#guaranteed monthly income plan

Text

hello hello! if youre usamerican with federal college debt thats about to start needing to be repaid, you should make sure youve gone to check out the new SAVE income based repayment plan the biden administration recently passed. this plan allows you to pay a monthly deposit that’s calculated based on your income. a few things make this different from the existing income based plans, including that your monthly repayment could be as low as $0 per month. if you pay the calculated amount, no further interest is accrued for the month, and if you keep up with these payments (which again, if youre like me and you dont make a lot of money might be ZERO dollars per month) then all your remaining debt will be forgiven after 12-25 years depending on your specific loans. the program application is very easy but processing takes about a month, so nows the time to get it in before repayment begins in november.

tldr: the SAVE federal aid plan can have you paying $0/month with no accruing interest on your student loans towards a guaranteed debt forgiveness after 12-25 years and you can read more about it and apply for it here!

#the plan doesnt apply to parent plus loans i believe but its still worth checking out the idr plans#kora.txt#got a letter today that im approved so yippeeeee

828 notes

·

View notes

Text

Major PSA: Patreon Changes & Discord Shutdown

Oh, I hate to be predictable lol.

What it comes down to is, I've lost the love in creating this story. (But this is NOT a "I'm not writing anymore of this story" post!)

I've put a lot of pressure on myself to put out bonus content on Patreon, and it and the Discord server hangs over my head - giving me that feeling like since I'm not constantly posting or growing an income around The Nameless, that I'm not doing enough or I'm not legit enough, etc.

I do want to stress that y'all are wonderful, and I'm honored that you've stuck around this long, and there has been absolutely NO pressure from you - it is self-inflicted guilt for sure.

The reality is that my day job workload is much more than it used to be with the new role I took earlier this summer - but it's work that I love. And I'm so thankful and pinching myself that I was able to find that.

In the end, I hope that will mean better things for you and the game - giving me the time and space to draw and write out of joy instead of guilt, getting to share a lot of content with everyone on tumblr again, and focusing my writing in on the game instead of trying to balance too much.

So, Patreon will be turning into a tip jar.

1. Currently, billing is paused. On September 2, the current tiers will be deleted and tiers will be added for (USD) $2, $5, and $7.

2. For current patrons, when a tier is deleted, your subscription IS NOT AUTOMATICALLY CANCELED. You must edit your pledge on your own to a lower tier if you don't want to be charged what you were before.

3. (EDITED) There will be no guaranteed bonus content, and the only difference in content will be that 18+ posts will be reserved for the $7 tier . I'm still planning to do the first meeting POVs and some art specials, it just may be slower and take a little while longer. I'm also hoping to at least post monthly progress reports, and will be figuring out how to open the current posts to the new tiers.

4. I will also be shutting down The Nameless Discord permanently today.

Thank you again for your patience with me, and I hope this will turn a new leaf and get me back in the head space for the actual game again.

Sending y'all much love, and thank you for everything. <3

Parker xoxo

175 notes

·

View notes

Text

Wrong on Multi Levels (Kamukoma Week '24)

"You attempted to brainwash him," repeated Izuru.

"And it went despairingly wrong."

"And it went wrong."

"I only wanted to show him the joys of despair!"

"I told you to leave him out of your schemes."

"Well, good friends share their toys!" said Junko Enoshima.

"You qualify as neither."

"And anyway it didn't work, so I don't see why you're bitching."

Izuru looked at his property. His property currently had two first-years cornered and was looming over them, trying to sell them 'reasonably-priced' starter kits.

"Interfere with him again and I shall make your life extremely unpleasant and despair-free," he told his omg✨bestie✨5✨eva. And Izuru Kamukura swished away.

---------

"The compensation plan is a little complicated and I'm gay, but I figured it out," Nagito was telling his classmates. "Each month you have two legs and the payout -- well, first I have to explain recruitment..."

"Wh-what's he on about?" whined Mikan. "I-I'm pretty sure he's d-delirious. He keeps talking about things that don't make sense -- more than usual,, I mean,,, like lines down and talentpreneurs--"

"Downline," corrected Izuru, making her shriek by appearing out of nowhere as usual. "Do not buy things from him and do not sign up for things."

"But he r-really wants me to,,, and he looks so sad if you say no,,,, and he said he's only ten sales away from ranking up his m-monthly bonus,,"

"He has an illness," Izuru said. "Recovery depends on his not being encouraged and not dragging others into the delusion."

("Holy shit, you guys!" said Leon, ignoring them on his way to talk to his friends. "I just got an amazing deal on some oils that'll make the chicks flock to me, guaranteed!"

"Guaranteed?" asked Kazuichi.

"And they disinfect your piercings, too!")

---------

"Quit?" repeated Nagito in shock. "But I'm already so successful! Half the school is signed up under my team and my personal sales volume is already at Premium Tiara Peach Passion level even before reinvesting my profits!"

"You are engaged in a business scam and dragging others into it," said Izuru. "Others who, lacking your luck, are 99.7% likely to lose money in this scheme."

"Well... maybe, if you trust the income disclosure documents," said Nagito with scorn. "But you know what I say. Never tell me the odds!"

"You have not said that, ever."

"If you'd just join, you could be my upline," said Nagito, whose eyes were big and practically rippling. "You could lock arms with me and my tribe of boss-Ultimates and change lives all over the world simply by sharing the incredible, organic, cruelty-free, vegan, hope-filled products you love. It would mean a lot to me. Please, hon?"

Izuru, faced with the full wattage of that smile, hesitated.

---------

"Well, you never said you wanted a way to undo it!" whined Ryota.

"You never said it'd go fucky-wucky and make him start a pyramid scheme!"

"It wasn't supposed to! You must've used it wrong!"

"Anyway, cure. Before I start cutting parts off you."

"I can't work in these conditions!" he bleated. "Mukuro's already tried to sell me a diffuser and it's not even morning bell!"

"Huh," said Junko. "Bitch didn't try to sell me a diffuser."

"That's not the point!"

"Just make an undo button for it already, hikikomori."

---------

"Further research," said Izuru, "has revealed that the proper treatment of this disease is to give Nagito Komaeda whatever he wants forever."

"U-um,," replied Mikan.

"And to tell him he is pretty. And cute, and good."

"I-I think it's,, getting worse,,," she told Ibuki.

"That stuff smells gross!" complained Akane.

"Just one drop of basil oil in your pasta will fill you with manly passion!" Nekomaru bellowed down at Teruteru.

"You can't ingest that stuff, cher!"

"You can! It's vegan and organic!"

"So is deadly nightshade..."

"They grow their own lavender!" Nekomaru roared at some fleeing freshmen.

---------

"I'll never live this down," Junko Enoshima moaned, kicking a broken stall off the school walkway.

"At least we stopped it," said Ryota. "And I can go outside again now that stinky stuff isn't giving me asthma attacks."

"I can't believe I saved this freaking school!"

"Um, well, I did all the--"

"And as for Izuru, that backstabbing hoe! Ditching me to play mommy's makeup store with some sickly luck slut!"

"That's not a nice thing to ca--"

"Can't rely on anyone for anything," snarled Junko, pausing to stomp a few discarded vials into an essential oil slick.

Ryota pulled on a face mask hurriedly. "Did anyone actually make any money, you think?"

"Well, I did."

"What? But you didn't even join in all the selling..."

"Bought a 50:50 share in Komaeda's outfit as soon as he started. That guy's luck is something else."

"Does that mean you're going to pay me for any of the work I've done?"

"No," said Junko.

