#Inheritance tax planning advice

Text

Discover essential advice on inheritance tax to help you understand your obligations and options. This resource covers key strategies for minimising tax liabilities, understanding exemptions, and planning your estate effectively. Equip yourself with the knowledge to protect your assets and ensure a smooth transfer to your beneficiaries.

#Inheritance tax planning#Inheritance tax advice#Inheritance tax advisor#Inheritance tax planning advice#Inheritance tax specialist#inheritance tax advice london

1 note

·

View note

Text

What is Inheritance Tax Planning Advice?

Inheritance tax planning advice is essential for managing the tax liabilities that may arise upon the transfer of an individual’s estate after their death. In the UK, inheritance tax (IHT) can significantly affect the value of what beneficiaries receive. This article will explore the intricacies of inheritance tax planning advice through eight question types, providing a comprehensive understanding of the subject.

1. What is Inheritance Tax?

Inheritance tax is a levy on the estate of someone who has died. In the UK, the standard inheritance tax rate is 40%, applied to the value of the estate above a certain threshold. As of 2024, this threshold, or nil-rate band, is £325,000. Estates valued above this amount are subject to inheritance tax, although various reliefs and exemptions can reduce the overall tax burden.

2. Why is Inheritance Tax Planning advice in Important?

Inheritance tax planning is crucial because it helps individuals legally minimize the tax liability on their estate, ensuring that more wealth is passed on to their beneficiaries. Without proper planning, a significant portion of an estate can be lost to taxation, which can be financially devastating for the heirs. Effective planning can also provide peace of mind, knowing that loved ones are cared for after one's passing.

3. How Can You Reduce Inheritance Tax Liability?

There are several strategies to reduce inheritance tax liability, including:

Utilizing the Nil-Rate Band: Ensuring the estate’s value remains below the £325,000 threshold.

Spousal Transfers: Assets transferred between spouses or civil partners are exempt from inheritance tax.

Gifts: Giving away assets during your lifetime can reduce the value of your estate, although rules apply.

Trusts: Setting up trusts can protect assets and reduce tax liabilities.

Charitable Donations: Leaving a portion of the estate to charity can reduce the inheritance tax rate.

4. Who Should Seek Inheritance Tax Planning Advice?

Anyone with an estate potentially liable for inheritance tax should consider seeking professional advice. This includes individuals with significant assets, business owners, and those with complex financial situations. Professional advice ensures that all available reliefs and exemptions are utilized and that the estate is structured in the most tax-efficient manner.

5. Where Can You Find Inheritance Tax Planning Advice in the UK?

Inheritance tax planning advice can be obtained from several sources in the UK:

Financial Advisors: Many financial advisors specialize in estate and tax planning.

Solicitors: Legal professionals can offer advice on wills, trusts, and estate planning.

Accountants: Accountants with expertise in tax can provide detailed guidance on minimizing tax liabilities.

Online Resources: Numerous websites and online tools offer valuable information and resources on inheritance tax planning.

6. What Are the Common Mistakes in Inheritance Tax Planning?

Common mistakes include:

Procrastination: Delaying estate planning can result in missed opportunities for tax savings.

Ignoring Potential Changes in Law: Tax laws can change, so it’s important to keep plans updated.

Overlooking Gifts and Exemptions: Failing to utilize annual gift allowances and other exemptions can result in higher tax liabilities.

Inadequate Documentation: Properly documenting all gifts and transfers is crucial for proving compliance with tax rules.

7. When Should You Start Inheritance Tax Planning?

It’s never too early to start inheritance tax planning. Ideally, individuals should begin planning as soon as they acquire significant assets. Early planning allows for a greater range of options and flexibility. Regular reviews and updates to the plan ensure it remains effective in light of changing personal circumstances and tax laws.

8. How Does Inheritance Tax Planning Impact Your Beneficiaries?

Effective inheritance tax planning ensures that beneficiaries receive the maximum possible value from an estate. It can prevent financial hardship and provide for the future needs of loved ones. Additionally, clear planning and communication can reduce the likelihood of disputes among beneficiaries and ensure that the estate is distributed according to the deceased’s wishes.

Conclusion

Inheritance tax planning advice is a vital component of managing one's estate in the UK. By understanding what inheritance tax is, why planning is important, and how to effectively reduce tax liabilities, individuals can safeguard their assets for future generations. Seeking professional advice, staying informed about tax laws, and starting planning early are key steps in ensuring that your estate is managed efficiently and your beneficiaries are well provided for.

