#PolicyInitiatives

Text

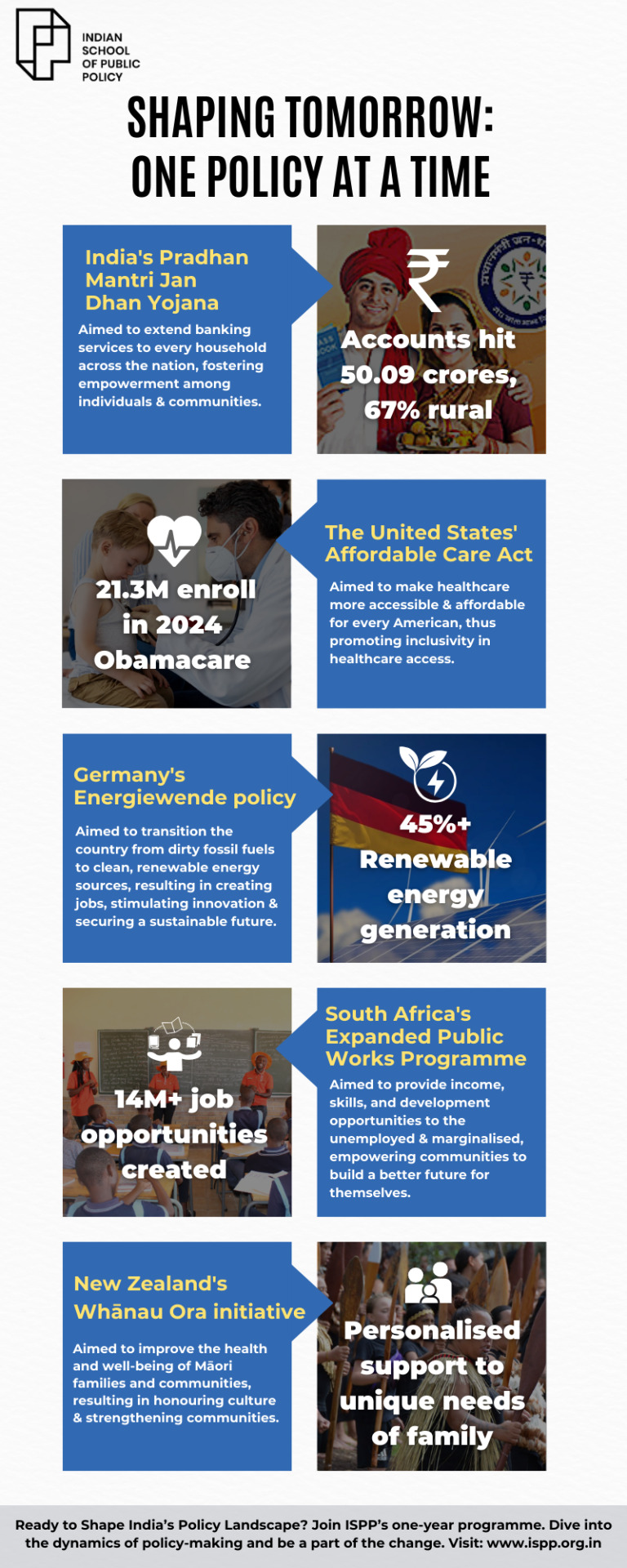

Shaping tomorrow: One Policy at a time - Indian School of Public Policy

Public policy initiatives around the world have significantly impacted the lives of millions, addressing the needs of marginalised communities and fostering inclusive development. In a world brimming with challenges, public policy emerges as a guiding light, illuminating pathways towards progress and inclusivity.

0 notes

Text

youtube

#IndustrialDevelopment#DriverstoDevelopment#PolicyInitiatives#Steps#SingleWindowSystem#IndustrialLandBank#Infrastructure#Entrepreneurship#ASI#LandSurveys#Process#Statistics#IncreaseinProduction#Growthrate#Share#SectorwiseGrowth#Factories#Employees#Youtube

0 notes

Text

A Turning Point: Advocates Push For Legal Reform On Marijuana In The Philippines

Advocates Push For Legal Reform On Marijuana In The Philippines: A Step Towards Progressive Drug Policy

In a landmark move, advocates in the Philippines are pushing for legal reform on marijuana, aiming to decriminalize its production, sale, and use. Spearheaded by former House Speaker Pantaleon Alvarez and supported by the lower chamber’s dangerous drugs committee, this initiative marks a significant step towards a more progressive drug policy in the country.At the forefront of this movement is the recognition of the inconsistencies within current drug classification systems. Alvarez boldly denounced the categorization of cannabis and its derivatives as dangerous drugs, labeling it as absurd. In his impassioned speech, he questioned why substances like alcohol, cigarettes, and sugary drinks, known for their harmful effects, are allowed while marijuana, which he argues is less harmful and potentially beneficial, remains criminalized.Indeed, the economic potential of legalizing marijuana cannot be ignored. Alvarez emphasized the wealth generation that could result from taxing cannabis production and sales. With billions of pesos in potential revenue, he proposed redirecting these funds towards vital public services and infrastructure projects, offering a solution to pressing societal needs exacerbated by the ongoing pandemic-induced economic crisis.The move towards marijuana legalization in the Philippines represents a paradigm shift in drug policy, moving away from punitive approaches towards a more evidence-based and pragmatic stance. By acknowledging the potential benefits of legalization, advocates are striving to address the societal, economic, and health-related challenges associated with current drug regulations.

