#Peer-to-peer lending blockchain

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr was created by web developers David Karp and Marco Arment.

Text

Can Blockchain Technology Improve Personal Loan Approvals?

The financial sector is rapidly evolving with new technologies, and blockchain is one of the most promising innovations transforming the personal loan industry. Traditionally, loan approvals have been time-consuming, requiring manual document verification, credit score analysis, and financial background checks. Blockchain technology is changing this by making the process faster, more secure, and more transparent.

With blockchain, lenders can streamline identity verification, enhance credit risk assessment, and prevent fraud, making personal loans more accessible and efficient. In this article, we explore how blockchain is improving loan approvals and why it could be the future of digital lending.

🔗 For hassle-free personal loan applications, visit FinCrif Personal Loan.

1. How Blockchain Enhances Loan Approvals

Faster and More Reliable Identity Verification

One of the biggest hurdles in personal loan approvals is verifying a borrower’s identity. Traditional Know Your Customer (KYC) processes require applicants to submit documents such as Aadhaar, PAN, and bank statements, which banks manually verify. This process can take several days, causing delays.

Blockchain eliminates redundant verification by storing identity records in a tamper-proof, decentralized ledger. Once an identity is verified and recorded on the blockchain, it can be accessed by lenders instantly, reducing processing time and ensuring authenticity.

Alternative Credit Scoring for Faster Loan Approvals

Many individuals struggle to get personal loans due to a lack of credit history or low CIBIL scores. Traditional lenders primarily rely on credit bureau scores, which do not always provide a complete picture of a borrower's financial behavior.

Blockchain allows lenders to use alternative data sources, such as utility bill payments, mobile phone transactions, and online spending patterns, to assess creditworthiness. This makes personal loans accessible to self-employed individuals, gig workers, and those without a strong credit history.

Automated Loan Processing with Smart Contracts

A smart contract is a self-executing agreement stored on a blockchain that automatically enforces the terms of a loan when certain conditions are met. These contracts eliminate the need for human intervention, making loan approvals much faster.

For example, once a borrower's identity and financial records are verified, a smart contract can instantly approve the loan and trigger fund disbursement. This removes bureaucratic delays, helping borrowers access funds within minutes instead of days.

2. Improved Security and Fraud Prevention

Prevention of Identity Theft and Fake Applications

One of the biggest challenges in personal lending is fraud. Many loan scams involve forged documents, fake identities, or manipulated financial records. Blockchain prevents fraud by ensuring that all transactions and data entries are permanent, transparent, and tamper-proof.

Lenders can verify borrower details on a shared blockchain network, making it impossible for fraudsters to manipulate loan applications. This enhances trust and reduces the risk of defaults.

Eliminating Credit Report Manipulation

In the current system, borrowers can sometimes manipulate their credit reports by temporarily improving their credit utilization before applying for a loan. Blockchain stores real-time financial data, making it impossible to alter past records. This ensures that lenders always have an accurate financial picture of borrowers, reducing lending risks.

3. Faster Loan Disbursement with Blockchain

In traditional lending, once a loan is approved, it may take several days for funds to be transferred due to interbank processes and verification checks. Blockchain speeds up disbursal by enabling direct peer-to-peer transactions without intermediary banks.

With blockchain-based digital wallets, borrowers can receive loan amounts instantly after approval, making it a game-changer for emergency loans and urgent financial needs.

🔗 Looking for a quick loan disbursal? Explore FinCrif Personal Loan.

4. Transparency and Reduced Loan Processing Costs

Lower Processing Fees for Borrowers

Loan processing involves multiple intermediaries, such as credit bureaus, third-party verifiers, and bank officers, each adding costs that are passed on to borrowers. Blockchain eliminates many of these middlemen by automating verification and reducing paperwork.

This leads to lower processing fees and better interest rates, making personal loans more affordable.

Complete Transparency in Loan Terms

Many borrowers struggle with hidden charges, fluctuating interest rates, and complex loan agreements. Blockchain ensures absolute transparency by recording all loan terms on an immutable ledger. Borrowers can access their loan history, EMI schedules, and outstanding balances without worrying about unexpected changes in loan conditions.

5. Challenges in Implementing Blockchain for Personal Loans

Despite its advantages, blockchain adoption in personal lending faces challenges, including regulatory concerns and technical barriers.

Regulatory Uncertainty: Many governments are still developing policies on blockchain-based lending, which slows adoption.

Integration with Existing Banking Systems: Most financial institutions operate on centralized databases, making integration with decentralized blockchain networks complex.

User Awareness: Many borrowers are unfamiliar with blockchain technology and may hesitate to trust a fully automated loan approval system.

However, as blockchain regulations become clearer and financial institutions invest in digital transformation, these challenges are expected to decrease.

6. The Future of Blockchain in Personal Loan Approvals

As blockchain technology continues to evolve, it will play an even bigger role in making personal loans more accessible, secure, and efficient. Some expected advancements include:

Instant Global Loan Access: Borrowers will be able to apply for and receive loans across borders without waiting for traditional bank approvals.

AI and Blockchain Integration: Combining artificial intelligence with blockchain will further enhance loan approvals by analyzing borrower behavior in real-time.

Decentralized Lending Platforms: More peer-to-peer (P2P) lending models will emerge, allowing borrowers to connect directly with lenders, bypassing traditional banks.

🔗 Be part of the future of lending! Explore AI-powered loan solutions at FinCrif Personal Loan.

Blockchain technology has the potential to redefine personal loan approvals by making them faster, more transparent, and secure. By reducing reliance on credit bureaus, enabling instant identity verification, and preventing fraud, blockchain can improve financial accessibility for millions of borrowers.

While challenges remain, the future of personal lending is increasingly digital. As blockchain adoption grows, borrowers can expect lower costs, faster approvals, and a more efficient lending experience.

For a seamless and secure personal loan application, visit FinCrif Personal Loan and explore the latest AI-driven financial solutions.

#Blockchain in personal loans#Blockchain loan approval#Blockchain technology in lending#Personal loan blockchain#Faster loan approvals with blockchain#Blockchain-based lending#Secure loan processing#Decentralized lending platforms#Smart contracts for loans#Instant loan approvals#How blockchain improves lending#Blockchain in financial services#Digital lending with blockchain#Alternative credit scoring with blockchain#AI and blockchain in loans#Fraud prevention in personal loans#Transparent loan processing#Peer-to-peer lending blockchain#Future of blockchain in banking#Secure identity verification for loans#finance#loan apps#personal loans#loan services#personal loan#fincrif#personal loan online#nbfc personal loan#bank#personal laon

0 notes

Text

The Rise of DeFi: Revolutionizing the Financial Landscape

Decentralized Finance (DeFi) has emerged as one of the most transformative sectors within the cryptocurrency industry. By leveraging blockchain technology, DeFi aims to recreate and improve upon traditional financial systems, offering a more inclusive, transparent, and efficient financial ecosystem. This article explores the fundamental aspects of DeFi, its key components, benefits, challenges, and notable projects, including a brief mention of Sexy Meme Coin.

What is DeFi?

DeFi stands for Decentralized Finance, a movement that utilizes blockchain technology to build an open and permissionless financial system. Unlike traditional financial systems that rely on centralized intermediaries like banks and brokerages, DeFi operates on decentralized networks, allowing users to interact directly with financial services. This decentralization is achieved through smart contracts, which are self-executing contracts with the terms of the agreement directly written into code.

Key Components of DeFi

Decentralized Exchanges (DEXs): DEXs allow users to trade cryptocurrencies directly with one another without the need for a central authority. Platforms like Uniswap, SushiSwap, and PancakeSwap have gained popularity for their ability to provide liquidity and facilitate peer-to-peer trading.

Lending and Borrowing Platforms: DeFi lending platforms like Aave, Compound, and MakerDAO enable users to lend their assets to earn interest or borrow assets by providing collateral. These platforms use smart contracts to automate the lending process, ensuring transparency and efficiency.