0 notes

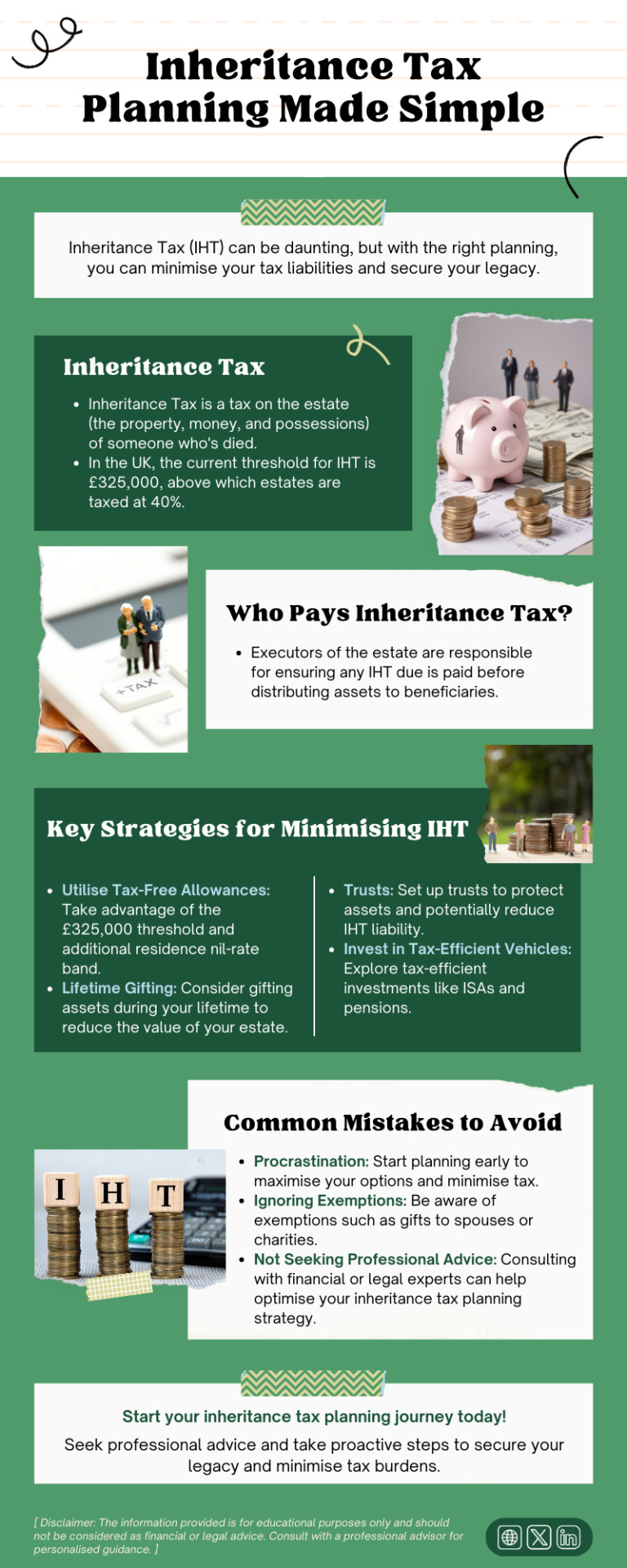

Text

Inheritance Tax (IHT) can be daunting, but with the right planning, you can minimise your tax liabilities and secure your legacy. This infographic provides a simple and straightforward guide to inheritance tax planning.

#Inheritance tax planning#Inheritance tax advice#Inheritance tax advisor#Inheritance tax specialist#inheritance tax advice london#Inheritancetaxplanning

2 notes

·

View notes

Text

Placing investments into a Family Investment Company (FIC) involves several key steps. First, establish the FIC as a private limited company, ensuring compliance with legal and regulatory requirements. Then, shareholders, typically family members, contribute capital to the company by purchasing shares.

These contributions can be in the form of cash, property, or other assets. The FIC then invests this capital in various assets, such as stocks, bonds, real estate, or other investment opportunities. It's crucial to have a clear investment strategy and governance structure, often outlined in a shareholders' agreement, to ensure alignment with family goals and values. Regular monitoring and management of the investments are essential, with professional advice recommended to optimize tax efficiency and compliance. This structure allows for centralized management of family wealth, succession planning, and potential tax advantages, making it a popular choice for wealth preservation and growth.

0 notes

Text

Inheritance Tax and What You Can Do To Reduce Your Liability

Inheritance tax (IHT) remains a topic that evokes confusion and concern for many individuals planning their estate. The complexities of the UK’s tax system make obtaining inheritance tax advice a crucial task. This blog describes 3 key strategies to effectively reduce any inheritance tax liability, namely:

Strategic Gifting

Contributing to a Pension and,

Optimising for Business Relief (BR) previously known as Business Property Relief (BPR)

To start off, let’s define Inheritance tax. Inheritance tax is a tax on the estate (the property, investments, and possessions) of someone who has passed away. An estate is not taxed on the first £325,000 known as the nil-rate band (NRB), this increases to £650,000 for a married couple or a couple in a civil partnership.

Furthermore, when passing on a home to direct descendants an estate can claim an additional exempt threshold known as the Residential Nil Rate Band (RNRB) which is a further allowance of £175,000 or £350,000 for a married couple. This means an individual can pass down £500,000 free of inheritance tax on their death, or if married, there’d be no inheritance tax to pay on first death if the beneficial interest passed to the surviving spouse, who could then use a total exempt threshold of £1,000,000, which will not be liable inheritance tax.

Anything above these allowances is taxed at a flat rate of 40%. This means most people in the UK will not face an inheritance tax liability. However, for those that do, there may be several options available to reduce this liability, but expert inheritance tax advice is needed. There are lots of moving parts.

