#HPC applications

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

69% of Tumblr users are millennials.

Text

The Evolution and Impact of Supercomputers and Servers in the Modern World

Introduction Supercomputers represent the pinnacle of computational power, evolving from massive, room-sized machines to sleek, compact devices with immense processing capabilities. These advancements have drastically transformed scientific research, industry, and even daily life. In parallel, server technology has undergone a rapid evolution, supporting the backbone of global networks and data…

#artificial intelligence#cloud computing#compact supercomputers#Cray supercomputers#Cray-1#Cryptography#exascale computing#Fugaku supercomputer#future of computing#Google Sycamore#high-performance computing#history of supercomputers#HPC applications#IBM 7030 Stretch#machine learning#massively parallel processing#NVIDIA DGX Station#parallel processing#personalized medicine#Q-bit theory#Q-bits#quantum algorithms#Quantum Computing#quantum servers#quantum supremacy#scientific simulations#server technology#Seymour Cray#supercomputing#technological advancements

0 notes

Text

#HighPoint#NVMe#AICs#GPUs#ideal for high-demand applications in#HPC#TechInnovation#powerelectronics#powermanagement#powersemiconductor

0 notes

Text

Future Applications of Cloud Computing: Transforming Businesses & Technology

Cloud computing is revolutionizing industries by offering scalable, cost-effective, and highly efficient solutions. From AI-driven automation to real-time data processing, the future applications of cloud computing are expanding rapidly across various sectors.

Key Future Applications of Cloud Computing

1. AI & Machine Learning Integration

Cloud platforms are increasingly being used to train and deploy AI models, enabling businesses to harness data-driven insights. The future applications of cloud computing will further enhance AI's capabilities by offering more computational power and storage.

2. Edge Computing & IoT

With IoT devices generating massive amounts of data, cloud computing ensures seamless processing and storage. The rise of edge computing, a subset of the future applications of cloud computing, will minimize latency and improve performance.

3. Blockchain & Cloud Security

Cloud-based blockchain solutions will offer enhanced security, transparency, and decentralized data management. As cybersecurity threats evolve, the future applications of cloud computing will focus on advanced encryption and compliance measures.

4. Cloud Gaming & Virtual Reality

With high-speed internet and powerful cloud servers, cloud gaming and VR applications will grow exponentially. The future applications of cloud computing in entertainment and education will provide immersive experiences with minimal hardware requirements.

Conclusion

The future applications of cloud computing are poised to redefine business operations, healthcare, finance, and more. As cloud technologies evolve, organizations that leverage these innovations will gain a competitive edge in the digital economy.

🔗 Learn more about cloud solutions at Fusion Dynamics! 🚀

#Keywords#services on cloud computing#edge network services#available cloud computing services#cloud computing based services#cooling solutions#cloud backups for business#platform as a service in cloud computing#platform as a service vendors#hpc cluster management software#edge computing services#ai services providers#data centers cooling systems#https://fusiondynamics.io/cooling/#server cooling system#hpc clustering#edge computing solutions#data center cabling solutions#cloud backups for small business#future applications of cloud computing

0 notes

Text

800G OSFP - Optical Transceivers -Fibrecross

800G OSFP and QSFP-DD transceiver modules are high-speed optical solutions designed to meet the growing demand for bandwidth in modern networks, particularly in AI data centers, enterprise networks, and service provider environments. These modules support data rates of 800 gigabits per second (Gbps), making them ideal for applications requiring high performance, high density, and low latency, such as cloud computing, high-performance computing (HPC), and large-scale data transmission.

Key Features

OSFP (Octal Small Form-Factor Pluggable):

Features 8 electrical lanes, each capable of 100 Gbps using PAM4 modulation, achieving a total of 800 Gbps.

Larger form factor compared to QSFP-DD, allowing better heat dissipation (up to 15W thermal capacity) and support for future scalability (e.g., 1.6T).

Commonly used in data centers and HPC due to its robust thermal design and higher power handling.

QSFP-DD (Quad Small Form-Factor Pluggable Double Density):

Also uses 8 lanes at 100 Gbps each for 800 Gbps total throughput.

Smaller and more compact than OSFP, with a thermal capacity of 7-12W, making it more energy-efficient.

Backward compatible with earlier QSFP modules (e.g., QSFP28, QSFP56), enabling seamless upgrades in existing infrastructure.

Applications

Both form factors are tailored for:

AI Data Centers: Handle massive data flows for machine learning and AI workloads.

Enterprise Networks: Support high-speed connectivity for business-critical applications.

Service Provider Networks: Enable scalable, high-bandwidth solutions for telecom and cloud services.

Differences

Size and Thermal Management: OSFP’s larger size supports better cooling, ideal for high-power scenarios, while QSFP-DD’s compact design suits high-density deployments.

Compatibility: QSFP-DD offers backward compatibility, reducing upgrade costs, whereas OSFP often requires new hardware.

Use Cases: QSFP-DD is widely adopted in Ethernet-focused environments, while OSFP excels in broader applications, including InfiniBand and HPC.

Availability

Companies like Fibrecross,FS.com, and Cisco offer a range of 800G OSFP and QSFP-DD modules, supporting various transmission distances (e.g., 100m for SR8, 2km for FR4, 10km for LR4) over multimode or single-mode fiber. These modules are hot-swappable, high-performance, and often come with features like low latency and high bandwidth density.

For specific needs—such as short-range (SR) or long-range (LR) transmission—choosing between OSFP and QSFP-DD depends on your infrastructure, power requirements, and future scalability plans. Would you like more details on a particular module type or application?

2 notes

·

View notes

Text

What Future Trends in Software Engineering Can Be Shaped by C++

The direction of innovation and advancement in the broad field of software engineering is greatly impacted by programming languages. C++ is a well-known programming language that is very efficient, versatile, and has excellent performance. In terms of the future, C++ will have a significant influence on software engineering, setting trends and encouraging innovation in a variety of fields.

In this blog, we'll look at three key areas where the shift to a dynamic future could be led by C++ developers.

1. High-Performance Computing (HPC) & Parallel Processing

Driving Scalability with Multithreading

Within high-performance computing (HPC), where managing large datasets and executing intricate algorithms in real time are critical tasks, C++ is still an essential tool. The fact that C++ supports multithreading and parallelism is becoming more and more important as parallel processing-oriented designs, like multicore CPUs and GPUs, become more commonplace.

Multithreading with C++

At the core of C++ lies robust support for multithreading, empowering developers to harness the full potential of modern hardware architectures. C++ developers adept in crafting multithreaded applications can architect scalable systems capable of efficiently tackling computationally intensive tasks.

C++ Empowering HPC Solutions

Developers may redefine efficiency and performance benchmarks in a variety of disciplines, from AI inference to financial modeling, by forging HPC solutions with C++ as their toolkit. Through the exploitation of C++'s low-level control and optimization tools, engineers are able to optimize hardware consumption and algorithmic efficiency while pushing the limits of processing capacity.

2. Embedded Systems & IoT

Real-Time Responsiveness Enabled

An ability to evaluate data and perform operations with low latency is required due to the widespread use of embedded systems, particularly in the quickly developing Internet of Things (IoT). With its special combination of system-level control, portability, and performance, C++ becomes the language of choice.

C++ for Embedded Development

C++ is well known for its near-to-hardware capabilities and effective memory management, which enable developers to create firmware and software that meet the demanding requirements of environments with limited resources and real-time responsiveness. C++ guarantees efficiency and dependability at all levels, whether powering autonomous cars or smart devices.

Securing IoT with C++

In the intricate web of IoT ecosystems, security is paramount. C++ emerges as a robust option, boasting strong type checking and emphasis on memory protection. By leveraging C++'s features, developers can fortify IoT devices against potential vulnerabilities, ensuring the integrity and safety of connected systems.

