#U.S. Machine Learning Market Size

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Kazakhstan’s Minister of Communications and Informatics has blocked the Tumblr site because it contained 60 sites of terrorism, extremism, and pornography in 2015.

Text

U.S. Machine Learning Market Size, Share | CAGR 37.2% During 2023-2030

The U.S. machine learning market share was valued at USD 4.74 billion in 2022 and is projected to grow from USD 6.49 billion in 2023 to USD 59.30 billion by 2030, at a CAGR of 37.2%. The U.S. Machine Learning (ML) market encompasses the development, deployment, and application of algorithms and statistical models that enable computer systems to perform tasks without explicit instructions, relying instead on patterns and inference. Machine Learning is a key subset of Artificial Intelligence (AI) and plays a vital role across a broad range of sectors, including healthcare, finance, retail, manufacturing, transportation, and government.

Market Scope:

Types of technology: supervised learning, unsupervised learning, reinforcement learning, deep learning, natural language processing (NLP), and neural networks.

Deployment Options: Cloud-hosted, local, and mixed solutions.

Applications: Predictive analysis, image and voice recognition, recommendation engines, fraud detection, robotic process automation, and self-operating systems.

Final Users: Businesses, research organizations, governmental bodies, and technology startups

Request for Free Sample Here: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/u-s-machine-learning-ml-market-107479

Key Players:

Amazon, Inc. (U.S.)

Fair Isaac Corporation (U.S.)

RapidMiner Inc. (U.S.)

Microsoft Corporation (U.S.)

H2O.ai (U.S.)

IBM Corporation (U.S.)

Oracle Corporation (U.S.)

Hewlett Packard Enterprise Company (U.S.)

Teradata (U.S.)

TIBCO Software Inc. (U.S.)

Key Development Industry:

June 2022– Teradata announced the integration of the Teradata Vantage multi-cloud data and analytics platform with Amazon SageMaker and its general availability. This initiative backs Teradata's Analytics 123 framework, providing organizations facing challenges with production-grade AI/ML projects a systematic method for expanding their analytical model implementation. October 2022 – IBM's artificial intelligence System-on-Chip (SoC) has been released to the public. The device is engineered to train and execute deep learning models much more efficiently and considerably quicker than CPUs. The SoC features 32 processing cores and contains 23 billion transistors, thanks to a 5 nm process node.

Market Trend:

Rising interest in explainable AI (XAI) and responsible ML practices.

Increased use of automated machine learning (AutoML) for non-experts.

Integration of ML with edge computing for real-time analytics.

Rapid adoption in healthcare, fintech, and cybersecurity domains.

Speak to Analyst: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/u-s-machine-learning-ml-market-107479

About Us:

At Fortune Business Insights, we empower businesses to thrive in rapidly evolving markets. Our comprehensive research solutions, customized services, and forward-thinking insights support organizations in overcoming disruption and unlocking transformational growth.

With deep industry focus, robust methodologies, and extensive global coverage, we deliver actionable market intelligence that drives strategic decision-making. Whether through syndicated reports, bespoke research, or hands-on consulting, our result-oriented team partners with clients to uncover opportunities and build the businesses of tomorrow.

We go beyond data offering clarity, confidence, and competitive edge in a complex world.

Contact Us:

US +1 833 909 2966

UK +44 808 502 0280

APAC +91 744 740 1245

Email: [email protected]

#U.S. Machine Learning Market Share#U.S. Machine Learning Market Size#U.S. Machine Learning Market Industry#U.S. Machine Learning Market Analysis#U.S. Machine Learning Market Driver#U.S. Machine Learning Market Research#U.S. Machine Learning Market Growth

0 notes

Text

How did COVID-19 accelerate demand for low-code development solutions globally

The Low Code Development Platform Market size was recorded at USD 22.80 Billion in 2023 and is expected to surpass USD 271.7 Billion by 2032, growing at a CAGR of 31.7% over the forecast period of 2024-2032.

The Low-Code Development Platform Market is rapidly redefining software creation, enabling organizations to build and deploy applications with unprecedented speed and efficiency. This transformative approach empowers both professional developers and "citizen developers" (non-technical business users) to collaborate seamlessly, bridging the traditional gap between business needs and IT capabilities. By minimizing manual coding and leveraging visual, drag-and-drop interfaces, low-code platforms are becoming indispensable tools for driving digital transformation across all industries.

U.S. PIONEERS RAPID ADOPTION AND INNOVATION IN LOW-CODE DEVELOPMENT

The Low-Code Development Platform Market is witnessing an exponential surge in adoption, fundamentally changing the landscape of application development. This growth is driven by the urgent need for businesses to innovate faster, respond agilely to market changes, and overcome the persistent shortage of skilled developers. Low-code platforms provide a powerful solution by democratizing software creation, allowing a broader range of individuals to contribute to the development process and accelerate the delivery of crucial business applications.

Get Sample Copy of This Report: https://www.snsinsider.com/sample-request/2877

Market Keyplayers:

Appian

LANSA

Pegasystems Inc.

AgilePoint

Oracle

Betty Blocks

Mendix Technology BV

Microsoft

OutSystems

Salesforce, Inc.

ServiceNow

Zoho Corporation Pvt. Ltd.

Quickbase

Creation

Market Analysis

The Low-Code Development Platform Market is experiencing robust growth, propelled by the increasing global demand for rapid application development and the widespread acceleration of digital transformation initiatives across various industries. This market's expansion is further fueled by the imperative for businesses to enhance operational efficiency, improve customer experience, and reduce development costs. Low-code platforms offer a compelling solution by simplifying complex coding tasks through intuitive visual interfaces and pre-built components, thereby empowering a wider range of users, including non-technical professionals, to contribute to software creation. Cloud-based deployments and the integration of advanced technologies like AI are also significant drivers of this market's upward trajectory.

Market Trends

Rise of Citizen Developers: Low-code platforms are empowering non-technical business users to develop applications, significantly reducing IT backlogs and accelerating innovation across departments.

Integration of AI and Automation: The incorporation of AI capabilities, including generative AI, machine learning, and intelligent automation, is enhancing the efficiency, accuracy, and sophistication of applications built with low-code.

Focus on Hybrid Development: Organizations are increasingly adopting a "fusion development" approach, combining low-code platforms with traditional coding to build more complex, enterprise-grade solutions.

Enhanced Security and Governance: Providers are continually improving built-in security features, compliance frameworks, and governance tools to address concerns related to data protection and regulatory adherence.

Scalability and Performance for Enterprise Applications: Low-code platforms are evolving to support the development of scalable, high-performance applications capable of handling complex enterprise-level demands.

Cloud-Native Adoption: A strong preference for cloud-based low-code solutions due to benefits such as rapid provisioning, operational efficiency, and enhanced security maturity.

Industry-Specific Solutions: A growing trend towards more specialized low-code platforms tailored to the unique needs and regulatory requirements of specific industries like healthcare, finance (BFSI), and manufacturing.

Seamless Data Integration: Continuous improvements in pre-built connectors and APIs facilitate effortless integration with existing enterprise systems (ERP, CRM) and third-party applications.

Market Scope

The reach of low-code development platforms is extensive, revolutionizing how businesses innovate and operate:

Accelerating Digital Transformation: Enabling companies to modernize legacy systems and build new digital capabilities with unparalleled speed.

Empowering Business Agility: Facilitating rapid response to market shifts and evolving customer demands through quick application iterations.

Boosting Developer Productivity: Streamlining routine tasks for professional developers, allowing them to focus on complex, high-value coding.

Democratizing Innovation: Allowing non-technical employees to develop custom applications, fostering a culture of innovation across the organization.

Optimizing Business Processes: Automating workflows and enhancing operational efficiency across various functions like HR, finance, and supply chain.

Enhancing Customer and Employee Experiences: Creating intuitive portals, mobile apps, and internal tools that improve engagement and productivity.

Low-code is proving to be a strategic asset for organizations aiming to achieve greater efficiency, adaptability, and competitive advantage in the digital age.

