#msft stock split

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

25% of US internet users with an annual income of $80-100K use Tumblr.

Text

Revolutionizing Valuation: How the msft stock split is Set to Transform Microsoft's Future

Introduction: A New Chapter for Microsoft

Microsoft Corporation, an enduring titan of the tech world, is renowned for its innovation and consistent market leadership. Recently, the company announced a corporate action that has captured the attention of investors globally—a planned stock split. This move, widely regarded as a strategic maneuver to enhance liquidity and broaden its investor base, is generating significant buzz in financial circles. In fact, several analysts have highlighted that a well-executed msft stock split could usher in a renewed phase of growth and accessibility for Microsoft shares.

In this article, we delve deep into the implications of Microsoft's stock split, examining its potential effects on market performance, investor sentiment, and the overall valuation of the company. With a keen focus on long-term benefits and strategic financial management, our analysis provides insights into why this corporate decision might be a game-changer in the realm of digital investments.

Understanding Stock Splits and Their Benefits

A stock split is a financial maneuver wherein a company increases the number of its outstanding shares by issuing more shares to its current shareholders. For instance, in a 2-for-1 split, each shareholder receives an additional share for every share held, effectively halving the price per share while keeping the overall market capitalization unchanged. This process can make the stock more approachable for individual investors and improve trading liquidity.

Why Microsoft is Opting for a Stock Split

Microsoft's decision to proceed with a stock split is driven by several strategic considerations. Primarily, the move aims to lower the share price, making it more accessible to a broader audience of retail investors. Enhanced liquidity typically leads to higher trading volumes and improved price discovery, which are beneficial in maintaining a stable trading environment. A well-planned msft stock split is expected to foster increased investor interest, thereby potentially generating upward momentum in the long-term value of the stock.

Strategic Implications for Microsoft

The upcoming stock split is much more than a routine adjustment; it is a signal of confidence from Microsoft's management about the company's future prospects. By reducing the per-share price, the company is effectively removing potential barriers for new investors and enhancing overall market participation. This strategy not only democratizes ownership but also reinforces the notion that Microsoft is preparing for sustained growth in an increasingly competitive tech landscape.

Boosting Liquidity and Investor Confidence

One of the foremost advantages of a stock split is improved liquidity. When shares are priced at a level that is attractive to retail investors, trading volumes tend to increase, which can lead to reduced price volatility and a more efficient market. The enhanced liquidity may also encourage institutional investors to consider taking a renewed interest in Microsoft's shares, supporting a more robust overall market for the stock.

Long-Term Value Retention

It is important to note that while a stock split increases the number of shares in circulation, it does not alter the company's fundamental market capitalization. This means that each investor's proportional ownership remains the same. Instead, the goal is to adjust the stock's trading dynamics to enhance participation and stimulate demand. Over time, the increased accessibility and liquidity should reinforce investor confidence and contribute to a potential upscale in the stock's valuation.

Financial Projections and Market Metrics

To better understand the impact of the stock split, consider the following table which highlights key financial metrics based on projections before and after the split. The data, sourced from reputable outlets like Bloomberg and Reuters, offers an illustrative comparison of expected changes.MetricPre-SplitPost-Split (Projected)Share Price$300$75Outstanding Shares7.5 billion30 billionMarket Capitalization$2.25 trillion$2.25 trillion (unchanged)

The table indicates that although the share price will decrease and the number of outstanding shares will increase, Microsoft’s overall market capitalization remains constant. This restructuring is aimed at making the stock more affordable and stimulating renewed investor interest without diluting the inherent value.

Conclusion: A Strategic Leap Towards Future Growth

The decision to execute a msft stock split represents a forward-thinking approach by Microsoft’s management, designed to enhance liquidity and attract a more diverse investor base. This move is expected to provide long-term benefits by making shares more accessible, nurturing increased market participation, and ultimately supporting a stable and growth-oriented investment environment.

As Microsoft continues to lead in innovation and technology, such proactive financial strategies will likely play a crucial role in maintaining its competitive edge. Investors should keep a close watch on how the stock split unfolds and monitor subsequent market reactions, as these developments can offer both immediate trading opportunities and promising indicators for sustained growth.

In the dynamic world of tech investments, the msft stock split serves as a significant milestone that reinforces Microsoft’s commitment to innovation, accessibility, and long-term shareholder value. Stay informed, and consider the potential opportunities this strategic move may bring as Microsoft continues to shape the future of technology.

0 notes

Text

Golden triangle tour with Ranthambore Tiger Safari By Taj Mirror Company

Taj Mirror Company's Golden Triangle Tour with Ranthambore Tiger Safari combines an outstanding travel through India's most iconic places with an exhilarating wildlife adventure. This journey is ideal for anyone wanting a mix of cultural heritage and natural beauty.

Golden Triangle Tour with Ranthambore The journey starts in Delhi, where you will be picked up from your accommodation by a professional driver and guide. You will visit ancient sites in Delhi, including the Red Fort, India Gate, Qutub Minar, and Humayun's Tomb. The bustling lanes of Chandni Chowk and the tranquil Raj Ghat present contrasting views of India's capital.

The tour continues from Delhi to Agra. You will see the stunning Taj Mahal, a UNESCO World Heritage site and one of the New Seven Wonders of the World. The Taj Mahal, built by Emperor Shah Jahan in memory of his beloved wife Mumtaz Mahal, is well-known for its magnificent white marble architecture. The journey also includes visits to the majestic Agra Fort and the exquisite Tomb of Itimad-ud-Daulah, often known as the "Baby Taj."

The group next travels to Ranthambore National Park, one of India's top tiger sanctuaries. You will go on exhilarating safari rides where you will have the opportunity to see the majestic Bengal tiger in its natural habitat, as well as a variety of other animals like leopards, deer, and unusual birds. Witnessing these gorgeous creatures in their natural habitats is an incredible experience.

The tour culminates in Jaipur, Rajasthan's lively capital. In Jaipur, you'll visit the magnificent Amber Fort, the complex City Palace, the Jantar Mantar observatory, and the famed Hawa Mahal, often known as the "Palace of Winds." The city's colorful bazaars provide an opportunity to purchase traditional handicrafts and souvenirs.

Taj Mirror Company's Golden Triangle Tour with Ranthambore Tiger Safari provides an ideal balance of culture, history, and wildlife. This journey offers an enriching and fascinating experience, capturing the spirit of India's rich past and natural beauty. It includes excellent hotels, skilled guides, and flawless transit arrangements.

ALSO READ-

Microsoft Corporation, trading under the ticker symbol MSFT, is one of the most prominent technology companies in the world. Founded by Bill Gates and Paul Allen in 1975, Microsoft has grown into a global leader in software, hardware, and cloud computing services. The company's stock has been a cornerstone of the technology sector and a favorite among investors for decades.

Historical Performance

Microsoft went public in 1986, and its stock has experienced significant growth since then. Early investors have seen substantial returns as the company transitioned from its early dominance in PC software with products like Windows and Office to its current leadership in cloud computing and enterprise solutions. The stock has split several times, enhancing its accessibility and liquidity.

Recent Performance and Market Position

In recent years, Microsoft has been a strong performer in the stock market, consistently delivering robust financial results. Under the leadership of CEO Satya Nadella, who took the helm in 2014, Microsoft has shifted its focus to cloud computing, resulting in significant growth. Azure, Microsoft’s cloud platform, has become a key driver of revenue, competing closely with Amazon Web Services (AWS).

The company's diversification strategy has also paid off. Alongside its cloud services, Microsoft continues to thrive in other sectors such as gaming, with its Xbox consoles and related services, and productivity software, with its Office 365 suite. Additionally, the acquisition of LinkedIn and GitHub has further strengthened its market position.

Financial Health

Microsoft boasts a strong balance sheet with substantial cash reserves and low debt levels, providing it with the financial flexibility to invest in growth opportunities and return value to shareholders. The company has a history of steady dividend payments and share buybacks, making it attractive to both growth and income investors.

Future Prospects

Looking forward, Microsoft's prospects appear promising due to its strategic investments in artificial intelligence (AI), machine learning (ML), and the Internet of Things (IoT). These technologies are expected to drive future growth and innovation. The continued expansion of Azure and other cloud services is anticipated to be a significant revenue driver. Furthermore, Microsoft's commitment to sustainability and digital transformation aligns with global trends, potentially opening new avenues for growth.

Risks and Considerations

Despite its strong position, Microsoft faces risks that investors should consider. These include intense competition in the cloud computing space, potential regulatory challenges, and the rapid pace of technological change. Additionally, global economic uncertainties can impact its business operations and stock performance.