28 notes

·

View notes

Text

I want to address a problem that seems to arise repeatedly in public discussions about green growth and degrowth. Some prominent commentators seem to assume that the debate here is primarily about the question of technology, with green growth promoting technological solutions to the ecological crisis while degrowth promotes only economic and social solutions (and in the most egregious misrepresentations is cast as “anti-technology”). This narrative is inaccurate, and even a cursory review of the literature is enough to make this clear. In fact, degrowth scholarship embraces technological change and efficiency improvements, to the extent (crucially) that these are empirically feasible, ecologically coherent, and socially just. But it also recognizes that this alone will not be enough: economic and social transformations are also necessary, including a transition out of capitalism. The debate is therefore not primarily about technology, but about science, justice, and the structure of the economic system.

[...]

Ecological economists point out that when we scale back our assumptions about technological change to levels that are, to quote the physicist and ecological economist Julia Steinberger, “non-insane,” and when we reject the idea that growth in rich countries should be maintained at the expense of the Global South, it becomes clear that relying on technological change is not enough, in and of itself, to solve the ecological crisis. Yes, we need fast renewable energy deployment, efficiency improvements, and dissemination of advanced technology (induction stoves, efficient appliances, heat pumps, electric trains, and so on). But we also need high-income countries dramatically to reduce aggregate energy and material use, at a speed faster than what efficiency improvements alone could possibly hope to deliver. To achieve this, high-income countries need to abandon growth as an objective and actively scale down less necessary forms of production, to reduce excess energy and material use directly.

[...]

Degrowth does not call for all forms of production to be reduced. Rather, it calls for reducing ecologically destructive and socially less necessary forms of production, like sport utility vehicles, private jets, mansions, fast fashion, arms, industrial beef, cruises, commercial air travel, etc., while cutting advertising, extending product lifespans (banning planned obsolescence and introducing mandatory long-term warranties and rights to repair), and dramatically reducing the purchasing power of the rich. In other words, it targets forms of production that are organized mostly around capital accumulation and elite consumption. In the middle of an ecological emergency, should we be producing sport utility vehicles and mansions? Should we be diverting energy to support the obscene consumption and accumulation of the ruling class? No. That is an irrationality that only capitalism can love.

At the same time, degrowth scholarship insists on strong social policy to secure human needs and well-being, with universal public services, living wages, a public job guarantee, working time reduction, economic democracy, and radically reduced inequality. These measures abolish unemployment and economic insecurity and ensure the material conditions for a universal decent living—again, basic socialist principles. This scholarship calls for efficiency improvements, yes, but also a transition toward sufficiency, equity, and a democratic postcapitalist economy, where production is organized around well-being for all, as Peter Kropotkin famously put it, rather than around capital accumulation.

The virtue of this approach should be immediately clear to socialists. Socialism insists on grounding its analysis in the material reality of the world economy. It insists on science and justice. Yes, socialism embraces technology—and credibly promises to manage technology better than capitalism—but socialist visions of technology should be empirically grounded, ecologically coherent, and socially just. They should emphatically not rely on speculation or magical thinking, much less the perpetuation of colonial inequalities. Green growth visions fall foul of these core socialist values.

94 notes

·

View notes

Note

As someone who is extremely new to using twitch but wants to support you, are bits better or is subbing better? Also I hope you're having a wonderful holiday!! ❤️🌻❤️🌻

It depends, they’re functionally very different!

Just as a quick answer before getting too in the weeds, GENERALLY I do prefer subs as long as it is something people are able and willing to do! Obviously no amount of financial support is ever necessary to be an appreciated member of the community, and bits are still generous simply by virtue of being opted into to help me out, but if subbing is an option for anyone it REALLY does go that little extra mile.

I say I prefer subs mainly due to the consistency of it. Subs are a majority of the time going to be a $5 monthly thing (though there are less-used higher tiers), and my cut of that is about 2.50. Assuming, say, 5 people begin a consistent monthly sub, that’s a guaranteed 12 bucks or so of income that I can reliable measure per month. If 3 of those 5 people mainly support with bits instead, I’m still getting support and it still contributes to the monthly payout, but there’s basically no way to predict how much it’ll show up in the total and plan accordingly. Could be like 50 extra bucks one time if people are feeling particularly generous, or it could amount to cents. One is consistent, the other is supplementary.

But again, both are appreciated! So really don’t fret too much either way. I always above all want to stress that continued support for my channels in ANY way you can afford, even if it’s just watching the YouTube highlights and sharing clips, makes a difference.

147 notes

·

View notes

Text

Two conservative groups say San Francisco and the state of California are racist for illegally giving away millions in tax money to three non-profits that exclude recipients based on race and gender identity.

The American Civil Rights Project and the Californians for Equal Rights Foundation say the city and state violate the law by picking who gets federal money based on skin color.

The suit names three guaranteed-income programs.

The Black Economic Equity Movement hands out $500 a month exclusively to young, Black Bay Area residents.

SAN FRANCISCO MAYOR PUSHES ADDICTION SCREENING FOR WELFARE RECIPIENTS

Guaranteed Income for Trans-people pays $1,200 a month to Black, Indigenous and Latino recipients, provided they are also transgender.

The Abundant Birth Project gives out $1,000 a month solely to pregnant Black and Pacific Islander women.

"We are asking for these programs to be halted until they are no longer discriminatory," says lawyer Dan Morenoff of the American Civil Rights Project.

"Each of these three programs qualifies and disqualifies individuals from participation and benefits based on their race."

San Francisco established the Abundant Birth Project in 2020 through its department of health. It provides $1,000 to $1,500 a month, for roughly nine months, solely to "Black and Pacific Islander women in San Francisco." Other races are not eligible for this "unconditional" income. Its annual budget is $1.8 million, but new $5 million in grants expand the program to four additional counties.

Advocates say that Black and Pacific Islander women need the help because of higher rates of premature birth. "This risk is primarily due to racism, both structural racism and racism that birthing people experience when they interact with physicians and other medical providers," says Dr. Zea Malawa of the San Francisco Department of Public Health.

True or not, the lawsuit claims, it remains illegal to exclude White and Latino women, especially those with higher risks of complication.

In November last year, San Francisco launched another guaranteed income program.

"To participate you must be Black, between the ages of 18 and 24, and live in certain areas within Oakland or San Francisco," according to BEEM guidelines. Those applying as 'White' on-line are told they are 'not eligible'.

The GIFT project provides $1,200 a month for 18 months to "Transgender, Non Binary, Gender Non-Conforming and Intersex" individuals provided they are "Black, Indigenous or People of Color." The program is run through the city's Office of Transgender Initiatives. Last week, the watchdog group Judicial Watch also sued San Francisco over the GIFT project.

The money in all three programs is provided with no strings attached, via a debit card replenished each month.

"Guaranteed Income is a temporary monthly payment made to people without any requirements or obligations," says BEEM. "It’s an approach to supporting people, so they have a little breathing room, can take care of immediate needs, and plan for the future."

Similarly, the GIFT project says, "the $1,200 stipend will be provided to participants so they may focus on their basic physical and mental health and wellness without worrying about income."

Fox News reached out to all three programs, but all declined an interview. Mayor London Breed's office said in a statement that the programs are legal and that it looks forward to addressing the charges in court.

