#Scaffold Technology Market Growing Popularity

Text

Scaffold Technology Market Industry Share, Size, Growth, Demands, Revenue, Top Leaders and Forecast to 2028

Industry Analysis

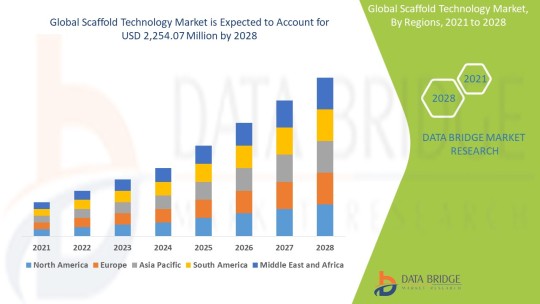

The scaffold technology market is expected to witness market growth at a rate of 8.89% in the forecast period of 2021 to 2028 and is expected to reach 2,254.07 USD million by 2028.

Additionally, the credible Scaffold Technology Market report helps the manufacturer in finding out the effectiveness of the existing channels of distribution, advertising programs, or media, selling methods and the best way of distributing the goods to the eventual consumers. Taking up such market research report is all the time beneficial for any company whether it is a small scale or large scale, for marketing of products or services. It makes effortless for healthcare industry to visualize what is already available in the market, what market anticipates, the competitive environment, and what should be done to surpass the competitor.

Get a Free Sample of The Report: https://www.databridgemarketresearch.com/request-a-sample/?dbmr=global-scaffold-technology-market

Market Insights and Scope

Scaffolds can be defined as the artificial extracellular matrices that support the 3D tissue regenerations and accommodate cells. These can be either permanent or temporary matrices which offer mechanical, chemical and biological support for the tissue formation. Scaffold technology is applied to present 3D culture assays that involve cell to cell interactions, high throughput screening, cell to matrix interactions, transfections, and cell migration assays.

An international Scaffold Technology Market research report examines competitive companies and manufacturers in the global market. Competitive analysis carried out in this market report puts forth the moves of the key players in the healthcare industry such as new product launches, expansions, agreements, joint ventures, partnerships, and recent acquisitions. This market report puts light on various aspects of marketing research that range from important industry trends, market size, market share estimates, sales volume, emerging trends, product consumption, customer preferences, historic data along with future forecast and key player analysis. It studies market by product type, applications and growth factors.

Get full access to the report: https://www.databridgemarketresearch.com/reports/global-scaffold-technology-market

Industry Segmentation

The scaffold technology market is segmented on the basis of type, application, disease and end use. The growth amongst these segments will help you analyse meagre growth segments in the industries, and provide the users with valuable market overview and market insights to help them in making strategic decisions for identification of core market applications.

On the basis of type, the scaffold technology market is segmented into hydrogels, wound healing, 3d bio printing, and immunomodulation. Hydrogels is further sub segmented into polymeric scaffolds, micropatterned surface microplates and nanofiber-based scaffolds.

On the basis of application, the scaffold technology market is segmented into stem cell therapy, regenerative medicine, and tissue engineering, drug discovery, and others.

On the basis of disease, the scaffold technology market is segmented into orthopaedics, musculoskeletal, and spine, cancer, skin and integumentary, dental, cardiology and vascular, neurology, urology, GI, gynaecology, and others.

On the basis of end use, the scaffold technology market is segmented into biotechnology and pharmaceutical industries, research laboratories and institutes, hospitals and diagnostic centers, and others.

Market Country Level Analysis

The countries covered in the scaffold technology market report are the

U.S., Canada and Mexico in North America, Germany, France, U.K., Netherlands, Switzerland, Belgium, Russia, Italy, Spain, Turkey, Rest of Europe in Europe, China, Japan, India, South Korea, Singapore, Malaysia, Australia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific (APAC) in the Asia-Pacific (APAC), Saudi Arabia, U.A.E, South Africa, Egypt, Israel, Rest of Middle East and Africa (MEA) as a part of Middle East and Africa (MEA), Brazil, Argentina and Rest of South America as part of South America.

An influential Scaffold Technology Market research report displays an absolute outline of the market that considers various aspects such as product definition, customary vendor landscape, and market segmentation. Currently, businesses are relying on the diverse segments covered in the market research report to a great extent which gives them better insights to drive the business on the right track. The competitive analysis brings into light a clear insight about the market share analysis and actions of the key industry players. With this info, businesses can successfully make decisions about business strategies to accomplish maximum return on investment (ROI).

Industry Share Analysis

The major players covered in the scaffold technology market report are

Thermo Fisher Scientific, Merck KGaA, Tecan Trading AG, REPROCELL Inc., 3D Biotek LLC, BD, Medtronic, XANOFI, Molecular Matrix, Inc., Matricel GmbH,, 4titude, Pelobiotech Corning Incorporated, Akron Biotechnology LLC, Bioquote Ltd, Avacta Life Sciences Limited., Nanofiber Solutions, Vericel Corporation, NuVasive, Inc., Allergan plc, among other domestic and global players. Market share data is available for global, North America, Europe, Asia-Pacific (APAC), Middle East and Africa (MEA) and South America separately. DBMR analysts understand competitive strengths and provide competitive analysis for each competitor separately.

Browse Related Reports@

Global Frozen Vegetables Market

South Africa Battery Market

Global Plant-Based Egg Market

Global Nutritional Beverages market

Spain Fuel Cards Market for Commercial Fleet

Europe Fall Detection System Market

About Us:Data Bridge Market Research set forth itself as an unconventional and neoteric Market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market

Contact:

Data Bridge Market Research

Tel: +1-888-387-2818

Email: [email protected]

#Scaffold Technology Market Growing Popularity#Scaffold Technology Market Global Leading Brands#Scaffold Technology Market drivers-advantages#Scaffold Technology Market Segmentation-CAGR rate#Scaffold Technology Market Demands-Size-Share-Top Trends#Scaffold Technology Market Industry-Competitors#Scaffold Technology Market Growth-Competition#Scaffold Technology Market 2028 by Types-Application#Scaffold Technology Market Healthcare Industry

0 notes

Text

Bamboos Market Dynamics: Global Growth and Trends (2023-2032)

The global bamboo market is projected to grow from USD 75,102.79 million in 2023 to USD 123,163.38 million by 2032, at a CAGR of 5.65%.

The bamboo market is experiencing robust growth due to its versatile applications and sustainable attributes. Bamboo, a fast-growing grass, is increasingly recognized for its eco-friendly properties, including its ability to sequester carbon and reduce soil erosion. Its applications span across various industries such as construction, where it is used as a strong and durable building material, and the textile industry, where bamboo fibers are utilized to produce soft, breathable, and biodegradable fabrics. Additionally, bamboo is popular in the production of household items, furniture, paper, and even food products. The rising consumer awareness about sustainability, coupled with the growing demand for renewable and biodegradable materials, is driving the market. Governments and environmental organizations are also promoting bamboo cultivation and utilization as a means to combat deforestation and promote sustainable agricultural practices. As a result, the bamboo market is poised for continued expansion, supported by technological advancements in processing and the increasing adoption of eco-friendly products across the globe.

Bamboo offers numerous advantages that make it a highly desirable material across various applications:

1. Sustainability and Environmental Benefits

Rapid Growth: Bamboo is one of the fastest-growing plants in the world, with some species capable of growing up to 3 feet in 24 hours, making it a highly renewable resource.

Carbon Sequestration: Bamboo absorbs carbon dioxide and releases oxygen at a higher rate compared to many trees, contributing to the reduction of greenhouse gases.

Soil Conservation: Bamboo roots help prevent soil erosion and improve soil health by stabilizing the soil and enhancing water retention.

Minimal Environmental Impact: Bamboo can be grown without the use of pesticides and fertilizers, reducing environmental pollution and promoting healthier ecosystems.

2. Versatility and Diverse Applications

Construction: Bamboo’s strength and flexibility make it an excellent material for construction, used in building homes, scaffolding, flooring, and roofing.