3. Gaming & VR Development

Pushing Immersive Experience Boundaries

In the dynamic domains of game development and virtual reality (VR), where performance and realism reign supreme, C++ remains the cornerstone. With its unparalleled speed and efficiency, C++ empowers developers to craft immersive worlds and captivating experiences that redefine the boundaries of reality.

Redefining VR Realities with C++

When it comes to virtual reality, where user immersion is crucial, C++ is essential for producing smooth experiences that take users to other worlds. The effectiveness of C++ is crucial for preserving high frame rates and preventing motion sickness, guaranteeing users a fluid and engaging VR experience across a range of applications.

C++ in Gaming Engines

C++ is used by top game engines like Unreal Engine and Unity because of its speed and versatility, which lets programmers build visually amazing graphics and seamless gameplay. Game developers can achieve previously unattainable levels of inventiveness and produce gaming experiences that are unmatched by utilizing C++'s capabilities.

Conclusion

In conclusion, there is no denying C++'s ongoing significance as we go forward in the field of software engineering. C++ is the trend-setter and innovator in a variety of fields, including embedded devices, game development, and high-performance computing. C++ engineers emerge as the vanguards of technological growth, creating a world where possibilities are endless and invention has no boundaries because of its unmatched combination of performance, versatility, and control.

FAQs about Future Trends in Software Engineering Shaped by C++

How does C++ contribute to future trends in software engineering?

C++ remains foundational in software development, influencing trends like high-performance computing, game development, and system programming due to its efficiency and versatility.

Is C++ still relevant in modern software engineering practices?

Absolutely! C++ continues to be a cornerstone language, powering critical systems, frameworks, and applications across various industries, ensuring robustness and performance.

What advancements can we expect in C++ to shape future software engineering trends?

Future C++ developments may focus on enhancing parallel computing capabilities, improving interoperability with other languages, and optimizing for emerging hardware architectures, paving the way for cutting-edge software innovations.

10 notes

·

View notes

Text

Intel Introduces New AI Solutions with Xeon 6 and Gaudi 3

Intel has launched its latest AI solutions featuring the Xeon 6 processors and Gaudi 3 AI accelerators. These advancements promise improved performance and efficiency for AI tasks. With the new Xeon 6, you get better AI and HPC workloads, while Gaudi 3 offers enhanced throughput and cost-effectiveness. Perfect for powering the next generation of AI applications! 🚀

#IntelAI #Innovation #TechNews

Read More Here

2 notes

·

View notes

Text

Amazon DCV 2024.0 Supports Ubuntu 24.04 LTS With Security

NICE DCV is a different entity now. Along with improvements and bug fixes, NICE DCV is now known as Amazon DCV with the 2024.0 release.

The DCV protocol that powers Amazon Web Services(AWS) managed services like Amazon AppStream 2.0 and Amazon WorkSpaces is now regularly referred to by its new moniker.

What’s new with version 2024.0?

A number of improvements and updates are included in Amazon DCV 2024.0 for better usability, security, and performance. The most recent Ubuntu 24.04 LTS is now supported by the 2024.0 release, which also offers extended long-term support to ease system maintenance and the most recent security patches. Wayland support is incorporated into the DCV client on Ubuntu 24.04, which improves application isolation and graphical rendering efficiency. Furthermore, DCV 2024.0 now activates the QUIC UDP protocol by default, providing clients with optimal streaming performance. Additionally, when a remote user connects, the update adds the option to wipe the Linux host screen, blocking local access and interaction with the distant session.

What is Amazon DCV?

Customers may securely provide remote desktops and application streaming from any cloud or data center to any device, over a variety of network conditions, with Amazon DCV, a high-performance remote display protocol. Customers can run graphic-intensive programs remotely on EC2 instances and stream their user interface to less complex client PCs, doing away with the requirement for pricey dedicated workstations, thanks to Amazon DCV and Amazon EC2. Customers use Amazon DCV for their remote visualization needs across a wide spectrum of HPC workloads. Moreover, well-known services like Amazon Appstream 2.0, AWS Nimble Studio, and AWS RoboMaker use the Amazon DCV streaming protocol.

Advantages

Elevated Efficiency

You don’t have to pick between responsiveness and visual quality when using Amazon DCV. With no loss of image accuracy, it can respond to your apps almost instantly thanks to the bandwidth-adaptive streaming protocol.

Reduced Costs

Customers may run graphics-intensive apps remotely and avoid spending a lot of money on dedicated workstations or moving big volumes of data from the cloud to client PCs thanks to a very responsive streaming experience. It also allows several sessions to share a single GPU on Linux servers, which further reduces server infrastructure expenses for clients.

Adaptable Implementations

Service providers have access to a reliable and adaptable protocol for streaming apps that supports both on-premises and cloud usage thanks to browser-based access and cross-OS interoperability.

Entire Security

To protect customer data privacy, it sends pixels rather than geometry. To further guarantee the security of client data, it uses TLS protocol to secure end-user inputs as well as pixels.

Features

In addition to native clients for Windows, Linux, and MacOS and an HTML5 client for web browser access, it supports remote environments running both Windows and Linux. Multiple displays, 4K resolution, USB devices, multi-channel audio, smart cards, stylus/touch capabilities, and file redirection are all supported by native clients.

The lifecycle of it session may be easily created and managed programmatically across a fleet of servers with the help of DCV Session Manager. Developers can create personalized Amazon DCV web browser client applications with the help of the Amazon DCV web client SDK.

How to Install DCV on Amazon EC2?

Implement:

Sign up for an AWS account and activate it.

Open the AWS Management Console and log in.

Either download and install the relevant Amazon DCV server on your EC2 instance, or choose the proper Amazon DCV AMI from the Amazon Web Services Marketplace, then create an AMI using your application stack.

After confirming that traffic on port 8443 is permitted by your security group’s inbound rules, deploy EC2 instances with the Amazon DCV server installed.

Link:

On your device, download and install the relevant Amazon DCV native client.

Use the web client or native Amazon DCV client to connect to your distant computer at https://:8443.

Stream:

Use AmazonDCV to stream your graphics apps across several devices.

Use cases

Visualization of 3D Graphics

HPC workloads are becoming more complicated and consuming enormous volumes of data in a variety of industrial verticals, including Oil & Gas, Life Sciences, and Design & Engineering. The streaming protocol offered by Amazon DCV makes it unnecessary to send output files to client devices and offers a seamless, bandwidth-efficient remote streaming experience for HPC 3D graphics.

Application Access via a Browser

The Web Client for Amazon DCV is compatible with all HTML5 browsers and offers a mobile device-portable streaming experience. By removing the need to manage native clients without sacrificing streaming speed, the Web Client significantly lessens the operational pressure on IT departments. With the Amazon DCV Web Client SDK, you can create your own DCV Web Client.

Personalized Remote Apps

The simplicity with which it offers streaming protocol integration might be advantageous for custom remote applications and managed services. With native clients that support up to 4 monitors at 4K resolution each, Amazon DCV uses end-to-end AES-256 encryption to safeguard both pixels and end-user inputs.

Amazon DCV Pricing

Amazon Entire Cloud:

Using Amazon DCV on AWS does not incur any additional fees. Clients only have to pay for the EC2 resources they really utilize.

On-site and third-party cloud computing

Please get in touch with DCV distributors or resellers in your area here for more information about licensing and pricing for Amazon DCV.

Read more on Govindhtech.com

#AmazonDCV#Ubuntu24.04LTS#Ubuntu#DCV#AmazonWebServices#AmazonAppStream#EC2instances#AmazonEC2#News#TechNews#TechnologyNews#Technologytrends#technology#govindhtech

2 notes

·

View notes

Text

Flip Chip Substrate Market : Global Trends and Forecast (2025 - 2032)

Global Flip Chip Substrate Market size was valued at US$ 8,730 million in 2024 and is projected to reach US$ 15,670 million by 2032, at a CAGR of 8.7% during the forecast period 2025-2032.