16 notes

·

View notes

Text

ProfitCodex: Your Guide to Effortless Mobile App Creation

Key Features of ProfitCodex

Unlimited Mobile App Creation:

ProfitCodex permits you to make a limitless number of genuine portable applications without any preparation utilizing its natural simplified proofreader. Express farewell to complex coding - this apparatus improves on the cycle for you.

iOS & Android Compatibility:

With only a single tick, you can distribute your applications straightforwardly to the iOS Application Store and Google Play Store. Arrive at a large number of possible clients across the two stages easily.

30+ Done-For-You Templates:

Browse north of 30 expertly planned layouts across different specialties. Whether you're building applications for yourself or clients, these layouts speed up your application improvement process.

Commercial License Included:

ProfitCodex isn't only for individual use. You can sell the applications you make to neighborhood organizations and online clients, opening up new income streams.

Built-In Traffic:

Get your applications positioned and highlighted on application stores, driving free, natural traffic to your manifestations. Don't bother agonizing over showcasing - ProfitCodex takes care of you.

Push Notifications:

Send limitless notices to clients' telephones and lock screens. Accomplish a 100 percent open rate and keep your crowd locked in.

No Monthly Fees:

Dissimilar to certain stages, ProfitCodex works on a one-time installment premise. No secret expenses, no repetitive charges - simply strong elements readily available.

100% Newbie Friendly:

Bit by bit preparing guarantees that fledglings can with certainty make and sell applications. You needn't bother with any related knowledge to get everything rolling.

Zero Coding or Hosting Required:

Everything occurs in the cloud. No requirement for a site, facilitating, or specialized arrangement - ProfitCodex handles everything.

ProfitCodex AppWizard (New for August 2024):

This element lawfully captures content and consequently transforms it into new, remarkable portable applications. Envision having an all day, every day application creation right hand!

>>>>>Get More Info

2 notes

·

View notes

Text

A Whole New Chapter

In past blogs I’ve written every week or two. Here I am nearly 3 months into this current adventure and I finally sit down to write. I was really planning to give this up but I’ve endured a fair amount of grief from some of my readers, and with a hopefully blog-worthy event coming up (road trip!) Georgia has encouraged me to get back with the program.

Lots of catching up to do! But before I even get to the Philippines, I’ll take you back all the way to our previous trip. One day, as I was paying the bills necessary to maintain a home in the mountains of California, I thought about the monthly costs for electricity, propane, water, sewer, home & auto insurance, property taxes, etc. and wondered why we were paying so dearly for a home we only used half the time, and planned to use even less in the future. Georgia and I thought about it and talked and decided to downsize and relocate our base in the US, and spend most of our time over here – maybe 9-10 months a year.

And between May 2023 and our return here in March, that’s just what we did. We first found a small home on a ¾ acre lot, still under construction, in Fernley, Nevada. This promised much lower expenses than Graeagle, plus Nevada has no state income tax. As one example, our homeowner’s insurance is $328 per year, while we paid more than that every month for the house in Graeagle. Everything else has scaled accordingly, and though we’re not particularly in love with Fernley, it gives us what we need when we’re there, and we feel safe just locking up the house and leaving for 5-6 months at a time.

The new US Headquarters in Fernley

The house in Graeagle was put on the market in September, and in one day we had a buyer, with cash, and the deal was done! We stayed in the house until after Georgia’s son Matt was married (in Graeagle) then began the move to Fernley. By November 15 we were Nevada residents.

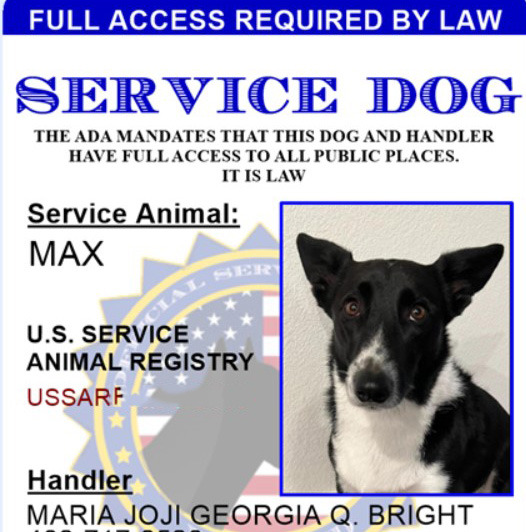

Max

Although Max was well taken care of while we were gone, by Georgia’s sister Dignah, we were the ones who suffered, missing him terribly. We decided to bring him with us, and leave him here during our short return trips to the US. Our caretakers love dogs so it should work out well.

I asked my nephew, who flies for a major airline, about the best way to fly a dog overseas. “Easy” he said, “he just needs to get registered as a medical service dog then he gets to fly in the cabin, for free.” Lucky for us, he’d done that for one of his own dogs and knew the ropes. Soon enough, Max was a “trained and certified” service dog, able to alert to Georgia’s condition. And no, ADA laws do not allow you to ask what that condition is.

Doesn't he look handsome on his ID card?

That was indeed the easy part, and only guaranteed Max a comfy seat on the plane. The path started with Max’s vet, who researched the health and vaccination requirements both for import to the Philippines and export from the US. Max got to know his vet well over the next few months but, as attested to by the lengthy USDA export form, he was perfectly healthy. A complete medical and vaccination history was provided to the Philippines Bureau of Animal Imports to receive an import clearance, and various US DOT forms had to be completed.

Thus armed with a large stack of paperwork, and a suitcase full of Wubbas and Chuckit balls, we set off for our flights from Reno to SFO, then SFO to Manila. The gate agent in Reno didn’t want to see any of the papers; she told us that it would be handled at SFO before the international flight. Nope, at SFO we just walked onto the plane and settled into our business class seats. Max had it pretty good for sure!

Surely we’ll have to provide paperwork to get Max through the airport in Manila, right? Well, again, no. Through Immigration, baggage claim, and Customs, Max just trotted along beside us. The whole trip and not once were we asked to provide any documentation. Welcome to the Philippines, Max!

The most amazing thing though, was Max’s bladder control. He used an animal relief area outside the Reno terminal before our first flight, wouldn’t go near the stinky in-terminal relief station in SFO, held it through both flights, then through the terminal in Manila, finally taking a potty break outside the terminal. Super-human!

Kawayan Cove

It was nice to get back to our home, after being back in the states for a very busy 10 months. Nice especially as the caretakers had done a good job maintaining both home and gardens. Ready to move in and relax!

After greeting everyone and making some instant friends, Max spotted the swimming pool. It was a hot day (and he soon found out that every day is hot here!) and in he went. A quick lesson on where the steps were so he can get in & out and now swimming is a daily activity. Usually when one of us is there to throw the Chuckit ball, but we’ve seen him go down by himself and sit on the bench with water up to his chest, just cooling off.

Mabini

Last trip, I wrote about our visit to nearby Mabini/Anilao, a famous dive spot in the Philippines. We noted that the second hotel we stayed in was dog-friendly so for Georgia’s birthday this year we decided to go back, taking Max this time. We all enjoyed relaxing, swimming (both pool and beach for Max), getting massages (sorry, not you, Max), and of course the bar and restaurant. We went diving one day and I got in a couple enjoyable dives, spotting lots of fish, octopus, nice corals and crinoids, turtles, and a number of colorful nudies (nudibranchs).

Where's Dad?

New Car

I had a plan for this trip to replace our Innova with a Toyota Fortuner SUV (a model not available in the US but similar to the Toyota Highlander). More luxurious, better ride and handling, but still retaining a lot of utility for hauling people and stuff around. Georgia had a better idea (as she's prone to have), to get a really small car mainly for use in and around town, something that will be easier to drive and park in the crowded markets.