Strategic Gifting

Lifetime gifting is a powerful strategy in IHT planning. By gifting assets during your lifetime, you can significantly reduce the value of your estate over time. There are several exemptions and allowances for gifts, including the:

Annual exemption – £3,000 per year

Small gifts exemption – £250 per person

Gifts in consideration of marriage or civil partnership – £5,000 for a child

These exemptions are too small to make a reasonable dent in a sizeable estate. This is where potential exempt transfers (PETs) and chargeable lifetime transfers (CLTs) come into play, both of which form critical components of inheritance tax advice. PETs refer to gifts made by an individual to another individual (not to a trust or a company) during their lifetime. A PET will only be exempt from inheritance tax if the donor lives for at least seven years after making the gift. There is no limit on how large a PET can be. CLTs refer to gifts made by an individual to a trust during their lifetime, which again, will only be exempt from inheritance tax if the donor survives at least seven years. There is no ‘limit’ per se on how large a CLT can be, however, it is common practice to limit CLTs to £325,000 every 7 years as anything above this would attract a lifetime inheritance tax charge of 20%. A further benefit of settling assets into a trust (CLT) vs. directly gifting to an individual (PET) is 3rd party protection. A gift to an individual will be at risk to divorce settlement claims, creditor claims and general financial mismanagement.

A gift to a trust, provided the trustees are managing the trust well, would provide far greater protection as a trust is a separate legal entity where the individual that the donor wants to benefit can be listed as a beneficiary of the trust, and the trust assets can be controlled by experts and only distributed in accordance with the trust deed and letters of wishes.

Pension Contributions

Pensions can be a potent tool in IHT planning, offering opportunities to pass on wealth outside of one’s estate, thus reducing an inheritance tax liability. A pensions’ primary use case is a vehicle to provide capital and income during retirement. However, if an individual can draw on other assets that are part of the estate first, such as cash, ISAs, and general investment accounts, then withdrawals from the pension can be deferred. In some cases, a pension can be left untouched as because it’s surplus to retirement income and capital needs and in such circumstances the pension becomes a great vehicle for passing on a tax-efficient legacy to chosen beneficiaries. Contributions to a pension attracts upfront tax relief and removes the cash invested from the estate immediately, making them an essential consideration in estate and financial planning.

Business Relief

Business Relief (BR) offers up to 100% relief from inheritance tax on business assets. Qualifying for BPR involves meeting specific criteria, such as holding the assets for at least two years, and ensuring the business is carrying out a trading activity. An investment activity is not considered a trading activity, therefore businesses primarily dealing in property letting and trading securities will not qualify for BPR.

If you own a trading business, it’s likely the shares you own will qualify for BR and the value of the shares will be exempt from inheritance tax. However, if there is any surplus cash on the balance sheet there is a risk this will be treated as an excepted asset. That is an asset that, despite being owned by the business, is not considered necessary for the future success of the business’s trading activities. This can impact the amount of BPR that can be claimed.

People approaching retirement typically look to sell their business. This is great from a cash flow point of view, as one can expect a generous windfall to fund their retirement needs. However, one loses the BR status of the shares sold with cash now sitting in their personal name which is liable to inheritance tax. To mitigate this one can explore deploying the proceeds into investments that qualify for BR such as:

Enterprise Investment Schemes (EIS) - Investments into UK start-ups and early-stage firms that attract very generous tax reliefs (including BR). This tends to be an investment into an unlisted company that in turn invests into crucial infrastructure projects. Provided you’re dealing with a mainstream provided these tend to have lower volatility than investing into an AIM IHT portfolio.

AIM IHT portfolios - Investments into AIM listed shares that qualify for BR.

Navigating the complexities of inheritance tax can seem overwhelming, but with the right inheritance tax advice and IHT planning, it’s possible to significantly reduce the tax burden on your estate. Effective estate planning allows you to pass on more of your wealth to your loved ones, highlighting the importance of seeking professional inheritance tax advice to guide you through the process. Whether it’s making strategic gifts, contributing to a pension scheme, or optimising for business property relief, each strategy offers a pathway to minimising inheritance tax and ensuring more of your estate passes to your children rather than the taxman.

Originally posted by - https://adlestateplanning.co.uk/inheritance-tax-and-what-you-can-do-to-reduce-your-liability/

0 notes

Text

Join Wills & Trusts for comprehensive seminars covering wealth management, from Wills and Inheritance Tax to Pensions and Investments. Our free seminars provide valuable insights into estate planning, ensuring you make informed decisions for your financial future. Learn from experts, gain clarity, and confidently plan your legacy.

#financial seminars#wealth management#estate planning#UK inheritance tax#investment advice#pension planning seminars#will preparation advice

0 notes

Text

Inheritance Tax Planning and Strategies | Inheritance-tax.co.uk

Inheritance tax planning and strategies are essential for anyone looking to protect their assets and pass them on to their loved ones. In the UK, inheritance tax is a tax paid by the inheritor on the value of their inheritance, and the more valuable the inheritance, the higher the tax paid. However, there are several ways to reduce or even eliminate inheritance tax, and we have outlined some of them below:

Use Trusts: Trusts are a legal arrangement between you and another person or organization that allows you to give property or money away without having to pay inheritance tax on it. There are several types of inheritance tax planning trusts you can use, including bare trusts, interest in possession trusts, discretionary trusts, accumulation trusts, mixed trusts, trusts for a vulnerable person, and non-resident trusts.

