#Tissue Diagnostics Market

Text

Future and Growth of Tissue Diagnostics Market by 2030

Tissue Diagnostics Market

The global tissue diagnostics market size was estimated at USD 5.19 billion in 2022 and is expected to grow at a compound annual growth rate (CAGR) of 7.15% from 2023 to 2030.

Tissue diagnostics remains a gold standard for cancer diagnosis as these technologies capture the anatomy of tumors. With rising incidences of cancer, the tissue diagnostics industry witnesses high demand with significant growth opportunities over the forecast period. The impact of COVID-19 on the tissue diagnostics industry has been significant. During the pandemic, there was a slowdown in routine medical procedures, including diagnostic testing, as healthcare resources were redirected toward managing the virus.

Gather more insights about the market drivers, restrains and growth of the Tissue Diagnostics Market

The pandemic led to a temporary decline in the demand for tissue diagnostics products and services. However, as the situation improved and healthcare systems adapted to the new normal, the market began to recover. The need for accurate diagnosis and monitoring of various diseases, including cancer, remained high, driving the demand for tissue diagnostics in the post-pandemic period.

Cancer incidences are increasing dramatically, which has caused a paradigm change in anatomic pathology. This, in turn, is contributing to the clinical pathology field's continued growth. Digitalization of diagnosis methods, increased use of liquid biopsy for cancer detection, and a continuous convergence of anatomical and molecular pathology. The importance of integrated bioinformatics and analyses increases as computational pathology gains momentum. Over the past two decades, the tissue diagnostics industry has changed as more advanced equipment has become available, making life easier for pathologists and physicians.

For instance, in May 2021, to increase the availability of precision medication for lung cancer, QIAGEN released its first FDA-approved tissue companion diagnostic to detect the KRAS G12C mutation in NSCLC tumors. The Rotor-Gene Q MDx instrument, a part of the modular QIAsymphony family of automation solutions, is used with the real-time qualitative PCR kit. This tool builds on QIAGEN's nine years of experience in researching and marketing KRAS CDx tests.

Globally, more than 14 million individuals are diagnosed with cancer each year, and by 2030, that figure is projected to increase to more than 21 million. Major market participants are introducing new cancer diagnosis products. For instance, Roche introduced its innovative BenchMark ULTRA PLUS system for cancer diagnostics in June 2022, enabling prompt, precise patient care. Pathologists can deliver high-quality, time-sensitive results to doctors and patients due to the BenchMark ULTRA PLUS tissue staining system's improved workflow, testing efficiency, and environmentally sustainable features.

Considering the rising worldwide cancer burden, various technologies, and improvements in tissue diagnostics (TDx) will increase pathology efficiency, which is essential for better cancer therapy and diagnosis. For example, Ibex Medical Analytics, the industry pioneer in AI-powered cancer diagnoses, and Alverno Laboratories announced a new deal in March 2023. It aims to expand the implementation of Ibex's Galen suite of Artificial Intelligence solutions to the entire Alverno network across Indiana and Illinois. The deployment comprises AI-powered solutions for cancer diagnosis across numerous tissue types and will help Alverno pathologists in providing the highest quality care for their patients.

A rise in the adoption rate of automated tissue-based diagnostic systems by research institutes enables them to diagnose tumors faster. In January 2023, MilliporeSigma announced its plans to expand its portfolio of antibodies for tissue diagnostics to help improve the classification of gliomas and other tumors in the nervous systems. Such R&D investments will ensure the market continues to grow.

Browse through Grand View Research's Clinical Diagnostics Industry Research Reports.

The global hematologic malignancies market size was valued at USD 67.23 billion in 2023 and is projected to grow at a CAGR of 8.0% from 2024 to 2030.

The global precision diagnostics market size was estimated at USD 15.60 billion in 2023 and is projected to grow at a CAGR of 18.4% from 2024 to 2030.

Key Companies & Market Share Insights

The tissue diagnostics market is fragmented due to the presence of several medium-to-small and large participants in the marketspace. The advent of novel diagnostic models by key players to enhance their technology portfolio has raised competitiveness in the market. For instance, in June 2022, Roche announced the launch of VENTANA DP 600 - the next-generation slide scanner. This high-capacity slide scanner provides the pathology lab with workflow flexibility and ease of use while producing stained histology slides with exceptional image quality from tissue samples. Some prominent players in the global tissue diagnostics market include:

F. Hoffmann-La Roche Ltd.

Abbott Laboratories

Thermo Fisher Scientific Inc.

Siemens

Danaher

bioMérieux SA

QIAGEN

BD

Merck KGaA

GE Healthcare

BioGenex

Cell Signaling Technology, Inc.

Bio SB

DiaGenic ASA

Agilent Technologies

Order a free sample PDF of the Tissue Diagnostics Market Intelligence Study, published by Grand View Research.

0 notes

Text

Tissue Diagnostics Market Business Growth, Opportunities and Forecast, 2030

The global tissue diagnostics market size was estimated at USD 5.19 billion in 2022 and is expected to grow at a compound annual growth rate (CAGR) of 7.15% from 2023 to 2030.

Tissue diagnostics remains a gold standard for cancer diagnosis as these technologies capture the anatomy of tumors. With rising incidences of cancer, the tissue diagnostics industry witnesses high demand with significant growth opportunities over the forecast period. The impact of COVID-19 on the tissue diagnostics industry has been significant. During the pandemic, there was a slowdown in routine medical procedures, including diagnostic testing, as healthcare resources were redirected toward managing the virus.

Gather more insights about the market drivers, restrains and growth of the Tissue Diagnostics Market

The pandemic led to a temporary decline in the demand for tissue diagnostics products and services. However, as the situation improved and healthcare systems adapted to the new normal, the market began to recover. The need for accurate diagnosis and monitoring of various diseases, including cancer, remained high, driving the demand for tissue diagnostics in the post-pandemic period.

Cancer incidences are increasing dramatically, which has caused a paradigm change in anatomic pathology. This, in turn, is contributing to the clinical pathology field's continued growth. Digitalization of diagnosis methods, increased use of liquid biopsy for cancer detection, and a continuous convergence of anatomical and molecular pathology. The importance of integrated bioinformatics and analyses increases as computational pathology gains momentum. Over the past two decades, the tissue diagnostics industry has changed as more advanced equipment has become available, making life easier for pathologists and physicians.

For instance, in May 2021, to increase the availability of precision medication for lung cancer, QIAGEN released its first FDA-approved tissue companion diagnostic to detect the KRAS G12C mutation in NSCLC tumors. The Rotor-Gene Q MDx instrument, a part of the modular QIAsymphony family of automation solutions, is used with the real-time qualitative PCR kit. This tool builds on QIAGEN's nine years of experience in researching and marketing KRAS CDx tests.

Globally, more than 14 million individuals are diagnosed with cancer each year, and by 2030, that figure is projected to increase to more than 21 million. Major market participants are introducing new cancer diagnosis products. For instance, Roche introduced its innovative BenchMark ULTRA PLUS system for cancer diagnostics in June 2022, enabling prompt, precise patient care. Pathologists can deliver high-quality, time-sensitive results to doctors and patients due to the BenchMark ULTRA PLUS tissue staining system's improved workflow, testing efficiency, and environmentally sustainable features.

Considering the rising worldwide cancer burden, various technologies, and improvements in tissue diagnostics (TDx) will increase pathology efficiency, which is essential for better cancer therapy and diagnosis. For example, Ibex Medical Analytics, the industry pioneer in AI-powered cancer diagnoses, and Alverno Laboratories announced a new deal in March 2023. It aims to expand the implementation of Ibex's Galen suite of Artificial Intelligence solutions to the entire Alverno network across Indiana and Illinois. The deployment comprises AI-powered solutions for cancer diagnosis across numerous tissue types and will help Alverno pathologists in providing the highest quality care for their patients.

A rise in the adoption rate of automated tissue-based diagnostic systems by research institutes enables them to diagnose tumors faster. In January 2023, MilliporeSigma announced its plans to expand its portfolio of antibodies for tissue diagnostics to help improve the classification of gliomas and other tumors in the nervous systems. Such R&D investments will ensure the market continues to grow.

