#Telecom Operations Management Market Size

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Premium Tumblr themes are available from anywhere between $9 to $49.

Text

#Telecom Operations Management Market#Telecom Operations Management Market Share#Telecom Operations Management Market Size#Telecom Operations Management Market Research#Telecom Operations Management Industry#What is Telecom Operations Management?

0 notes

Text

MPLS IP VPN Market Size, Share, Forecasted Growth, and Analysis to 2032

The MPLS IP VPN Market was valued at USD 60.69 billion in 2023 and is expected to reach USD 110.92 billion by 2032, growing at a CAGR of 6.99% from 2024-2032.

The MPLS IP VPN (Multiprotocol Label Switching Internet Protocol Virtual Private Network) market continues to gain traction as businesses across industries demand high-performance, scalable, and secure communication infrastructure. These solutions are widely adopted due to their ability to deliver seamless connectivity across geographically dispersed locations with superior data privacy and QoS (Quality of Service). Enterprises, government institutions, and service providers are shifting from legacy systems to MPLS IP VPNs for enhanced operational efficiency and reduced latency.

Multiprotocol Label Switching Internet Protocol Virtual Private Network solutions VPN Market are increasingly becoming the backbone of enterprise networking strategies. The market's upward trajectory is largely attributed to digital transformation, cloud adoption, and the need for secure, high-bandwidth communication channels. Vendors are investing in technology upgrades and service customization to meet the dynamic needs of modern enterprises. This evolution is fostering a competitive yet innovation-driven landscape.

Get Sample Copy of This Report: https://www.snsinsider.com/sample-request/5976

Market Keyplayers:

AT&T Inc. (AT&T VPN, AT&T NetBond)

British Group plc (BT IP VPN, BT Net Protect)

Lumen Technologies (Lumen MPLS VPN, Lumen Cloud Connect)

Cisco Systems, Inc. (Cisco SD-WAN, Cisco MPLS VPN)

GCX (GCX Global MPLS VPN, GCX IP Connect)

Reliance Globalcom Services Inc. (Reliance MPLS VPN, Reliance Cloud Connect)

Telefonica Group (Telefonica MPLS VPN, Telefonica SD-WAN)

Telstra Corporation (Telstra Global MPLS, Telstra VPN Services)

T‑Mobile USA, Inc. (T-Mobile MPLS VPN, T-Mobile SD-WAN)

Verizon Communications Inc. (Verizon MPLS VPN, Verizon SD-WAN)

Orange Business Services (Orange MPLS VPN, Orange SD-WAN)

CenturyLink (CenturyLink MPLS VPN, CenturyLink SD-WAN)

Sprint Nextel Corporation (Sprint MPLS VPN, Sprint Cloud Connect)

Charter Communications (Charter Enterprise VPN, Charter Cloud Solutions)

Vodafone (Vodafone MPLS VPN, Vodafone SD-WAN)

China Telecom (China Telecom VPN, China Telecom Cloud Connect)

China Unicom (China Unicom IP VPN, China Unicom SD-WAN)

WINDTRE (WINDTRE VPN, WINDTRE MPLS)

Comcast (Comcast Enterprise VPN, Comcast Cloud Solutions)

Deutsche Telekom (Deutsche Telekom MPLS VPN, Deutsche Telekom SD-WAN)

Market Analysis The MPLS IP VPN market is witnessing significant evolution due to the convergence of advanced networking technologies, the rise in remote workforces, and increasing security concerns. Organizations are prioritizing robust virtual networks to support hybrid cloud environments and IoT applications. This has led to a surge in demand for flexible, reliable, and cost-effective VPN services. Additionally, telecom operators are launching managed services to offer tailored VPN solutions, enhancing customer experience and retention.

Market Trends

Growing adoption of hybrid MPLS-VPN and SD-WAN solutions

Increased focus on network security and regulatory compliance

Rising demand from SMEs for affordable managed VPN services

Integration of AI and automation in VPN traffic management

Surge in VPN adoption across healthcare, finance, and retail sectors

Market Scope

Global Reach: Expansion of MPLS IP VPN services into emerging markets across APAC, Latin America, and Africa

Enterprise-Driven Growth: High uptake among large enterprises and government institutions

Versatile Applications: Ideal for supporting voice, video, and data applications across secure networks

Cloud Integration: Seamless compatibility with public and private cloud services

Carrier-Grade Services: Reliable QoS features ensuring consistent network performance

The market scope is characterized by its adaptability to diverse industry demands and its alignment with digital infrastructure growth. Service providers are leveraging these features to offer industry-specific solutions, enhancing user experience and service delivery.

Market Forecast The MPLS IP VPN market is set to grow steadily as businesses increasingly seek scalable and secure networking frameworks. The continued emphasis on digital agility and enterprise mobility will act as key catalysts. Strategic collaborations, technology convergence, and tailored service models will play a pivotal role in shaping the future of the market. As next-generation networks evolve, MPLS IP VPNs will remain essential in bridging legacy systems with modern IT ecosystems, ensuring continuity, security, and speed.

Access Complete Report: https://www.snsinsider.com/reports/mpls-ip-vpn-market-5976

Conclusion The MPLS IP VPN market stands at a transformative juncture, where innovation meets necessity. As organizations evolve in the digital era, their reliance on secure and high-performing virtual networks will only intensify. The market promises not just connectivity but a strategic enabler of growth, agility, and resilience. Forward-thinking enterprises and providers that embrace this shift are poised to lead in a hyper-connected world.

About Us:

SNS Insider is one of the leading market research and consulting agencies that dominates the market research industry globally. Our company's aim is to give clients the knowledge they require in order to function in changing circumstances. In order to give you current, accurate market data, consumer insights, and opinions so that you can make decisions with confidence, we employ a variety of techniques, including surveys, video talks, and focus groups around the world.

Contact Us:

Jagney Dave - Vice President of Client Engagement

Phone: +1-315 636 4242 (US) | +44- 20 3290 5010 (UK)

0 notes

Text

ASX 300 Index Sector Breakdown and Market Representation

Highlights

Covers a wide spectrum of listed entities on the Australian Securities Exchange

Features extensive participation from financials, energy, healthcare, industrial, and tech-related businesses

Rebalanced regularly to incorporate updated size and trading activity data

The ASX 300 Index reflects the equity landscape across a diverse array of industries in Australia. A large portion of the index consists of financial firms, including leading banks, insurers, and multi-service finance companies. These participants typically possess significant market capitalisation and play a key role in shaping the sector distribution within the index. Their size and liquidity often secure their inclusion in periodic index reviews.

Resources Segment Contribution

Energy and mining operations are well-represented within the ASX 300 Index, highlighting the sector’s role in Australia’s export-driven economy. Entities engaged in the extraction and supply of resources such as iron ore, natural gas, and coal are commonly found in the index. Their market movements often correlate with fluctuations in global commodity pricing and sector-specific developments.

Healthcare Industry Inclusion

Medical and life sciences companies make up another critical portion of the index. The healthcare component includes biotechnology innovators, pharmaceutical producers, medical equipment suppliers, and private healthcare operators. Several listed firms in this group have operations beyond Australia, providing further diversity in revenue streams and market exposure within the index.

Industrials Sector Composition

Firms involved in infrastructure delivery, engineering, transport logistics, and manufacturing are included under the industrials segment of the ASX 300 Index. These organisations are selected based on their relative size and market activity, and many offer both local and global services. Their presence provides broader visibility into sectors linked to construction and transportation.

Technology-Driven Companies

The index also features companies in software, fintech, cloud services, and digital infrastructure. These entities exemplify Australia’s growing presence in the tech sector and are part of the shift toward digital solutions in business and consumer markets. Their inclusion reflects technological innovation and emerging sector participation.

Consumer-Focused Enterprises

Retail and consumer product businesses—ranging from food producers and supermarkets to fashion retailers—are part of the index’s composition. These companies are sensitive to consumer confidence and expenditure levels, and their weighting within the index may vary with shifts in market demand and seasonal performance.