However, the journey towards legal reform is not without challenges. Opposition and skepticism persist, with concerns raised about the societal and medical implications of cannabis legalization. Policymakers must engage in informed discussions, considering expert opinions and international best practices, to address these concerns effectively.As the legislative process unfolds, transparency, inclusivity, and evidence-based decision-making must guide proceedings. Collaboration between the dangerous drugs committee and the health committee, as well as input from stakeholders and experts, will be essential in shaping comprehensive and effective marijuana regulation policies.Ultimately, the push for legal reform on marijuana in the Philippines reflects a broader global trend toward progressive drug policies. By embracing evidence-based approaches, prioritizing harm reduction, and fostering public dialogue, the Philippines has the opportunity to lead the way toward a more equitable, just, and forward-thinking drug policy framework.

Analyzing The Implications Of House Bill No. 6783In the ongoing debate over drug policy reform in the Philippines, House Bill No. 6783, proposed by former House Speaker Pantaleon Alvarez, has emerged as a focal point. This bill seeks to exclude cannabis, cannabis resin and extracts, and tinctures of cannabis from the list of dangerous drugs outlined in Republic Act No. 9165.Under the current law, individuals convicted of cultivating marijuana or possessing specified quantities of cannabis face severe penalties, including hefty fines and even life imprisonment. Alvarez's proposal challenges this punitive approach, arguing for the delisting of cannabis and its derivatives from the dangerous drugs list.However, concerns have been raised regarding the potential consequences of delisting cannabis. Batanes Representative Ciriaco Gato, for instance, expressed apprehension that such a move could pave the way for the recreational use of marijuana. Gato emphasized the need to consider the negative effects of cannabis, both from medical and social standpoints and urged caution in deliberating on the proposed bill.As the proposal progresses through the legislative process, it faces several challenges and uncertainties. Despite the formation of a technical working group (TWG) by the lower chamber's dangerous drugs committee, chaired by Robert Ace Barbers, 'House Bill Number NO. 6783 is not considered a priority by the Marcos administration.' Barbers himself has emphasized the importance of further discussions and expert opinions before advancing the measure.

Progress and ChallengesWhile there are multiple bills referred to the health committee seeking to legalize medicinal marijuana progress on this front has been slow. Although the House approved a bill on medical marijuana during the 17th Congress, it failed to gain traction in the Senate. Subsequent attempts in the 18th Congress also faced obstacles, highlighting the challenges of advancing drug policy reform in the Philippines.Despite these challenges, there is growing momentum towards a more progressive approach to marijuana regulation in the country. Advocates argue that legalizing cannabis could lead to significant economic benefits, including increased government revenue and job creation. Furthermore, there is increasing recognition of the potential therapeutic benefits of this plant, which could improve access to treatment for patients suffering from various ailments.As the debate continues, policymakers need to consider evidence-based approaches, prioritize harm reduction, and engage in transparent and inclusive discussions. By doing so, the Philippines has the opportunity to navigate the complexities of drug policy reform and move towards a more just, equitable, and forward-thinking approach to marijuana regulation.

Final ThoughtsIn conclusion, advocates' efforts to push for legal reform on marijuana in the Philippines represent a crucial step towards building a more progressive and humane drug policy. By challenging outdated paradigms and embracing evidence-based strategies, the country has the potential to pave the way for a brighter and more compassionate future for all its citizens.

FAQs about Marijuana in the Philippines

Is marijuana legal in the Philippines?

No, marijuana is currently illegal in the Philippines. It is classified as a dangerous drug under Republic Act No. 9165, also known as the Comprehensive Dangerous Drugs Act.

What are the penalties for possessing cannabis in the Philippines?

Penalties for possessing cannabis in the Philippines vary based on the quantity involved. Individuals convicted of possession can face fines and imprisonment, with more severe penalties for larger quantities.

Is medical marijuana legal in the Philippines?

As of now, medical cannabis is not legal in the Philippines. However, there have been efforts to legalize medicinal cannabis, with bills proposed in the Philippine Congress. These bills aim to allow the use of marijuana for medical purposes under regulated conditions.

What is the current status of marijuana legalization efforts in the Philippines?

There have been ongoing discussions and debates about marijuana legalization in the Philippines. While some lawmakers and advocates push for reform, others remain cautious or opposed to the idea. Various bills have been filed in Congress, but progress has been slow, and legalization has not yet been achieved.

Are there any initiatives to decriminalize cannabis in the Philippines?

Yes, there have been initiatives to decriminalize cannabis in the Philippines. Some lawmakers argue that the current approach to drug policy, particularly regarding cannabis, is ineffective and overly punitive. Decriminalization efforts aim to shift towards a more lenient approach, focusing on harm reduction rather than strict enforcement.

What are the arguments for legalizing cannabis in the Philippines?

Proponents of marijuana legalization in the Philippines often cite potential economic benefits, such as tax revenue and job creation. They also argue that legalization could reduce the burden on the criminal justice system, allowing resources to be allocated more effectively. Additionally, advocates highlight the therapeutic benefits of medical cannabis for patients suffering from various illnesses.

What are the concerns about marijuana legalization in the Philippines?

Opponents of marijuana legalization in the Philippines raise concerns about potential negative effects on public health and safety. They worry about increased substance abuse, especially among young people, and the potential for marijuana to serve as a gateway to other drugs. There are also cultural and social considerations, as some fear that legalization could lead to moral and societal decay.

Is there public support for marijuana legalization in the Philippines?

Public opinion on marijuana legalization in the Philippines is divided. While some segments of the population support reform, others remain skeptical or opposed. Factors such as age, education, and cultural background can influence attitudes toward marijuana legalization.

Are there any efforts to educate the public about the effects of marijuana in the Philippines?

Yes, there are ongoing efforts to educate the public about the effects of marijuana in the Philippines. Government agencies, non-profit organizations, and health professionals often conduct campaigns and provide information about the risks and consequences of marijuana use. These efforts aim to raise awareness and promote informed decision-making regarding drug use.

Where can I find reliable information about marijuana laws and regulations in the Philippines?

Reliable information about marijuana laws and regulations in the Philippines can be obtained from official government sources, such as the Philippine Drug Enforcement Agency (PDEA) and the Department of Health (DOH). Additionally, reputable news outlets and legal organizations may provide updates and analysis on drug policy developments in the country.

