#AccountingBasics

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr was attacked by a cross-site scripting worm deployed by the Internet troll group GNAA on Dec 3, 2012.

Text

Why is financial statement preparation so important?

It’s the process of organizing a company’s financial data into structured reports, including the balance sheet, income statement, and cash flow statement. These documents show your profits, losses, assets, and expenses over a specific period.

Why It Matters

Informed Decisions Well-prepared financial statements give business owners insights into spending, savings, and profitability. This helps in making smart, data-driven decisions.

Legal and Tax Compliance Accurate financial records ensure you meet government regulations and file taxes correctly, reducing the risk of fines or audits.

Attracting Investors and Loans Clear financials help build trust with banks and investors. They’re often a requirement when applying for funding or business partnerships.

Business Planning and Growth Financial statements reveal trends and performance, making it easier to plan for the future and set realistic goals.

Financial Statement Preparation isn’t just about staying organized; it’s about staying in control. Whether you’re a startup or an established business, proper financial reporting is the foundation for stability and growth.

0 notes

Text

Deferred Revenue vs. Accrued Revenue: Key Accounting Differences

Deferred income and accrued income are two key accounting concepts that determine how businesses report their earnings. While deferred income is paid before products or services are consumed, accumulated income is money generated but not yet received. Accurate financial reporting, accounting standard compliance, and effective cash flow management all rely on understanding of these concepts. This ensures that businesses comply with the law, maintain transparency, and avoid tax issues.

What is accrued revenue?

Accrued revenue is income a company generates but has not yet been paid for. Usually, accrued income arises when goods or services are given or completed before payment is received. Accrued income appears on the balance sheet as an asset—more accurately as a receivable—indicating that the company is entitled to payment for given goods or services. As soon as the company is paid, the realized income is cash; its financial records are updated suitably.

Examples of Accrued Revenue

Professional Services – In December a consulting company offers advise services; in January it bills the customer.

Interest Income – A bank earns interest on a loan but does not receive payment until the next quarter.

Utility Companies – Before billing, electricity companies accrue income then bill consumers after use.

What is deferred revenue?

Deferred revenue, often known as unearned income, is money received by a company for goods or services not yet delivered or completed. Paying a firm in advance causes the money to display under deferred income under liabilities on the balance sheet. This shows how dedicated the business is to offer future goods or services. As the company satisfies its supply-chain promise, the deferred money is gradually dropped and shown on the income statement as actual revenue.

Examples of Deferred Revenue

Subscription Services – Although an annual membership price is paid upfront, a magazine publisher delivers the publications over a period of time.

Advance Payments for Goods – Before ever delivering the finished item, a manufacturing business gets an order deposit.

Software Licenses – A software firm sells a one-year license but recognizes revenue incrementally over the contract duration.

Difference between Deferred Revenue and Accrued Revenue

Feature

Deferred Revenue

Accrued Revenue

Definition

Revenue received before delivering goods/services

Revenue earned but not yet received

Accounting Treatment

Recorded as a liability initially

Recorded as an asset under accounts receivable

Impact on Financial Statements

Increases liabilities until earned

Increases assets until payment is collected

Examples

Subscription fees, advance payments, prepaid rent

Consulting services, interest income, postpaid utilities

Recognition Timing

Recognized over time as goods/services are provided

Recognized when earned, even if payment is pending

Why Understanding These Concepts is Important?

Maintaining financial accuracy, compliance, and general corporate health depends on a grasp of these ideas. Here's the rationale:

Accurate Financial Reporting – Proper recognition of Deferred Revenue and Accrued Revenue ensures that financial statements reflect a company’s actual financial position.

Compliance with Accounting Standards – Using IFRS and GAAP's revenue recognition guidelines helps you avoid legal and regulatory problems.

Effective Cash Flow Management – Differentiating between cash received and revenue earned helps businesses manage their finances efficiently.

Investor and Stakeholder Confidence – Transparent financial statements increase investor trust and provide a clearer picture of business health.

Tax Implications – Correct categorization might result in tax fines or missed deductions as taxable income depends on recognized income.

