#Fastag API Service

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr has been providing a Korean-language service since 2013.

Text

Streamlining Fintech Solutions: PaySprint API Integrations by Infinity Webinfo Pvt Ltd

In the rapidly evolving fintech landscape, businesses require seamless, secure, and scalable solutions to stay competitive and meet customer expectations. Infinity Webinfo Pvt Ltd, a renowned name in digital innovation and technical support, has emerged as a key enabler in this space by offering robust PaySprint API integration services tailored to businesses of all sizes.

About PaySprint

PaySprint is a new-age fintech company recognized for its agile and powerful API stack that facilitates a range of banking and financial services. From Aadhaar Enabled Payment System (AEPS) and DMT (Domestic Money Transfer) to BBPS (Bharat Bill Payment System), recharges, PAN services, and UPI, PaySprint empowers businesses to deliver banking-grade services to their customers with high reliability and compliance.

Infinity Webinfo Pvt Ltd: Bridging Technology and Financial Services

As a trusted software solutions provider, Infinity Webinfo Pvt Ltd specializes in integrating third-party APIs for web, mobile, and enterprise platforms. Their PaySprint API integration services focus on streamlining operations for fintech startups, agents, retailers, and aggregators who wish to build custom platforms or expand their service offerings.

Key PaySprint APIs Offered by Infinity Webinfo:

AEPS (Aadhaar Enabled Payment System) Integration Enable your platform to offer cash withdrawal, balance inquiry, and mini statements through Aadhaar authentication. Ideal for rural banking and financial inclusion.

Micro ATM API Infinity integrates PaySprint's mATM APIs that turn any smartphone or POS device into a functional Micro ATM for real-time transactions.

DMT (Domestic Money Transfer) Integration Seamlessly transfer money to any bank account in India with instant confirmation. Useful for customer-facing businesses like retail stores, service centers, and agents.

Recharge & BBPS Integration Empower your users to recharge mobile/DTH or pay utility bills (electricity, gas, water, etc.) using a unified PaySprint BBPS API integrated by Infinity Webinfo.

PAN Card Services With PaySprint’s NSDL-approved PAN service APIs, businesses can offer new PAN card applications and corrections via a simple interface.

UPI Payout and Collection Add seamless UPI-based payment options, ensuring faster transactions and ease of use for both B2C and B2B models.

Fastag Recharge API Easily integrate Fastag recharges into your system, enabling your platform to become a one-stop financial services hub.

Why Choose Infinity Webinfo for PaySprint Integration?

✅ Certified Development Team familiar with PaySprint’s API architecture and compliance standards.

✅ Custom Dashboard Development for agents and admin users.

✅ Secure API Implementation with proper token management and encryption practices.

✅ Post-integration Support & Maintenance, ensuring business continuity.

✅ Scalable Architecture that grows with your business needs.

Use Case Spotlight

A regional retail chain partnered with Infinity Webinfo Pvt Ltd to integrate PaySprint’s AEPS, DMT, and BBPS services. Within a month, they had a fully operational portal and mobile app, enabling thousands of walk-in customers to access digital financial services at their nearest store—boosting revenue and customer footfall significantly.

Final Thoughts

In today’s digital age, integrating financial APIs is no longer a luxury—it’s a necessity. With Infinity Webinfo Pvt Ltd’s expertise in PaySprint API integration, businesses can launch, scale, and manage fintech services with confidence. Whether you're a startup aiming to enter the market or an enterprise looking to diversify your offerings, Infinity provides the technological backbone you need to succeed.

Would you like a version of this tailored for your website, brochure, or client pitch?