Tissue Diagnostic Market Segmentation

Grand View Research has segmented the global tissue diagnostics market report based on technology, application, end-use, and region:

Technology Outlook (Revenue, USD Million, 2018 - 2030)

• Immunohistochemistry

o Instruments

o Slide Staining Systems

o Tissue Microarrays

o Tissue Processing Systems

o Slide Scanners

o Other Products

o Consumables

o Antibodies

o Reagents

o Kits

• In Situ Hybridization

o Instruments

o Consumables

o Software

• Primary & Special Staining

• Digital Pathology and Workflow

o Whole Slide Imaging

o Image Analysis Informatics

o Information Management System Storage & Communication

• Anatomic Pathology

o Instruments

o Microtomes & Cryostat Microtomes

o Tissue Processors

o Automatic Strainers

o Other Products

o Consumables

o Reagents & Antibodies

o Probes & Kits

o Others

Application Outlook (Revenue, USD Million, 2018 - 2030)

• Breast Cancer

• Non-small Cell Lung Cancer

• Prostate Cancer

• Gastric Cancer

• Other Cancers

End-use Outlook (Revenue, USD Million, 2018 - 2030)

• Hospitals

• Research Laboratories

• Pharmaceutical Organizations

• Contract Research Organizations (CROs)

Regional Outlook (Revenue, USD Million, 2018 - 2030)

• North America

o U.S.

o Canada

• Europe

o UK

o Germany

o Spain

o France

o Italy

o Denmark

o Sweden

o Norway

• Asia Pacific

o Japan

o China

o India

o South Korea

o Singapore

o Australia

o Thailand

• Latin America

o Brazil

o Mexico

o Argentina

• Middle East and Africa (MEA)

o South Africa

o Saudi Arabia

o UAE

o Kuwait

Browse through Grand View Research's Clinical Diagnostics Industry Research Reports.

• The global hematologic malignancies market size was valued at USD 67.23 billion in 2023 and is projected to grow at a CAGR of 8.0% from 2024 to 2030.

• The global precision diagnostics market size was estimated at USD 15.60 billion in 2023 and is projected to grow at a CAGR of 18.4% from 2024 to 2030.

Key Companies & Market Share Insights

The tissue diagnostics market is fragmented due to the presence of several medium-to-small and large participants in the marketspace. The advent of novel diagnostic models by key players to enhance their technology portfolio has raised competitiveness in the market. For instance, in June 2022, Roche announced the launch of VENTANA DP 600 - the next-generation slide scanner. This high-capacity slide scanner provides the pathology lab with workflow flexibility and ease of use while producing stained histology slides with exceptional image quality from tissue samples. Some prominent players in the global tissue diagnostics market include:

• F. Hoffmann-La Roche Ltd.

• Abbott Laboratories

• Thermo Fisher Scientific Inc.

• Siemens

• Danaher

• bioMérieux SA

• QIAGEN

• BD

• Merck KGaA

• GE Healthcare

• BioGenex

• Cell Signaling Technology, Inc.

• Bio SB

• DiaGenic ASA

• Agilent Technologies

Order a free sample PDF of the Tissue Diagnostics Market Intelligence Study, published by Grand View Research.

#Tissue Diagnostics Market#Tissue Diagnostics Industry#Tissue Diagnostics Market size#Tissue Diagnostics Market share#Tissue Diagnostics Market analysis

0 notes

Text

#Tissue Diagnostics Market#Tissue Diagnostics Market Trends#Tissue Diagnostics Market Growth#Tissue Diagnostics Market Industry#Tissue Diagnostics Market Research#Tissue Diagnostics Market Report

0 notes

Link

According to the new market research report “Tissue Diagnostics Market by Product (Antibodies, Kits, Slide Staining System, Tissue Processing System), Technology(ISH, IHC, Special Staining), Disease(Breast Cancer, NSCLC, Lymphoma), End User (Hospitals, Research Laboratories) - Global Forecast to 2027”, published by MarketsandMarkets™, the Tissue Diagnostics Market is expected to reach USD 7.3 billion by 2027 from USD 5.3 billion in 2022, at a CAGR of 6.6% during the forecast period.

#marketsandmarkets research pvt. ltd.#tissue diagnostics market#tissue diagnostics market size#tissue diagnostics industry#tissue diagnostics

1 note

·

View note

Text

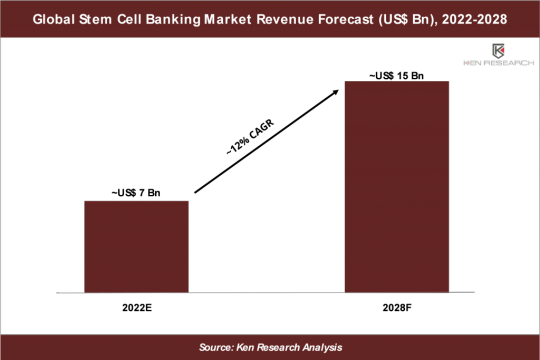

3 Key Insights on US$ 15 Bn Opportunity in the Global Stem Cell Banking Market - Ken Research

Driven By the increasing prevalence of infectious diseases and rising individuals’ awareness regarding the therapeutic potentials of stem cells, the Global Stem Cell Banking Market is forecasted to Cross US$ 15 Bn by 2028 says Ken Research Study.

Stem Cell Banking is the collection and cryogenic storage of stem cells from a newborn infant's umbilical cord blood and tissue which can be further used in cell treatments or clinical trials. It has the potential to treat a wide range of diseases, as well as the ability to mortgage stem cells from multiple family members and use an individual’s own stem cells (autologous transplant). Furthermore, individuals with spinal cord injuries, type 1 diabetes, Parkinson's disease, amyotrophic lateral sclerosis, Alzheimer's disease, heart disease, stroke, burns, cancer, and osteoarthritis may also benefit from stem cell therapies.

“Ken Research shares 3 key insights on this high opportunity market from its latest research study”

Stem Cell Banking Market Continues to Grow Owing to The Growing Newborn Population Worldwide.

The Global Stem Cell Banking Market is expected to witness stable growth during the forecast period, owing to the increasing newborn population, and rising individuals’ awareness regarding the therapeutic potentials of stem cells. The global stem cell banking market was valued at ~US$ 4 billion in 2017, it is estimated to be ~US$ 7 billion in 2022 and is expected to reach a market size of ~US$ 15 billion by 2028 growing with a CAGR of ~12%.

North America is the dominating region in the Global Stem Cell Banking Market due to the increasing incidence rates of diseases, such as cancer, neurological disorders, and diabetes. Furthermore, the growing government initiatives and investments in stem cell therapies are contributing to the region's growth in stem cell banking.

To learn more about this report Download A Free Sample Report

The Rising Prevalence of fatal Chronic Diseases, Such as Cancer, Cardiovascular Diseases, Neurological Disorders, Immunological Disorders, and Other Rare Metabolic Diseases is Propelling the Market Growth of Stem Cell Banking.

The growing geriatric population worldwide, who are more exposed to chronic and infectious diseases, including immunological disorders is propelling the stem cell banking market. In addition, the increasing prevalence of cancer, cardiovascular diseases, and autoimmune diseases, such as type 1 diabetes, and nephrological diseases is widening the use of stem cells as a potential treatment option.

For instance, according to Scientific American, an American science magazine that covers science, health, and social justice issues, several autoimmune diseases affected nearly 4.5% of the world's population in 2021.

According to the World Health Organization (WHO), a United Nations agency responsible for global public health, nearly 18 million people die every year as a result of cardiovascular diseases.

Visit This Link: - Request For Custom Report

High Operational Cost Associated with Stem Cell Banking, along with the stringent regulatory Frameworks May Impede the Market Growth of Stem Cell Banking.

Stem cell therapies have grown in popularity in recent years as individuals seek out alternative treatments for a variety of chronic diseases. Every day, new types of therapies are introduced, and individuals from all over the world are turning to them in place of traditional drug treatments and hospital visits. Despite the significant increase in demand for stem cell therapies, they remain prohibitively expensive to pursue. Simple joint injections cost close to US$ 5000, and more advanced treatments cost up to US$ 100,000, depending on the condition.

