#U.S. Machine Learning Market Share

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

BuzzFeed published a report claiming that Tumblr was utilized as a distribution channel for Russian agents to influence American voting habits during the 2016 presidential election in Feb 2018.

Text

U.S. Machine Learning Market Size, Share | CAGR 37.2% During 2023-2030

The U.S. machine learning market share was valued at USD 4.74 billion in 2022 and is projected to grow from USD 6.49 billion in 2023 to USD 59.30 billion by 2030, at a CAGR of 37.2%. The U.S. Machine Learning (ML) market encompasses the development, deployment, and application of algorithms and statistical models that enable computer systems to perform tasks without explicit instructions, relying instead on patterns and inference. Machine Learning is a key subset of Artificial Intelligence (AI) and plays a vital role across a broad range of sectors, including healthcare, finance, retail, manufacturing, transportation, and government.

Market Scope:

Types of technology: supervised learning, unsupervised learning, reinforcement learning, deep learning, natural language processing (NLP), and neural networks.

Deployment Options: Cloud-hosted, local, and mixed solutions.

Applications: Predictive analysis, image and voice recognition, recommendation engines, fraud detection, robotic process automation, and self-operating systems.

Final Users: Businesses, research organizations, governmental bodies, and technology startups

Request for Free Sample Here: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/u-s-machine-learning-ml-market-107479

Key Players:

Amazon, Inc. (U.S.)

Fair Isaac Corporation (U.S.)

RapidMiner Inc. (U.S.)

Microsoft Corporation (U.S.)

H2O.ai (U.S.)

IBM Corporation (U.S.)

Oracle Corporation (U.S.)

Hewlett Packard Enterprise Company (U.S.)

Teradata (U.S.)

TIBCO Software Inc. (U.S.)

Key Development Industry:

June 2022– Teradata announced the integration of the Teradata Vantage multi-cloud data and analytics platform with Amazon SageMaker and its general availability. This initiative backs Teradata's Analytics 123 framework, providing organizations facing challenges with production-grade AI/ML projects a systematic method for expanding their analytical model implementation. October 2022 – IBM's artificial intelligence System-on-Chip (SoC) has been released to the public. The device is engineered to train and execute deep learning models much more efficiently and considerably quicker than CPUs. The SoC features 32 processing cores and contains 23 billion transistors, thanks to a 5 nm process node.

Market Trend:

Rising interest in explainable AI (XAI) and responsible ML practices.

Increased use of automated machine learning (AutoML) for non-experts.

Integration of ML with edge computing for real-time analytics.

Rapid adoption in healthcare, fintech, and cybersecurity domains.

Speak to Analyst: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/u-s-machine-learning-ml-market-107479

About Us:

At Fortune Business Insights, we empower businesses to thrive in rapidly evolving markets. Our comprehensive research solutions, customized services, and forward-thinking insights support organizations in overcoming disruption and unlocking transformational growth.

With deep industry focus, robust methodologies, and extensive global coverage, we deliver actionable market intelligence that drives strategic decision-making. Whether through syndicated reports, bespoke research, or hands-on consulting, our result-oriented team partners with clients to uncover opportunities and build the businesses of tomorrow.

We go beyond data offering clarity, confidence, and competitive edge in a complex world.

Contact Us:

US +1 833 909 2966

UK +44 808 502 0280

APAC +91 744 740 1245

Email: [email protected]

#U.S. Machine Learning Market Share#U.S. Machine Learning Market Size#U.S. Machine Learning Market Industry#U.S. Machine Learning Market Analysis#U.S. Machine Learning Market Driver#U.S. Machine Learning Market Research#U.S. Machine Learning Market Growth

0 notes

Text

Editor's note: As schools across the United States and around the world face persistently high levels of student disengagement and chronic absenteeism, Rebecca Winthrop and Jenny Anderson offer parents a new way of assessing their children’s engagement in school and highlight the importance of children having agency in their own learning.

Erin Thomas: Rebecca, you’ve worked for a number of years, both nationally and internationally, on education and child development issues. As senior fellow and director of the Center for Universal Education, you lead both the center and (along with fellow Emily Morris) the Family, School, and Community Engagement initiative. Additionally, you are a seasoned researcher and leader and a mom to two middle schoolers. Can you share a bit about what drew you to this work?

Rebecca Winthrop: My focus on the role of families and communities grew out of my work on education innovations. For years, I had been working with policymakers and practitioners to encourage the take-up of education innovations that help all young people develop the skills they need to thrive in today’s fast-changing world. I found in this journey that we in the education sector often overlook the important role of families as partners in transforming education. During the COVID-19 pandemic, this issue hit me in a much more personal way. When my two boys’ schools switched to home-based learning, I realized I had misjudged which of my children were deeply engaged in their learning. My oldest son, who had always gotten top grades and liked school, lost all motivation when his school went online and moved to “pass/fail” grading. Meanwhile, my youngest son, who had struggled in school because of his dyslexia, blossomed and was deeply engaged in learning on his own. I realized that if I wasn’t able to tell which of my kids was deeply engaged in school as a global education expert, it would be very difficult for most parents and caregivers too. I know grades only tell part of the story of how well our children are doing in school. I also know that in the U.S. parents and caregivers frequently resist and challenge education reforms. But this isn’t their fault. We in the education community don’t do enough to help parents and caregivers understand what good learning looks like. I was interested in helping fill this gap and I knew to do that storytelling would have to be an important part of the process.

ET: Jenny, you were a finance journalist for years and then shifted to education. Why did you make the change?

Jenny Anderson: My interests shifted after I had my first child in 2008. After spending more than 10 years immersed in financial reporting, I suddenly became curious about how learning happens—what is developmental, what is environmental, what is experience? I was immediately struck by how little the mainstream media covered these topics. There were good “mommy bloggers” gaining traction and a few trailblazing parenting journalists (Anna Quindlen and Lisa Belkin come to mind). But how kids learn and develop was not considered a beat worthy of an editorial desk staffed with seasoned reporters and editors. Is how humans grow and learn and thrive really less important or sophisticated than the stock market, or culture? A generous explanation might be that learning and development are so core to what it is to be human that we don’t think too much about how we, or our children, do it. A more realistic one is that care and nurturing of kids has long been deemed women’s work, so not serious enough to warrant the resources to cover it well.

I became more interested in finding new and creative ways to understand how humans learn and change. It’s hardly new: We had to adapt from farming to factories and factories to offices, to a second machine age and then a fourth industrial revolution. Now we have Generative AI. I was consumed with the question: If humans are born and wired to learn, how can we help our kids to do this well?

ET: You collaborated on a new book, “The Disengaged Teen: How to Help Kids Learn better, Feel Better, and Live Better,” out on January 7. Why is this the moment for this book?

RW:More than ever before, what kids need now is to become better at learning. Generative AI is accelerating rapidly, and everyone agrees that the pace of change will continue to be dizzying. Uncertainty is the new norm. No one knows exactly what shifts in jobs and society are in store. What can best protect and prepare our children is to help them become excellent at learning and adapting. This is incredibly hard to do if you are coasting through school, bored and checked out. According to the U.S. Census, only 1 in 3 students are engaged in school. CUE’s research with the nonprofit Transcend found that less than 10% of students had school experiences that regularly let them explore their ideas and interests and practice building their independent learning skills. Resilient learners are not strong; they are flexible. Learning well is also closely tied to feeling well. When children are deeply engaged in their learning, they not only perform better but have better mental health outcomes.

ET: Jenny, how does the book help parents and educators address the major challenges adolescents face today?

JA: Teens are deeply disengaged in learning and are reporting alarmingly high mental health challenges, as Rebecca mentioned. A lot of this is pinned on social media, but kids have been disengaged from learning far longer than smartphones have been hijacking our kids’ attention.