Please leave this field empty

Subscribe to Our Newsletter

Get notified of the latest cannabis news, exclusive deals, and more!

We keep your data private and share your data only with third parties that make this service possible. Read our privacy policy for more info.

Email Address *

>Check your inbox or spam folder to confirm your subscription.

>

RECENT POSTS

href="https://getbudslegalize.com/push-for-reform-marijuana-in-the-philippines/"

title="A Turning Point: Advocates Push For Legal Reform On Marijuana In The Philippines"rel="nofollow"target="_blank">A Turning Point: Advocates Push For Legal Reform On Marijuana In The Philippines

href="https://getbudslegalize.com/push-for-reform-marijuana-in-the-philippines/"

rel="nofollow"target="_blank">Read More

href="https://getbudslegalize.com/wedding-cake-strain-review-growing-guide/"

title="Wedding Cake Strain Review & Growing Guide"rel="nofollow"target="_blank">Wedding Cake Strain Review & Growing Guide

href="https://getbudslegalize.com/wedding-cake-strain-review-growing-guide/"

rel="nofollow"target="_blank">Read More

href="https://getbudslegalize.com/guide-to-hydroponic-growing-media/"

title="A Comprehensive Guide to Hydroponic Growing Media: Pros and Cons"rel="nofollow"target="_blank">A Comprehensive Guide to Hydroponic Growing Media: Pros and Cons

href="https://getbudslegalize.com/guide-to-hydroponic-growing-media/"

rel="nofollow"target="_blank">Read More

href="https://getbudslegalize.com/complete-growing-guide-aeroponics-cannabis/"

title="Mastering Aeroponics: The Ultimate Guide to Growing Cannabis at Home"rel="nofollow"target="_blank">Mastering Aeroponics: The Ultimate Guide to Growing Cannabis at Home

href="https://getbudslegalize.com/complete-growing-guide-aeroponics-cannabis/"

rel="nofollow"target="_blank">Read More

Load More

BUY FROM OUR AFFILIATES AND SUPPORT US!

We rely on our partners to provide you with the best products and services. By purchasing from them, you support our website and get high-quality products. Thank you for being part of our community!

OUR FAVORITES SEED BANKS

Read the full article

0 notes

Text

China risks 1 million deaths from Covid in 'winter wave', models show

China risks 1 million deaths from Covid in ‘winter wave’, models show

A million Chinese are at risk of dying from Covid-19 over the coming winter months if President Xi Jinping continues his push to remove strict pandemic controls, new models show.

In a stunning reversal after protests against Xi’s zero-Covid policyIn the past week, Chinese officials have begun to dismantle the pandemic control system, which includes lockdowns, mass testing, state quarantine and…

View On WordPress

0 notes

Text

Blog Deliverable #1 :Inequality in the Justice System

I would like to explore the inequalities that many endure when encountering the United States’ criminal justice system. This topic will go beyond the Portland metropolitan area but does not exclude what many people in our community may experience. “The U.S locks up more people per capita than any other nation, at the staggering rate of 573 per 100,000 residents.” (Initiative & Wagner, n.d.)

Given this statistic, one can only begin to wonder what separates the United States’ criminal justice system from the rest of the world. To recognize this, we must critically analyze how our justice system is tailored at the local, state and federal level. “In addition to the 1.6 million people incarcerated in federal and state prisons, there are more than 600,000 people locked up in more than 3,000 local jails throughout the U.S. Over 70 percent of these people in local jails are being held pretrial — meaning they have not yet been convicted of a crime and are legally presumed innocent.” (Prison Policy Initiative, 2016) Jails are the first step in the criminal justice system process and it is imperative that we reflect on how people get to this first step.

My field of research will show how race, gender and socioeconomic factors play into incarceration and recidivism rates. This should encourage us to reevaluate how we structure our criminal justice system and its long-term relationship with public health and safety. Since men are the majority of the prison population, we also must consider how most correctional facilities are structured and do not accommodate the unique needs of other genders. When we consider the variable needs of people in our community and all across the nation, we can recognize that our criminal justice system is doing more harm than good. “At least 1 in 4 people who go to jail will be arrested again within the same year — often those dealing with poverty, mental illness, and substance use disorders, whose problems only worsen with incarceration.” (Prison PolicyInitiative, 2016)

It is my belief that Oregon should reform it’s sentencing policies to avoid over-criminalizing behavior that poses little threat to public safety. It is important for our criminal justice system to implement strategies that will ultimately rehabilitate an individual so they may successfully reenter the community and avoid recidivism.

Sawyer, W. (2022, March 14). Mass incarceration: The whole pie 2022. Prison Policy Initiative.Retrieved October 23, 2022, from https://www.prisonpolicy.org/reports/pie2022.html#reforms

Prison Policy Initiative. (2016, May 10). Detaining the Poor: How money bail perpetuates an endless cycle of poverty and jail time. Prisonpolicy.org. https://www.prisonpolicy.org/reports/incomejails.html

Prison Policy Initiative. (2016, May 10). Detaining the Poor: How money bail perpetuates an endless cycle of poverty and jail time. Prisonpolicy.org. https://www.prisonpolicy.org/reports/incomejails.html

1 note

·

View note

Text

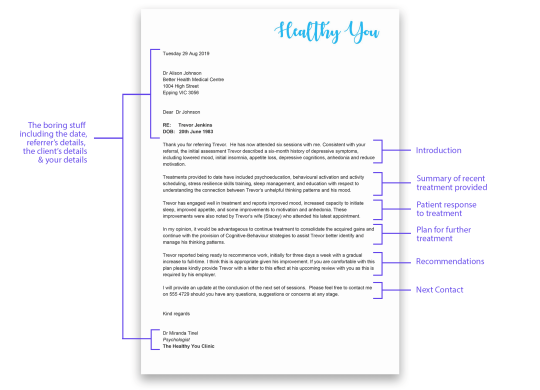

Example of a No Show Letter to Client

A no show letter to client is a type of reminder letter written by a service provider when a client does not show up for a meeting or appointment. A no show letter is sent when the client fails to show up, and they do not inform the service provider about their cancellation beforehand. The letter should be written in a polite manner, and the service provider should include the correct salutation and address in the letter. The following is an example of a no show letter to client.