We originally settled on a Toyota Wigo (again, no equivalent in the US), a very compact “city car” with a mighty 1.0L engine. Buying a new car here isn’t like in the US, where you practically have to shake salespeople off your legs. Even a test drive isn’t standard here; we actually had to go to 3 dealerships to get one. OK, one dealer did let us drive a Wigo, but only around the dealership parking lot! In the 3rd dealership though, we noticed a little bit larger mini-SUV called the Raize. About the same height and width as the Wigo, but somewhat longer and with lots more room inside. Comparison drives between the Wigo and Raize convinced us that the Raize’s even mightier 1.2L engine was worthwhile, plus it was more comfortable overall. A deal was struck and we’re now enjoying our new mini-SUV!

Georgia’s mom is also wanting a car for the Philippines, and it turns out that our Innova is exactly what she’s looking for. We’ve made a deal to sell it to her, so now we’re looking for its replacement. I may get my Fortuner after all!

Driver’s Licenses

Regarding the story above, I got to test drive the cars; Georgia didn’t. The salesperson noted that her license had expired the day before, which was her actual birthday. Mine didn't expire until July so I was good to go.

We’d been clued in to the existence of a Land Transportation Office (LTO) branch in a nearby shopping center that only handles driver’s license renewals, which was said to be very efficient compared to dealing with the full-service LTO. The requirements for renewal are basically passing a medical exam and a written test. We went to the medical office, conveniently next door to the LTO, for our exams. After filling out a short medical history, my exam consisted of getting weighed, height measured, and reading one line of inch-high letters on an eye chart. Every other result of the required “exam” was just filled in by the staff. And then, as I was waiting for my exam results to be registered, I was handed a certificate stating that I’d passed the written test with a score of 92%. VERY efficient indeed, considering that I’d never seen a test. I do wonder what questions I got wrong though…

In less than an hour overall, we both walked out with 10-year renewals on of driver’s licenses. I’ll be almost 80 when this one expires, hope I’m around to get it renewed!

And BTW, I’m mad because Georgia outscored me on the written test, getting a 96!

Billiards

Billiards is a popular activity in the Philippines, probably because it’s played indoors in air-conditioned rooms. I’ve played occasionally here with Herve, who has a table, but this year we’ve hooked up with Kawayan Cove neighbors Graham (of English garden fame) and Andy (a New Yorker who lives mostly in Singapore). Also in our group, from neighboring developments, are Jean (Belgian), and Robert (Canadian). We call our informal group the “Sandy Balls Billiards Club” and we play a “tournament” every weekend, each putting 100 Pesos (about $1.75) into a winner-take-all prize pool. I’ve won once, hoping to continue to improve my game.

L-R: Robert, Jean, Graham, me, Herve (Andy not pictured)

Road Trip!

We’ve been talking about a road trip to the far northern reaches of Luzon for some time; we finally decided to do it. And just like our road trip to Baguio and Sagada in 2018, we’re not driving or taking our car, rather hiring both. Reminds me of an old commercial…

Car rental = $40/day

Driver = $20/day

Food and Lodging for Driver = $10/day

Sitting in the back and enjoying the ride = Priceless!

Our itinerary will include La Union, Vigan, Pagudpud, Santa Teresita, Tuguegarao, and Baguio. Stay tuned!

Sunset(s)

We’re still enjoying our sunsets, nearly every evening. Since it’s been almost 3 months I’ll throw in some bonus photos!

From our home:

From Mabini:

All for now, take care everyone!

2 notes

·

View notes

Text

Why The Gang Became Robbers

CW: Discussions of Poverty and Money

So, it’s somewhat theorized that the gang started stealing because of financial reasons. There’s actually some allusions to this in the movie itself, with them planning to stop stealing after the heist they were eventually caught for, them seeming to live in the shop, Johnny’s clothes seeming to be hand-me-downs (his dad’s jacket, a shirt that’s a few sizes too big with worn out sleeves, well worn-too large jeans), and mostly using walkie talkies instead of their phones (data is expensive). I started to wonder how deep in debt they actually were sooo... I did some calculations.

--------------------------

Disclaimer: All of these were based of the average costs of everything in the state of California (Calatonia is based on LA and San Francisco). There were some generosity here in debt calculations including giving them a good credit score when they applied for the loan and assuming they had only been in the states 7 years. Oh and that they had a bit money when they came to the US.

----------------------------------------------------

Debts

The Garage Itself

Building Price: $2,250,00

Down Payment (20%): $450,000

30-Year Fixed Loan Plan with Interest of 5.395%

Credit Score (I’m trying to help them out here): 729

Annual Property Tax: $28,125

Annual Home Insurance: $7,875

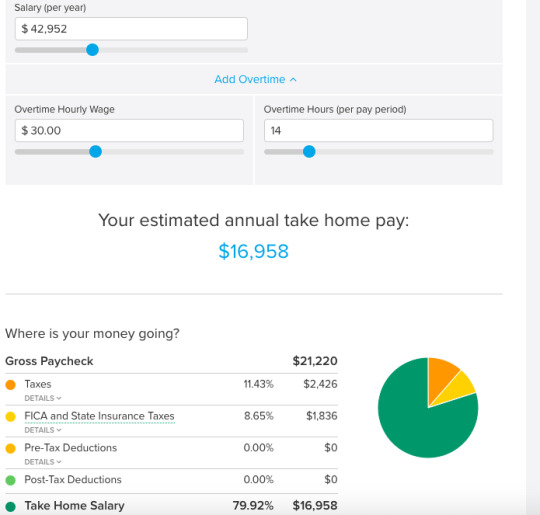

Monthly Payment: $13,102

Annual Total Building Payments: $193,224

Plus Other Expenses (calculated from average 2 person household costs)

Food, Water, Electricity: $24,475.8

Health Insurance: $0

Car Insurance: $0

----------------------------------------------------

Now, the total mortgage would be around 4.62708 million when calculating in 7 years of interest rates. And if we look at the average yearly income of a mechanic in California...

Yeah, Marcus is only taking home around $16,958 dollars per year, and that’s being generous with both rates and overtime. So, without even factoring in the debt, as well as assuming that Stan and Barry are not included in their household income, the Taylor family is almost $2,000 dollars below the Californian poverty line.

Now, let’s take a look at their plan here. We know that the gold shipment they were planning on stealing in Sing 1 was around 25 million dollars worth. Well, that would clearly pay off their entire mortgage, as well as probably help Stan and Barry with whatever financial issues they might be facing. It would also give them a good cushion for a few years going forward, preventing them from going into debt easily again.

With the seven years of payments totaling $599,844, and assuming that they have stolen at least $2.163,677 to pay towards the debt before, in Sing 1, they only owe a much more reasonable $1,863,559.

And while that is still a lot, if a rich person, say an old musical theatre star, wanted to guarantee that the performers at their old theatre troupe wouldn’t be falling onto a bad path, they could pay that off much easier than the full mortgage.

So, in conclusion, Johnny and his family, stolen money included in this, are still some of the poorest characters in all of Sing. They probably didn’t want to steal in the first place either, judging by how they were planning on stopping after the flubbed heist anyway. They were just desperate. they needed money, and clearly the garage plus whatever side jobs Johnny could have potentially had were not enough.

I believe that the main reason we don’t see them still stealing in Sing 2 is that their debts were paid off, more than likely by Nana Noodleman as she’s the only one with that amount of money lying around. This allowed them to begin working again without a immediate threat of debt, and with the money Johnny’s bringing in from the theatre, the family is probably in a bit better shape.