Adolescence is a period of staggering change, a period when brains are fundamentally reconstructed. It is a window of unique opportunity and vulnerability, when the stories young people tell themselves can become embedded in useful, and sometimes less useful, ways. How kids think about themselves as learners shapes the stories they tell, and as parents and educators we have influence to narrate and model one about growth, malleability, and possibility. During adolescence, parents can nudge their teens toward experiences and opportunities to help them understand who they are and who they hope to be. Grades and achieving are part of this; nurturing a robust learner identity—that is, developing what we call “Explorer muscles”—is both essential and overlooked. Becoming better learners will help kids accelerate toward goals they care about, unstoppable where they so often now seem stuck.

If COVID-19 showed us that kids need to be well to learn well, our research— and that of others—shows that kids also need to learn well to be well. The key to this is staying emotionally connected to teens, but then having better language to understand and talk about their learning.

ET: In the book, you develop the Four Modes of Engagement framework, which is intended to help parents and educators identify how students engage in school. Can you talk a bit about the framework and how it provides a new perspective on students’ learning and engagement?

RW: How deeply children engage in their learning shapes not only how they do in school but also the learning skills that they develop. When students are more engaged, they are more likely to attend school, have good grades, master content, graduate, and have prosocial behavior. The problem is that it can be quite hard for adults to accurately assess how deeply engaged their children are. Adults are good at understanding the behavioral dimensions of engagement in school, like attending class, not being disruptive, and turning in homework. They aren’t as good at assessing the emotional and cognitive dimensions of engagement, like being interested in what they are doing, feeling like they belong in school, and thinking deeply about what they are learning. In our research, we found that a student’s grades do not always reflect how engaged they are in their learning. Many students are disengaged but able to get good grades usually because the material is not sufficiently challenging.

It is hard to address a problem you cannot fully see. This is why we developed the four modes of engagement, to help parents and caregivers but also educators better assess and address their children’s level of engagement. Our research showed that young people engage in four main ways with school and learning:

Resister mode. When kids resist, they struggle silently with profound feelings of inadequacy or invisibility, which they communicate by ignoring homework, playing sick, skipping class, or acting out.

Passenger mode.When kids coast along, consistently doing the bare minimum and complaining that classes are pointless. They need help connecting school to their skills, interests, or learning needs.

Achiever mode. When kids show up, do the work, and get consistently high grades, their self-worth can become tied to high performance. Their disengagement is invisible, fueling a fear of failure and putting them at risk for mental health challenges.

Explorer mode. When kids are driven by internal curiosity rather than just external expectations, they investigate the questions they care about and persist to achieve their goals.

Students can move between all these modes in the course of a day, depending on their teachers, classes, or peers. Often, however, kids are in one mode in school but in another one after school.

ET: Jenny, how can parents and educators use this framework to help improve student engagement?

JA: They can use this framework in three ways. First, the modes can be used to identify where kids are, which enables adults to offer better support. Kids in Passenger mode often need more autonomy whereas kids in Resister mode might need us in the trenches with them problem solving. Kids in Achiever mode may look like they are hitting it out of the park, but they need more opportunities to take risks on behalf of their learning. The modes help us understand their learning and in time can be used by young people themselves to understand the choices they make on behalf of their learning.

Second, the framework can help adults support kids who get stuck in Resister, Passenger, or even Achiever mode to get out. These modes are dynamic and fluid, but when kids become entrenched in one, it can become an identity. Our goal is to help young people build self-awareness and regulation strategies. The modes are one way to understand what’s happening and to better identify when things are going off the rails. Disengagement does not happen overnight—it is gradual. We want to intervene earlier in the engagement continuum, before we hit a crisis point.

We hope parents and educators help kids spend as much time in Explorer mode as possible. The research with Transcend showed that only 33% of 10th graders report that they get to develop their own ideas in school. This can lead to real disengagement.

ET: Rebecca, one of the center’s workstreams is focused on youth agency. Can you define that and explain how it relates to the book?

RW: Agency is the ability to set meaningful goals and marshal resources to meet them. It isn’t just having a plan, it’s being able to design and execute that plan, even if it means overcoming barriers along the way. It requires tapping into internal resources, like effort, but also asking for help from external ones like teachers, parents, neighbors, pastors, peers, or a chatbot.

We know young people need agency, particularly to navigate the world that is to come. With generative AI able to synthesize knowledge to answer questions, students need to develop skills to ask the questions that matter to them, come up with creative new solutions, and harness resources, be they technological or human, to help them deliver on their vision.

When students are in Explorer mode, they are “agentically engaged” in their learning. This means they are constructively influencing the flow of instruction to be more supportive and interesting to them. They are proactive, asking to work on topics that interest them, suggesting different ways to learn, and taking opportunities to reflect on what they’re interested in. In school, too few students get the chance to regularly be in Explorer mode. But they should. After all, school is one of the important places where young people can learn to develop agency over their learning, an essential skill for all stages of life.

This is what we are working toward at CUE, and it’s also how we hope our book can help. We want to help parents, caregivers, and educators today support their children to have more Explorer moments at home and in class. We also want to invite families into the movement to change the design of the schools of tomorrow and make Explorer mode the default, not the exception.

7 notes

·

View notes

Text

U.S. Population Health Management Market expanding with digital tools to hit 20% CAGR by 2029

The U.S. population health management market is expected to grow at a significant CAGR of approximately 20% in the forecast period. This growth is driven by the transition to value-based care models, the increasing burden of chronic diseases, advancements in healthcare analytics, regulatory reforms, and the rising need for cost reduction and improved care outcomes. However, barriers such as high implementation costs and concerns over data privacy pose challenges to wider adoption.

The U.S. population health management (PHM) market focuses on improving health outcomes for defined populations by using various tools, including healthcare data analytics, care coordination, and patient engagement strategies. Its goal is to enhance the quality of care, reduce healthcare costs, and improve patient satisfaction by shifting from reactive care to preventive and proactive interventions. PHM typically involves collaboration between healthcare providers, payers, and public health entities to manage chronic diseases, reduce hospital admissions, and achieve value-based care outcomes.

To request a free sample copy of this report, please visit below https://meditechinsights.com/u-s-population-health-management-market/request-sample/

Emphasis on Value-Based Care Models: Driving Market Demand

A significant factor driving the demand for population health management is the growing shift from traditional fee-for-service models to value-based care. Value-based care focuses on improving patient outcomes and reducing costs through better care coordination, preventive care, and chronic disease management. This model incentivizes healthcare providers to prioritize long-term health and cost efficiency, aligning perfectly with the objectives of PHM. As healthcare systems aim to reduce hospital readmissions and lower overall costs, PHM strategies, supported by data-driven approaches, have become indispensable. The success of this shift depends on real-time data sharing, care integration, and collaborative decision-making, making PHM tools central to achieving these goals.

Market Trend: Rise of AI and Machine Learning in Population Health Management

One of the most transformative trends in the U.S. population health management market is the integration of AI and machine learning technologies. AI-driven analytics allow for the processing of vast amounts of healthcare data, providing insights that help predict patient risks, tailor treatment plans, and enhance care coordination. These technologies enable healthcare providers to identify high-risk patients early, automate repetitive tasks, and optimize population-level interventions. By leveraging AI, healthcare organizations can not only improve the accuracy of diagnoses and treatments but also deliver more personalized, efficient care, ultimately driving better health outcomes while reducing operational costs. The ability to predict health trends and deliver targeted preventive care is rapidly becoming a key advantage in PHM initiatives.

🔗 Want deeper insights? Download the sample report here: https://meditechinsights.com/u-s-population-health-management-market/request-sample/

Competitive Landscape Analysis

The U.S. population health management market is marked by the presence of established and emerging market players such as Cerner Corporation (Oracle); Veradigm LLC (Allscripts Healthcare, LLC); eClinicalWorks; Conifer Health Solutions, LLC; Cedar Gate Technologies (Enli Health Intelligence); McKesson Corporation; Medecision; Optum, Inc.; Koninklijke Philips N.V.; and Athenahealth, Inc. among others. Some of the key strategies adopted by market players include product innovation and development, strategic partnerships and collaborations.

