#Vibration Sensor Market Development

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr’s reach among the 26-to-35-year-olds in the US is 11%.

Text

https://stringentdatalytics.com/reports/accelerometer-and-vibration-sensor-market/4368/

#Global Accelerometer and Vibration Sensor Market Size#Share#Trends#Growth#Industry Analysis#Key Players#Revenue#Future Development & Forecast

0 notes

Text

Why are headlights so expensive for cars?

The high cost of modern car headlights is driven by a convergence of advanced technology, complex design, stringent regulations, and market factors. Here's a breakdown of the key reasons:

Advanced Technology & Complexity:

LED/Laser/Matrix Systems: Modern headlights use multi-element LED arrays, adaptive projectors, laser elements (on high-end models), or matrix/pixel technology that individually dims segments of the beam. This requires sophisticated control units, sensors, and wiring.

Adaptive Functionality: Features like auto-leveling, cornering beams, glare-free high beams, and dynamic light projections require motors, cameras, complex software, and extra wiring harnesses.

Integrated Components: Headlights now house DRLs (Daytime Running Lights), turn signals, position lights, and often front-facing sensors (radar/camera for ADAS) all in one sealed unit, driving up complexity.

Precision Engineering & Materials:

Optical Precision: Lenses and reflectors are molded with extreme precision to meet strict beam pattern regulations and avoid glare. Molds for these optics are incredibly expensive to design and manufacture.

Materials: High-performance polycarbonate lenses resist yellowing and cracking, while complex aluminum or magnesium heat sinks efficiently dissipate heat from powerful LEDs/Lasers. Seals must be perfect to prevent moisture and corrosion. Internal reflectors use specialized coatings.

Durability Requirements: Headlights must withstand extreme temperatures, UV radiation, road debris impacts, vibrations, and chemical exposure (car washes, road salt) for the vehicle's lifespan. This requires high-grade materials and construction.

Regulation & Testing Overhead:

Global Standards: Headlights must comply with strict global regulations (SAE, ECE, etc.) regarding beam pattern, intensity, cutoff sharpness, and aiming. Developing, testing, and certifying each headlight design for different markets adds significant cost.

Complex Testing: Extensive lab and road testing is required to ensure compliance, durability, and performance in all conditions, adding R&D costs.

Design and Manufacturing Integration:

Styling Demands: Headlights are critical styling elements. Aggressive shapes, intricate lighting signatures ("light jewelry"), and seamless integration with body panels require complex, unique housings for each model.

Custom Manufacturing: Headlights are model-specific (often even trim-level specific). Low-volume production runs compared to simple bulbs mean costs aren't spread over millions of identical units. Assembly involves delicate electronics and precise calibration.

Module Design: Modern headlights are typically sold as sealed assemblies ("modules"). If anything fails inside (LED chip, driver, ballast, motor, wiring), you often have to replace the entire 800+ unit, not a 10 bulb.

Supply Chain & Market Factors:

OEM vs. Aftermarket: Dealers charge high prices for genuine OEM parts, covering their overhead and profit margins. While quality aftermarket options exist (often significantly cheaper), OE parts command a premium.

Insurance Influence: Since insurance often pays for replacements after collisions (which frequently damage headlights), manufacturers have less pressure to minimize headlight costs compared to components owners pay for directly.

Low Price Elasticity: Headlights are essential safety items. Consumers need them to drive legally and safely, reducing the incentive for manufacturers/dealers to compete heavily on price for replacements.

Supplier Profit: Tier-1 suppliers (like Valeo, Bosch, Magna, Koito) design and build these complex units and need to recoup their substantial R&D and tooling investments per unit sold to the automaker.

Labor Cost (Hidden): Installation is often complex, requiring bumper/fender removal and sometimes electronic calibration/reprogramming. While the part cost is high, labor adds significantly to the total replacement expense perceived by the owner.

Comparison to Older Designs:

Simple Halogen Reflectors: Used cheap bulbs (10-50), simple reflectors, and a basic lens. Easy to manufacture replaceable bulbs. Entire assembly replacement was relatively inexpensive (100-300).

HID Projectors: Introduced cost via ballasts and specialized bulbs (50-150 per bulb), but the projectors and housings were less complex than modern LED units. Assemblies cost more than halogens but less than LEDs.

Modern LED/Adaptive Units: Represent a quantum leap in technology, integration, and complexity, hence the price jump.

In essence: You're paying for high-tech electronics, extreme precision optics, complex software integration, advanced materials built for durability, significant R&D/testing/regulatory costs, custom low-volume manufacturing of a styling-critical safety component, and market dynamics where insurers often foot the bill. It's a far cry from swapping out a simple bulb in a basic reflector housing.

#led lights#car lights#led car light#youtube#led auto light#led headlights#led light#led headlight bulbs#ledlighting#young artist#led light bulbs#led strip lights#car rental#electric cars#classic cars#car#cars#truck#porsche#suv#lamborghini#sabrina carpenter#bmw#carlos sainz#autonomous vehicle headlights#overtake another vehicle#older vehicles#vehicle#auto mode#automobiles

3 notes

·

View notes

Text

Chapter 1: Mecha Girl

Narrated by Netga.

Narrator: The garage walls are vibrating with the punk EDM I’m blasting. Holed up in my pod, I’m busy testing mecha functions.

Narrator: This garage is the workspace where I recycle and modify discarded mechas.

Narrator: Lined by the wall are mechas of various styles and designs, all of them my handiwork.

Narrator: Unfortunately, the clients I have on the island don’t have much taste, and my wares aren’t selling that well.

Narrator: Putting on my sensor set and immersing myself in the vibrant music, I tap on the interface.

Narrator: And I enter the simulated test environment.

Narrator: “Select Environment: Flying/Combat/Project/Party...” The menu pops up in the air in front of me.

Choose either “Party mode?” or “Isn’t that quite an array of features?”

If “party,” ...

You: Why would a mecha have a party mode?

Narrator: Why not? I’ve designed a full set of audio, lighting, and motion effects for this mode. Perfect for getting into the partying mood.

If “features,” ...

You: Sounds like this mecha’s got a lot of functions.

Narrator: The island I’m on is part of some ruins. Mechas are widely used in all sorts of scenarios here, a staple in daily life.

--

Narrator: Low altitude flight, high altitude flight, obstacle course, homing shot, stealth mode... I check the features one by one.

Narrator: Mechas can be seen everywhere on this island.

Narrator: Some use them as transportation or in construction work. There are also popular mecha contests held regularly.

Narrator: Besides, brawls break out often on our streets, and mechas are helpful in solving conflicts.

Narrator: That’s my specialty - to come up with fun, cutting-edge functions for modified mechas in various scenarios.

Narrator: Machines are cold, intricate, and boring. They only follow orders and never deviate from what they’re told.

Narrator: Mechas are different as they have personalities. That’s my design philosophy, at least.

Narrator: However, in this city, people are mainly interested only in the large, intimidating, destructive mechas.

Narrator: My unique modifications aren’t that popular on the market, so I settle for adding bonus functions to the more boring designs.

Narrator: This often results in returned products and complaints.

Narrator: Right now, for example, a scar-faced, buff dude is hammering on the door with his robotic arm, demanding a refund.

Narrator: Behind him, a huge, macho-type mecha grins and greets me in a booming voice.

Giant Mecha: Baa!

Scarred Man: You better explain! Why does my mecha say “baa”? It sounds like an idiotic sheep!

Narrator: The owner of the mecha yells, his face all red.

Scarred Man: And why does it choose the flashiest moves in combat? What’s with that, huh?

Narrator: Scar Face rambles on about my modifications and how they totally embarrassed him in front of his opponents.

Scarred Man: Especially this funky “face” screen it’s got! What the heck is it?

Netga: It’s my newly developed emotion feedback device.