Textiles: Bamboo fibers are used to produce soft, breathable, and hypoallergenic fabrics for clothing, bed linens, and towels.

Household Items: Bamboo is used to manufacture a wide range of household items, including furniture, kitchenware, and decorative items.

Paper and Pulp: Bamboo is a sustainable alternative to wood for paper and pulp production, reducing the pressure on forest resources.

Food Products: Bamboo shoots are edible and are a nutritious food source in many cultures.

3. Economic Benefits

Job Creation: Bamboo cultivation and processing create jobs in rural and urban areas, supporting local economies and providing livelihoods.

Market Potential: The increasing demand for sustainable and eco-friendly products opens up significant market opportunities for bamboo-based products.

4. Health and Safety

Anti-bacterial Properties: Bamboo fibers naturally possess anti-bacterial and anti-fungal properties, making them ideal for products like clothing and bedding that are in direct contact with the skin.

Hypoallergenic: Bamboo is hypoallergenic, making it suitable for individuals with sensitive skin or allergies.

5. Durability and Strength

High Strength-to-Weight Ratio: Bamboo has a high strength-to-weight ratio, making it an ideal material for construction and manufacturing durable goods.

Flexibility and Resilience: Bamboo’s natural flexibility allows it to withstand impacts and stresses better than many other materials.

6. Aesthetic Appeal

Natural Beauty: Bamboo has a natural, attractive appearance that enhances the aesthetic value of products and structures made from it.

Variety: It comes in various colors, patterns, and textures, allowing for diverse design possibilities.

7. Climate Adaptability

Grows in Diverse Climates: Bamboo can thrive in a variety of climates, from tropical to temperate regions, making it a versatile crop for different geographical areas.

Low Water Requirement: Some species of bamboo require relatively low amounts of water compared to other crops, making them suitable for areas with water scarcity.

8. Resource Efficiency

Minimal Land Use: Bamboo requires less land to grow compared to traditional timber, making it an efficient use of agricultural land.

Short Harvest Cycle: Bamboo can be harvested within 3-5 years, much shorter than the decades required for most hardwood trees, ensuring a quicker return on investment.

Key Player Analysis

MOSO International B.V.

Bamboo Australia

Bamboo Village Company Limited

Shanghai Tenbro Bamboo Textile Co., Ltd.

Simply Bamboo Pty Ltd.

Xiamen HBD Industry & Trade Co., Ltd.

Dassogroup

Smith & Fong

Anji Tianzhen Bamboo Flooring Co., Ltd.

Fujian HeQiChang Bamboo Product Co., Ltd.

More About Report- https://www.credenceresearch.com/report/bamboos-market

The bamboo market is influenced by several dynamic factors that shape its growth and development. Understanding these market dynamics is essential for stakeholders to navigate and capitalize on opportunities within the market. Here are the key dynamics affecting the bamboo market:

1. Market Drivers

a. Growing Demand for Sustainable Products

Environmental Awareness: Increasing consumer awareness about environmental sustainability and the impact of deforestation is driving demand for eco-friendly products, including bamboo-based goods.

Government Policies: Supportive government policies and initiatives promoting sustainable agriculture and the use of renewable resources are boosting bamboo cultivation and product development.

b. Versatile Applications

Construction: Bamboo’s strength and versatility make it an attractive material for construction, leading to its increased use in building materials, scaffolding, and flooring.

Textiles: The textile industry’s shift towards sustainable fibers is enhancing demand for bamboo fabrics, which are soft, breathable, and biodegradable.

c. Economic Benefits

Job Creation: Bamboo cultivation and processing create employment opportunities in rural and urban areas, supporting local economies.

Market Expansion: Expanding markets for bamboo products, including furniture, household items, and paper, contribute to economic growth.

2. Market Restraints

a. High Initial Costs

Investment Requirements: High initial investment costs for bamboo plantation and processing infrastructure can be a barrier for new entrants and small-scale farmers.

Processing Challenges: The need for specialized equipment and technology for processing bamboo into various products can also add to the cost.

b. Competition from Other Materials

Alternative Materials: Bamboo faces competition from other sustainable materials such as recycled plastics, organic cotton, and other eco-friendly alternatives, which can limit its market share.

c. Regulatory Hurdles

Standardization Issues: Lack of standardized regulations and quality control measures for bamboo products in some regions can affect market growth and consumer trust.

3. Market Opportunities

a. Technological Advancements

Innovations in Processing: Advances in processing technologies are making bamboo products more competitive by improving their quality and reducing production costs.

New Product Development: Continuous research and development efforts are leading to the creation of innovative bamboo products, expanding its application range.

b. Expansion into New Markets

Emerging Economies: Increasing demand for sustainable products in emerging economies presents significant growth opportunities for the bamboo market.

Diverse Applications: Exploring new applications for bamboo in sectors such as automotive interiors, renewable energy, and biodegradable plastics can drive market growth.

c. Sustainability Trends

Circular Economy: Emphasis on circular economy practices, including recycling and sustainable resource management, aligns well with bamboo’s eco-friendly properties, fostering market expansion.

4. Market Challenges

a. Supply Chain Issues

Logistics and Transportation: Efficient transportation and logistics are critical for the bamboo supply chain, especially for exporting bamboo products to international markets.

Supply Consistency: Ensuring a consistent supply of high-quality bamboo can be challenging due to variations in cultivation practices and environmental conditions.

b. Awareness and Education

Consumer Awareness: Increasing consumer awareness about the benefits of bamboo products is essential for market growth, requiring effective marketing and educational campaigns.

Farmer Education: Educating farmers on sustainable bamboo cultivation practices and efficient processing techniques is crucial for maintaining supply quality and consistency.

5. Competitive Landscape

a. Strategic Initiatives

Partnerships and Collaborations: Collaborations between companies, research institutions, and governments are fostering innovation and market development.

Mergers and Acquisitions: Strategic mergers and acquisitions are helping companies expand their market presence and leverage synergies.

Segmentations:

Based on End-Use Industry:

Wood and furniture

Timber Substitute

Plywood

Mat Boards

Flooring

Furniture

Outdoor Decking

Construction

Scaffolding

Housing

Roads

Food (bamboo shoots)

Pulp and paper

Textile

Agriculture

Others (charcoal and handicrafts)

Browse the full report – https://www.credenceresearch.com/report/bamboos-market

Browse Our Blog: https://www.linkedin.com/pulse/bamboos-market-analysis-global-industry-trends-forecast-lqsef

Contact Us:

Phone: +91 6232 49 3207

Email: [email protected]

Website: https://www.credenceresearch.com

0 notes

Text

SCALING NEW HEIGHTS: A COMPREHENSIVE ANALYSIS OF THE GLOBAL MOBILE ELEVATED WORK PLATFORM (MEWP) MARKET

In recent years, the global Mobile Elevated Work Platform (MEWP) market has witnessed significant growth and transformation, driven by a myriad of factors ranging from technological advancements to an increased emphasis on safety in the workplace. As industries across the globe continue to expand and diversify, the demand for efficient and versatile aerial work platforms has soared, leading to a robust market landscape. The Global Mobile Elevated Work Platform (MEWP) market is expected to increase from USD 1481 million in 2022 to USD 2626 million in 2029.

The primary driver propelling the MEWP market's growth is the escalating need for improved efficiency and safety in various industries. With a rising emphasis on stringent safety regulations and compliance standards globally, companies are increasingly adopting MEWPs to enhance workplace safety while boosting productivity. The versatility of MEWPs in providing access to elevated areas across different industries, including construction, manufacturing, maintenance, and logistics, further contributes to their growing popularity.

The construction industry stands out as a major contributor to the MEWP market's expansion, driven by urbanization, infrastructure development, and increasing construction activities worldwide. MEWPs offer a safer and more efficient alternative to traditional scaffolding, particularly in complex and high-rise construction projects. Moreover, the versatility of MEWPs allows for increased manoeuvrability in tight spaces, facilitating construction tasks in urban environments where space constraints are prevalent.