Flip chip substrates are critical components in semiconductor packaging, acting as miniature printed circuit boards (PCBs) that facilitate electrical connections between integrated circuits (ICs) and external circuitry. Unlike conventional PCBs, these substrates are designed to accommodate flip chip bonding, where ICs are mounted upside-down and connected directly to the substrate using solder bumps. Key materials used include ceramic, silicon, and organic substrates, each offering distinct advantages in thermal management and signal integrity.

Growth in the market is driven by rising demand for advanced semiconductor packaging solutions, particularly in high-performance computing (HPC), artificial intelligence (AI), and 5G applications. However, supply chain disruptions and fluctuating raw material costs pose challenges. Leading companies like Samsung Electronics, ASE Group, and Ibiden are investing in substrate technology to address the demand for finer pitch designs and improved thermal performance.

Get Full Report : https://semiconductorinsight.com/report/flip-chip-substrate-market/

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for High-Performance Computing Accelerates Flip Chip Adoption

The surging adoption of flip chip substrates is directly tied to explosive growth in high-performance computing applications from data centers to artificial intelligence. As computing architectures require higher bandwidth and lower latency, flip chip packaging provides superior electrical performance compared to wire bonding – achieving up to 40% reduction in signal delay while enabling higher pin counts. Leading semiconductor firms increasingly favor flip chip designs for advanced CPUs, GPUs, and AI accelerators where thermal management and interconnect density are critical. The market for AI chips alone is projected to expand at 35% CAGR through 2030, creating sustained demand for high-density flip chip substrates capable of supporting next-generation silicon.

5G Infrastructure Rollout Driving Advanced Packaging Requirements

Global 5G network deployments are creating ripple effects across semiconductor packaging, with flip chip substrates becoming essential for RF front-end modules and base station processors. These applications require packaging that minimizes parasitic effects while handling high-frequency signals – precisely where flip chip technology excels. As telecom operators invest over $250 billion annually in 5G infrastructure, substrate manufacturers are seeing unprecedented demand for low-loss dielectric materials and precision bumping technologies. The transition to mmWave frequencies in particular favors flip chip’s superior electrical characteristics, making it the packaging method of choice for next-generation wireless components.

➤ For instance, recent designs for 64T64R massive MIMO antennas now incorporate flip chip substrates exclusively to meet stringent RF performance requirements while minimizing footprint.

Furthermore, the automotive sector’s push toward autonomous driving systems represents another major growth vector. Advanced driver assistance systems (ADAS) relying on high-performance vision processors and radar modules increasingly adopt flip chip packaging to meet automotive-grade reliability standards while handling complex sensor fusion workloads.

MARKET RESTRAINTS

Complex Manufacturing Processes Constrain Market Expansion

While flip chip technology offers performance advantages, its manufacturing complexity presents significant barriers to adoption. The substrate fabrication process involves over 30 distinct production steps, from ultra-fine line patterning to precision bump placement, requiring specialized equipment with tight process controls. This complexity directly impacts yields and production costs, with defect rates in advanced substrates potentially reaching 15-20% for new process nodes. Many mid-tier semiconductor firms find the capital expenditure requirements prohibitive – a single bumping line can exceed $50 million in equipment investments.

Other Critical Challenges

Thermal Management Limitations Heat dissipation becomes increasingly problematic as flip chip densities rise. While solder bumps provide electrical connections, they create thermal resistance that can reduce chip reliability. Current substrate designs struggle to handle power densities exceeding 100W/cm² – a threshold being approached by next-generation AI accelerators and high-performance processors.

Material Compatibility Issues The coefficient of thermal expansion (CTE) mismatch between silicon dies and organic substrates remains an ongoing engineering challenge. Without perfect CTE matching, temperature cycling induces mechanical stress that can lead to solder joint failures and reduced product lifespan, particularly in automotive and industrial applications.

MARKET OPPORTUNITIES

Emerging 3D IC Technologies Create New Substrate Demand

The semiconductor industry’s shift toward 3D integration presents transformative opportunities for flip chip substrate providers. Advanced packaging architectures like chip-on-wafer-on-substrate (CoWoS) and integrated fan-out (InFO) require sophisticated interposers and redistribution layers that leverage flip chip technologies. As foundries invest heavily in 3D IC capabilities – with one leading player committing $30+ billion to advanced packaging R&D – substrate manufacturers able to deliver fine-pitch interconnects below 10μm stand to capture substantial market share.

Material Innovations Open New Application Verticals

Breakthroughs in substrate materials are expanding flip chip applications into previously inaccessible markets. Novel glass-based substrates demonstrate 50% lower signal loss compared to traditional organic materials while offering superior dimensional stability. These characteristics make them ideal for millimeter-wave automotive radar and high-frequency communications equipment. Similarly, developments in embedded passive components allow substrate manufacturers to integrate capacitors and inductors directly into the package, reducing board space requirements and improving electrical performance for IoT and mobile devices.

MARKET CHALLENGES

Geopolitical Factors Disrupt Supply Chain Stability

The flip chip substrate market faces growing uncertainty from trade restrictions and export controls affecting critical materials. Specialty resins and copper-clad laminates originating from specific regions now face 15-20% tariff premiums, increasing manufacturing costs across the supply chain. Furthermore, restrictions on advanced packaging equipment exports threaten to create technological bottlenecks, potentially delaying next-generation substrate development for non-approved regions.

Other Pressing Concerns

Workforce Development Lagging The industry faces an acute shortage of process engineers skilled in advanced substrate manufacturing techniques. With less than 30 accredited programs worldwide focused on semiconductor packaging, companies struggle to staff new production lines, slowing capacity expansion efforts despite strong demand.

Environmental Compliance Costs Stricter regulations on hazardous materials used in substrate fabrication, particularly concerning lead-free solder alternatives and solvent recovery, are adding 5-7% to production costs. These requirements vary significantly by region, complicating global manufacturing strategies for substrate suppliers.

FLIP CHIP SUBSTRATE MARKET TRENDS

Growing Demand for High-Performance Computing to Drive Market Expansion

The global flip chip substrate market is witnessing robust growth due to increasing demand for high-performance computing (HPC) applications in artificial intelligence, cloud computing, and data centers. Flip chip technology provides superior electrical performance compared to traditional wire bonding, offering higher signal density and better thermal dissipation. With semiconductor packaging evolving toward smaller form factors and higher power efficiency, flip chip substrates have become critical for advanced integrated circuits (ICs), CPUs, and GPUs. The market is projected to grow at a CAGR of over 6% from 2024 to 2032, driven by the semiconductor industry’s shift toward miniaturization and improved performance.

Other Trends

Advancements in Packaging Technologies

The growing adoption of fan-out wafer-level packaging (FOWLP) and 2.5D/3D IC packaging is influencing the flip chip substrate market, as these technologies require high-density interconnects for improved performance. Manufacturers are focusing on developing substrates with finer pitch capabilities and enhanced thermal management to meet the demands of advanced semiconductor nodes. Additionally, the rise of heterogeneous integration in chiplet-based designs is accelerating demand for flip chip substrates that can support multiple dies in a single package.

Increasing Investments in Electric Vehicles and 5G Infrastructure

The automotive and telecommunications sectors are emerging as key growth drivers for flip chip substrates, particularly with the rapid expansion of electric vehicles (EVs) and 5G networks. Flip chip technology is extensively used in power electronics for EV battery management systems (BMS) and ADAS applications, where thermal performance and reliability are critical. Meanwhile, 5G infrastructure development has heightened demand for high-frequency flip chip substrates in RF components, as they enable better signal integrity and power efficiency compared to conventional wire-bonded packages.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Expansions Drive Market Competition

The global flip chip substrate market exhibits a semi-consolidated competitive structure, with established semiconductor manufacturers and substrate specialists vying for market share. Samsung Electronics and ASE Group emerge as dominant players, leveraging their vertical integration capabilities and extensive manufacturing footprints across Asia and North America. Samsung’s leadership stems from its advanced packaging solutions for memory and logic devices, while ASE maintains strength through its comprehensive flip chip packaging services.