#sing#sing 2#sing johnny#sing marcus#sing stan (only mentioned)#sing barry (only mentioned)#sing nana noodleman (only mentioned)#this is a theory#you do not have to accept it as canon#i'm sorry if the math is off i tried#i was alway a reading and history kid#nana definitely helped buster johnny and ash out after the first movie#because theres literally no way the theatre could have turned that large of a profit that fast#this puts Johnny as the second poorest after Buster in sing 1 and the second after Nooshy in Sing 2#by my calculations at least

15 notes

·

View notes

Text

What Separates a 401(k) Plan from a Pension Plan

A 401(k) differs from a pension plan in that an employee can contribute to their retirement savings account through payroll deductions. Several employers also offer matching funds. On the other hand, pension plans are retirement accounts sponsored by employers and pay out a set sum of money when the employee retires. Your salary, number of years of service, and other factors will typically determine how much you receive.

It's crucial to comprehend the costs associated with a 401k or pension if you're considering getting one. The main causes of plan expenses are contributions, returns, and management fees. However, additional costs covered by the employer, such as administration and recordkeeping fees, can also impact the cost of a 401k. It would help if you asked for a fee schedule that lists all the costs related to your plan.

Asking about service fees, which vary by fund provider, is also a good idea. Some service providers charge fees for processing tax returns, moving assets between 401(k) plan providers, and other services. A typical pension has a cost advantage of 49% over a typical 401(k)-style retirement account, according to a recent National Institute on Retirement Security analysis. This cost advantage is primarily attributable to lower investment management fees, optimally balanced investment portfolios, and longevity risk pooling.

Employer-sponsored retirement savings vehicles include pensions and 401(k) plans, two distinct types. Even though they are both well-liked, one may be preferable to the other depending on your particular circumstances due to a few differences. A 401k and a pension are fundamentally different because a 401k allows you to choose how your money is invested. Several investment options are available, including stocks, bonds, and mutual funds.

As a defined-benefit plan, a traditional pension lets you know exactly how much money you'll receive each month when you retire. The sum is determined by years of service and past salaries. The benefit is typically paid out in lump sums when you reach a certain age, a process known as vesting, or in monthly payments. However, you won't get the entire sum if you quit your job before becoming vested.

Employees can make pretax contributions to a savings account through an employer-sponsored retirement plan known as a 401(k). Employees are allowed to contribute up to a certain amount each year, and occasionally, employers match the contributions. Unlike a pension funded by the company, a 401k is based on your contributions and investments and promises to pay you a set amount of money over time. The most common kind of tax-deferred retirement account in the US is this one, which is referred to as a "defined contribution" plan.

Similar to a 401(k), pension plans have rules governing how much of your pension is tax-deductible and how much is not. General Rule, which makes use of life expectancy tables, is used to calculate the taxable portion. The general Rule can be found in IRS Publication 939, or the Simplified Method can be applied to determine a more exact figure.

Both a 401k and a pension plan offer a range of investment options. Your financial objectives and current financial situation, among other things, will influence the type of investment that is best for your retirement needs.

Employees can save for retirement through a 401(k), a defined-contribution plan, and benefit from tax breaks on their contributions. Employers frequently match these contributions. A pension plan, however, is better suited for investors who want a lifetime income guarantee after retirement. Government regulations and expert fund managers oversee the management of these plans.

By investing in various asset classes, including stocks and bonds, pension funds seek to diversify their portfolios. Additionally, they can invest in derivatives and alternative investments, reducing the risk of losing money on a single investment.

2 notes

·

View notes

Text

Fitness Trainer Certification – An Overview

If you have a passion for fitness and love to help people lose body fat and become fit, you should consider a career as a Certified Fitness Personal Trainer after doing a Personal Trainer Course from a reputed Fitness Academy. This course will help you understand the human body better.

People have become very busy with work and have absolutely no time to dedicate to travel to a gym for their health & fitness. So many people who can afford the luxury of personal trainers have invested in “Home Gym” setups to help them achieve their weight loss goals (Actually Fat Loss goals), and maintain good fitness levels. If you ask most people, they will tell you that the money spent on a personal trainer is money well spent.

The Diploma in Personal Training (DPT) course is a relatively short course and you will be taught the basics of Anatomy, Physiology, Kinesiology, Nutrition and Supplementation, Flexibility Training, Weight Training, Exercise Programming, Cardiovascular Exercise, Health Screening & Evaluation, First Aid and Approach to Fat Loss.

Once you have done the Personal Trainers course, it is imperative that you increase your scope & money earning potential by doing The Certified Personal Trainer for Special Populations (CPT-SP) Course

In the advanced personal trainer course, you will be taught how to handle various clients with medical problems, ailments or injuries. This course teaches you Orthopedic Pathologies- joint wise, Cardiovascular & Respiratory Pathologies, Metabolic Disorders, Neurological Disorders, Kinesiology, Soft Tissue Injuries, Arthritis, Hernias and Fractures.

To further increase your result orientedness with your clients, you can also do an additional course in Sports Nutrition. (Being able to guide your clients in both exercise & Nutrition will help you almost guarantee results to your clients.

This is a great course to help nutritionists, personal trainers, gym instructors and group fitness instructors on how to recommend a good diet to gym members & Personal training clients the tenets of Sports nutrition will help you improve the performance of your clients (whether they are corporate Executives, Models, House Wives or competitive athletes).

This is a very upcoming career choice in India. The demand for Fitness solutions is increasing at an exponential rate & this will only get better. Every big brand of International Franchise chains of Health Clubs is investing in India in a big way with all of them having plans of 100-200 gyms per brand in India. All of these need qualified personnel & will not hire without a valid certification from a reputed Fitness Academy.

Whatever is your motivation to become a trainer, remember, you must be passionate about fitness and have a desire to really change people’s lives. A fitness trainer certification course will help you understand human anatomy better and you will be better equipped to train individuals.

It is one of the most rewarding fields & one of the few in which you get to see an incredible smile on your customers’ faces, when they tell you, “Thank you for changing my life”. Along with monthly incomes of INR 50k- 60k-, easily attainable through personal training. It also comes with a guarantee of incredible JOB SATISFACTION.

2 notes

·

View notes

Text

Proof that Short Term Cash Loans Is Exactly what You Need?

You are constantly looking for more money to deal with emergencies in your life. Here, we assist clients in choosing a suitable lender in the hopes of receiving additional funding while also understanding their loan needs. As a result, you don't travel far and wide before arriving at Classic Quid to submit an application for one of the best loan products based on your needs. Short term cash loans from direct lenders are a real option if you don't have a debit card in your wallet to serve as collateral for a loan. You don't have to wait to look for another loan because it enables you to address all of your urgent needs at once.

To make applying for a short term loans UK with us quick and simple, we especially developed our application process with the needs of our borrowers in mind. It will take you less than 5 minutes to finish our application because there isn't any documentation to submit or complicated questions to respond to.

Although the turnaround time for quick approval may vary, in most circumstances you should be able to get a short term loans UK direct lender decision on whether or not your application has been approved once you've completed it. This implies that you won't have to wait for hours or even days to find out if you've been accepted.

Find the Most Solid Momentary Advances Direct Loan specialists at classicquid.co.uk?

Classic Quid has focused on client insurance as a main concern as long as necessary. As the most legitimate direct moneylenders for short term loans UK direct lender in a spotted market, we have offered sensible and obliging reimbursement terms to our strength. We continually try to avoid potential risk to guarantee that the customer can manage the cost of the installments by doing exhaustive reasonableness checks. To guarantee that your funds won't put you in a tight monetary circumstance.