About Medi-Tech Insights

Medi-Tech Insights is a healthcare-focused business research & insights firm. Our clients include Fortune 500 companies, blue-chip investors & hyper-growth start-ups. We have completed 100+ projects in Digital Health, Healthcare IT, Medical Technology, Medical Devices & Pharma Services in the areas of market assessments, due diligence, competitive intelligence, market sizing and forecasting, pricing analysis & go-to-market strategy. Our methodology includes rigorous secondary research combined with deep-dive interviews with industry-leading CXO, VPs, and key demand/supply side decision-makers.

Contact:

Ruta Halde Associate, Medi-Tech Insights +32 498 86 80 79 [email protected]

0 notes

Text

Market Sees Growth in Cloud-Based Genomic Data Platforms

The Genomics in Cancer Care Market reached USD 13.4 billion in 2022 and is projected to grow to USD 51.1 billion by 2031, exhibiting a CAGR of 18.9% during the forecast period 2024–2031, driven by the growing role of precision medicine and targeted therapies in oncology. Genomic testing helps identify cancer-causing mutations, such as BRCA1 and BRCA2, enabling accurate diagnosis, prognosis, and treatment selection. By uncovering genetic changes in cancer cells, genomics supports the development of more effective, individualized therapies that significantly improve patient outcomes and survival rates.

Unlock exclusive insights with our detailed sample report :

Key Market Drivers

1. Rising Global Cancer Prevalence

According to WHO, cancer is a leading cause of death globally, with over 20 million new cases expected annually by 2030. This has created a demand for advanced genomic tools that facilitate early detection and personalized treatment strategies.

2. Advances in NGS and Genomic Sequencing

Technological breakthroughs in whole genome sequencing (WGS), targeted gene panels, and RNA sequencing are enhancing the ability to identify key mutations and develop tailored therapeutic approaches.

3. Shift Toward Precision Oncology

The era of one-size-fits-all cancer treatment is fading. Genomic testing enables oncologists to match therapies based on individual molecular profiles, increasing treatment success rates and reducing adverse effects.

4. Integration of AI and Machine Learning

AI-driven platforms are accelerating genomic data interpretation, assisting in variant classification, biomarker discovery, and real-time decision-making for clinicians and researchers.

5. Government and Industry Investments

Public and private investments are growing rapidly. For example:

The U.S. Cancer Moonshot initiative continues to support genomic cancer research.

Japan’s Genomic Medicine Plan is focused on nationwide whole-genome sequencing efforts and biomarker development.

Regional Highlights

United States

The U.S. is at the forefront of genomic integration in cancer care, with extensive use of NGS panels, companion diagnostics, and cloud-based genomic tools.

Leading institutions like Memorial Sloan Kettering and MD Anderson partner with biotech firms for tumor sequencing projects.

The FDA has increased approval of genomic-based cancer therapies and companion diagnostics, ensuring regulatory clarity and accelerating innovation.

Japan

Japan is heavily investing in aging-focused cancer genomics as over 28% of its population is aged 65 or above.

National cancer programs promote biobank development, data-sharing frameworks, and personalized therapeutic protocols.

Hospitals are piloting AI-integrated genomic dashboards to aid clinical decision-making for oncologists.

Speak to Our Senior Analyst and Get Customization in the report as per your requirements:

Key Segments

By Technology:

Next-Generation Sequencing (NGS)

PCR (Polymerase Chain Reaction)

Microarrays

Sanger Sequencing

By Application:

Diagnostics

Drug Discovery and Development

Prognostics and Screening

Companion Diagnostics

By Cancer Type:

Breast Cancer

Lung Cancer

Colorectal Cancer

Prostate Cancer

Others (Melanoma, Leukemia, etc.)

By End-User:

Hospitals & Clinics

Academic & Research Institutes

Biotech & Pharma Companies

Diagnostic Labs

Recent Industry Developments

Thermo Fisher Scientific launched an expanded NGS panel approved for solid tumors, improving turnaround times and reducing costs in hospitals.

Roche and Foundation Medicine extended collaboration to develop comprehensive genomic profiling (CGP) solutions for rare cancers.

Illumina and AstraZeneca announced a joint platform that integrates genomic sequencing with drug development, accelerating targeted therapy pipelines.

Japan’s National Cancer Center began a trial for population-level cancer genome screening, a first in Asia-Pacific’s clinical genomics ecosystem.

The NIH’s All of Us Research Program now includes cancer patients in its longitudinal genomic dataset, broadening ethnic and genetic diversity.

Buy the exclusive full report here:

Growth Opportunities

Expansion of Liquid Biopsy Testing: Non-invasive blood-based genomic testing is opening doors for real-time tumor monitoring and minimal residual disease detection.

Development of Multi-Cancer Early Detection (MCED) Tests: These tests use genomic signals to detect various cancer types at once, revolutionizing preventive oncology.

Decentralized Genomic Testing Platforms: The adoption of cloud and edge computing in diagnostics supports genomic data analysis even in smaller hospitals.

Increasing Partnerships with Pharma: Biopharma companies seek genomic data insights to design better trials, improving drug response and reducing trial failure rates.

Personalized Cancer Vaccines: Genomics is paving the way for neoantigen-based immunotherapies, which are now entering clinical trials globally.

Challenges and Considerations

High Costs of Sequencing: Despite decreasing, comprehensive genomic profiling remains expensive and is not uniformly reimbursed.

Data Privacy Concerns: Handling of sensitive genomic data raises questions around patient consent, security, and ownership.

Skill Gaps in Data Interpretation: Many healthcare providers still lack the training required to interpret complex genomic reports accurately.

Leading Market Players

Illumina, Inc.

Thermo Fisher Scientific

Agilent Technologies

Roche Diagnostics

Bio-Rad Laboratories

Qiagen N.V.

Foundation Medicine

Guardant Health

Fujifilm Holdings Corp. (Japan)

These companies are:

Launching multi-cancer panels

Building AI-enabled interpretation platforms

Partnering with governments and hospitals for clinical validation

Focusing on affordability and access in underserved regions

Stay informed with the latest industry insights-start your subscription now:

Conclusion

The genomics in cancer care market is not just expanding—it’s transforming the very fabric of oncology. From tumor characterization to tailored therapies, genomics is enabling a future where cancer care is not only more effective but also more humane and precise.

With growing government support, rapid adoption of AI tools, and unprecedented collaboration between diagnostics and therapeutics, the global healthcare ecosystem is on the brink of genomic-enabled cancer care at scale.

The next decade will not just be about treating cancer—but about predicting, preventing, and personalizing the battle against it.

About us:

DataM Intelligence is a premier provider of market research and consulting services, offering a full spectrum of business intelligence solutions—from foundational research to strategic consulting. We utilize proprietary trends, insights, and developments to equip our clients with fast, informed, and effective decision-making tools.

Our research repository comprises more than 6,300 detailed reports covering over 40 industries, serving the evolving research demands of 200+ companies in 50+ countries. Whether through syndicated studies or customized research, our robust methodologies ensure precise, actionable intelligence tailored to your business landscape.

Contact US:

Company Name: DataM Intelligence

Contact Person: Sai Kiran

Email: [email protected]

Phone: +1 877 441 4866

Website: https://www.datamintelligence.com

#Genomics in Cancer Care Market#Genomics in Cancer Care Market size#Genomics in Cancer Care Market growth#Genomics in Cancer Care Market share#Genomics in Cancer Care Market analysis

0 notes

Text

Government and Defense Fuel Global Supply Chain Protection Efforts

The Supply Chain Security Market market is on a strong growth trajectory, forecast to expand from USD 2.1 billion in 2023 to USD 4.9 billion by 2030. This represents a compound annual growth rate (CAGR) of approximately 11% over the forecast period. Increased cargo theft, cyber threats, and the need for regulatory compliance are prompting businesses worldwide to invest in advanced supply chain security solutions.

Industries such as retail, pharmaceuticals, automotive, and logistics are experiencing growing pressure to adopt proactive measures to mitigate physical and digital threats throughout their supply chains. Technologies like blockchain, IoT sensors, artificial intelligence, and cloud-based platforms are playing an integral role in shaping the market landscape.

