#Telecom Power System Market Trends

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

28.6 is the average number of monthly visits per US mobile user.

Text

Navigating the Telecom Power System Market: Global Industry Outlook

Increasing demand for compact and modular telecom power systems and the growing adoption of virtualization in telecom power systems are likely to drive the Market in the forecast period.

According to TechSci Research report, “Telecom Power System Market – Global Industry Size, Share, Trends, Competition Forecast & Opportunities, 2028”, the Global Telecom Power System Market is experiencing a surge in demand in the forecast period. A primary driver propelling the global Telecom Power System market is the widespread deployment of 5G technology. The advent of 5G has ushered in a new era of connectivity, offering faster data speeds, reduced latency, and increased network capacity. The implementation of 5G networks requires a significant upgrade of telecom infrastructure, driving the demand for advanced Telecom Power Systems. These systems play a pivotal role in providing the reliable and efficient power necessary to support the denser network of small cells characteristic of 5G deployment.

Telecom Power Systems must adapt to the unique requirements of 5G, accommodating the increased number of small cells and ensuring seamless integration into diverse environments. As the global demand for higher data speeds and enhanced connectivity continues to grow, the deployment of 5G technology acts as a potent driver, pushing the Telecom Power System market to innovate and evolve to meet the challenges of this next-generation network.

The exponential growth of the Internet of Things (IoT) is a significant driver fueling the global Telecom Power System market. The increasing prevalence of connected devices, from smart sensors to industrial machinery, demands a robust and reliable telecommunication infrastructure. Telecom Power Systems play a critical role in supporting the communication needs of IoT applications, providing the necessary power to base stations and data centers.

As industries across sectors embrace IoT for improved efficiency and real-time monitoring, the demand for Telecom Power Systems that can handle the unique challenges posed by IoT deployments is on the rise. These power systems must be scalable, energy-efficient, and capable of adapting to the diverse needs of IoT, contributing to the seamless integration and functionality of connected devices. The proliferation of IoT applications worldwide acts as a driving force, compelling Telecom Power System providers to develop innovative solutions to meet the evolving demands of this interconnected era.

Browse over XX Market data Figures spread through XX Pages and an in-depth TOC on "Global Telecom Power System Market.” https://www.techsciresearch.com/report/telecom-power-system-market/23070.html

The Global Telecom Power System Market is segmented into grid type, component, power source, and region.

Based on grid type, The On Grid segment held the largest Market share in 2022. On-Grid systems are well-suited for urban and developed areas where the power grid infrastructure is stable and reliable. In these regions, there is a consistent and uninterrupted power supply, making on-grid solutions a cost-effective and practical choice.

Connecting telecom infrastructure to an existing power grid is often more cost-effective than setting up independent power systems. The infrastructure is already in place, reducing the need for additional investment in off-grid or backup power solutions.

On-Grid systems benefit from the reliability and consistency of power supply from the main electrical grid. Telecom operations in areas with a stable grid connection experience minimal disruptions, ensuring continuous communication services.

Maintenance and servicing of on-grid power systems are generally more straightforward. The infrastructure is readily accessible, and any issues can be addressed without the complexity associated with off-grid solutions, where remote locations may pose logistical challenges.

In regions where the cost of energy from the grid is competitive or economical, telecom operators may opt for on-grid solutions. The availability of affordable grid electricity can make on-grid Telecom Power Systems a financially viable choice.

Regulatory frameworks and permitting processes often favor on-grid solutions, especially in urban areas. Connecting to the existing power grid may involve fewer regulatory hurdles compared to establishing off-grid or hybrid solutions with renewable energy sources.

On-Grid systems offer scalability, allowing telecom operators to easily expand their networks without significant modifications to the power infrastructure. This scalability is particularly beneficial in densely populated urban areas experiencing high demand for telecommunication services.

Based on power source, The diesel-Battery segment held the largest Market share in 2022. Diesel generators are known for their reliability and can provide a constant power supply. This is crucial for telecom infrastructure, where uninterrupted power is essential to ensure continuous communication.

Diesel generators can operate in various environmental conditions, making them suitable for telecom installations in diverse locations, including remote or challenging terrains.

Diesel generators can operate for extended periods without refueling, providing an autonomous power source. This is particularly important in areas with unreliable or no access to the electrical grid.

Combining diesel generators with battery systems allows for better energy management. Batteries can store excess energy generated by the diesel generator and release it during peak demand or in case of generator failure, providing a seamless power supply.

Modern diesel generators are designed to be fuel-efficient, reducing operational costs over time. The combination of diesel and battery systems allows for optimization of fuel usage.

While diesel generators are known for their emissions, advancements in technology have led to more fuel-efficient and environmentally friendly models. Additionally, the integration of battery systems helps reduce reliance on diesel power during periods of lower demand.

In regions with unreliable or underdeveloped power grids, telecom installations often need to operate independently. Diesel-battery systems provide a reliable off-grid solution.

Major companies operating in the Global Telecom Power System Market are:

Huawei Technologies Co., Ltd.

Ericsson AB

Nokia Corporation

ABB Ltd.

Emerson Electric Co.

Siemens AG

Eaton Corporation PLC

Schneider Electric SE

Hitachi Ltd.

Samsung Electronics Co., Ltd.

Download Free Sample Report https://www.techsciresearch.com/sample-report.aspx?cid=23070

Customers can also request for 10% free customization on this report.

“The Global Telecom Power System Market is expected to rise in the upcoming years and register a significant CAGR during the forecast period. The growth of the telecom power systems market is being driven by several factors, including the increasing demand for reliable and efficient power systems for telecommunications networks, the growing adoption of 5G networks, and the increasing need for renewable energy sources. Also, The Asia Pacific region is expected to be the fastest-growing market for telecom power systems, due to the rapid growth of the telecommunications industry in the region.

The Middle East and Africa region is also expected to witness significant growth, as countries in the region invest in upgrading their telecommunications infrastructure. The telecom power systems market is a fragmented market, with a large number of players. Some of the leading players in the market include Huawei, Ericsson, Nokia, ABB, and Emerson Electric. Therefore, the Market of Telecom Power System is expected to boost in the upcoming years.,” said Mr. Karan Chechi, Research Director with TechSci Research, a research-based management consulting firm.

“Telecom Power System Market - Global Industry Size, Share, Trends, Opportunity, and Forecast, 2018-2028 Segmented By Grid Type (On Grid, Off Grid, Bad Grid), By Component (Rectifier, Inverter, Converter, Controller, Heat Management Systems, Generators, Others), By Power Source (Diesel-Battery, Diesel-Solar, Diesel-Wind, Multiple Sources), By Region, By Competition”, has evaluated the future growth potential of Global Telecom Power System Market and provides statistics & information on Market size, structure and future Market growth. The report intends to provide cutting-edge Market intelligence and help decision-makers make sound investment decisions., The report also identifies and analyzes the emerging trends along with essential drivers, challenges, and opportunities in the Global Telecom Power System Market.