In terms of the growth prospects and the opportunities landscape, the Asia-Pacific region emerges as a key player in the MEWP Market accounting for a market value of USD 421.18 Million in 2022 with a market share of 28% in 2022, driven by rapid industrialization, urban development, and infrastructure projects. China, India, and Southeast Asian countries are witnessing a surge in construction activities, creating a robust demand for MEWPs. In the forecast period, the market is expected to witness a significant growth. The Middle East and Africa also exhibit substantial growth opportunities, fueled by ongoing investments in infrastructure and energy projects.

0 notes

Text

Dental Bone Graft Substitutes

Jun 15, 2020 (Market Insight Reports) -- A recent report on Dental Bone Graft Substitutes Market provides a close analysis on the trade size, revenue forecasts and geographical landscape referring to this business house. to boot, the report highlights primary obstacles and latest growth trends accepted by key players that kind a region of the competitive spectrum of this business.

Surgeons square measure choosing MIS over open surgery thanks to connected advantages like reduced post-operative length, nominal pain, and fewer injury to the tissue.

Factors like technological advancements within the field of dental bone grafts and increase within the range of bone graft procedures area unit expected to drive the expansion of the world dental bone grafts substitutes market. many insurance suppliers within the U.S. and varied countries within the European region have assisted the medical sector to introduce and encourage the usage of latest artificial bone grafts and demineralized allografts.

This report principally considers four varieties of dental bone graft substitutes – transplant, artificial bone grafts, allograft, and demineralized graft. exploitation patient’s own bone (autograft) has historically been the foremost most popular technique of bone grafting; but, increasing technological advancements have raised the amount of artificial graft choices. the advantages of artificial grafts embody accessibility, sterility, and reduced morbidity. Also, the artificial bone grafts have a extended time period and there's no risk of any unwellness. thanks to these edges, artificial bone graft is that the fastest-growing kind within the dental bone graft substitutes market.

sample link :https://brandessenceresearch.com/healthcare/dental-bone-graft-substitutes-market-size

Scope of The Report:

Dental bone grafts square measure ordinarily utilized as fillers or scaffolds, that facilitate formation of bone and assist in healing of wound. In bone affixation technique, a American state novo bone is created that assists to heal bones that were broken at the time of a dental extraction surgery.

The dental bone graft substitutes market is divided by application, material, end-user, and merchandise. By material, the market contains demineralized bone matrix, autograft, allograft, xenograft, and artificial bone graft substitute. In terms of application, the dental bone graft substitutes market contains periodontic defect regeneration, socket preservation, ridge augmentation, implant bone regeneration, sinus lift, and others. Socket preservation is foreseen to guide the world market, attributable to the increase within the quantity of dental extractions. By product, the market is split into osteograf, grafton, bio-oss, and others. In terms of end-user, the dental bone graft substitutes market is split into hospitals, mobile surgical centers, and dental clinics. The rising range of dental clinics institution in developing nations is foreseen to power the expansion of this section.

Dental Bone Graft Substitutes Companies:

The major players included in the global dental bone graft substitutes market forecast are,

· Geistlich

· Institut Straumann

· BioHorizons IPH

· Zimmer Biomet

· ACE Surgical Supply

· DENTSPLY International

· LifeNet Health

· Medtronic

· RTI Surgical

· Dentium.

Dental Bone Graft Substitutes Market Key Segments:

By Material Analysis: Demineralized Bone Matrix (DBM), Autograft, Allograft, Xenograft, artificial Bone Graft Substitute,

By Application Analysis: Ridge Augmentation, Socket Preservation, dentistry Defect Regeneration, Implant Bone Regeneration, Sinus Lift, Others

By Product Analysis: Bio-Oss, Osteograf, Grafton, Others

By End-User Analysis: Hospitals, mobile Surgical Centers, Dental Clinics

Market by Regional Analysis:

North America (USA, Canada, Mexico), Europe (UK, France, Germany, Russia, Rest of Europe), Asia-Pacific (China, South Korea, India, Japan, Rest of Asia-Pacific), LAMEA, Latin America, Middle East, Africa

2 notes

·

View notes

Text

Women’s Health : The Even Weaker Sex

https://femuscleblog.wordpress.com/2015/08/13/even-weaker-sex-from-fiji-times-online/

This was article was originally posted by Daily Mail in 2013. Known for its sensationalist style of reporting it does have the right idea about women’s health. Faddy diets and fears that muscles are not feminine enough have left women physically weaker than their grannies almost sounds like a comedic tabloid headline. Women do suffer from negative body image issues. The problem is the focus is always on the physiological element, rather than how this actually effects physical health. Women need to exercise and build muscle for the sake of their musculoskeletal health. Osteoporosis, sarcopenia, and heart disease become major threats to health the longer one lives. Women on average will live longer than men so the possibility of getting a chronic illness is higher. Both men and women are getting less exercise in highly developed nations due to poor diets and sedentary lifestyles. Women are effected the most. The reason is they have less strength and muscle mass to begin with. According to Grant Tomkinson of the University of South Australia muscular strength and endurance has declined by 8 to 10 % since the 1980s. This is based on data gathered from the US, UK, and Canada.

What appears in the data accumulated at the time was that muscle power peaked around 1985. Yet, body weight as it is claimed has increased immensely. Muscles have gotten weaker with women getting even more physically weak. Some would say that weakness is a woman’s natural state, but it clearly is not. Starvation diets and lack of physical activity is clearly harming women’s bodies.Physiotherapist Sammy Margo stated “ there are skinny women who have no muscles supporting their spine, and overweight ladies who don’t have any muscles under the fat.” The serious danger related to health could be the increase in arthritis, stress fractures, and back pain. Women should not focus on weight loss as a sole motivating factor to exercise. The intent should be to be active enough to give the muscular system and skeleton enough care to prevent chronic disease. There also needs to be a change in body image perception. Too often, the fitness industry presents thin as the only image of beauty. Rather than following gender stereotype conventions, women should seek to boost their fitness levels. According to the Women’s Sports Foundation 40% of women said feeling better about their appearance was the motivating factor to exercise. Their intent was to get thinner, which does not automatically mean healthy. Proper weight depends on one’s height and skeletal mass.

There is a body type prejudice against women who show significant muscle and strength. The sexist attitude is so powerful that it scares women away from weight training. Even Jessica Ennis stated one time she was concerned about getting too muscular. The term “bulky’” is normally used to describe relally muscular people. That term has no basis in exercise physiology. There are different levels of muscular development that a person can achieve. Even the largest women, who are bodybuilders weigh less during competition. Compared to the rest of the weight of the majority of the population they are not bulky at all. Colette Nelson during competition only weighed about 145 lbs. The average weight of an American woman according to the CDC is ( at 5ft 3 inches) is a 168.5 lbs. That means Colette despite her appearance is technically not carrying around as much mass a one would assume.

Women normally reject weights saying they may end up looking like a female bodybuilder. This is not a simple task. This requires consistent training, diet, and supplements. Some may resort to performing enhancing drugs as a short cut in the recovery and muscular hypertrophy process. However, it erroneous to think that women have less athletic potential. The article correctly states that testosterone is very helpful for building muscle to a high degree. Endocrine function is not the only factor in building muscle, which explains why some women can actually get muscular. Muscular hypertrophy functions in the same manner in both men and women. Endocrinology just gives men an advantage during puberty, when strength spurts and body composition is altered. Estrogen enables the female body to carry more fat for the sake of reproduction. Regardless of sex, genetics, height, somatotype, training method, and nutrition are factors in building muscle and strength. There is a difference between training for hypertrophy or just strength. Women with mesomorphic body types prior to training can achieve more gains relative to women of ectomorphic and endomorphic body types. A woman can gain as much strength as an average man. However ,a man on the same training regimen will most likely have more mass and strength. It should be understood that the idea of toning does not have an exercise physiology basis either. Professor Ken Fox was quoted saying “they can get toned but looking like Arnold Schwarzenegger isn’t an issue,’ he says.” There are different degrees of muscular development, but toning is just another colloquial terms to describe a woman of a certain fitness level. This term is never applied to men rather the term bulk is. The fact is men and women have the same muscles. Through progressive overload they can increase strength and mass. The difference is in physical fitness capacity.