Life Insurance Policy: A life insurance policy can help to pay any inheritance tax due, and placing your policy in a trust can help to ensure that it is not included in your estate for inheritance tax purposes.

Make Pension Plans: Pensions are not included in your estate for inheritance tax purposes, and by making pension plans, you can pay only 20% tax at retirement, as opposed to 40% inheritance tax. You can decide whether to withdraw your pension starting at age 55 or pass it on as an inheritance.

Give Away Gifts: You can give away gifts amounting to £3,000 each tax year, and these gifts will be counted toward your inheritance tax exemption. This can be an effective way to keep your estate tax-free over time.

Donate to Charity: Donating to charity is an excellent way to reduce your inheritance tax liability. Your estate won’t be subject to inheritance tax on anything you leave to charity, and the inheritance tax charged on the remaining part of your estate is reduced from 40% to 36% if you decide to donate at least 10% of your assets to charity.

Alternate Investments Market (AIM): The AIM is a market where you can invest in shares of smaller companies that are not listed on the main stock exchange. By investing in AIM shares that qualify for Business Relief, you can reduce the amount of inheritance tax due on your wealth.

Utilize Business Reliefs: Business reliefs enable you to remove your assets from your estate, relieving you of the burden of inheritance tax. By holding onto your assets for a few years, you can use business reliefs to remove them from your estate.

Overall, it's important to work with a trusted inheritance tax professional for inheritance tax planning advice. They can help you navigate the complex landscape of inheritance tax planning and ensure that your loved ones can pass on their assets without undue financial stress.

For More Information Visit Us: https://inheritance-tax.co.uk/area/inheritance-tax-planning-and-strategies/

#inheritance tax#inheritance#inheritance tax planning#tax planning#tax#property tax#finance#business#planning#inheritance tax specialist#planning and strategies#Estate planning#Paying Inheritance Tax#reduce the inheritance tax#calculate your taxable estate#calculated your taxable estate#inheritance tax advice#inheritance tax advice in London

0 notes

Text

Get the Best Inheritance Planning in UK

Ensure your legacy is protected with expert inheritance planning in the UK. Our tailored strategies will help minimize inheritance tax and maximize the value of your assets for your loved ones. Visit us now to secure your family's future.

1 note

·

View note

Text

Managing Wealth and Inheritance: Estate and Trust Administration Attorneys

Wealth management and estate planning are vital to preserving and growing your family's legacy. As individuals accumulate assets over time, it becomes essential to consider how those assets will be managed and passed on to future generations. Estate and trust administration attorneys play a pivotal role in this process by offering expert legal guidance. In this blog, we’ll explore the importance of estate and trust administration, the responsibilities of attorneys in these areas, and how they can help you protect your wealth and legacy for the long term.

Understanding Estate and Trust Administration

Estate administration refers to managing and distributing a person's assets after they pass away. This includes ensuring that debts are paid, taxes are filed, and remaining assets are transferred to beneficiaries by the deceased's will or applicable state law if there is no will. The process can be complex, especially if there are significant assets or if disputes arise among heirs.

Trust administration, on the other hand, involves managing the assets held within a trust according to the terms set out in the trust document. Trusts are often used as a tool to minimize estate taxes, avoid probate, and provide a structured distribution of assets over time. Trusts can be beneficial in cases where the grantor wants to ensure that beneficiaries, such as young children or those with special needs, receive ongoing financial support.

The Role of Estate and Trust Administration Attorneys

An estate attorney and trust administration attorney is a legal professional who specializes in helping clients manage and distribute their assets efficiently and according to their wishes. These attorneys play several critical roles throughout the process, including:

Legal Guidance and Compliance: Estate and trust laws can be intricate, and they often vary by jurisdiction. An experienced attorney ensures that all legal requirements are met and that the estate or trust complies with state and federal laws. This includes filing necessary paperwork, handling tax issues, and ensuring the terms of the will or trust are carried out correctly.

Asset Management and Distribution: One of the primary responsibilities of an estate and trust administration attorney is to oversee the proper distribution of assets. This can involve coordinating with financial institutions, ensuring that creditors are paid, and ensuring beneficiaries receive their inheritance as intended.

Probate Avoidance and Minimizing Tax Liability: Probate, the legal process of validating a will and distributing assets, can be lengthy, expensive, and stressful for families. Estate and trust administration attorneys can help design strategies to minimize or avoid probate altogether. Additionally, they provide valuable advice on reducing estate taxes, preserving wealth for beneficiaries.

Dispute Resolution: Unfortunately, disputes can arise during estate and trust administration, whether between heirs or regarding the validity of a will or trust. Attorneys act as mediators and legal advocates, working to resolve conflicts and ensure a fair outcome for all parties involved.

Trustee Support and Guidance: For individuals named as trustees (those responsible for managing the trust), the role can be daunting, as they have fiduciary duties to the beneficiaries. A trust administration attorney helps trustees navigate their responsibilities, from managing assets to making distributions and ensures they fulfill their obligations according to the terms of the trust.

Why You Need an Estate and Trust Administration Attorney

While it may be tempting to manage estate and trust administration on your own, especially for smaller estates, the potential pitfalls of doing so without professional guidance are numerous. Here’s why having an attorney by your side is crucial:

Complex Legal Framework: Estate and trust laws are complex and constantly evolving. Understanding the intricacies of probate, taxes, and legal obligations can be overwhelming for someone without legal training. An attorney ensures that every detail is addressed, reducing the risk of mistakes that could delay the process or lead to legal issues down the road.

