#Automotive Battery Management System Market Challenges

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Average visit duration of Tumblr.com is 10 mins and 25 secs.

Text

Automotive Battery Management System Market Set for Explosive Growth

Market Research Forecast released a new market study on Global Automotive Battery Management System Market Research report which presents a complete assessment of the Market and contains a future trend, current growth factors, attentive opinions, facts, and industry validated market data. The research study provides estimates for Global Automotive Battery Management System Forecast till 2032. The Automotive Battery Management System Marketsize was valued at USD 8.25 USD Billion in 2023 and is projected to reach USD 23.56 USD Billion by 2032, exhibiting a CAGR of 16.17 % during the forecast period. Key Players included in the Research Coverage of Automotive Battery Management System Market are: Robert Bosch GmbH (Germany), Continental AG (Germany), Toshiba Corporation (Japan), Intel Corporation (U.S.), NXP Semiconductors NV (Netherlands), Analog Devices, Inc. (U.S.), Denso Corporation (Japan), Johnson Matthey, Inc. (U.K.), LG Chem, Ltd. (South Korea), Midtronics, Inc. (U.S.) What's Trending in Market: Rising Adoption of Automation in Manufacturing to Drive Market Growth Market Growth Drivers: Increasing Demand for Forged Products in Power, Agriculture, Aerospace, and Defense to Drive Industry Expansion The Global Automotive Battery Management System Market segments and Market Data Break Down Propulsion Type: BEV, PHEV, and HEV","Vehicle Type: Passenger Cars and Commercial Vehicles GET FREE SAMPLE PDF ON Automotive Battery Management System MARKET To comprehend Global Automotive Battery Management System market dynamics in the world mainly, the worldwide Automotive Battery Management System market is analyzed across major global regions. MR Forecast also provides customized specific regional and country-level reports for the following areas.

• North America: United States, Canada, and Mexico. • South & Central America: Argentina, Chile, Colombia and Brazil. • Middle East & Africa: Saudi Arabia, United Arab Emirates, Israel, Turkey, Egypt and South Africa. • Europe: United Kingdom, France, Italy, Germany, Spain, Belgium, Netherlands and Russia. • Asia-Pacific: India, China, Japan, South Korea, Indonesia, Malaysia, Singapore, and Australia.

Extracts from Table of Contents Automotive Battery Management System Market Research Report Chapter 1 Automotive Battery Management System Market Overview Chapter 2 Global Economic Impact on Industry Chapter 3 Global Market Competition by Manufacturers Chapter 4 Global Revenue (Value, Volume*) by Region Chapter 5 Global Supplies (Production), Consumption, Export, Import by Regions Chapter 6 Global Revenue (Value, Volume*), Price* Trend by Type Chapter 7 Global Market Analysis by Application ………………….continued More Reports:

https://marketresearchforecast.com/reports/automotive-usage-based-insurance-market-2982 For More Information Please Connect MR ForecastContact US: Craig Francis (PR & Marketing Manager) Market Research Forecast Unit No. 429, Parsonage Road Edison, NJ New Jersey USA – 08837 Phone: (+1 201 565 3262, +44 161 818 8166)[email protected]

#Global Automotive Battery Management System Market#Automotive Battery Management System Market Demand#Automotive Battery Management System Market Trends#Automotive Battery Management System Market Analysis#Automotive Battery Management System Market Growth#Automotive Battery Management System Market Share#Automotive Battery Management System Market Forecast#Automotive Battery Management System Market Challenges

0 notes

Text

Printed Circuit Board Market Future Trends: Emerging Technologies and Growth Opportunities Driving Innovation

The printed circuit board market is witnessing significant transformation as innovation and technological advancements propel its growth. PCBs, the backbone of modern electronic devices, continue to evolve in response to emerging industry needs, consumer demands, and new applications. Understanding the future trends shaping the PCB market is essential for manufacturers, investors, and technology enthusiasts seeking to capitalize on opportunities and anticipate challenges.

One of the foremost trends in the PCB market is the increasing demand for miniaturization. As electronic devices become more compact and multifunctional, the need for smaller, lighter, and more efficient PCBs has intensified. This trend is especially prominent in sectors like consumer electronics, healthcare, and automotive, where space constraints and performance requirements drive innovation. Flexible PCBs and rigid-flex boards are gaining popularity as they allow intricate designs that fit into compact devices without compromising functionality.

Advanced materials are another crucial factor shaping the PCB market’s future. The traditional use of fiberglass and epoxy resins is gradually being supplemented or replaced by high-performance substrates such as polyimide, ceramic, and Teflon. These materials offer superior thermal stability, electrical performance, and mechanical strength, which are critical for high-frequency and high-speed applications. This shift supports the growing demands of 5G technology, aerospace, and military electronics where reliability under extreme conditions is vital.

The rise of 5G technology is a major catalyst driving the evolution of PCBs. The implementation of 5G networks requires PCBs that can handle high-frequency signals with minimal interference and signal loss. This has led to innovations in high-density interconnect (HDI) PCBs, which allow more components to be packed into a smaller area with enhanced electrical performance. The demand for HDI PCBs is expected to surge as 5G infrastructure expands globally, impacting telecommunications, IoT devices, and smart cities.

Sustainability and environmental concerns are increasingly influencing the PCB market’s future. The electronics industry is under pressure to reduce its environmental footprint, leading to the development of eco-friendly PCB manufacturing processes and materials. Lead-free soldering, recyclable substrates, and reduced hazardous chemical use are becoming standard practices. Companies that embrace green manufacturing are likely to gain competitive advantages as consumers and regulators prioritize sustainability.

Automation and Industry 4.0 integration are revolutionizing PCB manufacturing. The adoption of artificial intelligence (AI), robotics, and machine learning in production lines improves precision, reduces defects, and accelerates manufacturing cycles. Automated optical inspection (AOI) systems and real-time monitoring help maintain high-quality standards while reducing costs. This trend not only boosts efficiency but also allows manufacturers to respond swiftly to customized and small-batch orders, which are increasingly common due to diversified product demands.

The automotive industry continues to be a major driver of PCB market growth, especially with the rise of electric vehicles (EVs) and autonomous driving technology. PCBs in EVs must withstand higher temperatures and voltages while maintaining safety and durability. Advanced PCBs facilitate battery management systems, power electronics, and sensor integration crucial for EV performance. Additionally, autonomous vehicles rely heavily on sophisticated sensor arrays and computing power, all of which depend on innovative PCB designs.

Healthcare technology is another promising sector influencing PCB trends. The surge in wearable medical devices, telehealth solutions, and diagnostic equipment requires PCBs that offer reliability, miniaturization, and biocompatibility. Flexible PCBs enable comfortable and accurate wearable sensors, while multilayer PCBs support complex diagnostic devices. The ongoing digitalization of healthcare creates a continuous demand for cutting-edge PCB solutions tailored to medical applications.

Global supply chain dynamics also impact the PCB market’s future. The COVID-19 pandemic exposed vulnerabilities in electronics supply chains, prompting companies to rethink sourcing and manufacturing strategies. There is a noticeable trend toward regionalization and diversification to minimize risks and reduce lead times. This shift may result in increased investments in local PCB manufacturing capabilities, encouraging innovation and customization closer to end markets.

Another important future trend is the increasing use of embedded components within PCBs. Embedding passive and active components directly into the PCB substrate reduces assembly time, improves reliability, and enables higher circuit density. This technology is particularly valuable in compact and high-performance devices such as smartphones, tablets, and aerospace electronics, where every millimeter of space counts.

Lastly, the integration of PCBs with emerging technologies such as augmented reality (AR), virtual reality (VR), and artificial intelligence (AI) will open new growth avenues. These technologies demand highly complex, lightweight, and reliable PCBs to support sensors, processors, and communication modules. As these applications gain traction across entertainment, education, and industrial sectors, PCB manufacturers will need to innovate to meet their unique requirements.