Challenges in Managing Deferred and Accrued Revenue

Despite their significance, companies can struggle to manage these revenue sources:

Complexity in Tracking – Big companies with several sources of income might find it difficult to precisely track postponed and accumulated income.

Accounting Software Limitations - Not all program solutions effectively separate and automate income recognition.

Regulatory Changes – Standard changes in financial reporting criteria, including IFRS 15, need for constant adaption to follow rules.

Audit and Compliance Risks – Inaccurate identification might lead to financial misstatements, therefore influencing audits and compliance evaluations.

The Role of Accounting Software in Revenue Recognition

Modern accounting systems automate journal entries, financial statement generation, and compliance monitoring to facilitate the management of deferred income and accumulated revenue. Advanced solutions guarantee that income recognition aligns with contract criteria and delivery timelines by interacting with client invoicing systems.

Questions to understand your ability

What’s the deal with accrued revenue?

a) You get paid before doing the work. b) You earn it, but you haven’t seen a penny yet. c) You make money only after delivering the goods. d) It’s basically an expense, not revenue.

Answer: b) You earn it, but you haven’t seen a penny yet. Why? Because accrued revenue means you’ve done the work or delivered the product, but the money’s still on its way. Simple, right?

When you’ve got deferred revenue, where does it show up on the balance sheet?

a) As cash sitting in your pocket. b) As a liability because you owe the goods/services. c) Under "prepaid expenses" as a future expense. d) Straight-up as a revenue gain.

Answer: b) As a liability because you owe the goods/services. Why? You’ve already taken the money, but you still have to deliver. It’s a liability until you pull through with the product or service.

Which of the following screams “accrued revenue” in action?

a) You’re paid upfront for a one-year magazine subscription. b) You get a down payment for a custom product. c) The bank earns interest but hasn’t seen the money yet. d) You sell goods before the customer hands over cash.

Answer: c) The bank earns interest but hasn’t seen the money yet. Why? Accrued revenue is earned but not yet paid. Interest income grows over time, but the cash won’t arrive until later.

When dealing with deferred revenue, how does it mess with your financial statements?

a) It boosts your assets until the cash hits. b) It raises your liabilities until the service is provided. c) It increases your equity immediately. d) It slashes the cost of goods sold.

Answer: b) It raises your liabilities until the service is provided. Why? Though it resides in the liabilities part of your balance sheet until you provide the products or services, you already have the cash. It then starts to generate income.

Why should you even care about deferred and accrued revenue?

a) To help you with your tax returns. b) To manage cash flow and keep financials in check. c) To follow marketing trends. d) To lower costs on your balance sheet.

Answer: b) To manage cash flow and keep financials in check. Why? Understanding the variations between these two income sources guarantees accurate financial statements. It also helps with cash flow management and keeps you out of tax hotbeds.

Conclusion

In financial accounting, both deferred and accrued revenue are somewhat important as they affect corporate decisions, taxes, and financial statements. Accrued Revenue accounts for earnings still to be earned; Deferred Revenue describes pre-earned payments. Good control of this income guarantees correct financial reporting, regulatory compliance, and efficient cash flow management. Using accounting software allows companies to simplify income recognition procedures, therefore lowering mistakes and improving financial openness.

#AccountingBasics#AccruedRevenue#DeferredRevenue#FinancialStatements#RevenueRecognition#AccountingPrinciples

0 notes

Text

📊 Kickstart Your Accounting Journey with Tally Prime for Beginners

New to accounting? Tally Prime Basics course is your perfect starting point! Learn transaction recording, account management, and more with ease.

🌟 Why Choose Tally Prime?

Beginner-friendly modules.

Hands-on learning experience.

Certification to boost your career.

Start your journey in accounting with TallyPrime Basics course today!