Many healthcare providers have no show policies that require a client to sign an acknowledgement letter. Although most people read the handbook in advance, this is not a guarantee that the patient will be able to remember the policy. If the client fails to show up for the appointment, the letter will likely be returned to the practice by the mail courier. The no show letter is not just meant to make the client feel bad about canceling their appointment, it can also be used as a template for ghosting scenarios.

While a no show policy is a valuable part of managing your annual expenses, it can hurt the experience of the client. Studies show that ninety percent of clients would be willing to pay more for a better experience. For this reason, it's important to include a no show policyin your contract. A no show letter to client may seem harsh, but you should never let this deter you from implementing one.

youtube

SITES WE SUPPORT

Blogspot – Patient lettermail law

SOCIAL LINKS

Facebook

Twitter

LinkedIn

Instagram

Pinterest

0 notes

Link

Today Latest Update New Education Policy (NEP) Good Career in Fine Art, Design, Animation, Applied.

#art#artist#artwork#fineart#painting#kalabhumi#appliedart#animation#Neweducationpolicy#artchange#latesteducationpolicy#educationchange#career#design#sketchingclasses#drawing#diplomacourses#degree&certificatecourses#latesteducationchange#NEP2020#animationsketching#graphicdesigning#architecturedesign#kalabhumifineartcourses#careerinfineart#pencilsketch#kalabhumifounder#newpolicy

0 notes

Text

Curriculum for California School District Teaches Kindergartners That America Is Evil and Racist

Curriculum for California School District Teaches Kindergartners That America Is Evil and Racist

Piedmont Unified School District of Piedmont, California recently passed a policyin early September stating the district’s commitment to “equitable outcomes for students who identify as Black, Indigenous, and People of Color” through new race policies. These policies use tax dollars to teach children as young as kindergarten that their nation is evil, due to “our nation’s continuing history of…

View On WordPress

0 notes

Text

COVID-19 Environmental Law Implications

By Teresa Xu, Vanderbilt University Class of 2023

May 31, 2020

In the wake of the COVID-19 global pandemic and national emergency, the Environmental Protection Agency (EPA) has released a new temporary policyin which the EPA will not seek penalties for noncompliance with routine monitoring and reporting requirements if companies’ noncompliance was found to have been caused by the pandemic. Global efforts to combat climate change and improve upon plans have also been abandoned, with the 2020 climate summit postponed to next year. These actions seem to contradict the US’s extensive environmental laws and regulations and landmark international agreements to address climate change. These COVID-induced changes also have the potential to delay regulatory proposals due to lack of emissions data, exacerbate socioeconomic inequalities and health problems, disrupt foreign relations within North America, inflame nationalism and militarism, and overall impede global cooperation and crisis management. COVID-19 seems to intersect with climate change. However, lessons learned from the pandemic may be applied to our prevention and mitigation of climate change.Notably, the pandemic response has demonstrated that the global community can cooperate and invest in crisis-specific resources and even structural and legal shifts when an issue is deemed urgent enough and exemplified the devastating consequences of being unprepared to address a crisis.

For full article please visit

COVID-19 And Climate Change: Environmental Law Implications

at

Tennessee PreLaw Land

0 notes

Text

In Oval Office Meeting, Trump Expresses Regret on Vaping Policy

In Oval Office Meeting, Trump Expresses Regret on Vaping PolicyIn Oval Office Meeting, Trump Expresses Regret on Vaping Policy

NYT U.S. https://ift.tt/2RrtUhw

See More bd news live

See More visit live bangla news

0 notes

Text

Hunter Biden says he will resign from Chinese company board and won’t take foreign work if his father is president - The Washington Post

Hunter Biden says he will resign from Chinese company board and won’t take foreign work if his father is president – The Washington Post

Hunter Biden served, starting in 2014, as a paid board member for a Ukrainian gas company, Burisma Holdings, at a time when his father was shepherding U.S. policyin that country, including advocating for increased gas production. He left that position when his father announced his presidential candidacy earlier this year but has retained his role as a director and part owner of the Chinese…

View On WordPress

0 notes

Photo

SnehaTVLive/MidDayPolitics/28/8/19(11.30-12PM),Topic:NewRevenue PolicyIn T/'LAND' Rights& BoundariesBetterment OR?/AP(UP)Implements-T Still Publicizes?!/EarlierAttempts?/ 2019 “https://youtu.be/yR5WMamkhHg” Dr Tangella Siva Prasad Reddy, Independent Journalist.9440465339. https://www.instagram.com/p/B1szFVIl_Lk/?igshid=1rfbjjc37u964

0 notes

Photo

New Post has been published on https://fitnesstech.website/product/letscom-fitness-tracker-hr-activity-tracker-watch-with-heart-rate-monitor-w/

LETSCOM Fitness Tracker HR, Activity Tracker Watch with Heart Rate Monitor, W...