Stablecoins: Stablecoins are cryptocurrencies pegged to stable assets like fiat currencies to reduce volatility. They are crucial for DeFi as they provide a stable medium of exchange and store of value. Popular stablecoins include Tether (USDT), USD Coin (USDC), and Dai (DAI).

Yield Farming and Liquidity Mining: Yield farming involves providing liquidity to DeFi protocols in exchange for rewards, often in the form of additional tokens. Liquidity mining is a similar concept where users earn rewards for providing liquidity to specific pools. These practices incentivize participation and enhance liquidity within the DeFi ecosystem.

Insurance Protocols: DeFi insurance protocols like Nexus Mutual and Cover Protocol offer coverage against risks such as smart contract failures and hacks. These platforms aim to provide users with security and peace of mind when engaging with DeFi services.

Benefits of DeFi

Financial Inclusion: DeFi opens up access to financial services for individuals who are unbanked or underbanked, particularly in regions with limited access to traditional banking infrastructure. Anyone with an internet connection can participate in DeFi, democratizing access to financial services.

Transparency and Trust: DeFi operates on public blockchains, providing transparency for all transactions. This transparency reduces the need for trust in intermediaries and allows users to verify and audit transactions independently.

Efficiency and Speed: DeFi eliminates the need for intermediaries, reducing costs and increasing the speed of transactions. Smart contracts automate processes that would typically require manual intervention, enhancing efficiency.

Innovation and Flexibility: The open-source nature of DeFi allows developers to innovate and build new financial products and services. This continuous innovation leads to the creation of diverse and flexible financial instruments.

Challenges Facing DeFi

Security Risks: DeFi platforms are susceptible to hacks, bugs, and vulnerabilities in smart contracts. High-profile incidents, such as the DAO hack and the recent exploits on various DeFi platforms, highlight the need for robust security measures.

Regulatory Uncertainty: The regulatory environment for DeFi is still evolving, with governments and regulators grappling with how to address the unique challenges posed by decentralized financial systems. This uncertainty can impact the growth and adoption of DeFi.

Scalability: DeFi platforms often face scalability issues, particularly on congested blockchain networks like Ethereum. High gas fees and slow transaction times can hinder the user experience and limit the scalability of DeFi applications.

Complexity and Usability: DeFi platforms can be complex and challenging for newcomers to navigate. Improving user interfaces and providing educational resources are crucial for broader adoption.

Notable DeFi Projects

Uniswap (UNI): Uniswap is a leading decentralized exchange that allows users to trade ERC-20 tokens directly from their wallets. Its automated market maker (AMM) model has revolutionized the way liquidity is provided and traded in the DeFi space.

Aave (AAVE): Aave is a decentralized lending and borrowing platform that offers unique features such as flash loans and rate switching. It has become one of the largest and most innovative DeFi protocols.

MakerDAO (MKR): MakerDAO is the protocol behind the Dai stablecoin, a decentralized stablecoin pegged to the US dollar. MakerDAO allows users to create Dai by collateralizing their assets, providing stability and liquidity to the DeFi ecosystem.

Compound (COMP): Compound is another leading DeFi lending platform that enables users to earn interest on their cryptocurrencies or borrow assets against collateral. Its governance token, COMP, allows users to participate in protocol governance.

Sexy Meme Coin (SXYM): While primarily known as a meme coin, Sexy Meme Coin has integrated DeFi features, including a decentralized marketplace for buying, selling, and trading memes as NFTs. This unique blend of humor and finance adds a distinct flavor to the DeFi landscape. Learn more about Sexy Meme Coin at Sexy Meme Coin.

The Future of DeFi

The future of DeFi looks promising, with continuous innovation and growing adoption. As blockchain technology advances and scalability solutions are implemented, DeFi has the potential to disrupt traditional financial systems further. Regulatory clarity and improved security measures will be crucial for the sustainable growth of the DeFi ecosystem.

DeFi is likely to continue attracting attention from both retail and institutional investors, driving further development and integration of decentralized financial services. The flexibility and inclusivity offered by DeFi make it a compelling alternative to traditional finance, paving the way for a more open and accessible financial future.

Conclusion

Decentralized Finance (DeFi) represents a significant shift in the financial landscape, leveraging blockchain technology to create a more inclusive, transparent, and efficient financial system. Despite the challenges, the benefits of DeFi and its continuous innovation make it a transformative force in the world of finance. Notable projects like Uniswap, Aave, and MakerDAO, along with unique contributions from meme coins like Sexy Meme Coin, demonstrate the diverse and dynamic nature of the DeFi ecosystem.

For those interested in exploring the playful and innovative side of DeFi, Sexy Meme Coin offers a unique and entertaining platform. Visit Sexy Meme Coin to learn more and join the community.

254 notes

·

View notes

Text

The future of crypto: The delicate dance between innovation and regulation

The major crypto technologies we are now seeing touch on a range of areas affecting our everyday lives. Blockchain technology is allowing us to record and transport financial data far more securely, transparently and efficiently than before. This new way of financial recordkeeping is being used in areas ranging from supply chain management to healthcare.

Blockchain is the basis of many other crypto technologies such as smart contracts. They are making contractual obligations stronger and more automatized across industries. Similarly, tokenization is changing how we securely move and store sensitive data such as credit card numbers by using ‘tokens’ to represent data and information. We’re seeing these used even in the world of arts and collectibles where a new digital dimension of non-fungible tokens (NFTs) are certifying ownership and authenticity.

Decentralized financial systems are also changing how we are dealing with money. By using peer-to-peer lending and decentralized exchanges, these systems are breaking down barriers, particularly for marginalized groups including women.

But not far behind each of these advances are security risks and challenges. While decentralization might provide some advantages to marginalized groups, the gender gap remains an issue in the world of virtual assets and cryptocurrency. Indeed, women continue to be underrepresented in the crypto space. This disparity is evident not only in the number of female investors and developers but also in leadership roles within blockchain projects. The crypto industry has the potential to reshape traditional financial systems, and fostering gender diversity is crucial for ensuring a more equitable and innovative future. Efforts to close the gender gap in crypto involve initiatives to educate and empower women in blockchain technology, providing mentorship opportunities, and advocating for a more inclusive and diverse community.

And gender inequality isn’t the only challenge facing the world of crypto. The irreversible nature of most crypto transactions means hacking and exploiting vulnerabilities can have major, lasting consequences. And anonymity makes these technologies potential hotbeds for illegal activities by criminals and terrorists. Robust cybersecurity measures are crucial for addressing this.

But how?

Regulatory uncertainty is one of the foremost challenges in the crypto landscape. Authorities have to carefully consider a range of questions: How do you create a system that simultaneously protects innovation and people? Whose jurisdiction are these borderless technologies under? How do we standardize their regulation without overregulating? And many more.

If you look at the regulatory framework around Virtual Assets Service Providers, which are the bridges between crypto and government-issued currencies, regulation is helping to mitigate major risks such as money laundering, terrorism financing, and other illicit activities. Such a framework gives these digital entities clear legal boundaries that help safeguard the integrity of financial systems as well as adds an important layer of consumer protection for any transactions involving virtual assets.

Clear guidelines and oversight mechanisms help prevent fraud and ensure the security and integrity of digital transactions. This builds confidence in investors, businesses, and the public that these assets are subject to transparent and accountable practices, which, ultimately, helps to foster a healthy and sustainable digital asset ecosystem.

Here at the OSCE we are actively engaged in helping participating States forge solid regulatory frameworks that strike a delicate balance between oversight and fostering innovation. We advocate for regulations created in consultation with industry stakeholders and that set clear guidelines without imposing unnecessary restrictions.

We also recognize that regulations should be adaptable and not overwrought. The rapidly evolving nature of virtual assets will quickly outpace a framework that is too rigid, overregulated or static, which not only hinders progress but also creates new vulnerabilities.

Our project, ‘Innovative policy solutions to mitigate money laundering risks of virtual assets’, is a key driving force of our support to States. Along with raising awareness among public officials about crypto-related risks, we are also building law enforcement and supervisory bodies’ capacities in crypto-related investigations.

