Don't wanna be here? Send us removal request.

Statistics

We looked inside some of the posts by rutukdm and here's what we found interesting.

Average Info

Notes Per Post

0

Likes Per Post

0

Reblog Per Post

0

Reply Per Post

0

Time Between Posts

5 days

Number of Posts By Type

Text

17

Last Seen Tumblr Blogs

Fun Fact

In Q3 of 2020, 31% of US users access the Tumblr app daily.

Text

Animal Feed Market Trends and Forecast 2025

The Future of Animal Feed: How Market Growth Will Shape Global Meat Prices

The animal feed industry is undergoing a huge transition, which may influence how much we spend for meat in the next years. With billions of dollars in planned growth, understanding what is driving this expansion allows us to predict where food prices will go. What Does Market Growth Mean for Your Grocery Bill? The worldwide animal feed industry is now valued at approximately USD 533.4 billion in 2024, but experts anticipate that it will increase to USD 681.8 billion by 2033. That equates to a consistent CAGR of 2.8% every year. Some studies believe it might potentially reach $1,008.8 billion by 2031, expanding at a CAGR of 4.7% each year.

Why should you care about feed prices? Simple - animal feed makes up 60-70% of what it costs to raise livestock. When feed gets more expensive, meat prices usually follow. The good news is that this steady growth suggests we won't see the wild price swings we've experienced recently. The bad news? Meat prices will likely keep creeping up gradually.

Think of it this way: better feed technology might help farmers raise animals more efficiently, which could keep some costs down. But as more people around the world want quality meat, the demand for good feed keeps pushing prices up. It's a balancing act that will probably result in slowly rising meat prices over the next decade.

Why Emerging Markets Are Driving Poultry Feed Demand

Chicken and other poultry are becoming the go-to protein choice worldwide, especially in developing countries. Poultry feed now represents 39.0% of the entire animal feed market, making it the biggest segment by far.

There are several reasons why poultry feed is booming in emerging markets. First, chicken is relatively affordable compared to beef or pork, making it accessible to growing middle-class populations in countries like India, Brazil, and parts of Southeast Asia. Second, raising chickens requires less time and money upfront than other livestock, so small-scale farmers can get started more easily.

The Asia-Pacific region perfectly shows this trend. It controls 39.2% of the global market, worth about USD 286.2 billion, and it's growing faster than anywhere else at CAGR of 5.9%. Countries across Asia are seeing explosive growth in chicken consumption as people earn more money and move to cities where fresh meat is more readily available.

This isn't just about economics - it's about changing lifestyles. As people in emerging markets become more urbanized and affluent, they're eating more protein, and chicken is often their first choice because it's affordable, versatile, and widely accepted culturally.

Why Pellets Are Taking Over Feed Manufacturing

Walk into any modern farm, and you'll likely see pellet feed rather than the traditional mash feed that farmers used decades ago. There's a good reason for this shift - pellets simply work better in almost every way.

Pellets are made by taking regular feed ingredients, adding steam and pressure, then forming them into small, hard nuggets. This process creates several advantages that farmers love. First, pellets are much easier to handle, store, and transport than loose feed. They don't separate into different components during shipping, so animals get consistent nutrition in every bite.

From a practical standpoint, pellets last longer without spoiling, which is crucial in hot climates or places where storage conditions aren't ideal. They also reduce waste because animals can't pick through them to eat only their favorite parts, leaving the rest behind.

However, the market shows that preferences vary by region. Traditional mash feed still holds about 60% of the poultry feed market, especially in cost-sensitive areas where the extra processing costs of pellets don't make economic sense. But overall, the trend is clearly moving toward pellets as farming operations become more mechanized and efficiency-focused.

How Industry Giants Are Shaping the Future

Two companies - Cargill and BASF SE - are playing a huge role in determining where the animal feed industry goes next. In January 2023, these companies extended their partnership to develop better enzyme solutions for animal feed in the US market. This might sound technical, but it's actually quite important for everyday consumers.

What these companies are doing is creating feed that helps animals digest their food better and grow more efficiently. When animals can convert feed into meat more effectively, it reduces costs and environmental impact. The partnership combines BASF's research expertise with Cargill's massive distribution network and practical farming knowledge.

This collaboration started back in October 2021, and it shows how the biggest players in the industry are working together rather than competing on everything. They're focusing on making feed more sustainable and efficient, which could help keep future price increases

What This Means for the Future

The animal feed industry's growth to USD 681.8 billion by 2033 represents more than just bigger numbers - it reflects fundamental changes in how the world produces food. As emerging markets continue developing and their populations demand more protein, the pressure on feed production will only increase.

For consumers, this likely means gradually rising meat prices, but not the dramatic spikes we've seen during supply chain disruptions. The industry is becoming more efficient and sustainable, which should help keep increases manageable.

The dominance of poultry feed reflects changing global eating habits, with more people choosing chicken over other meats. The shift toward pellet feed shows an industry focused on efficiency and reducing waste.

Key Players

The key players operating in the global animal feed market are Charoen Pokphand Foods PCL (Thailand), New Hope Liuhe Co., Ltd. (China), Cargill, Incorporated (U.S.), Brf S.A. (Brazil), Tyson Foods, Inc. (U.S.), Nutreco N.V. (Netherlands), Archer-Daniels-Midland Company (U.S.), Alltech Inc. (U.S.), ForFarmers N.V. (Netherlands), De Heus Animal Nutrition (Netherlands), Royal Agrifirm Group (Netherlands), and Guangdong HAID Group Co., Ltd. (China).

Download Sample Report Here @ https://www.meticulousresearch.com/download-sample-report/cp_id=5393

Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

#AnimalFeed#LivestockNutrition#FeedAdditives#PoultryFeed#CattleFeed#Aquafeed#PetFoodMarket#AnimalHealth#AgricultureIndustry#FeedMarketTrends#AnimalNutrition#LivestockIndustry#CompoundFeed#FeedIngredients#FeedManufacturing

0 notes

Text

ADAS Market Size Share and Industry Forecast

Meticulous Research®—a leading global market research company, published a research report titled, ‘ADAS Market by Type (Blind Spot Detection Systems, Automatic Emergency Braking Systems), Automation (Level 1, 2, and 3), Component (Vision Camera Systems, Sensors), Vehicle, End Use (Passenger, Commercial), and Geography - Global Forecast to 2031.’

According to the latest publication from Meticulous Research®, the ADAS market is projected to reach $122.86 billion by 2031, at a CAGR of 14.6% during the forecast period 2024–2031. The growth of the ADAS market is driven by stringent vehicle safety regulations, the rising demand for luxury cars, and the increasing integration of safety and comfort features in high-end vehicles. However, the lack of supporting infrastructure in developing countries restrains the growth of this market.

Moreover, the emergence of autonomous vehicles, increasing developments in the autonomous shared mobility space, and the rising adoption of electric vehicles are expected to generate market growth opportunities. However, environmental and data security risks and the high costs of implementing ADAS are major challenges for the players operating in this market.

The global ADAS market is segmented based on system type (adaptive cruise control systems, blind spot detection systems, automatic parking systems, pedestrian detection systems, traffic jam assistance systems, lane departure warning systems, tire pressure monitoring systems, automatic emergency braking systems, adaptive front-lighting systems, traffic sign recognition systems, forward collision warning systems, driver monitoring systems, and night vision systems), level of automation (level 1, level 2, and level 3), component (vision camera systems, sensors, ECU, software, and actuators), vehicle type (internal combustion engine, hybrid, and electric vehicles), end use (passenger vehicles and commercial vehicles), and geography. The study also evaluates industry competitors and analyses the regional and country-level markets.