Japanese firms Ibiden and SHINKO command significant market positions due to their expertise in high-density interconnect (HDI) substrates and ceramic-based solutions. These companies benefit from strong relationships with automotive and high-performance computing clients, with Ibiden securing numerous design wins for advanced chiplet packaging applications.

Several players are actively expanding production capacity to meet growing demand. Unimicron recently announced a $1.2 billion investment to expand its substrate manufacturing facilities in Taiwan, while Kinsus Interconnect Technology is increasing its focus on advanced substrate technologies for artificial intelligence processors. Meanwhile, European supplier AT&S is strengthening its position through strategic technology partnerships and new manufacturing sites in Southeast Asia.

The competitive intensity is further heightened by Chinese players like Zhen Ding Technology and Shennan Circuit, who are rapidly catching up technologically while competing aggressively on price. These companies benefit from government subsidies and growing domestic demand, posing both challenges and opportunities for established market leaders.

List of Key Flip Chip Substrate Companies Profiled

Samsung Electronics (South Korea)

ASE Group (Taiwan)

Ibiden (Japan)

SHINKO (Japan)

Unimicron (Taiwan)

Kinsus Interconnect Technology (Taiwan)

AT&S (Austria)

Kyocera (Japan)

Nan Ya PCB (Taiwan)

Zhen Ding Technology (China)

Shennan Circuit (China)

KLA (U.S.)

LG InnoTek (South Korea)

Daeduck Electronics (South Korea)

Segment Analysis:

By Type

Ceramic Substrate Dominates the Market Due to Superior Thermal Conductivity and Reliability

The market is segmented based on type into:

Ceramic Substrate

Subtypes: Alumina, Aluminum Nitride, and others

Silicon Substrate

Subtypes: Silicon Interposer, Silicon Wafer, and others

Others

By Application

Integrated Circuit Segment Leads Due to High Demand for Compact Electronics and Advanced Packaging

The market is segmented based on application into:

Integrated Circuit

CPU

Graphics Processing Unit

Others

By End-User Industry

Consumer Electronics Drives Market Growth with Increasing Adoption of Smart Devices

The market is segmented based on end-user industry into:

Consumer Electronics

Automotive

Telecommunications

Industrial

Aerospace & Defense

Healthcare

By Technology

Thermal Compression Bonding Technology Gains Traction for High-Density Packaging

The market is segmented based on technology into:

Mass Reflow

Thermal Compression Bonding

Others

Regional Analysis: Flip Chip Substrate Market

North America The North American flip chip substrate market is driven predominantly by the semiconductor industry’s strong presence and technological advancements in the U.S. and Canada. The region benefits from robust R&D investments, particularly in high-performance computing (HPC) and artificial intelligence (AI) applications, which demand advanced flip chip substrates. Major semiconductor players and packaging firms, such as Intel and ASE Group subsidiaries, are expanding their substrate manufacturing capabilities to accommodate next-generation designs. Additionally, government-backed initiatives, including the CHIPS and Science Act, which allocates $52 billion for semiconductor research and production, further propel market growth. However, the shift toward advanced substrates like silicon interposers presents challenges in terms of rising production costs.

Europe Europe emphasizes sustainable semiconductor manufacturing and technological innovation, which shapes the flip chip substrate market. Countries such as Germany, France, and the Netherlands are investing heavily in automotive and industrial IoT applications, where flip chip substrates provide superior thermal and electrical performance. The European semiconductor ecosystem, supported by companies including Infineon and STMicroelectronics, contributes to steady demand. However, reliance on Asian substrate suppliers and supply chain disruptions due to geopolitical tensions limit rapid expansion. Compliance with stringent EU environmental regulations further influences substrate material choices, with a shift toward lead-free and halogen-free alternatives gaining traction.

Asia-Pacific As the dominant region in the flip chip substrate market, Asia-Pacific accounts for over 60% of global production and consumption, led by semiconductor powerhouses China, Japan, South Korea, and Taiwan. Taiwan, home to major players like Unimicron and Nan Ya PCB, remains a hub for high-density flip chip substrate manufacturing. China’s aggressive push toward semiconductor self-sufficiency, backed by government subsidies, is increasing domestic substrate production. Japan and South Korea specialize in high-end substrates for memory and logic applications, catering to industry giants such as Samsung Electronics and SK Hynix. Despite cost-sensitive demand in emerging Southeast Asian markets, advancements in packaging technologies sustain steady adoption.

South America The flip chip substrate market in South America is nascent but growing, predominantly fueled by Brazil’s automotive and consumer electronics sectors. However, limited semiconductor fabrication capabilities and reliance on imports hinder market expansion. Economic instability in key countries like Argentina further restricts large-scale investments in advanced packaging solutions. Nonetheless, increasing demand for IoT devices and telecommunications infrastructure presents long-term opportunities for incremental growth.

Middle East & Africa This region exhibits emerging demand for flip chip substrates, primarily driven by telecommunications and data center expansions in the UAE, Saudi Arabia, and South Africa. While the lack of indigenous semiconductor manufacturing limits immediate adoption, partnerships with global substrate suppliers are gradually improving accessibility. Government-led tech diversification initiatives, such as Saudi Arabia’s Vision 2030, could accelerate regional growth, though geopolitical and logistical challenges remain obstacles.

Get A Detailed Sample Report : https://semiconductorinsight.com/download-sample-report/?product_id=97593

Report Scope

This market research report provides a comprehensive analysis of the Global Flip Chip Substrate Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Flip Chip Substrate market was valued at USD million in 2024 and is projected to reach USD million by 2032.

Segmentation Analysis: Detailed breakdown by product type (Ceramic Substrate, Silicon Substrate, Others), application (Integrated Circuit, CPU, Graphics Processing Unit, Others), and end-user industry to identify high-growth segments and investment opportunities.

Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific remains the dominant market due to semiconductor manufacturing concentration.

Competitive Landscape: Profiles of leading market participants including Samsung Electronics, ASE Group, SHINKO, Ibiden, and Unimicron, including their product offerings, R&D focus, and recent developments such as mergers and acquisitions.

Technology Trends & Innovation: Assessment of emerging technologies in semiconductor packaging, advanced substrate materials, and evolving industry standards like heterogeneous integration.

Market Drivers & Restraints: Evaluation of factors driving market growth including demand for high-performance computing and advanced packaging, along with challenges like supply chain constraints and material shortages.

Stakeholder Analysis: Insights for semiconductor manufacturers, substrate suppliers, foundries, OSATs, and investors regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

Related Reports :

https://semiconductorinsight.com/report/global-gesture-sensor-market/

https://semiconductorinsight.com/report/iris-recognition-access-control-system-market/

Contact us:

+91 8087992013

0 notes

Text

What Is an S3-Compatible Cloud Storage Solution and Why Is It Important for AI?

In today's data-driven world, AI applications rely heavily on seamless access to vast datasets, ranging from image classification and NLP to generative models and real-time inference. With rising demand for cost-effective and scalable storage, S3-compatible cloud storage solutions have become a fundamental building block of modern AI infrastructure.

What Is S3-Compatible Cloud Storage? S3-compatible cloud storage refers to any storage that runs on the same API (Application Programming Interface) as Amazon's Simple Storage Service (S3). This allows users to import or merge data between various cloud environments without needing to rewrite their applications.

The key characteristics of S3-compatible storage are:

Object storage (ideal for unstructured data like images, videos, logs, etc.)

Scalability from gigabytes to petabytes

S3 API support, tools, and integrations

Cost flexibility compared to block or file storage

Why AI Needs S3-Compatible Cloud Data StorageAI workloads are getting more complex, often demanding the ingestion and processing of terabytes—or even petabytes—of data. Whether you're training a deep learning model or running inference workloads at scale, your platform must read and write data with low latency and high dependability.