Whether the term bulk or tone is applied they are relative terms. The women displayed above are different depictions of levels of muscularity. What people refer to as toned is the woman at the top. There is a middle level that can best be described as a figure physique. Then there is the bulky look that normally is demonized in women. All these women have different degrees of muscular development so the terms “bulky” or “toned” are just not applicable. Women for a longtime were discouraged from use and control of their own bodies. Besides limiting reproductive rights, body image conformity had been imposed through various points in history. This encouraged women to either have their feet bound or wear corsets. The latest unhealthy measure is to make the body extra thin. Such obsession could put women and girls at risk for anorexia or bulimia. The problems with health and body image start in youth. Girls are not encouraged to be physically active as boys at home or in school. Children are also being negatively effected by a sedentary lifestyle in which video games and TV have replaced playing outside. Also sexist prejudice develops around this age. According to a Women’s Sports Foundation study of 15,000 school children half the 14 years girls surveyed claimed that getting sweaty was not feminine and a third of boys stated sporty women are not feminine. Already in youth children are absorbing the negative stereotypes and frailty myth related to women and their bodies.

This reveals their still is much to be done even though Title IX has made much progress in getting girls physically active. The rise of obesity and childhood weight problems have made it so that people are facing more potential health issues at a younger age. Before such panic should be raised, the study by Dr, Gavin Sandercock only examine 315 children in 2008 and then compared it with data from ten years earlier. That sample is small, so it may not represent all of the UK. What the data showed was arm strength had fallen 26 % and grip strength 7%. The children of the 2008 group could only do two thirds amount of sit-ups from the 1998 group sample. The only thing this indicates is that physical education needs improvement. Many teachers that teach those classes may not have a background in exercise physiology, sports science, or coaching. There may be a generation of people who are physically illiterate. The question one may wonder is why would it be significant in a technological society. Maintaining health is critical not just for the individual, but the nation at large. Healthcare systems will soon feel the strain of aging populations or common chronic illnesses. Public health may reach a crisis if governments do not act. From a perspective of economics, a sick population can be liability. Disability and the personal financial burden on individuals could effect markets. This is why it is important to have a functional universal healthcare system and to educate the public about exercise. Making physical education a positive experience for youth will influence their future health related behaviors.

Women need muscle for their health. This is not discussed as much in academic circles focused on women’s health issues. Muscle acts as a scaffolding for joints and bones in the human body. There are stages in which musculoskeletal mass grows in the body and at a certain age it will decline. The result could be sarcopenia and reduced mobility.

There are some studies that show that muscular strength can contribute to longevity. Losing balance and falling can be detrimental for older people. Broken bones and specifically broken hips may cause the loss of independent living. Contrary to popular belief, when bones heal they do not comeback stronger. Healthy muscles mean more mobility and possibly less falls later in life.J anet Lord, director of the Arthritis Research UK Centre for Musculoskeletal Ageing Research claims strong muscles will enable you to control your movement more preventing harmful incidents. The rise in back pain can be linked not only prolonged periods of sitting rather weak core muscles. The muscles of the stomach are responsible for holding up the body when sitting. If these muscles are too weak,then the labor is shifted to muscles in the back. That results in more pressure in strain causing increases in back pain. Posture is also effected causing some people to slump over. The tendons and ligaments in the back are also effected as well. This can also effect the neck and knees.

Women are not eating or dieting correctly. They may not eat enough or there protein consumption is low. Muscles need protein for cells.The sudden rise of whole food movements and veganism may be driving a trend to excluding meat or protein completely may not be the healthiest activity. Protein can be found in dairy products and meat. If one does not get enough, the body could cannibalize itself. Organs could be at risk in extreme cases. There still is debate on what is the correct amount of protein. If there is an attempt to manage weight eating less would be ineffective. Excluding sugar and fats would be more helpful combining it with exercise. The goal is to get enough protein based foods along with vegetables to ensure normal metabolic function. There are some positive developments that can be taken away from this. Women are now becoming more active in strength sports and see that lifting can be an effective means of weight loss. Positive depictions of female athletes can counter sexism and body image issues. The important revelation is that exercise physiology should be incorporated more into women’s health assessments. Doing so would be effective against common chronic illnesses later in life.

#women's health#sexism#female muscle#body image#fitness#physical education#exercise#health science#exercise physiology#public health

2 notes

·

View notes

Text

Bone Void Fillers Market is expected to witness Incredible Growth during 2021-2031 | Arthrex Inc., Baxter International Inc., Depuy Synthes Companies

Global Bone Void Fillers Market report from Global Insight Services is the single authoritative source of intelligence on Bone Void Fillers Market. The report will provide you with analysis of impact of latest market disruptions such as Russia-Ukraine war and Covid-19 on the market. Report provides qualitative analysis of the market using various frameworks such as Porters’ and PESTLE analysis. Report includes in-depth segmentation and market size data by categories, product types, applications, and geographies. Report also includes comprehensive analysis of key issues, trends and drivers, restraints and challenges, competitive landscape, as well as recent events such as M&A activities in the market.

A bone void filler is a material that is used to fill in empty spaces in bones. These materials are typically made of synthetic or biological materials. Bone void fillers are used to treat a variety of conditions, including osteonecrosis, non-unions, and congenital defects. The goal of treatment with a bone void filler is to improve the strength and stability of the bone and to provide a scaffold for new bone growth. Bone void fillers are typically used in combination with other treatments, such as surgery, to achieve the best possible outcome.

Get Access to A Free Sample Copy of Our Latest Report – https://www.globalinsightservices.com/request-sample/GIS21605/

Key Trends

The key trends in bone void fillers technology are:

1. The use of biodegradable materials: Biodegradable materials are becoming increasingly popular as bone void fillers because they are absorbed by the body over time, eliminating the need for surgery to remove the implant.

2. The use of natural materials: Natural materials, such as bone grafts from the patient’s own body, are also being used more frequently as bone void fillers.

Key Drivers

The key drivers of the Bone Void Fillers market are the increasing number of hip and knee surgeries, the rising geriatric population, and the growing preference for minimally invasive surgeries. The rising number of hip and knee surgeries is a major driver of the Bone Void Fillers market. Hip and knee surgeries are often required to treat conditions such as osteoarthritis, rheumatoid arthritis, and trauma.

Market Segmentation

By End-Use

Hospital

Specialty Clinics

By Application

Spine Fusion

Bone Fracture

By Type

Demineralized Bone Matrix

Collagen Matrix

By Region

North AmericaUS

Get A Customized Scope to Match Your Need Ask an Expert – https://www.globalinsightservices.com/request-customization/GIS21605

Key Players

Arthrex Inc.

Baxter International Inc.

Depuy Synthes Companies

Medtronic plc

NuVasive Inc.

Orthofix Medical Inc.

Smith and Nephew plc

With Global Insight Services, you receive:

10-year forecast to help you make strategic decisions

In-depth segmentation which can be customized as per your requirements

Free consultation with lead analyst of the report

Excel data pack included with all report purchases

Robust and transparent research methodology

Ground breaking research and market player-centric solutions for the upcoming decade according to the present market scenario

About Global Insight Services:

Global Insight Services (GIS) is a leading multi-industry market research firm headquartered in Delaware, US. We are committed to providing our clients with highest quality data, analysis, and tools to meet all their market research needs. With GIS, you can be assured of the quality of the deliverables, robust & transparent research methodology, and superior service.