Based on system type, the ADAS market is broadly segmented into adaptive cruise control systems, blind spot detection systems, automatic parking systems, pedestrian detection systems, traffic jam assistance systems, lane departure warning systems, tire pressure monitoring systems, automatic emergency braking systems, adaptive front-lighting systems, traffic sign recognition systems, forward collision warning systems, driver monitoring systems, and night vision systems. In 2024, the adaptive cruise control systems segment is expected to account for the largest share of the market. The growth of this segment is mainly attributed to the need to maintain a comfortable driving experience, supportive government regulations, and advancements in adaptive cruise control systems.

However, the blind spot detection systems segment is projected to register the highest CAGR during the forecast period. The growth of this segment is attributed to the expanding e-commerce and logistics sector, the increasing adoption of BSD systems in vehicles, and the rising use of complementary metal oxide semiconductors (CMOS) image sensors.

Based on level of automation, the ADAS market is broadly segmented into level 1, level 2, and level 3. In 2024, the level 1 segment is expected to account for the largest share of the market. The growth of this segment is attributed to the growing investments in vehicle electrification, the rising demand for driver assistance systems, and the increasing number of Level 1 vehicles on the road.

However, the level 3 segment is projected to register the highest CAGR during the forecast period. The growth of this segment is attributed to the rising demand for self-driving vehicles and the increasing initiatives by major market players aimed at launching advanced Level 3 autonomous cars.

Based on component, the ADAS market is broadly segmented into vision camera systems, sensors, ECU, software, and actuators. In 2024, the sensors segment is expected to account for the largest share of the market. However, the sensors segment is projected to register the highest CAGR during the forecast period. The growth of this segment is attributed to the rising need to reduce greenhouse gas emissions and the increasing demand for sensors in hybrid powertrains.

Also, this segment is projected to register the highest CAGR during the forecast period.

Based on vehicle type, the ADAS market is broadly segmented into internal combustion engine, hybrid, and electric vehicles. In 2024, the internal combustion engine vehicles segment is expected to account for the largest share of the market. Internal combustion engine (ICE) vehicles are automobiles that use an internal combustion engine (ICE) to power the vehicle. ICEs are typically powered by fossil fuels such as gasoline or diesel, but they can also be powered by alternative fuels such as ethanol or compressed natural gas. ICE vehicles have been the dominant form of transportation for the past century.

However, the electric vehicles segment is projected to register the highest CAGR during the forecast period. The supportive government policies and regulations, increasing investments by leading automotive OEMs, rising environmental concerns, decreasing prices of batteries, and advancements in charging technologies are the key factors driving the growth of electric vehicles in the ADAS market.

Based on end use, the ADAS market is broadly segmented into passenger and commercial vehicles. In 2024, the passenger vehicles segment is expected to account for the larger share of the ADAS market. The growth of this segment is attributed to the growing awareness regarding the hazards associated with greenhouse gas emissions and environmental pollution, stringent emission norms, and demand for premium cars among consumers.

However, the commercial vehicles segment is projected to register the highest CAGR during the forecast period. The growth of this segment is attributed to the increase in fuel prices and stringent emission norms set by governments, the growing adoption of autonomous delivery vehicles, and the increasing adoption of electric buses and trucks.

Based on geography, the ADAS market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. In 2024, Asia-Pacific is expected to account for the largest share of the ADAS market. The growth of ADAS in APAC is attributed to the growing automotive manufacturing sector in countries such as Japan, China, India, and South Korea, supportive government regulations, and the rising popularity of Electric Vehicles (EVs).

However, Europe is expected to command the highest CAGR of the global ADAS market. The market growth in the region is attributed to the huge presence of component manufacturers, the growth of the overall automotive sector, and the high demand for sensors for automated vehicle prototypes.

Key Players:

The key players profiled in the global ADAS market study include Continental AG (Germany), Valeo SA (France), Robert Bosch GmbH (Germany), ZF Friedrichshafen AG (Germany), and Aptiv PLC (Ireland), Autoliv, Inc. (Sweden), Denso Corporation (Japan), Garmin Ltd. (U.S.), Infineon Technologies AG (Germany), Magna International Inc. (Canada), Mobileye B.V. (Israel), Huawei Technologies Co., Ltd. (China), Qualcomm Technologies, Inc. (U.S.), Microsoft (U.S.), and NXP Semiconductors N.V. (Netherlands).

Download Sample Report Here @ https://www.meticulousresearch.com/download-sample-report/cp_id=5377

Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

#ADAS#AdvancedDriverAssistanceSystems#AutomotiveTechnology#SensorFusion#AutonomousDriving#VehicleSafety#ADASMarket#RadarSensors#CameraSystems#CollisionAvoidance#LaneDepartureWarning#BlindSpotDetection#AdaptiveCruiseControl#AutomotiveElectronics#DriverAssistance

0 notes

Text

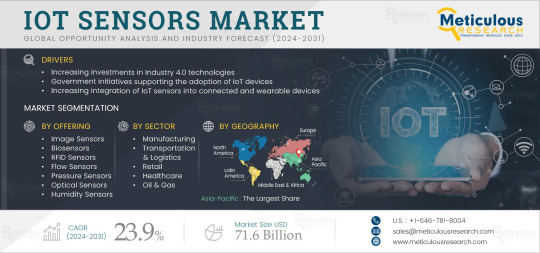

Regional Analysis of the IoT Sensors Market

Meticulous Research®—a leading global market research company, published a research report titled, ‘IoT Sensors Market by Offering (Image Sensors, RFID Sensors, Biosensors, Humidity Sensors, Optical Sensors, Others), Technology (Wired, Wireless), Sector (Manufacturing, Retail, Consumer Electronics, Others), & Geography - Global Forecast to 2031.’

According to this latest publication from Meticulous Research®, in terms of value, the IoT sensors market is projected to reach $71.6 billion by 2031, at a CAGR of 23.9% during the forecast period. Also, in terms of volume, the IoT sensors market is projected to reach 5,93,79,81,126 units by 2031, at a CAGR of 25.2% during the forecast period. The growth of the IoT sensors market is driven by the increasing investments in Industry 4.0 technologies, government initiatives supporting the adoption of IoT devices, and the increasing integration of IoT sensors into connected and wearable devices. However, data security and privacy concerns restrain the growth of this market.

The growing use of IoT sensors for predictive maintenance and the proliferation of smart cities are expected to create growth opportunities for the players operating in the IoT sensors market. However, the high initial investment required for IoT ecosystem implementation is a major challenge for market growth. Additionally, the rising adoption of industrial robots and increasing integration of artificial intelligence into IoT sensors are key trends in the market.

Meticulous Research® has segmented this market based on offering, technology, sector, and geography for efficient analysis. The study also evaluates industry competitors and analyzes the market at the regional and country levels.

Based on offering, the IoT sensors market is segmented into humidity sensors, temperature sensors, proximity sensors, pressure sensors, image sensors, gas sensors, level sensors, accelerometer sensors, flow sensors, biosensors, RFID sensors, optical sensors, and other IoT sensors. In 2024, the image sensors segment is expected to account for the largest share of the IoT sensors market. The large market share of this segment is attributed to the rising demand for image sensors in mobile devices and increasing developments by market players in this market. Image sensors offer several advantages, such as increased sensitivity, reduced dark noise resulting in higher image fidelity, enhanced pixel well depth, and lower power consumption, among other benefits. Moreover, these sensors are utilized in both analog and digital electronic imaging devices, including digital cameras, camera modules, mobile phones, optical mouse devices, medical imaging equipment, night vision devices like thermal imaging systems, as well as applications in radar, sonar, and various other imaging and sensing technologies. Moreover, this segment is also projected to register the highest CAGR during the forecast period.

Based on technology, the IoT sensors market is segmented into wired technology and wireless technology. In 2024, the wireless technology segment is expected to account for the larger share of the IoT sensors market. The large market share of this segment is attributed to the increasing use of wireless sensor networks for various applications and the increasing adoption of IoT devices across various sectors. The demand for wireless IoT sensors is increasing as they require less maintenance and power. Additionally, these sensors can run IoT applications for an extended period without requiring battery replacement or recharging. Moreover, this segment is also projected to register the highest CAGR during the forecast period.

