#Fuel Cell For Data Centers Fuel Cell For Data Centers Market 2022

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Women make up for the other 50% of Tumblr’s audience.

Text

The Role of Telecom Power Systems in the 5G Revolution

The global telecom power system market, valued at USD 4.9 billion in 2023, is set to experience a significant growth trajectory, reaching USD 8.0 billion by 2034, with a CAGR of 4.5% from 2024 to 2034. This growth is propelled by the rising number of mobile subscribers, expanding telecom infrastructure in rural and remote areas, and the increasing deployment of 5G technology.

Market Overview: Telecom power systems are crucial for powering telecommunication infrastructure, ensuring uninterrupted operations for base transceiver stations, data centers, and internet backbones. These systems are designed to handle power interruptions and fluctuations while supporting the demand for high-performance telecommunication networks. Advanced telecom power solutions, such as AC-DC and DC-DC power supply units (PSUs), uninterruptible power supplies (UPS), and industrial battery management systems, are gaining traction for their energy efficiency and reliability.

Access our report for a comprehensive look at key insights - https://www.transparencymarketresearch.com/telecom-power-system-market.html

Key Market Drivers

Increasing Number of Mobile Subscribers:

The growing global population and surge in internet adoption are driving the demand for mobile connectivity. Major markets like India, Indonesia, the U.S., and Brazil are leading in the number of mobile users.

The rise of IoT devices, powered by 4G and 5G, further boosts the need for robust telecom power systems.

Expansion of Telecom Infrastructure in Rural Areas:

Public and private stakeholders are investing heavily in expanding connectivity to underserved regions.

Renewable energy solutions, such as solar-powered telecom towers, are facilitating the deployment of telecom infrastructure in remote areas.

Transition to Renewable Energy:

High-efficiency telecom power systems utilizing renewable energy sources are increasingly preferred due to growing environmental concerns.

The shift to green energy solutions supports sustainability while reducing carbon emissions from telecom operations.

Key Market Trends

Shift to Hybrid Power Systems: Combining multiple power sources, such as diesel-solar and diesel-wind, to enhance reliability and sustainability.

Development of Compact Power Solutions: Introduction of space-efficient and high-performance telecom power systems for urban deployments.

Integration of Renewable Energy: Growing preference for solar and wind energy solutions to reduce dependency on fossil fuels.

Key Player Strategies

Major players in the telecom power system market are leveraging innovative strategies to maintain competitive edges:

Hitachi Energy: Secured a contract for substation automation and telecommunications systems in Brazil.

Delta Electronics: Launched the IPack65 compact outdoor rectifier system designed for 5G cell sites with dustproof and waterproof capabilities.

AcBel Polytech Inc.: Rebranded its ABB Power Conversion division to OmniOn Power, focusing on advanced power solutions.

Other notable players include ABB, Alpha Technologies, Cummins Inc., Huawei Technologies Co., Ltd., Schneider Electric, and Vertiv Group Corp. These companies emphasize product innovation, partnerships, and sustainability to strengthen their market positions.

Regional Analysis

The Asia Pacific region dominated the telecom power system market in 2023 and is expected to maintain its leadership during the forecast period. Key growth factors include:

High Mobile Penetration: China’s mobile penetration rate reached nearly 72% by the end of 2022, driving demand for telecom power solutions.

Government Initiatives: India’s Universal Service Obligation Fund (USOF) is enhancing digital services in rural areas through collaborations with organizations like Prasar Bharati and ONDC.

Other regions, such as North America, Europe, and the Middle East & Africa, are also witnessing steady growth driven by advancements in telecom technologies and increasing investments in digital infrastructure.

Market Segmentation

The telecom power system market is segmented based on:

Component: Rectifiers, inverters, converters, controllers, generators, and others (e.g., batteries, solar cells).

Grid Type: On-grid and off-grid systems.

Power Rating: Up to 10 kW, 10-20 kW, and above 20 kW.

Technology: AC and DC power systems.

Power Source: Diesel-battery, diesel-solar, diesel-wind, and multiple power sources.

Regions Covered: North America, Europe, Asia Pacific, Middle East & Africa, and South America.

Contact:Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

Expanding Horizons: Growth and Innovation in the Single Cell Genome Sequencing Market

The single cell genome sequencing market is a rapidly evolving sector within genomics research, offering unprecedented insights into the genetic makeup of individual cells. This technique enables researchers to analyze the genomic composition of a single cell, identifying unique variations and mutations that may be lost in bulk cell sequencing. Due to its critical role in understanding cellular heterogeneity, the single cell genome sequencing market has gained traction in applications such as cancer research, immunology, neurobiology, and developmental biology. This market is expected to grow significantly, driven by advances in technology, increasing applications in personalized medicine, and heightened demand for innovative genomic solutions in research and clinical diagnostics.

The Single Cell Genome Sequencing Market Size was projected to reach 5.68 billion USD in 2022, according to MRFR analysis. By 2032, it is anticipated that the single cell genome sequencing market will have grown from 6.88 billion USD in 2023 to 38.5 billion USD. The single cell genome sequencing market is anticipated to increase at a rate of about 21.09% between 2024 and 2032.

Single Cell Genome Sequencing Market Size and Share

The size of the single cell genome sequencing market has been expanding, with recent estimates suggesting it could grow at a CAGR of over 15% in the coming years. This growth is fueled by the increasing need for precision medicine and the advancement of sequencing technologies, which have made single cell sequencing more accessible and cost-effective. The market share is currently dominated by North America due to the high concentration of biotechnology firms and research institutes. However, regions like Europe and Asia-Pacific are catching up due to increased investment in healthcare infrastructure, advancements in genomics research, and government initiatives promoting precision medicine. Asia-Pacific, in particular, is expected to witness rapid growth due to a rising focus on research and development.

Single Cell Genome Sequencing Market Analysis

An analysis of the single cell genome sequencing market reveals a competitive landscape with major players such as Illumina, Inc., Thermo Fisher Scientific, 10x Genomics, and Fluidigm Corporation, who continuously innovate to improve the precision, throughput, and cost-effectiveness of their sequencing solutions. The market is segmented by application (cancer research, immunology, neurobiology, microbiology, and prenatal diagnostics), by end-user (research institutions, diagnostic centers, and pharmaceutical and biotechnology companies), and by technology (Next-Generation Sequencing, Polymerase Chain Reaction, and Microarray). Each segment provides unique growth opportunities, with cancer research applications currently holding a dominant position due to the increased focus on understanding tumor heterogeneity and developing targeted therapies.

Single Cell Genome Sequencing Market Trends

Several trends are shaping the single cell genome sequencing market. First, the integration of artificial intelligence (AI) and machine learning in genomic data analysis has accelerated the speed and accuracy of single cell sequencing, providing researchers with deeper insights into complex datasets. Second, there is a growing emphasis on multi-omics approaches that combine genomics, transcriptomics, and proteomics data to offer a more comprehensive understanding of cellular function. Third, single cell sequencing is expanding into clinical applications, especially in oncology, where it aids in identifying biomarkers for personalized treatments. Lastly, the trend toward miniaturization of sequencing instruments is making single cell genome sequencing more accessible in clinical and research laboratories worldwide.

Reasons to Buy the Report on Single Cell Genome Sequencing Market

Comprehensive Market Insights: The report offers in-depth information on the size, share, and projected growth of the single cell genome sequencing market, helping stakeholders make informed decisions.

Competitive Landscape Analysis: It includes a detailed analysis of key players and their strategies, providing valuable insights for new entrants and existing market participants.

Trend Identification: By analyzing emerging trends, the report enables businesses to capitalize on technological advancements and market shifts.

Application-Based Segmentation: The report's segmentation by application and end-user helps stakeholders identify specific growth opportunities within each segment.

Investment Insights: With data on regional market dynamics, the report serves as a valuable resource for investors looking to expand into high-growth areas.