Browse Related Reports

Air-Operated Grease Market https://www.techsciresearch.com/report/air-operated-grease-market/23568.html

Portable Grease Pumps Market https://www.techsciresearch.com/report/portable-grease-pumps-market/23569.html

Industrial Belt Drives Market https://www.techsciresearch.com/report/industrial-belt-drives-market/23573.html Contact Us-

TechSci Research LLC

420 Lexington Avenue, Suite 300,

New York, United States- 10170

M: +13322586602

Email: [email protected]

Website: www.techsciresearch.com

#Telecom Power System Market#Telecom Power System Market Size#Telecom Power System Market Share#Telecom Power System Market Trends#Telecom Power System Market Growth

0 notes

Text

Exploring the Growth and Opportunities in the Telecom Tower Power Systems Market

The Telecom Tower Power Systems Market is witnessing significant growth, driven by the rising demand for seamless connectivity, increased mobile data traffic, and the expansion of telecom infrastructure in remote and rural areas. As the telecom industry rapidly evolves to support 5G technology, the need for robust and efficient power systems becomes increasingly critical. This market is poised…

#Telecom Tower Power Systems Market#Telecom Tower Power Systems Market Demand#Telecom Tower Power Systems Market Forecast#Telecom Tower Power Systems Market Growth#Telecom Tower Power Systems Market Report#Telecom Tower Power Systems Market Share#Telecom Tower Power Systems Market Size#Telecom Tower Power Systems Market Trends

0 notes

Text

5 Trends in ICT

Exploring the 5 ICT Trends Shaping the Future The Information and Communication Technology (ICT) landscape is evolving at a rapid pace, driven by advancements that are transforming how we live, work, and interact. Here are five key trends in ICT that are making a significant impact:

1. Convergence of Technologies

Technologies are merging into integrated systems, like smart devices that combine communication, media, and internet functions into one seamless tool. This trend enhances user experience and drives innovation across various sectors

Convergence technologies merge different systems, like smartphones combining communication and computing, smart homes using IoT, telemedicine linking healthcare with telecom, AR headsets overlaying digital on reality, and electric vehicles integrating AI and renewable energy.

2. Social Media

Social media platforms are central to modern communication and marketing, offering real-time interaction and advanced engagement tools. New features and analytics are making these platforms more powerful for personal and business use.

Social media examples linked to ICT trends include Facebook with cloud computing, TikTok using AI for personalized content, Instagram focusing on mobile technology, LinkedIn applying big data analytics, and YouTube leading in video streaming.

3. Mobile Technologies

Mobile technology is advancing with faster 5G networks and more sophisticated devices, transforming how we use smartphones and tablets. These improvements enable new applications and services, enhancing connectivity and user experiences.

Mobile technologies tied to ICT trends include 5G for high-speed connectivity, mobile payment apps in fintech, wearables linked to IoT, AR apps like Pokémon GO, and mobile cloud storage services like Google Drive.

4. Assistive Media

Assistive media technologies improve accessibility for people with disabilities, including tools like screen readers and voice recognition software. These innovations ensure that digital environments are navigable for everyone, promoting inclusivity.

Assistive media examples linked to ICT trends include screen readers for accessibility, AI-driven voice assistants, speech-to-text software using NLP, eye-tracking devices for HCI, and closed captioning on video platforms for digital media accessibility.

5. Cloud Computing

Cloud computing allows for scalable and flexible data storage and application hosting on remote servers. This trend supports software-as-a-service (SaaS) models and drives advancements in data analytics, cybersecurity, and collaborative tools.

Cloud computing examples related to ICT trends include AWS for IaaS, Google Drive for cloud storage, Microsoft Azure for PaaS, Salesforce for SaaS, and Dropbox for file synchronization.

Submitted by: Van Dexter G. Tirado

3 notes

·

View notes

Text

Horizontal Directional Drilling Market Demand, Trends, Forecast 2022-2029

BlueWeave Consulting, a leading strategic consulting and market research firm, in its recent study, estimated the Global Horizontal Directional Drilling Marketsize at USD 9.46 billion in 2022. During the forecast period between 2023 and 2029, BlueWeave expects Global Horizontal Directional Drilling Marketsize to grow at a significant CAGR of 5.7% reaching a value of USD 13.21 billion by 2029. Major growth drivers for the Global Horizontal Directional Drilling Marketinclude the increasing adoption of HDD technology for precise and minimally invasive drilling operations. This technique facilitates the drilling and reverse reaming of pipes with precision, navigating through obstacles in the underground terrain while minimizing harm to ecosystems. Market expansion is further fueled by increasing investments in shale gas projects and the ongoing development of high-speed connectivity in the telecom industry. Notably, The global surge in oil and gas activities has spurred an increase in horizontal directional drilling (HDD) worldwide. Recognizing the environmental impact of conventional drilling methods, there is a growing emphasis on employing eco-friendly drilling technology, leading to the expansion of the Global Horizontal Directional Drilling Market. The horizontal directional drilling approach stands out for its precision and reduced power consumption compared to vertical maneuvering techniques. Another significant driving force is the rapid globalization and urbanization, fueled by the escalating energy and fuel demand in developing nations. This surge in demand is closely tied to ongoing infrastructure development, utility system construction, and advancements in the telecommunications sector, including 5G testing. These factors, along with related developments, are anticipated to contribute significantly to the market's swift growth during the forecast period. The increasing utilization of horizontal directional drilling products in surveying, designing, and installing subsurface electrical systems for subterranean cables further propels the expansion of the market. Also, the rising demand for natural gas and electricity distribution in middle and upper pipeline lines is expected to drive market growth. The use of horizontal directional drilling fasteners in utility, communications, and oil and gas industries offers benefits such as increased stability, enhanced device management, and improved treatment and monitoring outcomes. However, high costs and technical challenges are anticipated to restrain the overall market growth during the forecast period.

Impact of Escalating Geopolitical Tensions on Global Horizontal Directional Drilling Market

The Global Horizontal Directional Drilling Market has been significantly impacted by intensifying geopolitical disruptions in recent times. For instance, the ongoing Russia-Ukraine conflict has disrupted supply chains decreased service demand, and increased uncertainty for businesses. This turmoil extended to energy markets, causing turbulence due to Russia's significant role as a major gas supplier, resulting in noticeable price fluctuations. In addition, the sanctions imposed on Russia by the United States and other have had widespread implications, injecting a level of risk for investors across various sectors. Beyond the war zones and disputed areas, the ongoing crisis jeopardizes stability on a global scale. It becomes imperative for businesses and investors alike to comprehend and adeptly manage these interconnected challenges.

Despite the current challenges posed by geopolitical tensions, there are potential growth opportunities for the Global Horizontal Directional Drilling Market. The ongoing infrastructure projects, utility installations, and the continuous expansion of the telecommunications industry. This demand underscores the market's resilience. Emphasizing strategic adaptation is crucial in navigating these complex circumstances, ensuring sustained success amid global challenges and uncertainties.

Sample Request @ https://www.blueweaveconsulting.com/report/biodegradable-sanitary-napkins-market/report-sample

Global Horizontal Directional Drilling Market – By End User

On the basis of end user, the Global Horizontal Directional Drilling Market is divided into Oil & Gas Excavation, Utilities, and Telecommunication segments. The oil & gas excavation segment holds the highest share in the Global Horizontal Directional Drilling Market by end user. The existing and robust infrastructure generates a significant demand for drilling rigs, contributing to the predominant market position of the oil and gas excavation segment. Also, efforts to manage the increasing expenses linked to exploration and production endeavors in untapped regions are anticipated to strengthen the prominence of this segment. Meanwhile, the telecommunications segment holds the highest share in the Global Horizontal Directional Drilling Market. The increasing need for faster broadband access propels telecommunications operators to adopt advanced and reliable drilling services, including horizontal directional drilling. This method facilitates the expansion of optic fiber cable networks by deploying conduits and pipes through holes nearly 4 feet in diameter and 6,500 feet in length, particularly in offshore locations. The growing demand for 4G and 5G networks is expected to contribute significantly to the segment's growth throughout the forecast period.

Global Horizontal Directional Drilling Market – By Region

The in-depth research report on the Global Horizontal Directional Drilling Market covers various country-specific markets across five major regions: North America, Europe, Asia Pacific, Latin America, and Middle East and Africa. North America holds the highest share in the Global Horizontal Directional Drilling Market. According to the U.S. Energy Information Administration, liquid fuel consumption in 2022 was reported at 8.8 billion barrels per day. The growing prevalence of infrastructure and utility projects in North America is a key driver for the increased demand in horizontal directional drilling equipment and services. The Middle East and Africa (MEA) region emerged as the second-largest user of drilling services for oil and gas excavation activities.