Essential Services and Utilities

Companies supplying power, water, and gas—alongside those maintaining public infrastructure—form the utilities component of the ASX 300 Index. These entities often operate under regulatory frameworks or long-term agreements and serve as a measure of essential service activity and urban expansion across regions.

Real Estate and Property Holdings

Entities managing real estate portfolios, including office towers, industrial parks, and residential complexes, contribute to the property segment of the index. This includes Real Estate Investment Trusts (REITs) and development groups, which collectively broaden exposure to real asset markets and rental-based income streams.

Communications and Media Organisations

Telecom networks, internet service providers, and digital media broadcasters are covered under the communication services group. These companies play a central role in the delivery of mobile, broadband, and entertainment services, reinforcing the sector’s importance within the broader Australian share market.

0 notes

Text

🌐 Global Network Transformation Market: Building the Future of Connectivity 🚀

Market Size and Overview:

The Global Network Transformation Market was valued at USD 46.48 billion in 2024 and is projected to reach a market size of USD 367.30 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 51.2%.

➡️ 𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐒𝐚𝐦𝐩𝐥𝐞: @ https://tinyurl.com/4jvaafps

The Network Transformation Market refers to the global shift from traditional network architectures to more agile, software-defined, and virtualized network infrastructures. This transformation is fueled by the rapid adoption of advanced technologies such as 5G, edge computing, IoT, and cloud services, which demand more scalable, flexible, and efficient network systems. Organizations across industries are embracing network transformation to improve connectivity, reduce operational costs, and meet the evolving needs of digital communication. The market is witnessing significant momentum as service providers and enterprises prioritize automation, security, and high-performance networks to support future-ready digital ecosystems.

Key Market Insights:

The deployment of 5G networks is one of the strongest driving forces behind network transformation, with over 250 commercial 5G networks active globally as of 2024. This growth has led telecom operators to rapidly upgrade legacy infrastructure to support faster data speeds, low latency, and massive device connectivity.

The surge in data consumption is staggering—global internet traffic grew by more than 30% in 2023, pushing enterprises and service providers to modernize their networks for better bandwidth efficiency and management. This has led to increased investment in automation and AI-driven network management solutions that ensure predictive maintenance, real-time insights, and faster decision-making.

Security and sustainability are becoming central to network transformation strategies. Around 60% of organizations report prioritizing green networking technologies and energy-efficient infrastructure upgrades. At the same time, nearly 70% of telecom operators are incorporating AI-based threat detection systems to build secure, adaptive, and resilient network environments, indicating a strategic shift toward long-term, intelligent network planning.

Network Transformation Market Drivers:

Surging Demand for High-Speed Connectivity and Low Latency is Powering Market Growth

The growing consumption of high-definition content, cloud-based services, and data-intensive applications has drastically increased the demand for faster and more reliable networks. Network transformation enables telecom providers to meet this demand by transitioning from legacy infrastructures to more agile, high-capacity networks. The need for real-time communication and ultra-low latency has become a priority for businesses and consumers alike, pushing service providers to invest in advanced technologies like 5G, fiber optics, and edge computing.

Proliferation of IoT Devices is Driving the Need for Network Upgrades

The increased adoption of Internet of Things (IoT) devices across industries such as healthcare, manufacturing, and smart cities has created an unprecedented load on existing networks. These connected devices generate large volumes of data that require fast processing and minimal latency. Network transformation provides the scalability and agility needed to support billions of devices simultaneously, paving the way for seamless connectivity and data management in an IoT-dominated environment.

Shift Toward Virtualization and Software-Defined Networking is Accelerating Market Evolution

Organizations are increasingly moving toward network virtualization and Software-Defined Networking (SDN) to improve efficiency, reduce operational costs, and achieve greater control. By decoupling the hardware from the control functions, SDN and Network Function Virtualization (NFV) enable dynamic configuration, centralized management, and improved network agility.

➡️ 𝐁𝐮𝐲 𝐍𝐨𝐰 @ https://tinyurl.com/4bwhbtus

Rising Adoption of Cloud Computing and Edge Infrastructure is Reshaping Network Architecture

With businesses increasingly migrating to the cloud, the demand for modernized and distributed network infrastructure is more critical than ever. Traditional centralized networks are not equipped to handle the volume and speed required by cloud-native applications. Edge computing is emerging as a key solution by bringing data processing closer to the source, and this shift is accelerating the adoption of network transformation strategies to support decentralized architectures and ensure seamless cloud performance.

Network Transformation Market Restraints and Challenges:

Security Concerns and High Implementation Costs Pose Major Challenges to Market Growth

Despite the significant advantages of network transformation, several challenges continue to hinder its widespread adoption. One of the key concerns is cybersecurity, as modernized networks—particularly those utilizing virtualization and cloud-based technologies—can be vulnerable to new forms of cyberattacks. Additionally, the high capital expenditure required for upgrading legacy systems to advanced, software-defined infrastructure remains a barrier for many enterprises, especially small and medium-sized businesses. The complexity of integration with existing systems, regulatory compliance, and the need for skilled professionals further complicate the transformation process.

➡️ Enquire Before Buying @ https://tinyurl.com/yc4tbzjx

Network Transformation Market Opportunities:

The Network Transformation Market presents substantial opportunities fueled by the rapid proliferation of 5G networks, increasing demand for edge computing, and the expansion of Internet of Things (IoT) ecosystems. As businesses embrace digital transformation, there is a growing need for agile, scalable, and intelligent network infrastructures that support real-time data processing and automation. This shift creates room for innovative solutions such as Software-Defined Networking (SDN), Network Functions Virtualization (NFV), and AI-powered network management systems. Moreover, the push toward sustainable and energy-efficient networks align with global environmental goals, offering vendors the chance to develop greener technologies and tap into new markets focused on eco-conscious infrastructure solutions.

0 notes

Text

Middle East and Africa Freight Transportation Management Market Size, Share, Trends, Opportunities, Key Drivers and Growth Prospectus

Middle East and Africa Freight Transportation Management Market - Size, Share, Demand, Industry Trends and Opportunities

Middle East and Africa Freight Transportation Management Market, By Transportation Mode (Roadways, Railways, Marine and Airways),Offering (Solutions and Services), Deployment Mode (Cloud or Hosted and On Premise), Organization Size (Large Enterprises and SME'S), Industry (Manufacturing, Retail & E-Commerce, Transportation, Fast Moving Consumer Goods (FMCG), Healthcare, Food & Beverages, Oil & Gas, Energy & Utility, Electronics, Automotive, IT & Telecom and Others) – Industry Trends.

Get the PDF Sample Copy (Including FULL TOC, Graphs and Tables) of this report @

**Middle East and Africa Freight Transportation Management Market Analysis**

The Middle East and Africa Freight Transportation Management market is witnessing significant growth and transformation driven by various factors such as advancements in technology, globalization of trade, and the increasing need for efficient logistics solutions. According to data from a reputable source, the market is poised for substantial growth in the coming years. The region's strategic location as a gateway between Asia, Europe, and Africa further enhances its importance in the global supply chain network. The demand for freight transportation management solutions is increasing as companies strive to streamline their operations, reduce costs, and enhance overall efficiency.

**Segments**

The Middle East and Africa Freight Transportation Management market can be segmented based on various factors such as transportation mode, deployment type, application, and end-user industry.

1. **Transportation Mode**: This segment includes roadways, railways, airways, and seaways. Each mode of transportation has its unique requirements and challenges, and freight management solutions need to be tailored to meet the specific needs of each mode.

2. **Deployment Type**: The market can be segmented based on deployment types such as cloud-based and on-premises solutions. Cloud-based solutions are gaining traction due to their scalability, cost-effectiveness, and ease of implementation.