WhatsApp: +91 9711090237

#PaySprint API Integration#PaySprint API#api integration#infinity webinfo pvt ltd#travel portal development#travel portal company#travel portal solutions#payment gateway api integration#white label#white label portal

0 notes

Text

Fastag Recharge API: Offering Convenience for Toll Payments

With the widespread adoption of FASTag for toll payments in India, integrating a Fastag Recharge API can provide significant value to your users. This API allows your customers to conveniently recharge their FASTag accounts directly through your platform, eliminating the need to visit separate portals or use physical recharge methods. A reliable Fastag Recharge API should support all major FASTag issuers, provide real-time recharge status updates, ensure secure transaction processing, and offer easy integration into your existing application or website. By offering this convenient service, you can enhance user experience, increase engagement with your platform, and tap into the growing market for digital toll payments across India.

visit site: https://cyrusrecharge.com/fasttag-payment-api

0 notes

Text

𝗙𝗔𝗦𝘁𝗮𝗴 Recharge 𝗔𝗣𝗜

FASTag Recharge API

In today's fast-paced world, digital payments have become the norm. One of the most significant advances in the world of digital payments has been the introduction of Fast Tags. These tags have revolutionized the way we pay for our toll fees on highways. Instead of stopping to pay cash or card, drivers can simply drive through a Fast Tag lane and have their toll fees deducted from their Fast Tag account.

To facilitate the recharge of Fast Tag accounts, InsPay Digital Private Limited provides a Fast Tag Recharge API. This API is a software interface that enables businesses to integrate Fast Tag recharge services into their existing platforms, such as websites or mobile applications.

Using the Fast Tag Recharge API, businesses can offer their customers a convenient way to recharge their Fast Tag accounts without having to leave the business's platform. The API allows customers to make payments for their Fast Tag account recharge using a variety of digital payment methods such as credit/debit cards, net banking, or UPI.

The InsPay Digital Fast Tag Recharge API is designed to be easy to use and integrate, even for businesses without prior experience in API integration. The API supports multiple programming languages such as Java, PHP, .NET, and Python, making it accessible to a broad range of businesses.

The API is also highly secure, ensuring that all transactions made through it are protected. It uses advanced encryption and authentication mechanisms to safeguard user data and prevent any unauthorized access or fraud. Additionally, the API complies with all regulatory guidelines for digital payments, ensuring that businesses using it remain compliant with relevant laws and regulations.

With the InsPay Digital Fast Tag Recharge API, businesses can offer their customers a seamless and hassle-free experience for recharging their Fast Tag accounts. This API enables businesses to expand their service offerings and reach a wider customer base while also improving customer satisfaction by providing a convenient payment option.

In summary, the InsPay Digital Fast Tag Recharge API provides a powerful tool for businesses looking to integrate Fast Tag recharge services into their platforms. The API offers a secure, user-friendly, and accessible solution for Fast Tag recharge, making it an ideal choice for businesses of all sizes. By using this API, businesses can offer their customers a convenient way to recharge their Fast Tag accounts while also improving their overall service offerings.

0 notes

Text

ECOFincare Provides a Digital Online Payment Services Platform. Provides Banking, Money Transfer Services, Aadhaar-based Payment Services, Utility Bills Payment & Recharge Services, UPI Services, New Fastag & Recharge, Travel Booking Services, New Bank accounts, Credit Card & Pancard Services, and more.

Also, Provide Software API and Payment Gateway Solutions and White Label Payment Solutions for your own financial business.

1 note

·

View note

Text

Paytrav is a leading API integration company in India, offering direct API solutions for various products such as AEPS, MATM, DMT, Multi-recharge, and Fastag. If you're looking to integrate APIs into your website or white label solution, we have dedicated software and digital solutions available.

#dmt api provider#bus api provider#travel api provider#flight api provider#aeps api provider#matm api#bus booking portal

0 notes

Text

Long to pay toll tax on the toll plaza

We tell you about the services of Fastag, if you have Fastag services, then you will not have to pay any tax on the toll plaza, and vehicles will not have to wait long to pay toll tax on the toll plaza.

FASTAG API INTEGRATION

Can do But we want to tell you, people say that Fastag only increased people’s trouble. Sometimes money is deducted somewhere else, in many places, Fastag does not read, but Startling World Services gives you the best approval, where you will not face any such problem. Yes, there is a case that the car was parked at home and toll tax was deducted, it does not happen.