Here's why S3-compatible cloud data storage matters to powering AI:

Scalability for Growing Datasets AI models get better with more data. An S3-compatible storage solution allows you to store virtually unlimited amounts of unstructured data—text, video, audio, image, and sensor data—without performance bottlenecks or costly upgrades.

Easy Integration with AI Frameworks Most AI and ML tools—TensorFlow, PyTorch, Apache Spark, Kubeflow—are already S3-compatible API-aware. This allows your team to keep using familiar tools but reap the benefits of a cloud-native storage backend. No need to re-architect workflows or re-configure pipelines.

Cost-Efficiency and Flexibility Compared to on-premises hardware or proprietary cloud storage, S3-compatible cloud storage offerings are cost-effective. You only pay for what you use and are not locked into a single cloud provider. This flexibility is particularly advantageous for AI start-ups and research organizations with tight budgets but large amounts of data.

Performance at Scale Training AIs often requires concurrent access to thousands of objects or files. S3-compliant storage systems—especially those built atop low-latency, redundant infrastructure like that offered by Sharon AI—can supply data access that is high-throughput and low-latency. That means faster model training, rapid iterations, and rapid time to production.

Hybrid and Multi-Cloud ReadyWith S3-compatible cloud storage, businesses are not locked in by vendors and can build hybrid or multi-cloud AI environments. It is ideal for businesses that must combine on-premise compute with cloud scale or execute specific workloads on multiple cloud vendors.

How Sharon AI Enables S3-Compatible Cloud Storage for AISharon AI offers high-performance S3-compatible cloud data storage optimized for AI, machine learning, and HPC workloads.

Our infrastructure is engineered for speed, reliability, and scalability with:

Ultra-high-speed object storage

API-level integration with AWS S3

Integration with GPU-accelerated AI compute clusters

Support for cloud-native and colocated workloads

Whether you're building a vision model, training an LLM, or storing terabytes of sensor data, Sharon AI's S3-compatible cloud storage solution provides the performance and flexibility you need, without the burden of legacy storage platforms.

Affordable S3-Compatible Cloud Storage Solutions for AI and HPC Workloads If you're scaling AI or HPC infrastructure, storage costs can become a major barrier. That’s why our S3-Compatible Cloud Storage Solutions offer the ideal balance of performance and affordability, starting at just $8/TB/month.

Unlike traditional hyperscaler options, we provide high-performance, low-cost S3-compatible cloud data storage built specifically for the demanding needs of AI, deep learning, and large-scale simulations. You get predictable pricing without compromising speed, availability, or security.

Our infrastructure supports over 50 petabytes of scalable storage, ensuring your workloads can grow without limitations. Thanks to full S3 API compatibility, you can migrate to our platform with zero disruption. No code rewrites. No downtime. Just a seamless, drop-in replacement for your current S3-based workflows.

Whether you’re training large models, running GPU-intensive tasks, or managing complex research data, our S3-Compatible Cloud Storage Solutions provide the flexibility and reliability you need to focus on innovation, not infrastructure.

Real-World AI Use Cases Powered by S3-Compatible StorageHere are some real-world applications taking direct benefit of S3-compatible cloud storage solutions:

Autonomous car video and LIDAR data caching to train perception models

Medical AI processing medical imaging large datasets on distributed systems

Retail AI handles product images, product reviews, and customer engagement data

Natural Language Processing (NLP) models to retrieve vast text corpora from object-based storage

In each of these scenarios, fast, safe, and flexible access to unstructured data is essential—and that's exactly what S3-compatible cloud data storage delivers.

Final Thoughts As AI continues to grow and develop, so does the infrastructure upon which it rides. S3-compatible cloud storage platforms are no longer a nicety but a strategic necessity. From flexibility and cost savings to seamless tool integration and high-speed data access, S3-compatible cloud data storage is designed for the scale and speed required by AI. If your team is building or scaling AI systems, now is the time to rethink your storage strategy and explore how Sharon AI’s infrastructure can power your next breakthrough. Explore Sharon AI’s S3-Compatible Cloud Storage Solutions and see how we can help your AI infrastructure grow fast, secure, and future-ready.

#CloudStorage#ObjectStorage#S3Compatiblestorage#AIInfrastructure#AIStorage#AITechnology#S3Compatible#CloudInfrastructure#CloudComputing

0 notes

Text

FinFET Technology Market Size Elevating Semiconductor Performance to New Heights

The FinFET Technology Market Size marks a significant milestone in semiconductor fabrication, offering higher performance, lower power consumption, and enhanced scalability compared to traditional planar transistors. With devices shrinking to sub-10 nm nodes, the introduction of FinFETs—transistors featuring a 3D fin structure—has become pivotal for sustaining Moore's Law. These advancements are redefining computing, cellular, automotive, and edge AI applications.

According to Market Size Research Future, global FinFET technology is projected to grow significantly by 2030, driven by increasing demand for high-performance ASICs, 5G infrastructure, and AI accelerators. The shift toward smaller process nodes and energy-efficient designs continues to fuel investment across foundries and OEMs.

Overview of FinFET Technology

FinFET (Fin Field-Effect Transistor) represents a 3D transistor family designed for low leakage and efficient switching at nanometer-scale nodes. By wrapping a thin silicon fin around the gate, FinFETs improve electrostatic control and reduce short-channel effects—critical for modern chip performance.

You'll find FinFETs at the core of system-on-chip (SoC) architectures powering smartphones, high-speed computing, networking hardware, and high-throughput mobile devices. Applications span from Qualcomm's Snapdragon processors to Nvidia’s Ampere GPUs, as both industries prioritize performance-per-watt and thermal limits.

Key Growth Drivers

Advanced Process Node Demand The continuous scaling to 7 nm, 5 nm, and beyond requires FinFETs to maintain channel control, reduce leakage, and boost transistor density.

5G and Networking Infrastructure Infrastructure equipment—like RF front-end modules and baseband SoCs—rely on FinFETs to support high frequencies and low power under elevated thermal loads.

AI Accelerators & Edge Compute FinFETs offer the transistor scaling needed to maintain performance gains in data centers and energy-efficient edge AI processors.

Automotive and Industrial Electronics With automotive electronics requiring high reliability and low power, FinFET integration in ADAS, radar, and EV power components is rising sharply.

Market Size Segmentation

By Node Range: 14 nm & below / 10 nm–7 nm / 5 nm and below

By Transistor Type: High Performance (HP), Low Leakage (LO), High Voltage (HV)

By End‑User: Smartphones, Data Centers, 5G Infrastructure, Automotive, Defense & Aerospace, Consumer Electronics, Industrial IoT

Regional Dynamics

Asia-Pacific leads due to TSMC, Samsung, and Chinese foundries aggressively ramping advanced nodes.

North America excels in design leadership through companies like Intel and Nvidia, including advanced integration of FinFETs in HPC and AI chips.

Europe focuses on automotive-grade FinFETs, with contributions from Infineon and STMicroelectronics in the energy and mobility sectors.

Key Industry Players

TSMC – Dominant pure-play foundry with leadership in high-volume 5 nm and 3 nm FinFET production.

Samsung Foundry – Offers advanced FinFET nodes and innovative packaging through SoC integration.

Intel – Transitioning to FinFET and gate-all-around architectures in its IDM 2.0 strategy.

GlobalFoundries, UMC, and SMIC – Deliver mature FinFET nodes for automotive, industrial, and mid-range SoCs.

Cadence, Synopsys, Mentor (Siemens) – Provide EDA tools for FinFET-based design, modeling, and verification.

ARM, Qualcomm, Broadcom, Nvidia – Utilize FinFET technologies in their SoC portfolio.

Emerging Trends

Gate-All-Around (GAA) Evolution – Next-gen FETs transition from FinFET towards GAA structures (e.g., nanosheet), extending device scaling.

2.5D/3D Chiplets & Heterogeneous Packaging – Integrating FinFET chips via advanced interconnects for modular, multi-die systems.