3. **Application**: Applications of freight transportation management solutions include warehouse management, freight auditing and payment, route optimization, and tracking and monitoring. Each application plays a crucial role in enhancing the overall logistics efficiency.

4. **End-User Industry**: The market caters to various industries such as manufacturing, retail, healthcare, automotive, and others. Each industry has unique requirements when it comes to freight transportation management, and solutions need to be customized to meet these specific needs.

**Market Players**

- Company 1 - Company 2 - Company 3 - Company 4 - Company 5

The market for freight transportation management in the Middle East and Africa region is highly competitive, with several key players vying for market share. These players offer a wide range of solutions and services to meet the diverse needs of customers in the region. Companies are focusing on innovation, strategic partnerships, and mergers and acquisitions to stay ahead in the market.

One of the key growth drivers for the market is the increasing adoption of technology such as artificial intelligence, Internet of Things (IoT), and blockchain in freight transportation management. These technologies enable real-time tracking, predictive analytics, and automation, leading to improved operational efficiency and cost savings. Additionally, the growing e-commerce sector in the region is fueling the demand for advanced logistics solutions to manage the increasing volume of shipments.

However, the market also faces challenges such as infrastructure bottlenecks, regulatory hurdles, and security concerns. Addressing these challenges will be crucial for the sustainable growth of the freight transportation management market in the Middle East and Africa region.

In conclusion, the Middle East and Africa Freight Transportation Management market is poised for significant growth driven by technological advancements, increasing trade activities, and the need for efficient logistics solutions. Companies that can innovate and adapt to the evolving market dynamics will be well-positioned to capitalize on the opportunities in this dynamic market.

Access Full 350 Pages PDF Report @

Key Coverage in the Middle East and Africa Freight Transportation Management Market Report:

Detailed analysis of Middle East and Africa Freight Transportation Management Market by a thorough assessment of the technology, product type, application, and other key segments of the report

Qualitative and quantitative analysis of the market along with calculation for the forecast period

Investigative study of the market dynamics including drivers, opportunities, restraints, and limitations that can influence the market growth

Comprehensive analysis of the regions of the Middle East and Africa Freight Transportation Management Market industry and their futuristic growth outlook

Competitive landscape benchmarking with key coverage of company profiles, product portfolio, and business expansion strategies

Table of Content:

Part 01: Executive Summary

Part 02: Scope of the Report

Part 03: Middle East and Africa Freight Transportation Management Market Landscape

Part 04: Middle East and Africa Freight Transportation Management Market Sizing

Part 05: Middle East and Africa Freight Transportation Management Market by Product

Part 06: Five Forces Analysis

Part 07: Customer Landscape

Part 08: Geographic Landscape

Part 09: Decision Framework

Part 10: Drivers and Challenges

Part 11: Market Trends

Part 12: Vendor Landscape

Part 13: Vendor Analysis

For More Insights Get Detailed TOC @

Reasons to Buy:

Review the scope of the Middle East and Africa Freight Transportation Management Market with recent trends and SWOT analysis.

Outline of market dynamics coupled with market growth effects in coming years.

Middle East and Africa Freight Transportation Management Market segmentation analysis includes qualitative and quantitative research, including the impact of economic and non-economic aspects.

Middle East and Africa Freight Transportation Management Market and supply forces that are affecting the growth of the market.

Market value data (millions of US dollars) and volume (millions of units) for each segment and sub-segment.

and strategies adopted by the players in the last five years.

Browse Trending Reports:

Middle East And Africa Parental Control Software Market North America Parental Control Software Market Asia Pacific Specialty Oilfield Chemicals Market Europe Specialty Oilfield Chemicals Market Middle East And Africa Specialty Oilfield Chemicals Market North America Specialty Oilfield Chemicals Market California Biostimulants Market Asia Pacific Biostimulants Market Europe Biostimulants Market Middle East And Africa Biostimulants Market North America Biostimulants Market

About Data Bridge Market Research:

Data Bridge set forth itself as an unconventional and neoteric Market research and consulting firm with unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email: [email protected]

#market share#market trends#market report#market analysis#market research#marketresearch#market size

0 notes

Text

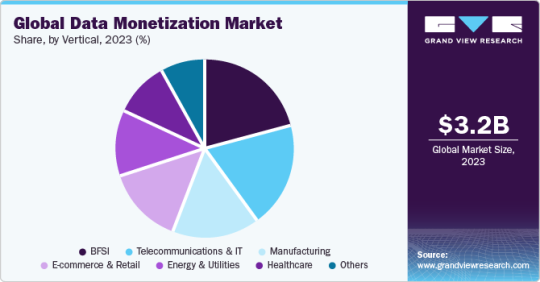

The Future is Now: Navigating the Data Monetization Market Evolution

Data Monetization Industry Overview

The global Data Monetization Market was valued at approximately USD 3.24 billion in 2023 and is projected to expand at a compound annual growth rate (CAGR) of 25.8% from 2024 to 2030. Data monetization involves the exchange of data between organizations to generate new revenue streams. This can be categorized into two main types: direct and indirect data monetization. Direct data monetization includes the sale of unprocessed data, the commercialization of a company's analyses, data bartering or trading, and the development of application programming interfaces (APIs). Conversely, indirect monetization focuses on leveraging data to achieve tangible benefits such as cost reduction, enhanced productivity and efficiency, the creation of novel products or services, and the identification of new customer segments or business opportunities. For example, with user consent, Uber shares its ride data with companies in the food and retail sectors, enabling these businesses to identify promising locations for new establishments.

Several factors are expected to propel market growth, including the increasing volume of enterprise data, a growing understanding of data monetization's potential, and the availability of external data sources. Additionally, the rising application of data processing and artificial intelligence, the increasing adoption of data-driven decision-making strategies, and advancements in big data analytics are anticipated to further stimulate growth throughout the forecast period.

Detailed Segmentation:

Method Insights

Embedded analytics segment is expected to witness a significant CAGR of 26.2% from 2024 to 2030. Embedded analytics can integrate existing applications with additional features such as data visualization, dashboard reporting, and analytics. This method accelerates time to market, creates customized embedded analytics solutions, and lowers TCO. Similarly, insight as a service combines external and internal data sources that use analytics to provide data insights. This method can support specific datasets and provide updated data to customers.

Organization Size Insights

The SMEs segment is expected to grow at the fastest CAGR of 29.4% from 2024 to 2030. The rising adoption of data monetization by SMEs to sustain in the competitive market is expected to power the segment growth over the forecast period. Furthermore, SMEs are expected to face resource shortages, resulting in business complexities and the increased need to optimize costs. In this situation, the rising presence of cloud-based data monetization is expected to play a pivotal role in ensuring reduced operations costs and increased efficiency, thereby positively affecting segment growth.

Vertical Insights

The telecommunications & IT segment is expected to witness a significant CAGR of 26.7% from 2024 to 2030. The increasing amount of data generated by these companies, the growing demand for data-driven decision-making, the increasing adoption of cloud computing, and the growing popularity of big data analytics. These factors make it easier for telecom and IT companies to store, analyze, and monetize their data.

Regional Insights

The data monetization market in the U.S. is growing significantly at a CAGR of 23.1% from 2024 to 2030. Growing government focus on encouraging digitization across industries to improve the transparency of processes is creating a positive outlook for the U.S. market. Furthermore, advancements in emerging technologies such as Artificial Intelligence (AI) and the Internet of Things (IoT) are expected to drive the market growth in the region. In addition, various IT and telecom companies are shifting their businesses to Software-as-a-Service (SaaS) and Infrastructure-as-a-Service (IaaS) platforms in the U.S. to initiate remote operation management. This has bolstered the demand for system infrastructure software in the IT and telecom sectors in the region.

Gather more insights about the market drivers, restraints, and growth of the Data Monetization Market

Key Companies & Market Share Insights

Some of the key companies include Accenture, Cisco, and IBM Corporation, and others are some of the leading participants in the global data monetization market.

