#FHA guidelines

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

The Tumblr app for Google Glass was released on May 16, 2013.

Text

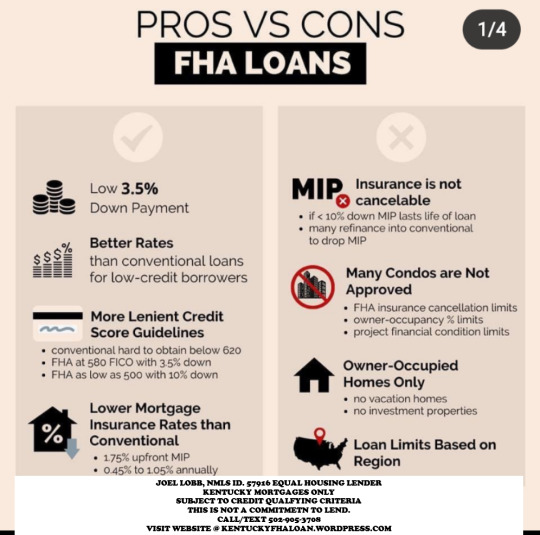

Kentucky FHA Loan Requirements

Kentucky FHA Mortgage Loan Lender Guidelines Kentucky FHA Loan Requirements The requirements for Kentucky FHA loans are set by HUD. Borrowers must have a steady employment history of the last two years within the same industry or line of work. Recent college graduates can use their transcripts to supplant the 2-year work history rule as long as it makes sense. Self-Employed will need a 2-year…

View On WordPress

#Appraisers FHA#bad credit fha loan#collections fha loan#credit scores fha loan#FHA#fha $100 down program#fha appraisals#FHA Approved Condos Louisville Kentucky#FHA Back to Work Program Ky#fha borrowers#FHA Co-signors#fha collections#fha credit score#fha foreclosure#FHA Guidelines#First-time buyer#Kentucky

0 notes

Text

Understanding the FHA Bankruptcy Waiting Period

Navigating the world of home loans can be particularly challenging if you've recently filed for bankruptcy. If you're thinking about an FHA loan, it's crucial to understand the FHA bankruptcy waiting period and how it impacts your eligibility. This comprehensive guide covers everything you need to know, answering key questions to help you along the way.

What Is an FHA Loan and How Does It Work?

An FHA loan is a mortgage insured by the Federal Housing Administration (FHA). These loans are designed to assist individuals who may not qualify for conventional mortgages, including first-time homebuyers, borrowers with lower credit scores, and those with adverse credit events such as bankruptcies. FHA loans typically feature lower down payments and more lenient credit requirements compared to conventional loans, making them an appealing option for many borrowers.

Benefits of an FHA Loan

Lower Down Payment Requirements: FHA loans allow down payments as low as 3.5%, making homeownership more accessible.

Flexible Credit Score Requirements: FHA loans are particularly accommodating for borrowers with lower credit scores or past bankruptcies.

Low Interest Rates: FHA interest rates are generally lower than those of conventional loans, such as those offered by Fannie Mae.

Cash-Out Refinances: FHA loans allow for cash-out refinances up to 80% loan-to-value, providing flexibility for homeowners needing access to cash.

A Note on Mortgage Insurance: While FHA loans require both upfront and monthly mortgage insurance, it's worth noting that conventional loans also require mortgage insurance when the down payment or equity is less than 20%. Mortgage insurance protects lenders in case a borrower defaults on their loan.

How Does Bankruptcy Affect Your FHA Loan Eligibility?

Bankruptcy can have a considerable impact on your credit history and financing options, but it doesn’t mean you’re permanently ineligible for an FHA loan. Understanding the waiting periods and specific requirements tied to different types of bankruptcy is crucial for determining your eligibility for an FHA loan, whether you're looking to refinance or purchase a home.

Chapter 7 Bankruptcy

For Chapter 7 bankruptcy, you generally need to wait at least two years from the discharge date before qualifying for an FHA loan. This waiting period is designed to give you time to rebuild your credit and show improved financial stability. During this time, you'll need to:

Rebuild Your Credit: Re-establish a good credit history and provide a satisfactory explanation for the bankruptcy.

Demonstrate Financial Stability: Show that you have managed your finances responsibly since the bankruptcy discharge.

Chapter 13 Bankruptcy

If you’re in a Chapter 13 repayment plan, you may qualify for an FHA loan under specific conditions:

While in Repayment Plan: You can apply for an FHA loan if you’ve made timely payments for at least one year and have received court approval.

After Discharge: There’s typically a 12-month waiting period post-discharge before you can apply for an FHA loan.

Consistent, timely payments during the repayment period are crucial to demonstrate financial responsibility.

FHA Chapter 7 Bankruptcy Waiting Period

The waiting period for an FHA loan following Chapter 7 bankruptcy is generally two years from the discharge date. This allows you time to rebuild your credit and demonstrate improved financial stability. Here's how to use this period effectively:

Rebuilding Credit: Key Steps to Improve Your Score

Obtain Secured Credit Cards: Secured credit cards require a cash deposit as collateral, which typically becomes your credit limit. Use these cards for small purchases and pay off the balance in full each month. This will help rebuild your credit score over time.

Pay Bills on Time: Consistently paying all bills, including utilities and rent, is crucial. Timely payments are the largest factor in your credit score, so set up automatic payments or reminders to avoid missing due dates.

Monitor Your Credit Report: Regularly check your credit report for errors or inaccuracies. You’re entitled to a free credit report from each major bureau (Experian, TransUnion, and Equifax) once a year. Dispute any incorrect information to ensure your report accurately reflects your financial behavior.

Keep Credit Utilization Low: Aim to keep your credit utilization ratio below 30%. This ratio is the percentage of your credit card balances relative to your credit limits. High credit utilization can negatively impact your score, while a lack of utilization can also be detrimental.