Based on sector, the IoT sensors market is segmented into agriculture, manufacturing, retail, energy & utilities, oil & gas, transportation & logistics, healthcare, consumer electronics, and other sectors. In 2024, the manufacturing segment is expected to account for the largest share of the IoT sensors market. The large market share of this segment is attributed to the supportive government initiatives aimed at promoting the adoption of IoT devices in manufacturing, the rising adoption of smart manufacturing across developing countries, and the increasing number of smart factories. Integrating sensor technologies with IoT devices enables manufacturers to optimize production. IoT technology ensures the security, efficient movement, and precise control of materials and end products throughout the entire manufacturing, distribution, warehousing, and storage process.

However, the healthcare segment is projected to register the highest CAGR during the forecast period. The growth of this segment is attributed to the increasing developments by market players, increasing integration of IoT sensors in medical equipment, and growing demand for IoT devices for patient monitoring applications. The technology benefits multiple healthcare stakeholders and makes telemedicine, patient monitoring, medication management, and imaging more effective. IoT sensors are integrated with medical equipment to collect, share, and analyze data to measure the probable outcome of the preventive treatment.

Based on geography, the IoT sensors market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. In 2024, Asia-Pacific is expected to account for the largest share of the IoT sensors market. The large market share of this segment is attributed to the surging demand for smart sensor-enabled wearable devices, growing technological advancements in industrial sensors, increasing adoption of industrial robots, the advent of Industry 4.0, and increasing adoption of IoT devices in the manufacturing and healthcare industries. The Asia-Pacific region presents several opportunities for adopting IoT sensors due to the presence of a massive manufacturing sector. Japan, China, India, Singapore, and South Korea are investing a significant portion of their GDP into the healthcare and manufacturing sectors, which is driving the market growth. Moreover, this region is also projected to register the highest CAGR during the forecast period.

Key Players

The key players operating in the IoT sensors market are Texas Instruments Incorporated (U.S.), TE Connectivity Ltd. (Switzerland), STMicroelectronics N.V. (Switzerland), OMRON Corporation (Japan), Honeywell International Inc. (U.S.), Murata Manufacturing Co., Ltd. (Japan), Bosch Sensortec GmbH (Germany), Analog Devices, Inc. (U.S.), NXP Semiconductors N.V. (Netherlands), Infineon Technologies AG (Germany), Broadcom Inc. (U.S.), and TDK Corporation (Japan).

Download Sample Report Here @ https://www.meticulousresearch.com/download-sample-report/cp_id=5738

Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

#IoTSensors#SmartSensors#ConnectedDevices#WirelessSensors#SensorTechnology#IndustrialIoT#SmartHomes#AutomotiveSensors#IoTApplications#MarketForecast

0 notes

Text

Meticulous Research®—a leading global market research company, published a research report titled, ‘South East Asia Food Processing Equipment Market by Type (Meat Processing Equipment, Beverage Processing Equipment, Dairy Processing Equipment, Fruit and Vegetable Processing Equipment), Mode of Operation (Semi-Automatic, Automatic), and Geography—Forecast to 2031.’What's Fueling the Growth Engine?

The numbers tell an impressive story. The global food processing equipment market is projected to reach $103.82 billion by 2031, at a CAGR of 5.6% during the forecast period. But what's behind these impressive figures?

Think about it – we're adding nearly 2 billion more people to the planet by 2050. That's a lot more mouths to feed, and traditional farming alone won't cut it. We need smarter, more efficient ways to process food, which means investing in better equipment.

But population growth is just part of the story. Walk through any major city today, and you'll see the real driver: urban lifestyles. More people are living in cities, working longer hours, and relying on processed foods for convenience. Families have less time to cook from scratch, and working professionals want quick, reliable meal solutions.

This shift is particularly dramatic in developing countries. The global consumption of processed foods has seen a significant uptick in recent decades, driven by urbanization, changing family structures, and women entering the workforce in greater numbers. When you combine this with rising disposable incomes, you get a recipe for sustained equipment demand.

Food safety has also become non-negotiable. Today's consumers expect their food to be safe, consistent, and traceable. This means food processors need equipment that can maintain strict hygiene standards while meeting regulatory requirements. It's not just about making food anymore – it's about making it safely and reliably.

The Automation Revolution

Here's where things get really interesting. While the semi-automatic segment is expected to account for the larger share of 60.3% of the global Food Processing Equipment market today, automation is rapidly gaining ground. The automatic segment is projected to register the higher CAGR of 6.4% during the forecast period of 2024–2031.

Why the shift? Automated systems offer something semi-automatic equipment can't match: consistency and safety. Machines don't get tired, don't make mistakes, and don't spread diseases. They can monitor production continuously, track individual batches, and maintain perfect cleaning protocols.

The productivity gains are substantial too. Automated systems can increase output by 25% while handling complex tasks like loading, unloading, and packaging more efficiently than human workers. For food processors dealing with tight margins and growing demand, these advantages are compelling.

But automation isn't just about replacing workers – it's about enabling new capabilities. Modern automated systems can handle multiple product variations, adapt to changing recipes, and integrate with broader supply chain systems. This flexibility has become essential as consumer preferences evolve rapidly.

Why Bakery Equipment Rules the Market

One segment consistently outperforms others: bakery and confectionery equipment. By application, the bakery & confectionery products segment contributed more than 22% of revenue share in 2023 and is predicted to have the largest market share by 2034.

There's something universally appealing about baked goods. Unlike other food categories that might be seasonal or culturally specific, bread, cakes, and confectionery products have consistent demand across all demographics and regions. Whether it's artisanal sourdough in San Francisco or mass-produced cookies in Mumbai, people always want baked goods.

The technical requirements also drive higher equipment values. Baking demands precise temperature control, exact timing, and specialized mixing technologies. These aren't simple machines – they're sophisticated systems that command premium prices and require regular upgrades as technology advances.

Innovation keeps this segment fresh too. Modern bakery processors need equipment that can handle organic ingredients, create gluten-free options, and adapt to health-conscious trends. Each new consumer preference creates opportunities for equipment manufacturers to develop specialized solutions.

How COVID-19 Changed Everything

The pandemic didn't just disrupt the food industry – it fundamentally transformed it. Supply chains broke down, workers got sick, and suddenly everyone realized how vulnerable our food system really was.

The response was swift and decisive: accelerate automation. As one industry expert noted, "Automated equipment does not catch or spread the flu, does not sneeze on the product coming down the packaging line or spread COVID-19." This harsh reality made automation investments essential for maintaining food safety and operational continuity.

But COVID-19 did more than just speed up automation adoption. It forced manufacturers to think differently about flexibility and resilience. Equipment that could quickly switch between products, adapt to new supply chains, and maintain strict hygiene standards became invaluable.

The pandemic also highlighted the importance of contactless technologies and enhanced sanitation capabilities. Equipment manufacturers responded by developing solutions that could provide end-to-end automation while maintaining the highest hygiene standards.

Asia Pacific: The Growth Engine

If you want to understand the future of food processing equipment, look east. Asia-Pacific is expected to account for the largest share of 43.0% of the global food processing equipment market, followed by Europe and North America. The region's market is already substantial – Asia-Pacific's food processing equipment market is estimated to be worth USD 30.38 billion in 2024.

But here's the kicker: this region is projected to register the highest CAGR of 6.1% during the forecast period, making it the fastest-growing market globally. The reasons are compelling: rapid urbanization, growing health awareness, and rising disposable income levels are creating perfect conditions for equipment demand.

Asian consumers are becoming increasingly sophisticated. They want international quality standards but with local flavors and preferences. This creates unique challenges for equipment manufacturers who must develop flexible systems capable of handling diverse ingredients and production methods.