Forecast Outlook

The trajectory for the Low-Code Development Platform Market is undeniably steep, indicating a future where this technology will be foundational to enterprise IT strategies. The continuous evolution of platforms, marked by deeper integration with artificial intelligence and advanced automation, will further amplify their capabilities. As the demand for bespoke applications continues to outpace traditional development capacities, low-code solutions are positioned to become the primary engine for digital innovation. This ongoing shift will enable organizations to not only meet immediate business needs but also to proactively explore new opportunities, fostering an environment of continuous improvement and strategic agility.

Access Complete Report: https://www.snsinsider.com/reports/low-code-development-platform-market-2877

Conclusion

The Low-Code Development Platform Market is not just a trend; it represents a fundamental paradigm shift in how software is created and deployed. By making application development more accessible, efficient, and collaborative, low-code platforms are empowering organizations to accelerate their digital journeys and unlock new levels of innovation. This technology is crucial for businesses aiming to thrive in an increasingly competitive and dynamic landscape, allowing them to rapidly build solutions that address evolving market demands and optimize internal operations. Embracing low-code is no longer an option but a strategic imperative for any enterprise seeking to maintain agility, reduce costs, and foster a truly innovative culture.

About Us:

SNS Insider is one of the leading market research and consulting agencies that dominates the market research industry globally. Our company's aim is to give clients the knowledge they require in order to function in changing circumstances. In order to give you current, accurate market data, consumer insights, and opinions so that you can make decisions with confidence, we employ a variety of techniques, including surveys, video talks, and focus groups around the world.

Related Reports:

U.S.A. Geospatial Analytics Market Gains Momentum with Tech-Driven Insights

U.S.A witnesses rising momentum in Synthetic Data Generation Market as demand for data privacy solutions grows

U.S.A gears up for AI revolution with booming Self-supervised Learning Market

Contact Us:

Jagney Dave - Vice President of Client Engagement

Phone: +1-315 636 4242 (US) | +44- 20 3290 5010 (UK)

Mail us: [email protected]

#Low Code Development Platform Market#Low Code Development Platform Market Scope#Low Code Development Platform Market Trends

0 notes

Text

Market Sees Growth in Cloud-Based Genomic Data Platforms

The Genomics in Cancer Care Market reached USD 13.4 billion in 2022 and is projected to grow to USD 51.1 billion by 2031, exhibiting a CAGR of 18.9% during the forecast period 2024–2031, driven by the growing role of precision medicine and targeted therapies in oncology. Genomic testing helps identify cancer-causing mutations, such as BRCA1 and BRCA2, enabling accurate diagnosis, prognosis, and treatment selection. By uncovering genetic changes in cancer cells, genomics supports the development of more effective, individualized therapies that significantly improve patient outcomes and survival rates.

Unlock exclusive insights with our detailed sample report :

Key Market Drivers

1. Rising Global Cancer Prevalence

According to WHO, cancer is a leading cause of death globally, with over 20 million new cases expected annually by 2030. This has created a demand for advanced genomic tools that facilitate early detection and personalized treatment strategies.

2. Advances in NGS and Genomic Sequencing

Technological breakthroughs in whole genome sequencing (WGS), targeted gene panels, and RNA sequencing are enhancing the ability to identify key mutations and develop tailored therapeutic approaches.

3. Shift Toward Precision Oncology

The era of one-size-fits-all cancer treatment is fading. Genomic testing enables oncologists to match therapies based on individual molecular profiles, increasing treatment success rates and reducing adverse effects.

4. Integration of AI and Machine Learning

AI-driven platforms are accelerating genomic data interpretation, assisting in variant classification, biomarker discovery, and real-time decision-making for clinicians and researchers.

5. Government and Industry Investments

Public and private investments are growing rapidly. For example:

The U.S. Cancer Moonshot initiative continues to support genomic cancer research.

Japan’s Genomic Medicine Plan is focused on nationwide whole-genome sequencing efforts and biomarker development.

Regional Highlights

United States

The U.S. is at the forefront of genomic integration in cancer care, with extensive use of NGS panels, companion diagnostics, and cloud-based genomic tools.

Leading institutions like Memorial Sloan Kettering and MD Anderson partner with biotech firms for tumor sequencing projects.

The FDA has increased approval of genomic-based cancer therapies and companion diagnostics, ensuring regulatory clarity and accelerating innovation.

Japan

Japan is heavily investing in aging-focused cancer genomics as over 28% of its population is aged 65 or above.

National cancer programs promote biobank development, data-sharing frameworks, and personalized therapeutic protocols.

Hospitals are piloting AI-integrated genomic dashboards to aid clinical decision-making for oncologists.

Speak to Our Senior Analyst and Get Customization in the report as per your requirements:

Key Segments

By Technology:

Next-Generation Sequencing (NGS)

PCR (Polymerase Chain Reaction)

Microarrays

Sanger Sequencing

By Application:

Diagnostics

Drug Discovery and Development

Prognostics and Screening

Companion Diagnostics

By Cancer Type:

Breast Cancer

Lung Cancer

Colorectal Cancer

Prostate Cancer

Others (Melanoma, Leukemia, etc.)

By End-User:

Hospitals & Clinics

Academic & Research Institutes

Biotech & Pharma Companies

Diagnostic Labs

Recent Industry Developments

Thermo Fisher Scientific launched an expanded NGS panel approved for solid tumors, improving turnaround times and reducing costs in hospitals.

Roche and Foundation Medicine extended collaboration to develop comprehensive genomic profiling (CGP) solutions for rare cancers.

Illumina and AstraZeneca announced a joint platform that integrates genomic sequencing with drug development, accelerating targeted therapy pipelines.

Japan’s National Cancer Center began a trial for population-level cancer genome screening, a first in Asia-Pacific’s clinical genomics ecosystem.

The NIH’s All of Us Research Program now includes cancer patients in its longitudinal genomic dataset, broadening ethnic and genetic diversity.

Buy the exclusive full report here:

Growth Opportunities

Expansion of Liquid Biopsy Testing: Non-invasive blood-based genomic testing is opening doors for real-time tumor monitoring and minimal residual disease detection.

Development of Multi-Cancer Early Detection (MCED) Tests: These tests use genomic signals to detect various cancer types at once, revolutionizing preventive oncology.

Decentralized Genomic Testing Platforms: The adoption of cloud and edge computing in diagnostics supports genomic data analysis even in smaller hospitals.

Increasing Partnerships with Pharma: Biopharma companies seek genomic data insights to design better trials, improving drug response and reducing trial failure rates.

Personalized Cancer Vaccines: Genomics is paving the way for neoantigen-based immunotherapies, which are now entering clinical trials globally.

Challenges and Considerations

High Costs of Sequencing: Despite decreasing, comprehensive genomic profiling remains expensive and is not uniformly reimbursed.

Data Privacy Concerns: Handling of sensitive genomic data raises questions around patient consent, security, and ownership.

Skill Gaps in Data Interpretation: Many healthcare providers still lack the training required to interpret complex genomic reports accurately.

Leading Market Players

Illumina, Inc.

Thermo Fisher Scientific

Agilent Technologies

Roche Diagnostics

Bio-Rad Laboratories

Qiagen N.V.

Foundation Medicine

Guardant Health

Fujifilm Holdings Corp. (Japan)

These companies are:

Launching multi-cancer panels

Building AI-enabled interpretation platforms

Partnering with governments and hospitals for clinical validation

Focusing on affordability and access in underserved regions

Stay informed with the latest industry insights-start your subscription now:

Conclusion

The genomics in cancer care market is not just expanding—it’s transforming the very fabric of oncology. From tumor characterization to tailored therapies, genomics is enabling a future where cancer care is not only more effective but also more humane and precise.

With growing government support, rapid adoption of AI tools, and unprecedented collaboration between diagnostics and therapeutics, the global healthcare ecosystem is on the brink of genomic-enabled cancer care at scale.