Time and Stress Reduction: Managing an estate or trust is time-consuming and emotionally taxing, particularly for family members grieving the loss of a loved one. By hiring an attorney, you can delegate much of the administrative work, allowing you to focus on supporting your family during a difficult time.

Avoiding Costly Errors: Mishandling estate or trust administration can result in costly penalties, tax issues, or even lawsuits from disgruntled beneficiaries. An attorney ensures that every step of the process is completed correctly and efficiently, minimizing the risk of expensive errors.

Expert Tax Advice: Estate taxes, inheritance taxes, and capital gains taxes can quickly erode the value of an estate. Estate and trust administration attorneys are well-versed in tax laws and can help structure the estate in a way that minimizes tax liabilities and preserves as much wealth as possible for the beneficiaries.

Safeguarding Beneficiaries' Interests: One of the most important roles of an attorney is to ensure that the wishes of the deceased are honored and that the beneficiaries' interests are protected. Whether by defending the validity of a will in court or ensuring that the trustee follows the terms of the trust, an attorney acts as a guardian of the estate plan’s integrity.

Key Considerations When Choosing an Estate and Trust Administration Attorney

When selecting an attorney to assist with estate and trust administration, it’s important to consider a few key factors:

Experience and Expertise: Look for an attorney who specializes in estate and trust law and has a proven track record in handling cases similar to yours. Experience is especially crucial if the estate is large, complex, or involves high-value assets.

Communication and Transparency: A good attorney will keep you informed throughout the process and provide clear explanations of each step. Make sure you choose someone who is accessible and responsive to your needs.

Fee Structure: Estate and trust administration attorneys typically charge either a flat fee, hourly rate, or a percentage of the estate’s value. It’s important to understand the attorney’s fee structure upfront and ensure it aligns with your budget.

Conclusion

Managing wealth and inheritance through estate and trust administration can be a daunting task, but with the right attorney by your side, the process becomes much more manageable. Estate and trust administration attorneys offer invaluable expertise in navigating the complex legal landscape, ensuring that your assets are protected and distributed according to your wishes. By working with a skilled attorney, you can safeguard your family’s future and leave behind a lasting legacy that reflects your values and intentions.

2 notes

·

View notes

Note

】 - Do you have anything in life you are particularly garetful for?

Positivity Munday meme - No Longer Accepting!

This is going to sound predictable/cheesy, but I'm going to say my parents. Yes, they've been able to provide a lot of opportunities for me, but I want to say I'm grateful for one thing in particular:

They have invested well, never have lived outside of their means, and saved well for retirement to include any and all in-house help they may need in their more infirm/frail years, including taking out substantial life insurance policies, writing their wills, and making very clear and specific financial trusts.

The older I get, the more I hear of friends whose parents decline rapidly or lose one or both parents and are just stuck with so much to deal with: how to afford a retirement home and/or specialized care they need (some friends have had to take part time or quit their jobs entirely to care for their aging parents), how to organize end of life decisions, how to deal with paying off debts and/or taxes on various inheritances/bequests, and that doesn't even begin to factor in the emotional toll taken on the members of the family left behind.

My parents have thought of pretty much every little thing that I will likely face as they decline and after they die, with specific instructions on how to handle everything and where everything goes. I am so grateful for that, knowing that I will not have to wonder how I'll take care of them and what to do with all of the stuff that's left to handle after they pass.

That said, my advice to my dash: if you have living parents or guardians and you have not talked to them about what will happen if, or more aptly when, they decline and pass on, the earlier you can begin making plans, the better. I keep seeing too many stories of friends who are emotionally and financially bankrupt trying to take care of their aging parents, who will likely never recover from it all, or take many years to finally begin to mend. It's not the most pleasant thing to think about, but there's only two guarantees in life: death and taxes.

Knowing how to do taxes or hiring someone you trust to do them for you is also good life advice

#more-than-a-princess answered#more-than-a-princess musings#mechatiqe#tw: death#tw: family death#(Positivity Munday meme)#(A part of me wants to apologize for the serious answer to this ask)#(But it's been on my mind a lot lately. Especially the past few years)#(As my offline friends group. Including me. is rapidly moving into late-thirties and beyond)

5 notes

·

View notes

Text

When your day job merges with your obsession....

--------------------------

Dear Gabriel

Overview / Inheritance and Succession Planning

Further to our recent meeting at the mansion, you were referred to me for advice in relation to setting up a suitable plan for passing on your inheritance as well as ensuring that your son Adrien (14) is looked after, following your death, where you have confirmed that you only have a few weeks left to live.

You confirmed that you have tried all forms of medical intervention, even time travel. However, this only worsened your condition.

I want to thank you for taking me into your confidence, as your circumstances are highly delicate. This letter will now summarise the key points of our discussion.

Background

You are 45 and widowed, your only child being Adrien. You work as a fashion designer and head the internationally successful Gabriel brand, in addition to your recent business ventures with Tomoe Tsurugi, including the smart ring / personal assistant device Alliance.