The plant-based food trend is particularly strong in Asia Pacific, where environmental consciousness meets traditional dietary preferences. The rapidly growing plant-based foods market is expected to offer growth opportunities for the players operating in the food processing equipment market, requiring specialized processing capabilities and innovative equipment solutions.

Looking Ahead

The food processing equipment market until 2034 will be shaped by these powerful forces: growing populations, urbanization, automation, safety requirements, and evolving consumer preferences. Success will require understanding regional dynamics, particularly the Asia Pacific growth engine, while addressing universal trends toward automation, food safety, and sustainable processing solutions.

Download Sample Report Here @Download Sample Report Here @ https://www.meticulousresearch.com/download-sample-report/cp_id=4194

Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

0 notes

Text

Opportunities in the 3D Printing Plastics Market

The Future of 3D Printing Plastics: A Journey Through Innovation, Sustainability, and Market Evolution

According to this latest publication from Meticulous Research®, the 3D printing plastics market is projected to reach $7.8 billion by 2032, at a CAGR of 23.2% from 2025 to 2032. The growth of the 3D printing plastics market is primarily driven by the rising demand for additive manufacturing across various industries, the increasing supply of 3D printing plastics, and government initiatives supporting the adoption of 3D printing technologies. However, environmental concerns related to the disposal of plastic products and regulations for the use of specific grades of plastic restrain the growth of this market.

The world of 3D printing plastics is experiencing a remarkable transformation that's reshaping how we think about manufacturing, sustainability, and innovation. As we stand at the crossroads of technological advancement and environmental responsibility, the industry is witnessing unprecedented changes that promise to revolutionize multiple sectors and create entirely new possibilities for businesses and consumers alike.

The Rise of Bioplastics: Nature's Answer to Manufacturing Challenges

Imagine a world where the plastic products we create today could naturally decompose tomorrow, leaving no trace of environmental damage. This vision is becoming reality through the revolutionary advancement of bioplastics in 3D printing applications. These remarkable materials, crafted from renewable resources like corn starch, sugarcane, and even algae, are fundamentally changing how manufacturers approach product development.

The story of bioplastics in 3D printing is one of remarkable growth and acceptance. Research indicates that polylactic acid, commonly known as PLA, is leading this charge and is expected to capture over 33% of the entire 3D printing plastics market by 2025. This dominance isn't accidental – it represents a conscious shift toward materials that offer the same functionality as traditional plastics while significantly reducing our environmental footprint.

What makes bioplastics particularly exciting is their versatility across industries. From creating biodegradable packaging prototypes to manufacturing temporary medical implants that safely dissolve in the human body, these materials are opening doors to applications we never thought possible. The entire 3D printing plastics market is projected to reach an impressive $7.8 billion by 2032, growing at a remarkable rate of 23.2% annually from 2025 to 2032, with bioplastics playing a starring role in this expansion.

.Recycling Revolution: Turning Waste into Wonder

The story of recycled materials in 3D printing reads like a modern-day alchemy tale, where yesterday's waste transforms into tomorrow's innovative products. This shift represents more than just environmental responsibility – it's a complete reimagining of how we approach manufacturing and resource utilization.

When we examine the environmental impact of increased recycled material use in 3D printing, the results are truly inspiring. Every recycled plastic bottle that becomes a prototype, every failed print that gets reprocessed into new filament, represents a victory against the mounting waste crisis. This circular approach to manufacturing is dramatically reducing the demand for virgin materials, which in turn significantly cuts down on energy consumption and carbon emissions associated with traditional plastic production.

AI Integration: Precision Manufacturing Revolution

Artificial Intelligence is revolutionizing 3D printing precision through sophisticated optimization algorithms and predictive analytics. AI systems analyze vast datasets to optimize printing parameters, resulting in improved dimensional accuracy, reduced material waste, and enhanced surface finish quality. Machine learning algorithms continuously learn from printing outcomes, automatically adjusting parameters for optimal results.

The fused deposition modeling (FDM) segment is expected to account for the largest share of the 3D printing plastics market in 2025, with AI integration significantly enhancing its capabilities. AI-powered systems can predict potential printing failures, automatically generate support structures, and optimize layer adhesion, resulting in higher success rates and reduced material consumption.

Advanced AI applications include real-time quality monitoring, where computer vision systems detect defects during printing and make immediate corrections. This technology is particularly valuable in high-precision applications such as medical device manufacturing and aerospace components, where quality standards are paramount.

Sustainable Development: Shaping Tomorrow's Manufacturing Landscape

The intersection of sustainable development and 3D printing regulation is creating a fascinating dynamic that's reshaping entire industries. Governments worldwide are recognizing that the future of manufacturing must balance economic growth with environmental responsibility, leading to innovative policies and regulations that encourage sustainable practices while fostering innovation.

This regulatory evolution is creating both challenges and tremendous opportunities for industry players. Companies are discovering that sustainable practices aren't just good for the environment – they're increasingly becoming essential for staying competitive in the global marketplace. The Asia-Pacific region is leading this charge and is expected to account for over 42% of the 3D printing plastics market in 2025, driven largely by government-led strategies that support sustainable manufacturing adoption.

Healthcare Applications: Where Innovation Meets Human Need

The healthcare sector's embrace of 3D printing is creating some of the most inspiring and impactful applications of this technology. The healthcare segment is projected to experience the highest growth rate during the forecast period, driven by an unprecedented demand for personalized medical devices, biocompatible materials, and custom therapeutic solutions that were simply impossible to create using traditional manufacturing methods.

Consider the profound impact of being able to create a perfectly fitted prosthetic limb, customized to an individual's exact specifications, or a surgical guide that matches a patient's unique anatomy. These aren't futuristic concepts – they're happening today, thanks to advances in 3D printing plastics specifically designed for medical applications.

The development of specialized medical-grade plastics, including resorbable materials for temporary implants and smart polymers for controlled drug delivery, represents just the beginning of what's possible. As our understanding of biocompatibility and material science advances, we can expect to see even more innovative applications that improve patient outcomes and reduce healthcare costs.

The Players Shaping Tomorrow's Industry

The key players operating in the 3D printing plastics market include 3D Systems Corporation (U.S.), Evonik Industries AG (Germany), Arkema (France), SABIC (Saudi Arabia), Stratasys Ltd. (U.S.), Materialise nv (Belgium), CRP TECHNOLOGY S.r.l. (Italy), Formlabs Inc. (U.S.), HP Development Company, L.P. (U.S.), Dassault Systemes (France), Proto Labs, Inc. (U.S.), EOS GmbH (Germany), Avient Corporation (U.S.), Henkel AG & Co. KGaA (Germany), and Huntsman International LLC (U.S.).than ever before.

Looking Toward Tomorrow: A Future Full of Promise

As we look toward the horizon of 3D printing plastics, we see an industry that's being transformed by remarkable innovation across multiple dimensions. The convergence of bioplastics, artificial intelligence, sustainable development, and healthcare applications is creating possibilities that seemed impossible just a few years ago.

The journey of bioplastics from experimental materials to mainstream solutions is reshaping how we think about manufacturing and environmental responsibility. The integration of AI is making precision manufacturing accessible to businesses of all sizes, while healthcare applications are literally saving lives and improving quality of life for patients around the world.

Download Sample Report Here @ https://www.meticulousresearch.com/download-sample-report/cp_id=5950

Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

#3DPrintingPlastics#AdditiveManufacturing#Healthcare3DPrinting#AerospaceApplications#AutomotiveInnovation#PlasticMaterials#3DPrintingTrends#GlobalMarketForecast#ManufacturingTechnology#Polymer3DPrinting

0 notes

Text

Autoinjectors Market Share and Competitive Landscape

Autoinjector Market Dynamics: Innovation, Regulation, and Growth Trends

The autoinjector industry stands at the forefront of medical device innovation, experiencing remarkable transformation driven by technological breakthroughs, evolving regulatory landscapes, and shifting patient needs. Industry analysts project the global autoinjector market will reach $3.76 billion by 2032, representing substantial growth at a CAGR of 8.3% from the current valuation of $2.16 billion in 2025. This expansion reflects the critical role these devices play in modern healthcare delivery.