Recent Developments in Single Cell Genome Sequencing Market

Recent developments in the single cell genome sequencing market include significant collaborations and product launches. For example, companies like Illumina and 10x Genomics have introduced high-throughput single cell analysis tools that reduce costs and improve scalability. Additionally, advancements in bioinformatics tools have made it easier to analyze complex single cell data, while collaborations between research institutions and biopharma companies are accelerating the translation of single cell sequencing insights into clinical applications. The recent shift toward cloud-based bioinformatics platforms is also noteworthy, as it enables seamless data sharing and storage, supporting global research efforts.

Related reports :

amniocentesis needle market

pet sitting market

fungal keratitis treatment market

gastrointestinal stent market

gene therapy clinical trial service market

0 notes

Text

Aptamers Market - Structure, Size, Trends, Analysis and Outlook 2030

The global aptamers market was valued at USD 1.94 billion in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 24.54% from 2023 to 2030. This rapid growth is being driven by significant advancements in the development, purification, and drug delivery systems for targeting and eliminating harmful cells, which have garnered the attention of researchers. Aptamers possess several competitive advantages over traditional antibodies, including smaller molecular size, lower immunogenicity (reduced immune response), reduced manufacturing costs, and fewer side effects. These benefits are encouraging research and development (R&D) efforts in the creation of new aptamers, fueling market expansion.

Despite considerable research, no highly effective treatments for COVID-19 have been identified, partly due to the virus's extensive genetic mutations. However, biotechnological approaches, including the use of aptamers, hold promise in combating COVID-19 infections. Nucleic acid-based aptamers and peptide aptamers are believed to offer potential therapeutic solutions for the virus, and various government initiatives are supporting the development of novel treatments for COVID-19. For example, in September 2020, the Department of Community & Economic Development awarded USD 320,000 to Aptagen LLC to fund research and development of a novel COVID-19 treatment. This investment reflects the growing recognition of aptamers' potential in addressing unmet medical needs.

Gather more insights about the market drivers, restrains and growth of the Aptamers Market

Aptamers are also proving valuable in diagnostics. Using SELEX (Systematic Evolution of Ligands by Exponential Enrichment) technology, aptamer-based diagnostic kits and assays can develop high-affinity neutralizers and bioprobes for detecting SARS-CoV-2 and other COVID-19 biomarkers. These innovations are expected to further drive market growth. For example, in December 2021, Achiko AG received approval from the Indonesian Ministry of Health for its COVID-19 diagnostic kit, Aptamex. Aptamex is a second-generation, cost-effective diagnostic tool based on DNA aptamer technology, representing an emerging solution in healthcare diagnostics.

Type Segmentation Insights:

The aptamers market is segmented into nucleic acid aptamers and peptide aptamers. In 2022, the nucleic acid aptamers segment dominated the market, holding a 78.19% share, and is expected to exhibit the highest growth during the forecast period. Many companies are actively exploring the therapeutic mechanisms of nucleic acid aptamers for treating various disorders, such as age-related macular degeneration (AMD). For instance, in June 2021, the U.S. Food and Drug Administration (FDA) granted IVERIC BIO (formerly Ophthotech Corporation) a written agreement under the Special Protocol Assessment (SPA) for the design of its phase 3 clinical trial, GATHER2. The trial aims to assess the efficacy of Zimura, a nucleic acid aptamer-based drug, for patients with geographic atrophy (GA) secondary to AMD. This FDA approval is expected to significantly bolster the growth of the nucleic acid aptamer segment.

The peptide aptamer segment is anticipated to experience substantial growth, with a projected CAGR of 22.77% from 2023 to 2030, driven by its broad applications in diagnostics and therapeutics. For instance, in August 2021, scientists from the Engineering Center for Microtechnology and Diagnostics developed an innovative biosensor for multiparametric express testing in the preclinical diagnostics of cardiovascular diseases. This testing uses next-generation biochips, which are based on a peptide aptamer marker system and molecular recognition technology. The researchers designed peptide aptamers using data from the Data Bank and Protein 3D software. The introduction of such advanced products in the market is likely to increase the utilization of peptide aptamers, contributing to the segment's growth.

In summary, the aptamers market is poised for rapid expansion due to the advantages of aptamers in therapeutic and diagnostic applications, advancements in technology, and ongoing R&D efforts. The market's growth is further supported by government initiatives, regulatory approvals, and the increasing use of aptamer-based solutions in areas such as COVID-19 treatment, diagnostics, and the management of other medical conditions.

Order a free sample PDF of the Aptamers Market Intelligence Study, published by Grand View Research.

0 notes

Text

Aptamers Market Size, Key Companies, Trends, Growth and Forecast Report, 2030

The global aptamers market size was valued at USD 1.94 billion in 2022 and is expected to grow at a compounded annual growth rate (CAGR) of 24.54% from 2023 to 2030.

Recent advancements in the generation, purification, and drug delivery for killing target cells have attracted the attention of many researchers towards aptamers due to the competitive advantages associated with them. Some of the advantages include small molecular size, low immunogenicity, low cost of manufacturing, and lesser side effects compared to antibodies; may fuel the R&D of novel aptamers, thereby driving market growth. Despite significant efforts, there are currently no highly effective treatments available against COVID-19 infections due to a large number of genetic mutations. However, biotechnological approaches appear to be promising in the treatment of COVID-19.

Consequently, nucleic-acid based aptamers & peptide aptamers might be effective against treating COVID-19 infection. Thus, various initiatives are being undertaken by the government to boost the R&D of novel treatment for COVID-19. For instance, in September 2020, the Department of Community & Economic Development awarded a contract of USD 320,000 to Aptagen LLC for the research and development of novel treatment for the COVID-19.

Gather more insights about the market drivers, restrains and growth of the Aptamers Market

Aptamers Market Report Highlights

• The nucleic acid aptamers segment dominated the market in 2022. The segment is set to grow at a rapid pace into areas such as therapeutics, diagnostics, research and development consumables, and biomarker discovery

• The research and development segment dominated the market in 2022 due to the growing interest of companies in aptamers; moreover, the rising awareness level coupled with favorable government initiatives are expected to stimulate the market growth of this applications segment during the study period

• The diagnostics segment is expected to be the fastest-growing segment during the forecast period due to the rising demand for aptamer-based diagnostic kits for the early diagnosis of diseases. For instance, in July 2021, SomaLogic and the CM Life Sciences announced the supply of 7,000-plex SomaScan Assay kits & SomaScan data to Beth Israel Deaconess Medical Center (BIDMC) for proteomics research

• North America dominated the market in 2022 due to the presence of key biopharmaceutical companies such as SomaLogic, IVERIC Bio, Inc., Aptagen LLC, Base Pair Biotechnologies, and their strategic initiatives for the development of new aptamers

Browse through Grand View Research's Biotechnology Industry Research Reports.

• The global live cell imaging market size was valued at USD 2.48 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 9.0% from 2024 to 2030.

• The global market for cell-free protein expression reached a value of USD 267.4 million in 2023 and is projected to grow at a CAGR of 8.6% from 2024 to 2030.

Aptamers Market Segmentation

Grand View Research has segmented the global aptamers market on the basis of type, application, and region:

Aptamers Type Outlook (Revenue, USD Million; 2018 - 2030)

• Nucleic Acid Aptamer

• Peptide Aptamer

Aptamers Application Outlook (Revenue, USD Million; 2018 - 2030)

• Diagnostics

• Therapeutics

• Research & Development

• Others

Aptamers Regional Outlook (Revenue, USD Million; 2018 - 2030)

• North America

o U.S.

o Canada

• Europe

o Germany

o UK

o France

o Italy

o Spain

o Denmark

o Sweden

o Norway

• Asia Pacific

o Japan

o China

o India

o Australia

o Thailand

o South Korea

• Latin America

o Brazil

o Mexico

o Argentina

• MEA

o South Africa

o Saudi Arabia

o UAE

o Kuwait

Order a free sample PDF of the Aptamers Market Intelligence Study, published by Grand View Research.

