#Europe Gas Generator Market Trends

Text

Europe Gas Generator Market Growth, Trends, Demand, Industry Share, Challenges, Future Opportunities and Competitive Analysis 2033: SPER Market Research

The Europe Gas Generator Market encompasses the production, distribution, and utilization of gas-powered generators across European countries. With increasing concerns about energy security, environmental sustainability, and power reliability, the demand for gas generators is rising. Key drivers include the transition to cleaner energy sources, infrastructure development, and backup power requirements. Additionally, advancements in gas generator technology, such as improved efficiency and reduced emissions, contribute to market growth. Key players focus on innovation, product differentiation, and service quality to meet the diverse needs of customers and capitalize on market opportunities in Europe.

#Europe Gas Generator Market#Europe Gas Generator Market Challenges#Europe Gas Generator Market Competition#Europe Gas Generator Market Demand#Europe Gas Generator Market Future Outlook#Europe Gas Generator Market Growth#Europe Gas Generator Market Report#Europe Gas Generator Market Revenue#Europe Gas Generator Market Segmentation#Europe Gas Generator Market Share#Europe Gas Generator Market Size#Europe Gas Generator Market Trends#Europe Hydrogen Gas Generator Market#Europe Industrial Gas Generator Market#Europe Laboratory Gas Generators Market#Europe Large Generator Market#Europe Natural Gas Generator Market#Europe Natural Gas Generator Market Forecast#Europe Natural Gas Generator Market Opportunities#Europe Power Generator Market#Europe Residential Gas Generator Market#Gas Generator Market

0 notes

Text

Nanocellulose 2023 Industry – Challenges, Drivers, Outlook, Segmentation - Analysis to 2030

Nanocellulose Industry Overview

The global nanocellulose market size was valued at USD 351.5 million in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 20.1% from 2023 to 2030.

The growth is attributable to the rise in demand for various applications and the shifting trend for using bio-based goods are the factors responsible to drive demand for product. Due to its various qualities, such as increased paper machine efficiency, better filler content, lighter base mass, and higher freeness, nanocellulose is suitable for the producing a wide range of products. The paper industry uses nanocellulose as a prominent sustainable nanomaterial additive owing to its high strength, strong oxygen barrier performance, low density, mechanical qualities, and biocompatibility among the available bio-based resources. Additionally, the construction of materials, aqueous coating, and others are some of the major uses of nanocellulose composite materials.

Gather more insights about the market drivers, restrains and growth of the Nanocellulose Market

The U.S. is the largest market for nanocellulose in North America contributing a considerable amount to global revenue. People in the U.S. are concerned about their health, which has greatly aided the use of MFC (Micro fibrillated Cellulose) and CNF (Cellulose nanofibers) in the production of functional food products thus increasing the demand for nanocellulose in the country.

The food & beverage, and paper & pulp industry are majorly driving product growth in the country. Demand in the country is majorly driven by the increasing awareness and insistence on highly advanced sustainable products along with paper-based packaging in the food & beverage industries.

The pulp & paper business heavily utilizes nanocellulose as an ingredient to create light and white paper that further accelerates the market growth. Owing to its benign qualities it is used in healthcare applications such as biomedicines and personal hygiene products. Additionally, owing to its superior adsorption abilities, Nanocellulose is a suitable constituent for sanitary napkins and wound dressings. The market has been further stimulated by expanding product research activity.

Nanocellulose Market Segmentation

Grand View Research has segmented the global nanocellulose market report based on the type, application, and region:

Type Outlook (Revenue, USD Million; Volume, Kilotons; 2018 - 2030)

CNF (NFC, MFC)

Bacterial Cellulose

CNC

Application Outlook (Revenue, USD Million; Volume, Kilotons; 2018 - 2030)

Pulp & Paperboard

Composites

Pharmaceuticals & Biomedical

Electronics

Food & Beverages

Others (Textile, Paints, cosmetics, Oil & Gas, Cement)

Regional Outlook (Revenue, USD Million; Volume, Kilotons; 2018 - 2030)

North America

US

Canada

Mexico

Europe

UK

Germany

Netherlands

France

Finland

Norway

Sweden

Switzerland

Spain

Asia Pacific

China

India

Japan

South Korea

Australia

Thailand

Malaysia

Singapore

Central & South America

Brazil

Colombia

Chile

Middle East & Africa

Saudi Arabia

South Africa

Israel

Iran

Browse through Grand View Research's Renewable Chemicals Industry Research Reports.

The global chondroitin sulfate market size was valued at USD 1.29 billion in 2023 and is projected to grow at a CAGR of 3.6% from 2024 to 2030.

The global pine-derived chemicals market size was estimated at USD 5.82 billion in 2023 and is projected to grow at a CAGR of 4.4% from 2024 to 2030.

Key Companies & Market Share Insights

The market is consolidated owing to the existence of a few major players in the market including Cellu Force, Fiber Lean, Kruger INC., and others. Manufacturers operating in the market engage in strategic mergers & acquisitions, geographical expansion, product developments, and innovation in order to strengthen their positions, increase profitability, and simultaneously generate innovations and advancements.

When compared to other nanotechnology high-performance materials, nanocellulose offers a lower cost and the potential to replace many products made from petrochemicals. It has exceptional qualities like biodegradability, transparency, flexibility, high mechanical strength, and barrier characteristics, among others. Growing interest in health issues and the food & beverage industries will both have a significant impact on the market share in the years to come.

Consequently, the focus on manufacture of the product has increased owing to increasing awareness about health and environmental concerns arising from harmful chemical products. The global market has witnessed several new product developments, mergers & acquisitions and joint ventures due to several industrial challenges. Some prominent players in the global nanocellulose market include:

Cellu Force

Fiber Lean

NIPPON PAPER INDUSTRIES CO., LTD.

Kruger INC

Borregaard AS

CelluComp

Melodea Ltd

Blue Goose Refineries

GranBio Technologies

Stora Enso Biomaterials

Order a free sample PDF of the Nanocellulose Market Intelligence Study, published by Grand View Research.

0 notes

Text

How Nano PLCs Are Transforming IoT and Smart Factory Operations

Allied Market Research, titled, Nano Programmable Logic Controller (PLC) Market by Component, Service, Type, and Industry Vertical: Global Opportunity Analysis and Industry Forecast, 2017-2023, the nano programmable logic controller (PLC) market was valued at $2,585 million in 2016, and is projected to reach $4,250 million by 2023, growing at a CAGR of 7.0% from 2017 to 2023. The Processor segment held nearly half of the total market in 2016

Nano programmable logic controller is used across numerous industries such as energy & power, automotive, oil & gas, pharmaceutical, and others. At present, rise in demand for automated electronic devices and increase in trend of artificial intelligence (AI) drive the market. Moreover, popularity of Internet of Things (IoT) is expected to provide lucrative opportunities to market players.

The processor segment is estimated to maintain its lead in the global nano programmable logic controller (PLC) market, as it is the most important part in the controller for operations. Moreover, input/output (I/O) segment is expected to grow, owing to its durability and easy replacement.

The fixed nano PLC segment dominated the global market in 2016, accounting for more than half of the total market share. Requirement for compact automation solutions, enhanced efficiency, and increased need for high-voltage operating devices fuel the market growth. However, the modular nano PLC segment is expected to grow at the highest CAGR of 6.3% during the forecast period, due to increase in demand for module rack system.

Asia-Pacific was the major revenue contributor in 2016, and is expected to maintain its dominance throughout the forecast period. This is attributed to the increase in number of automated devices and solutions. Moreover, developments in energy & power and automotive sectors are anticipated to boost the growth of the nano programmable logic controller (PLC) market, especially in the Asia-Pacific countries, such as China, Japan, South Korea, and India.

Europe is anticipated to grow at highest CAGR of 8.4% during the analysis period, owing to increase in demand for automated devices and rise in the adoption of controllers in automotive and oil & gas sectors. Moreover, technological advancements to overcome complexity of the circuit are expected to offer lucrative opportunities for market players in the near future.