That's what it follows, you simply have to fill in the sum that you consider you can bear to pay the sum in each period of portion, in light of your income and money related financial plan. Soon in the wake of entering the advance charges as loan fees of the credit that you intend to take. The vital sum that you will be gave as advance would be screened.

Modest short term loans UK direct banks are extremely easy to utilize and will help you in covering the general installments. You can make use of the number cruncher to consider about the amount of you'll possess to save beside your month income for taking care of the advance. Further you can likewise get an undeniable thought with respect to how much a credit arrangement will cost you in minutes by making not many snaps.

Short Term Loans UK for Any Financial Need

Short term loans for bad credit are available. They are not available from all loan providers, but those that do usually charge a higher APR because you are deemed a higher risk. Personal loans for bad credit can help you improve your credit score if you manage your monthly payments properly. If you use your home or another valuable item as collateral, the lender can repossess your property to recoup their losses if you fail to make payments. This is a higher risk option that should be carefully considered. This is why we only provide short term loans UK applications.

https://classicquid.co.uk/

4 notes

·

View notes

Text

Energy price

How to smooth over the energy price shock

Prime Minister Boris Johnson is under pressure to act on soaring energy prices and household costs as a jump in capped bills looms in April.

The government has a trilemma over energy prices: how to solve the cost-of-living crisis, while being focused on net-zero, and unwilling to increase taxation or borrowing.

There may be no ideal solution, but a number of questions need clarification.

Who should be shielded from a 50% rise in energy prices and for how long?

Who should bear the burden - bill payers or taxpayers? Are we willing to take a hit on government debt?

And do we want to smooth this over 25 years or two or three years?

·Boris Johnson promises action over rising energy bills

·Energy prices: Government must show more urgency, says Ova boss

Imminent rises

The energy price rises that are coming in April and again in the autumn will reach well beyond the "hard-up" or "fuel poor", possibly sending inflation towards an incredible 7%.

This is something not seen in three decades, since well before the independence of the Bank of England.

Such is the scale of the increases in the pipeline - with typical bills heading to £165 a month - which the pressure will affect millions of lower-middle-income households as well as poorer ones.

Average households, which currently spend 4% of their disposable income on energy, will see that almost double many business listing.

A recent poll suggested that half of Britons would not be able to afford a rise in their monthly bills of £50 a month. That's the increase which is coming in a few weeks' time.

All of this means there are some fundamental flaws with the three main solutions currently being floated.

Discount expansion

An expansion of the £140 Warm Home Discount scheme is the current most-talked-about plan.

The current budget of this scheme is less than £500m a year.

It is not really designed for a situation where several million people might need support to fund a £20bn energy price shock.

The "core" element of the scheme distributes payments automatically to low-income elderly using pension credit data.

But there are now more people in the broader part of the scheme for working-age recipients of the discount.

This part of the scheme is run on a first-come-first-served basis, where recipients have to apply for the discount from a fixed pot of funds at each energy company and hope that the fund isn't exhausted.

There are some different criteria applicable at each energy company so claimants may not be eligible if they have switched.

The most significant factor, though, is that no funds come from the taxpayer.

It is all funded by the energy companies, or rather, funded from energy bills.

Redistributing half a billion for the fuel poor on to wealthier people's bills is one thing.

Adding several times that, on top of the record increases, starts to assume the character of a new tax.

Cuts to VAT and green levies

A cut in VAT saves 5% or £95 off a £1900 predicted bill. This might prove a helpful addition, but will not fundamentally alter the picture.

It also gives more cashback to those with the biggest bills, or the largest, least well-insulated mansions. And it also loses revenue to the Exchequer.

And then there is getting rid of the "green levies". These are a range of policies that add about £170 to bills business listings.

They reflect the funding for historical investments in green energy and a range of social obligations.

They would be required instead to be funded by the taxpayer.

A version of this idea was floated four years ago in Professor Dieter Helm's "Cost of energy" report to the government. He said that report had been "shelved".

Putting off costs

There is another solution that the government is looking at: what is being termed a "cost deferral mechanism".

Essentially some big banks, possibly backed by a Treasury guarantee, lend billions to energy companies, who then spread a £600 immediate hike, into, say an additional £120 premium every year for five years, or less over a decade.

It is possible to do this without Treasury backing, but some sort of adaptation of rules governing existing deferral arrangements such as the last resort supplier schemes would be needed.

Another version of this scheme being pushed in Whitehall could utilize the pandemic rescue architecture at the Bank of England by providing up-front funding.

This could prove rather controversial, but some argue that the scheme could help prevent inflation from getting to 7%.

Some version of the scheme, or "smoothing mechanism", has been gaining traction in the energy sector, in some government departments, and among MPs keen for a plan.

But it doesn't have universal backing in the energy industry.

In an interview with the BBC, earlier this week Centrica chief executive Chris O 'Sheaf referred to it as a "bailout" for energy companies.

That in turn has led to some skepticism at the Treasury about how it can work.

But I understand that plans along these lines are being worked up, with some observers seeing this scheme as the cornerstone of a Prime Ministerial relaunch in the coming weeks.

Short or long-term hike?

The judgment on whether this is a one-off shock, or whether, as Mr O'Shea suggested, it will last two years or more, is critical here.

There are reasons to believe it is the consequence of an exceptional set of circumstances.

Firstly, the post-pandemic bounce-back led to unprecedented demand, including for gas.

Secondly, the fact that due to a late, cold, and long winter last year, crucial stores of gas in Europe never got full in the first place going into this winter.

And lastly, there is the Nordstrom 2 pipeline from Russia which is finished, but has not been certified by Germany free business listings.

The prediction that wholesale gas prices stay high for a year or two is a reflection of what futures markets are saying.

All of that could change rather rapidly with a speech from Russian President Vladimir Putin, or when the global economy normalizes.

But we cannot be certain either way.

If a smoothing mechanism is put into operation, and wholesale prices remain high, then households might get prolonged chronic pain and a never-ending scheme.

Does the political cycle lend itself to such a spread of the burden with a general election expected in 2024?

All of this points to the traditional moment where Number 10's First Lord of the Treasury - one of the Prime Minister's official titles - overrules a fiscally cautious Chancellor.

But the political backdrop of "party gate" adds some uncertainty to what actually happens here.

The fundamentals are this though: Is this a one-off price shock? And for how long does the government want to spread the energy price pain?

For ordinary households, there couldn't be a more important consequence to the nation's currently delicate political balance.

Boris Johnson says he is talking to Chancellor Rishi Sunak over how the government could help people with soaring energy prices.

The prime minister is under pressure to act on rising household costs, ahead of further increases to capped bills due in April.

Some Tory MPs want cuts to green levies and VAT to help bring bills down.

Labour, which also wants VAT suspended, is also demanding higher taxes on oil and gas producers.

The party said it would use money from the hike to pay for more generous government payments to help poorer households with costs.

On Monday, Mr Johnson said ministers understood the difficulties people were facing, and "we're certainly looking at what we can do".

·Labour demands energy firm tax hike to cut bills

·How can the government solve the energy crisis?

·How much would a VAT cut on my energy bill save?

Trade body Energy UK predicts bills will surge by up to 50% in April, when the change to the price cap, due to be determined in February, kicks in.

There have been warnings that average households could pay about £700 more per year, amid surging prices for wholesale gas worldwide.