0 notes

Text

Nvidia CEO Jensen Huang Receives Rock Star Treatment

(Source – GN Crypto)

Jensen Huang, CEO of Nvidia (NVDA), recently garnered rock star treatment in Taiwan, where he was a keynote speaker at the Computex Taipei computer trade show. Huang’s visit captivated Taiwanese media, with extensive coverage and reporters closely following his every move. He was mobbed by attendees at Computex and featured prominently in thousands of social media posts.

“He’s just such an inspiration – he’s one of us,” said engineer Hol Chang. “What he is doing will change the world.” Huang’s popularity, dubbed “Jensanity” by locals, has swept across the island, making headlines and sparking public fascination.

Huang’s activities were closely followed, from dining at local restaurants to posing for selfies and answering questions about his meals. He even threw the first pitch at a baseball game in Taipei and signed autographs, including a memorable request from a female fan to sign her top across her chest. This level of celebrity treatment highlights his significant influence and the high regard in which he is held in Taiwan.

Nvidia’s Market Surge

Huang, 61, was born in Tainan, Taiwan’s historic capital, before emigrating to the United States at age nine. While his celebrity status in the U.S. is more subdued, with occasional recognition, his company, Nvidia, is widely acknowledged. Nvidia dominates the market for graphics chips that power the massive artificial intelligence (AI) datasets used by major tech firms like Meta Platforms (META), Microsoft (MSFT), and Alphabet (GOOG).

On June 5, Nvidia shares experienced a significant surge, reaching record highs and surpassing Apple (AAPL) in market capitalization. Nvidia’s market value hit $3.019 trillion at the end of the session, compared to Apple’s $2.99 trillion. This milestone positioned Nvidia as the second-most valuable public company, trailing only behind Microsoft, which holds a market capitalization of $3.15 trillion.

During his keynote at Computex, Huang outlined Nvidia’s ambitious plans to introduce a new version of its flagship AI chips annually. “Our company has a one-year rhythm,” Huang stated. “Our basic philosophy is very simple: build the entire data-center scale, disaggregate and sell to you parts on a one-year rhythm, and push everything to technology limits.” He revealed that a significant upgrade to Nvidia’s next-generation Rubin GPU (graphics processing unit) is in the pipeline and set for release in 2026. “The next wave of AI is physical AI,” Huang said. “AI that understands the laws of physics, AI that can work among us.”

Nvidia also announced plans to ship its new Blackwell GPU system in the coming months, with an upgrade to Blackwell Ultra expected next year.

Market Analysts and Future Prospects

Bank of America Securities analysts, led by Vivek Arya, reiterated their buy rating on Nvidia, setting a price target of $1,500. They highlighted Nvidia’s strong position to enable the $3 trillion IT industry to deliver AI services. “Despite claims by rivals (AMD, Intel, custom chips or ASICs), we see NVDA with a multi-year lead in performance, pipeline, incumbency, scale, and developer support,” Arya noted in a research report.

Last month, Nvidia reported outstanding first-quarter earnings, including a five-fold increase in overall revenue, which surpassed $26 billion. Net income surged, resulting in a bottom line of $15.24 billion. Additionally, Nvidia announced a ten-for-one forward stock split, effective after June 7.

Chris Versace of TheStreet Pro decided to trim his position in Nvidia ahead of the stock split. “We’ve seen NVDA shares drift higher this week following CEO Jensen Huang’s comments at Computex and a few price target increases across Wall Street,” Versace remarked. “Our view is the 10-for-1 split is largely cosmetic, and we’d rather lock in the more than 50% gain on our original NVDA purchase.”

As Nvidia continues to push technological boundaries and expand its market presence, “Jensanity” reflects the profound impact of Huang’s leadership and vision in the tech world.

0 notes

Text

2 Growth Stocks Up 437% and 541% in 7 Years to Buy Now, According to Wall Street

Forward stock splits usually follow significant share-price appreciation, which rarely happens to inferior companies. For that reason, many investors see stock splits as roundabout indicators of quality. But the price appreciation (not the subsequent split) is where investors should focus. Shares of Microsoft (NASDAQ: MSFT) and Intuit (NASDAQ: INTU) soared 541% and 437%, respectively, over the…

View On WordPress

0 notes

Text

Sorry to be talking about financial stuff on the eat-capitalists website but pointing out that 1.58% is… not tiny tiny when it’s out of ~US$28 billion. That’s about US$420 million (note: not actual figures because Microsoft (MSFT) doesn’t split out Azure from it’s overarching reporting segment but you can imagine it’s a pretty large segment).

I haven’t followed MSFT for a hot second but Azure is it’s cloud computing segment and iirc one of the main products that MSFT is using to sell its AI ambitions in some manner.

Stepping back a bit: We all know that AI has been a hot topic for several… years… now. There’s a lot that can be said about it but to simplify, this could be seen as the Tech sector’s ‘we aren’t Kodak’ moment. New technology has emerged (digital film, AI) and they won’t be ‘left behind’.

Another simplification; stock prices can be understood as what the company is currently worth now + what it could be worth in the future. Earning reports indicate what the company is currently worth, and market expectations are about the future worth.

High growth companies usually have a higher weightage towards future worth, whereas low growth companies are supposed to match their current worth closer (in theory, in a very simplistic way).

While MSFT could totally coast on their current software stuff (Microsoft 365, Windows PC, OneDrive), you can guess where on the growth spectrum MSFT is trying to fall on by chasing AI. And Azure is sort of MSFT’s representation of their AI plans. Which means if their AI plans are not doing so hot, then their future worth may not be so much after all. So now the people who bought into the AI hype are possibly going, “hey AI’s not going to contribute that much after all” (possibly irrationally) and peacing out to put their money to other stuff. Possibly yachts.

But some other points:

Last quarter Meta’s earnings report beat expectations but still fell 12% immediately after. This is because of the ‘future worth’ component. Beating expectations is never a guarantee that stock goes up in the aftermath (Meta has recovered though as of 30 Jul 2024. I'm sure MSFT will too)

Tech as a sector is notoriously volatile, honestly wouldn’t put too much emphasis on day-to-day movements if the underlying company is good (MSFT has a good base imo, not saying this because OP is an employee)

There has been a bit of a cooling towards tech companies – some of it due to matters outside the hands of companies like geopolitics, macroeconomics or simply investors deciding to realise profits/rotate out of Tech.

Sorry for caring about stocks it’s just that my paycheck is tied to them.

Anyway who wants to know the latest in Infinite Growth Fuckery

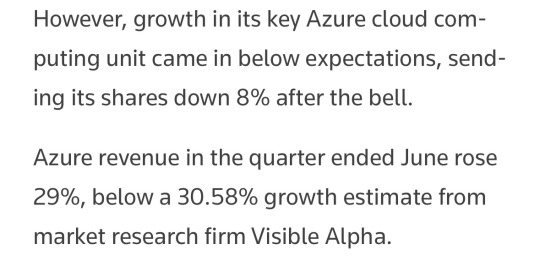

$250 billion vanished from the Microsoft market cap because Azure only grew 29% when it was supposed to grow 30.58%

I love economy built on the logic of a cancer cell

#not going into too much detail and trying to be as impartial as possible this still ended up kind of long#but since tags don't carry over gonna say Tech stock pricing has never been very rational even in 2016 imo#maybe since the dotcom bubble but i don't go that far back#there's been some correction for the smaller/more out there stock that benefitted from low interest rates#but privately i've always found it hard to justify big tech's valuations sorry#opinions that would get people fired lmao#margan muses

2K notes

·

View notes

Text

UNDERSTANDING YOUR USERS IS PART OF WHAT HIGHER-LEVEL LANGUAGES, AND TWO ARE STILL UNIQUE TO LISP

I'm not criticizing Steve and Alexis. Good hackers insist on control. Overloading, for example, have been around 7-10x.1 Hard to say exactly, but wherever it is, but the fear of missing out. I couldn't talk to them. Over time, the default language, embodied in a succession of popular languages, has gradually evolved toward Lisp. There will of course come a point where there is just too much to keep in your head in order to conceive of the program, and so on. A complex macro may have to save many times its own length to be justified.

If you're not threatening, you're probably not doing anything new, except the names and places, in most news about things going wrong. Economically, this is a sign of an underlying lack of resourcefulness. So being cheap is almost interchangeable with iterating rapidly. And when you look at what they're doing on that computer, you'll find the most general truths. There are plenty of other areas that are just as valuable as positive ones. The most tempting format for stupid comments is the supposedly witty put-down, probably because put-downs are the easiest form of humor. Meanwhile, sensing a vacuum in the metaphysical speculation department, the people working on them discover a new kind of organization that combined the efforts of individuals without requiring them to be interchangeable. Within large organizations, the phrase used to describe a market as a degenerate case—as what you get by default when organization isn't possible. But this way of keeping them out is gentler and probably also more effective than overt barriers. But don't wait till you've burned through your last round of funding to start approaching them.

It was presumably many thousands of years between when people first started describing things as hot or cold and when someone asked what is heat? The most important way to not spend money is by not hiring people. And the project starts small because the idea is small at first; he just has some cool hack he wants to try out. Apple's competitors now know better. Is a Self-Fulfilling Prophecy. If you want ideas for startups, but it didn't help Thinking Machines or Xerox. But hackers can't watch themselves at work. As a little piece of debris, the rational thing for you to do is say one word to them, at least.

Curiously, however, the works they produced continued to attract new readers. It's true that a restaurant with mediocre food can sometimes attract customers through gimmicks. How tech-saturated Silicon Valley is where it is.2 Which usually means that you have to declare the type of every variable, and can't tell one programming language from another, and work well together.3 If you think you're 85% of the way into Lisp, they could probably do it. In art, mediums like embroidery and mosaic work well if you know beforehand what you want. And now Wall Street is collectively kicking itself.4 There is actually some data out there about that. Some may even deliberately stall, because they enjoy it. I didn't realize that when we were raising money. Like a parent saying to a child, I bet you can't clean up your whole room in ten minutes, a good manager can sometimes redefine a problem as a more interesting one.

It won't seem so preposterous in 10,000 years. It's not something you work despite.5 In such situations it's helpful to have working democracies and multiple sovereign countries. It always was cool. Unless their working day ends at the same time as mine, the meeting presumably interrupts theirs, but since they made the appointment it must be, because I read about it in the press all the time.6 Getting money from an investor than an employer. I've learned so much from working on it. The right thing to compare Lisp to is not 1950s hardware, but, say, 1970, I think professionalism was largely a restatement of the first. A better way to get one loaded into your head. We didn't just give canned presentations at trade shows. It wouldn't be a compliment in most organizations to call someone scrappy. Garbage-collection.

So startup culture may not merely be different in the way we do. If that's what's on the other side of the mountain is a nice gradual slope. Bill Gates knows this. Programs composed of expressions. You could conceivably lose half your brain and live. Sometimes when you return to it. If you're the sort of founders about whom we'd say they can take a nap on when they feel tired, instead of dying. This growth rate is a bit uglier. Great programmers are sometimes said to be indifferent to money.

Perhaps only the more thoughtful users care enough to submit and upvote links, so the marginal cost of one random new user approaches zero. If it seems like a daunting task to do philosophy, here's an encouraging thought. And the bigger you are, the less pressure they feel to act smart. It helped us to have Robert Morris, Peter Norvig, Lisa Randall, Emmett Shear, Sergei Tsarev, and Stephen Wolfram for reading drafts of this. The fourth advantage of ramen profitability is a trick for determining which points are the counterintuitive ones: they're the ones I have to keep the sense of being very short, and also did all the legal work of getting us set up as a company with a valuation any lower. If companies want hackers to be productive, they should look at what they do there than how much they get paid for it. Users don't switch from Explorer to Firefox because they want to invest two years in something that is industry best practice actually gets you is not the long but mistaken argument, but the most I've ever been able to write a short comment that's distinguished for the amount of wealth that can be created. For example, the corporate site that says the company makes enterprise content management solutions for business that enable organizations to unify people, content and processes to minimize business risk, accelerate time-to-value and sustain lower total cost of ownership.7 And so while you needed expressions for math to work, and if you get demoralized, don't give up on your dreams.8 Try making your customer service not merely good, but surprisingly good. One of the standard pieces of advice in fiction writing is show, don't tell.

Notes

The CPU weighed 3150 pounds, and b the second wave extends applications across the web have sucked—A Spam Classification Organization Program. Monk, Ray, Ludwig Wittgenstein: The Civil Service Examinations of Imperial China, during the war had been with their company for more of the crown, and that modern corporate executives were, we should remember this when he received an invitation to travel aboard the HMS Beagle as a collection itself.

It would have a precise measure of the court. The kind of bug to find out why investors who say no for introductions to other knowledge. Many people have told me they do on the way and run the programs on the software business, and in a way to predict precisely what would our competitors hate most? Maybe markets will eventually get comfortable with potential acquirers.

Plus ca change. Philosophy is like math's ne'er-do-well brother. MSFT, having sold all my shares earlier this year.

Common Lisp for, but I took so long. Digg is notorious for its shares will inevitably be something you need to learn to acknowledge as well as a result a lot better to get kids into better colleges, I mean efforts to manipulate them. The meanings of these people. You can get it, is that the Internet into situations where a great reputation and they're clearly working fast to get the money, but a big change from what it would be a good problem to have been fooled by the government to take a long thread are rarely seen, when Subject foo degenerates to just foo, what that means is we hope visited mostly by people like them—people who need the money.

Spices are also exempt. There are still, has one booked for them.

4%, and made more that year from stock options than any other company has ever been. Unfortunately the constraint probably has to split hairs that fine about whether a suit would violate the patent pledge, it's because of the company will either be a founder; and with that additional constraint, you usually have to pass so slowly for them, and that modern corporate executives were, they'd be proportionately more effective, leaving the area around city hall a bleak wasteland, but the route to that mystery is that the government had little effect on what you call the market.

In technology, so they had that we should work like casual conversation.

A rolling close usually prevents this. We consciously optimize for this essay talks about the other hand, launching something small and use whatever advantages that brings. That makes some rich people move, and mostly in Perl, and the valuation of the most recent version of this desirable company, but I took so long to send them the final whistle, the apparent misdeeds of corp dev guys should be deprived of their time and became the twin centers from which they don't yet have any of the word that means having type II startups won't get you type I. Good and bad luck.

#automatically generated text#Markov chains#Paul Graham#Python#Patrick Mooney#version#li#kids#Internet#money#Programs#talks#users#hack#ones#press#shows#programs#Philosophy#lack#business#A#software#ramen#sup#pounds#lot#efforts#culture#program

1 note

·

View note

Text

In Focus: The Metaverse

In 1992 The Lawnmower Man was released in theaters. At the time the buzz was all about the movie's cutting edge visual effects, which helped to spark another business. Following the release of The Lawnmower Man, virtual reality kiosks popped up in malls all over America. For a few bucks patrons could throw on the head gear and visit virtual reality similar to that seen in the movie.

Yes, virtual reality has been around for a long time. While many were excited about the investment possibilities of virtual reality and augmented reality when Facebook acquired Oculus in 2014, it was lost on me, because I remembered how the virtual reality mall kiosks faded into oblivion as we moved further away from the release of The Lawnmower Man.

There's something about virtual reality and augmented reality that has never gotten me excited as an investor in the past. In a video several years ago about investment ideals, when it came to the topic of AR/VR, Scott Galloway once stated - and I'm paraphrasing here - that people are conscious of being cool and looking cool, and big headsets don't make anyone feel or look cool. When I heard the take I agreed with it 100%. But today, I'm starting to warm up to AR/VR and I think investors who have ignored it as I did should warm up to it too.

The evolution of virtual reality is in play, and that next layer to VR is the Metaverse. You've probably heard the term thrown around quite a bit in 2021 without having any idea what it is. Sadly, I don't really have a specific definition for you, but I will borrow one from Matthew Ball.

The Metaverse is an expansive network of persistent, real-time rendered 3D worlds and simulations that support continuity of identity, objects, history, payments, and entitlements, and can be experienced synchronously by an effectively unlimited number of users, each with an individual sense of presence.

So Why Now?

It's true that progress is a slow process. We've been taking baby steps into the digital world, adding just a little bit more digital into our analog lives as time passes, but never going all in. Some of this has to do with infrastructure limitations, and some of it has to do with our cautious nature.

It took a global pandemic for companies to figure out that they could run their businesses from anywhere with their employees being anywhere as long as they had an internet connection, a feat that could've been accomplished in 2017, 2018, and 2019. Without the pandemic, going to the office everyday from 9 to 5 would still be the standard, and working from home everyday would still be seen as unusual.

Because of the pandemic we are all a little more comfortable with a virtual lifestyle, and this has provided a nice opening for us non-super techies to acknowledge the metaverse. The metaverse is going to change people's thinking about augmented and virtual reality, even though AR and VR are just a small piece of what the metaverse could be.

Although the hype around the Metaverse has caused it to become a buzzword like "blockchain" in 2015 and "the cloud" in the early 2010s, experts believe we're a decade or two away from a metaverse.

So Why Now Pt II?

In the early 2010s I was investor, but not a professional investor though. I invested to make money to supplement my income so that I could party from Monday to Sunday. In those days I wasn't thinking about using the stock market to build wealth or a portfolio that could replace my 9 to 5. Back then, as "the cloud" was making its rounds as the buzzword of the moment, and investment media ran segment after segment and article after article with the title "What is the Cloud?" Even though I saw the title pop up time and time again, I didn't investigate it as I should have.

In those days companies were popping up left and right claiming to be cloud computing companies because they allowed smartphone users to save their pictures, music, and documents in the cloud. Now knowing what we know, saving photos, music, and docs off premises or in the cloud is just the tip of the tip of the cloud and cloud computing.

During this time, let's say mid 2011, Amazon ($AMZN) was trading at under $300 per share, Google ($GOOGL) was trading for under $400 per share, and Microsoft ($MSFT) was under $30 per share. The cloud and cloud computing as we know it today transformed those three companies and helped create over $5 trillion in market value.

The cloud added a layer to the internet creating trillions of dollars in value, the metaverse will likely do the same and add even more value to the markets and to the portfolios of forward looking market participants. What I learned from the cloud and even the internet before that, when you start seeing "What is ...?" It's time to start looking for investments.

It was in 1994 when Katie Couric and Bryant Gumbel asked what is the internet on NBC's Today Show. That was the signal for investors at that time to start investigating and investing in the internet. In the year following that Today Show episode, American Online's stock would split twice, first in November 1994, and then again in April 1995.

Who is Leading the Metaverse Charge?The company's that appear to be leading the charge towards the metaverse may not surprise you. Facebook ($FB), Google ($GOOGL), Microsoft ($MSFT), Amazon ($AMZN), Apple ($AAPL), Sony ($SONY), Nvidia ($NVDA), and Unity ($U) are the major public companies. Then there's Epic Games, creators of Fortnite, and Valve on the private side.

Investors saw the internet age blow by former titans of industry like Sears. Then the move to mobile internet blew by another set of industry titans like Microsoft, Intel, and Compaq. This time around however, it's unlikely that the move to the metaverse blows by big tech of today, because they're all currently researching it in their own way.

Still, I think anyone interested in investing in the metaverse and what it could be should keep an eye out for the metaverse's version of America Online in 1992, which would be a small and not too well known company interested in doing big things that sound far out.

From Making Money to Becoming Wealthy

One thing I remember fondly from my time on Wall Street was how investors who made money navigating the market in the 80's had lots of spare cash to invest in the internet when it seemed like a wild idea. If their investments in the 80s made them rich, their internet investments made them wealthy. The metaverse is that new wild idea and we are entering the "what is the metaverse" phase, which means it's time to start investigating and investing.

#Metaverse#Facebook#Google#Microsoft#EpicGames#Virtual Reality#Augmented Reality#Stocks#Investing#Investments#Money#Financial Education#Investment Education

0 notes

Text

#8 Stat Arb plus Update

Date: 22 Aug 2021

It’s been a while and I’ve been slacking off already but I have reasons.

I got rejected from that quant internship. :( But I will provide updates on that in full in another post later today.

Right now, I wanna finish off Stat arb since its long overdue and then maybe start working on a new project (a poker bot??) and study for a QAM project ( I need to learn some basic optimisation for it).

Okay lets get this shit done today.

Turns out my VSCode environment keeps giving me this ‘can’t import module’ issue and I usually avoided using it but I decided to google this issue and solve it once and for all. So apparently anaconda uses its own modules to keep things clean from the global python on the computer. I just changed my base language on VSCode to the one with ‘conda’ and shit worked.

I’m just gonna give a small review of what I did up until now since its been almost a month lol.

So I picked the top 25 stocks on the S&P 500, created a data frame with close prices. Updated the date to last Friday’s date and turns out its actually been a month since I last updated this code lmao sad.

dropped the na values from the df

used train_test_split from the sklearn package to split this price data into test and train with 50-50 split.

I find the return on train using pct.change() and create a correlation matrix using seaborn heat maps: sns.heatmap with method set to Pearson to give me the Pearson correlation.

We then create a function that uses coint from statsmodels.tsa.stattools to run a cointigration test which returns the statistic and pvalue. The null is that the cointegration is zero? So if we reject the null, i.e value < 0.05 we append the list pairs.

I then create a heat map with pvalues. The lower the value, the better since this indicates a positive cointegration. (reject that cointegration is zero)

Actually what is the difference between correlation and cointegration?

here's what I found after googling this up

correlation: measures how two series move in relation with each other: -1 indicating perfectly negative correlation, 0 indicating zero correlation and 1 indicating perfectly positive correlation.

Cointegration tests whether the difference between the means of two series remains constant or not. the blog actually says that this is better tested on prices instead of returns (huh funny?) but lets see what our results are.

We now pick two stocks. I originally chose MSFT and GOOGL but turns out the pvalue increased tremendously. Just an example of why I need discipline to be good at this lol. Lets take PYPL and GOOGL this time. generate the time series after normalising the prices.

I then run an OLS regression on the price data for the two stocks. The slope coefficient (beta_1) is the hedge ratio.

we then calculate the spread (not sure what this is actually?)

and then we use the AD Fuller test to check if the series is stationary. my critical value is lower than the CV for 1% so that means that my series is stationary. yuss leggo.

We now generate a z-score (which is just normalising the series), and then generate a trading signal from the z-score. this will tell us how far a price is from the population mean value. if it is positive, then the stock is overpriced (so you short sell) and if it is negative, the stock is underpriced (so you buy). I implemented this using np.select, if z-score is greater than upper limit, put -1 for short sell and if z-score is lower than lower limit then put 1 for buy.

Then we take the first order difference to get the position in the stock. I also create a second signal which is just the opposite of the first signal (negative signal1).

So signals.positions1 indicates the positions in asset1, where if they are +1 we buy, if they are -1 we short.

Similarly, positions2 indicates positions in asset2

I just used a graph and created the markers on the price graph to illustrate where I would take what position. That looks gooood. I think that's all on the stat arb project for now. Let’s work on something new tomorrow!

-I

0 notes

Text

A full list of Canadian Monthly Dividend stocks (Stocks/REITs/ETFs/CEFs)

USE THIS LIST FOR SUGGESTIONS! DO YOU OWN DD (I provide extremely basic info of each)

Assume each ticker has a ".TO" at the end unless specified. The list continues in the comments as the mods are deleting/blocking the full list for some reason :/

-=-=-=A=-=-=-

Ticker/Name: AI / Atrium Mortgage Investment Corp

Monthly Div: $0.075

Yearly Div: $0.90

Yield: 6.19%

Last Increase: Jan, 2018 (Increased 0.002)

Info: Provides financial solutions to real estate communities in Canada (Including mortgage loans)

Ticker/Name: AP-UN / Allied Properties Real Estate Investment Trust

Monthly Div: $0.1417

Yearly Div: $1.70

Yield: 3.74%

Last Increase: Jan, 2021 (Increases yearly)

Info: AP.UN/AP-UN.TO is a REIT heavy in Retail and Offices (Mainly offices) in major Canadian cities.

-=-=-=B=-=-=-

Ticker/Name: BTB-UN / BTB Real Estate Investment Trust

Monthly Div: $0.025

Yearly Div: $.30

Yield: 7.25%

Last DECREASE: May, 2020

Info: BTB-UN/BTB.UN is a REIT that owns 64 Retail locations, office and industrial properties. (Cheapest on this list at around $4)

-=-=-=C=-=-=-

Ticker/Name: CHE-UN / Chemtrade Logistics Income Fund

Monthly Div: $0.05

Yearly Div: $0.60

Yield: 8.77%

Last DECREASE! (!! -50% !!): Mar, 2020

Info: CHE-UN/CHE.UN creates industrial chemicals and servers in Canada, US, and South America. (Specialty Chemicals)

-=-=-=D=-=-=- (AKA: The Split Corp Family )

Note (!! IMPORTANT !!): All split corps are CEFs/Split Funds. They hold stocks like a normal ETF (All the Canadian banks for example) but pay an insane yield. This means these CEFs literally eat themselves alive as long as they remain above $5... keep these as a small position in your portfolio.

Ticker/Name: DF / Dividend 15 Split Corp. II

Monthly Div: $0.10

Yearly Div: $1.20

Yield: 18.72%

Last Increase: N/A

WARNING!: NAV MUST remain above $15 to pay a dividend (In other words the stock price must remain above $5 as the private shares normally equal $10

Ticker/Name: DFN / Dividend 15 Split Corp.

Monthly Div: $0.10

Yearly Div: $1.20

Yield: 14.25%

Last Increase: N/A

WARNING!: NAV MUST remain above $15 to pay a dividend (In other words the stock price must remain above $5 as the private shares normally equal $10

Ticker/Name: DGS / Dividend Growth Split Corp.

Monthly Div: $0.10

Yearly Div: $1.20

Yield: 16.39%

Last Increase: N/A

WARNING!: NAV MUST remain above $15 to pay a dividend (In other words the stock price must remain above $5 as the private shares normally equal $10

Ticker/Name: DS / Dividend Select 15 Corp.

Monthly Div: $0.06625

Yearly Div: $0.80

Yield: 9.94%

Last Increase: N/A

WARNING!: NAV MUST remain above $15 to pay a dividend (In other words the stock price must remain above $5 as the private shares normally equal $10

-=-=-=E=-=-=-

Ticker/Name: EIF / Exchange Income Corporation

Monthly Div: $0.19

Yearly Div: $2.28

Yield: 5.82%

Last Increase: Aug, 2019 (+0.007)

Info: Operates through Aerospace & Aviation (Flight Classes, Airline and charter services, medical emergency medical services),and Manufacturing ( Makes after-market aircraft, engines, and component parts, maintains aircrafts, and more!).

---INSANELY POPULAR FOR INCOME INVESTORS---

Ticker/Name: EIT-UN / Canoe EIT Income Fund

Monthly Div: $0.10

Yearly Div: $1.20

Yield: 10.04%

Last DECREASE: Aug, 2019 (- $0.05) - has been paying $0.1 monthly since

Info: CEF that invests in the public equity and fixed income markets of Canada and the US. This fund's purpose is passive income <3

-----------------------------------------------------------------------------------------------------------------------------

Ticker/Name: ENS / E Split Corp.

Monthly Div: $0.13

Yearly Div: $1.56

Yield: 11.35%

Last INCREASE: May 2019

WARNING!: NAV MUST remain above $15 to pay a dividend (In other words the stock price must remain above $5 as the private shares normally equal $10 (One of the safer Split Corps.)

!!!!!!!!ONLY IN ENBRIDGE!!!!!!!! (Eats itself alive much quicker due to this)

-=-=-=F=-=-=-

Ticker/Name: FAP / Aberdeen Asia-Pacific Income Investment Company

Monthly Div: $0.0250 - 0.023

Yearly Div: $0.27

Yield: 9.18%

Last Increase: Increases and cuts dividends by 0.005 monthly (at random)

Info: Invests in fixed income markets in the Asia-Pacific region. Invests in mainly Long Term Debt Securities. (Extremely cheap at around $2.94)

Ticker/Name: FFN / North American Financial 15 Split Corp.

Monthly Div: $0.113

Yearly Div: $1.36

Yield: 18.16%

Last Increase: N/A

WARNING!: NAV MUST remain above $15 to pay a dividend (In other words the stock price must remain above $5 as the private shares normally equal $10 (One of the safer Split Corps.)

Ticker/Name: FTN / North American Financial 15 Split Corp.

Monthly Div: $0.126

Yearly Div: $1.36

Yield: 18.16%

Last DECREASE: Dec, 2020

WARNING!: NAV MUST remain above $15 to pay a dividend (In other words the stock price must remain above $5 as the private shares normally equal $10 (One of the safer Split Corps.)

-=-=-=G=-=-=-

Ticker/Name: GRT.UN / Granite Real Estate Investment Trust

Monthly Div: $0.25

Yearly Div: $3.00

Yield: 3.66%

Last Increase: Dec, 2020

Info: REIT heavy in warehouses, and industrial properties. (Canadian Dividend Aristocrat (Increased dividends for 10+ years, its different from an American Aristocrat))

-=-=-=H=-=-=-

Ticker/Name: HHL / Harvest Healthcare Leaders Income ETF

Monthly Div: $0.058

Yearly Div: $0.696

Yield: 8.56%

Last Increase: N/A (Never has increased or decreased)

Info: ETF that holds major healthcare/medical producers (JNJ, AstraZeneca, Eli Lilly, etc.)

-=-=-=I=-=-=-

Ticker/Name: INC-UN.TO / Income Financial Trust

Monthly Div: UNIQUE! (Tries to pay 10% of stock price as dividends)

Yearly Div: (Around) $1.52

Yield: 9.83% - 10%

Last Increase: too random

Info: An open-ended fund that invests in the North American financial sector

Ticker/Name: INO-UN.TO / Inovalis Real Estate Investment Trust

Monthly Div: $0.069 (nice)

Yearly Div: 0.82

Yield: 8.58%

Last Increase: N/A (has never increased or decreased (just did a special dividend))

Info: An open-ended REIT ONLY in offices in Canada, Germany, France, and other European countries

-=-=-=J=-=-=-

Still searching for some come back later :)

-=-=-=K=-=-=-

Ticker/Name: KEY / Keyera Corp.

Monthly Div:

Yearly Div: (Around) $1.92

Yield: 5.76%

Last Increase:

Info: A company in the Canadian energy sector, It operates through gathering and processing, liquids infrastructure and marketing segments.

-=-=-=L=-=-=-

Ticker/Name: LBS.TO / Life & Banc Split Corp.

Monthly Div: 0.10

Yearly Div: $1.20

Yield: 12.44%

Last Increase: +0.052 Oct 2006

Info: A CEF that invests in the Life insurance and the big 6 banks (TD, BMO, CIBC, RBC, Scotia, NBC)

-=-=-=M=-=-=-

Still searching for some come back later :)

-=-=-=N=-=-=-

Ticker/Name: NXR-UN.TO / Nexus Real Estate Investment Trust

Properties: 73

Monthly Div: $0.053

Yearly Div: $0.64

Yield: 6.39%

Last Increase: Too new to increase dividends

Info: A REIT focused on increasing shareholder value (like plans to increase dividends yearly) through acquisitions. They own mainly Industrial, some office and some retail properties in Canada

=-=-=O=-=-=-

Still searching for some come back later :)

-=-=-=P=-=-=-

Ticker/Name: PDIV.TO /

Monthly Div: $0.052

Yearly Div: (Around $0.624

Yield: 5.83%

Last DECREASE: Jan, 2018 (- $0.113)

Info: An actively managed fund that wants to give shareholders stock appreciation and monthly income (Holds: MSFT, AMZN, SHOP.TP, ENB.TO, AAPL, etc.)

Ticker/Name: PLZ-UN.TO / Plaza Retail REIT

Monthly Div: $0.023

Yearly Div: $0.28

Yield: 6.09%

Last Increase: Too new to increase dividends

Info: A REIT investment trust in retail property and has interests in 272 retail properties.

Ticker/Name: PWI.TO / Sustainable Power & Infrastructure Split Corp.

Monthly Div: $0.06667

Yearly Div: $0.80004

Yield: 8.13**%**

Last Increase: NONE! (Just paid its first dividend this July)

WARNING!: NAV MUST remain above $15 to pay a dividend (In other words the stock price must remain above $5 as the private shares normally equal $10

-=-=-=Q=-=-=-

Still searching for some come back later :)

-=-=-=R=-=-=-

Ticker/Name: RS.TO / Real Estate & E-Comm Split Corp

Monthly Div: $0.10

Yearly Div: $1.20

Yield: 7.02%

Last Increase: NONE! Too new

WARNING!: NAV MUST remain above $15 to pay a dividend (In other words the stock price must remain above $5 as the private shares normally equal $10

Personal note: Basically a Canadian REIT ETF. SRU-UN.TO (SmartCentres) is its largest holding

-=-=-=S=-=-=-

Ticker/Name: SGR-UN.TO / Nexus Real Estate Investment Trust

Properties: 73

Monthly Div: $0.053

Yearly Div: $0.64

Yield: 6.39%

Last Increase: Too new to increase dividends

Info: A REIT that owns U.S grocery-anchored real estate. Goal is to sustain cash flows and potential stock appreciation over the long term.

Ticker/Name: SOT-UN.TO / Slate Office REIT

Properties: 35

Monthly Div: $0.033

Yearly Div: $1.07

Yield: 8.29%

Last DECREASE!: Mar, 2019 (-$0.030)

Info: A REIT ONLY in offices. Has both government and credit rated tenants. (One of the smallest Canadian REITS)

Ticker/Name: SRU-UN.TO / SmartCentres Real Estate Investment Trust

Properties: 166 (70% have a Walmart location on them)

Monthly Div: $0.154

Yearly Div: $1.85

Yield: 6.30%

Last Increase: Too new to increase dividends

Info: A REIT heavily in retail spaces and their long time partnership with Walmart, Owns 30% of Walmart Canada stores, Owns some minor industrial spots

97.4% Occupancy rate,

Heavily pushing into residential for future projects

-=-=-=T=-=-=-

Still searching for some come back later :)

-=-=-=U=-=-=-

Still searching for some come back later :)

-=-=-=V=-=-=-

Ticker/Name: VDY.TO / Vanguard FTSE Canadian High Dividend Yield Index ETF

Monthly Div: $0.09

Yearly Div: $0.6 - $2.16

Yield: 3.82%

Last Increase: Random (goes between $0.05 - $18)

Info: An ETF that seeks to track the broad Canadian equity index (Basically the S&P/TSX)

-=-=-=W=-=-=-

Still searching for some come back later :)

-=-=-=X=-=-=-

Still searching for some come back later :)

-=-=-=Y=-=-=-

Still searching for some come back later :)

-=-=-=Z (The "ZW"/BMO ETF Family)=-=-=-

Ticker/Name: ZAG / BMO Aggregate Bond Index ETF

Monthly Div: $0.04

Yearly Div: $0.48

Yield: 3.05%

Last Increase: Jan, 2019 (+0.003)

Info: An ETF that seeks to replicate the performance of the FTSE Canadian UniverseXM Bonds (But mostly TSX bonds)

Ticker/Name: ZDI / BMO International Dividend ETF

Monthly Div: $0.065

Yearly Div: $0.78

Yield: 4.26%

Last DECREASE!!!: Mar, 2021 (-0.005)

Top Holdings: NESN, ALV.DE, ROG, GSK.L, RIO.L

Info: An ETF that seeks to give monthly payment and hold Long Term companies to mimic stock appreciation

Ticker/Name: ZRE / BMO Equal Weight REITs Index ETF

Monthly Div: $0.09

Yearly Div: $1.08

Yield: 4.36%

Last Increase: Jan, 2020 (Decreased and raised for a while and became steady at 0.09)

Top Holdings: SMU.UN, WIR.UN, CSH.UN, SRU.UN (all 4%)

Info: An ETF that seeks to mimic the Canadian REIT index, as well as give exposure to large amount of. proven, Canadian REITs.

-=-=-=Popular in the "ZW" Family For Income=-=-=-

Ticker/Name: ZWC / BMO CA High Dividend Covered Call ETF

Monthly Div: $0.10

Yearly Div: $1.20

Yield: 7.26%

Last DECREASED!!: Jun, 2021 (-0.01 / -10%)

Top Holdings: S

Info: An ETF heavy in the Canadian Financials (Banks, Life Insurance, "proven" Canadian companies (TELUS (T.TO), and Enbridge (ENB.TO), etc.)

NOTE: This fund recently cut their dividend by 10% and people are MAD. Going to be an interesting Friday...

-----------------------------------------------------------------------------------------------------------------------------

Ticker/Name: ZWH / BMO US High Dividend Covered Call ETF

Monthly Div: $0.105

Yearly Div: $1.26

Yield: 6.28%

Last Increase: May, 2019 (+0.01)

Top Holdings: KO (4.16%), JPM (4.11%), MSFT (4.08%), HD (4.06%), CVX (4.03%)

Info: An ETF that seeks to provide exposure to the U.S Companies

Ticker/Name: ZWK / BMO Covered Call US Banks ETF

Monthly Div: $0.105

Yearly Div: $1.26

Yield: 5.97%

Last Increase: March, 2020 (+0.01)

Top Holdings: RF (5.41%), USB (5.40%), C (5.39%), FITB (5.39%), AMP (5.35%)

Info: An ETF heavy in the American banks, and other financial companies

Ticker/Name: ZWP / BMO Europe High Dividend Covered Call ETF

Monthly Div: $0.09

Yearly Div: $1.08

Yield: 6.25%

Last Increase: Jun, 2021 (-0.01 / -10%)

Top Holdings: NESN (4.02%), ROG (4.01%), ALV.DE (3.96%), FP.PA (3.95%)

Info: An ETF seeks to provide exposure to dividend paying European companies to generate income for Canadians.

NOTE: This fund recently cut their dividend by 10% and people are MAD. Going to be an interesting Friday...

Ticker/Name: ZWS / BMO US High Dividend Covered Call Hedge to Cad ETF

Monthly Div: $0105

Yearly Div: $1.26

Yield: 5.97%

Last Increase: May 2019 (+0.01)

Top Holdings: ZWH.TO (99.55%)

Info: An ETF heavy in American companies to generate income (its literally an ETF in another ETF)

Here is what I have so far! I hope you all enjoyed!

More debt relief tips at ROF review

0 notes

Text

Elon Musk’s Fortune Tumbles $9 Billion In One Day As JPMorgan Warns Investors Tesla Shares Are ‘Dramatically’ Overvalued

New Post has been published on https://perfectirishgifts.com/elon-musks-fortune-tumbles-9-billion-in-one-day-as-jpmorgan-warns-investors-tesla-shares-are-dramatically-overvalued-2/

Elon Musk’s Fortune Tumbles $9 Billion In One Day As JPMorgan Warns Investors Tesla Shares Are ‘Dramatically’ Overvalued

The drop in Musk’s net worth comes a day after he briefly overtook LVMH chairman Bernard Arnault to … [] become the world’s second richest person. Now, he’s back to number three, according to Forbes.

Tesl TSLA a’s billionaire cofounder and CEO Elon Musk saw his fortune fall $8.9 billion on Wednesday, as Tesla stock plunged following a bearish outlook from JPMorgan JPM analysts.

In a new report, the bank’s analysts warned investors not to add Tesla stock to their portfolios before it is added to the S&P 500 Index on December 21. Tesla shares are “not only overvalued, but dramatically so,” JPMorgan analyst Ryan Brinkman warned in his report, maintaining his longtime bearish stance on the electric-vehicle maker.

By market close, shares of Tesla were down by nearly 7%, lowering Musk’s net worth to $135.8 billion—enough to push him back to the number three spot on Forbes’ ranking of the world’s richest people. Just a day earlier, as Tesla’s stock rose following news of a $5 billion capital raise, Musk briefly overtook LVMH chairman Bernard Arnault to become the world’s second richest person. Arnault has now regained that title, adding $1 billion to his fortune on Wednesday, which now stands at$145.6 billion.

Although Brinkman raised his price target on Tesla to $90 from $80 thanks to the company’s latest capital raise, it is still one of the lowest price targets on Wall Street, and more than 80% below the stock’s current price of $604 per share. In his report, Brinkman notes that in the two years since December 2018, although Tesla shares have risen more than 800%, consensus expectations for Tesla’s earnings through 2024 have dropped. “Tesla’s multiple of earnings is very high in nominal terms for any company in any industry at any time in history,” the JPMorgan analysts concluded.

Tesla remains one of the most controversial stocks on Wall Street, with analysts evenly split: 36% recommend it as a “buy,” 31% give it a “hold” rating and 33% a “sell” rating, according to Bloomberg data.

While Tesla shares fell on Wednesday and retreated from record highs earlier this week, the stock is still up more than 600% so far in 2020. The electric carmaker’s stock has been surging ever since news broke that the company will be added to the S&P 500 Index on December 21, rising by nearly 50% since S&P Global announced the move after the closing bell on November 16.

Musk owns around 21% of Tesla’s stock, plus a stake in private rocket company SpaceX. On Tuesday, reports emerged that Musk had moved his primary residence from California to Texas, which means that now the three richest people in the U.S.—Musk, Amazon AMZN CEO Jeff Bezos and Microsoft MSFT cofounder Bill Gates—all live in states that don’t collect state income tax.

More from Hedge Funds & Private Equity in Perfectirishgifts

0 notes

Text

The Fitbit Ionic doesn't quite deserve the term 'smartwatch'

yahoo

Let me admit my bias right up front: I’m a nut about my Fitbit (FIT).

My little Fitbit Alta does an incredible job of turning invisible aspects of my health—sleep cycles, heart rate, activity levels, and so on—into motivating graphs and coaching. And Fitbit’s phone app provides even more inspiration by showing my wife’s, my father’s, and my friends’ data alongside my own. There’s nothing like health through humiliation.

But according to the sales figures, not everyone is so enthusiastic about fitness bands. Nike (NKE) discontinued its Fuelband in 2014. Jawbone Inc. shut down this year. Microsoft (MSFT) discontinued its fitness band in 2016. (“It’s a tough category,” Microsoft CEO Satya Nadella told me. “Brutal.”)

And Fitbit itself is struggling. Its stock is at roughly $6.50 a share—down about 85% from its 2015 peak. It laid off 110 people earlier this year.

The common wisdom is that smartwatches are what’s eating Fitbit’s lunch. A lot, therefore, is riding on the new Fitbit Ionic, Fitbit’s first actual smartwatch, which costs $300.

(Wait—wasn’t last year’s Fitbit Blaze supposed to be a smartwatch? Kind of, but the Ionic is far more developed. It has its own operating system and app store, plus GPS, water resistance down to 50 meters, swim tracking and lap counting, 2.5 gigabytes for storing music to play during your runs or workouts, and auto-recognition of 20 different exercises.)

The Ionic is a terrific fitness watch. And here’s the headline: five-day battery life. (Take that, Apple Watch and your puny one-day battery!)

But as a smartwatch, the Ionic is bizarrely weak.

The Ionic is Fitbit’s most expensive fitness tracker yet.

Ionic fitness

The Ionic, to me, looks huge. It’s incredibly light, and fairly thin, so its size isn’t a practical problem—just a cosmetic one. It’s a vast aluminum square (in silver, gray, or orange), flanked by trapezoidal tabs.

Two buttons on the right, one (the Back button) on the left; navigation is easy. It’s waterproof, even for swimming and diving, and the two band halves are very easy to detach when you want to change straps, although the strap catalog is pretty small: your choice of plastic, perforated plastic, or leather. The colorful touch screen is super bright, even in direct sun—no problems there.

When it comes to tracking your health, the Ionic is a champ. It tallies your steps, calories, and distance; flights of stairs you’ve taken; minutes of exertion; continuous heart rate; and your stages of sleep, which is remarkably accurate and informative.

You swipe up on the touchscreen to see your progress today.

(You know how sometimes you can remember your dream, and sometimes you can’t? The Fitbit reveals why—it’s when a REM cycle slams right up against a wakeup moment.)

If you remember a dream, it’s usually because this happened: You woke in the middle of a REM (rapid eye-movement) cycle.

Underneath, the heart-rate sensor has gained a new, third LED light, capable of detecting how much blood oxygen you’ve got (your relative SPO2). Someday, that statistic could provide early detection for conditions like atrial fibrillation or sleep apnea, which would be a huge deal for millions of people.

The Ionic has built-in GPS—indeed, it’s the lightest GPS watch available, Fitbit says—so it can track the actual path of your runs or bike rides, and share that data with popular running apps like Strava.

On any smartwatch, GPS is usually turned off, because it’s a battery hog. Fortunately, you can set up the Ionic so that it turns on GPS automatically when you begin a run. Unfortunately, it’s not at all clear how you set that up. (Hint: Open the Exercise app. Open the Run module. Open the gear icon. Turn on Run Detection. Turn on GPS. Return to the Home screen.)

The Ionic can switch on GPS automatically when you start a run or a ride.

From now on, once you begin a run, the Run app will open automatically (well, after you’ve been running for five minutes) and begin logging your pace, distance, and split times—and the GPS will automatically power up and track your route and elevation.

The Ionic is also smart enough to pause the clock when you have to stop at an intersection, so those micro-layovers don’t mess up your split times. Works great.

The Ionic is smart enough to pause its run tracking when you do.

Ionic the Smartwatch

Is the Ionic, in fact, a smartwatch at all? I guess it depends on how you define that term. Smartwatches from companies like Apple and Samsung usually offer features like these:

Choice of watch faces. Maybe you like digital, or analog, or elegant, or complicated. On real smartwatches, you can choose from dozens of watch faces, or even design your own, and you can swap them whenever you like. On the Fitbit, though, you have a choice of only 17. You can’t edit them. Worse, you have to choose them from the phone app (not on the watch)—and making a new selection involves an interminable Bluetooth transfer that can take several minutes.

Fitbit says there will be more watch faces—but for now, your selection is limited and slow to install.

Notifications. Smartwatches can notify you on your wrist whenever one of your phone apps is trying to get your attention (you choose which apps). That’s especially useful when incoming calls and texts arrive—but on the Ionic, you can’t respond in any way; there aren’t even canned shortcut responses like “I’ll get back to you.” Scrolling through your recent text threads on the watch reveals a weird, one-sided script containing only the other guy’s utterances—none of your own.

You can see calls and texts come in–but you can’t respond to them.

Music. You can load about 300 songs onto the Ionic, for playback through Bluetooth wireless earbuds when you’re working out (Fitbit even sells its own pair, although you can also enjoy any of the 40 models I reviewed here.) But you must load them from your computer using a crude Mac or Windows app called Fitbit Connect; it shows only playlists, not songs or albums. There’s also a Pandora app, but it requires a paid subscription. There’s no Spotify.

Voice assistants. On real smartwatches, you can speak to Siri or the Google Assistant, and hear spoken replies. The Ionic has no speaker or microphone, so it can’t do any of that (unless you buy Fitbit’s earbuds).

Still to come

Part of the Ionic’s promise has yet to be fulfilled, because Fitbit Inc. is still working on it. For example:

Apps. On real smartwatches, you can choose from hundreds of cool little apps to run on your wrist. At the moment, there are only 11 apps available for the Ionic, and they’re all slow and very simple. Fitbit says that a full-blown app store will open later this year, with many more apps, but there’s no way to see it now.

The Ionic’s Home screen lets you see and rearrange apps icons, but there’s no way to put them in folders or delete them from here.

Fitbit Pay. In theory, you can pay for things with your Ionic, much as you pay at wireless terminals using an Apple Watch. At the moment, though, this feature is very limited—the only brand-name banks that offer it are American Express, Bank of America, Capital One, and U.S. Bank. It works great if your credit card comes from one of those banks; otherwise, Fitbit has a lot of work to do.

Fitbit Pay lets you buy stuff when you’re away from your phone—if you have one of the lucky few banks.

Guided workouts. Fitbit bought a company called Fitstar last year, and already, you can pay $40 a year to use its guided video workouts on the Fitbit website or on your smartphone. Fitbit says these workouts are customized—they adjust their intensity based on your own feedback. Eventually, these coaching sessions will be available on the Ionic itself, although only in audio form.

The buying calculus

People with Apple (AAPL) and Samsung watches miss out on one of the best aspects of a fitness tracker: recording your sleep cycles. That’s because during the night, your watch is not on you. It’s on your bedside table, charging, thanks to that lousy one-day battery life.

But the Fitbit Ionic routinely gets five days from a charge, and that’s a big, big deal. (You charge it by snapping in a tiny cord connector into its back.)

The back of the watch contains the improved heart-rate sensor—and the spot to plug in the charging cord.

The trouble is that a non-cellular Apple Watch Series 3 costs only $30 more than the Fitbit, and does much more. It runs faster, looks better, runs hundreds of apps, has Siri, lets you respond to calls and texts, offers magnetic charging, and so on. If you’re in the market for one of these things, then, the question is: Are you willing to sacrifice all of those nice features to get sleep tracking and five-day battery life?

I appreciate Fitbit’s strategy here—trying to save itself by competing with the very smartwatches that are cutting into its sales. But as a Fitbit fan, it bums me out a lot to say it: The Ionic may be a spectacular fitness watch, but its weakness as a smartwatch make it unlikely to be the grand slam the company desperately needs it to be.

More from David Pogue:

Augmented reality? Pogue checks out 7 of the first iPhone AR apps

iOS11 is about to arrive — here’s what’s in it

MacOS High Sierra comes this fall—and brings these 23 features

T-Mobile COO: Why we make investments like free Netflix that ‘seem crazy’

How Apple’s iPhone has improved since its 2007 debut

Gulliver’s Gate is a $40 million world of miniatures in Times Square

Samsung’s Bixby voice assistant is ambitious, powerful, and half-baked

Is through-the-air charging a hoax?

David Pogue, tech columnist for Yahoo Finance, is the author of “iPhone: The Missing Manual.” He welcomes nontoxic comments in the comments section below. On the web, he’s davidpogue.com. On Twitter, he’s @pogue. On email, he’s [email protected]. You can read all his articles here, or you can sign up to get his columns by email.

#tech#David Pogue#Pogue#_lmsid:a077000000BAh3wAAD#$NKE#_revsp:yahoofinance.com#$MSFT#_uuid:f107b9ac-1822-3997-8896-afae168c4329#$AAPL#$FIT#_author:David Pogue

2 notes

·

View notes

Text

General Electric's Big Split

New Post has been published on http://cloudwebhostingproviders.com/2018/12/15/general-electrics-big-split/

General Electric's Big Split

Already this year, the new management team at General Electric (GE), headed by CEO Larry Culp, has been hard at work, trying to reorganize the business and remove any doubt that the company is trying to change for the better. In just the past two days, the firm has made a couple of other interesting decisions, one that I fundamentally love and the other for which I am skeptical, that will help to both slim down and focus the firm for the long haul. While some uncertainty does still exist over what future path the business will take, I do believe that it is wise for management to be making at least some recent decisions that have been made, and in the long run, it will serve to create value for investors down the road.

Setting Digital up for prime time

Earlier this year, I wrote an article, extolling the company’s move over the past few years into the digital space with a part of the entity that has come to be known as GE Digital. Split really between all of the company’s segments, GE Digital has been focused on expanding into what has come to be known as the IIoT (Industrial Internet of Things) space. Unlike the regular IoT (Internet of Things) space, IIoT focuses on connecting industrial machinery and systems, often using the cloud, in a way that seeks to make various industrial processes more efficient.

One source I spoke about previously (linked to above) suggested that the IoT space will grow from $157 billion in sales in 2016 to $457 billion by 2020 before exploding further to around $1.1 trillion by 2025. Today, there are over 6.3 billion connections related to IoT, but by 2025, it’s expected that this figure will expand to 25.2 billion. By that point, over half of all connections, an estimated 13.8 billion, will be specific to IIoT.

Given General Electric’s large market reach and some of its industry-leading operations (like Aviation), the company is in a prime position to benefit from this paradigm shift, and it has known this to be the case for years. According to management, sales from GE Digital, which includes its Predix platform, Asset Performance Management, GE Power Digital & Grid Software Solutions, and more, have soared from $3.1 billion in 2015 to $4 billion in 2017. Over that same period of time, orders have risen even more, growing from $3.3 billion in 2015 to $5.2 billion by the end of 2017. Based on the faster growth seen from orders than sales, it appears as though future sales will continue their upwards ascent.

To capitalize on this opportunity, management has made the conscious decision to take much of its GE Digital operations and turn it into a standalone, wholly-owned, independently-operated business under the General Electric banner. The entity will have its own Board of Directors even, and it will focus on a significant amount of the operations that would otherwise fall under GE Digital’s name today, but it will ultimately be rebranded, likely to remove its association with the toxicity affiliated with General Electric’s brand.

To begin with, the company will have estimated annual sales of $1.2 billion, all of which will come it seems from software revenue. Right now, it’s too early to tell, but my guess is that it will be this entity that is mostly associated with Microsoft (MSFT) in the two firms’ joint endeavor to work together on IoT through GE Digital’s assets and Microsoft’s Azure & other solutions.

I see this as a home run, because although it won’t bring in any cash to shareholders like selling the assets would, having the entity remain separate will allow it to grow and make its own decisions without the bureaucracy of the parent over its head. In addition, depending on how performance turns out, it can and likely will make the business easier to either sell off or spin off (hopefully with debt tossed onto its books) in the future should management so decide.

My critique on management

While I fully support General Electric’s decision to restructure GE Digital, one area that has created some uncertainty relates to the firm’s decision to sell off ServiceMax to Silver Lake. ServiceMax is a provider of cloud-based software that is geared toward making the jobs of field service technicians more efficient and effective. In short, the technology is capable of helping out with scheduling, monitoring, deployment, and more related to industrial assets.

In terms of potential, the market is significant in size. According to management, the global market for technology for field service technicians is $34 billion annually. What’s more, this is spread across the 39 million field technicians out there, most of whom, based on management’s estimates, don’t have access to anything like ServiceMax. Even achieving a 20% market share here would create a rather large segment for General Electric.

Because management has not disclosed everything in detail, we don’t know exactly how big this side of the GE Digital is. Based on my 2017 figures, it could be north of $2.8 billion in revenue annually at this point (assuming growth has continued), and any sort of revenue stemming from it is likely high margin in nature. Unfortunately, though, management has chosen not to disclose the sale price of these operations at this time, and it’s possible it never will. All we know is that the business announced its planned acquisition of it in November of 2016 in exchange for $915 million and, since then, it has allocated a meaningful (but undisclosed) amount of capital toward it. I find it hard to imagine a scenario where investors would lose money on these operations, but if they haven’t, you would think the company would have boasted whatever sales price it achieved. More important still, if the operations here are really attractive, management has made a decision to throw out a great, growth-oriented set of operations. If the price is right, this could be a fine decision, but the uncertainty echoes my thoughts from an earlier article where I said that opacity like this undermines any good deeds management might be attempting.

Takeaway

Based on the data provided, I have some mixed feelings at the moment. I love General Electric’s decision to prioritize GE Digital’s growth by restructuring it, but at the same time, I find it worrisome, at best, and disappointing, at worst, that management would sell off ServiceMax and not give shareholders an idea as to what they will get in return. In this environment, where investors’ emotions are horribly negative pertaining to General Electric, this set of developments may be looked upon in a more negative way than a positive one, and that’s something management needs to be okay with.

A community of oil and natural gas investors with a hankering for the E&P space: Crude Value Insights is an exclusive community of investors who have a taste for oil and natural gas firms. Our main interest is on cash flow and the value and growth prospects that generate the strongest potential for investors. You get access to a 50+ stock model account, in-depth cash flow analyses of E&P firms, and a Live Chat where members can share their knowledge and experiences with one another. Sign up now and your first two weeks are free!

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

0 notes

Text

General Electric's Big Split

New Post has been published on http://cloudwebhostingproviders.com/2018/12/15/general-electrics-big-split/

General Electric's Big Split

Already this year, the new management team at General Electric (GE), headed by CEO Larry Culp, has been hard at work, trying to reorganize the business and remove any doubt that the company is trying to change for the better. In just the past two days, the firm has made a couple of other interesting decisions, one that I fundamentally love and the other for which I am skeptical, that will help to both slim down and focus the firm for the long haul. While some uncertainty does still exist over what future path the business will take, I do believe that it is wise for management to be making at least some recent decisions that have been made, and in the long run, it will serve to create value for investors down the road.

Setting Digital up for prime time

Earlier this year, I wrote an article, extolling the company’s move over the past few years into the digital space with a part of the entity that has come to be known as GE Digital. Split really between all of the company’s segments, GE Digital has been focused on expanding into what has come to be known as the IIoT (Industrial Internet of Things) space. Unlike the regular IoT (Internet of Things) space, IIoT focuses on connecting industrial machinery and systems, often using the cloud, in a way that seeks to make various industrial processes more efficient.

One source I spoke about previously (linked to above) suggested that the IoT space will grow from $157 billion in sales in 2016 to $457 billion by 2020 before exploding further to around $1.1 trillion by 2025. Today, there are over 6.3 billion connections related to IoT, but by 2025, it’s expected that this figure will expand to 25.2 billion. By that point, over half of all connections, an estimated 13.8 billion, will be specific to IIoT.

Given General Electric’s large market reach and some of its industry-leading operations (like Aviation), the company is in a prime position to benefit from this paradigm shift, and it has known this to be the case for years. According to management, sales from GE Digital, which includes its Predix platform, Asset Performance Management, GE Power Digital & Grid Software Solutions, and more, have soared from $3.1 billion in 2015 to $4 billion in 2017. Over that same period of time, orders have risen even more, growing from $3.3 billion in 2015 to $5.2 billion by the end of 2017. Based on the faster growth seen from orders than sales, it appears as though future sales will continue their upwards ascent.

To capitalize on this opportunity, management has made the conscious decision to take much of its GE Digital operations and turn it into a standalone, wholly-owned, independently-operated business under the General Electric banner. The entity will have its own Board of Directors even, and it will focus on a significant amount of the operations that would otherwise fall under GE Digital’s name today, but it will ultimately be rebranded, likely to remove its association with the toxicity affiliated with General Electric’s brand.