#Educational loan with zero cost interest.

Text

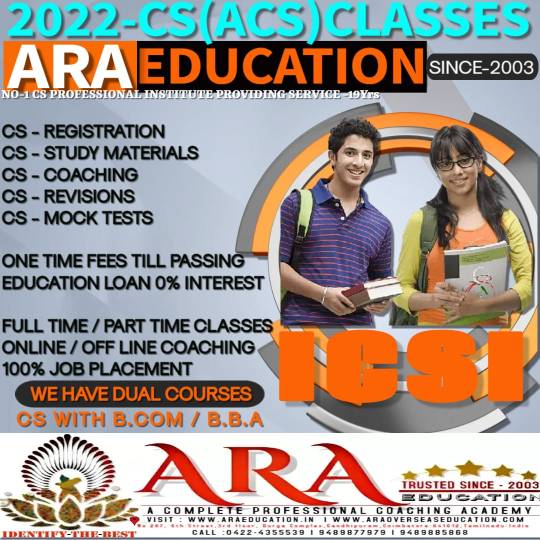

#ARA EDUCATION is the best CS coaching Institute for CSEET#CS EXEUTIVE#CS professional courses in coimbatore#Tamilnadu. Ara Education is the exclusive pioneer training academy for Company Secretary Course on ICSI. We provide coaching in online or#revision tests and finally mock test and model exam.#We are providing campus job placement for jobs and Articleship.#Educational loan with zero cost interest.#For more information#please call us @#+91 422 - 4355539 | 94 89 87 79 79 | 94 89 88 58 68 or#visit us @ www.araeducation.in#https://www.araeducation.in/cs-acs-coaching-classes#https://www.araeducation.in/cseet-coaching#https://www.araeducation.in/cs-executive-coaching#https://www.araeducation.in/cs-professional-coaching#acscoachingcoimbatore#cscoachingcoimbatore#bestcscoachingcoimbatore#bestacscoachingcoimbatore#cseetcoachingcoimbatore#csexecutivecoachingcoimbatore#csprofessionalcoachingcoimbatore#cseetcoachingtamilnadu

0 notes

Text

Why the Fed wants to crush workers

The US Federal Reserve has two imperatives: keeping employment high and inflation low. But when these come into conflict — when unemployment falls to near-zero — the Fed forgets all about full employment and cranks up interest rates to “cool the economy” (that is, “to destroy jobs and increase unemployment”).

An economy “cools down” when workers have less money, which means that the prices offered for goods and services go down, as fewer workers have less money to spend. As with every macroeconomic policy, raising interest rates has “distributional effects,” which is economist-speak for “winners and losers.”

Predicting who wins and who loses when interest rates go up requires that we understand the economic relations between different kinds of rich people, as well as relations between rich people and working people. Writing today for The American Prospect’s superb Great Inflation Myths series, Gerald Epstein and Aaron Medlin break it down:

https://prospect.org/economy/2023-01-19-inflation-federal-reserve-protects-one-percent/

Recall that the Fed has two priorities: full employment and low interest rates. But when it weighs these priorities, it does so through “finance colored” glasses: as an institution, the Fed requires help from banks to carry out its policies, while Fed employees rely on those banks for cushy, high-paid jobs when they rotate out of public service.

Inflation is bad for banks, whose fortunes rise and fall based on the value of the interest payments they collect from debtors. When the value of the dollar declines, lenders lose and borrowers win. Think of it this way: say you borrow $10,000 to buy a car, at a moment when $10k is two months’ wages for the average US worker. Then inflation hits: prices go up, workers demand higher pay to keep pace, and a couple years later, $10k is one month’s wages.

If your wages kept pace with inflation, you’re now getting twice as many dollars as you were when you took out the loan. Don’t get too excited: these dollars buy the same quantity of goods as your pre-inflation salary. However, the share of your income that’s eaten by that monthly car-loan payment has been cut in half. You just got a real-terms 50% discount on your car loan!

Inflation is great news for borrowers, bad news for lenders, and any given financial institution is more likely to be a lender than a borrower. The finance sector is the creditor sector, and the Fed is institutionally and personally loyal to the finance sector. When creditors and debtors have opposing interests, the Fed helps creditors win.

The US is a debtor nation. Not the national debt — federal debt and deficits are just scorekeeping. The US government spends money into existence and taxes it out of existence, every single day. If the USG has a deficit, that means it spent more than than it taxed, which is another way of saying that it left more dollars in the economy this year than it took out of it. If the US runs a “balanced budget,” then every dollar that was created this year was matched by another dollar that was annihilated. If the US runs a “surplus,” then there are fewer dollars left for us to use than there were at the start of the year.

The US debt that matters isn’t the federal debt, it’s the private sector’s debt. Your debt and mine. We are a debtor nation. Half of Americans have less than $400 in the bank.

https://www.fool.com/the-ascent/personal-finance/articles/49-of-americans-couldnt-cover-a-400-emergency-expense-today-up-from-32-in-november/

Most Americans have little to no retirement savings. Decades of wage stagnation has left Americans with less buying power, and the economy has been running on consumer debt for a generation. Meanwhile, working Americans have been burdened with forms of inflation the Fed doesn’t give a shit about, like skyrocketing costs for housing and higher education.

When politicians jawbone about “inflation,” they’re talking about the inflation that matters to creditors. Debtors — the bottom 90% — have been burdened with three decades’ worth of steadily mounting inflation that no one talks about. Yesterday, the Prospect ran Nancy Folbre’s outstanding piece on “care inflation” — the skyrocketing costs of day-care, nursing homes, eldercare, etc:

https://prospect.org/economy/2023-01-18-inflation-unfair-costs-of-care/

As Folbre wrote, these costs are doubly burdensome, because they fall on family members (almost entirely women), who have to sacrifice their own earning potential to care for children, or aging people, or disabled family members. The cost of care has increased every year since 1997:

https://pluralistic.net/2023/01/18/wages-for-housework/#low-wage-workers-vs-poor-consumers

So while politicians and economists talk about rescuing “savers” from having their nest-eggs whittled away by inflation, these savers represent a minuscule and dwindling proportion of the public. The real beneficiaries of interest rate hikes isn’t savers, it’s lenders.

Full employment is bad for the wealthy. When everyone has a job, wages go up, because bosses can’t threaten workers with “exile to the reserve army of the unemployed.” If workers are afraid of ending up jobless and homeless, then executives seeking to increase their own firms’ profits can shift money from workers to shareholders without their workers quitting (and if the workers do quit, there are plenty more desperate for their jobs).

What’s more, those same executives own huge portfolios of “financialized” assets — that is, they own claims on the interest payments that borrowers in the economy pay to creditors.

The purpose of raising interest rates is to “cool the economy,” a euphemism for increasing unemployment and reducing wages. Fighting inflation helps creditors and hurts debtors. The same people who benefit from increased unemployment also benefit from low inflation.

Thus: “the current Fed policy of rapidly raising interest rates to fight inflation by throwing people out of work serves as a wealth protection device for the top one percent.”

Now, it’s also true that high interest rates tend to tank the stock market, and rich people also own a lot of stock. This is where it’s important to draw distinctions within the capital class: the merely rich do things for a living (and thus care about companies’ productive capacity), while the super-rich own things for a living, and care about debt service.

Epstein and Medlin are economists at UMass Amherst, and they built a model that looks at the distributional outcomes (that is, the winners and losers) from interest rate hikes, using data from 40 years’ worth of Fed rate hikes:

https://peri.umass.edu/images/Medlin_Epstein_PERI_inflation_conf_WP.pdf

They concluded that “The net impact of the Fed’s restrictive monetary policy on the wealth of the top one percent depends on the timing and balance of [lower inflation and higher interest]. It turns out that in recent decades the outcome has, on balance, worked out quite well for the wealthy.”