Accenture provides technology solutions and professional services in areas such as network management and consulting. It operates through five business lines: Accenture Technology, Accenture Operations, Accenture Digital, Accenture Strategy, and Accenture Consulting. The company offers business process services, infrastructure services, security services, and cloud services under the Accenture Operations business line.

Cisco Systems, Inc. specializes in developing and distributing hardware and software solutions. The company serves industries such as mining, oil and gas, smart buildings, retail, education, financial services, government, transportation, utilities, healthcare, insurance, and entertainment. It offers solutions across a range of technologies, including cloud, data center, network infrastructure, mobility, IoT, security, AI, and analytics and automation.

Key Data Monetization Companies:

The following are the leading companies in the data monetization market. These companies collectively hold the largest market share and dictate industry trends.

Accenture

Adstra

Cisco Systems, Inc.

Comviva

Domo, Inc.

Thales (Gemalto NV)

Gulp Data

IBM Corporation

Order a free sample PDF of the Market Intelligence Study, published by Grand View Research.

Recent Developments

In February 2024, Gulp Data announced a partnership with Snowflake that enables organizations to explore, share, and unlock value from their data, providing data valuation, data-backed loans, and data monetization services.

In December 2023, Thales completed the acquisition of Imperva. By providing the most comprehensive solutions for the broadest range of application, data security, and identity use cases, Thales and Imperva will help customers address cybersecurity challenges that are increasing rapidly in frequency, severity, and complexity.

0 notes

Text

Empowering Communication: Trusted Call Center Suite Provider Company in UAE

In a digitally connected world, seamless customer interaction is no longer a luxury—it's a necessity. Businesses across the UAE are rapidly adopting unified communication tools to streamline operations, enhance productivity, and deliver world-class customer service. At the center of this transformation is a trusted Call Center Suite Provider Company in UAE like Aria Telecom, delivering end-to-end contact center solutions that redefine the way you connect with your customers.

From small businesses to large enterprises, companies are realizing the value of integrated communication platforms. If you’re searching for a reliable partner that combines innovation, efficiency, and localized support, Aria Telecom is your go-to solution.

Why Choose a Call Center Suite?

A call center suite isn’t just a set of phone lines. It’s an all-in-one communication hub that handles inbound and outbound calls, manages omnichannel engagement, integrates with CRM systems, and provides advanced analytics. Key features include:

Interactive Voice Response (IVR)

Automatic Call Distribution (ACD)

Predictive Dialers

Call Recording & Monitoring

SMS, Email & Social Media Integration

Real-Time Reporting Dashboards

These features empower businesses to manage higher call volumes, reduce operational costs, and deliver consistent customer experiences across platforms.

Aria Telecom: The Leading Call Center Suite Provider Company in UAE

As a top-tier Call Center Suite Provider Company in UAE, Aria Telecom delivers intelligent, scalable, and customizable solutions to suit every business size and industry. Whether you're in healthcare, finance, retail, education, or public services, we offer cloud-based and on-premise solutions tailored to your needs.

What makes Aria Telecom stand out?

Tailor-Made Solutions: We customize every suite to fit your specific operations, ensuring optimal performance and scalability.

Fast & Easy Deployment: With a skilled local team in the UAE, our installations are smooth, timely, and fully supported.

Advanced Analytics: Make data-driven decisions using real-time performance metrics, customer insights, and call reports.

Seamless Integrations: We integrate with leading CRM platforms, ERPs, and databases.

Omnichannel Support: Manage calls, chats, emails, and social interactions from one dashboard.

We understand the demands of the UAE market and provide localized support to ensure your business never misses a beat.

Benefits of Implementing a Call Center Suite

Companies that implement our suite see noticeable improvements in both operations and customer satisfaction:

Boosted Agent Productivity: With automation and simplified workflows, your team can handle more inquiries with less effort.

Enhanced Customer Satisfaction: Intelligent call routing and self-service options reduce wait times and resolve issues faster.

24/7 Availability: Cloud-based solutions allow your team to work from anywhere, anytime.

Stronger Compliance: We ensure that your customer interactions meet UAE's data security and regulatory standards.

Scalable Infrastructure: Easily add users, features, or communication channels as your business grows.

By choosing a trusted Call Center Suite Provider Company in UAE, you're setting your organization up for long-term communication success.

Who Can Benefit?

Our clients span diverse sectors, each with unique communication challenges that our platform helps solve:

E-commerce: Manage order inquiries, complaints, and returns with fast, multichannel support.

Banking & Finance: Improve verification processes, manage large call volumes, and ensure secure data handling.

Healthcare: Enable round-the-clock appointment booking, emergency response, and follow-up care coordination.

Real Estate: Streamline property inquiries, bookings, and agent-customer communication.

Government Services: Offer multilingual, automated public service support and helplines.

Future-Proofing Your Communication Strategy

The future of business communication lies in intelligent automation and omnichannel connectivity. At Aria Telecom, we stay ahead of the curve with:

AI-Powered Call Routing

Speech Analytics & Transcription

Chatbots & Virtual Assistants

WhatsApp Business Integration

Cloud-to-On-Premise Flexibility

These innovations ensure that your organization is equipped for both today’s needs and tomorrow’s expectations.

0 notes

Text

Centralized Radio Access Network (C-RAN) Market: Growth Strategies, Key Players, and Segmentation 2031.

Centralized Radio Access Network (C-RAN) Market: Growth Strategies, Key Players, and Segmentation 2031.

The report is segmented by Component (Solution, Services), by Network Type (2G and 3G, 4G, 5G), and by End User (Telecom Operators, Enterprises). The global analysis is further broken down at the regional level and major countries. The report offers the value in USD for the above analysis and segments.

Market Overview The centralized radio access network (C-RAN) market is expected to register a CAGR of 19.4 % from 2025 to 2031, with a market size expanding from US$ XX million in 2024 to US$ XX Million by 2031.

This growth is driven by various factors:

Increasing Demand for Better Network Performance: As there is a growing demand for high-speed internet and always-on connectivity, the centralized radio access network (C-RAN) market is witnessing strong growth. The centralized radio access network (C-RAN) market network employs Central Base Band Units in a central or cloud data center. This increases the network performance by minimizing latency and enhancing spectral efficiency. Due to this, mobile operators can effectively distribute and use their resources while fulfilling increasing consumer demand for speedy and reliable mobile service worldwide. The deployment of 5G networks globally: The deployment of 5G networks globally is also a key driver for the C-RAN market. With the need for increasingly complex infrastructure to enable high data rates and low latency with 5G networks, C-RAN offers an effective architecture that leverages existing and new cloud computing support to optimize performance. Cost Savings and Operational Efficiency: CRAN solutions offer telecom operators a means of centralizing and virtualizing network resources, decreasing the amount of physical infrastructure and maintenance required at distant cell sites. Through the use of cloud-based architectures and centralized control, CRAN lowers capital and operating costs while enhancing network management.

Growth Strategies Major strategies propelling the C-RAN market are:

1. Strategic Partnerships and Collaborations Telecom companies are aligning with technology vendors to spur centralized radio access network (C-RAN) market adoption. Bharti Airtel, for example, has signed multi-billion-dollar deals with Ericsson and Nokia to upgrade its 4G and 5G coverage in India. The partnerships target the deployment of centralized and Open RAN-capable solutions, with the objective of enhancing network speed, reliability, and coverage.

2. Research and Development Investment Firms are spending a lot on R&D to create sophisticated C-RAN solutions. Ericsson's partnership with Intel to open a C-RAN tech hub in California is an example of an attempts to innovate and enhance network performance through enterprise applications and energy-saving solutions.

3. Growth into Emerging Markets The Asia-Pacific region is seeing the adoption of centralized radio access network (C-RAN) market at a rapid pace with growing mobile data traffic and investment in telecom infrastructure. Nations with large optical fiber networks are especially well-positioned for C-RAN deployments, presenting tremendous growth opportunities.