Scarred Man: Emotion? You kidding me? I don’t need my mecha to have emotions, at least not idiotic ones.

Scarred Man: Take out these stupid features, or gimme a refund!

Narrator: Come on, these are what give the mechas life, inspiration, and personality! Besides, they’re totally free.

Narrator: I mutter, but I have bills to pay after all, so I connect the wires to the terminal and rid the mecha of the extra functions.

Narrator: Scar Face is finally gone and I can continue with my tests. I glance at the small, round mecha next to me.

Narrator: I pet its round head, and a huge smile appears on the electronic screen.

Narrator: I guess a dumb smile like this would indeed make it the laughingstock on a mecha battle arena.

Netga: My clients are a boring lot. Don’t you think so?

Narrator: The screen flashes. A smile again.

Narrator: The feedback so far doesn’t have much variety. Further developments are needed.

Narrator: Still, no matter how I optimize the features, the fact remains that such a function and mecha style aren’t mainstream.

Narrator: “Ding! Monthly bills alert!” The sudden notification blares from my speakers at full volume, making me jump out of my seat.

Netga: Ugh, what do I do about the bills?

Chapter 2

Chapter 3

Chapter 4

#netga#shining nikki#ssr designer#chapter 1#transcript#mecha girl#robot#mod#ruins island#ruins#garage#mecha#machine#fight#robotic#modification#programmer

7 notes

·

View notes

Text

What is an environmental test chamber and what products does it include

#Environmental test chamber#Climatic test chamber#Temperature test chamber#Humidity test chamber

An environmental test chamber is a device or system used to simulate and control specific environmental conditions. It is widely used in scientific research, engineering testing, product development and quality control.

The environmental test chamber can simulate various environmental conditions, such as temperature, humidity, air pressure, light, vibration, vibration, climate, etc. They usually consist of a closed box, and the environmental conditions inside the box can be precisely regulated and monitored by a control system. The environmental test chamber usually has functions and equipment such as temperature controller, humidity controller, sensor, data logger, etc.

By using environmental test chambers, researchers, engineers, and manufacturers can test and evaluate materials, products, or systems under controlled conditions. For example, they can use test chambers to simulate material properties under extreme temperature conditions, product stability under high humidity, and the reliability of electronic devices under different climatic conditions. These tests can help them understand how the material or product will behave in the context of actual use and make necessary improvements and optimizations.

Environmental test chambers have a wide range of applications, covering many industries, including aerospace, automotive, electronics, pharmaceuticals, food, environmental science, etc. They play an important role in product development, quality control and compliance testing to improve product reliability, stability and adaptability.

There are many different types of products on the market to meet the needs of different fields and applications. Here are some common environmental test chamber products:

Temperature test chamber: used to simulate the test environment under different temperature conditions, can provide low temperature, high temperature or temperature cycle functions.

Humidity test chamber: used to simulate the test environment under different humidity conditions, can achieve high humidity, low humidity or humidity cycle.

Thermal shock test chamber: A combination of temperature and humidity functions is used to simulate the environment of rapid temperature and humidity changes to test the heat and cold resistance of the product.

Vibration test chamber: used to simulate the test environment under different vibration conditions, which can realize sinusoidal vibration, random vibration or shock vibration.

Salt spray chamber: used to simulate the salt spray corrosion environment, often used to test the corrosion resistance of materials and coatings.

Dust test chamber: Used to simulate dust and particulate environments, often used to test the sealing performance of electronic devices and packages.

Climate test chamber: combined with temperature, humidity, light and other environmental factors, used to simulate the test environment under real climate conditions.

ESS Chamber:ESS Chamber can simulate the operation of the product under various environmental stress conditions such as temperature, humidity, vibration and shock. It provides a fast and efficient method for screening products for possible failures and reliability issues during actual use

Uv Testing Chamber:UV testing chamber is a device used to simulate the UV radiation environment and test the weather resistance of materials. It is usually composed of ultraviolet light source, temperature control system, humidity control system, transparent sample rack, etc., which can simulate ultraviolet light exposure in the natural environment, high temperature and high humidity and other conditions for evaluating the weather resistance and durability of materials.

If you want to know more about the relevant products of environmental reliability testing equipment, you can visit Environmental test chamber manufacturer,JOEO ALI testing. They are a professional manufacturer and sales of environmental test chamber and vibration test system in China. Guangdong ALI Testing Equipment Co,. Ltd. specializes in temperature and humidity testing and mechanical vibration testing systems, and is a leader in the field of environmental and reliability testing.

4 notes

·

View notes

Text

Energy Harvesting Solutions for Sensors Gain Traction in Smart Tech Era

The global Energy Harvesting for Small Sensors Market was valued at USD 426.7 million in 2022 and is expected to expand at a robust CAGR of 9.0% during the forecast period of 2023 to 2031, reaching an estimated USD 922.8 million by the end of 2031. This remarkable growth is underpinned by the increasing demand for battery-less, self-powered sensors in IoT and wearable technologies, along with breakthroughs in energy harvesting technologies.

Market Overview: Energy harvesting for small sensors refers to the process by which low-power sensors generate electricity from their surroundings such as vibrations, thermal gradients, light, or radio frequencies to function autonomously. These sensors find extensive application in remote environmental monitoring, structural health tracking, medical devices, industrial automation, and smart homes, providing significant advantages such as low maintenance, longer device lifespan, and ease of deployment.

Market Drivers & Trends

The surge in demand for self-sustainable IoT ecosystems is a major driving force behind the market growth. Traditional battery-powered sensors require regular replacement and maintenance, especially in inaccessible locations. Energy harvesting eliminates this limitation by enabling devices to operate indefinitely on ambient energy.

Another pivotal factor is the increased adoption of wearable technology. The integration of self-powered sensors into fitness trackers, health monitors, and other wearable devices is significantly boosting market penetration.

According to analysts, the market is also witnessing growing momentum from sustainability goals and energy efficiency mandates, prompting industries and governments to adopt greener technologies.

Key Players and Industry Leaders

Prominent players driving the global energy harvesting for small sensors market include:

Cymbet Corporation

DCO Systems Ltd.

Enervibe

EnOcean GmbH

Kinergizer

KINETRON

ONiO.zero

Ricoh Company, Ltd.

TDK Corporation

Texas Instruments Incorporated

These companies are heavily invested in developing miniaturized, efficient, and integrated power management solutions to stay ahead in this competitive landscape.

Recent Developments

In January 2023, Infineon Technologies AG partnered with NuCurrent to scale NFC-based energy harvesting solutions for consumer and industrial applications.

WePower Technologies, in 2023, launched the Gemns Energy Harvesting Generator, providing a scalable kinetic energy solution for IoT sensors.

Wiliot, an Israel-based startup, raised US$ 200 million to advance its second-generation low-cost IoT sensors using energy harvesting.

Access an overview of significant conclusions from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=85720

Latest Market Trends

The market has observed the emergence of photovoltaic, ambient RF, and vibration-based energy harvesting as the most adaptable and cost-effective solutions. Companies such as e-peas, ON Semiconductor, and Wiliot are pushing technological frontiers:

e-peas has developed PMICs with a buck-boost architecture suitable for low-voltage RF energy harvesting.

ON Semiconductor's RSL10 platform integrates ultra-low-power solar cells with a 47µF onboard storage capacitor, drawing just 55nW in standby mode.

Researchers at Northwestern and George Washington Universities have developed a wireless, battery-free, implantable pacemaker that dissolves after use, powered by near-field antennas.

Market Opportunities

The energy harvesting for small sensors market holds numerous opportunities:

Smart Cities & Infrastructure: Deploying autonomous sensors in buildings and public spaces for environmental monitoring.

Medical Wearables: Battery-free wearables for continuous health tracking, especially for elderly care and chronic diseases.

