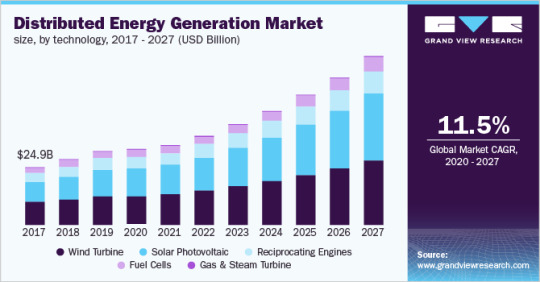

#Distributed Energy Generation Market Size

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Users from the US are the majority of Tumblr visitors.

Text

Distributed Energy Generation Market Size To Reach USD 580.8 Billion By 2027

Distributed Energy Generation Market Growth & Trends

The global distributed energy generation market size is expected to reach USD 580.8 billion by 2027 registering a CAGR of 11.5%, according to a new report by Grand View Research, Inc. The increasing need for energy and the high costs of grid expansion are the major factors driving the market growth. Low prices of Distributed Energy Generation (DEG) as compared to the conventional power generation methods are expected to provide a boost to the market.

Moreover, inventions in DEG techniques, including floating solar PV, is expected to drive the market. Declining costs of solar PVs is playing a contributory role in the expansion of the market. Feed-in tariffs in regions, such as North America, Europe, and the Asia Pacific, are poised to stir up the growth of the market. Favorable government policies and other government regulations including net metering are expected to increase the number of DEG installations at residential locations, such as underdeveloped and rural areas.

Extensive R&D, field trials, and demonstration projects have resulted in decreasing costs of DEG technologies, which, in turn, augmented market growth. China, India, and Japan are some of the key countries where energy demand has risen significantly. The grid connections are incapable of meeting such high demands that are further supplemented with energy loss problems and blackouts. As a result, institutions, schools, and universities opt for small power-generating stations using renewable sources. This is expected to grow the demand for this market.

Request a free sample copy or view report summary: https://www.grandviewresearch.com/industry-analysis/distributed-energy-generation-industry

Distributed Energy Generation Market Report Highlights

Growing demand for green energy owing to the increasing population across the globe coupled with rapid urbanization in developing countries is expected to be the main catalyst for the demand for DEG systems

The fuel cells technology segment led the global market in 2019 accounting for the largest market share and will continue to grow at a steady pace over the forecast years

However, the solar photovoltaic segment is estimated to register the fastest CAGR from 2020 to 2027

Asia Pacific is projected to be the largest as well as the fastest-growing regional market over the forecast period

China, in particular, is expected to account for the maximum share of the Asia Pacific regional market

Commercial & industrial is projected to be the largest application segment while the residential segment will have the maximum CAGR from 2020 to 2027

Distributed Energy Generation Market Segmentation

Grand View Research has segmented the global distributed energy generation market on the basis of technology, application, and region:

DEG Technology Outlook (Volume, MW; Revenue, USD Million, 2016 - 2027)

Wind Turbine

Solar Photovoltaic

Reciprocating Engines

Fuel Cells

Gas & Steam Turbine

DEG Application Outlook (Volume, MW; Revenue, USD Million, 2016 - 2027)

Residential

Commercial & Industrial

DEG Regional Outlook (Installed Capacity, KW; Revenue, USD Million, 2016 - 2027)

North America

The U.S.

Canada

Mexico

Europe

Germany

The U.K.

Italy

Asia Pacific

China

India

Australia

Central and South America

Brazil

The Middle East and Africa

List of Key Players of Distributed Energy Generation Market

Vestas Wind Systems A/S

Capstone Turbine Corp.

Caterpillar

Ballard Power Systems Inc.

Doosan Heavy Industries & Construction

Rolls-Royce plc.

Suzlon Energy Ltd.

General Electric

Siemens

Schneider Electric

ENERCON GmbH

Sharp Corp.

First Solar

Mitsubishi Electric Corp.

Toyota Turbine and Systems Inc.

Browse Full Report: https://www.grandviewresearch.com/industry-analysis/distributed-energy-generation-industry

#Distributed Energy Generation Market#Distributed Energy Generation Market Size#Distributed Energy Generation Market Share

0 notes

Text

Chicago, Dec. 06, 2023 (GLOBE NEWSWIRE) -- The global Gas Insulated Switchgear Market is expected to grow from USD 23.8 billion in 2023 to USD 31.6 billion by 2028, at a CAGR of 5.8% according to a new report by MarketsandMarkets™. The gas insulated switchgear market is poised for substantial growth during this period, primarily due to the expected strengthening of power distribution infrastructure in response to the growing demand for electricity. Furthermore, the expansion of renewable energy capacity and increased investments in industrial production are set to drive the demand for gas insulated switchgear. The market is expected to experience accelerated growth, particularly with the increasing use of high-voltage direct systems.

#gas insulated switchgear#gas insulated switchgear market#gas insulated switchgear (GIS)#switchgears#switchgear#switchgear market#switchgear industry#gas insulated switchgear market size#gas insulated switchgear market share#gas insulated switchgear industry#power#energy#energia#power generation#utilities#utility#electricity#renewableenergy#renewable resources#renewable energy#renewable electricity#HVDC#transmission and distribution#power transmission#power distribution

0 notes

Text

Distributed Energy Generation Market to Hit $694.66 Billion by 2032

The global Distributed Energy Generation Market was valued at USD 305.81 Billion in 2024 and it is estimated to garner USD 694.66 Billion by 2032 with a registered CAGR of 10.8% during the forecast period 2024 to 2032.

Are you looking for the Distributed Energy Generation Market Research Report? You are at the right place. If you desire to find out more data about the report or want customization, Contact us. If you want any unique requirements, please allow us to customize and we will offer you the report as you want.

The global Distributed Energy Generation Market can be segmented on the basis of product type, Applications, distribution channel, market value, volume, and region [North America, Europe, Asia Pacific, Latin America, Middle East, and Africa]. The Distributed Energy Generation Industry 2024 report provides a comprehensive overview of critical elements of the industry including drivers, restraints, and management scenarios.

Download Sample PDF: @ https://www.vantagemarketresearch.com/distributed-energy-generation-market-2013/request-sample

Top Players

Vestas (Denmark), Caterpillar (U.S.), Capstone Green Energy Corporation (U.S.), Doosan Heavy Industries & Construction (South Korea), Toyota Tsusho Corporation (Japan), Rolls-Royce PLC (U.K.), General Electric (U.S.), Mitsubishi Electric Corporation (Japan), Schneider Electric (France), Siemens (Germany), to name a few.