Key Findings of the Nano Programmable Logic Controller (PLC) Market:

In 2016, the processor segment dominated the global nano PLC market, in terms of revenue, and is anticipated to grow at a CAGR of 6.2% during the forecast period.

The modular nano PLC segment is expected to exhibit the highest growth rate, owing to the flexibility and durability.

The training segment dominated the global nano PLC market, accounting for nearly half of the total market share in 2016.

The key players operating in the nano programmable logic controller (PLC) market have adopted new product launch as their preferred strategy to expand their market foothold. The major players profiled in this report include Mitsubishi Electric Corporation, Rockwell Automation Inc., Schneider Electric SE, Siemens AG, ABB Ltd., Robert Bosch GmbH, Honeywell International, Hitachi Ltd., IDEC Corporation, and General Electric.

0 notes

Text

Hydraulic Generator Market Size | Industry Research by 2024-2032 | Reports and Insights

The Reports and Insights, a leading market research company, has recently releases report titled “Hydraulic Generator Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2024-2032.” The study provides a detailed analysis of the industry, including the global Hydraulic Generator Market share, size, trends, and growth forecasts. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

Report Highlights:

How big is the Hydraulic Generator?

The hydraulic generator market is expected to grow at a CAGR of 8.3% during the forecast period of 2024 to 2032.

What are Hydraulic Generator Market?

A hydraulic generator is a device that transforms hydraulic energy into electrical power by utilizing the flow of pressurized fluid to drive a generator. Commonly used in industries like construction, marine, and other sectors where hydraulic systems are present, these generators efficiently convert the kinetic energy of moving fluid into electricity. Known for their durability, compactness, and ability to generate power in remote or mobile settings, hydraulic generators offer a practical and reliable solution for applications that require on-demand electrical power without a conventional power grid.

Request for a sample copy with detail analysis: https://www.reportsandinsights.com/sample-request/1917

What are the growth prospects and trends in the Hydraulic Generator Market industry?

The hydraulic generator market growth is driven by various factors and trends. The hydraulic generator market is experiencing consistent growth, driven by the rising demand for dependable and efficient power generation solutions across industries such as construction, mining, marine, and heavy industrial operations. Hydraulic generators are highly regarded for their capability to generate electricity in remote or off-grid environments by leveraging existing hydraulic circuits, making them essential for mobile equipment and heavy-duty machinery. Market expansion is further supported by increasing infrastructure development, innovations in hydraulic systems, and a shift towards sustainable energy practices. Major regions driving this growth include North America, Europe, and Asia-Pacific. Hence, all these factors contribute to hydraulic generator market growth.

What is included in market segmentation?

The report has segmented the market into the following categories:

By Power Rating:

Low Power Hydraulic Generators

Medium Power Hydraulic Generators

High Power Hydraulic Generators

By Application:

Construction

Mining

Oil & Gas

Telecommunications

Marine

Others

By End-Use:

Residential

Commercial

Industrial

Market Segmentation By Region:

North America:

United States

Canada

Europe:

Germany

United Kingdom

France

Italy

Spain

Russia

Poland

BENELUX

NORDIC

Rest of Europe

Asia Pacific:

China

Japan

India

South Korea

ASEAN

Australia & New Zealand

Rest of Asia Pacific

Latin America:

Brazil

Mexico

Argentina

Rest of Latin America

Middle East & Africa:

Saudi Arabia

South Africa

United Arab Emirates

Israel

Rest of MEA

Who are the key players operating in the industry?

The report covers the major market players including:

Atlas Copco

Generac Power Systems, Inc.

Enerpac Tool Group

Wacker Neuson SE

HIMOINSA S.L.

KOHLER Co.

Caterpillar Inc.

Cummins Inc.

Stanley Infrastructure, Ltd.

Mitsubishi Heavy Industries, Ltd.

Briggs & Stratton Corporation

Doosan Corporation

Discover more: https://www.reportsandinsights.com/report/hydraulic-generator-market

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

Reports and Insights consistently mееt international benchmarks in the market research industry and maintain a kееn focus on providing only the highest quality of reports and analysis outlooks across markets, industries, domains, sectors, and verticals. We have bееn catering to varying market nееds and do not compromise on quality and research efforts in our objective to deliver only the very best to our clients globally.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

Contact Us:

Reports and Insights Business Research Pvt. Ltd.

1820 Avenue M, Brooklyn, NY, 11230, United States

Contact No: +1-(347)-748-1518

Email: [email protected]

Website: https://www.reportsandinsights.com/

Follow us on LinkedIn: https://www.linkedin.com/company/report-and-insights/

Follow us on twitter: https://twitter.com/ReportsandInsi1

#Hydraulic Generator Market Size#Hydraulic Generator Market Share#Hydraulic Generator Market Demand#Hydraulic Generator Market Analysis

0 notes

Text

Global Green Hydrogen Market: Growth Opportunities and Technological Barriers

According to a new report published by Allied Market Research, the green hydrogen market size was valued at $2.5 billion in 2022, and is estimated to reach $143.8 billion by 2032, growing at a CAGR of 50.3% from 2023 to 2032.

Green hydrogen, also known as renewable hydrogen, is a form of hydrogen produced using renewable energy sources, such as solar, wind, or geothermal power. Furthermore, the demand for proton exchange membrane electrolyzer is anticipated to witness growth during the forecast period, owing to economic growth in emerging markets continues to surge.

In 2023, Asia-Pacific accounts for the largest green hydrogen market share, followed by Europe and North America.

Major Companies

Green Hydrogen Systems, Air Liquide, Shell plc, Enapter S.r.l., Plug Power Inc., Ballard Power Systems, Linde plc, Reliance Industries, GAIL (India) Limited and Adani Green Energy Ltd.

The green hydrogen market is expected to be driven by factors such as the promising growth of the food and beverages, medical, chemical, and petrochemical industries.

Demand for power generation has escalated due to global population growth, coupled with urbanization and industrialization, leading to increase electricity consumption.

The food and beverage segment are projected to manifest a CAGR of 51.6% from 2023 to 2032, and has significant proportion in green hydrogen market size. Rise in the food and beverage industry significantly influences the green hydrogen market, primarily due to intensive energy demand of the industry.

Food and beverage production requires substantial energy for processing, packaging, refrigeration, and transportation. Green hydrogen presents a sustainable solution to meet these escalating energy demands, especially in processes were direct electrification not efficient.

Rise in living standards and technological advancements also contribute to higher energy needs, especially in emerging economies where electricity access has expanded rapidly.

Ongoing R&D efforts focus on enhancing electrolyzer efficiency, durability, and scaling up production, leading to cost reductions and improved performance. This trend aligns with ambitious governmental targets and corporate commitments aimed at fostering the green hydrogen industry, spurring innovation and market growth.

Increasingly stringent regulations and carbon pricing mechanisms incentivize to transition of industries into low-carbon alternatives, propelling its market penetration. These converging green hydrogen market trends collectively position green hydrogen as a pivotal player in the sustainable energy landscape, driving a fundamental shift toward cleaner, more resilient energy systems across the globe.

the electrification of transportation and heating sectors, driven by the push for cleaner energy sources, further amplifies the demand for power generation. This growth in demand provides a significant opportunity for the green hydrogen market.

Green hydrogen emerges as a versatile solution as traditional energy sources struggle to meet these escalating demands while maintaining environmental sustainability.

This symbiotic relationship between the rise in demand for power generation and the need for clean energy solutions positions green hydrogen as a key player in meeting the escalating energy needs sustainably.

The push toward decarbonization and the reduction of greenhouse gas emissions in the transportation sector amplifies the appeal of green hydrogen market opportunities.

Carbon Solutions, a greenhouse gas reduction consultancy, in May 2023, stated that less than 1% of the 10 million metric tons of hydrogen produced in the U.S. at present counts as green hydrogen. Instead, 76% is derived from natural gas or coal, and 23% is a by-product of petroleum refining or other chemical processes.