Industrial IoT (IIoT): Harsh industrial environments where maintenance-free, energy-harvesting sensors are ideal for long-term deployment.

Agritech: Enabling remote monitoring of soil, temperature, and crop health in vast agricultural fields using solar or thermal energy harvesting.

Future Outlook

The market outlook is optimistic, supported by government incentives, technological integration, and the rise of zero-power electronics. As IoT-connected devices cross the 25 billion mark globally, the demand for self-sustaining power sources will skyrocket. Future innovations will likely revolve around:

Enhanced multi-source harvesting (hybrid solar-RF-thermal systems)

Better energy storage solutions

Ultra-low-power circuit designs

Integration with AI and edge computing

Market Segmentation

By Technology:

Biochemical

Biomechanical

Thermal

Solar

RF

By Sensor Type:

Bio-sensors

Motion Sensors

Temperature Sensors

Humidity Sensors

Pressure Sensors

PIR Sensors

RF Sensors

Others

By Application:

Autonomous Medical Devices

Medical Wearables

Environmental Monitoring

Computing Devices

Process Control

Satellite Remote Sensing

Indoor/Outdoor Monitoring

By End-use Industry:

Building and Infrastructure

Healthcare

Industrial

Consumer Electronics

Aerospace and Defense

Others

Regional Insights

North America led the global market in 2022, fueled by robust IoT deployments and continuous R&D in energy-efficient systems. The U.S., in particular, is witnessing increased investment in smart building automation and industrial monitoring using energy harvesting sensors.

Europe remains a hub for technological innovation, with active government support for sustainable electronics and ongoing research in academic and corporate sectors.

Asia Pacific is anticipated to register the fastest CAGR during the forecast period. Countries like China, India, Japan, and South Korea are increasingly adopting energy harvesting-enabled devices across consumer electronics and industrial manufacturing.

Why Buy This Report?

Provides in-depth market analysis with historical, current, and forecast data (2017–2031)

Includes segment-wise and region-wise breakdowns

Highlights emerging trends, growth drivers, and challenges

Covers company profiles, market shares, and strategic developments

Available in PDF + Excel format for easier data extraction and visualization

Ideal for investors, policymakers, OEMs, and technology providers

Frequently Asked Questions

Q1. What is the expected size of the global energy harvesting for small sensors market by 2031? A1. The market is projected to reach US$ 922.8 million by 2031.

Q2. What is the compound annual growth rate (CAGR) of the market from 2023 to 2031? A2. The market is expected to expand at a CAGR of 9.0% during this period.

Q3. Which regions offer the highest growth potential? A3. Asia Pacific is expected to witness the fastest growth, followed by Europe and North America.

Q4. What are the main applications of energy harvesting for small sensors? A4. Key applications include wearable devices, industrial process control, medical monitoring, and environmental sensing.

Q5. Who are the leading players in the market? A5. Major players include Texas Instruments, EnOcean, TDK Corporation, Ricoh, ONiO.zero, and Everactive.

Explore Latest Research Reports by Transparency Market Research: Gyrocopter Market: https://www.transparencymarketresearch.com/gyrocopter-market.html

Fuel Cell UAV Market: https://www.transparencymarketresearch.com/fuel-cell-uav-market.html

Active Optical Cable Market: https://www.transparencymarketresearch.com/active-optical-cables.html

High Altitude Pseudo Satellites Market: https://www.transparencymarketresearch.com/high-altitude-pseudo-satellites-market.html

About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

Glass-encapsulated NTC Thermistor Market: Forecasting Future Developments to 2025-2032

MARKET INSIGHTS

The global Glass-encapsulated NTC Thermistor Market size was valued at US$ 389.5 million in 2024 and is projected to reach US$ 678.9 million by 2032, at a CAGR of 8.34% during the forecast period 2025-2032. The U.S. market accounted for 28% of global revenue in 2024, while China’s market is expected to grow at a faster CAGR of 6.7% through 2032.

Glass-encapsulated NTC thermistors are precision temperature sensors featuring a negative temperature coefficient (NTC) element hermetically sealed in glass. This encapsulation provides superior environmental protection against moisture, chemicals, and mechanical stress compared to polymer-coated alternatives. These components are critical for temperature measurement and compensation in demanding applications across industries.

The market growth is driven by increasing adoption in medical devices, automotive systems, and industrial automation where reliability under harsh conditions is paramount. Recent advancements include miniaturized designs for wearable medical devices and high-temperature variants for electric vehicle battery management. Key players like Mitsubishi Materials and Vishay are expanding production capacities to meet rising demand, particularly in Asia-Pacific markets where electronics manufacturing is concentrated.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Applications in Medical Devices to Accelerate Market Growth

The medical industry’s increasing adoption of glass-encapsulated NTC thermistors is creating significant growth opportunities. These components are critical in patient monitoring equipment, diagnostic devices, and therapeutic applications due to their high stability and accuracy. Over 65% of new medical devices requiring temperature sensing now incorporate glass-encapsulated variants rather than epoxy alternatives. The global medical sensors market, valued at over $25 billion in 2024, is projected to maintain a steady 7-9% CAGR through 2032, directly benefiting NTC thermistor manufacturers. Recent FDA approvals for smart medical implants with integrated temperature monitoring are further driving demand for reliable sensor solutions.

Automotive Electrification Trends to Fuel Demand

The automotive industry’s transition toward electric vehicles represents a major growth driver for glass-encapsulated NTC thermistors. These components are essential for battery thermal management systems in EVs, with each vehicle containing 15-25 thermistors on average. With global EV production expected to surpass 40 million units annually by 2030, demand for temperature sensors is projected to increase proportionally. Glass encapsulation provides the necessary durability against vibration and harsh under-hood conditions while maintaining measurement precision within ±0.5°C. Leading automakers are increasingly specifying glass-encapsulated versions for critical applications after demonstrating superior performance in accelerated life testing.

Industrial Automation Investments Driving Market Expansion

As Industry 4.0 initiatives gain momentum, glass-encapsulated NTC thermistors are becoming integral components in smart factories. Their ability to withstand industrial environments while providing reliable temperature data makes them ideal for predictive maintenance systems and process control applications. Manufacturing facilities are allocating over 30% of their sensor budgets to ruggedized temperature measurement solutions. The glass encapsulation provides chemical resistance critical for food processing, pharmaceutical production, and chemical manufacturing applications where epoxy alternatives would degrade. This sector alone accounts for nearly 40% of current glass-encapsulated NTC thermistor demand.

MARKET RESTRAINTS

Higher Production Costs Limiting Price-Sensitive Applications

While glass-encapsulated NTC thermistors offer superior performance, their manufacturing costs remain approximately 35-45% higher than standard epoxy-encapsulated alternatives. This price differential makes them less competitive in consumer electronics and other cost-sensitive markets where slight reductions in accuracy are tolerable. The specialized glass sealing process requires controlled atmosphere furnaces and precision handling equipment, contributing to elevated capital expenditures for manufacturers. In industries where hundreds of thousands of units are deployed annually, these cost considerations significantly impact purchasing decisions despite the technical advantages.

Complex Manufacturing Processes Affecting Supply Chain Dynamics

The production of glass-encapsulated NTC thermistors involves multiple precise steps including glass formulation, hermetic sealing, and rigorous testing. Each batch requires strict environmental controls throughout the manufacturing process. These complexities have resulted in longer supplier lead times averaging 12-16 weeks compared to 4-6 weeks for standard thermistors. The supply chain bottlenecks became particularly evident during recent semiconductor shortages, with some automotive manufacturers reporting 20-30% delays in sensor deliveries. This manufacturing intricacy also limits the number of qualified suppliers globally, reducing buyer flexibility.