Trending 2024: Distributed Energy Generation Market Report Highlights:

A comprehensive assessment of the parent Industry

Development of key aspects of the business

A study of industry-wide market segments

Evaluation of market value and volume in past, present, and future years

Evaluation of market share

Tactical approaches of market leaders

Innovative strategies that help companies to improve their position in the market

You Can Buy This Report From Here: https://www.vantagemarketresearch.com/buy-now/distributed-energy-generation-market-2013/0

Analysis Of The Top Companies, Product Types, and Applications In The Market Report:

This report provides sales, revenue growth rate, and verified information about the major players. Also includes a regional analysis and a labor cost analysis, tables, and figures. It also highlights characteristics such as technological growth. The product type segment is expected to continue to maintain its leading position in the future and capture a significant market share based on sales. This report provides analysis, discussion, forecast, and debate on key industry trends, market share estimates, Industry size, and other information. This report also discusses drivers, risks, and opportunities.

Global Distributed Energy Generation Market report contains detailed data and analysis on the Distributed Energy Generation Market drivers, restraints, and opportunities. Experts with market and industry knowledge as well as research experience from regional experts validate the report. The Distributed Energy Generation Market report provides forecast, historical and current revenue for each industry, region, and end-user segment.

Regions Included

-North America [United States, Canada, Mexico]

-South America [Brazil, Argentina, Columbia, Chile, Peru]

-Europe [Germany, UK, France, Italy, Russia, Spain, Netherlands, Turkey, Switzerland]

-Middle East & Africa [GCC, North Africa, South Africa]

-Asia-Pacific [China, Southeast Asia, India, Japan, Korea, Western Asia]

Global Distributed Energy Generation Market report data will help you make more informed decisions. For example, in relation to prices, distribution channels are means of marketing or identifying opportunities to introduce a new product or service. These results will also help you make more informed decisions about your existing operations and activities.

Read Full Research Report with [TOC] @ https://www.vantagemarketresearch.com/industry-report/distributed-energy-generation-market-2013

You Can Use The Distributed Energy Generation Market Report To Answer The Following Questions:

What are the growth prospects of the Distributed Energy Generation Market business?

Who are the key manufacturers in the Distributed Energy Generation Market space?

What Forecast Period for Global Distributed Energy Generation Industry Report?

What are the main segments of the global Distributed Energy Generation Market?

What are the key metrics like opportunities and market drivers?

The Distributed Energy Generation Market Insights

Product Development/Innovation: Detailed Information On Upcoming Technologies, R&D Activities, And Product Launches In The Market.

Competitive Assessment: In-Depth Assessment Of Market Strategies, Geographic And Business Segments Of Key Market Players.

Market Development: Comprehensive Information On Emerging Markets. This Report Analyzes The Market For Different Segments In Different Regions.

Market Diversification: Comprehensive Information On New Products, Untapped Regions, Latest Developments, And Investments In The Distributed Energy Generation Market.

Check Out More Reports

Global DNA Sequencing Market: Report Forecast by 2032

Global Agricultural Enzymes Market: Report Forecast by 2032

Global Healthy Snacks Market: Report Forecast by 2032

Global Smart Air Purifiers Market: Report Forecast by 2032

Global Breast Cancer Therapeutics Market: Report Forecast by 2032

#Distributed Energy Generation Market#Distributed Energy Generation Market 2024#Global Distributed Energy Generation Market#Distributed Energy Generation Market outlook#Distributed Energy Generation Market Trend#Distributed Energy Generation Market Size & Share#Distributed Energy Generation Market Forecast#Distributed Energy Generation Market Demand#Distributed Energy Generation Market sales & price

0 notes

Text

#Global Distributed Energy Generation Market Size#Share#Trends#Growth#Industry Analysis#Key Players#Revenue#Future Development & Forecast

0 notes

Text

The global Transformer Oil Market is projected to reach USD 3.0 billion in 2030 from USD 2.0 billion in 2023 at a CAGR of 5.9% according to a new report by MarketsandMarkets™.

#transformer#power transformers#distribution transformer#power transformer#transformers#transformer oil market 2021#transformer oil#transformer oil market size#transformer oil market#Transformer oil industry#utilities industry#energy#power#electricity#power generation#utilities#electric utilities#renewable energy#oil and gas#mineral oil#electrical utilities#utility#transmission and distribution#power transmission#power distribution

0 notes

Text

As a farmers market shopper, you are most likely familiar with the ‘Slow Food Movement’ that emphasizes the mindful consumption of unprocessed, seasonal foods that are locally grown and prepared using culturally traditional cooking techniques. It goes without saying that our farmers markets act as hubs for connecting people with all the ingredients they need to foster a healthy, slow food lifestyle and its thoughtful approach to eating. But did you know that this concept – and the larger ‘slow living’ umbrella that it is part of – has extended into many arenas of everyday life, including the purchasing of decorative, cut flowers? In fact, the very same principles that apply to the consumption of ‘slow foods’ also apply to the intentional choices we make when selecting fresh flowers to buy for ourselves and others.

Adorning one’s living space with colorful, sweetly scented flowers or gifting someone with a beautiful fresh bouquet is one of life’s simple pleasures that is accessible to most everyone. But behind those innocent-looking blooms sometimes lies a little-known dark side. Just as with modern-day industrial overproduction of food, the large-scale production, shipping and packaging of commercially grown cut flowers exacts a huge environmental toll that most consumers are generally not aware of. To address these issues, the slow flower movement encourages the sustainable, responsible and mindful consumption of decorative flowers. Along those lines, here are some things to keep in mind the next time you are looking to replace the desiccated, wilted stems in your hallway flower vase (hint: head directly to your local farmers market this summer).

Seasonal flowers When you purchase fresh flowers in the dead of winter here in the northeast, such as buying a dozen red roses for your Valentine in mid-February, it’s a safe assumption that those blooms were not grown anywhere nearby. In fact, the majority of cut flowers sold in the U.S. are grown in far-flung warmer climates that allow for year-round production, such as California and South America. Happily, the arrival of summer to this region brings with it an influx of fresh produce into our farmstalls along with displays of fresh flowers, from sweet posies of wildflowers to sturdy bunches of sunflowers. Unlike industrially grown flowers, farmers market flowers are only available when the growing conditions allow for their production in harmony with nature’s rhythms. Whereas commercial growers routinely spray their crops with copious amounts of chemicals such as pesticides, herbicides and fungicides to ensure a constant yield, the seasonally appropriate production of local flowers requires fewer inputs and synthetic applications.