Furthermore, the stem cell field remains highly specialized and has yet to be adopted by citizens or insurance companies. Additionally, the field is further limited by older laws in some countries, most notably the United States. That means that there are relatively few sources for stem cells, and labs equipped to perform stem cells.

Request Free 30 Minutes Analyst Call

Key Topics Covered in the Report

Snapshot of the Global Stem Cell Banking Market

Industry Value Chain and Ecosystem Analysis

Market size and Segmentation of the Global Stem Cell Banking Market

Historic Growth of the Overall Global Stem Cell Banking Market and Segments

Competition Scenario of the Market and Key Developments of Competitors

Porter’s 5 Forces Analysis of the Global Stem Cell Banking Industry

Overview, Product Offerings, and Strengths & Weaknesses of Key Competitors

Covid-19 Impact on the Overall Global Stem Cell Banking Market

Future Market Forecast and Growth Rates of the Total Global Stem Cell Banking Market and by Segments

Market Size of Source, Service Type, Application, Cell Type Segments with Historical CAGR and Future Forecasts

Analysis of the Global Stem Cell Banking Market

Major Production/Supply and Consumption/Demand Hubs within Each Region

Major Country-wise Historic and Future Market Growth Rates of the Total Market and Segments

Overview of Notable Emerging Competitor Companies within Each Region

Notable Key Players Mentioned in the Report

CBR Systems, Inc.

Cryo-Cell International, Inc.

ViaCord

Sartorius AG

StemCyte, Inc.

Smart Cells International Limited

Global Cord Blood Corporation

Vita 34

LifeCell International Pvt. Ltd

Cordlife Group Limited

Notable Emerging Companies Mentioned in the Report

CyroHoldco

Generate Life Sciences Inc.

Hope Biosciences

Cell Care

ReeLabs Pvt. Ltd.

BrainStorm Cell Therapeutics, Inc.

CellSave a CSG-BIO Company, Inc.

Bristol-Myers Squibb Company

Key Target Audience – Organizations and Entities Who Can Benefit by Subscribing This Report

Stem Cell Banking Companies

Biopharmaceuticals Companies

Cord Blood Banks

Machinery and Equipment Suppliers for Stem Cell Banking

Cryogenic Healthcare Equipment Manufacturers

Biotechnology - Therapeutics and Diagnostics Companies

Pharmaceutical Companies

World Marrow Donor Association

Cord Blood Association

The International Stem Cell Banking Initiative (ISCBI) – PubMed

Healthcare Research Institutes

Healthcare Technology Research Institutes

Healthcare Technology Regulatory Authorities

Government Ministries and Departments of Healthcare

Period Captured in the Report

Historical Period: 2017-2021

Forecast Period: 2022E-2028F

For more insights on the market intelligence, refer to the link below: -

Global Stem Cell Banking Market

Related Reports By Ken Research: -

Global Stem Cell Banking Market Outlook to 2028

#Adipose Tissue-Derived Stem Cells Market#Africa Stem Cell Banking Market#Asia Pacific Stem Cell Banking Market#Biopharmaceuticals Companies#Biotechnology - Therapeutics and Diagnostics Companies#Bone Marrow-Derived Stem Cells Market#CBR Systems Stem Cell Banking Market#Challenges in Stem Cell Banking Industry#Cordlife Stem Cell Banking Market#Cryogenic Healthcare Equipment Manufacturers#Dental Pulp-Derived Stem Cells Market#Emerging Companies in Stem Cell Banking Market#Europe stem cell banking market#Global Players in Stem Cell Banking Market#Global Stem Cell Banking Application#Global Stem Cell Banking Industry#Global Stem Cell Banking Industry Outlook#Global Stem Cell Banking Market#Human Embryo-Derived Stem Cells Market#Key Competitors in Stem Cell Banking Market#Latin America Stem Cell Banking Market#Leading Players in Stem Cell Banking Industry#LifeCell Stem Cell Banking Market#Machinery and Equipment Suppliers for Stem Cell Banking#Major Companies in Stem Cell Banking Market#Middle East Stem Cell Banking Market#North America Stem Cell Banking Market#Opportunities in the Stem Cell Banking Market#Placental Stem Cells (PSCS) Banking Market#Sartorius Stem Cell Banking Market

0 notes

Text

HLA Typing for Transplant Market: Exploring the Rise in Demand for Organ Compatibility Testing

The HLA Typing for Transplant Market plays a crucial role in ensuring the success of organ and tissue transplants. As the healthcare sector increasingly recognizes the importance of human leukocyte antigen (HLA) typing in transplant compatibility, the market is projected to grow from USD 767 million in 2023 to approximately USD 1,138 million by 2030, reflecting a compound annual growth rate (CAGR) of 5.8% during this period. This growth is driven by advancements in diagnostic technologies, increasing transplant procedures, and a rising prevalence of chronic diseases.

Understanding HLA Typing

HLA typing is a medical test that identifies specific proteins on the surface of cells that are critical for the immune system's ability to recognize foreign substances. This is particularly important in the context of transplants, as compatibility between the donor and recipient can significantly reduce the risk of transplant rejection.

Access Full Report @ https://intentmarketresearch.com/latest-reports/hla-typing-for-transplant-market-3148.html

Key Drivers of the HLA Typing for Transplant Market

Increase in Transplant Procedures

As the number of organ transplants continues to rise due to factors such as aging populations and the prevalence of diseases like diabetes and heart disease, the demand for HLA typing services is also increasing. With more patients requiring transplants, accurate HLA matching becomes essential for improving outcomes.

Technological Advancements

Recent innovations in molecular biology and genetic testing technologies have made HLA typing more accurate, faster, and cost-effective. Techniques like next-generation sequencing (NGS) are revolutionizing the way HLA typing is performed, leading to more precise matching and reduced risks of rejection.

Rising Incidence of Chronic Diseases

The increasing prevalence of chronic conditions that may lead to the need for transplants—such as kidney disease, liver cirrhosis, and heart failure—also contributes to market growth. As more patients require transplants, the need for effective HLA typing becomes even more critical.

Challenges Facing the HLA Typing for Transplant Market

High Costs of HLA Typing Procedures

Despite advancements in technology, the costs associated with HLA typing can be a barrier for some healthcare facilities and patients. This can limit access to necessary testing, particularly in low-income areas or regions with limited healthcare resources.

Regulatory Hurdles

The HLA typing market is subject to stringent regulatory requirements that can vary by region. These regulations can complicate the development and distribution of new HLA typing technologies, potentially slowing market growth.

Shortage of Organ Donors

While the demand for transplants is growing, the availability of suitable organ donors has not kept pace. This mismatch can limit the overall impact of HLA typing in improving transplant outcomes.

Market Segmentation

By Product Type

Reagents and Consumables: Items required for conducting HLA typing tests, including kits and supplies.

Instruments: Equipment used for HLA typing, such as sequencers and analyzers.

Software: Platforms for managing and analyzing HLA typing data.

By Testing Method

Molecular Typing: Techniques involving DNA analysis for HLA typing.

Serological Typing: Traditional methods that analyze antibodies in the blood.

By End-User

Hospitals: Major facilities conducting HLA typing for transplant compatibility.

Diagnostic Laboratories: Specialized labs providing HLA typing services.

Research Institutions: Entities involved in HLA typing for studies and advancements in transplant medicine.

Download Sample Report @ https://intentmarketresearch.com/request-sample/hla-typing-for-transplant-market-3148.html

Geographical Insights

North America

North America holds a significant share of the HLA typing for transplant market, driven by advanced healthcare infrastructure, high transplant rates, and robust research activities. The U.S. leads in organ transplant procedures, further fueling the demand for HLA typing.

Europe

Europe is also a key player, with several countries investing in transplant services and HLA typing. The growing awareness of the importance of compatible organ transplants is boosting the market in this region.

Asia-Pacific

The Asia-Pacific region is expected to witness the highest growth during the forecast period. Rapid advancements in healthcare, increasing disposable incomes, and rising awareness of transplant procedures are driving the demand for HLA typing services in countries like China and India.

Key Players in the HLA Typing for Transplant Market

Thermo Fisher Scientific

A leading provider of HLA typing solutions, Thermo Fisher offers a range of reagents, instruments, and software for transplant compatibility testing.

Illumina, Inc.