Globally, the hydrogen market is about 96 million metric tons per year. The report from Carbon Solutions puts number of electrolyzers operating in the U.S. at just 42, with a combined hydrogen production capacity of about 3,000 tons per year.

The U.S. Department of Energy (DOE) aims to have 10 million tons of clean hydrogen flowing per year by 2030, 20 million tons by 2040, and 50 million tons by 2050. About half that production is expected to come from renewably powered electrolysis. The U.S. government is projected to invest $8 billion in several hydrogen hubs across the country by 2026 and produce about 250 times as much hydrogen per day.

Trending Reports in Energy and Power Industry:

Electrolyzer Market Trend Analysis Report, by Application, by Capacity, by Product : Global Opportunity Analysis and Industry Forecast, 2023-2032

Renewable Energy Market Trend Analysis Report, by Type, by End Use : Global Opportunity Analysis and Industry Forecast, 2024-2033

Clean Energy Infrastructure Market Size, Share, Competitive Landscape and Trend Analysis Report, by Infrastructure Type, by End-Use : Global Opportunity Analysis and Industry Forecast, 2024-2033

About Us

Allied Market Research (AMR) is a full-service market research and business-consulting wing of Allied Analytics LLP based in Portland, Oregon. Allied Market Research provides global enterprises as well as medium and small businesses with unmatched quality of "Market Research Reports" and "Business Intelligence Solutions." AMR has a targeted view to provide business insights and consulting to assist its clients to make strategic business decisions and achieve sustainable growth in their respective market domain.

Pawan Kumar, the CEO of Allied Market Research, is leading the organization toward providing high-quality data and insights. We are in professional corporate relations with various companies and this helps us in digging out market data that helps us generate accurate research data tables and confirms utmost accuracy in our market forecasting. Each and every data presented in the reports published by us is extracted through primary interviews with top officials from leading companies of domain concerned. Our secondary data procurement methodology includes deep online and offline research and discussion with knowledgeable professionals and analysts in the industry.

#energy#power#business#news#solar#green hydrogen#clean energy#renewableenergy#renewablepower#hydrogen electrolyzer market#electrolysis

0 notes

Text

Wood Charcoal Market Landscape: Trends, Drivers, and Forecast (2023-2032)

The Wood Charcoal Market is projected to grow from USD 21989.7 million in 2024 to an estimated USD 25363.05 million by 2032, with a compound annual growth rate (CAGR) of 1.8% from 2024 to 2032.

Wood charcoal, a traditional fuel and industrial material, is produced by the pyrolysis of wood, a process that involves heating wood in the absence of oxygen. This method decomposes the wood into charcoal, leaving behind a carbon-rich product that has been used for thousands of years as a fuel source, in metallurgy, and for various other applications. The production of wood charcoal typically involves burning hardwoods like oak, maple, or hickory, as these types of wood yield a high-quality charcoal with a dense carbon content, making it highly efficient as a fuel. One of the key characteristics of wood charcoal is its ability to burn at high temperatures while producing minimal smoke, which makes it particularly valuable for cooking and grilling. It is widely favored in barbecue culture, especially in traditional and artisanal grilling methods, where the flavor of the smoke from the wood adds a unique taste to food.

In addition to its use in cooking, wood charcoal plays a crucial role in various industrial applications. In metallurgy, for instance, charcoal is used as a reducing agent in the smelting of metals like iron. The high carbon content of wood charcoal helps in extracting metal from its ore by reducing the metal oxides to pure metal, a process that has been fundamental to metalworking for centuries. Furthermore, wood charcoal is utilized in the production of activated charcoal, a form of carbon that is processed to have a high surface area and is used extensively in filtration systems, medical applications, and environmental protection. Activated charcoal is particularly effective at adsorbing impurities from air and water, making it a critical component in water purification, air filters, and even in poison control treatments.

The wood charcoal market is driven by a variety of factors that contribute to its sustained demand across different regions and applications. Here are some of the key drivers:

1. Growing Demand for Charcoal in Cooking and Grilling:

The increasing popularity of outdoor cooking, particularly barbecuing and grilling, is a major driver of the wood charcoal market. In many cultures, especially in North America, Europe, and parts of Asia, wood charcoal is preferred for its ability to impart a unique smoky flavor to food. The rise of artisanal and gourmet cooking trends has further fueled demand for high-quality, hardwood charcoal, which is prized for its clean burn and high heat output.

2. Traditional Use in Developing Regions:

In many developing countries, particularly in Africa and parts of Asia and Latin America, wood charcoal remains a primary fuel source for cooking and heating. Its affordability, availability, and efficiency compared to other fuels like electricity or gas make it indispensable for millions of households. This sustained demand in rural and low-income areas continues to drive the market, despite efforts to transition to cleaner energy sources.

3. Industrial Applications:

Wood charcoal is extensively used in various industrial processes, especially in metallurgy, where it serves as a reducing agent in the smelting of metals like iron. Its high carbon content and ability to generate intense heat without producing a lot of smoke make it ideal for these applications. Additionally, wood charcoal is used in the production of activated carbon, which is vital in water purification, air filtration, and other environmental and medical applications. The demand for activated carbon, in particular, is growing as concerns about water and air quality increase globally.

4. Increasing Popularity of Activated Charcoal:

Activated charcoal, derived from wood charcoal, is experiencing growing demand due to its wide range of applications in health, beauty, and environmental sectors. It is used in products like water filters, air purifiers, cosmetics, and even as a detoxifying agent in food and beverages. This demand is driving the market for high-quality wood charcoal, which serves as the base material for activated carbon production.

5. Sustainability and Environmental Concerns:

While traditional charcoal production has environmental drawbacks, there is a growing movement towards sustainable practices in the industry. Consumers and businesses are increasingly seeking sustainably produced charcoal, which is made using waste wood, plantation timber, or through improved production methods that reduce emissions and conserve resources. The shift towards sustainability is creating new opportunities within the market for certified eco-friendly charcoal products.

6. Expansion of the Global Barbecue Market:

The global barbecue market is expanding, particularly in regions where grilling has become a popular social activity. The proliferation of barbecue restaurants, the growing number of barbecue competitions, and the increasing popularity of grilling at home are all contributing to the rising demand for wood charcoal. In countries like the United States, Brazil, Australia, and South Korea, barbecue culture is deeply ingrained, supporting steady market growth.

7. Urbanization and Population Growth:

As urbanization increases, particularly in developing countries, the demand for accessible and affordable cooking fuels like wood charcoal is likely to grow. Urban populations in regions with limited access to electricity or gas often rely on charcoal as a primary or supplementary fuel source, driving market demand. Additionally, population growth in these regions contributes to the overall increase in charcoal consumption.

8. Economic Factors:

The affordability of wood charcoal compared to other energy sources is a significant driver, especially in regions where income levels are low and access to modern fuels is limited. Economic downturns or fluctuations in energy prices can lead to increased reliance on charcoal as a cost-effective alternative for cooking and heating.

9. Cultural and Traditional Practices:

In many parts of the world, the use of wood charcoal is deeply rooted in cultural and traditional practices, particularly in cooking. For instance, traditional dishes and cooking methods in Africa, Asia, and Latin America often rely on charcoal for the distinctive flavors it imparts. These cultural practices ensure a continued demand for wood charcoal, even as alternative energy sources become more available.

10. Regulatory Environment and Policy Support:

In some regions, governments are promoting sustainable charcoal production through policy support, subsidies, and incentives for eco-friendly practices. This support helps drive the market by encouraging producers to adopt sustainable methods, which can also meet the growing consumer demand for environmentally responsible products.

Key Player Analysis:

BandB Charcoal

Cooks International LLC

Duraflame Inc.