Your main residence is fully unencumbered and valued at c €40m, while your net worth is estimated at around €11 bn.

You have few liabilities, aside from business costs, although you noted that you recently spent €100m constructing sensory deprivation rooms in London for Adrien and Tomoe’s daughter Kagami, to ‘keep them out of harm’s way’ as you initiate your final business enterprise.

We agreed it was ‘not worth your time’ to undertake a full income and expenditure analysis. Suffice to say, you generate substantial surplus income each and every month to fund your lifestyle.

You are in the process of drafting a new will, leaving a portion to Tomoe, nominal amounts to your staff including Adrien’s bodyguard, and the remaining estate to Adrien.

As Adrien is a minor, his inheritance will be placed into trust until he attains age 18. Previously, you willed guardianship of Adrien to your assistant, Nathalie Sancoeur. However, due to personal differences, as well as her own failing health, you will now determine a new guardian, potentially your sister-in-law Amelie, who resides in London, although you are not on good terms and you are concerned that your nephew Felix is a ‘bad influence’.

You will also nominate someone to take over the Gabriel brand, as Adrien has expressed that he does not wish to continue in the fashion industry, having resigned as a model.

On a more personal note, you play piano, you are a keen fencer, and you recently took up cooking – thank you for the pancakes! You also enjoy the occasional game of golf.

Objectives

These are all very short-term, due to your unfortunate terminal illness:

Obtain the ladybug and cat miraculous

Bring your wife Emilie back from the dead

Ensure Adrien is looked after

Ensure Adrien marries the girl you have selected for him – namely, Kagami

Remove Marinette Dupain-Cheng from Adrien’s life ‘permanently’

Minimise the level of inheritance tax that will be payable by Adrien upon your passing, wherever possible

Arrange life cover for Adrien, to ensure the estate is not lost should someone wish to ‘make him disappear’

Ensure the miracle box and associated kwamis are passed on to a new guardian, after your passing – potentially to Adrien, although this would involve a difficult conversation with him, to spare him learning your secrets posthumously

Protect your secret identity as Hawk Moth / Shadow Moth / Monarch after your passing – this will entail some costs, as you will need to dismantle the missile security system in ‘the dome’ and seal off the underground lair in the secret basement

Should you not succeed in reviving Emilie, you will need to relocate her body, to ensure she can remain in suspended animation – you also wish to ensure that your mission for revival is picked up by a successor, namely Tomoe

Ensure the security of the ring that controls Adrien

Totally random - Keep reading at Ao3

#ml fanfic#ml fic#ml gabriel#Gabriel Agreste's A+ Parenting#ml adrien#adrien agreste#ml kagami#ml felix#ml representation#crack fic#crack treated seriously

9 notes

·

View notes

Text

Understanding Inheritance Tax Planning Advice: A Comprehensive Guide

Introduction:

Inheritance tax (IHT) can significantly impact the assets passed down to loved ones after someone passes away. However, with proper planning and advice, individuals can minimize the tax burden on their estate. Let's explore what inheritance tax planning advice entails and how it can benefit you and your family.

How Inheritance Tax Planning Works:

Inheritance tax planning advice involves arranging your finances and assets in a way that minimizes the amount of tax payable on your estate after your death. It aims to maximize the value of the inheritance you leave behind for your beneficiaries.

How to Assess Your Inheritance Tax Liability:

The first step in inheritance tax planning is to assess the value of your estate and determine your potential tax liability. This includes calculating the value of your property, savings, investments, and any other assets you own.

How Inheritance Tax Exemptions and Reliefs Work:

Understanding inheritance tax exemptions and reliefs is essential for effective tax planning. These provisions allow certain assets or transfers to be excluded from the calculation of inheritance tax, thereby reducing the overall tax liability.

How to Utilize Annual Gift Allowances:

One strategy for minimizing inheritance tax is to take advantage of annual gift allowances. These allowances enable you to gift assets or money to your loved ones tax-free up to a certain limit each year.

How Trusts Can Help with Inheritance Planning:

Setting up trusts can be a valuable tool in inheritance tax planning. By transferring assets into a trust, you can remove them from your estate for inheritance tax purposes while still retaining control over how they are managed and distributed.

How to Make Use of Spousal and Charitable Exemptions:

Married couples and civil partners benefit from spousal exemptions, which allow them to pass assets to each other free of inheritance tax. Additionally, charitable donations made in your will or during your lifetime are exempt from inheritance tax.

How to Plan for Business and Agricultural Assets:

Business and agricultural assets may qualify for special reliefs, such as business property relief (BPR) and agricultural property relief (APR), which can reduce or eliminate their inheritance tax liability. Proper planning is crucial to ensure these reliefs are maximized.

How to Structure Life Insurance Policies:

Life insurance policies can play a role in inheritance tax planning by providing funds to cover any tax liabilities without depleting the estate's assets. Setting up policies in trust can ensure that the proceeds are not subject to inheritance tax.

How to Seek Professional Advice:

Given the complexities of inheritance tax planning, seeking professional advice from a qualified financial advisor or estate planning specialist is highly recommended. They can assess your individual circumstances and recommend tailored strategies to minimize your tax liability.

