#Medical Device Reprocessing Market Size

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

In 2020, 27% of US Tumblr users had an annual household income of over $100,000.

Text

#Medical Device Reprocessing Market#Medical Device Reprocessing Market Share#Medical Device Reprocessing Market Size#Medical Device Reprocessing Market Trends

0 notes

Text

#Medical Device Reprocessing Market#Medical Device Reprocessing Market Size#Medical Device Reprocessing Market Report#Medical Device Reprocessing Market growth#Medical Device Reprocessing Market Share

0 notes

Text

Automated Endoscope Reprocessing Market Overview: Global Industry Snapshot

The Automated Endoscope Reprocessing Market has emerged as a pivotal segment within the broader landscape of medical device disinfection and sterilization. As minimally invasive surgeries (MIS) continue to gain traction, the demand for high-level disinfection of endoscopic instruments has become increasingly critical. Automated endoscope reprocessors (AERs) have thus transformed from optional support systems into indispensable components of modern healthcare infrastructure.

What is Automated Endoscope Reprocessing?

Automated Endoscope Reprocessing refers to the use of specialized machines to clean, disinfect, and dry endoscopes after clinical use. The process ensures a standardized, consistent, and safe method of preparing endoscopes for reuse. AERs reduce the risks associated with human error in manual cleaning and provide traceable documentation to meet stringent regulatory compliance standards.

Market Size and Dynamics

The global Automated Endoscope Reprocessing Market has experienced consistent growth over the past decade. This growth is driven by a combination of rising surgical procedures, hospital-acquired infection (HAI) prevention protocols, and global health initiatives pushing for sterilization automation in medical settings. The market is projected to continue expanding from 2025 to 2032 due to:

Increasing geriatric population and chronic illnesses requiring endoscopy

Surge in demand for MIS procedures

Regulatory enforcement for infection control

Rising investment in hospital infrastructure

As of 2024, the market valuation is estimated to be in the range of USD 1.5 to 2 billion, with robust CAGR expectations of around 8–10% through the forecast period.

Key Market Segments

The Automated Endoscope Reprocessing Market can be segmented based on product types, end users, and regions:

Product Types: Single basin, double basin, and advanced multi-cycle units

End Users: Hospitals, ambulatory surgical centers (ASCs), specialty clinics

Geography: North America leads due to strict regulations and advanced hospital facilities, followed by Europe and Asia-Pacific, where rapid infrastructure growth is boosting demand.

Drivers of Market Growth

Several factors fuel the adoption of automated endoscope reprocessors:

Stringent Regulatory Requirements: Regulatory bodies like the U.S. FDA, CDC, and European CE authorities mandate validated cleaning protocols.

HAI Prevention and Patient Safety: AERs reduce the risk of cross-contamination and infection outbreaks.

Growing Demand for Reusable Endoscopes: Single-use scopes are costlier in the long term; thus, proper reprocessing becomes essential.

Operational Efficiency: Automated systems reduce manpower needs and provide traceable reports for compliance audits.

Challenges in the Market

Despite its rapid growth, the Automated Endoscope Reprocessing Market faces several obstacles:

High Initial Investment: The cost of acquiring and maintaining AER systems may be prohibitive for small healthcare providers.

Complexity in Operation and Maintenance: Technical training and ongoing support are critical to ensure safe and correct use.

Infrastructure Gaps in Low-Income Regions: Limited access to utilities and space can hinder adoption in rural or underdeveloped areas.

Competitive Landscape

Major players in the Automated Endoscope Reprocessing Market include:

Olympus Corporation

Getinge AB

Cantel Medical (Steris)

Ecolab Inc.

Advanced Sterilization Products (ASP)

These companies are investing in technological innovation, AI integration, and ergonomically designed units to offer better cleaning efficiency, traceability, and operator convenience.

Global Trends and Future Outlook

Global trends in the Automated Endoscope Reprocessing Market include the adoption of smart reprocessors with integrated software systems for performance monitoring, IoT-based devices for maintenance alerts, and energy-efficient designs to align with green hospital initiatives.

Moreover, the COVID-19 pandemic has led to heightened awareness of sterilization and disinfection in healthcare settings. The resulting surge in sterilization compliance continues to positively influence market growth even in the post-pandemic era.

Conclusion

The Automated Endoscope Reprocessing Market represents a critical aspect of infection control within the healthcare system. With rising emphasis on patient safety, regulatory compliance, and healthcare automation, the market is poised for significant expansion in the coming years. As technology evolves and cost-effectiveness improves, adoption is expected to widen globally—particularly in emerging healthcare markets seeking to enhance their clinical hygiene standards.