To Get Free Sample Report: https://www.datamintelligence.com/download-sample/supply-chain-security-market

Key Market Drivers

Rising Cargo Theft and Physical Threats Supply chain theft and fraud continue to grow in sophistication, with incidents of fake shipping documentation and identity-based theft. These risks are prompting businesses to adopt real-time monitoring, tracking systems, and secure transportation protocols.

Cybersecurity Challenges Supply chains are increasingly vulnerable to cyberattacks, particularly ransomware and data breaches affecting logistics software, warehouse systems, and supplier communication networks. This has spurred a significant rise in cybersecurity integration across supply chain infrastructures.

Stringent Regulatory Compliance Governments and international agencies have implemented regulatory standards such as ISO 28000, C-TPAT (Customs-Trade Partnership Against Terrorism), and the European Union’s supply chain visibility directives. Compliance is no longer optional it is central to operations and partnerships.

Demand for End-to-End Visibility Enterprises require uninterrupted visibility into their supply networks to mitigate disruption risks, enhance inventory management, and preemptively address vulnerabilities. IoT devices, GPS trackers, and RFID chips are becoming integral tools for real-time logistics management.

Adoption of Advanced Technologies Technologies like AI-driven analytics, machine learning, blockchain, and digital twins are transforming how businesses monitor, secure, and optimize supply chain operations.

Regional Insights

North America North America holds the largest market share, fueled by advanced technological infrastructure, strong cyber regulations, and high demand from logistics, defense, and healthcare sectors. The U.S. is the dominant market, supported by substantial government and private sector investments.

Europe Europe accounts for a significant portion of global market revenue, supported by strict data protection laws (GDPR), regulatory enforcement on product traceability, and a focus on supply chain transparency in cross-border trade.

Asia-Pacific Asia-Pacific is the fastest-growing regional market, forecast to expand at a CAGR of around 16%. Rapid industrialization, the expansion of e-commerce, increasing cases of cargo fraud, and growing awareness around cybersecurity are key factors propelling growth in countries like China, India, and Japan.

Latin America and Middle East & Africa (MEA) These emerging markets are witnessing rising investments in logistics, port security, and smart infrastructure, especially in industries like oil & gas, pharmaceuticals, and food logistics.

Market Segmentation

By Component

Hardware: Includes GPS trackers, RFID tags, and IoT sensors, essential for physical asset tracking.

Software: Encompasses risk analytics platforms, monitoring dashboards, and AI-based threat detection systems.

Services: Consulting, deployment, compliance audits, and managed monitoring services are growing in demand.

By Application

Data Security and Integrity

Real-Time Monitoring and Alerts

Access Control and Authentication

Risk Assessment and Compliance Management

By Industry

Retail & E-Commerce: High theft vulnerability, especially in last-mile delivery and warehouse operations.

Healthcare & Pharmaceuticals: Demand for secure handling of biologics and anti-counterfeiting systems.

Manufacturing and Automotive: Focus on supplier verification and just-in-time delivery security.

Defense & Aerospace: National security-related logistics demand top-tier surveillance and risk minimization.

Transportation & Logistics: Adoption of end-to-end digital security systems and cold-chain monitoring.

Market Challenges

High Implementation Costs The cost of integrating AI, IoT, and blockchain into supply networks can be substantial, particularly for small-to-medium enterprises.

Lack of Standardization Global supply chains span diverse regulatory environments, making standardization difficult across industries and countries.

Evolving Threat Landscape Cyber threats evolve rapidly, requiring continuous investment in security upgrades, staff training, and threat intelligence.

Subscribe for Insights: https://www.datamintelligence.com/reports-subscription

Future Market Opportunities

Blockchain for Tamper-Proof Verification Blockchain’s ability to provide immutable transaction records is enabling secure verification of product movement, improving transparency and trust across stakeholders.

AI and Predictive Analytics AI models can now identify patterns of potential fraud, shipment delays, and operational anomalies before they escalate into major disruptions.

Cloud-Based Platforms The shift to SaaS-based supply chain security platforms is growing, especially among multinational organizations seeking centralized control and scalability.

Government and Defense Support Public sector programs promoting secure trade and protected infrastructure (such as defense-grade cybersecurity for transport systems) are expected to drive substantial growth.

Key Market Players

Leading vendors include IBM Corporation, Cisco Systems, Oracle Corporation, Honeywell International, Siemens AG, Sensitech, Huawei Technologies, Check Point Software Technologies, Johnson Controls, Securitas AB, and Intel Corporation. These players focus on integrated platforms offering visibility, risk analysis, and automated threat detection.

Conclusion

The global supply chain security market is evolving rapidly in response to rising physical and cyber threats. As businesses strive to protect assets, ensure regulatory compliance, and optimize global operations, the need for integrated, intelligent security solutions continues to grow. With strong growth expected through 2030, organizations that prioritize transparency, tech-enabled risk management, and regulatory readiness will be best positioned to thrive in this complex and competitive environment.

0 notes

Text

Electronic Stethoscope Market Growing at 7.8% CAGR | Forecast Report 2025–2033

What Is an Electronic Stethoscope?

An electronic stethoscope enhances traditional auscultation by converting acoustic sounds from the body into electronic signals. These signals are then amplified, filtered, and converted into digital data. Core benefits include

Amplification for clearer detection of faint sounds

Noise reduction via active filters

Recording and playback for clinical review and telemedicine

Visualization through waveform display or frequency spectra

Integration with smartphones or health platforms

This technology supports telehealth diagnostics, education, remote consultations, and advanced patient evaluations.

To buy the report, click on https://www.datamintelligence.com/buy-now-page?report=electronic-stethoscope-market

Global Market Overview

The demand for electronic stethoscopes has been steadily rising:

The global market was valued in the range of USD 200–250 million in recent years.

It is projected to grow to approximately USD 350–400 million by 2030, with a CAGR of 8.2%.

Key growth regions include North America due to technological adoption, Europe as a secondary market, and fast growth in Asia-Pacific.

Growth is primarily driven by:

Expanding telemedicine

Professional-grade diagnostic tools

Technological innovation in amplification and connectivityTo get the free sample report, click on https://www.datamintelligence.com/download-sample/electronic-stethoscope-market

Market Drivers & Growth Opportunities

1. Expansion of Telemedicine

Remote patient monitoring and virtual care have surged post-pandemic. Electronic stethoscopes enable physicians to conduct remote heart and lung exams—critical for rural, pandemic, and global health contexts.

2. Aging Population & Chronic Illness

An aging demographic with higher incidence of cardiovascular and respiratory conditions (e.g. COPD, heart valve diseases) is driving demand for better diagnostic tools in home and clinical settings.

3. Technological Advancements

Modern electronic stethoscopes feature high-fidelity recording, AI-assisted auscultation, voice commands, Bluetooth, smartphone apps, and cloud data integration—making them powerful diagnostic and educational tools.

4. Clinical & Home Use Integration

Medical societies are increasingly recommending advanced auscultation. Over time, electronic stethoscopes are expected to become standard tools for clinicians and caregivers in hospitals and homes.

5. Data-Driven Healthcare

Ability to store and visualize auscultation data supports clinical auditing, diagnostic workflows, machine learning training, and detailed tracking of patient vitals.

6. Healthcare Infrastructure Push

Governments and private investors are promoting telehealth and remote diagnostics—boosting procurement of digital stethoscopes in primary care and rural clinics.

To get the unlimited market intelligence, subscribe, https://www.datamintelligence.com/download-sample/electronic-stethoscope-market

U.S. Market Trends

The U.S. leads global electronic stethoscope adoption, accounting for over 40% market share.

Major hospitals and telehealth providers are integrating digital auscultation into standard care.

Research institutions are developing algorithms to detect murmurs and cardiac anomalies automatically.

Health tech companies are producing sub-$200 models suitable for medical students and home monitoring.

Insurance reimbursement is increasingly covering telemedicine devices, encouraging broader adoption.

Japan & Asia-Pacific Market Trends

Japan offers strong growth due to an aging population and universal healthcare infrastructure.

Domestic manufacturers prioritize ultra-compact and wireless models suitable for home visits and elderly care.