Fire & Flavor Grilling Company

Fogo Charcoal

Greencoal Namibia CC

Hans Enterprises

P.BIOCOAL

Kamodo Joe

Kingsford Products Company

Royal Oak Company

Saint Louis Charcoal Company

Southern Fuelwood

The Charcoal Supply Company

The Clorox Company

The Original Charcoal Company

Two Trees Products

More About Report- https://www.credenceresearch.com/report/wood-charcoal-market

The wood charcoal market exhibits significant regional variations driven by differences in cultural practices, industrial applications, economic conditions, and environmental policies. Here’s a breakdown of the regional insights for the wood charcoal market:

1. Africa:

Dominance of Charcoal as a Primary Fuel: In Africa, wood charcoal is a critical source of energy, particularly for cooking and heating in rural and urban households. In countries like Nigeria, Kenya, Tanzania, and the Democratic Republic of Congo, a large portion of the population relies on charcoal due to the limited access to electricity and other modern fuels. The demand for wood charcoal in Africa is sustained by its affordability and availability, despite environmental concerns associated with deforestation and inefficient production methods.

Environmental Impact and Sustainability Efforts: The widespread use of charcoal in Africa has led to significant deforestation, prompting efforts by governments and NGOs to promote sustainable charcoal production practices. Initiatives include the development of more efficient charcoal kilns, reforestation programs, and the promotion of alternative fuels to reduce the environmental impact.

2. Asia-Pacific:

Diverse Market Dynamics: The Asia-Pacific region has diverse market dynamics with significant demand for wood charcoal in both domestic and industrial applications. Countries like Indonesia, Vietnam, and the Philippines are major producers of wood charcoal, often exporting to other regions. In rural areas of Southeast Asia and South Asia, charcoal remains an important cooking fuel.

Export-Oriented Production: Indonesia, in particular, is one of the largest exporters of wood charcoal, with substantial production driven by both domestic use and international demand, particularly from countries in the Middle East and Europe. The region's vast tropical forests provide abundant raw materials for charcoal production, although sustainability remains a concern.

Growing Demand for Activated Charcoal: The demand for activated charcoal, particularly in India, China, and Japan, is driving the market. Activated charcoal is used in various applications, including water purification, air filtration, and cosmetics, contributing to the growth of the wood charcoal market in this region.

3. North America:

High Demand for Barbecue Charcoal: In North America, particularly in the United States and Canada, wood charcoal is widely used for outdoor cooking and barbecuing. The market is characterized by a strong preference for high-quality, artisanal charcoal made from hardwoods like oak and hickory, which provide superior heat and flavor for grilling. The popularity of barbecue culture, coupled with seasonal demand peaks during summer, drives the market.

Sustainability and Eco-Friendly Products: There is a growing consumer preference for sustainably produced charcoal, with an increasing demand for products that are certified as eco-friendly or made from renewable resources. Companies in North America are responding to this trend by offering sustainably sourced and produced charcoal products, often highlighting their environmental credentials as a key selling point.

4. Europe:

Demand Driven by Barbecue and Industrial Use: In Europe, the demand for wood charcoal is driven by both consumer and industrial applications. Barbecuing is popular in countries like Germany, France, and the United Kingdom, where consumers seek high-quality charcoal for outdoor cooking. Additionally, wood charcoal is used in industrial processes, particularly in the production of activated carbon and in metallurgy.

Environmental Regulations: Europe is at the forefront of environmental sustainability, with strict regulations governing charcoal production and trade. The European Union has implemented policies that encourage sustainable forest management and the use of eco-friendly production methods. As a result, there is a growing market for certified sustainable charcoal products, which comply with environmental standards and appeal to environmentally conscious consumers.

5. Latin America:

Significant Production and Export: Latin America, particularly Brazil, is a major producer and exporter of wood charcoal. Brazil’s vast forests provide ample resources for charcoal production, much of which is exported to other regions, including Europe and the Middle East. The country’s charcoal is used both domestically and internationally, with significant applications in the steel industry and in barbecue cultures.

Sustainability Challenges: The charcoal industry in Latin America faces challenges related to deforestation and environmental degradation. In response, there are ongoing efforts to promote sustainable charcoal production practices, including the use of plantation-grown timber and the implementation of more efficient production technologies to reduce environmental impact.

6. Middle East:

Import-Driven Market: The Middle East is a significant consumer of wood charcoal, particularly for traditional cooking methods and shisha (hookah) use. Countries in the region, including Saudi Arabia, the UAE, and Egypt, import large quantities of charcoal, primarily from Africa and Southeast Asia, to meet domestic demand.

Cultural Significance: In the Middle East, the use of charcoal is deeply embedded in cultural practices, especially in food preparation and social gatherings involving shisha. This cultural significance ensures steady demand, with consumers favoring high-quality, long-burning charcoal for both cooking and recreational purposes.

7. Global Trends:

Shift Towards Sustainability: Across all regions, there is a noticeable shift towards more sustainable production and consumption of wood charcoal. Consumers are increasingly aware of the environmental impact of traditional charcoal production, leading to greater demand for sustainably sourced and produced charcoal. This trend is prompting producers to adopt certification schemes, improve production efficiency, and explore alternative raw materials to reduce environmental impact.

Segmentation:

By Product Type

Lump charcoal,

Briquettes,

Charcoal powder.

By Wood Type

Hardwood,

Softwood,

By Application

Residential,

Commercial,

Industrial applications.

By End-Use

Food preparation,

Metallurgy,

Chemical production.

Browse the full report – https://www.credenceresearch.com/report/wood-charcoal-market

Browse Our Blog: https://www.linkedin.com/pulse/wood-charcoal-market-report-opportunities-ikhcf

Contact Us:

Phone: +91 6232 49 3207

Email: [email protected]

Website: https://www.credenceresearch.com

0 notes

Text

The Future of Pumping: A Dive into the Global Pumps Market

Pumps are the lifeblood of countless industries, quietly ensuring liquids flow where they need to be. But this seemingly simple technology boasts a complex and ever-evolving market. Today, we'll explore the global pumps market landscape using insights from Mordor Intelligence's latest report.

Growth on the Horizon

The global pumps market is currently estimated at a staggering USD 68.46 billion, and Mordor Intelligence forecasts it to reach USD 86.07 billion by 2029. This translates to a compound annual growth rate (CAGR) of 3.37%. This steady growth is driven by several key factors:

Infrastructure Boom: Increased investment in infrastructure development projects, especially in water and wastewater management, is creating a strong demand for pumps.

Industrial Expansion: Growth across various industries like power generation, oil & gas, and chemicals is driving the need for efficient and reliable pumping solutions.

Focus on Sustainability: Advancements in technology are leading to the development of more energy-efficient pumps, aligning with the growing focus on environmental sustainability across industries.

Market Segmentation: A Closer Look

The pumps market is segmented based on several key factors:

Type: This includes centrifugal pumps, reciprocating pumps, rotary pumps, and other pump types. Each type has its own unique set of functionalities and applications.

End-User Industry: Pumps cater to a wide range of industries, including oil & gas, water & wastewater, chemicals & petrochemicals, mining, power generation, and others.

Geography: The report analyzes the market size and growth forecasts across major regions like North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

Key Trends Shaping the Future

The pumps market is constantly evolving, with several trends shaping its future:

Digitalization: The integration of digital technologies like sensors and the Internet of Things (IoT) is enabling smarter pumps with improved efficiency and predictive maintenance capabilities.

Sustainable Materials: The increasing focus on sustainability is leading to the development of pumps made from recycled materials and those that offer lower energy consumption.

Regional Variations: Growth in emerging economies, particularly in Asia-Pacific, is expected to be a significant driver in the coming years.

Mordor Intelligence's Report: A Valuable Resource

For businesses looking to navigate the global pumps market, Mordor Intelligence's comprehensive report offers valuable insights. It provides detailed analysis on:

Market trends and growth forecasts

Key drivers and challenges impacting the market

Technological advancements and innovations

Competitive landscape and profiles of major players

Market size and forecasts by segment and region

By accessing this report, you can gain a deeper understanding of the market dynamics and identify potential opportunities for growth.