In conclusion, the printed circuit board market is poised for dynamic growth fueled by miniaturization, advanced materials, 5G adoption, sustainability initiatives, and Industry 4.0 automation. Key industries such as automotive, healthcare, and telecommunications will continue to drive demand for innovative PCB solutions. Manufacturers who embrace emerging technologies, invest in eco-friendly processes, and adapt to shifting supply chain models will be best positioned to thrive. As the market evolves, staying informed about these future trends will be essential for all stakeholders navigating the complex landscape of PCB technology.

0 notes

Text

Global Second-Life EV Batteries Market | BIS Research

The Global Second-life EV Batteries Market focuses on repurposing used electric vehicle batteries for secondary applications. This market provides substantial prospects in both the automotive and non-automotive sectors, driven by the growing number of retired EV batteries and the need for affordable, sustainable energy storage solutions. Insights into market dynamics, important drivers, constraints, and opportunities in the changing global scene are provided by thorough analysis, such as supply chain evaluations, R&D reviews (including patent trends), and regulatory assessments.

The second-life EV batteries market presents significant growth opportunities driven by the rising volume of retired EV batteries and increasing demand for sustainable, cost-effective energy storage solutions.

Market Segmentation

By Application

Non-Automotive Applications:

Power Backup

Grid Connection

Renewable Energy Storage

Others

Automotive Applications:

EV Charging

Vehicle Applications

By Product

Lithium-Ion

Lead-Acid

Nickel-based

By Region

North America

Europe

Asia-Pacific

Rest-of-the-World

Research Methodology

The research methodology is built on a robust framework that combines trend assessments, value chain evaluations, and pricing forecasts to provide in-depth market insights. It contains a thorough analysis of R&D efforts, with an emphasis on trends in patent filings by nation and business. To provide a comprehensive picture of the market for used EV batteries, the report also includes stakeholder assessments and regulatory reviews, which provide in-depth viewpoints on use cases and purchasing criteria.

Market Drivers

Growing volumes of end-of-life EV batteries and demand for sustainable storage: The demand for second-life battery solutions is being driven by the growing quantity of retired EV batteries as well as the global push for reasonably priced and environmentally responsible energy storage.

Advancements in battery technology and repurposing efficiency: Innovations in diagnostics, battery management systems, and reconditioning processes are making second-life batteries more reliable, cost-effective, and easier to integrate across various applications.

Market Restraints

Battery degradation, recycling complexities, and integration challenges: Degradation causes second-life batteries to behave inconsistently, which complicates evaluation and reuse. Furthermore, recycling procedures continue to present technological and financial difficulties, and compatibility and safety issues can make integration with current energy systems tough.

Regulatory hurdles and inconsistent quality standards: Scalability and broad adoption are restricted by the uncertainty created by manufacturers and users by the absence of accepted quality benchmarks and uniform worldwide laws for second-life batteries.

Key Market Players

B2U Storage Solutions, Inc.

BeePlanet Factory

Cactos

Connected Energy Ltd.

DB Schenker

ECO STOR

Element Energy

Forsee Power

Download TOC for this report. Click Here!

Gain deep information on Automotive Vertical. Click Here!

Conclusion

The second-life EV batteries market is gaining momentum as more end-of-life batteries become available and industries seek sustainable energy storage solutions. Technological developments are increasing the efficiency of battery repurposing and broadening the range of applications in both the automotive and non-automotive industries. To fully achieve the market's potential, however, issues including battery deterioration, recycling difficulties, legal restrictions, and uneven quality standards must be resolved. The market is positioned for sustainable growth as it supports the shift to a circular and cleaner energy economy, with major players aggressively developing and growing their footprint globally.

#Global Second-Life EV Batteries Market#Global Second-Life EV Batteries Industry#Global Second-Life EV Batteries Report

0 notes

Text

Silicone Fluids Market Size, Share, Demand & Growth by 2035

The Silicone Fluid Market is widely recognized for its applications in personal care, lubricants, and industrial coatings. However, one niche segment is rapidly gaining strategic importance but remains underexplored in conventional market reports—the use of silicone fluids in thermal interface materials (TIMs) for electric vehicles (EVs) and advanced computing systems. As global industries push the boundaries of energy efficiency and miniaturization, the heat generated by tightly packed electronics demands materials with superior thermal control. In this context, silicone fluids—especially high-purity polydimethylsiloxane (PDMS) fluids—are stepping into the spotlight as enablers of thermal innovation. This article dives deep into this overlooked domain, uncovering how silicone fluids are poised to shape the future of heat transfer technology.

𝐌𝐚𝐤𝐞 𝐈𝐧𝐟𝐨𝐫𝐦𝐞𝐝 𝐃𝐞𝐜𝐢𝐬𝐢𝐨𝐧𝐬 – 𝐀𝐜𝐜𝐞𝐬𝐬 𝐘𝐨𝐮𝐫 𝐒𝐚𝐦𝐩𝐥𝐞 𝐑𝐞𝐩𝐨𝐫𝐭 𝐈𝐧𝐬𝐭𝐚𝐧𝐭𝐥𝐲! https://www.futuremarketinsights.com/reports/sample/rep-gb-928

The Role of Silicone Fluids in EV Thermal Management Systems

Thermal stability is mission-critical in electric vehicles. Power electronics, battery packs, and electric drivetrains all operate under high thermal stress, which directly affects performance and safety. Traditionally, phase-change materials and thermal pastes have played a central role in dissipating heat, but these solutions often degrade under cyclic loading and prolonged operation. Silicone fluids, particularly volatile silicone oils, are increasingly being formulated into next-generation TIMs due to their superior thermal conductivity, low volatility, and excellent dielectric properties.

Recent innovations in the EV sector—such as the use of direct-contact liquid cooling systems—have triggered demand for silicone-based heat transfer fluids. Tesla, for instance, has filed patents discussing the use of silicone-enhanced thermal pastes to improve the heat dissipation of battery modules. These silicone fluids not only offer a broader operating temperature range but also maintain their properties after repeated thermal cycling, reducing maintenance needs. Their non-reactive chemical profile further ensures compatibility with sensitive electronic components, making them ideal for automotive electronics that demand both durability and safety.

Polydimethylsiloxane Fluids in High-Performance Computing Systems

In the realm of high-performance computing (HPC), including artificial intelligence servers and advanced gaming consoles, managing thermal output is a formidable challenge. The transition from air-cooling to liquid cooling is already underway, and silicone-based coolants are becoming integral to this shift. Polydimethylsiloxane fluids are preferred due to their precise viscosity control, long-term chemical stability, and resistance to thermal oxidation.

For example, researchers at Stanford University recently conducted experiments involving silicone-based TIMs integrated into microprocessor packaging. The results demonstrated a 30% improvement in thermal dissipation compared to conventional materials. Similarly, tech companies like IBM and Google are exploring immersion cooling solutions using specialty silicone fluids to manage the heat generated by AI and cloud infrastructure. These use cases underscore the rising relevance of silicone fluids not just in managing heat, but in enabling the performance of data-driven technologies.

𝐔𝐧𝐥𝐨𝐜𝐤 𝐂𝐨𝐦𝐩𝐫𝐞𝐡𝐞𝐧𝐬𝐢𝐯𝐞 𝐌𝐚𝐫𝐤𝐞𝐭 𝐈𝐧𝐬𝐢𝐠𝐡𝐭𝐬 – 𝐄𝐱𝐩𝐥𝐨𝐫𝐞 𝐭𝐡𝐞 𝐅𝐮𝐥𝐥 𝐑𝐞𝐩𝐨𝐫𝐭 𝐍𝐨𝐰: https://www.futuremarketinsights.com/reports/silicone-fluid-market

The Rise of High-Purity and Specialty Grade Silicone Fluids

While silicone fluids are generally produced in bulk for commodity uses, a small but growing segment of the market is centered on high-purity and specialty-grade variants. These fluids are engineered with extremely tight tolerances for impurity content and molecular weight distribution, making them suitable for cutting-edge applications such as chip manufacturing, nano-engineered cooling solutions, and aerospace electronics.