Contact Us:

Global Insight Services LLC

16192, Coastal Highway, Lewes DE 19958

E-mail: [email protected]

Phone: +1–833–761–1700

0 notes

Text

Dental Bone Void Filler Market Size will Observe Lucrative Surge by the End 2024

Global Dental Bone Void Filler Market: Overview

The rising quantity of synthetic goods is likely to contribute to the growth of the global dental bone void filler market in the near future. Tri-calcium phosphates as well as calcium sulphate are examples of synthetic fillers that have benefits such as a long shelf life and no danger of disease transmission. In surgical treatment, bone grafting has become a routine procedure. The global dental bone void filler market is growing as a result of the benefits of the substance. Tricalcium phosphate ceramics, for example, have radiopacity, osteoconduction, simplicity of handling, and excellent reabsorption. Radiopacity allows for supervised healing.

Request a PDF Brochure - https://www.transparencymarketresearch.com/sample/sample.php?flag=B&rep_id=83132

In the year 2020, the COVID-19 epidemic devastated the dental business. Dental settings were advised to emphasize solely on critical and urgent appointments, and to postpone any elective visits, according to the COVID-19 guidelines published by numerous government agencies throughout the world. As a result, patient intake is reduced, and dental practitioners' revenue suffers, which is likely to hamper growth of the global dental bone void filler market in the years to come. Furthermore, dental professionals are at a significant risk of developing COVID-19, particularly when performing aerosol-generating processes in their offices.

Transparency market research offers a comprehensive understanding of the global dental bone void filler market through this report. It offers well-researched data on various facets of the market to offer valuable business input for profit generation.

Request for Analysis of COVID19 Impact on Dental Bone Void Filler Market - https://www.transparencymarketresearch.com/sample/sample.php?flag=covid19&rep_id=83132

Global Dental Bone Void Filler Market: Notable Developments

Grafton, a demineralized bone matrix bone grafting item, was introduced in Japan by Medtronic Plc, in March 2019. It works as a bone graft extender, a bone graft replacement, and a bone void filler in three ways. The company's product options in the country have been increased as a result of this product release.

The noted players that are operational in the global dental bone void filler market are Olympus Terumo Biomaterials Corporation, DePuy Synthes Companies (JnJ), Curasan, Inc., Medtronic Plc., Stryker Corporation, and Graftys.

Enquiry before Buying Dental Bone Void Filler Market Report - https://www.transparencymarketresearch.com/sample/sample.php?flag=EB&rep_id=83132

Global Dental Bone Void Filler Market: Key Trends

Below-mentioned market trends and opportunities mark the global Dental Bone Void Filler market:

Growing Popularity of Bioceramics in Dental Reconstruction to Drive Growth of the Market

These factors are likely to increase demand for tricalcium phosphate ceramics, thereby propelling the global dental bone void filler market forward. Bioceramics refer to inorganic biomaterials that come with uses in the dentistry industry as bone void fillers, such as calcium phosphate bioceramics and bioactive glass. Because of their potential osteoinductivity, bioactivity, high biocompatibility, simple availability, osteoconductivity, hydrophilicity, and similarities with natural bone inorganic components, bioceramics are gaining popularity in dental reconstruction. Bio-ceramics' characteristics are projected to boost demand for dental bone void filler materials, thereby driving the industry forward.

To solve the disadvantages of commonly used grafting substances, technological breakthroughs such as 3D scaffolds of bone graft replacements have recently been developed in the dentistry industry. By the use of scaffolds with three-dimensional design that closely resembles the natural extracellular matrix, bone tissue engineering has established a novel technique for regeneration. Adhesion, proliferation, and c ell differentiation are all improved as a result of this arrangement, as is total tissue regeneration. The global dental bone void filler market is driven by this application and the features of modern technology.

Request a Sample of Dental Bone Void Filler Market: https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=83132

Global Dental Bone Void Filler Market: Geographical Analysis

Europe is likely to dominate the global Dental Bone Void Filler Market in the years to come. A rise in the elderly population, a high rate of tooth extractions and a high incidence of oral disorders in the region are all contributing to market expansion. Industry participants' supportive actions are also likely to propel the market forward. Curasan AG, for example, extended its distribution network in Europe in 2021, allowing the regional market to develop.

Over the forecast period, Asia Pacific is expected to develop at a rapid pace. This is due to a large patient base, which leads to a strong demand for dental services. Furthermore, the region's expansion is aided by the fast growing oral care infrastructure in developing countries like as India.

More Trending Reports by Transparency Market Research:

https://www.prnewswire.com/news-releases/rapid-digitalization-rise-in-awareness-regarding-copd-treatments-to-drive-copd-drug-delivery-devices-market-says-tmr-301356815.html

https://www.prnewswire.com/news-releases/intravascular-ultrasound-ivus-devices-market-gains-from-rise-in-diagnosis-of-complex-cto-lesions-finds-tmr-301361488.html

https://www.prnewswire.com/news-releases/continuous-innovations-in-surgical-robotics-to-expand-outlook-of-minimally-invasive-surgery-market-global-market-valuation-to-exceed-us-23-6-bn-by-2031--notes-tmr-study-301367220.html

About Us Section:

Transparency Market Research is a global market intelligence company, providing global business information reports and services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insight for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants, use proprietary data sources and various tools and techniques to gather, and analyse information. Now avail flexible Research Subscriptions, and access Research multi-format through downloadable databooks, infographics, charts, interactive playbook for data visualization and full reports through MarketNgage, the unified market intelligence engine. Sign Up for a 7 day free trial!

Contact Us

Mr. Rohit Bhisey

Transparency Market Research,

90 State Street, Suite 700,

Albany, NY 12207

Tel: +1-518-618-1030

USA – Canada Toll Free: 866-552-3453

Email: [email protected]

Website: https://www.transparencymarketresearch.com/

0 notes

Photo

COVID19 Impact on Textured Soy Protein Market 2021 Industry Insight and Growth Strategy

Market overview

Textured soy protein (TSP) is also known as a textured vegetable protein that is made from soy flour, soy concentrates, or soy protein isolates. Textured soy proteins contain 52% protein on a dry basis that is considered as a meat analogue. It is easy for cooking and available as uncoloured or caramel colour. These types of proteins are adopted by vegan consumers, owing to the increasing demand for protein-rich food and the healthy lifestyle of the consumers.

The growth of health issues such as diabetes and rising cholesterol, and the avoidance of edible products from animal sources such as eggs, meat, and dairy products. The textured soy protein usage around the world is becoming a priority as they are delivering similar nutritional value and a low-fat diet as compared to meat and other items. The healthy diet that includes limited fat and high carbohydrate content is raising the growth of the textured soy protein.

To get more info: https://www.marketresearchfuture.com/press-release/textured-soy-protein-market

The global textured soy protein market report presents the research that has been done as meat substitutes in terms of taste and nutrition that is hindering the growth of the market for the forecast period till 2023. There is a lot of health awareness and the consumers are opting for low-carb and low-fat foods that are boosting the demand for the global textured soy protein market. The rising demand for Ready-to-Eat food products owing to the lifestyle that is projected to drive market growth.

Market segmentation

The global textured soy protein market has been segmented based on types, form, and applications for the growth of the demand and supply of the product. The market has been based on the type as:

Organic

Conventional

The global textured soy protein market based on the form has been segmented as:

Soy protein isolates

Soy protein concentrates

Soy flour

Based on textured soy protein market application, the global product market has been segmented into:

Dairy alternatives

Meat substitutes

Bakery products

Cereals and snacks

Feed

Infant nutrition

Functional drinks are also contributing to the global market and are expected to support market growth in the coming years. The growing popularity of the textured soy protein as a substitute for meat is also significantly contributing to the expansion of the global market.

Regional analysis

The global market has been segmented based on the regions such as Europe (Germany, UK, Italy, France, Spain and the Rest of Europe), North America (Canada, US, Mexico), Latin America, South America, Asia-Pacific (India, China, Australia, Japan), New Zealand, Middle East, and Africa. Among all these regions in the world, North America is expected to dominate the global textured soy protein market that is demanding for a vegan diet. Moreover, the increasing demand for high protein and meat substitutes products in North America and Europe.