By working together using a careful and balanced approach, we can create an agile crypto regulation system that mitigates risks, protects consumers and fosters innovation. This is key to tapping into the world of possibilities crypto offers and paving the way for a brighter and better future for us all.

2 notes

·

View notes

Text

Shocking Impact of Blockchain: Is Traditional Finance Doomed?

👀 The financial world is changing fast—and blockchain is leading the charge. Traditional banks are no longer the only gatekeepers of money. With decentralized apps and platforms offering faster, cheaper, and smarter alternatives, blockchain is forcing the financial industry to evolve or dissolve.

Smart contracts eliminate the need for trust. Peer-to-peer lending is now global. Investing no longer needs a broker. This is the age of financial empowerment, and it's powered by code—not banks.

But is traditional finance really doomed? Not yet. But if it doesn’t catch up soon, it just might be.

🚀 Check out our latest breakdown of how blockchain is disrupting global finance: 👉 Check Out This

#BlockchainRevolution #CryptoWorld #FintechTakeover #TumblrFinance #MoneyTalks #TradFiVsDeFi

2 notes

·

View notes

Text

25 Passive Income Ideas to Build Wealth in 2025

Passive income is a game-changer for anyone looking to build wealth while freeing up their time. In 2025, technology and evolving market trends have opened up exciting opportunities to earn money with minimal ongoing effort. Here are 25 passive income ideas to help you grow your wealth:

1. Dividend Stocks

Invest in reliable dividend-paying companies to earn consistent income. Reinvest dividends to compound your returns over time.

2. Real Estate Crowdfunding

Join platforms like Fundrise or CrowdStreet to invest in real estate projects without the hassle of property management.

3. High-Yield Savings Accounts

Park your money in high-yield savings accounts or certificates of deposit (CDs) to earn guaranteed interest.

4. Rental Properties

Purchase rental properties and outsource property management to enjoy a steady cash flow.

5. Short-Term Rentals

Leverage platforms like Airbnb or Vrbo to rent out spare rooms or properties for extra income.

6. Peer-to-Peer Lending

Lend money through platforms like LendingClub and Prosper to earn interest on your investment.

7. Create an Online Course

Turn your expertise into an online course and sell it on platforms like Udemy or Teachable for recurring revenue.

8. Write an eBook

Publish an eBook on Amazon Kindle or similar platforms to earn royalties.

9. Affiliate Marketing

Promote products or services through a blog, YouTube channel, or social media and earn commissions for every sale.

10. Digital Products

Design and sell digital products such as templates, printables, or stock photos on Etsy or your website.

11. Print-on-Demand

Use platforms like Redbubble or Printful to sell custom-designed merchandise without inventory.

12. Mobile App Development

Create a useful app and monetize it through ads or subscription models.

13. Royalties from Creative Work

Earn royalties from music, photography, or artwork licensed for commercial use.

14. Dropshipping

Set up an eCommerce store and partner with suppliers to fulfill orders directly to customers.

15. Blogging

Start a niche blog, grow your audience, and monetize through ads, sponsorships, or affiliate links.

16. YouTube Channel

Create a YouTube channel around a specific niche and earn through ads, sponsorships, and memberships.

17. Automated Businesses

Use tools to automate online businesses, such as email marketing or subscription box services.

18. REITs (Real Estate Investment Trusts)

Invest in REITs to earn dividends from real estate holdings without owning property.

19. Invest in Index Funds

Index funds provide a simple way to earn passive income by mirroring the performance of stock market indexes.

20. License Software

Develop and license software or plugins that businesses and individuals can use.

21. Crypto Staking

Participate in crypto staking to earn rewards for holding and validating transactions on a blockchain network.

22. Automated Stock Trading

Leverage robo-advisors or algorithmic trading platforms to generate passive income from the stock market.

23. Create a Membership Site

Offer exclusive content or resources on a membership site for a recurring subscription fee.

24. Domain Flipping

Buy and sell domain names for a profit by identifying valuable online real estate.

25. Invest in AI Tools

Invest in AI-driven platforms or create AI-based products that solve real-world problems.

Getting Started

The key to success with passive income is to start with one or two ideas that align with your skills, interests, and resources. With dedication and consistency, you can build a diversified portfolio of passive income streams to secure your financial future.

2 notes

·

View notes

Text

The Rise of Fintech: Transforming Financial Services for the Digital Age

In recent years, Fintech—short for Financial Technology—has emerged as a disruptive force in the financial services industry. From mobile payments to blockchain technology, fintech innovations are reshaping how individuals, businesses, and financial institutions interact with money. As digital tools continue to evolve, they offer new ways to improve financial efficiency, transparency, and inclusivity.

The rapid rise of fintech is not just a trend; it's a transformative shift that’s reshaping financial landscapes globally. In this article, we will explore what fintech is, how it’s transforming various sectors of financial services, and what the future holds for this exciting industry.

1. What is Fintech?

Fintech is a term that encompasses any technology that improves and automates financial services. This can include innovations in areas like mobile payments, online banking, investment platforms, and even the use of artificial intelligence in managing financial portfolios.

Fintech aims to make financial services more accessible, efficient, and secure. By leveraging digital tools, it allows individuals to manage their finances with ease, whether they're sending money across borders, applying for a loan, or investing in the stock market.

2. The Evolution of Fintech

The roots of fintech can be traced back to the late 20th century, with the introduction of online banking and electronic payments. However, it wasn't until the late 2000s, with the rise of smartphones and digital apps, that fintech truly took off.

The 2008 financial crisis also played a significant role in the development of fintech. Traditional banks struggled, leading to the rise of alternative financial solutions. Startups began creating apps and platforms to offer services such as peer-to-peer lending, robo-advisors, and even digital currencies like Bitcoin.

Today, fintech is booming, with countless companies and startups offering innovative financial products and services that rival traditional financial institutions.

3. The Key Sectors of Fintech

Fintech covers a broad range of sectors, each offering unique innovations that are transforming the way we think about and use financial services. Here are some of the key areas:

a. Digital Payments

One of the most recognizable sectors of fintech is digital payments. Apps like PayPal, Venmo, and Apple Pay have made sending and receiving money faster, more convenient, and cheaper than traditional methods.

Consumers can now make purchases, pay bills, and send money internationally with just a few taps on their smartphone, without needing to rely on banks or physical cash.

b. Lending and Borrowing

Fintech has disrupted the lending industry by providing alternatives to traditional bank loans. Peer-to-peer lending platforms such as LendingClub and Funding Circle allow individuals to lend directly to borrowers, cutting out the middleman and often providing better rates for both parties.

Additionally, fintech lenders have made it easier for small businesses and individuals with less-than-perfect credit scores to access loans through automated credit scoring systems.

c. Investment Platforms

The rise of fintech has made investing more accessible to the general public. Gone are the days when investing required a hefty minimum deposit and working with a financial advisor.

Now, thanks to robo-advisors like Betterment and Wealthfront, individuals can invest with little to no minimum, receiving tailored investment advice through algorithms that automatically adjust portfolios based on risk tolerance and market conditions.

d. Insurtech (Insurance Technology)

Insurtech is another growing sector of fintech, aiming to simplify and improve the insurance industry. From comparing quotes to filing claims, insurance technology platforms like Lemonade are providing a seamless, user-friendly experience for consumers.

These innovations are making insurance more affordable and efficient, particularly for younger consumers who value the convenience of digital interactions.

e. Cryptocurrency and Blockchain

Perhaps the most transformative development in fintech is the rise of cryptocurrencies and blockchain technology. Cryptocurrencies like Bitcoin and Ethereum offer decentralized alternatives to traditional currencies, while blockchain technology provides a secure and transparent way to record transactions.

While still relatively new, cryptocurrencies and blockchain are expected to have far-reaching implications for everything from cross-border payments to smart contracts.