The next decade will not just be about treating cancer—but about predicting, preventing, and personalizing the battle against it.

About us:

DataM Intelligence is a premier provider of market research and consulting services, offering a full spectrum of business intelligence solutions—from foundational research to strategic consulting. We utilize proprietary trends, insights, and developments to equip our clients with fast, informed, and effective decision-making tools.

Our research repository comprises more than 6,300 detailed reports covering over 40 industries, serving the evolving research demands of 200+ companies in 50+ countries. Whether through syndicated studies or customized research, our robust methodologies ensure precise, actionable intelligence tailored to your business landscape.

Contact US:

Company Name: DataM Intelligence

Contact Person: Sai Kiran

Email: [email protected]

Phone: +1 877 441 4866

Website: https://www.datamintelligence.com

#Genomics in Cancer Care Market#Genomics in Cancer Care Market size#Genomics in Cancer Care Market growth#Genomics in Cancer Care Market share#Genomics in Cancer Care Market analysis

0 notes

Text

Video Surveillance Hardware System Market: Strategic Developments and Forecast 2025–2032

MARKET INSIGHTS

The global Video Surveillance Hardware System Market size was valued at US$ 23.8 billion in 2024 and is projected to reach US$ 45.6 billion by 2032, at a CAGR of 8.5% during the forecast period 2025-2032. The U.S. market was estimated at USD 14.7 billion in 2024, while China is expected to grow to USD 22.1 billion by 2032.

Video surveillance hardware systems comprise essential components like cameras, storage devices, and monitors that work together to capture, store, and display security footage. These systems have evolved significantly from analog CCTV to advanced IP-based solutions featuring high-definition imaging, AI-powered analytics, and cloud connectivity. The camera segment alone is projected to reach USD 52.8 billion by 2032, growing at 9.1% CAGR.

Market growth is driven by rising security concerns across commercial and residential sectors, government mandates for public safety infrastructure, and technological advancements in AI-based surveillance. Recent developments include Axis Communications’ 2024 launch of thermal cameras with onboard analytics and Hikvision’s partnership with Microsoft to integrate Azure AI into their surveillance ecosystem. Leading players like Bosch Security Systems, Hanwha Techwin, and Avigilon continue to dominate the competitive landscape through innovation in edge computing and 5G-enabled devices.

MARKET DYNAMICS

MARKET DRIVERS

Rising Security Concerns and Crime Rates to Accelerate Video Surveillance Adoption

Global security threats and increasing crime rates are driving significant investments in video surveillance infrastructure. The global security equipment market continues to expand as organizations prioritize asset protection and public safety. Video surveillance systems offer proactive monitoring capabilities that deter criminal activities while providing crucial forensic evidence. Industrial facilities, transportation hubs, and government institutions are particularly investing in advanced surveillance to mitigate risks. This trend is further intensified by geopolitical tensions and the growing need for border security worldwide.

Technological Advancements in AI-Powered Video Analytics to Fuel Market Growth

The integration of artificial intelligence with surveillance hardware is transforming traditional monitoring systems into intelligent security solutions. Modern surveillance cameras now incorporate advanced features such as facial recognition, license plate detection, and behavioral analysis through machine learning algorithms. Edge computing capabilities enable real-time processing directly on cameras, reducing bandwidth requirements while improving response times. These innovations significantly enhance threat detection accuracy and operational efficiency across various sectors.

Moreover, the emergence of 5G networks facilitates high-speed data transmission, enabling more sophisticated remote monitoring applications. Cloud-based video surveillance solutions offer scalable storage and analytics, further driving adoption among SMEs and large enterprises alike.

Government Regulations and Smart City Initiatives to Drive Market Expansion

Governments worldwide are implementing stringent security regulations and investing heavily in smart city projects, creating substantial demand for surveillance hardware. Many countries now mandate video surveillance in public spaces, commercial buildings, and transportation systems. The allocation of substantial budgets for urban security infrastructure demonstrates the strategic importance of surveillance technology in modern governance and public safety management.

➤ For instance, several metropolitan cities have deployed thousands of surveillance cameras as part of comprehensive safe city programs, often integrating them with centralized command centers.

MARKET RESTRAINTS

High Installation and Maintenance Costs to Limit Market Penetration

While surveillance technology offers significant benefits, the substantial capital expenditure required for system deployment poses a major barrier, particularly for small businesses and developing regions. High-quality surveillance hardware demands significant upfront investment, with additional costs for installation, integration, and ongoing maintenance. The total cost of ownership extends beyond equipment to include network infrastructure, storage solutions, and software licensing fees.

Other Restraints

Data Privacy Regulations Stringent data protection laws in various regions create compliance challenges for surveillance system operators. Privacy concerns have led to restrictions on video recording in certain areas, requiring businesses to navigate complex legal frameworks when deploying surveillance solutions.

Cybersecurity Vulnerabilities The increasing connectivity of surveillance equipment exposes systems to potential cyber threats, deterring some organizations from adoption. Networked cameras and connected devices can become entry points for security breaches if not properly secured.

MARKET CHALLENGES

Integration Complexities with Legacy Systems to Pose Implementation Challenges

Many organizations face technical difficulties when upgrading or expanding existing surveillance infrastructure. Compatibility issues between new hardware and older systems often require additional investments in interfaces or complete system replacements. The migration to IP-based solutions from analog systems presents particular challenges in terms of network readiness and staff training.

Other Challenges

Storage Management The exponential growth in video data volume creates storage capacity and management challenges, requiring innovative compression technologies and efficient data retention policies.

False Alarm Rates Advanced analytics systems sometimes generate false alerts due to environmental factors or algorithm limitations, potentially reducing operational efficiency and user confidence.

MARKET OPPORTUNITIES

Expansion of IoT and Edge Computing to Create New Growth Avenues

The convergence of surveillance technology with IoT ecosystems presents significant opportunities for market players. Smart sensors and edge devices enable more distributed and intelligent security architectures. The ability to process video data locally reduces bandwidth requirements while enabling faster response times—particularly valuable for time-sensitive applications.

Emerging Applications in Retail Analytics and Business Intelligence

Beyond security, video surveillance hardware is finding new applications in customer behavior analysis and operational optimization. Retailers leverage advanced camera systems to track foot traffic, analyze shopping patterns, and measure promotional effectiveness. These commercial applications represent a growing revenue stream for surveillance solution providers.

The development of specialized surveillance solutions for vertical markets such as healthcare, education, and manufacturing continues to expand the addressable market for hardware vendors. Customized systems designed for specific industry requirements demonstrate strong growth potential.

VIDEO SURVEILLANCE HARDWARE SYSTEM MARKET TRENDS

AI-Powered Video Analytics Driving Smart Surveillance Adoption

The integration of artificial intelligence (AI) and machine learning (ML) into video surveillance hardware represents one of the most transformative trends in the security industry. Advanced analytics capabilities now enable real-time object detection, facial recognition, and behavioral pattern analysis, significantly enhancing threat detection accuracy. The global market for AI-based surveillance cameras is projected to grow at a CAGR of approximately 22% from 2024 to 2032 as enterprises and governments increasingly adopt these solutions. Edge computing has further accelerated this trend by allowing cameras to process data locally, reducing bandwidth requirements while improving response times for critical security events.

Other Trends

Shift Toward IP-Based Network Cameras

The transition from analog CCTV to IP-based network cameras continues to reshape the surveillance hardware landscape, with IP cameras expected to account for over 75% of total installations by 2026. This shift is driven by superior resolution capabilities (4K and beyond), easier integration with cloud platforms, and enhanced cybersecurity features. The industrial sector shows particularly strong adoption rates, with manufacturers leveraging networked surveillance for both security and operational monitoring purposes. Meanwhile, thermal imaging cameras are gaining traction in perimeter security applications, demonstrating annual growth rates exceeding 18%.