How well? “Without intervention by the Fed, a 6 percent acceleration of inflation would erode their wealth by around 30 percent in real terms after three years…when the Fed intervenes with an aggressive tightening, the 1%’s wealth only declines about 16 percent after three years. That is a 14 percent net gain in real terms.”

This is why you see a split between the one-percenters and the ten-percenters in whether the Fed should continue to jack interest rates up. For the 1%, inflation hikes produce massive, long term gains. For the 10%, those gains are smaller and take longer to materialize.

Meanwhile, when there is mass unemployment, both groups benefit from lower wages and are happy to keep interest rates at zero, a rate that (in the absence of a wealth tax) creates massive asset bubbles that drive up the value of houses, stocks and other things that rich people own lots more of than everyone else.

This explains a lot about the current enthusiasm for high interest rates, despite high interest rates’ ability to cause inflation, as Joseph Stiglitz and Ira Regmi wrote in their recent Roosevelt Institute paper:

https://rooseveltinstitute.org/wp-content/uploads/2022/12/RI_CausesofandResponsestoTodaysInflation_Report_202212.pdf

The two esteemed economists compared interest rate hikes to medieval bloodletting, where “doctors” did “more of the same when their therapy failed until the patient either had a miraculous recovery (for which the bloodletters took credit) or died (which was more likely).”

As they document, workers today aren’t recreating the dread “wage-price spiral” of the 1970s: despite low levels of unemployment, workers wages still aren’t keeping up with inflation. Inflation itself is falling, for the fairly obvious reason that covid supply-chain shocks are dwindling and substitutes for Russian gas are coming online.

Economic activity is “largely below trend,” and with healthy levels of sales in “non-traded goods” (imports), meaning that the stuff that American workers are consuming isn’t coming out of America’s pool of resources or manufactured goods, and that spending is leaving the US economy, rather than contributing to an American firm’s buying power.

Despite this, the Fed has a substantial cheering section for continued interest rates, composed of the ultra-rich and their lickspittle Renfields. While the specifics are quite modern, the underlying dynamic is as old as civilization itself.

Historian Michael Hudson specializes in the role that debt and credit played in different societies. As he’s written, ancient civilizations long ago discovered that without periodic debt cancellation, an ever larger share of a societies’ productive capacity gets diverted to the whims of a small elite of lenders, until civilization itself collapses:

https://www.nakedcapitalism.com/2022/07/michael-hudson-from-junk-economics-to-a-false-view-of-history-where-western-civilization-took-a-wrong-turn.html

Here’s how that dynamic goes: to produce things, you need inputs. Farmers need seed, fertilizer, and farm-hands to produce crops. Crucially, you need to acquire these inputs before the crops come in — which means you need to be able to buy inputs before you sell the crops. You have to borrow.

In good years, this works out fine. You borrow money, buy your inputs, produce and sell your goods, and repay the debt. But even the best-prepared producer can get a bad beat: floods, droughts, blights, pandemics…Play the game long enough and eventually you’ll find yourself unable to repay the debt.

In the next round, you go into things owing more money than you can cover, even if you have a bumper crop. You sell your crop, pay as much of the debt as you can, and go into the next season having to borrow more on top of the overhang from the last crisis. This continues over time, until you get another crisis, which you have no reserves to cover because they’ve all been eaten up paying off the last crisis. You go further into debt.

Over the long run, this dynamic produces a society of creditors whose wealth increases every year, who can make coercive claims on the productive labor of everyone else, who not only owes them money, but will owe even more as a result of doing the work that is demanded of them.

Successful ancient civilizations fought this with Jubilee: periodic festivals of debt-forgiveness, which were announced when new monarchs assumed their thrones, or after successful wars, or just whenever the creditor class was getting too powerful and threatened the crown.

Of course, creditors hated this and fought it bitterly, just as our modern one-percenters do. When rulers managed to hold them at bay, their nations prospered. But when creditors captured the state and abolished Jubilee, as happened in ancient Rome, the state collapsed:

https://pluralistic.net/2022/07/08/jubilant/#construire-des-passerelles

Are we speedrunning the collapse of Rome? It’s not for me to say, but I strongly recommend reading Margaret Coker’s in-depth Propublica investigation on how title lenders (loansharks that hit desperate, low-income borrowers with triple-digit interest loans) fired any employee who explained to a borrower that they needed to make more than the minimum payment, or they’d never pay off their debts:

https://www.propublica.org/article/inside-sales-practices-of-biggest-title-lender-in-us

[Image ID: A vintage postcard illustration of the Federal Reserve building in Washington, DC. The building is spattered with blood. In the foreground is a medieval woodcut of a physician bleeding a woman into a bowl while another woman holds a bowl to catch the blood. The physician's head has been replaced with that of Federal Reserve Chairman Jerome Powell.]

#pluralistic#worker power#austerity#monetarism#jerome powell#the fed#federal reserve#finance#banking#economics#macroeconomics#interest rates#the american prospect#the great inflation myths#debt#graeber#michael hudson#indenture#medieval bloodletters

465 notes

·

View notes

Text

Pat Bagley, Salt Lake Tribune

* * * *

LETTERS FROM AN AMERICAN

January 19, 2024

HEATHER COX RICHARDSON

JAN 19, 2024

President Joe Biden today signed the continuing resolution that will keep the government operating into March.

Meanwhile, the stock market roared as two of the three major indexes hit new record highs. The S&P 500, which measures the value of 500 of the largest companies in the country, and the Dow Jones Industrial Average, which does the same for 30 companies considered to be industry leaders, both rose to all-time highs. The third major index, the Nasdaq Composite, which is weighted toward technology stocks, did not hit a record high, although its 1.7% jump was higher than that of the S&P 500 (1.2%) or the Dow (1.1%).

Investors appear to be buoyed by the fact the rate of inflation has come down in the U.S. and by news that consumers are feeling better about the economy. A report out today by Goldman Sachs Economics Research noted that consumer spending is strong and predicted that “job gains, positive real wage growth, will lead to around 3% real disposable income growth” and that “household balance sheets have strengthened.” It also noted that “[t]he US has led the way on disinflation,” and it predicted further drops in 2024. That will likely mean the sort of interest rate cuts the stock market likes.

The economic policies of the Biden-Harris administration have also benefited workers. The unemployment rate has been under 4% for more than two years, and wages have risen higher than inflation in that same period. Production is up as well, to 4.9% in the third quarter of 2023 (the U.S. growth rate under Trump even before the pandemic was 2.5%).

The administration has worked to end some of the most obvious financial inequities in the U.S., such as the unexpected “junk fees” tacked on to airline or concert tickets, or to car or apartment rentals. On Wednesday the Consumer Financial Protection Bureau announced a proposed rule for bank overdraft fees at banks that have more than $10 billion in assets.

While banks now can charge what they wish if a customer’s balance falls below zero, the proposed rule would allow them to charge no more than what it cost them to break even on providing overdraft services or, alternatively, an industry-wide fee that reflects the amount it costs to deal with overdrafts: $3, $6, $7, or $14. The amount will be established after a public hearing period.

Ken Sweet and Cora Lewis of the Associated Press note that while the average overdraft is $26.61, some banks charge as much as $39 per overdraft. The CFPB estimates that in the past 20 years, banks have collected more than $280 billion in overdraft fees. (One bank’s chief executive officer named his boat “Overdraft.”) Over the past two years, pressure has made banks cut back on their fees and they now take in about $8 billion a year from those overdraft fees.

Bankers say regulation is unnecessary and will force them to end the overdraft service, pushing people out of the banking system. Biden said that the rule would save U.S. families $3.5 billion annually.

The administration has also addressed the student loan crisis by reexamining the loan histories of student borrowers. An NPR investigation led by Cory Turner revealed that banks mismanaged loans, denying borrowers the terms under which they had signed on to them. Rather than honoring the government’s promise that so long as a borrower paid what the government thought was reasonable on a loan for 20 or 25 years (undergrad or graduate), the debt would be forgiven, banks urged borrowers to put the loan into “forbearance,” under which payments paused but the debt continued to accrue interest, making the amount balloon.