Known for its innovative sequencing technologies, Illumina is making significant strides in molecular typing for HLA analysis.

BGI Group

BGI provides comprehensive genetic testing services, including HLA typing, and is a key player in the Asian market.

Emerging Trends in the HLA Typing for Transplant Market

Personalized Medicine

The trend towards personalized medicine is driving advancements in HLA typing. Tailoring transplant protocols to individual genetic profiles can enhance compatibility and improve patient outcomes.

Automation in Testing

Automated HLA typing solutions are gaining popularity as they reduce human error, increase throughput, and provide faster results.

Increased Collaboration

Collaborations between hospitals, research institutions, and diagnostic laboratories are enhancing the development of new HLA typing technologies and methodologies, fostering innovation in the field.

Future Outlook for the HLA Typing for Transplant Market

The HLA typing for transplant market is poised for substantial growth in the coming years. As technology continues to advance and the demand for transplants rises, the importance of accurate HLA typing will only increase. With a projected market size of USD 1,138 million by 2030, this sector presents significant opportunities for innovation and improvement in transplant success rates.

Conclusion

The HLA Typing for Transplant Market is on an upward trajectory, driven by the growing number of transplant procedures, technological advancements, and the rising prevalence of chronic diseases. Despite challenges such as high costs and regulatory hurdles, the future of HLA typing looks promising, with the potential to significantly enhance transplant compatibility and patient outcomes.

FAQs

What is HLA typing?

HLA typing is a test that identifies specific proteins on cells, crucial for matching organ donors and recipients to reduce transplant rejection.

Why is HLA typing important for transplants?

It ensures compatibility between the donor and recipient, which is vital for the success of organ transplants.

What are the main drivers of growth in the HLA typing market?

Increasing transplant procedures, technological advancements, and the rise in chronic diseases are key drivers.

What challenges does the HLA typing market face?

High costs, regulatory hurdles, and a shortage of organ donors pose challenges to market growth.

How is technology influencing the HLA typing for transplant market?

Advancements in molecular typing and automation are making HLA typing faster, more accurate, and cost-effective.

About Us

Intent Market Research (IMR) is dedicated to delivering distinctive market insights, focusing on the sustainable and inclusive growth of our clients. We provide in-depth market research reports and consulting services, empowering businesses to make informed, data-driven decisions.

Our market intelligence reports are grounded in factual and relevant insights across various industries, including chemicals & materials, healthcare, food & beverage, automotive & transportation, energy & power, packaging, industrial equipment, building & construction, aerospace & defense, and semiconductor & electronics, among others.

We adopt a highly collaborative approach, partnering closely with clients to drive transformative changes that benefit all stakeholders. With a strong commitment to innovation, we aim to help businesses expand, build sustainable advantages, and create meaningful, positive impacts.

Contact Us

US: +1 463-583-2713

0 notes

Text

Artificial Intelligence in Breast Imaging Market 2024-Global Industry Analysis, by Key Players, Segmentation, Trends and Forecast by 2032

The global artificial intelligence in breast imaging market is experiencing rapid growth, with its value estimated at USD 423.9 million in 2023 and expected to surge to USD 1.89 billion by 2032. With a projected compound annual growth rate (CAGR) of 16.1% over the forecast period from 2024 to 2032, AI-driven innovations are set to revolutionize breast cancer detection and diagnosis.

Breast imaging is a crucial component of breast cancer diagnosis and management, and AI-powered technologies are playing an increasingly significant role in enhancing the accuracy, speed, and efficiency of this process. The adoption of AI in breast imaging helps radiologists identify potential abnormalities, including cancers, at earlier stages, thereby improving patient outcomes and reducing the number of unnecessary biopsies.

Key Drivers of Market Growth

Increasing Incidence of Breast Cancer: The rising global incidence of breast cancer is one of the primary drivers for the adoption of AI in breast imaging. According to the World Health Organization (WHO), breast cancer is the most prevalent cancer among women worldwide. The demand for advanced diagnostic tools to detect cancer early and accurately is fueling the development and implementation of AI-based imaging solutions. These technologies can analyze mammograms, ultrasounds, and MRI scans with greater precision, aiding in early detection and personalized treatment planning.

Advancements in AI and Machine Learning: AI and machine learning (ML) algorithms are transforming breast imaging by offering unparalleled accuracy in detecting even subtle abnormalities that may go unnoticed by human radiologists. AI-driven tools have the potential to reduce false-positive and false-negative results, minimize diagnostic errors, and streamline the workflow of radiologists. By enhancing diagnostic confidence, these technologies help reduce the workload for healthcare professionals, while improving patient care.

Growing Adoption of Personalized Medicine: The push towards personalized medicine in cancer care has bolstered the demand for AI-based breast imaging solutions. AI tools can analyze vast datasets from imaging, clinical history, and genomics, providing individualized risk assessments and treatment options. This ability to personalize care based on unique patient characteristics is expected to drive further adoption of AI in breast imaging over the coming years.

Integration with Advanced Imaging Modalities: AI is being increasingly integrated with advanced imaging technologies such as 3D mammography (tomosynthesis), ultrasound, and magnetic resonance imaging (MRI). These integrated AI tools provide a more comprehensive analysis of breast tissue, allowing for better lesion characterization and improving diagnostic accuracy. AI-driven software can process high volumes of imaging data quickly, leading to faster diagnosis and treatment planning, which is crucial for improving patient outcomes in breast cancer management.

Access Free Sample Report: https://www.snsinsider.com/sample-request/4488

Challenges and Opportunities

While the benefits of AI in breast imaging are clear, challenges remain. The high cost of AI-based systems, coupled with the need for specialized training for radiologists to interpret AI-assisted results, may hinder adoption, particularly in low-resource healthcare settings. Additionally, there are concerns related to data privacy, regulatory approvals, and the integration of AI systems into existing healthcare infrastructures.

However, these challenges are creating opportunities for continued innovation. Ongoing research into AI algorithms, coupled with collaborations between healthcare providers, AI developers, and regulatory bodies, is expected to streamline the approval process and enhance the scalability of AI-based breast imaging solutions. As AI technology matures, cost-effective solutions tailored to various healthcare settings are anticipated to emerge.

Regional Insights

North America is expected to dominate the AI in breast imaging market, driven by high healthcare spending, a strong focus on early cancer detection, and the presence of leading AI technology developers. Europe follows closely, with increasing government initiatives to promote cancer screening and AI integration into healthcare systems.

The Asia-Pacific region is forecast to witness the highest growth during the forecast period, due to the rising incidence of breast cancer, expanding healthcare infrastructure, and growing investments in medical technology across countries like China, Japan, and India.

Future Outlook

The future of breast cancer diagnosis is becoming increasingly dependent on AI-driven innovations. With growing awareness about the importance of early detection, the demand for AI-powered breast imaging tools will continue to rise. These technologies promise to reduce diagnostic errors, enhance patient outcomes, and streamline radiology workflows.

As the market continues its upward trajectory, AI in breast imaging is expected to grow at a CAGR of 16.1%, reaching a valuation of USD 1.89 billion by 2032. Advances in AI algorithms, integration with imaging modalities, and a stronger focus on personalized medicine are set to reshape breast cancer diagnosis and care.

In conclusion, the AI in breast imaging market is poised for significant growth, transforming the landscape of breast cancer detection and improving patient care globally.

Other Trending Reports

Functional Endoscopic Sinus Surgery Market Size

Artificial Intelligence in Healthcare Market Size

Radiotherapy Market Size

Nicotine Replacement Therapy Market Size

0 notes

Text

The In Vivo Imaging Market is projected to grow from USD 2915 million in 2024 to an estimated USD 3880.233 million by 2032, with a compound annual growth rate (CAGR) of 3.64% from 2024 to 2032.The in vivo imaging market is a dynamic and rapidly expanding sector in the healthcare industry, playing a pivotal role in preclinical and clinical research. In vivo imaging refers to the visualization of biological processes and structures within a living organism. This technology is instrumental in understanding disease progression, evaluating therapeutic efficacy, and accelerating drug development. The demand for non-invasive, high-resolution, and real-time imaging solutions is propelling the growth of this market across the globe. This article explores the key drivers, technologies, and trends shaping the in vivo imaging market.