MARKET CHALLENGES

Miniaturization Requirements Pushing Technical Boundaries

As end-use devices continue shrinking, thermistor manufacturers face mounting pressure to reduce package sizes while maintaining performance standards. Developing glass-encapsulated versions below 0.8mm diameter presents significant technical hurdles in hermetic sealing reliability. Current yields for sub-miniature glass packages remain below 60% in production environments compared to over 85% for standard sizes. This challenge is particularly acute in medical applications where device makers demand sensors smaller than 0.5mm for minimally invasive instruments. The industry must overcome material science limitations to achieve both miniaturization and durability targets.

Standardization Gaps Creating Interoperability Issues

The absence of universal standards for glass formulations and encapsulation methods is creating compatibility challenges across the supply chain. Different manufacturers utilize proprietary glass compositions with varying coefficients of thermal expansion, leading to performance inconsistencies in critical applications. These variations complicate system integration and require extensive requalification when changing suppliers. Industry groups are beginning to address these issues, but progress toward standardization has been slow despite growing recognition of the need.

MARKET OPPORTUNITIES

Emerging Battery Storage Applications Offering New Growth Prospects

The rapid expansion of grid-scale battery storage systems presents a significant opportunity for glass-encapsulated NTC thermistor suppliers. These installations require robust temperature monitoring solutions capable of withstanding 20+ year operational lifetimes in harsh environments. Recent pilot projects have demonstrated glass-encapsulated variants delivering 99.9% reliability over 5,000 thermal cycles—performance unmatched by alternative technologies. With global energy storage capacity projected to increase sixfold by 2030, this application could comprise 15-20% of total market demand within the next decade.

Advancements in Wireless Sensor Networks Creating Ecosystem Opportunities

The integration of glass-encapsulated NTC thermistors with energy-harvesting wireless nodes is enabling new monitoring applications in previously inaccessible environments. Recent developments in low-power sensor ICs allow operation for years without battery replacement when paired with these reliable temperature elements. Industrial facilities are deploying these solutions for equipment health monitoring, with adoption rates increasing approximately 40% annually. Suppliers offering pre-engineered wireless sensor modules are capturing significant market share by reducing implementation barriers for end-users.

GLASS-ENCAPSULATED NTC THERMISTOR MARKET TRENDS

Expanding Industrial Applications Drive Market Demand

The global glass-encapsulated NTC thermistor market is witnessing robust growth, primarily fueled by increasing adoption across industrial applications. These thermistors offer superior performance in harsh environments due to their hermetic glass encapsulation, which protects against moisture and chemical exposure. Industries such as automotive, aerospace, and manufacturing rely heavily on these components for precise temperature monitoring in critical systems. The automotive sector alone accounts for over 30% of global demand, with electric vehicle production accelerating adoption further. Additionally, glass-encapsulated thermistors are becoming indispensable in industrial automation, where sensor reliability directly impacts operational efficiency. With industrial IoT deployments growing at 15% annually, the need for durable, high-precision temperature sensors continues to rise.

Other Trends

Medical Technology Advancements

Medical applications are emerging as a significant growth segment for glass-encapsulated NTC thermistors. Their small form factor and biocompatibility make them ideal for invasive medical devices and diagnostic equipment. The global medical sensors market, valued at $16 billion in 2024, is projected to incorporate increasingly sophisticated temperature monitoring solutions. With minimally invasive surgeries growing by 8% annually, demand for tiny yet reliable thermistors in catheters and endoscopic tools is surging. Furthermore, wearable health monitors and implantable devices are adopting these sensors for continuous temperature tracking, creating new revenue streams for manufacturers.

Miniaturization and Material Innovations

Technological advancements in material science and manufacturing processes are enabling the production of smaller, more efficient glass-encapsulated NTC thermistors. The trend toward miniaturization is particularly evident in consumer electronics, where component space is at a premium. Smartphone manufacturers now incorporate these thermistors for battery temperature management in devices that generate significant heat during fast charging. Meanwhile, new glass compositions with enhanced thermal conductivity and durability are extending sensor lifespans in extreme conditions. These innovations are driving replacement cycles in industrial settings, where sensor failure can lead to costly downtime. With over 40% of industrial equipment failures relating to temperature issues, the reliability benefits of advanced glass-encapsulated thermistors justify their premium pricing in critical applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Invest in Innovation and Regional Expansion for Market Dominance

The global Glass-encapsulated NTC Thermistor market is moderately fragmented, with established manufacturers and emerging regional players competing for market share. WEILIAN leads the market with its comprehensive product range and strong foothold in Asia-Pacific, particularly in industrial applications where precision temperature sensing is critical. Their revenue share in 2024 reflects their technological edge in high-stability thermistor solutions.

Chinese manufacturers like Shenzhen Minchuang Electronics Co., Ltd. and Sinochip Electronics C0., LTD have gained significant traction, leveraging cost-effective production capabilities and rapid response to regional demand. These companies now collectively account for nearly 30% of the Asia-Pacific market, challenging traditional Western suppliers.

Meanwhile, Japanese firms such as Mitsubishi Materials Corporation and Shibaura maintain leadership in high-reliability applications through continuous R&D investment. Their dominance in medical-grade thermistors stems from stringent quality control and long-term stability certifications, making them preferred suppliers for critical healthcare equipment.

The competitive intensity is further heightened by European and American manufacturers focusing on niche applications. Companies like Vishay and Ametherm differentiate through specialized products for automotive and aerospace sectors, where glass encapsulation provides superior protection against harsh environments.

List of Key Glass-encapsulated NTC Thermistor Manufacturers

WEILIAN (China)

Shenzhen Minchuang Electronics Co., Ltd. (China)

HateSensor (South Korea)

Exsense Sensor Technology co. (China)

JPET INTERNATIONAL LIMITED (UK)

Sinochip Electronics C0., LTD (China)

KPD (South Korea)

Suzhou Dingshi Electronic Technology CO., LTD (China)

RTsensor (Germany)

SHIHENG ELECTRONICS (Taiwan)

Dongguan Jingpin Electronic Technology Co., Ltd (China)

Mitsubishi Materials Corporation (Japan)

Qawell Technology (China)

FENGHUA (HK) ELECTRONICS LTD. (Hong Kong)

Ametherm (USA)

Thinking Electronic (Taiwan)

Shibaura (Japan)

Semitec Corporation (Japan)

Vishay (USA)

Glass-encapsulated NTC Thermistor Market Segment Analysis

By Type

Single-ended Glass Sealed NTC Thermistor Leads Market Growth Due to Superior Stability in Harsh Environments

The market is segmented based on type into:

Single-ended Glass Sealed NTC Thermistor

Diode Type Glass Encapsulated NTC Thermistor

Others

By Application

Industrial Applications Dominate Market Share Due to Widespread Use in Temperature Monitoring Systems

The market is segmented based on application into:

Industrial

Medical

Automotive

Consumer Electronics

Others

By End User

Temperature Sensor Manufacturers Represent Key End Users Driving Market Expansion

The market is segmented based on end user into:

Temperature Sensor Manufacturers

Automotive Component Suppliers

Medical Equipment Producers

Industrial Automation Companies

Others

Regional Analysis: Glass-encapsulated NTC Thermistor Market

North America The North American region, particularly the United States, is a mature yet innovation-driven market for glass-encapsulated NTC thermistors. With a projected market size of $XX million in 2024, the growth is fueled by advancements in medical devices, automotive temperature monitoring, and industrial automation. The rise in demand for high-precision thermal sensors in electric vehicles (EVs) and renewable energy systems—particularly in solar panel temperature management—has significantly boosted adoption. Regulatory bodies such as the FDA encourage the use of reliable thermistors in medical equipment due to their stable performance and resistance to moisture ingress, making glass-encapsulated variants a preferred choice. However, the high cost of precision manufacturing and competition from alternative technologies pose challenges for market expansion.