The market for these high-purity silicone fluids is still developing but commands a high value per kilogram due to the complexity of production and the stringent performance requirements. Companies such as Shin-Etsu Chemical and Elkem Silicones have recently expanded their product portfolios to include such high-end offerings. This emerging trend is driving growth in what could be termed the “ultra-premium” segment of the polydimethylsiloxane fluids market, which remains largely absent from most mainstream market analyses.

Asia-Pacific’s Quiet Leadership in Thermal-Grade Silicone Production

Despite China’s dominance in overall silicone production, the production of thermal-grade silicone fluids is seeing specialized leadership from countries like Japan and South Korea. These nations benefit from tightly integrated supply chains, high R&D spending, and close collaborations between academic institutions and manufacturers. Japan’s Shin-Etsu and South Korea’s KCC Corporation have made significant investments in scaling up the production of thermally optimized silicone fluids, particularly for electronics and automotive sectors.

South Korea’s Ministry of Trade, Industry and Energy has also supported initiatives aimed at domestic innovation in thermal materials, recognizing their role in boosting the competitiveness of the nation’s EV and semiconductor industries. These efforts have translated into export growth for thermal-grade silicone oils, even amid broader geopolitical and trade tensions.

Polymers & Plastics: https://www.futuremarketinsights.com/industry-analysis/polymers-and-plastics

Current Challenges and the Road Ahead

Despite their potential, silicone fluids for thermal applications face some challenges. One major concern is the thermal degradation of silicone oils over extended use, particularly at extremely high temperatures. Additionally, recycling and disposal of used silicone-based TIMs remain complex due to their chemical stability. High-purity grades also incur high manufacturing costs and require advanced handling and processing infrastructure.

However, the industry is responding with innovation. Research is underway into hybrid TIMs that encapsulate silicone fluids within solid-state matrices to improve thermal efficiency and prevent leakage. Startups and academic labs are exploring surface-modified PDMS fluids that offer enhanced heat transfer without sacrificing stability. These breakthroughs could address existing limitations and broaden the applications of silicone fluids across new verticals.

Key Segments Profiled in the Silicone Fluids Industry Survey

Type:

Straight Silicone Fluid

Dimethyl Silicone Fluid

Methylphenyl Silicone Fluid

Methylhydrogen Silicone Fluid

Modified

Reactive Silicone Fluid

Non-Reactive Silicone Fluid

End Use Industry:

Agriculture

Energy

Homecare

Personal Care

Textiles

Pharmaceuticals

Other End Use Industries

Region:

North America

Latin America

Western Europe

Eastern Europe

APEJ

Japan

Middle East & Africa

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analysts worldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries.

Join us as we commemorate 10 years of delivering trusted market insights. Reflecting on a decade of achievements, we continue to lead with integrity, innovation, and expertise.

Contact Us:

Future Market Insights Inc. Christiana Corporate, 200 Continental Drive, Suite 401, Newark, Delaware - 19713, USA T: +1-347-918-3531 For Sales Enquiries: [email protected] Website: https://www.futuremarketinsights.com LinkedIn| Twitter| Blogs | YouTube

0 notes

Text

Avery Dennison at The Battery Show 2025

Avery Dennison will return to The Battery Show Europe 2025 in Stuttgart to showcase its latest innovations in pressure-sensitive adhesives and RFID technologies — designed to meet the evolving needs of electric vehicle (EV) battery manufacturers and OEMs.

Under the theme 'Making Possible,' the company will present how its solutions connect the physical and digital to ensure safety, performance and longevity across the battery lifecycle. With a portfolio that spans bonding, insulating, protecting and tracking, Avery Dennison supports every layer of EV battery design — from cell to pack.

“We’re focused on delivering solutions that help our customers meet the industry’s toughest demands,” said Martin Dolezal, marketing manager, automotive and energy storage. “Whether it’s enhancing thermal management, achieving digital traceability or reducing material impact, our technologies are built to perform in real-world conditions and ready for what’s next.”

Performance tapes: Electrical insulation and tailored venting films

Attendees will find out more about two key tape technologies essential to modern EV battery architecture, including electrical insulation films that deliver robust dielectric protection for critical components like cell connections, busbars, module plates and cooling ribbons. Designed as a high-performance alternative to coatings, these thin yet powerful films enhance thermal flow while meeting demanding electrical insulation needs.

Attendees will also discover the benefits of venting films that tackle one of today’s most complex battery challenges: balancing airtight protection with emergency pressure relief. These engineered membranes block moisture and particles under normal conditions — but when thermal runaway occurs, they release gas and heat while shielding neighboring cells.

“Effective venting and insulation are essential for thermal control and system safety,” said Andrew Christie, business development manager, automotive. “With growing complexity in cell-to-pack designs, we deliver reliable solutions that meet those functional and regulatory challenges.”

Label and packaging materials: Lightweight and sustainable innovations

New from Avery Dennison is a composite current collector — a PET film coated with a highly conductive metallized copper layer — offering a safer, lightweight alternative to traditional copper foil in anode applications. By reducing material mass and thermal risk, this solution enables easier processing, potential mileage gains and greater design flexibility for battery manufacturers.

Also featured are electrical insulation wrapping films made with up to 70% post-consumer recycled PET. These solvent-free solutions are available in single and dual-layer constructions, supporting enhanced safety and material flexibility. A range of color modifications and flame-retardant enhancements is also available for customers looking for customized performance.

Yongle: Next-generation PVC 2.0 low-VOC tapes

Avery Dennison Yongle will showcase its new generation of PVC 2.0 low-VOC tapes, engineered for automotive interiors and environments where low fogging, odor and emissions are required. Using a patented UV-cured hot melt adhesive and solvent-free coating process, the tapes eliminate low-molecular-weight plasticizers and leave no solvent residue.

“As sustainability and interior air quality become higher priorities, our PVC 2.0 tapes provide OEMs with a future-ready solution,” said Lisa Zhuang, senior sales manager Yongle EU. “They’re proof that innovation and responsibility can go hand in hand.”

Intelligent labeling: Connecting the physical and digital

With a growing need for traceability and supply chain transparency, Avery Dennison will also spotlight its RFID-enabled labeling solutions — designed to create a digital twin of the battery or component they’re applied to. As the world’s largest UHF RFID inlay manufacturer, Avery Dennison enables EV battery makers to unlock item-level tracking, support compliance and deliver full lifecycle visibility from cell manufacturing to pack integration and end-of-life.

Providing global coverage and local support, Avery Dennison combines material science expertise with forward-looking innovation to help customers meet the evolving needs of the EV battery industry.

0 notes

Text

Electronic Grade Copper Oxide Powder Market Report: Trends, Opportunities, and Forecast 2025-2031

Electronic Grade Copper Oxide Powder Market, Global Outlook and Forecast 2025-2032

The global Electronic Grade Copper Oxide Powder Market valuation reached USD 182.90 million in 2023, with projections indicating steady growth at a CAGR of 2.60% to reach USD 230.43 million by 2032. This specialized material—with copper oxide content exceeding 99.0%—has become indispensable for high-precision electronics manufacturing, particularly in PCB production and advanced interconnect technologies where microscopic honeycomb structures enable superior electroplating performance.

Electronic grade copper oxide powder demonstrates exceptional characteristics including uniform particle distribution, rapid dissolution rates, and plating consistency—properties critical for HDI boards and IC carrier boards. As miniaturization trends accelerate across consumer electronics and automotive applications, demand surges for materials that balance conductivity with precise deposition characteristics.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/290264/electronic-grade-copper-oxide-powder-market

Market Overview & Regional Analysis

Asia-Pacific commands the lion's share of production, fueled by China's dominance in PCB manufacturing and Taiwan's advanced semiconductor ecosystem. The region benefits from vertically integrated electronics supply chains and aggressive R&D investment in material science. Japan maintains leadership in nanoparticle technologies, while South Korea's display industry drives specialized demand.

North America shows robust growth particularly in military/aerospace applications, where stringent reliability requirements justify premium pricing. Europe's market thrives on automotive electronics innovation, with German chemical giants pioneering eco-friendly production methods. Emerging economies in Southeast Asia demonstrate accelerating uptake as electronics manufacturing migrates from traditional hubs.