Telehealth acceptance is rising, prompting clinic and hospital upgrades to digital fundsets.

Japan also contributes significantly to regulatory standards and clinical trial backing for stethoscope innovation.

Other APAC nations—China, India, South Korea—are rapidly adopting lower-cost digital devices in remote and primary care settings.

Europe & Emerging Regions

Europe follows the U.S. and Japan in digital auscultation adoption.

Public healthcare systems in the UK, Germany, and France are incorporating these devices to support telemedicine.

Sustainability and cross-border interoperability are driving further innovation.

Emerging markets in Latin America, Africa, and the Middle East are growing more slowly—limited by cost, infrastructure, and telehealth penetration—but represent high-volume future opportunities.

Competitive Landscape

Key players include:

3M Littmann – Traditional stethoscope leader advancing into digital systems

Eko Devices – Offering AI-support for murmur detection and telehealth use

Thinklabs – Known for the ultra-portable Model One

Welch Allyn (Hill-Rom) – Focusing on hospital-grade recording systems

ADC (American Diagnostic Corporation) – Entry-level digital models targeting education and home use

Philips and GE Healthcare – Integrating stethoscopes into wider monitoring systems

Market strategies focus on:

Healthcare partnerships

Product bundling with health platforms

AI-based diagnostic support

Training programs for clinicians

Challenges & Market Considerations

Cost Barrier: Digital stethoscopes remain several times more expensive than analog.

Clinical Validation: Medical providers require strong clinical evidence and integration.

Data Privacy and Security: Recorded auscultation data must comply with HIPAA, GDPR, and other laws.

Technical Integration: Seamless EMR and telehealth platform compatibility is essential.

Training Needs: Clinicians must adapt to new workflows and potential added tonal complexity.

Strategic Growth Recommendations

Expand Telemedicine Alignment Create bundled solutions with telehealth providers and remote monitoring platforms.

Enhance Clinical Evidence Partner with hospitals for trial data and peer-reviewed evidence to support diagnostics.

Smart & Connected Devices Integrate AI diagnostics, cloud storage, smartphone apps, and multilingual user support.

Education and Training Collaborate with medical schools for curriculum inclusion and improve usability training.

Affordable Models for Emerging Markets Develop low-cost yet reliable models for rural clinics and developing country healthcare providers.

Regulatory Strategy & Data Security Ensure GDPR and HIPAA compliance, structured data encryption, and user privacy controls.

Conclusion

The Electronic Stethoscope Market is poised for continued growth, shaped by telehealth expansion, chronic disease prevalence, and technological innovation. With projected growth driven by North America, Europe, and especially Japan/Asia-Pacific, demand is rising across hospital, clinical, and home-use segments.

As smart healthcare becomes standard, electronic stethoscopes represent a fundamental shift—from analog auscultation to digitally enabled, connected diagnostics. For manufacturers, investors, and healthcare providers, adoption depends on combining affordability, interoperability, clinical validation, and robust data security.

About Us

DataM Intelligence is a global market research and consulting firm specializing in high-growth healthcare, clean tech, and advanced technology markets. We provide in-depth strategic insights, competitive benchmarking, and custom research solutions to support informed decisions in rapidly evolving sectors.

Contact Us

DataM Intelligence

Email: [email protected]

Phone: +1 877 441 4866

0 notes

Text

AI Platform Cloud Service Market Size, Share & Growth Analysis 2034: Accelerating the Future of Intelligent Computing

AI Platform Cloud Service Market is evolving at a rapid pace, fueled by the growing need for scalable, cost-efficient, and intelligent digital solutions. These platforms provide a comprehensive cloud-based infrastructure, enabling the development, deployment, and management of AI applications across industries.

With components like machine learning, data storage, and integrated development environments, the market is empowering organizations to accelerate innovation and streamline decision-making processes. As of 2024, the market has shown exceptional momentum, reaching a volume of 320 million metric tons and projected to grow at a remarkable CAGR of 22% through 2034. Increasing demand for AI-driven automation and real-time data analytics is reshaping how businesses operate, making AI platforms an indispensable asset.

Click to Request a Sample of this Report for Additional Market Insights: https://www.globalinsightservices.com/request-sample/?id=GIS23260

Market Dynamics

The primary driver behind the AI Platform Cloud Service Market is the seamless integration of AI with cloud computing. This combination allows companies to leverage powerful AI tools without investing heavily in on-premises infrastructure. Demand for real-time predictive analytics, intelligent automation, and personalized services is pushing enterprises toward cloud-based AI platforms. However, challenges such as data privacy concerns, high implementation costs, and a shortage of AI-skilled professionals continue to restrict market expansion. Despite these hurdles, technological advancements in deep learning, NLP, and robotic process automation are opening up new frontiers for market growth.

Key Players Analysis

The competitive landscape is dominated by tech giants such as Microsoft Azure, Amazon Web Services (AWS), and Google Cloud Platform, all of whom offer robust AI capabilities and global cloud infrastructure. These players invest heavily in R&D and regularly enhance their platforms to support evolving AI needs. Alongside them, innovative firms like C3.ai, DataRobot, and H2O.ai are making significant strides by offering niche, specialized AI services. Emerging startups like Cognify Labs, Quantum Leap Technologies, and Neura Cloud Innovations are contributing fresh perspectives and driving disruption with agile, cutting-edge platforms tailored to specific industries and use cases.

Regional Analysis

North America leads the AI Platform Cloud Service Market, thanks to its advanced tech infrastructure and strong R&D investment, particularly in the U.S., where companies are aggressively adopting AI for digital transformation. Europe is also showing robust growth, with nations like Germany, the UK, and France making AI central to their industrial and healthcare strategies. The Asia-Pacific region is rapidly catching up, bolstered by government initiatives and digital transformation efforts in China, India, and Japan. Meanwhile, countries in the Middle East & Africa, including the UAE and Saudi Arabia, are making notable progress in adopting AI solutions to power smart cities and digital governance.

Recent News & Developments

Recent developments have significantly influenced the AI Platform Cloud Service Market. Major providers are adopting competitive pricing models, ranging from $100 to $500 per service, to cater to a broad spectrum of users — from startups to large enterprises. Strategic collaborations and acquisitions are on the rise, as players seek to enhance their offerings and broaden their global footprint. Companies are also prioritizing sustainability, focusing on energy-efficient data centers to align with global environmental goals. Simultaneously, evolving regulations around data privacy and cybersecurity are reshaping operational strategies, compelling providers to enhance compliance frameworks and data governance practices.

Browse Full Report : https://www.globalinsightservices.com/reports/ai-platform-cloud-service-market/

Scope of the Report

This report offers comprehensive insights into the AI Platform Cloud Service Market, covering all critical aspects from market size and forecasts to competitive landscape and regulatory impact. It analyzes key market segments such as public, private, and hybrid cloud deployments, along with a diverse array of AI applications including fraud detection, customer service, and supply chain optimization. The report also examines technological frameworks — ranging from machine learning and speech recognition to computer vision — and evaluates their relevance across verticals such as BFSI, retail, healthcare, telecom, and education. By identifying challenges, growth drivers, and emerging opportunities, the report equips stakeholders with the intelligence necessary for strategic decision-making in a rapidly transforming digital landscape.

#aiincloud #cloudai #aiplatforms #machinelearning #artificialintelligence #cloudcomputing #digitaltransformation #predictiveanalytics #aitechnology #cloudsolutions

Discover Additional Market Insights from Global Insight Services:

Cloud Based Contact Center Market : https://www.globalinsightservices.com/reports/cloud-based-contact-center-market/

Digital Content Creation Market : https://www.globalinsightservices.com/reports/digital-content-creation-market/

Field Service Management Market ; https://www.globalinsightservices.com/reports/field-service-management-market/

Regulatory Risk Management Market : https://www.globalinsightservices.com/reports/regulatory-risk-management-market/

Speech Analytics Market ; https://www.globalinsightservices.com/reports/speech-analytics-market/

About Us:

Global Insight Services (GIS) is a leading multi-industry market research firm headquartered in Delaware, US. We are committed to providing our clients with highest quality data, analysis, and tools to meet all their market research needs. With GIS, you can be assured of the quality of the deliverables, robust & transparent research methodology, and superior service.