Cloud-Based Video Surveillance Gaining Momentum

Cloud-managed video surveillance systems are experiencing rapid adoption as organizations seek scalable, maintenance-free security solutions. These systems eliminate the need for on-premise servers while offering remote accessibility through web and mobile interfaces. The healthcare and education verticals are leading this transition, with cloud deployments growing at approximately 27% year-over-year. Cybersecurity remains a critical consideration, prompting hardware manufacturers to embed end-to-end encryption and multi-factor authentication directly into cameras and storage devices. Hybrid cloud/on-premise solutions currently dominate enterprise implementations, balancing data control requirements with operational flexibility.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Expand AI and Cloud-Based Solutions to Gain Competitive Edge

The global video surveillance hardware system market features a dynamic competitive landscape, blending established security technology giants with agile innovators. Axis Communications maintains a dominant position, credited to its pioneering work in network cameras and intelligent analytics, holding approximately 18% revenue share in 2024. The company’s strength lies in its end-to-end solutions spanning cameras, recording devices, and AI-powered video management software.

Close competitors Hikvision and Dahua Technology have significantly increased their market penetration through aggressive pricing strategies and government contracts, particularly in the Asia-Pacific region. These Chinese manufacturers now collectively account for nearly 30% of global shipments, leveraging China’s robust electronics manufacturing ecosystem and government-led Smart City initiatives.

The market has seen intensified competition following strategic acquisitions, with notable examples including Motorola’s purchase of Avigilon and Teledyne’s acquisition of FLIR. These moves have created integrated solution providers capable of combining thermal imaging, AI analytics, and traditional surveillance hardware into comprehensive security packages.

Emerging players like Verkada and Rhombus Systems are disrupting the market through cloud-native architectures, challenging traditional on-premise solutions. These companies recorded triple-digit growth rates from 2022-2024 by targeting the mid-market segment with subscription-based models and simplified deployments.

List of Key Video Surveillance Hardware Companies Profiled

Axis Communications (Sweden)

Bosch Security and Safety Systems (Germany)

Hanwha Techwin (South Korea)

Avigilon (Canada)

Teledyne FLIR (U.S.)

Honeywell International (U.S.)

Panasonic i-PRO Sensing Solutions (Japan)

Hikvision (China)

Dahua Technology (China)

Verkada (U.S.)

Genetec (Canada)

NEC Corporation (Japan)

Segment Analysis:

By Type

Camera Segment Dominates with Rising Demand for High-Resolution and AI-Enabled Surveillance Systems

The market is segmented based on type into:

Camera

Subtypes: Analog, IP, Thermal, PTZ, and others

Storage Device

Subtypes: NVR, DVR, and cloud-based storage

Monitor

Subtypes: LCD, LED, and OLED displays

Accessories

Subtypes: Mounting brackets, cables, enclosures, and others

By Application

Government Sector Leads Owing to Increased Security Spending on Public Safety Infrastructure

The market is segmented based on application into:

Government

Sub-applications: City surveillance, critical infrastructure protection, and border control

Industrial

Sub-applications: Factory monitoring, warehouse security, and remote site surveillance

Transport

Sub-applications: Traffic monitoring, vehicle surveillance, and smart parking

Commercial

Sub-applications: Retail stores, office buildings, and hospitality facilities

Residential

Sub-applications: Smart homes, apartment complexes, and gated communities

By Technology

IP-Based Surveillance Gains Traction Due to Network Connectivity Advantages

The market is segmented based on technology into:

Analog CCTV

IP-Based Surveillance

AI-Enabled Surveillance

Cloud-Based Surveillance

Regional Analysis: Video Surveillance Hardware System Market

North America The North American market is characterized by high adoption rates of advanced surveillance technologies, driven by stringent security regulations and increasing investment in smart city initiatives. The U.S. Department of Homeland Security has been actively promoting the use of AI-powered surveillance systems for critical infrastructure protection. Major players like Avigilon and Verkada have established strong footholds, providing integrated solutions with edge analytics capabilities. While analog systems are being phased out, the transition to IP-based and cloud-connected surveillance is accelerating. Data privacy concerns, however, remain a key challenge, particularly with increasing scrutiny on facial recognition technologies.

Europe Europe’s market is shaped by strict GDPR compliance requirements and a growing emphasis on cybersecurity in video surveillance systems. The region shows strong preference for hybrid solutions that combine local storage with cloud backup capabilities to meet data sovereignty rules. Countries like Germany and the UK are leading in adopting AI-based video analytics for traffic monitoring and retail customer behavior analysis. Recent terrorist threats have spurred additional public sector investments, though debates about surveillance ethics continue to influence procurement policies. Thermal cameras for fever detection have gained traction post-pandemic, particularly in transportation hubs.

Asia-Pacific As the fastest growing region, Asia-Pacific benefits from massive urbanization projects and government-led safe city programs. China dominates both as a manufacturing hub and end-user market, with Hikvision and Dahua capturing significant market share. India’s Smart Cities Mission has spurred deployment of over 1 million surveillance cameras nationwide, while Southeast Asian countries are upgrading coastal surveillance systems. However, price sensitivity remains high, driving demand for cost-effective solutions over premium features. The region also sees rapid adoption of 5G-connected cameras for real-time monitoring in dense urban environments.

South America Market growth in South America has been uneven, with Brazil and Chile showing more stable investments in surveillance infrastructure compared to economically volatile nations. Retail and banking sectors represent key demand drivers, though public sector projects frequently face funding delays. Chinese manufacturers have gained prominence by offering competitive pricing, while local players focus on customized solutions for specific verticals like mining and oil facilities. Power reliability issues continue to hinder system uptime, creating opportunities for solar-powered surveillance solutions in remote areas.

Middle East & Africa The Middle East leads regional adoption through massive smart city developments like NEOM in Saudi Arabia and Expo 2020 Dubai infrastructure projects. Gulf countries particularly favor high-end thermal and panoramic camera systems for border security applications. In Africa, South Africa remains the most mature market, while East African nations are investing in surveillance for port security and anti-poaching initiatives. Political instability in some regions creates demand for ruggedized systems, though budget constraints often limit deployments to essential infrastructure only. The lack of technical expertise continues to drive demand for managed surveillance services across the continent.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Video Surveillance Hardware System markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 50.2 billion in 2024 and is projected to reach USD 89.7 billion by 2032.

Segmentation Analysis: Detailed breakdown by product type (cameras, storage devices, monitors), technology (IP-based, analog), application (government, industrial, transport), and end-user industry.

Regional Outlook: Insights into market performance across North America (36% market share), Europe (28%), Asia-Pacific (fastest growing at 9.2% CAGR), Latin America, and the Middle East & Africa.

Competitive Landscape: Profiles of 25+ leading market participants including Axis Communications (12% market share), Hikvision (18%), and Bosch Security Systems (8%), covering product portfolios and strategic developments.

Technology Trends & Innovation: Assessment of AI-powered analytics (adopted by 42% of new installations in 2024), 4K/8K resolution, cloud-based solutions, and thermal imaging technologies.

Market Drivers & Restraints: Evaluation of factors including rising security concerns (45% of enterprises increased budgets in 2024), smart city initiatives (USD 1.2 trillion global investment by 2030), and data privacy regulations.

Stakeholder Analysis: Insights for component manufacturers, system integrators, and government agencies regarding the USD 12.5 billion VMS software market opportunity.

Related Reports:https://semiconductorblogs21.blogspot.com/2025/06/inductive-proximity-switches-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/cellular-iot-module-chipset-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/sine-wave-inverter-market-shifts-in.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/pilot-air-control-valves-market-cost.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/video-multiplexer-market-role-in.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/semiconductor-packaging-capillary.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/screw-in-circuit-board-connector-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/wafer-carrier-tray-market-integration.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/digital-display-potentiometer-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/glass-encapsulated-ntc-thermistor.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/shafted-hall-effect-sensors-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/point-of-load-power-chip-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/x-ray-grating-market-key-players-and.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/picmg-single-board-computer-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/lighting-control-dimming-panel-market.html

0 notes

Text

AI Platform Cloud Service Market Size, Share & Growth Analysis 2034: Accelerating the Future of Intelligent Computing

AI Platform Cloud Service Market is evolving at a rapid pace, fueled by the growing need for scalable, cost-efficient, and intelligent digital solutions. These platforms provide a comprehensive cloud-based infrastructure, enabling the development, deployment, and management of AI applications across industries.