Key Market Drivers and Opportunities

Three seismic shifts propel market expansion: First, the 5G infrastructure rollout demands high-frequency PCBs requiring ultra-fine copper deposition. Second, electric vehicle adoption expands applications in power electronics and battery management systems. Third, AI hardware development necessitates advanced packaging solutions leveraging copper's superior conductivity.

Opportunity abounds in developing copper oxide formulations optimized for: - Additive manufacturing of electronic components - Low-temperature sintering processes - Hybrid conductive pastes These innovations could unlock new applications in flexible electronics and IoT devices, potentially adding USD 15-20 million to the addressable market by 2028.

Challenges & Restraints

The market faces headwinds from: - Copper price volatility impacting production costs - Tightening REACH and RoHS regulations on heavy metal content - Emergence of conductive polymer alternatives - Technical hurdles in achieving sub-20nm particle consistency

Supply chain vulnerabilities surfaced during recent semiconductor shortages, prompting manufacturers to diversify sourcing strategies. Meanwhile, environmental concerns drive investment in closed-loop recycling systems for copper recovery.

Market Segmentation by Type

Below 20nm

20-50nm

50-100nm

Above 100nm

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/290264/electronic-grade-copper-oxide-powder-market

Market Segmentation by Application

PCB Manufacturing Industry

HDI Board

IC Carrier Board

Others

Market Segmentation and Key Players

Strem Chemicals

Nanoshel

American Elements

SkySpring Nanomaterials

SAT Nano Technology Material

NGimat

Jiangxi Jiangnan New Material

Report Scope

This comprehensive analysis covers the global electronic grade copper oxide powder market from 2024-2032, featuring:

Market size projections with 8-year forecasts

Application-specific demand analysis across electronics verticals

Particle size segmentation and growth potential

The report delivers actionable intelligence through:

Competitive benchmarking of 15+ manufacturers

Production capacity assessments by region

Emerging application pipeline analysis

Regulatory impact assessment

Get Full Report Here: https://www.24chemicalresearch.com/reports/290264/electronic-grade-copper-oxide-powder-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

Plant-level capacity tracking

Real-time price monitoring

Techno-economic feasibility studies

With a dedicated team of researchers possessing over a decade of experience, we focus on delivering actionable, timely, and high-quality reports to help clients achieve their strategic goals. Our mission is to be the most trusted resource for market insights in the chemical and materials industries.

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Follow us on LinkedIn: https://www.linkedin.com/company/24chemicalresearch

0 notes

Text

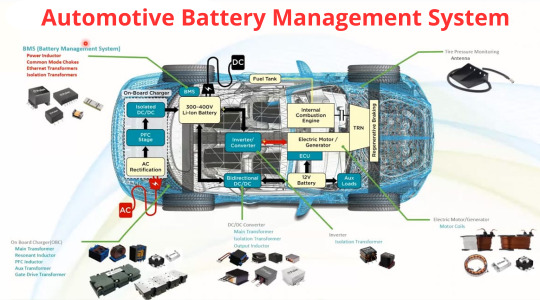

Automotive Battery Management System Market Size, Analyzing Trends and Projected Outlook for 2025-2032

Fortune Business Insights released the Global Automotive Battery Management System Market Trends Study, a comprehensive analysis of the market that spans more than 150+ pages and describes the product and industry scope as well as the market prognosis and status for 2025-2032. The marketization process is being accelerated by the market study's segmentation by important regions. The market is currently expanding its reach.

The Automotive Battery Management System Market is experiencing robust growth driven by the expanding globally. The Automotive Battery Management System Market is poised for substantial growth as manufacturers across various industries embrace automation to enhance productivity, quality, and agility in their production processes. Automotive Battery Management System Market leverage robotics, machine vision, and advanced control technologies to streamline assembly tasks, reduce labor costs, and minimize errors. With increasing demand for customized products, shorter product lifecycles, and labor shortages, there is a growing need for flexible and scalable automation solutions. As technology advances and automation becomes more accessible, the adoption of automated assembly systems is expected to accelerate, driving market growth and innovation in manufacturing. Automotive Battery Management System Market Size, Share & Industry Analysis, By Type (Lithium-ion, Lead Acid, Nickel-based), By Connection Topology (Centralized , Distributed , Modular), By Vehicle type (Electric Vehicles, E-bikes) And Regional Forecast 2021-2028

Get Sample PDF Report: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/105479

Major Automotive Battery Management System Market Manufacturers covered in the market report include:

Some of the major companies that are present in the automotive battery management system market include Thyssenkrupp AG, Nippon Steel Integrated Battery Management LLC, Braynt Racing Inc., Arrow Precision Ltd., Maschinenfabrik Alfing Kessler GmbH, Mahindra CIE, Tianrun Battery Management Co., Ltd., among others.

Owing to this, many Battery Management manufacturers are developing advanced Battery Management with improved fatigue strength, reliability, and quality. Also, the crankshafts are manufactured with the latest trend of steelmaking processes by materials with high strength, and this factor is also expected to drive the automotive Battery Management market.

Geographically, the detailed analysis of consumption, revenue, market share, and growth rate of the following regions:

The Middle East and Africa (South Africa, Saudi Arabia, UAE, Israel, Egypt, etc.)

North America (United States, Mexico & Canada)

South America (Brazil, Venezuela, Argentina, Ecuador, Peru, Colombia, etc.)

Europe (Turkey, Spain, Turkey, Netherlands Denmark, Belgium, Switzerland, Germany, Russia UK, Italy, France, etc.)

Asia-Pacific (Taiwan, Hong Kong, Singapore, Vietnam, China, Malaysia, Japan, Philippines, Korea, Thailand, India, Indonesia, and Australia).

Automotive Battery Management System Market Research Objectives:

- Focuses on the key manufacturers, to define, pronounce and examine the value, sales volume, market share, market competition landscape, SWOT analysis, and development plans in the next few years.

- To share comprehensive information about the key factors influencing the growth of the market (opportunities, drivers, growth potential, industry-specific challenges and risks).

- To analyze the with respect to individual future prospects, growth trends and their involvement to the total market.

- To analyze reasonable developments such as agreements, expansions new product launches, and acquisitions in the market.

- To deliberately profile the key players and systematically examine their growth strategies.

Frequently Asked Questions (FAQs):

► What is the current market scenario?

► What was the historical demand scenario, and forecast outlook from 2025 to 2032?

► What are the key market dynamics influencing growth in the Global Automotive Battery Management System Market ?

► Who are the prominent players in the Global Automotive Battery Management System Market ?

► What is the consumer perspective in the Global Automotive Battery Management System Market ?

► What are the key demand-side and supply-side trends in the Global Automotive Battery Management System Market ?

► What are the largest and the fastest-growing geographies?

► Which segment dominated and which segment is expected to grow fastest?

► What was the COVID-19 impact on the Global Automotive Battery Management System Market ?

FIVE FORCES & PESTLE ANALYSIS:

In order to better understand market conditions five forces analysis is conducted that includes the Bargaining power of buyers, Bargaining power of suppliers, Threat of new entrants, Threat of substitutes, and Threat of rivalry.

Political (Political policy and stability as well as trade, fiscal, and taxation policies)

Economical (Interest rates, employment or unemployment rates, raw material costs, and foreign exchange rates)

Social (Changing family demographics, education levels, cultural trends, attitude changes, and changes in lifestyles)

Technological (Changes in digital or mobile technology, automation, research, and development)

Legal (Employment legislation, consumer law, health, and safety, international as well as trade regulation and restrictions)

Environmental (Climate, recycling procedures, carbon footprint, waste disposal, and sustainability)

Points Covered in Table of Content of Global Automotive Battery Management System Market :

Chapter 01 - Automotive Battery Management System Market for Automotive Executive Summary

Chapter 02 - Market Overview

Chapter 03 - Key Success Factors

Chapter 04 - Global Automotive Battery Management System Market - Pricing Analysis

Chapter 05 - Global Automotive Battery Management System Market Background or History

Chapter 06 - Global Automotive Battery Management System Market Segmentation (e.g. Type, Application)

Chapter 07 - Key and Emerging Countries Analysis Worldwide Automotive Battery Management System Market .