The Education Department has been reexamining all those old loans to find this sort of mismanagement as well as other problems, like borrowers not getting credit for payments to count toward their 20 years of payments, or borrowers who chose public service not receiving the debt relief they were promised.

Today the administration announced $4.9 billion of student debt cancellation for almost 74,000 borrowers. That brings the total of borrowers whose debt has been canceled to 3.7 million Americans, with an erasure of $136.6 billion. Nearly 30,000 of today’s relieved borrowers had been in repayment for at least 20 years but never got the relief they should have; nearly 44,000 had earned debt forgiveness after 10 years of public service as teachers, nurses, and firefighters.

Biden has been traveling the country recently, touting how the economic policies of the Biden-Harris administration have benefited ordinary Americans. In Emmaus, Pennsylvania, last Friday he visited a bicycle shop, a running shoe store, and a coffee shop to emphasize how small businesses are booming under his administration: in the three years since he took office, there have been 16 million applications to start new businesses, the highest number on record.

Biden was in Raleigh, North Carolina, yesterday to announce another $82 million in support for broadband access, bringing the total of government infrastructure funding in North Carolina during the Biden administration to $3 billion.

On social media, the administration compared its investments in the American people to those of President Franklin Delano Roosevelt’s New Deal in the 1930s, which were enormously popular.

They were popular, that is, until those opposed to business regulation convinced white voters that the government’s protection of civil rights, which came along with its protection of ordinary Americans through regulation of business, provision of a basic social safety net, and promotion of infrastructure, meant redistribution of white tax dollars to undeserving Black people.

The same effort to make sure that ordinary Americans don’t work together to restore basic fairness in the economy and rights in society is visible now in the attempt to attribute a recent Boeing airplane malfunction, in which a door panel blew off mid-flight, to diversity, equity, and inclusion (DEI) efforts. Tesnim Zekeria at Popular Information yesterday chronicled how that accusation spread across the right-wing ecosystem and onto the Fox News Channel, where Fox Business host Sean Duffy warned: “This is a dangerous business when you’re focused on DEI and maybe less focused on engineering and safety.”

As Zekeria explains, “this narrative has no basis in fact.” Neither Boeing nor its supplier, Spirit AeroSystems, is particularly diverse, either at the workforce level, where minorities make up 35% of Boeing employees and 26% of those at Spirit AeroSystems, or on the corporate ladder, where the overwhelming majority of executives are white men. Zekeria notes that right-wing media figures have also erroneously blamed last year’s train derailment in Ohio and the collapse of the Silicon Valley Bank on DEI initiatives.

The real culprit at Boeing, Zekeria suggests, was the weakened regulations on Boeing and Spirit thanks to more than $65 million in lobbying efforts.

Perhaps an even more transparent attempt to keep ordinary Americans from working together is the attacks former Fox News Channel personality Tucker Carlson has launched against Vice President Kamala Harris, calling her “a member of the new master race” who “must be shown maximum respect at all times, no matter what she says or does.” Philip Bump of the Washington Post noted yesterday that this construction suggests that Harris, who identifies as both Black and Indian, represents all nonwhite Americans as a united force opposed to white Americans.

But Harris’s actions actually represent something else altogether. She has crossed the country since June 2022, when the Supreme Court overturned the 1973 Roe v. Wade decision that recognized the constitutional right to abortion, talking about the right of all Americans to bodily autonomy. That the Supreme Court felt able to take away a constitutional right has worried many Americans about what they might do next, and people all over the country have been coming together in opposition to the small minority that appears to have taken over the levers of our democracy.

Driving the wedge of racism into that majority coalition seems to be a desperate attempt to stop ordinary Americans from taking back control of the country.

LETTERS FROM AN AMERICAN

HEATHER COX RICHARDSON

#Letters from An American#Heather Cox Richardson#US Economy#Kamala Harris#reproductive rights#women's rights#income inequality#student loans#stock market

10 notes

·

View notes

Note

You’re retarded if you think getting rid of interest on student loans is a bad idea. You clearly have no fucking idea how student loans work. There are so many people who never miss payments yet their debt increases due to interest! FUCK YOU ASSHOLE

Unfortunately, you are incorrect.

The reason people's student loan balances increase is due to them:

Choosing an alternate repayment plan than the default repayment plan (10 year fixed payments)

Paying less than the interest amount; i.e. also less than the principal amount, so even if interest were 0, they couldn't afford the loan's standard terms.

To put it in perspective,

The average borrower takes out $29k~.

The Federal Stafford interest rate for 2020-2021 (before they were put into forbearance) was 2.75%.

That puts them at a default repayment schedule for $277/month for 10 years.

Alternatively, if you removed interest it would become $241/month for 10 years. Is there a segment of borrowers who can afford $241, but not $277? Sure, but it's hardly a significant portion to be a viable solution.

Furthermore, the bigger issue with a zero-interest policy is due to the fact that it would basically be used as alternative financing and disincentives repayment, plus from an investment standpoint, it would effectively be resulting in a negative direct return. This doesn't even take into consideration the root cause of the problem though, which is the drastic rising cost of higher education and is heavily correlated to the accessibility of funding (i.e. this would lead to even greater costs, in turn leading to greater total borrowed amounts).

133 notes

·

View notes

Note

Popping in as a super-duper anonymous anon for this one because internships as part of education are just so complicated. I fully, completely understand where that anon is coming from and I can’t say I disagree.

But also, it’s so much harder than that.

I’m a pharmacist. The last year of schooling for a PharmD degree (what most US pharmacists under age…50 or so will have outside of a research setting) is 45 weeks of practical rotations.

I learned a shit-ton in those 45 weeks, and they were absolutely necessary for my education.

They also cost me $20k at my low-rent state school, and I’m pretty sure I wasn’t even allowed to work? Like, my university actively discouraged (forbade?) us from doing so because we were required to work 40 hour weeks for our internships.

So instead, I went twenty (additional) grand into debt and my newlywed husband and I signed up for a credit card that had zero percent interest for the first year so that we could just pay the minimum and carry the debt until I started my adult job. I have no idea how other people without fully employed partners made it through that year. They probably worked anyway, or else took out some hefty personal loans to live on. I definitely cried on my way to work more than once knowing how broke I was, though.

i'm just going to leave this here.

but also, i just want to say how much of a systemic issue this is?? and its a much much bigger conversation than just "i wish people with degrees also had experience working at some point!"

because SAME. but fields like medicine, law, education actively DISCOURAGE students from working while attending school, especially in higher ed by making their workloads and courseloads a certain way. and its largely because of who they want in higher ed and who they don't. There is a REASON academia and higher ed (I'm looking at YOU med-school) is made so rigorous and its to prevent certain folk from obtaining higher degrees. You can @ me all you want about this, but like...I'm not wrong.

so when your company is hiring people who have x amount of degrees instead of people with experience...we can think about that too, yeah?

however, i WILL say i think the education system IS responsible for:

creating sustainable curriculum that promotes diversity amongst grad students and is student centered (not university-centered)

creating policies within universities that also support this (i am looking at you, punitive attendance policies that literally drop students if they miss two classes for "inexcusable reasons". guess what isn't excused? having to work a shift at a job.)

diversifying their course material and implementing experiential and interactive methods of teaching IN the classroom that can provide students opportunities to experiment and learn and reflect on.

11 notes

·

View notes

Text

Robert F Kennedy Jr Policies

As president, one of Robert F. Kennedy Jr.’s top priorities will be to dissolve the corrupt merger of state and corporate power. That means freeing government agencies from the control of big corporations.