LETSCOM Fitness Tracker HR, Activity Tracker Watch with Heart Rate Monitor, Waterproof Smart Fitness Band with Step Counter, Calorie Counter, Pedometer Watch for Kids Women and Men LETSCOM Fitness Tracker HR, Activity Tracker Watch with Heart Rate Monitor, Waterproof Smart Fitness Band with Step Counter, Calorie Counter, Pedometer Watch for Kids Women and Men 24 Hour Shipping — Hassle Free Returns — Fast and Free ShippingDescription Heart Rate & Sleep Monitoring: Tracks real-time heart rate automatically & continuously and automatically tracks your sleep duration & consistency with comprehensive analysis of sleep quality data, helping you adjust yourself for a healthier lifestyle All-day Activity Tracking: Accurately record all-day activities like steps, distance, calories burned, active minutes and sleep status Multi-Sport Modes & Connected GPS: 14 exercise modes help you better understand specific activity data; Connect the GPS on your cellphone can show run stats like pace and distance and record a map of your workout route See Calls & Messages on Your Wrist: Receive call, calendar, SMS and SNS (Facebook, WhatsApp, LinkedIn, Instagram, and Twitter) notifications on display; never miss the messages that matter Built-in USB Plug: Easy to charge with any USB block and computer; no charging cable and dock needed; one single charge gives you up to 7 days of working time iPhone Egglettes ShippingOur orders are generally handled and processed within 1-2 business days, with most items being delivered within 3-5 business days. Your item(s) will be shipped using the most efficient carrier to your area (USPS, UPS, FedEx, Lasership, etc), which is determined once the order is received. Expedited shipping options are also available and can be selected during checkout. At this time, we only ship to physical addresses that are located within the 48 contiguous states of the United States of America. We are unable to ship to P.O. boxes, APO or FPO addresses, or international addresses directly. Some items may be elegable for purchase using eBay’s Global Shipping Program. For your protection and to ensure consistency in the Marketplace, all orders are shipped to your PayPal address provided at time of sale. Please ensure it is up to date prior to finalizing your purchase. We are not responsible for undeliverable / incorrect addresses. Return PolicyIn the unlikely event that you would like to return your purchase, we allow returns that are processed within 30 days of receipt of the merchandise. Please contact us for a return authorization and the return shipping address. Open software, music, games, movies, consumable items and personal hygiene products are not eligible for returns.PaymentWe want to ensure that our buyers receive all the benefits that eBay has to offer. In order to ensure that all of our buyers qualify for eBay Buyer Protection, we only accept payment through PayPal. Paypal allows you to complete your purchase quickly and securely. It offers a variety of payment options including all major credit cards. In order to ensure that all of our customers have equal access to our inventory, we require immediate payment.

MPN: ID115Plus HR

EAN: 0643824555228

UPC: 643824555228

Brand: LETSCOM

Label: LETSCOM

Manufacturer: LETSCOM

Color: Blue

Part Number: ID115Plus HR

Model: LS-004

ISBN: Does Not Apply

0 notes

Text

How tradition companies make customer-led change a reality - CIO New Zealand

Being extremely honest about the obstacles your organisation faces, and guaranteeing groups can trade stories with each other, are crucial ingredients in initiating a customer-led change.

That was the suggestions given by executive leaders from Fonterra, Mercury and Yellow Pages NZ, who spoke on a recent panel as part of the annual CIO-CMO Exchange occasion in Auckland. The panel discussion, entitled 'Actioning your organisation's CX ambitions', concentrated on what it requires to rearrange an existing, longstanding organisation around the customer.

Giant food producer, Fonterra, has actually just completed stage one of its digital change, which extremely much started with the consumer in mind, GM of digital improvement, Dominic Quin, said.

" There was recognition that consumer expectations were changing greatly and we required to equip ourselves to manage that," he informed participants. "We export to 100 markets and have great deals of various divisions. Back in 2015, we did a review and saw we were entering silos rather than in a cohesive manner. We produced our own strategy, digital 1.0, and built out an environment with Adobe, Salesforce, SAP ERP system and so on, so we can cohesively move forward and fulfill those expectations.".

Technology showed a natural location to begin and the way to unite groups that had been working very various across the organisation, Quin continued. The transformation also required Fonterra to press infrastructure and applications to the cloud with minimal customisation.

" We had 300+ sites globally, nobody understood how they were performing, if the material was right, or if we were geared up for a personalisation future, plus we had 37 CRMs all operating separately and nothing coming together," Quin said. "It's extremely tough to change an organisation when you're all on different technology stacks so you can find out off each other."

Probably, one of the greatest lessons learnt was letting individuals share stories and utilize cases with each other, Quin said.

" What we have formed recently is a little central group are 'adoption guilds'. These are very users who walk around and are enthusiastic about what they perform in the business and they share stories," he said. "They all talk the same language, since they're all on Salesforce or Adobe, they are all doing client journeys, they're all doing it the same method and using the basics the same."

Innovation might have supplied the platform for a standardisation of language and method, but it's the conversations and insights between groups that now drive improvement forward.

" When you speak about adoption, you've also got things like marketing automation, sales and service coming together. We have the components organisation talking to the customer service, talking to the food service organisation stating this is how we're utilizing our user interface between service and sales clouds, and how we get the best out of that," Quin added. "We being in the middle and foster that relationship.

" You need to get the buy in at the top table for the board and management team. But truly where it takes place remains in the everyday. If you can get purchase in actually early to go from 37 CRMs to one platform, which is hard, there's this natural flywheel of adoption and satisfaction with it."

Honesty as the very best policy

In a comparable vein, Yellow Pages CEO, Darren Linton, said it's on a whole-of-business improvement to become New Zealand's largest digital marketing company for SMEs, and one that has digital capability at its core. It already produces 50 percent of earnings through digital items and services, is Google's largest partner in the local market, and develops more sites for small company than anybody else in New Zealand and is working with the new brand promise, 'To help every company thrive'.

The issue is, many people don't comprehend what the organisation means today. "When I first came in as CMO, the discussion was 'are you men still around? And how do I cancel my book?'" Linton stated. "This service needs to transform. It's not a digital however service change we're undertaking. And it's that kind of brutal honesty we require to have in business to deliver."