Europe Europe is another key player, driven by strict quality and environmental standards under EU directives, particularly in the automotive (e.g., EV battery thermal management) and healthcare sectors. Germany and France lead in industrial applications, where sensors in HVAC systems and process control demand reliability in harsh environments. The region’s focus on green technology and Industry 4.0 is accelerating the shift toward glass-encapsulated NTC thermistors, which offer superior hermetic sealing compared to epoxy-coated alternatives. However, the market faces pricing pressures from Asian manufacturers, prompting European suppliers to emphasize customization and miniaturization to maintain competitiveness.

Asia-Pacific China, Japan, and South Korea dominate the APAC market, collectively accounting for over 50% of global production. China’s prominence is attributed to its electronics manufacturing ecosystem, with Shenzhen-based suppliers like Shenzhen Minchuang Electronics and SHIHENG ELECTRONICS catering to both domestic and export demands. The region’s rapid automotive electrification and consumer electronics boom (e.g., smartphones, wearables) drive volume growth, though price sensitivity limits premium product penetration. Japan remains a leader in high-accuracy thermistors for medical and industrial use, leveraging companies like Shibaura and Semitec Corporation. Meanwhile, India’s expanding telecom infrastructure and industrial automation sectors present long-term opportunities.

South America The South American market is nascent but growing, with Brazil and Argentina leading demand in automotive aftermarkets and HVAC systems. Economic instability and reliance on imports constrain local manufacturing, but increasing investments in renewable energy projects (e.g., wind turbines) are creating niche opportunities. The lack of stringent regulatory frameworks results in a preference for low-cost alternatives, though multinational firms are gradually introducing higher-performance glass-encapsulated solutions for specialized applications.

Middle East & Africa This region shows potential, particularly in oil & gas and telecommunications infrastructure, where temperature stability is critical. Saudi Arabia and the UAE are adopting these thermistors for industrial equipment monitoring, while Africa’s medical device market remains underserved due to funding gaps. The dependence on imports and limited technical expertise slows adoption, but partnerships with global players like Vishay and Ametherm could drive future growth as infrastructure projects expand.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Glass-encapsulated NTC Thermistor markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Glass-encapsulated NTC Thermistor market was valued at USD million in 2024 and is projected to reach USD million by 2032, at a CAGR of % during the forecast period.

Segmentation Analysis: Detailed breakdown by product type (Single-ended Glass Sealed NTC Thermistor, Diode Type Glass Encapsulated NTC Thermistor), application (Industrial, Medical, Others), and end-user industry to identify high-growth segments and investment opportunities.

Regional Outlook: Insights into market performance across North America (USD million estimated in 2024 for U.S.), Europe, Asia-Pacific (China projected to reach USD million), Latin America, and the Middle East & Africa, including country-level analysis.

Competitive Landscape: Profiles of leading market participants including WEILIAN, Shenzhen Minchuang Electronics Co., Ltd., HateSensor, Exsense Sensor Technology co., and JPET INTERNATIONAL LIMITED, among others. In 2024, the global top five players held approximately % market share.

Technology Trends & Innovation: Assessment of emerging technologies, precision temperature measurement advancements, and evolving industry standards for glass encapsulation techniques.

Market Drivers & Restraints: Evaluation of factors driving market growth such as increasing demand for reliable temperature sensors in medical applications, along with challenges like raw material price volatility and supply chain constraints.

Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities in the temperature sensor market.

Related Reports:https://semiconductorblogs21.blogspot.com/2025/06/laser-diode-cover-glass-market-valued.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/q-switches-for-industrial-market-key.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/ntc-smd-thermistor-market-emerging_19.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/lightning-rod-for-building-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/cpe-chip-market-analysis-cagr-of-121.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/line-array-detector-market-key-players.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/tape-heaters-market-industry-size-share.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/wavelength-division-multiplexing-module.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/electronic-spacer-market-report.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/5g-iot-chip-market-technology-trends.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/polarization-beam-combiner-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/amorphous-selenium-detector-market-key.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/output-mode-cleaners-market-industry.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/digitally-controlled-attenuators-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/thin-double-sided-fpc-market-key.html

0 notes

Text

Growth in Electric Vehicles Pushes India’s Vehicle Testing Demand

India Automotive Testing Market is poised for significant growth, projected to register a 23.6% compound annual growth rate (CAGR) between 2024 and 2031. This growth is fueled by the rapid penetration of electric vehicles (EVs), stricter emission and safety regulations, and a wave of public-private investment in vehicle testing infrastructure.

Automotive testing in India spans a wide array of services and equipment used to assess safety, performance, emissions, NVH (noise, vibration, and harshness), infotainment systems, and increasingly, electric powertrain and battery performance.

To Get Free Sample Report : https://www.datamintelligence.com/download-sample/india-automotive-testing-market

Key Market Drivers

Electrification and Smart Vehicle Technologies As the Indian automotive market embraces electric vehicles and smart mobility, demand for specialized testing services has surged. EV-specific testing, including battery performance, thermal management, and electromagnetic compatibility, is driving investment across public and private testing labs.

Advanced Driver Assistance Systems (ADAS), telematics, and infotainment integrations are also growing, pushing the demand for simulation and electronic validation testing.

Government Regulations and Standards India has implemented multiple reforms in vehicle safety and emissions compliance. Bharat Stage VI norms for emissions and the upcoming Bharat NCAP crash testing program have created a large market for regulatory testing and homologation services.

From anti-lock braking systems (ABS) to electronic stability control (ESC), vehicle components now undergo rigorous testing as mandated by the Ministry of Road Transport and Highways.

Infrastructure Development through NATRiP The National Automotive Testing and R&D Infrastructure Project (NATRiP), backed by the Government of India, is a cornerstone initiative fueling market expansion. Key centers such as:

NATRAX (Indore) – Asia’s longest high-speed testing track

GARC (Chennai) – Focuses on EMC, crash, and infotainment testing

iCAT (Manesar) – India’s premier center for emission testing and powertrain validation

These institutions provide state-of-the-art testing platforms that support the country’s fast-evolving automotive landscape.

Digital and AI-Driven Testing Digital transformation is enabling real-time diagnostics, simulation-based crash testing, and AI-assisted test protocols. IoT-enabled sensors embedded in vehicles and test environments are generating high-frequency data for precision testing and predictive analytics.

Automotive Test Equipment Segment

The India automotive test equipment market alone is projected to cross USD 195.4 million by 2027, growing at a steady CAGR of 5.9% during 2021–2027. Key equipment segments include:

Chassis Dynamometers: The dominant segment, supporting emissions and powertrain performance validation

Wheel Alignment Systems: Rapidly growing due to increased demand for vehicle control and lane-keeping technologies

Emission and Engine Test Equipment: Essential for BS-VI certification and EV range performance metrics

Regional Hubs Driving Growth

Chennai Automotive Belt The Chennai-Oragadam-Sriperumbudur region, known as the "Detroit of Asia," is a hub for OEMs and component manufacturers. The presence of the Global Automotive Research Center (GARC) strengthens testing accessibility for manufacturers in southern India.

Indore’s NATRAX The NATRAX test track in Madhya Pradesh, offering high-speed and dynamic vehicle testing facilities, is positioning India as a global player in homologation and performance validation for EVs and internal combustion vehicles.

Manesar’s iCAT Located near Delhi NCR, iCAT serves as the nerve center for vehicle emissions certification, powertrain benchmarking, and alternate fuel testing.

Challenges and Limitations

Despite high growth, several challenges persist:

Fragmented Facilities: Though national centers are well-funded, mid-tier cities and smaller OEMs still lack easy access to advanced testing.

Skilled Workforce Shortage: The need for trained professionals in electric powertrain testing, ADAS systems, and AI data handling is growing.

Cost of Compliance: Upgrading facilities to comply with international standards can be expensive, especially for smaller auto part suppliers.