Install honest, competent leadership throughout the federal bureaucracy, agency by agency

Root out corruption and replace corporate-friendly agency leaders with reformers and whistleblowers dedicated to the national interest.

Shut the revolving door by executive order with a five year ban on administration officials lobbying their former government agency.

Make the agencies transparent to public view, so that the American people can once again have faith that their government works for them — not big corporations.

Raise the minimum wage to $15, which is the equivalent to its 1967 level.

Prosecute union-busting corporations so that labor can organize and negotiate fair wages.

Expand free childcare to millions of families with programs like that pioneered by the state of New Mexico.

Drop housing costs by $1000 per family and make home ownership affordable by backing 3% home mortgages with tax-free bonds.

Cut energy prices by restricting natural gas exports.

Support small businesses by redirecting regulatory scrutiny onto large corporations.

Secure the border and bring illegal immigration to a halt, so that undocumented migrants won’t undercut wages.

Negotiate trade deals that prevent low-wage countries from competing with American workers in a “race to the bottom.”

Rein in military spending and use the resources to fund infrastructure, health care, higher education, child care, and domestic prosperity.

Reverse the chronic disease epidemic that is a $3.7 trillion drag on families and the American economy.

Clean out the corruption in Washington, D.C., which funnels so much of our nation’s wealth to giant corporations and billionaires.

Establish addiction healing centers on organic farms across the country.

Make student debt dischargeable in bankruptcy and cut interest rates on student loans to zero.

Cut drug costs by half to bring them in line with other nations.

Tax-free 3% government-backed mortgage bonds, to bring the mortgage interest rate back to 2019 levels and even lower

Bring derelict land and buildings back online. Many cities have thousands of vacant lots and buildings that have been seized for tax arrears or other reasons. The Kennedy administration will incentivize local governments to bring city-owned land and buildings back onto the market.

As President, Robert F. Kennedy, Jr. will start the process of unwinding empire. We will bring the troops home. We will stop racking up unpayable debt to fight one war after another. The military will return to its proper role of defending our country. We will end the proxy wars, bombing campaigns, covert operations, coups, paramilitaries, and everything else that has become so normal most people don’t know it’s happening. But it is happening, a constant drain on our strength. It’s time to come home and restore this country.

In Ukraine, the most important priority is to end the suffering of the Ukrainian people, victims of a brutal Russian invasion, and also victims of American geopolitical machinations going back at least to 2014. We must first get clear: Is our mission to help the brave Ukrainians defend their sovereignty? Or is it to use Ukraine as a pawn to weaken Russia? Kennedy will choose the first. He will find a diplomatic solution that brings peace to Ukraine and brings our resources back where they belong. We will offer to withdraw our troops and nuclear-capable missiles from Russia's borders. Russia will withdraw its troops from Ukraine and guarantee its freedom and independence. UN peacekeepers will guarantee peace to the Russian-speaking eastern regions. We will put an end to this war. We will put an end to the suffering of the Ukrainian people. That will be the start of a broader program of demilitarization of all countries.

We have to stop seeing the world in terms of enemies and adversaries. As John Quincy Adams wrote, “Americans go not abroad in search of monsters to destroy.” Kennedy will revive a lost thread of American foreign policy thinking, the one championed by his uncle, John F. Kennedy who, over his 1000 days in office, had become a firm anti-imperialist. He wanted to exit Vietnam. He defied the Joint Chiefs of Staff and refused to bomb Cuba, thus saving us from nuclear Armageddon. He wanted to reverse the imperialistic policies of Truman and Eisenhower, rein in the CIA, and support freedom movements around the world. He wanted to revive Roosevelt’s impulse to dissolve the British empire rather than take it over.

John F. Kennedy’s vision was tragically cut short by an assassin’s bullet. But now we have another chance. The country is ailing, yes, but underneath there is vitality still. America is a land rich in resources, creativity, and intelligence. We just need to get serious about healing our society, to become strong again from the inside.

America was once an inspiration to the world, a beacon of freedom and democracy. Our priority will be nothing less than to restore our moral leadership. We will lead by example. When a warlike imperial nation disarms of its own accord, it sets a template for peace everywhere. It is not too late for us to voluntarily let go of empire and serve peace instead, as a strong and healthy nation.

Zoning changes. We will encourage municipalities to change zoning laws to allow ancillary dwelling units (granny flats) on more properties, to make housing available, bring families together, and provide homeowners with rental income. More supply means lower prices.

Tax code changes. Small changes to the tax code can make corporate investments in single-family homes uneconomic. For example, we can change business depreciation rules and reform the “enterprise zones” that have contributed so much to gentrification.

control over the border. We will use technology that was installed at the border then dismantled by the Biden administration, such as cameras, lights, and motion detectors, coupled with physical barriers in key areas (there is no need to build a wall across the entire 2,000-mile border). We have the technology to prevent people from getting through undetected. We can control the border. We have the technology. We can deploy the personnel. All we need is the will.

Get on top of asylum claims. We have to fully fund courts, services, and border agencies to allow lawful immigration in accordance with U.S. law and deny non-compliant access, and appoint more judges to handle asylum cases. There are woefully few asylum judges to process even the legitimate claims of political refugees. If claimants of political asylum knew their case would be heard swiftly, and that specious claims would be met with swift deportation, the cartels’ business model would fail.

Abortion is one of the most divisive issues in American politics. We’ve been offered two positions — pro-life and pro-choice — with hardly any room between or outside them. This wedge issue keeps Americans fighting with each other and destroys our most promising alliances. Robert F. Kennedy Jr.’s policy won’t end the debate, but it offers a way forward that most Americans can support. It is called “More Choices, More Life.”

Robert F. Kennedy Jr. is a medical freedom advocate and supports a woman’s right to choose until a fetus is viable. At the same time, Kennedy’s policy will dramatically reduce abortion in our country, and it will do so by offering more choices for women and families, not less.

Mr. Kennedy will defend these worker’s rights:The right to organize.The right to collective bargaining.The right to strike.The right to meaningful wages and benefits, which includes a significant increase to the minimum wage .The right to a healthy and safe workplace with appropriate working conditions.The right to compensation if injured on the job.The right to a dignified and secure retirement.

Global Leadership: Keep America a world leader in blockchain development by ending unjust legal prosecution against developers of open-source software.

Right to Privacy: Guarantee financial freedom including the right to self-custody, peer-to-peer transactions, and freedom from financial surveillance or censorship.

Thoughtful Regulation: End the politically motivated regulatory assault on financial services providers seeking to operate in the crypto-sector and create a regulatory environment designed to expand, not limit, the adoption of blockchain technologies.

Incentivizing Development: Encourage and normalize the adoption of bitcoin as a free-market, rules-based collaboration network that promotes voluntary exchange and global economic development.

Promote Peace: Recognize that bitcoin is a helpful tool for diminishing the power of the military industrial complex and can serve as an ambassador for American values like free speech, strong property rights and open capital markets all over the world.

Keeping Government Honest: Promote transparency and reign in public corruption by implementing a blockchain-based solution to track and monitor all federal budget expenditures.

Building a Strategic Reserve: Stop liquidating all bitcoin held by the U.S. Government and instead continue building a strategic reserve that can be used to back the U.S. Dollar and curtail the inflationary impact of fiat money printing.

Incentivizing Clean Energy: Create incentives for bitcoin miners who operate using renewable energy sources or who can mitigate methane emissions.

Fixing Unfair Tax Regimes: Recognize cryptocurrency as a currency, not an asset. End the treatment of de-minimis Bitcoin transactions as taxable events.

Preventing a CBDC: Never allow the U.S. to adopt a CBDC (Central Bank Digital Currency), which can be used as an instrument of totalitarian control over the American people.

Uproot the influence of Big Pharma and Wall Street firms that are heavily invested in the medical industry from medical regulatory agencies.

Transition from a toxic, degenerative industrial food system to an organic, regenerative system of agriculture.