Speaking to reporters during a visit to a vaccination center, Mr Johnson said rises were driven by "general inflationary pressure" caused by the world economy "coming back from Covid".

But he added: "We've got to help people, particularly people in low incomes, we've got to help people with the cost of their fuel - and that's what we're going to do."

Asked if he would meet Mr Sunak this week, he replied: "I've been meeting the chancellor constantly. I met the chancellor last night to talk about it."

Mr Johnson is expected to hold his first formal discussions with Mr Sunak on Monday, although a decision on what to do is not expected imminently.

1 note

·

View note

Text

CLICK n’BANK AI Review – Unlimited Free Buyer Traffic & Commission System

Welcome to my CLICK n’BANK AI Review, I will cover its features, upgrades, price, demo, bonuses, benefits, and my own personal opinion. The new “Copy & Paste” AI system Exploits ClickBank Every 60 Seconds For Set & Forget $50-$100/Paydays And Unlimited Free Buyer Traffic.

Do you ever wish that fixing your systems was as simple as pressing a single button? But with CLICK n’BANK, you connect to X’s unstoppable traffic courtesy of Elon’s strategic planning, as well as the optimal platform that handles all the hard work. You also need to factor the ClickBank commissions. Even better, CLICK n’BANK Affiliate marketers designed a breakthrough AI system called CLICK n’BANK that makes the process of driving targeted traffic and earning commissions much smoother. It says it is compatible with any affiliate network including Warrior plus Click bank, Digistore24, Amazon affiliate, and others. Another advantage of using CLICK n’BANK AI software is that it can help make and improve affiliate campaigns no matter the level of the marketer. It employs artificial intelligence to search for various affiliate offers to identify which of them is most profitable and then it redirects the traffic to the offer sites and earns commissions without any further efforts.

What Is Click n’Bank AI?

CLICK n’ BANK AI is an affiliate marketing AI which is perfect for making earning process as easy as possible. It employs artificial intelligence in features such as Identifying profitable offers, Traffic generation, Commission tracking among others. The platform is to ensure that affiliate marketing is enhanced by making it easy for the marketers, whether new or old since most of the work is done by the platform.

The main advantages include the access to the carefully selected and high converting offers list, multiple opportunities to create marketing campaigns quickly, as well as traffic generated by CLICK n’ BANK AI. This can be quite useful in saving much time and energy on the process and channel the efforts and resources more effectively to another genre of the online business or some personal problems.

Click n’Bank AI Review: Overview

Product Creator: Glynn Kosky

Product Name: CLICK n’BANK AI

Launch Date: 2024-Sep-24

Launch Time: 10:00 EDT

Front-End Price: $17 (One-time payment)

Official Website: Click Here To Visit Official Salespage

Product Type: Tools And Software

Support: Effective Response

Discount: Get The Best Discount Right Here!

Recommended: Highly Recommended

Bonuses: YES, Huge Bonuses

Skill Level Required: All Levels

Refund: YES, 180 Days Money-Back Guarantee

<<>> Get Access Now Click n’ Bank AI Discount Price Here <<>>

Click n’Bank AI Review: Key Features of Click n’Bank AI

Turn Clickbank & X Into A Viral ATM

Newbie Friendly Interface

Profitable Templates To Choose From

Intuitive Drag-and-Drop Interface

Built-In AI Powered Content Creator

Built-in AI-Generated Cash Campaigns

ClickBank Income Potential

High Ticket Campaigns Included

System Works On All Popular Devices

All Major 3rd Party Integrations Supported

Automated AI Traffic Feature Built-In

DFY Business Commercial Licence Included

No Monthly Fees

Built-In Offers Included

Click n’Bank AI Review: How Does It Work?

You’re Now Just 3 Steps Away From Job Replacing Freedom! (Do it from your phone, from your laptop from anywhere)

Step #1: Login

Access Click n’Bank AI On Your Computer or Mobile Phone Works on ANY Device

Step #2: Copy & Paste

Simply Copy & Paste ONE Secret ClickBank Affiliate Link into Our DFY A.I Traffic System Zero Extra Work Required

Step #3: Get Results!

Each Time We Copy & Paste Our Affiliate Link, We Make Around $50-$100 Sent To Our PayPal Or Bank Account

Click n’Bank AI Review: Why You Must Grab It

Tap Into Set ’n’ Forget Automated System Powered by A Simple Copy & Paste!

Get Unlimited Free Traffic In 1-Click.

The Price Goes Up Every 60 Minutes

Our Members Get Paid Daily

With Click n’Bank AI You Don’t Need Anything Else

Click n’Bank AI Makes Us $ Without Doing Any Selling

No Monthly Fees, Register Once & Use Forever

Act Fast For $$$$s In Premium Bonuses

Do This from Your Phone

Zero Overhead Costs

Risk-Free 180-day Money Back Guarantee

Legendary Customer Support

The Price Is Rising, If You Wait, You’ll Pay More!

<<>> Get Access Now Click n’ Bank AI Discount Price Here <<>>

Verify Users Say About Click n’Bank AI

Click n’Bank AI Is The All-in-One System For You

Cutting edge AI technology

Push-button simple (proven by newbies)

Industry leading support as voted by our customers

World-class training from a 7-figure marketer

Done-for-you monetization

No monthly costs (when you act now)

Takes nanoseconds to activate

No maintenance or setup hassles

Self-updating app

Everything you need is included

Click n’Bank AI Review: Who Should Use It?

Teenagers

College Students

People In Their 20s

Housewives

Stay At Home Dads

Busy People

The Family Man

Old Age Pensioners

Click n’Bank AI Review: OTO’s And Pricing

Front End Price: CLICK n’BANK AI ($17)

OTO 1: Unlimited Version ($67/$37)

OTO 2: 100% DONE-FOR-YOU ($97/47)

OTO 3: Unlimited Traffic ($97/47)

OTO 4: AUTOMATION ($67/37)

OTO 5: ATM ($197/$47)

OTO 6: ULTIMATE ($197/$47)

OTO 7: License Rights ($67/37)

<<>> Get Access Now Click n’ Bank AI Discount Price Here <<>>

My Own Customized Incredible Bonus Bundle

How To Claim These Bonuses*

Step #1:

Complete your purchase of the Click n’Bank AI: My Special Unique Bonus Bundle will be visible on your access page as an Affiliate Bonus Button on WarriorPlus immediately after purchase. And before ending my honest Click n’Bank AI Review, I told you that I would give you my very own unique PFTSES formula for Free.

Step #2:

Send the proof of purchase to my e-mail “[email protected]” (Then I’ll manually Deliver it for you in 24 HOURS).

Click n’Bank AI Free Premium Bonuses

Bonus #1: $997 Daily ZERO-COST Auto Bot

Swipe the same method we’ve used to generate an average of $997 a day every single day for the past 12 months.

Bonus #2: $300 Per Day Auto Affiliate Check

Activate the same system we use to get multiple $300 commissions daily. Works perfectly with the system you’re buying today.

Bonus #3: Zero To $1K In Seven Days

You’re invited to the private LIVE online event where we’ll reveal how we make $1,000 in the next few days.

Bonus #4: First Sale In 60 Minutes

This unique loophole lets us make our first sale in 60 minutes without a list, paid traffic, or anything else complicated, it’s all revealed to you inside.

Bonus #5: Commercial License

You’ll Also Get a Commercial Licence So You Can Sell This System To Others For $500 — $1,000 Over & Over.