Avoid Opening Too Many Credit Accounts: While having at least three credit accounts is beneficial, opening too many accounts in a short period can lower your credit score due to hard inquiries. Focus on managing your existing accounts before considering new credit.

Saving for a Down Payment: Why It Matters

Even though FHA loans require a lower down payment, saving more can enhance your loan application and provide several benefits:

Strengthen Your Loan Application: A larger down payment reduces the lender’s risk and demonstrates financial discipline, which can be especially important after bankruptcy.

Lower Monthly Payments: A bigger down payment reduces the amount you need to borrow, lowering your monthly mortgage payments and making homeownership more affordable.

Better Loan Terms: While less of a factor with FHA loans, a substantial down payment might help you negotiate better terms, such as a lower interest rate.

Emergency Fund: Extra savings not only aid with the down payment but also provide a safety net for unexpected expenses, helping you avoid future financial difficulties.

What Is the FHA Chapter 13 Bankruptcy Waiting Period?

If you've filed for Chapter 13 bankruptcy, the waiting period to qualify for an FHA loan differs from that of Chapter 7. Here’s a breakdown of what you need to know to prepare for your FHA loan application after a Chapter 13 bankruptcy:

While in the Chapter 13 Repayment Plan

Eligibility: You may qualify for an FHA loan while still in the Chapter 13 repayment plan if you meet specific criteria.

Timely Payments: You must have made at least 12 months of timely payments to the bankruptcy trustee and/or creditors.

Court Approval: You need to obtain written approval from the bankruptcy court. This approval indicates that the court believes you can handle new debt without jeopardizing your repayment plan.

After Chapter 13 Discharge

12-Month Waiting Period: Once your Chapter 13 bankruptcy is discharged, there is typically a 12-month waiting period before you can apply for an FHA loan.

Maintaining Stability: During this period, continue to manage your finances responsibly. Ensure timely payments on all remaining debts and avoid any new derogatory marks on your credit report.

Document Financial Improvement: Be prepared to provide documentation of your financial history and improvements since your bankruptcy discharge. This includes your credit report, proof of income, and a letter explaining your bankruptcy and the steps you've taken to improve your financial situation.

Understanding these timelines and requirements will help you navigate the FHA loan process more effectively and increase your chances of securing financing for your future home.

During the Repayment Plan: Can I Qualify for an FHA Loan?

Yes, it's possible to qualify for an FHA loan while you're still in a Chapter 13 repayment plan, but there are specific conditions you need to meet. Here’s what you need to know:

Timely Payments

Requirement: You must have made at least 12 months of timely payments to the bankruptcy trustee and/or creditors as specified in your Chapter 13 repayment plan.

Purpose: This shows lenders that you have successfully managed your financial obligations and regained financial stability.

Court Approval

Obtain Approval: You’ll need written approval from the bankruptcy court to proceed with an FHA loan application.

Reason: This approval confirms that the court has reviewed your financial situation and agrees that you can handle new debt without disrupting your repayment plan.

Conditions: The court’s permission is often based on your ability to continue making Chapter 13 payments while managing a new mortgage.

Documenting Your Financial Responsibility

Payment Documentation: Prepare to provide detailed records of your payment history during the Chapter 13 plan. This includes receipts or statements showing consistent, on-time payments.

Explanation Letter: Write a letter explaining the circumstances of your bankruptcy and how your financial situation has improved. This letter helps lenders understand your financial journey and the steps you’ve taken to improve your creditworthiness.

Assistance

Seek Expert Help: Work with a lender who has experience handling bankruptcies. An experienced lender can guide you through the process, answer your questions, and help ensure that you meet all the necessary requirements for your FHA loan application.

By following these steps and meeting the requirements, you can navigate the FHA loan process more effectively while still in a Chapter 13 repayment plan.

After Discharge: What Are the Next Steps?

Once you've successfully completed your Chapter 13 repayment plan and received your discharge, you're looking at a 12-month waiting period before you can apply for an FHA loan. Here’s what you need to focus on during this time:

12-Month Waiting Period

Start Date: The waiting period begins from the date of your Chapter 13 discharge.

Purpose: This period is designed to help you further stabilize your financial situation and continue rebuilding your credit profile.

Maintaining Financial Stability

Timely Payments: Continue to make timely payments on all your remaining debts and obligations. Maintaining a clean payment history is crucial.

Avoid Negative Marks: Steer clear of late payments or any new derogatory marks on your credit report, as these can impact your FHA loan application.

Saving for a Down Payment

Importance: While FHA loans require a down payment as low as 3.5% (for those with credit scores of 580 or higher), saving more can strengthen your application.

Benefits: A larger down payment not only improves your attractiveness as a borrower but can also lower your monthly mortgage payments and potentially secure better loan terms.

Documentation and Proof of Financial Improvement

Prepare Documentation: Gather comprehensive documentation of your financial history and improvements since your bankruptcy discharge. This should include:

Credit report

Proof of income

Employment history

Any other relevant financial documents

Explanation Letter: Write a letter explaining your bankruptcy and how your financial situation has improved since then. This can help lenders understand your financial journey better.

Consultation with a Mortgage Professional

Seek Expertise: Engage with a mortgage professional who has experience handling cases involving bankruptcy. They can provide valuable guidance and help you navigate the FHA loan application process effectively.

By focusing on these steps, you'll be better prepared to apply for an FHA loan once the waiting period has elapsed, and you’ll be on your way to achieving your homeownership goals.

How Can I Improve My Chances of Getting an FHA Loan After Bankruptcy?

Improving your chances of securing an FHA loan after bankruptcy involves several key steps. Here’s how you can enhance your application:

Build a Positive Credit History

Make On-Time Payments: Ensure all your current debts and bills are paid on time. Payment history is a significant factor in your credit score.

Keep Credit Utilization Low: Maintain a low ratio of credit card balances to credit limits, ideally below 30%.

Avoid New High-Interest Debt: Be cautious about taking on new debt, especially high-interest loans, which can negatively impact your credit profile.