1. It has been seen in many places that people are facing a lot of problems due to Fastag, fraudulent portals are responsible for double recovery in many places. Startling World Services‘ Fastag API does that.

2. We have seen this many times, fines are charged from the carriers despite the fast tag, the queue is kept for hours.

3. It has been seen with many people, Fastag is also reporting fraud, sometimes complaining of double amount deduction.

Those who work in the field of business know that being on the road is not an easy feat. We know that the issues for them range from bad weather to pressure to deliver on time to find the right route which is not easy. However, we know that after conversations with various lorry drivers, we or all of them were able to conclude that the biggest challenge in their jobs is wearables and never ending toll queues. In this article, we will discuss FASTag problems and their solutions in detail. Join Startling World and use our services without any hassle.

In view of the traffic these days, Fastag service was introduced, a hassle-free option for the payer and the collector for smooth and efficient toll operations. The bid was meant to make toll collection easier on all highways across India. To reduce human error, waste of time and unnecessary fuel consumption, FASTag came into the picture in the Indian transport industry We provide B2B, B2C and Software Development

We provide B2B, B2C and Software Development

0 notes

Text

instagram

Start your Bussiness with Most reliable and leading brand in

Recharge software industry.

We are offering the following services in our *Rental Based software.

In Rs 1999 /- Package :

1. B2B Recharge Service (Prepaid, Postpaid, DTH)

2. API reselling (Only For Recharge

3.Electricity Bill Payment

4.Domestic Money Transfer

5.BBPS (Bharat Bill Payment Services)_

6.B2B eCommerce.

In Rs 1499 /- Package :

Only B2B Recharge Services With Web & App (Prepaid, Postpaid, DTH)

New Services: Pan card & AePs (One-time setup Fee ₹15000/+18% GST

Two Wheeler Insurance

FOR DEMO: https://goo.gl/oKdv6k

FOR MARGIN: https://goo.gl/b8KhWS

DEDICATED B2B:http://tiny.cc/v2s-recharge-dedicated

FULL DETAILS: http://tiny.cc/v2s-rental-1

Facebook: v2sinfosystem

Instagram: v2s.infosystem

WhatsApp: 8375012908, 9310052981

Google: g.page/v2sinfosystem

Website: v2sinosystem.com

#b2b #b2bsoftware #b2bmultirecharge #software #multirechargesoftware #multirechargebusiness #lawestprice #android #androidapp #bbps #aeps#recharge #dth #dthrecharge #bikeinsurance #moneytransfer #pancard #ecommerce #fastag #electricity #electricitybillpayment #waterbillpayment

1 note

·

View note

Text

No Need to Travel long, When Micro ATM Has Come Along

Micro ATM is the solution for the areas where large or traditional ATMs and bank branches are hard to reach. So, to solve the cash crunch in remote areas, RBP Finivis Pvt. Ltd. has come forward as an API Provider in India with an extremely useful product. It offers Micro ATM API & SDK for the businesses to emerge and occupy space in the rapidly evolving FinTech industry. It is available 24/7 and 365 days to deliver various banking services such as cash withdrawal, balance inquiry, mini statement, and more.

What is Micro ATM and how it works?

Micro ATM is basically a card swipe machine that works on a point of sale terminal with minimal power consumption. It is a handheld portable device that contains a card reader to verify debit cards from any bank, makes it interoperable, and offers desired financial transaction services to individuals. Some Micro ATMs are also available with a fingerprint scanner. It is connected to the central banking servers through GPRS technology. Hence, Micro ATMs are a safe, secure, and instant solution to get banking transactions done.

Is That Amazing for Rural India? Let Us Discuss Benefits of Micro ATM for Them-

Micro ATM is really an amazing thing launched by the government of India under the guidelines of the National Payment Corporation of India (NPCI). As it is a mini version of traditional ATMs, it doesn’t require much space for its setup and it is also very cost-effective. Hence, Micro ATMs can be set up anywhere without much effort.

