#banking and finance software development

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Mobile Tumblr US users spend an average of 4.04 minutes per session on the app.

Text

Banking and Finance Software Development: Transforming the Financial Landscape in the USA, India, and the UK

The financial sector is experiencing unprecedented transformation, driven by advances in technology and shifting consumer expectations. At the heart of this change lies banking and finance software development, a crucial element in enabling institutions to offer seamless, secure, and innovative services. As digital banking becomes the norm rather than the exception, understanding the nuances of software development in this space is essential. In this blog, we will explore how software development is reshaping the financial landscape in the USA, India, and the UK, highlighting the trends, challenges, and future prospects of this dynamic industry.

The Growing Need for Advanced Banking Software Solutions

Modern banking goes beyond handling transactions; it’s about delivering a holistic, user-centric experience. Customers now expect digital-first solutions that allow them to manage their finances anytime, anywhere, with minimal friction. To meet these expectations, financial institutions are increasingly turning to custom software development. This includes a wide array of solutions such as:

1. Core Banking Solutions

Core banking software is the backbone of financial institutions, handling all aspects of daily operations like deposits, withdrawals, loans, and more. Modern core banking solutions are designed to be scalable and flexible, enabling banks to operate seamlessly across multiple channels and locations. This is particularly crucial for banks with a global presence, such as in the USA, India, and the UK.

2. Digital Payment Systems

The rise of cashless transactions has been a significant driver of software development in the banking sector. Digital payment systems, including mobile wallets, UPI (Unified Payments Interface), and contactless payments, have become integral to the financial ecosystem. These systems not only provide convenience to users but also offer enhanced security features like multi-factor authentication and real-time fraud detection.

3. Risk Management and Compliance Software

Compliance with regulatory requirements is a major concern for financial institutions, especially in diverse markets like the USA, India, and the UK, where regulations can vary significantly. Software solutions that automate compliance processes, manage risk, and ensure data integrity are essential. These solutions help banks and financial institutions avoid hefty fines and protect their reputation.

Software Development Trends in the USA

In the USA, the financial sector is at the forefront of adopting cutting-edge technologies. The focus is on enhancing user experience, ensuring data security, and complying with stringent regulations. Key trends include:

1. Adoption of Blockchain Technology

Blockchain is revolutionizing the way financial transactions are conducted, offering unparalleled transparency and security. In the USA, both traditional banks and fintech startups are leveraging blockchain for various applications, from cross-border payments to digital identity verification. The immutable nature of blockchain makes it ideal for recording financial transactions, reducing the risk of fraud and ensuring compliance.

2. AI and Machine Learning

Artificial Intelligence (AI) and Machine Learning (ML) are transforming customer service and risk management in the financial sector. Banks are using AI-powered chatbots to provide 24/7 customer support, while ML algorithms are being deployed to detect fraudulent activities in real-time. Moreover, predictive analytics, driven by AI, enables banks to offer personalized financial advice to customers, enhancing their overall experience.

3. Embracing Open Banking

Open banking is gaining traction in the USA, albeit at a slower pace compared to Europe. By utilizing APIs (Application Programming Interfaces), banks can share financial data with third-party developers, fostering innovation in financial services. This enables the creation of new products and services, such as budgeting tools and investment platforms, tailored to meet the unique needs of individual users.

India: A Hotbed of Fintech Innovation

India's financial landscape has undergone a dramatic transformation in recent years, driven by a combination of regulatory support and a burgeoning digital economy. The country is now a global leader in fintech innovation, with a focus on making financial services accessible to all.

1. The Rise of UPI and Digital Wallets

The introduction of UPI has revolutionized digital payments in India, making it possible for users to transfer money instantly between bank accounts using their mobile devices. This has spurred the growth of digital wallets like Paytm and PhonePe, which offer a range of services from bill payments to investment options. The seamless integration of these platforms into everyday life has made cashless transactions the norm for millions of Indians.