Beyond FinFET – Research into nanosheet, nanowire transistors, and monolithic 3D stacking is progressing rapidly to sustain scaling.

AI/ML for Process Control – real-time analytics optimize yields and lower defects in FinFET production.

Challenges Ahead

Rising manufacturing costs at sub-5 nm nodes, requiring ROI over large orders.

Thermal management and interconnect resistance, demanding advanced packaging materials and cooling solutions.

Design complexity, requiring sophisticated EDA tools and IP for timing and variability control.

Geopolitical constraints and supply chain uncertainties necessitating diversification and capacity investment.

Future Outlook

FinFET technology will remain dominant through the 2025–2028 horizon, enabling cutting-edge applications in AI, 5G, and edge computing. The transition to GAA and further miniaturization promises continued performance gains. With increasing investment in specialized FinFET fabs and design platforms, this evolution supports the growing demands of intelligent, connected devices.

Related Insights

Explore adjacent technology fields shaping chip innovation:

Radar Lidar Technology for Railway Applications Market Size

Quadruped Robot Market Size

Oxygen Gas Sensor Market Size

E‑Tailing Solution Market Size

Consumer Electronics Mini LED Market Size

D‑Shaped Connector Market Size

Debris Extraction Tool Market Size

Diaper Attachment Sensor Market Size

Digital Holographic Display Market Size

Digital Photo Printing Market Size

Discrete Graphics Microprocessor and GPU Market Size

Diving Compressor Market Size

Explosion Proof Mobile Communication Device Market Size

0 notes

Text

4 PhD positions in High-Performance Scientific Computing @Unipisa! Deadline: J...

🚀 4 PhD positions in High-Performance Scientific Computing @Unipisa! 📅 Deadline: July 18, 2025 🎯 Research at the intersection of HPC, AI, medicine & more 🌍 Open to EU & non-EU applicants 🔗 Apply now: #PhD #HPC #AI #ScientificComputing #PhDposition Source by Fabio Durastante

#from:agristok#from:MathJobs1#fully funded phd programs#phd position in europe#phd position in norway#phd positions#phd positions in germany#phd positions in usa#postdoc jobs#postdoc position in germany#postdoc positions#postdoc positions in europe#postdoc positions in usa#postdoctoral fellowship

0 notes

Text

Available Cloud Computing Services at Fusion Dynamics

We Fuel The Digital Transformation Of Next-Gen Enterprises!

Fusion Dynamics provides future-ready IT and computing infrastructure that delivers high performance while being cost-efficient and sustainable. We envision, plan and build next-gen data and computing centers in close collaboration with our customers, addressing their business’s specific needs. Our turnkey solutions deliver best-in-class performance for all advanced computing applications such as HPC, Edge/Telco, Cloud Computing, and AI.

With over two decades of expertise in IT infrastructure implementation and an agile approach that matches the lightning-fast pace of new-age technology, we deliver future-proof solutions tailored to the niche requirements of various industries.

Our Services

We decode and optimise the end-to-end design and deployment of new-age data centers with our industry-vetted services.

System Design

When designing a cutting-edge data center from scratch, we follow a systematic and comprehensive approach. First, our front-end team connects with you to draw a set of requirements based on your intended application, workload, and physical space. Following that, our engineering team defines the architecture of your system and deep dives into component selection to meet all your computing, storage, and networking requirements. With our highly configurable solutions, we help you formulate a system design with the best CPU-GPU configurations to match the desired performance, power consumption, and footprint of your data center.

Why Choose Us

We bring a potent combination of over two decades of experience in IT solutions and a dynamic approach to continuously evolve with the latest data storage, computing, and networking technology. Our team constitutes domain experts who liaise with you throughout the end-to-end journey of setting up and operating an advanced data center.

With a profound understanding of modern digital requirements, backed by decades of industry experience, we work closely with your organisation to design the most efficient systems to catalyse innovation. From sourcing cutting-edge components from leading global technology providers to seamlessly integrating them for rapid deployment, we deliver state-of-the-art computing infrastructures to drive your growth!

What We Offer The Fusion Dynamics Advantage!

At Fusion Dynamics, we believe that our responsibility goes beyond providing a computing solution to help you build a high-performance, efficient, and sustainable digital-first business. Our offerings are carefully configured to not only fulfil your current organisational requirements but to future-proof your technology infrastructure as well, with an emphasis on the following parameters –

Performance density

Rather than focusing solely on absolute processing power and storage, we strive to achieve the best performance-to-space ratio for your application. Our next-generation processors outrival the competition on processing as well as storage metrics.

Flexibility

Our solutions are configurable at practically every design layer, even down to the choice of processor architecture – ARM or x86. Our subject matter experts are here to assist you in designing the most streamlined and efficient configuration for your specific needs.

Scalability

We prioritise your current needs with an eye on your future targets. Deploying a scalable solution ensures operational efficiency as well as smooth and cost-effective infrastructure upgrades as you scale up.

Sustainability

Our focus on future-proofing your data center infrastructure includes the responsibility to manage its environmental impact. Our power- and space-efficient compute elements offer the highest core density and performance/watt ratios. Furthermore, our direct liquid cooling solutions help you minimise your energy expenditure. Therefore, our solutions allow rapid expansion of businesses without compromising on environmental footprint, helping you meet your sustainability goals.

Stability

Your compute and data infrastructure must operate at optimal performance levels irrespective of fluctuations in data payloads. We design systems that can withstand extreme fluctuations in workloads to guarantee operational stability for your data center.

Leverage our prowess in every aspect of computing technology to build a modern data center. Choose us as your technology partner to ride the next wave of digital evolution!

#Keywords#services on cloud computing#edge network services#available cloud computing services#cloud computing based services#cooling solutions#hpc cluster management software#cloud backups for business#platform as a service vendors#edge computing services#server cooling system#ai services providers#data centers cooling systems#integration platform as a service#https://www.tumblr.com/#cloud native application development#server cloud backups#edge computing solutions for telecom#the best cloud computing services#advanced cooling systems for cloud computing#c#data center cabling solutions#cloud backups for small business#future applications of cloud computing

0 notes

Text

Multi-Core Computer Processors Market: Policy Impact and Regulatory Landscape 2025–2032

MARKET INSIGHTS

The global Multi-Core Computer Processors Market size was valued at US$ 67.34 billion in 2024 and is projected to reach US$ 128.67 billion by 2032, at a CAGR of 8.4% during the forecast period 2025-2032. The U.S. market accounted for 32% of global revenue in 2024, while China is expected to witness the fastest growth with a projected CAGR of 9.2% through 2032.

Multi-core processors are integrated circuits containing two or more processing units (cores) that read and execute program instructions simultaneously, significantly enhancing computational power and energy efficiency. These processors are categorized into dual-core, quad-core, eight-core, and higher configurations, each designed to meet specific performance requirements across various computing applications. The technology enables parallel processing, allowing multiple tasks to be executed simultaneously rather than sequentially.

The market growth is driven by increasing demand for high-performance computing across industries, particularly in data centers, AI applications, and gaming. The shift toward cloud computing and edge computing infrastructure has further accelerated adoption, as these technologies require processors capable of handling complex workloads efficiently. Meanwhile, innovations in semiconductor manufacturing, including the transition to smaller nanometer nodes, continue to push performance boundaries while improving power efficiency - a critical factor for mobile devices and IoT applications.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for High-Performance Computing to Accelerate Market Growth

The global multi-core processor market is experiencing robust growth, driven by increasing demand for high-performance computing (HPC) across industries. Data centers, AI applications, and cloud computing require processors that can handle parallel processing efficiently. Multi-core processors deliver superior performance by distributing workloads across multiple cores, enabling faster data processing and improved energy efficiency. The shift toward 5G networks and edge computing further amplifies the need for advanced multi-core solutions, as these technologies demand processors capable of handling real-time data processing with minimal latency. Recent advancements in artificial intelligence and machine learning applications have particularly fueled demand for processors with higher core counts, as they are essential for training complex neural networks.