These are some reasons; Micro ATM is a boon for rural India. People don’t need to travel long distances and waste time in long queues to get facilities of banking services. People can easily withdrawal cash up to Rs. 10,000 using their debit card just by visiting their nearest business correspondent. Also, they get access to some other basic banking services too. So, to co-operate government in the motive of bringing financial inclusion in the country, RBP Finivis Pvt. Ltd. emerged as an API Provider Company. It offers an opportunity for businesses, become a part of the FinTech industry and help rural people & weaker sections of society to come under the banking framework and enjoy financial services at their doorsteps.

Objectives Of RBP Towards Developing Micro ATM API

Objectives of this specification are as follows-

To bring down transaction cost

To guarantee interoperability

Ensure security and transparency of transaction

Provide a uniform customer experience

As the API is customized, it is user friendly that reduces agent training needs

To bring down the cost of being compatible with an existing banking system

Conclusion

RBP Finivis is a Micro ATM API Provider company in India located in Haryana that contributes to making Digital Bharat as it provides reliable services for easy transactions. It is an integrated programming facility that guarantees secured payments. Along with Micro ATM API, RBP offers a few more APIs for businesses to grow to earn and offer the best financial/e-commerce transactions on fingertips to everyone. Such APIs are –

AePS API

Micro ATM API

DMT API

BBPS API

Fastag Recharge API

AePS Cash Withdrawal

#micro atm api#micro atm api provider#matm api provider#mini atm api provider#white label api provider#micro atm software#aeps api#aeps admin portal#high commission aeps api#aeps api provider#aadhaar pay api#aeps software#aeps business#cashout api#payout api#cash withdrawal api

1 note

·

View note

Photo

High commission multi recharge software in Jharkhand

Start your own mobile recharge business. the Vast web India High Commission Multi recharge Software Provider company to help you provide your customers to avail HIgh commission Recharge, bill payments, and other services from the comfort of your shop.

Vast Web India offers various utility services such as Recharge, Bill Payments, and Pan Card. mobile and DTH recharge using our portal and earn commission per transaction.

We have launched AePS, PAN Card, FasTag Recharge Good Technical Support with 24X7 Availability.

SERVICES:- Multi Recharge Software | Whitelabel Recharge Software | all in one recharge | multi recharge website | multi recharge portal | multi recharge app | multi recharge business Software | Mobile Recharge Services | Mobile Recharge Software | Lapu Sim Recharge Software | white label recharge portal | multi recharge service provider | Mobile Recharge API | Multi Recharge Api | Utility Bill Payment API | White Label Recharge API | Dth Recharge Api | Mobile Recharge Software | Mobile Recharge RetailersSingle Sim Multi Recharge Software | Whitelabel Recharge SoftwareRecharge | Lapu Software | Reseller Recharge Software| Mobile Recharge Website | B2B Recharge Software | high commission multi recharge | multi recharge software provider |multi recharge company | multi recharge software | mobile recharge software development | recharge software provider | recharge software development | Recharge software development | High Commission Multi recharge Software

High Commission Multi recharge Software available in Andhra Pradesh | Assam | Arunachal Pradesh | Bihar | Chhattisgarh | Goa | Gujarat | Haryana | Himachal Pradesh | Jharkhand | Karnataka | Kerala | Madhya Pradesh | Maharashtra | Manipur | Meghalaya | Mizoram | Nagaland | Odisha| Punjab | Rajasthan | Sikkim| Tamil Nadu | Telangana | Tripura| Uttarakhand | Uttar Pradesh | West Bengal

Visit now - www.vastwebindia.com

Contact us - +917230882222

0 notes

Photo

Now you can create a company in your name, by making your name a brand, you can use API's services (AEPS, BBPS, Money Transfer, Payout, Aadhar Pay, Recharge, UPI & QR Code, Fastag etc.) as well as white label software. Make it And reach your business to the people and earn maximum income. Don't delay, start business by making your name brand company today!!!

Call Now: +91 9956951008 Website: www.suprosoft.in

0 notes

Text

Why Your Business Needs a Reliable Flight Booking API Provider in India

In India's rapidly expanding travel market, offering seamless flight booking services is no longer a luxury, but a necessity. Whether you're a travel agency, an online travel portal, or a business looking to integrate travel services into your platform, a reliable Flight Booking API Provider in India is essential. This article explores the compelling reasons why your business needs a robust fastag recharge api and how it can drive growth and enhance customer satisfaction.

The Indian aviation sector is experiencing unprecedented growth, with an increasing number of people opting for air travel. To capitalize on this trend, businesses need to provide convenient and efficient flight booking solutions. A reliable Flight Booking API Provider enables businesses to access real-time flight data, automate booking processes, and offer a seamless user experience.

Key Benefits of Integrating a Flight Booking API:

Real-Time Data Access: APIs provide access to up-to-date flight information, including availability, fares, and schedules, ensuring accuracy and reliability.

Automation and Efficiency: Automating the booking process reduces manual effort, minimizes errors, and streamlines operations.

Enhanced Customer Experience: Offering a seamless and user-friendly booking experience enhances customer satisfaction and loyalty.

Increased Revenue: Integrating a flight booking API can open new revenue streams by allowing businesses to offer a wider range of travel services.

Scalability: APIs allow businesses to scale their operations as demand grows, without the need for significant infrastructure investments.

Competitive Advantage: Offering convenient and efficient flight booking services can give businesses a competitive edge in the market.

Integration with Other Services: A good flight booking API can integrate with other essential services, like Bus Booking API Solution in India, allowing your business to offer a complete travel package.

Enhancing Security and Payment Options:

In today’s digital age, security and diverse payment options are critical. Integrating services like an Aadhar Verification API Solution in India can significantly enhance security by verifying customer identities. Offering diverse payment methods, including those facilitated by a UPI eCollection API Solution in India, ensures a smooth and convenient transaction process.

Why Cyrus Recharge Stands Out:

Cyrus Recharge is a leading software development and API provider in India, offering robust and reliable flight booking API solutions. Their expertise in API integration and commitment to customer satisfaction make them a valuable partner for businesses looking to enhance their travel services.

Frequently Asked Questions (FAQs):

What key features should I look for in a Flight Booking API Provider?

Key features include real-time data access, API reliability, ease of integration, scalability, robust security, and comprehensive customer support.

How can integrating an Aadhar Verification API Solution benefit my flight booking business?

Integrating an Aadhar Integration Service Provider in India enhances security by verifying customer identities, reducing the risk of fraud, and ensuring compliance with regulatory requirements.

Why is offering diverse payment options, like UPI, important for flight bookings?

Offering diverse payment options, including those facilitated by a UPI eCollection API Solution in India, provides customers with flexibility and convenience, enhancing their booking experience and increasing conversion rates.

fssai verification api

0 notes

Text

Setu raises $15M to help developers connect with banks to offer Indians ‘sachet-sized’ financial products

India’s push to digital payments in the last three years has seen tens of millions of people get comfortable with exchanging money online for the first time. But most businesses in the country are still offline and relying on traditional ways to engage with their customers. A Bangalore-based startup that is attempting to bring a similar digitization to them just got a nod from high profile investors.

Setu, a two-year-old startup, said on Wednesday that it has raised $15 million in its Series A financing round from Falcon Edge and Lightspeed Venture Partners U.S. Existing investors Lightspeed India Partners and Bharat Inclusion Seed Fund also participated in the round.

Setu is an API infrastructure provider that allows financial institutions such as banks to connect with companies and small businesses that want to provide financial services to their customers.

The idea is to connect small businesses such as a local cable TV operator or a neighborhood store that is already engaging with thousands of people to serve their customers better by offering formal financial services such as credit. Local kirana stores already have a great understanding of their customers and offer them informal credit. Could they work with financial institutions to formalize their services?