Key Market Players Ceragon Networks Ltd. Actix Ltd. Aricent Technologies JDSU 6WIND MTI Radio comp Altera Corp. Mindspeed Technologies, Inc. Intel Corporation Vitesse Semiconductor

Market Segmentation The market for centralized radio access network (C-RAN) market may be segmented in terms of architecture, component, and region:

1. By Architecture Centralized C-RAN: This is focused on centralizing baseband processing units within a data center, reducing cell site hardware needs and allowing for effective resource management.

Cloud C-RAN: Builds on the centralized architecture by virtualizing the network functions, which allows for dynamic resource allocation and increased scalability.

2. By Component Baseband Units (BBUs): These are the central processing unit, carrying out activities like signal processing and resource management.

Remote Radio Heads (RRHs): In cell sites, RRHs receive and transfer radio signals to centralized BBUs via high-speed links.

Fronthaul Networks: Connecting RRHs and BBUs, requiring high-bandwidth, low-latency backhaul connectivity.

3. By Region North America: Embracing centralized radio access network (C-RAN) market at a leadership level due to early 5G deployments and massive investments from communications operators.

Asia-Pacific: Experiencing high growth through massive infrastructure development and increasing mobile data consumption.

Europe: Emphasis on network efficiency improvement and serving IoT applications via C-RAN solutions.

Middle East and Africa: Developing markets spending on telecom infrastructure to address increasing connectivity needs.

Future Outlook The C-RAN market will expand further with telecom service providers seeking efficient solutions to meet the requirements of 5G and beyond. Trends to watch for are:

Integration with Open RAN: Open RAN adoption promotes openness and vendor variety and benefits a more agile and cost-effective network ecosystem.

Edge Computing: centralized radio access network (C-RAN) market and edge computing combined facilitate low-latency processing, which is critical for use in autonomous cars and real-time analytics.

Sustainability Initiatives: Operators are concentrating on energy-efficient technology to minimize the environmental footprint of network operations.

Conclusion The centralized radio access network (C-RAN) market industry is seeing a complete paradigm shift, triggered by technological innovations and strategic developments by the dominant industry players. With demand for high-speed quality connections continuing unabated, C-RAN solutions provide a tantalizing roadmap to the future, allowing telecom operators to establish future-proof, efficient, and scalable networks.

1 note

·

View note

Text

North America Voice Biometrics Market - Business Prospects

Business Market Insights recently announced the release of the market research titled North America Voice Biometrics Market Outlook to 2028 | Share, Size, and Growth. The report is a stop solution for companies operating in the North America Voice Biometrics market. The report involves details on key segments, market players, precise market revenue statistics, and a roadmap that assists companies in advancing their offerings and preparing for the upcoming decade. Listing out the opportunities in the market, this report intends to prepare businesses for the market dynamics in an estimated period.

Is Investing in the Market Research Worth It?

Some businesses are just lucky to manage their performance without opting for market research, but these incidences are rare. Having information on longer sample sizes helps companies to eliminate bias and assumptions. As a result, entrepreneurs can make better decisions from the outset. North America Voice Biometrics Market report allows business to reduce their risks by offering a closer picture of consumer behavior, competition landscape, leading tactics, and risk management.

A trusted market researcher can guide you to not only avoid pitfalls but also help you devise production, marketing, and distribution tactics. With the right research methodologies, Business Market Insights is helping brands unlock revenue opportunities in the North America Voice Biometrics market.

If your business falls under any of these categories – Manufacturer, Supplier, Retailer, or Distributor, this syndicated North America Voice Biometrics market research has all that you need.

What are Key Offerings Under this North America Voice Biometrics Market Research?

Global North America Voice Biometrics market summary, current and future North America Voice Biometrics market size

Market Competition in Terms of Key Market Players, their Revenue, and their Share

Economic Impact on the Industry

Production, Revenue (value), Price Trend

Cost Investigation and Consumer Insights

Industrial Chain, Raw Material Sourcing Strategy, and Downstream Buyers

Production, Revenue (Value) by Geographical Segmentation

Marketing Strategy Comprehension, Distributors and Traders

Global North America Voice Biometrics Market Forecast

Study on Market Research Factors

Who are the Major Market Players in the North America Voice Biometrics Market?

North America Voice Biometrics market is all set to accommodate more companies and is foreseen to intensify market competition in coming years. Companies focus on consistent new launches and regional expansion can be outlined as dominant tactics. North America Voice Biometrics market giants have widespread reach which has favored them with a wide consumer base and subsequently increased their North America Voice Biometrics market share.

Report Attributes

Details

Segmental Coverage

Component

Solution and Services

Type

Active Voice Biometrics and Passive Voice Biometrics

Authentication Process

Automated IVR

Agent-assisted

Mobile Application

and Employee Authentication

Deployment

Cloud and On-premise

Vertical

BFSI

Retail & E-commerce

Government & Defense

IT & Telecom

Healthcare & Life Sciences

Transportation & Logistics

Travel & Hospitality

Energy & Utilities

and Others

Application

Authentication and Customer Verification

Forensic Voice Analysis and Criminal Investigation

Fraud Detection and Prevention

Risk and Emergency Management

Transaction Processing

Access Control

Wor

Regional and Country Coverage

North America (US, Canada, Mexico)

Europe (UK, Germany, France, Russia, Italy, Rest of Europe)

Asia Pacific (China, India, Japan, Australia, Rest of APAC)

South / South & Central America (Brazil, Argentina, Rest of South/South & Central America)

Middle East & Africa (South Africa, Saudi Arabia, UAE, Rest of MEA)

Market Leaders and Key Company Profiles

Aculab

Auraya, Inc.

Aware Inc

NICE Ltd

Nuance Communications, Inc

Pindrop

Verint Systems, Inc

Other key companies

What are Perks for Buyers?

The research will guide you in decisions and technology trends to adopt in the projected period.

Take effective North America Voice Biometrics market growth decisions and stay ahead of competitors

Improve product/services and marketing strategies.

Unlock suitable market entry tactics and ways to sustain in the market

Knowing market players can help you in planning future mergers and acquisitions

Visual representation of data by our team makes it easier to interpret and present the data further to investors, and your other stakeholders.

Do We Offer Customized Insights? Yes, We Do!

The Business Market Insights offer customized insights based on the client’s requirements. The following are some customizations our clients frequently ask for:

The North America Voice Biometrics market report can be customized based on specific regions/countries as per the intention of the business

The report production was facilitated as per the need and following the expected time frame

Insights and chapters tailored as per your requirements.

Depending on the preferences we may also accommodate changes in the current scope.

About Us:

Business Market Insights is a market research platform that provides subscription services for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductors, Aerospace & Defense, Automotive & Transportation, Energy & Power, Healthcare, Manufacturing & Construction, Food & Beverages, Chemicals & Materials, and Technology, Media & Telecommunications.

Contact Us: : www.businessmarketinsights.com

0 notes

Text

From Decommission to Opportunity: A Comprehensive ITAD Market Analysis

The global IT asset disposition market size is projected to be USD 54,535.4 million by 2030, according to the latest study conducted by Grand View Research, Inc. The market is expected to exhibit a CAGR of 13.3% from 2023 to 2030. The growth of the ITAD market can be attributed to the increasing e-waste and the rising requirement for recycling in consideration of sustainability and a green planet.

For instance, according to the Indian Ministry of Electronics and Information Technology, India generated 3.2 million tonnes of electronic waste in 2019, and only 10% of e-waste was taken up for recycling. Such an alarming figure has resulted in the demand for ITAD solutions, thereby driving the market’s growth.

Various companies have been coming up with ITAD solutions with enhanced capabilities, which can serve multiple industries. Moreover, companies operating in the ITAD market have also been involved in various strategic initiatives and R&D, among others, to improve their share in the ITAD market. For instance, in January 2023, ERI announced that it had become 100% carbon neutral for all its operational emissions across the U.S.