4. How Fintech is Changing Financial Services

Fintech’s influence is broad and deep, transforming almost every facet of financial services. Here’s a closer look at how it’s reshaping the industry:

a. Improving Access to Financial Services

One of the biggest advantages of fintech is that it provides greater access to financial services, particularly for underserved populations. For example, fintech platforms allow people in developing countries, who might not have access to traditional banking, to open accounts and manage their finances using just a smartphone.

Fintech has also revolutionized access to credit. Through digital lending platforms, individuals and small businesses can get loans faster and more easily than ever before, often bypassing the hurdles of traditional banks.

b. Lowering Costs

Fintech companies operate more efficiently than traditional financial institutions, often passing these savings on to consumers in the form of lower fees and better interest rates. This is especially true in sectors like peer-to-peer lending and digital payments, where middlemen have been cut out of the equation.

c. Faster Transactions

In the traditional financial world, sending money, especially internationally, can be a slow and expensive process. Fintech has made these transactions faster, with some payments happening in real time. Digital wallets, payment processors, and blockchain technology are all contributing to instantaneous money transfers, no matter where you are in the world.

d. Personalized Financial Management

Thanks to the use of big data and machine learning, fintech companies can provide highly personalized services. For example, investment platforms use algorithms to create tailored portfolios, while budgeting apps help users track and optimize their spending habits based on individual behavior.

This level of personalization is helping consumers and businesses alike make better financial decisions, driving growth and improving financial health.

5. The Role of Artificial Intelligence in Fintech

Artificial intelligence (AI) is playing a significant role in the fintech industry. AI is used to streamline processes, enhance customer experiences, and improve security measures. For example, chatbots powered by AI can handle basic customer inquiries, freeing up human agents to focus on more complex tasks.

AI also plays a crucial role in fraud detection and cybersecurity, identifying unusual patterns in data and flagging potential threats in real time.

6. Fintech Regulations and Challenges

As fintech continues to grow, so do the regulatory challenges that come with it. Governments and financial institutions around the world are working to create regulatory frameworks that both encourage innovation and protect consumers.

Some key concerns in fintech include data privacy, cybersecurity, and the risk of financial exclusion if certain populations are unable to keep up with technological advances.

There’s also the challenge of navigating the global landscape, as fintech companies often operate in multiple countries, each with its own regulations and standards.

7. The Future of Fintech

The future of fintech looks incredibly promising, with AI, blockchain, and cryptocurrencies leading the charge. Experts predict that in the next few years, we’ll see even more integration between traditional financial institutions and fintech companies, blurring the lines between the two.

In addition to more widespread adoption of digital currencies, the fintech industry is expected to play a key role in financial inclusion, helping to bridge the gap for the 1.7 billion people globally who remain unbanked.

8. How to Get Started in Fintech

If you're interested in fintech, there are plenty of ways to get started. Whether you’re a consumer looking to take advantage of new financial tools, or a professional considering a career in the industry, now is the perfect time to dive in.

Explore Fintech Platforms: Start using digital banking apps, robo-advisors, or digital wallets to familiarize yourself with how fintech works.

Learn About Blockchain and AI: These two technologies are central to the future of fintech. There are plenty of online courses and resources available to help you learn the basics.

Invest in Fintech: Many fintech companies are publicly traded, offering opportunities for you to invest in the future of finance.

9. The Benefits of Fintech for Businesses

Fintech isn’t just changing the landscape for consumers—it’s also revolutionizing how businesses operate. From streamlining payment processes to improving access to capital, fintech is enabling businesses to operate more efficiently and scale faster.

Some benefits for businesses include:

Lower Transaction Fees: Fintech payment processors offer competitive rates compared to traditional banks.

Access to Funding: Digital lending platforms and crowdfunding have opened up new ways for businesses to access funding.

Improved Cash Flow Management: With real-time payment solutions, businesses can improve cash flow and reduce the wait times associated with traditional banking.

10. Conclusion: Fintech is Here to Stay

In conclusion, fintech is not just a buzzword—it’s a revolution that’s changing the way we interact with money and financial services. Whether it’s through digital payments, AI-powered financial tools, or blockchain-based systems, fintech is making finance faster, more accessible, and more secure.

The rise of fintech has already transformed many aspects of financial services, and it shows no signs of slowing down. As technology continues to advance, we can expect fintech to play an even larger role in the global economy.

Are you ready to explore the future of finance? Click here to learn more and stay ahead of the curve with the latest insights: The Rise of Fintech.

#fintech#financetips#investing stocks#personal finance#management#investing#finance#crypto#investment#blockchain#solana#crypto market

2 notes

·

View notes

Text

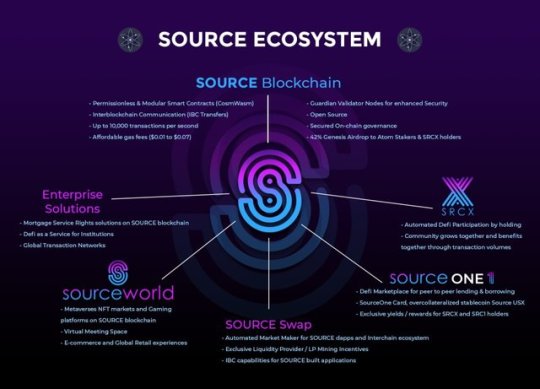

SOURCE PROTOCOL

SOURCE is building limitless enterprise applications on a secure and sustainable global network. Defi white-labelled services, NFT markets, RWA tokenization, play-to-earn gaming, Internet of Things, data management and more. SOURCE is providing blockchain solutions to the real world and leveraging the power of interoperability.

SOURCE competitive advantages over other blockchain projects

For builders & developers — Source Chain’s extremely high speeds (2500–10000+ tx / per second), low cost / gas fees ($0.01 average per tx), and scalability (developers can deploy apps in multiple coding languages using CosmWasm smart contract framework), set it apart as a blockchain built to handle mass adopted applications and tools. Not to mention, it’s interoperable with the entire Cosmos ecosystem.

For users — Source Protocol’s DeFi suite is Solvent and Sustainable (Automated liquidity mechanisms create a continuously self-funded, solvent and liquid network), Reduces Complexity (we’re making Web 3.0 easy to use with tools like Source Token which automate DeFi market rewards), and we’ve implemented Enhanced Security and Governance systems (like Guardian Nodes), which help us track malicious attacks and proposals to create a safer user environment.

For Enterprises — Source Protocol is one of the first to introduce DeFi-as-a-Service (DaaS) in order for existing online banking and fintech solutions to adopt blockchain technology with ease, and source also provides Enterprise Programs which are complete with a partner network of OTC brokerages, crypto exchanges, and neobanks that create a seamless corporate DeFi experience (fiat onboarding, offboarding, and mutli-sig managed wallets)

Why Source Protocol

Firstly, many protocols are reliant on centralized exchanges for liquidity, limiting their ability to scale independently. This creates a lot of the same issues traditional finance has been plagued with for decades.

Next — slow tx speeds, high costs, limited scalability, and inability to collaborate with other chains, has created severe limitations in Gen 2 blockchain infrastructure.

Lastly, there still exists a level of complexity in blockchain applications that remains a barrier to entry for the average user, and there is not enough focus on building “bridges” for the enterprise to adopt this technology easily and quickly.

In summary, consumers are eager for a blockchain ecosystem that can securely and sustainably support mass adopted applications. That’s why we’ve built Source!

Source Protocol’s ecosystem

Source Protocol’s ecosystem includes a full DeFi Suite, a members rewards program and white-label integration capabilities with existing online Web 2.0 enterprises:

Source Swap — An Interchain DEX & AMM built on Source Chain for permission-less listing of $SOURCE-based tokens, native Cosmos SDK assets, cw-20’s, and wrapped Binance Smart Chain (BEP-20) assets.

Source One Market — A peer to peer, non-custodial DeFi marketplace for borrowing, lending, staking, and more. Built on Binance Smart Chain with bridging to Source Chain & native Cosmos SDK assets.