Start a national fitness program like the one his uncle, JFK, implemented.

End the corporate capture of environmental regulatory agencies, including the EPA, USDA, DOI, DOE, USFWS, and USFS.

Reduce toxic chemical pollution and plastic waste.

Protect forests, rivers, fisheries, and wildlife habitats from corporate abuse.

Adopt a wildfire management plan to keep forests resilient and communities safe.

Stop big corporations and corrupt government officials who are using the environment as an excuse for profit-making schemes and power grabs.

All of his policies are in this link: https://www.kennedy24.com/policies

Robert Kennedy Jr is the only candidate who is willing to fight the system and end this nation divide. He has a huge chance of winning the election id we can get out of the whole ‘spoils candidate’ since most people are independent.

Kennedy 2024 🇺🇸🇺🇸🇺🇸🇺🇸

#AmericaStrong

Down with the Two Party System, both parties failed us.

0 notes

Text

<img src="https://lh3.googleusercontent.com/drive-storage/AJQWtBNj0ugQqRMkfwiCYV6P8_xCK4lS9nrxE0h9_UYhchC7wF3Qwy3453LGuA516mIvYIBSPBYxd8lcEdYad0iPDpuKfqgzaXgYdJMFQC5l165qCw=s700"> Mastering NJ Mortgage Rates: 2024 Homebuyer's Essential Guide

The real estate market remains highly competitive as we approach 2024, with mortgage rates playing a crucial role in homebuyers' decisions. Staying informed about mortgage rate trends and understanding financing options is essential for New Jersey homebuyers. According to recent forecasts, the average 30-year fixed mortgage rate should hover around [XX.XX]% in 2024. Monitoring these changes helps buyers make educated decisions and secure the most advantageous deals available.

Comparing Mortgage Rates

Securing the most favorable mortgage rate requires careful research and strategic comparisons. Here’s a step-by-step guide to ease your efforts: Research Multiple Lenders: Expand your search to include both local and national lenders. Some of the top mortgage lenders in New Jersey include Wells Fargo, Quicken Loans, and loanDepot. Request Personalized Quotes: Contact your selected lenders for tailored mortgage rate quotes based on your specific financial situation, including credit score, down payment, and loan amount. Compare Rates and Fees: Evaluate each quote by comparing the interest rates, annual percentage rates (APRs), and closing costs. A lower interest rate might not be the best choice if the associated fees are exceptionally high. Negotiate Terms: Don’t shy away from negotiating your mortgage terms. With some negotiation, you may secure a better interest rate or reduced fees.

Understanding Financing Options

Choosing the appropriate financing option is vital for homebuyers. Here are some popular choices along with their unique features:

Fixed-rate Mortgages: Provide a fixed interest rate and consistent monthly payments throughout the loan term, offering predictability.

Adjustable-rate Mortgages (ARMs): Feature initially lower rates that can adjust over time based on market conditions, beneficial if you plan to sell or refinance before rates adjust.

FHA Loans: Insured by the Federal Housing Administration, these loans have lower down payment requirements and lenient credit standards, perfect for first-time buyers and those with lower credit scores.

VA Loans: Available to eligible veterans, military members, and surviving spouses. VA loans offer competitive rates, no down payment, and lower closing costs.

USDA Loans: Offered by the U.S. Department of Agriculture, these loans assist rural and suburban homebuyers with low to moderate incomes, providing zero down payment and competitive interest rates.

Here's a quick comparison table to help you understand the key differences:

Loan Type Interest Rate Down Payment Eligibility Fixed-rate Consistent 5-20% General ARMs Initially low, adjustable 5-20% General FHA Varies 3.5% First-time buyers, low credit scores VA Competitive None Veterans, military members USDA Competitive None Rural/suburban, low to moderate income

Gathering Necessary Documentation

Preparing for your mortgage application involves assembling essential documents to expedite the process. Ensure you have:

Photo ID

Social Security numbers

W-2 forms or tax returns from the past two years

Pay stubs from the past 30 days

Bank statements from the past two months

Proof of other income sources

Credit history reports

Purchase agreement

Home appraisal and inspection reports

Navigating Mortgage Rates and Financing Options

Successfully navigating mortgage rates and financing options in 2024 necessitates strategy and foresight:

Monitor Rate Trends: Regularly check mortgage rate trends to identify the optimal time for applying.

Compare Rates and Fees: Review multiple lenders to ensure you secure the most favorable rate and terms.

Explore Financing Options: Determine which type of financing best suits your financial situation.

Prepare Your Documents: Gather all necessary documentation in advance to streamline the application process.

Consider a Broker: Working with a mortgage broker can simplify the process and provide access to a broad range of lending options.

By remaining informed and prepared, New Jersey homebuyers can confidently navigate the mortgage landscape in 2024, securing the best possible financing for their dream homes. #MortgageRates #HomeBuying #NewJersey #HomeLoans #RealEstate2024 Don't wait on favorable rates! Explore your financing options at https://www.kvibe.com/blog-posts/navigating-new-jersey-mortgage-rates-2024

0 notes

Text

HDFC Overdraft : Your Key to Financial Fluidity

HDFC Overdraft:

HDFC Bank, a trusted name in the financial sector, extends its expertise through Overdraft Services, providing customers with a reliable source of funds when they need it the most. But what exactly is an overdraft?

An overdraft is a credit facility that allows individuals or businesses to withdraw funds from their account even if the hdfc bank overdraft interest rate in their balance reaches zero or goes into negative territory. It serves as a cushion against unexpected expenses or temporary cash shortages, offering a convenient way to manage liquidity without disrupting financial plans.

Overdraft Loan HDFC:

One of the key offerings under HDFC's Overdraft Services is the Overdraft Loan. This financial tool empowers individuals and businesses to access funds beyond their account balance, up to a predetermined limit. Whether it's for expanding a business, funding education expenses, or managing medical emergencies, the HDFC Overdraft Loan provides the necessary financial support with minimal hassle.

HDFC OD Loan Interest Rates

Interest rates play a crucial role in determining the cost of borrowing, and HDFC ensures competitive rates to make borrowing affordable for its customers. The HDFC OD Loan interest rates are designed to be competitive, offering value for money while ensuring financial feasibility. By providing transparent and competitive interest rates, HDFC enables customers to make informed borrowing decisions without worrying about hidden costs.

HDFC Bank Overdraft Facility

With HDFC Bank's Overdraft Facility, customers gain access to a wide range of benefits beyond just the funds. Convenience, flexibility, and reliability are at the core of this offering, ensuring that customers can meet their financial obligations with ease. Whether it's withdrawing funds, making payments, or managing transactions, HDFC's Overdraft Facility simplifies financial management, allowing customers to focus on what matters most.

HDFC Overdraft Against FD

For customers looking to leverage their Fixed Deposits (FDs) to access additional funds, HDFC offers the option of Overdraft Against FD. This innovative solution allows individuals to maintain their FD investments intact while unlocking liquidity as and when needed. By pledging their FD as collateral, customers can access funds at attractive interest rates, ensuring that their investments continue to work for them even during financial emergencies.

HDFC Overdraft Eligibility

While the benefits of HDFC's Overdraft Services are undeniable, eligibility criteria play a crucial role in determining who can avail of these services. Factors such as credit history, income stability, and relationship with the bank are taken into consideration when assessing eligibility. By maintaining a healthy financial profile and fulfilling the necessary requirements, customers can maximize their chances of accessing HDFC's Overdraft Services.

HDFC Bank Overdraft Interest Rate

HDFC Bank offers competitive overdraft interest rates, providing customers with financial flexibility. These rates are structured to suit various borrowing needs, ensuring affordability and convenience. With HDFC Bank's overdraft facility, customers can access funds seamlessly while managing their finances efficiently.

hdfc overdraft home loan

HDFC Overdraft Home Loan offers flexibility by allowing borrowers to deposit surplus funds into their loan account, reducing interest burden. This unique feature enables individuals to manage their finances efficiently, utilizing their savings to offset interest costs while retaining liquidity. With HDFC's Overdraft Home Loan, customers can access funds when needed, making it a versatile option for those seeking financial agility in managing their home loans.