Browse the full report at https://www.credenceresearch.com/report/in-vivo-imaging-market

Key Market Drivers

1. Growing Preclinical Research and Drug Development:

In vivo imaging techniques have become a cornerstone in preclinical research, particularly in the pharmaceutical and biotechnology sectors. As the demand for new drug development and personalized medicine increases, researchers rely on imaging technologies to visualize the biological effects of therapeutic candidates in real-time. This accelerates the drug development pipeline by providing critical data on safety, efficacy, and pharmacokinetics.

2. Advances in Molecular Imaging:

Molecular imaging technologies, such as positron emission tomography (PET), single-photon emission computed tomography (SPECT), and optical imaging, are increasingly being used to study biological pathways at the molecular and cellular levels. These advancements enable researchers to detect diseases earlier, monitor treatment responses, and even predict outcomes in preclinical models. The precision offered by these tools has further driven their adoption in research institutions and pharmaceutical companies.

3. Rising Prevalence of Chronic Diseases:

The increasing global incidence of chronic diseases such as cancer, cardiovascular diseases, and neurological disorders has underscored the need for effective diagnostic and therapeutic monitoring tools. In vivo imaging systems are critical in detecting tumors, assessing cardiovascular health, and tracking neurological changes in conditions like Alzheimer's and Parkinson's disease. This surge in chronic diseases directly boosts the demand for advanced imaging solutions.

4. Technological Innovations:

Significant strides in imaging technologies have been made in recent years. Innovations such as hybrid imaging systems (e.g., PET-CT and PET-MRI), which combine different imaging modalities, have enhanced image resolution, accuracy, and functional data acquisition. These technologies offer a more comprehensive understanding of biological processes, helping clinicians make better-informed decisions.

5. Increased Government and Private Funding:

Government and private sector investments in healthcare research and innovation are providing significant financial support to the in vivo imaging market. Research initiatives focusing on cancer, cardiovascular diseases, and other critical health concerns are leading to increased utilization of advanced imaging technologies.

Types of In Vivo Imaging Technologies

1. Magnetic Resonance Imaging (MRI):

MRI is one of the most commonly used in vivo imaging techniques due to its ability to generate high-resolution images of soft tissues. It is particularly useful in neurology and cardiology research for imaging the brain, heart, and vascular structures.

2. Positron Emission Tomography (PET):

PET imaging is crucial for studying metabolic processes and is widely used in cancer research and neurology. It allows for the real-time assessment of cellular and molecular activity, providing valuable data on tumor metabolism and brain function.

3. Optical Imaging:

Optical imaging techniques such as bioluminescence and fluorescence imaging are extensively used in preclinical studies. These non-invasive methods are ideal for monitoring gene expression, protein-protein interactions, and tracking disease progression in animal models.

4. Computed Tomography (CT):

CT scanning provides detailed cross-sectional images of bones, organs, and tissues, making it an important tool for studying skeletal structures, lung diseases, and cardiovascular conditions in animal models.

5. Ultrasound Imaging:

Ultrasound is widely used in cardiovascular and obstetric research for real-time imaging of blood flow, heart function, and fetal development. It is favored for its non-invasive nature and cost-effectiveness.

Challenges Facing the In Vivo Imaging Market

Despite its rapid growth, the in vivo imaging market faces several challenges. High costs associated with advanced imaging systems, the need for specialized training to operate complex technologies, and ethical concerns regarding animal research are some of the major hurdles. Additionally, integrating these imaging technologies into clinical practice remains a significant challenge, particularly in low-resource settings where access to advanced equipment is limited.

Market Trends and Future Outlook

The future of the in vivo imaging market is promising, with several key trends emerging:

1. Artificial Intelligence (AI) Integration:

AI-powered imaging systems are becoming increasingly popular for automating image analysis and improving diagnostic accuracy. Machine learning algorithms are enabling researchers to extract more information from imaging data, leading to better predictive models and personalized treatment plans.

2. Expansion of Optical and Hybrid Imaging:

The integration of optical imaging with other modalities like MRI and PET is expected to continue, offering improved sensitivity and resolution for preclinical research. This trend is likely to expand the applications of imaging technologies beyond oncology and neurology into fields like immunology and infectious diseases.

3. Increased Adoption of Imaging in Drug Development:

As pharmaceutical companies continue to adopt imaging for drug discovery and development, the market is poised to see increased demand. Imaging will play an increasingly important role in evaluating drug safety and efficacy, reducing the time and cost associated with clinical trials.

Key Player Analysis:

Aspect Imaging Ltd. (Israel)

Biospace Lab (France)

Bruker (U.S.)

CMR Naviscan (U.S.)

FUJIFILM Holdings America Corporation (Canada)

General Electric (U.S.)

Guerbet (France)

Hitachi, Ltd. (Japan)

Koninklijke Philips N.V (Netherlands)

LI-COR, Inc. (U.S.)

Mediso Ltd. (U.S.)

MILabs B.V. (Netherlands)

Miltenyi Biotec (Germany)

MR Solutions (U.K.)

PerkinElmer Inc. (U.S.)

SCANCO Medical AG (Switzerland)

Siemens (Germany)

Takara Bio Inc. (Japan)

Trifoil Imaging (U.S.)

Segmentation:

By Modality:

Optical imaging,

Nuclear imaging,

Magnetic resonance imaging (MRI),

Ultrasound,

Others

By Reagents:

Bioluminescent and fluorescent labels,

Radioisotopes,

Nanoparticles,

Others

By Technique:

Radiography,

Optical imaging,

Magnetic resonance imaging,

Others

By End User:

Hospitals and clinics,

Research institutions,

Pharmaceutical and biotechnology companies,

Others

By Region

North America

The U.S

Canada

Mexico

Europe

Germany

France

The U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/in-vivo-imaging-market

About Us:

Credence Research is committed to employee well-being and productivity. Following the COVID-19 pandemic, we have implemented a permanent work-from-home policy for all employees.

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

Website: www.credenceresearch.com

0 notes

Text

Understanding the Idiopathic Pulmonary Fibrosis (IPF) Market: Growth, Challenges, and Innovations

Idiopathic Pulmonary Fibrosis (IPF) is a progressive and life-threatening lung disease characterized by the scarring of lung tissue, making breathing increasingly difficult. The Idiopathic Pulmonary Fibrosis market is experiencing steady growth, driven by advancements in drug therapies, increased awareness, and funding for research and development. According to market research, the IPF market size is projected to reach USD 4.60 billion in 2024 and is expected to grow to USD 6.43 billion by 2029, with a CAGR of 6.95% over the forecast period (2024-2029). This expansion reflects the increasing demand for innovative treatments and improved diagnostic capabilities.

Market Overview

The rising incidence of IPF, particularly among people over 50, is a key factor driving the growth of the market. With improved diagnostics and a better understanding of the disease, healthcare providers are diagnosing IPF earlier, leading to a surge in demand for effective treatment options.

Key Market Drivers:

Growing Disease Prevalence: As the global population ages, the number of people diagnosed with IPF is rising, creating a growing need for advanced therapies.

Advanced Diagnostic Tools: Innovations in imaging technologies and the use of biomarkers have enabled early and more accurate diagnoses, which is crucial for effective treatment.

Drug Therapies and Approvals: The approval of antifibrotic drugs like pirfenidone and nintedanib has revolutionized IPF treatment, helping to slow the progression of the disease and improve patient outcomes.

Challenges in the IPF Market

Despite significant advancements, the IPF market still faces several hurdles:

High Treatment Costs: The high cost of antifibrotic therapies can place a heavy financial burden on patients, particularly in regions with limited access to affordable healthcare.

Limited Treatment Options: While existing treatments can slow disease progression, they are not curative, highlighting the unmet need for more effective drugs.

Side Effects: Current medications often come with side effects, affecting patients' adherence to long-term treatment plans. Balancing efficacy with tolerability remains a key challenge for drug developers.

Regional Insights

North America holds the largest share of the Idiopathic Pulmonary Fibrosis market, thanks to advanced healthcare infrastructure and early adoption of new treatments.

Europe follows closely behind, supported by growing government initiatives, robust healthcare systems, and increased R&D funding.