How Bluetooth and Smart Technology Are Revolutionizing Autoinjector Usability

Modern autoinjectors have evolved far beyond simple injection devices, incorporating sophisticated connectivity features that fundamentally change how patients interact with their medications. Smart autoinjectors now leverage Wi-Fi and Bluetooth connectivity alongside dedicated mobile applications to create comprehensive healthcare ecosystems. These connected devices enable real-time data collection, allowing patients to track injection histories, receive timely medication reminders, and seamlessly share treatment information with their healthcare providers.

The integration of digital health platforms with autoinjector technology represents a paradigm shift in patient care management. Healthcare providers can now monitor patient adherence remotely, adjust treatment protocols based on real-time data, and intervene proactively when adherence issues arise. This technological convergence has positioned smart autoinjectors as the fastest-growing segment, with analysts projecting a CAGR of 9.7% through 2032.

Companies like Phillips-Medisize have pioneered this transformation with innovations such as the Aria Smart Autoinjector platform, specifically engineered to deliver differentiation and sustainability in digital drug delivery. These advanced devices offer personalized dose customization, real-time injection guidance, and comprehensive feedback systems including audible confirmations and visual indicators that ensure patients complete their injections correctly.

Beyond connectivity, modern autoinjectors incorporate sophisticated safety mechanisms that address longstanding concerns about self-injection. Needle-retraction systems automatically secure needles post-injection, virtually eliminating needlestick injuries. Meanwhile, precision dosing mechanisms ensure consistent medication delivery, while ergonomic designs accommodate patients with varying levels of manual dexterity, particularly benefiting elderly users who may struggle with traditional injection methods.

Regulatory Frameworks Shaping Market Expansion

Regulatory agencies worldwide have recognized the transformative potential of autoinjector technology, implementing policies that accelerate market access while maintaining stringent safety standards. The regulatory emphasis on home healthcare solutions has prompted agencies to streamline approval pathways for self-administration devices, acknowledging their potential to reduce healthcare costs while improving patient outcomes.

Recent regulatory approvals demonstrate this supportive environment. Taisho Pharmaceutical's Nanozora 30mg Autoinjector, approved in January 2025, exemplifies how regulatory bodies are embracing single-use autoinjector innovations that address safety concerns while preventing needle-related accidents. These approvals reflect regulatory recognition that autoinjectors can maintain clinical efficacy while empowering patients to manage their treatments independently.

Chronic Disease Trends Driving Design Innovation

The escalating prevalence of chronic diseases is fundamentally reshaping autoinjector design philosophy. Diabetes represents the most significant driver, with cases projected to surge from 537 million globally in 2021 to 783 million by 2045 according to the International Diabetes Federation. This dramatic increase has positioned diabetes as the largest application segment for autoinjectors, demanding devices optimized for frequent, long-term use.

The aging population presents both challenges and opportunities for device manufacturers. The Joint Center for Housing Studies at Harvard University projects that by 2035, one in every three American households will be headed by individuals aged 65 or older. This demographic shift has prompted manufacturers to reimagine device interfaces, prioritizing larger grip surfaces, simplified activation mechanisms, and enhanced visual indicators that accommodate age-related changes in vision and motor skills.

Device designers are also addressing the psychological barriers to self-injection. Needle phobia affects significant portions of the patient population, leading companies to develop innovative solutions that minimize anxiety while ensuring reliable medication delivery. The growing emphasis on home healthcare has accelerated demand for devices that enable patients to actively participate in their treatment while reducing the burden on healthcare facilities and providers.

Regional Market Dynamics: North America Leading, Asia-Pacific Accelerating

North America maintains its position as the global leader in autoinjector adoption, capturing 36.5% of the market share in 2025. This dominance stems from several factors: the presence of major manufacturers including Halozyme, Inc. and Becton, Dickinson and Company, sophisticated healthcare infrastructure, and high patient acceptance of self-administration technologies. The region's established reimbursement systems and regulatory framework further support market growth.

European markets demonstrate steady growth characterized by strong regulatory support for innovative medical devices and increasing patient awareness of autoinjector benefits. The region's emphasis on patient-centered care and established healthcare systems create favorable conditions for autoinjector adoption across multiple therapeutic areas. European manufacturers like Ypsomed AG and SHL Medical AG have established themselves as global leaders through strategic partnerships and continuous technological innovation.

Biologics Revolution and Its Impact on Device Development

The increasing adoption of biologic therapies has created new imperatives for autoinjector development. Biologics often require specialized storage conditions, precise dosing protocols, and specific delivery methods that demand advanced device capabilities. The recent partnership between FUJIFILM Diosynth Biotechnologies U.S.A., Inc. and SHL Medical AG in January 2025 exemplifies industry efforts to meet the growing demand for biologics-compatible autoinjectors.

Biologic medications frequently require subcutaneous administration, aligning with current market trends where subcutaneous delivery dominates the autoinjector market. Companies like Jabil have responded with innovations such as the Qfinity modular solution launched in May 2022, which addresses the need for cost-effective delivery of expensive biologic therapies while maintaining rigorous safety and efficacy standards.

Industry Leaders Driving Innovation and Market Expansion

The key players operating in the autoinjectors market are Becton, Dickinson and Company (U.S.), Ypsomed AG (Switzerland), SHL Medical (Switzerland), Recipharm AB (Sweden), Owen Mumford Limited (U.K), Halozyme, Inc. (U.S.), AstraZeneca (U.K.), Teva Pharmaceutical Industries Ltd. (Israel), Solteam Incorporation Co., Ltd. (China), Gerresheimer AG (Germany), West Pharmaceutical Services, Inc. (U.S.), Bayer AG (Germany), and Union Medico ApS. (Denmark).

The Future of Home Healthcare and Self-Administration

The home care segment represents the largest and fastest-growing application for autoinjectors, commanding 57.6% of the market share in 2025. This growth reflects patients' increasing preference for self-administration and the convenience offered by advanced autoinjector technologies. The trend toward home healthcare has accelerated significantly, driven by cost considerations, patient preferences, and the proven safety and efficacy of modern autoinjector systems.

Download Sample Report Here @ https://www.meticulousresearch.com/download-sample-report/cp_id=5899

Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

#Autoinjectors#DrugDelivery#HealthcareInnovation#SelfAdministration#Biopharmaceuticals#ChronicDiseases#MedicalDevices#AutoInjection#MarketResearch#MeticulousResearch

0 notes

Text

#Hemostats#SurgicalDevices#MinimallyInvasiveSurgery#HealthcareMarket#WoundCare#MedicalDevices#GlobalHemostatsMarket#MarketForecast#SurgicalInnovation#HemostasisSolutions

0 notes

Text

#FleetManagement#TransportationTechnology#Telematics#VehicleTracking#LogisticsSolutions#SmartTransportation#AIinFleet#MobilitySolutions#FleetAnalytics#ConnectedVehicles

0 notes

Text

Savory Ingredients Market to Reach $11.3 Billion by 2031

Meticulous Research®—a leading global market research company, published a research report titled ‘Savory Ingredients Market—Global Opportunity Analysis and Industry Forecast (2025-2032)’. According to this latest publication from Meticulous Research®, the savory ingredients market is expected to reach $13.38 billion by 2032, at a CAGR of 5.7% from 2025 to 2032.

The increasing demand for convenience foods, along with a shift towards wholesome and healthy alternatives, is driving growth in the savory ingredients market. Additionally, the rising demand for naturally sourced savory ingredients and a surge in end-use applications are contributing to this growth. However, high raw material costs and stringent regulations are constraining market growth.

In addition, emerging economies in Asia-Pacific, Latin America, and the Middle East & Africa provide potential growth opportunities for market players. The market faces substantial challenges, including the complex sourcing of natural ingredients. Moreover, the increasing demand for functional ingredients and clean labels are a prominent trend in the savory ingredients market.