Stay Ahead of the Curve

The global pumps market is a dynamic and ever-changing landscape. By staying informed about the latest trends and insights, businesses can make informed decisions and capitalize on the opportunities this vital industry presents.

#pumps market#pumps industry#pumps market size#pumps market analysis#pumps market share#pumps market trends

0 notes

Text

Europe Green Hydrogen Market, Key Players, Market Size, Future Outlook | BIS Research

A lithium-ion battery (Li-ion battery) is a type of rechargeable battery that uses lithium ions as the primary component of its electrochemistry.

During discharge, lithium ions move from the negative electrode (typically made of graphite) to the positive electrode (commonly made of a lithium compound) through an electrolyte.

The Europe Green Hydrogen market was valued at $253.8 million in 2023, and it is expected to grow with a CAGR of 66.72% during the forecast period 2023-2033 to reach $42,108.6 million by 2033

Europe Green Hydrogen Overview

Green hydrogen refers to hydrogen gas produced through a process that uses renewable energy sources, such as wind, solar, or hydropower, to power the electrolysis of water. During electrolysis, water (H₂O) is split into hydrogen (H₂) and oxygen (O₂) using electricity.

The electricity comes from renewable sources, this method of producing hydrogen results in very low or zero greenhouse gas emissions, making it a sustainable and environmentally friendly alternative to hydrogen produced from fossil fuels.

Download the Report Page Click Here!

The European green hydrogen market is expanding rapidly as the region works to transition to a more sustainable energy future. Green hydrogen, produced by electrolysis of water using renewable energy sources such as wind and solar power, is emerging as a critical solution for carbon neutrality.

Several European countries are at the forefront of green hydrogen production and utilization, propelled by ambitious climate goals and significant investments in renewable energy infrastructure

Market Segmentation

By Application

By Technology

By Renewable Energy Source

By Country

Market Drivers

Decarbonization goals and Climate Policies: Green hydrogen is seen as a crucial tool to decarbonize sectors like heavy industry, transportation, and energy, where direct electrification is challenging.

Renewable Energy Growth: The rapid expansion of renewable energy sources like wind and solar power makes green hydrogen more viable.

Industrial Demand: Industries such as steel, chemicals, and refining are seeking low-carbon alternatives to reduce their carbon footprint.

Transportation Sector Shift: The push for zero-emission vehicles, especially in sectors like trucking, shipping, and aviation, is driving demand for green hydrogen-powered fuel cells.

Energy Storage and Grid Balancing: Green hydrogen can serve as an energy storage solution, helping balance intermittent renewable energy sources by storing excess electricity and converting it back into power when needed.

Market Segmentation

1 By Application

Oil and Gas

Mobility and Power Generation

And many others

2 By Technology

Protein Exchange Membrane Electrolyzer

Alkaline Electrolyzer

Solid Oxide Electrolyzer

3 By Renewable Energy Sources

Wind Energy

Solar Energy

Others

4 By Country

France

Germany

U.K.

Spain

Grab a look at our sample page click here!

Key Companies

Linde plc

Air Liquide

Engie

Uniper SE

Siemens Energy

Green Hydrogen Systems

Nel ASA

Visit our Advanced Materials and Chemical Vertical Page !

Future of Europe Green Hydrogen Market

The key trends and drivers for lithium ion battery market affecting the future of lithium ion battery market is as follows

Cost Reduction

Technological Innovation

Global Hydrogen Economy

Cross Sector Collaborations

Conclusion

In conclusion, the green hydrogen market stands at a transformative juncture, with the potential to significantly impact the global energy landscape. As a clean and sustainable energy carrier, green hydrogen offers a promising solution to some of the most challenging aspects of decarbonization, particularly in sectors where direct electrification is difficult.

The market for green hydrogen is poised for substantial growth, driven by several factors including advancements in technology, decreasing production costs, supportive government policies, and increasing demand from industrial and transportation sectors

0 notes

Text

Flocculants Market - Forecast 2024-2030

Flocculants Market Overview:

Flocculants Market size is forecast to reach $1.4 Billion by 2030, after growing at a CAGR of 7.9% during 2024-2030. This growth is driven by the Flocculants Market witnessing a burgeoning trend driven by the growing demand for water treatment solutions. Escalating concerns over waterborne diseases and the imperative for freshwater conservation fuels this trend. Municipalities and industries alike are increasingly turning to flocculants and coagulants to purify water effectively. As populations expand and industrial activities intensify, the necessity for robust water treatment processes becomes paramount. Consequently, there's a notable upsurge in the adoption of these chemicals across water treatment facilities worldwide, ensuring the delivery of safe and clean water to communities and industries alike.

Additionally, the Flocculants Market experiences a significant trend with North America emerging as a dominant player, poised to capture around 28.5% market share by 2033. This growth trajectory is propelled by several factors, including stringent government regulations concerning public health and water management. Additionally, the region's pressing need for efficient water treatment solutions drives the heightened demand for flocculants and coagulants. As North America continues to prioritize environmental sustainability and water quality, the market for these chemicals is expected to witness sustained growth, solidifying the region's position as a key market leader in the global flocculants industry.

Flocculants Market - Report Coverage:

The “Flocculants Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Flocculants Market.

By Type: Natural (Chitosan, Cellulose, Gum and Mucilage and Starch Derivative), Synthetic (Polyacrylamide, Polyethylene Oxide and Polyethylene Amine) and Inorganic (Activated Silica, Metallic Hydroxide and Colloidal Clays).

By Application: Water Processing, Mineral Dressing, Fermentation and Others.

By End-User Industry: Oil & Gas Industry (On-shore and Off-shore), Food & Beverage (Dairy, Soft Drinks, Alcohol Drinks and Others), Wastewater Treatment (Industrial and Municipal), Mining Industry, Paper & Pulp, Power Generation (Hydro, Wind, Nuclear and Others) and Others.

By Geography: North America, South America, Europe, APAC, and RoW.

Request Sample

COVID-19 / Ukraine Crisis - Impact Analysis:

• The Covid-19 pandemic significantly impacted the flocculants market, presenting a mixed bag of challenges and opportunities. On one hand, the pandemic-induced economic slowdown temporarily slowed down industrial activities, leading to reduced demand for flocculants across various sectors such as mining, oil and gas, and water treatment. Supply chain disruptions and logistical challenges also hampered the market's growth during the initial phases of the pandemic. Conversely, the increased focus on hygiene and sanitation during the pandemic spurred demand for water treatment solutions, including flocculants, particularly in healthcare facilities and municipal water treatment plants. Moreover, the gradual recovery of industrial activities and the resumption of infrastructure projects post-lockdowns provided a stimulus to the market's rebound. Overall, while Covid-19 initially posed obstacles to the flocculants market, the renewed emphasis on water treatment and gradual economic recovery has fuelled its resurgence, indicating a resilient trajectory amidst challenging circumstances.

• The Russia-Ukraine crisis exerts a notable impact on the flocculants market due to its implications for the global supply chain. Ukraine is a significant producer of raw materials used in flocculants manufacturing, including chemicals and minerals. The conflict disrupts supply chains, leading to potential shortages and price fluctuations in the market. Additionally, heightened geopolitical tensions can create uncertainties, prompting companies to reassess their sourcing strategies and seek alternative suppliers, which could further strain supply and affect pricing. Moreover, instability in the region may hamper logistics and transportation networks, impeding the timely delivery of flocculants to end-users. Overall, the Russia-Ukraine crisis underscores the interconnectedness of global markets and highlights the need for resilience and diversification strategies within the flocculants industry to mitigate risks associated with geopolitical conflicts.

Key Takeaways:

• Asia-Pacific dominates the Flocculants Market owing to the rapid development in the wastewater treatment sector which is significantly influencing the demand for Flocculating agents in the region for removing suspended solids.

• Growing production of crude oil resulting from high petroleum demand has accelerated the demand and usage of Flocculating agents for wastewater treatment in the oil & gas sector, which has positively impacted the Flocculants industry outlook.