2. Empowering Rural and Underserved Markets

Despite the rapid growth of digital banking in urban areas, a significant portion of India’s population remains underserved. Software developers are focusing on creating solutions that cater to the unique needs of rural areas, such as microfinance platforms and rural banking solutions. These platforms provide essential financial services like loans and insurance to those who have traditionally been excluded from the formal banking system.

3. Regtech and Compliance Solutions

Navigating India’s complex regulatory environment can be challenging for financial institutions. Regtech solutions, which leverage technology to manage regulatory processes, are becoming increasingly popular. These solutions help banks comply with regulations such as the Goods and Services Tax (GST) and Know Your Customer (KYC) norms, ensuring smooth and compliant operations.

The UK: Leading the Charge in Open Banking

The UK has been a pioneer in implementing open banking regulations, which are reshaping the financial sector by promoting competition and innovation. The introduction of the Second Payment Services Directive (PSD2) has set the stage for a more open and interconnected financial ecosystem.

1. Open Banking Platforms

Open banking allows customers to share their financial data with third-party providers, enabling the development of innovative financial products and services. This has led to the rise of fintech startups offering everything from personal finance management apps to digital-only banks. By leveraging open APIs, these platforms provide customers with a more integrated and personalized banking experience.

2. The Growth of Digital-Only Banks

Digital-only banks, or “challenger banks,” such as Monzo, Revolut, and Starling Bank, are disrupting the traditional banking model in the UK. These banks operate entirely online, offering a range of services from current accounts to loans without the need for physical branches. Their streamlined operations and focus on customer experience have made them particularly popular among tech-savvy millennials.

3. Compliance with PSD2 and GDPR

Compliance with PSD2 and the General Data Protection Regulation (GDPR) is a top priority for financial institutions in the UK. Software solutions that ensure secure data sharing and protect customer privacy are in high demand. These solutions not only help institutions comply with regulations but also build trust with customers by safeguarding their personal information.

Challenges in Banking Software Development

While the opportunities for innovation are vast, banking and finance software development comes with its own set of challenges. Some of the key challenges include:

1. Regulatory Compliance

Navigating the complex regulatory landscape is a major challenge for software developers in the banking sector. Regulations vary significantly across regions, and staying compliant requires a deep understanding of local laws. For instance, the USA has stringent regulations like the Dodd-Frank Act, while India’s banking sector is governed by the Reserve Bank of India (RBI). In the UK, compliance with PSD2 and GDPR is critical. Developing software that meets these diverse regulatory requirements is no small feat.

2. Cybersecurity Threats

As financial institutions increasingly move their operations online, the risk of cyber-attacks grows. Protecting sensitive financial data from hackers is a top priority for banks. Software solutions must incorporate advanced security features such as end-to-end encryption, multi-factor authentication, and real-time threat detection to safeguard customer data.

3. Legacy Systems

Many financial institutions still rely on outdated legacy systems that were not designed to handle the demands of modern digital banking. Upgrading these systems to integrate with new technologies while maintaining service continuity is a significant challenge. Software developers must find ways to modernize these systems without disrupting existing operations, which can be a complex and resource-intensive process.

The Future of Banking and Finance Software Development

The future of banking and finance software development is filled with exciting possibilities. Emerging technologies are set to further revolutionize the industry, offering new ways to enhance customer experience, improve security, and streamline operations. Some of the key trends to watch include:

1. AI-Powered Chatbots and Virtual Assistants

AI-powered chatbots are becoming an integral part of customer service in the banking sector. These virtual assistants can handle a wide range of tasks, from answering queries to assisting with transactions, 24/7. As AI technology advances, these chatbots are expected to become even more sophisticated, offering personalized financial advice and proactive support.

2. Smart Contracts and Blockchain

Smart contracts, powered by blockchain technology, have the potential to automate complex financial transactions, reducing the need for intermediaries and cutting costs. These self-executing contracts are tamper-proof and can be programmed to execute specific actions when predefined conditions are met. This has wide-ranging applications, from loan disbursements to insurance claims processing.

3. Quantum Computing

Quantum computing, though still in its early stages, has the potential to revolutionize the banking sector by performing complex calculations at unprecedented speeds. This could transform areas like risk assessment and fraud detection, enabling banks to process vast amounts of data in real-time and make more informed decisions.

Conclusion

Banking and finance software development is at the heart of the financial revolution, driving innovation and enhancing customer experience. In markets as diverse as the USA, India, and the UK, the focus is on leveraging technology to meet the unique needs of customers while navigating complex regulatory environments. As the industry continues to evolve, so too must the technology that supports it. For software developers and financial institutions alike, staying ahead of the curve will be key to success in this dynamic and rapidly changing landscape.

Whether it's through the adoption of AI, the integration of blockchain, or the implementation of open banking platforms, the future of banking and finance software development promises to be both challenging and exciting. As financial institutions continue to embrace digital transformation, the opportunities for innovation are limitless—making this an exciting time for all stakeholders involved.

0 notes

Text

Introduction to Banking And Finance Software Development

In today's fast-paced digital world, the banking and finance industry is undergoing a significant transformation. One of the critical drivers of this change is the development of sophisticated banking software. With the rise of digital banking, customers now expect seamless, secure, and efficient services from their financial institutions. This is where banking software development comes into play.

The Importance of Software for Banks

Why is software so crucial for banks? Well, think about it. Imagine trying to handle millions of transactions manually every day. It's practically impossible, right? That's where banking software steps in, automating processes, reducing errors, and enhancing overall efficiency. It's not just about keeping up with the times; it's about staying ahead in a highly competitive industry.

Evolution of Banking Software

Banking software has come a long way since its inception. From the early days of basic transaction processing systems to today's sophisticated, AI-powered platforms, the evolution has been nothing short of remarkable. Each phase of this evolution has brought new capabilities, improved security, and enhanced user experiences.

Key Features of Banking Software

Banking software isn't just about handling transactions. It's packed with features designed to make banking safer, more efficient, and user-friendly.

Security Features

First and foremost, security is paramount. Banking software incorporates advanced security measures such as encryption, multi-factor authentication, and real-time fraud detection to safeguard sensitive data and protect against cyber threats.

User Experience and Interface

A seamless user experience is a must. Modern banking software offers intuitive interfaces, easy navigation, and personalized experiences to keep customers engaged and satisfied.

Integration Capabilities

Integration is another key feature. Banking software needs to integrate smoothly with various third-party services and legacy systems to provide a cohesive and comprehensive service offering.

Types of Banking Software

Banking software isn't one-size-fits-all. Different types of software cater to different banking needs.

Core Banking Systems

Core banking systems form the backbone of banking operations, handling transactions, customer accounts, and other essential functions.

Payment Processing Software

Payment processing software is all about facilitating secure and efficient payment transactions, whether it's through credit cards, online transfers, or mobile payments.

Loan Management Software

Loan management software streamlines the loan application process, automates approvals, and manages repayment schedules, making it easier for banks and customers alike.

Investment Banking Software

Investment banking software supports complex financial activities, including trading, portfolio management, and risk assessment, helping investment banks operate more effectively.

Finance Software Development Trends

The world of finance software development is ever-evolving, with new trends emerging regularly.

AI and Machine Learning

AI and machine learning are game-changers. They enable predictive analytics, personalized financial advice, and automated customer service, revolutionizing the way banks operate.

Blockchain Technology

Blockchain technology promises to enhance transparency, reduce fraud, and streamline processes through its decentralized, immutable ledger system.

Cloud Computing in Finance

Cloud computing offers scalability, cost savings, and enhanced collaboration. More and more financial institutions are moving to cloud-based solutions to stay agile and competitive.

Benefits of Custom Banking Software Development

Custom banking software development has its unique set of advantages.

Tailored Solutions

Custom software provides tailored solutions that meet specific business needs, ensuring that banks can offer unique and differentiated services.

Competitive Edge

In a crowded market, custom software can give banks a competitive edge by enabling them to innovate and respond quickly to changing market demands.

Scalability and Flexibility

Custom solutions are scalable and flexible, allowing banks to adapt to growth and changes in the industry without overhauling their entire system.

Challenges in Banking Software Development

However, developing banking software isn't without its challenges.

Regulatory Compliance

Banks must adhere to strict regulatory requirements, which can complicate software development and implementation.

Data Security

Data security is a constant concern, requiring robust measures to protect sensitive information from breaches and cyber-attacks.

Integration with Legacy Systems

Integrating new software with existing legacy systems can be tricky, requiring careful planning and execution to avoid disruptions.

Choosing the Right Development Partner

Choosing the right software development partner is crucial for success.

Evaluating Experience and Expertise

It's important to evaluate the partner's experience and expertise in banking software development. Look for a track record of successful projects and deep industry knowledge.

Considering Cost and Timeline

Consider the cost and timeline of the project. A good partner will provide a realistic estimate and work within your budget and schedule constraints.

Checking Client Testimonials

Client testimonials and reviews can provide valuable insights into the partner's reliability, quality of work, and customer satisfaction.

Conclusion

In conclusion, banking and finance software development is a dynamic and critical field that drives the efficiency, security, and innovation of financial institutions. By embracing the latest technologies and trends, banks can offer superior services, meet regulatory requirements, and stay competitive in a rapidly changing market.

FAQs

Q1: What are the key benefits of custom banking software development?

A1: Custom banking software development offers tailored solutions, competitive edge, and scalability, allowing banks to meet specific business needs and adapt to market changes.

Q2: How does AI and machine learning impact banking software?

A2: AI and machine learning enable predictive analytics, personalized financial advice, and automated customer service, significantly enhancing banking operations and customer experiences.

Q3: What are the main challenges in banking software development?

A3: The main challenges include regulatory compliance, data security, and integration with legacy systems, all of which require careful planning and robust measures.

Q4: Why is security important in banking software?

A4: Security is crucial to protect sensitive financial data from breaches and cyber-attacks, ensuring customer trust and regulatory compliance.

Q5: How do banks choose the right software development partner?

A5: Banks should evaluate the partner's experience and expertise, consider cost and timeline, and check client testimonials to ensure reliability and quality of work.

#Banking software development#finance software development#banking and finance course#Banking and finance software development

0 notes

Text

Smart Tech for Small Finance: The Future of Microfinance is Now

Microfinance institutions today are no longer bound by manual records or outdated systems. With the rise of advanced microfinance software solutions, rural lending is getting smarter, faster, and far more inclusive. From loan origination and KYC to credit scoring and collections—everything is now digitized, secure, and scalable.

For MFIs, this isn’t just a digital upgrade—it’s a mission enabler. Software platforms are not only improving operational efficiency but also expanding the reach of micro-credit to remote areas with real-time analytics and mobile-ready tools.

In a world where every second counts and every rupee matters, the right microfinance software is your edge.

#microfinance software solutions#financial services technology#artificial intelligence#banking software development#digital transformation in banking and finance

1 note

·

View note

Text

Transform Banking with AI & Blockchain Technology

Future-proof your financial services with TechMave’s innovative FinTech solutions.

0 notes

Text

Fintech built smarter. 🤓💻

SDH integrates cutting-edge technologies with your vision. Digital banking, blockchain, personal finance apps—done right. Explore:

#financial software development#custom app solutions#fintech#SDH#digital banking#blockchain#personal finance apps

0 notes

Text

#On-Demand Banking & Finance Software Development Company#Banking Software Development#Banking Website Development Company#Banking & Finance Software Development Solutions UAE

0 notes

Text

Top 5 Industries Revolutionizing Software Development in Australia

Find out which industries are leading the way in software development in Australia. From financial services to healthcare, see how these top 5 sectors are benefiting their businesses

To know more...

#jhavtech studios#mobileapps#jhavtechstudios#app development#web developer#technology#app developers#website designing#webdesign#mobile apps#software services#education#finance and accounting#banking

1 note

·

View note

Text

A Comprehensive Guide to Integrating Fintech in Corporate Banking Strategies

In the ever-evolving realm of corporate banking, the integration of fintech solutions has become not just a choice but a necessity for institutions striving to stay competitive and relevant in the digital age. As fintech continues to disrupt traditional banking models, corporate banks must embrace innovation to streamline processes, enhance efficiency, and deliver superior customer experiences. This comprehensive guide outlines key strategies for integrating fintech into corporate banking operations, with a focus on leveraging Xettle Technologies' cutting-edge solutions to drive sustainable growth and success.

Understanding the Fintech Landscape: Before embarking on the journey of fintech integration, it is essential for corporate banks to gain a comprehensive understanding of the fintech landscape. Fintech encompasses a broad spectrum of technologies and solutions, including artificial intelligence, blockchain, data analytics, and digital payment systems. By staying abreast of emerging trends and innovations, corporate banks can identify opportunities to leverage fintech to their advantage. Xettle Technologies, with its diverse portfolio of fintech solutions, offers a one-stop-shop for corporate banks seeking to integrate cutting-edge technologies into their operations.

Aligning Fintech with Strategic Objectives: Successful fintech integration begins with aligning fintech initiatives with corporate banking's strategic objectives. Whether the goal is to enhance operational efficiency, improve risk management, or elevate customer experiences, fintech solutions must be integrated in a manner that supports these overarching goals. Xettle Technologies works closely with corporate banking partners to tailor solutions that align with their unique strategic priorities, ensuring maximum impact and return on investment.

Identifying Key Areas for Fintech Integration: Corporate banks must identify key areas within their operations where fintech integration can drive the most significant value. This may include areas such as payments and transaction processing, risk management and compliance, customer relationship management, and data analytics. Xettle Technologies offers a wide range of fintech solutions spanning these areas, enabling corporate banks to address their most pressing challenges and capitalize on new opportunities.

Building Collaborative Ecosystems: Collaboration is key to successful fintech integration in corporate banking. Corporate banks can leverage partnerships with fintech startups, technology vendors, regulatory bodies, and industry associations to access expertise, share knowledge, and drive innovation. Xettle Technologies fosters a collaborative ecosystem, partnering with leading financial institutions and fintech firms to co-create solutions that meet the evolving needs of corporate banking clients.

Embracing Agile Development Practices: In the fast-paced world of fintech, agility is paramount. Corporate banks must adopt agile development practices to rapidly prototype, test, and iterate fintech solutions. Xettle Technologies' agile development methodology enables rapid deployment and iteration of fintech solutions, ensuring that corporate banks can adapt to changing market dynamics and customer preferences with ease.

Prioritizing Security and Compliance: Security and compliance are non-negotiables in corporate banking. When integrating fintech solutions, corporate banks must prioritize data security, privacy, and regulatory compliance. Xettle Technologies adheres to the highest standards of security and compliance, implementing robust encryption protocols, multi-factor authentication, and comprehensive risk management frameworks to safeguard sensitive financial data and mitigate cybersecurity risks.

Measuring and Monitoring Performance: Finally, corporate banks must establish metrics and KPIs to measure the performance and impact of fintech integration initiatives. By tracking key performance indicators such as cost savings, revenue growth, customer satisfaction, and operational efficiency, corporate banks can assess the effectiveness of fintech solutions and make data-driven decisions to optimize their integration efforts. Xettle Technologies provides advanced analytics and reporting capabilities, enabling corporate banks to gain actionable insights into the performance of their fintech initiatives.

In conclusion, integrating fintech corporate banking into corporate banking strategies is no longer a choice but a strategic imperative in today's digital-first landscape. By following the comprehensive guide outlined above and leveraging Xettle Technologies' innovative solutions, corporate banks can unlock new opportunities for growth, differentiation, and success in the era of fintech disruption.

#Fintech Corporate Banking#Finance#Financial Planning#Fintech#Corporate#development#fintech software#programming#technology#keywords fintech development#marketing

1 note

·

View note

Text

Is your organization struggling to manage risk? Learn how custom software and cutting-edge technologies like AI and blockchain can help you build a robust risk management framework and safeguard your future success.

#banking and finance software solution#fintech software development company#fintech software development services

0 notes

Text

Software developers are implementing. advanced cybersecurity measures such as data encryption and secure transactions.

#banking app#finance#software development#app development#code#developer#web development#fintech technology#technology#finances#artificial intelligence#machine learning ai#ai machine learning

0 notes

Text

#Certifications in Generative AI#Generative AI#Generative AI In Business#Generative AI In Cybersecurity#Generative AI In Finance And Banking#Generative AI In HR & L&D#Generative AI In Marketing#Generative AI In Project Management#Generative AI In Retail#Generative AI In Risk And Compliance#Generative AI In Software Development#Generative AI Professional Certification

1 note

·

View note

Text

6 benefits of cloud computing in banking

Greater scalabilityFraud detection

Reduced costs

Tightened security

Compliance with regulations

Customer relationship management (CRM)

Greater scalability

#digital transformation#technology#tech#it consulting#it services#mobile app developers#cloud adoption#cloud computing#banking software#finance industry#cloud transformation

1 note

·

View note

Text

LETTERS FROM AN AMERICAN

January 1, 2025

Heather Cox Richardson

Jan 01, 2025

Twenty-five years ago today, Americans—along with the rest of the world—woke up to a new century date…and to the discovery that the years of work computer programmers had put in to stop what was known as the Y2K bug from crashing airplanes, shutting down hospitals, and making payments systems inoperable had worked.

When programmers began their work with the first wave of commercial computers in the 1960s, computer memory was expensive, so they used a two-digit format for dates, using just the years in the century, rather than using the four digits that would be necessary otherwise—78, for example, rather than 1978. This worked fine until the century changed.

As the turn of the twenty-first century approached, computer engineers realized that computers might interpret 00 as 1900 rather than 2000 or fail to recognize it at all, causing programs that, by then, handled routine maintenance, safety checks, transportation, finance, and so on, to fail. According to scholar Olivia Bosch, governments recognized that government services, as well as security and the law, could be disrupted by the glitch. They knew that the public must have confidence that world systems would survive, and the United States and the United Kingdom, where at the time computers were more widespread than they were elsewhere, emphasized transparency about how governments, companies, and programmers were handling the problem. They backed the World Bank and the United Nations in their work to help developing countries fix their own Y2K issues.

Meanwhile, people who were already worried about the coming of a new century began to fear that the end of the world was coming. In late 1996, evangelical Christian believers saw the Virgin Mary in the windows of an office building near Clearwater, Florida, and some thought the image was a sign of the end times. Leaders fed that fear, some appearing to hope that the secular government they hated would fall, some appreciating the profit to be made from their warnings. Popular televangelist Pat Robertson ran headlines like “The Year 2000—A Date with Disaster.”

Fears reached far beyond the evangelical community. Newspaper tabloids ran headlines that convinced some worried people to start stockpiling food and preparing for societal collapse: “JANUARY 1, 2000: THE DAY THE EARTH WILL STAND STILL!” one tabloid read. “ALL BANKS WILL FAIL. FOOD SUPPLIES WILL BE DEPLETED! ELECTRICITY WILL BE CUT OFF! THE STOCK MARKET WILL CRASH! VEHICLES USING COMPUTER CHIPS WILL STOP DEAD! TELEPHONES WILL CEASE TO FUNCTION! DOMINO EFFECT WILL CAUSE A WORLDWIDE DEPRESSION!”

In fact, the fix turned out to be simple—programmers developed updated systems that recognized a four-digit date—but implementing it meant that hardware and software had to be adjusted to become Y2K compliant, and they had to be ready by midnight on December 31, 1999. Technology teams worked for years, racing to meet the deadline at a cost that researchers estimate to have been $300–$600 billion. The head of the Federal Aviation Administration at the time, Jane Garvey, told NPR in 1998 that the air traffic control system had twenty-three million lines of code that had to be fixed.

President Bill Clinton’s 1999 budget had described fixing the Y2K bug as “the single largest technology management challenge in history,” but on December 14 of that year, President Bill Clinton announced that according to the Office of Management and Budget, 99.9% of the government's mission-critical computer systems were ready for 2000. In May 1997, only 21% had been ready. “[W]e have done our job, we have met the deadline, and we have done it well below cost projections,” Clinton said.

Indeed, the fix worked. Despite the dark warnings, the programmers had done their job, and the clocks changed with little disruption. “2000,” the Wilmington, Delaware, News Journal’s headline read. “World rejoices; Y2K bug is quiet.”

Crises get a lot of attention, but the quiet work of fixing them gets less. And if that work ends the crisis that got all the attention, the success itself makes people think there was never a crisis to begin with. In the aftermath of the Y2K problem, people began to treat it as a joke, but as technology forecaster Paul Saffo emphasized, “The Y2K crisis didn’t happen precisely because people started preparing for it over a decade in advance. And the general public who was busy stocking up on supplies and stuff just didn’t have a sense that the programmers were on the job.”

As of midnight last night, a five-year contract ended that had allowed Russia to export natural gas to Europe by way of a pipeline running through Ukraine. Ukraine president Volodymyr Zelensky warned that he would not renew the contract, which permitted more than $6 billion a year to flow to cash-strapped Russia. European governments said they had plenty of time to prepare and that they have found alternative sources to meet the needs of their people.

Today, President Joe Biden issued a statement marking the day that the new, lower cap on seniors’ out-of-pocket spending on prescription drugs goes into effect. The Inflation Reduction Act, negotiated over two years and passed with Democratic votes alone, enabled the government to negotiate with pharmaceutical companies over drug prices and phased in out-of-pocket spending caps for seniors. In 2024 the cap was $3,400; it’s now $2,000.

As we launch ourselves into 2025, one of the key issues of the new year will be whether Americans care that the U.S. government does the hard, slow work of governing and, if it does, who benefits.

Happy New Year, everyone.

LETTERS FROM AN AMERICAN

HEATHER COX RICHARDSON

#Con Man#Mike Luckovich#Letters From An American#heather cox richardson#history#American History#Y2K#do your job#the work of government#Inflation Reduction Act#technology management#the hard slow work of governing

14 notes

·

View notes

Text

Redefining the Future: Embracing Digital Transformation in Banking and Finance

The banking and finance sector is rapidly evolving with digital transformation in banking and finance at its core. From AI-driven personalization to cloud-based platforms and real-time payments, financial institutions are embracing technology to enhance customer experience, streamline operations, and boost security. With trends like embedded finance, digital onboarding, and blockchain gaining momentum, the future of finance is smarter, faster, and more inclusive. Banks that adapt to this shift will lead in innovation and trust.

#digital transformation in banking and finance#digital transformation in banking#financial services technology#banking software development

0 notes

Note

What's up bro? After that lunar landing, India seems like the place to be! Problem is, I don't think the suitcase I brought will be enough for me to last seeing everything from the Taj Mahal to the golden temple. Can I borrow one of the DEL suitcases?

There is actually another suitcase. A fairly new aluminum suitcase from RIMOWA. Looks very expensive. And doesn't necessarily match your dusty and sweaty tourist outfit…. But since no one else has contacted me: Have fun with it!

Delhi… A really huge city. But also really challenging for a tourist who doesn't speak Hindi. But slowly you get used to the strange English they speak here. And somehow you finally find the Airbnb in the old city, a stone's throw from the Red Fort. It smells of sweat, urine and exotic spices in the stairwell. The stairs are steep and you are pretty tired. Heaving your suitcases up is really exhausting. But you have made it. You'll see what's in the big new suitcase tomorrow. You just want to sleep. It looks like the bed in the room hasn't even been made yet. You don't care about that now. Just sleep…

When you wake up the next morning, your old suitcase is gone. But also your old pajamas are gone. You lie naked in bed. And something is different… Your morning wood is hard as steel. Hehehehe, that's not bad… But it's also darker somehow. A shade like a coffee with a shot of milk. Coffee! Yes, you need it now. You get out of the silk-sheeted bed and your boner leads you like a divining rod to the coffee maker in the alcove between your dressing room and the master bath. After the first coffee, quickly take a shower and then get dressed.

And then a second coffee. Your driver will be here soon. Good thing your suitcase is already packed next to you.

You don't like Noida. But many of your friends live there because they have located their startup companies there and it is easier to find capable software developers. But that's not your world either. Your family made their money generations ago in real estate and in the textile industry. And you now head the banking and finance division in your family holding company. After all, you have financed some of your friends' startups. And today one of your friends is getting married. In Noida. You'll survive that, too.

The journey was long, as usual. Getting out of Delhi takes time. But at least you were able to make a number of phone calls while your driver navigated the car safely through the traffic chaos. Now you have moved into your suite. In the corridor hectic movements between the rooms. Bridesmaids and other guests scurry from room to room. You hate this hassle. In life, you would never think of getting married. But the bellboy who carried your suitcase upstairs was hot. You call the front desk and ask for someone to help you unpack your luggage and get dressed. The hotel is one of the most preferred locations for weddings in Noida. You are a regular guest here. They know your preferences. And the bellboys love your cock. You can already imagine that now there will be a fight again, who is allowed to blow you and gets the tip for it.

Yes, that was good… Your cock dangles relaxed between your legs. Your clothes fit perfectly. So on to the ballroom. And let's see who is your boring dinner companion this time.

88 notes

·

View notes

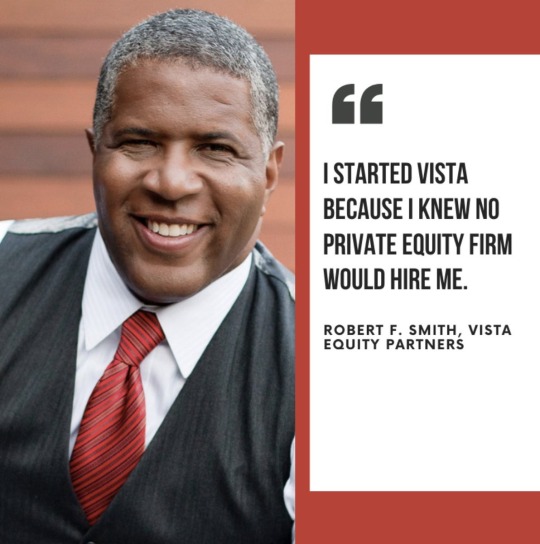

Text

Robert Frederick Smith (December 1, 1962) is a businessman, philanthropist, chemical engineer, and investor. He is the Founder, Chairman, and CEO of private equity firm Vista Equity Partners.

In high school, he applied for an internship at Bell Labs but was told the program was intended for college students. He persisted, calling each Monday for five months. When a student from M.I.T. did not show up, he got the position, and that summer he developed a reliability test for semiconductors. He earned a BS in chemical engineering from Cornell University. He became a brother of Alpha Phi Alpha. He received his MBA from Columbia University with concentrations in finance and marketing.

He worked at Goodyear Tire and Rubber Company, Air Products & Chemicals, and Kraft General Foods as a chemical engineer, where he registered two US and two European patents. He worked for Goldman Sachs in technology investment banking, first in New York City and then in Silicon Valley. He advised on mergers and acquisition activity with companies such as Apple and Microsoft. He was included in Vanity Fair’s New Establishment List, which is an annual ranking of individuals who have made impactful business innovations.

He founded Vista Equity Partners, a private equity and venture capital firm of which he is the principal founder, chairman, and chief executive. He is credited with generating a 30 percent rate of return for his investors from the company’s inception to 2020. Vista Equity Partners was the fourth largest enterprise software company after Microsoft, Oracle, and SAP, including all their holdings. Vista has invested in companies such as STATS, Ping Identity, and Jio. Vista Equity Partners had closed more than $46 billion of funding.

He was named Private Equity International’s Game Changer of the Year for his work with Vista.

The 2019 PitchBook Private Equity Awards named Vista Equity Partners “Dealmaker of the Year”. #africanhistory365 #africanexcellence #alphaphialpha

9 notes

·

View notes