Refrigeration and transportation After industrially grown flowers are harvested from fields and greenhouses, they are stored in chilled warehouses to preserve their freshness before being transported via refrigerated trucks to the airport where they are then flown to their various destinations via cargo planes. Upon arrival, they are transferred back into refrigerated trucks and driven to retailers and other commercial distribution centers. The long-haul transportation and extended refrigeration of these flowers before they reach their point-of-sale requires an enormous expenditure of energy that balloons the size of their carbon footprint. Alternatively, the farmers market flowers that you see have been grown locally and have made only a short trip from the field to the marketplace. They’ll be fresher by the time you get them home and your purchase helps support a small farm or flower vendor versus a large faceless corporation.

Native flowers The range of exotic blooms you’ll find at a commercial florist or supermarket are typically not indigenous to the northeast, having been grown in different countries and warmer states. Amongst the cheerful posies of fresh flowers populating the farmstalls, you’ll find a preponderance of native plant varieties that have been growing in this area for thousands of years. These native flowers are uniquely adapted to thrive in the specific growing conditions of this region and have co-evolved alongside our local pollinators and wildlife forming a beneficial symbiosis and helping to promote biodiversity. For instance, Rudbeckia (aka black-eyed-susan or coneflower) is an herbaceous perennial native to North America that is prized for its showy golden yellow flowers that are being sold in our farmers markets right now. The nectar and pollen its flowers produce feeds native bees, butterflies, and other pollinators and it is also a larval host plant for Silvery Checkerspot (Chlosyne nycteis) caterpillars. Sticking within the yellow flower theme, all 52 varieties of sunflowers (Helianthus) are indigenous to North America while their seeds have formed a staple part of the American Indian diet for thousands of years.

Packaging Unlike the bouquets sold by commercial florists and retailers that are often heavily packaged in plastic cellophane, when you purchase a bouquet in the farmers market, it may come wrapped in kraft paper or simply bundled up, ready to be tucked into your shopping tote. Whereas plastic film is hard to recycle and adding to our planet’s ongoing plastic pollution problem, paper is biodegradable and can be tossed in the compost along with your cut flowers once they have reached the end of their useful life.

And there you have it! We wish you a very happy summer season of ‘slow food’ AND ‘slow flower’ shopping in our Down to Earth farmers markets.

#downtoearthmkts#farmersmarket#farmersmarkets#eatlocal#shoplocal#localfood#buylocal#eatdowntoearth#local flowers#slow food#slow living#native plants#native species

3 notes

·

View notes

Text

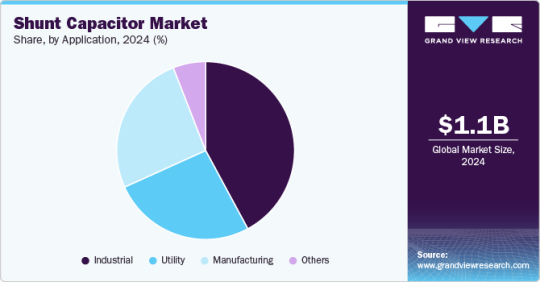

Why the Shunt Capacitor Market Is Booming in Asia-Pacific

The global shunt capacitor market, valued at USD 1.08 billion in 2024, is projected to reach USD 1.61 billion by 2030, exhibiting a Compound Annual Growth Rate (CAGR) of 7.0% from 2025 to 2030. This expansion is significantly driven by the increasing global demand for electricity and the growing complexity of power grids. Shunt capacitors are crucial for enhancing power factor, minimizing line losses, and stabilizing voltage within transmission and distribution networks.

Both utilities and industrial facilities are increasingly investing in solutions to improve power quality, which further stimulates market growth. Additionally, governmental mandates for grid modernization, the integration of renewable energy sources, and the promotion of energy efficiency initiatives are all contributing to the escalating demand for shunt capacitors.

Key Market Trends & Insights:

Regional Dominance: The Asia Pacific region commanded the largest share of the shunt capacitor market, holding 45.04% of the revenue in 2024. This is primarily due to the region's rapid industrialization, expanding power transmission and distribution infrastructure, and substantial investments in renewable energy projects.

Voltage Rating Focus: The low and medium voltage shunt capacitor segment is experiencing significant growth, driven by the increasing demand for energy efficiency, power factor correction, and grid stability across industrial, commercial, and utility sectors.

Application Leadership: The industrial segment holds the largest revenue share in the market, approximately 42% in 2024. This is attributed to the rising need for power factor correction, voltage stabilization, and energy efficiency within diverse industrial applications.

Order a free sample PDF of the Shunt Capacitor Market Intelligence Study, published by Grand View Research.

Market Size & Forecast

2024 Market Size: USD 1.08 Billion

2030 Projected Market Size: USD 1.61 Billion

CAGR (2025 - 2030): 7.0%

Asia Pacific: Largest market in 2024

Key Companies & Market Share Insights

Key players in the shunt capacitor market, including ABB Ltd., Schneider Electric, General Electric Company, Siemens AG, and Larsen & Toubro Ltd., are strategically focusing on innovation and enhancing their product portfolios to gain a competitive edge. These leading manufacturers are actively investing in research and development to create high-performance capacitors with extended lifespans, improved reliability, and integrated smart monitoring capabilities. This includes leveraging IoT and AI-driven predictive maintenance to optimize operational efficiency. Market competition is also shaped by economies of scale, as major players expand their production capacities to meet global demand while maintaining cost competitiveness.

ABB has made significant investments in smart grid technologies, incorporating shunt capacitors with advanced monitoring and control systems to bolster grid stability and efficiency. Furthermore, the company is dedicated to developing environmentally friendly shunt capacitors with a reduced ecological footprint, aligning with global sustainability objectives.

Schneider Electric focuses on power factor correction and energy efficiency solutions, offering a range of shunt capacitors designed to optimize electrical systems in various sectors. Their product portfolio emphasizes reliability and smart features to meet the evolving demands of industrial, commercial, and utility applications.

General Electric Company (GE) provides high-voltage capacitors engineered for robust performance and improved power quality. GE's offerings include a variety of fusing schemes and are designed to enhance system capacity, stability, and efficiency across power generation, transmission, distribution, and industrial applications.

Siemens has integrated IoT-enabled shunt capacitors to facilitate real-time monitoring and predictive maintenance, thereby improving operational efficiency. The company is committing substantial resources to research and development aimed at producing next-generation shunt capacitors that offer superior efficiency and extended lifespans.