Contact Us:

Global Insight Services LLC 16192, Coastal Highway, Lewes DE 19958 E-mail: [email protected] Phone: +1–833–761–1700 Website: https://www.globalinsightservices.com/

0 notes

Text

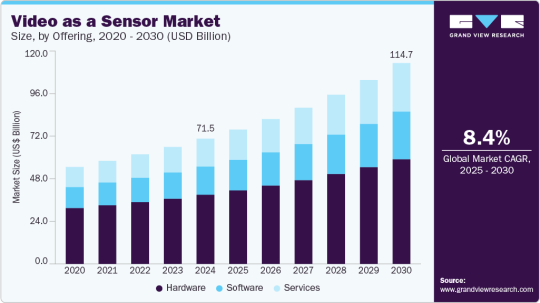

The Future of Analytics: How Video As A Sensor is Redefining Data Capture

The global Video As A Sensor Market, estimated at USD 71.50 billion in 2024, is forecast to reach USD 114,664.7 million by 2030, exhibiting a Compound Annual Growth Rate (CAGR) of 8.4% from 2025 to 2030. This growth is propelled by rapid technological advancements that have transformed conventional video systems and recording tools into sophisticated, intelligent decision-making instruments.

A significant catalyst for VaaS adoption is the technology's capacity to deliver real-time insights, including capabilities like facial recognition, anomaly detection, and behavior prediction. These features render VaaS highly suitable for contemporary security and surveillance systems, where prompt threat identification is crucial. Beyond security applications, the versatility of video sensors is increasingly evident across various sectors. In smart city initiatives, they play a vital role in enhancing urban infrastructure, contributing to public safety, optimizing energy consumption, and improving waste management efforts.

Key Market Trends & Insights:

North American Dominance: North America led the market with a 35.5% share in 2024. This leadership is driven by substantial investments in advanced surveillance systems and the early adoption of cutting-edge technologies such as Artificial Intelligence (AI) and machine learning.

U.S. Market Expansion: The video as a sensor market in the U.S. is experiencing notable growth, corresponding with increasing regional demand. The accelerating pace of industrialization and the integration of advanced technologies are key factors driving this market's expansion.

Video Surveillance Product Leadership: By product type, video surveillance accounted for the largest market revenue share in 2024. This segment's dominance is primarily due to escalating security concerns across residential, commercial, and public domains, coupled with rapid advancements in technologies like AI-driven analytics, cloud computing, and high-resolution imaging.

Security & Surveillance Application Dominance: In terms of application, the security and surveillance segment held the largest market revenue share in 2024. This is attributed to VaaS's ability to automate real-time threat detection, significantly reduce false alarms, and efficiently manage large volumes of video footage, thereby lessening the workload on security personnel.

Commercial End-Use Sector Growth: The commercial segment accounted for the largest market revenue share in 2024. This is driven by the growing need for enhanced security and surveillance solutions in commercial environments, including office buildings and retail establishments, to protect assets and ensure safety.

Order a free sample PDF of the Video As A Sensor Market Intelligence Study, published by Grand View Research.

Market Size & Forecast

2024 Market Size: USD 71.50 Billion

2030 Projected Market Size: USD 114,664.7 Million

CAGR (2025-2030): 8.4%

North America: Largest market in 2024

Asia Pacific: Fastest growing market

Key Companies & Market Share Insights

Leading firms in the Video As A Sensor (VaaS) market are employing a range of strategic initiatives to expand their market presence. These primarily include product launches and developments, alongside expansions, mergers and acquisitions, contracts, agreements, partnerships, and collaborations. Companies are leveraging diverse techniques to enhance market penetration and strengthen their competitive standing.

Axis Communications, a prominent player, specializes in network video surveillance and intelligent security solutions. Their comprehensive offerings, including a wide array of cameras, video management software, analytics, and access control systems, enable businesses and smart cities to utilize video as a sensor for real-time insights, improved safety, and enhanced operational efficiency. Axis's commitment to innovation, sustainability, and fostering a robust partner ecosystem underpins their goal of contributing to a smarter and safer global environment.

Hikvision is a significant force in video-centric IoT solutions, with a strong focus on advanced video-as-a-sensor technologies for both security and intelligent monitoring. By integrating state-of-the-art AI, deep learning, and high-performance video analytics, Hikvision delivers real-time surveillance, environmental sensing, and actionable insights. Their solutions are deployed across various sectors globally, including smart cities, transportation systems, and commercial enterprises.

Key Players

Axis Communications AB

Hangzhou Hikvision Digital Technology Co., Ltd.

Bosch Sicherheits systeme GmbH

Dahua Technology Co., Ltd.

Sony Corporation

Honeywell International Inc.

Sportradar AG

i-PRO

Johnson Controls

OMNIVISION

Browse Horizon Databook for Global Video As A Sensor Market Size & Outlook

Conclusion

The global Video As A Sensor (VaaS) market is experiencing rapid growth, driven by technological advancements transforming video into intelligent decision-making tools. Its ability to provide real-time insights makes it crucial for security, surveillance, and smart city initiatives. North America leads the market, with video surveillance and security applications dominating across commercial sectors. Leading companies are strategically innovating and collaborating to further expand their market share in this dynamic industry.

0 notes

Text

Glucose Sensors Market: A Comprehensive Global Overview and Future Outlook

Introduction

The Glucose Sensors Market is at the forefront of innovation in the global healthcare landscape, particularly in the management of diabetes—a chronic condition affecting over 500 million people worldwide. With increasing emphasis on early diagnosis, real-time monitoring, and patient-centered care, glucose sensors have evolved from traditional finger-prick devices to advanced wearable and continuous monitoring systems. This article presents a global overview of the glucose sensors market, analyzing current dynamics, key regions, technological shifts, and future outlook.

Market Overview

Glucose sensors are critical components in glucose monitoring devices that measure blood sugar levels. These sensors are utilized in:

Continuous Glucose Monitoring (CGM) Systems

Flash Glucose Monitoring (FGM) Devices

Traditional Blood Glucose Meters

Non-invasive and Minimally Invasive Devices

As the prevalence of diabetes continues to rise—particularly Type 2 diabetes—there’s a growing need for accurate, real-time, and user-friendly monitoring solutions.

Current Market Size and Growth Trajectory

As of 2024, the global Glucose Sensors Market is valued at over USD 12 billion and is expected to reach USD 25 billion by 2030, growing at a compound annual growth rate (CAGR) of 10–12%. This rapid expansion is being driven by:

Increasing diabetic population

Growing awareness and adoption of preventive healthcare

Technological advancements in sensor design

Expanding insurance coverage and reimbursement support in developed countries

Key Regional Insights

1. North America

Largest market share, dominated by the U.S.

Strong presence of top players like Dexcom, Abbott, and Medtronic

High adoption of CGM devices among Type 1 diabetics

Robust insurance infrastructure and supportive FDA pathways

2. Europe

Strong growth in countries like Germany, UK, and France

Growing elderly population and national diabetes screening programs

Emphasis on digital health integration in public healthcare systems

3. Asia-Pacific

Fastest-growing region due to increasing diabetic prevalence in China, India, and Japan

Rise in middle-class income, digital literacy, and wearable adoption

Government health campaigns encouraging early screening and remote care

4. Latin America, Middle East & Africa

Emerging opportunities driven by urbanization and changing lifestyles

Limited penetration of advanced glucose monitoring technologies

Potential for growth through public-private partnerships and mobile health solutions

Market Segmentation

The Glucose Sensors Market can be segmented based on:

Technology: Enzymatic sensors, optical sensors, electrochemical sensors

Type: Continuous sensors, strip-based sensors, non-invasive sensors

End-User: Hospitals, clinics, home care settings, fitness & wellness centers

Distribution Channel: Retail pharmacies, online platforms, direct medical device sales

Key Industry Drivers

Rising Diabetes Prevalence

The global diabetic population is expected to surpass 643 million by 2030.