With components like machine learning, data storage, and integrated development environments, the market is empowering organizations to accelerate innovation and streamline decision-making processes. As of 2024, the market has shown exceptional momentum, reaching a volume of 320 million metric tons and projected to grow at a remarkable CAGR of 22% through 2034. Increasing demand for AI-driven automation and real-time data analytics is reshaping how businesses operate, making AI platforms an indispensable asset.

Click to Request a Sample of this Report for Additional Market Insights: https://www.globalinsightservices.com/request-sample/?id=GIS23260

Market Dynamics

The primary driver behind the AI Platform Cloud Service Market is the seamless integration of AI with cloud computing. This combination allows companies to leverage powerful AI tools without investing heavily in on-premises infrastructure. Demand for real-time predictive analytics, intelligent automation, and personalized services is pushing enterprises toward cloud-based AI platforms. However, challenges such as data privacy concerns, high implementation costs, and a shortage of AI-skilled professionals continue to restrict market expansion. Despite these hurdles, technological advancements in deep learning, NLP, and robotic process automation are opening up new frontiers for market growth.

Key Players Analysis

The competitive landscape is dominated by tech giants such as Microsoft Azure, Amazon Web Services (AWS), and Google Cloud Platform, all of whom offer robust AI capabilities and global cloud infrastructure. These players invest heavily in R&D and regularly enhance their platforms to support evolving AI needs. Alongside them, innovative firms like C3.ai, DataRobot, and H2O.ai are making significant strides by offering niche, specialized AI services. Emerging startups like Cognify Labs, Quantum Leap Technologies, and Neura Cloud Innovations are contributing fresh perspectives and driving disruption with agile, cutting-edge platforms tailored to specific industries and use cases.

Regional Analysis

North America leads the AI Platform Cloud Service Market, thanks to its advanced tech infrastructure and strong R&D investment, particularly in the U.S., where companies are aggressively adopting AI for digital transformation. Europe is also showing robust growth, with nations like Germany, the UK, and France making AI central to their industrial and healthcare strategies. The Asia-Pacific region is rapidly catching up, bolstered by government initiatives and digital transformation efforts in China, India, and Japan. Meanwhile, countries in the Middle East & Africa, including the UAE and Saudi Arabia, are making notable progress in adopting AI solutions to power smart cities and digital governance.

Recent News & Developments

Recent developments have significantly influenced the AI Platform Cloud Service Market. Major providers are adopting competitive pricing models, ranging from $100 to $500 per service, to cater to a broad spectrum of users — from startups to large enterprises. Strategic collaborations and acquisitions are on the rise, as players seek to enhance their offerings and broaden their global footprint. Companies are also prioritizing sustainability, focusing on energy-efficient data centers to align with global environmental goals. Simultaneously, evolving regulations around data privacy and cybersecurity are reshaping operational strategies, compelling providers to enhance compliance frameworks and data governance practices.

Browse Full Report : https://www.globalinsightservices.com/reports/ai-platform-cloud-service-market/

Scope of the Report

This report offers comprehensive insights into the AI Platform Cloud Service Market, covering all critical aspects from market size and forecasts to competitive landscape and regulatory impact. It analyzes key market segments such as public, private, and hybrid cloud deployments, along with a diverse array of AI applications including fraud detection, customer service, and supply chain optimization. The report also examines technological frameworks — ranging from machine learning and speech recognition to computer vision — and evaluates their relevance across verticals such as BFSI, retail, healthcare, telecom, and education. By identifying challenges, growth drivers, and emerging opportunities, the report equips stakeholders with the intelligence necessary for strategic decision-making in a rapidly transforming digital landscape.

#aiincloud #cloudai #aiplatforms #machinelearning #artificialintelligence #cloudcomputing #digitaltransformation #predictiveanalytics #aitechnology #cloudsolutions

Discover Additional Market Insights from Global Insight Services:

Cloud Based Contact Center Market : https://www.globalinsightservices.com/reports/cloud-based-contact-center-market/

Digital Content Creation Market : https://www.globalinsightservices.com/reports/digital-content-creation-market/

Field Service Management Market ; https://www.globalinsightservices.com/reports/field-service-management-market/

Regulatory Risk Management Market : https://www.globalinsightservices.com/reports/regulatory-risk-management-market/

Speech Analytics Market ; https://www.globalinsightservices.com/reports/speech-analytics-market/

About Us:

Global Insight Services (GIS) is a leading multi-industry market research firm headquartered in Delaware, US. We are committed to providing our clients with highest quality data, analysis, and tools to meet all their market research needs. With GIS, you can be assured of the quality of the deliverables, robust & transparent research methodology, and superior service.

Contact Us:

Global Insight Services LLC 16192, Coastal Highway, Lewes DE 19958 E-mail: [email protected] Phone: +1–833–761–1700 Website: https://www.globalinsightservices.com/

0 notes

Text

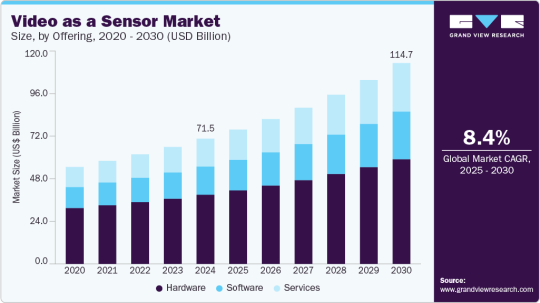

The Future of Analytics: How Video As A Sensor is Redefining Data Capture

The global Video As A Sensor Market, estimated at USD 71.50 billion in 2024, is forecast to reach USD 114,664.7 million by 2030, exhibiting a Compound Annual Growth Rate (CAGR) of 8.4% from 2025 to 2030. This growth is propelled by rapid technological advancements that have transformed conventional video systems and recording tools into sophisticated, intelligent decision-making instruments.

A significant catalyst for VaaS adoption is the technology's capacity to deliver real-time insights, including capabilities like facial recognition, anomaly detection, and behavior prediction. These features render VaaS highly suitable for contemporary security and surveillance systems, where prompt threat identification is crucial. Beyond security applications, the versatility of video sensors is increasingly evident across various sectors. In smart city initiatives, they play a vital role in enhancing urban infrastructure, contributing to public safety, optimizing energy consumption, and improving waste management efforts.

Key Market Trends & Insights:

North American Dominance: North America led the market with a 35.5% share in 2024. This leadership is driven by substantial investments in advanced surveillance systems and the early adoption of cutting-edge technologies such as Artificial Intelligence (AI) and machine learning.

U.S. Market Expansion: The video as a sensor market in the U.S. is experiencing notable growth, corresponding with increasing regional demand. The accelerating pace of industrialization and the integration of advanced technologies are key factors driving this market's expansion.

Video Surveillance Product Leadership: By product type, video surveillance accounted for the largest market revenue share in 2024. This segment's dominance is primarily due to escalating security concerns across residential, commercial, and public domains, coupled with rapid advancements in technologies like AI-driven analytics, cloud computing, and high-resolution imaging.

Security & Surveillance Application Dominance: In terms of application, the security and surveillance segment held the largest market revenue share in 2024. This is attributed to VaaS's ability to automate real-time threat detection, significantly reduce false alarms, and efficiently manage large volumes of video footage, thereby lessening the workload on security personnel.

Commercial End-Use Sector Growth: The commercial segment accounted for the largest market revenue share in 2024. This is driven by the growing need for enhanced security and surveillance solutions in commercial environments, including office buildings and retail establishments, to protect assets and ensure safety.

Order a free sample PDF of the Video As A Sensor Market Intelligence Study, published by Grand View Research.