Larsen & Toubro Ltd., a prominent Indian multinational conglomerate, is a significant player in the electrical and automation segment, including the shunt capacitor market. Their strategy often involves catering to large-scale infrastructure projects and industrial applications, contributing to grid stability and power quality enhancement in emerging markets.

Key Players

ABB Ltd.

Schneider Electric

General Electric Company

Siemens AG

Larsen & Toubro Ltd

Eaton Corporation Plc

Aerovox Corp.

Magnewin Energy Private Limited

CIRCUTOR, SA

Energe Capacitors Pvt Ltd.

Explore Horizon Databook - The world's most expansive market intelligence platform developed by Grand View Research.

Conclusion

The shunt capacitor market is growing steadily, driven by increasing global electricity demand and complex power grids. These capacitors are crucial for power quality, reducing losses, and stabilizing voltage. Utilities, industries, and government-mandated grid modernization, renewable integration, and energy efficiency initiatives further fuel this growth. Asia Pacific leads the market, with low/medium voltage and industrial applications being key segments. Leading companies are investing in R&D for advanced, reliable, and smart capacitors while expanding production to meet demand.

0 notes

Text

Tubular Cable Termination Market: Demand and Supply Forecast 2025–2032

MARKET INSIGHTS

The global Tubular Cable Termination Market size was valued at US$ 1,890 million in 2024 and is projected to reach US$ 3,240 million by 2032, at a CAGR of 8.09% during the forecast period 2025-2032. The U.S. market accounted for 25% of global revenue in 2024, while China’s market is expected to grow at a faster CAGR of 6.8% through 2032.

Tubular cable terminations are specialized components designed to provide secure and reliable electrical connections while protecting cables from environmental factors. These terminations come in two primary types: insulated variants for enhanced safety in residential and commercial applications, and uninsulated versions typically used in industrial settings where additional protection layers exist. The insulation segment currently dominates with 68% market share but is projected to grow slightly slower than uninsulated variants due to increasing industrial automation demands.

Market growth is driven by escalating infrastructure development, particularly in emerging economies, coupled with rising investments in renewable energy projects requiring robust cable management solutions. Recent industry developments include 3M’s 2023 launch of Cold Shrink QT-III tubular terminations with improved moisture resistance, reflecting the ongoing technological advancements in this space. Leading players like TE Connectivity and Hubbell continue to expand their product portfolios through strategic acquisitions, intensifying competition in both developed and developing markets.

MARKET DYNAMICS

MARKET DRIVERS

Increased Infrastructure Development to Drive Tubular Cable Termination Demand

The global construction boom is creating substantial demand for tubular cable terminations across residential, commercial, and industrial applications. With urbanization rates climbing steadily worldwide, particularly in emerging economies, the need for reliable electrical infrastructure has never been higher. The construction sector accounts for approximately 35% of global cable termination usage, driven by new building projects and renovation activities. Recent housing shortages in major economies have prompted governments to initiate large-scale affordable housing projects, further fueling cable accessory requirements. These terminations are critical components in ensuring safe and efficient power distribution within modern structures.

Rising Focus on Renewable Energy Projects Creates New Installation Demand

The global shift toward renewable energy is generating significant opportunities for tubular cable termination manufacturers. Solar and wind farm installations require extensive cabling networks with specialized terminations to handle challenging environmental conditions while maintaining operational efficiency. The renewable sector is projected to account for over 40% of power generation investments in the next decade, creating parallel demand for quality cable accessories. Offshore wind projects particularly require corrosion-resistant, high-performance terminations capable of withstanding saltwater exposure and extreme weather conditions. This sector’s growth directly correlates with increasing orders for marine-grade tubular cable terminations from energy developers.

The industrial automation wave is also contributing to market expansion as manufacturing facilities upgrade their electrical systems to support smart factory initiatives. This transition requires modernization of power distribution networks with reliable cable accessories to minimize downtime risks.

MARKET RESTRAINTS

Volatile Raw Material Pricing Impacts Manufacturing Stability

Manufacturers face significant challenges from fluctuating prices of key raw materials like copper, aluminum, and specialized polymers. These commodities can experience price swings exceeding 25% annually, making production cost forecasting extremely difficult. Copper alone represents about 60% of material costs for many cable termination products, and its pricing has shown persistent volatility in recent years. This uncertainty forces manufacturers to either absorb margin pressures or implement frequent price adjustments, both of which can negatively impact customer relationships and long-term contracts.

Supply chain disruptions further compound these challenges, with lead times for certain materials extending unpredictably. The industry has faced component shortages averaging 20-30 weeks for specialized insulating materials, delaying production schedules. These conditions create bidding disadvantages against competitors with stronger supplier networks or alternative material sources.

MARKET CHALLENGES

Technical Complexity in High-Voltage Applications Limits Market Penetration

The development of reliable terminations for ultra-high voltage (UHV) applications above 500kV presents substantial technical hurdles. These systems require advanced materials and precision engineering to prevent partial discharge issues and thermal runaway failures. Field data indicates that roughly 15% of UHV cable failures originate from termination points, highlighting the critical performance requirements. The specialized expertise needed for these applications creates barriers to entry for smaller manufacturers while increasing R&D costs across the industry.

Installation skill gaps represent another persistent challenge, particularly in emerging markets where experienced technicians are scarce. Improper termination installation accounts for nearly 30% of premature cable system failures, according to industry maintenance reports. This situation necessitates extensive training programs and detailed installation guidelines – both of which add to product lifecycle costs.

MARKET OPPORTUNITIES

Smart City Initiatives Create Demand for Advanced Termination Solutions

Global smart city projects present significant growth potential through their integrated infrastructure requirements. These developments demand cable accessories with monitoring capabilities, including temperature sensors and partial discharge detection features. The smart city component market is projected to grow substantially, with electrical infrastructure representing a major segment. Terminations that enable condition monitoring and predictive maintenance align perfectly with smart grid philosophies, opening premium product niches.

Electric vehicle charging infrastructure expansion provides another substantial opportunity. The planned installation of millions of charging stations globally will require robust cable terminations capable of handling frequent high-current cycles. Manufacturers developing specialized solutions for this segment can capture early market positioning advantages.