Competitive Landscape

Major players operating in the Global Horizontal Directional Drilling Market include Baker Hughes Company, Barbco Inc., China Oilfield Services Limited, Ellingson Companies, Halliburton Company, Helmerich & Payne Inc., Herrenknecht AG, Nabors Industries Ltd, NOV Inc., Schlumberger Limited, The Toro Company, Vermeer Corporation, Weatherford International plc, Drillto Trenchless Co. Ltd, Laney Directional Drilling, Prime Drilling GmbH, XCMG Group, and TRACTO. To further enhance their market share, these companies employ various strategies, including mergers and acquisitions, partnerships, joint ventures, license agreements, and new product launches

Contact Us:

BlueWeave Consulting & Research Pvt. Ltd

+1 866 658 6826 | +1 425 320 4776 | +44 1865 60 0662

2 notes

·

View notes

Text

Back Office Workforce Management Market Size, Share & Growth Analysis 2034: Optimizing Operations with Automation & AI

Back Office Workforce Management Market is rapidly evolving as organizations seek smarter ways to handle non-customer-facing operations. Encompassing solutions such as task scheduling, labor forecasting, performance analytics, and time and attendance systems, this market is pivotal for businesses striving to increase operational efficiency. From banking to retail, companies are turning to these tools to automate manual processes, manage human capital effectively, and support strategic decision-making. With a market value of $3.1 billion in 2024 and projected growth to $6.4 billion by 2034, the sector is gaining strong momentum with a healthy CAGR of 7.5%.

Market Dynamics

What’s fueling this growth is a mix of technological innovation, rising labor costs, and the growing demand for transparency and accountability in business operations. The cloud-based deployment model leads with a 45% market share, offering flexibility, real-time access, and scalability to enterprises of all sizes. This is followed by on-premise (30%) and hybrid (25%) solutions, each addressing unique organizational needs.

Click to Request a Sample of this Report for Additional Market Insights: https://www.globalinsightservices.com/request-sample/?id=GIS24564

The top-performing sub-segment is scheduling and forecasting, as organizations seek accurate, automated methods to deploy resources more efficiently. Close behind is analytics and reporting, where businesses are capitalizing on real-time data to fine-tune productivity and performance. As hybrid and remote work become the norm, solutions that support workforce visibility and self-service functionality are in high demand.

Key Players Analysis

Major players such as Verint Systems, NICE Systems, and Aspect Software are leading the charge with robust platforms that integrate AI, machine learning, and mobile capabilities. These companies continue to innovate, delivering tools that not only optimize task assignments but also offer insights into workforce trends and operational gaps.

Emerging players like Work Sync Innovations, Back Office Dynamics, and Efficient Ops are also disrupting the space. Their agility in customizing niche solutions for SMEs and specific industries such as healthcare or retail makes them strong contenders. A common thread among these players is a focus on subscription-based models and user-friendly interfaces, making their platforms more accessible and cost-effective.

Regional Analysis

North America holds the dominant position in the back office workforce management market. The United States, with its strong presence of large enterprises and advanced tech infrastructure, drives innovation and adoption. Cloud-based tools and AI-powered platforms are becoming staples in sectors such as finance and telecom.

Europe follows closely, where compliance with labor laws and a structured approach to workforce efficiency have spurred adoption. Countries like Germany, France, and the UK are investing in data-driven performance tracking systems, particularly in industrial and government sectors.

The Asia Pacific region is emerging as a growth hub, thanks to the expanding service sector in India, China, and Southeast Asia. Digital transformation, coupled with a rising middle class and rapid urbanization, is accelerating demand for scalable workforce solutions.

Latin America and the Middle East & Africa are showing promising signs of adoption as businesses in these regions move toward operational maturity. Government support for digital infrastructure and increasing awareness of workforce optimization benefits are contributing to gradual but steady market penetration.

Recent News & Developments

The integration of AI and machine learning has revolutionized forecasting and performance analytics in workforce management. These technologies enable predictive insights, helping organizations proactively manage staffing, avoid bottlenecks, and ensure regulatory compliance. Companies like NICE Systems have introduced intelligent platforms that analyze employee behavior, forecast workloads, and generate actionable strategies in real time.

Another significant trend is the rise of subscription-based pricing models, which provide flexibility for smaller businesses to access enterprise-grade solutions. Additionally, cloud adoption continues to rise, enhancing real-time collaboration and mobility — a must-have in today’s hybrid working world.

Recent product launches and strategic partnerships between software vendors and system integrators are shaping the competitive landscape. These developments aim to deliver more integrated, customizable, and mobile-friendly platforms, especially for industries undergoing rapid digital shifts like retail, education, and healthcare.

Browse Full Report : https://www.globalinsightservices.com/reports/back-office-workforce-management-market/

Scope of the Report

This report presents a comprehensive overview of the Back Office Workforce Management Market, analyzing trends, opportunities, and challenges across types, applications, technologies, and regions. It covers historical data from 2018 to 2023, with forecasts up to 2034, providing businesses with deep insights into market growth and technological advancements.

Key areas explored include cloud versus on-premise deployments, AI integration, regulatory compliance strategies, and emerging use cases in hybrid work environments. The report also profiles key and emerging players, offering competitive intelligence on mergers, partnerships, and innovation strategies shaping the future of back office management.

#workforcemanagement #backofficeautomation #cloudsolutions #remoteworktools #aibusinesssolutions #digitaltransformation #employeeefficiency #hybridworktech #taskoptimization #enterprisetechnology

Discover Additional Market Insights from Global Insight Services:

Commercial Drone Market : https://www.globalinsightservices.com/reports/commercial-drone-market/

Product Analytics Market : https://www.globalinsightservices.com/reports/product-analytics-market/

Streaming Analytics Market : https://www.globalinsightservices.com/reports/streaming-analytics-market/

Cloud Native Storage Market ; https://www.globalinsightservices.com/reports/cloud-native-storage-market/

Alternative Lending Platform Market : https://www.globalinsightservices.com/reports/alternative-lending-platform-market/

About Us:

Global Insight Services (GIS) is a leading multi-industry market research firm headquartered in Delaware, US. We are committed to providing our clients with highest quality data, analysis, and tools to meet all their market research needs. With GIS, you can be assured of the quality of the deliverables, robust & transparent research methodology, and superior service.

Contact Us:

Global Insight Services LLC 16192, Coastal Highway, Lewes DE 19958 E-mail: [email protected] Phone: +1–833–761–1700 Website: https://www.globalinsightservices.com/

0 notes

Text

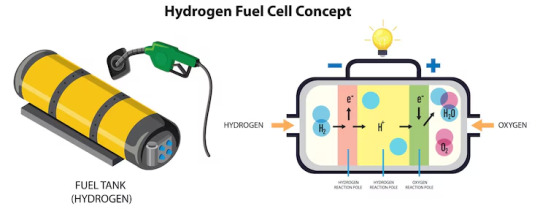

Global SOFC Market to Reach Multibillion-Dollar Milestone by 2030

Solid Oxide Fuel Cell Market Set for Multi-Billion Dollar Expansion by 2030, Driven by Clean Energy Demand and Fuel Flexibility

The solid oxide fuel cell (SOFC) market is undergoing unprecedented growth as global demand for cleaner, more resilient energy solutions intensifies. Valued at around USD 3.0 billion in 2024, the market is projected to expand at a compound annual growth rate (CAGR) of 26% to 30% over the next decade, reaching over USD 20 billion by 2032. The surge is fueled by increasing adoption across stationary power systems, the push for hydrogen-based energy, and major investments in fuel cell technologies from leading economies like the United States and Japan.

To Get Free Sample Report : https://www.datamintelligence.com/download-sample/solid-oxide-fuel-cell-market

Key Market Drivers

1. Clean Energy and Decarbonization Goals SOFCs generate electricity with high efficiency and low emissions by using fuels like hydrogen, natural gas, or biogas. Their ability to produce power at efficiencies above 60% and over 80% when used in combined heat and power (CHP) configurations makes them attractive for industrial, commercial, and residential applications aiming to reduce carbon footprints.