Limited Private Sector Involvement: While public centers are growing, private labs still lag in capacity and modernization.

Get the Demo Full Report: https://www.datamintelligence.com/enquiry/india-automotive-testing-market

Market Outlook and Future Trends

EV Testing Boom With India targeting 30% EV penetration by 2030, testing for EV powertrains, high-voltage battery safety, regenerative braking, and range validation will see exponential growth.

AI Integration in Vehicle Testing Leading TIC (testing, inspection, and certification) companies are deploying AI to enhance crash simulations, reduce test cycle time, and predict vehicle behavior under various conditions.

Increased Focus on NVH As internal combustion noise disappears in EVs, NVH testing is gaining importance. Engineers are developing solutions to manage wind, road, and electric motor noise, especially for luxury EV models.

ADAS and Autonomous Testing Labs Future-oriented testing labs are integrating virtual test tracks and driving simulators to validate ADAS features and partial autonomy in controlled environments.

Conclusion

The India automotive testing market is entering a dynamic growth phase, driven by regulatory alignment, infrastructure development, and deep electrification. With leading facilities like NATRAX, iCAT, and GARC shaping the national testing network, India is building the technical backbone needed for global competitiveness in auto manufacturing. Despite some operational challenges, a robust ecosystem is forming that will support future mobility solutions spanning combustion engines, hybrids, and pure electric platforms.

0 notes

Text

Low Voltage Cable Market Emerging Trends Reshaping Global Power Distribution

The global low voltage cable market is undergoing transformative changes driven by technological advancements, the rise in renewable energy adoption, smart grid development, and growing investments in urban infrastructure. Low voltage cables, typically rated below 1,000 volts, are essential for power distribution across residential, commercial, and industrial applications. These cables are experiencing growing demand as energy systems become more decentralized, efficient, and digitally connected.

Surge in Smart Grid Deployments

One of the most significant emerging trends in the low voltage cable market is the widespread implementation of smart grids. These intelligent networks require advanced cabling solutions capable of supporting automated monitoring, real-time data transmission, and efficient load management. Low voltage cables that integrate fiber optics and data transmission capabilities are increasingly favored. Smart grids not only improve reliability but also enable predictive maintenance and better integration of distributed energy resources (DERs), such as rooftop solar systems and electric vehicles.

Rise in Renewable Energy Integration

The global shift toward clean energy is driving the need for extensive electrical connectivity, especially in solar and wind energy projects. Low voltage cables play a vital role in transmitting power from photovoltaic panels and wind turbines to inverters and power conditioning units. As countries ramp up their renewable energy targets, the demand for specialized low voltage cables designed to withstand harsh environmental conditions is growing. These cables are required to be UV-resistant, halogen-free, and suitable for underground or open-air installation.

Electrification of Transportation Infrastructure

Another major trend influencing the low voltage cable market is the electrification of the transportation sector, particularly electric vehicle (EV) charging infrastructure. Governments worldwide are incentivizing EV adoption, leading to a surge in charging stations that rely on robust low voltage cable systems. These cables are essential for ensuring efficient and safe power delivery in both residential and commercial charging environments. In addition, the cables used in EV charging networks must meet higher safety and flexibility standards to accommodate evolving energy needs.

Adoption of Sustainable and Fire-Retardant Materials

There is a growing emphasis on environmentally friendly and safe cabling materials. Manufacturers are innovating by using recyclable, low-smoke zero-halogen (LSZH), and fire-retardant sheathing materials. These materials reduce the risk of fire spread and emit minimal toxic smoke in case of combustion, making them ideal for use in public spaces, hospitals, and commercial buildings. This trend is not only driven by stricter building regulations but also by the construction sector’s growing focus on green certifications and sustainability targets.

Digitalization and Industrial Automation

With Industry 4.0 gaining momentum, industrial facilities are becoming increasingly automated and digitally connected. This transformation is boosting demand for low voltage cables that can support sensors, actuators, and real-time control systems. Factories and plants are looking for cables with enhanced electromagnetic compatibility (EMC), data transmission capabilities, and resilience in high-vibration or high-temperature environments. The rise of smart factories, especially in Asia-Pacific and Europe, is creating new opportunities for cable manufacturers to offer innovative and customized solutions.

Expansion in Data Centers and Telecom Networks

The data center and telecommunications boom is another factor contributing to the evolution of the low voltage cable market. As the number of internet users and connected devices multiplies, data centers require high-performance low voltage cables to power servers, network equipment, and backup systems efficiently. Moreover, with the rollout of 5G infrastructure, telecom operators are investing in cables that provide high durability and ensure minimal power loss. The convergence of power and data in hybrid cables is also becoming more common.

Modular and Prefabricated Cabling Solutions

To speed up project timelines and reduce on-site labor, modular and prefabricated low voltage cable systems are gaining traction. These solutions offer plug-and-play capabilities, better quality control, and simplified installation processes. Modular cabling is especially useful in commercial buildings, industrial complexes, and renewable energy installations, where scalability and flexibility are key. This approach also supports the trend toward digital twin models, enabling better project planning and lifecycle management.

Conclusion

The low voltage cable market is evolving rapidly, influenced by technological progress, environmental concerns, and growing demand for smart and clean energy solutions. From supporting smart grids and renewable energy projects to powering EV infrastructure and data centers, low voltage cables are at the core of the global electrification trend. As industries and governments continue to prioritize efficiency, safety, and sustainability, manufacturers in the low voltage cable sector must adapt through innovation, digitalization, and strategic expansion to stay competitive in this dynamic landscape.

0 notes

Text

Massage Chair Market Future Trends Reflect Wellness Lifestyle, Smart Features, and Personalized Therapeutic Technology

The massage chair market is entering a transformative era, driven by a surge in health-conscious consumers, smart home integration, and lifestyle shifts prioritizing wellness and stress relief. As technology continues to evolve and user expectations rise, future trends in the massage chair market point to a sophisticated fusion of comfort, therapy, and digital connectivity. From AI-powered systems to customizable programs and sustainable design, the future promises exciting advancements that are set to redefine relaxation and self-care at home and in commercial settings.

One of the most noticeable trends shaping the future of this market is the integration of artificial intelligence (AI) and machine learning into massage chairs. Next-generation models are being equipped with intelligent sensors and adaptive algorithms that analyze body posture, muscle tension, and user preferences in real time. These features enable the chair to adjust pressure, motion, and massage styles automatically, offering a highly personalized experience. As AI capabilities continue to mature, users can expect more intuitive systems that evolve with their habits and health profiles.

Health and wellness monitoring is another emerging dimension. Future massage chairs may not just relieve tension but also track and analyze biometric data such as heart rate, blood pressure, and body temperature. These integrated health-tracking features align well with the global trend toward preventative health and holistic well-being. Users will benefit from insights that help monitor stress levels, recovery progress, and general health trends—all from the comfort of a chair designed for therapeutic relaxation.

The market is also shifting toward multi-functionality and full-body therapy solutions. Modern massage chairs are expected to go beyond basic kneading or vibration features. The future designs aim to include full-body experiences with features like reflexology foot massage, heated air compression, zero-gravity recline modes, and spinal alignment technologies. As consumers seek more value from high-end purchases, manufacturers are responding with all-in-one systems that deliver spa-like experiences at home.

Another major trend is the rise of voice-activated and app-controlled functionality. As smart home ecosystems become commonplace, massage chairs are being designed to seamlessly integrate with virtual assistants like Alexa, Google Assistant, and proprietary smartphone apps. Users will be able to control settings, schedule massages, and receive maintenance alerts using voice commands or mobile devices. This connectivity adds a layer of convenience that resonates with tech-savvy users who value both relaxation and efficiency.