TUBULAR CABLE TERMINATION MARKET TRENDS

Increasing Demand for Reliable Power Distribution to Drive Market Growth

The global tubular cable termination market is experiencing significant growth due to the rising demand for efficient and reliable power distribution networks. With urbanization accelerating worldwide, particularly in developing economies, investments in grid infrastructure upgrades have surged. The market was valued at $X million in 2024 and is projected to reach $Y million by 2032, growing at a CAGR of Z% during the forecast period. Industrial and commercial sectors, which require secure and durable cable connections to minimize downtime, are major contributors to this expansion. Additionally, the increasing adoption of high-voltage underground cabling systems in urban environments further fuels demand for robust termination solutions.

Other Trends

Advancements in Material Technology

Innovations in polymer-based insulation materials have significantly enhanced the performance and longevity of tubular cable terminations. Manufacturers are increasingly focusing on heat-resistant and weatherproof materials to improve durability in harsh environments. The insulation segment alone is expected to grow at a CAGR of A% through 2032, driven by the need for higher dielectric strength and thermal stability. Furthermore, breakthroughs in silicone rubber and ethylene propylene rubber (EPR) compounds have enabled lighter, more flexible terminations without sacrificing reliability—a key factor for installations in confined spaces.

Expansion of Renewable Energy Infrastructure

The global push toward renewable energy projects, including offshore wind farms and solar parks, has created substantial opportunities for the tubular cable termination market. These installations require specialized terminations capable of withstanding extreme environmental conditions while maintaining uninterrupted power transmission. In 2024, renewable energy applications accounted for approximately B% of total market demand, with projections indicating accelerated growth as countries ramp up clean energy investments. The increasing complexity of subsea cable networks for offshore wind projects has particularly driven innovation in corrosion-resistant termination solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Focus on Innovation and Expansion to Capture Growing Demand

The global tubular cable termination market features a mix of multinational corporations and specialized manufacturers competing across residential, commercial, and industrial applications. 3M and TE Connectivity dominate the competitive landscape, collectively holding over 30% market share in 2024. Their leadership stems from comprehensive product portfolios covering both insulated and uninsulated termination solutions, combined with strong distribution networks across North America and Europe.

While established players maintain dominance through brand recognition, mid-sized companies like Brugg Kabel AG and ENSTO are gaining traction by offering customized solutions for specific industrial applications. These challengers compete effectively by focusing on high-performance materials and quick turnaround times for specialized orders.

The market has seen increased M&A activity as companies seek to expand their geographic footprint. Hubbell Incorporated recently acquired a regional player to strengthen its position in the Asian market, while Pioneer Power International expanded its product line through strategic partnerships with material suppliers. Such moves are reshaping competitive dynamics as companies position themselves for the projected 5.8% CAGR through 2032.

Emerging markets are becoming battlegrounds for market share, with ZMS Cables and A-1 Electricals making significant investments in Southeast Asia and Africa. These regions present growth opportunities due to infrastructure development projects and increasing electrification rates, prompting both global and local players to enhance their production capabilities.

List of Key Tubular Cable Termination Manufacturers

3M (U.S.)

TE Connectivity (Switzerland)

Brugg Kabel AG (Switzerland)

Nelco Products (U.S.)

ZMS Cables (China)

ENSTO (Finland)

MECATRACTION (France)

LML Products (U.K.)

Raytech S.r.l. (Italy)

Connection Systems group (U.S.)

Compaq International (India)

KONTECH INDUSTRIES (India)

A-1 Electricals (India)

Hubbell (U.S.)

Pioneer Power International (U.S.)

Segment Analysis:

By Type

Insulated Segment Dominates Due to Rising Safety Regulations in Electrical Installations

The market is segmented based on type into:

Insulated

Uninsulated

By Application

Industrial Segment Leads Owing to Extensive Usage in Heavy-Duty Electrical Infrastructure

The market is segmented based on application into:

Residential

Commercial

Industrial

By Voltage Rating

Medium Voltage Segment Holds Significant Share Due to Widespread Power Distribution Needs

The market is segmented based on voltage rating into:

Low Voltage

Medium Voltage

High Voltage

By Material

Copper-Terminated Cables Remain Preferred Choice for Superior Conductivity

The market is segmented based on material into:

Copper

Aluminum

Others

Regional Analysis: Tubular Cable Termination Market

North America The North American market for tubular cable terminations is driven by high infrastructure investments and stringent safety standards, particularly in the U.S. and Canada. With an estimated market size of $X million in 2024, the region benefits from extensive utility upgrades and industrial expansion. Key players like 3M and TE Connectivity dominate due to their technological advancements in insulated termination solutions. The growing renewable energy sector also fuels demand for reliable cable termination systems, especially in solar and wind power applications. However, strict regulatory compliance—including UL and IEEE standards—increases production costs but ensures long-term reliability.

Europe Europe’s market is characterized by strong emphasis on sustainability and energy efficiency, with countries like Germany and France leading in adoption. The EU’s focus on smart grid modernization and underground cabling projects supports demand for high-performance terminations. Innovations in heat-shrink and cold-shrink technologies from companies like Brugg Kabel AG and ENSTO cater to the region’s strict environmental and safety norms. Southeast European nations are gradually catching up, driven by cross-border electricity projects and grid interconnections. The market, however, faces challenges from fluctuating raw material prices and competition from low-cost Asian imports.

Asia-Pacific As the fastest-growing regional market, Asia-Pacific is projected to reach $X million by 2032, led by China, India, and Japan. Rapid urbanization, industrial growth, and government-led power infrastructure programs (e.g., China’s State Grid expansions) are primary drivers. While cost-effective uninsulated terminations dominate in developing economies due to budget constraints, adoption of advanced solutions is rising in sectors like oil & gas and data centers. Local manufacturers, including ZMS Cables and KONTECH INDUSTRIES, compete with global brands by offering customized solutions. However, inconsistent quality standards and supply chain disruptions remain hurdles.

South America South America’s market is emerging, backed by investments in mining, utilities, and renewable energy projects. Brazil and Argentina are key contributors, though economic instability slows large-scale adoption. The region shows preference for medium-voltage terminations in industrial applications, with Compaq International and Hubbell gaining traction. Limited local manufacturing capacity leads to dependency on imports, increasing costs. Nevertheless, upcoming energy reforms and foreign investments hint at long-term potential, especially in offshore wind and hydropower sectors.

Middle East & Africa This region presents niche opportunities, with GCC countries spearheading demand via megaprojects and oilfield expansions. The UAE and Saudi Arabia prioritize durable, high-temperature-resistant terminations for harsh environments. Pioneer Power International and A-1 Electricals are expanding their presence to cater to these needs. Sub-Saharan Africa lags behind due to underdeveloped grid infrastructure and financing challenges, though rural electrification initiatives are gradually boosting demand. Strategic partnerships with global suppliers and localization efforts are expected to drive future growth.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Tubular Cable Termination markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Tubular Cable Termination market was valued at USD million in 2024 and is projected to reach USD million by 2032.