2. Government Policy and Incentives Supportive energy policies are a primary catalyst for SOFC adoption. In the United States, federal energy departments are investing heavily in SOFC R&D and pilot projects for defense, data centers, and critical infrastructure. Japan's Green Growth Strategy promotes widespread use of SOFCs in residential and commercial sectors. These programs are accelerating commercialization and technological maturity.

3. Advancements in Materials and Stack Design Recent breakthroughs in ceramic electrolytes, anode-supported cells, and metal-supported stack designs are reducing costs and improving durability. Companies like Bosch, Mitsubishi Heavy Industries, and Ceres Power are deploying scalable, modular SOFC systems with longer life cycles and faster ramp-up capabilities.

4. Demand for Distributed and Backup Power SOFCs are ideal for backup power in data centers, hospitals, and telecom infrastructure due to their low noise, low emissions, and minimal maintenance requirements. Their fuel flexibility ensures deployment in remote or off-grid areas, expanding their utility across regions with limited energy access.

Regional Insights: U.S. and Japan Lead Global Momentum

United States North America holds a substantial share of the SOFC market, led by major companies like Bloom Energy. The country is investing in hydrogen hubs and SOFC deployments for utility-scale and microgrid systems. Favorable tax credits and funding for energy resilience are further accelerating SOFC integration across public and private sectors.

Japan Japan is one of the world’s most aggressive adopters of SOFC technology. With a focus on energy security and net-zero goals, the country has launched initiatives to deploy millions of residential and commercial SOFC units. Companies such as Mitsubishi and Aisin are leading commercialization, while the government continues to subsidize installations and system development.

Market Segmentation and Technology Trends

Planar vs. Tubular SOFCs Planar solid oxide fuel cells dominate the market due to their modularity and lower manufacturing costs. Tubular designs are valued for their mechanical robustness but face challenges in scalability.

Stationary Applications Stationary SOFC systems remain the largest segment, accounting for more than 80% of the market. These are used in buildings, manufacturing plants, and district energy systems. Applications include backup power, grid balancing, and CHP.

Transport and Auxiliary Power Units (APUs) SOFCs are emerging in heavy-duty vehicles, marine transport, and aviation as auxiliary power sources. Their high energy density and quiet operation make them suitable for electrifying long-haul and industrial vehicles.

Portable and Remote Power Smaller SOFC units are being explored for military, camping, and disaster-recovery applications, especially where long-duration, off-grid energy is needed.

Get the Demo Full Report : https://www.datamintelligence.com/enquiry/solid-oxide-fuel-cell-market

Growth Opportunities

1. Hydrogen Integration and Reversible Systems SOFCs can run on hydrogen, and next-generation reversible SOFCs (rSOFCs) offer bidirectional functionality producing hydrogen when excess electricity is available and generating power when needed. This makes them ideal for future hydrogen grid integration.

2. Low-Temperature SOFC Development Companies are developing SOFCs that operate below 600°C, which reduces material costs and allows faster startup. This opens up new possibilities in transport and consumer electronics.

3. Marine and Defense Applications SOFC systems are being tested in naval vessels and defense infrastructure due to their stealth capabilities and independence from traditional fuel logistics.

4. Emerging Markets and Rural Electrification Regions in Southeast Asia, Africa, and South America are investing in decentralized energy solutions. SOFC systems provide clean, stable energy for off-grid villages and industrial operations.

Challenges and Constraints

High Capital Costs: While prices are falling, SOFC systems still carry high upfront costs due to materials and system integration.

Durability and Thermal Cycling: High operating temperatures lead to thermal stress. Innovation in stack materials and coatings is required for broader adoption.

Regulatory and Infrastructure Gaps: Deployment is constrained by a lack of uniform codes for hydrogen infrastructure and distributed generation.

Fuel Supply Chain: Access to affordable and clean hydrogen remains a bottleneck in many markets.

Conclusion

The global solid oxide fuel cell market is on a transformative path, aligning with the world’s urgent push toward clean and distributed energy. Governments, enterprises, and technology developers are now working together to scale up production, reduce costs, and expand SOFC applications across sectors.

With projected market values surpassing USD 20 billion by 2032, companies that innovate in stack design, fuel flexibility, and system integration will lead the next wave of sustainable power solutions. As the U.S. and Japan continue to drive research and commercialization, the SOFC industry is well-positioned to become a cornerstone of the global green energy future.

0 notes

Text

CPE Chip Market Analysis: CAGR of 12.1% Predicted Between 2025–2032

MARKET INSIGHTS

The global CPE Chip Market size was valued at US$ 1.58 billion in 2024 and is projected to reach US$ 3.47 billion by 2032, at a CAGR of 12.1% during the forecast period 2025-2032. This growth trajectory aligns with the broader semiconductor industry expansion, which was valued at USD 579 billion in 2022 and is expected to reach USD 790 billion by 2029 at a 6% CAGR.

CPE (Customer Premises Equipment) chips are specialized semiconductor components that enable network connectivity in devices such as routers, modems, and gateways. These chips power critical functions including signal processing, data transmission, and protocol conversion for both 4G and 5G networks. The market comprises two primary segments – 4G chips maintaining legacy infrastructure support and 5G chips driving next-generation connectivity with higher bandwidth and lower latency.

Market expansion is being propelled by three key factors: the global rollout of 5G infrastructure, increasing demand for high-speed broadband solutions, and the proliferation of IoT devices requiring robust connectivity. However, supply chain constraints in the semiconductor industry and geopolitical factors affecting chip production present ongoing challenges. Major players like Qualcomm and MediaTek are investing heavily in R&D to develop advanced CPE chipsets, while emerging players such as UNISOC and ASR are gaining traction in cost-sensitive markets. The Asia-Pacific region dominates production and consumption, accounting for over 45% of global CPE chip demand in 2024.

MARKET DYNAMICS

MARKET DRIVERS

5G Network Expansion Accelerates Demand for Advanced CPE Chips

The global transition to 5G networks continues to drive exponential growth in the CPE chip market. As telecom operators roll out next-generation infrastructure, the demand for high-performance customer premise equipment has surged by over 40% in the past two years. Modern 5G CPE devices require specialized chipsets capable of supporting multi-gigabit speeds, ultra-low latency, and massive device connectivity. Leading chip manufacturers are responding with integrated solutions that combine baseband processing, RF front-end modules, and AI acceleration. For instance, Qualcomm’s latest 5G CPE platforms deliver 10Gbps throughput while reducing power consumption by 30% compared to previous generations.

IoT Adoption Creates New Growth Avenues for CPE Chip Vendors

The proliferation of Internet of Things (IoT) applications across smart cities, industrial automation, and connected homes is generating significant opportunities for CPE chip manufacturers. With over 15 billion IoT devices projected to connect to networks by 2025, telecom operators require CPE solutions that can efficiently manage diverse traffic patterns and quality-of-service requirements. This has led to the development of specialized chipsets featuring advanced traffic management, edge computing capabilities, and enhanced security protocols. Recent product launches demonstrate this trend, with companies like MediaTek introducing chips optimized for IoT gateways that support simultaneous connections to hundreds of endpoints while maintaining reliable performance.

Remote Work Infrastructure Investments Fuel Market Expansion

The permanent shift toward hybrid work models continues to stimulate demand for enterprise-grade CPE solutions. Businesses worldwide are upgrading their network infrastructure to support distributed workforces, driving a 25% year-over-year increase in CPE deployments. This trend has particularly benefited manufacturers of chips designed for business routers and SD-WAN appliances, which require robust performance for VPNs, unified communications, and cloud applications. Leading semiconductor firms have responded with system-on-chip solutions integrating Wi-Fi 6/6E, multi-core processors, and hardware-accelerated encryption to meet these evolving requirements.