0 notes

Text

Understanding the Difference between Bookkeeping and Accounting

For companies of all sizes managing financial data is an important job. Although accounting and bookkeeping are often referred to as in conjunction, they are two distinct processes with different goals. Knowing the distinction between the two is a good way to assist business owners to ensure the financial stability of their company. Let’s look at the main distinctions and the ways in which they are essential to the business process. How do you define bookkeeping? Bookkeeping is a systematic method of recording the financial transactions that occur on a daily basis. The main purpose of bookkeeping is keeping an exact record of all financial transactions. This serves as a basis for subsequent financial analysis and reports. Bookkeeping-related tasks can includes: 1. Recording purchases and sales 2. Invoices and receipts are managed 3. Reconciling bank statements 4. Indicating income and expenses 5 Maintaining journals and ledgers

Bookkeeping is a way to ensure that the firm’s financial information is properly updated and well-organized. Bookkeepers play an essential part in the process of financial reporting in ensuring that every transaction is correctly documented and categorize. What is accounting? Accounting draws on the information that bookkeeping provides to analyze interpret, summarize, and present financial data. The main goal of accounting is to offer insight into the financial health of a business and help in making strategic decisions. The most important responsibilities in accounting are: Making financial statements including balance sheets and income statements

1. Conducting financial analysis and forecasting

2. Ensure compliance with the tax regulations

3. Advice on financial strategies

4. Managing budgets

Accounting transforms financial information into meaningful reports that stakeholders and business owners can utilize to make educated decisions. Key Differences Between Bookkeeping and Accounting Accounting and bookkeeping are inextricably linked but the distinctions between them depend on their responsibilities and the focus they have: Purpose:

Skillset:

1. Attention to detail is required in bookkeeping and the ability to record transactions. 2. Accounting requires analytical skills as well as a knowledge of the financial concepts.

Outputs:

1. Bookkeeping creates ledgers and the records of transactions. 2. Accounting generates financial statements as well as forecasts and strategic recommendations.

Decision-Making:

1. Bookkeeping is the source of information to make a decision. 2. Accounting aids businesses in making the right decisions based upon that information.

The Importance of Both Roles Accounting and bookkeeping are vital to the efficient functioning of a business’s finances. A well-organized bookkeeping system assures that the company’s financial information is accurate and accounting gives the tools necessary to analyze those data and prepare to plan for the coming years. Inattention to either of these functions could result in financial mistakes and legal problems. For example, BMAS Accountants understands the importance of precise bookkeeping and accurate accounting. Their team makes sure that companies have access to well-organized financial data and skilled guidance in achieving their financial objectives. How to Decide What Your Business Needs The particular requirements of your company will determine if you need bookkeeping, accounting or both. In general, small companies begin with bookkeeping in order to keep records of transactions that occur daily. As businesses grow and the complexity of financial transactions increases the need to have accounting support becomes evident. BMAS Accountants offers a comprehensive array of services that can help companies at all stages. From keeping precise financial records to offering accurate financial analysis BMAS Accountants ensures that businesses have the right tools to make educated choices. Final Thoughts While accounting and bookkeeping have different functions however, both are integral to the financial success of any business. Understanding the different roles they play can assist business owners in managing their finances more efficiently and plan for future growth. No matter if you’re just beginning your journey or operating an established business having a thorough knowledge of your financial information is vital. By working with seasoned professionals such as BMAS Accountants, you can make sure that your company is in a sound financial position and is prepared for the future issues.

#BookkeepingVsAccounting#FinancialManagement#SmallBusinessFinance#UnderstandingBookkeeping#AccountingBasics#FinancialHealth#BusinessSuccess#BMASAccountants#AccurateBookkeeping#StrategicAccounting

0 notes

Text

#Sriina#books#online bookstore#BasicAccounting#AccountingTips#FinancialLiteracy#MoneyManagement#AccountingBasics#LearnAccounting#FinanceEducation#SmallBusinessFinance#Budgeting101

1 note

·

View note

Text

youtube

#Bookkeeping#SmallBusinessTips#Entrepreneurship#BusinessFinance#WealthBuilding#AccountingBasics#FinancialSuccess#MoneyManagement#CashFlow#SmallBusinessGrowth#BusinessStrategy#TaxPlanning#FinancialLiteracy#ProfitPlanning#SmallBusinessOwner#EntrepreneurLife#BudgetingTips#BusinessGoals#StartupTips#MoneyMatters#youtube#Youtube

0 notes

Text

#ShortCourses#OfficeAdministration#CustomerServiceSkills#AccountingBasics#IncomeTaxTraining#ClientServicesExcellence#ProfessionalDevelopment#SkillBuilding#LifelongLearning#ShortCourseBenefits#InvestInYourself#FutureReady

0 notes

Text

Overhead Explained: Simple Calculation for Business Success!