Key Players

The savory ingredients market is characterized by a moderately competitive scenario due to the presence of many large- and small-sized global, regional, and local players. The key players operating in the savory ingredients market are Ajinomoto Co., Inc. (Japan), AngelYeast Co., Ltd. (China), Kerry Group plc (Ireland), Vedan International (Holdings) Limited (Hong Kong), Sensient Technologies Corporation (U.S.), Tate & Lyle PLC (U.K.), Archer-Daniels-Midland Company (U.S.), DSM-Firmenich AG (Switzerland), Givaudan SA (Switzerland), Associated British Foods plc (U.K.), Lesaffre (France), Synergy Flavors, Inc. (U.S.), Ohly GmbH (Germany), and SPAC Starch Products (India) Private Limited (India).

The savory ingredients market is segmented based on ingredient type, source, form, and application. The report also evaluates industry competitors and analyzes the savory ingredients market at the regional and country levels.

Among the ingredient types studied in this report, the monosodium glutamate (MSG) segment is anticipated to hold the dominant position, with a share of 55.4% of the market in 2025. This segment's substantial market share is primarily driven by its capacity to enhance flavor, making it a widely used additive in processed and packaged foods. The growing demand for sauces, cheeses, dairy and meat products, baked goods, and instant noodles has notably increased the adoption of MSG. As urbanization continues to rise and consumers seek more flavorful and convenient food options, the reliance on MSG as a cost-effective flavor enhancer is expected to further boost the growth of this segment.

Among the sources studied in this report, the synthetic segment is anticipated to hold the dominant position, with a large share of the savory ingredients market in 2025. This segment's substantial market share is attributed to its enhanced stability, extended shelf life, and lower cost compared to natural savory ingredients. Additionally, synthetic savory ingredients are produced in a consistent and controlled manner, allowing manufacturers to meet high demand without facing the supply and price fluctuations that often affect natural options. This cost-effective advantage positions synthetic savory ingredients as an economical choice for food manufacturers.

Among the forms studied in this report, the powder segment is anticipated to hold the dominant position, with a large share of the savory ingredients market in 2025. The substantial market share of this segment is attributed to its versatility and convenience. These ingredients can be easily integrated into a variety of food and beverage products. Their powdered form allows for uniform distribution, ensuring consistent flavor in every application. Moreover, powdered savory ingredients offer a longer shelf life compared to liquid alternatives, minimizing the risk of spoilage and waste. This results in a cost-effective solution for both manufacturers and consumers, as they can be stored for extended periods without compromising flavor intensity.

Among the applications studied in this report, the food & beverages segment is anticipated to hold the dominant position, with a large share of the savory ingredients market in 2025. The substantial market share of this segment is primarily attributed to evolving consumer lifestyles and a growing preference for convenience foods driven by busy schedules and increased disposable incomes. The expansion of international cuisines, including Asian, Mediterranean, and Latin American dishes, is fostering the use of savory ingredients that enhance flavor complexity and authenticity. Furthermore, consumers are increasingly attracted to umami-rich foods, which offer a savory and satisfying taste experience, further expected to boost demand for savory ingredients.

Geographic Review

This research report analyzes major geographies and provides a comprehensive analysis of North America (U.S., Canada), Europe (Germany, France, U.K., Italy, Spain, Poland, Netherlands, Belgium, and Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Australia, Indonesia, Malaysia, Thailand, Singapore, and Rest of Asia-Pacific), Latin America (Brazil, Mexico, Argentina, and Rest of Latin America), and the Middle East & Africa (Saudi Arabia, South Africa, UAE, and Rest of Middle East & Africa).

Among the geographies studied in this report, Asia-Pacific is anticipated to hold the dominant position, with a share of 62.9% of the market in 2025, followed by North America, Europe, Latin America, and the Middle East & Africa. Asia-Pacific's savory ingredients market is estimated to be worth USD 5,699.2 million in 2025. The substantial market share in this region is attributed to various factors, including accelerated urbanization, growing disposable incomes, the expansion of the food processing sector, the rising popularity of international cuisines, the adoption of Western dietary habits, and an increase in the consumption of savory snacks and ready-to-eat meals.

Download Sample Report Here @ https://www.meticulousresearch.com/download-sample-report/cp_id=6031

Key Questions Answered in the Report:

What is the value of revenue generated by the sale of savory ingredients?

At what rate is the global demand for savory ingredients projected to grow for the next five to seven years?

What is the historical market size and growth rate for the savory ingredients market?

What are the major factors impacting the growth of this market at global and regional levels?

What are the major opportunities for existing players and new entrants in the market?

Which ingredient type, source, form, and application segments create major traction for the manufacturers in this market?

What are the key geographical trends in this market? Which regions/countries are expected to offer significant growth opportunities for the manufacturers operating in the savory ingredients market?

Who are the major players in the savory ingredients market? What are their specific product offerings in this market?

What recent developments have taken place in the savory ingredients market? What impact have these strategic developments created on the market?

Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

0 notes

Text

The Natural Flavors Market

Meticulous Research®—a leading global market research company, published a research report titled ‘Natural Flavors Market—Global Opportunity Analysis and Industry Forecast (2025-2032)’. According to this latest publication, the natural flavors market is expected to reach $12.05 billion by 2032, at a CAGR of 7.2% from 2025 to 2032. The natural flavors market is experiencing growth driven by the rising demand for clean labels and natural products, increased awareness of health and wellness, and robust expansion in the food and beverage industry. However, the high cost of natural flavors constrains market growth. Additionally, emerging economies in Asia, Latin America, and the Middle East & Africa and the incorporation of flavors in functional foods, present significant opportunities for market participants. However, the market also faces considerable challenges related to compliance with quality and regulatory standards. Furthermore, a rising preference for natural ingredients and the adoption of advanced extraction techniques are prominent trends shaping the natural flavors market. Key Players: The natural flavors market is characterized by a moderately competitive scenario due to the presence of many large- and small-sized global, regional, and local players. The key players operating in the natural flavors market are International Flavors & Fragrances Inc. (U.S.), DSM-Firmenich AG (Switzerland), Givaudan SA (Switzerland), Symrise AG (Germany), Sensient Technologies Corporation (U.S.), Corbion N.V. (Netherlands), Tate & Lyle PLC (U.K.), Archer-Daniels-Midland Company (U.S.), Kerry Group plc (Ireland), Takasago International Corporation (Japan), Robertet Group (France), Huabao International Holdings Limited (Hong Kong), MANE Group (France), Döhler GmbH (Germany), and Axxence Aromatic GmbH (Germany). The natural flavors market is segmented based on type, source, technology, form, and application. The report also evaluates industry competitors and analyzes the natural flavors market at the regional and country levels. Among the types studied in this report, the essential oils segment is anticipated to hold the dominant position, with a share of 69.8% of the market in 2025. The substantial market share of this segment is attributed to the versatile application of these products as aromatic and flavoring agents across various sectors, including food and beverage, healthcare, and wellness industries. Furthermore, essential oils have experienced robust demand as a key raw material in the personal care market, driven by their recognized anti-cancer, anti-depression, antioxidant, and weight loss benefits. Among the sources studied in this report, the fruits & nuts segment is anticipated to hold the dominant position, with a large share of the natural flavors market in 2025. The substantial market share of this segment is driven by the growing demand for plant-based and functional foods, which has intensified the use of natural flavors derived from fruits and nuts. Fruits deliver refreshing, fruity notes that attract consumers seeking healthier options, while nuts provide rich, earthy flavors that enhance indulgent and wholesome product formulations. Among the technologies studied in this report, the extraction segment is anticipated to hold the dominant position, with a large share of the natural flavors market in 2025. The substantial market share of this segment is attributed to its benefits, including enhanced extraction yields, reduced extraction times, lower operational costs, efficient heating, and expedited energy transfer. Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