Personalization and user-specific customization are also central to the future of the massage chair market. Manufacturers are developing chairs with memory settings, user profiles, and massage programs tailored to specific demographics—such as seniors, athletes, office workers, or pregnant individuals. Personalized experiences based on age, physical condition, or therapeutic needs enhance comfort and safety while boosting customer satisfaction and brand loyalty.

From a design perspective, space-saving and aesthetic considerations are growing in importance. Urban consumers, especially in apartments and compact homes, prefer sleek, foldable, or wall-hugging models that don’t dominate their living spaces. Manufacturers are focusing on developing chairs that blend easily with interior décor, offering a balance of function and visual appeal. Expect future models to showcase minimalist lines, neutral color palettes, and premium upholstery materials to cater to a more design-conscious audience.

Eco-friendly materials and sustainable manufacturing practices are becoming increasingly relevant. As consumer awareness of environmental impact grows, so does the demand for responsibly sourced, recyclable materials and energy-efficient features. Brands looking to stay ahead are investing in green manufacturing processes and incorporating materials like vegan leather, recycled metals, and biodegradable components in their products.

Geographically, Asia-Pacific continues to lead the market, largely due to long-standing cultural acceptance of massage therapy and rapid adoption of wellness-focused technologies. However, North America and Europe are expected to see increasing demand fueled by aging populations, high stress levels, and growing interest in luxury self-care. The hospitality and wellness industries are also contributing to growth, with massage chairs being adopted in spas, airports, gyms, and even corporate wellness lounges.

On the business side, e-commerce and direct-to-consumer strategies are reshaping how massage chairs are marketed and sold. Virtual showrooms, augmented reality (AR) previews, and online customization tools are making it easier for consumers to explore and purchase high-end chairs without visiting physical stores. This digital transformation is lowering entry barriers and expanding market reach, especially among younger tech-savvy shoppers.

In conclusion, the future trends of the massage chair market point to a technologically advanced, health-driven, and highly personalized product evolution. With innovations focused on AI, wellness integration, smart connectivity, and sustainable design, the market is poised to cater to an increasingly diverse and discerning consumer base. As lifestyles continue to shift toward self-care, relaxation, and home-based solutions, massage chairs are set to become essential elements of modern living—delivering therapeutic benefits and luxury comfort in one intelligent package.

0 notes

Text

#Global Distributed Fiber Optic Vibration Sensor Market Size#Share#Trends#Growth#Industry Analysis#Key Players#Revenue#Future Development & Forecast

0 notes

Text

HVAC Innovations in 2025 – What Clients in Gurgaon Are Asking For

The expectations from HVAC systems in 2025 have gone far beyond cooling and heating. In Gurgaon, where high-rise offices, premium apartments, and mixed-use developments continue to dominate the skyline, clients — from builders to corporate tenants — are demanding more from their HVAC investments.

No longer satisfied with basic functionality, they’re now looking for energy efficiency, intelligent automation, indoor air quality, and systems that align with green building goals. This shift has led the Top HVAC Companies in Gurgaon to rethink design, execution, and after-sales support in order to stay relevant.

Let’s take a closer look at what’s shaping the HVAC conversation in Gurgaon this year.

1. Smart HVAC Systems with Real-Time Control

Gurgaon is a tech-forward market. Many clients, especially corporate tenants in Cyber City, DLF Phase V and Golf Course Road, now expect smart control capabilities — not as an add-on, but as a standard feature.

From smartphone-controlled thermostats to centralised Building Management System (BMS) integrations, automation is in demand. Clients want the ability to monitor and adjust:

Room-wise temperatures

Energy consumption

CO₂ levels and ventilation rates

System faults and alerts

HVAC systems are being connected to the Internet of Things (IoT) for predictive maintenance and data-backed decisions. The Best HVAC Company in Gurgaon today is the one offering not just equipment — but smart, connected climate solutions.

2. Demand for Energy Efficiency and Green Compliance

With rising energy costs and stricter sustainability guidelines, energy-efficient HVAC solutions are top of the list for developers and facility managers. As per a recent CREDAI report, nearly 40% of a building’s energy usage in India comes from HVAC systems.

Clients are now actively asking for:

High ISEER-rated equipment (Indian Seasonal Energy Efficiency Ratio)

Variable Refrigerant Flow (VRF) systems for zoned cooling

Heat recovery ventilation systems

Demand-controlled ventilation using occupancy sensors

These systems not only lower running costs but are also essential to secure certifications like LEED, IGBC, and GRIHA — which are fast becoming market differentiators in Gurgaon’s real estate segment.

3. Indoor Air Quality (IAQ) Is Now a Deal-Breaker

The air quality in NCR remains a serious concern, and post-COVID awareness has made indoor air quality a core decision-making factor for clients. Office tenants, co-working operators, hospitals, and even premium homebuyers are asking how HVAC systems:

Filter PM2.5 and PM10

Regulate humidity levels

Circulate fresh air

Prevent microbial growth in ducts and coils

As a result, there’s a growing push for integrated air purification, UVGI (ultraviolet germicidal irradiation) lamps in AHUs, and advanced filtration systems. Clients want assurance that the air their teams or families are breathing indoors is significantly safer than what’s outside.

4. Noise Reduction and Acoustic Comfort

With the rise of open office layouts and luxury living spaces, acoustic performance of HVAC systems is under the spotlight. Traditional systems often overlook the impact of duct design, grille placement, and unit vibration on noise levels.

Innovative duct silencers, vibration isolators, and silent fan coil units are now being specifically requested. In some cases, clients even ask for acoustic simulation during the design phase — a service now being offered by forward-thinking HVAC consultants.

5. Customisation for Mixed-Use Developments

Gurgaon has seen a surge in integrated developments — retail, commercial, co-living and co-working spaces under one roof. These require HVAC systems that are:

Modular and scalable

Designed to handle varied peak loads

Capable of operating 24/7 in some zones and intermittently in others

This level of complexity demands HVAC partners who can tailor solutions rather than follow a one-size-fits-all approach. It’s one of the key reasons developers are turning only to Top HVAC Companies that have proven experience across sectors.

6. Strong After-Sales Support and Remote Monitoring

Clients are also prioritising post-installation service. With real-time monitoring becoming the norm, many facility heads in Gurgaon now demand:

Remote diagnostics and system health checks

AMCs that include sensor calibration and IAQ reporting

Fast response times in the event of faults

The HVAC partner is expected to not only install but also manage and optimise the system’s performance year after year. The trend clearly shows that best-in-class HVAC providers are investing in tech-enabled service infrastructure.

Final Thoughts

The HVAC industry in Gurgaon is undergoing a quiet revolution — one driven not by suppliers, but by clients who are far more informed and forward-thinking than ever before. They don’t just want cool air. They want clean, efficient, quiet, adaptable systems that evolve with their spaces and support their sustainability goals.

For HVAC firms, staying ahead means embracing innovation, offering smart custom solutions, and becoming long-term partners in performance.

#HVAC contractor in gurgaon#HVAC Consultants in Gurgaon#HVAC Company in Gurgaon#Best HVAC company in gurgaon#Top HVAC companies in gurgaon#Unique Engineers

0 notes

Text

Heat Resistant LED Lights Market Features: Revolutionizing Lighting in Extreme Environments

The Heat Resistant LED Lights Market features innovative lighting solutions designed to withstand high-temperature environments without compromising performance or longevity. As industries push the boundaries of technology and infrastructure, the demand for durable lighting that can function reliably under extreme heat has surged. These specialized LED lights are transforming sectors ranging from manufacturing and automotive to aerospace and oil and gas, where conventional lighting systems often fail or require frequent replacement.

Understanding Heat Resistant LED Lights

Heat resistant LED lights are engineered with advanced materials and thermal management systems that allow them to operate efficiently at elevated temperatures, sometimes exceeding 150°C. Unlike standard LEDs, which may degrade or fail under heat stress, these robust LEDs incorporate heat sinks, specialized coatings, and resilient semiconductor materials. This ensures consistent brightness, reduced energy consumption, and a longer operational life span in harsh conditions.