0 notes

Text

Navigating Texas State Financial Aid: A Guide for Students

For many students in Texas, pursuing higher education is a dream that may seem out of reach due to financial constraints. However, the state of Texas offers various financial aid programs to help students afford the cost of college. From grants to scholarships to work-study opportunities, Texas state financial aid can make higher education more accessible and affordable. Let's explore some of the key financial aid programs available to students in the Lone Star State.

1. TEXAS Grant Program: The TEXAS Grant Program provides need-based financial assistance to eligible students to help cover the cost of tuition and fees at Texas public universities and colleges. To qualify for the TEXAS Grant, students must demonstrate financial need, be Texas residents, enroll in an eligible degree or certificate program, and meet certain academic requirements. The award amount varies based on financial need and available funding.

2. Texas Public Education Grant (TPEG): The Texas Public Education Grant (TPEG) provides financial aid to eligible students attending public community colleges, technical colleges, and universities in Texas. TPEG funds can be used to cover tuition, fees, and other educational expenses. Eligibility criteria for TPEG vary by institution, but generally, students must demonstrate financial need and be enrolled in an eligible degree or certificate program.

3. Texas Educational Opportunity Grant (TEOG): The Texas Educational Opportunity Grant (TEOG) is a need-based grant program for Texas residents who demonstrate financial need and are enrolled in an eligible public community college or technical college in Texas. TEOG funds can be used to cover tuition and fees for up to 75 credit hours of coursework. Eligible students must enroll in a degree or certificate program and maintain satisfactory academic progress.

4. Texas College Work-Study Program: The Texas College Work-Study Program provides part-time employment opportunities to eligible students attending public colleges and universities in Texas. Through the work-study program, students can earn money to help cover the cost of tuition, fees, and other educational expenses while gaining valuable work experience related to their field of study. Eligibility criteria and available positions vary by institution.

5. Texas Armed Services Scholarship Program: The Texas Armed Services Scholarship Program provides financial assistance to eligible students who commit to serving in the Texas Army National Guard, Texas Air National Guard, Texas State Guard, United States Coast Guard, or United States Merchant Marine after graduation. Recipients of the scholarship receive up to $10,000 per academic year to help cover tuition and fees at Texas public colleges and universities.

6. Texas Grant Program for Non-Traditional Students: The Texas Grant Program for Non-Traditional Students provides financial aid to eligible students who are considered non-traditional or adult learners. To qualify for the program, students must be Texas residents, demonstrate financial need, and be enrolled in an eligible degree or certificate program at a public college or university in Texas. The award amount varies based on financial need and available funding.

7. Texas B-On-Time Loan Program: The Texas B-On-Time Loan Program provides zero-interest loans to eligible students who are Texas residents and demonstrate financial need. If students meet certain academic requirements and graduate on time, the loan is forgiven, effectively turning it into a grant. The B-On-Time Loan can help students cover the cost of tuition, fees, and other educational expenses.

In conclusion, Texas state financial aid programs play a vital role in helping students afford the cost of higher education. From grants to scholarships to work-study opportunities, these programs provide financial assistance to eligible students across the state. By exploring and applying for Texas state financial aid programs, students can pursue their educational goals without being burdened by excessive financial debt.

0 notes

Note

Do you think college should be free?

ehhh. not exactly. (this one is kinda long)

i definitely think it should be more affordable, but free? i dunno.

generally, i think there should always be /some/ cost because i think it makes people feel more invested and plus that money, however small, can be an actual investment.

but also, most people who go to college are already fairly wealthy (middle to upper class). and so making college free would basically just be the taxpayers subsidizing the already wealthy. but the wealthy are the ones who are in the best position to afford college. so it doesn't really make sense.

if the goal is to get more talented but poor people in college in a more efficient and equitable manner then we just gotta give poor students low-to-zero interest loans and provide myriad ways for the loan to be forgiven. or i've seen systems where students get a loan but they don't have to pay it back until they get a job that pays them above a certain threshold. also, obviously, some amount of subsidies to help universities pay costs.

but this sort of reform should also be joined with major primary education reform and investment. cost is a part of the reason why more poor people aren't going to college but it's not the only reason. another major reason is because a lot of poor people just wouldn't be able to make the cut.

another thing i think is important is getting it through everyone's head that you don't need to go to college. growing up it was really drilled into everyone's heads that you /have/ to go to college. like they'd straight up tell us if you don't go to college you'll end up a loser. it's just the next step you take after high school. you just go to college.

and we just gotta balance that message with vocational schools. college is a good option but so is vocational school. not everyone can become doctors. we also need plumbers and electricians and so on. and they make pretty decent money too. and i think that's another important thing. making these "low class" jobs pay better. make it even more lucrative.

but the point is, if vocational schools become more attractive then demand will shift and less demand means maybe college will become more affordable.

but also this gets into my dream where a lot of jobs stop demanding/expecting college degrees. and maybe other schools that offer other credentials or certificates can compete. if you have to choose between paying 40k to go to a university for four years or 5k for a year or two but with similar outcomes, which are you gonna choose? i mean, there are a lot of jobs out there that demand you have a four year degree that i don't really think you need a four year degree for. especially when many of them do their own in-house training.

but at the same time, i want there to be a new class of universities which are TRUE universities. essentially, i want them to become state-subsidized monasteries for "geniuses" (am using the term genius loosely here). just centers of learning are 100% dedicated to research, development, debate, artistic creation, etc. has extremely high standards. but if you meet them then you basically just get to live on a campus for free and spend all day collaborating with other "geniuses". and these campuses would just exist to produce culture, scientific discoveries, and technological innovations. just throw money at a bunch of geniuses/creatives from all levels of society and put them in a room together and see what they can come up with.

if i could choose where my taxes go like that anon said the other day i would put 100% of my taxes to something like this. i think an institution like that would be amazing. it's like how lords during the renaissance would patronize musicians and philosophers and alchemists and just pay them to increase the grandeur and prestige of their court. we should be doing that but on a society-wide scale. plus it'd be a nice neet-savant subsidy. so many brilliant minds are wasting away in some midwestern basement playing minecraft all day or something when they should be having their genius cultivated in a monastery.

so yeah, overview: more affordable but not necessarily free because free is basically just a subsidy for the rich. but yeah there should be some tools available to make college less cost prohibitive or risky for the poorest talent (some combinations of subsidies and no-interest loans and generous forgiveness and stuff). but also we gotta reform and invest in primary education to make sure more poor people even have a chance of meeting the standards necessary for higher education. but also we need to reduce demand and provide alternatives for people who can make it by encouraging people to go to trade school and making those jobs pay better. but also we should just create genius monasteries.

0 notes

Text

BEST USCMA COACHING CENTRE IN COIMBATORE.- ARA EDUCATION

Ara Education is the No.1 USCMA Coaching in Tamilnadu. ARA OVERSEAS EDUCATION has skilled and experienced faculty members in Coimbatore. ARA OVERSEAS EDUCATION in Coimbatore offers the best USCMA Classes for both parts, each with six sections.

We provide USCMA coaching through online or off line programme with full/ part time modes. We also provide study material for this courses and doubt clarification session. We are also conducting weekly test, revision tests, finally mock test and model exam.

We are providing campus placement for jobs and Articleship.

Educational loan with zero cost interest.

For more information, please call us @

+91 422 - 4355539 | 94 89 87 79 79 | 94 89 88 58 68 or

visit us @ www.araeducation.in

#uscmacoachingcoimbatore#bestuscmacoachingcoimbatore#uscmaprofessionalcoachingcoimbatore#uscmacoachingtamilnadu

0 notes

Text

First Home Owners Grant Programs

Buying your first home may seem intimidating, but there are many resources available to make the process easier. Some are loans, and others are grants. The main difference is that loans must be repaid while grants do not.