Growth in Gaming and Content Creation Industry to Propel Market Expansion

The gaming and content creation industries are increasingly adopting high-core-count processors to enhance performance and user experience. Gamers and creative professionals require CPUs that can handle resource-intensive tasks such as 4K video editing, 3D rendering, and high-FPS gaming. The rising popularity of esports and live streaming has further accelerated the adoption of multi-core processors, as they allow for seamless multitasking while maintaining optimal performance. Leading manufacturers continue to innovate, launching processors with higher core counts and improved thermal efficiency to cater to this growing segment.

➤ For instance, AMD's Ryzen Threadripper PRO series processors with 64 cores have gained significant traction among professionals in the media and entertainment sector due to their exceptional multi-threading capabilities.

Additionally, the COVID-19 pandemic accelerated digital transformation across enterprises, pushing organizations to upgrade their IT infrastructure, which in turn boosted demand for high-performance computing solutions.

MARKET RESTRAINTS

Thermal and Power Constraints to Limit Processor Performance Gains

While multi-core processors offer substantial computing advantages, they face significant thermal and power-related challenges. As core counts increase, managing heat dissipation becomes increasingly complex. Thermal throttling—where processors reduce clock speeds to prevent overheating—can negatively impact performance, particularly in compact devices such as laptops and smartphones. Additionally, higher core counts demand more power, which can strain battery life in portable devices, presenting a barrier to widespread adoption in the mobile computing segment.

Other Constraints

Software Optimization Challenges Not all software applications efficiently utilize multiple cores, limiting the performance benefits of high-core-count processors. Legacy applications, in particular, may not take full advantage of parallel processing capabilities, reducing the incentive for consumers to upgrade.

Manufacturing Costs Developing multi-core processors with advanced fabrication processes increases production costs, which can result in higher prices for end-users. This pricing pressure may restrain market growth in cost-sensitive regions.

MARKET CHALLENGES

Supply Chain Disruptions and Semiconductor Shortages Hamper Market Stability

The semiconductor industry has faced persistent supply chain disruptions over recent years, directly impacting the production and availability of multi-core processors. Geopolitical tensions, trade restrictions, and fluctuations in raw material supply have exacerbated these challenges, leading to increased lead times and price volatility. The global chip shortage has particularly affected the automotive and consumer electronics industries, forcing manufacturers to reassess their supply chain strategies and inventory management. These constraints could potentially slow market expansion in the short term.

Intense Competition Among Chip Manufacturers Puts Pressure on Profit Margins

The market is witnessing fierce competition among key players such as Intel, AMD, and Arm-based manufacturers, each striving to push the boundaries of core-count and efficiency. While this competition drives innovation, it also exerts downward pressure on profit margins as companies engage in aggressive pricing strategies. Furthermore, the rapid pace of technological advancements means that manufacturers must continuously invest in R&D to remain competitive, increasing operational costs. Smaller players may struggle to keep up, potentially leading to industry consolidation.

Additionally, shifting consumer preferences towards system-on-a-chip (SoC) solutions in mobile and IoT sectors pose a challenge for traditional multi-core processor manufacturers.

MARKET OPPORTUNITIES

Expansion into AI and Edge Computing Applications Opens New Revenue Streams

The proliferation of AI-powered applications and edge computing presents significant growth opportunities for multi-core processor vendors. AI workloads require processors with high parallel processing capabilities, making multi-core architectures well-suited for neural network training and inference tasks. The Internet of Things (IoT) ecosystem is also driving demand for energy-efficient multi-core solutions that can perform real-time analytics at the edge, reducing latency and bandwidth usage. Companies developing specialized processors optimized for AI and edge deployments stand to gain a competitive advantage.

Increasing Adoption in Automotive and Industrial Applications Creates Untapped Potential

The automotive sector is undergoing a technological transformation with the rise of connected vehicles, autonomous driving systems, and advanced driver-assistance systems (ADAS). These applications require powerful multi-core processors to handle sensor data processing and decision-making in real time. Similarly, industrial automation and Industry 4.0 initiatives are driving demand for ruggedized multi-core processors capable of operating in harsh environments. As these segments continue to evolve, they present lucrative opportunities for processor manufacturers to diversify their product portfolios and enter high-growth verticals.

Furthermore, government initiatives supporting semiconductor manufacturing self-sufficiency in various regions are likely to create new investment opportunities in the multi-core processor market.

MULTI-CORE COMPUTER PROCESSORS MARKET TRENDS

Growing Demand for High-Performance Computing Driving Market Growth

The global multi-core computer processors market is experiencing significant growth, fueled by the increasing demand for high-performance computing (HPC) across industries. With applications ranging from artificial intelligence to cloud computing, multi-core processors have become essential for handling complex workloads efficiently. In 2024, the market was valued at $XX million, projected to grow at a CAGR of X% through 2032. Companies like Intel and AMD continue to push boundaries with architectures featuring up to 128 cores, enabling faster data processing for machine learning, real-time analytics, and gaming applications. The shift toward heterogeneous computing, combining CPU and GPU cores, further enhances performance while optimizing power efficiency.

Other Trends

Expansion of Edge Computing and IoT Devices

The proliferation of edge computing and Internet of Things (IoT) devices has created new opportunities for multi-core processors, particularly in low-power, high-efficiency applications. Manufacturers are developing energy-efficient quad-core and octa-core processors to meet the demands of smart devices, autonomous systems, and 5G infrastructure. For instance, the automotive sector relies on multi-core processors for advanced driver-assistance systems (ADAS), with Qualcomm and NXP Semiconductors leading innovation. Such advancements are expected to drive the smart mobile device segment to over $XX million by 2032, outpacing traditional computing applications.

AI and Machine Learning Fueling Processor Innovation

AI and machine learning workloads demand parallel processing capabilities, accelerating the adoption of multi-core architectures. Leading chipmakers are integrating AI accelerators and specialized cores to optimize neural network training and inference tasks. AMD's Ryzen Threadripper and Intel's Xeon Scalable processors demonstrate this trend, offering up to 96 cores for data centers. Concurrently, ARM-based designs are gaining traction in mobile and embedded systems, with Samsung and MediaTek incorporating multi-core configurations for on-device AI processing. Research indicates that over 60% of new server deployments now utilize multi-core processors, highlighting their dominance in enterprise infrastructure.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Partnerships Define the Multi-Core Processor Race

The global multi-core processor market remains highly competitive, dominated by established semiconductor giants while facing disruption from agile innovators. Intel Corporation continues to lead the market with a 2024 revenue share of approximately 28%, leveraging its x86 architecture dominance and continuous advancements in Core i-series processors. However, their position faces mounting pressure from competitors adopting ARM-based designs.

Advanced Micro Devices (AMD) has been gaining significant traction, capturing nearly 22% market share in 2024 through its Ryzen and EPYC processor lines. The company's chiplet design approach and superior multi-threading performance have been particularly disruptive in both consumer and data center segments. Meanwhile, Qualcomm and MediaTek are asserting dominance in mobile processors, collectively holding over 40% of the smartphone SoC market.

The competitive intensity is further amplified by vertical integration strategies, with companies like Samsung Electronics and Apple developing custom silicon for their devices. This trend is reshaping industry dynamics, as evidenced by Apple's M-series chips achieving 15% performance gains over x86 alternatives in benchmark tests.

Emerging players are focusing on niche segments - NXP Semiconductors and Texas Instruments lead in embedded systems, while Marvell Technology specializes in networking processors. The industry is witnessing increased R&D expenditure across the board, with top players allocating 18-25% of revenues to develop next-generation architectures.

List of Key Multi-Core Processor Manufacturers

Intel Corporation (U.S.)

Advanced Micro Devices (AMD) (U.S.)

Qualcomm Technologies (U.S.)

Samsung Electronics (South Korea)

Apple Inc. (U.S.)

MediaTek (Taiwan)

NXP Semiconductors (Netherlands)

Texas Instruments (U.S.)