Market Size & Forecast

2024 Market Size: USD 71.50 Billion

2030 Projected Market Size: USD 114,664.7 Million

CAGR (2025-2030): 8.4%

North America: Largest market in 2024

Asia Pacific: Fastest growing market

Key Companies & Market Share Insights

Leading firms in the Video As A Sensor (VaaS) market are employing a range of strategic initiatives to expand their market presence. These primarily include product launches and developments, alongside expansions, mergers and acquisitions, contracts, agreements, partnerships, and collaborations. Companies are leveraging diverse techniques to enhance market penetration and strengthen their competitive standing.

Axis Communications, a prominent player, specializes in network video surveillance and intelligent security solutions. Their comprehensive offerings, including a wide array of cameras, video management software, analytics, and access control systems, enable businesses and smart cities to utilize video as a sensor for real-time insights, improved safety, and enhanced operational efficiency. Axis's commitment to innovation, sustainability, and fostering a robust partner ecosystem underpins their goal of contributing to a smarter and safer global environment.

Hikvision is a significant force in video-centric IoT solutions, with a strong focus on advanced video-as-a-sensor technologies for both security and intelligent monitoring. By integrating state-of-the-art AI, deep learning, and high-performance video analytics, Hikvision delivers real-time surveillance, environmental sensing, and actionable insights. Their solutions are deployed across various sectors globally, including smart cities, transportation systems, and commercial enterprises.

Key Players

Axis Communications AB

Hangzhou Hikvision Digital Technology Co., Ltd.

Bosch Sicherheits systeme GmbH

Dahua Technology Co., Ltd.

Sony Corporation

Honeywell International Inc.

Sportradar AG

i-PRO

Johnson Controls

OMNIVISION

Browse Horizon Databook for Global Video As A Sensor Market Size & Outlook

Conclusion

The global Video As A Sensor (VaaS) market is experiencing rapid growth, driven by technological advancements transforming video into intelligent decision-making tools. Its ability to provide real-time insights makes it crucial for security, surveillance, and smart city initiatives. North America leads the market, with video surveillance and security applications dominating across commercial sectors. Leading companies are strategically innovating and collaborating to further expand their market share in this dynamic industry.

0 notes

Text

Glucose Sensors Market: A Comprehensive Global Overview and Future Outlook

Introduction

The Glucose Sensors Market is at the forefront of innovation in the global healthcare landscape, particularly in the management of diabetes—a chronic condition affecting over 500 million people worldwide. With increasing emphasis on early diagnosis, real-time monitoring, and patient-centered care, glucose sensors have evolved from traditional finger-prick devices to advanced wearable and continuous monitoring systems. This article presents a global overview of the glucose sensors market, analyzing current dynamics, key regions, technological shifts, and future outlook.

Market Overview

Glucose sensors are critical components in glucose monitoring devices that measure blood sugar levels. These sensors are utilized in:

Continuous Glucose Monitoring (CGM) Systems

Flash Glucose Monitoring (FGM) Devices

Traditional Blood Glucose Meters

Non-invasive and Minimally Invasive Devices

As the prevalence of diabetes continues to rise—particularly Type 2 diabetes—there’s a growing need for accurate, real-time, and user-friendly monitoring solutions.

Current Market Size and Growth Trajectory

As of 2024, the global Glucose Sensors Market is valued at over USD 12 billion and is expected to reach USD 25 billion by 2030, growing at a compound annual growth rate (CAGR) of 10–12%. This rapid expansion is being driven by:

Increasing diabetic population

Growing awareness and adoption of preventive healthcare

Technological advancements in sensor design

Expanding insurance coverage and reimbursement support in developed countries

Key Regional Insights

1. North America

Largest market share, dominated by the U.S.

Strong presence of top players like Dexcom, Abbott, and Medtronic

High adoption of CGM devices among Type 1 diabetics

Robust insurance infrastructure and supportive FDA pathways

2. Europe

Strong growth in countries like Germany, UK, and France

Growing elderly population and national diabetes screening programs

Emphasis on digital health integration in public healthcare systems

3. Asia-Pacific

Fastest-growing region due to increasing diabetic prevalence in China, India, and Japan

Rise in middle-class income, digital literacy, and wearable adoption

Government health campaigns encouraging early screening and remote care

4. Latin America, Middle East & Africa

Emerging opportunities driven by urbanization and changing lifestyles

Limited penetration of advanced glucose monitoring technologies

Potential for growth through public-private partnerships and mobile health solutions

Market Segmentation

The Glucose Sensors Market can be segmented based on:

Technology: Enzymatic sensors, optical sensors, electrochemical sensors

Type: Continuous sensors, strip-based sensors, non-invasive sensors

End-User: Hospitals, clinics, home care settings, fitness & wellness centers

Distribution Channel: Retail pharmacies, online platforms, direct medical device sales

Key Industry Drivers

Rising Diabetes Prevalence

The global diabetic population is expected to surpass 643 million by 2030.

Increasing obesity and sedentary lifestyles are accelerating Type 2 diabetes cases.

Preference for Continuous and Real-Time Monitoring

CGMs offer better glucose trend data, helping reduce hypoglycemic episodes.

Real-time data enables personalized treatment adjustments.

Technological Advancements

Use of AI, machine learning, and cloud-based platforms

Sensors with longer lifespan, smaller sizes, and enhanced accuracy

Non-invasive solutions under development (e.g., via sweat or interstitial fluids)

Shift Toward Preventive Healthcare

Early detection and management of pre-diabetes using wearable sensors

Integration of glucose tracking into smartwatches and fitness devices

Challenges and Restraints

Despite rapid growth, the glucose sensors market faces several challenges:

High cost of advanced devices like CGMs in low-income regions

Accuracy and calibration issues, especially in non-invasive sensors

Lack of awareness among newly diagnosed patients

Limited insurance coverage in some emerging markets

Competitive Landscape

The Glucose Sensors Market is highly competitive and led by both established players and startups:

Abbott Laboratories – Leader with FreeStyle Libre systems

Dexcom, Inc. – Pioneer in real-time CGM technology

Medtronic plc – Innovator in sensor-integrated insulin pumps

Senseonics – Known for implantable CGM solutions (Eversense)

New Entrants – Apple, Samsung, and various healthtech startups are investing in non-invasive glucose sensing technologies integrated into wearables

Strategic collaborations, FDA approvals, and R&D investments are key areas of focus for companies aiming to gain a competitive edge.

Future Outlook

The next five years will be defined by:

Integration with AI and predictive analytics for proactive diabetes management

Expansion of non-invasive glucose sensors targeting fitness and wellness markets

Growing emphasis on personalized care, with data-driven therapy planning

Remote monitoring capabilities tied to telemedicine platforms

Regulatory innovation, expediting approval and reimbursement pathways

Conclusion

The Glucose Sensors Market is undergoing a transformative shift—from basic glucose tracking to comprehensive, connected, and user-friendly healthcare solutions. With continued innovation, market expansion in emerging economies, and increasing consumer awareness, the industry is poised for sustained growth and technological disruption. Stakeholders that prioritize accessibility, affordability, and data integration will lead the next wave of advancements in this critical segment of diabetes care.

0 notes

Text

How AI-Powered Analytics Is Transforming Healthcare in 2025

In healthcare, seconds save lives. Imagine AI predicting a heart attack hours before symptoms strike or detecting cancer from a routine scan. This isn’t science fiction—AI-powered analytics in healthcare is making this a reality, turning data into life-saving insights.

By analyzing vast amounts of data, AI healthcare analytics help decode hidden patterns, improving diagnoses and personalizing treatments, which were unimaginable until a few years ago. The global healthcare analytics market is projected to hit $167 billion by 2030, growing at a 21.1% CAGR, thereby proving that data is becoming the foundation of modern medicine.

From real-time analytics in healthcare to AI-driven insights, the industry is witnessing a revolution—one that enhances patient care, optimizes hospital operations, and accelerates drug discovery. The future of healthcare is smarter, faster, and data-driven.

What Is AI-Powered Analytics in Healthcare?