• Rapid growth in mineral mining production due to the high demand for minerals in manufacturing products such as plastics, paints, and ceramics has accelerated the demand and usage of Flocculants in the mining industry for the removal of suspended solids during mineral extraction.

• The establishment of effective and eco-friendly alternative water treatment technologies would hamper the usage of chemicals in such applications. It would decrease the market growth of Flocculants, thereby negatively impacting the Flocculants Market size.

Inquiry Before Buying

Flocculants Market Segment Analysis – By Type

Natural type emerges as the leading contender in the flourishing flocculants market due to its eco-friendly nature and superior performance and it has a market share of 39.5% in 2023. Unlike conventional flocculants derived from synthetic chemicals, Natural types harness the power of natural polymers sourced from renewable resources such as plants or microorganisms. This sustainable approach not only mitigates environmental impact but also addresses consumer concerns regarding toxicity and biodegradability. Moreover, Natural flocculants exhibit remarkable efficacy in water treatment, industrial processes, and wastewater management, surpassing traditional alternatives in performance metrics like sedimentation efficiency and residue minimization. As industries increasingly prioritize sustainability and regulatory compliance, the demand for Natural flocculants continues to surge, marking a paradigm shift towards greener solutions in the global market landscape.

Flocculants Market Segment Analysis – By Application

Water processing has emerged as the fastest-growing application of flocculants in the market with a CAGR of 8.5% during the forecast period. With increasing industrialization and urbanization, the demand for clean water has escalated, necessitating advanced treatment methods. Flocculants play a pivotal role in water processing by effectively removing suspended particles and contaminants, thus improving water quality. The adoption of flocculants is particularly significant in industries such as mining, oil and gas, and municipal water treatment plants. Moreover, stringent regulations regarding wastewater discharge further drive the demand for efficient flocculation processes. Additionally, advancements in flocculant formulations, such as eco-friendly and biodegradable options, cater to the growing environmental concerns. As water scarcity becomes a pressing global issue, the water processing segment is poised for sustained growth, underscoring the indispensable role of flocculants in ensuring clean water supply.

Schedule a Call

Flocculants Market Segment Analysis – By End-User Industry

The pulp and paper industry stands out as the fastest-growing end-use sector within the flocculants market with a CAGR of 8.3% during the forecast period. Flocculants play a pivotal role in this industry by aiding in water purification and recovery processes during paper production. As environmental regulations tighten, the demand for efficient water treatment solutions escalates, propelling the adoption of flocculants. Additionally, the burgeoning demand for paper products globally fuels the expansion of pulp and paper production facilities, further boosting the requirement for effective flocculants. Moreover, advancements in flocculant technologies tailored to address the unique challenges of the pulp and paper sector contribute to its rapid growth. With sustainability concerns driving industry practices, the use of flocculants becomes indispensable, positioning the pulp and paper industry as a key driver in the flourishing flocculants market.

Flocculants Market Segment Analysis – By Geography

The Asia Pacific region stands out as the dominant market for flocculants within the global market landscape and it has a market share of 43% in 2023. Several factors contribute to this burgeoning growth trajectory. Firstly, rapid industrialization across countries such as China, India, and Southeast Asian nations fuels increased demand for water treatment solutions, where flocculants play a vital role in purifying water for various industrial processes and municipal use. Moreover, stringent environmental regulations drive industries to adopt advanced water treatment technologies, further propelling the demand for flocculants. Additionally, the expanding population in the region amplifies the need for clean water, stimulating investments in water infrastructure and treatment facilities. Furthermore, the flourishing mining sector in countries like Australia and Indonesia necessitates effective water management practices, boosting the uptake of flocculants in mineral processing operations. The Asia Pacific's dynamic economic landscape, coupled with rising environmental concerns and infrastructure developments, positions it as the leading growth hub for flocculants in the global market, offering lucrative opportunities for market players to capitalize on.

Buy Now

Flocculants Market Drivers

Increase in Mineral Mining Output

The increase in mineral mining output serves as a significant driver in the flocculants market due to its direct correlation with the demand for water treatment solutions. As mining activities escalate worldwide to meet the growing demand for essential minerals such as gold, silver, copper, iron ore, and rare earth elements, the need for effective water management practices becomes imperative. Flocculants play a crucial role in the mineral processing industry by facilitating the separation of solid particles from water during the extraction and refining processes. The rising mining output leads to higher volumes of wastewater containing suspended solids, metals, and other contaminants, necessitating efficient treatment methods to meet environmental regulations and ensure water reuse or safe discharge. Consequently, the demand for flocculants surges as mining companies seek cost-effective and sustainable solutions to optimize their water treatment operations. This trend presents a lucrative opportunity for flocculant manufacturers to cater to the evolving needs of the mineral mining sector and capitalize on its growth trajectory.

Bolstering Growth in Oil Production

Bolstering growth in oil production serves as a significant driver in the flocculants market, amplifying demand for these chemicals due to their crucial role in the oil and gas industry's water management processes. With the global energy demand persistently rising, oil exploration and production activities are expanding, particularly in regions such as North America, the Middle East, and parts of Asia. As oil extraction involves the use of large volumes of water for processes such as drilling, hydraulic fracturing, and enhanced oil recovery, there's a growing need for efficient water treatment solutions, including flocculants, to manage wastewater and ensure compliance with environmental regulations. Moreover, as oil reserves become more challenging to extract, unconventional extraction methods like shale oil and deep-sea drilling become more prevalent, further driving the demand for flocculants to treat the associated wastewater. This trend positions the flocculants market for sustained growth, with oil production serving as a key catalyst.

Flocculants Market Challenges

Introduction of Alternative Technologies

The introduction of alternative technologies poses a significant market challenge for the flocculants industry. As sustainability and environmental concerns escalate, industries are increasingly exploring and adopting alternative water treatment solutions that may compete with traditional flocculants. Advanced technologies such as membrane filtration, ultraviolet (UV) disinfection, and electrocoagulation offer more efficient and eco-friendly alternatives to flocculation processes. Furthermore, the emergence of nanotechnology and bio-based polymers presents innovative solutions that can potentially replace conventional flocculants. These alternatives often boast lower environmental footprints, reduced chemical usage, and enhanced treatment efficiencies, making them attractive options for various applications. However, while these alternative technologies offer promising benefits, their widespread adoption may challenge the market dominance of traditional flocculants. Market players in the flocculants industry must adapt by investing in research and development to innovate and improve their products, ensuring competitiveness in the face of evolving market dynamics and shifting consumer preferences toward more sustainable solutions.

Market Landscape

Product/Service launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the Flocculants Market. The top 10 companies in this industry are: BASF SE, SNF Floerger, Ecolab Inc., Kemira, Solenis LLC, Buckman Laboratories, Feralco AB, Suez S.A., Ixom Operations Pty Ltd., Kurita Water Industries

Developments:

Kemira focused on sustainability in the flocculants market. In May 2022, they launched "Superfloc® BioMB," the world's first biomass-balanced flocculant. This eco-friendly option offers similar performance to traditional solutions but with a lower environmental impact.

Solenis bolstered its global presence in the flocculants market through their acquisition of Diversey Holdings in July 2023. This deal, valued at $4.6 billion, expands Solenis' reach to 130 countries and strengthens their position as a key player. While not directly focused on flocculants, it suggests continued growth ambitions.

#Flocculants Market#Flocculants Market size#Flocculants industry#Flocculants Market share#Flocculants top 10 companies#Flocculants Market report#Flocculants industry outlook

0 notes

Text

Next-Gen Shipping: Market Forecast and Trends 2024–2030

Cargo Shipping Market Overview

Request Sample

Report Coverage

The report: “Cargo Shipping Industry Outlook — Forecast (2021–2026)”, by IndustryARC covers an in-depth analysis of the following segments of the Cargo Shipping industry.

By Type: Linear Ships, Tramp Ships.