Source Token $SRCX (BEP-20) — the first automated liquidity acquisition and DeFi market participation token built on Binance Smart Chain.

Source One Token $SRC1 (BEP-20) — a governance and incentivized earnings token that powers Source One Market.

Source USX $USX (BEP-20) — Source One Market stablecoin backed and over collateralized by a hierarchy of blue chip crypto assets and stablecoins.

Source Launch Pad — Empowering projects to seamlessly distribute tokens and raise liquidity. ERC-20 and BEP-20 capable.

Source One Card & Members Rewards Program — users can earn from a robust suite of perks and rewards. In the future, Source One Card will enable users to swipe with their crypto assets online and at retail locations in real time.

DeFi-as-a-Service (DaaS) — Seamless white-label integration of Source One Market, Source Swap, Source Launch Pad, and/or Source One Card with existing online banking and financial applications, allowing businesses to bring their customers DeFi capabilities.

Source Protocol Key Components

Sustainable Growth model built for enterprise involvement and mass application adoption

Guardian Validator Nodes for enhanced network security

Integration with Source Protocol’s Binance Smart Chain Ecosystem and Decentralized Money Market, Source One Market

Source-Drop (Fair community airdrop and asset distribution for ATOM stakers and SRCX holders)

Interoperable smart contracts (IBC)

High speed transaction finality

Affordable gas fees (average of $0.01 per transaction)

Highly scalable infrastructure

Open-source

Permission-less Modular Wasm + (EVM)

Secured on-chain governance

Ease of use for developers

conclusion

SOURCE is a comprehensive blockchain technology suite for individuals, enterprises and developers to easily use, integrate and build web3.0 applications. It is a broad-spectrum technology ecosystem that transforms centralized web tools and financial instruments into decentralized ones. Powering the future of web3,

Next — slow tx speeds, high costs, limited scalability, and inability to collaborate with other chains, has created severe limitations in Gen 2 blockchain infrastructure.

Lastly, there still exists a level of complexity in blockchain applications that remains a barrier to entry for the average user, and there is not enough focus on building “bridges” for the enterprise to adopt this technology easily and quickly.

In summary, consumers are eager for a blockchain ecosystem that can securely and sustainably support mass adopted applications. That’s why we’ve built Source!

For More Information about Source Protocol

Website: https://www.sourceprotocol.io

Documents: https://docs.sourceprotocol.io

Twitter: https://www.twitter.com/sourceprotocol_

Instagram: https://www.instagram.com/sourceprotocol

Telegram: https://t.me/sourceprotocol

Discord: https://discord.gg/zj8xxUCeZQ

Author

Forum Username: Java22

Forum Profile Link: https://bitcointalk.org/index.php?action=profile;u=3443255

SOURCE Wallet Address: source1svnzfy5fafuskeaxmf2sgvgcn6k3sggmssl8d7

2 notes

·

View notes

Text

Bitcoin's role in the future of finance

In the ever-evolving landscape of finance, one digital currency has captured the world's attention like no other: Bitcoin. Since its inception in 2009, Bitcoin has transcended from being a mere experimental concept to a transformative force, challenging traditional financial systems and reshaping our perception of money. As we navigate through the complexities of the modern financial world, it's imperative to understand Bitcoin's role in shaping the future of finance.

Bitcoin's Rise to Prominence: Bitcoin's journey from obscurity to prominence has been nothing short of remarkable. Introduced by the pseudonymous Satoshi Nakamoto, Bitcoin was envisioned as a decentralized digital currency, free from the control of central authorities such as banks or governments. Its underlying technology, blockchain, revolutionized the way transactions are recorded and verified, offering transparency, security, and immutability.

Initially met with skepticism and skepticism, Bitcoin gradually gained traction among tech enthusiasts, libertarians, and early adopters seeking an alternative to traditional fiat currencies. As its utility and acceptance grew, Bitcoin's value soared, attracting mainstream attention and investment from institutional players and retail investors alike.

Bitcoin's Role in the Future of Finance: Now, as we stand on the precipice of a new era in finance, Bitcoin's significance cannot be overstated. Here's how Bitcoin is poised to shape the future of finance:

Decentralization and Financial Inclusion: At the heart of Bitcoin lies its decentralized nature, which empowers individuals to take control of their financial destinies. Unlike traditional banking systems, where intermediaries dictate transactions and impose fees, Bitcoin allows for peer-to-peer transactions without the need for intermediaries. This decentralization fosters financial inclusion by providing access to banking services for the unbanked and underbanked populations worldwide.

Hedge Against Inflation and Economic Uncertainty: In an era marked by economic volatility and uncertainty, Bitcoin offers a hedge against inflation and currency devaluation. With a finite supply of 21 million coins, Bitcoin is immune to the whims of central banks and government policies that often erode the value of fiat currencies. As central banks continue to print money to stimulate economies, Bitcoin's scarcity and deflationary nature make it an attractive store of value and a hedge against economic downturns.

Innovation in Financial Services: Bitcoin's underlying technology, blockchain, has paved the way for innovative financial services and applications. From decentralized finance (DeFi) platforms to non-fungible tokens (NFTs) and smart contracts, Bitcoin's ecosystem continues to expand, offering new avenues for investment, lending, and asset management. These innovations have the potential to democratize finance, making it more accessible and inclusive for individuals worldwide.

Global Payments and Remittances: As a borderless digital currency, Bitcoin facilitates fast, low-cost cross-border payments and remittances. Unlike traditional banking systems, which are plagued by high fees and long processing times, Bitcoin enables instant transactions without the need for intermediaries. This has significant implications for global commerce, enabling businesses to streamline payments and expand their reach to new markets.

Institutional Adoption and Mainstream Acceptance: In recent years, we've witnessed a surge in institutional adoption of Bitcoin, with major corporations and financial institutions incorporating Bitcoin into their investment portfolios. This institutional endorsement not only lends credibility to Bitcoin but also paves the way for mainstream acceptance. As more businesses and individuals embrace Bitcoin, its role in the future of finance is poised to become even more pronounced.

Conclusion: In conclusion, Bitcoin's role in the future of finance is multifaceted and profound. From decentralization and financial inclusion to innovation and global payments, Bitcoin has the potential to reshape the way we perceive and interact with money. As we embrace the digital revolution, Bitcoin stands at the forefront, offering a glimpse into a future where financial empowerment and freedom reign supreme. As we embark on this journey, one thing is clear: Bitcoin is not just a digital currency; it's a catalyst for change, ushering in a new era of finance for generations to come.

How will Bitcoin be used in the future?

In the ever-evolving landscape of digital currencies, Bitcoin stands tall as a pioneer, offering a glimpse into the future of finance. But how will Bitcoin be used in the future? Let's delve into the possibilities and potential of this groundbreaking cryptocurrency.

Global Transactions and Remittances: Bitcoin's borderless nature makes it ideal for facilitating international transactions and remittances. As traditional banking systems struggle with high fees and lengthy processing times, Bitcoin offers a faster, more cost-effective alternative. In the future, we can expect to see Bitcoin used as a primary means of transferring value across borders, empowering individuals and businesses alike.

Store of Value: With its finite supply and decentralized nature, Bitcoin has emerged as a reliable store of value akin to digital gold. As economic uncertainty looms and traditional fiat currencies face inflationary pressures, Bitcoin offers a hedge against depreciation. In the future, we may witness a significant portion of wealth stored in Bitcoin, safeguarding against currency devaluation and economic downturns.

Mainstream Adoption: While Bitcoin has already gained widespread recognition, its adoption is poised to skyrocket in the future. As more merchants accept Bitcoin as a form of payment and financial institutions integrate it into their services, Bitcoin will become increasingly accessible to the masses. This mainstream adoption will fuel its use in everyday transactions, from purchasing goods and services to receiving salaries.

Financial Inclusion: Bitcoin has the potential to bridge the gap between the banked and unbanked populations, particularly in developing countries. individuals who have been excluded from the formal financial system, fostering greater financial inclusion and economic empowerment.