The company achieved this by implementing carbon-reducing measures such as energy-efficient lighting, using zero-emission vehicles, fleet management, and using electric forklifts, among others. 100% Carbon neutrality would help the company better position in the ITAD market, which would thereby help in driving the growth of the ITAD market over the forecast period.

Cloud transition is another significant aspect that has been pivotal in driving the growth of the IT asset disposition industry over the forecast period. Cloud migration's benefits include increased flexibility and agility, reduced costs, enhanced cybersecurity, simplified management, and disaster recovery. All these attributes have made it a go-to area for businesses operating in various industries.

Moreover, the presence of ITAD solution providers in the market who are equipped to assist in cloud migration services and ITAD has been a significant boost to the growth of the IT asset disposition industry. For instance, Apto Solutions Inc. offers cloud migration services, in which the company handles the existing hardware for carrying out the following operations.

Data destruction

Asset inventory

Logistics to one of the company’s certified facilities

Post carrying out these operations, the company either sells or recycles the hardware component. The presence of companies that offers a total solution, as in the case of Apto Solutions Inc., has been a significant boon to the growth of the IT asset disposition industry.

IT Asset Disposition Market Report Highlights

The computers/laptops segment is expected to occupy the largest revenue share by asset type in 2030. The growth can be attributed to digitalization, especially in low-income countries, and rising internet users, among others

The smartphone segment is expected to witness the highest CAGR by asset type during the forecast period. The growth can be attributed to increased smartphone sales, increasing internet penetration, and smartphones coming up with enhanced smartphones quite often, among others

The IT & telecom industry is expected to occupy the largest share of the market in terms of end-use by 2030, owing to an increase in internet users, adoption of 5G technology, and increased demand for connectivity worldwide, among others

Asia Pacific is projected to witness the highest CAGR from 2023 to 2030. The region is home to some tech giants such as Samsung, Sony Corporation, and LG electronics, among others. Moreover, the increasing digitalization in countries such as Indonesia, Vietnam, and Bangladesh is another factor contributing to the growth of the Asia Pacific region

Global players include Apto Solutions Inc.; Dell Inc.; IBM Corporation; and Iron Mountain. These major players are embracing organic and inorganic growth strategies, which include product innovation, investments in R&D, and M&A activities to acquire a larger industry share

Curious about the IT Asset Disposition Market? Download your FREE sample copy now and get a sneak peek into the latest insights and trends.

IT Asset Disposition Market Segmentation

Grand View Research has segmented the global IT asset disposition market based on asset type, end-use, and region:

IT Asset Disposition Asset Type Outlook (Revenue; USD Billion, 2018 - 2030)

Computers/Laptops

Smartphones and Tablets

Peripherals

Storages

Servers

Others

IT Asset Disposition End-use Outlook (Revenue; USD Billion, 2018 - 2030)

BFSI

IT & Telecom

Government

Energy and Utilities

Healthcare

Media and Entertainment

Others

IT Asset Disposition Regional Outlook (Revenue; USD Billion, 2018 - 2030)

North America

US

Canada

Europe

Germany

UK

France

Italy

Spain

Asia Pacific

China

India

Japan

Singapore

South Korea

Rest of Asia Pacific

Latin America

Brazil

Mexico

Argentina

Middle East & Africa

UAE

Saudi Arabia

South Africa

Key Players in the IT Asset Disposition Market

Apto Solutions Inc.

CompuCom Systems, Inc.

Dell Inc.

Hewlett Packard Enterprise Development LP

IBM Corporation

Ingram Micro Services

Iron Mountain

ITRenew

LifeSpan International Inc.

Sims Lifecycle Services, Inc.

Order a free sample PDF of the IT Asset Disposition Market Intelligence Study, published by Grand View Research.

0 notes

Text

Internet of Things Market (2025 – 2030)

Internet of Things Market (2025 – 2030)

The Internet of Things (IoT) Market was valued at USD 308.97 billion in 2024 and is projected to reach a market size of USD 996.90 billion by 2030. Over the forecast period of 2025-2030, the market is expected to grow at a CAGR of 26.4%.

Market Size and Overview:

The Internet of Things (IoT) refers to a network of physical objects—"things"—embedded with sensors, software, and other technologies that connect to and exchange data with other devices and systems over the Internet or other communications networks. These connected devices collect and transmit data, which can then be analysed to optimize processes, predict maintenance needs, enhance user experiences, or provide valuable insights. The true power of IoT comes from the combination of these interconnected devices, their data collection capabilities, and the analytics that transform raw data into actionable information. The Global Internet of Things (IoT) Market is experiencing exponential growth due to increasing connectivity, cloud computing advancements, and widespread sensor adoption. As per industry reports, the number of IoT-connected devices is expected to exceed 30 billion by 2030. The industrial IoT segment accounts for a significant market share, driven by smart manufacturing and automation solutions. Governments worldwide are also pushing smart city projects, further accelerating IoT adoption. Additionally, edge computing is transforming data processing by reducing latency and enhancing security.

👉 Request Free Sample : https://tinyurl.com/2s36vsdr

Key Market Insights:

The number of IoT-connected devices worldwide is projected to surpass 30 billion by 2030, driven by smart home adoption, industrial automation, and healthcare IoT. Businesses leveraging IoT-enabled predictive maintenance report a 25% reduction in operational costs. 5G and IoT integration are set to revolutionize industries, with 80% of global telecom operators investing in 5 G-powered IoT solutions. By 2026, 90% of new vehicles will be IoT-connected, enhancing safety and autonomous driving.

The Industrial IoT (IIoT) segment is expanding rapidly, with a CAGR of 16%, particularly in manufacturing, energy, and logistics. Smart factories implementing AI-powered IoT report up to 50% reduction in downtime and 30% higher productivity. According to Gartner, 75% of enterprises will adopt IoT-enabled technology, revolutionizing sectors such as healthcare, automotive, and retail.

The global smart home device shipments crossed 1.6 billion units in 2022, led by smart security systems, smart speakers, and connected appliances. The consumer IoT market is expected to grow by 15% annually, as home automation becomes mainstream.

Internet of Things Market Drivers:

An incredible rise in the use of digital and smart devices has placed IOT at the centre of things, There have been various industrial uses for it also which has meant that the demand has increased for devices integrated with this tech.

The explosion of smart devices and the rise in cloud computing are key factors driving IoT expansion. Businesses are leveraging IoT to enhance real-time analytics, automate workflows, and improve customer experiences. Companies like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud are aggressively investing in IoT ecosystems, offering AI-driven analytics and scalable solutions. The shift toward Industry 4.0 has also fuelled demand for sensor-enabled automation and predictive maintenance in sectors such as oil & gas, automotive, and logistics. Additionally, the healthcare industry is embracing IoT-powered wearable devices for real-time patient monitoring, while smart cities are integrating IoT to optimize traffic management, waste collection, and energy usage. With over $150 billion allocated globally for smart infrastructure projects, IoT remains at the core of digital transformation. IoT is also redefining supply chain efficiency. Connected logistics solutions enable real-time tracking, inventory management, and automated restocking. Companies using IoT in supply chain operations report a 20-25% increase in efficiency, reducing waste and optimizing fleet management.

The growth of AI is coinciding with the integration of IOT and the automation materials and technology across industry is seeking to profit majorly from the AI and IOT integration.