MARKET RESTRAINTS

Supply Chain Disruptions Continue to Challenge Production Stability

Despite strong demand, the CPE chip market faces persistent supply chain constraints that limit growth potential. The semiconductor industry’s reliance on advanced fabrication nodes has created bottlenecks, with lead times for certain components extending beyond 12 months. These challenges are compounded by geopolitical tensions affecting rare earth material supplies and export controls on specialized manufacturing equipment. While the situation has improved from pandemic-era shortages, inventory levels remain below historical averages, forcing many CPE manufacturers to implement allocation strategies and redesign products with available components.

Rising Component Costs Squeeze Profit Margins

Escalating production expenses present another significant restraint for CPE chip suppliers. The transition to more advanced process nodes has increased wafer costs by approximately 20-30% across the industry. Additionally, testing and packaging expenses have risen due to higher energy prices and labor costs. These factors have compressed gross margins, particularly for mid-range CPE chips where pricing pressure is most intense. Manufacturers are responding by optimizing chip architectures, consolidating IP blocks, and investing in yield improvement initiatives, but these measures require significant R&D expenditures that may take years to yield returns.

Regulatory Complexity Slows Time-to-Market

The CPE chip industry faces growing regulatory scrutiny that delays product launches and increases compliance costs. New spectrum regulations, cybersecurity requirements, and equipment certification processes have extended development cycles by 3-6 months on average. In particular, the automotive and industrial sectors now demand comprehensive safety certifications that require extensive testing and documentation. These regulatory hurdles disproportionately affect smaller chip vendors who lack dedicated compliance teams, potentially limiting innovation and competition in certain market segments.

MARKET CHALLENGES

Technology Complexity Increases Design and Validation Costs

Modern CPE chips incorporate increasingly sophisticated architectures that pose significant engineering challenges. Designs now routinely integrate multiple processor cores, AI accelerators, and specialized radio interfaces, requiring advanced simulation tools and verification methodologies. The associated R&D costs have grown exponentially, with some 5G chip development projects now exceeding $100 million in budget. This creates a high barrier to entry for potential competitors and forces established players to carefully prioritize their product roadmaps. Furthermore, the complexity makes post-silicon validation more difficult, potentially leading to costly respins if critical issues emerge late in the development cycle.

Talent Shortage Constrains Innovation Capacity

The semiconductor industry’s rapid expansion has created intense competition for skilled engineers, particularly in critical areas like RF design, digital signal processing, and physical implementation. CPE chip manufacturers report vacancy rates exceeding 30% for certain technical positions, with hiring cycles stretching to 9-12 months for specialized roles. This talent crunch limits companies’ ability to execute aggressive product roadmaps and forces difficult tradeoffs between projects. While firms are investing in training programs and academic partnerships, the pipeline for experienced chip designers remains insufficient to meet current demand.

Standardization Gaps Create Integration Headaches

The evolving nature of 5G and edge computing technologies has led to fragmented standards across different markets and regions. CPE chip vendors must support multiple protocol variants, frequency bands, and security frameworks, complicating both hardware and software development. This fragmentation increases testing overhead and makes it difficult to achieve economies of scale across product lines. While industry groups continue working toward greater harmonization, interim solutions often require additional engineering resources to implement customized features for specific customers or geographies.

CPE CHIP MARKET TRENDS

5G Network Expansion Accelerates Demand for Advanced CPE Chips

The rapid global deployment of 5G networks is significantly driving the CPE (Customer Premises Equipment) chip market, with the segment projected to grow at over 30% CAGR through 2032. Telecom operators worldwide invested nearly $280 billion in 5G infrastructure in 2023 alone, creating substantial demand for compatible CPE devices. Chip manufacturers are responding with innovative solutions featuring multi-band support and improved power efficiency, with next-generation modem-RF combos now achieving throughputs exceeding 7Gbps. While 4G CPE chips still dominate current installations, representing about 65% of 2024 shipments, 5G solutions are rapidly gaining share due to superior performance in high-density urban environments.

Other Trends

Smart Home Integration

The proliferation of IoT devices in residential settings, expected to reach 29 billion connected units globally by 2027, is creating new requirements for CPE chips that can handle simultaneous broadband and IoT traffic management. Modern gateway solutions now incorporate AI-powered traffic prioritization and mesh networking capabilities to maintain quality of service across dozens of connected devices. Semiconductor vendors have responded with system-on-chip (SoC) designs integrating Wi-Fi 6/6E, Bluetooth, and Zigbee radios alongside traditional cellular modems. North America leads this adoption curve, with over 75% of new home internet subscriptions in 2023 opting for smart gateway solutions compared to just 32% in 2020.

Edge Computing and Network Virtualization Impact Chip Designs

Emerging virtualization technologies are reshaping CPE architectures, creating demand for chips with enhanced processing capabilities beyond traditional modem functions. Virtual CPE (vCPE) solutions now account for 18% of business installations, requiring chipsets that can efficiently run containerized network functions (CNFs) while maintaining low power envelopes. The enterprise segment has proven particularly receptive, with large-scale adoption in multi-tenant office buildings and smart city applications. Meanwhile, silicon designed for edge computing applications is increasingly incorporating hardware acceleration blocks for AI inference, allowing real-time processing of video analytics and other bandwidth-intensive applications at the network periphery. This evolution has prompted traditional chip vendors to expand their portfolios through strategic acquisitions in the FPGA and specialty processor spaces.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Partnerships Fuel Growth in the CPE Chip Market

The global CPE (Customer Premises Equipment) chip market remains highly competitive, characterized by technological innovation and aggressive expansion strategies. Qualcomm dominates the market with its extensive portfolio of 4G and 5G chipsets, capturing approximately 35% revenue share in 2024. The company’s leadership stems from its strong foothold in North America and strategic partnerships with telecom operators.

MediaTek and Intel follow closely, collectively accounting for 28% market share, owing to their cost-effective solutions for emerging markets and industrial applications. These players continue investing heavily in R&D, particularly for energy-efficient 5G chips catering to IoT deployments and smart city infrastructure.

Chinese manufacturers like Hisilicon and UNISOC are rapidly gaining traction through government-supported initiatives and localized supply chains. Their aggressive pricing strategies and custom solutions for Asian markets have enabled 18% year-over-year growth in 2024, challenging established western players.

Meanwhile, specialized firms such as Eigencomm and Sequans are carving niche positions through innovative chip architectures optimized for low-power wide-area networks (LPWAN) and private 5G deployments. Their collaborations with network equipment providers have become crucial differentiators in this evolving landscape.

List of Key CPE Chip Manufacturers Profiled

Qualcomm Technologies, Inc. (U.S.)

UNISOC (Shanghai) Technologies Co., Ltd. (China)

ASR Microelectronics Co., Ltd. (China)

HiSilicon (Huawei Technologies Co., Ltd.) (China)

XINYI Semiconductor (China)

MediaTek Inc. (Taiwan)

Intel Corporation (U.S.)

Eigencomm (China)

Sequans Communications S.A. (France)

Segment Analysis:

By Type

5G Chip Segment Dominates the Market Due to its High-Speed Connectivity and Low Latency

The CPE Chip market is segmented based on type into:

4G Chip

5G Chip

By Application

5G CPE Segment Leads Due to Escalated Demand for High-Performance Wireless Broadband

The market is segmented based on application into:

4G CPE

5G CPE

By End User

Telecom Operators Segment Dominates with Growing Infrastructure Investments

The market is segmented based on end user into:

Telecom Operators

Enterprises

Residential Users

Regional Analysis: CPE Chip Market

North America The mature telecommunications infrastructure and rapid 5G deployments in the U.S. and Canada are fueling demand for high-performance 5G CPE chips, particularly from vendors like Qualcomm and Intel. With major carriers investing over $275 billion in network upgrades, chip manufacturers are prioritizing low-latency, power-efficient designs. However, stringent regulatory scrutiny on semiconductor imports creates supply chain challenges. The region also leads in IoT adoption, driving demand for hybrid 4G/5G chips in smart city solutions and enterprise applications. Local chip designers benefit from strong R&D ecosystems but face growing competition from Asian suppliers.