The Asia-Pacific region is anticipated to witness rapid growth, fueled by rising healthcare expenditures and greater focus on the treatment of rare diseases such as IPF.

Conclusion

The Idiopathic Pulmonary Fibrosis market is positioned for continued growth, driven by innovations in diagnostics, drug therapies, and increased awareness of the disease. While challenges such as treatment costs and limited options persist, ongoing research and new drug development offer promising avenues for improvement. By 2029, with a projected market value of USD 6.43 billion, the industry is expected to make significant strides, potentially transforming the outlook for IPF patients around the world.

For a detailed overview and more insights, you can refer to the full market research report by Mordor Intelligence https://www.mordorintelligence.com/industry-reports/idiopathic-pulmonary-fibrosis

#marketing#Idiopathic Pulmonary Fibrosis market#Idiopathic Pulmonary Fibrosis market size#Idiopathic Pulmonary Fibrosis market share#Idiopathic Pulmonary Fibrosis industry#Idiopathic Pulmonary Fibrosis market trends#Idiopathic Pulmonary Fibrosis market growth

0 notes

Text

Menkes Disease Treatment Market Will Grow At Highest Pace Owing To Rising Orphan Drug Designations

Menkes disease is an X-linked neurodegenerative disorder caused by mutations in the ATP7A gene. Symptoms include sparse, brittle hair; impaired vascular tissue growth; low serum copper levels; and delayed development. Treatment for Menkes disease primarily involves replacement of copper through intravenous administration of copper histidine. Currently, there are only a few FDA-approved treatment options for Menkes disease. Patients primarily rely on off-label use of existing copper histidine products.

The Menkes Disease Market size is estimated to be valued at US$ 165.1 million in 2024 and is expected to exhibit a CAGR of 6.6% over the forecast period 2024-2031.

Key Takeaways

Key players operating in the Menkes disease treatment market are Fortress Biotech, Inc., Teva Pharmaceutical Industries Ltd., Amerigen Pharmaceuticals Limited, Mylan N.V., and Bausch Health Companies Inc. Fortress Biotech launched MNK-6105, a novel formulation of copper histidine for the treatment of Menkes disease in 2020.

The growing diagnosis of Menkes disease, especially in developed regions, is expected to drive the demand for treatment drugs. According to CDC, an estimated 1 in 34,000 to 39,000 newborn males are affected by Menkes disease each year in the United States.

Technological advancements in drug design and manufacturing, such as modified drug delivery systems and novel formulations, are generating lucrative opportunities in the market. Companies are focusing on developing orphan drugs with improved bioavailability and fewer side effects.

Market Trends

Increasing collaborations between biotech companies and research institutes is one of the key trends witnessed in the market. For instance, in 2019 Fortress Biotech partnered with the University of Connecticut to develop treatments for rare genetic disorders like Menkes disease.

Emergence of novel drug formulations is another major trend. MNK-6105 developed by Fortress Biotech is a nano-particle formulation of copper histidine, resulting in enhanced absorption and lowering the dosing frequency.

Market Opportunities

Orphan drug designations by regulatory bodies provide significant market opportunities. Drugs in development for rare diseases like Menkes enjoy benefits like tax credits, waiver of application fees, and market exclusivity for a period of 7 years in the US.

Geographic expansion in developing Asian countries and Latin America presents untapped growth prospects. Availability of low-cost manufacturing infrastructure and emergence of local biotech companies also supports market expansion.

Impact Of COVID-19 On Menkes Disease Market Growth

The outbreak of COVID-19 pandemic has adversely impacted the growth of Menkes disease market globally. Several factors such as restrictions on non-essential medical services, disruptions in supply chain, difficulty in conducting clinical trials, etc contributed to slowed market growth during the crisis. However, with gradual lifting of lockdowns and restoration of healthcare facilities post-recovery from first and second waves, the market is expected to regain lost momentum. Teleconsultations helped to sustain continuity of care for Menkes disease patients during lockdowns. Development of vaccines and treatments have improved disease management, though challenges persist in some geographical regions with limited resources. In the post-pandemic scenario, partnerships involving stakeholders would be pivotal to ensure uninterrupted access to diagnostics and therapeutics. Long-term strategies focusing on decentralized community-based services may help boost early diagnosis and effective treatment interventions.

Menkes Disease Market In North America

North America holds the major share of the Menkes Disease Market in terms of value. This can be mainly attributed to factors such as availability of advanced healthcare infrastructure, growing healthcare expenditure, presence of major market players, and high diagnosis and treatment rates in the region. The United States commands the lion's share within the North America regional market. Favorable reimbursement policies have ensured high adoption of screening and treatment options for Menkes disease. Furthermore, continuous research activities have led to development of new treatment approaches, driving the regional market growth. Other countries in North America such as Canada are also lucrative markets expected to register significant growth over the forecast period.

Fastest Growing Region - Asia Pacific

The Asia Pacific region is poised to witness the fastest growth in the Menkes disease market during the forecast period. This growth can be credited to rising medical tourism, increasing patient population due to growing birth rates, and improving healthcare expenditures in emerging economies of the region. In addition, heightened awareness about early diagnosis and availability of generic medications are supporting the Asia Pacific market expansion. Countries such as China and India with their large population bases and significant improvements in healthcare access present immense growth opportunities. Initiatives by governments towards strengthening newborn screening programs would boost early diagnosis and treatment uptake. Overall, the Asia Pacific Menkes disease market is anticipated to attract higher investments from global players over the coming years.

Get more insights on this topic: https://www.trendingwebwire.com/menkes-disease-market-estimated-to-witness-high-growth-owing-to-advancements-in-gene-therapy/

Author Bio

Vaagisha brings over three years of expertise as a content editor in the market research domain. Originally a creative writer, she discovered her passion for editing, combining her flair for writing with a meticulous eye for detail. Her ability to craft and refine compelling content makes her an invaluable asset in delivering polished and engaging write-ups. (LinkedIn: https://www.linkedin.com/in/vaagisha-singh-8080b91)

What Are The Key Data Covered In This Menkes Disease Market Report?

:- Market CAGR throughout the predicted period

:- Comprehensive information on the aspects that will drive the Menkes Disease Market's growth between 2024 and 2031.

:- Accurate calculation of the size of the Menkes Disease Market and its contribution to the market, with emphasis on the parent market

:- Realistic forecasts of future trends and changes in consumer behaviour

:- Menkes Disease Market Industry Growth in North America, APAC, Europe, South America, the Middle East, and Africa

:- A complete examination of the market's competitive landscape, as well as extensive information on vendors

:- Detailed examination of the factors that will impede the expansion of Menkes Disease Market vendors

FAQ’s

Q.1 What are the main factors influencing the Menkes Disease Market?

Q.2 Which companies are the major sources in this industry?

Q.3 What are the market’s opportunities, risks, and general structure?

Q.4 Which of the top Menkes Disease Market companies compare in terms of sales, revenue, and prices?

Q.5 Which businesses serve as the Menkes Disease Market’s distributors, traders, and dealers?

Q.6 How are market types and applications and deals, revenue, and value explored?

Q.7 What does a business area’s assessment of agreements, income, and value implicate?

*Note:

1. Source: Coherent Market Insights, Public sources, Desk research

2. We have leveraged AI tools to mine information and compile it

#Menkes Disease Market Trend#Menkes Disease Market Size#Menkes Disease Market Information#Menkes Disease Market Analysis#Menkes Disease Market Demand

0 notes

Text

Biopreservation Market by Regions, Type & Applications During 2023-2030

Biopreservation Market Size & Trends

The global biopreservation market size was valued at USD 2.18 billion in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 28.30% from 2023 to 2030.

Biopreservation is experiencing growth due to various factors such as extensive usage in hospitals and labs, rising funding assistance from government and private partners in healthcare, an upsurge in research & development, and growing advancement in terms of product development. For example, in April 2021, BioLife Solutions launched a new high-capacity controlled freezer to cater to the cell and gene therapy market, which helped the company expand its existing product portfolio. The market experienced a major hindrance during the COVID-19 pandemic with supply chain issues, unavailability of raw materials, and hindrances in research activities among other reasons. However, the pandemic also accelerated the growth of novel biologics, and vaccine technologies. Due to these factors, opportunities for biologics manufacturing and preservation are anticipated to increase, thus generating further demand for biopreservation.