Increasing obesity and sedentary lifestyles are accelerating Type 2 diabetes cases.

Preference for Continuous and Real-Time Monitoring

CGMs offer better glucose trend data, helping reduce hypoglycemic episodes.

Real-time data enables personalized treatment adjustments.

Technological Advancements

Use of AI, machine learning, and cloud-based platforms

Sensors with longer lifespan, smaller sizes, and enhanced accuracy

Non-invasive solutions under development (e.g., via sweat or interstitial fluids)

Shift Toward Preventive Healthcare

Early detection and management of pre-diabetes using wearable sensors

Integration of glucose tracking into smartwatches and fitness devices

Challenges and Restraints

Despite rapid growth, the glucose sensors market faces several challenges:

High cost of advanced devices like CGMs in low-income regions

Accuracy and calibration issues, especially in non-invasive sensors

Lack of awareness among newly diagnosed patients

Limited insurance coverage in some emerging markets

Competitive Landscape

The Glucose Sensors Market is highly competitive and led by both established players and startups:

Abbott Laboratories – Leader with FreeStyle Libre systems

Dexcom, Inc. – Pioneer in real-time CGM technology

Medtronic plc – Innovator in sensor-integrated insulin pumps

Senseonics – Known for implantable CGM solutions (Eversense)

New Entrants – Apple, Samsung, and various healthtech startups are investing in non-invasive glucose sensing technologies integrated into wearables

Strategic collaborations, FDA approvals, and R&D investments are key areas of focus for companies aiming to gain a competitive edge.

Future Outlook

The next five years will be defined by:

Integration with AI and predictive analytics for proactive diabetes management

Expansion of non-invasive glucose sensors targeting fitness and wellness markets

Growing emphasis on personalized care, with data-driven therapy planning

Remote monitoring capabilities tied to telemedicine platforms

Regulatory innovation, expediting approval and reimbursement pathways

Conclusion

The Glucose Sensors Market is undergoing a transformative shift—from basic glucose tracking to comprehensive, connected, and user-friendly healthcare solutions. With continued innovation, market expansion in emerging economies, and increasing consumer awareness, the industry is poised for sustained growth and technological disruption. Stakeholders that prioritize accessibility, affordability, and data integration will lead the next wave of advancements in this critical segment of diabetes care.

0 notes

Text

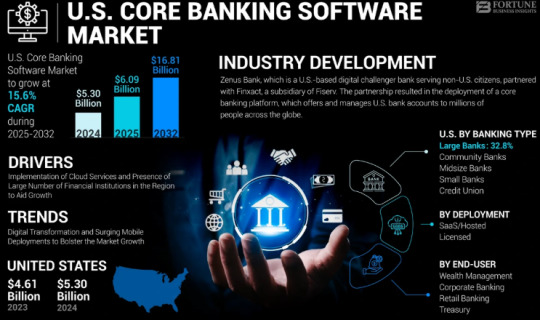

The U.S. Core Banking Software Market Size, Share | CAGR 15.6% during 2024-2030

The U.S. core banking software market Size was valued at USD 5.30 billion in 2024 and is projected to grow from USD 6.09 billion in 2025 to USD 16.81 billion by 2032, exhibiting a CAGR of 15.6% during the forecast period. Driven by the modernization of legacy banking systems, increasing customer demand for digital-first banking experiences, and adoption of cloud-native platforms, the U.S. banking industry is rapidly shifting toward agile, API-driven core banking systems.

Key Market Highlights:

2024 U.S. Market Size: USD 5.30 billion

2025 U.S. Market Size: USD 6.09 billion

2032 U.S. Market Size: USD 16.81 billion

CAGR (2025–2032): 15.6%

Market Outlook: Cloud-first transformation of retail and commercial banking infrastructure

Leading Players in the U.S. Market:

FIS (Fidelity National Information Services)

Finastra

Temenos USA

Oracle Financial Services Software

Jack Henry & Associates

SAP America

nCino

Infosys (EdgeVerve)

Thought Machine

Backbase

Mambu

Q2 Holdings

TCS BaNCS (U.S. operations)

Request Free Sample PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/u-s-core-banking-software-market-107481

Market dynamics:

Growth Drivers:

Legacy System Modernization: Traditional banks are replacing decades-old core systems to enable agility, scalability, and faster innovation.

Rise of Digital-Only Banks & Neobanks: Challenger banks are opting for coreless and cloud-native platforms to deliver real-time banking experiences.

Regulatory Mandates: U.S. regulations increasingly demand transparency, real-time compliance, and modular tech stacks.

Omnichannel and Mobile Banking Boom: Surge in mobile-first customers is accelerating demand for flexible and API-driven core systems.

Adoption of BaaS & Embedded Finance: Banks are embedding financial services into non-banking platforms, requiring agile backend core systems.

Key Opportunities:

AI-Powered Core Modernization: Integration of AI for risk scoring, predictive analytics, and process automation

Cloud Migration Projects: Large-scale re-platforming from on-premise to cloud-native or hybrid models

Banking-as-a-Service (BaaS): U.S. institutions offering core services to fintechs and enterprises

Open Banking APIs: Ecosystem expansion through developer-friendly, regulatory-compliant APIs

Personalized Customer Experience Engines: Data-driven personalization built directly into core systems

Technology & Application Scope:

Deployment Models:

Cloud-native

On-premises

Hybrid (transitional)

Core Features:

Customer and account management

Payments and transaction processing

Lending and credit modules

Risk and compliance automation

Real-time reporting and dashboards

Target Users:

Retail banks

Credit unions

Community banks

Commercial and corporate banks

Neobanks and fintechs

Speak to Analysts: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/u-s-core-banking-software-market-107481

Recent Developments:

January 2024 – A top-10 U.S. bank announced a $700M multiyear plan to migrate its entire core system to a cloud-native microservices architecture with Temenos and AWS.

October 2023 – Jack Henry & Associates launched a new AI-powered fraud prevention module integrated into its core platform, reducing false positives by 45%.

July 2023 – A mid-sized credit union in the Midwest completed a legacy core banking system overhaul, leading to a 22% increase in customer satisfaction due to improved digital banking capabilities.

Trends Shaping the U.S. Core Banking Market:

Composable Banking Architecture: Shift toward modular, plug-and-play architecture

AI & Machine Learning in Core: Real-time fraud detection, dynamic credit risk models, and intelligent automation

Blockchain Integration: Experiments in real-time settlement, decentralized identity, and smart contracts

Low-Code/No-Code Customization: Democratization of development within banking teams

Cybersecurity Embedded in Core: Zero-trust frameworks and secure-by-design approaches

Conclusion:

The U.S. core banking software market is undergoing a significant transformation, driven by rising customer expectations, digital competition, and the imperative to stay compliant and resilient. The future belongs to banks that embrace modular, cloud-native, and API-driven core platforms—designed to scale, personalize, and evolve. As the market accelerates toward modernization, technology vendors and banks alike are finding immense value in flexible ecosystems, open banking capabilities, and real-time innovation.

Frequently Asked Questions: 1. What is the projected value of the global market by 2032?

2. What was the total market value in 2024?

3. What is the expected compound annual growth rate (CAGR) for the market during the forecast period of 2025 to 2032?

4. Which industry segment dominated market in 2023?

5. Who are the major companies?

6. Which region held the largest market share in 2023?

#U.S. Core Banking Software Market Share#U.S. Core Banking Software Market Size#U.S. Core Banking Software Market Industry#U.S. Core Banking Software Market Driver#U.S. Core Banking Software Market Growth#U.S. Core Banking Software Market Analysis#U.S. Core Banking Software Market Trends

0 notes

Text

Rising Demand for Safer Spaces: A Strategic Analysis of the Global Smoke Detector Market (2022–2030)

Smoke Detector Market Overview

The global smoke detector market has witnessed consistent growth over the past decade, driven by increasing awareness of fire safety, stringent building safety regulations, and technological advancements. The rise in urban infrastructure, smart home adoption, and industrial safety mandates are key factors propelling market expansion.