Save for a Down Payment

Increase Your Down Payment: Although FHA loans have a lower down payment requirement, saving more can strengthen your application. A larger down payment not only demonstrates financial responsibility but can also help reduce your monthly mortgage payments.

Provide a Detailed Explanation

Explain Your Bankruptcy: Prepare a clear, honest explanation of the circumstances that led to your bankruptcy and how your financial situation has improved since then. This explanation can help lenders understand your financial journey and assess your current stability.

Obtain Court Approval (For Chapter 13 Applicants)

Seek Court Permission: If you are still under a Chapter 13 repayment plan, make sure to obtain written approval from the bankruptcy court. This approval indicates that the court believes you can manage a new mortgage without disrupting your repayment plan.

By following these steps, you’ll be better positioned to navigate the FHA loan process and enhance your chances of approval, paving the way toward your homeownership goals.

What Are the Exceptions to the FHA Bankruptcy Waiting Period?

While FHA guidelines typically adhere to standard waiting periods after bankruptcy, there are exceptions for cases involving extenuating circumstances. If you can prove that your bankruptcy resulted from factors beyond your control, you might be eligible for a waiver. Here are some scenarios that might qualify for an exception:

Significant Income Loss

Criteria: Demonstrate a temporary loss of at least 20% of your income for a minimum of six months.

Evidence: Provide documentation such as unemployment records, income statements, or other proof of reduced earnings.

Medical Emergencies

Criteria: Severe illness or injury that led to substantial financial hardship.

Evidence: Medical records, hospital bills, or other documentation showing the impact of the medical emergency on your finances.

Death of the Primary Earner

Criteria: The death of the main income earner in your household.

Evidence: Death certificate, financial statements showing the impact on household income.

To qualify for an exception, you’ll need to present thorough documentation of these extenuating circumstances and show that you have maintained responsible financial behavior since your bankruptcy discharge.

Frequently Asked Questions

What is the FHA bankruptcy dismissal waiting period?

If your Chapter 13 bankruptcy case is dismissed rather than discharged, you must wait two years before qualifying for an FHA loan. This waiting period provides time to re-establish your credit and demonstrate financial stability.

How Long Does It Take to Get an FHA Loan?

Once you meet the qualifications, securing an FHA loan typically takes 30 to 45 days. Here’s a quick breakdown:

Application and Documentation: 1-2 weeks to submit and review documents.

Loan Processing: 2-3 weeks for verification and appraisal.

Underwriting: 1-2 weeks for final approval.

Closing: About 1 week to sign documents and finalize the loan.

Factors that can affect timing include the lender’s processing speed, the complexity of your financial situation, and any property issues. Staying prompt with your paperwork can help expedite the process.

How to Rebuild Your Credit After Bankruptcy

Get Secured Credit Cards: Apply for one or more secured credit cards and make timely payments to start rebuilding your credit.

Manage Credit Utilization: Keep your credit utilization below 30% and avoid high-interest debt.

Pay Bills on Time: Consistently pay existing debts like rent and utilities to build a positive payment history.

Establish Credit Accounts: Aim to have at least three credit accounts, which can be a mix of credit cards and installment loans.

FHA Loan Requirements for 2024

Credit Score:

580 or higher for a 3.5% down payment.

500–579 for a 10% down payment.

Debt-to-Income Ratio:

Typically under 43%, though exceptions can apply.

Income & Employment:

Proof of steady income and employment is required

Property Use:

The home must be your primary residence.

Yes, the same guidelines apply to both refinances and purchases when it comes to bankruptcies. You can refinance your existing mortgage during and after bankruptcy, following the same rules as for new home purchases.

The Bottom Line

Navigating the FHA bankruptcy waiting period can be complex, but you don’t have to do it alone. At JVM Lending, we specialize in helping borrowers with unique financial situations, including those who have filed for bankruptcy. Our team of experts is dedicated to providing personalized service and guiding you through every step of the loan process. Whether you’re rebuilding your credit, saving for a down payment, or looking to refinance, JVM Lending is here to help.

Read more

#FHA bankruptcy waiting period#home loan options#FHA loans#bankruptcy impact#real estate financing#mortgage guidelines#loan approval

0 notes

Text

How to Meet Conventional Loan Home Condition Requirements?

Found your dream home? Congratulations! But before you pop the champagne, there are a few hurdles to clear, especially if you’re financing with a conventional loan. Unlike Government-backed loans, conventional loans don’t have super strict requirements for the house itself. That might sound like good news, but it also means understanding what kind of condition your future home needs to be in to…

View On WordPress

#conventional appraisal guidelines#conventional appraisal requirements#conventional financing for manufactured homes#conventional loan appraisal requirements#conventional loan home condition requirements#conventional loan home inspection#conventional loan inspection requirements#conventional loan property requirements#conventional loan requirements#conventional loan requirements 2024#conventional loan vs fha#do conventional loans require inspection#does a conventional loan require a home inspection#financing for mobile homes#guidelines for conventional mortgage#how to buy a mobile home with no money down#manufactured home mortgage#mortgage for mobile home#mortgage manufactured home#mortgage on manufactured home#requirements for conventional loan#what are the requirements for a conventional mortgage

0 notes

Text

History of Red Lining

Redlining is a malicious practice that has plagued the United States for decades, with its effects still being felt by marginalized communities today. This discriminatory practice has its roots in the early 20th century, when federal housing policies and mortgage lending practices effectively institutionalized segregation and economic disenfranchisement of minority communities. The history of redlining is a dark stain on the social fabric of this country, and it is crucial to understand its origins and impact in order to combat its lasting effects.

The term “redlining” originated from the practice of marking certain neighborhoods on maps with red lines to indicate high-risk areas for mortgage lending. This practice became widespread after the passage of the National Housing Act of 1934, which established the Federal Housing Administration (FHA) and the Home Owners’ Loan Corporation (HOLC). These agencies were responsible for establishing lending guidelines and rating systems that effectively excluded minority communities from accessing affordable housing and loans.