Find out more AMP, Starlight discuss improvement journey: Salesforce World Tour One method Telephone directory is improving collaboration across groups is by welcoming agile-based scrums. The

objective is for staff to fret less about who they report to and take more responsibility around the project teams they're assigned to." Something that's made a huge distinction is what your reward and identify with people -there's nothing like putting genuine targets around customer NPS in individuals's remuneration," Linton continued." We're also really clear about the sorts of people we wish to come and work for us." We talk a lot about interest, determination and humility. You require individuals to be very open and work this out as you go, due to the fact that no one has all the answers

. You then need to persevere, since it's tough, and then you require to be modest enough to share across the teams.". Over at Mercury, GM of digital services, Kevin Angland, said the organisation is 100 per cent customer-led. However this wasn't the case three

or 4 years ago with earlier attempts at digital change." If I return 3-4 years back, it was an IT-led digital change," he remembered, adding this led to siloed teams that no one interacted with and who would shut

themselves away for months without any results to speak of. In Mercury's case, renewal of the brand name and alignment served as a driver for a transformation and customer-led mindset." We have actually lined up the organisation behind that customer-led pledge, inspiring and making it much easier for consumers," Angland stated." We do not have a digital 1.0 strategy since it

's all around the client. For that reason what we're delivering needs to line up behind the client pledge. It's about developing and preserving significance." That requires triggering both a reasonable and psychological response. As Angland pointed out, it's tough to get psychological about electricity. He pointed to recently launched' complimentary power days' as an

attempt to attach something psychological to what is a logical purchase. All of this sees Angland work together with Mercury's CMO. "I have obligation for service and functional elements of retail consumer proposition; she has obligation for the sales and marketing

aspects. In particular responsibility for result, we remain in it together and joined at the hip," he stated. Equally so is the remainder of the executive group." We're all behind that customer with the brand name, client pledge and experience throughout the enterprise, "Angland said." We're an organisation of engineers, and it's hard at

times to get them to create the emotional connection. What I can say in the last 12 months, every one of those personnel has actually spoken to a reality customer and discussed their experience." Construct on the client's terms Previous director of IT services at the University of Auckland and now head for Tech Solutions for Service( TS4B), Liz Coulter, said the experience of orchestrating a customer-led transformation is remarkably similar across both organisations, and

comes back to comprehending customer journey. That requires groups to realign and work in a nimble way to help bring the customer experience into planning and thinking. At the uni, for instance, a lot of work went into comprehending the trainee journey, experience and where digital could help."

At TS4B, it's about the consumer journey and how to make better experience for consumer end-to-end and offer much better IT service," she said." I remain in a group that's very highly focused who I want to alter to be more client

focused but from a digital options perspective. How do we transfer to that digital transition and create digital experiences for them." Once again, this comes back to team alignment and Angland stated the hearts and minds of individuals are the secret." There will be pockets that resist the change and want it to fail," he added. "Be successful breeds success." And it's success on the customer's terms that counts, Angland

added, so measure worth of work based upon the value it creates for clients." Two years earlier, the IT teams declared success at 3am, when a release was released in production and smoke tests showed whatever was

working. Not any longer. Success is identified by what's the capability doing for the consumer and what the groups are stating.

". Follow CMO on Twitter: @CMOAustralia, take part in the CMO conversation on LinkedIn: CMO ANZ, join us on Facebook: https://www.facebook.com/CMOAustralia, or examine us out on Google+: google.com/+CmoAu Sign up with the

CIO New Zealand group on LinkedIn. The group is open to CIOs, IT Directors, COOs, CTOs and senior IT supervisors. Sign up to get exclusive access to email subscriptions , event invites, competitors, giveaways, and a lot more. Subscription is free, and your security and privacy stay protected. View our privacy policy

before registering. Mistake: Please examine your e-mail address.

0 notes

Text

Is Suicide Covered Under Life Insurance Policy In India?

Is Suicide Covered Under Life Insurance Policy In India?

Multiple data sources show that India’s suicide rate is among the highest in the world. When a member of a family dies, it sometimes leaves the dependents financially crippled. It is an unexpected event for the family. An insurer usually gets his/her life insured to protect his/her from the difficult consequences of a loss of income. However, does the life insurance policy cover death by suicide?

View On WordPress

0 notes

Text

Types of Life Insurance Policies

Types of Life Insurance Policies | asuranci.com

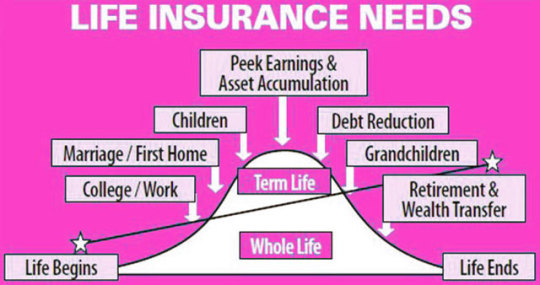

Insurance companies have present different levels of policies to suit different needs of public. At the time of confirming to buy a policy, a person must know firstly the amount of premium he will have to pay, secondly time span of insurance, and thirdly.sum insured with or without bonus. The following are the types of life insurance policies:

Types Of Life Insurance Policies

Whole life policy

Endowment policy

Term policy

Other life policies

Types Of Life Insurance Policies

1) Whole Life policy

In this type of policy the insured have to pay premium throughout his life or up to limited years. The amount is paid to the nominee of the insured on his death. This done for the protection of nominee's family. The rate of premium in the policy is low as compared to other policies of life insurance because amount is payable in the whole life. This type of policy has no financial gain to insured. It can be further classified into following types:

Ordinary whole life policy

Limited Premium whole life policy

Single Premium whole life policy

2) Endowment Policy

This type of policy is issued for a fixed specific period of time. Insured is payable to the policyholder on the maturity of the policy. Endowment policy is very popular because it makes provision for the security of the family. The following are the types of this policy:

Ordinary endowment policy

Pure endowment policy

Double Endowment policy

Deferred endowment policy.