Segmentation Analysis: Detailed breakdown by product type (insulated and uninsulated), application (residential, commercial, industrial), and end-user industry to identify high-growth segments and investment opportunities.

Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. market size is estimated at USD million in 2024, while China is projected to reach USD million.

Competitive Landscape: Profiles of leading market participants including 3M, TE Connectivity, Brugg Kabel AG, and others, covering their product offerings, market share, and recent developments.

Technology Trends & Innovation: Assessment of emerging materials, manufacturing techniques, and evolving industry standards in cable termination technology.

Market Drivers & Restraints: Evaluation of factors driving market growth including infrastructure development and energy demand, along with challenges like raw material price volatility.

Stakeholder Analysis: Insights for cable manufacturers, electrical component suppliers, system integrators, and investors regarding the evolving market ecosystem.

Related Reports:https://semiconductorblogs21.blogspot.com/2025/06/inductive-proximity-switches-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/cellular-iot-module-chipset-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/sine-wave-inverter-market-shifts-in.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/pilot-air-control-valves-market-cost.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/video-multiplexer-market-role-in.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/semiconductor-packaging-capillary.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/screw-in-circuit-board-connector-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/wafer-carrier-tray-market-integration.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/digital-display-potentiometer-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/glass-encapsulated-ntc-thermistor.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/shafted-hall-effect-sensors-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/point-of-load-power-chip-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/x-ray-grating-market-key-players-and.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/picmg-single-board-computer-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/lighting-control-dimming-panel-market.html

0 notes

Text

Should You Invest in Ellenbarrie Industrial Gases IPO? Key Insights Revealed

The Indian IPO market has seen a surge in activity across various sectors, and industrial gases are no exception. One of the recent additions drawing investor attention is the Ellenbarrie Industrial Gases IPO. Known for its significant presence in the industrial gases sector, Ellenbarrie’s move to go public is a strategic step aimed at expansion, modernization, and unlocking value for stakeholders. But what makes this IPO noteworthy? Let’s dive into all the key details, investor takeaways, and expert insights.

About Ellenbarrie Industrial Gases

Ellenbarrie Industrial Gases Limited is a prominent manufacturer and supplier of industrial and medical gases across India. With decades of experience, the company has established a strong distribution network and serves industries ranging from steel and pharmaceuticals to electronics and food processing. Its core product portfolio includes oxygen, nitrogen, argon, and carbon dioxide, along with specialty gases tailored to specific industry needs.

The company's reputation for reliability, safety compliance, and customer-centric approach has helped it become a trusted name in eastern and southern India. The Ellenbarrie Industrial Gases IPO seeks to leverage this trust by raising funds to further expand operations and improve infrastructure.

Ellenbarrie Industrial Gases IPO Details

While the final dates and pricing are expected to be released shortly, the IPO is anticipated to include a combination of fresh issue and offer for sale (OFS) components. The fresh issue portion will be utilized primarily for capacity expansion, upgrading gas plants, and strengthening logistics capabilities.

Retail and institutional investors are keeping a close eye on the issue size, price band, and lot size, which will be announced in the official red herring prospectus. The Ellenbarrie Industrial Gases IPO could also see participation from anchor investors, reflecting broader market confidence in the industrial gases sector.

Why Is This IPO Gaining Attention?

There are several factors that make the Ellenbarrie Industrial Gases IPO attractive:

Essential Industry: Industrial gases are crucial to multiple sectors and show consistent demand, regardless of economic cycles.

Healthcare Demand: Post-COVID, the need for medical oxygen and gas infrastructure has surged, positioning companies like Ellenbarrie for long-term growth.

Growth Plans: The proceeds from the IPO are expected to be deployed in high-impact projects, boosting production efficiency and supply chain agility.

ESG Focus: The company has taken steps to reduce emissions and adopt cleaner technologies, aligning with global ESG trends.

Risks to Consider

While the Ellenbarrie Industrial Gases IPO offers significant upside potential, investors should consider certain risks:

Raw Material Costs: Fluctuations in electricity and energy prices can impact margins.

Regulatory Environment: Industrial gas handling is highly regulated, and non-compliance can lead to operational disruptions.

Market Competition: Players like Linde India and INOX Air Products present stiff competition, especially in urban and industrial hubs.

Investor Sentiment and Grey Market Buzz

Initial reactions from analysts and grey market watchers indicate positive sentiment. While it’s too early to comment on listing gains, the industry tailwinds and solid fundamentals are working in favor of the Ellenbarrie Industrial Gases IPO. If the GMP (grey market premium) continues to trend upward, it will likely generate significant interest from retail investors.

Final Thoughts

The Ellenbarrie Industrial Gases IPO represents an opportunity to invest in a vital and resilient sector of the Indian economy. With a proven business model, industry relevance, and well-defined growth strategy, Ellenbarrie has the potential to offer both stability and returns to its investors.

However, like all investments, one should not rely solely on market sentiment or GMP trends. A thorough analysis of the IPO prospectus, company financials, and risk factors is essential before making an informed investment decision.

Stay tuned as more details about the Ellenbarrie Industrial Gases IPO become available in the coming days.

0 notes

Link

0 notes

Text

Sheet Fed Paper Bag Machines

In the global push toward sustainable solutions, the paper bag industry has stepped into the spotlight. As consumer demand shifts from plastic to paper, manufacturers have embraced advanced machinery to meet market needs. Among the most transformative technologies is the sheet fed paper bag machine, a system designed to convert flat sheets of paper into eco-friendly bags with efficiency, precision, and speed.Get more news about sheet fed paper bag machine manufacture,you can vist our website!

Unlike roll-fed machines, sheet fed paper bag machines utilize pre-cut sheets rather than continuous paper rolls. This method offers several advantages: it allows for greater material control, better printing alignment, and more customized production runs. Particularly useful for boutique retailers, luxury packaging, and small to medium enterprises, sheet fed systems support flexibility without sacrificing performance.

How It Works

The process begins with loading stacks of printed or unprinted sheets into the feeder section. The machine then guides each individual sheet through a series of mechanical stages: gluing, folding, bottom forming, and gusseting. Advanced models also include inline printing, die-cut handles, and bottom pasting options, resulting in fully formed paper bags ready for distribution.