The HOLC implemented a system of color-coded maps to assess the risk of lending in different neighborhoods, using racial demographics as a major factor in determining the risk level. Neighborhoods with predominantly white residents were typically graded as safe and received favorable lending terms, while those with minority populations, particularly African American and Latino communities, were graded as high-risk and were denied access to fair lending practices.

This deliberate and systematic discrimination led to the physical and economic segregation of communities, as minority residents were effectively blocked from accessing homeownership and the wealth-building opportunities that come with it. This practice perpetuated the cycle of poverty and reinforced the systemic inequality that still plagues American society today.

The impact of redlining is evident in the persistent wealth gap between white and minority communities, with minority households significantly lagging behind in homeownership rates and household wealth. The legacy of redlining is also seen in the disparities in access to quality education, healthcare, and economic opportunities in predominantly minority neighborhoods.

While redlining was officially banned with the passage of the Fair Housing Act of 1968, its effects continue to reverberate in the present day. The discriminatory lending practices that stemmed from redlining have contributed to the racial wealth gap and the continued segregation of neighborhoods across the country.

It is imperative to recognize the history of redlining as a form of institutionalized racism and to work towards remedying its lasting effects. Efforts to address these disparities must include policies that promote equitable access to housing, financial resources, and economic opportunities for marginalized communities. This includes initiatives to increase affordable housing options, improve access to fair lending practices, and invest in underserved neighborhoods to promote economic development and revitalization.

Additionally, addressing the legacy of redlining requires acknowledging the systemic racism that underlies these disparities and working towards creating a more just and equitable society. This involves confronting deep-rooted prejudices and biases, dismantling discriminatory policies, and actively promoting diversity, inclusion, and equality in all facets of society.

Photo by Unseen Histories on Unsplash

4 notes

·

View notes

Text

FHA Guidelines

FHA guidelines refer to the specific rules and requirements set forth by the Federal Housing Administration (FHA) for mortgage loans insured by the FHA. These guidelines are established to ensure that borrowers who seek FHA-insured loans meet certain criteria and that lenders follow standardized procedures when originating and underwriting these loans. The primary goal of FHA guidelines is to make homeownership more accessible to a broader range of borrowers, including those with lower credit scores or smaller down payments. These guidelines are subject to change, so borrowers and lenders should always consult the latest FHA requirements and work with FHA-approved lenders to understand and meet the criteria for FHA-insured loans. FHA guidelines are designed to promote responsible homeownership and expand access to mortgage financing for a wide range of individuals and families.

#fha loan#gca mortgage#property#real estate#united states#gustancho associates#usa#first time home buyer#va loans#bad credit score

2 notes

·

View notes

Link

10 FHA Guidelines EVERY Home Buyer Should Know https://www.madisonmortgageguys.com/fha-guidelines/

4 notes

·

View notes

Text

What types of properties qualify for a reverse mortgage?

A reverse mortgage allows homeowners to convert part of their home equity into cash without selling the property or making monthly mortgage payments. In the United States, the most common reverse mortgage is the Home Equity Conversion Mortgage (HECM), insured by the Federal Housing Administration (FHA). Understanding which properties qualify for a reverse mortgage is essential for homeowners considering this financial option.

Eligible Property Types for a Reverse Mortgage

To qualify for a reverse mortgage, the property must meet specific criteria set by the FHA:

Single-Family Homes: Traditional single-family residences are eligible, provided they serve as the homeowner's primary residence.

Multi-Family Homes: Properties with up to four units qualify if the homeowner occupies one of the units as their primary residence.

Approved Condominiums: Condominium units are eligible if they are part of FHA-approved complexes. It's important to verify the approval status, as not all condominiums meet FHA requirements.

Manufactured Homes: Manufactured homes can qualify if they meet FHA standards, including being built after June 15, 1976, and adhering to specific foundation and property guidelines.

Primary Residence Requirement

The property must be the homeowner's primary residence. Second homes and investment properties do not qualify for a reverse mortgage. The homeowner is required to certify annually that the property remains their primary residence.

Property Condition and Standards

The home must meet FHA minimum property standards to ensure safety and livability. An appraisal will assess the property's condition, and any necessary repairs may need to be completed before loan approval.

Financial Obligations of the Homeowner

While a reverse mortgage doesn't require monthly mortgage payments, homeowners are responsible for:

Property Taxes: Timely payment of property taxes is mandatory.

Homeowners Insurance: Maintaining adequate homeowners insurance is required.

Home Maintenance: The property must be kept in good repair to meet FHA standards.

Failure to meet these obligations can lead to loan default and potential foreclosure.

Conclusion

Understanding the types of properties that qualify for a reverse mortgage is essential for homeowners exploring this financial option. Eligible properties typically include single-family homes, select multi-family residences (up to four units, with one occupied by the borrower), FHA-approved condominiums, and certain manufactured homes that meet FHA guidelines. These homes must be used as the borrower’s primary residence and must meet basic property standards set by the FHA. By confirming your property qualifies and staying current on taxes, insurance, and maintenance, you can potentially tap into your home equity through a reverse mortgage.

Want to find out if your home qualifies? Contact Citizens Lending Group, a trusted mortgage lender in Anaheim, California, to speak with a reverse mortgage specialist today.

1 note

·

View note

Text

All Types of Home Loans (Conventional, FHA, Jumbo, VA, USDA Loans) in Dallas, TX

Buying a home in Dallas, TX, is an exciting journey, but navigating the various home loan options can be overwhelming. Whether you're a first-time homebuyer or looking to refinance, understanding the different types of home loans available—including Conventional, FHA, Jumbo, VA, and USDA loans—can help you make the best financial decision. At Edge Home Finance Inc, we specialize in guiding borrowers through the mortgage process, ensuring they secure the best loan for their needs. In this guide, we’ll break down each loan type, their benefits, and how they can help you purchase your dream home in Dallas.