Gather more insights about the market drivers, restrains and growth of the Biopreservation Market

Biopreservation is a process that helps maintain the integrity and functionality of biological products such as stem cells, DNA, tissues, and organs under different temperatures, thereby prolonging their lifespan outside their natural environment. Technology innovations include microarrays or incorporation of a wide range of predictive models, such as hybrid models, and various API algorithms which help reduce the time, cost and complexity of the overall process. Furthermore, the advent of multiplex cellular imaging platforms is anticipated to enhance the biopreservation ability to help understand disease progression and suggest suitable diagnostic & treatment measures to follow, specifically for cardiology, gynecology, and point-of-care applications.

In recent years, there has been an upsurge in demand for use of biopreservation to develop biological products in R&D of various sectors such as immunotherapies, vaccine production, antibody production, enzyme technology, and biologically produced chemicals. This impact is due to the rising number of chronic disease incidences globally. For instance, according to the Centers for Disease Control and Prevention, cardiovascular disorders and cancer are among the leading causes of disease-related mortality in adults in the U.S.

Furthermore, the government and private sectors have shown interest and supported funding activities in research & development, leading to immense market developments. In recent years, the growing demand for preserving stem cells and developing biological medicines and products has gained investors' focus in this field. This considerable healthcare spending is expected to fuel market growth during the forecast period.

However, the growing biopreservation market is associated with challenges such as the unavailability of skilled professionals and the lack of stringent cybersecurity measures. The high cost of labor training and software standardization are some of the contributing factors. These challenges could potentially impact overall market growth.

Biopreservation Market Segmentation

Grand View Research has segmented the global biopreservation market report on the basis of product, application, and region:

Product Outlook (Revenue, USD Billion, 2018 - 2030)

Equipment

Freezers

Refrigerators

Consumables

Vials

Straws

Microtiter Plates

Bags

Liquid Nitrogen

Media

Pre-formulated

Home-brew

Laboratory Information Management System (LIMS)

Application Outlook (Revenue, USD Billion, 2018 - 2030)

Regenerative Medicine

Cell Therapy

Gene Therapy

Others

Bio-banking

Human Eggs

Human Sperms

Veterinary IVF

Drug Discovery

Regional Outlook (Revenue, USD Billion, 2018 - 2030)

North America

US

Canada

Europe

Germany

UK

France

Italy

Spain

Denmark

Sweden

Norway

Asia Pacific

China

Japan

India

Australia

Thailand

South Korea

Latin America

Brazil

Mexico

Argentina

Middle East and Africa (MEA)

South Africa

Saudi Arabia

UAE

Kuwait

Browse through Grand View Research's Biotechnology Industry Research Reports.

The global optical genome mapping market size was valued at USD 104.1 million in 2023 and is expected to grow at a CAGR of 26.76% from 2024 to 2030.

The global therapeutic drug monitoring market size was valued USD 1.80 billion in 2023 and is projected to grow at a CAGR of 3.8% from 2024 to 2030.

Key Companies & Market Share Insights

Key players in the market are opting for strategic initiatives, funding facilities for geographical expansion, partnerships, mergers and acquisitions in key regions. For instance, in January 2023, the Hamad Medical Corporation and Qatar BioBank launched a new tissue biobank service in Qatar to provide researchers the access to high-quality tissue samples. Some of the key players in the biopreservation market include:

Azenta US, Inc.

Biomatrica, Inc.

BioLife Solutions

MVE Biological Solutions

LabVantage Solutions, Inc.

Taylor-Wharton.

Thermo Fisher Scientific, Inc.

Panasonic Corporation

X-Therma Inc.

PrincetonCryo.

Stirling Ultracold

Order a free sample PDF of the Biopreservation Market Intelligence Study, published by Grand View Research.

0 notes

Text

Breast Biopsy Devices Market | Future Growth Aspect Analysis to 2030

The Breast Biopsy Devices Market is expected to grow from USD 1.8 billion in 2023-e to USD 3.4 billion by 2030, at a CAGR of 9.7% during the forecast period. Breast cancer is one of the most prevalent forms of cancer among women globally, making early detection and accurate diagnosis critical for effective treatment. A breast biopsy is a key procedure that allows healthcare professionals to determine whether a suspicious lump or mass in the breast is malignant.

Over the years, advancements in breast biopsy devices have revolutionized the diagnostic process, leading to improved patient outcomes. The breast biopsy devices market has witnessed significant growth in recent years, driven by technological innovations, rising awareness, and the increasing prevalence of breast cancer. In this blog, we will explore the key trends, opportunities, and challenges in this expanding market.

Read More about Sample Report: https://intentmarketresearch.com/request-sample/breast-biopsy-devices-market-3017.html

Key Market Trends

Technological Advancements

The evolution of breast biopsy devices is largely fueled by continuous innovation in technology. Devices like vacuum-assisted biopsy (VAB), core needle biopsy (CNB), and fine needle aspiration biopsy (FNAB) have seen improvements in accuracy, precision, and minimally invasive procedures. The introduction of real-time imaging, such as ultrasound, MRI, and stereotactic guidance, has enhanced the ability to detect and sample tissue from suspicious areas, reducing the need for repeat biopsies.

Rising Prevalence of Breast Cancer

The increasing incidence of breast cancer, especially in developing countries, is one of the primary drivers of market growth. According to the World Health Organization (WHO), breast cancer accounts for approximately 30% of all new cancer cases in women globally. With a greater emphasis on early detection, the demand for breast biopsy devices is projected to grow steadily.

Growing Awareness and Screening Programs

Initiatives by governments and healthcare organizations to promote breast cancer screening and awareness campaigns have played a significant role in encouraging women to undergo regular check-ups. Programs like mammography screening help detect abnormalities early, leading to more biopsies for diagnostic confirmation. This increase in screenings is positively impacting the breast biopsy devices market.

Shift Toward Minimally Invasive Procedures

Minimally invasive procedures are becoming the gold standard in healthcare due to reduced patient discomfort, faster recovery times, and lower risk of complications. In the context of breast biopsies, vacuum-assisted biopsy devices have gained popularity due to their precision and the ability to collect multiple tissue samples through a single incision.

Market Opportunities

Emerging Markets

Emerging economies, particularly in Asia-Pacific and Latin America, offer lucrative opportunities for the breast biopsy devices market. These regions are witnessing rapid urbanization, improved healthcare infrastructure, and increased healthcare expenditure, leading to a growing demand for diagnostic tools like breast biopsy devices.

Innovations in AI and Machine Learning

Artificial intelligence (AI) and machine learning (ML) are transforming the medical field, including breast cancer diagnostics. Companies are developing AI-powered systems that assist in biopsy image analysis, improving the accuracy of cancer detection. The integration of AI into breast biopsy devices can further enhance diagnostic precision, offering significant potential for market growth.

Expansion of Telemedicine

The COVID-19 pandemic has accelerated the adoption of telemedicine, making remote consultations and diagnostics more common. As telemedicine platforms evolve, they may incorporate diagnostic devices, including biopsy tools, enabling faster and more convenient diagnosis for patients. This trend could further boost the demand for biopsy devices globally.

Ask for Customization Report: https://intentmarketresearch.com/ask-for-customization/breast-biopsy-devices-market-3017.html

Challenges Facing the Market

High Cost of Devices

Despite technological advancements, the high cost of breast biopsy devices and procedures remains a major barrier to widespread adoption, especially in low- and middle-income countries. Many healthcare systems struggle with affordability, limiting access to these advanced diagnostic tools.

Regulatory Hurdles

Stringent regulatory frameworks pose challenges to market growth. Regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) require thorough testing and approval of new devices, which can be a time-consuming and costly process. Manufacturers need to ensure compliance with these regulations while keeping up with technological advancements.

Lack of Skilled Professionals

While breast biopsy devices are becoming more sophisticated, they require skilled professionals to operate them. In many parts of the world, there is a shortage of trained radiologists and pathologists, limiting the widespread adoption of advanced biopsy technologies.