The integration of Artificial Intelligence (AI) with IoT is enhancing automation across industries. AI-powered IoT solutions can predict machine failures, optimize energy usage, and improve safety monitoring in high-risk environments. For example, AI-driven IoT sensors in industrial plants can reduce downtime by up to 50% by providing real-time diagnostics. Furthermore, consumer IoT applications continue to expand, with smart home devices becoming mainstream. The popularity of smart assistants like Amazon Alexa, Google Assistant, and Apple Siri has skyrocketed, with over 500 million active users globally. The rapid growth of Artificial Intelligence (AI) is fuelling the expansion of the Internet of Things (IoT) as industries increasingly integrate these technologies to drive automation, efficiency, and cost reduction. AI-powered IoT systems enable real-time data analysis, predictive maintenance, and autonomous decision-making, significantly improving operational workflows across multiple sectors. Smart factories, for instance, are leveraging AI-driven Industrial IoT (IIoT) to optimize production lines, reduce downtime, and enhance safety.

Internet of Things Market Restraints and Challenges:

Safety concerns and cybersecurity threats are the biggest challenges related to IOT.

Security concerns remain a major challenge in IoT adoption. Cybersecurity threats, data breaches, and unauthorized access to IoT networks have raised concerns, leading to stricter compliance regulations such as GDPR and CCPA. According to industry reports, over 60% of IoT devices remain vulnerable to cyberattacks due to outdated security protocols. Interoperability is another hurdle, as IoT ecosystems often use different communication protocols, making integration complex and costly. Additionally, the high initial investment for enterprise-scale IoT implementation deters small and medium-sized businesses from adopting IoT solutions. . These challenges, combined with persistent connectivity issues in rural and developing regions where internet infrastructure remains limited, create significant barriers to achieving the full potential of IoT technologies across global markets.

Internet of Things Market Opportunities:

The IoT market presents substantial growth opportunities, particularly in emerging application areas and previously underserved sectors. Healthcare IoT solutions show remarkable potential, with the remote patient monitoring segment projected to grow at a CAGR of 31.3% through 2030, driven by aging populations and healthcare cost pressures. Smart city initiatives represent another high-growth opportunity, with global investment expected to reach USD 189.5 billion by 2025. These projects encompass traffic management, waste management, and energy conservation solutions that leverage IoT capabilities to enhance urban living quality. Agricultural IoT applications are gaining significant traction, with precision farming technologies demonstrating yield improvements of up to 15% while reducing water usage by 30%. The emergence of IoT-as-a-Service business models has lowered barriers to entry, allowing smaller enterprises to implement solutions without substantial capital expenditure, thus expanding the total addressable market. Strategic partnerships between hardware manufacturers, software developers, and cloud service providers are creating integrated solutions that address complex industry-specific challenges, opening new revenue streams across the IoT ecosystem.

IoT Market Segmentation:

Market Segmentation: By Component:

• Hardware • Software

Hardware components currently dominate the IoT market landscape, accounting for approximately 42.3% of market share in 2022. This segment encompasses sensors, processors, connectivity modules, and other physical elements essential to IoT functionality. The decreasing cost of these components, with sensor prices declining at an average rate of 8-10% annually, has been instrumental in driving widespread adoption across various applications from consumer electronics to industrial equipment. The software and services segment, while representing a smaller share at 38.7% of the market in 2022, is projected to grow at the fastest CAGR of 29.6% through 2030. This growth is fueled by increasing demand for analytics platforms, security solutions, and management systems that enhance the value derived from IoT hardware deployments. Cloud-based IoT platforms alone generated approximately USD 16.9 billion in revenue during 2024, highlighting the critical role of software infrastructure in the IoT ecosystem.

Market Segmentation: By Application:

• Industrial IOT • Commercial/Industrial IOT

The industrial IoT segment accounted for the largest market share at 31.5% in 2022, with manufacturing, energy, and utilities being primary adopters. Smart factories implementing IoT solutions have reported productivity improvements of 20-30% and maintenance cost reductions of up to 25%. The industrial segment's dominance stems from clear ROI metrics, with companies typically recovering implementation costs within 12-18 months through operational efficiencies and reduced downtime. The consumer IoT segment, encompassing smart home devices, wearables, and connected vehicles, represented 28.4% of the market in 2022 but is expected to grow at a CAGR of 28.3% through 2030. This growth is driven by increasing consumer awareness, declining device prices, and improved user interfaces that simplify adoption. Smart home penetration is particularly notable, with approximately 258 million homes worldwide featuring at least one connected device in 2022, a figure projected to exceed 478 million by 2025.

0 notes

Text

5G NTN Market Size, Share, Growth Analysis, Forecast, and Trends to 2032

The 5G NTN Market was valued at USD 5.5 Billion in 2023 and is expected to reach USD 77.9 Billion by 2032, growing at a CAGR of 34.14% from 2024-2032.

The 5G Non-Terrestrial Network (NTN) market is witnessing exponential growth as it reshapes global communication infrastructure. Integrating satellite and airborne platforms with terrestrial 5G, NTNs promise unprecedented coverage, bridging the digital divide across remote and underserved areas. Major technology firms and telecom operators are investing heavily in NTN solutions to power industries like maritime, aviation, defense, and emergency services, where terrestrial networks fall short. This global push is further fueled by rising demand for real-time data, low latency, and seamless mobility across geographies.

5G NTN Market Transforming traditional limitations, 5G NTN enhances connectivity through a seamless blend of satellite and terrestrial systems. It empowers a broad range of applications—from autonomous transport to remote healthcare—bringing ubiquitous, resilient, and scalable communications to the forefront. This fusion is instrumental in the rollout of future-ready networks, enabling countries and enterprises to boost digital infrastructure and achieve economic and technological advancements.

Get Sample Copy of This Report: https://www.snsinsider.com/sample-request/5978

Market Keyplayers:

SpaceX – Starlink

OneWeb – OneWeb LEO Satellite Network

Telesat – Lightspeed Constellation

Amazon (Project Kuiper) – Kuiper Satellite System

AST SpaceMobile – BlueWalker 3

SES S.A. – O3b mPOWER

Eutelsat – EUTELSAT KONNECT VHTS

Inmarsat (Viasat Inc.) – ORCHESTRA Network

Thales Group – Thales Alenia Space SATCOM Solutions

Lockheed Martin – Pony Express 1

Hughes Network Systems – Jupiter 3 Satellite

Nokia – Nokia AVA for NTN

Ericsson – Ericsson 5G Core for NTN

Huawei – 5G NTN Integrated Solutions

Intelsat – FlexMove Connectivity

Market Analysis

The global 5G NTN market is characterized by intense innovation and strategic collaborations. Key players are entering partnerships with satellite operators, device manufacturers, and governments to accelerate the deployment of NTN-enabled services. The competitive landscape is dynamic, with startups and legacy firms racing to launch Low Earth Orbit (LEO) satellite constellations and integrate AI-based traffic and signal management. Regulatory progress across regions is also accelerating the time-to-market for NTN solutions.

The market is being shaped by various use cases across sectors such as aerospace, transportation, agriculture, mining, and defense. Demand for reliable, always-on connectivity is a strong catalyst, particularly in geographically challenged areas like rural zones, oceans, and disaster-hit regions. Government initiatives for rural broadband and smart infrastructure are significantly driving adoption.

Market Trends

Integration of LEO satellites with 5G terrestrial networks

Growth in IoT and M2M applications via NTN infrastructure

Emergence of hybrid networks combining air, ground, and sea coverage

Partnerships between telecom providers and space tech firms

Focus on energy-efficient NTN hardware and network sustainability

Regulatory frameworks being adapted to enable commercial NTN use

Increased use of AI and edge computing in NTN systems

Market Scope

Global Reach: Expands high-speed connectivity to the most inaccessible terrains

Emergency Services: Ensures robust communication during natural disasters

Autonomous Systems: Enables operation of drones, vehicles, and machinery in remote areas

Maritime & Aviation: Delivers uninterrupted coverage over sea and air routes

Government & Defense: Secures mission-critical and surveillance communications

The scope of the 5G NTN market is vast and transformative, impacting industries that rely on connectivity beyond traditional cellular networks. Its cross-sectoral applications position it as a pivotal enabler of Industry 4.0 and next-generation digital infrastructure.