0 notes

Text

0 notes

Text

freeze Drying Equipment Industry Analysis

Meticulous Research®—a leading global market research company, published a research report titled ‘Freeze Drying Equipment Market—Global Opportunity Analysis and Industry Forecast (2025-2032)’. According to this latest publication from Meticulous Research®, the freeze drying equipment market is projected to reach $8.4 billion by 2032, at a CAGR of 7.9% from 2025–2032.The expanding usage of the lyophilization process for food preservation, developments in automation within the lyophilization procedure, and the rapid expansion of the cosmetics and personal care products sector are all important drivers of the freeze drying equipment market.However, market expansion is hampered by high capital costs and tight regulatory compliance standards. Furthermore, rising demand for lyophilized products in the pharmaceutical industry, as well as increased investment in R&D laboratories, provide substantial prospects for market competitors. However, the market confronts hurdles such as complicated operational processes and competition from other drying technologies. Furthermore, important technical advancements in the freeze drying equipment market include compact and portable freeze drying units, as well as customized freeze drying solutions.Key Players:The freeze drying equipment market is characterized by a moderately competitive scenario due to the presence of many large- and small-sized global, regional, and local players. The key players operating in the freeze drying equipment market are GEA Group Aktiengesellschaft (Germany), Tofflon Science and Technology Co., Ltd (China), Labconco Corporation (U.S.), Azbil Corporation (Japan), Millrock Technology, Inc. (U.S.), Cuddon Freeze Dry (New Zealand), HOF Sonderanlagenbau GmbH (Germany), I.M.A. Industria Macchine Automatiche S.p.A. (Italy), ZIRBUS technology GmbH (Germany), MechaTech Systems Ltd (U.K.), BÜCHI Labortechnik AG (Switzerland), OPTIMA packaging group GmbH (Germany), Scala Scientific B.V. (Netherlands), Martin Christ Gefriertrocknungsanlagen GmbH (Germany), and Biopharma Process Systems Ltd. (U.K.)..Download Sample Report Here @ https://www.meticulousresearch.com/download-sample-report/cp_id=6033Contact Us:Meticulous Research®Email- [email protected] Sales- +1-646-781-8004Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

#FreezeDryingEquipment#Lyophilization#FoodPreservation#PharmaceuticalProcessing#Biotechnology#CosmeticsIndustry#Automation#MarketForecast#IndustrialEquipment#GlobalMarketTrends

0 notes

Text

Warehouse Robotics Market Analysis

Meticulous Research®, a leading global market research company, published a report titled ‘Warehouse Robotics Market—Global Opportunity Analysis and Industry Forecast (2025-2032)’. According to this latest publication, the warehouse robotics market is expected to reach $15.1 billion by 2032, at a CAGR of 14.4% from 2025 to 2032.

The warehouse robotics market is expanding primarily due to a greater emphasis on optimizing warehouse operations for faster product delivery, the increased use of autonomous mobile robots (AMRs), and the growing popularity of e-commerce shopping platforms. However, the market's growth may be limited by the high expenses associated with warehouse setup and infrastructure development. At the same time, major breakthroughs in robotics, artificial intelligence (AI), and machine learning technologies are projected to open up new growth potential for enterprises in this field. Nonetheless, the security threats associated with linked autonomous robots remain a significant challenge that may impede market expansion.

This market is divided into product types, functions, payload capacity, and end users. It also covers competitive analyses at the regional and national levels. Autonomous mobile robots are expected to be the most popular product category in 2025, accounting for more than 29% of the market. This is due to rising demand for warehouse automation, increasing expansion in the e-commerce sector, and the need for efficient AMRs to increase productivity. The move for customized AMRs built to handle fragile or specific sorts of commodities reinforces this segment's leadership.

Geographically, the Asia-Pacific region is expected to dominate the warehouse robots market with a 52.7% share by 2025. This region is home to major robotics manufacturers such as Daifuku, FANUC, Hikrobot, and Omron, and their presence helps to strengthen the region's market position significantly. Furthermore, the region's growth is driven by a thriving e-commerce industry, a focus on operational efficiency, and the usage of robotics in industries such as semiconductors, electronics, and automobiles.

Key Players

Some of the major players studied in this report are Daifuku Co., Ltd. (Japan), KUKA AG (Germany), ABB Ltd. (Switzerland), FUNUC Corporation (Japan), Toyota Material Handling India Pvt. Ltd.(India), Omron Corporation (Japan), Honeywell International Inc. (U.S.), Yaskawa Electric Corporation (Japan), Onward Robotics (U.S.), Zebra Technologies Corporation (U.S.), Hikrobot Co., Ltd. (China), SSI SCHÄFER - Fritz Schäfer GmbH (Germany), Onward Robotics (U.S.), TGW Logistics Group (Austria), and Addverb Technologies Limited. (India).

Download Sample Report Here @ https://www.meticulousresearch.com/download-sample-report/cp_id=6027

Key Questions Answered in the Report-

What is the value of revenue generated by the sale of warehouse robotics?

At what rate is the global demand for warehouse robotics projected to grow for the next five to seven years?

What is the historical market size and growth rate for the warehouse robotics market?

What are the major factors impacting the growth of this market at global and regional levels?

What are the major opportunities for existing players and new entrants in the market?

Which product type, function, payload capacity, and end user segments create major traction in this market?

What are the key geographical trends in this market? Which regions/countries are expected to offer significant growth opportunities for the manufacturers operating in the warehouse

Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

0 notes

Text

Meticulous Research®—a leading global market research company, published a research report titled, ‘AI Chatbots Market - Global Opportunity Analysis and Industry Forecast (2025-2032)’. According to this latest publication, the AI chatbots market is expected to reach $22.6 billion by 2032, at a CAGR of 27.8% from 2025 to 2032.

The AI chatbots market is expanding rapidly, owing to a number of key factors, including increased adoption in the IT and telecom sectors, a strong emphasis on improving self-service operations, the increasing use of generative models in AI chatbots, and an increased demand for 24/7 customer support. However, its expansion is hampered by worries about data privacy and security. Despite these limitations, there are significant potential for market participants, such as increased demand for corporate process automation, AI chatbot integration with smart devices, and growing usage of AI chatbots in the retail and e-commerce sectors.

Nonetheless, the market confronts significant hurdles, including misconceptions and a lack of awareness of AI chatbot solutions. Furthermore, notable trends affecting the AI chatbots market include the growing usage of voice-enabled chatbots, the increased use of AI chatbots for customer interactions, and the improved integration of chatbots with natural language processing (NLP) technologies.

Key Players:

The AI chatbots market is characterized by a moderately competitive scenario due to the presence of many large and small-sized global, regional, and local players. The key players operating in the AI chatbots market are OpenAI OpCo, LLC (U.S.), Microsoft Corporation (U.S.), Google LLC (U.S.), Amazon Web Services, Inc. (U.S.), NVIDIA Corporation (U.S.), International Business Machines Corporation (U.S.), Perplexity AI, Inc. (U.S.), Zoho Corporation Pvt. Ltd. (U.S.), GET JENNY OY (Finland), Acuvate (U.K.), Freshworks Inc. (U.S.), Jasper AI, Inc. (U.S.), Anthropic PBC (U.S.), Writesonic, Inc. (U.S.), Next IT & Systems LLC (UAE).

The AI chatbots market is segmented by offering, organization size, deployment mode, medium, and end-use industry. The report also evaluates industry competitors and analyzes the market at the regional and country levels.

The platforms sector is expected to be the most prevalent among the products analyzed in this report, accounting for 73% of the market in 2025. The IT and telecommunications sector's dominance is attributed to the increased use of AI chatbot platforms to respond to various customer inquiries, the high demand for multilingual support to engage customers in their native languages, and the ability to reduce operational costs by managing multiple users at once.