1. Conventional Loans: Flexible Financing for Strong Credit

Conventional loans are one of the most popular mortgage options, backed by private lenders rather than government agencies. These loans are ideal for borrowers with good to excellent credit (typically 620 or higher) and a stable income.

Key Features of Conventional Loans in Dallas:

Down Payment Options: As low as 3% for qualified buyers (though 20% avoids PMI).

Loan Limits: Up to $766,550 for 2024 in Dallas (conforming loan limits).

Flexible Terms: 15-, 20-, or 30-year fixed-rate or adjustable-rate options.

If you have strong credit and want to avoid mortgage insurance or secure competitive interest rates, a Conventional loan from Edge Home Finance Inc may be the best choice.

2. FHA Loans: Low Down Payment & Lenient Credit Requirements

For buyers with lower credit scores or limited savings, an FHA loan (insured by the Federal Housing Administration) provides an accessible path to homeownership.

Why Choose an FHA Loan in Dallas?

Low Down Payment: Just 3.5% with a credit score of 580+ (or 10% for 500-579).

Easier Credit Approval: More forgiving of past financial challenges.

Competitive Rates: Often lower than Conventional loans for buyers with lower credit.

Edge Home Finance Inc helps many first-time buyers and those with limited funds secure FHA loans with minimal hassle.

3. Jumbo Loans: Financing High-Value Dallas Homes

If you’re looking to buy a luxury home in Dallas that exceeds conforming loan limits, a Jumbo loan is the solution. These loans finance properties above $766,550 (as of 2024) and require strong financial credentials.

Jumbo Loan Highlights:

Higher Loan Amounts: Covers luxury homes in Dallas’s upscale neighborhoods.

Strict Requirements: Excellent credit (700+), low debt-to-income ratio, and significant reserves.

Competitive Terms: Fixed or adjustable rates available.

Edge Home Finance Inc works with high-net-worth buyers to secure Jumbo loans with favorable terms.

4. VA Loans: Zero Down Payment for Veterans & Military

Active-duty service members, veterans, and eligible spouses can benefit from VA loans, backed by the U.S. Department of Veterans Affairs.

Advantages of VA Loans in Dallas:

No Down Payment Required: 100% financing available.

No PMI: Lower monthly payments compared to Conventional loans.

Flexible Credit Guidelines: Easier approval for qualified borrowers.

At Edge Home Finance Inc, we honor veterans by helping them secure VA loans with unbeatable benefits.

5. USDA Loans: Affordable Rural & Suburban Homeownership

The USDA loan program supports low-to-moderate-income buyers in eligible rural and suburban areas around Dallas.

Why Consider a USDA Loan?

Zero Down Payment: 100% financing for qualified buyers.

Low Mortgage Insurance: Lower costs than FHA loans.

Income & Location Eligibility: Must meet USDA property and income limits.

Edge Home Finance Inc helps buyers explore USDA loan options in Dallas’s qualifying areas.

6. Comparing Home Loan Options in Dallas, TX

Choosing the right loan depends on your financial situation, credit score, and homebuying goals. Here’s a quick comparison:Loan TypeDown PaymentCredit ScoreBest ForConventional3%-20%620+Buyers with strong creditFHA3.5%-10%500+First-time buyers, lower creditJumbo10%-20%+700+Luxury home purchasesVA0%VariesVeterans & militaryUSDA0%640+Rural/suburban buyers

7. Why Choose Edge Home Finance Inc for Your Dallas Home Loan?

At Edge Home Finance Inc, we simplify the mortgage process by:

Offering personalized loan recommendations based on your needs.

Providing competitive rates and fast approvals.

Guiding you through pre-approval to closing with expert support.

Whether you need a Conventional, FHA, Jumbo, VA, or USDA loan, we’re here to help you secure the best financing in Dallas.

8. Get Started on Your Dallas Home Loan Today!

Ready to buy a home in Dallas? Edge Home Finance Inc makes it easy with tailored loan solutions. Contact us today to explore your options and get pre-approved for the perfect mortgage!

By understanding the different types of home loans in Dallas, TX, you can confidently choose the best financing path. Let Edge Home Finance Inc be your trusted partner in homeownership!

0 notes

Text

youtube

Unlock Homeownership with FHA’s 3.5% Down Strategy Ready to unlock homeownership with FHA’s 3.5% down strategy? In this video, I break down everything you need to know about FHA loans, from qualification requirements to money-saving tips that can help you avoid costly mistakes. With over 19 years as a mortgage broker, I’ve helped first-time homebuyers navigate the complexities of FHA loans, and now I’m sharing those insights with you. Here’s what you’ll learn: - How FHA loans make homeownership accessible with low credit score requirements (as low as 500!). - The difference between a 3.5% and 10% down payment—and how improving your credit score could save you thousands. - FHA’s unique advantages for first-time homebuyers, including forgiving credit guidelines and flexible debt-to-income ratios. - How to use FHA loans to build wealth through house hacking with multi-unit properties. - Strategies like the bridge plan to refinance and eliminate long-term mortgage insurance costs. Whether you’re looking for home buying tips, expert mortgage advice, or smart financial strategies, this guide has you covered. FHA loans aren't just for getting approved—they’re a tool for creating opportunities and building a brighter financial future. Hit the like button if you found this helpful, subscribe for more first-time homebuyer and mortgage tips, and comment below with your questions. Let’s make your dream of homeownership a reality together! #mortgagerates #househacking #realestatemarket #conventionalloanvsfha #mortgagebroker CHAPTERS: 00:00 - FHA Loans: Analysis 00:50 - FHA Loans: Design 05:10 - FHA Loans: Development 11:36 - FHA Loans for Multifamily Property Investing 14:01 - Automated vs Manual Underwriting Explained 18:31 - The Bridge Strategy: Transitioning to Conventional Financing 21:05 - FHA 203k Loans: Financing Property Renovations 22:12 - FHA vs VA vs USDA Loans Comparison 22:43 - Success Stories: FHA Loan Borrowers 23:15 - The Bridge Strategy: Real Opportunities 23:30 - When to Refinance: FHA to Conventional Loans 23:55 - Connect with David Xi, Mortgage Expert via David Xie Mortgage Guy https://www.youtube.com/channel/UCYTXRSUzyEq7H_HSUyFzpoQ June 16, 2025 at 02:00AM