Market Forecast

The market is projected to grow rapidly over the coming years, driven by the confluence of satellite advancements, 5G proliferation, and the demand for resilient, global connectivity. Continuous innovation in satellite technology, cost-effective deployment strategies, and international collaborations are expected to fuel this momentum. As commercial launches accelerate, NTN is set to become a cornerstone of next-generation telecommunications, complementing terrestrial 5G to provide truly borderless network access.

Access Complete Report: https://www.snsinsider.com/reports/5g-ntn-market-5978

Conclusion

The 5G NTN market is not just a technological leap—it is a bridge to an interconnected future where no location is left behind. As it continues to mature, it will redefine how businesses, governments, and individuals communicate across the globe. With strategic foresight and global collaboration, 5G NTN stands as the next frontier of wireless innovation, promising an inclusive, always-connected world that meets the evolving needs of the digital age.

About Us:

SNS Insider is one of the leading market research and consulting agencies that dominates the market research industry globally. Our company's aim is to give clients the knowledge they require in order to function in changing circumstances. In order to give you current, accurate market data, consumer insights, and opinions so that you can make decisions with confidence, we employ a variety of techniques, including surveys, video talks, and focus groups around the world.

Contact Us:

Jagney Dave - Vice President of Client Engagement

Phone: +1-315 636 4242 (US) | +44- 20 3290 5010 (UK)

0 notes

Text

Europe Artificial Intelligence (AI) Chip Market Size, Share, Comprehensive Analysis, Opportunity Assessment (2019-2027)

Europe Artificial Intelligence (AI) Chip Market is expected to grow from US$ 1.25 Bn in 2018 to US$ 16.04 Bn by the year 2027 with a CAGR of 33.0% from the year 2019 to 2027.

Europe Artificial Intelligence (AI) Chip Market Introduction

A key driver fueling the expansion of the European AI Chip market is the substantial capital investment directed towards artificial intelligence chip start-ups. The escalating demand for real-time consumer behavior insights, alongside the pursuit of enhanced operational efficiency, are also significant factors propelling the broader integration of AI across diverse industries. Furthermore, the anticipated incorporation of AI chips into edge computing devices is poised to further stimulate the market's growth throughout the forecast period. Across the globe, major industries spanning BFSI, retail, IT & telecom, automotive & transportation, healthcare, media & entertainment, manufacturing, government, and energy & power are actively embracing and investing in transformative technologies such as artificial intelligence, the Internet of Things (IoT), big data, and predictive analytics. This widespread adoption is a direct consequence of the demonstrated successes of AI applications, leading to improved operational efficiency, increased sales revenue, and enhanced interactions with customers.

Download our Sample PDF Report

@ https://www.businessmarketinsights.com/sample/TIPRE00005730

Europe Artificial Intelligence (AI) Chip Strategic Insights

Strategic insights concerning the Europe Artificial Intelligence (AI) Chip market deliver a data-centric examination of the industry's structure, encompassing prevailing trends, key market participants, and specific regional characteristics. These insights offer practical recommendations, empowering readers to distinguish themselves from competitors by discovering unexploited market segments or formulating distinctive value propositions. By effectively utilizing data analytics, these insights assist industry stakeholders, whether they are investors, manufacturers, or other actors, in anticipating shifts in the market. A forward-looking viewpoint is crucial, aiding stakeholders in predicting market changes and strategically positioning themselves for sustained success in this evolving European region. Ultimately, impactful strategic insights equip readers to make well-informed decisions that foster profitability and support the realization of their business goals within the market.

Europe Artificial Intelligence (AI) Chip Regional Insights

The geographic scope of the Europe Artificial Intelligence (AI) Chip market defines the specific territories in which a business operates and competes. Comprehending local variations, such as diverse consumer preferences (for instance, the need for specific plug types or battery backup durations), differing economic landscapes, and regulatory frameworks, is vital for adapting strategies to particular markets. Businesses can broaden their market reach by identifying markets that are currently underserved or by modifying their offerings to align with local requirements. A focused market approach enables more effective resource management, targeted marketing efforts, and improved competitive positioning against local players, ultimately driving expansion in those targeted regions.

Europe Artificial Intelligence (AI) Chip Market Segmentation

Europe Artificial Intelligence (AI) Chip Market: By Segment

Data Center

Edge

Europe Artificial Intelligence (AI) Chip Market: By Type

CPU

GPU

ASIC

FPGA

Others

Europe Artificial Intelligence (AI) Chip Market: By Industry Vertical

BFSI

Retail

IT & Telecom

Automotive & Transportation

Healthcare

Media & Entertainment

Others

Europe Artificial Intelligence (AI) Chip Market: By Country

Germany

France

Italy

UK

Russia

Rest of Europe

Europe Artificial Intelligence (AI) Chip Market: Companies Mentioned

Advanced Micro Devices, Inc.

Alphabet Inc. (Google)

Huawei Technologies Co., Ltd.

IBM Corporation

Intel Corporation

Micron Technology, Inc.

NVIDIA Corporation

Qualcomm Incorporated

Samsung Electronics Co., Ltd.

Xilinx, Inc.

About Us:

Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications

#Europe Artificial Intelligence (AI) Chip Market#Europe Artificial Intelligence (AI) Chip Market Size#Europe Artificial Intelligence (AI) Chip Market Share

0 notes

Text

RF Filter Market Strengthens in Asia-Pacific With Rising Electronics and Telecom Manufacturing Base

The RF (radio frequency) filter market has witnessed remarkable growth in recent years, driven by rapid advancements in wireless communication technologies, the expansion of 5G networks, and the increasing need for signal clarity in connected devices. RF filters, which are essential in allowing or blocking specific frequency ranges in electronic systems, play a vital role in minimizing interference and maintaining high-quality signal transmission across multiple communication bands.

At the heart of any modern wireless system, RF filters are critical in ensuring the efficient operation of devices ranging from smartphones and base stations to radar systems and satellite communications. These components selectively allow desired frequencies to pass through while rejecting unwanted signals, enabling cleaner transmission and reception.

One of the key drivers fueling the RF filter market is the rollout of 5G infrastructure. As global telecom providers continue to invest in 5G technology, the demand for high-performance filters has surged. Unlike previous generations of mobile technology, 5G requires operation across a broader spectrum, including sub-6 GHz and millimeter wave bands. This complexity necessitates the use of more advanced RF filters to manage increased signal density and prevent cross-channel interference.

Moreover, the growing trend of IoT (Internet of Things) devices and the proliferation of smart consumer electronics have added momentum to the RF filter market. From smart home systems to wearable gadgets and connected vehicles, these devices rely heavily on RF filters to ensure seamless and uninterrupted communication. As more devices connect to networks, the need for better signal isolation and integrity grows proportionally.

Another significant factor contributing to market expansion is the increased usage of RF filters in the aerospace and defense sectors. Military-grade communication systems, surveillance equipment, radar, and electronic warfare systems all depend on high-reliability RF filters that can withstand harsh environments and deliver consistent performance. Governments across various regions are investing heavily in defense modernization, further spurring demand in this segment.

In terms of technology, the RF filter market includes various types such as surface acoustic wave (SAW) filters, bulk acoustic wave (BAW) filters, and ceramic filters. SAW and BAW filters are among the most widely used, especially in mobile and wireless applications due to their compact size, high efficiency, and cost-effectiveness. SAW filters are typically used in lower frequency ranges, while BAW filters perform better at higher frequencies, making them particularly suitable for 5G applications.

Regionally, Asia-Pacific dominates the RF filter market due to the strong presence of consumer electronics manufacturers and mobile device production hubs, especially in countries like China, South Korea, and Japan. The region’s fast-growing telecommunications infrastructure and increasing smartphone penetration further boost market growth. North America and Europe also hold significant market shares, primarily due to their early adoption of advanced technologies and continued investments in defense and aerospace sectors.