3) Term Policy

It's a very old policy which is for 1, 2, 5 or 10 years. The money is paid back only after the death of the nominee. If the nominee survives more than the insured time than company will not pay back the amount. We have to make knowledge that it's neither saving nor investment. It has following types:

Straight Term policy

Convertible Term Policy

Decreasing Term Policy

Renewal Term Policy

4) Other Life Policies

Some of the types of life insurance are as follows:

Single Premium Insurance

Joint Life Policy

Group Life Insurance

Multipurpose Insurance Policy

Maybe you want to know about:

Basic Concepts of Insurance

10 Reasons Why Insurance is Important

Health Insurance Policy

Types of Life Insurance Policies

What Is Insurance : Insurance Definition

Types of Life Insurance

Life insurance protection comes in many forms, and not all policies are created equal, as you will soon discover. While the death benefit amounts may be the same, the costs, structure, durations, etc. vary tremendously across the types of policies.

Whole Life

Whole life insurance provides guaranteed insurance protection for the entire life of the insured, otherwise known as permanent coverage. These policies carry a "cash value" component that grows tax deferred at a contractually guaranteed amount (usually a low interest rate) until the contract is surrendered. The premiums are usually level for the life of the insured and the death benefit is guaranteed for the insured's lifetime.

With whole life payments, part of your premium is applied toward the insurance portion of your policy, another part of your premium goes toward administrative expenses and the balance of your premium goes toward the investment, or cash, portion of your policy. The interest you accumulate through the investment portion of your policy is tax-free until you withdraw it (if that is allowed under the terms of your policy). Any withdrawal you make will typically be tax free up to your basis in the policy. Your basis is the amount of premiums you have paid into the policy minus any prior dividends paid or previous withdrawals. Any amounts withdrawn above your basis may be taxed as ordinary income. As you might expect, given their permanent protection, these policies tend to have a much higher initial premium than other types of life insurance. But, the cash build up in the policy can be used toward premium payments, provided cash is available. This is known as a participating whole life policy, which combines the benefits of permanent life insurance protection with a savings component, and provides the policy owner some additional payment flexibility.

Universal Life

Universal life insurance, also known as flexible premium or adjustable life, is a variation of whole life insurance. Like whole life, it is also a permanent policy providing cash value benefits based on current interest rates. The feature that distinguishes this policy from its whole life cousin is that the premiums, cash values and level amount of protection can each be adjusted up or down during the contract term as the insured's needs change. Cash values earn an interest rate that is set periodically by the insurance company and is generally guaranteed not to drop below a certain level.

Variable Life

Variable life insurance is designed to combine the traditional protection and savings features of whole life insurance with the growth potential of investment funds. This type of policy is comprised of two distinct components: the general account and the separate account. The general account is the reserve or liability account of the insurance provider, and is not allocated to the individual policy. The separate account is comprised of various investment funds within the insurance company's portfolio, such as an equity fund, a money market fund, a bond fund, or some combination of these. Because of this underlying investment feature, the value of the cash and death benefit may fluctuate, thus the name "variable life".

Variable Universal Life

Variable universal life insurance combines the features of universal life with variable life and gives the consumer the flexibility of adjusting premiums, death benefits and the selection of investment choices. These policies are technically classified as securities and are therefore subject to Securities and Exchange Commission (SEC) regulation and the oversight of the state insurance commissioner. Unfortunately, all the investment risk lies with the policy owner; as a result, the death benefit value may rise or fall depending on the success of the policy's underlying investments. However, policies may provide some type of guarantee that at least a minimum death benefit will be paid to beneficiaries.

Term Life

One of the most commonly used policies is term life insurance. Term insurance can help protect your beneficiaries against financial loss resulting from your death; it pays the face amount of the policy, but only provides protection for a definite, but limited, amount of time. Term policies do not build cash values and the maximum term period is usually 30 years. Term policies are useful when there is a limited time needed for protection and when the dollars available for coverage are limited. The premiums for these types of policies are significantly lower than the costs for whole life. They also (initially) provide more insurance protection per dollar spent than any form of permanent policies. Unfortunately, the cost of premiums increases as the policy owner gets older and as the end of the specified term nears. (To learn more, read Buying Life Insurance: Term Vs. Permanent and What is term insurance?)

Term polices can have some variations, including, but not limited to:

Annual Renewable and Convertible Term: This policy provides protection for one year, but allows the insured to renew the policy for successive periods thereafter, but at higher premiums without having to furnish evidence of insurability. These policies may also be converted into whole life policies without any additional underwriting.

Level Term: This policy has an initial guaranteed premium level for specified periods; the longer the guarantee, the greater the cost to the buyer (but usually still far more affordable than permanent policies). These policies may be renewed after the guarantee period, but the premiums do increase as the insured gets older.

Decreasing Term: This policy has a level premium, but the amount of the death benefit decreases with time. This is often used in conjunction with mortgage debt protection.

Many term life insurance policies have major features that provide additional flexibility for the insured/policyholder. A renewability feature, perhaps the most important feature associated with term policies, guarantees that the insured can renew the policy for a limited number of years (ie. a term between 5 and 30 years) based on attained age. Convertibility provisions permit the policy owner to exchange a term contract for permanent coverage within a specific time frame without providing additional evidence of insurability.

Food for Thought

Many insurance consumers only need to replace their income until they've reached retirement age, have accumulated a fair amount of wealth, or their dependents are old enough to take care of themselves. When evaluating life insurance policies for you and your family, you must carefully consider the purchase of temporary versus permanent coverage. As you have just read, there are many differences in how policies may be structured and how death benefits are determined. There are also vast differences in their pricing and in the duration of life insurance protection.