#mortgagerates#realestatetips#selfemployed#realestate#mortgage#wealthbuilding#investing#entrepreneur#Youtube

0 notes

Text

How FHA Loans Empower Homebuyers and Communities

In the heart of a bustling city, a young entrepreneur named Maya stood at the threshold of her first home. After years of saving, she was ready to take the leap—but the down payment felt like an insurmountable wall. Then she discovered the Federal Housing Administration (FHA). With its low down payment requirements and flexible credit guidelines, Maya was able to secure a mortgage and turn her…

0 notes

Text

Best Kentucky FHA lenders to get an Approval to buy a house.

How to Qualify for a Kentucky FHA Loan Approval: If you’re looking to buy a home in Kentucky and are considering a Kentucky FHA loan, it’s essential to understand the qualifying criteria and the necessary steps. This article covers all the crucial aspects you need to know, from credit scores, bankruptcy, work history, collections, closing, home insurance, title, debt ratio , down payment and…

View On WordPress

#$100 Down FHA Mortgage#2020 Kentucky FHA Mortgage Guidelines#and work history requirements for Kentucky Mortgage loan approval for FHA#Credit score#FHA#fha $100 down program#fha 2014 fico score requirements#fha appraisals#FHA Approved Condos Louisville Kentucky#FHA Back to Work Program Ky#fha borrowers#FHA Co-signors#fha collections#fha credit score#First-time buyer#Kentucky#louisville#Mortgage#Mortgage loan#Zero down home loans

0 notes

Video

youtube

FHA Guidelines & Building Wealth Through Real Estate | Henry Cossio Real...

#youtube#RealEstateShow HenryCossio OwnItGroup RealEstateInvesting PropertyWealth HomeBuyingTips InvestInRealEstate SmartInvesting FinancialFreedom R

0 notes

Text

The Role of a Mortgage Broker in South Jordan’s Competitive Real Estate Market

South Jordan, Utah, has become one of the most sought-after areas for homebuyers in recent years. With its strong community feel, scenic surroundings, and growing amenities, the demand for housing has skyrocketed. As a result, the local real estate market has become increasingly competitive, with multiple buyers often bidding on the same property. In this high-stakes environment, working with a skilled mortgage broker is more important than ever.

A local mortgage broker in South Jordan plays a critical role in helping buyers navigate the financial aspects of purchasing a home. Unlike a traditional lender who only offers products from one institution, a mortgage broker works with multiple lenders to find the best loan options for their clients. In South Jordan’s fast-paced market, having this level of flexibility and personalized service can make all the difference.

Helping Buyers Get Pre-Approved Quickly

In a competitive market, speed is essential. One of the first things a mortgage broker can do is help buyers get pre-approved for a mortgage. This not only shows sellers that the buyer is serious but also gives the buyer a clear understanding of what they can afford.

“A strong pre-approval letter gives buyers a competitive edge,” says a South Jordan mortgage broker. “Sellers are more likely to accept offers from buyers who are already financially vetted.”

Brokers know which lenders can process pre-approvals quickly and can guide clients through the paperwork efficiently.

Offering Access to a Wide Range of Loan Products

Every buyer’s financial situation is different. Some may have excellent credit and steady income, while others might be self-employed or have unique income sources. A mortgage broker has access to a broad network of lenders and loan products conventional loans, FHA, VA, jumbo loans, and more.

This flexibility is particularly useful in South Jordan, where homes can vary greatly in price and style. Whether a buyer is purchasing a starter home or upgrading to a larger property, a broker can help match them with a loan that fits their needs and budget.

Navigating Changing Market Conditions

Interest rates and lending guidelines are constantly changing. A mortgage broker stays up to date with the latest market conditions and adjusts their recommendations accordingly. In a market like South Jordan’s, where competition is high and timing is everything, this knowledge is incredibly valuable.

“We monitor market changes daily,” says the broker. “If rates drop or if a new loan program becomes available, we immediately let our clients know.”

This level of attention can help buyers lock in better rates or take advantage of special programs that national lenders might overlook.

Providing Personalized Guidance and Support

Buying a home is one of the biggest financial decisions a person can make. For many buyers especially first-timers the process can feel overwhelming. A mortgage broker offers one-on-one support, walking clients through every step of the loan process.

From gathering documents and submitting applications to coordinating with real estate agents and title companies, brokers serve as a central point of contact to keep the process moving smoothly.

“In a fast-moving market, buyers don’t have time to waste,” the broker explains. “We handle the details so they can focus on finding the right home.”

Increasing the Chances of a Successful Closing

In South Jordan’s competitive market, deals can fall through due to financing issues. A mortgage broker’s job is to prevent that from happening. By thoroughly reviewing a buyer’s financial profile and selecting the right lender, brokers help reduce the risk of surprises during underwriting or closing.

They also troubleshoot any issues that arise during the process, working with lenders to resolve problems quickly and keep the deal on track.

The role of a mortgage broker in South Jordan’s competitive real estate market is more important than ever. With their ability to offer personalized service, access to multiple lenders, and expertise in local market conditions, brokers help buyers move faster, make stronger offers, and close with confidence.

For anyone looking to buy a home in South Jordan, partnering with a knowledgeable mortgage broker could be the key to success in today’s fast-paced market.

0 notes

Text

Buying a Manufactured Home: A Guide to Affordable Financing

Many people find rising home prices intimidating, but purchasing a manufactured home can offer a more affordable path to homeownership. If you’re exploring this option, understanding the financing landscape is important to secure the best deal. This guide will help you navigate loan types, credit requirements, and down payment options so you can confidently move forward with your manufactured home purchase.

