#gmm 354

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

69% of Tumblr users are millennials.

Text

20 Season Premiere Episodes of GMM

January 9, 2012 to September 13, 2021

#rhett and link#link neal#randl#rhett mclaughlin#good mythical morning#gmm 1#gmm 130#gmm 215#gmm 275#gmm 354#gmm 482#gmm 597#gmm 732#gmm 832#gmm 947#gmm 1052#gmm 1161#gmm 1248#gmm 1248.1#gmm 1360#gmm 1455#gmm 1580#gmm 1665#gmm 1810#gmm 1880#gmm 2019

66 notes

·

View notes

Photo

Agreed, I don't care if your glasses are on. I'm gonna reblog that sweet beardy face all over this blog. 😘

[x]

64 notes

·

View notes

Text

Season 5 Episodes 1-10 (354-363)

S5 Ep 1 (354)-Battery Powered Gift Card

Link’s blue vest and grew a beard

Make gift cards fun for adults

BoJangles

Barbara Mandrell

Link’s mom likes shopping on QVC

WoM- Rhett gets into Link’s taxi

S5 Ep 2 (355)- Future v Past You

Message from your past you to the future you to keep you motivated

Link biting his lip or tongue

Double Shirt

Poop Log Sweatshirt

Rhett’s definition of a sculpture- Must require a 2 man lift

S5 Ep 3 (356)- Pteromerhanophobia- fear of flying

Link going to sleep instantly

Link trying to help his wife while flying

S5 Ep 4 (357)- Presidents

George Washington

Doughnuts

Martin Van Buren

Spider is hidden on the $1 bill

Kotula Metal Corrugated Flag

Canadians

Rhett gets to be the American for the day

More-Challenging Jen with US Trivia

S5 Ep 5 (358)- 12 Worst Inventions

1910- Parachute Jacket

1922- The Baby Cage

1935- Ice Skating Baby Carrie

1938- The Fire Box

1950- The Cigarette Holder for Two

1962- Sea Shoes

1963- Anti- Bandit Bag

1964- Phone Answering Robot

1970- The Shower Hood

1982- The Anti-Eating Mask

2001- The Segway

2010- The Hula Chair

TV Hat

Auctioneer School- how to learn how to speak like one

S5Ep 6 (359)- Fake Bacon Test

Rub Some Bacon on It

Turkey Bacon

Veggie Bacon

Smell the food before tasting it

Thumb Wrestle

S5 Ep 7 (360)- Ways to Stay Warm

Their friend Mike getting lost in woods with the person, he went to and had to share the heat with that person

Butter Churn Shoes

Link feeding Rhett

Fast Food Scented Candle

More- Song that doesn’t go anywhere

S5 Ep 8 (361)- Mars Audition Videos

Wet Wipes

Bodily Functions/ Potty Humor

Rhett’s Size

Astronaut

Buies Creek

Fainting while opening a barbie

Fine Brothers

S5 Ep 9 (362)- Cryptocurrency

Bit Coin

Research- Link’s version

Papa John’s

Space Tourism

S5 Ep 10 (363)- Worst Hairstyles & Good hair

Cat Turds

Jellyfish

Mall Food Court

Merle Haggard

Jill Wagner

Grace Helbig

8 notes

·

View notes

Note

hii! Thank you for your lovely gifs <3 I check them every day. I was wondering if it was okay to ask: do you remember this one gmm/gmmore episode where Rhett says that Link is a "good drawer" or "good at drawing," and Link said, "Thanks man, I didn't know you thought that about me!" with a big ol' smile? That episode warmed my heart and I am going crazy trying to find it again! continued

Anonymous said: (continued) I thought I'd try asking you bc I think you may have gifed that moment in the past. I remember Link had his wings and neckbeard in that episode, if that helps provide context (btw i think link with a beard is v hot) It's okay if you don't remember that episode, thank you!

You’re welcome! I don’t remember that specific quote and I don’t have the time to look for it now (and I haven’t giffed much from the early episodes). :S But the episodes where Link has his wings and beard are GMM 354 - GMM 359. I hope that helps!

#answer#anon#I liked that look too#:D#I might watch those episodes later#and gif the moment if I find it#^^

7 notes

·

View notes

Text

The determinants of utility of international currencies

Digital Elixir The determinants of utility of international currencies

If money could buy happiness: The determinants of utility of international currencies

The US dollar was a key currency in the Bretton Woods international monetary system. The monetary authority of the US fixed the dollar to gold, while those of other countries fixed their home currencies to the US dollar under the Bretton Woods system. This maintained the stability of exchange rates between currencies. However, the Bretton Woods system was dismantled in 1971 by the US monetary authority, bringing to an end the US dollar to gold conversion. The dollar’s position as a key currency in the current international monetary system remains, even though there is no rule under which it must be used. This phenomenon is known as the inertia of the key currency.

Given that a key currency is chosen for economic reasons that include the costs and benefits of the international currency, a comparison of these factors determines which key currency is quoted in current international monetary policy. Additionally, the inertia of a key currency should be linked to the inertia of costs and/or benefits of holding the international currency. The costs of holding the currency are related to the depreciation caused by inflation in the relevant country. In one way, the benefits of holding an international currency are the result of the utility of holding it.

Various related studies have focused on the individual roles of the US dollar as a key currency in the international monetary system. For example, Chinn and Frankel (2007, 2008) focused on its role as an international reserve currency. Eichengreen et al. (2016) analysed the role of an international reserve currency, investigating whether there was a change in the determinants of the currency composition of international reserves before and after the collapse of the Bretton Woods regime. Goldberg and Tille (2008) analysed the US dollar and other currencies as invoice currencies in international economic transactions. Ito et al. (2013) conducted a survey of all Japanese manufacturing firms listed in the Tokyo Stock Exchange on their preference of invoice currency. The ECB (2015) reported the increasing prominence of the euro as an international currency in terms of its three functions as an international reserve, in international trade, and in financial markets.

In a Sidrauski (1967)-type money-in-the-utility model (Calvo 1981, 1985, Obstfeld 1981, Blanchard and Fischer 1989), real balances of money and consumption are used as explanatory variables in a utility function. We can use this model to analyse the costs and benefits of holding international currencies. In a pair of papers (Ogawa and Muto 2017a, 2017b), we used expected inflation rates and BIS data on the total of domestic-currency-denominated debt and foreign-currency-denominated debt for the euro currency market to estimate a time series of coefficients for international currencies in a utility function. We call these coefficients the utility of international currencies.

Liquidity risk premium in an international currency affects its utility

In a later paper (Ogawa and Muto 2018) we investigated what determines the utility of four international currencies: the US dollar, the euro, the Japanese yen, and the British pound. We used a dynamic panel data model on the entire sample period from 2006Q3 to 2017Q4 to analyse the problem using generalised method of moments (GMM). Specifically, a liquidity shortage in terms of an international currency means that it is inconvenient for economic agents to use the relevant currency for international economic transactions, reducing its utility. In this analysis we focus on the liquidity premium, which represents a liquidity shortage in terms of an international currency. We conducted an empirical analysis of whether the liquidity risk premium in an international currency affects its utility.

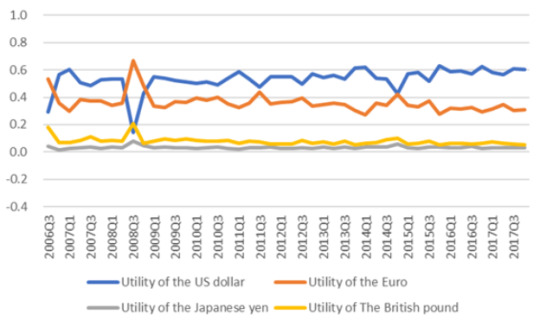

Figure 1 shows the time series of the utility of four international currencies that were estimated by using an equation based on the money-in-the-utility model. Throughout the period, changes in the utility of the US dollar, the euro, the Japanese yen and the British pound fluctuated around 0.55, 0.35, 0.02 and 0.08, respectively. We found that the utility of the US dollar sharply decreased while that for other currencies increased in 2008Q3. In particular, the utility of the euro greatly increased during that quarter.

Figure 1 Utility of international currencies

Source: Ogawa and Muto (2018) Notes: the four lines represent a time series of estimated coefficients for four international currencies (the US dollar, the euro, the Japanese yen, and the British pound) in a money-in-the-utility function. The coefficients were estimated from share of holdings of an international currency and expected inflation rates with a real interest rate estimated at 2.0%. We used BIS data on total of domestic-currency-denominated debt and foreign-currency-denominated debt of the euro currency market as the share of holdings of an international currency. The expected inflation rates are the calculated rate of change of actual CPI level and expected CPI level estimated under the assumption that the price level of each period follows ARIMA (p, d, q) process.

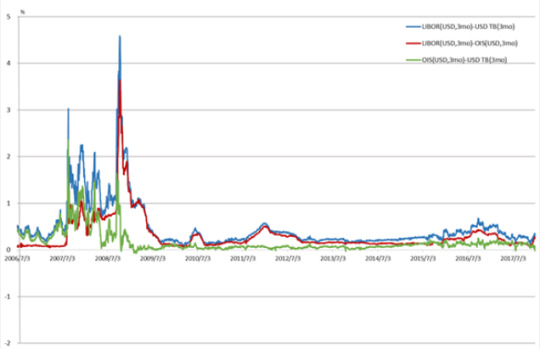

Figure 2 shows movements in three spreads of LIBOR (USD, 3 months) minus the Treasury Bills (TB) rate (USD, 3 months), LIBOR (USD, 3 months) minus the Overnight Indexed Swap (OIS) rate (USD, 3 months) (the credit risk premium), and the OIS rate (USD, 3 months) minus the TB rate (USD, 3 months) (the liquidity risk premium). We found that the US dollar liquidity shortage continued from 2006 to 2008. However, it decreased to a level less than 0.1% after the FRB started its quantitative easing monetary policy in late 2008 when at the same time it concluded and extended currency swap arrangements1 with other major central banks to provide US dollar liquidity to other countries.

Figure 2 Credit risk premium and liquidity risk premium for the US dollar

Source: Ogawa and Muto (2018). Notes: data: Datastream, Credit risk premium= LIBOR (USD, 3months) minus OIS rate (USD, 3 months), liquidity risk premium = OIS (USD, 3 months) minus US TB rate (USD, 3 months)

We obtained the following results from our empirical analysis. First, the change in the currency’s utility in the previous period has a significant positive effect on the change of the currency’s utility in the current period. This suggests that the utility of a currency tends to fluctuate in the same direction as the change in the previous period. For example, if the utility of the currency declines, we assumed that the currency is less likely to be used than in the previous period, which then continues in the next period. Second, the change of liquidity risk premium has a significant negative effect on the change in utility of the currency. This suggests that a liquidity shortage reduces the utility of an international currency. Third, the change in the share of capital flows has a significant positive effect on the change of utility of the currency. This suggests that changes in economic scale, specifically capital flows, affect the utility of the international currency.

We extracted policy implications from the empirical results. As mentioned above, liquidity risk premium and capital flows influenced the utility of the international currency. If the monetary authorities are striving to internationalise their home currencies, it is necessary to focus on these variables. It is considered that the utility of the international currency increases by conducting policies that increase the liquidity of the currency or increase international capital flows. It might be possible to push internationalisation of the home currencies through this increase of utility of the international currencies.

References

Blanchard, O J, and S Fischer (1989), Lectures on Macroeconomics, Cambridge, MA: MIT Press.

Calvo, G A (1981), “Devaluation: Level Versus Rates,” Journal of International Economics, 11 (2), 165-172.

Calvo, G A (1985), “Currency Substitution and the Real Exchange Rate: The Utility Maximization Approach,” Journal of International Money and Finance, 4 (2), 175-188.

Chinn, M, and J A Frankel (2007), “Will the Euro eventually surpass the dollar as leading international reserve currency?” In R H Clarida (ed.), G7 current account imbalances: Sustainability and adjustment, 283–338, Chicago: University of Chicago Press.

Chinn, M, and J A Frankel (2008), “Why the Euro will rival the dollar,” International Finance, 11 (1), 49–73.

European Central Bank (2015), The international role of the Euro, Frankfurt, Germany: European Central Bank.

Eichengreen, B, L Chiţu, and A Mehl (2016), “Stability or upheaval? The currency composition of international reserves in the long run,” IMF Economic Review 64 (2), 354–80.

Goldberg, L S, and C Tille (2008), “Vehicle currency use in international trade,” Journal of International Economics 76 (2), 177–92.

Ito, T, S Koibuchi, K Sato, and J Shimizu (2013), “Choice of invoicing currency: New evidence from a questionnaire survey of Japanese export firms,” RIETI Discussion Paper Series no. 13-E-034.

Obstfeld, M (1981), “Macroeconomic Policy, Exchange-rate Dynamics, and Optimal Asset Accumulation,” Journal of Political Economy, 89 (6), 1142-1161.

Ogawa, E, and M Muto (2017a), “Inertia of the US Dollar as a Key Currency through the Two Crises,” Emerging Markets Finance and Trade, 53 (12), 2706-2724.

Ogawa, E, and M Muto (2017b), “Declining Japanese Yen in the Changing International Monetary System,” East Asian Economic Review, 21 (4), 317-342.

Ogawa, E, and M Muto (2018), “What Determines Utility of International Currencies?”, RIETI Discussion Paper Series no. 18-E-077.

Sidrauski, M (1967), “Rational choice and patterns of growth in monetary economy,” American Economic Review, 57 (2), 534–44.

Endnotes

[1] The FRB concluded new currency swap arrangements with the ECB and the Swiss National Bank on December 12, 2007. Afterwards, it increased the amount of currency swap arrangements and concluded them with other central banks.

The determinants of utility of international currencies

from WordPress https://ift.tt/2GvJAeJ via IFTTT

0 notes

Photo

[x]

414 notes

·

View notes

Photo

“How was your break?” [x]

232 notes

·

View notes

Photo

“I had these two men...” [x]

229 notes

·

View notes

Photo

“There’s something different about you, Link.” [x]

#rhett and link#good mythical morning#gmm#gmm 354#gif#link looks like a hipster dude that talked my ear off about shisha once

154 notes

·

View notes

Photo

“We need to enter some sort of national competition.” [x]

126 notes

·

View notes

Photo

[x]

122 notes

·

View notes

Photo

“Tunnel vision.” [x]

112 notes

·

View notes

Photo

[x]

110 notes

·

View notes

Photo

“I think we’re gonna have to start bodyguard school.” [x]

73 notes

·

View notes

Photo

[x]

64 notes

·

View notes