How to Review and Update Your Plan Regularly:

Inheritance tax planning is not a one-time task but an ongoing process. It's essential to review and update your plan regularly to account for changes in your financial situation, tax laws, and personal circumstances.

Conclusion:

Inheritance tax planning advice is vital for anyone concerned about minimizing the tax burden on their estate and maximizing the inheritance they leave behind for their loved ones. By understanding the various strategies and exemptions available and seeking professional advice when needed, individuals can ensure that their assets are passed down as efficiently as possible. Start planning today to secure your family's financial future.

0 notes

Text

Men and women have very different approaches to money — and that affects how they pass on wealth to their children.

Many women look beyond their family when thinking about what to do with their wealth, according to a new report from UBS that compiled surveys and data from the Swiss Bank and other sources.

“For women, legacy often means more than passing wealth down to the next generation; it also means being capable of positively impacting the lives of others,” Marianna Mamou, head of “advice beyond investing” at UBS Global Wealth Management, told CNBC Make It.

For example, the way women invest their wealth is often aligned with their personal values or in service of causes. Those could be anything from supporting charities to helping their heirs start a business they believe in or purchase a home, the report says.

Women also view their wealth overall in a specific way according to the report.

“Women tend to perceive and value wealth mainly as a source of security and tend to focus on being financially secure and able to afford a certain lifestyle for themselves and their loved ones over the long term,” it says.

How women pass on their wealth

Women also tackle questions about how to pass on their wealth to their heirs differently from men, the report noted.

As for the question of when to pass on wealth, the differences between men and women are especially pronounced, the report found, citing data from the 2022 UBS Investor Watch survey.

“More women prefer to wait and pass on wealth after their death as they don’t want their heirs to worry about their health. In addition, more women than men worry about disputes between heirs,” Mamou says.

For example, 44% of women are concerned about the latter point, compared to 37% of men.

“Another reason that women prefer to delay handover of wealth while they are alive is that they want to remain flexible,” Mamou adds. Sixty-three percent of women and 53% of men gave this reason in the UBS survey.

When it comes to arguments for passing on assets while they’re still alive, 66% of women say younger generations already need monetary support, compared to 61% of men. They are also slightly more motivated by educating heirs about handling wealth.

Men, on the other hand, are more likely to transfer money before their death for tax reasons (65% of men and 61% of women said this) or to watch their heirs make use of it.

Succession planning

The gender differences don’t stop there.

In addition to women being unsure about how much wealth they can pass on, the report found that one of the reasons they are hesitant to do so before they die is that they aren’t sure how.

“There is a gender gap in the understanding around succession planning,” the report concludes.

Getting expert advice — including on how to invest in a way that ensures wealth growth is balanced with values — and making plans sooner rather than later are therefore key, the report says.

One thing that might help with this is that women say they find it easier than men to talk about money with their families, according to UBS data. Such discussions around wealth can also help with concerns like conflicts around inheritance and financial skills, Mamou adds.

“Including younger generations in investment decisions should lead to a smoother transfer of wealth with fewer surprises. Furthermore, incorporating sustainable investing solutions can also be a great way to engage with, and bring in, the next generation,” she says.

“Investing together with the next generation provides a great opportunity to pass on the values and financial lessons that matter when the next generation comes of age.”

A final point the report makes is that women often outlive — and therefore inherit money from — men. That means they have more wealth to transfer to the next generation — making plans and conversations about this even more important.

13 notes

·

View notes

Text

youtube

This video delves into multiple strategies for transferring cash and other assets into a trust, covering topics such as opening a bank account in the trust's name, transferring share portfolios by renaming brokerage accounts, the significance of a deed of assignment, and the legal and tax considerations of such transfers. It's crucial to consult with experienced legal professionals to fully grasp the implications and procedures involved.

#IHT#Tax#Trust#trust planning#inheritance tax planning#tax planning#estate planning#tax advice#Youtube

0 notes

Text

Why Inheritance Tax Planning is Crucial for Your Financial Future in the UK

Inheritance tax planning is not merely a consideration but a necessity for anyone looking to manage their estate effectively. The concept of inheritance tax (IHT) centres around the tax your estate owes upon your death, if the value exceeds certain thresholds set by the government. Understanding the basics of inheritance tax and its implications is crucial, as it directly impacts the legacy you leave behind for your loved ones.

The mechanics of inheritance tax involve several key elements, including thresholds, rates, and available reliefs. Currently, the IHT threshold, also known as the nil-rate band, stands at £325,000 for individuals. This means that estates valued below this figure are exempt from inheritance tax. For estates exceeding this value, the standard IHT rate applied is 40%. However, strategic inheritance tax planning can significantly reduce this liability, leveraging various reliefs such as the spousal exemption and business property relief (BPR). As well as strategic gifting to individuals or trusts during lifetime.

Inheritance tax can affect various types of assets within an estate, from real estate and investments to personal chattels. Real estate, often the most valuable asset individuals own, can significantly increase the overall value of an estate, potentially leading to a sizable inheritance tax bill. Similarly, investments and businesses that do not qualify for BPR (such as companies that own residential property) are also assessable for IHT purposes. Understanding the impact of inheritance tax on these assets is pivotal in inheritance tax & estate planning advice, ensuring beneficiaries receive the maximum possible from their inheritance.