First home owners grant programs offer mortgage and down payment assistance. Program requirements vary by state and county.

1. Down Payment Assistance

Down payment assistance can come in the form of grants or low-interest loans, and it's usually reserved for borrowers who qualify as first-time home buyers. Many programs also require that borrowers complete a homebuyer education course. Program requirements vary, but some may have income limits and only offer funds for a single-family home, condominium, co-op or manufactured home. Loans typically have deferred payment options and can be forgiven after a certain period of time.

One common requirement is that a buyer must contribute to the purchase through a cash contribution or a zero-interest loan. Additionally, most programs restrict their availability to borrowers who earn no more than 80 percent of the area median income and may enforce minimum credit score requirements. Local and state governments also run programs that are geared toward specific cities, neighborhoods or communities. These often include additional eligibility criteria, such as requiring that a buyer work in a specific field. In the case of a forgivable loan, this means that a homebuyer will have to live in the property for at least five years before the loan is forgiven.

2. Mortgage Assistance

Homeownership is the centerpiece of many local economies and is important to society, which is why federal and state governments offer incentives and down payment assistance programs. Some of these programs combine 30-year fixed rate mortgage loans with cash grants for buyers who meet income limits and are purchasing their first home.

Those interested in buying their first homes in New York should look for local downpayment programs that can help cover their closing costs. These programs range from grants to SONYMA mortgage loans.

For example, the Housing Opportunities Foundation offers a grant program for those buying their first homes in New York City. There are also various other grants available if you live in Essex, Chemung, Cortland, Schuyler or Tioga Counties. The NeighborhoodLIFT program in Ithaca, New York, offers a payback loan to assist with closing costs for those who qualify. In Suffolk County, a deferred loan is offered to those buying their first homes in Brookhaven, Islip, Huntington or Riverhead.

3. Homeownership Education

Homebuyer education classes help first-time buyers understand the process of purchasing a home and how to avoid financial pitfalls. CHFA offers these educational workshops on weekday evenings and Saturdays throughout the state through a network of participating counselor agencies.

These educational courses are often required for buyers to receive down payment assistance or qualify for a mortgage Home loans. They teach homeowners how to manage their credit, how to calculate and budget for homeownership costs, and other important topics.

Homeownership education classes are offered by many lenders, real estate agents, and government programs. Some of them are free, but it’s important to make sure that the class you choose is HUD-certified and meets the requirements of the lender or agency you are working with. You should also check if the class is online to be sure you can attend it when it’s convenient for you. Most first home buyers will benefit from attending a homeownership education course.

4. Tax Credits

There are a variety of federal and state programs that offer credits, deductions and grants to help first-time homebuyers. These incentives can reduce the cost of purchasing a new home significantly.

These incentives can include tax credits that reduce the amount of taxes a person owes, as well as mortgage interest deductions that reduce the amount of money a person needs to spend to purchase a home. Other incentive types can include down payment assistance and homeownership education courses that are required to qualify for certain grant programs.

While these incentive types can save you money when buying a home, the most significant first-time homebuyer financial assistance comes in the form of cash grants. These types of grants do not require you to pay them back and are a great way to mitigate upfront expenses when buying your first home. The Biden first-time homebuyer tax credit is an example of this type of assistance. This bill aims to encourage more people to buy homes and promote economic growth.

0 notes

Text

Looking at the most up-to-date Chaldal Offers throughout Bangladesh

Should you be a new informed customer throughout Bangladesh, you happen to be probable zero new person on the amazing discounts along with savings proposed by Chaldal, one of several state's primary on-line grocers. Chaldal presents a multitude of special offers along with savings that will serve your assorted requires with their buyers. On this page, we shall learn about the globe involving Chaldal offers, displaying among the best discounts you will discover. We shall in addition, educate you on an upmarket present via Goinmart that is certainly worth looking at.

Why is Chaldal Gives Consequently Interesting?

Chaldal can be well-known due to the motivation for you to delivering good quality goods along with house goods in cut-throat price ranges. His or her standard special offers along with distinctive gives help it become more appealing pertaining to customers for you to check out his or her on-line podium.

Varieties of Chaldal Gives

Savings in Vital Goods: Chaldal usually gives savings in every day requirements similar to almond, gas, sweets, along with lentils. These kind of savings could cover anything from a percentage off of the standard price tag for you to buy-one-get-one-free discounts.

In season Income: Chaldal generally celebrates particular instances along with conditions using distinctive savings. Through conventions similar to Eid as well as Durga Puja, you could come across deals in sugars, appetizers, and also other fun goods.

Package Discounts: Chaldal also provides package discounts which you could invest in combining solutions at the diminished price tag. These kind of bundles are generally curated to deliver greatest price for you to buyers.

Procuring Gives: Be on the lookout pertaining to procuring gives that will let you have a area of your current invest in volume rear while Chaldal loans, that is used by potential order placed.

Distinctive Software Savings: Chaldal generally supplies more savings for you to buyers whom employ his or her portable software. This specific motivates consumers for you to acquire your software and enjoy distinctive personal savings.

Membership rights Positive aspects: Chaldal's Leading membership rights software gives users first entry to discounts, deals, along with no cost supply in a candidate order placed.

Refer-a-Friend Advantages: Chaldal advantages buyers whom recommend pals on the podium. Once your called close friend creates his or her 1st invest in, two of you could get pleasure from savings as well as various other positive aspects.

End of the week Deals: Chaldal usually capabilities end of the week deals using diminished price ranges in decide on goods. It can be a thrilling time for you to extra service in goods to the 1 week ahead of time.

Brand-new Buyer Gives: First-time consumers involving Chaldal generally get preliminary savings for you to cause them to become have the simplicity of on-line grocery shopping.

Trip Savings: Getaways similar to The holiday season along with Brand-new Year's generally take holiday-themed savings in such things as accessories, cakes, along with bash items.

Seeking the Most up-to-date Chaldal Gives

To be current for the most up-to-date Chaldal gives, be sure you pay a visit to his or her site often. Moreover, you'll be able to enroll in his or her e-zine as well as comply with these people in social websites to take delivery of signal with regards to future special offers along with distinctive discounts.

Check out Distinctive Chaldal Gives via Goinmart

Even though Chaldal gives numerous savings along with discounts, it's also possible to check out distinctive gives via various other websites similar to Goinmart. Goinmart is well know due to the motivation for you to delivering good quality services for you to their buyers. They generally work together using Chaldal to create anyone particular special offers that you just will not likely come across any place else.

Important things about Deciding on Goinmart's Distinctive Chaldal Gives

While you choose Goinmart's distinctive Chaldal gives, you will probably have this positive aspects:

Exclusive Discounts: Goinmart performs tightly using Chaldal for you to curate distinctive gives that will serve your personal preferences with their buyers. Therefore you'll be able to gain access to exclusive discounts that will will not be offered by way of various other routes.

Further Personal savings: Goinmart generally sweetens the offer by simply giving more savings as well as procuring advantages if you look by way of his or her podium. This specific permits you to improve your current personal savings.

Easy Searching Expertise: Goinmart gives a user-friendly podium which make it all to easy to surf and choose Chaldal gives. You'll be able to comprehensive your current invest in flawlessly, guaranteeing a new hassle-free searching expertise.

Immediate Supply: Goinmart usually takes pleasure throughout their useful supply assistance, making sure that your current goods along with house goods are generally shipped to your current doorway immediately.