Conclusion

The breast biopsy devices market is poised for growth in the coming years, driven by technological innovations, rising breast cancer cases, and increasing awareness about the importance of early diagnosis. While challenges such as high device costs and regulatory hurdles exist, the opportunities in emerging markets and the potential of AI-driven solutions offer promising prospects. As the healthcare landscape continues to evolve, the breast biopsy devices market will play a pivotal role in improving breast cancer detection and patient outcomes.

0 notes

Text

Medical Polymer Market: Trends, Innovations, and Growth

The medical polymer market has seen remarkable growth in recent years, driven by technological advancements, increasing healthcare demands, and a growing preference for lightweight, biocompatible materials in the medical field. As polymers continue to replace traditional materials like metals and ceramics, their role in medical devices, drug delivery systems, and implants is becoming more significant.

Market Overview

Medical polymers, which include resins, fibers, and elastomers, play a crucial role in healthcare. These materials offer a variety of benefits such as flexibility, durability, and biocompatibility, making them suitable for a range of medical applications, including:

Medical devices: Polymers are commonly used in manufacturing surgical instruments, diagnostic equipment, and prosthetics due to their sterilizability and resistance to chemicals.

Implants: Medical-grade polymers are increasingly favored in implants for their biocompatibility, helping to reduce the risk of infection and improving patient recovery time.

Pharmaceuticals: Polymers are utilized in controlled drug delivery systems and packaging, ensuring medication is delivered effectively and safely.

The global medical polymer market was valued at USD 20.2 billion in 2021 and is expected to grow at a compound annual growth rate (CAGR) of around 8.5% from 2021 to 2028. This growth is primarily driven by the increasing use of minimally invasive procedures, the rising geriatric population, and the ongoing need for advanced medical devices.

Key Trends and Drivers

Growing Demand for Biocompatible and Biodegradable Polymers Biocompatibility is essential in medical devices and implants, where materials must not react negatively with the human body. Biodegradable polymers are gaining traction in wound care, tissue engineering, and drug delivery, as they reduce the need for second surgeries to remove devices, such as stitches or implants.

Advances in 3D Printing Technology 3D printing, or additive manufacturing, has revolutionized the medical polymer market by allowing for customized, patient-specific medical devices and implants. This technology facilitates the creation of complex structures that were previously impossible with traditional manufacturing methods. Polymers used in 3D printing include polyether ether ketone (PEEK) and polylactic acid (PLA), both of which are biocompatible and ideal for producing precise medical parts.

Rise in the Use of Polymeric Nanomaterials Nanotechnology is reshaping healthcare, particularly in drug delivery and diagnostics. Polymeric nanoparticles are used to create more efficient drug delivery systems, improving the bioavailability and targeting of medications. These nanomaterials enable the delivery of drugs directly to diseased tissues, minimizing side effects and enhancing patient outcomes.

Increased Focus on Sustainable Healthcare Solutions As the world becomes more focused on sustainability, the healthcare industry is no exception. There is a growing interest in developing eco-friendly medical polymers that not only meet regulatory standards but also minimize environmental impact. Companies are exploring alternatives to petroleum-based polymers, including bio-based plastics and recycling initiatives, to reduce waste in the medical sector.

Key Players in the Market

Some of the leading companies in the medical polymer market include:

BASF SE: A global leader in chemical manufacturing, BASF offers a wide range of medical polymers, including biocompatible and biodegradable materials.

Dow Inc.: Known for its extensive polymer portfolio, Dow provides medical-grade polymers that meet stringent regulatory requirements.

Celanese Corporation: A key player in the development of high-performance medical polymers, Celanese focuses on creating materials that are resistant to heat and chemicals, making them ideal for surgical instruments.

Eastman Chemical Company: With a focus on innovation, Eastman develops advanced polymers for medical devices and packaging, particularly those that prioritize patient safety and hygiene.

These companies are investing heavily in research and development (R&D) to create next-generation medical polymers that can address the evolving needs of the healthcare industry.

Challenges Facing the Medical Polymer Market

While the medical polymer market is growing rapidly, it also faces certain challenges:

Stringent Regulatory Approvals: Medical polymers must meet rigorous safety and performance standards set by regulatory bodies such as the FDA and EMA. This can slow down the introduction of new materials into the market.

High Production Costs: The manufacturing process for medical-grade polymers is often complex and costly. Companies must balance the need for innovative materials with cost-effective production methods to remain competitive.

Environmental Concerns: The medical industry generates significant amounts of plastic waste, particularly from disposable medical devices. Finding sustainable solutions while maintaining product safety and efficacy is a pressing concern for manufacturers.

Future Outlook

The future of the medical polymer market looks promising, with several factors contributing to its continued expansion. Technological innovations, such as 4D printing (which allows materials to change shape in response to stimuli) and smart polymers (that can respond to changes in their environment), are set to revolutionize the industry. Moreover, the increasing demand for personalized medicine will drive the need for custom-made medical devices and implants, further fueling the growth of 3D printing in healthcare.

Additionally, as healthcare providers seek to improve patient outcomes while reducing costs, medical polymers will continue to be a preferred choice due to their versatility, cost-effectiveness, and ability to meet the stringent requirements of the medical industry.

Download PDF Brochure :

The medical polymer market is poised for robust growth, driven by advances in technology, an aging population, and the rising demand for biocompatible materials in healthcare. Industry experts should pay close attention to the developments in biodegradable polymers, 3D printing, and nanotechnology, as these trends will shape the future of the market. With the right balance of innovation and sustainability, the medical polymer industry will continue to play a vital role in improving healthcare outcomes worldwide.

#MedicalPolymers#HealthcareInnovation#BiocompatibleMaterials#MedicalDevices#3DPrinting#SustainableHealthcare#MedicalPolymerMarket#Nanotechnology#BiodegradablePolymers#MedicalImplants#DrugDelivery#HealthcareTrends#MedicalMaterialScience#MedicalPolymerIndustry#MedicalGradePolymers

0 notes

Text

DNA and RNA Sample Preparation Market is Estimated to Witness High Growth Owing to Increasing Adoption

The DNA and RNA sample preparation market involves processes associated with isolation, extraction, purification and quantification of nucleic acids DNA and RNA from various sources like tissues, blood, sperm, cells etc. for downstream applications in genomics, molecular diagnostics, personalized medicine and others. The sample preparation is a critical and initial step before conducting various genomic tests including Next Generation Sequencing, polymerase chain reaction and other assays. Growing awareness and adoption of precision medicine and genetic/molecular testing is driving demand for efficient nucleic acid isolation and downstream analysis.

The Global DNA and RNA Sample Preparation Market is estimated to be valued at US$ 2262.46 Mn in 2024 and is expected to exhibit a CAGR of 5.8% over the forecast period 2024 To 2031.

Key Takeaways

Key players operating in the DNA and RNA sample preparation are Agilent Technologies, Inc., Becton, Dickinson and Company, Bio-Rad Laboratories Inc., DiaSorin S.p.A, F. Hoffmann-La Roche, Miroculus, Inc., Illumina, Inc., PerkinElmer, Inc., QIAGEN, Sigma Aldrich Corp., Tecan Group AG, and Thermo Fisher Scientific, Inc. Growing prominence of personalized medicine is creating opportunities for development of new sample preparation methods and kits which can extract nucleic acids from various types of samples. Rising incidence of chronic and infectious diseases worldwide is increasing diagnostic testing which will propel sample preparation market growth. Global expansion of key market players through acquisitions and partnerships with regional diagnostic labs and research institutes will further augment market revenues.

Market Drivers

Increasing funding for Genomic and genetic research from government bodies as well as private sector is one of the key factors driving the DNA and RNA Sample Preparation Market Size. Government initiatives aimed at large scale population screening and clinical testing for various genetic disorders, infectious diseases and cancers are also creating demand for high throughput nucleic acid preparation. Growing geriatric population and rising healthcare spending in developing nations also provides growth opportunities for market players in the forecast period.

PEST Analysis

Political: Laws and regulations imposed by governments for research using DNA and RNA samples could impact the market. Changes in healthcare policies will also have effects.

Economic: Factors like GDP growth, income levels, healthcare spending will drive demand. Rise in research activities and focus on precision medicine boost the market.

Social: Growing awareness about personalized medicine and importance of genetic testing are important. Social trends also promote preventive healthcare and wellness.