AI-powered analytics uses artificial intelligence and machine learning to analyze patient data, detect patterns, and predict health risks. This empowers healthcare providers to make smarter, faster, and more personalized decisions. Here’s how this data revolution is reshaping healthcare:

1. Early Diagnosis and Predictive Analytics

AI-powered analytics can analyze massive datasets to identify patterns beyond human capability. Traditional diagnostic methods often rely on visible symptoms, but AI can detect subtle warning signs long before they manifest.

For example, real-time analytics in healthcare is proving life-saving in sepsis detection. Hospitals that employ AI-driven early warning systems have reported a 20% drop in sepsis mortality rates as these systems detect irregularities in vitals and trigger timely interventions.

2. Personalized Treatment Plans

AI-powered analytics can customize plans for individual patients based on genetic data, medical history, and lifestyle. This shift towards precision medicine eliminates the conventional one-size-fits-all approach.

AI also enables real-time patient monitoring and adjusting treatments based on continuous data collection from wearable devices and electronic health records (EHRs). This level of personalization is paving the way for safer, more effective treatments.

3. Smarter Hospital Operations

Hospitals generate 2,314 exabytes of data annually, yet much of it remains underutilized. AI-powered analytics is changing that by optimizing hospital operations to reduce inefficiencies and improve patient flow management.

For instance, Mount Sinai Hospital in New York uses AI-powered analytics for patient care by predicting life-threatening complications before they escalate. A clinical deterioration algorithm analyzes patient data daily, identifying 15 high-risk patients for immediate intervention by an intensive care rapid response team. Beyond emergency care, AI also prevents falls, detects delirium, and identifies malnutrition risks, ensuring proactive treatment.

4. Drug Discovery and Development

Developing a new drug is expensive and time-consuming, often taking 10-15 years and costing over $2.6 billion. However, AI-powered analytics is significantly reducing both time and costs by analyzing millions of chemical compounds, predicting potential drug candidates, and streamlining clinical trials faster than traditional methods.

During the COVID-19 pandemic, AI played a crucial role in identifying potential antiviral treatments by rapidly analyzing millions of drug interactions – a process that would have taken human researchers years. Additionally, AI is now being used to repurpose existing drugs, optimize trial designs, and predict patient responses, making pharmaceutical development faster, more efficient, and data-driven.

5. 24/7 Patient Support with AI Chatbots and Virtual Assistants

A survey by Accenture estimates that AI applications, including chatbots, could save the U.S. healthcare system around $150 billion annually by 2026. These savings stem from improved patient access and engagement, as well as a reduction in costs linked to in-person medical visits. AI-driven healthcare analytics is making healthcare more efficient, patient-centric, and responsive to individual needs.

Challenges in AI-Driven Healthcare

Despite its potential to revolutionize healthcare, AI-powered healthcare data & analytics come with challenges that must be addressed for widespread adoption. Some of the challenges are:

Data Privacy and Security: Healthcare systems handle sensitive patient data, making them prime targets for cyberattacks. Ensuring robust encryption, strict access controls, and compliance with HIPAA and GDPR is critical to maintaining patient trust and regulatory adherence.

Bias in AI Models: If AI systems are trained on biased datasets, they can perpetuate healthcare disparities, thereby leading to misdiagnoses and unequal treatment recommendations. Developing diverse, high-quality datasets and regularly auditing AI models can help mitigate bias.

Regulatory Compliance: AI-driven healthcare solutions must align with strict regulations to ensure ethical use. Organizations must work closely with regulatory bodies to maintain transparency and uphold ethical AI practices.

What’s Next in Smart Healthcare?

AI-Powered Surgeries: Robotic assistance enhances precision and reduces risks.

Smart Wearables: Track vital signs in real-time and alert patients to anomalies.

Mental Health Tech: Predictive tools offer proactive support and personalized therapy.

Why It Matters

AI isn’t replacing doctors—it’s augmenting their decision-making with data-driven insights. Healthcare systems that adopt analytics will see:

Improved patient outcomes

Reduced costs

Streamlined operations

#data analytics#no code platforms#business intelligence#ai tools#software#predictiveinsights#predictive modeling#tableau#tableau alternative#agentic ai#textile manufacturing analytics#analytics tools

0 notes

Text

What’s the Best Way to Start a Palm Leaf Plate Wholesale Business

Let’s be honest — finding a business idea that’s both profitable and meaningful isn’t easy. But every once in a while, something comes along that checks both boxes. That’s exactly what palm leaf plates offer: a chance to make good money while doing something that’s genuinely good for the planet.

If you’ve been thinking about starting your own wholesale business, palm leaf plates wholesale might be your golden ticket — especially now, as more people shift toward sustainable living and eco-friendly products.

Let’s walk through how you can actually get started — from understanding the product to setting up your operations and landing your first customers.

Why Palm Leaf Plates? Why Now? In a world drowning in plastic, palm leaf plates offer something refreshingly different.

They’re made from naturally fallen Areca palm leaves — no trees are cut, and no chemicals are used. They’re biodegradable, compostable, and surprisingly strong. That means they’re perfect for restaurants, events, catering companies, and even exports.

What makes this even more exciting is the timing. Countries are banning single-use plastics, and businesses are looking for planet-friendly options. That creates a real demand — and real opportunity — for smart entrepreneurs like you to step in.

Step 1: Understand What You're Selling Before you jump in, take time to really understand the product. Palm leaf plates come in all sorts of shapes and sizes — round dinner plates, square lunch plates, bowls, trays, and even compartment thalis.

Think about:

What kind of buyers you want to target (restaurants? event companies? exporters?)

Which styles and sizes are in high demand

What kind of quality and price range you want to offer

Knowing your product makes you a better seller — and it builds trust with your customers.

Step 2: Choose Your Business Model — Source or Manufacture Here’s the big decision: Do you want to source your plates from a manufacturer or make them yourself?

Option 1: Source and Sell This is the easier and faster route. You buy palm leaf plates in bulk from a trusted manufacturer and resell them to your customers. It’s low investment, and great if you're just starting out or want to focus on sales and marketing.

Option 2: Set Up a Manufacturing Unit This route takes more effort and money — but gives you full control. You’ll need machines, raw materials (palm leaves), and workers. A small setup in India can cost around ₹6–7 lakhs.

The process itself is straightforward:

Collect naturally fallen palm leaves

Wash and dry them

Press them into shape using heat molds

Trim, check quality, and pack

If you're based in southern India (Karnataka, Kerala, Tamil Nadu), where palm leaves are abundant, this could be a smart long-term play.

Step 3: Handle the Legal Stuff Don’t worry — this part sounds more intimidating than it is. Here’s what you’ll typically need to run a legit wholesale business:

GST registration (mandatory in India)

Udyam/MSME registration (helps with bank loans and subsidies)

FSSAI license (since these plates are used with food)

If you're thinking about exports, you might also need certifications like:

Compostability certification (BPI or EN13432)

ISO or food safety standards

These add credibility and help you access international markets.

Step 4: Figure Out Who You’re Selling To Since this is a wholesale business, you’ll be selling in bulk. So who are your ideal buyers?

Restaurants and cafés going plastic-free

Wedding and event planners

Organic stores and retailers

Exporters targeting markets in Europe, the U.S., or the Middle East

Each type of buyer will have different needs. An exporter might care more about certifications. A restaurant may want fast delivery and consistent quality. Learn what your customers want — and deliver it better than the next guy.

Step 5: Build a Basic Online Presence No need for a fancy e-commerce website (at least not yet). But having a clean, simple site or landing page makes a big difference.

Here’s what it should include:

Product photos and descriptions

Your story — what makes your business eco-conscious

How to place bulk orders

Contact form or WhatsApp link for quick inquiries

Also list your business on platforms like IndiaMART, TradeIndia, or ExportersIndia — many wholesale buyers use these sites to find suppliers.

And don’t underestimate Instagram and LinkedIn. Posting real photos, customer stories, or even short videos of how the plates are made can go a long way.