Finish

Chaldal gives throughout Bangladesh can be a amazing approach to preserve on the food market charges and enjoy good quality solutions. By simply being current on the most up-to-date special offers along with looking at distinctive discounts via websites similar to Goinmart, you can create your current searching expertise more fulfilling. Of your house savings in every day requirements as well as deals through conventions, Chaldal features a thing for every single customer throughout Bangladesh. Consequently, never will lose out on these kind of amazing chances to avoid wasting whilst you search for your selected goods.

0 notes

Text

HDFC Overdraft Limit: Your Key to Financial Fluidity

HDFC Overdraft:

HDFC Bank, a trusted name in the financial sector, extends its expertise through Overdraft Services, providing customers with a reliable source of funds when they need it the most. But what exactly is an overdraft?

An overdraft is a credit facility that allows individuals or businesses to withdraw funds from their account even if the hdfc bank overdraft interest rate in their balance reaches zero or goes into negative territory. It serves as a cushion against unexpected expenses or temporary cash shortages, offering a convenient way to manage liquidity without disrupting financial plans.

Overdraft Loan HDFC:

One of the key offerings under HDFC's Overdraft Services is the Overdraft Loan. This financial tool empowers individuals and businesses to access funds beyond their account balance, up to a predetermined limit. Whether it's for expanding a business, funding education expenses, or managing medical emergencies, the HDFC Overdraft Loan provides the necessary financial support with minimal hassle.

HDFC OD Loan Interest Rates

Interest rates play a crucial role in determining the cost of borrowing, and HDFC ensures competitive rates to make borrowing affordable for its customers. The HDFC OD Loan interest rates are designed to be competitive, offering value for money while ensuring financial feasibility. By providing transparent and competitive interest rates, HDFC enables customers to make informed borrowing decisions without worrying about hidden costs.

HDFC Bank Overdraft Facility

With HDFC Bank's Overdraft Facility, customers gain access to a wide range of benefits beyond just the funds. Convenience, flexibility, and reliability are at the core of this offering, ensuring that customers can meet their financial obligations with ease. Whether it's withdrawing funds, making payments, or managing transactions, HDFC's Overdraft Facility simplifies financial management, allowing customers to focus on what matters most.

HDFC Overdraft Against FD

For customers looking to leverage their Fixed Deposits (FDs) to access additional funds, HDFC offers the option of Overdraft Against FD. This innovative solution allows individuals to maintain their FD investments intact while unlocking liquidity as and when needed. By pledging their FD as collateral, customers can access funds at attractive interest rates, ensuring that their investments continue to work for them even during financial emergencies.

HDFC Overdraft Eligibility

While the benefits of HDFC's Overdraft Services are undeniable, eligibility criteria play a crucial role in determining who can avail of these services. Factors such as credit history, income stability, and relationship with the bank are taken into consideration when assessing eligibility. By maintaining a healthy financial profile and fulfilling the necessary requirements, customers can maximize their chances of accessing HDFC's Overdraft Services.

HDFC Bank Overdraft Interest Rate

HDFC Bank offers competitive overdraft interest rates, providing customers with financial flexibility. These rates are structured to suit various borrowing needs, ensuring affordability and convenience. With HDFC Bank's overdraft facility, customers can access funds seamlessly while managing their finances efficiently.

hdfc overdraft home loan

HDFC Overdraft Home Loan offers flexibility by allowing borrowers to deposit surplus funds into their loan account, reducing interest burden. This unique feature enables individuals to manage their finances efficiently, utilizing their savings to offset interest costs while retaining liquidity. With HDFC's Overdraft Home Loan, customers can access funds when needed, making it a versatile option for those seeking financial agility in managing their home loans.

0 notes

Text

How many types of unsecured loans are available in India?

In India, there are several types of unsecured loans available to borrowers. Here are some common types:

1)Personal Loans: These are versatile loans that can be used for various purposes, such as funding medical expenses, home renovations, or travel. Personal loans will be avail based on the customer's credit score and income.

2)Credit Card Loans: Credit card companies offer pre-approved loans known as credit card loans or cash advances. Borrowers can withdraw cash against their credit limit and repay it over time.

3)Education Loans: These loans are designed to finance education expenses, including tuition fees, books, and living costs. Education loans typically have flexible repayment terms and competitive interest rates.

4)Medical Loans: These loans are specifically tailored to cover medical expenses, including surgeries, treatments, or hospital bills. Some financial institutions offer medical loans with special features like zero-interest EMIs or cashless hospitalization.

5)Wedding Loans: Wedding loans help individuals cover the expenses associated with weddings, including venue bookings, catering, decorations, and other related costs. These loans are designed to provide funds upfront and can be repaid over a specified period.

6)Consumer Durable Loans: These loans allow individuals to purchase consumer durables such as electronic appliances, furniture, or home appliances. The loan amount is typically repaid in equated monthly instalments (EMIs) over a fixed tenure.

It’s important to note that the availability and terms of unsecured loans can vary among financial institutions, and interest rates may differ based on the borrower’s credit history and income.

The specific documents required for unsecured loans in India may vary depending on the lender and the type of loan. However, usually, the following documents are commonly needed:

1)dentity proof: A valid government-issued ID such as an Aadhaar card, PAN card, passport, or driver’s license.

2)Address proof: Documents like an Aadhaar card, passport, utility bills (electricity, water, gas), or rental agreement that establish your residential address.

3)Income proof: Salary slips, bank statements, Form 16, or income tax returns (ITR) for the past few months or years, depending on the lender’s requirements.

4)Employment proof: Proof of employment, such as an employment letter, offer letter, or appointment letter from your current employer.

5)Bank statements: Typically, bank statements for the past six months or a year, show your income, expenses, and financial transactions.

6)Photographs: Recent passport-sized photographs.

7)Loan application form: The lender’s application form, is filled out with accurate and complete information.

It’s important to note that these are general requirements, and additional documents may be requested based on the lender’s policies and the specific loan product you are applying for. It’s recommended to check with the lender or financial institution for the precise documentation needed.

#financialadvisor#mutualfunds#health insurance#term insurance#termlifeinsurance#loan services#auto title loans#business loan#financial#investor#invest#payday loans#companies#quick cash loans#financialconsultant

0 notes

Text

Innovative Agricultural Policies And Farmer Welfare Under Chandrababu Naidu’s Leadership in AP.

Under the leadership of Chandrababu Naidu, the Telugu Desam Party (TDP) government in Andhra Pradesh has implemented numerous innovative policies aimed at promoting agricultural development in the state. These policies have been designed to improve agricultural productivity, increase farmer incomes, and create a sustainable agricultural ecosystem.

One of the key Achievements of the TDP government under Chandrababu Naidu's leadership has been the introduction of micro-irrigation systems. The government has invested heavily in drip irrigation and sprinkler systems to help farmers conserve water and optimize their use of fertilizers and pesticides. This has led to a significant increase in crop yields and reduced the environmental impact of agricultural practices. Another Major Contribution of Chandrababu Naidu has been the introduction of the 'Zero Budget Natural Farming' (ZBNF) policy in the state. This policy encourages farmers to adopt natural farming methods that do not require any external inputs such as chemical fertilizers and pesticides. Instead, farmers use locally available resources such as cow dung and urine, crop residues, and other organic materials to fertilize their fields. This has helped to reduce the cost of farming and increase the sustainability of agricultural practices.

The TDP government has also introduced a number of other policies to support agricultural development in the state. For example, the government has implemented a crop insurance scheme to protect farmers from the risks associated with crop failures due to natural disasters or other unforeseen events. This has helped to provide a safety net for farmers and enabled them to invest in their farms without fear of losing everything due to unforeseen circumstances. In addition, the TDP government has focused on improving the market access for farmers by establishing a number of 'Rythu Bazaars' or farmer markets across the state. These markets provide a platform for farmers to sell their produce directly to consumers, thereby eliminating intermediaries and improving their profitability. The government has also established cold storage facilities and other infrastructure to help farmers store their produce and reduce post-harvest losses. All these stats are seen by the people on Live TDP Updates.