Unpacking the Variations: Mobile Homes vs. Manufactured Homes

Understanding the distinct differences between mobile and manufactured homes can help you make better-informed buying decisions. Mobile homes, built before June 15, 1976, lack the enhanced safety and construction standards that HUD introduced for manufactured homes built after that date. These differences affect everything from build quality and durability to financing options, insurance requirements, and long-term value. Knowing which category your prospective home falls into enables you to evaluate affordability, safety, and resale potential more accurately.

Key Characteristics and Definitions

Mobile homes are prefabricated structures constructed on a permanent chassis before June 15, 1976. Manufactured homes, while also factory-built and placed on a chassis, were produced after that date and must comply with HUD’s stricter safety and construction standards. Most manufactured homes are designed to remain permanently installed, whereas mobile homes were often built for easier relocation. These definitions set the framework for distinctions in regulations, financing, and even insurance options available to you.

Implications of Regulatory Changes

The 1976 HUD regulations transformed mobile homes into manufactured homes by introducing nationwide construction and safety standards. These rules mandate specific structural requirements, fire safety features, energy efficiency measures, and plumbing and electrical standards. Compliance improves safety and durability, which often makes manufactured homes more attractive to lenders and insurers compared to older mobile homes.

These regulatory updates also influence financing availability. Lenders generally view manufactured homes as less risky investments because they meet HUD’s uniform code. This acceptance often results in better loan terms and more accessible mortgage options, such as FHA-backed or conventional loans through specialized programs. In contrast, mobile homes built before 1976 may face limited financing opportunities and may require chattel loans with higher interest rates or shorter repayment terms. Understanding these regulatory impacts helps you anticipate the kinds of loans or insurance policies you can pursue, as well as the potential resale value differences between mobile and manufactured homes.

Modular Homes: The Unseen Contender

Modular homes offer an alternative path into homeownership that blends factory precision with traditional construction standards. Built in sections at a factory and then assembled on-site, these homes adhere to local building codes rather than federal HUD regulations. This approach often means higher construction quality and greater flexibility in design while typically costing less than conventional homes. If you’re considering affordable housing options, modular homes deserve a closer look for their balance of cost, durability, and long-term value.

Construction Process and Building Codes

Your modular home is constructed in a controlled factory environment, allowing for consistent quality and accelerated build times. Unlike manufactured homes that follow HUD guidelines, modular homes must meet the same local and state building codes as site-built houses. This means inspections occur both during off-site fabrication and after on-site assembly, helping ensure structural integrity and adherence to zoning laws, giving your home the same safety and reliability as traditional builds.

Real Property Status Compared to Mobile Homes

Modular homes are classified as real property, meaning they become permanently attached to the land and are taxed as real estate. In contrast, many manufactured homes are often considered personal property, similar to vehicles, especially when not permanently affixed to land. This distinction affects financing, resale value, and the types of loans available to you, making modular homes easier to finance like conventional houses and potentially more attractive to future buyers.

Key Differences Between Modular and Mobile Homes

Aspect

Modular Homes

Construction Location

Factory-built sections assembled on-site

Building Codes

Local/state codes (same as traditional homes)

Property Status

Considered real property once installed

Mobility

Typically permanent, not designed to move

Key Differences Between Modular and Mobile Homes

Aspect

Mobile Homes

Construction Date

Built before June 15, 1976

Building Codes

HUD standards (pre-1976), fewer safety regulations

Property Status

Often considered personal property, movable

Mobility

Built to be transportable

The real property classification of modular homes impacts financing options significantly. Because they are taxed like site-built homes and permanently affixed to land, lenders are more willing to offer traditional mortgage loans with competitive rates. This contrasts with mobile homes, which can be harder to finance due to their personal property status and potential mobility. You benefit from stronger resale potential and wider loan availability with modular homes, helping you invest confidently even if your budget limits you from purchasing a conventional home.

Navigating the Financing Maze

Financing a manufactured home requires a clear understanding of available loan options and lender requirements. Programs from FHA, VA, Fannie Mae, and Freddie Mac often provide more flexible terms, but eligibility hinges on factors like credit score, down payment, and home specifications. Chattel loans and personal loans serve as alternatives when traditional mortgages aren’t an option, though often at higher costs. Exploring multiple lenders and loan types can help you find the best fit and improve your approval chances in this complex financing landscape.

Understanding Credit Scores and Their Impact

Your credit score significantly affects loan approval and interest rates. Scores between 740 and 799 are deemed very good, while scores 800 and above are exceptional, increasing your chances for favorable mortgage terms. Lower scores might mean higher rates or difficulty qualifying. Pulling free reports from Experian, Equifax, or TransUnion allows you to spot errors and improve your profile by paying bills on time and reducing debt, strengthening your application for a manufactured home loan.

The Importance of Down Payments in Home Purchases

Down payments reduce the amount you borrow and can lower monthly payments and interest rates. A minimum of 5% is often required for manufactured homes. Larger down payments regularly result in better loan terms and can boost lender confidence in your financial readiness, ultimately saving you money over time.

Putting down a substantial down payment, such as 10% or more, can improve loan approvals and lower your interest rate, making monthly payments more manageable. Beyond saving money, a larger down payment reduces your loan-to-value ratio, signaling less risk to lenders and potentially shortening the loan term or enhancing your eligibility for special programs.

Exploring Diverse Financing Options

You have various ways to finance a manufactured home, each with its own requirements and benefits. From conventional loans with government backing to alternative paths like chattel and personal loans, understanding these options helps you identify which fits your financial situation best. Exploring different lenders and programs can open doors to competitive rates and terms, potentially lowering your upfront costs and monthly payments as you step into homeownership on a budget.