Effective inheritance tax planning involves maximizing your available allowances to minimise the IHT liability. The nil-rate band offers an opportunity to pass on assets up to £325,000 tax-free. For married couples and civil partners, this allowance can be transferred, effectively doubling the nil-rate band to £650,000. Moreover, the residence nil-rate band (RNRB) provides an additional allowance of £175,000 for individuals, and £350,000 for married couples, when passing on a family home to direct descendants. However, the RNRB is tapered down by £1 for every £2 the estate value exceeds £2,000,000, underlining the importance of thorough planning and understanding of these allowances in inheritance tax planning.

For property owners, inheritance tax planning encompasses several innovative strategies to mitigate tax liabilities. A Holdover Gift Trust can offer a structured way to manage and pass on equity in property efficiently, potentially reducing the inheritance tax burden and deferring any capital gains tax liability. Rental income is given up using this strategy though, so section 102 (b)(iii) planning may be a more suitable option if rental income is still required. If an individual, or couple, own a significant amount in property, then structuring the property in a clever alphabet share class company would offer the ideal solution to optimise against inheritance tax. There are several options available to property owners, however, it is critical to seek inheritance tax & estate planning advice as there are different tax implications for each solution that needs to be considered carefully.

At the heart of inheritance tax planning is the creation of a Will, a fundamental document that dictates the distribution of your estate according to your wishes. Without a Will, your estate is subject to the rules of intestacy, which may not align with your intentions. Additionally, Immediate Post-Death Interest (IPDI) trusts represent a sophisticated planning tool, allowing for greater control over how and when assets are distributed, providing a tax-efficient way to manage inheritance.

In conclusion, inheritance tax planning is an indispensable element of financial and estate management. It ensures your assets are passed on to your beneficiaries in the most tax-efficient manner possible. By understanding the nuances of inheritance tax, from thresholds and rates to the impact on different assets, individuals can craft a strategy that aligns with their goals. Maximising allowances, utilising reliefs, strategic gifting, and ensuring the proper legal foundations are in place via a Will and IPDI trusts are all critical steps in safeguarding your estate for future generations. With the right inheritance tax & estate planning advice, you can secure your financial legacy and provide for your loved ones long after you’re gone.

Originally posted by - https://adlestateplanning.co.uk/

0 notes

Text

Tax advisory services in UK

The UK tax system, with its intricacies and constant updates, can feel like a labyrinth for individuals and businesses alike. One wrong turn, and you could find yourself entangled in unexpected liabilities. That's where Masllp's expert Tax advisory services in UK come in – your trusted guide to navigating the maze and emerging with both your sanity and finances intact.

Why Choose Masllp?

Comprehensive Expertise: Our team boasts seasoned tax professionals with extensive knowledge of UK tax law, covering everything from individual income tax to complex corporate structures. No matter your tax needs, we have the expertise to handle them.

Personalized Approach: We understand that your tax situation is unique. We take the time to understand your specific circumstances and tailor our advice to your individual needs and goals.

Proactive Planning: We don't just react to the latest tax changes; we anticipate them. We work with you to develop proactive tax strategies that minimize your liabilities and maximize your financial advantage in the long run.

Compliance Confidence: Rest assured, with Masllp by your side, you'll stay compliant with all HMRC regulations. We handle all your tax filings and representations, ensuring you meet deadlines and avoid penalties.

Stress-Free Experience: We take the burden of taxes off your shoulders. We handle the complex forms, negotiations, and communication with HMRC, so you can focus on what you do best.

Our Services:

Individual Tax Returns: We ensure you claim all eligible allowances and deductions, leaving you with the maximum return.

Self-Assessment Support: Navigating self-assessment can be daunting. We guide you through the process, ensuring accuracy and minimizing your tax bill.

Corporate Tax Planning: We help you optimize your business structure and operations to minimize your corporate tax liability.

VAT Registration and Returns: We handle the VAT registration process and ensure your quarterly returns are filed accurately and on time.

Inheritance Tax Planning: Preserving your wealth for future generations is crucial. We help you develop strategies to minimize inheritance tax and protect your loved ones.

International Tax Advice: Operating cross-border? We have the expertise to navigate the complexities of international tax law and ensure your compliance.

Investing in your tax future:

Investing in Masllp's Tax advisory services in UK is an investment in your financial security and peace of mind. We partner with you to unlock tax efficiencies, optimize your financial decisions, and ensure you stay on the right side of HMRC.

Contact Masllp today:

Don't let the UK tax labyrinth overwhelm you. Take the first step towards a clearer tax future. Contact Masllp today for a free consultation and discover how our expert Tax advisory services in UK can guide you to financial success.

Remember, with Masllp, you're not just navigating the tax labyrinth – you're conquering it.

I hope this gives you a good starting point for your blog!

Tax advisory services in UK | Tax advisory services

#audit#accounting & bookkeeping services in india#ajsh#income tax#auditor#businessregistration#chartered accountant#foreign companies registration in india#taxation#Tax advisory services in UK | Tax advisory services

2 notes

·

View notes

Last Seen Blogs

lechugasblog

☆Lechuga☆

milk-luvr-dot-com

Let's see Paul Allen's tumblr page!

bloom-edits

bloom edits 🏐

mywifesindependence

Hotwife

ramonarappaport-blog

black sheep