Click n’Bank AI Review: Money Back Guarantee

The Iron-Clad 180-Day 100% Money-Back Guarantee

Try out the Click n’Bank AI and every asset and bonus (including the bonuses) for the next 180 days, for free. Watch for yourself how the system successfully transforms even a double tap into the real outcomes. Do not hesitate to contact our support team if you have any questions, all our specialists work in the USA and are available round the clock. But just in case you wake up one morning with a new resolve of changing your mind, for any reason or for no reason at all Then you have got six full months of trial period during which you have the complete freedom to ask for a refund if you desire. PLUS — prove to us that you tried Click n’Bank AI for at least 30 days And we will double your money back PLUS, I’ll work with you one-on-one for 6 weeks! That is the level you should expect from a company that aims to help you build your dream business. Therefore, invest confidently knowing that we’ll follow through any means necessary to get you the results you have been yearning for.

<<>> Get Access Now Click n’ Bank AI Discount Price Here <<>>

Click n’Bank AI Review: Pros and Cons

Pros:

Automation: Simplifies the affiliate marketing process and saves time.

AI-Powered: Leverages advanced technology to optimize results.

Beginner-Friendly: Accessible to users of all levels.

Potential for High Earnings: Can generate significant income if used effectively.

Excellent Customer Support: Provides helpful assistance to users.

Cons:

You need internet for using this product.

No issues reported, it works perfectly!

Frequently Asked Questions (FAQ’s)

Q. What devices does this work on?

Click n’Bank AI is web-based so it works on every device out there. All you need is an internet connection.

Q. Is there a money-back guarantee?

Yes, you are covered by our 180-day money-back guarantee. There is absolutely no risk when you act now. The only way you lose is if you don’t grab Click n’Bank AI at the special discount…

Q. Is this beginner-friendly?

Absolutely — the majority of our beta testers were brand new to making money online. And you also won’t need any technical skills or previous experience.

Q. Are there any monthly costs or fees?

Nope! Click n’Bank AI includes everything you need. Because there are no extra costs involved, this is as close to a ‘pure profit’ model as you’ll get.

Q. How long does it take to set up?

Even if you’re brand new you can be up and running in 5 minutes. Click n’Bank AI is a self-updating system that requires no daily maintenance.

Q. What if I need help or support?

We love helping our customers! Professional, patient & friendly support staff are on hand to answer any questions you may have.

Q. How do I get started?

Easy! Just click the button below to get in at the lowest possible price before the next price increase.

Click n’Bank AI Review: My Recommendation

Click n’ Bank AI is an excellent tool that assists in promoting affiliate links and could help you make money online. It is not a sinecure to success but, it could be a plus for the people who are willing to work it and wanted to know how it operates. Summing up, if you would like to switch your work in affiliate marketing to a more automatic level and, maybe, gain more profit — try the Click n’ Bank AI.

<<>> Get Access Now Click n’ Bank AI Discount Price Here <<>>

Check Out My Previous Reviews: MusicPal Review, Traffit Review, PLR Cash Review, ADASuite Review, Magnus Review, Themes Ninja Review, and ProfitList Review.

Thank for reading my CLICK n’BANK AI Review till the end. Hope it will help you to make purchase decision perfectly.

Disclaimer:

Please note: This Click n’ Bank AI review is based on publicly available information and user reviews. We cannot guarantee the accuracy of the platform’s claims, and individual experiences may vary. It’s important to conduct thorough research before making any purchase decisions.

Note: This is paid software, and the one-time price is $17.

#ClickNBankAI#ClickNBankAIreview#ClickNBankAIfeatures#ClickNBankAIworks#WhatisClickNBankAI#buyClickNBankAI#ClickNBankAIprice#ClickNBankAIdiscount#ClickNBankAIoto#GetClickNBankAI#ClickNBankAIbenefits#ClickNBankAIbonus#ClickNBankAIsoftware#ClickNBankAIApp#ClickNBankAIFunnels#marketingprofitmedia#ClickNBankAIUpsell#ClickNBankAIinfo#PurchaseClickNBankAI#ClickNBankAIexample#ClickNBankAIworthgorbuying#software#AISoftware#AIApp#AITool#ClickNBankAIreviews#ClickNBankAIreviewwalkthrough#ClickNBankAIreviewbonus#ClickNBankAIreviewWarriorPlus#Affiliate

0 notes

Text

How to Use an FD (Fixed Deposit) Calculator and SWP (Systematic Withdrawal Plan) Calculator Together for Better Financial Planning

Modern financial planning must balance growth and stability. Fixed deposits (FDs) and systematic withdrawal plans (SWPs) meet various financial needs. SWPs withdraw from mutual funds to generate income, unlike FDs, which offer stable returns with low risk. Use an FD and SWP calculator to maximise these investment options. You can optimise savings and income by doing so.

What is an FD Calculator?

The online FD (Fixed deposit) calculator estimates fixed deposit investment returns. FDs are popular for their safety and guaranteed returns, and the FD (Fixed deposit) calculator shows how much interest you will earn at the end of the deposit term. By entering the principal amount, bank interest rate, and FD tenure, you can easily calculate the maturity amount.

Anyone planning a fixed income portfolio needs this tool. The FD (Fixed deposit) calculator shows you how much your savings will grow over time, whether you're saving for a car or an emergency fund.

What is an SWP (Systematic Withdrawal Plan) Calculator?

A SWP (Systematic Withdrawal Plan) calculator serves a different purpose. It estimates regular mutual fund income from systematic withdrawals. SWPs allow you to withdraw a fixed amount from your mutual fund investment at regular intervals, making them popular with retirees and others seeking a steady income.

This calculator requires the investment amount, expected rate of return, withdrawal amount, and withdrawal frequency. It then calculates the investment's lifespan to help you budget.

Using FD (Fixed deposit) Calculator and SWP (Systematic Withdrawal Plan) Calculator Together

By combining the FD (Fixed deposit) calculator and SWP (Systematic Withdrawal Plan) calculator, you can plan both your short-term savings and long-term income needs. Here’s how you can use these tools together for better financial planning:

Balancing Stability and Growth: FDs are stable, while mutual funds offer higher returns but market risk. Using an FD calculator, you can invest some of your savings in fixed deposits for guaranteed returns. In addition, use the SWP (Systematic Withdrawal Plan) calculator to set up regular mutual fund withdrawals to supplement your income.

Setting Financial Goals: An FD (Fixed deposit) calculator can help you calculate how much fixed deposits you need for big expenses like college or a house down payment. After saving enough, use the SWP (Systematic Withdrawal Plan) calculator to generate a steady income from mutual funds to cover expenses.

Creating a Retirement Plan: Many people build retirement wealth with fixed deposits and mutual funds. The FD and SWP (Systematic Withdrawal Plan) calculators can help you plan for retirement with a lump sum and regular income. FD returns can cover large, one-time expenses, while SWP returns can cover monthly living costs.

Managing Cash Flow: Using both calculators improves cash flow management. The FD (Fixed deposit) calculator shows when and how much you will receive from your fixed deposit, while the SWP (Systematic Withdrawal Plan) calculator shows how much you can withdraw from mutual funds without depleting the investment. This helps manage a financial plan smoothly.

0 notes

Last Seen Blogs

josebekmiccaly

Josebek Miccaly & Francisco Javier

violetmile

Nowhere Again

shbetsy

Shbet – Cổng game Cá Cược Uy Tín An Toàn Đến Từ C

ihopeyourapplepieisfreaknwo-blog

I'm just reserving this url because i love this qu

sunshine-polls

Daily polls for Tumblr folks