Among the organization sizes evaluated, the big enterprises segment is expected to dominate, accounting for 64% of the market in 2025. This dominance is motivated by the increased requirement to manage a huge amount of questions and complaints, a significant demand for avoiding long wait times in

The cloud-based deployment mode is predicted to dominate the market, accounting for 57% in 2025. This supremacy is bolstered by the widespread adoption of cloud-based AI chatbots, which enable 24-hour customer service from any location. The widespread use of these chatbots in the retail and e-commerce sectors, the increasing demand for omnichannel service, and their data collection, analysis, and scalability capabilities all contribute to this rise.

Among the channels evaluated, the internet sector is expected to be the most dominant, accounting for 63% of the market in 2025. The increasing adoption of website-based AI chatbots, which provide an excellent online interaction model, strengthens this dominance. Additionally, the expanding use of AI chatbots on websites to boost customer engagement across digital channels, as well as the emphasis on improving organizations' digital presence, contribute to this trend. Among the end-use sectors evaluated, the IT and telecoms segment is predicted to dominate, accounting for 31% of the market by 2025. This is due to the increasing use of AI chatbots to handle large numbers of requests, enhance operational efficiency, cut costs, and boost customer happiness. Furthermore, there is an increasing need to evaluate customer data to improve

Geographical Review: This research report examines major geographies: North America (U.S., Canada), Europe (Germany, U.K., France, Italy, Spain, Switzerland, Netherlands, Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Singapore, Australia & New Zealand, Indonesia, Rest of Asia-Pacific), Latin America (Brazil, Mexico, Rest of Latin America), and the Middle East & Africa (UAE, Israel, Rest of Middle East & Africa). Among these regions, North America is expected to dominate, accounting for 39% of the market in 2025. The region's leadership is bolstered by the presence of top companies that provide AI chatbot solutions, rising demand for AI-driven customer support services, and a focus on strengthening customer engagement methods by aligning with consumer preferences.

Download Sample Report Here @ https://www.meticulousresearch.com/download-sample-report/cp_id=6026

Key questions answered in the report-

Which are the high-growth market segments based on offering, organization size, deployment mode, medium, and end use industry?

What was the historical market for AI chatbots?

What are the market forecasts and estimates for the period 2025–2032?

What are the major drivers, restraints, and opportunities in the AI chatbots market?

Who are the major players, and what shares do they hold in the AI chatbots market?

How is the competitive landscape in the AI chatbots market?

What are the recent developments in the AI chatbots market?

What are the different strategies adopted by the major players in the AI chatbots market?

What are the key geographic trends, and which are the high-growth countries?

Who are the local emerging players in the AI chatbots market, and how do they compete with the other players?

Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

0 notes

Text

Meticulous Research®—a leading global market research company, published a research report titled, ‘AI Chatbots Market - Global Opportunity Analysis and Industry Forecast (2025-2032)’. According to this latest publication, the AI chatbots market is expected to reach $22.6 billion by 2032, at a CAGR of 27.8% from 2025 to 2032.

The AI chatbots market is expanding rapidly, owing to a number of key factors, including increased adoption in the IT and telecom sectors, a strong emphasis on improving self-service operations, the increasing use of generative models in AI chatbots, and an increased demand for 24/7 customer support. However, its expansion is hampered by worries about data privacy and security. Despite these limitations, there are significant potential for market participants, such as increased demand for corporate process automation, AI chatbot integration with smart devices, and growing usage of AI chatbots in the retail and e-commerce sectors.

Nonetheless, the market confronts significant hurdles, including misconceptions and a lack of awareness of AI chatbot solutions. Furthermore, notable trends affecting the AI chatbots market include the growing usage of voice-enabled chatbots, the increased use of AI chatbots for customer interactions, and the improved integration of chatbots with natural language processing (NLP) technologies.

Key Players:

The AI chatbots market is characterized by a moderately competitive scenario due to the presence of many large and small-sized global, regional, and local players. The key players operating in the AI chatbots market are OpenAI OpCo, LLC (U.S.), Microsoft Corporation (U.S.), Google LLC (U.S.), Amazon Web Services, Inc. (U.S.), NVIDIA Corporation (U.S.), International Business Machines Corporation (U.S.), Perplexity AI, Inc. (U.S.), Zoho Corporation Pvt. Ltd. (U.S.), GET JENNY OY (Finland), Acuvate (U.K.), Freshworks Inc. (U.S.), Jasper AI, Inc. (U.S.), Anthropic PBC (U.S.), Writesonic, Inc. (U.S.), Next IT & Systems LLC (UAE).

The AI chatbots market is segmented by offering, organization size, deployment mode, medium, and end-use industry. The report also evaluates industry competitors and analyzes the market at the regional and country levels.

The platforms sector is expected to be the most prevalent among the products analyzed in this report, accounting for 73% of the market in 2025. The IT and telecommunications sector's dominance is attributed to the increased use of AI chatbot platforms to respond to various customer inquiries, the high demand for multilingual support to engage customers in their native languages, and the ability to reduce operational costs by managing multiple users at once.

Among the organization sizes evaluated, the big enterprises segment is expected to dominate, accounting for 64% of the market in 2025. This dominance is motivated by the increased requirement to manage a huge amount of questions and complaints, a significant demand for avoiding long wait times in

The cloud-based deployment mode is predicted to dominate the market, accounting for 57% in 2025. This supremacy is bolstered by the widespread adoption of cloud-based AI chatbots, which enable 24-hour customer service from any location. The widespread use of these chatbots in the retail and e-commerce sectors, the increasing demand for omnichannel service, and their data collection, analysis, and scalability capabilities all contribute to this rise.

Among the channels evaluated, the internet sector is expected to be the most dominant, accounting for 63% of the market in 2025. The increasing adoption of website-based AI chatbots, which provide an excellent online interaction model, strengthens this dominance. Additionally, the expanding use of AI chatbots on websites to boost customer engagement across digital channels, as well as the emphasis on improving organizations' digital presence, contribute to this trend. Among the end-use sectors evaluated, the IT and telecoms segment is predicted to dominate, accounting for 31% of the market by 2025. This is due to the increasing use of AI chatbots to handle large numbers of requests, enhance operational efficiency, cut costs, and boost customer happiness. Furthermore, there is an increasing need to evaluate customer data to improve

Geographical Review: This research report examines major geographies: North America (U.S., Canada), Europe (Germany, U.K., France, Italy, Spain, Switzerland, Netherlands, Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Singapore, Australia & New Zealand, Indonesia, Rest of Asia-Pacific), Latin America (Brazil, Mexico, Rest of Latin America), and the Middle East & Africa (UAE, Israel, Rest of Middle East & Africa). Among these regions, North America is expected to dominate, accounting for 39% of the market in 2025. The region's leadership is bolstered by the presence of top companies that provide AI chatbot solutions, rising demand for AI-driven customer support services, and a focus on strengthening customer engagement methods by aligning with consumer preferences.

Download Sample Report Here @ https://www.meticulousresearch.com/download-sample-report/cp_id=6026

Key questions answered in the report-

Which are the high-growth market segments based on offering, organization size, deployment mode, medium, and end use industry?

What was the historical market for AI chatbots?

What are the market forecasts and estimates for the period 2025–2032?

What are the major drivers, restraints, and opportunities in the AI chatbots market?

Who are the major players, and what shares do they hold in the AI chatbots market?

How is the competitive landscape in the AI chatbots market?

What are the recent developments in the AI chatbots market?

What are the different strategies adopted by the major players in the AI chatbots market?

What are the key geographic trends, and which are the high-growth countries?

Who are the local emerging players in the AI chatbots market, and how do they compete with the other players?

Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

0 notes

Text

Global Kombucha Market Forecast

Meticulous Research®, a leading global market research company, published a report titled ‘Kombucha Market—Global Opportunity Analysis and Industry Forecast (2025-2032)’. According to this latest publication, the kombucha market is expected to reach $12.36 billion by 2032, at a CAGR of 19.9% from 2025 to 2032.