Marvell Technology (U.S.)

ARM Holdings (U.K.)

Recent developments include AMD's acquisition of Xilinx to bolster its adaptive computing capabilities, while Intel's foundry services expansion aims to regain process technology leadership. The competitive landscape continues evolving as companies balance between architectural innovation, manufacturing capabilities, and ecosystem development to secure their positions in this trillion-transistor era.

Segment Analysis:

By Type

Quad-core Processors Lead Market Share Due to Optimal Performance and Energy Efficiency

The market is segmented based on type into:

Dual-core Processor

Quad-core Processor

Eight-core Processor

Others (Hexa-core, Deca-core, etc.)

By Application

Smart Mobile Devices Segment Dominates with Growing Demand for High-Performance Processors

The market is segmented based on application into:

Laptops

Desktop Computers

Smart Mobile Devices

Others (Servers, Gaming Consoles, etc.)

By End User

Consumer Electronics Sector Maintains Strong Position Due to Continuous Technological Advancements

The market is segmented based on end user into:

Consumer Electronics

Enterprise

Data Centers

Others (Industrial, Automotive, etc.)

Regional Analysis: Multi-Core Computer Processors Market

North America The North American market remains at the forefront of multi-core processor adoption, driven by robust demand from enterprise computing, gaming, and AI-driven applications. The U.S. accounts for over 60% of regional revenue, with Intel and AMD dominating processor shipments. Recent innovations such as Intel’s 14th Gen Core processors and AMD’s Ryzen 7000 series highlight the region’s emphasis on power efficiency and AI acceleration. However, supply chain constraints linked to semiconductor manufacturing persist as a challenge. The growing adoption of edge computing and data center expansions further stimulates growth, supported by government incentives like the CHIPS Act for domestic semiconductor production.

Europe Europe exhibits steady growth, with Germany, France, and the UK leading in demand for high-performance processors in automotive and industrial automation sectors. Strict EU energy-efficiency regulations are pushing manufacturers toward advanced multi-core designs with lower thermal design power (TDP). ARM-based processors are gaining traction, particularly in mobile and IoT applications, while x86 architectures dominate enterprise environments. The region also sees strong R&D investments from companies like NXP Semiconductors and STMicroelectronics. However, inflationary pressures and geopolitical uncertainties pose risks to supply chain stability.

Asia-Pacific Asia-Pacific is the largest and fastest-growing market, fueled by China’s semiconductor self-sufficiency initiatives and India’s booming consumer electronics sector. China’s domestic players, such as Huawei’s HiSilicon and Phytium, are aggressively competing in server-grade multi-core processors. Meanwhile, Taiwan remains a global hub for fabrication, accounting for over 60% of global foundry output. Mobile device manufacturers in Southeast Asia continue driving demand for energy-efficient octa-core processors. Despite this growth, export restrictions on advanced chipmaking technologies have slowed progress in some countries. Infrastructure gaps in testing and packaging also pose bottlenecks.

South America The South American market is emerging slowly due to economic volatility, but Brazil and Argentina show increasing demand for multi-core processors in budget laptops and localized server deployments. Import dependency raises costs, limiting penetration of high-end processors. Governments are incentivizing local assembly plants to reduce reliance on foreign suppliers, though currency fluctuations hinder long-term investments. Gaming and content creation markets present untapped opportunities if affordability improves. Nonetheless, the lack of domestic semiconductor ecosystems constrains innovation.

Middle East & Africa This region demonstrates fragmented growth, with the UAE, Saudi Arabia, and South Africa as primary markets. Demand is fueled by datacenter construction and smart city initiatives like Saudi’s NEOM project. However, limited local manufacturing forces heavy reliance on imports, leading to higher prices for end-users. While some nations invest in AI infrastructure, broader adoption of multi-core processors is hindered by low purchasing power outside urban hubs. Strategic partnerships with global suppliers could unlock potential, particularly in telecommunications and oil/gas automation applications.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Multi-Core Computer Processors market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

Segmentation Analysis: Detailed breakdown by product type (Dual-core, Quad-core, Eight-core), technology, application (Laptops, Desktops, Smart Mobile Devices), and end-user industry to identify high-growth segments.

Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis.

Competitive Landscape: Profiles of leading market participants including Intel, AMD, Qualcomm, Samsung, and their product portfolios, R&D investments, and strategic developments.

Technology Trends: Assessment of emerging processor architectures, AI integration, chiplet designs, and advanced manufacturing processes (5nm, 3nm nodes).

Market Drivers & Restraints: Evaluation of factors such as demand for high-performance computing, gaming industry growth, 5G adoption, alongside supply chain challenges and geopolitical factors.

Stakeholder Analysis: Strategic insights for semiconductor manufacturers, OEMs, cloud service providers, and investors regarding market opportunities.

The research methodology combines primary interviews with industry experts and analysis of verified market data from authoritative sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Multi-Core Computer Processors Market?

-> Multi-Core Computer Processors Market size was valued at US$ 67.34 billion in 2024 and is projected to reach US$ 128.67 billion by 2032, at a CAGR of 8.4% during the forecast period 2025-2032.

Which key companies operate in this market?

-> Dominant players include Intel, Advanced Micro Devices (AMD), Qualcomm, Samsung Electronics, and Apple, with the top five companies holding ~68% market share.

What are the key growth drivers?

-> Primary drivers include rising demand for high-performance computing, growth in cloud infrastructure, gaming industry expansion, and proliferation of AI/ML applications.

Which region dominates the market?

-> Asia-Pacific holds the largest market share (42% in 2024), driven by semiconductor manufacturing in Taiwan/South Korea and strong demand from China. North America leads in advanced processor adoption.

What are the emerging trends?

-> Key trends include heterogeneous computing architectures, chiplet-based designs, integration of AI accelerators, and transition to 3nm/2nm process nodes.

Related Reports:https://semiconductorblogs21.blogspot.com/2025/06/ssd-processor-market-segmentation-by.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/semiconductor-wafer-processing-chambers.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/medical-thermistor-market-supply-chain.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/industrial-led-lighting-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/fz-polished-wafer-market-demand-outlook.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/fanless-embedded-system-market-regional.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/ceramic-cement-resistor-market-emerging.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/universal-asynchronous-receiver.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/fbg-strain-sensor-market-competitive.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/led-display-module-market-industry-size.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/gain-and-loss-equalizer-market-growth.html

0 notes

Text

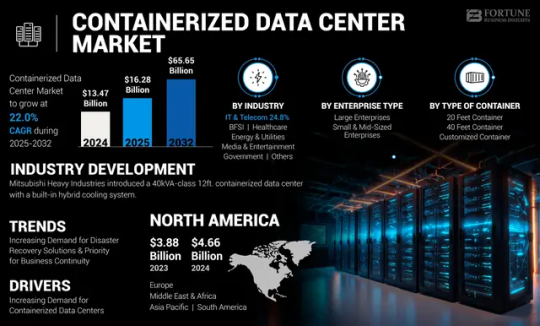

Containerized Data Center Market Size Expected to Reach USD 65.65 Bn By 2032

The global Containerized Data Center Market Industry was valued at USD 13.47 billion in 2024 and is projected to grow to USD 65.65 billion by 2032, exhibiting a CAGR of 22.0% during the forecast period (2025–2032). As organizations worldwide seek scalable, portable, and energy-efficient IT infrastructure, containerized solutions are rapidly transforming the data center landscape.

Key Market Highlights:

2024 Global Market Size: USD 13.47 billion

2025 Forecast Start: USD 16.28 billion

2032 Global Market Size: USD 65.65 billion

CAGR (2025–2032): 22.0%

U.S. Forecast (2032): USD 16.81 billion

Primary Growth Drivers: Surge in edge computing, need for rapid deployment, and energy-efficient infrastructure

U.S. Market Outlook:

The U.S. containerized data center market is forecasted to reach USD 16.81 billion by 2032, supported by: