#General Liability Insurance coverage

Text

General Liability Insurance Coverage

In today’s unpredictable business world, having General Liability Insurance coverage isn’t just smart; it’s essential. It protects your finances, boosts your credibility, and gives you peace of mind. So, before you set sail on your business journey, make sure you have the right protection in place. Don’t let unexpected accidents sink your ship—invest in your future now! General Liability Insurance coverage acts as a financial buffer, covering these expenses and ensuring your business can weather the storm.

0 notes

Text

#General Liability Insurance#General Liability Insurance coverage#Importance of General Liability Insurance

0 notes

Text

Understanding General Liability Insurance: A Comprehensive Guide

General liability insurance is an essential coverage that protects businesses from various risks and potential lawsuits. Whether you're a small startup or a well-established company, having adequate general liability insurance coverage is crucial to safeguarding your business interests. In this article, we will explore the importance of general liability insurance and how it can benefit businesses in California, particularly in Fontana.

The Significance of General Liability Insurance:

General liability insurance serves as a safety net for businesses, providing financial protection against claims for property damage, bodily injury, and personal injury arising from business operations. Accidents and unforeseen incidents can occur at any time, and being unprepared can have devastating consequences for your business.

For instance, if a customer slips and falls in your store, they could hold your business liable for their injuries. Without adequate insurance, you might have to pay for medical expenses, legal fees, and even settlements out of pocket. However, with general liability insurance, you can have peace of mind knowing that your insurer will handle these costs, allowing you to focus on running your business.

General Liability Insurance in California:

California, with its thriving business landscape, requires businesses to have proper insurance coverage. General liability insurance is a crucial aspect of protecting your business in the state. It not only shields your business from potential lawsuits but also ensures compliance with legal requirements.

Whether you run a small retail store, a construction company, or provide professional services, having general liability insurance in California is vital. From bodily injury claims to property damage lawsuits, this coverage offers comprehensive protection against a wide range of risks that businesses commonly face.

Business Liability Insurance in Fontana, California:

Fontana, located in San Bernardino County, is a bustling city with a diverse range of businesses. From manufacturing and logistics to retail and service industries, businesses in Fontana can benefit greatly from business liability insurance.

By obtaining business liability insurance in Fontana, California, business owners can safeguard their assets and interests. This insurance coverage provides protection against potential lawsuits, whether it's a customer injury, property damage, or a product liability claim. With the right insurance policy, you can minimize financial risks and ensure the longevity of your business.

Conclusion:

Investing in general liability insurance is a wise decision for businesses operating in California, including Fontana. It offers financial protection, mitigates risks, and allows you to focus on growing your business. By choosing a reliable insurance provider like 2autoinsurance, you can find the right coverage tailored to your business needs. Don't leave your business exposed to potential liabilities; secure the future of your enterprise with comprehensive general liability insurance.

#general liability insurance California #general liability insurance coverage #commercial general liability insurance #general liability insurance california #business liability insurance Fontana California #business liability insurance #liability insurance #2autoinsurance

#general liability insurance California#general liability insurance coverage#commercial general liability insurance#general liability insurance california#business liability insurance Fontana California#business liability insurance#liability insurance#2autoinsurance

0 notes

Text

Where Can I Find a List of All The Insurance Companies Who Cover General Liability?

Operating a business of any size comes with inherent risks that can lead to substantial financial and legal consequences if not properly insured against. From customer injuries sustained on premises to vendor supply chain disruptions, unanticipated incidents can quickly derail companies without adequate protection. Read more:- https://qr.ae/psF5zw

0 notes

Text

General Liability Insurance in Coral Springs, FL

For all of your insurance needs in West Palm Beach, including Palm Beach, Delray Beach, Lake Worth, Boca Raton, and the surrounding areas, Innovative Insurance is your one-stop shop. General Liability Coverage is one of the many business insurance products that our full-service firm specializes in. For your company, we provide the best rates on general liability insurance together with unmatched service. You can always rely on Innovative Insurance's skilled and courteous agents to give you the individual attention you require.

After being called in, all certificates are issued within minutes, and all calls are answered quickly. It makes sense why we are routinely included among the top 5 producers for our main insurance providers! We are also honored to be a member of FCCI Insurance Company's Presidents Club and to have been awarded the esteemed Gold Medallion Agent award by Zurich Insurance Company for exceptional performance.

0 notes

Text

Navigating Healthcare Supplement Plans and Understanding Umbrella Insurance with Kang Group Services

Introduction:

In today's complex insurance landscape, understanding healthcare supplement plans and umbrella insurance is crucial for comprehensive coverage. Kang Group Services specializes in guiding individuals towards optimal insurance solutions, offering expertise in healthcare supplements and umbrella coverage.

Healthcare Supplement Plans:

Healthcare supplement plans, also known as Medigap policies, are designed to cover gaps in Medicare coverage. These plans, offered by private insurance companies, help pay for healthcare costs that Medicare doesn't cover, such as copayments, deductibles, and coinsurance. Kang Group Services assists clients in selecting the most suitable supplement plan based on individual needs, ensuring comprehensive coverage and peace of mind.

Key Points about Healthcare Supplement Plans:

Enrolment Eligibility: Individuals typically need to enroll in a supplement plan during their open enrollment period to guarantee coverage without medical underwriting. Kang Group Services advises on enrollment periods and the best time to secure a plan.

Cost and Affordability: Premiums for supplement plans vary based on coverage level and location. Kang Group Services helps clients balance coverage benefits with affordability, ensuring they get the most value from their plan.

Plan Flexibility: As healthcare needs evolve, Kang Group Services assists in assessing plan changes or upgrades, ensuring ongoing suitability and alignment with evolving healthcare requirements.

Best Practices for Understanding Umbrella Insurance:

Best umbrella insurance serves as an additional layer of liability protection beyond standard home and auto insurance policies. It provides extended liability coverage, offering financial protection against lawsuits and claims that exceed the limits of primary policies. Kang Group Services offers comprehensive guidance on umbrella insurance to safeguard clients' financial well-being.

Insights into Umbrella Insurance:

Coverage Scope: Umbrella insurance covers a broad range of scenarios, including personal injury claims, property damage liability, and legal fees. Kang Group Services helps clients understand the scope of coverage and its relevance to their unique circumstances.

Adequate Coverage Limits: Assessing the appropriate coverage limit is critical. Kang Group Services evaluates clients' assets and potential risks to recommend suitable coverage limits that protect against unforeseen circumstances.

Supplementing Existing Policies: Umbrella insurance supplements underlying policies, enhancing coverage where primary policies fall short. Kang Group Services ensures clients have a comprehensive insurance portfolio that aligns with their risk exposure.

Customization Options: Kang Group Services offers tailored umbrella insurance solutions, allowing clients to customize coverage to suit their specific needs and lifestyle.

Conclusion:

Navigating healthcare supplement plans and understanding umbrella insurance can be intricate without expert guidance. Kang Group Services stands as a trusted advisor, providing clarity and personalized assistance in selecting the right healthcare supplement plan and umbrella coverage.

From assessing healthcare needs to extending liability protection, Kang Group Services' expertise ensures individuals have comprehensive insurance coverage tailored to their requirements. Contact Kang Group Services today for expert advice and personalized insurance solutions that prioritize your financial security and well-being.

#health insurance obamacare#obamacare health coverage#supplemental insurance policy#private health quote#best dental and vision insurance#intact umbrella insurance#umbrella company insurance cover#general liability insurance near me#commercial property insurance companies

0 notes

Text

https://www.globalresearch.ca/american-healthcare-corrupt-broken-lethal/5865983

American Healthcare: Corrupt, Broken and Lethal. “Politically and Morally Wrong, Health Care is A Human Right”

By Richard Gale and Dr. Gary Null

Global Research, August 22, 2024

For a nation that prides itself on being the world’s wealthiest, most innovative and technologically advanced, the US’ healthcare system is nothing less than a disaster and disgrace. Not only are Americans the least healthy among the most developed nations, but the US’ health system ranks dead last among high-income countries. Despite rising costs and our unshakeable faith in American medical exceptionalism, average life expectancy in the US has remained lower than other OECD nations for many years and continues to decline. The United Nations recognizes healthcare as a human right. In 2018, former UN Secretary General Ban Ki-moon denounced the American healthcare system as “politically and morally wrong.”

During the pandemic it is estimated that two to three years was lost on average life expectancy. On the other hand, before the Covid-19 pandemic, countries with universal healthcare coverage found their average life expectancy stable or slowly increasing. The fundamental problem in the U.S. is that politics have been far too beholden to the pharmaceutical, HMO and private insurance industries. Neither party has made any concerted effort to reign in the corruption of corporate campaign funding and do what is sensible, financially feasible and morally correct to improve Americans’ quality of health and well-being.

The fact that our healthcare system is horribly broken is proof that moneyed interests have become so powerful to keep single-payer debate out of the media spotlight and censored. Poll after poll shows that the American public favors the expansion of public health coverage. Other incremental proposals, including Medicare and Medicaid buy-in plans, are also widely preferred to the Affordable Care Act or Obamacare mess we are currently stuck with.

It is not difficult to understand how the dismal state of American medicine is the result of a system that has been sold out to the free-market and the bottom line interests of drug makers and an inflated private insurance industry. How advanced and ethically sound can a healthcare system be if tens of millions of people have no access to medical care because it is financially out of their reach?

The figures speak for themselves. The U.S. is burdened with a $41 trillion Medicare liability. The number of uninsured has declined during the past several years but still lingers around 25 million. An additional 30-35 million are underinsured. There are currently 65 million Medicare enrollees and 89 million Medicaid recipients. This is an extremely unhealthy snapshot of the country’s ability to provide affordable healthcare and it is certainly unsustainable. The system is a public economic failure, benefiting no one except the large and increasingly consolidated insurance and pharmaceutical firms at the top that supervise the racket.

Our political parties have wrestled with single-payer or universal healthcare for decades. Obama ran his first 2008 presidential campaign on a single-payer platform. Since 1985, his campaign health adviser, the late Dr. Quentin Young from the University of Illinois Medical School, was one of the nation’s leading voices calling for universal health coverage.

2 notes

·

View notes

Text

GL and WC Insurance: A Comprehensive Guide for Businesses

Understanding and securing the right insurance coverage is a cornerstone of responsible business ownership. Two types of insurance that often cause confusion, but are essential for different reasons, are General Liability (GL) insurance and Workers' Compensation (WC) insurance. This guide will delve into the specifics of each, highlighting their importance, what they cover, and why every business owner needs to understand their differences.

https://sihasah.com/gl-and-wc-insurance-a-comprehensive-guide-for-businesses/

2 notes

·

View notes

Text

What is Commercial Inland Marine Insurance?

– Provides 24/7, 365-day coverage.

– Safeguards businesses involved in importing, exporting, or transporting goods within India.

– Covers goods in transit via various modes, including road, rail, and air.

– Protects against potential damage, loss, accidents, and perils during operations

Key Benefits in a Nutshell

– Extensive coverage for various risks.

– Damage due to accidents, theft, natural disasters, and fire incidents included.

– General expenses like contributions to general average, salvage costs, and sue and labour expenses covered.

– Protection against liabilities arising from collisions, contact with other vessels, or property damage.

– Coverage for delays in transit, quarantine compensation, temperature-controlled cargo, and more.

Who Needs Commercial Inland Marine Insurance?

– Essential for importers, exporters, manufacturers, distributors, and businesses involved in goods transportation.

– Beneficial for those dealing with valuable items.

The Crucial Coverage – Explained

– Comprehensive coverage for goods in transit via various modes.

– Includes protection for damage due to accidents, theft, natural disasters, and fire incidents.

Standard Coverage under Marine Insurance Policy:

1. Accident Cover : This covers damage to cargo due to accidents during transportation.

2. Theft Cover: This covers the loss of cargo due to theft or pilferage.

3. Natural Disaster:This covers damage caused by natural disasters such as storms, floods, or earthquakes.

4. Fire Accident Cover: It provides coverage for losses resulting from fire incidents during transit.

5. General Expenses Cover:This covers general average contributions, salvage, and sue and labor expenses.

6. Liability Cover: It offers protection against liabilities arising from collisions, contact with other vessels, or property damage.

7. Delay in Transit Cover:This provides coverage for delays in transit that lead to financial losses.

8. Quarantine Compensation:This offers compensation for expenses incurred due to vessel detention or quarantine.

9. Temperature Sense Cover:This covers the deterioration or spoilage of perishable goods.

10. Riots, War & Civil War etc:It provides protection against risks associated with war or political unrest affecting transportation routes.

11. Business Financial Safety:It offers financial security for businesses involved in international trade or shipping.

Riding the Wave of Additional Coverage Options.

– Flexibility with additional coverage options.

– Protection for high-value goods.

– Coverage against strikes, riots, civil commotions, war, terrorism, and temperature-controlled cargo.

– Specialized coverage for items exhibited at trade shows or transported via oversized cargo.

Additional Add-ons Under the Open Marine Insurance Policy:

1. Extended Coverage for High-Value Goods: This add-on provides extra protection for transporting

valuable items, ensuring they are fully covered in case of any unforeseen incidents during transit.

2. Strikes, Riots, and Civil Commotions (SRCC) Coverage:This protects against losses or damages

caused by strikes, riots, or civil commotions during transit.

3. War and Terrorism Coverage: This provides coverage for losses or damages resulting from acts of war, terrorism, or political violence.

4. Temperature-controlled Cargo Coverage: This offers protection for perishable goods that require temperature-controlled transportation, covering losses caused by temperature deviations or equipment failures.

5. Exhibition or Trade Show Coverage: This extends coverage to goods displayed or exhibited at trade shows, exhibitions, or fairs.

6. Customised Coverage:This tailors the policy to meet the specific needs and requirements of the insured, providing additional coverage for unique or specialised goods or circumstances.

7. Valuable Papers and Documents Coverage: This add-on ensures the safety of important business documents during transit, covering the loss or damage of these valuable papers, offering financial security and minimising disruptions to your operations.

8. Loading and Unloading Clause: This clause provides coverage for any damages that occur while goods are being loaded onto or unloaded from the transport vehicle, protecting against potential losses during these critical stages.

9. ODC (Over Dimensional Cargo) Clause: The ODC clause offers specialised coverage specifically for transporting large or oversized cargo, ensuring protection for these unique shipments and addressing any potential risks associated with their transportation.

6. The Art of Claiming: How it Works

The claiming process involves systematic steps.

– Promptly notify the insurance company about the loss.

– Provide necessary documentation, including policy copy, a detailed statement, shipping documents, proof of value, and relevant evidence.

– The claim is assessed, and the eligible amount is determined for settlement.

6.1 Where are the following step which are carried out when a claim arises.

Notification: You should promptly inform the insurance company about any loss or damage that occurs during transit.

Documentation:You are required to submit necessary documents, including a copy of the policy, a detailed statement, shipping documents, proof of value, and relevant evidence.

Detailed Sales and Purchase Proofs: These documents should demonstrate your financial transactions from the policy start date to the claim initiation date.

Claim Form: You should complete and submit the provided claim form with essential information.

Additional KYC Documents: This involves including copies of identification documents, such as the Aadhaar card and PAN card, as well as a self-declaration letter of ownership.

Verification:The insurance company assesses the claim, conducts investigations if necessary, and may appoint a surveyor for assessment.

Settlement Decision:The insurance company determines the eligible amount and communicates this decision to the insured.

Additional Supporting Documents: You should also provide an image of a cancelled cheque, a subrogation letter (if applicable), and a discharge voucher.

#insurance#marine#marines#marinelife#marinette#insuranceagent#aquamarine#lifeinsurance#marinettedupaincheng#marinecorps#submariner#spacemarines#healthinsurance#insurancepolicy#policy#marinebiology#mariners#marinedrive#insurancebroker#marineconservation#insuranceagency#marineaquarium#submarine#usmarines#marinetank#carinsurance#autoinsurance#homeinsurance#insuranceagents#marinemammals

2 notes

·

View notes

Text

Protecting Your Business: The Essentials of General Liability Insurance

View On WordPress

0 notes

Text

Does Ohio Require a Permit for Roof Replacement?

Considering a roof replacement in Ohio? It's a big project, and navigating the permit process can add another layer of complexity. This blog post will break down the permit requirements for roof replacement in Ohio, helping you determine if you need one and guiding you through the application process if necessary.

Understanding the Rules: Ohio Building Code

The Ohio Building Code dictates permit requirements for various construction projects, including roof replacement. Section 1507 of the code outlines the specific scenarios when a permit becomes mandatory.

In general, a permit is required for roof replacements that involve:

Structural Changes: Any alterations or replacements to the roof's structural components, such as rafters, trusses, or sheathing, necessitate a permit.

Mechanical Equipment: Replacing rooftop mechanical equipment like vents, skylights, or chimneys typically requires a permit.

Simple Roof Replacement vs. Complex Projects

For a standard roof replacement that solely involves replacing the existing roofing material (shingles, metal, etc.), you likely won't need a permit. However, there are some exceptions:

Number of Layers: If your existing roof has two or more layers of shingles, removing them all before installing the new roof might be mandatory. This can impact the overall project scope and potentially require a permit.

Historic Districts: Residing in a designated historic district often comes with additional regulations. You might need a Certificate of Appropriateness (COA) to ensure the new roof adheres to the district's aesthetic guidelines.

Benefits of Obtaining a Permit

Even if your project seems straightforward, obtaining a permit offers several advantages:

Safety Assurance: The permitting process involves inspections by qualified professionals who ensure the project adheres to building codes, promoting the structural integrity and safety of your roof.

Increased Value: A permitted roof replacement can enhance your property value as it demonstrates adherence to safety standards.

Peace of Mind: Having a permit removes the worry of potential future complications during resale or insurance claims.

The Permit Application Process

If your roof replacement falls under the permit-required category, here's a general overview of the application process:

Contact Your Local Building Department: The first step is to get in touch with your local building department. They will provide specific details on permit requirements and application procedures in your area.

Project Details and Drawings: Prepare a detailed description of your project, including the scope of work, materials to be used, and any relevant drawings or plans.

Fees and Inspections: Pay the associated permit fees and schedule inspections with building officials throughout the project.

Finding Qualified Roofers in Milford, Ohio

Now that you understand the permit requirements, it's crucial to find qualified and experienced roofers in Milford, Ohio, to handle your project. Here are some tips for your search:

Licensing and Insurance: Ensure the roofers hold valid licenses and carry adequate insurance coverage for liability and worker's compensation.

Experience and References: Look for roofers with a proven track record in roof replacement projects similar to yours. Ask for references and check online reviews.

Warranties and Guarantees: Inquire about the warranties offered on materials and workmanship. A reputable roofing company will stand behind their work.

Roof Leak Repair vs. Full Replacement

When considering a roof replacement, it's essential to differentiate between a full replacement and a roof leak repair. A minor leak might be addressed through repairs, potentially avoiding the permit process. However, extensive leaks or widespread damage often necessitate a complete roof replacement, which might fall under permit requirements. Consulting a qualified roofer will help you determine the best course of action for your specific situation.

Conclusion

Navigating the permit process for a roof replacement in Ohio can seem daunting. However, with this information as a guide, you can determine if a permit is necessary and ensure your project adheres to safety regulations. Remember, a permitted roof replacement offers peace of mind, protects your investment, and enhances the value of your property.

For roof leak repair, roof replacement, or to connect with qualified roofers in Milford, Ohio, don't hesitate to contact us today!

3 notes

·

View notes

Text

Although the media has dismissed previous calculations that Covid is now more contagious than measles, the current data tells a different story. According to the Pandemic Mitigation Project, we'll soon be averaging 2 million cases per day. If nothing else, that gives the flu a run for its money. As we've seen now, Covid spreads in the spring, the summer, the fall, and the winter. This is what your friends and family think you should be fine with.

In response, governments are rolling out plans to reduce the number of people who qualify for disability benefits. In the U.S., the Census Bureau plans a new survey that will lower their official disability count by 20 million people. As a piece in STAT warns, this change "will artificially reduce national estimates of disability almost by half." The Bureau acknowledges this intent. That's the entire point. As Nate Bear writes, Britain is making a similar move, eliminating their minister for the disabled.

As OK Doomer previously wrote, the CDC has stopped reporting excess mortality, after manipulating their own data. Insurance companies are changing their eligibility guidelines and denying claims. In many cases, your health insurance provider now requires you to report Covid infections, and they use that information to reject coverage.

Meanwhile, you can now find Covid liability disclaimers almost everywhere, even on your concert tickets.

3 notes

·

View notes

Text

Decoding the Basics: Understanding Different Types of Insurance

Introduction

Protection is a fundamental part of our lives, giving a security net in the midst of vulnerability and unanticipated occasions. A monetary plan offers insurance against expected misfortunes, relieving the effect of mishaps, diseases, or other unfriendly circumstances. While protection is a typical term, understanding its different sorts can be perplexing. In this article, we will disentangle the nuts and bolts and dig into the various sorts of protection that take care of assorted needs.

Kinds of Protection

Extra security:

One of the principal kinds of protection, extra security offers monetary help to recipients in case of the policyholder's passing. This guarantees that wards are not left in a monetary sway, covering memorial service costs, obligations, and continuous living expenses. There are two essential kinds of disaster protection: term life coverage, which gives inclusion to a predetermined term, and entire extra security, which covers the policyholder for as long as they can remember.

Health care coverage:

With the increasing expenses of medical services, it is critical to have health care coverage. Health care coverage covers clinical costs, including medical clinic stays, medical procedures, meds, and preventive consideration. It goes about as a safeguard against over the top medical care costs, offering people admittance to important clinical benefits without devastating monetary weights. Health care coverage plans shift generally, from essential inclusion to exhaustive strategies that incorporate extra advantages.

Accident coverage:

Collision protection is a legitimate prerequisite for vehicle proprietors in many spots. It gives inclusion to harms and liabilities emerging from mishaps. This incorporates fixes to your vehicle, clinical costs, and legitimate expenses. Accident coverage can likewise offer assurance against robbery, defacing, and cataclysmic events. The degree of inclusion relies upon the kind of approach and the particular requirements of the policyholder.

Property holders/Leaseholders Protection:

Whether you own or lease a home, having protection to safeguard your residence is crucial. Mortgage holders protection covers the construction of the house, individual possessions, and responsibility for wounds that might happen on the property. Leaseholders protection, then again, safeguards the occupant's very own property and gives risk inclusion. The two kinds of protection guarantee that startling occasions like fire, burglary, or catastrophic events don't prompt crushing monetary misfortunes.

Travel Protection:

Go protection is intended to cover startling occasions during trips, including trip retractions, health related crises, lost things, and travel delays. It gives a security net to explorers, offering true serenity and monetary assurance notwithstanding unanticipated conditions. The inclusion shifts, so fundamental to pick a strategy lines up with the kind of movement and potential dangers implied.

Particular Protection: Fitting Inclusion to Remarkable Necessities

Past the central sorts of protection, there exists a range of specific inclusion custom fitted to exceptional necessities and enterprises. These approaches address explicit dangers that may not be satisfactorily covered by standard protection plans. The following are a couple of models:

Proficient Obligation Protection:

Experts like specialists, legal counselors, and advisors frequently settle on proficient risk protection, otherwise called mistakes and oversights protection. This inclusion safeguards against cases of carelessness or inability to enough perform proficient obligations. In fields where counsel and administrations can have huge results, proficient risk protection is a critical shield.

Digital Protection:

As our reality turns out to be progressively computerized, the requirement for security against digital dangers has flooded. Digital protection assists organizations and people with alleviating the monetary effect of information breaks, hacking, and other digital occurrences. It covers costs connected with information recuperation, legitimate liabilities, and notice costs, giving a wellbeing net in the perplexing domain of computerized security.

Pet Protection:

For some, pets are vital individuals from the family, and their wellbeing and prosperity are of central significance. Pet protection covers veterinary costs, medical procedures, and therapies, guaranteeing that pet people can give the best consideration to their shaggy sidekicks without the weight of extreme doctor's visit expenses.

Occasion Protection:

Arranging occasions, whether weddings, shows, or meetings, includes huge ventures. Occasion protection safeguards coordinators against unexpected conditions that might prompt abrogations or disturbances. This can incorporate outrageous climate, seller flake-outs, or other unforeseen difficulties, offering monetary response for occasion organizers.

Long haul Care Protection:

As individuals live longer, the requirement for long haul care protection has become progressively significant. This kind of protection takes care of the expenses related with broadened clinical consideration or help with day to day living exercises for people who can't really enjoy themselves because old enough, ailment, or handicap.

The Significance of Sufficient Inclusion

While protection is a significant device for moderating dangers, the critical lies in picking the perfect proportion of inclusion. Underinsuring can leave people powerless against startling monetary weights, while overinsuring may bring about superfluous costs. Standard evaluations of inclusion needs, particularly during life changes like marriage, the introduction of a kid, or significant buys, are fundamental to guarantee that insurance contracts line up with current conditions.

In addition, the agreements of insurance contracts can be unpredictable. It's urgent for people to completely figure out the subtleties of their inclusion, including deductibles, prohibitions, and guarantee processes. Customary correspondence with insurance suppliers and occasional contract surveys can assist people with remaining informed about changes in inclusion and guarantee that their assurance stays satisfactory.

In the multifaceted trap of life's vulnerabilities, protection fills in as a balancing out force, offering a security net for people, families, and organizations. From primary approaches like life, wellbeing, and accident protection to specific inclusion taking care of remarkable dangers, the assorted cluster of protection choices mirrors the unique idea of our cutting edge lives.

Interpreting the essentials of protection includes understanding the sorts accessible as well as perceiving the significance of customization. Every individual's circumstance is novel, and protection ought to be custom fitted to individual requirements and conditions. As you explore the scene of protection, think of it as a monetary item as well as an essential instrument for invigorating your future against the unexplored world.

Fundamentally, protection is a proactive interest in versatility. It changes the capricious into the sensible and enables people to confront life's vulnerabilities with certainty. Thus, whether you're shielding your business, safeguarding your computerized resources, or guaranteeing the prosperity of your darling pets, understanding the subtleties of protection is the way in to a safer and strong future.

Conclusion

Protection is a diverse idea that assumes a crucial part in defending people and their resources. From extra security, which guarantees monetary solidness for friends and family after one's downfall, to medical coverage, offering a wellbeing net in the midst of sickness, and accident coverage, safeguarding against the vulnerabilities out and about — each type fills a remarkable need.

Understanding the various sorts of protection is urgent for coming to informed conclusions about inclusion that lines up with individual requirements and conditions. While these are only a couple of models, there are numerous other particular insurance contracts taking care of explicit dangers and businesses.

In our current reality where vulnerabilities are unavoidable, protection gives a conviction that all is good and monetary security. It's not just a monetary item but rather an instrument that enables people to explore life's difficulties with versatility. As you investigate the different kinds of insurance accessible, think about your remarkable circumstance, survey possible dangers, and pick contracts that offer exhaustive inclusion.

Generally, protection is a proactive measure — one that changes unexpected dangers into sensible difficulties. Thus, whether it's getting your family's future, safeguarding your wellbeing, or guaranteeing your property and possessions, unraveling the essentials of protection is the most important move toward a safer and tough future.

2 notes

·

View notes

Text

Choosing a Music Dealer Insurance Plan: Crucial Aspects to Consider

Running a music instrument dealership means many facets to consider. From managing inventory to providing excellent customer service, the responsibilities can be endless and, sometimes, overwhelming. Among these responsibilities, one often overlooked but essential aspect is insurance. The right Music Dealer Insurance plan can safeguard your business against unexpected events and liabilities. Let's dive into the crucial aspects to consider when choosing music instrument dealer insurance.

The Music Industry Landscape

Before we dive into the intricacies of insurance, it is essential to understand the unique landscape of the music instrument industry. Music stores and dealerships vary widely, from small, independent shops to large, multi-location retailers. The inventory may range from guitars and pianos to rare and valuable vintage instruments. Therefore, the insurance needs of each music instrument dealer can be diverse.

Types of Insurance Coverage You May Need

• General Liability Insurance: This is a foundational coverage that every music instrument dealer should have. It protects your business from third-party claims of bodily injury, property damage, or advertising injury.

• Property Insurance: Your inventory is the lifeblood of your business. Property insurance will protect your music instruments, equipment, and the physical structure of your store from fire, theft, vandalism, and other perils.

• Product Liability Insurance: Do you sell musical instruments? Product liability insurance is crucial. It protects you if a product you sell causes harm or injury to a customer. It is particularly vital if you sell instruments with electrical components or accessories.

• Business Interruption Insurance: This type of coverage can be a lifeline if your store has to shut down temporarily due to a covered event. It helps cover ongoing expenses like rent, payroll, and utilities, ensuring your business can survive challenging times.

Assessing Your Needs

Now that you are familiar with the types of insurance coverage available, it is necessary to assess your specific needs. Every music instrument dealer is unique, and your insurance requirements may differ from others. Here are some factors to consider:

• Inventory Value: The total value of your inventory plays a significant role in determining your insurance needs. Make sure your Music Dealer Insurance coverage adequately reflects the worth of your musical instruments.

• Location: The geographic location of your store can impact your insurance rates. High-crime areas or regions prone to natural disasters may require additional coverage.

• Business Size: The size and scale of your music instrument dealership will influence your insurance needs. Larger businesses with multiple locations may need broader coverage than a small, single-store operation.

• Customer Base: Consider the demographics of your customer base. Are you catering to professional musicians, beginners, or collectors? The type of clientele you serve can affect your liability exposure.

Finding the Right Insurance Provider

Choosing the right insurance provider is as crucial as selecting the right coverage. Here are some tips to help you make an informed decision:

• Specialization: Look for insurance providers with experience in the music instrument industry. They will be more attuned to your specific needs and potential risks.

• Reputation: Research the reputation of the insurance company. Read reviews and ask for referrals from fellow music instrument dealers. A reliable insurer should have a track record of fair claims handling.

• Customization: Seek an insurer who can customize your insurance plan to suit your unique needs. A one-size-fits-all approach may not provide the necessary protection for your business.

• Cost and Deductibles: Compare quotes from multiple insurers to find a balance between coverage and cost. Consider the deductibles and premium rates to ensure they align with your budget.

Conclusion

In the world of music instrument dealerships, insurance is a vital aspect that should not be overlooked. Choosing the right insurance plan involves careful consideration of your unique needs, assessing the types of coverage required, and selecting a reputable insurance provider. By investing time and effort into securing the right insurance, you can protect your music instrument dealership from unforeseen challenges and continue to make beautiful music for years to come.

#music#musicians#music dealer insurance#musical instrument#insurance#insurance coverage#insurance company

3 notes

·

View notes

Text

Auto Liability Insurance Coverage: A Comprehensive Guide for Drivers

Introduction:

Auto liability insurance coverage serves as a cornerstone of responsible vehicle ownership, providing essential financial protection in the event of accidents. Understanding the nuances of auto liability insurance coverage is paramount for drivers, as it not only safeguards their financial well-being but also ensures compliance with legal requirements. In this comprehensive guide, we delve into the intricacies of auto liability insurance coverage, exploring its types, benefits, factors influencing premiums, and strategies for maximizing protection while minimizing costs.

Exploring Types:

Auto liability insurance typically comprises two primary components: bodily injury liability coverage and property damage liability coverage. Bodily injury liability coverage offers protection against medical expenses, lost wages, and legal fees incurred by other parties involved in accidents where the insured driver is at fault. Conversely, property damage liability coverage covers the cost of repairing or replacing damaged property, such as vehicles or structures, belonging to others.

Benefits of Coverages:

The benefits of auto liability insurance coverage extend beyond financial protection. Firstly, it shields drivers from substantial out-of-pocket expenses arising from accidents, providing invaluable peace of mind. Additionally, auto liability insurance coverage facilitates compliance with legal mandates, as most states require drivers to carry a minimum level of liability insurance. Moreover, possessing adequate auto liability insurance coverage instills confidence in drivers, allowing them to navigate roads without undue worry.

Factors Influencing Insurance Premiums:

Several factors play a pivotal role in determining auto liability insurance premiums. These include the driver's age, driving record, location, and the type of vehicle being insured. Drivers with a history of accidents or traffic violations typically face higher premiums, as they are perceived as higher-risk individuals. Similarly, those residing in areas prone to accidents or vehicle theft may also encounter elevated premiums. Additionally, coverage limits and deductibles chosen by drivers can impact premiums, with higher coverage limits and lower deductibles often resulting in increased costs.

Strategies for Optimizing Insurance Coverage:

To maximize auto liability insurance coverage while minimizing costs, drivers can employ several strategies. Maintaining a clean driving record is paramount, as it demonstrates responsible driving behavior and can lead to lower premiums over time. Additionally, opting for higher deductibles and periodically reviewing coverage limits can help balance protection and affordability. Comparing quotes from multiple insurers and taking advantage of available discounts, such as those for bundling policies or completing defensive driving courses, can also result in cost savings.

Conclusion:

Auto liability insurance coverage serves as a critical safeguard for drivers, offering financial protection and peace of mind on the road. By understanding the types of coverage available, the benefits it provides, and the factors influencing premiums, drivers can make informed decisions when selecting auto liability insurance policies. With diligent attention to coverage needs and cost-saving strategies, drivers can navigate the complex landscape of insurance coverage effectively by trucking insurance agency, ensuring comprehensive protection without breaking the bank.

Source: https://bityl.co/OEvP

#southwestern insurance#trucking insurance agency#southwestern trucking#general liability insurance cost#cargo liability insurance#auto liability insurance coverage#liability insurance coverage#trucking insurance services

0 notes

Text

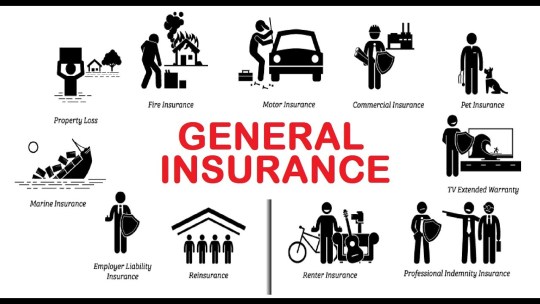

What is general insurance? - Insurance

What is general insurance? — Insurance

Understanding General Insurance: A Comprehensive Guide

General — Insurance plays a vital role in safeguarding individuals and businesses from unforeseen risks and financial uncertainties. One of the most common types of insurance is general insurance, which encompasses a wide range of policies designed to protect against non-life risks. In this article, we will delve into the world of general insurance, exploring its definition, key categories, importance, and how to choose the right coverage for your needs.

What is General Insurance?

General insurance, also known as non-life insurance, is a financial product that provides protection against various risks, excluding life-related risks. Unlike life insurance, which pays out benefits upon the policyholder’s death or maturity, general insurance policies offer coverage for specific contingencies, such as accidents, theft, property damage, and liability claims.

Key Categories of General Insurance

Health Insurance:

Health insurance policies cover medical expenses incurred due to illness, injury, or accidents. They can include individual health plans, family floater policies, and group health insurance provided by employers.

Motor Insurance:

Motor insurance encompasses policies for automobiles, including cars, motorcycles, and commercial vehicles. The two primary types are:

Third-party liability insurance, which covers damages and injuries caused to third parties.

Comprehensive insurance, which also covers damages to the insured vehicle.

Home Insurance:

Home insurance protects your residence and its contents against various risks, including fire, theft, natural disasters, and structural damage. It includes building insurance and content insurance.

Travel Insurance:

Travel insurance provides coverage for unforeseen events while traveling, such as trip cancellations, medical emergencies, baggage loss, and personal liability.

Property Insurance:

Property insurance extends beyond homes and covers commercial properties, warehouses, and other assets. It safeguards against fire, theft, vandalism, and natural disasters.

Liability Insurance:

Liability insurance protects individuals and businesses from legal claims arising from injuries, damages, or accidents for which they may be held responsible. Examples include professional liability insurance, public liability insurance, and product liability insurance.

Marine Insurance:

Marine insurance covers goods and cargo transported via sea, air, or land. It mitigates risks associated with damage, theft, or loss during transit.

Also Check: <<< Trending Topics >>>

Importance of General Insurance

Financial Protection: General insurance provides a safety net, ensuring that individuals and businesses do not face significant financial losses in the event of unforeseen incidents.

Legal Requirements: In many countries, certain types of general insurance, such as motor insurance, are mandatory by law to protect third parties in case of accidents.

Peace of Mind: Knowing that you have insurance coverage gives peace of mind, reducing stress and anxiety related to potential risks.

Risk Management: General insurance allows individuals and businesses to manage risks effectively by transferring them to insurance companies.

How to Choose the Right General Insurance Coverage

Assess Your Needs: Identify the specific risks you want to protect against and assess your budget to determine the coverage you require.

Research Insurers: Compare policies and quotes from different insurance companies to find the most suitable option for your needs.

Understand Policy Terms: Carefully read and understand the terms and conditions, including coverage limits, deductibles, and exclusions.

Seek Professional Advice: Consult with insurance agents or brokers who can provide expert guidance on selecting the right coverage.

Review Regularly: Reevaluate your insurance needs regularly, especially when major life events occur, such as marriage, the birth of a child, or buying a new home or vehicle.

Conclusion

General insurance is a crucial component of financial planning, offering protection against a wide range of non-life risks. Whether it’s safeguarding your health, home, vehicle, or business, having the right general insurance coverage can provide peace of mind and financial security when you need it most. By understanding the different types of general insurance and assessing your needs, you can make informed decisions to ensure your protection in an unpredictable world.

NEXT TO >>>

3 notes

·

View notes

Last Seen Blogs

accidentallyhaikud

Accidentally Haikud

linkbrix09

The Blogging of Rutledge 789

aucklandoutsider-blog

AucklandOutSider

maybeimjustpretending-blog

well i’m stuck in 2006

cantsayitbywords-blog

So many reason to smile