Chapter 08 - Global Automotive Battery Management System Market Structure & worth Analysis

Chapter 09 - Global Automotive Battery Management System Market Competitive Analysis & Challenges

Chapter 10 - Assumptions and Acronyms

Chapter 11 - Automotive Battery Management System Market Research Methodology

About Us:

Fortune Business Insights™ delivers accurate data and innovative corporate analysis, helping organizations of all sizes make appropriate decisions. We tailor novel solutions for our clients, assisting them to address various challenges distinct to their businesses. Our aim is to empower them with holistic market intelligence, providing a granular overview of the market they are operating in.

Contact Us:

Fortune Business Insights™ Pvt. Ltd.

US:+18339092966

UK: +448085020280

APAC: +91 744 740 1245

0 notes

Text

Global MEMS Market Set for Steady Growth at 4.4% CAGR Through 2034

The global Micro‑electromechanical System (MEMS) market was valued at US$ 17.7 billion in 2023. Driven by innovations across healthcare, consumer electronics and automotive sectors, the industry is projected to expand at a CAGR of 4.4 percent between 2024 and 2034, reaching an estimated value of US$ 28.6 billion by December 2034. MEMS technology integrates microscopic mechanical and electrical components such as sensors, actuators and control electronics into single chip‐scale devices that detect and react to environmental stimuli including motion, pressure, temperature and chemical changes. As miniaturization, cost‑efficiency and performance demands intensify, MEMS finds new applications from smartphones to implantable medical diagnostics.

Download to explore critical insights from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=86128

Market Drivers & Trends

Innovative Medical Solutions: The rise in non‑communicable diseases and an aging global population fuels demand for compact, accurate medical devices. MEMS‑based point‑of‑care systems enable rapid diagnostics at the bedside or in remote settings, reducing turnaround time and improving patient outcomes.

Consumer Electronics Adoption: Accelerometers, gyroscopes and micro‑compasses are standard in smartphones, wearables and AR/VR headsets. MEMS‑based inertial measurement units (IMUs) enhance electronic and optical image stabilization, motion sensing and user interface controls. Proliferation of 5G networks (over 1 billion subscriptions by end‑2022) further drives high‑frequency MEMS integration in next‑gen mobile devices.

Automotive & EV Integration: Stringent safety and emission regulations boost MEMS sensors for advanced driver‑assistance systems (ADAS), tire pressure monitoring and EV battery management. MEMS devices offer high reliability under harsh engine conditions, aiding in lightweight, energy‑efficient designs.

Latest Market Trends

Miniaturization & Integration: Fabrication at 1–100 µm scale allows fully integrated MEMS chips with on‑board processing, reducing PCB footprint and power consumption.

Multi‑Parameter Sensing: Hybrid MEMS sensors capable of measuring pressure, humidity, gas composition and temperature on a single die are gaining traction in industrial IoT and environmental monitoring.

Bio‑MEMS for Wearables: Flexible, biocompatible MEMS platforms for continuous glucose, lactate and sweat analysis are emerging, driven by demand for personalized health monitoring.

3D Packaging & System‑in‑Package (SiP): Advanced packaging techniques enable stacking MEMS devices with CMOS logic, offering modular solutions that balance performance and cost.

Key Players and Industry Leaders The competitive landscape features a mix of semiconductor giants, specialized MEMS firms and emerging innovators:

Analog Devices, Inc.

Broadcom

Goertek Microelectronics Inc.

Honeywell International Inc.

Infineon Technologies AG

Knowles Electronics, LLC.

Murata Manufacturing Co., Ltd.

OMRON Corporation

Panasonic Corporation

Qorvo, Inc

Robert Bosch GmbH

STMicroelectronics

TDK Corporation

Texas Instruments Incorporated

Goertek Inc.

Sensata Technologies, Inc.

Melexis

Amphenol Corporation

Recent Developments

Jan 2023 – TDK Corp. announced the SmartSound One Development Platform, offering plug‑and‑play evaluation for multiple MEMS microphone configurations.

Jan 2023 – Knowles Corp. launched its Titan, Falcon and Robin MEMS microphone series, targeting space‑constrained ear‑wearable applications.

Mar 2024 – STMicroelectronics introduced a hybrid pressure‑and‑temperature MEMS sensor for industrial IoT nodes, enabling remote monitoring with enhanced accuracy.

Apr 2024 – Analog Devices unveiled a next‑gen MEMS IMU with on‑chip sensor fusion, reducing system‑level calibration by 50 percent.

Market Opportunities and Challenges Opportunities

Healthcare Expansion: Development of implantable MEMS pumps and bio‑chips for organ‑on‑chip research.

5G & Edge AI: Integration of MEMS sensors with edge‑AI accelerators for real‑time analytics in smart cities and autonomous systems.

Green Mobility: MEMS‑based flow and pressure sensors for hydrogen fuel cells and EV thermal management.

Challenges

Manufacturing Complexity: High‑volume, defect‑free MEMS fabrication demands advanced cleanroom processes and wafer‑level packaging, increasing capital expenditure.

Standardization: Lack of universal MEMS interface standards complicates system integration across different OEMs and end‑use industries.

Supply Chain Disruptions: Geopolitical tensions and raw‑material shortages may impact silicon and specialty substrate availability, potentially delaying product launches.

Future Outlook Looking ahead to 2034, the MEMS market will be shaped by converging trends in miniaturization, AI‑enhanced sensing and sustainable manufacturing. By mid‑2030s, novel materials such as graphene‑based membranes and piezoelectric polymers could unlock ultra‑sensitive gas and biosensing platforms. Cross‑industry collaborations—between semiconductor foundries, healthcare providers and automotive OEMs—will accelerate tailored MEMS solutions, while democratized design tools (MEMS CAD libraries) will broaden participation from startups. Overall, the outlook remains positive: annual revenue growth above 4 percent, with pockets of double‑digit expansion in biomedical and automotive electric‑mobility applications.

Market Segmentation

By Type

Accelerometers

Gyroscopes

Digital E‑compasses

Temperature, Pressure, Humidity Sensors

MEMS Microphones

Inertial Measurement Units (IMUs)

Others (Spectrum, Optical)

By Actuation

Thermal, Magnetic, Piezoelectric, Electrostatic, Chemical

By End‑Use Industry

Automotive, Consumer Electronics, Defense, Aerospace, Industrial, Healthcare, IT & Telecom, Others (Agriculture, Energy)

By Region

North America, Europe, Asia Pacific, Middle East & Africa, South America

Regional Insights Asia Pacific leads the global MEMS market, accounting for the largest share in 2023 due to:

Smartphone & 5G Penetration: High adoption of 5G services and smartphone shipments in China, India, South Korea and ASEAN.

Automotive Manufacturing Hub: Strong presence of EV and auto component OEMs integrating MEMS for ADAS and battery management.

Industrial Automation: Rapid Industry 4.0 deployments in China, Japan and South Korea fueling demand for MEMS‑based IoT sensors. North America and Europe follow, driven by healthcare innovation clusters (Boston, Silicon Valley; Berlin, Stockholm) and defense contracts requiring ruggedized MEMS devices.

Why Buy This Report?

Comprehensive Coverage: Quantitative forecasts (2024–2034) and historical data (2020–2022) across value (US$ Bn) and volume (’000 units).

In‑Depth Analysis: Porter’s Five Forces, value‑chain assessment, competitive benchmarking and segment‑level deep dives.

Strategic Insights: Analyst recommendations on R&D prioritization, geographic expansion and M&A targets.

Excel Database: Customizable tables and charts enable scenario modelling and peer‑group financial comparisons.

Explore Latest Research Reports by Transparency Market Research: High Voltage Solid-state Transformer Market: https://www.transparencymarketresearch.com/high-voltage-solid-state-transformer-market.html

Ultrasonic Air in Line Sensor Market: https://www.transparencymarketresearch.com/ultrasonic-air-line-sensor-market.html

Gyroscope Market: https://www.transparencymarketresearch.com/gyroscope-market.html

Optical Sorters Market: https://www.transparencymarketresearch.com/optical-sorters-market.html

About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

Graphene Paper Market Size, Demand & Supply, Regional and Competitive Analysis 2025–2032

Definition

Graphene paper is a lightweight, flexible material composed of stacked graphene sheets. It retains many of graphene’s unique properties—such as high thermal conductivity, electrical conductivity, and mechanical strength—while offering additional advantages like flexibility and ease of integration into devices. Graphene paper is increasingly used in applications across energy storage (batteries and supercapacitors), flexible electronics, aerospace, and thermal management systems.

Due to its multifunctional properties, graphene paper is drawing significant interest from researchers and industries aiming to develop next-generation materials for high-performance and lightweight applications. The global market is expected to grow substantially over the next decade, driven by innovation in electronics, renewable energy, and advanced materials.

Market Size

📥 Download a Free Sample Report PDF https://www.24chemicalresearch.com/download-sample/292632/global-graphene-paper-market-2025-2032-67

As of 2024, the global graphene paper market is estimated at USD 1.22 billion. It is projected to reach USD 2.67 billion by 2032, expanding at a CAGR of 10.2% during the forecast period. Growth is being driven by rising demand in sectors like electronics, aerospace, and energy, where lightweight and high-performance materials are increasingly necessary.

Growth Projections and Trends

Graphene paper’s market outlook remains highly positive due to increasing investment in nanotechnology and material science. Innovations in supercapacitors and lithium-ion batteries are significantly contributing to the demand for graphene paper. Additionally, the rapid commercialization of flexible electronic components and printed sensors is enhancing graphene paper’s practical use.

Notable trends include:

Growing research into composite materials using graphene paper.

Integration in wearable technologies and flexible displays.

Expanded R&D funding across the EU, U.S., and Asia-Pacific for graphene-based applications.

Market Dynamics (Drivers, Restraints, Opportunities, Challenges)

Drivers

Energy Storage Applications: Growing demand for high-capacity, fast-charging batteries and supercapacitors is fueling the use of graphene paper as a conductive electrode material.

Lightweight and Durable Material: The aerospace and automotive industries are adopting graphene paper for its strength-to-weight ratio and thermal conductivity.

Flexible Electronics Boom: The rise in consumer electronics requiring foldable or bendable components is accelerating adoption.

Restraints

High Production Costs: Despite progress, the cost of producing graphene paper remains high due to expensive precursor materials and complex fabrication methods.

Lack of Standardization: Absence of industrial-scale standardization for graphene paper hinders widespread adoption.

Opportunities

Green Energy Initiatives: Government and private sector investment in renewable energy and smart grid infrastructure create opportunities for graphene paper in energy storage systems.

Expansion in Emerging Economies: Industrialization in Asia-Pacific, Latin America, and Africa presents new growth avenues for manufacturers.

Challenges

Scalability Issues: Difficulty in scaling lab-scale production to industrial volumes limits market growth.

Environmental & Regulatory Concerns: Manufacturing processes may require hazardous chemicals, raising environmental and safety concerns.

Regional Analysis

North America

North America is a major hub for graphene R&D and commercialization, especially in the United States. Strong investment in electronics, aerospace, and military sectors is boosting the adoption of graphene paper.

Europe

Europe, led by countries like Germany, the UK, and France, is heavily involved in advanced materials research. The EU’s Graphene Flagship program is further accelerating innovation and commercialization in the region.

Asia-Pacific

Asia-Pacific holds the largest share of the global graphene paper market, driven by the presence of major battery manufacturers and tech firms in China, South Korea, and Japan. The region is a production powerhouse with significant end-use demand.

Latin America

Latin America is emerging as a promising region due to increasing investments in renewable energy and infrastructure modernization. Brazil and Mexico are primary contributors.

Middle East & Africa

With growing focus on sustainability and technological innovation, the Middle East and Africa are showing moderate but rising interest in graphene materials for energy and water filtration technologies.

Competitive Analysis

Key Players in the Graphene Paper Market

The market is characterized by strong research-oriented companies and emerging startups. Leading companies include:

Haydale Graphene Industries – Develops functionalized graphene materials and composite solutions.

Graphenea – A European leader in graphene oxide and graphene paper products.

ACS Material LLC – Supplies high-quality graphene and advanced nanomaterials globally.

XG Sciences, Inc. – Focuses on graphene nanoplatelets and paper for energy applications.

These firms are investing in R&D partnerships, expanding production capacities, and engaging in strategic collaborations to enhance their market share and develop scalable graphene solutions.

Global Graphene Paper: Market Segmentation Analysis

By Application

Energy Storage Devices (Batteries, Supercapacitors)

Flexible Electronics

Thermal Management

Aerospace & Defense

Others (Filtration, Conductive Composites)

By Type

Graphene Oxide Paper

Reduced Graphene Oxide Paper

Conductive Graphene Paper

Others

By Region

North America

Europe

Asia-Pacific

Latin America

Middle East & Africa

FAQs

1. What is the current market size of the Graphene Paper Market? As of 2024, the market size is estimated at USD 1.22 billion and projected to reach USD 2.67 billion by 2032.

2. What are the major applications driving the Graphene Paper Market? Key applications include energy storage (batteries, supercapacitors), flexible electronics, aerospace, and thermal management systems.

3. Who are the leading players in the Graphene Paper Market? Major players include Haydale Graphene Industries, Graphenea, ACS Material LLC, and XG Sciences.

4. Which region dominates the Graphene Paper Market? Asia-Pacific leads the market due to large-scale industrialization and advanced battery manufacturing capabilities.

5. What are the major challenges faced by the Graphene Paper Market? Challenges include high production costs, lack of standardization, and scalability issues in mass manufacturing.

📘 Get the Complete Report & TOC https://www.24chemicalresearch.com/reports/292632/global-graphene-paper-market-2025-2032-67

🔗 Follow Us on LinkedIn https://www.linkedin.com/company/24chemicalresearch/

CONTACT US 203A, City Vista, Fountain Road, Kharadi, Pune, India - 411014 International: +1 (332) 2424 294 Asia: +91 9169162030

About 24ChemicalResearch Founded in 2015, 24ChemicalResearch is a leading market research firm in the chemical industry, delivering critical data and forecasts that support strategic business decisions. Our client base includes over 30 Fortune 500 companies worldwide.

0 notes

Text

Automated Guided Vehicle (AGV) Market Drivers Accelerating Growth Across Diverse Industrial Sectors

The Automated Guided Vehicle (AGV) market is experiencing rapid growth, driven by a combination of technological advancements, increasing demand for automation in manufacturing and logistics, and the global shift toward Industry 4.0. As companies across various sectors aim to streamline operations, improve productivity, and reduce labor costs, AGVs are emerging as indispensable tools. This article delves deep into the core drivers propelling the AGV market forward and examines the broader implications of these trends on industrial operations worldwide.

Rising Demand for Automation in Material Handling One of the most significant drivers of the AGV market is the rising demand for automation in material handling processes. With the need for enhanced efficiency and reduced human error, industries such as automotive, food & beverage, electronics, and e-commerce are integrating AGVs into their supply chains. These vehicles offer consistent performance, 24/7 operational capability, and can handle repetitive tasks without fatigue, resulting in cost savings and improved throughput.

Labor Shortages and Rising Labor Costs The global labor market is undergoing a major shift, characterized by a shortage of skilled workers and rising labor costs. In response, businesses are increasingly turning to AGVs as a reliable alternative. AGVs can operate in harsh or hazardous environments where human labor may be unsuitable or expensive. This driver is particularly prominent in regions like North America and Europe, where demographic changes and evolving workforce expectations are contributing to persistent labor challenges.