Europe EU initiatives like the 2030 Digital Compass (targeting gigabit connectivity for all households) are accelerating CPE chip demand, though adoption varies across nations. Germany and the U.K. lead in 5G CPE deployments using chips from MediaTek and Sequans, while Eastern Europe still relies heavily on cost-effective 4G solutions. Strict data privacy laws and emphasis on open RAN architectures are reshaping chip design requirements. The region faces headwinds from component shortages but maintains steady growth through government-industry partnerships in semiconductor sovereignty programs.

Asia-Pacific Accounting for over 60% of global CPE chip consumption, the region is driven by China’s massive “5G+” infrastructure push and India’s expanding broadband networks. Local giants HiSilicon and UNISOC dominate low-to-mid range segments, while South Korean/Japanese firms focus on premium chips. Southeast Asian markets show explosive growth (20%+ CAGR) due to rural connectivity projects. However, geopolitical tensions and import restrictions create supply volatility. Price sensitivity remains high, favoring integrated 4G/5G combo chips over standalone 5G solutions in emerging economies.

South America Limited 5G spectrum availability keeps the market reliant on 4G LTE chips, though Brazil and Chile are early adopters of 5G CPEs using ASR and MediaTek solutions. Economic instability and currency fluctuations hinder large-scale infrastructure investments, causing operators to prioritize cost-effective Chinese chip suppliers. The lack of local semiconductor manufacturing creates import dependency, but recent trade agreements aim to improve component accessibility. Enterprise demand for industrial IoT routers presents niche opportunities for mid-tier chip vendors.

Middle East & Africa Gulf nations (UAE, Saudi Arabia) drive premium 5G CPE adoption through smart city projects, leveraging Qualcomm and Eigencomm chips. Sub-Saharan Africa depends on affordable 4G solutions from Chinese vendors, with mobile network operators deploying low-power chips for extended coverage. While underdeveloped fiber backhaul limits 5G potential, satellite-CPE hybrid chips are gaining traction in remote areas. Political instability in some markets disrupts supply chains, though rising digitalization funds (like Saudi’s $6.4bn ICT strategy) indicate long-term growth potential.

Report Scope

This market research report provides a comprehensive analysis of the global and regional CPE Chip markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global CPE Chip market was valued at USD million in 2024 and is projected to reach USD million by 2032.

Segmentation Analysis: Detailed breakdown by product type (4G Chip, 5G Chip), application (4G CPE, 5G CPE), and end-user industry to identify high-growth segments and investment opportunities.

Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific currently dominates the market due to rapid 5G adoption.

Competitive Landscape: Profiles of leading market participants including Qualcomm, UNISOC, ASR, Hisilicon, and MediaTek, including their product offerings, R&D focus, and recent developments.

Technology Trends & Innovation: Assessment of emerging technologies in semiconductor design, fabrication techniques, and evolving industry standards for CPE devices.

Market Drivers & Restraints: Evaluation of factors driving market growth such as 5G rollout and IoT expansion, along with challenges including supply chain constraints and regulatory issues.

Stakeholder Analysis: Insights for chip manufacturers, network equipment providers, telecom operators, investors, and policymakers regarding the evolving ecosystem.

Related Reports:https://semiconductorblogs21.blogspot.com/2025/06/fieldbus-distributors-market-size-and.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/consumer-electronics-printed-circuit.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/metal-alloy-current-sensing-resistor.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/modular-hall-effect-sensors-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/integrated-optic-chip-for-gyroscope.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/industrial-pulsed-fiber-laser-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/unipolar-transistor-market-strategic.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/zener-barrier-market-industry-growth.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/led-shunt-surge-protection-device.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/type-tested-assembly-tta-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/traffic-automatic-identification.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/one-time-fuse-market-how-industry.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/pbga-substrate-market-size-share-and.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/nfc-tag-chip-market-growth-potential-of.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/silver-nanosheets-market-objectives-and.html

0 notes

Text

Top Platforms Enterprises Are Switching to in 2025

A Strategic Look at What’s Powering the Next Wave of Digital Transformation

According to our further move into 2025, the enterprise technology sphere is massively changing. Companies do not expect to be content anymore with the legacy platforms that provide inflexible silo solutions. They are instead going to the latest, cloud-native, artificial intelligence-enriched platforms that drive agility, scale, and customer-centric innovation.

We at Alt Digital Technologies are partnering with progressive businesses that are transitioning through this transformation. In our experience in the industry, these are the best platforms to which organizations are currently migrating in 2025, and the reason why these platforms are taking the lead.

1. commercetools – The Rise of Composable Commerce

With monolithic eCommerce systems starting to display their weakness, companies are turning toward commercetools, due to its headless/ API-first features. It provides the opportunity to create unique storefronts, connect new services fast, and provide their customers with omnichannel experiences.

Why enterprises are switching:

True composability for rapid experimentation

Seamless integration with CMS, ERP, CRM

Ideal for global commerce scalability

Alt Digital Insight: As a team of commercetools experts, we are supporting brands in starting to move beyond out-of-the-box eCommerce designs to more tail objet-oriented, top-performing digital shops.

2. Salesforce Industries (Vlocity) – Personalized Engagement at Scale

Salesforce still defines the CRM sector, but it is its industry cloud products (such as Vlocity) that are attracting the attention of big enterprises in 2025. Whether in financial services or telecom, they provide domain capabilities that are deeply coupled with the power of Salesforce data and AI.

Why it’s trending:

Industry-tailored data models and workflows

Built-in AI for guided selling and service

Faster time-to-market for CX innovations

Alt Digital Insight: Our area of expertise is to tailor Salesforce Industries so that businesses can get the most out of automation, compliance, and personalization of customers.

3. Adobe Experience Platform (AEP) – The Experience Data Powerhouse

Adobe Experience Platform is gaining some popularity as the customer data serve as the foundation of the marketing and CX strategies. AEP is a point where data of various sources can be centralized, subject to real-time intelligence, and drives continuous customer smooth, personalization.

Why it’s rising:

Unified customer profiles with real-time updates

Integration with Adobe Campaign, Target, and AEM

Scalable AI-driven personalization

Alt Digital Insight: We are an Adobe Experience Cloud partner. This is why we assist brands in unleashing the full power of AEP transforming disjointed data into linked experiences.

4. SAP S/4HANA Cloud – The New Core of Digital ERP

The ease of doing business, its intelligent automation, and real-time analytics are fast decommissioning legacy ERP systems in favor of SAP S/4HANA Cloud. Later in 2025, S/4HANA is being migrated by many large enterprises in their digital core transformation.

Why it matters:

Real-time data for faster decisions

Embedded AI for predictive insights

Seamless integration with supply chain, finance, HR

Alt Digital Insight: We also use custom workflows to support the needs of larger enterprises, and our ERP experts can make the migrating to S/4HANA effortless.

5. ServiceNow – Reimagining Digital Workflows

Companies are putting on ServiceNow to automate and streamline the mundane workflows inside and outside. ServiceNow has end-to-end visibility and efficiency, supplemented by a strong low-code platform, in all aspects of IT operations, customer service and beyond.

Why it’s winning:

Unified platform for ITSM, HR, and CX operations

AI-powered automation and workflow orchestration

Scalable for global enterprise needs

Alt Digital Insight: We also enable clients to digitize their operations and diminish friction in business processes with the help of modular capabilities of ServiceNow.

6. Microsoft Power Platform – Low-Code Revolution in Action

As digital agility has become a central enterprise objective, Microsoft Power Platform (Power BI, Power Apps, Power Automate, and Power Virtual Agents) is allowing citizen development in ways it has never been done before.