We break down overhead costs: insurance, office expenses, CRM, and more! We calculate total overhead, multiplying by 10% (0.10) to arrive at the final overhead figure. #OverheadCosts #BusinessFinance #AccountingBasics #SmallBusinessTips #FinancialManagement #BusinessExplained #ProfitMargin #CostAnalysis #BusinessStrategy #Accounting101 from TENACITY ACADEMY (Cleaning Business Channel )…

#cleaning#cleaningbusiness#cleaningbusinessmentor#cleaningbusinesstip#cleaningindustry#cleaningservice#service#tenacityclean

0 notes

Link

0 notes

Text

Why is an invoice number so important?

In any business, keeping track of payments and records is essential. One simple but powerful tool that helps with this is the invoice number. While it may seem like a small detail, it plays a big role in staying organized and keeping communication clear.

What Is an Invoice Number?

An invoice number is a unique code given to each invoice sent to a client. It helps businesses and customers track, sort, and manage payments easily.

Why Is It Important?

Easy Tracking: A unique invoice number makes it easy to find and follow up on specific invoices, improving cash flow management. Prevents Duplicate Payments: It avoids mix-ups and ensures that no invoice is paid more than once. Improves Communication: If there’s a payment issue, referring to the invoice number helps both parties quickly identify the correct invoice. Helps with Legal and Tax Records: Tax authorities require clear records. Invoice numbers help businesses stay organized and ready for audits.

An invoice number might look small, but it’s a key part of smooth business operations. It keeps things clear, prevents mistakes, and builds trust with clients.

0 notes

Text

Ledger Posting in Bookkeeping: A Step-by-Step Guide

In the accounting process, ledger posting—the process of moving entries entered into a journal to individual ledger accounts—is absolutely vital. Officially recording financial transactions, a ledger groups them into certain accounts including assets, obligations, income, and spending. This system guarantees correct financial reporting by helping to track and arrange all financial interactions. Important information like the transaction date, the amount, and the pertinent account names is found in every ledger entry. Organization of transactions in this manner guarantees effective accounting, mistake detection, and the generation of trial balances for financial reporting by use of ledger posting.

What is Ledger Posting?

Ledge is a term that means ‘shelf’. The term ‘ledger’ is derived from the word ‘ledge.’. A ledger is the official record of significant transactions that occur.

An individual asset, person, revenue, or expense is represented by each ledger. Entering all the transactions from the journal to the ledger is known as ledger posting. Examples include all transactions involving banks, cash, buildings, land, salaries, and inventory.

Sorting individual transactions into distinct personal accounts is a key function of a ledger. Transactions of comparable topic matter and character into personal groupings are made simple by ledgers. Accounting may be completed efficiently and successfully with the help of the ledger posting system.

Important Characteristics of Ledger

A ledger account has a few salient features among others:

A ledger comprises all the accounts—that of sales, purchases, purchases, and so on. Thus, one may consider a ledger as a register or a book including all the accounts. Accounts are opened in the ledger at the beginning of a company or during a year.

The first notable feature of the ledger is the sequence of monetary exchange. Ledger accounts mostly aim to classify all the exchanges into the accounts. Every trade is classified in the several ledger accounts found in a ledger.

One of the key traits of a ledger is data optimizing. Mistakes are corrected via mix-up tracking. In a perfect world, for instance, if a purchase is inflated at that moment, the bookstore must follow the slip-up and inspect all the purchasing records.

One major feature of ledger accounting is the ability to hold relevant data in one location.

The general ledger, which includes all of the accounts for budgetary items, is used by small associations. The large association, on the other hand, uses the subsidiary ledger as a memoranda ledger, which includes the accounts of the clients and creditors. Similarly, the total accounts for each of these items make up the general ledger. These are a few of a ledger's attributes.

The trial balance is subtracted from the general ledger preparation closing balance. In this sense, the ledger is crucial to the preparation of fiscal reports. Trial balance extraction is the initial step in both ledger and journal entry for budget report layouts.

Columns in a Ledger

From the books of initial entities or journals, transactions show up into the ledger account. Every transaction always moves from a journal to a ledger. There exist the following columns in a ledger:

Particulars: Specifically, the name of the correct account holder is shown. Every transaction is likewise displayed or mirrored here.

Date: The date when the transaction took place is depicted in this date column.

Amount: The amount associated with each entry is shown in this column.

Journal Folio (JF): This column is used to denote the page numbers once the journal entry has passed

Step-by-Step Guide to Ledger Posting

Step 1: Record Transactions in the Journal

Start here. The Journal is where every transaction lives first—raw and unfiltered. Use the double-entry system: every transaction hit two accounts (one debit, one credit).

Example: On 15th March, TechGadgets buys office chairs for ₹20,000 cash.

Debit: Furniture Account ₹20,000 (asset increases).

Credit: Cash Account ₹20,000 (cash decreases).

Journal Entry:

Date

Particulars

Debit (₹)

Credit (₹)

JF

2024-03-15

Furniture A/c Dr.

20,000

–

45

To Cash A/c

–

20,000

45

Note the Journal Folio (JF) column—it tracks the journal page number (e.g., page 45).

Step 2: Post to the Ledger – Column by Column

Transfer journal entries to the Ledger using these columns:

Date Column

What: The exact date of the transaction.

How: Copy it directly from the journal.

Example: 2024-03-15 from the journal entry above.

Particulars Column

What: The name of the other account involved in the transaction.

How:

In the Furniture Account Ledger: Write “To Cash A/c” (you received furniture by paying cash).

In the Cash Account Ledger: Write “By Furniture A/c” (cash was spent on furniture).

Amount Column

What: The transaction value. Specify Debit (Dr) or Credit (Cr).

How:

Furniture Account (Debit): ₹20,000.

Cash Account (Credit): ₹20,000.

Journal Folio (JF) Column

What: The journal page number where the original entry lives.

How: Write “45” in both ledger accounts (as in the journal example).

Ledger in Action: See the Columns Work

Furniture Account Ledger:

Date

Particulars

Amount (₹)

JF

2024-03-15

To Cash A/c

20,000 (Dr)

45

Cash Account Ledger:

Date

Particulars

Amount (₹)

JF

2024-03-15

By Furniture A/c

20,000 (Dr)

45

Step 3: Balance the Ledger Accounts

At month-end, tally totals:

Debit Side Total (Furniture A/c): ₹20,000.

Credit Side Total (Cash A/c): ₹20,000. Check: Debits = Credits. If not, hunt for errors.

Step 4: Prep a Trial Balance

List all ledger balances to verify accuracy.

Account

Debit (₹)

Credit (₹)

Furniture

20,000

-

Cash

-

20,000

Total

20,000

20,000

Questions to understand your ability

What is the primary purpose of ledger posting in accounting?

A) To record raw transactions B) To transfer journal entries to individual accounts C) To create the general ledger D) To calculate net profit

Answer: B) To transfer journal entries to individual accounts Reason: Ledger posting is the process of transferring journal entries to specific accounts, categorizing financial transactions into asset, liability, revenue, or expense accounts.

Which of the following is a feature of a ledger account?

A) It stores only credit transactions B) It does not track errors C) It contains both debit and credit entries D) It only includes sales accounts

Answer: C) It contains both debit and credit entries Reason: A ledger contains both debit and credit entries and is used to record all financial transactions, ensuring accuracy through the double-entry system.

What is the purpose of the Journal Folio (JF) column in a ledger?

A) To show the balance of an account B) To indicate the date of the transaction C) To track the journal page number where the entry is recorded D) To categorize the type of transaction

Answer: C) To track the journal page number where the entry is recorded Reason: The Journal Folio (JF) column is used to reference the page number in the journal from where the transaction entry is taken.

Which of the following is true regarding the balancing of ledger accounts?

A) Debit entries are never balanced against credit entries B) At the end of the month, the debit and credit sides should be equal C) Only the credit side is balanced D) Ledger accounts are balanced once at the end of the fiscal year

Answer: B) At the end of the month, the debit and credit sides should be equal Reason: Ledger accounts are balanced at the end of the period to ensure the total debits equal the total credits, which confirms the accuracy of the transactions.

What is the significance of the trial balance in ledger posting?

A) It helps in finalizing the company's profits B) It lists all ledger balances to verify accuracy C) It is used to prepare the general ledger D) It provides information about future transactions

Answer: B) It lists all ledger balances to verify accuracy Reason: The trial balance is prepared to ensure that the total debits equal the total credits, confirming the accuracy of ledger accounts and supporting the preparation of financial reports.

Conclusion

In conclusion, ledger posting is an essential step in accounting that ensures proper categorization and recording of transactions. By transferring journal entries to the ledger, businesses can organize their financial activities effectively. This process involves posting transactions in various columns, balancing accounts, and preparing trial balances. Proper ledger management supports accurate financial reporting, error detection, and provides a clear overview of a company’s financial standing, ultimately aiding in efficient accounting practices.

0 notes

Text

Accrual Accounting System for Businesses in Cameroon

Businesses under the actual earnings regime need to follow standard accounting practices (accrual accounting) as per OHADA standards. #CameroonTaxCompliance #AccountingBasics #OHADA #BusinessLaw

Businesses in Cameroon with an annual turnover above 50,000,000F are classified under Actual Earnings Tax System. These businesses need to prepare their accounts using the standard accounting techniques. The accrual accounting system is provided by the OHADA law. This system demands more detail, tracking not just cash flow but all income earned and expenses incurred within the year. While it’s a…

0 notes

Photo

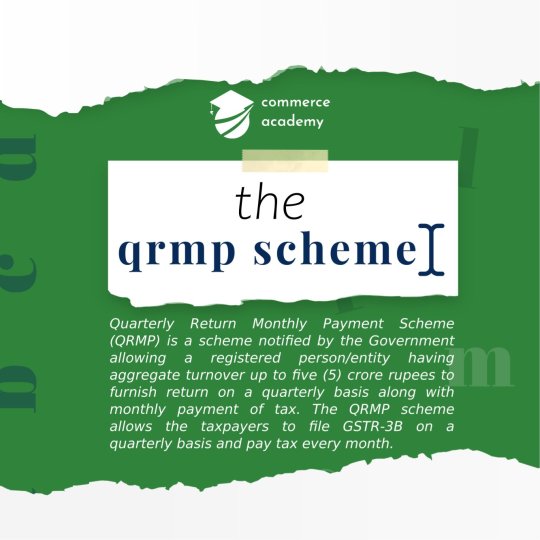

The Central Board of Indirect Taxes & Customs (CBIC) introduced Quarterly Return Filing and Monthly Payment of Taxes (QRMP) scheme under Goods and Services Tax (GST) to help small taxpayers whose turnover is less than Rs.5 crores. The QRMP scheme allows the taxpayers to file GSTR-3B on a quarterly basis and pay tax every month. We did a separate video introducing this new reform a while back. Click on the following link to watch it: https://youtu.be/H853FManxEM. To learn more about accounting, head onto our YouTube channel: youtube.com/c/AcademyCommerce. #commerceacademy #learningcommerce #academycommerce #GST #gstn #gstreforms #accounts #accountingbasics #elearning #youtuber #youtube #accountingonline #staysafe #learncommerce #learnaccounts #basics #likeforlike #followforfollow https://www.instagram.com/p/CJV71nXhgnu/?igshid=u6wrhwkkypem

#commerceacademy#learningcommerce#academycommerce#gst#gstn#gstreforms#accounts#accountingbasics#elearning#youtuber#youtube#accountingonline#staysafe#learncommerce#learnaccounts#basics#likeforlike#followforfollow

2 notes

·

View notes

Text

SAP FICO (Financial Accounting & Management Accounting)

SAP FICO (Financial Accounting & Management Accounting)

The course covers both configuration and end-user processes for SAP FICO module Requirements Basic knowledge of AccountingBasic knowledge of Finance Business ProcessesAccess to SAP ERP system (Optional) Description SAP FICO Course will prepare the students to learn and understand all the end-to-end implementation steps to configure SAP FI and CO modules for any organization. The course also…

View On WordPress

0 notes

Photo

How To Do A Bank Reconciliation (EASY WAY) http://ehelpdesk.tk/wp-content/uploads/2020/02/logo-header.png [ad_1] Bank Reconciliation Cheat Sheet ... #accounting #accountingbasics #agile #amazonfba #analysis #bankrec #bankrecaccounting #bankrectutorial #bankreconciliation #bankreconciliationaccounting #bankreconciliationstatement #bankreconciliationtemplate #bankreconciliationtutorial #bankstatement #business #businessfundamentals #excel #financefundamentals #financialanalysis #financialmodeling #forex #howtodoabankrec #howtodoabankreconciliation #howtoprepareabankrec #howtoprepareabankreconciliation #investing #microsoft #pmbok #pmp #realestateinvesting #reconcilebankstatement #reconcilecashbook #sql #stocktrading #tableau #whatisabankrec #whatisabankreconciliation

0 notes

Text

Basics of Accounts Payable and Accounts Receivable: What Every Accountant Must Know

Cash coming in and out are the two unseen motors that power any firm. These engines are a treasure trove for accountants. The foundation of this apparatus is made up of accounts payable (AP) and accounts receivable (AR). The system will malfunction if you mess things up. If you master them, you'll be the unsung hero responsible for efficient operations. Let's go past the technicalities and explain what these phrases represent, how they operate in India, and why they are essential to financial stability.

Accounts Payable vs Accounts Receivable

Consider accounts payable as your "to-pay" file. It is the debt your company owes suppliers, vendors, or tax authorities. Conversely, accounts receivable is your "to-collect" list—the money people owe you for goods or services supplied. Straight forward? Not rather. In India, where vendor negotiations, TDS deductions, and GST compliance rule, AP and AR necessitate accuracy.

Accounts Payable Cycle: Starts when you receive a bill or invoice. Verify it (check GST details, purchase order matching), approve it, schedule payment (factoring in credit terms like “Net 30”), and finally, record the transaction. One slip-up here—like missing a TDS cut-off—can mean penalties or pissed-off suppliers.

Accounts Receivable Cycle: Begins with invoicing clients. Send the bill (with proper GSTIN and HSN codes), track due dates, follow up relentlessly (because late payments are an epidemic), and log receipts. Missed follow-ups? Say hello to cash crunches.

The difference? AP is about managing outflows (don’t pay late, but don’t pay too early either). AR is about accelerating inflows (get cash faster, always). Both cycles keep the business alive.

Accounts Payable Journal Entries: Recording the Outflow

Every rupee leaving the company needs a paper trail. Let’s say you buy raw materials worth ₹1,00,000 from a vendor, with 18% GST. Here’s how it looks:

Purchase Entry:

Debit: Purchase Account – ₹1,00,000

Debit: GST Input Credit – ₹18,000

Credit: Accounts Payable – ₹1,18,000

Payment Entry (when you clear the dues):

Debit: Accounts Payable – ₹1,18,000

Credit: Bank Account – ₹1,18,000

Forget to reverse input credits? The taxman will hunt you down.

Accounts Receivable Journal Entries: Tracking the Inflow

Sold goods worth ₹2,50,000 to a client with 12% GST? Here’s the drill:

Sales Entry:

Debit: Accounts Receivable – ₹2,80,000

Credit: Sales Account – ₹2,50,000

Credit: GST Output Liability – ₹30,000

Receipt Entry (when payment lands):

Debit: Bank Account – ₹2,80,000

Credit: Accounts Receivable – ₹2,80,000

Pro tip: Always reconcile AR balances with GST returns. Mismatches? Instant red flags during audits.

Accounts Payable Management

Managing AP isn’t about paying bills on time. It’s strategy.

Negotiate Terms: Stretch payment periods without burning vendor relationships. “Net 45” instead of “Net 30”? Yes, please.

Leverage Discounts: Some suppliers offer 2% off for early payments. Crunch the numbers—sometimes saving ₹2,000 on a ₹1 lakh bill beats holding cash.

Automate: Use software to track due dates, auto-calculate TDS, and generate payment schedules. Manual tracking? A one-way ticket to errors.

In India, AP management also means staying sharp on GST input claims. Lost invoices mean lost credits—direct hit on profits.

Accounts Receivable Management

AR management is a mix of charm and aggression.

Credit Policies: Check a client’s CIBIL score before offering credit. Trust everyone? Prepare to bleed cash.

Aging Reports: Classify dues as 0-30 days, 31-60 days, etc. Stuck with 90+ days? Escalate. Send reminders, charge interest (yes, you can legally do this), or threaten legal notices under the Companies Act.

Factor Receivables: Sell overdue invoices to banks or NBFCs for instant cash (at a discount). Not ideal, but better than a liquidity crisis.

Bonus: Use GST-compliant invoices. No proper HSN codes? Say goodbye to input credits for your clients—and expect delayed payments.

The Reasons AP and AR Are Inseparable

AP and AR aren’t rivals—they’re partners. Strong accounts payable management ensures suppliers stay happy, keeping your supply chain intact. Efficient accounts receivable management keeps cash flowing, funding day-to-day ops. Together, they balance the working capital cycle. Ignore one, and the other collapses.

In India, where businesses juggle MSME compliance, GST filings, and tight margins, mastering both cycles isn’t optional. It’s survival.

Questions to Understand your Ability

What is the primary difference between Accounts Payable (AP) and Accounts Receivable (AR)? a) AP deals with managing the inflow of cash, and AR handles outflows b) AP manages payments the business owes, while AR tracks payments owed to the business c) AP is about taxes, and AR is about financial planning d) AP is for goods bought, and AR is for goods sold

Answer: b) AP manages payments the business owes, while AR tracks payments owed to the business

Which of the following is a key step in the Accounts Payable (AP) cycle? a) Send reminders to clients b) Verify GST details and match purchase orders c) Offer early payment discounts to clients d) Negotiate better credit terms with customers

Answer: b) Verify GST details and match purchase orders

In Accounts Receivable (AR) management, what should you do if you are stuck with 90+ days overdue invoices? a) Wait for the client to pay b) Offer a discount to encourage payment c) Send reminders, charge interest, or escalate to legal action d) Ignore the overdue payment

Answer: c) Send reminders, charge interest, or escalate to legal action

When managing Accounts Payable (AP), what is a recommended strategy for handling supplier relationships? a) Always pay as early as possible b) Negotiate for longer payment periods without damaging relationships c) Avoid automating AP processes d) Never negotiate payment terms

Answer: b) Negotiate for longer payment periods without damaging relationships

Why is it important to reconcile Accounts Receivable (AR) balances with GST returns? a) To avoid delays in payments b) To ensure accurate tax reporting and avoid audit red flags c) To calculate interest on overdue payments d) To maintain a good credit score

Answer: b) To ensure accurate tax reporting and avoid audit red flags

Conclusion

Accounts payable and accounts receivable aren’t just “accounting topics.” They’re the heartbeat of your business’s cash flow. Learn the cycles, nail the journal entries, and manage them like a pro. Whether you’re dealing with a local vendor in Chennai or a corporate client in Mumbai, the rules stay the same: Track diligently, enforce ruthlessly, reconcile religiously.

0 notes