Many consumers opt to buy term insurance as a temporary risk protection and then invest the savings (the difference between the cost of term and what they would have paid for permanent coverage) into an alternative investment, such as a brokerage account, mutual fund or retirement plan.

TYPES OF LIFE INSURANCE POLICIES

You know that you need life insurance. However, with the wide variety of insurance policies available, you may find choosing the right one difficult. It's really not as confusing as it seems, however, once you understand the basic types of life insurance policies.

Term life insurance

With a term policy, you get "pure" life insurance coverage. Term insurance provides a death benefit for only a specific period of time. If you die during the coverage period, your beneficiary (the person you named to collect the insurance proceeds) receives the death benefit (the face amount of the policy). If you live past the term period, your coverage ends, and you get nothing back.

Term insurance is available for periods ranging from 1 year to 30 years or more. You may be able to renew the policy for a new term without regard to your health, but at a higher rate. Your premium goes toward administrative expenses, company profit, and a reserve account that pays claims to those who die during the term period. As you get older, the chance that you will die increases. To cover this increasing risk, your premiums will likewise rise at regular intervals. For this reason, premiums that were quite inexpensive at the time you initially purchased your term policy will become much more expensive as you get older. Most term insurance also has a conversion feature that allows you to switch your coverage to some type of permanent insurance without answering health questions.

Traditional whole life insurance--guaranteed premiums

Whole life insurance is a type of permanent insurance or cash value insurance. Unlike term insurance, which provides coverage for a particular period of time, permanent insurance provides coverage for your entire life. When you make premium payments, you pay more than is needed to pay for the current costs of insurance coverage and expenses. The excess payment is credited to a cash value account. This cash value account allows the insurance company to charge a level, guaranteed premium* and to provide a death benefit and cash value throughout the life of the policy.

As you make payments, the cash value account grows. With traditional whole life insurance, the cash value account is guaranteed* and held in the insurance company's general portfolio--you don't get to choose how the cash value account is invested. However, the cash value can potentially grow beyond its guaranteed amount through the payment of dividends (profits earned by a "mutual" insurer). The cash value grows tax deferred and can either be used as collateral to borrow from the insurance company or be directly accessed through a partial or complete surrender of the policy. It is important to note, however, that a policy loan or partial surrender will reduce the policy's death benefit, and a complete surrender will terminate coverage altogether.

If you live to the policy's maturity date, the policy will "endow," and the insurance company will pay the accumulated cash value (equal at maturity to the death benefit) to you.

Universal life--openness and flexibility

Universal life is another type of permanent life insurance with a death benefit and a cash value account. Like whole life insurance, the cash value is held in the insurance company's general portfolio--you don't get to choose how the account is invested. Unlike traditional whole life, universal life insurance allows you flexibility in making premium payments.

A universal life insurance policy will generally provide very broad premium guidelines (i.e., minimum and maximum premium payments), but within these guidelines you can choose how much and when you pay premiums. Reducing or increasing premiums will impact the growth of the cash value component and possibly the death benefit. You are also free to change the policy's death benefit directly (again, within the limits set out by the policy) as your financial circumstances change. Be aware, however, that if you want to raise the amount of coverage, you'll need to go through the insurability process again, probably including a new medical exam, and your premiums will increase.

Universal life policies reveal all aspects of the policy's cost structure, including the cost of insurance (the portion set aside to pay claims) and expenses. This information is not always available with other types of policies. Another feature of universal life is the option to add the cash value to the face amount when the death benefit is paid. For example, say you die when you have $200,000 of cash value within your $1 million policy. If you chose the enhanced benefit option, your beneficiary receives $1.2 million. Keep in mind, however, that nothing is free--the increased benefit is reflected in premium calculations.

Variable life--you make the investment decisions

Like other types of permanent life insurance, variable life insurance has a cash value account. A variable life insurance policy, however, allows you to choose how your cash value account is invested. A variable life policy generally contains several investment options, known as subaccounts, that are professionally managed to pursue a stated investment objective. Choices can range from a fixed interest subaccount to a highly volatile international growth subaccount. Variable life insurance policies require a fixed annual premium for the life of the policy and may provide a minimum guaranteed death benefit*. If the cash value account exceeds a certain amount, the death benefit will increase.

Variable universal life--the ultimate in flexibility

Variable universal life combines all of the options and flexibility of universal life with the investment choices of a variable policy. It is a true hybrid product, and you make most of the policy decisions. You decide how often and how much your premium payments are to be, within guidelines. With most variable universal life policies, you get no guaranteed minimum cash value or death benefit. Your premium payments in excess of administrative costs and the cost of insurance are invested in the variable subaccounts that you choose.

As with both variable and universal life insurance, your policy may lapse if the cash value account falls below a certain level. Low-interest loans can be taken against your cash value account, and cash withdrawals are available. However, keep in mind that your policy's face amount is reduced by the amount of a policy withdrawal, and withdrawals may be taxable. You have the option of choosing a fixed or enhanced death benefit. Today, most variable universal life policies offer a rider that guarantees the death benefit at a certain level regardless of the performance of the subaccounts, provided that a stated minimum premium is paid for a predetermined number of years*.

*Any guarantees associated with payment of death benefits, income options, or rates of return are subject to the claims-paying ability of the insurer.

Joint or survivorship life for you and your spouse

Some married couples choose to buy insurance together within the same policy. These policies take the form of either a joint first-to-die or a joint second-to-die (survivorship) design. With first-to-die, the death benefit is paid at the death of the spouse who dies first. With second-to-die, no death benefit is paid until both spouses are deceased. Second-to-die policies are commonly used in estate planning to create a pool of funds to pay estate taxes and other expenses due at the death of the second spouse. Joint and survivorship policies are generally available under any type of permanent life insurance. Other than the fact that two people are insured under one policy, the policy characteristics remain the same.

0 notes

Last Seen Blogs