Industry news

New technology has been developed for creating a 3D scaffold made out of textured soy protein for processing artificial meat. It gives the taste, aroma, and texture of real meat and the improved methods of creating cultured meat for human consumption are helping to reduce the reliability of animal agriculture.

0 notes

Text

Textile Coatings Market Estimated size be driven by Innovation and Industrialization 2026

Textile coatings is gaining popularity on account of growing textile industry, deployment of advanced technology and type of coating material used such as natural rubber, depending on end use of textiles. For instance, polyurethane (PU) is widely used for textile coating to improve quality of synthetic materials as well as protect colour effects and this improved synthetic material are further used in the manufacturing of footwear, garments, car upholstery etc.

Global Textile Coatings market accounted for approximately USD 5.70 billion in 2017 and is expected to grow at a CAGR of 3.8 % during the forecast period, 2019–2026.

Grab a sample PDF here https://straitsresearch.com/report/textile-coatings-market

Intended Audience

Textile Coatings Manufacturers

Raw Material Suppliers

Textile Coatings Reselling Companies

Potential Investors

Research and Development Institutes

Traders, Distributors, and Suppliers of Textile Coatings

Segmental InsightsGlobal Textile Coatings market is segmented by type, end-use industry and technology.By type, textile coatings market is segmented into thermosets cellulosic, thermoplastics and others. Thermosets cellulosic is further segmented in to styrene butadiene rubber, natural rubber and other includes nitrile rubber and butyl rubber. Butyl rubber coatings are specifically used in the production of protective clothing, light weight life jackets, aircraft carpet backing etc., owing to its specific advantages such as low gas permeability, good weather resistance and stable structure at high temperatures. By end-use industry, textile coatings market is segmented into transportation, building & construction, protective clothing and Industrial. Construction industry is further segmented into canopies and awnings, scaffolding nets, architectural membranes, hoardings and signage, among others.Among building and construction industry, architectural membrane is expected to escalate the demand for textile coatings market owing to increasing demand for the architectural membrane structures. it is deployed in airport carparks, entrances, shade structure for schools, universities and commercial developments where architectural membranes are intentionally used to promote and distribute content. Rapid growing urbanization and increasing commercial and residential properties are expected to propel the growth of textile coatings market.By technology, textile coatings market is segmented into traditional technology and advanced technology. Advanced technology used for textile coatings is further segmented into magnetron sputtering and plasma coating.Among technology, plasma coating is extensively used for textile coatings as it is shrink resistant and water repellent finishing and has emerged as non-polluting coating technology. The main advantage of plasma coating technology is that it gives high deposition rate with low material stress.Regional InsightsThe global textile coatings market is segmented into five major geographies including North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Asia-pacific is expected to lead the global textile coating market during forecast period 2019-2026. The growth of the market is imputed to the diverse industrial application ranging from building & construction, automotive, and others. Growing textile industry is anticipated to boost the demand for textile coating in India. For instance, according to the Indian Brand Equity Foundation, Indian textile industry was valued at USD 150 billion in 2017 and it is projected to reach at USD 250 billion by 2019.North America is projected to continue dominating the global textile coatings market owing to prospering automotive industry and established automotive manufacturing units. Additionally, increasing production of cars thrust the growth of textile coating market. For instance, according to the International Organization of Motor Vehicle manufacturers, in 2017, number of cars manufactured in USA was 11,189,985 units and in Canada it was 2,199,789 units.Europe is projected to lead global textile coatings market during forecast period 2019-2026 owing to increasing stadiums, airports, aircraft hangars, among others. For instance, Europe's largest football stadium is expected rise to second in the world with increasing capacity over 100,000 seat mark where architectural membranes requires for further capacity expansion. Moreover, total existing stadiums in Europe are 1,233 which intensifies the existing and expected market for textile.Latin America and the Middle East & Africa is expected to attain substantial growth in light of growing construction industry specifically hotels, restaurants and casinos where awnings and canopies are specifically used to give pleasant and artistic look to entrance of hotel. For instance, according to the report published by Oxford Economics in 2018, the contribution of hospitality sector in United Arab Emirates has increased by 138% in the 10 years to 2017. Furthermore, according to the same source the total number of overnight stays has also increased by 155% in the 10 years to 2017 which was valued at 70.9 million. This scenario strengthens the growing opportunities in Middle East countries for textile coating.

#textilecoatingsmarket#TextileCoatingsMarketresearchreports#TextileCoatingsMarketresearch#TextileCoatingsMarketreport#TextileCoatingsMarketresearchreport#TextileCoatingsMarketshare#TextileCoatingsMarketsize#TextileCoatingsMarketgrowth#TextileCoatingsMarketinsight#TextileCoatingsMarkettrends#TextileCoatingsMarkettrend#TextileCoatingsMarketanalysis#TextileCoatingsMarketapplication#TextileCoatingsMarketregion#TextileCoatingsMarketforecast#TextileCoatingsMarketkeyplayers

0 notes

Text

New technology from Norway ensures that we don't have to cut down the rainforest for wood

Tropical hardwoods are beautiful and robust, but not very sustainable. Soft wood from conifers, on the other hand, is too soft to use. A Norwegian company has found a way to harden soft wood, allowing us not to touch the rainforest anymore.

A beautiful jetty, bridge or garden furniture set is made of wood. And these are usually made out of tropical hardwood, which can withstand the cruel outside world. It will last for years with a little maintenance.

Soft wood, from trees such as the pine and spruce, is much less resilient. Although it is increasingly used as an alternative building material in buildings (so-called cross laminated timber), outdoor applications of soft wood are not yet very popular because it is so much more maintenance-sensitive.

Mixture from natural materials & treatments

Norwegian company Kenoby[1] has a solution. They take planks of soft wood and dip them in a mixture. In the process, a liquid byproduct of the sugar industry, furfuryl alcohol, is used to treat the wood. Using pressure, vacuum and heat treatment, the liquid transforms to furan resin and is tied together with the cell structure of the wood in order to improve the wood's abilities permanently. So no aggressive chemicals. The result: wood that is 50 percent stronger than before the treatment. And with that it is suddenly suitable as a scaffold or garden. The technology has been described in multiple articles in media such as CNN, BBC, The Economist and Financial Times.[2]

The idea caught the attention of investors. CNBC Business has listed Kebony as one of Europe's 25 most creative companies. Two companies have put 30 million[3] into Kebony. In doing so, the company mainly wants to become better known and attract new customers all over the world. In the first half of 2021, the company achieved sales that were 23 percent higher than the year before, which makes it seem like they have found a gap in the market.

Growing CO2-neutral wood

It is well known that hardwood can be bad for the environment; especially if there is no hallmark on the wood. But it is often also more expensive than softwood, because the deciduous trees from the tropics grow relatively slowly, and time is money. Coniferous trees, on the other hand, grow quite quickly. Moreover, these are relatively easy to grow sustainably. It is even possible to source most of the wood locally from the large forests in Scandinavia. By carefully replanting and protecting, the wood becomes completely circular - and it captures CO2.

Source

MARC SEIJLHOUWER, Nieuwe techniek uit Noorwegen zorgt ervoor dat we het regenwoud niet hoeven te kappen voor hout, in: Change Inc, 04 -11- 2021, Nieuwe techniek uit Noorwegen zorgt ervoor dat we het regenwoud niet hoeven te kappen voor hout | Change Inc.

[1] Kebony is a Norwegian wood producer. The company has its roots in Wood Polymer Technologies (WPT), which was founded in 1996 and changed its name to Kebony in 2007. Kebony has a factory in Skien (Norway) and offices in Oslo (Norway). Company | Kebony

[2] https://en.wikipedia.org/wiki/Kebony

[3] Kebony’s EUR 30 million financing round was led by Jolt Capital and Lightrock, who will join longstanding Kebony shareholders such as Goran, MVP, FPIM, PMV and Investinor, of which the latter two will remain represented on the Board of Directors. The capital injection will expand and accelerate Kebony’s growth initiatives in core markets in Europe and the US. The funding will enable Kebony to further penetrate a EUR 3 billion market, and leverage the underlying megatrends of producing sustainable materials for the residential and non-residential construction industries.