An important aspect of this equipment is automation. Modern sheet fed machines integrate PLC control systems, touchscreen interfaces, and automatic error detection features. These enhancements reduce manual labor, increase output, and minimize waste—making them ideal for eco-conscious manufacturers.

Benefits to Businesses and the Environment

Environmentally, the switch from plastic to paper bags is only meaningful if production itself is sustainable. Sheet fed paper bag machines typically accommodate recyclable kraft paper and water-based adhesives, minimizing environmental impact. What’s more, manufacturers can use paper made from responsibly managed forests or even recycled stock.

Economically, these machines reduce dependency on long material rolls, simplify logistics, and enable just-in-time production. Businesses can respond swiftly to small orders, seasonal packaging designs, or localized branding—all without committing to excessive inventory or waste.

Industry Applications

This technology finds application in several sectors: food and beverage (think bakery bags or takeout carriers), fashion retail, cosmetics, and even pharmaceuticals. The flexibility to adjust bag sizes, handle types, and printed content makes sheet fed machines suitable for a variety of branding needs.

With e-commerce growth driving demand for attractive and sustainable packaging, many firms are investing in in-house paper bag production. Sheet fed machines offer a compact footprint, making them ideal even for urban factories or decentralized workshops. For global brands seeking green credentials and fast turnarounds, this is a valuable investment.

Future Trends

As artificial intelligence, machine learning, and the Internet of Things (IoT) continue to influence industrial manufacturing, we can expect sheet fed paper bag machines to evolve. Smart sensors for real-time diagnostics, predictive maintenance, and energy-efficient motors will shape the next generation of machines.

Ultimately, as consumers become more environmentally aware and legislative pressure builds against single-use plastics, the role of the sheet fed paper bag machine becomes not just practical—but essential.

0 notes

Text

Why Wilden Pumps Are The Best For Viscous And Abrasive Fluid Handling

Air-operated double diaphragm (AODD) pumps are currently a standard in companies that need dependable, energy-efficient, and multitalented fluid handling. Wilden Pump is one of the top brands in the market that has the privilege of being a byword for innovation, build quality, and performance.

Overview of Wilden Pump

Wilden, the leader in AODD technology, has set industry standards since the company began. Wilden pumps can handle abrasive materials, high-viscosity slurries, chemicals, and water. The pumps range in size from 203 mm (8") to 6 mm (¼"). They can be used in many industrial applications and provide high flow rates along with operational flexibility.

Important attributes and advantages

Energy-efficient: Compared to other AODD technologies, Wilden's Pro-Flo SHIFT Air Distribution System (ADS) offers 34% higher flow rates and 60% energy savings. All of this means lower operating costs and also, generally doubles the MTBR, an advantage that leads to improved productivity overall.

Long-Term Construction: Wilden pumps can come with bolted and clamped types. Bolted types provide improved product containment with increased flow rates, whereas clamped types are appreciated for simplicity of installation and maintenance.

Flexibility: The mining, oil and gas, food and beverage, water and wastewater treatment, chemical processing, and biopharmaceutical industries all use the pumps extensively.

Handling Sensitive Products: Sensitive or shearing-prone fluids can be managed by the Wilden AODD pumps. They suit industries where product quality has to be preserved, including the food, beverage, and pharmaceutical sectors.

Self-running capability refers to Wilden pumps' capacity to self-prime and run dry without endangering themselves. This feature guarantees their reliability, even in tough working conditions.

Solids Handling: Certain models, such as the Stallion Series, are built to handle solid-charge slurries. They are therefore very useful in mining and other high-usage applications.

Uses in Various Industries

Numerous industries make use of wilden pumps:

Chemical processing: Apply the polymers to dosing, acid transferring, and solvent control.

Mining: The abrasion-resistant types are able to transfer abrasive slurries and heavy solids without plugging.

Food and Beverage: The Sanitary types are FDA, EHEDG, and 3A compliant for safe and sanitary product handling.

Oil and gas: You need reliable performance and strong containment for high-risk use.

Water and Wastewater: Made to improve the efficiency of treating fluids with abrasives or particles.

Why Choose Wilden Pump?

Wilden's dedication to the latest in technology is realized in its ongoing product improvements, including Chem-Fuse Diaphragm for leak protection and FIT metal pump series for flow efficiency and ease of maintenance. Years of demonstrated reliability, technical assistance, and full line of accessories to ensure pump performance form the foundation of their global reputation.

Conclusion

A globally recognized leader in the AODD technology, Wilden Pump offers heavy-duty, energy-efficient, and highly versatile solutions for nearly all fluid handling issues. Wilden pumps combine uncompromising reliability, operating efficiency, and ease of maintenance for demanding industrial applications or severe sanitary environments-which is why the first choice for companies whose pay for results and Peace of Mind.

0 notes

Text

#Global Distributed Energy Generation Systems Market Size#Share#Trends#Growth#Industry Analysis#Key Players#Revenue#Future Development & Forecast

0 notes

Text

The global Transformer Oil Market is projected to reach USD 3.0 billion in 2030 from USD 2.0 billion in 2023 at a CAGR of 5.9% according to a new report by MarketsandMarkets™.

#transformer#transformers#transformer oil market size#energy#power#electricity#power generation#utilities#electric utilities#renewable energy#oil and gas#transformer oil market 2021#transformer oil#transformer oil market#transformer oc#transformer manufacturers#power transformers#distribution transformer#power transformer#small transformers#electrical utilities#utilities industry#utility#power transmission#power distribution

0 notes

Text

Why Customized Lighting Solutions Are Popular in Bangalore

Bangalore, a city known for its vibrant architecture, tech-forward homes, and stylish interiors, is witnessing a significant shift in how people light up their spaces. More than ever before, homeowners, architects, and business owners are seeking lighting solutions that are tailored to their specific needs. Instead of settling for generic options, people are exploring unique lighting designs that match their layout, mood, and lifestyle. This rising demand has led to a boom in customized lighting solutions, easily found in any major decorative lights store in Bangalore. Combined with innovations from the best LED light companies, the city is embracing lighting as a form of personal and architectural expression.

But what exactly makes customized lighting solutions so popular in Bangalore today? Let’s explore.

1. Tailored to Interior Themes and Styles

Every home and office has a different layout, color palette, and architectural design. Customized lighting allows residents and designers to align fixtures with their interiors—whether it's a modern apartment, a classic villa, or a minimalistic office space. You can adjust size, finish, light temperature, and placement based on your exact vision.