The global smoke detector market was valued at USD 1.1 billion in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 7.30% from 2022 to 2030, reaching approximately USD 1.9 billion by the end of the forecast period.

Market Dynamics

Drivers

Increasing Fire Safety Regulations: Governments and regulatory bodies worldwide are implementing stricter fire codes in commercial and residential buildings.

Smart Home Integration: Integration of IoT in fire safety systems has spurred the demand for smart smoke detectors.

Growing Awareness: Public awareness campaigns about fire hazards and preventive systems are boosting adoption in emerging economies.

Restraints

High Installation Costs: Advanced and interconnected systems can be costly, especially for small businesses or older infrastructure retrofits.

False Alarms & Maintenance Issues: Traditional detectors can trigger false alarms, leading to user dissatisfaction and additional maintenance needs.

Opportunities

AI-Powered Detection Systems: Use of AI and machine learning in detection mechanisms can enhance accuracy and response time.

Expansion in Emerging Markets: Untapped markets in Asia, Africa, and Latin America present lucrative opportunities due to rising construction activity.

Regional Analysis

North America

Dominates the market due to early adoption of smart technologies and stringent building codes, especially in the U.S. and Canada.

Europe

Holds a significant share, with strong fire safety legislation across the UK, Germany, France, and Nordic countries.

Asia-Pacific

Expected to witness the fastest growth rate. Urbanization, smart city projects, and expanding real estate in China, India, and Southeast Asia drive demand.

Latin America and Middle East & Africa

Gradual growth driven by infrastructure development and increasing awareness of fire safety regulations.

Segmental Analysis

By Product Type

Ionization Smoke Detectors

Photoelectric Smoke Detectors

Dual Sensor Smoke Detectors

Photoelectric detectors dominate due to better performance in detecting smoldering fires.

By Power Source

Battery-Powered

Hardwired with Battery Backup

Hardwired Only

Battery-powered detectors lead due to ease of installation and flexibility.

By End User

Residential

Commercial

Industrial

The residential segment holds the largest share, driven by consumer safety awareness and home insurance incentives.

Request PDF Brochure: https://www.thebrainyinsights.com/enquiry/sample-request/13143

List of Key Players

Honeywell International Inc.

Johnson Controls

Siemens AG

Schneider Electric

Hochiki Corporation

Robert Bosch GmbH

BRK Brands Inc. (Newell Brands)

Nest Labs (Google LLC)

Halma plc

United Technologies Corporation

Key Trends

Shift towards smart, connected detectors with mobile alerts and remote control.

Integration with home automation systems and voice assistants like Alexa and Google Assistant.

Rising investment in AI-enhanced fire detection solutions.

Emergence of eco-friendly and low-power detection technologies.

Conclusion

The smoke detector market is poised for robust growth, fueled by regulatory backing, technological innovation, and increasing demand for residential and industrial safety. As smart city initiatives and building modernization accelerate, so will the opportunities in this critical life-saving sector.

For Further Information:

Market Introduction

Market Dynamics

Segment Analysis

Some of the Key Market Players

0 notes

Text

Pharmacy Benefit Manager Market Set to Expand with Growing Demand for Cost-Effective Drug Management

The global Pharmacy Benefit Manager market is undergoing significant transformation driven by the evolving healthcare ecosystem, rising prescription drug spending, and growing emphasis on cost containment. Pharmacy Benefit Managers entities that act as intermediaries between insurers, pharmacies, and drug manufacturers play a crucial role in managing drug formularies, negotiating rebates, and streamlining access to medications. As stakeholders seek greater efficiency and transparency in pharmaceutical spending, the PBM market is emerging as a critical component of healthcare management, especially in the United States, where prescription drug costs represent a substantial share of healthcare expenditure.

Market Dynamics and Growth Drivers

Several key factors are contributing to the growth of the PBM market. Firstly, the increasing burden of chronic diseases such as diabetes, cardiovascular conditions, and mental health disorders has led to a surge in prescription drug utilization. This, in turn, has amplified the need for effective drug benefit management solutions. PBMs are instrumental in implementing evidence-based formularies and utilization management programs that help curb unnecessary spending while ensuring appropriate patient care.

Secondly, rising healthcare costs continue to pressure payers, prompting a greater reliance on PBMs to control drug prices through rebate negotiations and formulary management. The ability of PBMs to aggregate demand and negotiate discounts with manufacturers provides a powerful cost-containment mechanism for health plans and employers.

Moreover, technological advancements such as real-time benefit tools, electronic prior authorization systems, and data analytics platforms are enhancing PBMs’ ability to optimize drug selection, track patient adherence, and predict outcomes. Integration of AI-driven analytics and machine learning is also allowing PBMs to deliver more personalized, value-based services.

Market Segmentation and Key Players

The PBM market is segmented based on service type (formulary management, benefit plan design, specialty pharmacy services, drug utilization review), end-users (employers, insurance companies, government programs), and region. North America, particularly the United States, dominates the global market due to the country’s complex pharmaceutical supply chain and the critical role of PBMs in healthcare cost control.

Some of the leading PBM providers include CVS Caremark, Express Scripts (a Cigna company), OptumRx (a subsidiary of UnitedHealth Group), Prime Therapeutics, and MedImpact Healthcare Systems. These firms have integrated vertically with insurers, health systems, and retail pharmacies, creating consolidated healthcare networks that manage both cost and care delivery.

Regulatory and Transparency Challenges

Despite their growing importance, PBMs have faced increasing scrutiny from regulators and stakeholders due to concerns about opaque pricing practices and rebate retention. Critics argue that PBMs may not always pass negotiated rebates and discounts on to payers or patients, thereby contributing to high out-of-pocket drug costs.

In response, several legislative and regulatory initiatives have emerged, aiming to enhance transparency and accountability. The U.S. Federal Trade Commission (FTC) and state governments have initiated investigations and proposed new rules requiring PBMs to disclose rebate structures, pricing agreements, and conflicts of interest. These regulatory efforts are expected to reshape the market by encouraging more open and equitable practices.

Emerging Trends and Strategic Shifts

One of the most notable trends in the PBM market is the rise of transparent and pass-through PBM models. Unlike traditional models, transparent PBMs charge a flat administrative fee and pass 100% of manufacturer rebates to clients. This shift is gaining momentum among employers and health plans seeking more predictable drug benefit costs.

Another emerging trend is the integration of specialty pharmacy management. Specialty drugs, which are high-cost medications used to treat complex conditions, now account for a large portion of pharmaceutical spending. PBMs are investing in dedicated specialty pharmacy divisions to provide tailored services such as medication therapy management, patient education, and adherence monitoring.

Additionally, value-based contracting is gaining traction. Under this model, drug reimbursement is linked to clinical outcomes rather than volume. PBMs are increasingly entering outcome-based agreements with pharmaceutical manufacturers to ensure that drug spending translates into measurable health improvements.

Outlook and Conclusion

The Pharmacy Benefit Manager market is poised for continued expansion, driven by the dual imperatives of cost containment and value optimization. However, the market’s future trajectory will depend heavily on regulatory developments, market consolidation trends, and the ability of PBMs to adapt to evolving payer and patient expectations.

As the healthcare industry shifts toward value-based care models, PBMs that embrace transparency, innovation, and collaborative partnerships will be best positioned to thrive. The next phase of the PBM market will likely be characterized by tighter oversight, enhanced digital capabilities, and a renewed focus on aligning incentives across the healthcare value chain.

0 notes

Text

Cardiac Monitoring Devices Market Forecast to Reach $48.6B by 2032

The Cardiac Monitoring Devices Market is undergoing robust expansion. In 2021, it was valued at approximately USD 7.7 billion and is projected to grow at a steady compound annual growth rate (CAGR) of around 5.9% through 2031. Other forecasts suggest the market may grow from USD 29.1 billion in 2023 to USD 48.6 billion by 2032. This growth is being driven by the rising global burden of cardiovascular diseases, aging demographics, and technological advancements in wearable and implantable cardiac monitoring solutions.

To Get Free Sample Report :https://www.datamintelligence.com/download-sample/cardiac-monitoring-devices-market

Key Market Drivers