Smart Contracts and Decentralized Finance (DeFi): Bitcoin's underlying technology, blockchain, enables the creation of smart contracts and decentralized finance applications. In the future, we can expect to see Bitcoin utilized in a variety of DeFi platforms, offering innovative financial services such as lending, borrowing, and trading. These decentralized applications will revolutionize traditional financial systems, providing greater accessibility and transparency to users.

Hedging Against Geopolitical Risks: As geopolitical tensions rise and governments impose sanctions, Bitcoin provides a means of circumventing restrictions on capital flows. In the future, we may see individuals and businesses turn to Bitcoin as a hedge against geopolitical risks, preserving their wealth in a borderless and censorship-resistant asset.

Integration with Central Bank Digital Currencies (CBDCs): While Bitcoin operates independently of central banks, it may complement the emerging trend of central bank digital currencies (CBDCs). In the future, we could see interoperability between Bitcoin and CBDCs, facilitating seamless exchange between digital and traditional currencies.

In conclusion, the future of Bitcoin is filled with promise and potential. From facilitating global transactions to fostering financial inclusion, Bitcoin is poised to revolutionize the way we think about money. As we embrace this digital frontier, Bitcoin will continue to shape the future of finance, empowering individuals, businesses, and economies worldwide.

What is the future of long term Bitcoin?

In the ever-evolving realm of cryptocurrencies, Bitcoin stands as the pioneer, the trailblazer that ignited a digital revolution. From its inception in 2009 by the mysterious Satoshi Nakamoto to its current status as a trillion-dollar asset, Bitcoin has captured the imagination of investors, tech enthusiasts, and economists alike. But what does the future hold for long-term Bitcoin? Let's embark on a journey to unravel the mysteries and explore the potential trajectory of this digital gold.

As we gaze into the crystal ball of cryptocurrency, one thing becomes clear: Bitcoin's long-term future is intricately tied to its ability to adapt and overcome challenges. Like any revolutionary technology, Bitcoin has faced its fair share of hurdles, from scalability issues to regulatory scrutiny. Yet, with each obstacle, Bitcoin has emerged stronger, more resilient, and more ingrained in the fabric of our digital economy.

So, what can we expect from long-term Bitcoin? Let's delve into the key factors that will shape its future:

Adoption and Integration: The widespread adoption of Bitcoin as a mainstream asset class is perhaps the most crucial determinant of its long-term success. As more institutions, corporations, and individuals embrace Bitcoin as a store of value and hedge against traditional financial systems' uncertainties, its long-term viability strengthens. With the recent trend of institutional adoption and the emergence of Bitcoin-based financial products, such as ETFs, the path towards mainstream acceptance becomes clearer.

Technological Advancements: The underlying technology behind Bitcoin, the blockchain, continues to evolve at a rapid pace. From scalability solutions to privacy enhancements, ongoing developments in blockchain technology promise to address Bitcoin's current limitations and unlock new possibilities. Layer 2 solutions like the Lightning Network offer faster and cheaper transactions, making Bitcoin more practical for everyday use.

Regulatory Clarity: Regulatory uncertainty has been a lingering shadow over Bitcoin's journey. However, as governments worldwide grapple with the complexities of cryptocurrency regulation, clarity begins to emerge. Clear and balanced regulatory frameworks can provide legitimacy and stability to the Bitcoin market, paving the way for greater institutional involvement and investor confidence.

Market Dynamics: The dynamics of the cryptocurrency market play a pivotal role in shaping Bitcoin's long-term trajectory. Price volatility, market sentiment, and macroeconomic factors all influence Bitcoin's price movements. However, as Bitcoin matures and its market cap grows, it becomes less susceptible to manipulation and wild price swings, leading to a more stable long-term outlook.

Global Socioeconomic Trends: Bitcoin's future is intertwined with broader socioeconomic trends, such as the shift towards digitalization, the erosion of trust in traditional financial institutions, and the quest for financial sovereignty. As individuals seek alternative forms of money and value preservation, Bitcoin's role as a decentralized, censorship-resistant asset becomes increasingly relevant.

In conclusion, the future of long-term Bitcoin is a tale of resilience, innovation, and adaptation. While challenges remain, Bitcoin's journey from obscurity to ubiquity reflects its intrinsic value and disruptive potential. As we navigate the ever-changing landscape of cryptocurrency, one thing is certain: Bitcoin's legacy will endure, shaping the future of finance and technology for generations to come.

3 notes

·

View notes

Text

How Are Blockchain and Smart Contracts Revolutionizing Personal Loans?

Introduction

The personal loan industry is undergoing a significant transformation, thanks to emerging technologies like blockchain and smart contracts. These innovations are making loan processing faster, more secure, and transparent. Traditional personal loan processes often involve lengthy paperwork, high-interest rates, and bureaucratic delays. However, with blockchain-powered lending, borrowers can experience streamlined approvals, reduced costs, and improved security.

As digital finance continues to evolve, understanding how blockchain and smart contracts impact the personal loan sector is crucial for both lenders and borrowers. This article explores how these technologies work and their benefits in revolutionizing the lending landscape.

What Is Blockchain and How Does It Apply to Personal Loans?

Blockchain is a decentralized, distributed ledger technology that records transactions securely and transparently. Unlike traditional banking systems, where a central authority controls loan transactions, blockchain ensures that all records are immutable and tamper-proof.

Key Features of Blockchain in Lending:

Decentralization – Eliminates the need for intermediaries like banks and credit agencies.

Transparency – Every transaction is recorded and accessible to relevant parties.

Security – Reduces fraud and unauthorized data access.

Efficiency – Speeds up loan approvals and fund disbursements.

By integrating blockchain, personal loan providers can reduce inefficiencies, making borrowing more accessible and affordable.

What Are Smart Contracts and Their Role in Personal Loans?

Smart contracts are self-executing contracts with terms directly written into code. These contracts automatically execute actions when predefined conditions are met, eliminating the need for intermediaries.

How Smart Contracts Work in Personal Lending:

Borrower Applies for a Loan – Details like loan amount, interest rate, and tenure are recorded on a blockchain.

Smart Contract Verification – The contract checks the borrower's credentials using blockchain data.

Automatic Loan Approval – If all criteria are met, the smart contract executes the loan agreement.

Instant Fund Disbursement – Upon approval, funds are transferred without manual intervention.

Automated Repayment Tracking – Payments are automatically deducted and recorded on the blockchain.

With smart contracts, borrowers benefit from a seamless lending experience, while lenders reduce risks associated with fraud and late repayments.

Benefits of Blockchain and Smart Contracts in Personal Loans

1. Faster Loan Approvals and Disbursements

Traditional personal loan applications can take days or weeks for approval due to manual verification. With blockchain and smart contracts:

Real-time verification speeds up approval processes.

Instant fund transfers ensure quick access to borrowed funds.

Automated underwriting reduces paperwork and delays.

2. Increased Security and Fraud Prevention

One of the biggest challenges in lending is fraud and identity theft. Blockchain technology mitigates these risks by:

Creating tamper-proof transaction records.

Eliminating data manipulation through decentralized verification.

Ensuring borrower identity verification using encrypted blockchain records.

3. Reduced Costs for Borrowers

Banks and traditional lenders charge high processing fees and interest rates due to administrative overheads. Blockchain-based personal loans minimize these costs by:

Removing middlemen like banks and credit agencies.

Lowering transaction fees using decentralized finance (DeFi) platforms.

Providing competitive interest rates through peer-to-peer lending.

4. Transparency and Trust in Lending

Blockchain records all transactions publicly, ensuring transparency in lending agreements. Borrowers and lenders can:

Track loan agreements in real time.

Avoid hidden fees or unfair lending terms.

Ensure compliance with agreed-upon loan conditions.

5. Improved Accessibility to Credit

Many individuals lack a formal credit history, making it difficult to obtain loans from traditional banks. Blockchain lending platforms use alternative credit assessment models, enabling:

Loans for the unbanked and underbanked populations.

Alternative credit scoring using transaction history and blockchain reputation.