Key Drivers Propelling Market Growth

One of the primary drivers behind the growth of the heat resistant LED lights market is the expanding industrial sector. Manufacturing plants, metal processing units, and chemical factories often have environments where ambient temperatures soar. Traditional lighting in such conditions not only risks premature burnout but also poses safety hazards. Heat resistant LEDs offer a safer, energy-efficient alternative, reducing maintenance costs and downtime.

Additionally, the automotive industry is witnessing a rising demand for heat resistant LEDs, particularly in engine compartments, brake lights, and headlamps. Vehicles, especially electric and high-performance models, generate significant heat, and these LEDs help enhance reliability and safety.

The aerospace and defense sectors also contribute to market expansion. Aircraft cabins, cockpits, and exterior lighting systems require durable LEDs capable of operating under extreme thermal fluctuations and vibrations. Heat resistant LEDs ensure optimal performance and energy efficiency in these critical applications.

Innovations Driving Technological Advancements

Technological innovations are a cornerstone of the heat resistant LED lights market. Manufacturers are focusing on developing LEDs with enhanced thermal conductivity through the use of novel substrates such as ceramics and metal-core printed circuit boards (MCPCBs). These materials dissipate heat more effectively than traditional plastic or fiberglass boards.

Another breakthrough is in encapsulation technology. Heat resistant LEDs use specially formulated silicone and epoxy resins that protect the internal components from thermal degradation while maintaining transparency for optimal light output.

Smart lighting solutions are being integrated with heat resistant LEDs as well. Sensors and controllers can monitor temperature and adjust brightness levels dynamically to prevent overheating, further extending the LED lifespan and energy savings.

Market Segmentation and Applications

The heat resistant LED lights market is segmented based on product type, application, and end-user industry. Key product categories include high-power LEDs, LED modules, and LED strips, each designed to meet specific heat resistance requirements.

In terms of applications, industrial lighting leads the demand due to the necessity for durable and energy-efficient lighting in factories, warehouses, and processing plants. Automotive lighting is another major segment, as heat resistant LEDs improve vehicle safety and aesthetics.

Other notable applications include outdoor lighting for high-temperature climates, marine lighting, and specialty lighting for equipment such as ovens, furnaces, and heat exchangers. These diverse applications underscore the versatility and critical importance of heat resistant LED technology.

Regional Insights

Asia-Pacific holds a significant share of the heat resistant LED lights market, driven by rapid industrialization and automotive manufacturing in countries like China, India, and Japan. Investments in smart factories and green energy initiatives further boost adoption in this region.

North America and Europe also exhibit robust market growth due to stringent energy efficiency regulations and growing awareness of LED benefits. These regions focus heavily on research and development, fostering innovation in heat resistant LED materials and designs.

Challenges and Market Restraints

Despite the promising outlook, the heat resistant LED lights market faces several challenges. The higher initial cost of these specialized LEDs compared to conventional lighting can be a barrier for small and medium enterprises. Additionally, the complexity involved in designing heat resistant LEDs that maintain optimal light quality at high temperatures requires advanced manufacturing capabilities.

Another restraint is the competition from alternative lighting technologies such as high-intensity discharge (HID) lamps and halogen lights, which still find usage in certain extreme environments despite their inefficiencies.

Future Outlook and Opportunities

The future of the heat resistant LED lights market is bright, with significant growth opportunities on the horizon. Increasing emphasis on energy conservation and sustainable industrial practices will continue to drive demand. Moreover, ongoing research into novel materials such as gallium nitride (GaN) and advances in nano-coatings are expected to enhance heat resistance and LED efficiency further.

Emerging applications in electric vehicles, renewable energy installations, and smart cities offer new avenues for market expansion. The integration of heat resistant LEDs with Internet of Things (IoT) platforms can enable predictive maintenance and adaptive lighting systems, making these lights more intelligent and user-friendly.

Conclusion

The Heat Resistant LED Lights Market features a dynamic and rapidly evolving sector that addresses the critical need for durable, energy-efficient lighting solutions in high-temperature environments. By combining cutting-edge materials science with innovative design, these LEDs are redefining how industries illuminate their operations under extreme conditions. As technology advances and awareness grows, heat resistant LED lights are poised to become indispensable in sectors demanding reliability, safety, and sustainability in lighting.

0 notes

Text

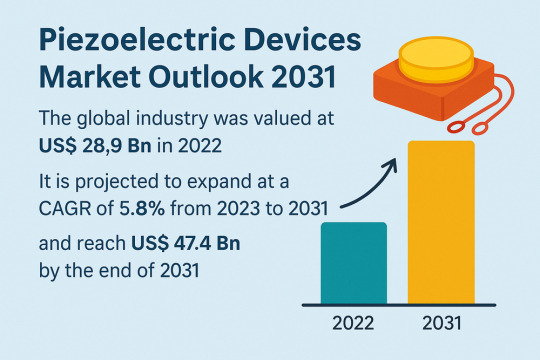

Versatile Applications Power Global Piezoelectric Devices Market to USD 47.4 Bn by 2031

The global piezoelectric devices market was valued at USD 28.9 Bn in 2022 and is anticipated to reach USD 47.4 Bn by 2031, expanding at a CAGR of 5.8% during the forecast period (2023–2031). Piezoelectric devices, which convert mechanical stress into electrical signals and vice versa, are becoming indispensable across a wide array of industries including consumer electronics, automotive, industrial automation, and healthcare. Their ability to deliver high sensitivity, quick response, and energy efficiency has made them critical components in modern technological systems.

Market Drivers & Trends One of the primary growth drivers is the increasing consumption of piezoelectric devices in consumer electronics, such as smartphones, wearables, and touchscreen interfaces. Additionally, automotive advancements, especially in electric and autonomous vehicles, are fueling demand for precision sensors and actuators based on piezoelectric technology.

Another key trend is the integration of piezoelectric materials in energy harvesting applications, enabling the capture of ambient vibrations or movements to power small devices. Moreover, the miniaturization of electronic components and the growing demand for compact, energy-efficient solutions across sectors continue to support market expansion.

Key Players and Industry Leaders The global market is moderately fragmented, with key players focusing on technological innovation and strategic collaborations. Prominent companies include:

APC International Ltd.

Cedrat Technologies S.A

CeramTec GmbH

Ionix Advanced Technologies

KEMET Corporation

KYOCERA Corporation

L3harris Technologies, Inc.

Morgan Advanced Materials plc

Nanomotion Ltd.

Physik Instrumente (PI) GmbH & Co. KG

Piezo Kinetics, Inc.

piezosystem jena GmbH

These companies are investing heavily in R&D to develop next-generation piezoelectric materials and solutions.

Discover essential conclusions and data from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=34574

Recent Developments

KAIST, April 2023: Developed wearable piezoelectric sensor for continuous blood pressure monitoring.

SFedU, March 2023: Created piezoelectric generators from carbon nanotubes for urban noise-to-energy applications.

Piezo Motion Corp., March 2021: Acquired Discovery Technology International to diversify into precision piezoelectric motors.

Latest Market Trends

Wearable Sensors for Health Monitoring: In April 2023, KAIST developed a highly sensitive wearable piezoelectric blood pressure sensor, paving the way for real-time health monitoring applications.

Energy Harvesting Innovations: Russian researchers at SFedU have developed piezoelectric generators based on nitrogen-alloyed carbon nanotubes to transform urban vibrations into usable power.

Affordable Precision Motors: In March 2021, Piezo Motion Corp. acquired Discovery Technology International, expanding its offering of affordable, energy-efficient piezoelectric motors.

Market Opportunities The piezoelectric devices market offers numerous growth opportunities: