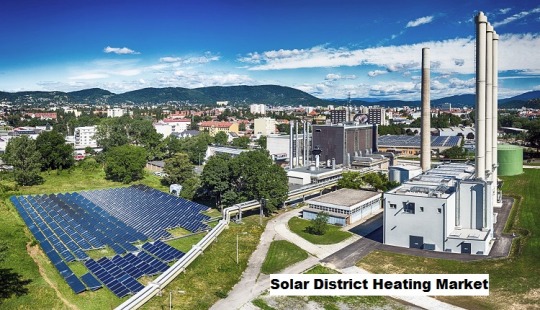

#Solar District Heating Market Growth

Text

Solar District Heating Market Expected to Expand with Shift Towards Sustainable Energy Mix

Global Solar District Heating Market is expected to grow owing to renewable energy targets to shift their energy mix towards sustainable sources by various countries throughout the forecast period.

According to TechSci Research report, “Solar District Heating Market - Global Industry Size, Share, Trends, Opportunity, and Forecast 2019-2029”, the Global Solar District Heating Market is expected to register robust growth during the forecast period. A primary driver for the adoption of solar district heating is the global commitment to reducing carbon emissions and mitigating climate change. Solar thermal energy is a clean and renewable resource, and its integration into district heating systems helps decrease reliance on fossil fuels, leading to a substantial reduction in greenhouse gas emissions.

The increasing global commitment to decarbonize the energy sector presents a significant opportunity for the solar district heating market. Countries and regions aiming to transition to renewable energy sources as part of their climate action plans can leverage solar district heating to replace or complement conventional heating systems, reducing carbon emissions. Solar district heating systems can be integrated into broader renewable energy portfolios. Combining solar thermal energy with other renewable sources, such as wind and geothermal, creates opportunities for hybrid systems that offer reliable, resilient, and sustainable heating solutions.

Based on system, the Large-scale segment is expected to dominate the market during the forecast period. Large-scale systems often feature centralized infrastructure, consolidating the collection, storage, and distribution components. This centralized approach allows for optimized energy management, easier maintenance, and the ability to serve diverse end-users within a concentrated area. While flat-plate and evacuated tube collectors are common in large-scale systems, technological advancements in these collector types continue to enhance their efficiency and cost-effectiveness for large-scale applications. The large-scale segment is particularly relevant for industrial applications, providing the necessary high-temperature heat for various industrial processes.

Browse over XX market data Figures spread through XX Pages and an in-depth TOC on the "Global Solar District Heating Market"

https://www.techsciresearch.com/report/solar-district-heating-market/23131.html

Industries with significant heat demand, such as manufacturing, food processing, and chemical production, benefit from the reliable and sustainable heat supply offered by large-scale solar district heating. Countries in the Asia-Pacific region, especially China, are witnessing a surge in large-scale solar district heating projects. Rapid urbanization and the need for sustainable heating solutions are driving significant investments in infrastructure to meet the heat demand of growing urban populations. The United States and Canada are also exploring large-scale solar district heating initiatives, with a focus on integrating renewable energy into district heating systems. Urban planning and sustainability goals contribute to the adoption of large-scale solutions in metropolitan areas.

Based on end-user, the Residential segment is projected to dominate the market throughout the forecast period. The prospect of long-term cost savings is a significant driver for residential solar district heating. While the upfront costs may be a consideration, the reduced reliance on conventional energy sources leads to lower operational costs over the system's lifespan, providing an attractive proposition for homeowners seeking energy-efficient solutions. In some regions, community-based solar district heating initiatives are gaining traction. Residential communities, housing cooperatives, or neighborhood associations collaborate to implement shared solar heating systems, making the technology more accessible and cost-effective for individual homeowners.

Advancements in thermal storage technologies enhance the efficiency and reliability of residential solar district heating. Improved storage solutions allow homeowners to store excess solar heat for later use, ensuring a continuous and reliable supply of thermal energy, even during periods of low sunlight. In North America, particularly in the United States and Canada, the residential segment is gaining momentum. Government incentives, energy efficiency programs, and a growing interest in sustainable living contribute to the increasing adoption of solar district heating in residential areas. In the Asia-Pacific region, countries like China are witnessing a rise in residential solar district heating projects. Urbanization, coupled with governmental initiatives to promote renewable energy, is driving the adoption of solar thermal systems in residential developments.

Key market players in the Global Solar District Heating Market are:-

Aalborg CSP A/S

Alfa Laval AB

Bosch Thermotechnology Ltd

Fortum Corporation

Göteborg Energi AB

LOGSTOR A/S

Ramboll Group A/S

Savosolar Oyj

Soltigua S.r.l

Vattenfall AB

Download Free Sample Report:

https://www.techsciresearch.com/sample-report.aspx?cid=23131

Customers can also request for 10% free customization on this report.

“The Global Solar District Heating Market in Europe is poised to be the dominant force in the industry. Europe stands out as a leading market for solar district heating, with countries like Denmark, Germany, and Sweden taking significant strides in the adoption of solar thermal systems for district heating applications. The European solar district heating market has experienced steady growth, driven by a combination of government support, environmental consciousness, and advancements in technology. The market is expected to continue expanding as more regions within Europe embrace renewable heating solutions.” said Mr. Karan Chechi, Research Director with TechSci Research, a research-based global management consulting firm.

“Solar District Heating Market - Global Industry Size, Share, Trends, Opportunity, and Forecast Segmented By System (Small-scale and Large-scale), By End-User (Residential, Commercial and Industrial), By Region, and By Competition 2019-2029” has evaluated the future growth potential of Global Solar District Heating Marketand provides statistics & information on market size, structure, and future market growth. The report intends to provide cutting-edge market intelligence and help decision makers take sound investment decisions. Besides the report also identifies and analyzes the emerging trends along with essential drivers, challenges, and opportunities in Global Solar District Heating Market.

Browse Related Research

Sensor Cable Market

https://www.techsciresearch.com/report/sensor-cable-market/19591.html

Automotive Secondary Battery Market

https://www.techsciresearch.com/report/automotive-secondary-battery-market/19565.html

Floating Tidal Power Market

https://www.techsciresearch.com/report/floating-tidal-power-market/19569.html

Contact

TechSci Research LLC

420 Lexington Avenue,

Suite 300, New York,

United States- 10170

M: +13322586602

Email: [email protected]

Website: https://www.techsciresearch.com

#Solar District Heating Market#Solar District Heating Market Size#Solar District Heating Market Share#Solar District Heating Market Trends#Solar District Heating Market Growth

0 notes

Text

Hybrid Solar Wind Energy Storage Market Analysis Key Trends, Growth Opportunities, Outlook to 2032

Overview of the Market:

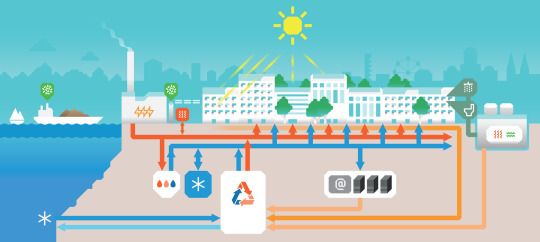

The district heating market is an integral part of the global energy industry and has been experiencing promising growth in recent years. District heating systems provide heating and hot water to residential, commercial, and industrial buildings through a centralized network of pipes that distribute thermal energy generated from various sources. This approach offers several advantages, including energy efficiency, reduced carbon emissions, and cost savings for end users.

The global Hybrid Solar Wind Energy Storage Market size is projected to reach USD 3.69 Billion by 2030, growing at a CAGR of 10.18% from 2023 to 2030

Platform Type: District heating systems can be categorized into two main platform types: centralized and decentralized.