Why it’s popular:

Democratizes app development across teams

Strong integration with Microsoft 365 and Azure

Speeds up automation and data visualization efforts

Alt Digital Insight: We help organizations develop enterprise level apps and workflows to help them move faster with making decisions and to make them less manual.

7. Kubernetes & Cloud-Native Ecosystems (AWS, Azure, GCP)

Digital transformation is based on cloud-native infrastructure. Businesses are adopting Kubernetes and AWS, Azure, and Google cloud services to construct scalable, resilient, and modern applications architecture.

Why it’s foundational:

Enables microservices, containerization, and CI/CD

Greater scalability, cost-efficiency, and uptime

Supports innovation velocity with DevOps best practices

Alt Digital Insight: Our cloud engineering and DevOps professionals assist companies to modernize existing systems and enable businesses to run scalable and safe solutions.

Final Thoughts: The Shift Is Strategic, Not Just Technological

Not only do all these platforms possess superior technology, but they also have something in common, which is business agility, data intelligence, and user-centered design. They are not only implementing tools, but they are creating digital ecosystems that can change with their customers and markets.

We not only implement things at Alt Digital Technologies, but we are partners in transformation. Whatever the force to change the platform to the headless commerce model, unleash the potential of AI in CRM, or re-architect your data layer, our expertise is comprehensive to ensure your platform shift turns out to be a success.

0 notes

Text

2025 Trends in Telecom BPO Every SME Should Watch

In the dynamic world of telecommunications, 2025 marks a turning point for small and medium-sized enterprises (SMEs) that rely on Business Process Outsourcing (BPO). With advancements in AI, automation, and omnichannel strategies, Telecom BPO services have evolved from cost-saving tools into strategic growth enablers.

At Sphere Global Solutions, we help SMEs across the globe harness the latest in telecom BPO innovation—streamlining operations, reducing churn, and improving customer satisfaction.

In this article, we explore the top Telecom BPO trends in 2025 that every SME should pay attention to, backed by insights and action points.

1. Rise of Hyper-Automation in Customer Support

What’s Changing: In 2025, hyper-automation is no longer optional. Telecom BPOs are automating repetitive tasks using a blend of robotic process automation (RPA), AI, and machine learning.

Why It Matters for SMEs:

Reduces dependency on large customer support teams

Increases resolution speed and customer satisfaction

Cuts costs by up to 40% on repetitive call center operations

Example: Automating SIM activation, billing queries, or service upgrades through AI chatbots.

Learn how our Telecommunications BPO services use hyper-automation to scale your SME support operations.

2. Omnichannel Engagement Becomes the Norm

What’s Changing: Customers expect seamless communication across channels—voice, email, chat, WhatsApp, and social media.

Why It Matters for SMEs:

Creates a unified customer experience

Increases first-contact resolution

Boosts customer loyalty

Real-World Impact: Companies using omnichannel support see up to 91% higher year-over-year customer retention (Aberdeen Research).

Discover how Sphere Global’s BPO Solutions can help you deliver consistent omnichannel support tailored for telecom SMEs.

3. Conversational AI Takes Over Tier-1 Support

What’s Changing: AI-driven voice assistants and smart chatbots are now handling over 70% of first-level customer queries in telecom.

Why It Matters for SMEs:

Reduces agent workload

Delivers 24/7 customer support

Handles high call volumes without hiring more agents

Next Step: Use AI to prequalify leads, route queries to the right team, and gather feedback in real-time.

4. Globalization of Telecom Support Operations

What’s Changing: Geographical boundaries are fading as BPOs provide multilingual, round-the-clock support globally.

Why It Matters for SMEs:

Allows expansion into new markets

Supports international customers cost-effectively

Enables faster SLA adherence with distributed teams

Tip: Choose a BPO partner like Sphere Global Solutions that provides consulting and localization strategies for global telecom operations.

5. Data-Driven Decision Making Using Predictive Analytics

What’s Changing: BPO providers are using AI-powered analytics to forecast churn, identify upsell opportunities, and optimize workflows.

Why It Matters for SMEs:

Retain more customers through proactive support

Track and reduce dropped calls and escalations

Optimize staffing and support hours using trends

Stats: Predictive support models can reduce churn by up to 25%, according to McKinsey.

6. Telecom-Specific PMaaS (Project Management as a Service)

What’s Changing: More BPOs are offering PMaaS models tailored for telecom SMEs needing tech migrations, CRM integration, or system upgrades.

Why It Matters for SMEs:

Avoid hiring expensive in-house project managers

Get access to telecom project specialists on demand

Speed up digital transformation with expert guidance

Learn more about our Consulting Services for telecom SMEs seeking efficient project delivery.

7. Enhanced Cybersecurity in BPO Operations

What’s Changing: Telecom BPOs now prioritize end-to-end encryption, multi-layered access controls, and compliance with GDPR, ISO 27001, and HIPAA.

Why It Matters for SMEs:

Protects sensitive customer data

Ensures regulatory compliance

Builds brand trust and transparency

Tip: Ask your BPO partner for regular security audits and secure cloud infrastructure.

8. Knowledge-Centered Service (KCS) for Agent Enablement

What’s Changing: KCS systems allow telecom agents to access and update a central knowledge base in real-time, improving accuracy and speed.

Why It Matters for SMEs:

Reduces training costs

Improves first-call resolution

Builds long-term process intelligence

Best Practice: Use AI to automatically update your KCS with frequently asked questions, solutions, and SOPs.

9. Feedback-Driven Optimization

What’s Changing: AI tools are analyzing voice calls and customer messages to identify sentiment, satisfaction, and feedback trends.

Why It Matters for SMEs:

Catch customer dissatisfaction early

Personalize follow-ups and offers

Improve agent behavior through analytics

Stat: Companies using voice sentiment analysis improve CX scores by up to 18%.

10. Sustainable BPO Practices

What’s Changing: Eco-conscious telecom BPOs are embracing paperless workflows, green infrastructure, and remote teams to reduce carbon footprint.

Why It Matters for SMEs:

Aligns with ESG goals

Improves brand image with sustainability-conscious consumers

Reduces utility and infrastructure costs

Partner with a BPO provider like Sphere Global Solutions that supports your sustainability goals with energy-efficient telecom processes.

🧭 What Should SMEs Do Now?

To stay competitive in the telecom space, SMEs must move from reactive to proactive support models. Partnering with the right BPO and consulting provider helps you achieve:

Scalability without increasing costs

AI-powered support with human oversight

Real-time data to drive business decisions

Future-proof operations through agile practices

Final Thoughts

The telecom BPO landscape is transforming fast—and SMEs that adopt these 2025 trends early will lead their market segments. At Sphere Global Solutions, we help telecom businesses like yours make that shift with confidence.

Whether you need an AI-enabled BPO team, smart automation, or consulting support—we’re here to drive measurable business impact.

FAQs: 2025 Telecom BPO Trends for SMEs

1. What is the biggest telecom BPO trend in 2025?

The integration of hyper-automation and conversational AI is revolutionizing customer support and operational efficiency.

2. How can SMEs benefit from telecom BPO?

SMEs benefit by reducing overhead, improving customer retention, gaining access to advanced technologies, and scaling faster.

3. Is BPO only for large telecom companies?

No, modern BPO services are now highly customizable and scalable—ideal for SMEs with lean teams.

4. Can Sphere Global handle international telecom BPO?

Yes. We offer multilingual, 24/7 support with global reach and localized expertise.

5. How do I get started?

Contact Sphere Global Solutions for a free discovery session to assess your telecom BPO needs.