Financial inclusion for freelancers, gig workers, and small business owners.

The Rise of Decentralized Finance (DeFi) in Personal Loans

Decentralized Finance (DeFi) is a blockchain-based financial ecosystem that eliminates intermediaries, allowing direct lending and borrowing between individuals.

Features of DeFi Lending:

Smart contract-based lending platforms.

Lower interest rates compared to traditional banks.

Access to global lenders without geographical restrictions.

Popular DeFi lending platforms like Aave, Compound, and MakerDAO are already revolutionizing the way personal loans are issued, making borrowing easier and more cost-effective.

Challenges and Risks of Blockchain-Based Personal Loans

Despite its advantages, blockchain lending faces some challenges:

1. Regulatory Uncertainty

Governments and financial institutions are still working on regulations for blockchain-based personal loans, which could impact widespread adoption.

2. Volatility in Crypto-Backed Loans

Some blockchain loans are backed by cryptocurrencies, which are highly volatile, posing risks for borrowers and lenders.

3. Technical Complexity

Borrowers may need basic knowledge of blockchain and digital wallets, making accessibility a challenge for non-tech-savvy individuals.

4. Limited Consumer Protection

Unlike traditional banks, blockchain-based lending platforms may lack consumer protection mechanisms in case of disputes or fraud.

The Future of Blockchain in the Personal Loan Market

As blockchain and smart contracts gain acceptance, the personal loan industry is expected to undergo further innovations:

1. Mainstream Adoption of Blockchain-Based Lending

More traditional banks may integrate blockchain technology into their lending processes for faster approvals and increased security.

2. Government-Backed Blockchain Lending Platforms

Governments may introduce blockchain-based loan programs to enhance financial inclusion and transparency.

3. AI and Blockchain Integration for Enhanced Credit Scoring

Combining AI with blockchain will enable more accurate borrower assessments, leading to fairer lending practices.

4. Smart Loans with Customizable Terms

Future personal loans may be fully customizable, allowing borrowers to set their preferred repayment structures and interest rates through AI-driven smart contracts.

Conclusion

Blockchain and smart contracts are revolutionizing the personal loan industry by making lending faster, more transparent, and secure. These technologies eliminate the need for intermediaries, reducing costs and improving accessibility for borrowers worldwide. While challenges like regulatory uncertainty and crypto volatility remain, the future of blockchain lending looks promising.

As financial institutions and fintech companies continue to innovate, borrowers can expect a seamless and efficient personal loan experience in the years to come. Understanding how blockchain-based lending works today will help individuals make informed borrowing decisions and take advantage of future advancements in digital finance.

#personal loan#loan apps#fincrif#bank#nbfc personal loan#personal loan online#personal loans#loan services#finance#personal laon#Personal loan#Blockchain in lending#Smart contracts for personal loans#Decentralized finance (DeFi) loans#Blockchain-based personal loans#Crypto-backed personal loans#Smart contract lending#Peer-to-peer lending with blockchain#Digital lending platforms#Fintech and blockchain loans#Secure loan transactions with blockchain#Instant loan approvals with smart contracts#Automated loan disbursement#Personal loan fraud prevention#AI and blockchain in lending#Digital identity verification for loans#Smart loan agreements#Alternative credit scoring with blockchain#Secure lending platforms#Financial inclusion through blockchain

1 note

·

View note

Text

What is BitNest Loop DeFi?

BitNest Loop is a core decentralized finance (DeFi) application in the BitNest platform, focusing on providing lending services. This system allows users to lend and lend cryptocurrencies to each other in a decentralized environment, enhancing the liquidity and utilization efficiency of capital. Here are a few key features of BitNest Loop DeFi:

Decentralized Lending BitNest Loop enables users to borrow or lend cryptocurrency directly from other users without the need for traditional financial intermediaries such as banks. This peer-to-peer lending model is automated through smart contracts, increasing the transparency and security of the process.

Smart contract control All lending activities are conducted through smart contracts, which means that once the lending conditions are set and both parties agree, the contract automatically performs lending and repayment operations. Smart contracts also ensure the immutability of transactions and the automation of execution.

Capital efficiency By providing lending services, BitNest Loop helps users use their idle assets efficiently. Borrowers can access necessary funds to invest or meet other short-term financial needs, while lenders earn income through interest.

Liquidity provision BitNest Loop typically has a liquidity pool where users can deposit their cryptocurrencies to provide liquidity as part of lending funds. These liquidity providers are rewarded for the interest on their loans, thus incentivizing more users to deposit assets into the platform.

Risk management While a decentralized environment reduces the need for intermediaries and associated fees, it also introduces credit risk. BitNest Loop may include mechanisms such as collateral management and interest rate adjustment to mitigate lending risks. These mechanisms help balance risk and reward between borrowers and lenders.

Accessibility and Inclusion As part of the BitNest DeFi ecosystem, Loop aims to improve the accessibility of financial services through simplified user interfaces and processes, allowing more users to easily participate in DeFi lending.

Overall, BitNest Loop DeFi is an innovative financial tool that promotes the development and popularity of decentralized finance by leveraging blockchain technology and smart contracts to provide a secure, transparent, and efficient lending platform.

#BitNest#BitNestLoop#BitNestPureContract#BitNestis the best project in the currency circle#BitNestSecurely#BitNestAutonomously#BitNestDecentralizedly#BitNestCryptographically

5 notes

·

View notes

Text

What is BitNest Loop DeFi?

BitNest Loop is a core decentralized finance (DeFi) application in the BitNest platform, focusing on providing lending services. This system allows users to lend and lend cryptocurrencies to each other in a decentralized environment, enhancing the liquidity and utilization efficiency of capital. Here are a few key features of BitNest Loop DeFi:

Decentralized Lending BitNest Loop enables users to borrow or lend cryptocurrency directly from other users without the need for traditional financial intermediaries such as banks. This peer-to-peer lending model is automated through smart contracts, increasing the transparency and security of the process.

Smart contract control All lending activities are conducted through smart contracts, which means that once the lending conditions are set and both parties agree, the contract automatically performs lending and repayment operations. Smart contracts also ensure the immutability of transactions and the automation of execution.

Capital efficiency By providing lending services, BitNest Loop helps users use their idle assets efficiently. Borrowers can access necessary funds to invest or meet other short-term financial needs, while lenders earn income through interest.

Liquidity provision BitNest Loop typically has a liquidity pool where users can deposit their cryptocurrencies to provide liquidity as part of lending funds. These liquidity providers are rewarded for the interest on their loans, thus incentivizing more users to deposit assets into the platform.

Risk management While a decentralized environment reduces the need for intermediaries and associated fees, it also introduces credit risk. BitNest Loop may include mechanisms such as collateral management and interest rate adjustment to mitigate lending risks. These mechanisms help balance risk and reward between borrowers and lenders.

Accessibility and Inclusion As part of the BitNest DeFi ecosystem, Loop aims to improve the accessibility of financial services through simplified user interfaces and processes, allowing more users to easily participate in DeFi lending.

Overall, BitNest Loop DeFi is an innovative financial tool that promotes the development and popularity of decentralized finance by leveraging blockchain technology and smart contracts to provide a secure, transparent, and efficient lending platform.

#BitNest#BitNestLoop#BitNestPureContract#BitNestis the best project in the currency circle#BitNestSecurely#BitNestAutonomously#BitNestDecentralizedly#BitNestCryptographically

5 notes

·

View notes

Text

What is BitNest Loop DeFi?

BitNest Loop is a core decentralized finance (DeFi) application in the BitNest platform, focusing on providing lending services. This system allows users to lend and lend cryptocurrencies to each other in a decentralized environment, enhancing the liquidity and utilization efficiency of capital. Here are a few key features of BitNest Loop DeFi:

Decentralized Lending BitNest Loop enables users to borrow or lend cryptocurrency directly from other users without the need for traditional financial intermediaries such as banks. This peer-to-peer lending model is automated through smart contracts, increasing the transparency and security of the process.

