#affordable homeownership

Text

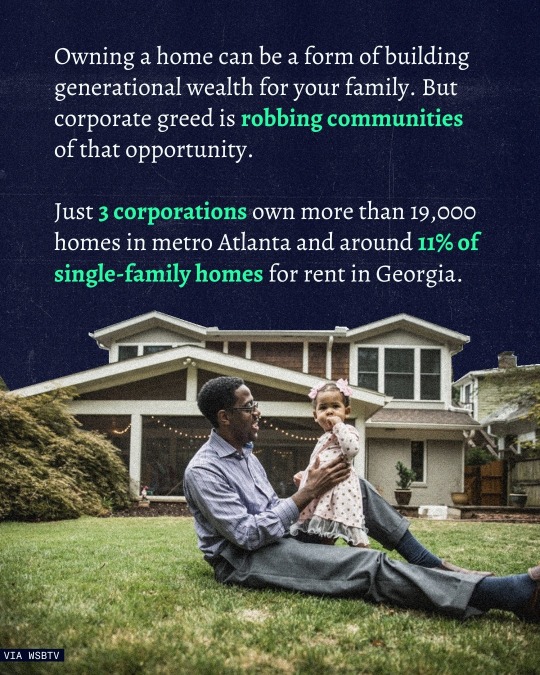

#housing inequality#corporate ownership#home equity#affordable housing#real estate market#wealth disparity#housing crisis#single-family homes#working-class families#corporate landlords#Georgia housing market#property investment#economic disparity#housing affordability#rental market#housing market inequality#corporate real estate#wealth gap#homeownership barriers#housing investment#financial disparity#real estate monopoly#housing affordability crisis#rental housing#economic inequality#property ownership#housing accessibility#corporate influence#affordable homeownership#investment firms in real estate

1K notes

·

View notes

Text

Low-income Mortgage Opportunities for First-Time Buyers in 2024

My partners and I have qualified for dozens of mortgages ourselves, and I have helped many clients through the process of obtaining a mortgage of their own. I spent many years working as a full-time professional real estate investor.

In the dynamic landscape of Canadian real estate, securing a mortgage as a first-time buyer with limited income can be challenging but not impossible. we understand…

View On WordPress

#Affordable Homeownership#Alternative Mortgage Options#First-Time Buyers#Home Financing Solutions#Low-Income Mortgage Opportunities#Specialized Mortgage Products

0 notes

Text

The Rent Is Too Damn High: The Affordable Housing Crisis, Explained

If you found this helpful, consider joining our Patreon.

#affordable housing#Affordable Housing Crisis#affordable housing movement#basic human rights#buying a house#homeownership#renting

21 notes

·

View notes

Text

By Thom Hartmann

Back in 1967, a friend of mine and I hitchhiked from East Lansing, Michigan to San Francisco to spend the summer in Haight-Ashbury. One ride dropped us off in Sparks, Nevada, and within minutes of putting our thumbs out a city police car stopped and arrested us for vagrancy.

The cop, a young guy with an oversized mustache who was apologetic for the city’s policy, drove us to the desert a mile or so beyond the edge of town, where we hitchhiked standing by a distressing light-post covered with graffiti reading “39 hours without a ride,” “going on our third day,” and “anybody got any water?”

Vagrancy laws were so 20th century.

Today, the US Supreme Court heard a case involving efforts by the City of Grants Pass, Oregon to keep homeless people off its streets and out of its parks and other public property. The city had tried a number of things when the problem began to explode in the last year of the Trump administration, as The Oregonian newspaper notes:

“They discussed putting them in their old jail, creating an unwanted list, posting signs at the city border or driving people out of town... Currently, officers patrol the city nearly every day, Johnson said, handing out [$295] citations to people who are camping or sleeping on public property or for having too many belongings with them.”

The explosion in housing costs has triggered two crises: homelessness and inflation. The former is harming the livability of our cities and towns, and the Fed’s reaction to the latter threatens an incumbency-destroying recession just as we head into what will almost certainly be the most important election in American history.

The problem with housing inflation is so severe today that without it the nation’s overall core CPI inflation rate would be in the neighborhood of Fed Chairman Jerome Powell’s 2% goal.

Graphic based on BLM data and interpretation by The Financial Times

Both homelessness and today’s inflation are the result of America — unlike many other countries — allowing housing to become a commodity that can be traded and speculated in by financial markets and overseas investors.

Forty-three years into America’s Reaganomics experiment, homelessness has gone from a problem to a crisis. Rarely, though, do you hear that Wall Street — a prime beneficiary of Reagan’s deregulation campaign — is helping cause it.

32% seems to be the magic threshold, according to research funded by the real estate listing company Zillow. When neighborhoods hit rent rates in excess of 32% of neighborhood income, homelessness explodes.

And we’re seeing it play out right in front of us in cities across America because a handful of Wall Street billionaires want to make a killing.

It wasn’t always this way in America.

Housing prices have spun out of control since my dad bought his house in 1957 when I was six years old. He got a Veteran’s Administration-subsidized loan and picked up the brand-new 3-bedroom-1-bath ranch house my 3 brothers and I grew up in, in suburban south Lansing, Michigan. It cost him $13,000, which was about twice what he made every year working a good union job in a tool-and-die shop.

When my dad bought his home in the 1950s the median price of a single-family house was 2.2 times the median American family income. Today, the Fed says, the median house sells for $479,500 while the median American personal income is $41,000 — a ratio of more than ten-to-one between housing costs and annual income.

As the Zillow study notes:

“Across the country, the rent burden already exceeds the 32% [of median income] threshold in 100 of the 386 markets included in this analysis….”

And wherever housing prices become more than three times annual income, homelessness stalks like the grim reaper.

We’re told that America’s cities have seen this increase in housing costs since the 1950s in some part because of the growing wealth and population of this country. There were, after all, 168 million people in the US the year my dad bought his house; today there are 330 million.

And it’s true that we haven’t been building enough new housing, particularly low-income housing, as 43 years of neoliberal Reaganomics have driven down wages and income for working-class people relative to all of their expenses while stopping the construction of virtually any new subsidized low-income housing.

But that’s not the only, or even the main dynamic, driving housing prices into the stratosphere — and, as a consequence, the crisis in homelessness — over the past decade. You can thank speculation for much of that.

As the Zillow-funded study noted:

“This research demonstrates that the homeless population climbs faster when rent affordability — the share of income people spend on rent — crosses certain thresholds. In many areas beyond those thresholds, even modest rent increases can push thousands more Americans into homelessness.”

So how did we get here?

It started with a wave of foreign buyers over the past 30 years (particularly from China, Canada, Mexico, India and Colombia) who, in just the one single year of 2020, picked up over 154,000 homes as their way of parking money in America. Which is part of why there are over 20 times more empty houses in America than there are homeless people.

As Marketwatch noted in a 2015 article titled “The Danger of Foreign Buyers Gobbling Up American Homes”:

“Unusual high appreciation of the aforementioned urban centers is due to the ever growing influx of foreign buyers — mostly wealthy Chinese — who view American residential real estate as the safest investment commodity. … According to a National Realtors Association survey, the Chinese spent $22 billion on U.S. housing in 12 months through March 2014…. [Other foreign buyers primarily include] Canadians, British, Indians and Mexicans.”

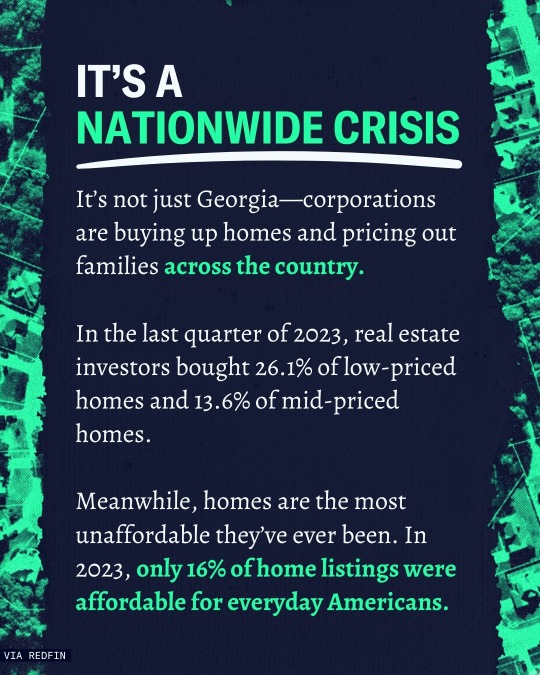

But foreign investment has been down for the past few years; what’s taken over and is really driving home prices today are massive, multi-billion-dollar US-based funds that sweep into neighborhoods and buy everything available, bidding against families and driving up housing prices.

As noted in a Wall Street Journal article titled “Meet Your New Landlord: Wall Street,” in just one suburb (Spring Hill) of Nashville, “In all of Spring Hill, four firms … own nearly 700 houses … [which] amounts to about 5% of all the houses in town.”

This is the tiniest tip of the iceberg.

“On the first Tuesday of each month,” notes the Journal article about a similar phenomenon in Atlanta, investors “toted duffels stuffed with millions of dollars in cashier’s checks made out in various denominations so they wouldn’t have to interrupt their buying spree with trips to the bank…”

The same thing is happening in cities and suburbs all across America; the investment goliaths use finely-tuned computer algorithms to sniff out houses they can turn into rental properties, making over-market and unbeatable cash bids often within minutes of a house hitting the market.

After stripping neighborhoods of homes families can buy, they then begin raising rents as high as the market will bear.

In the Nashville suburb of Spring Hill, for example, the vice-mayor, Bruce Hull, told the Journal you used to be able to rent “a three bedroom, two bath house for $1,000 a month.” Today, the Journal notes:

“The average rent for 148 single-family homes in Spring Hill owned by the big four [Wall Street investor] landlords was about $1,773 a month…”

Ryan Dezember, in his book Underwater: How Our American Dream of Homeownership Became a Nightmare, describes the story of a family trying to buy a home in Phoenix. Every time they entered a bid, they were outbid instantly, the price rising over and over, until finally the family’s father threw in the towel.

“Jacobs was bewildered,” writes Dezember. “Who was this aggressive bidder?”

Turns out it was Blackstone Group, now the world’s largest real estate investor. At the time they were buying $150 million worth of American houses every week, trying to spend over $10 billion. And that’s just a drop in the overall bucket.

In 2018, corporations bought 1 out of every 10 homes sold in America, according to Dezember, noting that, “Between 2006 and 2016, when the homeownership rate fell to its lowest level in fifty years, the number of renters grew by about a quarter.”

This all really took off around a decade ago, when Morgan Stanley published a 2011 report titled “The Rentership Society,” arguing that — in the wake of the 2008 Bush Housing Crash — snapping up houses and renting them back to people who otherwise would have wanted to buy them could be the newest and hottest investment opportunity for Wall Street’s billionaires and their funds.

Turns out, Morgan Stanley was right. Warren Buffett, KKR, and The Carlyle Group have all jumped into residential real estate, along with hundreds of smaller investment groups, and the National Home Rental Council has emerged as the industry’s premier lobbying group, working to block rent control legislation and other efforts to regulate the industry.

As John Husing, the owner of Economics and Politics Inc., told The Tennessean newspaper:

“What you have are neighborhoods that are essentially unregulated apartment houses. It could be disastrous for the city.”

Meanwhile, as unionization levels here remain among the lowest in the developed world, Reagan’s ongoing war on working people continues to wipe out America’s families.

At the same time that housing prices, both to purchase and to rent, are being driven through the roof by foreign and Wall Street investors, a survey published by NPR, the Robert Wood Johnson Foundation, and the Harvard TH Chan School of Public Health found that American families are in crisis.

Their study found:

— “Thirty-eight percent (38%) of [all] households across the nation report facing serious financial problems in the previous few months.

— “There is a sharp income divide in serious financial problems, as 59% of those with annual incomes below $50,000 report facing serious financial problems in the past few months, compared with 18% of households with annual incomes of $50,000 or more.

— “These serious financial problems are cited despite 67% of households reporting that in the past few months, they have received financial assistance from the government.

— “Another significant problem for many U.S. households is losing their savings during the COVID-19 outbreak. Nineteen percent (19%) of U.S. households report losing all of their savings during the COVID-19 outbreak and not currently having any savings to fall back on.

— “At the time the Centers for Disease Control and Prevention’s (CDC) eviction ban expired, 27% of renters nationally reported serious problems paying their rent in the past few months.”

These are not separate issues, and they are driving an explosion in homelessness.

The Zillow study found similarly damning data:

— “Communities where people spend more than 32% of their income on rent can expect a more rapid increase in homelessness.

— “Income growth has not kept pace with rents, leading to an affordability crunch with cascading effects that, for people on the bottom economic rung, increases the risk of homelessness.

— “The areas that are most vulnerable to rising rents, unaffordability, and poverty hold 15% of the U.S. population — and 47% of people experiencing homelessness.”

The Zillow study makes grim reading and is worth checking out. In community after community, when rent prices exceeded 32% of median household income, homelessness exploded. It’s measurable, predictable, and is destroying what’s left of the American working class, particularly minorities.

The loss of affordable homes also locks otherwise middle-class families out of the traditional way wealth is accumulated — through homeownership: Over 61% of all American middle-income family wealth is their home’s equity. And as families are priced out of ownership and forced to rent, they become more vulnerable to long-term economic struggles and homelessness.

Housing is one of the primary essentials of life. Nobody in America should be without it, and for society to work, housing costs must track incomes in a way that makes housing both available and affordable. This requires government intervention in the so-called “free market.”

— Last year, Canada banned most foreign buyers from buying residential property as a way of controlling their housing inflation.

— New Zealand similarly passed its no-foreigners law (except for Singaporeans and Australians) in 2018.

— Thailand requires a minimum investment of $1.2 million and the equivalent of a green card.

— Greece bans most non-EU citizens from buying real estate in most of the country.

— To buy residential housing in Denmark, it must be your primary residence and you must have lived in the country for at least 5 years.

— Vietnam, Austria, Hungary, and Cyprus also heavily restrict who can buy residential property, where, and under what terms.

This isn’t rocket science; the problem could be easily fixed by Congress if there was a genuine willingness to protect our real estate market from the vultures who’ve been circling it for years.

Unfortunately, when Clarence Thomas was the deciding vote to allow billionaires and hedge funds to legally bribe members of Congress in Citizens United, he and his four fellow Republicans opened the floodgates to “contributions” and “gifts” from foreign and Wall Street interests to pay off legislators to ignore the problem.

Because there’s no lobbying group for the interests of average homeowners or the homeless, it’s up to us to raise hell with our elected officials. The number for the Congressional switchboard is 202-224-3121.

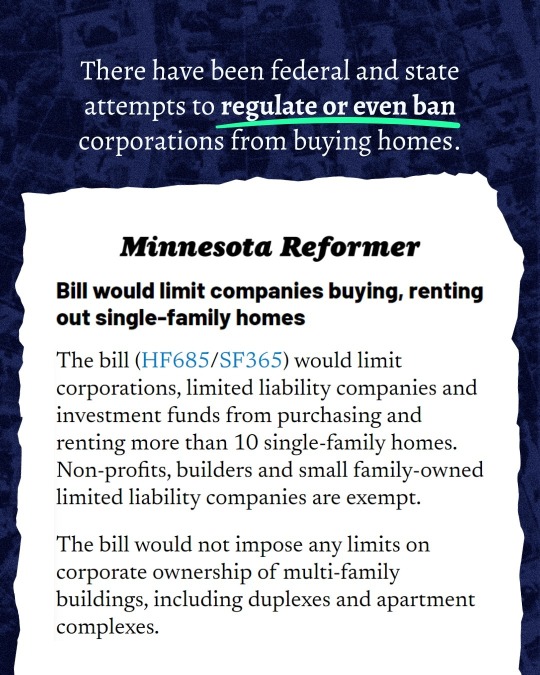

If ever there was a time to solve this problem — and regulate corporate and foreign investment in American single-family housing — it’s now.

#us politics#op ed#thom hartmann#hartmann report#common dreams#homelessness#end homelessness#housing#housing market#2024#Reaganomics#zillow#foreign buyers#Marketwatch#the Oregonian#Wall Street Journal#Ryan Dezember#Underwater: How Our American Dream of Homeownership Became a Nightmare#The Rentership Society#Morgan Stanley#The Tennessean#NPR#Robert Wood Johnson Foundation#Harvard TH Chan School of Public Health#affordable housing

16 notes

·

View notes

Text

I wanna live in the spy kids house. not for the gadgets or anything, just cause it's the most gorgeous house I've ever seen and I'm a boring adult who cares about tile backsplashes these days 🥲

#megan whines into the empty abyss of cyberspace#spy kids#the spectre of homeownership is haunting#not least of which is just because the market makes me wanna lay down and cry#why is it that only rich people can afford to have taste and then they have absolutely dogshit taste

16 notes

·

View notes

Text

cant wait to buy a house one day and have it called homeownercore by someone

#we will ignore the fact that i am an art student for the comedic effect#and also bc i really would like to be able to afford a house one day so im manifesting it for myself#homeownership

3 notes

·

View notes

Text

Exciting News from Habitat for Humanity of Greater Palm Beach County

Event Announcement

PALM BEACH COUNTY, FL– (September 4, 2024) Habitat for Humanity of Greater Palm Beach County (HFHGPBC) is excited to announce its annual Veterans Build event, generously presented by Vertical Bridge. This year’s event will take place on November 1, 2024, featuring multiple job sites across Palm Beach County. This significant fundraiser and community effort aims to support veterans and active service members.

Honoring Our Veterans

With nearly 76,000 veterans residing in Palm Beach County, Habitat for Humanity is dedicated to honoring these heroes by promoting homeownership. The Veterans Build program is pivotal in ensuring that veterans can achieve or maintain the American dream of homeownership, providing them with a secure and affordable place to live.

How You Can Get Involved

There are several impactful ways for the community to contribute to Veterans Build 2024. You can become a sponsor, participate in or organize fundraising activities and volunteer for building projects, or donate to the American Dream Fund, a special fund dedicated to Veterans Build 2024. Immediately following the build, join us for the American Dream BBQ at the Boynton Beach Arts & Cultural Center. This reception will celebrate the event’s success and honor the veterans and active service members in attendance.

Sponsor Spotlight

This year’s event is proudly presented by Vertical Bridge, a committed partner and champion for veterans in Palm Beach County. Ron Bizick, CEO of Vertical Bridge, stated, “We are honored to sponsor the Veterans Build with Habitat for Humanity of Greater Palm Beach County, marking our seventh consecutive year of support. Giving back and making a difference in our communities is profoundly important to us. Seeing the stability this housing provides to those who have devoted themselves to defending our nation’s freedom is especially fulfilling.”

Leadership and Committees

Veterans Build 2024 is co-chaired by Clint Lowe, Director of Engineering Transformation & Footprint Strategy at Carrier and U.S. Army Veteran, and Michael Maglio, Vice President of Industrial Sales at NuStar Building Materials and U.S. Marine Veteran. Both co-chairs are honored to lead this year’s event, dedicated to ensuring veterans in our community feel supported and connected as they transition from military to civilian life.

Habitat for Humanity of Greater Palm Beach County extends its gratitude to all sponsors, including Vertical Bridge read more

#Habitat for Humanity#Veterans Build#Palm Beach County#Vertical Bridge#community support#affordable housing for veterans#American Dream Fund#homeownership for veterans#charity event Palm Beach County#LoveWellington#WellingtonLiving#WellingtonNeighborhoods#WellingtonLifestyle#ExploreWellington

0 notes

Text

Housing market forecasts for the second half of the year say price growth will moderate, rates could come down slightly, and home sales will hold steady. Want to talk about what these forecasts mean for you? Reach out and let’s chat.

#losangeles#homeequity#homeownership#affordability#exprealty#reguy2009#realestatetips#smartmoves#homepriceappreciation#homevalues#realestategoals#opportunity#sellyourhouse#househunting#homegoals#realestateagent#firsttimehomebuyer#homebuying#realestateexperts#instarealtor#houseshopping#housegoals#keepingcurrentmatters

0 notes

Text

What You Need To Know About Today's Down Payment Programs

Down Payment Programs Explained

Tina Marie Miller | Loving Az Homes

Wednesday June 22nd, 2024

Buying a home has undoubtedly become more challenging, especially with today’s mortgage rates and home price appreciation. And that may be one of the big reasons you’re eager to look into grants and assistance programs to see if you qualify for anything that can help. But unfortunately, many homebuyers…

View On WordPress

#affordable housing#down payment#down payment assistance#down payment programs#first-time buyers#homebuyer assistance programs#homebuying grants#homeownership programs#mortgage rates#real estate professionals#repeat buyers

0 notes

Text

Realize Your Homeownership Dreams with SRG Housing Finance

Open the door to your dream home with SRG Housing Finance. Specializing in turning homeownership dreams into reality, we offer expert guidance and support in regional languages. Visit our website or call us at 1800 121 2399 for more details.

#SRG Housing Finance services#Home loan assistance#Affordable housing finance#Homeownership support programs#Regional housing finance options

0 notes

Link

Beverly Hills Real Estate-Beverly Hills Homes For Sale Luxury - christophechoo.com

0 notes

Text

Calculating Your New Home Budget: How Much Can You Afford to Spend?

The dream of homeownership is a beacon of hope, a testament to your aspirations and hard work. It’s the vision of your sanctuary, where the morning sun filters through the curtains and the laughter of loved ones fills the air. But before you get lost in the reverie of choosing paint colours and arranging furniture, there’s a practical question that requires your attention: How much can you…

View On WordPress

#Budgeting#debt-to-income ratio#down payment impact#Financial planning#future financial goals#home purchase finances#homeownership decision#mortgage calculations#new home affordability#PITI expenses#pre-approval process#real estate budgeting#real estate budgetingbudgeting

0 notes

Video

youtube

Fighting the Battle for Affordable Housing Bluffton SC Video #Shorts

#youtube#affordablehousing FightingtheBattle realestate affordable homeownership housing Bluffton SC Video Shorts renting renters rent homebuyers hom

0 notes

Photo

If you’ve been following the housing market over the last couple of years, you’ve likely heard about growing affordability challenges. But according to experts, the key factors that determine housing affordability are projected to improve this year. The three measures used to establish home affordability are home prices, mortgage rates, and wages. Here’s a closer look at each one. >>1. Mortgage Rates Mortgage rates shot up to over 7% last year, causing many buyers to put their plans on hold. But things are looking different today as rates are starting to come down. Even a small change in rates can impact your purchasing power. If 7% rates paused your homebuying plans last year, this could be the opportunity you need to get back in the game. >>2. Home Prices The second factor at play is home prices. Home prices have made headlines over the past few years because they skyrocketed during the pandemic. So, while prices will likely be flat this year in some markets, others could see small gains or slight declines. It all depends on your local area. >>3. Wages The final component in the affordability equation is wages. Because wages have been rising, many buyers have renewed opportunity in the market. While affordability hurdles are not completely going away this year, based on current trends and projections, 2023 should bring some sense of relief to homebuyers who have faced growing challenges. If you have questions, DM me to explore your options. You may be closer to owning a home than you think. #expertanswers #purchasingpower #buyingpower #homepriceappreciation #affordability #realestate #homevalues #homeownership #homebuying #realestategoals #realestatetips #realestatelife #realestatenews #realestateagent #realestateexpert #realestateagency #realestateadvice #realestateblog #realestatemarket #realestateexperts #instarealestate #instarealtor #realestatetipsoftheday #realestatetipsandadvice #keepingcurrentmatters (at Destin, Florida) https://www.instagram.com/p/CoAtNjNOVaj/?igshid=NGJjMDIxMWI=

#expertanswers#purchasingpower#buyingpower#homepriceappreciation#affordability#realestate#homevalues#homeownership#homebuying#realestategoals#realestatetips#realestatelife#realestatenews#realestateagent#realestateexpert#realestateagency#realestateadvice#realestateblog#realestatemarket#realestateexperts#instarealestate#instarealtor#realestatetipsoftheday#realestatetipsandadvice#keepingcurrentmatters

1 note

·

View note

Text

Central Oklahoma Habitat for Humanity’s Home Dedication Celebration Jan. 4, 2023

Central Oklahoma Habitat for Humanity’s Home Dedication Celebration Jan. 4, 2023

m.facebook.com/story.php

View On WordPress

#cohfh thanks homeownership affordable mortgage nonprofit Fox25 OKCDodgers#communications#Help#media#PR#compassion#Corporate Communications Director#Media Releases#Oklahoma

0 notes

Text

New Year 2023 Donations- Dallas Area Habitat For Humanity

Dallas Area Habitat for Humanity is a non-profit organization that works to provide affordable housing to low-income families in the Dallas area. One way the organization raises funds and collects New Year 2023 Donations is through its Habitat ReStores, retail outlets selling gently used furniture, home decor, home appliances, and other household items.

Several options are available if you are interested in donating to Dallas Area Habitat for Humanity. You can donate gently used furniture, home decor, and home appliances to a local Habitat ReStore. These donations are then sold to the public, with the proceeds going to support the organization's mission of building and repairing homes for low-income families.

In addition to donating physical items, you can also financially donate to Dallas Area Habitat for Humanity. These New Year 2023 Donations help to fund the organization's various programs and initiatives, including home construction, home repairs, and community development projects.

If you require furniture, home decor, or home appliances, you can also shop at Habitat ReStore and receive a discount on your purchases. This not only helps you save money on home goods but also supports the important work of Dallas Area Habitat for Humanity.

Your contribution can make a real difference in the lives of low-income families in the Dallas area and start the new year off positively.

New Year 2023 Donations to Dallas Area Habitat for Humanity are a great way to support the organization's mission and help positively impact the Dallas community.

0 notes

Last Seen Blogs

taradisechic-tara

@Taradisechic

random-dnd-minis

Random dnd Mini Designs

zwei2x

I sell profane and profane accessories.

bookloversreviewer

Untitled

raregildraws

Rare Gil Hi!