Traditional Mortgages vs. Government-Backed Loans

Traditional mortgages for manufactured homes often come through Fannie Mae or Freddie Mac programs like MH Advantage or CHOICEHome, which typically require your home to meet specific property standards and location rules. Government-backed loans from the FHA and VA can offer lower down payments or even no down payment, with more flexible credit requirements, making them a viable choice if your credit isn’t perfect or you’re buying both the home and the land.

Alternative Financing: From Chattel Loans to Personal Loans

Chattel loans target movable manufactured homes not attached to land, often featuring shorter repayment terms and higher interest rates, but easier qualification. Personal loans can finance lower-cost homes or cover part of the cost, but usually come with higher rates and smaller loan amounts, requiring careful budgeting to avoid stretching your finances too thin.

Chattel loans are designed specifically for buyers purchasing homes without land ownership, making them common for manufactured homes on leased lots. While approval criteria tend to be more lenient than traditional mortgages, expect higher interest rates, shorter terms than typical 30-year mortgages. Personal loans might provide quick cash and flexible use but often carry rates upwards of 10% to 15% and loan limits around $50,000 to $100,000, which might not cover your full home cost. Carefully comparing these options alongside your credit profile and payment ability helps ensure you choose the most affordable and sustainable financing method.

Common Hurdles and Smart Strategies

Getting financing for a manufactured home often brings unique challenges like higher interest rates and limited lender options. You may also face restrictions on home size or location that impact your choices. Staying proactive by improving your credit score, comparing multiple lenders, and exploring specialized government loan programs can make a significant difference. Understanding the nuances between loan types helps you identify the best fit for your financial situation. After careful preparation, you’ll increase your chances of securing affordable financing without unexpected delays or obstacles.

Overcoming Myths: Down Payments and Home Types

Many assume down payments for manufactured homes must be large, but FHA loans may require as little as 3.5%, and VA loans can require none at all. Single-wide or smaller homes can sometimes disqualify you from certain lenders, but seeking multiple quotes expands your options. Loans like chattel or personal loans often have more flexible down payment requirements. After reviewing your loan options thoroughly, you can debunk these myths and find financing tailored to your specific home type.

Hurdle

Smart Strategy

Limited traditional lenders

Tap into FHA, VA, Fannie Mae, and Freddie Mac programs

Higher interest rates on chattel loans

Improve your credit score to qualify for better terms

Down payment concerns

Explore loans with low or no down payment options

Size restrictions on single-wide homes

Shop around for lenders with flexible minimum size requirements

Insurance requirements

Obtain homeowners' insurance to meet lender conditions

Essential Insurance and Maintenance Considerations

Once your home is financed, securing homeowners insurance that covers manufactured dwellings protects your investment and may be required by lenders. Maintenance needs differ from traditional homes—foundation stability, roof upkeep, and weatherproofing are key to preserving value. Locating nearby service providers experienced with manufactured homes ensures timely repairs and inspections. After establishing insurance and routine care, your home remains safe, comfortable, and marketable for years to come.

Is a Manufactured Home Right for You?

The path to owning a manufactured home is within your reach, especially with the variety of financing options available to fit your situation. By understanding the differences between home types, checking your credit, saving for a down payment, and shopping for the right lender, you can improve your chances of securing a loan that works for you. Whether you explore FHA, VA, conventional, or chattel loans, you have opportunities to break into the housing market affordably. Taking these steps equips you to make informed decisions and move closer to owning your own home.

#Manufactured Home Financing#Manufactured Home Loans#Affordable Homeownership#No Down Payment Manufactured Home#FHA Manufactured Home Loan#Mobile Home vs Manufactured Home#Modular Home vs Manufactured Home#HUD Manufactured Homes#Chattel Loans#Manufactured Home Credit Score

0 notes

Text

Suntel Global - Residential Appraisal QC Review Services Suntel Global is proud to offer a comprehensive suite of Residential Appraisal QC Review services tailored to meet the evolving needs of lenders, AMCs and real estate professionals. Our quality control process ensures accuracy, compliance and consistency across all appraisal types. Our services include: Drive-By Appraisals Efficient exterior-only property evaluations for lending or investment purposes. Desktop Appraisals Cost-effective property assessments conducted remotely using reliable data sources and digital tools. Full Residential Appraisals Complete on-site inspections offering detailed and accurate property valuation. FHA Appraisals Appraisals conducted in full compliance with HUD guidelines to support FHA-backed loan approvals. Conventional Appraisals Standard property evaluations used in traditional mortgage financing. Non-Conforming Property Appraisals Specialized reviews for properties that do not meet standard lending criteria or have unique characteristics. Broker Price Opinions (BPOs) Reliable property value estimates prepared by licensed real estate professionals for investment or disposition strategies. Our trained reviewers apply industry best practices, regulatory compliance standards and attention to detail to ensure every report meets both internal quality benchmarks and external regulatory requirements. Partner with Suntel Global for precise, dependable and timely appraisal QC reviews. For more details, please email us at: [email protected]

#hashtag#SuntelGlobal hashtag#suntelglobal hashtag#appraisalqcreviewservices hashtag#appraisalqcreview hashtag#appraisalqc hashtag#MortgageLending hashtag#AppraisalQC hashtag#mortgageprocessing hashtag#Outsourcing hashtag#fullserviceappraisals hashtag#residentialappraisalexperts hashtag#allytypesofappraisals hashtag#trustedappraisalsolutions hashtag#fullresidentialappraisals hashtag#desktopappraisals hashtag#drivebyappraisals hashtag#fhaappraisals hashtag#conventionalappraisals hashtag#nonconformingpropertyappraisals hashtag#marketanalysisreport hashtag#QualityControlReview hashtag#ResidentialAppraisal hashtag#ComplianceMatters hashtag#RealEstateSupport hashtag#LendingSolutions hashtag#LendingExcellence hashtag#RiskManagement hashtag#TrustTheProcess hashtag#MortgageIndustry hashtag

0 notes