#Aptamers Market#Aptamers Market size#Aptamers Market share#Aptamers Market Analysis#Aptamers Industry

1 note

·

View note

Text

Personalized Medicine Market Size, Share & Review 2024-2030

Personalized Medicine Industry Overview

The global personalized medicine market was valued at USD 529.28 billion in 2023 and is projected to grow at a CAGR of 8.20% from 2024 to 2030. The personalized medicine market is driven majorly by the growing demand for novel drug discovery to combat the rising incidence of cancers and other diseases across the globe. Moreover, numerous collaborations among researchers and market players are also anticipated to have a positive impact on the personalized medicine market growth.

For instance, in February 2023, Roche extended its partnership with Janssen Biotech Inc., intensifying efforts in the development of companion diagnostics for targeted therapies. This expanded collaboration encompasses various precision technologies, such as immunohistochemistry, digital pathology, next-generation sequencing, polymerase chain reaction, and immunoassays, fostering advancements in research and innovation

Gather more insights about the market drivers, restrains and growth of the Personalized Medicine Market

One of the most important factors expected to have a significant impact on the market is how much and to what extent the growth of Next-Generation Sequencing (NGS) will affect the adoption of personalized medicine(PM) in the coming seven years. The exponentially decreasing cost of sequencing whole genomes and technological advancements in NGS in a way with Moore’s law for semiconductors in the field of life sciences. For instance, as per the Medical Device Network article published in 2023, sequencing costs have significantly decreased over time as a result of increased competition and advancements in technology.

The increasing prevalence of rare diseases is also anticipated to boost the demand for growth of the market. The increasing level of understanding and correlation of characteristics of the human genome paved the way for efforts in devising various precision medicine and therapeutic exercises. For instance, in September 2022, a research study carried out at the University of California at Irvine, proposed a novel technique for the management of inherited retinal diseases (IRDs) by using precision genome editing that is very specific to an individual’s requirements.

Companion diagnostics are tests or assays that are specifically designed to identify biomarkers for patient stratification, ensuring that the right patients receive the right therapies at the right time. Many companies are embracing this approach to tailor treatments based on individual patient characteristics, optimizing therapeutic outcomes while minimizing potential adverse effects. For instance, in November 2023, Foundation Medicine announced a partnership with Pierre Fabre Laboratories aimed at advancing the development of FoundationOneCDx and FoundationOneLiquidCDx, which are high-quality genomic tests. The goal is to establish these tests as companion diagnostics for novel targeted therapies designed to treat individuals diagnosed with Non-Small Cell Lung Cancer (NSCLC).

Personalized medicine is poised to reshape the healthcare landscape in the coming years, fueled by four prominent trends. This evolution is driven by decision support techniques utilizing the potential of the human genome, the integration of big data analytics and machine learning in healthcare practices, reimbursement strategies promoting preventative care within health systems, and the introduction of advanced tools facilitating increased data accessibility and interoperability. For instance, in June 2023, Dartmouth inaugurated its Center for Precision Health and Artificial Intelligence (CPHAI) propelled by an initial USD 2 million funding. CPHAI is dedicated to advancing interdisciplinary research exploring the application of artificial intelligence and biomedical data in enhancing personalized medicine and health outcomes. Emphasizing the importance of maintaining ethical standards in health AI, the center aims to leverage AI's transformative potential in addressing real-world clinical challenges, improving patient outcomes, and ensuring equitable healthcare access.

Browse through Grand View Research's Biotechnology Industry Research Reports.

The global plasmid purification market size was estimated at USD 1.72 billion in 2023 and is projected to grow at a CAGR of 11.60% from 2024 to 2030.

The global enzymatic DNA synthesis market size was estimated at USD 232.4 million in 2023 and is projected to grow at a CAGR of 26.4% from 2024 to 2030.

Key Personalized Medicine Company Insights

Some key players operating in the market include Abbott; GE Healthcare., Inc.; Illumina, Inc., and Danaher Corporation. Established players focus majorly on innovation & technology advancements to develop cutting-edge diagnostic solutions and partner with emerging players to leverage their technology. Mature players also have a strong global presence with a diverse portfolio of genetic testing products and a well-established brand reputation which gives them a competitive edge.

Emerging players however focus on launching products in limited countries and then expanding regionally. Some operating strategies also include strategic partnerships, acquisitions, or collaborations to enhance their capabilities and market presence. Additionally, these players may be more flexible and agile than established players in terms of responding and changing to market needs and demand, allowing them to quickly adapt and develop new technologies.

Key Personalized Medicine Companies:

The following are the leading companies in the personalized medicine market. These companies collectively hold the largest market share and dictate industry trends.

GE Healthcare

Illumina, Inc.

ASURAGEN, INC.

Abbott

Dako A/S

Exact Sciences Corporation

Danaher Corporation (Cepheid, Inc.)

Decode Genetics, Inc.

QIAGEN

Exagen Inc.

Precision Biologics

Celera Diagnostics LLC.

Biogen

Genelex

International Business Machines Corporation (IBM)

Genentech, Inc.

23andMe, Inc.

Recent Developments

In September 2023, A Memorandum of Understanding (MOU) was signed by Agilent Technologies & Advanced Cell Therapy and Research Institute, Singapore (ACTRIS) to advance in gene and cell therapy over the next 3 years.

In July 2023, As a part of Illumina's oncology product portfolio, Pillar Biosciences and Illumina formed a strategic partnership to commercialize Pillar's suite of oncology assays worldwide. Completing the agreement will lead to an unparalleled offering of additional Next-Generation Sequencing (NGS) solutions, improving patient access to personalized cancer treatment solutions.

In June 2023, GE Healthcare and DePuy Synthes signed a distribution agreement to expand the reach of OEC 3D Imaging System and product offerings of DePuy Synthes to more surgeons & patients in the U.S.

In June 2023, Exact Sciences Corp. collaborated independently with two distinguished healthcare institutions at the forefront of cancer research. The agreements seek to increase access to genomic information in order to enhance patient care.

Order a free sample PDF of the Personalized Medicine Market Study, published by Grand View Research.

0 notes

Text

Exosomes Market Size: Technological Advancements and Impacts

The Exosomes Market size was estimated USD 113.3 million in 2022 and is expected to reach USD 1076.35 million by 2030 at a CAGR of 32.5% during the forecast period of 2023-2030.The exosomes market is rapidly gaining traction as these small extracellular vesicles hold immense potential in diagnostics and therapeutics. With the ability to facilitate intercellular communication, exosomes are being explored for their roles in cancer treatment, regenerative medicine, and drug delivery systems. Advances in exosome isolation and characterization techniques are driving the market's growth, while increasing investment in research and development by pharmaceutical and biotech companies is further fueling innovation.

Get Sample Of This Report @ https://www.snsinsider.com/sample-request/4091

Market Scope & Overview

The market report gives thorough information to help readers comprehend the current situation of the industry. The report relied on primary and secondary research, as well as private databases and a paid data source. The market research report sheds light on the history and future of the Exosomes Market business. The report analyses the market size and includes information on market drivers, limitations, and opportunities.

The market research report examines the primary strategies used by top industry players to advance their operations in the worldwide market while maintaining a competitive advantage over their competitors. The Exosomes Market study also depicts the competitive landscape of the industry's major competitors, as well as the top organizations’ percentage market share.

Market Segmentation Analysis

By Product

Kits & Reagents

Instruments

Services

By Workflow

Isolation Methods

Ultracentrifugation

Immunocapture on beads

Precipitation

Filtration

Others

Downstream Analysis

Cell surface marker analysis using flow cytometry

Protein analysis using blotting & ELISA

RNA analysis with NGS & PCR

Proteomic analysis using mass spectroscopy

Others

Cancer

Neurodegenerative diseases

Cardiovascular diseases

Infectious diseases

Others

By End User

Pharmaceutical & biotechnology companies

Hospitals & diagnostics centers

Academic & research institutes

COVID-19 Pandemic Impact Analysis

In this Exosomes Market analysis, the impact of COVID-19 on the market is analyzed at both the global and country levels. According to this analysis, the COVID-19 pandemic and the post-pandemic phase had a significant impact on both the supply and demand sides of the market.

Regional Outlook

The report's accurate data will help market participants make informed decisions about regional expansions and investments. The report looks at the dynamics of the Exosomes Market in relation to worldwide market conditions.

Competitive Analysis

The data in this section will assist readers in understanding the primary strategies used by leading market players to control the global Exosomes Market . The research report includes a PORTER, SVOR, and PESTEL analysis, as well as an examination of the potential impact of microeconomic market variables. External and internal elements that are projected to have an impact on the company have been studied, presenting decision-makers with a clear picture of the industry's future.

Key Questions Answered in the Exosomes Market Report

What is the forecasted growth rate, market share, and m market size?

Who are the market's dominant players, and how have they gained a competitive advantage over their competitors?

Conclusion

The Exosomes Market research report's estimations and estimates examine the impact of different political, social, and economic factors, as well as current market conditions, on market growth. All of this important information will assist the reader in better understanding the market.

About US

SNS Insider is a market research and insights firm that has won several awards and earned a solid reputation for service and strategy. We are a strategic partner who can assist you in reframing issues and generating answers to the trickiest business difficulties. For greater consumer insight and client experiences, we leverage the power of experience and people.

When you employ our services, you will collaborate with qualified and experienced staff. We believe it is crucial to collaborate with our clients to ensure that each project is customized to meet their demands. Nobody knows your customers or community better than you do. Therefore, our team needs to ask the correct questions that appeal to your audience in order to collect the best information.

Related Reports

Genomics Services Industry

Analgesics Industry

Immunomodulators Industry

Glaucoma Therapeutics Industry

DNA Synthesis Industry

0 notes

Text

Navigating the Telecom Power System Market: Global Industry Outlook

Increasing demand for compact and modular telecom power systems and the growing adoption of virtualization in telecom power systems are likely to drive the Market in the forecast period.

According to TechSci Research report, “Telecom Power System Market – Global Industry Size, Share, Trends, Competition Forecast & Opportunities, 2028”, the Global Telecom Power System Market is experiencing a surge in demand in the forecast period. A primary driver propelling the global Telecom Power System market is the widespread deployment of 5G technology. The advent of 5G has ushered in a new era of connectivity, offering faster data speeds, reduced latency, and increased network capacity. The implementation of 5G networks requires a significant upgrade of telecom infrastructure, driving the demand for advanced Telecom Power Systems. These systems play a pivotal role in providing the reliable and efficient power necessary to support the denser network of small cells characteristic of 5G deployment.

Telecom Power Systems must adapt to the unique requirements of 5G, accommodating the increased number of small cells and ensuring seamless integration into diverse environments. As the global demand for higher data speeds and enhanced connectivity continues to grow, the deployment of 5G technology acts as a potent driver, pushing the Telecom Power System market to innovate and evolve to meet the challenges of this next-generation network.

The exponential growth of the Internet of Things (IoT) is a significant driver fueling the global Telecom Power System market. The increasing prevalence of connected devices, from smart sensors to industrial machinery, demands a robust and reliable telecommunication infrastructure. Telecom Power Systems play a critical role in supporting the communication needs of IoT applications, providing the necessary power to base stations and data centers.

As industries across sectors embrace IoT for improved efficiency and real-time monitoring, the demand for Telecom Power Systems that can handle the unique challenges posed by IoT deployments is on the rise. These power systems must be scalable, energy-efficient, and capable of adapting to the diverse needs of IoT, contributing to the seamless integration and functionality of connected devices. The proliferation of IoT applications worldwide acts as a driving force, compelling Telecom Power System providers to develop innovative solutions to meet the evolving demands of this interconnected era.

Browse over XX Market data Figures spread through XX Pages and an in-depth TOC on "Global Telecom Power System Market.” https://www.techsciresearch.com/report/telecom-power-system-market/23070.html

The Global Telecom Power System Market is segmented into grid type, component, power source, and region.

Based on grid type, The On Grid segment held the largest Market share in 2022. On-Grid systems are well-suited for urban and developed areas where the power grid infrastructure is stable and reliable. In these regions, there is a consistent and uninterrupted power supply, making on-grid solutions a cost-effective and practical choice.

Connecting telecom infrastructure to an existing power grid is often more cost-effective than setting up independent power systems. The infrastructure is already in place, reducing the need for additional investment in off-grid or backup power solutions.

On-Grid systems benefit from the reliability and consistency of power supply from the main electrical grid. Telecom operations in areas with a stable grid connection experience minimal disruptions, ensuring continuous communication services.

Maintenance and servicing of on-grid power systems are generally more straightforward. The infrastructure is readily accessible, and any issues can be addressed without the complexity associated with off-grid solutions, where remote locations may pose logistical challenges.

In regions where the cost of energy from the grid is competitive or economical, telecom operators may opt for on-grid solutions. The availability of affordable grid electricity can make on-grid Telecom Power Systems a financially viable choice.

Regulatory frameworks and permitting processes often favor on-grid solutions, especially in urban areas. Connecting to the existing power grid may involve fewer regulatory hurdles compared to establishing off-grid or hybrid solutions with renewable energy sources.

On-Grid systems offer scalability, allowing telecom operators to easily expand their networks without significant modifications to the power infrastructure. This scalability is particularly beneficial in densely populated urban areas experiencing high demand for telecommunication services.

Based on power source, The diesel-Battery segment held the largest Market share in 2022. Diesel generators are known for their reliability and can provide a constant power supply. This is crucial for telecom infrastructure, where uninterrupted power is essential to ensure continuous communication.

Diesel generators can operate in various environmental conditions, making them suitable for telecom installations in diverse locations, including remote or challenging terrains.

Diesel generators can operate for extended periods without refueling, providing an autonomous power source. This is particularly important in areas with unreliable or no access to the electrical grid.

Combining diesel generators with battery systems allows for better energy management. Batteries can store excess energy generated by the diesel generator and release it during peak demand or in case of generator failure, providing a seamless power supply.

Modern diesel generators are designed to be fuel-efficient, reducing operational costs over time. The combination of diesel and battery systems allows for optimization of fuel usage.

While diesel generators are known for their emissions, advancements in technology have led to more fuel-efficient and environmentally friendly models. Additionally, the integration of battery systems helps reduce reliance on diesel power during periods of lower demand.

In regions with unreliable or underdeveloped power grids, telecom installations often need to operate independently. Diesel-battery systems provide a reliable off-grid solution.

Major companies operating in the Global Telecom Power System Market are:

Huawei Technologies Co., Ltd.

Ericsson AB

Nokia Corporation

ABB Ltd.

Emerson Electric Co.

Siemens AG

Eaton Corporation PLC

Schneider Electric SE

Hitachi Ltd.

Samsung Electronics Co., Ltd.

Download Free Sample Report https://www.techsciresearch.com/sample-report.aspx?cid=23070

Customers can also request for 10% free customization on this report.

“The Global Telecom Power System Market is expected to rise in the upcoming years and register a significant CAGR during the forecast period. The growth of the telecom power systems market is being driven by several factors, including the increasing demand for reliable and efficient power systems for telecommunications networks, the growing adoption of 5G networks, and the increasing need for renewable energy sources. Also, The Asia Pacific region is expected to be the fastest-growing market for telecom power systems, due to the rapid growth of the telecommunications industry in the region.

The Middle East and Africa region is also expected to witness significant growth, as countries in the region invest in upgrading their telecommunications infrastructure. The telecom power systems market is a fragmented market, with a large number of players. Some of the leading players in the market include Huawei, Ericsson, Nokia, ABB, and Emerson Electric. Therefore, the Market of Telecom Power System is expected to boost in the upcoming years.,” said Mr. Karan Chechi, Research Director with TechSci Research, a research-based management consulting firm.

“Telecom Power System Market - Global Industry Size, Share, Trends, Opportunity, and Forecast, 2018-2028 Segmented By Grid Type (On Grid, Off Grid, Bad Grid), By Component (Rectifier, Inverter, Converter, Controller, Heat Management Systems, Generators, Others), By Power Source (Diesel-Battery, Diesel-Solar, Diesel-Wind, Multiple Sources), By Region, By Competition”, has evaluated the future growth potential of Global Telecom Power System Market and provides statistics & information on Market size, structure and future Market growth. The report intends to provide cutting-edge Market intelligence and help decision-makers make sound investment decisions., The report also identifies and analyzes the emerging trends along with essential drivers, challenges, and opportunities in the Global Telecom Power System Market.

Browse Related Reports

Air-Operated Grease Market https://www.techsciresearch.com/report/air-operated-grease-market/23568.html

Portable Grease Pumps Market https://www.techsciresearch.com/report/portable-grease-pumps-market/23569.html

Industrial Belt Drives Market https://www.techsciresearch.com/report/industrial-belt-drives-market/23573.html Contact Us-

TechSci Research LLC

420 Lexington Avenue, Suite 300,

New York, United States- 10170

M: +13322586602

Email: [email protected]

Website: www.techsciresearch.com

#Telecom Power System Market#Telecom Power System Market Size#Telecom Power System Market Share#Telecom Power System Market Trends#Telecom Power System Market Growth

0 notes

Text

Flexible Graphite Bipolar Plates for Fuel Cells, Global Market Size Forecast, Top 9 Players Rank and Market Share

Flexible Graphite Bipolar Plates for Fuel Cells Market Summary

Flexible graphite bipolar plates are an important component in fuel cells. They play a crucial role in facilitating the electrochemical reactions that occur within the fuel cell, as well as providing structural support and gas flow channels.

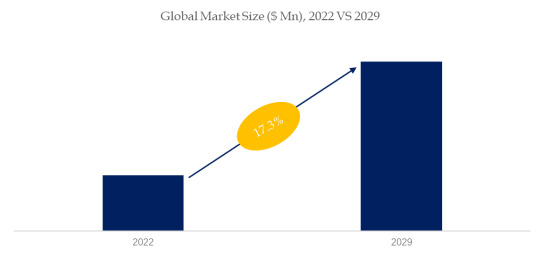

According to the new market research report “Global Flexible Graphite Bipolar Plates for Fuel Cells Market Report 2023-2029”, published by QYResearch, the global Flexible Graphite Bipolar Plates for Fuel Cells market size is projected to reach USD 0.22 billion by 2029, at a CAGR of 17.3% during the forecast period.

Figure. Global Flexible Graphite Bipolar Plates for Fuel Cells Market Size (US$ Million), 2022VS2029

Above data is based on report from QYResearch: Global Flexible Graphite Bipolar Plates for Fuel Cells Market Report 2023-2029 (published in 2023). If you need the latest data, plaese contact QYResearch.

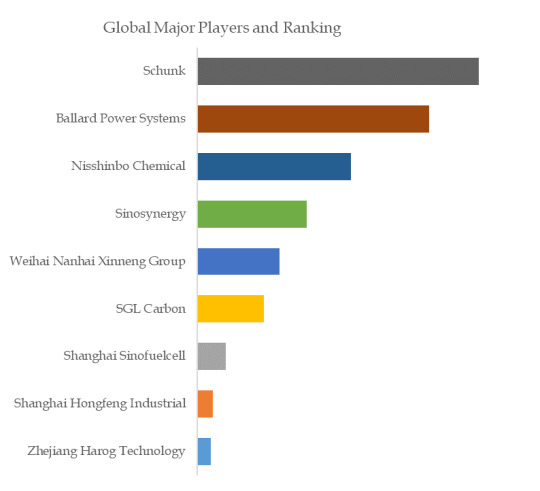

Figure. Global Flexible Graphite Bipolar Plates for Fuel Cells Top 9 Players Ranking and Market Share (Ranking is based on the revenue of 2022, continually updated)

Above data is based on report from QYResearch: Global Flexible Graphite Bipolar Plates for Fuel Cells Market Report 2023-2029 (published in 2023). If you need the latest data, plaese contact QYResearch.

According to QYResearch Top Players Research Center, the global key manufacturers of Flexible Graphite Bipolar Plates for Fuel Cells include Schunk, Ballard Power Systems, etc. In 2022, the global top three players had a share approximately 51.0% in terms of revenue.

Market Drivers:

Electrical conductivity: Flexible graphite bipolar plates exhibit excellent electrical conductivity, allowing for efficient electron transfer within the fuel cell. This helps to maximize the power output and overall efficiency of the fuel cell system.

Corrosion resistance: Flexible graphite is highly resistant to corrosion, making it ideal for use in the harsh operating conditions of fuel cells, such as high temperatures and corrosive electrolytes. This ensures the longevity and reliability of the bipolar plates.

Gas permeability: The structure of flexible graphite allows for the efficient passage of gases, such as hydrogen and oxygen, through the bipolar plates. This enables uniform distribution of reactant gases across the electrode surfaces, enhancing the overall performance of the fuel cell.

Restraint:

Graphite bipolar plates were the earliest commercially applied bipolar plates, but they have disadvantages such as large thickness and low mechanical strength. In recent years, with technological progress, metal bipolar plates have become an emerging product of bipolar plates, and the industry's prosperity has been continuously improving. Metal bipolar plates have the advantages of low production cost, light weight, and high mechanical strength. With the acceleration of automotive lightweighting, metal bipolar plates, as high-end fuel cell bipolar plates, have continuously increased their market share, reaching 53.6% in 2022, which has brought certain impacts to the development of the graphite bipolar plate industry.

About The Authors

Yunmei Sun---Lead Author

Email: [email protected]

Sun Yunmei has 2 years of industry research experience, focusing on research in the chemical industry chain related fields, including medical grade reagents, high-purity reagents for semiconductors, and chemical laboratory equipment.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 16 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting, industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

0 notes

Text

Solid Oxide Fuel Cell Market to Observe Highest Growth in APAC

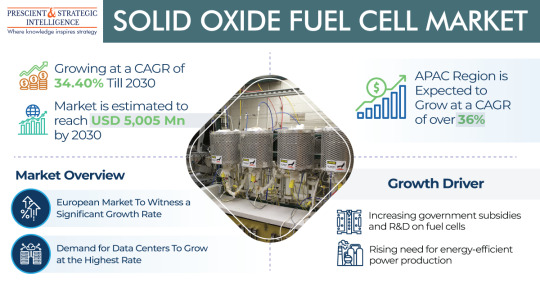

The solid oxide fuel cell market was USD 470 million in 2022, which will rise to USD 5,005 million, advancing at a 34.4% compound annual growth rate, by 2030.

This is because of its superior and cost efficiencies, rising government subsidies & R&D on fuel cells, fuel flexibility & long-term stability, stringent pollution regulations, and the increasing requirement for energy-efficient energy generation.

The rising strictness of government rules as well as the increasing energy charges is a major trend being witnessed in this industry.

With the rising consciousness of alternative power sources, combustion-based energy generators are being substituted by renewable power systems like solar panels, which demonstrate greater efficiency in power conversion.

Additionally, the fuel cells employed in these devices don’t cause any dangerous emissions, as a result, these are ideal for use in backup or stationary, portable power, and transportation.

The planar category, on the basis of type, was the larger contributor to the industry, with over 60% share, and it is likely to retain this position in the years to come. This can be mainly because of its ease of geometry, low operating expense, and relatively simpler construction process.

In 2022, the stationary category, based on application, was the largest contributor to the solid oxide fuel cell market, and it is likely to remain the largest during this decade. This can be because of the rising emphasis on fuel cells driven by hydrogen for backup energy, and the stationary solid oxide fuel cell technique is one of the most efficient and purest electricity & heat generation technologies.

In 2022, the data centers category, on the basis of end user, held a revenue share, of over 38%, and it will propel at the highest rate in the coming years. This is because data centers are extremely power-consuming as well as power-intensive, and these require a constant supply of power to avoid data loss.

North America was the largest contributor to the industry in 2022, and it is likely to remain the largest in the years to come. This can be ascribed to the robust backing of government initiatives and policies, including the Department of Energy’s Solid-State Energy Conversion Alliance programs.

APAC is likely to advance at the highest compound annual growth rate in the years to come. This will be because the governments of Japan, South Korea, and China are positively concentrating on employing renewable power and, therefore, choosing utility-scale solid oxide fuel cell (SOFC) power plants.

With the increasing requirement for energy-efficient energy production, the solid oxide fuel cell industry will advance continuously in the coming years.

Source: P&S Intelligence

#Solid Oxide Fuel Cell Market Share#Solid Oxide Fuel Cell Market Size#Solid Oxide Fuel Cell Market Growth#Solid Oxide Fuel Cell Market Applications#Solid Oxide Fuel Cell Market Trends

1 note

·

View note

Text

Liquid Biopsy Market Size-Share, Growth Factors, Forecast 2023-2030

The Global Liquid Biopsy Market size is expected to grow from USD 1.59 billion in 2022 to USD 7.02 billion by 2030, at a CAGR of 20.4% during the forecast period (2023-2030).

The liquid biopsy market has witnessed substantial growth in recent years, driven by advancements in cancer diagnostics and personalized medicine. Unlike traditional biopsy methods, liquid biopsy offers a non-invasive approach to detect and monitor various conditions, particularly cancer, by analyzing circulating tumor DNA (ctDNA), circulating tumor cells (CTCs), and other biomarkers present in blood or other bodily fluids. The market's growth is propelled by the rising incidence of cancer, increased emphasis on early detection, and the growing adoption of precision medicine.

Request Sample Copy@:

https://introspectivemarketresearch.com/request/16300

Leading Key Players Covered Liquid Biopsy Market: -

F. Hoffmann-La Roche Ltd. (Switzerland), Myriad Genetics Inc. (US), QIAGEN N.V. (Netherlands), Thermo Fisher Scientific Inc. (the US), Guardant Health Inc. (the US), BIOCEPT Inc. (the US), Illumina Inc. (the US), Angle plc (UK), Oncimmune(UK), Lucence health Inc. (US), FreenomeHoldings Inc. (US) and Other Major Players.

Market Driver:

One key driver fueling the liquid biopsy market is the demand for less invasive and more accessible diagnostic methods. Traditional biopsies are often invasive, requiring surgical procedures that can be uncomfortable and carry potential risks. Liquid biopsies, on the other hand, offer a minimally invasive alternative, reducing patient discomfort and complications. This non-invasiveness enhances patient compliance and enables the monitoring of disease progression over time. As a result, liquid biopsies are increasingly becoming the preferred choice for cancer screening and monitoring, contributing significantly to the market's expansion.

Market Opportunity:

A significant market opportunity lies in the integration of liquid biopsy technologies with artificial intelligence (AI) and machine learning (ML) algorithms. The vast amount of data generated by liquid biopsy tests can be effectively analyzed and interpreted using these advanced technologies. AI and ML can enhance the accuracy of diagnosis, identify subtle biomarker patterns, and provide valuable insights for personalized treatment strategies. Integrating liquid biopsy with AI not only improves the diagnostic capabilities but also opens avenues for predictive and preventive healthcare. This convergence presents a promising opportunity for companies to develop innovative solutions that combine molecular diagnostics with cutting-edge data analytics.

Segmentation of Liquid Biopsy Market: -

By Cancer Type

By Circulating Biomarker

By End-User

If You Have Any Queries Regarding Liquid Biopsy Market, Please Visit:

https://introspectivemarketresearch.com/inquiry/16300

Owning our reports (For More, Buy Our Report) will help you solve the following issues:

1. Uncertainty about the future?

Our research and insights help our clients to foresee upcoming revenue pockets and growth areas. This helps our clients to invest or divest their resources.

2. Understanding market sentiments?

It is imperative to have a fair understanding of market sentiments for a strategy. Our insights furnish you with a hawk-eye view on market sentiment. We keep this observation by engaging with Key Opinion Leaders of a value chain of each industry we track.

3. Understanding the most reliable investment centers?

Our research ranks investment centers of the market by considering their returns, future demands, and profit margins. Our clients can focus on the most prominent investment centers by procuring our market research.

4. Evaluating potential business partners?

Our research and insights help our clients in identifying compatible business partners.

Acquire This Report: -

https://introspectivemarketresearch.com/checkout/?user=1&_sid=16300

About us:

Introspective Market Research (introspectivemarketresearch.com) is a visionary research consulting firm dedicated to helping our clients grow and successfully impact the marketplace. Our team at IMR is ready to help our clients grow their businesses by offering strategies to achieve success and monopoly in their respective fields. We are a global market research company, specializing in the use of big data and advanced analytics to gain a broader picture of market trends. We help our customers to think differently and build a better tomorrow for all of us. As a technology-driven research company, we consider extremely large data sets to uncover deeper insights and provide conclusive consulting. We don't just provide intelligence solutions, we help our clients achieve their goals.

Contact us:

Introspective Market Research

3001 S King Drive,

Chicago, Illinois

60616 USA

Ph no: +1-773-382-1049

Email: [email protected]

#Liquid Biopsy Market#Liquid Biopsy Market Size#Liquid Biopsy Market Share#Liquid Biopsy Market Growth#Liquid Biopsy Market Trend#Liquid Biopsy Market segment#Liquid Biopsy Market Opportunity#Liquid Biopsy Market Analysis 2022#US Liquid Biopsy Market#Liquid Biopsy Market Forecast#Liquid Biopsy Industry#Liquid Biopsy Industry Size

0 notes

Text

Fuel Cell Generator Market Is Driven by Minimalization of Carbon Residues

The size of the fuel cell generator market was USD 330 million in 2022, and the figure is set to rise at a CAGR of 17.50% from 2022 to 2030 and reach USD 1,199 million by the end of this decade.

There are several reasons for this development, including the minimalization of CO2 emissions, the easy availability of fuel cells, and their ability to renew energy. The snowballing need for the production of clean power along with minimal releases from CO2 will drive the market.

Numerous regions and nations throughout the globe are targeting to decrease overall releases of CO2 to zero by 2050, To achieve CO2 neutrality. The government's focus has amplified on making a decarbonized civilization in the past few years. To achieve this aim, the introduction of renewable sources, including solar, biomass, hydro, wind, and geothermal, is vital.

The production of electricity with the support of solar and wind has a few drawbacks, like the lack of ability to regulate the generation and huge quantity of output disparities reliant on weather conditions.

Aquaculture is the fastest-rising end-user developing at a CAGR of approximately 19.2%, credited to the increasing quantity of aquaculture amenities and increasing ecological impacts related to it such as the consumption of electricity and water. Mainly to lessen the environmental effects, governments have taken numerous steps to utilize fuel cell-based generators as an alternative to diesel generators.

North America is dominating the fuel cell generator market and is projected to continue with this dominance throughout the decade. This can be ascribed to the growing concentration and fast acceptance of clean sources.

In North America, the U.S. is leading the market, and it will develop with a CAGR of 18.1%, credited to solid economic support. The innovative growth in the usage of renewable sources and snowballing electricity needs from the aquaculture and data centers industry are the major reasons that will boost the industry in the future as well.

Hence, the minimalization of CO2 emissions, the easy availability of fuel cells, and their ability to renew energy are the major factors contributing to the growth of the fuel cell generator market.

#Fuel Cell Generator Market#Market Trends#Fuel Cell Technologies#Clean Power Generation#Backup Power Systems#Mobile Applications#Market Dynamics#Key Players#Emerging Opportunities#Energy Solutions#Telecommunications#Automotive Industries#Sustainability#Resilience#Decentralized Power Generation

0 notes

Text

Top Trends in Fleet Management Software 2023

Fleet industry is on the boom around the world. The fleet management market is anticipated to increase from USD 25.5 billion in 2022 to USD 52.4 billion by 2027, according to a recent Markets and Markets research. In the post-pandemic environment, the fleet management sector has advanced faster as businesses adopt new digital trends to boost productivity and cut expenses. New options are presented by service providers like white label GPS tracking software to cater to the varying needs of businesses.

Let us look at some of the top trends Fleet Management System trends of 2023.

1) Growing Adoption of Autonomous and Electronic Vehicles

As more businesses release high-end versions that improve communication through greater data sharing and sophisticated fleet software, EV usage is anticipated to increase even further in 2023. The global market for zero-emission trucks is expected to increase quickly over the following ten years, according to an IDTechEx analysis titled "Electric and Fuel Cell Trucks 2023-2043." By 2043, the market for medium- and heavy-duty zero-emission trucks will be valued more than $200 billion a year.

As the sector lessens its reliance on diesel-powered cars and transitions to electronic and autonomous fleets, technology like fleet management software will be crucial in assisting organizations in achieving their sustainability goals.

2) Greater General Safety

Advancements in GPS tracking software will lead to an increased focus on safety resulting in more innovation related to it. To lower risks and accidents, key elements including geofencing, driver behavior, alarm systems, and others will be strengthened. Accurate vehicle and driver activity notifications are anticipated to be sent by intelligent monitoring systems. Additionally, deeper insights and reports will help you find flaws in your safety-related operations and fix them.

3) Pay attention to telematics tracking

Fleet managers will use telematics and GPS fleet tracking to for achieving real-time diagnostics. In addition to knowing the status of their vehicles and tracking the whereabouts of their fleet drivers, they can also make sure that they are adhering to safety procedures. With new features like voice integration, improved Artificial Intelligence (AI), and sophisticated data analytics, tracking solutions will improve in 2023. In modern GPS tracking software, In-cab video is amongst the most popular emerging technologies.

4) Remote Fleet Administration

The COVID-19 epidemic has put remote fleet management at the center of transportation operations. Fleet managers are concentrating on new approaches to handle activities in a remote setting and track the efficiency of their fleet drivers. With the use of efficient fleet management software, managers can better interact with their team, track statistics in real-time, and communicate with their executives.

5) Additional Data Security

Fleet vehicles contain a substantial amount of confidential information that must be safeguarded. Fleet managers will concentrate on enhancing their cybersecurity measures in 2023. Many fleet managers are upskilling in IT to take on fresh tasks and moving their attention from tactical to strategic management. As data visibility rises, they will concentrate more on gathering and analyzing data.

6) Mobility-as-a-Service (MaaS) to Emerge Mobility-as-a-Service

MaaS will grow in prominence as fleet managers can tailor their services and modify their conventional methodology. According to estimates, the size of the worldwide MaaS market would rise from USD 52.56 billion in 2019 to USD 280.77 billion in 2027.

Fleet managers may try leasing or even using company-owned vehicles. MaaS will assist fleet managers in reevaluating existing fleet management procedures. Businesses may better utilize idle vehicles, manage costs, and lower their carbon footprint by embracing vehicle sharing. The most important fleet metrics will change as well, moving away from vehicle counts and statistics and towards things like timing, trip success rates, attendance rates, and annual cost.

7) The development of 5G networks

The top trend this year will be 5G fleet management. Fleets will be able to take advantage of 5G's key characteristics to improve productivity and decrease latency. The reach of tracking solutions will change as a result of the development of this technology resulting in more productivity. Employees can receive instructions from managers in real-time, which improves the overall operational productivity. With 5G widely available everywhere, now is the ideal time to invest in best white label GPS tracking software to maximize productivity and stay ahead of the competition.

Businesses that use a fleet management app will gain from 5G's enhanced coverage and productivity since it will improve communication. According to estimates, 5G signals can travel 20 times quicker than 4G. The developed nations of the globe already have 5G. However, it will be spreading worldwide in 2023-2024.

8) Increased Traffic Safety Procedures

Due to the pandemic, fleet owners and managers will concentrate on fleet and driver security. They will prioritize driver safety by tightening sanitization controls during vehicle inspections and ensuring they have the necessary equipment. Modern white label GPS tracking software can also be used to ensure that safety protocols are met by the staff. This will benefit your drivers and employees and show that you are ready to reduce risks and virus exposure.

Achieving fuel efficiency and cutting down fuel expense will be a main concern for commercial fleets in 2023 due to a record-high rise in diesel prices. In 2023, the fleet industry will experience advancements in technology and stronger tech integration, which will enhance the capabilities of GPS tracking software. Utilizing fleet management software will improve fleet tracking and management and operational efficiency.

Are you trying to find the best white label GPS tracking software for cars? Flotilla IoT is the ideal choice for you.

0 notes

Text

According to a new market research report "Fuel Cell Market by Type (PEMFC, SOFC, PAFC, MFC, DMFC, AFC), Application (Portable, Stationary, Vehicles (FCV)), Size (Small & Large), End User (Residential, C&l, Transportation, Data Center, Military & Defense, Utility), Region - Global Forecast to 2027", The global fuel cell market size is estimated to be USD 2.9 billion in 2022 and projected to reach USD 9.1 billion by 2027, at a CAGR of 26.0%. The emissions from vehicles account for more than 15% of the global greenhouse emissions. Hence, governments all over the world are finding alternative power sources for use in the transportation sector. The adoption of fuel cell vehicles (FCVs) in the sector is expected to increase in the near future, as there is zero owing to the absence of CO2 emissions during vehicle operation. Therefore, many automotive manufacturers are making considerable investments to incorporate fuel cell vehicles in their product offerings.

0 notes

Text

Fuel Cell For Data Centers Market By New Business Developments, Innovations, Forecast To 2028 And Top Companies

Qurate Business Intelligence introducing new research on Global Fuel Cell For Data Centers covering micro level of analysis by competitors and key business segments (2022-2028). The Global Fuel Cell For Data Centers explores comprehensive study on various segments like opportunities, size, development, innovation, sales and overall growth of major players. The research is carried out on primary and secondary statistics sources and it consists both qualitative and quantitative detailing.

Major Key players profiled in the study

Hydrogenics Logan Energy Plug Power Toshiba Fuel Cell Power Systems Corporation Doosan Fuel Cell America AFC Energy FuelCell Energy Panasonic Bloom Energy Ballard

Get Free Sample Report + All Related Table and Graphs @ https://www.qurateresearch.com/report/sample/EnP/2020-2025-global-fuel-cell-for-data-centers-market/QBI-MR-EnP-971008

Key Points in the Market: The key features of this Fuel Cell For Data Centers market report includes production, production rate, revenue, price, cost, market share, capacity, capacity utilization rate, import/export, supply/demand, and gross margin. Key market dynamics plus market segments and sub-segments are covered.

Key Growths in the Market: This section of the report incorporates the essential enhancements of the marker that contains assertions, coordinated efforts, R&D, new item dispatch, joint ventures, and associations of leading participants working in the market.

on the basis of types, the Fuel Cell For Data Centers market from 2015 to 2025 is primarily split into: Hydrogen Fuel Cells Solid Oxide Fuel Cells Molten Carbonate Fuel Cells Phosphoric Acid Fuel Cells

on the basis of applications, the Fuel Cell For Data Centers market from 2015 to 2025 covers: Telecoms Industry ISPs (Internet Service Provider) CoLos (Co-Located Server Hosting Facilities) Server Farms Corporate Data Centers Universities/National Laboratories Other

Interpretative Tools in the Market: The report integrates the entirely examined and evaluated information of the prominent players and their position in the market by methods for various descriptive tools. The methodical tools including SWOT analysis, Porter's five forces analysis, and investment return examination were used while breaking down the development of the key players performing in the market.

Region Segmentation

North America (United States, Canada, Mexico)

South America (Brazil, Argentina, Other)

Asia Pacific (China, Japan, India, Korea, Southeast Asia)

Europe (Germany, UK, France, Spain, Italy)

Middle East and Africa (Middle East, Africa)

Basic Questions Answered

*who are the key market players in the Fuel Cell For Data Centers Market?

*Which are the major regions for dissimilar trades that are expected to eyewitness astonishing growth for the

*What are the regional growth trends and the leading revenue-generating regions for the Fuel Cell For Data Centers Market?

*What are the major Product Type of Fuel Cell For Data Centers?

*What are the major applications of Fuel Cell For Data Centers?

*Which Fuel Cell For Data Centers technologies will top the market in next 5 years?

Table of Content

Chapter One: Industry Overview

Chapter Two: Major Segmentation (Classification, Application and etc.) Analysis

Chapter Three: Production Market Analysis

Chapter Four: Sales Market Analysis

Chapter Five: Consumption Market Analysis

Chapter Six: Production, Sales and Consumption Market Comparison Analysis

Chapter Seven: Major Manufacturers Production and Sales Market Comparison Analysis

Chapter Eight: Competition Analysis by Players

Chapter Nine: Marketing Channel Analysis

Chapter Ten: New Project Investment Feasibility Analysis

Chapter Eleven: Manufacturing Cost Analysis

Chapter Twelve: Industrial Chain, Sourcing Strategy and Downstream Buyers

Buy the Full Research report of Global Fuel Cell For Data Centers Market@: https://www.qurateresearch.com/report/buy/EnP/2020-2025-global-fuel-cell-for-data-centers-market/QBI-MR-EnP-971008

Thanks for reading this article; you can also get individual chapter wise section or region wise report version like North America, Europe or Asia.

A free report data (as a form of Excel Datasheet) will also be provided upon request along with a new purchase.

Note – In order to provide more accurate market forecast, all our reports will be updated before delivery by considering the impact of COVID-19.

(*If you have any special requirements, please let us know and we will offer you the report as you want.)

Contact Us:

Qurate Business Intelligence delivers unique Market study with COVID-19 Impact research solutions to its customers and help them to get equipped with refined information and Market study with COVID-19 Impact insights derived from reports. We are committed to providing best business services and easy processes to get the same. Qurate Business Intelligence considers themselves as strategic partners of their customers and always shows the keen level of interest to deliver quality.

Web: www.qurateresearch.com

E-mail: [email protected]

Ph: US – +13393375221, IN – +919881074592

0 notes

Text

Cartilage Repair Market is Expected to Generate Huge Profits by 2032

The global cartilage repair market is expected to reach a value of US$ 3.9 Bn by 2032, with the market growing at a stellar CAGR of 13.9% from 2022 to 2032. Scaling up from a value of US$ 1.60 Bn in 2021, the target market is set to reach an estimated US$ 1 Bn in 2022. The rising cases of osteoarthritis are fueling the demand for the cartilage repair market during the forecast period.

In the recent past, cases of osteoarthritis have become more prevalent all over the world. As per a report by the University of North Carolina, around one million knee and hip replacement operations are conducted annually in the United States. In the U.S., osteoarthritis cases are accountable for a financial burden of $136.8 Bn per year. A study published by the Arthritis Foundation in 2019 estimated that degenerative joint diseases like osteoarthritis will impact more than 130 million people by 2050.

Again, it is expected that the growing cases of osteoarthritis will propel the demand for cartilage repair and regeneration products. The most frequently used treatments for osteoarthritis include autologous chondrocyte implantation and scaffold implants. All of this positively influence the market for cartilage repair. Additionally, as opposed to total knee replacement surgeries, cartilage repair surgeries deliver better and longer-lasting results than other surgeries.

Furthermore, in the past few years, more and more companies are focusing on the development of cartilage regeneration products. This is because governments across the globe are increasing investments in regenerative medicine for cartilage regeneration research. There has also been a surge in clinical trials and the development of new treatments for cartilage regeneration. Besides, the development of a strong pipeline of products based on various methods of cartilage repair available in the market owing to considerable investments in R&D by key market players will further propel the target market growth during the forecast period.

“Increasing osteoarthritis cases coupled with rising demand for treatment will further supplement the global growth of the cartilage repair market over the forecast period,” says an FMI analyst.

Key Takeaways:

The high costs of these procedures are expected to restrict the growth of the cartilage repair market.

By treatment modalities, the cell-based segment will continue to dominate the global marketplace.

On the basis of end-user, the hospital segment will account for the largest market share.

The cartilage repair market in the United States will grow at a CAGR of 13.7% during 2022-2032.

China’s cartilage repair market will register a CAGR of 13.2% during the assessment period.

Competitive Landscape

DePuy Synthes, Smith & Nephew plc, Zimmer Biomet, CONMED Corporation, and Stryker Corporation among others are some of the major players in the cartilage repair market profiled in the full version of the report.

Key market participants are focusing on utilizing various organic and inorganic strategies. These firms are investing in research and development activities, introducing new products, and upgrading current ones. Inorganic tactics like mergers, acquisitions, and partnerships are also employed by these businesses.

For More Information : https://www.futuremarketinsights.com/reports/cartilage-repair-market

More Insights into Cartilage Repair Market Report

In its latest report, FMI offers an unbiased analysis of the global cartilage repair market, providing historical data from 2015 to 2021 and forecast statistics for 2022 to 2032. To understand the global market potential, growth, and scope, the market is segmented on the basis of application (hyaline cartilage, fibrocartilage), site (knee, hip, ankle and foot, other application sites), end user (hospitals, ambulatory surgery centers and clinics), and region.

According to the latest FMI reports, based on segmentation, the knee segment is expected to dominate the global marketplace. This segment will contribute considerably to the overall market revenue. This is due to a surge in arthroscopy procedures. In terms of end-user, the hospital segment will lead the global market growth.

Based on region, the cartilage repair market in the United States will present impressive growth over 2022-2032. The target market in this country will register a CAGR of 13.7%. Owing to the rising incidences of bone and joint disorders along with a growing geriatric population pushes the growth of the cartilage repair market in the U.S. In addition, South Korea, China, Japan, and United Kingdom are some of the other countries that demonstrate impressive growth during the forecast period.

Key segments

By Application:

Hyaline Cartilage

Fibrocartilage

By Site:

Knee

Hip

Ankle and Foot

Other Application Sites

By End-User:

Hospitals

Ambulatory Surgery Centres and Clinics

0 notes

Text

Vehicle Tracking System Market: Benefits, Differences & Demand Analysis

A vehicle tracking system entails a software solution utilized by transportation companies to monitor the location of trailers, trucks, as well as other vehicles. The software is connected to automobiles via GPS, providing users with real-time insights into the vehicles’ geographic positions.

Often referred to as fleet management systems, vehicle tracking systems also support vehicle maintenance, in addition to managing fuel consumption and assessing driving behavior. These factors are essential in fueling their demand and adoption across various industry verticals, thus providing the market with lucrative expansion opportunities. According to Inkwood Research, the global vehicle tracking system market is anticipated to grow with a CAGR of 15.66% over the forecasting period of 2022 to 2030.

Top Advantages of Vehicle Tracking Systems: An Overview

From improved employee and fleet safety to higher cost savings, vehicle tracking systems bring about multiple advantages. For instance, when equipped with AI-enabled features, fleet managers can acquire better insights about distracted driving, red-light violations, and tailgating.

Aligning with this, here are the top advantages of vehicle tracking systems:

Improved Connectivity– Globally, commercial fleet operations are on the rise. Moreover, with an increase in transportation & logistics activities, road transport is emerging as one of the most convenient ways of ensuring products’ availability, even in remote regions. In such a scenario, GPS/satellite, set to be the fastest-growing technology, provides tracking information pertaining to automobiles even in remote areas that lack cell phone coverage.

Lower Operational Costs– Since vehicle tracking systems facilitate vehicle protection and reduce idle time, enterprises can implement improved measures to enhance security, thereby reducing operational costs. Fleet operators can also monitor vehicle usage via vehicle tracking systems, in addition to optimizing vehicle utilization.

Vehicle and Driver Safety– The integration of vehicle tracking systems in automobiles has enabled manufacturers to provide add-on features that increase vehicle safety, especially in the case of thefts or similar losses. In addition, numerous companies are launching products and devices focused on automobile and driver security, as well. For example, the 3G Guardian GPS Tracker by Trackimo is a compact and portable device that can be utilized for tracking shipments, people, and luggage, in order to ensure their safety.