Industry 4.0 and Smart Factory Initiatives The adoption of Industry 4.0 technologies is playing a crucial role in accelerating AGV deployment. Smart factories leverage interconnected devices, AI, machine learning, and robotics to optimize manufacturing processes. AGVs are central to this transformation as they enable seamless integration with warehouse management systems (WMS) and enterprise resource planning (ERP) platforms. The ability to gather data in real time and respond dynamically to changing conditions is fueling their adoption.

E-Commerce and the Need for Faster Fulfillment The explosive growth of the e-commerce sector has placed immense pressure on logistics networks to deliver goods faster and more accurately. AGVs offer a scalable solution to handle fluctuating demand while reducing human dependency. From automated guided carts in warehouses to complex fleet systems in distribution centers, AGVs improve order picking efficiency and accuracy, making them critical to modern retail and fulfillment operations.

Technological Advancements in Navigation and Safety Innovations in sensor technology, artificial intelligence, and machine vision have significantly enhanced AGV capabilities. Modern AGVs now feature advanced navigation systems such as LiDAR, SLAM (Simultaneous Localization and Mapping), and obstacle detection. These technologies improve route flexibility and operational safety, making AGVs suitable for a wider range of applications. Enhanced battery life, wireless charging, and predictive maintenance are additional technological drivers influencing market growth.

Sustainability and Energy Efficiency As organizations prioritize sustainability and energy efficiency, AGVs present an environmentally friendly alternative to traditional internal combustion-powered material handling equipment. Many AGVs are electric-powered and offer lower emissions and noise levels. Their ability to optimize routing and reduce unnecessary movements also contributes to energy savings. This aligns with corporate ESG (Environmental, Social, and Governance) goals and regulatory compliance.

Customization and Modularity Manufacturers are now offering customizable AGVs tailored to specific industrial requirements. From towing vehicles and unit load carriers to forked AGVs, modular designs allow end-users to configure systems based on their workflow needs. This flexibility is a key driver for adoption, particularly in dynamic production environments where agility and scalability are essential.

Government Support and Infrastructure Development Several governments are supporting the development of smart logistics infrastructure through incentives and policy frameworks. For instance, initiatives promoting automation in manufacturing and logistics hubs are facilitating AGV integration. Investment in 5G and industrial IoT ecosystems is also creating a conducive environment for real-time vehicle communication and coordination.

Conclusion The AGV market is poised for sustained growth, fueled by powerful drivers including the push for automation, labor challenges, and smart manufacturing strategies. As these vehicles become more intelligent, versatile, and accessible, their role in transforming logistics and production environments will only expand. Companies that invest in AGV technologies today are likely to gain a competitive edge in efficiency, cost management, and innovation tomorrow.

0 notes

Text

⚡ Tiny Sensors, Huge Growth: Current Sensor Market to Reach $7.8B by 2034

Current Sensor Market is on an impressive upward trajectory, expected to surge from $3.1 billion in 2024 to $7.8 billion by 2034, growing at a strong CAGR of 9.7%. This growth mirrors the increasing demand for current measurement in smart technologies, electric vehicles, renewable energy systems, and advanced industrial machinery. Current sensors play a crucial role in monitoring and regulating electric currents to enhance system efficiency, safety, and energy savings. From managing battery systems in electric cars to powering smart grid infrastructure, their role is more vital than ever.

Market Dynamics

The market is being driven by a combination of technological innovations, rising renewable energy adoption, and the global transition to electric mobility. The demand for Hall Effect sensors, due to their reliability and cost-effectiveness, remains dominant across several sectors. Shunt-based sensors, gaining ground due to their versatility, are widely used in energy management and automation.

Click to Request a Sample of this Report for Additional Market Insights: https://www.globalinsightservices.com/request-sample/?id=GIS20825

On the flip side, challenges such as the rising cost of raw materials, integration complexities with IoT, and regulatory compliance across geographies could hinder short-term growth. Yet, the ongoing miniaturization of sensors and increased investment in AI-driven monitoring systems are expected to unlock new opportunities.

Key Players Analysis

Some of the major players steering the current sensor industry include Allegro MicroSystems, Infineon Technologies, Honeywell International, LEM Holding, and Melexis NV. These companies are setting benchmarks through innovation, mergers, and partnerships aimed at improving sensor accuracy, energy efficiency, and real-time data capabilities. Emerging names like Volt Guard, Sense Stream, and Electra Sense are also entering the competitive arena, bringing niche innovations and disrupting traditional sensor models. Strategic moves by these players — especially toward sustainable manufacturing and smart applications — are reshaping the competitive landscape.

Regional Analysis

The Asia-Pacific region continues to lead the current sensor market, driven by rapid industrial growth and tech innovation in countries like China, Japan, and India. Smart city initiatives and the boom in EV adoption have further accelerated sensor deployment. North America follows closely, where focus on IoT, energy-efficient infrastructure, and robust automotive markets — especially in the United States — are fueling demand. Europe, led by Germany and France, maintains strong growth through regulatory pushes for sustainability and automation. Meanwhile, Latin America, the Middle East, and Africa are emerging as high-potential markets, thanks to infrastructure development and increasing renewable energy projects.

Recent News & Developments

Recent years have seen an evolution in sensor pricing and design, with costs ranging from $1 to $50 per unit, depending on type and functionality. Innovations like wireless current sensors, non-invasive technologies, and AI-integrated systems are redefining application scopes. Companies such as Aceinna and Analog Devices have introduced advanced sensor models supporting real-time analytics and predictive maintenance. Moreover, global supply chain challenges and trade policy shifts are prompting businesses to invest in localized manufacturing and sustainable sourcing. Regulatory developments, especially around energy efficiency and data security, are also shaping R&D focus.

Browse Full Report : https://www.globalinsightservices.com/reports/current-sensor-market/

Scope of the Report

This report offers a detailed snapshot of the current sensor industry, spanning segmentation by type, technology, material, and application. It analyzes both quantitative trends — such as unit sales and CAGR — and qualitative dynamics, including SWOT, PESTLE, and competitive strategies. It highlights regional performance, emerging market entrants, and key development strategies like partnerships, acquisitions, and R&D investment. From OEMs to aftermarket trends, and from analog to digital sensor tech, the report lays out a comprehensive roadmap for stakeholders. With detailed insights into cross-segmental opportunities, demand-supply analysis, and local regulatory landscapes, it empowers strategic decision-making for sustainable and profitable growth in this evolving market.

Discover Additional Market Insights from Global Insight Services:

Asset Integrity Management Market : https://www.globalinsightservices.com/reports/asset-integrity-management-market/

Printed Circuit Board Market : https://www.globalinsightservices.com/reports/printed-circuit-board-market/

Medical Sensors Market : https://www.globalinsightservices.com/reports/medical-sensors-market/

Fiber Optic Cables Market : https://www.globalinsightservices.com/reports/fiber-optic-cables-market/

Smart Factory Market : https://www.globalinsightservices.com/reports/smart-factory-market/

#currentmarkettrends #currentsensormarket #iotdevices #energyefficiency #automotivesensors #smartgridtech #hallfx #digitalsensors #industryautomation #techdriven #renewableenergygrowth #electricvehicles #embeddedtech #standaloneelectronics #asiapacificgrowth #europetechmarket #northamericainnovation #industrialsolutions #automotiveinnovation #sensorfusion #smartdevices #powersystems #futuretech #sensorinnovation #aiintegration #minisensors #costefficienttech #energymanagement #techtrends2025 #sensorrevolution #microelectronics #semiconductortechnology #globaltechmarket #batterymanagement #cleantech #sustainablesolutions #iotintegration #powersensing #currentmeasurement #smartmobility

About Us:

Global Insight Services (GIS) is a leading multi-industry market research firm headquartered in Delaware, US. We are committed to providing our clients with highest quality data, analysis, and tools to meet all their market research needs. With GIS, you can be assured of the quality of the deliverables, robust & transparent research methodology, and superior service.