0 notes

Text

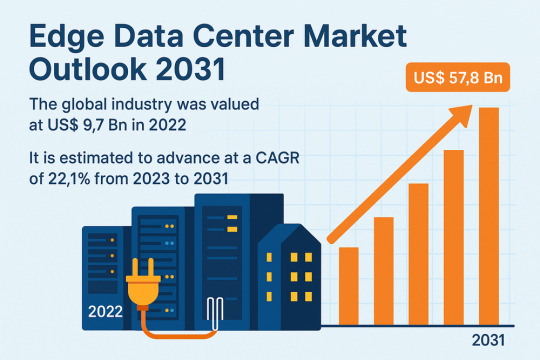

Edge Computing Demand Accelerates Market Growth at 22.1% CAGR

The global Edge Data Center Market was valued at USD 9.7 Bn in 2022 and is projected to reach USD 57.8 Bn by the end of 2031, expanding at an impressive CAGR of 22.1% from 2023 to 2031. This rapid growth is fueled by the increasing demand for real-time data processing, the rise of streaming services, growth in IoT and AI-driven technologies, and the adoption of autonomous vehicles.

Market Overview: Edge data centers are smaller, decentralized data facilities located close to the end-users and connected devices. These centers reduce latency, improve bandwidth efficiency, and enable faster data processing by bringing computation and storage closer to the data source.

Edge computing is being adopted across a variety of sectors, including healthcare, manufacturing, automotive, and telecom, as organizations seek to leverage real-time analytics and improve user experience. With 5G networks and AI-based solutions gaining traction globally, the need for edge infrastructure is growing significantly.

Market Drivers & Trends

One of the primary market drivers is the surge in demand for video streaming services. Platforms such as Netflix, YouTube, and Disney+ are increasingly dependent on edge data centers to deliver content with minimal latency and buffering. For instance, Netflix uses edge infrastructure to reduce content delivery costs and ensure a seamless user experience.

Additionally, the rapid adoption of IoT devices and AI technologies has heightened the need for low-latency data processing. Applications like autonomous vehicles, smart cities, industrial automation, and digital healthcare depend on instantaneous data collection and response, which edge data centers facilitate.

The expansion of 5G networks further accelerates edge data center deployment. As bandwidth and connection speeds increase, so does the demand for faster and more reliable data delivery.

Latest Market Trends

Increased deployment in rural and semi-urban areas: Edge data centers are being built in remote areas to bridge the digital divide. For example, RailTel Corp. is constructing 102 edge data centers across rural and semi-urban India to support digital services with minimal latency.

Integration of edge with AI and ML: Enterprises are leveraging edge computing to run machine learning models directly at the source of data. This results in faster decision-making and enhances operational efficiency.

Sustainable data centers: Growing environmental concerns are pushing companies to build eco-friendly edge data centers powered by renewable energy and equipped with energy-efficient cooling systems.

Key Players and Industry Leaders

Some of the leading players in the global edge data center market include:

365 Data Centers

Eaton Corporation plc

EdgeConneX Inc.

Vertiv Group Corp.

Reichle & De-Massari (R&M)

Dätwyler IT Infra GmbH

L&T Smart World

Siemon

Rittal GmbH & Co. KG

H5 Data Centers

NEXTDC LTD.

These companies are investing heavily in R&D and strategic collaborations to expand their edge capabilities, enhance service offerings, and cater to new markets.

Recent Developments

November 2022: 365 Data Centers acquired Sungard Availability Services’ U.S. colocation and network operations, expanding its footprint in high-growth edge markets.

April 2022: EdgeConneX acquired Indonesia’s GTN to develop a 90MW data center in Jakarta, highlighting the growing edge data center demand in Southeast Asia.

January 2022: RailTel Corp. announced its plan to build 102 edge data centers across India to promote digital transformation in underdeveloped regions.

Market Opportunities

The proliferation of autonomous vehicles opens new frontiers for edge data centers. An autonomous car can generate up to 5 TB of data per hour, necessitating real-time processing capabilities only edge facilities can offer. According to MIT (2022), over 30 million autonomous vehicles are already on the roads globally, a number that will increase exponentially.

Similarly, the growth of eSports and gaming platforms, which require ultra-low latency, will boost the demand for local data processing units. Industrial automation and smart manufacturing further contribute to the rising demand for edge data infrastructure.

Preview essential insights and takeaways from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=79151

Future Outlook

With businesses and governments increasing their focus on digital transformation, the edge data center market is expected to witness widespread adoption across industries. The combination of 5G, AI, IoT, and cloud computing is expected to shape the future of decentralized data management.

Companies are likely to prioritize edge data centers to ensure compliance with data localization regulations, optimize service delivery, and maintain high-security standards.

By 2031, the edge data center industry will play a crucial role in reshaping the global data processing ecosystem, especially as the number of connected devices continues to rise.

Market Segmentation

By Component:

Solutions

Services

Designing & Consulting

Implementation & Integration

Support & Maintenance

By Enterprise Size:

SMEs

Large Enterprises

By Industry:

BFSI

IT & Telecom

Healthcare

Manufacturing

Automotive

Others

By Region:

North America

Europe

Asia Pacific

Middle East & Africa

South America

Regional Insights

North America currently dominates the global edge data center market, led by the U.S., which boasts high internet penetration, advanced telecom infrastructure, and robust digital consumption.

Asia Pacific is projected to register the fastest CAGR through 2031, driven by increasing 5G deployment, digital business expansion, and the presence of major tech hubs in countries like China, India, and Japan.

Europe follows closely with significant investments in edge technologies to support the growing demand for smart cities and Industry 4.0 initiatives.

Why Buy This Report?

Gain insights into a market poised to grow at a CAGR of 22.1%

Understand emerging trends, technological advancements, and opportunities

Analyze competitive landscape with detailed company profiles

Evaluate the impact of regional growth trends on market performance

Identify potential investment areas and target customer segments

This comprehensive analysis helps stakeholders make informed strategic decisions based on in-depth market intelligence.

Frequently Asked Questions (FAQs)

1. What is the current size of the global edge data center market? The market was valued at US$ 9.7 Bn in 2022.

2. What is the projected market size by 2031? The edge data center market is expected to reach US$ 57.8 Bn by 2031.

3. What is the CAGR for the forecast period 2023–2031? The market is anticipated to grow at a CAGR of 22.1%.

4. Which region leads the global edge data center market? North America dominates the market due to its mature technology landscape and early adoption of edge computing.

5. What are the key factors driving market growth? Rising demand for low-latency data processing, streaming services, 5G expansion, IoT device proliferation, and AI-based applications.

6. Who are the key players in the market? Major players include 365 Data Centers, EdgeConneX, Eaton, Vertiv, H5 Data Centers, and NEXTDC LTD.

Explore Latest Research Reports by Transparency Market Research: 3D Modeling, 3D Visualization, and 3D Data Capture Market: https://www.transparencymarketresearch.com/3d-modeling-3d-visualization-and-3d-data-capture-market.html

IT Asset Disposition (ITAD) Market: https://www.transparencymarketresearch.com/it-asset-disposition-market.html

Identity-as-a-Service (IDaaS) Market: https://www.transparencymarketresearch.com/identity-as-a-service-market.html

Point-of-Sale [POS] Terminal Market: https://www.transparencymarketresearch.com/point-of-sale-terminals-market.html

About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

Low Voltage Cable Market Emerging Trends Reshaping Global Power Distribution

The global low voltage cable market is undergoing transformative changes driven by technological advancements, the rise in renewable energy adoption, smart grid development, and growing investments in urban infrastructure. Low voltage cables, typically rated below 1,000 volts, are essential for power distribution across residential, commercial, and industrial applications. These cables are experiencing growing demand as energy systems become more decentralized, efficient, and digitally connected.

Surge in Smart Grid Deployments

One of the most significant emerging trends in the low voltage cable market is the widespread implementation of smart grids. These intelligent networks require advanced cabling solutions capable of supporting automated monitoring, real-time data transmission, and efficient load management. Low voltage cables that integrate fiber optics and data transmission capabilities are increasingly favored. Smart grids not only improve reliability but also enable predictive maintenance and better integration of distributed energy resources (DERs), such as rooftop solar systems and electric vehicles.

Rise in Renewable Energy Integration