Step 6: Don’t Ignore Packaging and Shipping Palm leaf plates are tough, but smart packaging still matters. Go for simple, eco-friendly cartons — they look good and match your values. Include care instructions if needed.

As for logistics:

For local deliveries, use couriers like Delhivery, DTDC, or India Post

For exports, partner with freight forwarders who understand food-grade and eco-packaged products

If possible, always send a few samples first — it builds confidence and helps close the deal.

Step 7: Promote Smart, Not Loud Marketing doesn’t mean spending lakhs on ads. You can start small and still make an impact.

Here’s what works:

Send free samples to local restaurants or event planners

Share your story on social media (authentic always beats “salesy”)

Write short blog posts with keywords like “palm leaf plates wholesale” — Google loves helpful content

Follow up with leads from B2B marketplaces and always respond quickly

The more human and real your brand feels, the more people will trust you.

Final Thoughts: At the end of the day, this business isn’t just about plates. It’s about solving a real-world problem: plastic waste. You’re offering an alternative that’s better for the earth — and still practical, affordable, and beautiful.

With smart sourcing, the right connections, and a little hustle, starting a palm leaf plates wholesale business can be both rewarding and impactful. And the best part? You don’t need a huge investment to get going — just the right mindset and a clear plan.

FAQs 1. Are palm leaf plates microwave-safe? Yes! They’re heat-resistant and perfectly safe for microwaves and even ovens (up to a certain temperature).

2. How long can I store palm leaf plates? If kept dry and sealed, they can last up to 18 months without any problem.

3. Can I sell these plates internationally? Absolutely. Just make sure you get the right certifications and understand the import rules of your target countries.

4. What’s the minimum investment to start this business? If you're reselling, you can start with ₹1–2 lakhs. If you're manufacturing, expect around ₹6–7 lakhs for a basic unit setup.

5. Where can I find good suppliers? IndiaMART is a great starting point. You can also visit manufacturing hubs in South India to meet suppliers in person — that’s always a plus.

#ecofriendlytableware#sustainabledinnerware#palmleafplateswholesale#ecodisposableplateseurope#arecaleafplates#compostableplatesusa#arecaleafplatesuppliers#disposablearecaleafplates#naturalpalmleafplates

0 notes

Text

U.S. ERP Software Market Growth Potential for the Period 2025 to 2032 | At a CAGR of 3.6%

The U.S. Enterprise Resource Planning (ERP) software market size was valued at USD 12.84 billion in 2024, and it is projected to grow from USD 13.29 billion in 2025 to USD 16.99 billion by 2032, registering a CAGR of 3.6% during the forecast period. While growth is moderate, market dynamics are shifting due to increasing demand for integrated platforms, cloud ERP deployment, and regulatory compliance needs across industries.

Key Market Highlights:

2024 Market Size (U.S.): USD 12.84 billion

2025 Market Size (U.S.): USD 13.29 billion

2032 Market Size (U.S.): USD 16.99 billion

CAGR (2025–2032): 3.6%

Market Outlook: Stable growth supported by manufacturing digitization, financial process automation, and cloud migration

Top ERP Vendors in the U.S. Market:

SAP America

Oracle Corporation

Microsoft (Dynamics 365)

Workday

Infor

Epicor Software

Sage Group

Acumatica

Unit4

IFS

Plex Systems

NetSuite (Oracle)

Request for Free Sample PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/u-s-enterprise-resource-planning-erp-software-market-107427

Market Dynamics:

Key Growth Drivers:

Demand for Real-Time Operational Visibility: Organizations increasingly rely on centralized ERP platforms to consolidate finance, inventory, HR, and supply chain data.

Cloud-First IT Transformation: Adoption of cloud-based ERP solutions is accelerating among SMBs and large enterprises for improved scalability and cost-efficiency.

Compliance and Audit Readiness: ERP systems are instrumental in maintaining SOX compliance and audit trails for public and private firms.

Integration with Emerging Tech: ERP platforms are being enhanced with AI, machine learning, and robotic process automation (RPA) for smarter business operations.

Manufacturing Sector Revamp: U.S.-based manufacturers are adopting ERP to support smart factories, procurement digitization, and resource optimization.

Key Opportunities:

AI-Enhanced ERP Modules: Use of AI for demand forecasting, predictive maintenance, and anomaly detection in operations

ERP for Services Sector: Rapid expansion of ERP adoption in healthcare, legal, and professional services for project accounting and compliance

Mid-Market Expansion: Growing availability of modular, affordable ERP offerings for mid-sized U.S. firms

Vertical-Specific ERP: Tailored ERP systems for construction, education, manufacturing, and logistics industries

Mobile and Edge ERP Solutions: Expanding need for mobile-first and field-accessible ERP dashboards

Technology & Application Landscape:

Deployment Models:

Cloud ERP (SaaS)

On-Premises ERP

Hybrid ERP

Key ERP Modules:

Financial Management

Human Capital Management (HCM)

Inventory & Supply Chain Management

Manufacturing & Production

CRM & Order Management

Business Intelligence & Reporting

End Users:

Manufacturing

Retail

Healthcare

Education

Construction

Public Sector

Speak to Analysts: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/u-s-enterprise-resource-planning-erp-software-market-107427

Recent Developments:

February 2024 – Oracle introduced new GenAI-powered features in Oracle Fusion Cloud ERP for U.S. enterprises, enhancing real-time decision-making and scenario modeling.

July 2023 – SAP launched its Green Ledger initiative within SAP S/4HANA Cloud to help American enterprises track carbon emissions as part of their ERP reporting.

September 2023 – Workday extended its ERP offering for mid-sized U.S. companies with tailored HCM and finance tools, offering a low-code configuration engine.

Trends Shaping the U.S. ERP Market:

AI and Predictive Analytics: ERP systems integrating ML algorithms for forecasting demand, sales, and workforce needs

Composable ERP: Rise of microservices and modular ERP architectures that let organizations customize solutions based on evolving needs

Cybersecurity Integration: Emphasis on data security, access control, and compliance built into ERP layers

IoT and Edge Connectivity: ERP platforms are increasingly linking with smart devices and edge hardware in logistics and manufacturing

User-Centric Interfaces: Simplified dashboards, voice-enabled commands, and mobile app expansion

Conclusion:

Though the U.S. ERP software market is experiencing steady, moderate growth, the market remains strategically important as enterprises look to digitally transform core business operations. The future of ERP in the U.S. is cloud-first, intelligent, and composable, offering agility, compliance, and performance across verticals. As legacy systems are phased out, ERP vendors that offer modular, AI-powered, and industry-specific solutions will lead the next wave of enterprise efficiency.

Frequently Asked Questions:

1. What is the projected value of the global market by 2032?

2. What was the total market value in 2024?

3. What is the expected compound annual growth rate (CAGR) for the market during the forecast period of 2025 to 2032?

4. Which industry segment dominated market in 2023?

5. Who are the major companies?

6. Which region held the largest market share in 2023?

#U.S. Enterprise Resource Planning Software Market Share#U.S. Enterprise Resource Planning Software Market Size#U.S. Enterprise Resource Planning Software Market Industry#U.S. Enterprise Resource Planning Software Market Analysis#U.S. Enterprise Resource Planning Software Market Driver#U.S. Enterprise Resource Planning Software Market Research#U.S. Enterprise Resource Planning Software Market Growth

0 notes

Text

Procurement Software Market 2032: Will Cloud-Based Platforms Dominate by Decade’s End

Procurement Software Market size was valued at USD 7.71 Billion in 2023. It is expected to Reach USD 18.76 Billion by 2032 and grow at a CAGR of 10.40% over the forecast period of 2024-2032.

Procurement Software Market is witnessing robust growth as organizations across sectors modernize their purchasing processes to drive efficiency, transparency, and cost savings. The demand for integrated solutions that streamline supplier management, automate procurement workflows, and enhance spend visibility is gaining traction globally.

U.S. leads the adoption curve with a focus on automation, supplier risk management, and real-time analytics