By Cargo Type: Passenger, Liquid, Container, Dry, General, Bulk, Others.

By Vessel Type: Multi-Purpose Vessels, Dry-Bulk Carriers, Tankers, Container Vessels, Bulk Vessels, Reefer Vessels, Ro-Ro Vessels, Others.

By Vessel Cargo Capacity: <1000 TEU, 1000–4000 TEU, 4000–8000 TEU, 8000–12000 TEU, 12000–16000 TEU, 16000–20000 TEU, >20000 TEU.

By End Use Industry: Food and Beverages, Electrical & Electronics, Manufacturing, Oil & Gas, Metal and Mining, Logistics and E-commerce, Consumer Goods, Chemicals, Medical and Pharmaceutical, Others.

By Geography: North America, South America, Europe, APAC and RoW.

Inquiry Before Buying

Key Takeaways

Improving port infrastructures and incorporation of favourable trade agreements overtime is analyzed to significantly drive the cargo shipping market during the forecast period 2021–2026.

Tankers had accounted for the largest market share in 2020, attributed to the factors including longer sailing, involvement of lesser number of ports and many others, making it highly preferable for conducting marine transportation.

Presence of some key players such as Evergreen Marine, Yang Ming Marine Transport Corporation, Pacific International Lines and so on opting for partnerships, product launches or expansion to improve cargo shipping facilities have helped in boosting its growth within APAC region.

Schedule a Call

Cargo Shipping Market Segment Analysis- By Vessel Type

By vessel type, the cargo shipping market is segmented into multi-purpose vessels, dry-bulk carriers, tankers, container vessels, bulk vessels, reefer vessels, ro-ro vessels and many others. Tankers had dominated the cargo shipping market with $3234.07 million tons in 2020 and are analyzed to grow at a CAGR of 3.4% during the forecast period 2021–2026. Tankers generally refers to those cargo shipping vessels used in transportation of bulks of liquids and gases, which had emerged as an ideal mode of transportation for chemicals, petrochemicals as well as gas refineries. Oil tankers, chemical tankers, gas carriers are some of the common type of tankers utilized for serving applications based on load carrying capacities for the shipping goods. Compared to other types, these vessels are capable of offering advantages be it longer sailing, involvement of lesser number of ports and so on, thus creating its higher adoption within marine transportation facilities. Factors such as economic slowdown owing to COVID-19, decarbonization measures as well as dropping oil prices are some of the threats encountering the tanker vessels across cargo shipping markets. However, with slow economic recovery post the global pandemic situation, the demand towards crude oil imports or exports are bound to surge in order to begin with various industrial or commercial operations, thereby promoting the market growth of tankers in the long run. In 2021, Shell had signed an agreement to charter crude tankers including very large crude carriers from Advantage Tankers, AET and International Seaways, powered with dual-fuel liquefied natural gas engines. Owing to capability of lowest possible methane slip and highest fuel efficiency with an average 20% less fuel consumption, this is further anticipated to mark an important step towards increasing LNG-fuelled vessels on the water by 2023.

Cargo Shipping Market Segment Analysis- By Vessel Cargo Capacity

By vessel cargo capacity, the cargo shipping market is segmented under <1000 TEU, 1000–4000 TEU, 4000–8000 TEU, 8000–12000 TEU, 12000–16000 TEU, 16000–20000 TEU and >20000 TEU. Vessel cargo capacity of 12000–16000 TEU had held the largest share in the cargo shipping market with of $3269.44 million tons in 2020, thus analyzed to grow further with a CAGR of 4.0% during 2021–2026. Neo panamax vessels with capacity (10000–14500 TEU) and ultra-large container vessels with capacity (14500 and above) have been considered under this segment. Neo panamax refers to those medium to large sized vessels, capable of carrying about 19 rows of containers with a beam of 43 m, with comparable size of Suezmax tankers, while ultra large container vessels are considered as the biggest container ships with capabilities being at least 366 meters long, 49 meters wide, draught of at least 15.2 meters, causing its dominance within the hazardous end-use markets. Due to flexibility perspective, vessels with load carrying capacity ranging from 10000 to 15000 TEU are generally capable of allowing carriers to deploy largest ships which can traverse Panama Canal, gaining popularity in transport of goods including metal ores, coal and so on. In 2020, Evergreen Line had revealed about delivering two 12000 TEU class F-type container ships, featuring an optimized hull design as well as a smart ship system. Since these containers are equipped with a main engine of 58,000 horsepower, along with preventing containers on the deck from affecting the view from the bridge as well as maximizing cargo loadability prior to its configuration, these vessels are further analyzed to create a significant impact towards the market growth of cargo vessels with 12000 TEU capacity in the long run.

Buy Now

Cargo Shipping Market Segment Analysis- Geography

APAC had accounted for the largest share of $6589.12 Million Tons in 2020, analyzed to grow with a CAGR of 4.1% for the Cargo Shipping market during the forecast period 2021–2026. Growth of various end-use industries including food & beverage, consumer goods and so on, initiatives towards improving as well as incorporating new trade agreements, improving sea port infrastructures, rising technological advancements along with many others can be considered as some of the crucial factors which had attributed towards the market growth of cargo shipping across APAC region. Presence of some of the key cargo shipping companies including Evergreen Marine, Mitsui O.S.K Lines Ltd., Yang Ming Marine Transport Corporation, Pacific International Lines and others have also helped in creating a positive impact within the Asia-Pacific ocean freight shipping facilities. Partnerships, expansion, R & D investments and so on were considered as some of the key strategies adopted by the market players to drive cargo shipping services within the region. In 2020, Yang Ming Marine Transport Corporation announced about expanding its Intra-Asia service networking through extending Japan-Taiwan-South China Express (JTS) to Malaysia, Philippines and Singapore. This expansion was meant to optimize the competitiveness between Japan, Taiwan, South China as well as Southeast Asia, while improving the linkage connection of Yang Ming’s main port, Kaohsiung. Such factors are further set to create a positive impact towards adoption of these shipping services in order to facilitate sea transport in the long run.

Cargo Shipping Market Drivers

Growing initiatives towards improving port infrastructure:

Growing initiatives towards improving port infrastructures either by governmental support or shipping company investments can be analyzed as one of the major drivers impacting the growth of cargo shipping during the forecast period 2021–2026. Port infrastructure plays a crucial role in cargo shipping operations be it handling of bulks of goods, which had been creating high need towards upgrading, modernizing or constructing new ports to support growing trade businesses around the world. Increasing demand towards consumer products, crude oil and many other related commodities have been also raising the requirement of infrastructural growth of sea ports in order to help in meeting the consumer demands overtime. Factors such as adaptive secured communication, IT architecture and so on within the ports are getting introduced to benefit strategic traffic while assisting ship infrastructures, thus positively impacting the cargo shipping growth. Sea port infrastructures have been also getting upgraded with advanced handling systems capable of autonomous or semi-autonomous operation to achieve higher throughput levels. In addition, government along with various private infrastructure companies across developed as well as developing countries have started to focus towards establishing new ports, upgrade or expand the existing ones through investments as a move towards supporting growing trade volumes. In 2021, Adani Ports and Special Economic Zone (APSEZ) had revealed about completing its acquisition of Dighi Port Ltd for a value of INR 705 cr (around $97million), alongside an investment of INR 10,000 cr (around $1375 million) to upgrade the existing port into a multi-cargo port. Such measures are further set to boost the market growth of cargo shipping industry in near future.