2. Perfect Fit for Unconventional Layouts

Standard lighting fixtures may not always suit angled ceilings, long corridors, or split-level rooms. Customized solutions are designed to fit odd shapes and challenging layouts, ensuring that light distribution is even and aesthetically pleasing. This flexibility has made customized lighting especially appealing for homes in Bangalore where space and layout vary widely.

3. Greater Control Over Ambience and Mood

With customized lighting, homeowners can define how a room should feel—warm and cozy, bright and energetic, or soft and romantic. Working with the best LED light companies, many providers offer adjustable lighting features like color temperature control, dimming, and zoning, so you can adapt lighting to suit the time of day or activity.

4. Integration with Smart Lighting and Automation

Customization isn’t just about appearance—it’s also about function. Many custom lighting systems in Bangalore are now integrated with smart home technology. This includes app control, voice-activated commands, and scheduling features. Residents can set lighting scenes for reading, relaxing, or entertaining—all at the push of a button.

5. Wide Variety of Decorative Fixtures

Walk into a decorative lights store in Bangalore, and you’ll see everything from handcrafted chandeliers to artistic pendant lights and LED wall art. These stores cater to the demand for unique styles by offering customizable options, where customers can choose colors, finishes, and materials to suit their personal aesthetic.

6. Energy Efficiency with Modern LED Technology

Customization doesn’t mean compromising on performance. On the contrary, many tailored lighting systems use high-efficiency components from the best LED light companies, ensuring energy savings, long life, and reduced heat output. This combination of style and sustainability appeals to Bangalore’s eco-conscious residents.

7. Enhancing Property Value and Design Appeal

Custom lighting adds a high-end, curated look to homes and commercial spaces. It’s a simple way to elevate a property's appeal without major renovations. In the competitive Bangalore real estate and rental market, such unique features often make a lasting impression on visitors or potential buyers.

Conclusion

The growing popularity of customized lighting solutions in Bangalore is a result of changing lifestyles, evolving design preferences, and the availability of advanced LED technology. From functional upgrades to luxurious enhancements, tailored lighting is now a key part of how spaces are designed and experienced. With the creative range found in every decorative lights store in Bangalore and the innovation delivered by the best LED light companies, residents have more choices than ever to light up their world—exactly the way they envision it.

0 notes

Text

The Business Case for Volt VAR Management: Driving ROI

The global Volt VAR management market recorded a valuation of USD 481.0 million in 2023 and is predicted to reach USD 715.1 million by 2030, exhibiting a Compound Annual Growth Rate (CAGR) of 5.0% from 2024 to 2030. A key factor propelling this market is the escalating need for energy efficiency within power distribution systems. Utilities and grid operators are increasingly focused on reducing losses and optimizing voltage. VVM systems are instrumental in achieving this, enhancing the operational efficiency of electrical networks by optimizing reactive power and thereby minimizing energy wastage during transmission and distribution. This push for more environmentally friendly and efficient power systems, supported by various regulatory mandates and incentives, continues to fuel market demand.

Moreover, the increasing integration of renewable energy sources like solar and wind power into the grid introduces complex challenges for voltage and reactive power management. The inherently intermittent and variable nature of renewable energy generation can lead to voltage fluctuations and impact grid stability. Volt/VAR management technologies are vital for maintaining optimal voltage levels and ensuring a dependable power supply despite these variations. Consequently, the rising incorporation of renewables into the energy mix is a significant driver of overall product growth.

Key Market Trends & Insights

Regional Dominance: In 2023, North America held the leading position in the Volt/VAR management market, capturing a significant 39.9% of the total revenue. This leadership is largely attributed to the increasing adoption of VVM systems across the U.S. and Canada. These systems are crucial for reducing energy losses and enhancing grid reliability, especially as these nations integrate more renewable energy sources into their power grids.

Application Focus: The distribution segment emerged as the primary application area for Volt/VAR management in 2023, accounting for the largest revenue share of 68.1%. This segment is also anticipated to experience substantial growth throughout the forecast period, highlighting the critical role of VVM in optimizing power delivery to end-users.

Order a free sample PDF of the Volt VAR Management Market Intelligence Study, published by Grand View Research.

Market Size & Forecast

2023 Market Size: USD 481.0 Million

2030 Projected Market Size: USD 715.1 Million

CAGR (2024-2030): 5.0%

North America: Largest market in 2023

Key Companies & Market Share Insights

Leading the Volt VAR management market are key players such as ABB Ltd., Siemens AG, Schneider Electric, Eaton, and General Electric.

ABB Ltd., headquartered in Zurich, Switzerland, is a major manufacturer of electrification and automation products. Their extensive portfolio includes innovative products, services, and solutions for industries like energy, transportation, and manufacturing. For Volt/VAR management, ABB provides advanced grid automation solutions, transformers, and switchgear, all essential for optimizing voltage levels and reactive power within power distribution networks.

Siemens AG, a multinational conglomerate based in Munich, Germany, maintains a robust presence across industrial, energy, healthcare, and infrastructure sectors. Their offerings encompass a wide array of products and solutions, including smart grid technologies, digital substations, and comprehensive energy automation systems.

Several emerging participants are also making their mark in this market, including S&C Electric Company, DC Systems, Beckwith Electric, Utilidata, and Open Systems International.

S&C Electric Company, based in Chicago, Illinois, specializes in the design and manufacturing of switching and protection products for electric power transmission and distribution. The company is recognized for its solutions that significantly enhance grid reliability and operational efficiency. Their product lineup features voltage regulators, capacitor banks, and automation systems, all designed to assist utilities in effectively managing voltage and reactive power.

DC Systems focuses on developing software and hardware solutions specifically for utility and industrial markets, with a strong emphasis on digitalization and smart grid technologies. They provide advanced SCADA systems, sophisticated grid automation software, and comprehensive VVM solutions, enabling efficient grid management and optimized energy usage.

Key Players

ABB Ltd.

Siemens AG

S&C Electric Company

DC Systems

Beckwith Electric

Utilidata

Open Systems International

Landis+Gyr

Advanced Control Systems

Schneider Electric

Eaton

General Electric

Browse Horizon Databook for Global Volt Var Management Market Size & Outlook

Conclusion

The Volt/VAR management (VVM) market is on a growth trajectory, driven by the critical need for energy efficiency in power distribution and the increasing integration of renewable energy sources. These systems are vital for optimizing reactive power, minimizing energy wastage, and maintaining grid stability despite variable renewable generation. North America currently leads the market, with the distribution segment dominating applications. This upward trend is expected to continue, supported by ongoing grid modernization efforts and technological advancements from key industry players.

0 notes