Centralized Systems: Centralized district heating systems involve a large-scale heating plant that generates thermal energy from one or multiple sources, such as combined heat and power (CHP) plants, waste-to-energy facilities, geothermal energy, or biomass boilers. The heat is then distributed through a network of pipes to connected buildings.

Decentralized Systems: Decentralized district heating systems, also known as communal or block heating, are smaller-scale systems that serve a localized area or a specific group of buildings. These systems typically utilize smaller heat generation units, such as individual boilers or heat pumps, and provide heating to a limited number of buildings.

Technology: Various technologies are employed in district heating systems to generate thermal energy efficiently and sustainably. Some common technologies include:

Combined Heat and Power (CHP): CHP plants simultaneously generate electricity and usable heat from a single fuel source. This technology offers high energy efficiency by utilizing the waste heat produced during electricity generation for district heating purposes.

Biomass Boilers: Biomass boilers utilize organic materials, such as wood pellets or agricultural waste, as fuel to generate heat. This renewable energy source helps reduce greenhouse gas emissions and dependence on fossil fuels.

Geothermal Energy: Geothermal district heating systems extract heat from the Earth's subsurface using geothermal wells. This technology is sustainable, as it harnesses the natural heat available underground.

Waste-to-Energy: Waste-to-energy plants convert municipal solid waste or industrial waste into thermal energy. These facilities help reduce landfill waste and utilize the energy content of waste materials.

End User Industry: District heating systems cater to a wide range of end user industries, including:

Residential Sector: District heating is commonly used to provide heating and hot water to residential buildings, such as apartment complexes or housing estates. This sector represents a significant portion of the district heating market.

Commercial Sector: District heating is adopted by various commercial buildings, such as office buildings, shopping malls, hotels, and hospitals. These establishments benefit from the centralized supply of heat, which eliminates the need for individual heating systems.

Industrial Sector: Industries with high heat demand, such as manufacturing facilities, chemical plants, and food processing units, can benefit from district heating systems. These systems offer cost-effective and reliable heat supply, enabling efficient industrial processes.

Statistics and Demand:

The district heating market has witnessed steady growth due to several factors, including increasing focus on energy efficiency, government initiatives promoting sustainable heating solutions, and the rising demand for low-carbon heating systems. While specific statistics may vary, the market is projected to experience continued growth in the coming years.

The demand for district heating systems is driven by the need for sustainable and cost-effective heating solutions, particularly in urban areas where buildings are densely concentrated. Additionally, as governments worldwide strive to reduce carbon emissions and achieve climate targets, the adoption of district heating systems is expected to increase, further driving market demand.

Scope:

The scope of the district heating market extends globally, with both developed and developing countries actively adopting district heating systems. Europe, in particular, has a well-established district heating infrastructure, with countries like Denmark, Sweden, and Finland leading in adoption rates. However, there is increasing interest and market growth in regions such as North America, Asia Pacific, and the Middle East.

In terms of scope, the district heating market encompasses various stakeholders, including equipment manufacturers, heat generation and distribution companies, construction firms, energy service companies (ESCOs), and regulatory bodies. These stakeholders work together to develop, implement, and operate district heating systems, ensuring efficient and sustainable heat supply to end users.

In conclusion, the district heating market is experiencing promising growth globally, driven by the advantages it offers in terms of energy efficiency, reduced carbon emissions, and cost savings. The market is characterized by various platform types, technologies, and end user industries. As the world continues to prioritize sustainable heating solutions, the demand for district heating systems is expected to grow, presenting significant opportunities for industry players.

We recommend referring our Stringent datalytics firm, industry publications, and websites that specialize in providing market reports. These sources often offer comprehensive analysis, market trends, growth forecasts, competitive landscape, and other valuable insights into this market.

By visiting our website or contacting us directly, you can explore the availability of specific reports related to this market. These reports often require a purchase or subscription, but we provide comprehensive and in-depth information that can be valuable for businesses, investors, and individuals interested in this market. “Remember to look for recent reports to ensure you have the most current and relevant information.”

Click Here, To Get Free Sample Report: https://stringentdatalytics.com/sample-request/hybrid-solar-wind-energy-storage-market/11329/

Market Segmentations:

Global Hybrid Solar Wind Energy Storage Market: By Company

• ReGen Powertech

• General Electric

• Siemens(Gamesa)

• Vestas

• Vattenfall

• Goldwind

• Suzlon Energy

• Alpha Windmills

• Blue Pacific Solar Products

• Zenith Solar Systems

• UNITRON Energy System

• Alternate Energy Company

• Supernova Technologies Private

Global Hybrid Solar Wind Energy Storage Market: By Type

• Standalone Storage

• Grid Connected

• Others

Global Hybrid Solar Wind Energy Storage Market: By Application

• Residential

• Commercial

• Utility

• Industrial

• Others

Global Hybrid Solar Wind Energy Storage Market: Regional Analysis

The regional analysis of the global Hybrid Solar Wind Energy Storage market provides insights into the market's performance across different regions of the world. The analysis is based on recent and future trends and includes market forecast for the prediction period. The countries covered in the regional analysis of the Hybrid Solar Wind Energy Storage market report are as follows:

North America: The North America region includes the U.S., Canada, and Mexico. The U.S. is the largest market for Hybrid Solar Wind Energy Storage in this region, followed by Canada and Mexico. The market growth in this region is primarily driven by the presence of key market players and the increasing demand for the product.

Europe: The Europe region includes Germany, France, U.K., Russia, Italy, Spain, Turkey, Netherlands, Switzerland, Belgium, and Rest of Europe. Germany is the largest market for Hybrid Solar Wind Energy Storage in this region, followed by the U.K. and France. The market growth in this region is driven by the increasing demand for the product in the automotive and aerospace sectors.

Asia-Pacific: The Asia-Pacific region includes Singapore, Malaysia, Australia, Thailand, Indonesia, Philippines, China, Japan, India, South Korea, and Rest of Asia-Pacific. China is the largest market for Hybrid Solar Wind Energy Storage in this region, followed by Japan and India. The market growth in this region is driven by the increasing adoption of the product in various end-use industries, such as automotive, aerospace, and construction.

Middle East and Africa: The Middle East and Africa region includes Saudi Arabia, U.A.E, South Africa, Egypt, Israel, and Rest of Middle East and Africa. The market growth in this region is driven by the increasing demand for the product in the aerospace and defense sectors.

South America: The South America region includes Argentina, Brazil, and Rest of South America. Brazil is the largest market for Hybrid Solar Wind Energy Storage in this region, followed by Argentina. The market growth in this region is primarily driven by the increasing demand for the product in the automotive sector.

Click Here, To Purchase Premium Report: https://stringentdatalytics.com/purchase/hybrid-solar-wind-energy-storage-market/11329/?license=single

Reasons to Purchase Hybrid Solar Wind Energy Storage Market Report:

Informed Decision-Making: A comprehensive market research report provides valuable insights and analysis of the district heating market, including market size, growth trends, competitive landscape, and key drivers and challenges. This information allows businesses to make informed decisions regarding investments, expansion strategies, and product development.

Market Understanding: Research reports offer a deep understanding of the district heating market, including its current state and future prospects. They provide an overview of market dynamics, such as industry trends, regulatory frameworks, and technological advancements, helping businesses identify opportunities and potential risks.

Competitive Analysis: Market research reports often include a competitive analysis, profiling key players in the district heating market. This analysis helps businesses understand their competitors' strategies, market share, and product offerings. It enables companies to benchmark themselves against industry leaders and identify areas for improvement or differentiation.

Market Entry and Expansion: For companies planning to enter the district heating market or expand their existing operations, a market research report provides crucial information about market saturation, customer preferences, and regional dynamics. It helps businesses identify viable market segments, target demographics, and potential growth areas.

Investment Opportunities: Market research reports highlight investment opportunities in the district heating market, such as emerging technologies, untapped regions, or niche markets. This information can assist investors in making informed decisions about capital allocation and portfolio diversification.

Risk Mitigation: By analyzing market trends, customer preferences, and regulatory frameworks, market research reports help businesses identify and mitigate potential risks and challenges. This proactive approach can minimize uncertainties and optimize decision-making processes.

Cost Savings: Investing in a market research report can potentially save businesses time and resources. Rather than conducting extensive primary research or relying on fragmented information sources, a comprehensive report consolidates relevant data, analysis, and insights in one place, making it a cost-effective solution.

Industry Benchmarking: Market research reports provide benchmarks and performance indicators that allow businesses to compare their performance with industry standards. This evaluation helps companies identify areas where they excel or lag behind, facilitating strategic improvements and enhancing their competitive position.

Long-Term Planning: A global market research report offers a forward-looking perspective on the district heating market, including growth projections, emerging trends, and future opportunities. This insight aids businesses in long-term planning, resource allocation, and adapting their strategies to changing market dynamics.

Credibility and Authority: Market research reports are typically prepared by industry experts, analysts, and research firms with in-depth knowledge of the subject matter. Purchasing a reputable report ensures access to reliable and credible information, enhancing decision-making processes and providing confidence to stakeholders. In general, market research studies offer companies and organisations useful data that can aid in making decisions and maintaining competitiveness in their industry. They can offer a strong basis for decision-making, strategy formulation, and company planning.

About US:

Stringent Datalytics offers both custom and syndicated market research reports. Custom market research reports are tailored to a specific client's needs and requirements. These reports provide unique insights into a particular industry or market segment and can help businesses make informed decisions about their strategies and operations.

Syndicated market research reports, on the other hand, are pre-existing reports that are available for purchase by multiple clients. These reports are often produced on a regular basis, such as annually or quarterly, and cover a broad range of industries and market segments. Syndicated reports provide clients with insights into industry trends, market sizes, and competitive landscapes. By offering both custom and syndicated reports, Stringent Datalytics can provide clients with a range of market research solutions that can be customized to their specific needs

Contact US:

Stringent Datalytics

Contact No - +1 346 666 6655

Email Id - [email protected]

Web - https://stringentdatalytics.com/

#Hybrid Solar Wind Energy Storage Market Analysis Key Trends#Growth Opportunities#Outlook to 2032#Overview of the Market:#The district heating market is an integral part of the global energy industry and has been experiencing promising growth in recent years. D#commercial#and industrial buildings through a centralized network of pipes that distribute thermal energy generated from various sources. This approac#including energy efficiency#reduced carbon emissions#and cost savings for end users.

0 notes

Text

"A 1-megawatt sand battery that can store up to 100 megawatt hours of thermal energy will be 10 times larger than a prototype already in use.

The new sand battery will eliminate the need for oil-based energy consumption for the entire town of town of Pornainen, Finland.

Sand gets charged with clean electricity and stored for use within a local grid.

Finland is doing sand batteries big. Polar Night Energy already showed off an early commercialized version of a sand battery in Kankaanpää in 2022, but a new sand battery 10 times that size is about to fully rid the town of Pornainen, Finland of its need for oil-based energy.

In cooperation with the local Finnish district heating company Loviisan Lämpö, Polar Night Energy will develop a 1-megawatt sand battery capable of storing up to 100 megawatt hours of thermal energy.

“With the sand battery,” Mikko Paajanen, CEO of Loviisan Lämpö, said in a statement, “we can significantly reduce energy produced by combustion and completely eliminate the use of oil.”

Polar Night Energy introduced the first commercial sand battery in 2022, with local energy utility Vatajankoski. “Its main purpose is to work as a high-power and high-capacity reservoir for excess wind and solar energy,” Markku Ylönen, Polar Nigh Energy’s co-founder and CTO, said in a statement at the time. “The energy is stored as heat, which can be used to heat homes, or to provide hot steam and high temperature process heat to industries that are often fossil-fuel dependent.” ...

Sand—a high-density, low-cost material that the construction industry discards [Note: 6/13/24: Turns out that's not true! See note at the bottom for more info.] —is a solid material that can heat to well above the boiling point of water and can store several times the amount of energy of a water tank. While sand doesn’t store electricity, it stores energy in the form of heat. To mine the heat, cool air blows through pipes, heating up as it passes through the unit. It can then be used to convert water into steam or heat water in an air-to-water heat exchanger. The heat can also be converted back to electricity, albeit with electricity losses, through the use of a turbine.

In Pornainen, Paajanen believes that—just by switching to a sand battery—the town can achieve a nearly 70 percent reduction in emissions from the district heating network and keep about 160 tons of carbon dioxide out of the atmosphere annually. In addition to eliminating the usage of oil, they expect to decrease woodchip combustion by about 60 percent.

The sand battery will arrive ready for use, about 42 feet tall and 49 feet wide. The new project’s thermal storage medium is largely comprised of soapstone, a byproduct of Tulikivi’s production of heat-retaining fireplaces. It should take about 13 months to get the new project online, but once it’s up and running, the Pornainen battery will provide thermal energy storage capacity capable of meeting almost one month of summer heat demand and one week of winter heat demand without recharging.

“We want to enable the growth of renewable energy,” Paajanen said. “The sand battery is designed to participate in all Fingrid’s reserve and balancing power markets. It helps to keep the electricity grid balanced as the share of wind and solar energy in the grid increases.”"

-via Popular Mechanics, March 13, 2024

--

Note: I've been keeping an eye on sand batteries for a while, and this is really exciting to see. We need alternatives to lithium batteries ASAP, due to the grave human rights abuses and environmental damage caused by lithium mining, and sand batteries look like a really good solution for grid-scale energy storage.

--

Note 6/13/24: Unfortunately, turns out there are substantial issues with sand batteries as well, due to sand scarcity. More details from a lovely asker here, sources on sand scarcity being a thing at the links: x, x, x, x, x

#sand#sand battery#lithium#lithium battery#batteries#technology news#renewable energy#clean energy#fossil fuels#renewables#finland#good news#hope#climate hope

1K notes

·

View notes

Text

Top Real Estate Investment Trends for 2024

The real estate market has always been a dynamic space, influenced by a blend of economic, social, and technological trends. As we head into 2024, the sector continues to evolve, driven by changes in consumer preferences, advances in technology, and broader economic conditions. Understanding these trends can help investors navigate the market effectively and identify opportunities for growth. Here are the top real estate investment trends to watch in 2024.

1. Sustainability and Green Buildings

The global push for sustainability has reached new heights, and the real estate sector is no exception. As climate change becomes a central issue, both tenants and investors are prioritizing environmentally friendly buildings. Green buildings, which are designed to reduce environmental impacts, use less energy, and provide healthier living and working environments, are becoming increasingly valuable assets.

In 2024, expect an increased focus on sustainable real estate, especially in urban areas. This trend includes the development of energy-efficient homes, the incorporation of renewable energy sources like solar panels, and the use of sustainable materials in construction. Additionally, green certifications such as LEED (Leadership in Energy and Environmental Design) are becoming a key consideration for tenants and buyers who want to reduce their carbon footprint.

For investors, properties that adhere to sustainability standards tend to attract higher-quality tenants and command higher rents, making them a smart investment. Governments are also incentivizing green construction through tax breaks and grants, adding further appeal to sustainable projects.

2. The Rise of Smart Homes and Buildings

The integration of smart technology into homes and commercial buildings is another major trend reshaping the real estate landscape. Smart homes are no longer a luxury; they are becoming the new norm as consumers demand more convenience, security, and energy efficiency. With advancements in the Internet of Things (IoT), real estate developers are increasingly incorporating smart devices into their properties to make them more attractive to tech-savvy buyers and renters.

In 2024, expect to see more properties equipped with smart thermostats, lighting systems, and security features that can be controlled remotely via smartphones or voice-activated assistants. Smart technology not only enhances convenience but also provides energy savings, contributing to the growing demand for eco-friendly solutions. For investors, smart properties can command premium prices or rents, especially in markets targeting younger demographics.

Moreover, the concept of smart buildings is extending to commercial real estate, where IoT and artificial intelligence (AI) are used to optimize energy usage, reduce operational costs, and improve tenant experiences. Smart offices and retail spaces, for instance, are being designed to adjust lighting, heating, and ventilation automatically based on real-time data, providing both sustainability and cost-efficiency benefits.

3. Suburban Expansion and Hybrid Living

The COVID-19 pandemic permanently altered many aspects of life, including where and how people live. One of the lasting impacts has been the migration from urban centers to suburban and rural areas, as remote work and hybrid work models allow people to live farther from their workplaces. While cities are bouncing back, the appeal of suburban living has remained strong, especially for families looking for more space and a quieter environment.

In 2024, the trend of suburban expansion will continue, fueled by demand for larger homes, better school districts, and access to green spaces. Suburban areas that are well-connected to urban centers via transportation networks or have strong local economies will become hotbeds of real estate activity. Developers are focusing on creating master-planned communities with amenities such as parks, fitness centers, and retail spaces to cater to the needs of remote workers.

For investors, suburban areas offer great potential, particularly for single-family homes and multifamily housing developments. Suburbs are often more affordable than urban centers, providing higher profit margins. Additionally, as more companies adopt permanent remote or hybrid work policies, these areas are becoming long-term options for people who once needed to live closer to city centers.

4. Short-Term Rentals and Vacation Homes

With the rise of platforms like Airbnb and VRBO, short-term rentals have become a major player in the real estate market. The trend was temporarily interrupted by the pandemic, but it is now bouncing back, especially as more people return to travel. Vacation home markets are booming, with both domestic and international travelers seeking flexible and unique accommodation options.

In 2024, investing in short-term rentals will continue to be an attractive opportunity, especially in tourist destinations and areas with a high demand for temporary housing, such as near hospitals or universities. Investors who own vacation homes can often achieve higher returns through short-term rentals compared to traditional long-term leasing, though they do require more management and attention.

The key to success in this market will be understanding local regulations, as many cities and municipalities are introducing restrictions or requirements on short-term rentals. Investors should stay informed about these regulations and consider hiring property managers to handle the operational challenges of short-term rentals, such as guest turnover and maintenance.

5. Multifamily Housing: A Safe Bet in an Uncertain Economy

As economic uncertainty looms, multifamily housing continues to be a solid investment for those seeking stability. Even as inflation and interest rates fluctuate, people will always need a place to live. Multifamily housing, especially affordable units, remains in high demand across many markets.

In 2024, affordable housing shortages will persist in major metropolitan areas, leading to increased demand for multifamily investments. Investors are likely to focus on properties that cater to lower- and middle-income tenants, as these segments of the population are the most affected by rising housing costs. Additionally, multifamily housing provides a hedge against vacancy risks since even if one unit is empty, others continue to generate income.

Developers are also turning to modular and prefabricated construction methods to create multifamily housing more quickly and affordably. These innovations help address the growing demand for affordable housing while keeping construction costs in check. As affordability becomes a critical issue in many cities, multifamily properties that are well-located and reasonably priced will continue to offer consistent returns.

6. Commercial Real Estate and the Future of Offices

The commercial real estate sector has undergone significant transformation due to the rise of remote work, with traditional office spaces facing declining demand. However, 2024 presents new opportunities for investors, particularly in flexible office spaces and coworking environments. As companies adapt to hybrid work models, the need for dynamic and flexible office space has increased.

In major cities and secondary markets, coworking spaces are thriving, providing businesses with flexibility to downsize or expand their office footprint depending on their workforce needs. Investors in commercial real estate should focus on properties that offer flexibility, adaptability, and modern amenities. Office spaces that can be easily reconfigured for different uses, such as coworking hubs or shared office spaces, are likely to attract businesses looking for short-term leases and collaboration environments.

Additionally, retail real estate is showing signs of recovery, particularly in experiential retail spaces. While e-commerce has disrupted traditional brick-and-mortar stores, malls and retail centers that provide unique experiences—such as entertainment venues, restaurants, or fitness studios—are drawing in foot traffic. Investors should look for opportunities in mixed-use developments where retail spaces are combined with residential or office units, creating vibrant, multifaceted communities.

7. Real Estate Investment Trusts (REITs): A Popular Alternative

Real Estate Investment Trusts (REITs) remain a popular investment vehicle for individuals who want exposure to real estate without directly owning property. In 2024, REITs will continue to provide an attractive option, particularly as more people seek passive income streams or diversify their portfolios. With inflation concerns and stock market volatility, REITs offer a relatively stable and liquid alternative, while still providing exposure to the real estate sector.

There are several types of REITs, including those that invest in residential, commercial, industrial, or specialized sectors such as healthcare or data centers. In particular, data center and industrial REITs are expected to perform well, given the increasing demand for digital infrastructure and e-commerce fulfillment centers. As the digital economy grows, so too will the need for properties that support it, such as server farms and distribution hubs.

Investors should also keep an eye on REITs that focus on essential sectors like healthcare facilities, which are likely to see continued demand as the population ages. The key advantage of REITs is that they allow investors to access large-scale, income-producing real estate projects without needing substantial capital, making them an excellent choice for those looking to diversify their real estate holdings.

8. Real Estate Crowdfunding and Fractional Ownership

Another trend gaining traction in 2024 is real estate crowdfunding and fractional ownership. These innovative models allow individual investors to pool their resources to invest in larger real estate projects. This democratization of real estate investing has opened doors for those who might not have the capital to invest in properties on their own.

Crowdfunding platforms enable investors to buy shares in specific properties or portfolios, often with relatively low minimum investments. Fractional ownership takes this concept a step further, allowing multiple people to jointly own a single property. These platforms provide transparency and liquidity, which were traditionally lacking in the real estate market.

For investors, real estate crowdfunding offers access to higher-end projects that would typically be out of reach, while also spreading risk across multiple properties. As technology continues to advance and regulations evolve, expect this trend to grow, offering more opportunities for individuals to invest in real estate without the need for full ownership or property management.

Conclusion

As we move into 2024, the real estate market presents a mix of opportunities and challenges for investors. Trends like sustainability, smart technology, suburban expansion, and the rise of short-term rentals are reshaping the way people live and work. At the same time, economic uncertainty is driving demand for stable investments like multifamily housing and REITs. Whether you're a seasoned investor or just starting out, staying informed about these trends will help you make savvy decisions in an ever-changing market. By keeping an eye on these key developments, you'll be well-positioned to capitalize on the opportunities that lie ahead in the real estate landscape.

#real estate#real estate india#real estate trends#property consultant#residential real estate#commercial real estate

1 note

·

View note

Text

Thermal Energy Storage Market Report: Industry Manufacturers Analysis 2020-2027

Thermal Energy Storage Market

The global thermal energy storage market size was valued at USD 4.1 billion in 2019 and is projected to grow at a compound annual growth rate (CAGR) of 9.45% from 2020 to 2027.

Shifting preference towards renewable energy generation, including concentrated solar power, and rising demand for thermal energy storage (TES) systems in HVAC are among the key factors propelling the industry growth. Growing need for enhanced energy efficiency, coupled with continuing energy utilization efforts, will positively influence the thermal energy storage demand. For instance, in September 2018, the Canadian government updated a financial incentive plan “Commercial Energy Conservation and Efficiency Program” that offers USD 15,000 worth rebates for commercial sector energy upgrades.

Gather more insights about the market drivers, restrains and growth of the Thermal Energy Storage Market

The market in the U.S. is projected to witness substantial growth in the forthcoming years on account of increasing number of thermal energy storage projects across the country. For instance, in 2018, the U.S. accounted for 33% of the 18 under construction projects and 41% of the total 1,361 operational projects globally. Presence of major industry players in the country is expected to further propel the TES market growth in the U.S.

The U.S. Department of Energy (DoE) evaluates thermal energy storage systems for their safety, reliability, cost-effective nature, and adherence to environmental regulations and industry standards. It also stated that Europe and the Asia Pacific display higher fractions of grid energy storage as compared to North America. Rising need for a future with clean energy is prompting governments across the globe to take efforts towards developing innovative energy storage systems.

The primary challenge faced by the thermal energy storage sector is the economical storage of energy. An important advancement in this sector has been the usage of lithium-ion batteries. These batteries exhibit high energy density and long lifespans of 500 deep cycles, i.e. the number of times they can be charged from 20% to their full capacity before witnessing a deterioration in performance. They can also be utilized in electric vehicles, district cooling and heating, and power generation.

Thermal Energy Storage Market Segmentation

Grand View Research has segmented the global thermal energy storage market report on the basis of product type, technology, storage material, application, end user, and region:

Product Type Outlook (Revenue, USD Million, 2016 - 2027)

Sensible Heat Storage

Latent Heat Storage

Thermochemical Heat Storage

Technology Outlook (Revenue, USD Million, 2016 - 2027)

Molten Salt Technology

Electric Thermal Storage Heaters

Solar Energy Storage

Ice-based Technology

Miscibility Gap Alloy Technology

Storage Material Outlook (Revenue, USD Million, 2016 - 2027)

Molten Salt

Phase Change Material

Water

Application Outlook (Revenue, USD Million, 2016 - 2027)

Process Heating & Cooling

District Heating & Cooling

Power Generation

Ice storage air-conditioning

Others

End-user Outlook (Revenue, USD Million, 2016 - 2027)

Industrial

Utilities

Residential & Commercial

Regional Outlook (Revenue, USD Million, 2016 - 2027)

North America

US

Canada

Mexico

Europe

UK

Russia

Germany

Spain

Asia Pacific

China

India

Japan

South Korea

Central & South America

Brazil

Middle East and Africa (MEA)

Saudi Arabia

Browse through Grand View Research's Power Generation & Storage Industry Research Reports.

The global energy storage for unmanned aerial vehicles market size was estimated at USD 413.25 million in 2023 and is expected to grow at a CAGR of 27.8% from 2024 to 2030.

The global heat recovery steam generator market size was estimated at USD 1,345.2 million in 2023 and is projected to reach USD 1,817.0 million by 2030 and is anticipated to grow at a CAGR of 4.5% from 2024 to 2030.

Key Companies & Market Share Insights

Industry participants are integrating advanced technologies into the existing technology to enhance the product demand through the provision of improved thermal energy management systems. Furthermore, eminent players are emphasizing on inorganic growth ventures as a part of their strategic expansion. Some of the prominent players in the global thermal energy storage market include:

BrightSource Energy Inc.

SolarReserve LLC

Abengoa SA

Terrafore Technologies LLC

Baltimore Aircoil Company

Ice Energy

Caldwell Energy

Cryogel

Steffes Corporation

Order a free sample PDF of the Thermal Energy Storage Market Intelligence Study, published by Grand View Research.

0 notes

Text

Thermal Energy Storage Market is Estimated to Witness Double Digit Growth due to Rising Demand for Renewable Energy Sources

Thermal energy storage (TES) offers solutions for energy storage, load shifting and improved power plant efficiency. It enables shifting renewable power generation to better match electricity demand. Thermal energy, in the form of heat or cold, is captured and stored for later use in district heating or cooling applications and industrial processes. Key advantages of thermal energy storage over electrical storage technologies include relatively low costs, large energy storage capacities, and near-room-temperature operation. Rapid growth of renewable generation from solar and wind is driving the need for energy storage solutions to utilize surplus renewable power.

The Global Thermal Energy Storage Market is estimated to be valued at US$ 5.66 Bn in 2024 and is expected to exhibit a CAGR of 10% over the forecast period 2024 To 2031.

Key Takeaways

Key players operating in the Thermal Energy Storage market are BrightSource Energy, Inc., EnergyNest AS., Ice Energy, Baltimore Aircoil Company, Inc., Abengoa Solar, S.A, Burns and McDonnell, Inc., and DC Pro Engineering. These players are focusing on contracts and agreements strategies to strengthen their foothold in the thermal energy storage market.

Development of innovative and cost-effective thermal energy storage technologies Thermal Energy Storage Market Demand Advances in phase change materials, thermo-chemical energy storage, and other storage media will facilitate commercialization of large-scale thermal storage systems.

North America dominates the global thermal energy storage market due to rising emphasis on renewable integration and decarbonization of power grids. However, Asia Pacific is expected to witness the fastest growth on account of rapidly increasing energy demand and government initiatives to adopt renewable energy in countries like China and India.

Market Drivers

Rising demand for renewable energy integration is a major driver of the thermal energy storage market. As the share of variable solar and wind power increases, cost-effective long-duration energy storage solutions are required to balance intermittent renewable resources. Thermal storage technologies help overcome the mismatch between power generation and usage more effectively than intermittent battery storage. Government policies and targets related to renewable portfolio standards, carbon emission reduction also support the demand for TES worldwide.

PEST Analysis

Political: Thermal energy storage faces regulations around safety and emissions. Various government policies and subsidies can promote its adoption for managing peak power loads and integrating renewable resources.

Economic: Rising energy costs and demand are driving interest Thermal Energy Storage Market Size And Trends to reduce costs and maximize renewable energy usage. Its ability to store heat cheaply and discharge it on demand adds economic value to various industries and buildings.

Social: Thermal storage helps boost energy access and affordability for residential and commercial users. Its role in supporting renewable energy adoption aligns with public sentiment around cleaner energy and climate change mitigation.

Technological: Advancements are occurring in materials, phase-change technologies, and integrated smart control systems to improve storage density, cycling efficiency and usability of thermal energy storage across applications. Its integration with existing HVAC and power facilities utilizes latest digitalization.

Geographical concentration of market value

Europe accounts for a major share of the global thermal energy storage market value currently due to supportive policies and initiatives for renewable integration and decarbonization of heat in buildings. Countries like Germany, France and the UK have demonstrated leadership. North America is another significant regional market backed by initiatives to modernize energy infrastructure.

Fastest growing region

Asia Pacific region is projected to witness the highest growth in the thermal energy storage market during the forecast period driven by increasing government focus as well as private sector investments in renewable energy adoption, district heating and cooling systems in countries like China, India and Japan. Rapid urbanization and rising energy demand in the developing economies of the region present compelling opportunities.

Get More Insights On, Thermal Energy Storage Market

About Author:

Money Singh is a seasoned content writer with over four years of experience in the market research sector. Her expertise spans various industries, including food and beverages, biotechnology, chemical and materials, defense and aerospace, consumer goods, etc. (https://www.linkedin.com/in/money-singh-590844163)

#Thermal Energy Storage Market Size#Thermal Energy Storage Market Trends#Thermal Energy Storage Market Demand#Thermal Energy Storage#Thermal Energy Storage Market

0 notes

Text

The global thermal energy storage market size was valued at USD 4.1 billion in 2019 and is projected to grow at a compound annual growth rate (CAGR) of 9.45% from 2020 to 2027.

Shifting preference towards renewable energy generation, including concentrated solar power, and rising demand for thermal energy storage (TES) systems in HVAC are among the key factors propelling the industry growth. Growing need for enhanced energy efficiency, coupled with continuing energy utilization efforts, will positively influence the thermal energy storage demand. For instance, in September 2018, the Canadian government updated a financial incentive plan “Commercial Energy Conservation and Efficiency Program” that offers USD 15,000 worth rebates for commercial sector energy upgrades.

Gather more insights about the market drivers, restrains and growth of the Thermal Energy Storage Market

The market in the U.S. is projected to witness substantial growth in the forthcoming years on account of increasing number of thermal energy storage projects across the country. For instance, in 2018, the U.S. accounted for 33% of the 18 under construction projects and 41% of the total 1,361 operational projects globally. Presence of major industry players in the country is expected to further propel the TES market growth in the U.S.

The U.S. Department of Energy (DoE) evaluates thermal energy storage systems for their safety, reliability, cost-effective nature, and adherence to environmental regulations and industry standards. It also stated that Europe and the Asia Pacific display higher fractions of grid energy storage as compared to North America. Rising need for a future with clean energy is prompting governments across the globe to take efforts towards developing innovative energy storage systems.

The primary challenge faced by the thermal energy storage sector is the economical storage of energy. An important advancement in this sector has been the usage of lithium-ion batteries. These batteries exhibit high energy density and long lifespans of 500 deep cycles, i.e. the number of times they can be charged from 20% to their full capacity before witnessing a deterioration in performance. They can also be utilized in electric vehicles, district cooling and heating, and power generation.

Thermal Energy Storage Market Segmentation

Grand View Research has segmented the global thermal energy storage market report on the basis of product type, technology, storage material, application, end user, and region:

Product Type Outlook (Revenue, USD Million, 2016 - 2027)

• Sensible Heat Storage

• Latent Heat Storage

• Thermochemical Heat Storage

Technology Outlook (Revenue, USD Million, 2016 - 2027)

• Molten Salt Technology

• Electric Thermal Storage Heaters

• Solar Energy Storage

• Ice-based Technology

• Miscibility Gap Alloy Technology

Storage Material Outlook (Revenue, USD Million, 2016 - 2027)

• Molten Salt

• Phase Change Material

• Water

Application Outlook (Revenue, USD Million, 2016 - 2027)

• Process Heating & Cooling

• District Heating & Cooling

• Power Generation

• Ice storage air-conditioning

• Others

End-user Outlook (Revenue, USD Million, 2016 - 2027)

• Industrial

• Utilities

• Residential & Commercial

Regional Outlook (Revenue, USD Million, 2016 - 2027)

• North America

o U.S.

o Canada

o Mexico

• Europe

o U.K.

o Russia

o Germany

o Spain

��� Asia Pacific

o China

o India

o Japan

o South Korea

• Central & South America

o Brazil

• Middle East and Africa (MEA)

o Saudi Arabia

Browse through Grand View Research's Power Generation & Storage Industry Research Reports.

• The global energy storage for unmanned aerial vehicles market size was estimated at USD 413.25 million in 2023 and is expected to grow at a CAGR of 27.8% from 2024 to 2030.

• The global heat recovery steam generator market size was estimated at USD 1,345.2 million in 2023 and is projected to reach USD 1,817.0 million by 2030 and is anticipated to grow at a CAGR of 4.5% from 2024 to 2030.

Key Companies & Market Share Insights

Industry participants are integrating advanced technologies into the existing technology to enhance the product demand through the provision of improved thermal energy management systems. Furthermore, eminent players are emphasizing on inorganic growth ventures as a part of their strategic expansion. Some of the prominent players in the global thermal energy storage market include:

• BrightSource Energy Inc.

• SolarReserve LLC

• Abengoa SA

• Terrafore Technologies LLC

• Baltimore Aircoil Company

• Ice Energy

• Caldwell Energy

• Cryogel

• Steffes Corporation

Order a free sample PDF of the Thermal Energy Storage Market Intelligence Study, published by Grand View Research.

#Thermal Energy Storage Market#Thermal Energy Storage Industry#Thermal Energy Storage Market size#Thermal Energy Storage Market share#Thermal Energy Storage Market analysis

0 notes

Text

Meticulous Research®, a prominent global market research firm, has released an in-depth analysis titled, "Hydrogen Generation Market by Type (Gray, Green, Blue), Process (Hydrogen Generation, Hydrogen Storage), Source (Fossil Fuels, Nuclear, Solar), Application (Ammonia Production, Petroleum Refinery, E-mobility, Power Generation) - Global Forecast to 2030."

According to this latest report, the global hydrogen generation market is projected to reach $188.2 billion by 2030, growing at a CAGR of 8.4% from 2023 to 2030. The market expansion is primarily driven by the surging demand for hydrogen within the chemicals sector and robust governmental initiatives promoting the shift towards clean energy. Despite the substantial capital costs associated with hydrogen storage, the market is set to grow due to the increasing focus on green hydrogen production technologies and the burgeoning use of hydrogen in fuel cell electric vehicles (FCEVs). However, challenges such as the lack of secure infrastructure for hydrogen transport and storage persist.

Download Free Sample Report Here: https://www.meticulousresearch.com/download-sample-report/cp_id=5600

Market Segmentation and Key Insights:

By Type: The market is segmented into gray hydrogen, blue hydrogen, green hydrogen, and others. In 2023, gray hydrogen is expected to dominate the market share, driven by its demand in fertilizer production and fuel applications. Meanwhile, green hydrogen is anticipated to exhibit the highest growth rate, attributed to advancements in electrolysis technologies and the rising demand in FCEVs and the power sector.

By Process: The segmentation includes hydrogen generation and hydrogen storage processes. The hydrogen generation segment is forecasted to lead, spurred by industrial demand and efforts to reduce greenhouse gas emissions through renewable energy sources and decarbonization technologies.

By Source: This includes fossil fuels, nuclear, water, solar, biomass, and others. The fossil fuels segment is set to hold the largest share in 2023 due to efforts in reducing emissions and government incentives. However, the solar segment is poised for the highest growth, propelled by the demand for green hydrogen and low-cost production methods.

By Application: The applications cover ammonia production, petroleum refinery, E-mobility, methanol production, district heating, power generation, manufacturing, and synfuel production. Ammonia production is projected to lead in 2023, driven by its use as a low-carbon fuel and in industry decarbonization. The E-mobility segment will grow the fastest due to the rising adoption of FCEVs and expanding hydrogen fueling infrastructure.

By Geography: The report covers North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific is anticipated to dominate the market, followed by Europe and North America, due to the region’s commitment to carbon-free hydrogen production and renewable energy initiatives.

Quick Buy: https://www.meticulousresearch.com/Checkout/85905435

Key Market Players:

The leading companies in the hydrogen generation market include Plug Power Inc. (U.S.), Linde GmbH (Germany), Air Products and Chemicals, Inc. (U.S.), L’AIR LIQUIDE S.A. (France), Matheson Tri-Gas, Inc. (U.S.), SOL Spa (Italy), Cummins Inc. (U.S.), Siemens Energy AG (Germany), Shell plc (U.K.), Messer SE & Co. KGaA (Germany), Ballard Power Systems Inc. (Canada), FuelCell Energy, Inc. (U.S.), Iwatani Corporation (Japan), Enapter AG (Germany), CALORIC Anlagenbau GmbH (Germany), SPG Hydrogen Co., Ltd. (South Korea), Uniper SE (Germany), and Nel ASA (Norway).

Download the Sample Report Here: Sample Report

Key Questions Addressed:

What are the high-growth market segments by type, process, source, application, and geography?

How has the hydrogen generation market evolved historically, and what are the forecasts for 2023–2030?

What are the key drivers, restraints, opportunities, and challenges in the market?

Who are the major players, and what are their market shares?

What is the competitive landscape and recent developments in the hydrogen generation market?

What strategies are major players adopting to compete in the market?

What are the key geographic trends, and which countries exhibit high growth?

Contact Us:

Meticulous Research®

Email: [email protected]

Phone: +1-646-781-8004

Connect with us on LinkedIn

0 notes

Text

District Heating Market Analysis: Global Perspective

The growing district heating market is entering an era of energy transition driven by the increasing focus on renewable and clean energy sources. District heating involves the distribution of steam, hot water or chilled liquids for heating and cooling multiple buildings in a designated area through an underground network of insulated pipelines. It provides an efficient space heating alternative for residential, commercial and industrial buildings. The global district heating market is estimated to be valued at US$ 50.8 billion in 2024 and is expected to exhibit a CAGR of 1.5% over the forecast period 2023 to 2030.

Key Takeaways

Key players operating in the district heating market: Key players operating in the district heating market are Vattenfall AB, SP Group, Danfoss Group, Engie, NRG Energy Inc., Statkraft AS, Logstor AS, Shinryo Corporation, Vital Energi Ltd, Göteborg Energi, Alfa Laval AB, Ramboll Group AS, Keppel Corporation Limited, FVB Energy. The major players are focusing on renewable energy sourced heating solutions to gain a competitive edge in the growing market.

Growing demand in the market: There is a growing demand for district heating solutions across the commercial, residential and industrial sectors due to their cost effectiveness and energy savings. The increasing focus on reducing carbon emissions is also driving the adoption of low carbon district heating technologies in many countries.

Global expansion of the market: Major district heating companies are expanding their global footprint by entering new markets through strategic partnerships and acquisitions. The European countries continue to dominate the market while Asia Pacific region is expected to exhibit fastest growth over the forecast period led by increasing investments in renewable energy based heating projects in China and India.

Market Key Trends

The increased focus on renewable energy based district heating is one of the key trends in this market. Renewable sources such as solar, geothermal, biomass are increasingly being used to power district heating plants across regions. This is helping reduce reliance on fossil fuels for heating buildings and lower carbon footprint of the heating sector. Countries like Denmark have adopted renewable sourced district heating at a large scale.

Porter's Analysis

Threat of new entrants: High capital requirements act as a barrier for new companies to enter the district heating market. Bargaining power of buyers: Buyers have low bargaining power due to the essential heating services provided by existing district heating companies. Bargaining power of suppliers: Supplier power is moderate as district heating companies can switch between different fuel sources like natural gas, biomass and waste heat based on prices. Threat of new substitutes: threat is low as there are limited substitutes for district heating networks that provide heating at large scale. Competitive rivalry: Competitive rivalry is high between existing established players owing to their large geographical presence and long term customer contracts.

Geographical Regions

Europe accounts for the major share of the district heating market in terms of value due to stringent government policies and initiatives in countries like Germany, Poland, Sweden, Denmark and Finland that have enabled large scale development and adoption of district heating networks. Asia Pacific region is expected to be the fastest growing regional market for district heating over the forecast period supported by ongoing expansion of heating infrastructure in countries like China and Japan.

0 notes

Text

0 notes

Text

Unlocking the Potential of Renewable Energy in District Heating: Market Analysis

District Heating Market will witness highest growth driven by Infrastructural Developments

The global district heating market is estimated to be valued at US$ 50.8 Bn in 2024 and expected to exhibit a CAGR of 1.5% over the forecast period 2023 to 2030. District heating refers to the distribution of steam, hot water or chilled water from a central plant for residential and commercial heating requirements such as space heating and water heating. It is considered an efficient method to heat multiple buildings through a system of insulated pipes which transfers heat generated from centralized location through steam or hot water. District heating is advantageous as it provides reliable and sustainable method of heating with greater efficiency while minimizing carbon footprint.

Key Takeaways

Key players operating in the district heating market are Vattenfall AB, SP Group, Danfoss Group, Engie, NRG Energy Inc., Statkraft AS, Logstor AS, Shinryo Corporation, Vital Energi Ltd, Göteborg Energi, Alfa Laval AB, Ramboll Group AS, Keppel Corporation Limited, and FVB Energy. The global demand for district heating is growing due to rising energy demand from industrial, commercial and residential sectors. Technological advancements such as operation optimization, automation and integration of renewable energy are improving the efficiency of district heating systems.

Market Trends

The district heating market is witnessing growing focus on renewable energy and low carbon fuels to integrate sustainable heating solutions. Most district heating utilities are investing in renewable technologies such as solar thermal, geothermal, biomass and heat pumps. Secondly, the development of fourth-generation district heating is gaining momentum which utilizes lower temperature heat sources that can be extracted from sewage, ambient heat from rivers and lakes.

Market Opportunities

Rising investments in infrastructural development of smart cities and urbanization in developing countries provide lucrative opportunities. Advancing technology will play a vital role to develop efficient and low-cost systems. Growing awareness regarding environment protection and policies promoting use of renewable energy will further drive the adoption of district heating solutions.

Geographical Concentration of District Heating Market

In terms of value, Europe accounts for the largest share of the global district heating market, led by countries like Germany, Poland, Sweden, Denmark and Russia. Europe has a well-established district heating infrastructure serving over 60% of residential heating demand. Central and Eastern European countries are actively investing in network expansion driven by low carbon targets.

Asia Pacific is recognized as the fastest growing regional market for district heating globally. Rapid urbanization and industrialization are driving the demand in China, India and Southeast Asian nations. Supportive policies and incentives are encouraging adoption of district heating especially in northern China provinces. Development of new systems integrated with renewable energy and waste heat recovery will accelerate the market growth in Asia Pacific.

0 notes

Text

District Heating Market: Regulatory Framework and Impact Analysis

The global district heating market is estimated to be valued at US$ 50.8 Bn in 2024 and is expected to exhibit a CAGR of 1.5% over the forecast period 2023 to 2030.

District heating, also known as teleheating, involves the distribution of steam, hot water or hot air to multiple buildings in a designated area for space or water heating purposes. District heating plants produce steam or hot water at a centralized location and deliver it through a system of insulated pipes in order to supply space heating and hot water to residential and commercial buildings in the area. It is an efficient way of sourcing heat for communities as it reduces infrastructure costs involved in individual heating systems. Rising awareness about carbon footprint reduction and the need for sustainable heating solutions have boosted the adoption of district heating across both developed and developing economies.

Key Takeaways

Key players operating in the district heating market are Vattenfall AB, SP Group, Danfoss Group, Engie, NRG Energy Inc., Statkraft AS, Logstor AS, Shinryo Corporation, Vital Energi Ltd, Göteborg Energi, Alfa Laval AB, Ramboll Group AS, Keppel Corporation Limited, FVB Energy. Vattenfall AB and SP Group collectively account for over 30% share of the global market.

Growing focus on reducing carbon emissions from the building sector has significantly boosted the demand for district heating systems. Stringent regulations pertaining to energy efficiency and use of renewable energy are encouraging utilities as well as commercial and residential complexes to adopt district heating.

Technological advancements such as integration of IoT capabilities and advanced sensing equipment in district heating systems allow for improved monitoring and control of the entire network. This has enhanced the operational efficiency and reliability of district heating infrastructure. Use of 4G/5G based communication technologies is also enabling utilities to implement predictive analytics for predictive maintenance.

Market Trends

Use of renewable and waste heat sources: Growing focus on utilizing renewable and untapped waste heat sources like solar thermal, geothermal, biomass and industrial waste heat for district heating applications presents significant opportunities. Countries like Denmark have successfully demonstrated the potential of renewable district heating.

Digitalization of infrastructure: Integration of sensors, IoT, cloud computing, data analytics and automation enables utilities to remotely monitor heat networks and optimize operations. This helps improve efficiency, flexibility and reliability of district heating services. Ongoing development of advanced smart grids supports the use of smart technologies.

Market Opportunities

Combined heat and power (CHP) plants: Widening scope of cogeneration/CHP technology enables further recovery of waste heat from power generation for district heating. It provides an environment-friendly and cost-effective option for utilities.