0 notes

Text

Trocars Market : Size, Trends, and Growth Analysis 2032

The Trocars Market was valued at US$ 820.90 million in 2024 and is projected to grow at a CAGR of 5.90% from 2025 to 2032. This growth is propelled by the global shift toward minimally invasive surgeries (MIS), which offer significant benefits such as faster recovery times, reduced patient trauma, and lower hospital costs. Trocars — key components in laparoscopic, thoracoscopic, and endoscopic procedures — play a vital role in enabling this transformation in surgical care.

What Are Trocars?

Trocars are specialized surgical instruments that serve as gateways into body cavities during minimally invasive procedures. A typical trocar assembly includes three parts:

Cannula: The hollow tube inserted into the body, allowing access for instruments.

Seal: Maintains insufflation pressure and prevents fluid or gas leakage.

Obturator: A pointed or blunt-tipped device used to puncture tissue and facilitate cannula insertion.

Trocars are designed to safely introduce surgical tools like cameras, scissors, graspers, and energy devices into the operative field without requiring large incisions, supporting enhanced surgical precision and patient outcomes.

Key Market Drivers

1. Rising Adoption of Minimally Invasive Surgery (MIS)

The growing preference for MIS in treating gastrointestinal, gynecological, urological, and cardiovascular conditions is a key growth factor. These procedures use fewer and smaller incisions, leading to shorter hospital stays and lower risk of complications — advantages that have made them a gold standard in many surgical disciplines.

2. Technological Advancements in Trocar Design

The market has seen continuous innovation, including bladeless and optical trocars that reduce insertion-related injuries. Newer models offer integrated valves, ergonomic handles, and anti-leakage seals, improving surgeon control and patient safety.

3. Increased Surgical Volumes Worldwide

An aging population, rising prevalence of chronic conditions like obesity and cancer, and the growing availability of healthcare services are leading to higher surgical volumes — particularly in Asia-Pacific and Latin America. This directly boosts the demand for reliable and efficient trocar systems.

4. Surge in Outpatient and Ambulatory Surgeries

With healthcare systems encouraging cost-effective treatments, many laparoscopic procedures are shifting to outpatient settings. Trocars enable these surgeries to be performed efficiently and safely with minimal infrastructure.

5. Surgeon Training and MIS Education

Medical education has increasingly integrated laparoscopic techniques into curricula, and professional bodies are encouraging adoption. The resulting increase in trained surgeons is expanding the global MIS footprint.

Product Types and Features

Bladed vs. Bladeless Trocars: Bladed trocars are sharp-tipped and used for easier penetration, while bladeless (dilating tip) trocars minimize tissue trauma and bleeding.

Optical Trocars: Equipped with a clear pathway for endoscope insertion, these allow real-time visualization during entry, reducing the risk of accidental injury.

Disposable vs. Reusable: Disposable trocars ensure sterility and eliminate reprocessing costs. Reusable trocars, while more expensive upfront, are preferred in cost-sensitive facilities.

Insufflation Trocars: These allow the introduction of CO₂ gas to expand the operative field, especially in laparoscopic procedures.

Radially Expanding Trocars: Designed to stretch tissue instead of cutting it, reducing the incidence of hernia formation at the insertion site.

Key Application Areas

General Surgery: Includes appendectomy, hernia repair, and gallbladder removal. These procedures often rely on multiple trocar ports for effective access.

Gynecology: Laparoscopic hysterectomy, ovarian cyst removal, and endometriosis treatment rely heavily on trocars.

Urology: Trocars are essential in prostatectomy and nephrectomy surgeries.

Bariatric Surgery: In weight-loss procedures like sleeve gastrectomy, multiple access points created by trocars facilitate organ resection and stapling.

Pediatric Surgery: Smaller trocar sizes are tailored for child patients, ensuring minimal impact and faster recovery.

Regional Insights

North America: Leads the market due to the high volume of minimally invasive procedures, advanced healthcare systems, and early adoption of innovative surgical technologies.

Europe: Follows closely with strong demand driven by government-funded healthcare, supportive regulatory policies, and the presence of leading manufacturers.

Asia-Pacific: The fastest-growing region, attributed to rising medical tourism, healthcare infrastructure development, and increasing awareness about MIS benefits in countries like China, India, and Japan.

Latin America and Middle East & Africa: These are emerging markets with increasing surgical intervention rates, though limited by affordability and access to advanced medical devices in certain regions.

Competitive Landscape

Global trocar manufacturers are focusing on R&D, product innovation, and strategic partnerships to expand market reach. Key players include:

Medtronic A leader in MIS equipment, Medtronic offers a wide portfolio of bladed, bladeless, and optical trocars with advanced sealing technology for enhanced surgical outcomes.

Johnson & Johnson (Ethicon Division) Offers innovative trocar systems under the Endopath brand, known for ergonomic designs, secure seals, and intuitive insertion mechanisms.

B. Braun Melsungen AG Provides high-precision trocar systems that integrate seamlessly with B. Braun's comprehensive laparoscopic surgery suite.

Teleflex Incorporated Offers disposable trocar products that ensure sterility and efficiency in high-volume surgical centers.

CONMED Corporation Supplies a range of access devices, including optical and radially expanding trocars, emphasizing surgeon comfort and patient safety.

The Cooper Companies, Inc. Through its medical device subsidiary, CooperSurgical, offers gynecology-focused trocar systems designed for precision and safety.

GENICON, INC. Specializes in cost-effective and intuitive laparoscopic access systems that cater to both developed and emerging markets.

LaproSurge and Purple Surgical UK-based manufacturers known for customizable, single-use trocar systems with competitive pricing.

Applied Medical Resources Corporation A well-known brand for its Kii® trocar line, combining high flow, low profile, and safe entry systems.

Trocar Site Closure Systems Focuses on post-procedure closure solutions that complement trocar usage and reduce postoperative complications such as hernias.

Browse more Report:

Translation Management Systems Market

Smart Implants Market

Small Molecule Sterile Injectable Drugs Market

Respiratory Syncytial Virus Therapeutics Market

Pulmonary Fibrosis Biomarkers Market

0 notes

Text

Titanium Recycling Market Growth Analysis, Market Dynamics 2025

The global Titanium Recycling market was valued at US$ 998.43 million in 2023 and is anticipated to reach US$ 1,812.07 million by 2030, witnessing a CAGR of 9.10% during the forecast period 2024-2030.

Get more reports of this sample : https://www.intelmarketresearch.com/download-free-sample/489/titanium-recycling-market

Titanium recycling is the process of recovering and reprocessing titanium and titanium-based alloys from scrap or used products for use in new applications.

Titanium is a valuable and widely used metal in a variety of industries, including aerospace, automotive, and medical devices, but it can be difficult and expensive to extract from natural sources. As a result, there is a growing interest in recycling titanium and titanium-based alloys to reduce the environmental impact and cost of production.

The major global companies of Titanium Recycling include TIMET, Kymera International, Metraco NV, EcoTitanium (Aubert & Duval), Monico Alloys, Baoji Titanium, Mega Metals, United Alloys and Metals, and Globe Metal, etc. In 2023, the world's top three vendors accounted for approximately 12% of the revenue.

This report aims to provide a comprehensive presentation of the global market for Titanium Recycling, with both quantitative and qualitative analysis, to help readers develop business/growth strategies, assess the market competitive situation, analyze their position in the current marketplace, and make informed business decisions regarding Titanium Recycling.

The Titanium Recycling market size, estimations, and forecasts are provided in terms of and revenue ($ millions), considering 2023 as the base year, with history and forecast data for the period from 2019 to 2030. This report segments the global Titanium Recycling market comprehensively. Regional market sizes, concerning products by Type, by Application, and by players, are also provided.

For a more in-depth understanding of the market, the report provides profiles of the competitive landscape, key competitors, and their respective market ranks. The report also discusses technological trends and new product developments.

The report will help the Titanium Recycling companies, new entrants, and industry chain related companies in this market with information on the revenues for the overall market and the sub-segments across the different segments, by company, by Type, by Application, and by regions.

Market Segmentation

By Company

TIMET

Kymera International

Metraco NV

EcoTitanium (Aubert & Duval)

Monico Alloys

Baoji Titanium

Mega Metals

United Alloys and Metals

Globe Metal

Grandis Titanium

Goldman Titanium

Hanwa

Toho Titanium

OSAKA Titanium

Kobe Steel

Dong-A Special Metal

Hansco

Posco

Western Metal Materials

Pangang Group Titanium Metal Materials

Qinghai Supower Tianium

Segment by Type

Titanium Solids

Titanium Turnings

Segment by Application

Titanium Ingot

Steel Industry

Others

By Region

North America

United States

Canada

Asia-Pacific

China

Japan

South Korea

Southeast Asia

India

Australia

Rest of Asia

Europe

Germany

France

U.K.

Italy

Russia

Rest of Europe

Latin America

Mexico

Brazil

Rest of Latin America

Middle East & Africa

Turkey

Saudi Arabia

UAE

Rest of MEA

Drivers

The titanium recycling market is driven by increasing demand across aerospace, automotive, and medical industries due to titanium's lightweight and corrosion-resistant properties. Recycling titanium is essential to meet supply challenges and environmental mandates, as primary titanium extraction is energy-intensive. The growing adoption of sustainable manufacturing practices further bolsters market growth. North America and Europe dominate the market due to robust aerospace industries and stringent environmental regulations.

Restraints

Despite its growth potential, the market faces challenges such as high costs associated with titanium scrap processing and limited technological advancements in some regions. The industry also grapples with supply chain issues, particularly in collecting and sorting high-quality scrap.

Opportunities

Emerging economies in Asia-Pacific present lucrative opportunities due to expanding manufacturing bases and increasing awareness about sustainable practices. Innovations in recycling technologies, such as more efficient separation and refinement processes, are anticipated to enhance market dynamics.

Get more reports of this sample : https://www.intelmarketresearch.com/download-free-sample/489/titanium-recycling-market

0 notes

Text

0 notes

Text

0 notes

Text

0 notes

Text

Disposable Endoscopes Market: Emerging Trends Shaping Future Medical Practices

The disposable endoscopes market is rapidly gaining traction within the medical device industry, driven by the increasing demand for cost-effective, safe, and infection-free diagnostic and surgical procedures. Unlike traditional reusable endoscopes, disposable variants offer single-use functionality, eliminating the risk of cross-contamination and reducing the need for complex reprocessing. This market has witnessed significant evolution due to technological innovations, rising healthcare awareness, and growing regulatory support, positioning itself as a transformative force in modern medical diagnostics and treatment.

Market Overview

Disposable endoscopes are being widely adopted across various medical specialties including urology, pulmonology, gastroenterology, and otolaryngology. With healthcare providers under constant pressure to enhance patient safety and streamline operational efficiency, single-use devices have emerged as a practical solution. The demand is particularly high in outpatient settings, emergency rooms, and intensive care units, where rapid turnaround and infection prevention are top priorities.

The global market size for disposable endoscopes has been growing steadily and is expected to continue on an upward trajectory. This growth is largely attributed to the increasing prevalence of hospital-acquired infections, the rising geriatric population, and a broader shift toward value-based healthcare models.

Key Emerging Trends

1. Integration of Smart Technologies

One of the most influential trends in the disposable endoscopes market is the integration of smart and digital technologies. Many new devices now feature advanced imaging capabilities such as high-definition visualization, real-time data transmission, and AI-assisted diagnostics. These innovations are enhancing clinical outcomes by improving diagnostic accuracy and procedure efficiency.

2. Expansion into New Specialties

Initially concentrated in urology and bronchoscopy, disposable endoscopes are now finding applications in other fields such as gastrointestinal endoscopy and ENT (ear, nose, and throat) diagnostics. As manufacturers refine designs to suit the unique needs of each specialty, the scope of application is expanding, bringing with it a broader customer base.

3. Regulatory Momentum and Guidelines

Regulatory agencies around the world are increasingly acknowledging the safety advantages of disposable medical devices. Guidelines promoting single-use endoscopes to reduce infection risks have bolstered their adoption. This regulatory backing has encouraged hospitals to invest more in these devices, especially in high-risk procedures and vulnerable patient populations.

4. Cost-Benefit Analysis Favoring Single-Use

While disposable endoscopes might seem costlier per unit compared to reusable ones, they eliminate hidden costs associated with cleaning, maintenance, repair, and sterilization. Studies and internal hospital audits have begun to reveal the long-term economic advantages of adopting single-use endoscopes, especially when factoring in litigation risks and costs of treating infections.

5. Sustainability Concerns and Eco-Friendly Initiatives

A growing concern with disposable medical devices is environmental sustainability. However, recent advancements have seen the development of recyclable materials and eco-friendly disposal solutions. Companies are increasingly focusing on designing biodegradable or low-impact devices to align with healthcare institutions' environmental goals.

Competitive Landscape

The disposable endoscopes market is highly competitive, with both established medical device giants and innovative startups vying for market share. Leading players are investing heavily in R&D to improve device performance, miniaturize components, and enhance user ergonomics. Strategic partnerships, mergers, and acquisitions are also common, as companies seek to broaden their product portfolios and gain competitive advantages.

Startups are contributing significantly by offering niche solutions with specialized functionalities, catering to underserved segments of the market. This has resulted in a dynamic ecosystem that fosters rapid innovation and responsiveness to clinical needs.

Regional Insights

North America currently holds a significant share of the global disposable endoscopes market, driven by stringent infection control protocols and advanced healthcare infrastructure. Europe follows closely, supported by favorable regulatory frameworks and rising healthcare expenditures. Meanwhile, the Asia-Pacific region is expected to witness the fastest growth due to increasing healthcare access, a growing middle-class population, and expanding hospital networks in countries like China and India.

Future Outlook

The future of the disposable endoscopes market looks promising, with continuous improvements in materials science, imaging technology, and AI integration likely to revolutionize diagnostic and surgical procedures. As healthcare systems worldwide strive for improved outcomes, patient safety, and operational efficiency, the demand for single-use endoscopic devices is expected to rise further.

In the coming years, expect to see greater standardization, cost reduction through mass production, and deeper penetration into low- and middle-income countries. These trends, combined with a proactive regulatory environment and shifting clinical preferences, position the disposable endoscopes market as a pivotal component of the evolving global healthcare landscape.

0 notes

Text

How does risk management factor into ISO 13485 Certification in Kenya?

What is ISO 13485 Certification?

ISO 13485 certification in Kenya is a worldwide standard for quality-management structures in the therapeutic gadget business. It provides the essentials for businesses, including the developing, designing introduction, adjusting and dispersing restorative devices and services.

Certification confirms that your business:

Keeps the consistency of the item and quality

Meets the requirements of the administrative department.

Uses a security approach based on risk and performance

Why is ISO 13485 Certification Imperative in Kenya?

Kenya The Drug Store and Harms Board (PPB) controls restorative devices in Kenya. In compliance with ISO 13485 consultant in Kenya:

Encourages the enrollment of items and endorsement by the PPB

Validity upgrades in contract tenders as well as open segment agreements.

Underpins will send instructions to markets like the EU and the ISO 13485 consultant in Kenya

Shows its commitment to quiet security and item dependability

Reduces the risk of product reviews and non-compliance

Who Ought to Get ISO 13485 Certified in Kenya?

ISO 13485 is perfect for:

Medical device manufacturers

The importers and exporters who deal in equipment for therapeutic use

Wholesalers and distributors

Sterilization benefit providers

Companies are creating software for the use of restorative technology.

Health offices are part of the item Reprocessing.

Steps to Get ISO 13485 Certification in Kenya

1. Hole Analysis:

Find any gaps between your frameworks currently in use and ISO 13485 requirements.

2. Documentation:

Create required documents such as a quality guide, chance management record, and strategies.

3. Framework Implementation:

Implement the standards’ requirements for operations, starting from acquisition up to the generation stage and distribution.

4. Inner Audit:

Conduct internal reviews to determine the framework’s suitability and to ensure compliance.

5. Administration Review:

Senior management assesses the results of reviews and validates preparation for external certification.

6. Certification Audit:

A certified certification body performs a two-stage audit to ensure the certification complies.

7. Certification Issuance:

After a successful test, Your company will be granted ISO 13485 consultant services in Kenya certification, which is typically large for 3 years.

Documents Required for ISO 13485 Certification

Quality method and manual

Risk administration procedures

Plan of product development and advanced files

Traceability records, as well as item labeling

Complaint handling, as well as an input system

Control and assessment of suppliers’ records

Internal Review and Remediation Activity ISO 13485 consultant services in Kenya Reports

Cost of ISO 13485 Certification in Kenya

The shiftings that are fetched are based on these factors:

Company size

Numerous facilities and products

Operation complexity

Certification body chosen

On average, ISO 13485 certification in Kenya costs between KES 200,000 to KES 800,000, which includes discussions, documentation, preparation, and audit.

Benefits of ISO 13485 Certification in Kenya

Made strides in quiet security and also changed control

Supply chain management upgraded

The showcase is available to all consumers and regulators.

Better documentation and transparency

Increased competitiveness in the private and public healthcare sectors

ISO 13485 and Kenyan Administrative Compliance

Affiliating your QMS to ISO 13485 auditor in Kenya makes a difference in ensuring that your QMS complies with local laws. By:

Pharmacy and Harms Board (PPB)

Kenya Bureau of Guidelines (KEBS)

Ministry of Wellbeing (MOH)

It will also prepare your store to be eligible for CE Checking (EU) or FDA endorsement (USA), which often requires ISO 13485 auditor in Kenya compliance.

Why Factocert for ISO 13485 Certification in Kenya?

We provide the best ISO Consultants in Kenya who are knowledgeable and provide the best solutions. Kindly contact us at [email protected]. ISO Certification consultants in Kenya and ISO auditors in Kenya work according to ISO standards and help organizations implement ISO Certification with proper documentation.

For more information, visit ISO 13485 certification in Kenya

0 notes

Text

0 notes

Text

Medical Device Reprocessing Market: Market Trends and Competitive Analysis 2024-2032

The Medical Device Reprocessing Market was estimated at USD 2.69 billion in 2023 and is projected to reach USD 9.63 billion by 2032, growing at a compound annual growth rate (CAGR) of 15.29% during the forecast period of 2024-2032. Get Free Sample Report @ https://www.snsinsider.com/sample-request/3485 Regional Analysis North America: Dominates the market due to advanced healthcare infrastructure and stringent regulatory standards promoting reprocessing practices. Europe: Exhibits significant growth driven by cost-containment measures in healthcare and increasing adoption of reprocessed devices. Asia-Pacific: Anticipated to witness rapid expansion owing to rising healthcare expenditures, growing awareness about reprocessing benefits, and the presence of a large patient pool. Market Segmentation By Type: Reprocessing Support & Services Reprocessed Medical Devices By Device Category: Critical Devices Semi-Critical Devices Non-Critical Devices By Application: Surgical Instruments Endoscopy Equipment Respiratory Care Devices Others Key Players The major key players are Stryker, Innovative Health, NEScientific, Inc., Medline Industries, LP, Arjo, Vanguard AG, Cardinal Health, SureTek Medical, Soma Tech Intl, Johnson & Johnson MedTech and other players. Key Points Reusable medical devices, such as surgical forceps and endoscopes, are essential in healthcare for their cost-effectiveness and utility across multiple patients. Proper reprocessing of these devices is crucial to eliminate contaminants and prevent infections, thereby ensuring patient safety. The increasing prevalence of chronic diseases, like asthma and COPD, underscores the importance of reprocessed surgical instruments in managing healthcare costs and sustainability efforts. Adherence to industry standards and best practices in medical device reprocessing significantly reduces infection risks and enhances patient outcomes. Supply chain challenges, including material shortages and manufacturing complexities, can impact the availability and cost of reprocessed devices. Future Scope The future of the medical device reprocessing market appears promising, with technological advancements enhancing the efficiency and safety of reprocessing methods. Innovations in sterilization technologies and the development of more durable medical devices suitable for multiple reprocessing cycles are expected to drive market growth. Additionally, increasing environmental concerns and the push for sustainable healthcare practices will likely encourage the adoption of reprocessed devices, further propelling the market forward. Conclusion The medical device reprocessing market is set for substantial growth, driven by the need for cost-effective healthcare solutions, environmental sustainability, and stringent infection control measures. As healthcare systems worldwide strive to balance quality patient care with economic and environmental considerations, the role of medical device reprocessing becomes increasingly vital. Contact Us: Jagney Dave - Vice President of Client Engagement Phone: +1-315 636 4242 (US) | +44- 20 3290 5010 (UK) Other Related Reports: Fertility Services Market Medical Power Supply Market Post Traumatic Stress Disorder Treatment Market MRI Guided Neurosurgical Ablation Market

#Medical Device Reprocessing Market#Medical Device Reprocessing Market Share#Medical Device Reprocessing Market Trends#Medical Device Reprocessing Market Size

0 notes

Link

0 notes

Text

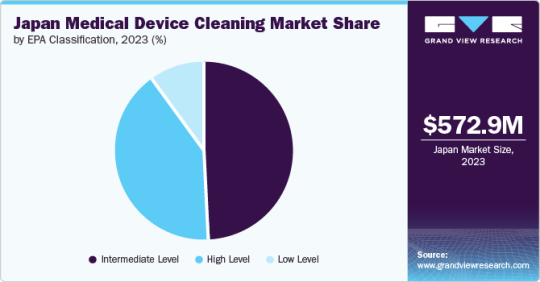

The Clean Sweep: A Report on the Japan Medical Device Cleaning Market

Japan Medical Device Cleaning Market Growth & Trends

The Japan Medical Device Cleaning Market size is anticipated to reach USD 1,169.49 million by 2030 and is projected to grow at a CAGR of 10.83% over the forecast period, according to a new report by Grand View Research, Inc. This growth can be attributed to the increasing competition among the market players and the growing efforts to reduce hospital-acquired infections.

Several studies are being published focusing on the increasing number of infections acquired in hospitals and the measures that can prevent them. For instance, a study published by the National Library of Medicine in May 2020 found that nosocomial infections, also known as healthcare-acquired infections, are a significant burden on hospitalized patients in Japan. This study analyzed the Japanese claims database and found that out of 73,962,409 inpatients registered in the database, 9.7% had community-acquired infections (CAI), and 4.7% had nosocomial infections (NI). As a result, the growing burden of hospital-acquired infections is expected to increase the demand for medical device cleaning products in Japan.

Moreover, the growing use of single-use devices and the rising manufacturing of medical devices are anticipated to propel the Japanese medical device cleaning market. Industry stakeholders are focusing on increasing the development of medical devices in the country. For instance, in May 2023, Terumo Corporation, a medical device company, invested around USD 360 million to construct a new manufacturing facility for the Medical Care Solutions Company in Japan.

In addition, in January 2022, Kaneka Corporation invested around USD 69 million to build a new medical device plant in the Tomatoh Industrial Area in the northern area of Japan. Companies are expanding their manufacturing facilities. These expanding manufacturing facilities will require medical device cleaning solutions for sterilization, reprocessing, and cleaning in the future. Thus, the rise in investments in medical device manufacturing and development in Japan is projected to increase the demand for medical device cleaning products in the coming years.

Curious about the Japan Medical Device Cleaning Market? Download your FREE sample copy now and get a sneak peek into the latest insights and trends.

Japan Medical Device Cleaning Market Report Highlights

Based on device type, the semi-critical segment dominated the market in 2023 and accounted for 46.02% of revenue share. However, the critical segment is anticipated to grow fastest over the forecast period due to the increasing infection control awareness and growing aging population.

Based on technique, the disinfection segment dominated the market in 2023 and accounted for 49.53% of the revenue share. However, the sterilization segment is anticipated to grow fastest from 2024 to 2030. Advancements in sterilization technologies are expected to boost segment growth in the coming years.

Based on EPA classification, the intermediate-level segment dominated the Japan market and accounted for the largest revenue share, 48.84%, in 2023. In contrast, the high-level segment is expected to grow fastest, with the fastest CAGR over the forecast period.

Japan Medical Device Cleaning Market Segmentation

Grand View Research has segmented the Japan Medical device cleaning market based on the device type, technique, and EPA classification:

Japan Medical Device Cleaning Device Type Outlook (Revenue, USD Million, 2018 - 2030)

Non-Critical

Semi-Critical

Critical

Japan Medical Device Cleaning Technique Outlook (Revenue, USD Million, 2018 - 2030)

Cleaning

Detergents

Buffers

Chelators

Enzymes

Others

Disinfection

Chemical

Alcohol

Chlorine & Chorine Compounds

Aldehydes

Others

Metal

Ultraviolet

Others

Sterilization

Heat Sterilization

Ethylene Dioxide (ETO) Sterilization

Radiation Sterilization

Japan Medical Device Cleaning EPA Classification Outlook (Revenue, USD Million, 2018 - 2030)

High Level

Intermediate Level

Low Level

Download your FREE sample PDF copy of the Japan Medical Device Cleaning Market today and explore key data and trends.

0 notes

Text

Single-Use Medical Device Reprocessing Market: Innovations Driving a 15% CAGR Through 2030

The global single-use medical device reprocessing market is set to witness a growth rate of 15% in the next 5 years. Rising awareness among healthcare practitioners; cost reduction pressure on hospitals and healthcare systems; increasing awareness around environmental sustainability; technological advancements in reprocessing; and rising focus on healthcare provider efficiency are some of the key factors driving the single-use medical device reprocessing market.

Single-Use Medical Device Reprocessing (SUDR) involves cleaning, sterilizing, and testing single-use medical devices (SUDs) to make them safe for reuse. This process helps reduce healthcare costs, minimize medical waste, and promote sustainability without compromising patient safety. Reprocessing includes steps such as disinfection, functional testing, and re-certification to ensure the device meets regulatory standards and performs as intended. Governed by strict guidelines from regulatory bodies like the FDA and EMA, SUDR is widely adopted in hospitals and healthcare facilities for devices such as surgical instruments, catheters, and cardiac electrodes, offering both economic and environmental benefits in modern healthcare settings.

Download a free sample report for in-depth market insights

Cost reduction pressure on hospitals and healthcare systems to propel market demand

Cost reduction pressure on hospitals and healthcare systems is a major driver of the single-use medical device reprocessing market. Reprocessing allows healthcare providers to reuse devices like surgical instruments and catheters, significantly lowering procurement costs. Hospitals can save significant costs by opting for reprocessed devices, helping them manage tightening budgets while maintaining quality care. As healthcare costs rise due to advanced treatments and an aging population, reprocessing offers an effective strategy to reduce operational expenses without compromising patient safety. These cost benefits make SUDR an attractive solution for financially constrained healthcare systems, fueling its widespread adoption.

Rising awareness among healthcare practitioners is driving the market growth

Rising awareness among healthcare practitioners about the safety, cost benefits, and environmental advantages of SUDR is driving market growth. Practitioners increasingly recognize that reprocessed devices undergo stringent cleaning, sterilization, and safety testing to meet regulatory standards, ensuring patient safety and device efficacy. This awareness is breaking down misconceptions about reprocessing, boosting confidence in its use. Additionally, healthcare professionals are becoming more attuned to the role of reprocessing in reducing medical waste and promoting sustainability. As practitioners advocate for these benefits, healthcare facilities are more likely to adopt reprocessing programs, driving the expansion of the SUDR market.

Competitive Landscape Analysis

The global single-use medical device reprocessing market is marked by the presence of established and emerging market players such as Stryker, Johnson & Johnson, SureTek Medical, Medline Industries, Inc., Vanguard AG, Arjo, Innovative Health, NEScientific, Inc., SteriPro, and MedSalv; among others. Some of the key strategies adopted by market players include new product development, strategic partnerships and collaborations, and geographic expansion.

Unlock key data with a sample report for competitive analysis:

Global Single-Use Medical Device Reprocessing Market Segmentation

This report by Medi-Tech Insights provides the size of the global single-use medical device reprocessing market at the regional- and country-level from 2023 to 2030. The report further segments the market based on device type, service provider, application, and end user.

Market Size & Forecast (2023-2030), By Device Type, USD Million

Class I Devices

Class II Devices

Market Size & Forecast (2023-2030), By Service Provider, USD Million

In-House Reprocessing

Third-Party Reprocessing

Market Size & Forecast (2023-2030), By Application, USD Million

General Surgery

Orthopaedic

Cardiology

Gastroenterology

Urology

Gynaecology

Others

Market Size & Forecast (2023-2030), By End User, USD Million

Hospitals

Ambulatory Surgical Centers (ASCs)

Others

Market Size & Forecast (2023-2030), By Region, USD Million

North America

US

Canada

Europe

UK

Germany

France

Italy

Spain

Rest of Europe

Asia Pacific

China

India

Japan

Rest of Asia Pacific

Latin America

Middle East & Africa

About Medi-Tech Insights

Medi-Tech Insights is a healthcare-focused business research & insights firm. Our clients include Fortune 500 companies, blue-chip investors & hyper-growth start-ups. We have completed 100+ projects in Digital Health, Healthcare IT, Medical Technology, Medical Devices & Pharma Services in the areas of market assessments, due diligence, competitive intelligence, market sizing and forecasting, pricing analysis & go-to-market strategy. Our methodology includes rigorous secondary research combined with deep-dive interviews with industry-leading CXO, VPs, and key demand/supply side decision-makers.

Contact:

Ruta Halde Associate, Medi-Tech Insights +32 498 86 80 79 [email protected]

0 notes

Text

Ortho Phthalaldehyde Market Size, Share, and Competitive Landscape

Rising Demand for High-Efficiency Disinfectants Drives Growth in the Ortho Phthalaldehyde Market

The Ortho Phthalaldehyde Market size was valued at USD 5.83 billion in 2023. It is expected to grow to USD 9.25 billion by 2032 and grow at a CAGR of 5.26% over the forecast period of 2024-2032.

The Ortho Phthalaldehyde (OPA) Market is driven by increasing demand for high-performance disinfectants in healthcare, pharmaceuticals, and industrial applications. OPA is widely recognized for its superior antimicrobial properties, making it a preferred alternative to traditional disinfectants like glutaraldehyde. The rising need for effective sterilization solutions, coupled with stringent hygiene regulations in hospitals and medical facilities, is fueling the market expansion. Additionally, its applications in chemical synthesis and water treatment contribute to the growing global demand.

Key Players in the Market

The Ortho Phthalaldehyde market features a competitive landscape, with key industry players focusing on product innovation, regulatory compliance, and sustainability. Leading companies in the sector include:

AK Scientific Inc.

Alfa Aesar

MP Biomedicals

DPX Fine Chemicals

Virox

Thermo Fisher Scientific Inc.

Parchem Fine & Specialty Chemicals

TCI America

Merck Millipore Corporation

Sigma-Aldrich Co. LLC

These companies are investing in advanced formulations and expanding their production capacities to cater to the growing demand for OPA-based disinfectants.

Future Scope and Emerging Trends

The future of the Ortho Phthalaldehyde Market looks promising as healthcare facilities worldwide prioritize infection control and patient safety. The shift toward non-toxic and biodegradable disinfectants is driving research into environmentally friendly OPA formulations. Moreover, the rising adoption of automated disinfection systems in hospitals and laboratories is increasing the use of OPA-based solutions. Additionally, innovations in high-purity OPA for pharmaceutical and biotechnology applications are expanding its market potential. With growing concerns over hospital-acquired infections (HAIs), the demand for OPA in sterilization and medical device reprocessing is expected to surge.

Key Market Points:

✅ Rising Healthcare Demand: Increased usage of OPA-based disinfectants in medical facilities. ✅ Superior Antimicrobial Properties: Preferred over glutaraldehyde for sterilization due to enhanced safety and efficacy. ✅ Growth in Water Treatment Applications: Expanding use in industrial and municipal water treatment processes. ✅ Regulatory Compliance: Companies focusing on meeting stringent safety and environmental standards. ✅ Advancements in Chemical Research: Ongoing R&D to develop safer and more sustainable OPA formulations.

Conclusion

The Ortho Phthalaldehyde Market is set for continued growth, driven by increasing hygiene awareness, advancements in disinfection technologies, and expanding industrial applications. As industries and healthcare providers seek safer and more effective sterilization solutions, OPA is emerging as a key component in infection control. Companies investing in sustainable production methods and innovative applications will be well-positioned to capitalize on this growing market.

Read Full Report: https://www.snsinsider.com/reports/ortho-phthalaldehyde-market-3861

Contact Us:

Jagney Dave — Vice President of Client Engagement

Phone: +1–315 636 4242 (US) | +44- 20 3290 5010 (UK)

#Ortho Phthalaldehyde Market#Ortho Phthalaldehyde Market Size#Ortho Phthalaldehyde Market Share#Ortho Phthalaldehyde Market Report#Ortho Phthalaldehyde Market Forecast

0 notes