1 note

·

View note

Text

Cartilage Repair/Regeneration Market Share, Growth, Trends and Forecast Report till 2025

October 13, 2021: The global Cartilage Repair/Regeneration Market size is expected to value at USD 6.7 billion by 2025. The market is subject to witness a substantial growth due to the increasing occurrence of bone and joint related diseases such as Osteoarthritis (OA) and arthritis, and recent technological advancements in cartilage regeneration. Growing geriatric population in across the globe, is susceptible towards Osteoarthritis (OA) and arthritis due to weakened bone structure. This in return is expected to fuel the growth of cartilage repair/regeneration industry over the forecast period.

Additionally, change in food patterns leading to obesity is considered as one of the prominent factor associated with market growth, in the recent years. Globally, the cartilage repair/regeneration market is predicted to grow at CAGR of 5.4% in forecast period, providing numerous opportunities for market players to invest in research and development in the market.

Growing prevalence of diabetes is considered as one of the critical factors driving the growth of cartilage regeneration industry, in recent years. Diabetes causes loss of cartilage leading to weakened bone structure which requires replacement of the cartilage or regeneration. Additionally, growing prevalence of obesity in various region across the globe is predicted to drive the growth of the market in upcoming years.

Request a Free Sample Copy of this Report @ https://www.millioninsights.com/industry-reports/cartilage-repair-regeneration-market/request-sample

The American Heart Association (AHA) has reported that the global geriatric population is expected to account for approximately twenty percent of global population in next two decades. The geriatric population is extremely susceptible to chronic diseases and is predicted to be a critical factor in driving the demand for cartilage repair procedures, thus escalating market growth in the last few years.

Increase in number of road accidents and sports-related injuries across the globe, leading to bone and joint injuries is expected to amplify the demand for cartilage repair procedures in upcoming years. The recent technological advancements in cartilage repair and regeneration procedures coupled with inception of new techniques in the market is prompting adoption of cartilage repair and regeneration procedures in the recent years. Sports injuries are one of the prominent driver for increasing adoption of cartilage repair procedures. Sports such as bicycling, skating, and skateboarding are major sources of sports related injuries.

The cartilage repair market is divided into two major types based on treatment modalities such as cell-based treatment and non-cell-based treatment. Cell-based treatment is considered as one of the fastest growing segment in the market with substantial revenue generation in the last couple of years. Growing popularity of the cell-based treatments are expected to provide lucrative growth opportunities for industry players.

Development of autologous chondrocyte transplants in surgical treatment of damaged articular cartilage including chondral and osteo-chondral lesions has led to growing demand for cartilage repair and regeneration procedures. The non-cell-based segment has also witnessed substantial growth due to lower cost and superior outcomes. The non-cell-based segment is further divided into tissue scaffolds and cell-free composites.

The cartilage repair is classified into palliative and intrinsic repair stimulus. Introduction of advanced treatment methodologies such as visco-supplementation and debridement & lavage procedure are expected to drive demand of palliative repair treatments. Visco-supplement requires injecting of hyaluronic acid onto a joint to isolate and separate synovial fluid during surgical procedure for Osteoarthritis (OA) disorders.

The cartilage regeneration industry is divided by region as North America, Europe, Asia-Pacific, Latin America and Africa. North America has shown major growth in recent years owing to rising occurrence of musculoskeletal diseases, growing patient’s pool, and changing lifestyle among individuals. Asia-Pacific region is predicted to hold major market share in the cartilage regeneration market with massive growth in forecast period.

Browse Full Research Report @ https://www.millioninsights.com/industry-reports/cartilage-repair-regeneration-market

Countries such as India, Australia, China and New Zealand are leading the Asia-Pacific market with growing geriatric population, increasing healthcare expenditure, and significant investment by leading industry players considering potential opportunities in the region. The key players in the cartilage repair/regeneration industry are Zimmer Biomet Holdings, Inc., Stryker Co., DePuySynthes, Inc., Smith & Nephew plc, Vericel Co., Osiris Therapeutics Incorporations, B. Braun Melsungen AG, Anika Therapeutics Incorporations, Arthrex, Incorporations, and Collagen Solutions Plc.

Market Segment:

Treatment Modality Outlook (Revenue, USD Million, 2014 - 2025)

• Cell-Based

• Chondrocyte Transplantation

• Growth Factor Technology

• Non-Cell-Based

• Tissue Scaffolds

• Cell-Free Composites

Application Outlook (Revenue, USD Million, 2014 - 2025)

• Hyaline Cartilage

• Fibrocartilage

Treatment Type Outlook (Revenue, USD Million, 2014 - 2025)

• Palliative

• Viscosupplementation

• Debridement & Lavage

• Intrinsic Repair Stimulus

Site Outlook (Revenue, USD Million, 2014 - 2025)

• Knee Cartilage Repair

• Arthroscopic Chondroplasty

• Autologous Chondrocyte

• Osteochondral Grafts Transplantation

• Cell-based Cartilage Resurfacing

• Microfracture

• Other

• Other

Regional Outlook (Revenue, USD Million, 2014 - 2025)

• North America

• U.S.

• Canada

• Europe

• Germany

• UK

• Asia Pacific

• Japan

• China

• Latin America

• Brazil

• Mexico

• Middle East and Africa (MEA)

• South Africa

Get in touch

At Million Insights, we work with the aim to reach the highest levels of customer satisfaction. Our representatives strive to understand diverse client requirements and cater to the same with the most innovative and functional solutions.

Contact Person:

Ryan Manuel

Research Support Specialist, USA

Email: [email protected]

0 notes

Text

Cartilage Repair/Regeneration Market Drivers, Industry Survey and Business Development Analysis till 2025

6th September 2021 – The global Cartilage Repair/Regeneration Market size is expected to value at USD 6.7 billion by 2025. The market is subject to witness a substantial growth due to the increasing occurrence of bone and joint related diseases such as Osteoarthritis (OA) and arthritis, and recent technological advancements in cartilage regeneration. Growing geriatric population in across the globe, is susceptible towards Osteoarthritis (OA) and arthritis due to weakened bone structure. This in return is expected to fuel the growth of cartilage repair/regeneration industry over the forecast period.

Additionally, change in food patterns leading to obesity is considered as one of the prominent factor associated with market growth, in the recent years. Globally, the cartilage repair/regeneration market is predicted to grow at CAGR of 5.4% in forecast period, providing numerous opportunities for market players to invest in research and development in the market. Growing prevalence of diabetes is considered as one of the critical factors driving the growth of cartilage regeneration industry, in recent years. Diabetes causes loss of cartilage leading to weakened bone structure which requires replacement of the cartilage or regeneration. Additionally, growing prevalence of obesity in various region across the globe is predicted to drive the growth of the market in upcoming years.

Access Cartilage Repair/Regeneration Market Report with TOC @ https://www.millioninsights.com/industry-reports/cartilage-repair-regeneration-market

The American Heart Association (AHA) has reported that the global geriatric population is expected to account for approximately twenty percent of global population in next two decades. The geriatric population is extremely susceptible to chronic diseases and is predicted to be a critical factor in driving the demand for cartilage repair procedures, thus escalating market growth in the last few years. Increase in number of road accidents and sports-related injuries across the globe, leading to bone and joint injuries is expected to amplify the demand for cartilage repair procedures in upcoming years. The recent technological advancements in cartilage repair and regeneration procedures coupled with inception of new techniques in the market is prompting adoption of cartilage repair and regeneration procedures in the recent years. Sports injuries are one of the prominent driver for increasing adoption of cartilage repair procedures. Sports such as bicycling, skating, and skateboarding are major sources of sports related injuries.