Smart contract control All lending activities are conducted through smart contracts, which means that once the lending conditions are set and both parties agree, the contract automatically performs lending and repayment operations. Smart contracts also ensure the immutability of transactions and the automation of execution.

Capital efficiency By providing lending services, BitNest Loop helps users use their idle assets efficiently. Borrowers can access necessary funds to invest or meet other short-term financial needs, while lenders earn income through interest.

Liquidity provision BitNest Loop typically has a liquidity pool where users can deposit their cryptocurrencies to provide liquidity as part of lending funds. These liquidity providers are rewarded for the interest on their loans, thus incentivizing more users to deposit assets into the platform.

Risk management While a decentralized environment reduces the need for intermediaries and associated fees, it also introduces credit risk. BitNest Loop may include mechanisms such as collateral management and interest rate adjustment to mitigate lending risks. These mechanisms help balance risk and reward between borrowers and lenders.

Accessibility and Inclusion As part of the BitNest DeFi ecosystem, Loop aims to improve the accessibility of financial services through simplified user interfaces and processes, allowing more users to easily participate in DeFi lending.

Overall, BitNest Loop DeFi is an innovative financial tool that promotes the development and popularity of decentralized finance by leveraging blockchain technology and smart contracts to provide a secure, transparent, and efficient lending platform.

#BitNest#BitNestLoop#BitNestPureContract#BitNestis the best project in the currency circle#BitNestSecurely#BitNestAutonomously#BitNestDecentralizedly#BitNestCryptographically

4 notes

·

View notes

Text

What is BitNest Loop DeFi?

BitNest Loop is a core decentralized finance (DeFi) application in the BitNest platform, focusing on providing lending services. This system allows users to lend and lend cryptocurrencies to each other in a decentralized environment, enhancing the liquidity and utilization efficiency of capital. Here are a few key features of BitNest Loop DeFi:

Decentralized Lending BitNest Loop enables users to borrow or lend cryptocurrency directly from other users without the need for traditional financial intermediaries such as banks. This peer-to-peer lending model is automated through smart contracts, increasing the transparency and security of the process.

Smart contract control All lending activities are conducted through smart contracts, which means that once the lending conditions are set and both parties agree, the contract automatically performs lending and repayment operations. Smart contracts also ensure the immutability of transactions and the automation of execution.

Capital efficiency By providing lending services, BitNest Loop helps users use their idle assets efficiently. Borrowers can access necessary funds to invest or meet other short-term financial needs, while lenders earn income through interest.

Liquidity provision BitNest Loop typically has a liquidity pool where users can deposit their cryptocurrencies to provide liquidity as part of lending funds. These liquidity providers are rewarded for the interest on their loans, thus incentivizing more users to deposit assets into the platform.

Risk management While a decentralized environment reduces the need for intermediaries and associated fees, it also introduces credit risk. BitNest Loop may include mechanisms such as collateral management and interest rate adjustment to mitigate lending risks. These mechanisms help balance risk and reward between borrowers and lenders.

Accessibility and Inclusion As part of the BitNest DeFi ecosystem, Loop aims to improve the accessibility of financial services through simplified user interfaces and processes, allowing more users to easily participate in DeFi lending.

Overall, BitNest Loop DeFi is an innovative financial tool that promotes the development and popularity of decentralized finance by leveraging blockchain technology and smart contracts to provide a secure, transparent, and efficient lending platform.

#BitNest#BitNestLoop#BitNestPureContract#BitNestis the best project in the currency circle#BitNestSecurely#BitNestAutonomously#BitNestDecentralizedly#BitNestCryptographically

5 notes

·

View notes

Text

Financial Sovereignty: How Bitcoin and DeFi Empower Individuals

Introduction: Defining Financial Sovereignty

In today’s world, financial sovereignty is increasingly becoming a priority. Financial sovereignty is the ability to fully control one’s financial assets and decisions without interference from external entities. In the face of rising inflation, unpredictable bank policies, and growing government interventions, this concept has gained importance. With innovations like Bitcoin and decentralized finance (DeFi), individuals can now take significant steps toward gaining control over their financial futures.

The Current Financial System’s Limitations

The traditional financial system, despite its familiarity and pervasiveness, has significant limitations. Banks often impose excessive fees, impose arbitrary limits on transactions, and face inherent risks of collapse. Government monetary policies, such as quantitative easing, can lead to inflation and devaluation of the currency, eroding people’s savings. Such vulnerabilities can leave individuals without the ability to protect their wealth.

Bitcoin as a Path to Financial Sovereignty

Bitcoin provides a decentralized alternative that empowers individuals to regain control over their finances. With its limited supply and borderless transactions, Bitcoin is designed to resist inflation, censorship, and external manipulation. It operates on a peer-to-peer network, meaning no central authority controls its value or distribution. Its properties offer a means for anyone to hold and transfer wealth securely, regardless of government regulations or the stability of the banking system.

Decentralized Finance (DeFi) as an Alternative Financial System

Decentralized finance takes the concept of financial sovereignty even further. By leveraging blockchain technology, DeFi platforms offer a new financial system without traditional intermediaries. Individuals can participate in borrowing, lending, and trading directly with others, often at lower fees than banks. DeFi’s trustless protocols enable a broader range of financial activities without requiring centralized permission.

Becoming Your Own Bank: Practical Steps to Financial Independence

So how does one achieve financial sovereignty? Here are some practical steps:

Research and Educate: Learn about Bitcoin and DeFi to understand their benefits, risks, and how to safely participate.

Set up a Bitcoin Wallet: Create a secure, non-custodial Bitcoin wallet to hold your cryptocurrency.

Diversify Investments: Develop a strategy that may include holding Bitcoin alongside other assets or investing in a diverse portfolio of DeFi tokens.

Explore DeFi Platforms: Carefully explore decentralized lending, borrowing, and yield-earning opportunities.

Case Studies: Real-World Examples

Individuals and even countries have found financial sovereignty through Bitcoin and DeFi. In Venezuela, where hyperinflation rendered the local currency nearly worthless, many turned to Bitcoin as a stable store of value. In El Salvador, Bitcoin adoption aimed to provide financial inclusion for the unbanked. These examples highlight how Bitcoin and DeFi can offer meaningful protection against monetary instability.

Conclusion: Taking Control of Your Financial Future

In a world where economic uncertainty prevails, financial sovereignty is an invaluable goal. Bitcoin and DeFi provide unique opportunities for individuals to protect their wealth and make independent financial decisions. By becoming educated and carefully engaging with these technologies, anyone can become their own bank and secure their financial future.

For those interested in this journey, take the next step by continuing to research, asking questions, and exploring the potential of decentralized finance. Your financial future is worth the effort.

#bitcoin#financial empowerment#financial freedom#financial planning#finance#financial education#bitcoin revolution

3 notes

·

View notes

Text

From Bitcoin to Beyond: Exploring the Evolving Landscape of Cryptocurrencies

Over the past decade, cryptocurrencies have emerged as a disruptive force in the world of finance and technology, with Bitcoin leading the way as the pioneering digital currency. The concept of a decentralized, borderless, and secure form of money challenged the traditional financial system, opening the door to a myriad of new possibilities. As the blockchain technology behind cryptocurrencies continues to evolve, the landscape of digital finance is undergoing a transformation that reaches far beyond the realms of Bitcoin.

The Genesis: Bitcoin's Impact and Legacy

Bitcoin, created by the pseudonymous Satoshi Nakamoto in 2009, was the first successful implementation of a peer-to-peer electronic cash system that operates without the need for intermediaries like banks. Its underlying technology, blockchain, introduced a distributed and immutable ledger, ensuring transparency and security in financial transactions.

Bitcoin's rise in popularity sparked interest among tech enthusiasts, libertarians, and investors seeking an alternative to the traditional financial system. Its decentralized nature and limited supply, capped at 21 million coins, instilled confidence in its ability to act as a store of value akin to digital gold.

The Altcoin Era: Diverse Cryptocurrencies Emerge