Renovation of aging infrastructure: As a significant part of the installed district heating systems in Europe and North America is approaching end of life, renovation and modernization of existing pipelines and equipment provides lucrative opportunities.

Impact of COVID-19 on the District Heating Market

The COVID-19 pandemic has adversely impacted the growth of the district heating market globally. During the outbreak, commercial and industrial activities came to a halt which lowered the demand for district heating from these sectors. This led to a substantial decline in sales revenue for district heating companies in 2020. Many planned projects were deferred or delayed due to supply chain disruptions and halted construction activities during the peak pandemic phase.

0 notes

Text

Non-Concentrating Solar Collector Market: Global Demand Analysis & Opportunity Outlook 2036

Research Nester’s recent market research analysis on “Non-Concentrating Solar Collector Market: Global Demand Analysis & Opportunity Outlook 2036” delivers a detailed competitors analysis and a detailed overview of the global Non-Concentrating Solar Collector market in terms of market segmentation by type, device type, indication, distribution channel, and by region.

Growing Construction of Smart Cities to Promote Global Market Share of Non-Concentrating Solar Collector

Smart cities depend on information and communication technology (ICT) to increase operational efficiency and raise living standards for their citizens. Their primary objective is to maximize city services and encourage economic growth via the use of smart technologies and data analysis. Smart cities improve public health in addition to public safety. As a result, governments everywhere are initiating efforts to create smart cities, increasing the need for sustainable energy sources. Solar thermal collectors are being placed in various smart city regions, and households are being pushed to convert from traditional energy sources to solar energy in order to reduce pollution and foster a sustainable lifestyle. The number of smart cities is increasing across the globe. As per the Smart City pitchbook published by the government of United Kingdom, in 2020, the global smart cities sector was estimated to value £900 billion. This growing construction of smart cities is estimated to result in the growth of non-concentrating solar collector market. Some of the major growth factors and challenges that are associated with the growth of the global Non-Concentrating Solar Collector market are:

Growth Drivers:

Growing Concern Regarding the Effects of Fossil Fuels

Increasing Government Initiatives

Challenges:

The erratic availability of solar radiation and inadequate sunshine in some parts of the world. Additionally, solar energy can still be captured on cloudy days, although the efficiency of the system declines. Sunlight is necessary for solar panels to efficiently gather solar energy. That's why a couple of cloudy, rainy days may really affect the energy system. Thus, this is one of the main issues that could prevent the market for non-concentrating solar collectors from expanding.

Furthermore, high initial and maintenance costs, and shortage of space for setting up the systems are other factors that may hamper the growth of the non-concentrating solar collector market.

By application, the global Non-Concentrating Solar Collector market is segmented into residential, commercial, and industrial. The residential segment is anticipated to hold a share of 46% by the end of 2036. The primary use of solar thermal systems in residential settings is for domestic hot water systems, which produce hot water. The main driver of the home solar thermal business is the global expansion of solar district heating projects. In addition to meeting the increasing need for ecologically friendly solutions for space and domestic water heating, among other heating demands, they are crucial to the decarbonization of the heating sector. The market will develop even more as a result of new regulations pertaining to the implementation of green building codes, such as energy-saving building codes in the US, China, India, and other countries. Growth in the market will also be fueled by increased investment in the construction industry for the re-establishment and renovation of structures.

Request Report Sample@

By region, the Asia Pacific Non-Concentrating Solar Collector market is to hold the largest share of 36% during the foreseen period. Because of the growing demand for both ongoing and future solar power projects, the industry is expanding in the region. In China, solar power increased by 33.7% while coal power increased by 1.8% in the first quarter. China already has nearly half of its 1,130 GW of coal power plants online due to the 430 GW of solar energy generated thus far. Additionally, it is projected that the industry would gain from enticing government initiatives and funding for clean, renewable energy. For example, the "Top Runner Program" was introduced by the Chinese government to encourage the adoption of solar photovoltaic (PV) panels that are incredibly efficient. China uses efficiency criteria for PV modules as part of this plan, which drives manufacturers to create and market more efficient solar panels.

Access our detailed report at:

0 notes

Text

EMERGING TRENDS IN GEOTHERMAL ENERGY

Geothermal energy is a renewable energy source derived from the heat stored beneath the Earth's surface. It involves tapping into the natural heat of the Earth to generate electricity or provide direct heating. Over the years, several emerging trends have been shaping the development and utilization of geothermal energy. These trends reflect advancements in technology, changes in market dynamics, and growing environmental concerns. Let's delve into these emerging trends in elaborate detail:

Enhanced Geothermal Systems (EGS): Enhanced Geothermal Systems involve creating artificial reservoirs by injecting water into hot rock formations, fracturing them to increase permeability, and then extracting the heated water or steam to generate electricity. EGS has the potential to expand the geographical range of geothermal power generation, making it feasible in areas previously considered non-viable for conventional geothermal projects. Research and development efforts are focusing on improving the efficiency of EGS, reducing costs, and minimizing environmental impacts.

Direct Use Applications: Geothermal energy is not only used for electricity generation but also for direct heating in various applications, such as district heating systems, greenhouses, aquaculture, and industrial processes. The trend is towards expanding these direct use applications, as they offer an efficient and cost-effective means of utilizing geothermal resources while reducing greenhouse gas emissions in sectors beyond electricity generation.

Geothermal Heat Pumps (GHPs): Geothermal heat pumps, also known as ground source heat pumps, use the relatively constant temperature of the Earth's subsurface to provide heating, cooling, and hot water for buildings. This technology is gaining traction as an energy-efficient alternative to traditional heating and cooling systems. GHPs can significantly reduce energy consumption and related carbon emissions in residential, commercial, and industrial buildings.

Geothermal Desalination: Geothermal energy can be used to power desalination processes, converting seawater or brackish water into freshwater. This emerging trend holds promise for addressing water scarcity issues, especially in regions where both water and geothermal resources are abundant. Geothermal desalination projects are being explored as a sustainable solution to provide a constant supply of freshwater for agriculture, drinking, and industrial purposes.

Integration with Other Renewable Energy Sources: Geothermal energy can complement other renewable sources, such as solar and wind power, by providing baseload electricity generation that's not dependent on weather conditions. Hybrid systems that combine geothermal power with other renewables and energy storage technologies are being developed to create more stable and reliable energy generation profiles.

Innovations in Exploration and Resource Assessment: Advanced exploration techniques, such as seismic imaging, remote sensing, and geochemical analysis, are being used to locate and characterize geothermal reservoirs with greater accuracy. This helps reduce exploration risks, lower upfront costs, and increase the overall efficiency of geothermal projects.

Global Market Growth: The growing emphasis on decarbonization and the transition to clean energy sources has led to increased interest in geothermal energy worldwide. Governments, international organizations, and private investors are recognizing its potential and providing support for research, development, and deployment of geothermal projects.

Decentralized and Off-Grid Systems: Geothermal energy can play a crucial role in providing reliable and sustainable energy access to remote and off-grid communities. Decentralized geothermal power plants and microgrids are being developed to meet the energy needs of such communities, reducing their reliance on fossil fuels and diesel generators.

Environmental Sustainability: Geothermal energy is considered one of the most environmentally friendly energy sources, producing minimal greenhouse gas emissions and having a small land footprint compared to other renewable sources. As environmental concerns become more pronounced, geothermal's eco-friendliness is becoming a more significant driver for its adoption.

Mr. Jayesh Saini notes that, “The emerging trends in geothermal energy are characterized by technological advancements, expanded applications, increased integration with other renewable sources, and a growing global interest in harnessing its potential. These trends collectively contribute to positioning geothermal energy as a key player in the global transition towards a more sustainable and low-carbon energy future.”

#jayeshsaini #healthcare #LifeCareHospitals #Kenya #NHIF #NPS #TSC

0 notes

Text

District Heating Market Will Grow the Fastest in APAC