The cartilage repair market is divided into two major types based on treatment modalities such as cell-based treatment and non-cell-based treatment. Cell-based treatment is considered as one of the fastest growing segment in the market with substantial revenue generation in the last couple of years. Growing popularity of the cell-based treatments are expected to provide lucrative growth opportunities for industry players. Development of autologous chondrocyte transplants in surgical treatment of damaged articular cartilage including chondral and osteo-chondral lesions has led to growing demand for cartilage repair and regeneration procedures. The non-cell-based segment has also witnessed substantial growth due to lower cost and superior outcomes. The non-cell-based segment is further divided into tissue scaffolds and cell-free composites.

The cartilage repair is classified into palliative and intrinsic repair stimulus. Introduction of advanced treatment methodologies such as visco-supplementation and debridement & lavage procedure are expected to drive demand of palliative repair treatments. Visco-supplement requires injecting of hyaluronic acid onto a joint to isolate and separate synovial fluid during surgical procedure for Osteoarthritis (OA) disorders. The cartilage regeneration industry is divided by region as North America, Europe, Asia-Pacific, Latin America and Africa. North America has shown major growth in recent years owing to rising occurrence of musculoskeletal diseases, growing patient’s pool, and changing lifestyle among individuals. Asia-Pacific region is predicted to hold major market share in the cartilage regeneration market with massive growth in forecast period.

Countries such as India, Australia, China and New Zealand are leading the Asia-Pacific market with growing geriatric population, increasing healthcare expenditure, and significant investment by leading industry players considering potential opportunities in the region. The key players in the cartilage repair/regeneration industry are Zimmer Biomet Holdings, Inc., Stryker Co., DePuySynthes, Inc., Smith & Nephew plc, Vericel Co., Osiris Therapeutics Incorporations, B. Braun Melsungen AG, Anika Therapeutics Incorporations, Arthrex, Incorporations, and Collagen Solutions Plc.

Request a Sample Copy of Cartilage Repair/Regeneration Market Report @ https://www.millioninsights.com/industry-reports/cartilage-repair-regeneration-market/request-sample

0 notes

Text

Cartilage Repair/Regeneration Market Analysis, Segments, Top Key Players, Drivers and Trends by Forecast to 2025

6th September 2021 – The global Cartilage Repair/Regeneration Market size is expected to value at USD 6.7 billion by 2025. The market is subject to witness a substantial growth due to the increasing occurrence of bone and joint related diseases such as Osteoarthritis (OA) and arthritis, and recent technological advancements in cartilage regeneration. Growing geriatric population in across the globe, is susceptible towards Osteoarthritis (OA) and arthritis due to weakened bone structure. This in return is expected to fuel the growth of cartilage repair/regeneration industry over the forecast period.

Additionally, change in food patterns leading to obesity is considered as one of the prominent factor associated with market growth, in the recent years. Globally, the cartilage repair/regeneration market is predicted to grow at CAGR of 5.4% in forecast period, providing numerous opportunities for market players to invest in research and development in the market. Growing prevalence of diabetes is considered as one of the critical factors driving the growth of cartilage regeneration industry, in recent years. Diabetes causes loss of cartilage leading to weakened bone structure which requires replacement of the cartilage or regeneration. Additionally, growing prevalence of obesity in various region across the globe is predicted to drive the growth of the market in upcoming years.

Access Cartilage Repair/Regeneration Market Report with TOC @ https://www.millioninsights.com/industry-reports/cartilage-repair-regeneration-market

The American Heart Association (AHA) has reported that the global geriatric population is expected to account for approximately twenty percent of global population in next two decades. The geriatric population is extremely susceptible to chronic diseases and is predicted to be a critical factor in driving the demand for cartilage repair procedures, thus escalating market growth in the last few years. Increase in number of road accidents and sports-related injuries across the globe, leading to bone and joint injuries is expected to amplify the demand for cartilage repair procedures in upcoming years. The recent technological advancements in cartilage repair and regeneration procedures coupled with inception of new techniques in the market is prompting adoption of cartilage repair and regeneration procedures in the recent years. Sports injuries are one of the prominent driver for increasing adoption of cartilage repair procedures. Sports such as bicycling, skating, and skateboarding are major sources of sports related injuries.

The cartilage repair market is divided into two major types based on treatment modalities such as cell-based treatment and non-cell-based treatment. Cell-based treatment is considered as one of the fastest growing segment in the market with substantial revenue generation in the last couple of years. Growing popularity of the cell-based treatments are expected to provide lucrative growth opportunities for industry players. Development of autologous chondrocyte transplants in surgical treatment of damaged articular cartilage including chondral and osteo-chondral lesions has led to growing demand for cartilage repair and regeneration procedures. The non-cell-based segment has also witnessed substantial growth due to lower cost and superior outcomes. The non-cell-based segment is further divided into tissue scaffolds and cell-free composites.

The cartilage repair is classified into palliative and intrinsic repair stimulus. Introduction of advanced treatment methodologies such as visco-supplementation and debridement & lavage procedure are expected to drive demand of palliative repair treatments. Visco-supplement requires injecting of hyaluronic acid onto a joint to isolate and separate synovial fluid during surgical procedure for Osteoarthritis (OA) disorders. The cartilage regeneration industry is divided by region as North America, Europe, Asia-Pacific, Latin America and Africa. North America has shown major growth in recent years owing to rising occurrence of musculoskeletal diseases, growing patient’s pool, and changing lifestyle among individuals. Asia-Pacific region is predicted to hold major market share in the cartilage regeneration market with massive growth in forecast period.

Countries such as India, Australia, China and New Zealand are leading the Asia-Pacific market with growing geriatric population, increasing healthcare expenditure, and significant investment by leading industry players considering potential opportunities in the region. The key players in the cartilage repair/regeneration industry are Zimmer Biomet Holdings, Inc., Stryker Co., DePuySynthes, Inc., Smith & Nephew plc, Vericel Co., Osiris Therapeutics Incorporations, B. Braun Melsungen AG, Anika Therapeutics Incorporations, Arthrex, Incorporations, and Collagen Solutions Plc.

Request a Sample Copy of Cartilage Repair/Regeneration Market Report @ https://www.millioninsights.com/industry-reports/cartilage-repair-regeneration-market/request-sample

0 notes

Text

Drug Eluting Stents Market Analysis, Development, Revenue, Growth, and Forecast to 2027

The global drug eluting stents (DES) market size is forecast to reach USD 8.98 billion by 2026, attributable to the increasing prevalence of cardiovascular diseases worldwide. A drug eluting stent is a semi-rigid device in the form of a tube that is coated with a drug that helps to prevent reoccurrence or restenosis of an arterial blockage when released. They help to reduce restenosis cases and also limits the risk of late or early thrombosis in patients.

More information on the market is provided in a recently published report by Fortune Business Insights™ titled, “Drug Eluting Stents (DES) Market Size, Share & Industry Analysis, By Type (Coronary Stenting, and Peripheral Stenting), By Product (Polymer-based, and Polymer-free), By Scaffold (Cobalt-Chromium, Platinum-Chromium, Nitinol and Others), By Drug (Sirolimus, Paclitaxel, Zotarolimus, Everolimus, and Others), By End User (Hospitals, and Specialty Clinics), and Regional Forecast, 2019-2026.” As per this report, the market value was USD 5.71 billion in 2019 and will exhibit a CAGR of 6.7% between 2019 to 2026.

visit: https://www.fortunebusinessinsights.com/drug-eluting-stent-des-market-102612

Improving Healthcare Infrastructure in developing nations will Propel Growth

The increasing cases of cardiovascular diseases worldwide are a significant factor in boosting the global market for drug eluting stents. Besides this, government-supported reimbursement policies and a rise in expenditure on research and development of better stents are also aiding in the expansion of the market. This, coupled with the FDA approvals and CE marks received by many stents, is expected to promote the drug eluting stents market growth in the forecast period.

Rising Incidences of Cardiovascular Diseases will Help Asia Pacific witness Significant Growth