Contact Us:

Global Insight Services LLC 16192, Coastal Highway, Lewes DE 19958 E-mail: [email protected] Phone: +1–833–761–1700 Website: https://www.globalinsightservices.com/

0 notes

Text

Automotive Collision Repair Market Size, Share & Demand Outlook 2033

The global automotive collision repair market is undergoing significant transformations, driven by advancements in vehicle technology, changing consumer behaviours, and evolving industry dynamics. As of 2024, the market is valued at approximately USD XXX billion and is projected to reach USD XXX billion by 2033, growing at a CAGR of XX% .

Market Drivers

1. Technological Advancements

Modern vehicles are increasingly equipped with Advanced Driver Assistance Systems (ADAS), such as lane-keeping assist and adaptive cruise control. These systems, while enhancing safety, have also increased repair costs. For instance, replacing components like side mirrors with sensors can average over USD 1,000, and even minor collisions can escalate repair expenses by up to 37.6% .

2. Shift Towards Electric Vehicles (EVs)

The rise of EVs introduces new challenges in collision repair due to their unique components, such as high-voltage batteries. In regions like Australia, the shortage of skilled mechanics trained to handle EV repairs has led insurers to write off EVs after minor accidents, highlighting the need for specialized training and infrastructure.

3. Integration of Artificial Intelligence (AI)

AI is streamlining collision repair processes by automating routine tasks, enhancing diagnostic accuracy, and improving customer service. AI-driven systems assist in estimating repair costs, managing inventory, and optimizing repair workflows, leading to increased efficiency and customer satisfaction.

Download a Free Sample Report: - https://tinyurl.com/4ydx2a8n

Regional Insights

Europe: Dominated the market with a 41.69% share in 2024. The region's growth is attributed to stringent vehicle safety standards, high vehicle ownership rates, and a strong presence of luxury and electric vehicle manufacturers.

Asia-Pacific: Expected to witness the highest growth rate, with a projected CAGR of 3.5% from 2024 to 2030. Factors contributing to this growth include increasing vehicle sales, rising traffic accidents, and the adoption of advanced repair technologies.

North America: In the U.S., the market was valued at USD 36.66 billion in 2023 and is projected to grow at a CAGR of 0.8% from 2024 to 2030. Factors influencing this growth include high vehicle miles driven, stringent safety regulations, and a robust insurance framework.

Market Segmentation

By Product: Spare parts accounted for approximately 65% of the market share in 2024. The paints and coatings segment is projected to grow at a CAGR of 2.72% during the forecast period, driven by environmental concerns and regulatory standards.

By Service Channel: Original Equipment Manufacturers (OEMs) held a 56% share in 2024, offering long-term warranties and fostering customer loyalty. However, the aftermarket segment is gaining traction due to cost-effectiveness and a wide range of options.

By Vehicle Type: Light-duty vehicles, including sedans, hatchbacks, and SUVs, represented 72% of the market share in 2024. The increasing adoption of electric and autonomous vehicles is expected to influence repair requirements and service offerings.

Challenges Facing the Industry

Skilled Labor Shortage: The complexity of modern vehicles, especially EVs and those equipped with ADAS, requires specialized training. The lack of skilled technicians is leading to increased repair times and costs, and in some cases, vehicles are being written off due to the unavailability of qualified repair personnel.

High Repair Costs: The integration of advanced technologies in vehicles has escalated repair costs. Components like sensors and electronic systems are expensive to replace and require specialized equipment and expertise, making repairs more costly for consumers and insurers alike.

Regulatory Compliance: Adhering to evolving environmental and safety regulations necessitates continuous investment in training, equipment, and processes. Repair shops must stay updated with the latest standards to ensure compliance and maintain competitiveness.

Future Outlook

The automotive collision repair market is poised for steady growth, driven by technological advancements, increasing vehicle complexity, and evolving consumer preferences. Key trends shaping the future include:

Adoption of Digital Tools: The use of digital estimating software, mobile applications, and online booking platforms is enhancing customer experience and operational efficiency.

Sustainability Initiatives: Repair shops are increasingly adopting eco-friendly practices, such as using water-based paints and recycling materials, to meet environmental standards and appeal to environmentally conscious consumers.

Mobile Repair Services: The rise of on-demand and mobile repair services offers convenience to customers, reducing downtime and providing cost-effective solutions for minor repairs.

Read Full Report: - https://www.uniprismmarketresearch.com/verticals/automotive-transportation/automotive-collision-repair

0 notes

Text

EV Battery Fire Protection Materials Market Future Trends Shaping Safety Innovations and Industry Growth

The EV battery fire protection materials market is poised for significant growth, driven by the surging demand for electric vehicles (EVs) and the pressing need for enhanced battery safety. As EV adoption accelerates globally, safety concerns surrounding battery fires have emerged as a critical challenge, prompting manufacturers and researchers to develop advanced fire protection materials tailored specifically for EV batteries. This article explores the future trends shaping the EV battery fire protection materials market, highlighting technological advancements, regulatory impacts, and key industry drivers.

Rising Importance of Battery Safety in EVs

The core of every electric vehicle is its battery pack, typically consisting of lithium-ion cells known for their high energy density. However, this high energy storage capacity comes with inherent risks, including thermal runaway, which can lead to catastrophic fires. These battery fires can be difficult to control and pose significant safety hazards to drivers, passengers, and first responders.

Consequently, the development of fire protection materials designed to prevent, delay, or mitigate the spread of fire in battery systems has become a priority. Materials such as fire-retardant coatings, insulating foams, and heat-resistant barriers are being integrated into battery packs to improve overall safety.

Future Trends Driving Market Growth

1. Advanced Fire-Resistant Materials

Innovations in materials science are leading to the creation of fire protection materials with superior thermal stability and flame-retardant properties. For example, ceramic-based coatings and intumescent materials that expand when exposed to heat can provide an effective barrier, limiting oxygen supply and reducing fire intensity. These materials not only protect battery cells but also enhance the structural integrity of the battery pack during fire incidents.

Nanotechnology is also playing a vital role by enabling the development of lightweight, high-performance fire-resistant composites that maintain the vehicle’s efficiency without adding excessive weight.

2. Integration of Smart Detection Systems

Beyond passive fire protection materials, the market is witnessing a trend towards integrating active safety systems within battery packs. These systems incorporate sensors and early fire detection technologies that can trigger cooling mechanisms or safely shut down battery operation at the first sign of thermal anomalies.

This holistic approach—combining fire protection materials with real-time monitoring—offers a more robust defense against battery fires, increasing confidence among manufacturers and consumers alike.

3. Stringent Regulatory Frameworks

Governments worldwide are implementing stringent regulations to ensure EV safety standards keep pace with industry growth. Regulatory bodies are mandating rigorous testing protocols for battery packs, including fire resistance and thermal management.

Compliance with these regulations requires automakers and battery manufacturers to invest in certified fire protection materials and technologies, fueling market demand. Moreover, safety certifications and standards are becoming key differentiators for companies competing in the EV sector.

4. Focus on Sustainable and Eco-Friendly Materials

As the EV market is closely tied to environmental sustainability, the development of eco-friendly fire protection materials is gaining momentum. Manufacturers are exploring bio-based and recyclable fire-retardant materials that reduce environmental impact while maintaining high safety performance.

Sustainability trends are likely to influence material selection and production processes, aligning with the broader green agenda of the electric vehicle industry.

5. Collaboration Between Material Scientists and Automotive OEMs

To accelerate innovation and market adoption, partnerships between material developers, battery manufacturers, and automotive original equipment manufacturers (OEMs) are becoming more common. These collaborations facilitate the integration of tailored fire protection solutions into EV battery designs early in the development process.

Joint research initiatives and pilot projects help validate the effectiveness of new materials under real-world conditions, expediting commercialization.

Market Challenges and Opportunities

While the market outlook for EV battery fire protection materials is optimistic, challenges remain. Cost considerations are a significant factor, as advanced fire protection materials can increase the overall cost of battery packs. Balancing cost, weight, and performance is critical to ensuring widespread adoption.

Furthermore, the rapid pace of battery technology innovation, such as solid-state batteries and alternative chemistries, requires fire protection materials to continuously adapt to new risks and specifications.