Increasing number of trade agreements drives the market forward:

Increasing number of favourable trade agreements in a motive towards enhancing the trade business between countries can be considered as one of the major driving factors impacting the growth of cargo shipping market. Trade agreements are essential towards helping the importers or businesses access to low cost goods at reasonable prices, making it one of the crucial factors to drive better and optimum level of sea trades. Regional trade agreements have been increasing over the years towards extending geographic reach within the last five years, including significant increase in pluri lateral agreements with negotiations, as a way behind improving bilateral relations between developed as well as developing economies across the world. In 2020, various Asia-Pacific countries including China, Japan, South Korea, Australia, New Zealand, Indonesia, Malaysia, Laos, Philippines, Thailand, Myanmar, Cambodia, Brunei, Singapore and Vietnam had signed the Regional Comprehensive Economic Partnership (RCEP), making it one of the largest free-trade agreements. This trade agreement was meant to focus at lowering tariffs, increasing investment as well as streamlining customs procedures in order to facilitate free movement of goods. Such initiatives are further set to strengthen the economic integration between these member countries, while creating more growth opportunities in the cargo shipping market in the long run.

Cargo Shipping Market Challenges

Growing incidences of cargo rollover:

Growing incidences of cargo rollover due to ocean freight supply chain issues act as one of the major challenging factors restraining the market growth of cargo shipping. Cargo rollover situations arise mainly due to growing levels of demand at times of usually low volume or traditional seasonal decline in cargo flows, which tends to create shipping delays. Owing to the increase of container demand from U.S as well as Europe terminals and carriers, the Asian port hubs witnessed a rapid surge in cargo rollover in December 2020. Prior to economic shutdowns amidst the COVID-19 pandemic, there was recovering demand from U.S and Europe during the second half of 2020, resulting in creating disruption in the container shipping sector. Moreover, growing rollover incidences result towards clogging in major ports, forcing various carriers to cancel out sailing in order to catch up with the disrupted schedules. Supply chain disruptions are further poised to continue post the pandemic situation, prior to incapability of meeting increasing shipping requirements simultaneously, thus analyzed to hamper the market growth of cargo shipping services. Additionally, shift towards alternatives like air cargo transport can also adversely impact the cargo shipping prior to ocean freight supply chain disruptions as well as port clogging issues in the long run.

Cargo Shipping Market Landscape

Product launches, acquisitions, and R&D activities are key strategies adopted by players in the Cargo Shipping market. The key players in the Cargo Shipping market include A.P Moller-Maersk Group, CMA CGM Group, Evergreen Marine, Hapag-Lloyd, Mediterranean Shipping Company S.A (MSC), China Ocean Shipping (Group) Company (COSCO), Hamburg Sud Group, Mitsui O.S.K Lines, Ltd., Pacific International Lines (PIL) and Yang Mang Marine Transport Corporation among others.

Acquisitions/Technology Launches/Partnerships

In February 2020, a container shipping company, Hapag-Lloyd had launched a remote reefer supply chain monitoring tool, named Hapag-Lloyd LIVE. Development of this real time monitoring solution was done in order to increase transparency of cold chain by providing customers with number of data sets related to condition as well as location of their reefer containers.

In March 2019, Yang Ming announced about the launch of two ultra large container vessels, namely YM Warranty and YM Wellspring, under the 14,000 TEU capacity range. These vessels were designed with a nominal capacity of 14,220 TEU, equipped with 1000 reefer plugs, capable of reaching speeds upto 23 knots.

For more Automotive Market reports — Please click here

0 notes

Text

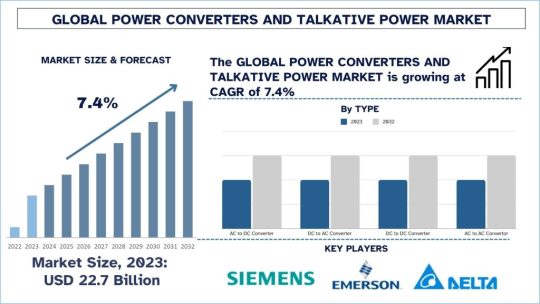

Power Converters and Talkative Power Market Soars: Driven by Electric Vehicles, Renewable Energy, and Government Support

According to the UnivDatos Market Insights analysis, the rising electric vehicles, renewable energy, and substantial government support would drive the global scenario of the Power Converters and Talkative Power market. As per their “Power Converters and Talkative Power Market” report, the global market was valued at USD 22.7 Billion in 2023, growing at a CAGR of 7.4% during the forecast period from 2024 - 2032 to reach USD XX Billion by 2032.

A converter is an electrical circuit which accepts a DC input and generates a DC output of a different voltage, usually achieved by high frequency switching action employing inductive and capacitive filter elements. A power converter is an electrical circuit that changes the electric energy from one form into the desired form optimized for the specific load. A converter can perform one or more functions to provide an output different from the input. It can be used to provide input voltage, reverse polarity, or generate multiple output voltages of same polarity, different polarity, or mixed polarity with input as in computer power supplies As renewable energy is becoming more widely accepted , growing trend of electric vehicles and energy efficient solutions are driving the market worldwide energy consumption is increasing and demand for energy conversion is high as renewable sources of will connect to the existing grid has become increasingly important.

Growing trends toward new technologies and production scale efficiencies are key contributors to increased business investments, which is another factor propelling the power converters market. The influx of investment is driven by an increased need for sustainable energy solutions in several sectors, including renewable energies, electric vehicles, and industrial automation. Globally renowned companies are focusing on R&D to develop the next generation of power conversion systems designed for enhanced efficiency, reliability, and built-in scalability. Automotive supplier Marelli is establishing a strategic relationship with power conversion company Transphorm. The partnership is intended to allow Marelli a close look at and practical experience with how high-tech products used in the electric and hybrid-electric powertrains of vehicles—including power converters or onboard chargers for EV separators and inverters—are developed.

Electric Vehicles

The global transportation sector is undergoing a tectonic shift at present, with the electric vehicle (EV) industry leading this transformation supported by technological advancements and increasing attention to environmental concerns, along with shifts in consumer preferences. Electric vehicles (EVs) have many advantages compared to conventional gasoline-powered cars, such as significantly lower greenhouse gas emissions and fuel costs, in addition to far better energy efficiency. As demand grows for EV, the demand for power converters will grow as well during the forecast period.

Request Free Sample Pages with Graphs and Figures Here https://univdatos.com/get-a-free-sample-form-php/?product_id=64868

Examples:

Volkswagen Group: The company intends to be net carbon neutral by 2050 at the latest. A new interim milestone is the targeted 40-percent reduction in CO2 emissions per vehicle in Europe by 2030 – substantially outperforming the Group target of 30 percent.

USA Inflation Reduction Act: As part of President Biden’s goal of having 50 percent of all new vehicle sales be electric by 2030, the White House is announcing public and private commitments to support America’s historic transition to electric vehicles (EV) under the EV Acceleration Challenge. President Biden’s Inflation Reduction Act adds and expands tax credits for purchases of new and used EVs—helping bring the benefits of clean energy to communities across the nation.

Government Support for Renewable Energy: Specifically, the government is promoting electric vehicles and encouraging renewable energy uptake. The global power converters' direct consumer markets gained an increase due to government support, incentives, regulations, etc. The government has subsidized clean energy and transportation technology with tax credits, grants, and subsidies. Such a factor would serve to support the expansion of the power converter market over the course of the forecast period.

Examples:

The European Union Green Deal: The European Commission has adopted a set of proposals to make the EU's climate, energy, transport and taxation policies fit for reducing net greenhouse gas emissions by at least 55% by 2030.

NEV Policy of China: The Chinese government has actively introduced various policies and standards to promote the development of the Chinese NEV industry effectively. With more than half of the world’s electric cars and having already exceeded its 2025 target for new energy vehicles (NEVs) sales, China has become a global leader in the electric vehicle (EV) industry. To further boost domestic sales in this sector, the country has now announced an extension of its tax exemption policy for NEVs. The tax break, initially set to expire in 2023, will now be extended until 2027.

Conclusion

Electric vehicles and renewable energy will be key developments for converters in the new era in global geopolitics. Electric vehicles have grown rapidly due to the next generation of technologies and the demand for sustainable mobility solutions. At the same time, the ever-increasing use of renewable generators is a reality due to downstream costs and advanced technologies, which are effective in providing stimulation planning activities and reduce carbon dioxide emissions contributing to a clean energy future.

Contact Us: