#Importance of General Liability Insurance

Text

#General Liability Insurance#General Liability Insurance coverage#Importance of General Liability Insurance

0 notes

Text

5 Important Facts You Should Know About Auto Insurance in Louisiana

5 Important Facts You Should Know About Auto Insurance in Louisiana

Driving is a privilege, not a right. Anyone that owns or operates a vehicle on public roads needs to understand the risks involved and take steps to protect themselves if something goes wrong. Auto insurance is one of the primary ways to do that, as it helps you recover from financial loss after an accident. But what kind of auto insurance do you need in Louisiana and how much coverage do you…

View On WordPress

#5 Important Facts You Should Know About Auto Insurance in Louisiana#Business Insurance Louisiana#General Liability Insurance Louisiana#Independent insurance Agents#Independent insurance Brokers

0 notes

Text

GL and WC Insurance: A Comprehensive Guide for Businesses

Understanding and securing the right insurance coverage is a cornerstone of responsible business ownership. Two types of insurance that often cause confusion, but are essential for different reasons, are General Liability (GL) insurance and Workers' Compensation (WC) insurance. This guide will delve into the specifics of each, highlighting their importance, what they cover, and why every business owner needs to understand their differences.

https://sihasah.com/gl-and-wc-insurance-a-comprehensive-guide-for-businesses/

2 notes

·

View notes

Text

You know I’ve been thinking

Since Kidd has been offed by Shanks, it made me realize that, as far as I am aware in the anime, we never really learned about Kidd’s backstory with Victoria. We never really got to know Kidd. So it made him more of a liability like the rest of the worst generation who got offed.

However on the other hand you have Law, who yes I am aware of what is going to happen to him.

But he has two bits of insurance.

1. This voice line which is the last time he speaks to Luffy at Wano

“The next time we meet, we’ll be enemies”

We know if Law shows up again, that is not going to be the case, he (and Bepo) is probably going to end up in the Straw Hats’ laps somewhere after Egghead.

He has nothing, he’s desperate to salvage what he has left, and the only person who can help him do that, is Luffy. If Law is going to break down and show his emotions for real, this is going to be the moment where he shines.

It also gives Luffy the leverage he needs to kick Blackbeard’s shit in (even if he had some leverage already, and if Koby shows up to this party it’s a goddamned war now), despite that Law shot first, (because Law shooting first kickstarted the whole Plan. He knew Shanks was too god damned OP, so it’s why he took shots at Blackbeard, or if he took shots at Shanks, he would have lost all hope of making an alliance with Luffy). He trusts Law regardless that he made the right decisions. They’ve been through hell together and it is just Luffy’s nature to be like that.

If they are going to kill off Law, which is possible, they are going to wait until Elbaf, where he uses his power of immortality to take his own life to save Luffy when he possibly gets to the brink of death when fighting Blackbeard. Or he’s going to give to someone who knows they need it most. Because you can’t just throw away such an important concept such as that during Dressrosa since that was the whole REASON Doffy wanted the Ope-Ope no Mi in the FIRST PLACE.

It’s why Law is so IMPORTANT to the plot because of his last ace in the hole.

I mean, Oda DEFINITELY wouldn’t throw that away, would he?

2. Bepo

Let’s be real if Oda were to kill off Law, there would be riots (But also Law is integral to the whole story to the end of the line), but if he killed off Bepo, the community would do so much worse. They would probably commit an act of domestic terrorism.

4 notes

·

View notes

Text

What is Commercial Inland Marine Insurance?

– Provides 24/7, 365-day coverage.

– Safeguards businesses involved in importing, exporting, or transporting goods within India.

– Covers goods in transit via various modes, including road, rail, and air.

– Protects against potential damage, loss, accidents, and perils during operations

Key Benefits in a Nutshell

– Extensive coverage for various risks.

– Damage due to accidents, theft, natural disasters, and fire incidents included.

– General expenses like contributions to general average, salvage costs, and sue and labour expenses covered.

– Protection against liabilities arising from collisions, contact with other vessels, or property damage.

– Coverage for delays in transit, quarantine compensation, temperature-controlled cargo, and more.

Who Needs Commercial Inland Marine Insurance?

– Essential for importers, exporters, manufacturers, distributors, and businesses involved in goods transportation.

– Beneficial for those dealing with valuable items.

The Crucial Coverage – Explained

– Comprehensive coverage for goods in transit via various modes.

– Includes protection for damage due to accidents, theft, natural disasters, and fire incidents.

Standard Coverage under Marine Insurance Policy:

1. Accident Cover : This covers damage to cargo due to accidents during transportation.

2. Theft Cover: This covers the loss of cargo due to theft or pilferage.

3. Natural Disaster:This covers damage caused by natural disasters such as storms, floods, or earthquakes.

4. Fire Accident Cover: It provides coverage for losses resulting from fire incidents during transit.

5. General Expenses Cover:This covers general average contributions, salvage, and sue and labor expenses.

6. Liability Cover: It offers protection against liabilities arising from collisions, contact with other vessels, or property damage.

7. Delay in Transit Cover:This provides coverage for delays in transit that lead to financial losses.

8. Quarantine Compensation:This offers compensation for expenses incurred due to vessel detention or quarantine.

9. Temperature Sense Cover:This covers the deterioration or spoilage of perishable goods.

10. Riots, War & Civil War etc:It provides protection against risks associated with war or political unrest affecting transportation routes.

11. Business Financial Safety:It offers financial security for businesses involved in international trade or shipping.

Riding the Wave of Additional Coverage Options.

– Flexibility with additional coverage options.

– Protection for high-value goods.

– Coverage against strikes, riots, civil commotions, war, terrorism, and temperature-controlled cargo.

– Specialized coverage for items exhibited at trade shows or transported via oversized cargo.

Additional Add-ons Under the Open Marine Insurance Policy:

1. Extended Coverage for High-Value Goods: This add-on provides extra protection for transporting

valuable items, ensuring they are fully covered in case of any unforeseen incidents during transit.

2. Strikes, Riots, and Civil Commotions (SRCC) Coverage:This protects against losses or damages

caused by strikes, riots, or civil commotions during transit.

3. War and Terrorism Coverage: This provides coverage for losses or damages resulting from acts of war, terrorism, or political violence.

4. Temperature-controlled Cargo Coverage: This offers protection for perishable goods that require temperature-controlled transportation, covering losses caused by temperature deviations or equipment failures.

5. Exhibition or Trade Show Coverage: This extends coverage to goods displayed or exhibited at trade shows, exhibitions, or fairs.

6. Customised Coverage:This tailors the policy to meet the specific needs and requirements of the insured, providing additional coverage for unique or specialised goods or circumstances.

7. Valuable Papers and Documents Coverage: This add-on ensures the safety of important business documents during transit, covering the loss or damage of these valuable papers, offering financial security and minimising disruptions to your operations.

8. Loading and Unloading Clause: This clause provides coverage for any damages that occur while goods are being loaded onto or unloaded from the transport vehicle, protecting against potential losses during these critical stages.

9. ODC (Over Dimensional Cargo) Clause: The ODC clause offers specialised coverage specifically for transporting large or oversized cargo, ensuring protection for these unique shipments and addressing any potential risks associated with their transportation.

6. The Art of Claiming: How it Works

The claiming process involves systematic steps.

– Promptly notify the insurance company about the loss.

– Provide necessary documentation, including policy copy, a detailed statement, shipping documents, proof of value, and relevant evidence.

– The claim is assessed, and the eligible amount is determined for settlement.

6.1 Where are the following step which are carried out when a claim arises.

Notification: You should promptly inform the insurance company about any loss or damage that occurs during transit.

Documentation:You are required to submit necessary documents, including a copy of the policy, a detailed statement, shipping documents, proof of value, and relevant evidence.

Detailed Sales and Purchase Proofs: These documents should demonstrate your financial transactions from the policy start date to the claim initiation date.

Claim Form: You should complete and submit the provided claim form with essential information.

Additional KYC Documents: This involves including copies of identification documents, such as the Aadhaar card and PAN card, as well as a self-declaration letter of ownership.

Verification:The insurance company assesses the claim, conducts investigations if necessary, and may appoint a surveyor for assessment.

Settlement Decision:The insurance company determines the eligible amount and communicates this decision to the insured.

Additional Supporting Documents: You should also provide an image of a cancelled cheque, a subrogation letter (if applicable), and a discharge voucher.

#insurance#marine#marines#marinelife#marinette#insuranceagent#aquamarine#lifeinsurance#marinettedupaincheng#marinecorps#submariner#spacemarines#healthinsurance#insurancepolicy#policy#marinebiology#mariners#marinedrive#insurancebroker#marineconservation#insuranceagency#marineaquarium#submarine#usmarines#marinetank#carinsurance#autoinsurance#homeinsurance#insuranceagents#marinemammals

2 notes

·

View notes

Text

Who understands auto insurance?

When you think of getting a new insurance policy, what is the first thing that comes to mind? HEADACHE! Avoid at all costs.. renew my current policy even if the cost keeps going up.

Insurance is an incredibly complex product and one that most consumers do not understand well. Auto insurance is no exception. As we learned in the Concha y Toro case, cognitive associations are particularly important when the product's quality attributes are opaque to consumers. Just like the average consumer cannot differentiate the quality of different wines, the average consumer does not know how to effectively evaluate the quality of auto insurance policies because the product is opaque and complex.

Dall E 3

Given that the quality of different policies is difficult to evaluate and consumer are sticky after having picked a policy, auto insurers invest significantly in brand as a tool for customer acquisition. Auto insurers use their brand in order to create strong cognitive associations of trust that will make it more likely for consumers to pick them when they are evaluating options. The importance of brand and trust in customer purchasing decisions for auto insurance makes insurers more likely to pursue a branded house strategy, in which they use a singular brand for all products and services, as opposed to a house of brands strategy. The branded house strategy enables insurers to scale their significant investments in creating cognitive associations of trust across all of their products and thus is more operationally efficient. Most auto insurance carriers also offer adjacent products, such as home insurance, liability insurance, and commercial insurance, so the branded house strategy further makes it easier to cross-sell customers because there is already the positive cognitive associations of trust.

While most auto insurance providers pursue a branded house strategy, there are some auto insurance providers than pursue a house of brands strategy in order to target different segments of consumers effectively. Just as Toyota created Lexus to target higher end consumers, American Family Insurance maintains a separate brand under The General to target non-standard and standard drivers (aka those that have not-great driving records) and Allstate operates a separate brand, Esurance, to target younger, more tech-enabled consumers. This strategy enables auto insurers to create separate brand strategies that speak to specific customer segments without harming their overall brand image which is so important to customer-purchasing decisions.

Just like in wine choice, cognitive associations play a huge role in insurance policy choice and so must be managed effectively in order to be successful.

2 notes

·

View notes

Text

Decoding the Basics: Understanding Different Types of Insurance

Introduction

Protection is a fundamental part of our lives, giving a security net in the midst of vulnerability and unanticipated occasions. A monetary plan offers insurance against expected misfortunes, relieving the effect of mishaps, diseases, or other unfriendly circumstances. While protection is a typical term, understanding its different sorts can be perplexing. In this article, we will disentangle the nuts and bolts and dig into the various sorts of protection that take care of assorted needs.

Kinds of Protection

Extra security:

One of the principal kinds of protection, extra security offers monetary help to recipients in case of the policyholder's passing. This guarantees that wards are not left in a monetary sway, covering memorial service costs, obligations, and continuous living expenses. There are two essential kinds of disaster protection: term life coverage, which gives inclusion to a predetermined term, and entire extra security, which covers the policyholder for as long as they can remember.

Health care coverage:

With the increasing expenses of medical services, it is critical to have health care coverage. Health care coverage covers clinical costs, including medical clinic stays, medical procedures, meds, and preventive consideration. It goes about as a safeguard against over the top medical care costs, offering people admittance to important clinical benefits without devastating monetary weights. Health care coverage plans shift generally, from essential inclusion to exhaustive strategies that incorporate extra advantages.

Accident coverage:

Collision protection is a legitimate prerequisite for vehicle proprietors in many spots. It gives inclusion to harms and liabilities emerging from mishaps. This incorporates fixes to your vehicle, clinical costs, and legitimate expenses. Accident coverage can likewise offer assurance against robbery, defacing, and cataclysmic events. The degree of inclusion relies upon the kind of approach and the particular requirements of the policyholder.

Property holders/Leaseholders Protection:

Whether you own or lease a home, having protection to safeguard your residence is crucial. Mortgage holders protection covers the construction of the house, individual possessions, and responsibility for wounds that might happen on the property. Leaseholders protection, then again, safeguards the occupant's very own property and gives risk inclusion. The two kinds of protection guarantee that startling occasions like fire, burglary, or catastrophic events don't prompt crushing monetary misfortunes.

Travel Protection:

Go protection is intended to cover startling occasions during trips, including trip retractions, health related crises, lost things, and travel delays. It gives a security net to explorers, offering true serenity and monetary assurance notwithstanding unanticipated conditions. The inclusion shifts, so fundamental to pick a strategy lines up with the kind of movement and potential dangers implied.

Particular Protection: Fitting Inclusion to Remarkable Necessities

Past the central sorts of protection, there exists a range of specific inclusion custom fitted to exceptional necessities and enterprises. These approaches address explicit dangers that may not be satisfactorily covered by standard protection plans. The following are a couple of models:

Proficient Obligation Protection:

Experts like specialists, legal counselors, and advisors frequently settle on proficient risk protection, otherwise called mistakes and oversights protection. This inclusion safeguards against cases of carelessness or inability to enough perform proficient obligations. In fields where counsel and administrations can have huge results, proficient risk protection is a critical shield.

Digital Protection:

As our reality turns out to be progressively computerized, the requirement for security against digital dangers has flooded. Digital protection assists organizations and people with alleviating the monetary effect of information breaks, hacking, and other digital occurrences. It covers costs connected with information recuperation, legitimate liabilities, and notice costs, giving a wellbeing net in the perplexing domain of computerized security.

Pet Protection:

For some, pets are vital individuals from the family, and their wellbeing and prosperity are of central significance. Pet protection covers veterinary costs, medical procedures, and therapies, guaranteeing that pet people can give the best consideration to their shaggy sidekicks without the weight of extreme doctor's visit expenses.

Occasion Protection:

Arranging occasions, whether weddings, shows, or meetings, includes huge ventures. Occasion protection safeguards coordinators against unexpected conditions that might prompt abrogations or disturbances. This can incorporate outrageous climate, seller flake-outs, or other unforeseen difficulties, offering monetary response for occasion organizers.

Long haul Care Protection:

As individuals live longer, the requirement for long haul care protection has become progressively significant. This kind of protection takes care of the expenses related with broadened clinical consideration or help with day to day living exercises for people who can't really enjoy themselves because old enough, ailment, or handicap.

The Significance of Sufficient Inclusion

While protection is a significant device for moderating dangers, the critical lies in picking the perfect proportion of inclusion. Underinsuring can leave people powerless against startling monetary weights, while overinsuring may bring about superfluous costs. Standard evaluations of inclusion needs, particularly during life changes like marriage, the introduction of a kid, or significant buys, are fundamental to guarantee that insurance contracts line up with current conditions.

In addition, the agreements of insurance contracts can be unpredictable. It's urgent for people to completely figure out the subtleties of their inclusion, including deductibles, prohibitions, and guarantee processes. Customary correspondence with insurance suppliers and occasional contract surveys can assist people with remaining informed about changes in inclusion and guarantee that their assurance stays satisfactory.

In the multifaceted trap of life's vulnerabilities, protection fills in as a balancing out force, offering a security net for people, families, and organizations. From primary approaches like life, wellbeing, and accident protection to specific inclusion taking care of remarkable dangers, the assorted cluster of protection choices mirrors the unique idea of our cutting edge lives.

Interpreting the essentials of protection includes understanding the sorts accessible as well as perceiving the significance of customization. Every individual's circumstance is novel, and protection ought to be custom fitted to individual requirements and conditions. As you explore the scene of protection, think of it as a monetary item as well as an essential instrument for invigorating your future against the unexplored world.

Fundamentally, protection is a proactive interest in versatility. It changes the capricious into the sensible and enables people to confront life's vulnerabilities with certainty. Thus, whether you're shielding your business, safeguarding your computerized resources, or guaranteeing the prosperity of your darling pets, understanding the subtleties of protection is the way in to a safer and strong future.

Conclusion

Protection is a diverse idea that assumes a crucial part in defending people and their resources. From extra security, which guarantees monetary solidness for friends and family after one's downfall, to medical coverage, offering a wellbeing net in the midst of sickness, and accident coverage, safeguarding against the vulnerabilities out and about — each type fills a remarkable need.

Understanding the various sorts of protection is urgent for coming to informed conclusions about inclusion that lines up with individual requirements and conditions. While these are only a couple of models, there are numerous other particular insurance contracts taking care of explicit dangers and businesses.

In our current reality where vulnerabilities are unavoidable, protection gives a conviction that all is good and monetary security. It's not just a monetary item but rather an instrument that enables people to explore life's difficulties with versatility. As you investigate the different kinds of insurance accessible, think about your remarkable circumstance, survey possible dangers, and pick contracts that offer exhaustive inclusion.

Generally, protection is a proactive measure — one that changes unexpected dangers into sensible difficulties. Thus, whether it's getting your family's future, safeguarding your wellbeing, or guaranteeing your property and possessions, unraveling the essentials of protection is the most important move toward a safer and tough future.

2 notes

·

View notes

Text

Steps to Take Filing a Motor Vehicle Accident Claim in NJ

Motor vehicle accidents in New Jersey can be distressing and life-altering experiences. When you or a loved one is involved in a car crash, it's important to understand the steps to take when filing a motor vehicle accident claim. These steps are essential for ensuring your rights are protected, seeking compensation for damages, and navigating the complex legal and insurance processes. In this blog, we'll guide you through the crucial steps involved in filing a motor vehicle accident claim in New Jersey.

Step 1: Ensure Safety and Seek Medical Attention

Immediately after an accident, the safety and well-being of all involved parties should be the top priority. Ensure that everyone is out of harm's way and call for medical assistance if necessary. It's essential to get a medical evaluation even if you don't appear to be seriously injured, as some injuries may not manifest immediately but could have long-term consequences.

Step 2: Contact Law Enforcement

In New Jersey, it is generally required to report any accident involving injuries, fatalities, or property damage exceeding $500 to the local law enforcement agency. Contact the police and request an officer to come to the scene of the accident. They will prepare a police report, which is an important document for your accident claim.

Step 3: Gather Evidence

While at the accident scene, collect as much information as possible. This includes:

Exchange Information: Obtain contact and insurance information from all parties involved in the accident. This information is vital for the insurance claim process.

Witness Statements: If there are witnesses to the accident, collect their contact information and statements. Their testimony can be invaluable in establishing fault.

Photographs: Take pictures of the accident scene, vehicle damage, road conditions, and any visible injuries. Visual evidence can be compelling in proving your case.

Step 4: Seek Medical Treatment

Even if your injuries seem minor, it's important to see a healthcare professional promptly. This not only ensures your health but also creates a medical record of your injuries, which is crucial for your claim. Delayed medical treatment can weaken your case, as insurance companies may question the severity and cause of your injuries.

Step 5: Notify Your Insurance Company

Report the accident to your insurance company as soon as possible. Even if you are not at fault, your insurance company needs to be informed. Be prepared to provide them with the basic details of the accident. Avoid making any statements or admissions to the insurance adjuster that could be used against you later.

Step 6: Consult an Attorney

Consider consulting with a skilled motor vehicle accident attorney in New Jersey. An experienced attorney can provide invaluable guidance through the claim process, help you understand your rights, and ensure that you receive fair compensation. They can also assist in dealing with insurance companies and navigating legal complexities.

Step 7: Determine Fault and Liability

In New Jersey, the concept of comparative negligence is used to determine liability. This means that fault can be distributed among multiple parties involved in the accident. New Jersey follows a modified comparative negligence rule, where you can recover damages if you are less than 50% at fault. Your attorney will help investigate the accident, gather evidence, and establish fault, which is crucial for determining the compensation you are entitled to.

Step 8: File a Personal Injury Claim

If you've sustained injuries in the accident, you may be eligible to file a personal injury claim to seek compensation for medical expenses, pain and suffering, lost wages, and more. Your attorney will guide you through the process of filing a personal injury claim, ensuring that it is properly documented and filed within the statute of limitations in New Jersey, which is typically two years from the date of the accident.

Step 9: Negotiate with Insurance Companies

Insurance companies will often attempt to settle motor vehicle accident claims quickly and for the least amount possible. Your attorney will negotiate with the insurance companies on your behalf, ensuring that you receive a fair settlement that covers your damages. If the initial settlement offer is inadequate, your attorney will work to secure a better outcome, even if it requires litigation.

Step 10: Prepare for Litigation (if Necessary)

If a fair settlement cannot be reached through negotiation, your attorney may recommend pursuing a lawsuit. This involves initiating legal proceedings, presenting your case in court, and letting a judge or jury determine the compensation you are entitled to. Litigation can be a lengthy and complex process, but your attorney will guide you through every step.

Conclusion

Filing a motor vehicle accident claim in New Jersey is a multifaceted process that requires careful attention to detail, a deep understanding of the law, and the ability to navigate insurance negotiations. By following the steps outlined in this blog and enlisting the expertise of a qualified motor vehicle accident attorney in New Jersey, you can maximize your chances of obtaining fair compensation for your injuries, damages, and losses. It's crucial to act promptly, protect your rights, and seek the support you need to effectively address the aftermath of a motor vehicle accident.

2 notes

·

View notes

Text

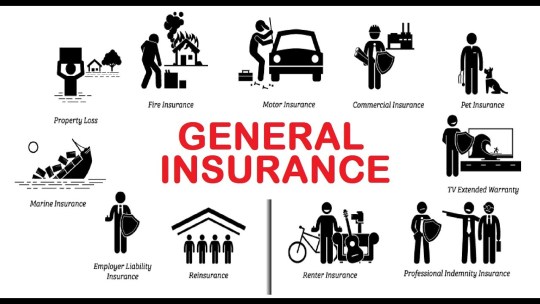

What is general insurance? - Insurance

What is general insurance? — Insurance

Understanding General Insurance: A Comprehensive Guide

General — Insurance plays a vital role in safeguarding individuals and businesses from unforeseen risks and financial uncertainties. One of the most common types of insurance is general insurance, which encompasses a wide range of policies designed to protect against non-life risks. In this article, we will delve into the world of general insurance, exploring its definition, key categories, importance, and how to choose the right coverage for your needs.

What is General Insurance?

General insurance, also known as non-life insurance, is a financial product that provides protection against various risks, excluding life-related risks. Unlike life insurance, which pays out benefits upon the policyholder’s death or maturity, general insurance policies offer coverage for specific contingencies, such as accidents, theft, property damage, and liability claims.

Key Categories of General Insurance

Health Insurance:

Health insurance policies cover medical expenses incurred due to illness, injury, or accidents. They can include individual health plans, family floater policies, and group health insurance provided by employers.

Motor Insurance:

Motor insurance encompasses policies for automobiles, including cars, motorcycles, and commercial vehicles. The two primary types are:

Third-party liability insurance, which covers damages and injuries caused to third parties.

Comprehensive insurance, which also covers damages to the insured vehicle.

Home Insurance:

Home insurance protects your residence and its contents against various risks, including fire, theft, natural disasters, and structural damage. It includes building insurance and content insurance.

Travel Insurance:

Travel insurance provides coverage for unforeseen events while traveling, such as trip cancellations, medical emergencies, baggage loss, and personal liability.

Property Insurance:

Property insurance extends beyond homes and covers commercial properties, warehouses, and other assets. It safeguards against fire, theft, vandalism, and natural disasters.

Liability Insurance:

Liability insurance protects individuals and businesses from legal claims arising from injuries, damages, or accidents for which they may be held responsible. Examples include professional liability insurance, public liability insurance, and product liability insurance.

Marine Insurance:

Marine insurance covers goods and cargo transported via sea, air, or land. It mitigates risks associated with damage, theft, or loss during transit.

Also Check: <<< Trending Topics >>>

Importance of General Insurance

Financial Protection: General insurance provides a safety net, ensuring that individuals and businesses do not face significant financial losses in the event of unforeseen incidents.

Legal Requirements: In many countries, certain types of general insurance, such as motor insurance, are mandatory by law to protect third parties in case of accidents.

Peace of Mind: Knowing that you have insurance coverage gives peace of mind, reducing stress and anxiety related to potential risks.

Risk Management: General insurance allows individuals and businesses to manage risks effectively by transferring them to insurance companies.

How to Choose the Right General Insurance Coverage

Assess Your Needs: Identify the specific risks you want to protect against and assess your budget to determine the coverage you require.

Research Insurers: Compare policies and quotes from different insurance companies to find the most suitable option for your needs.

Understand Policy Terms: Carefully read and understand the terms and conditions, including coverage limits, deductibles, and exclusions.

Seek Professional Advice: Consult with insurance agents or brokers who can provide expert guidance on selecting the right coverage.

Review Regularly: Reevaluate your insurance needs regularly, especially when major life events occur, such as marriage, the birth of a child, or buying a new home or vehicle.

Conclusion

General insurance is a crucial component of financial planning, offering protection against a wide range of non-life risks. Whether it’s safeguarding your health, home, vehicle, or business, having the right general insurance coverage can provide peace of mind and financial security when you need it most. By understanding the different types of general insurance and assessing your needs, you can make informed decisions to ensure your protection in an unpredictable world.

NEXT TO >>>

3 notes

·

View notes

Text

Key questions to consider when hiring commercial general contractors

Choosing the right commercial general contractor is crucial for the success of your construction project. Before making a hiring decision, it's important to ask pertinent questions that can help you evaluate their expertise, reliability, and suitability for your specific needs. Consider the following key questions before hiring a commercial general contractors:

1. What is your experience in commercial construction?

Understanding the contractor's experience in commercial projects is essential. Inquire about the number of years they have been in the industry, their portfolio of completed projects, and any relevant certifications or licenses they hold.

2. Can you provide references from previous clients?

Requesting references allows you to gauge the contractor's reputation and track record. Contact their previous clients to inquire about the quality of work, adherence to timelines, communication skills, and overall satisfaction with the contractor's services.

3. Do you have the necessary insurance coverage?

It is vital to confirm that the contractor carries adequate insurance coverage, including general liability insurance and workers' compensation insurance. This ensures that you are protected from potential liabilities and accidents that may occur during the project.

4. How do you handle subcontractors and vendor selection?

Many commercial projects require subcontractors or specialized vendors. Inquire about the contractor's process for selecting and managing subcontractors. Ensure they have a robust network of reliable professionals and a thorough vetting process to maintain quality standards.

5. How do you approach project scheduling and timeline management?

Time is often a critical factor in commercial construction. Ask the contractor about their approach to project scheduling, their ability to meet deadlines, and how they handle potential delays or unexpected circumstances.

6. What is your communication strategy during the project?

Clear and efficient communication plays a pivotal role in ensuring the success of any construction project. Inquire about the contractor's preferred communication methods, how often they provide progress updates, and how they handle change orders or project modifications.

7. Can you provide a detailed cost estimate and payment schedule?

Obtain a comprehensive cost estimate that includes all aspects of the project, such as materials, labour, permits, and any potential additional costs. Additionally, discuss the payment schedule and terms to ensure they align with your financial plans.

8. How do you address quality control and inspections?

Ask about the contractor's quality control processes and how they ensure that the work meets industry standards and regulations. Inquire about their inspection procedures, both during and after the project, to guarantee that the final result is of the highest quality.

9. What is your approach to safety on the construction site?

Safety is paramount in construction projects. Inquire about the contractor's safety protocols, training programs, and their commitment to adhering to local building codes and regulations. A safe work environment protects both workers and your investment.

10. What warranty or post-construction support do you offer?

Discuss the contractor's warranty policy and post-construction support. Understand what types of issues are covered, the duration of the warranty, and how they handle any necessary repairs or corrections after project completion.

By asking these essential questions, you can gather valuable information and make an informed decision when selecting a commercial general contractor. Remember, thorough due diligence and open communication are vital for a successful partnership and the timely completion of your construction project.

#commercial general contractors#commercial contractors#general contractor#construction#construction contractors

2 notes

·

View notes

Text

Bring Mental Peace and Financial Security with Viola Insurance

Are you a professional viola player, an amateur musician, or simply an avid collector of fine instruments? Musical instrument insurance can provide peace of mind by offering financial protection against a range of potential threats.

Music equipment protection plans come for all sorts of musical instruments. Viola Insurance is a comprehensive type of insurance coverage that protects viola players and owners against various risks and probable financial losses.

Types of coverage you can trust your music gear and finances with

There are several music gear insurance policies available in the market, each with its own unique features and coverage options. The most common types of coverage include instrument insurance, third-party liability coverage, and personal accident insurance. Let’s take a quick look at them:

Coverage for musical instruments provides all-encompassing protection to your voila against damage, loss, or theft. This type of policy can be particularly beneficial for professional viola players or collectors who own expensive musical instruments. The reason is - it can help protect their investment and ensure that they can continue to perform or enjoy their art without the fear of financial loss in case of an unexpected event.

Liability insurance is another type of coverage that guards against legal claims or liability arising from injury or damage caused by the instrument to third parties or their properties. This type of policy is particularly critical for professional viola players who perform in public or private events, as it can help protect against claims of property damage, bodily injury, or other types of harm caused by the instrument.

Personal accident coverage is an insurance product that provides protection for injury or illness suffered by the player, preventing them from performing. This type of policy can be particularly beneficial for professional musicians who earn their bread and butter from their craft. It can help provide financial support during a period of recovery or rehabilitation.

Choosing an Insurance Plan: Things to Consider

When purchasing a musical instrument insurance product, it is important to consider the level of coverage required, the deductible, and the premium cost. Most policies will cover the cost of repairing or replacing the instrument if it is damaged, lost, or stolen. However, some policies may have certain exclusions or limitations depending on the circumstances and insurance provider.

Make sure to read the terms and conditions of the policy carefully to ensure that it meets your specific needs and requirements. Some policies may have exclusions or caps that may not be immediately apparent. However, it is necessary to understand these before making a claim.

Deciding on an insurance provider: Factors to count in

Just like insurance policies, the market is full of musical instrument insurance companies that specialize in providing musical instrument insurance. Therefore, you need to be careful when picking one and choose a reliable vendor. Reputable service providers have a better understanding of the unique risks and requirements associated with owning a viola. Most importantly, they offer tailored coverage options or better rates than general insurance providers. So, do keep this in mind when choosing an insurance provider.

When selecting an insurance company for buying comprehensive Viola Insurance, it's essential to consider factors such as their reputation, level of customer service, and claims handling processes. A customer-centric insurance company is responsive and transparent when it comes to claims. So, they offer clear and concise information about their coverage options and policies.

Summing Up!

Last but not least, buying an instrument-specific insurance policy is a significant step for anyone who owns or plays a viola, whether as a hobby or for the sake of a profession. By providing protection against a range of possible risks and financial losses, such insurance plans can offer peace of mind and allow players and owners to enjoy their instruments without fear of financial harm.

So, regardless of your professional standing, investing in a high-quality dedicated music gear policy is a wise move in regard to protecting your instrument and your financial security.

2 notes

·

View notes

Text

Recognizing the Basics of General Insurance Coverage

Insurance policy is a kind of risk management that gives financial protection versus uncertain events. General insurance policy is a wide term utilized to describe insurance coverage that cover a vast array of dangers, consisting of health, residential property, liability, and also other sorts of insurance. Comprehending the basics of general insurance coverage can assist you make educated decisions when choosing an insurance coverage policy.One of one of the most usual sorts of basic insurance policy is medical insurance, which covers medical costs incurred as a result of health problems or accidents. Residential property insurance policy, on the other hand, secures versus damage or loss of building triggered by all-natural disasters, burglary, or various other unexpected occasions. Liability insurance coverage covers lawful expenses and also damages emerging from crashes or injuries that occur on your residential property or due to your activities. Various other kinds of basic insurance coverage consist of travel insurance coverage, auto insurance, and also organization insurance policy. It is important to analyze your private insurance needs and also select plans that offer sufficient insurance coverage for your certain circumstance.

Read more here corporate insurance

2 notes

·

View notes

Text

Comprehending the Fundamentals of General Insurance Coverage

Insurance coverage is a type of risk administration that gives financial defense versus unpredictable occasions. General insurance policy is a wide term utilized to explain insurance coverage plans that cover a vast array of threats, including health, home, liability, and also various other kinds of insurance. Understanding the basics of basic insurance policy can assist you make educated decisions when picking an insurance policy policy.One of the most common types of basic insurance policy is medical insurance, which covers medical expenses incurred as a result of ailments or crashes. Building insurance policy, on the various other hand, protects against damages or loss of residential property caused by all-natural catastrophes, theft, or various other unanticipated occasions. Liability insurance covers legal expenses and damages emerging from mishaps or injuries that happen on your home or because of your actions. Other kinds of basic insurance coverage consist of travel insurance, car insurance, and organization insurance. It is very important to analyze your specific insurance coverage needs as well as select plans that provide appropriate coverage for your specific circumstance.

Read more here corporate insurance

2 notes

·

View notes

Text

2 notes

·

View notes

Text

How to Get Cheaper Car Insurance

Having car insurance is an essential requirement in most countries and not only provides protection for the vehicle itself, but also covers any financial responsibility that may arise if an accident were to occur. The cost of car insurance can be a large expense, especially when compared to other bills, such as utilities. However, there are a number of ways in which you can save money on your car insurance premiums and make them more affordable.

The first step to getting cheaper car insurance is understanding the factors that influence your premium. Your insurer will take into account things such as your age, gender, driving record and occupation. It’s important to know how each of these factors can affect your premium so that you can find ways to lower it. For example, some insurers offer discounts to young drivers or experienced drivers with no tickets or accidents on their records. Similarly, if you have a higher-paying job or belong to certain professional associations or organizations, some insurers may provide you with discounted rates.

You should also consider shopping around for quotes from multiple providers before deciding on one insurer for your car insurance needs. Different companies often offer different levels of coverage and prices so by doing this you can compare policies side-by-side to get the best deal possible. Furthermore, look out for deals or promotions from your chosen provider; they may provide incentives such as multi-car discounts if more than one person in the family has car insurance through them.

Additionally, consider raising your deductible. This means the amount you need to pay before the insurer takes over coverage of expenses in the event of an accident. Generally speaking, a higher deductible means lower premiums - but this will mean having to pay out more if something does go wrong! You should assess what is manageable for you financially in terms of deductibles versus monthly payments and choose an option that works best for your individual situation.

Finally, remember that safety comes first when it comes to operating a vehicle and this should be reflected in how you use it too; always drive carefully and avoid dangerous habits such as drinking while driving or speeding on highways. Insurers consider this kind of behavior high risk and reward those who display responsible behavior with reduced premiums accordingly. Additionally make sure all regular maintenance work on the vehicle is completed at timely intervals; a well-maintained car often commands lower insurance costs than cars requiring constant repair work and servicing fees.

Overall, reducing car insurance costs requires research as well as being mindful of any associated risks; always consider potential savings alongside possible consequences when making decisions regarding which policies are best suited to you personally in order to achieve maximum benefits from them without putting yourself or others at risk from preventable accidents or costly liabilities due to negligence . Following these tips will help ensure you have the coverage necessary whilst keeping monthly payments at a minimum so that you can save money on your auto insurance costs without compromising on safety or quality of service.

3 notes

·

View notes

Text

Travel Insurance: What’s Covered and What’s Not?

Traveling can be one of the most exciting experiences, but it’s not without risks. Whether it’s a missed flight, a sudden illness, or lost luggage, unexpected issues can arise. This is where travel insurance becomes essential. But before you rush to buy travel insurance online, it’s crucial to understand what’s covered and what isn’t. Knowing the fine details can help you choose the best travel insurance plan that fits your needs.

In this blog, we’ll explore the typical coverage of travel insurance and highlight what is generally excluded from policies, helping you make a well-informed decision.

What is Covered by Travel Insurance?

Trip Cancellation or Interruption One of the primary reasons travelers opt for travel insurance is to protect their investment if they need to cancel or cut short their trip due to unforeseen circumstances. This could include:

Illness or injury (yourself or a family member)

Natural disasters

Death of a family member

Strikes or terrorism affecting your destination

Popular policies from providers like ICICI Lombard travel insurance and Bajaj Allianz travel insurance offer robust trip cancellation coverage, ensuring you’re reimbursed for any non-refundable expenses.

Medical Emergencies Health emergencies can occur at any time, especially when traveling. Travel health insurance or travel medical insurance is designed to cover medical expenses such as hospital stays, doctor visits, and emergency surgeries.

Coverage typically includes medical evacuation if local hospitals cannot treat you adequately.

Providers like Reliance travel insurance offer comprehensive travel medical insurance, ensuring you’re financially protected in case of a medical emergency.

Lost, Stolen, or Damaged Luggage Losing your luggage can be one of the most frustrating experiences during travel. Most travel insurance plans will reimburse you for lost, damaged, or stolen baggage. They may also cover expenses if your luggage is delayed for an extended period.

Flight Delays or Missed Connections If your flight is delayed, you could miss important connections or even spend extra on accommodation and meals. Many travel insurance policies cover expenses related to:

Flight delays

Missed connections

Cancelled flights due to weather or other external factors

ICICI Lombard travel insurance and Bajaj Allianz travel insurance offer this coverage, making them popular options for frequent flyers.

Personal Liability Some travel insurance policies cover personal liability if you’re involved in an accident that causes injury or damage to someone else’s property. This can provide peace of mind during activities that may carry some risks.

Emergency Evacuation and Repatriation In case of a severe medical emergency, evacuation to a medical facility or repatriation back to your home country may be necessary. Comprehensive plans like those from Reliance travel insurance often cover these costs, ensuring you’re not left stranded.

What’s Not Covered by Travel Insurance?

While travel insurance provides critical coverage, there are certain exclusions that you need to be aware of before purchasing a plan. Here’s what is typically not covered:

Pre-Existing Medical Conditions Most travel health insurance plans won’t cover pre-existing medical conditions unless specified. If you suffer from a chronic illness or medical condition, make sure to review the policy carefully or look for specialized coverage.

High-Risk Activities or Sports Planning to go skydiving or skiing on your vacation? Many standard travel insurance policies exclude coverage for high-risk activities or adventure sports unless you purchase additional riders.

Traveling Against Medical Advice If you travel despite a doctor’s advice not to, your travel insurance may not cover any medical emergencies or cancellations related to your health condition.

Losses Due to Negligence If you lose your belongings due to your own negligence, such as leaving your phone unattended, most insurance providers will not cover the loss.

War, Terrorism, and Civil Unrest While some policies cover trip cancellations due to terrorism, many exclude coverage if you choose to travel to a country that is at war or experiencing civil unrest.

Pandemics and Epidemics While some policies have adapted post-COVID-19, many travel insurance plans exclude coverage related to pandemics. It’s always best to confirm with your insurer whether medical expenses or trip cancellations due to pandemics are included.

Non-Medical Evacuations Evacuation due to political unrest or natural disasters is generally not covered unless you have a specific rider in your travel insurance plan.

How to Buy the Best Travel Insurance

To get the most out of your travel insurance, you need to carefully compare plans and providers. Whether you’re looking at ICICI Lombard travel insurance, Bajaj Allianz travel insurance, or Reliance travel insurance, here are a few tips to help you choose the best coverage:

Compare Travel Insurance Quotes: It’s important to get multiple travel insurance quotes online to find the best deal. Look for plans that fit your budget while offering the coverage you need.

Buy Travel Insurance Online: Purchasing travel insurance online is the easiest and quickest way to get covered. Many providers, including ICICI Lombard and Bajaj Allianz, allow you to compare and buy travel insurance online within minutes.

Look for Customization: If you’re engaging in adventure sports or have pre-existing conditions, look for policies that offer riders to cover your unique needs.

Understand the Fine Print: Always read the policy details to ensure you’re aware of any exclusions or limitations. The best travel insurance plans are transparent and provide comprehensive coverage without hidden surprises.

Having travel insurance is an essential safety net for any trip, but it’s equally important to understand what is and isn’t covered in your policy. From travel medical insurance to baggage loss protection, a good travel insurance plan can save you from unexpected expenses and stress during your journey.

Before your next adventure, compare travel insurance quotes and buy travel insurance online to ensure you’re fully protected. Whether you choose ICICI Lombard travel insurance, Bajaj Allianz travel insurance, or Reliance travel insurance, being covered means traveling with peace of mind.

By being informed about your coverage, you can ensure a worry-free trip every time!

#travel insurance#travel insurance online#travel insurance safety#travel insurance policy#travelling#travel insurance plans#travel insurance market#insurance

0 notes

Last Seen Blogs

irxn--fxst

|[ 𝐉 𝐔 𝐒 𝐓 𝐈 𝐅 𝐈 𝐄 𝐃 ]|

drgeetikapaliwal

Untitled

stormbringrr

theStormBringrr

clnnamon-rolls

rotating harry osborn in my brain