Even as India’s mobile payments market has grown exponentially in the last three years — and saw the arrival of companies such as Amazon, Facebook, Google, and emergence of dozens of local players to help people pay digitally — much of the nation’s population still needs access to formal sachet-ized financial products and services.

“Poor product design, high distribution costs, and legacy technology have been barriers to make this happen,” said Nikhil Kumar, co-founder of Setu.

Kumar, and Sahil Kini, the other co-founder, are especially well-suited to tackle this challenge. Kumar previously worked as a fellow at iSPIRT Foundation that built an ecosystem for UPI, an infrastructure developed by a coalition of banks and backed by the Indian government that has amassed over 100 million users and clocks over a billion transactions a month. Kini worked at Aspada Investments.

The startup today offers open APIs across four categories — bills, savings, credit, and payments. Any developer can access its sandbox to build an application and go through a rigorous developer certification program to go live, the startup said. This makes it easy for any company to acquire plug-and-play financial services and become a fintech player.

“We are big believers in Setu’s vision to build infrastructure that enables the large-scale distribution of, and access to, financial products. Sahil, Nikhil, and the Setu team have an exciting roadmap for the future of financial services in India and we’re proud to support their journey,” said Bejul Somaia, Managing Partner at Lightspeed India, in a statement.

Setu recently launched Collect, an API bundle designed for developers to build their own custom collections product. For instance, lending collection companies are using Setu to build an omni-channel collections stack for banks and NBFCs. “This API platform is built on top of public infrastructure such as UPI and BBPS by partnering with some of India’s leading banks — Kotak, ICICI, & Axis Bank,” said Kumar.

It is now working on building blocks for digital financial services across FASTag, savings, credit, and data, he said.

from Facebook – TechCrunch https://ift.tt/3a9QD97 via IFTTT

0 notes

Text

Mobile payments firms in India are now scrambling to make money – DailyKhaleej

Vijay Shekhar Sharma, founder and chief govt of India’s most respected startup, Paytm, posed an existential query in a current press convention.

“What do you consider the business mannequin for digital cellular payments. How will we make money?” Sharma requested Nandan Nilekani, one of many key architects of the Common Payments Infrastructure that created a digital payments revolution in the nation.

It’s the multi-billion-dollar query that scores of native startups and worldwide giants have been scrambling to reply as a lot of them aggressively shift their focus to serving retailers and constructing lending merchandise and different monetary providers .

New Delhi’s abrupt transfer to invalidate a lot of the paper payments in the cash-dominated nation in late 2016 despatched a whole bunch of hundreds of thousands of individuals to money machines for months to observe.

For a handful of startups akin to Paytm and MobiKwik, this money crunch meant netting tens of hundreds of thousands of latest customers in a span of some months.

India then moved to work with a coalition of banks to develop the payments infrastructure that, not like Paytm and MobiKwik’s earlier system, didn’t act as an middleman “cellular pockets” to function an middleman between customers and their banks, however facilitated direct transaction between two customers’ financial institution accounts.

Silicon Valley firms shortly took discover. For years, Google and the likes have tried to change the buying habits of individuals in many Asian and African markets, the place they’ve amassed a whole bunch of hundreds of thousands of customers.

In Pakistan, as an illustration, most individuals nonetheless run errands to neighborhood shops when they need to high up credit score to make telephone calls and entry the web.

With China conserving its doorways largely closed for overseas firms, India, the place many American giants have already poured billions of {dollars} to discover their subsequent billion customers, it was a no brainer name.

“In contrast to China, we’ve given equal alternatives to each small and enormous home and overseas firms,” stated Dilip Asbe, chief govt of NPCI, the payments physique behind UPI.

And thus started the race to take part in the grand Indian experiment. Buyers have adopted go well with as properly. Indian fintech startups raised $2.74 billion final yr, in contrast to 3.66 billion that their counterparts in China secured, in accordance to analysis agency CBInsights.

And that guess in a market with greater than half a billion web customers has already began to repay.

“In the event you take a look at UPI as a platform, we’ve by no means seen progress of this sort earlier than,” Nikhil Kumar, who volunteered at a nonprofit group to assist develop the payments infrastructure, stated in an interview.

In October, simply three years after its inception, UPI had amassed 100 million customers and processed over a billion transactions. It has sustained its progress since, clocking 1.25 billion transactions in March — regardless of one of many nation’s largest banks going by means of a meltdown final month.

“All of it comes down to the issue it’s fixing. In the event you take a look at the western markets, digital payments have largely been centered on an individual sending money to a service provider. UPI does that, nevertheless it additionally allows peer-to-peer payments and throughout a wide-range of apps. It’s interoperable,” stated Kumar, who’s now working at a startup known as Setu to develop APIs to assist small companies simply settle for digital payments.

Vice-president of Google’s Subsequent Billion Customers Caesar Sengupta speaks in the course of the launch of the Google “Tez” cellular app for digital payments in New Delhi on September 18, 2017 (Photograph: Getty Photos through AFP PHOTO / SAJJAD HUSSAIN)

The Google Pay app has amassed over 67 million month-to-month lively customers. And the corporate has discovered the UPI pipeline so fascinating that it has really helpful related infrastructure to be constructed in the U.S.

In August, the Federal Reserve proposed to develop a brand new inter-bank 24×7 real-time gross settlement service that will assist sooner payments in the nation. In November, Google really helpful (PDF) that the U.S. Federal Reserve implement a real-time payments platform akin to UPI.

“After simply three years, the annual run fee of transactions flowing by means of UPI is about 19% of India’s Gross Home Product, together with 800 million month-to-month transactions valued at roughly $19 billion,” wrote Mark Isakowitz, Google’s vp of Authorities Affairs and Public Coverage.

Paytm itself has amassed greater than 150 million customers who use it yearly to make transactions. Total, the platform has 300 million cellular pockets accounts and 55 million financial institution accounts, stated Sharma.

Seek for a enterprise mannequin

However regardless of on-boarding greater than 100 million customers on their platform, cost firms are struggling to minimize their losses — not to mention flip a revenue.

At an occasion in Bangalore late final yr, Sajith Sivanandan, managing director and enterprise head of Google Pay and Subsequent Billion Person Initiatives, stated present native guidelines have compelled Google Pay to function in India with no clear enterprise mannequin.

Mobile cost firms by no means levied any price to customers as a method to develop their attain in the nation. A current directive from the federal government has now put an finish to the minimize they have been receiving to facilitate UPI transactions between customers and retailers.

Google’s Sivanandan urged the native cost our bodies to “discover methods for cost gamers to make money” to guarantee each stakeholder had incentives to function.

Paytm, which has raised greater than $Three billion to date, reported a lack of $549 million in the monetary yr ending in March 2019.

The agency, backed by SoftBank and Alibaba, has expanded to a number of new companies in current years, together with Paytm Mall, an e-commerce enterprise, social commerce, monetary providers arm Paytm Money and a motion pictures and ticketing class.

This yr, Paytm has expanded to serve retailers, launching new devices akin to a stand that shows QR check-out codes that comes with a calculator and a battery pack, a conveyable speaker that gives voice confirmations of transactions and a point-of-sale machine with built-in scanner and printer.

In an interview with DailyKhaleej, Sharma stated these units are already garnering spectacular demand from retailers. The corporate is providing these devices to them as a part of a subscription service that helps it set up a gentle circulation of income.

The agency’s Money arm, which affords lending, insurance coverage and investing providers, has amassed over Three million customers. The top of Paytm Money, Pravin Jadhav, resigned from the corporate this week, an individual acquainted with the matter stated. A Paytm spokeswoman declined to remark. (Indian information outlet Entrackr first reported the event.)

Flipkart’s PhonePe, one other main participant in India’s payments market, immediately serves greater than 175 million customers, and over eight million retailers. Its app serves as a platform for different companies to attain customers, defined Rahul Chari, co-founder and CTO of the agency, in an interview with DailyKhaleej. The corporate is at present not taking a minimize for the true property on its app, he added.

However these startups’ enlargement into new classes signifies that they now have to face off much more rivals, and spend extra money to acquire a foothold. Within the social commerce class, as an illustration, Paytm is competing with Naspers-backed Meesho and a handful of latest entrants; and heavily-backed OkCredit and KhataBook immediately lead the bookkeeping market.

BharatPe, which raised $75 million two months in the past, is digitizing mother and pop shops and granting them working capital. And PineLabs, which has already turn into a unicorn, and MSwipe have flooded the market with their point-of-sale machines.

A vendor holds an Mswipe terminal, operated by M-Swipe Applied sciences Pvt Ltd., in an organized {photograph} at a roadside stall in Bengaluru, India, on Saturday, Feb. 4, 2017. (Photographer: Dhiraj Singh/Bloomberg through Getty Photos)

“They haven’t any alternative. Cost is the gateway to companies akin to e-commerce and lending you could monetize. In Paytm’s case, their earlier guess was Paytm Mall,” stated Jayanth Kolla, founder and chief analyst at analysis agency Convergence Catalyst.

However Paytm Mall has struggled to compete with giants Amazon India and Walmart’s Flipkart. Final yr, Mall pivoted to offline-to-online and online-to-offline fashions, whereby orders positioned by clients are serviced from native shops. The corporate additionally secured about $160 million from eBay final yr.

An govt who beforehand labored at Paytm Mall stated the enterprise has struggled to develop as a result of its goal-post has continuously shifted over time. It has lately began to give attention to promoting fastags, a system that permits car house owners to swiftly pay toll charges. At the least two extra executives on the agency are on their approach out, an individual acquainted with the matter stated.

Kolla stated the present dynamics of India’s cellular payments market, the place greater than 100 firms are chasing the identical set of viewers, is harking back to the telecom market in the nation from greater than a decade in the past.

“When there have been simply 4 to 5 gamers in the telecom market, the prospect of them turning into worthwhile was a lot greater. They have been scaling like loopy. They grew with the bottom ARPU in the world (at about $2) and have been nonetheless worthwhile.

“However the second that quantity grew to greater than a dozen in a single day, and the brand new gamers began providing extra inexpensive plans to subscribers, that’s when profitability began to turn into elusive,” he stated.

To high that off, the arrival of Reliance Jio, a telecom operator run by India’s richest man, in 2016 in the nation with the most cost effective tariff plans in the world, upended the market as soon as once more, forcing a number of gamers to go away the market, or declare bankruptcies, or consolidate.

India’s cellular payments market is now heading to an analogous path, stated Kolla.

If there weren’t sufficient gamers combating for a slice of India’s cellular payments market that Credit score Suisse estimate might attain $1 trillion by 2023, WhatsApp, the preferred app in the nation with extra that 400 million customers, is ready to roll out its cellular payments service in the nation in a few months.

On the aforementioned press convention, Nilekani suggested Sharma and different gamers to give attention to monetary providers akin to lending.

Sadly, the coronavirus outbreak that promoted New Delhi to order a three-week lockdown final month is probably going going to influence the flexibility of hundreds of thousands of individuals to use such providers.

“India has greater than 100 million microfinance accounts, serviced in money each week by gig-economy employees, who hawk greens on avenue corners or embroider saris bought in malls, amongst different issues. Three out of 4 employees make a dwelling by working casually for others or at their household firms and farms. Extended shutdowns will impair their potential to repay loans of two.1 trillion rupees ($28.5 billion), placing the world’s largest microfinance business in danger,” wrote Bloomberg columnist Andy Mukherjee.

from WordPress https://ift.tt/2X0li5E via IFTTT

0 notes

Text

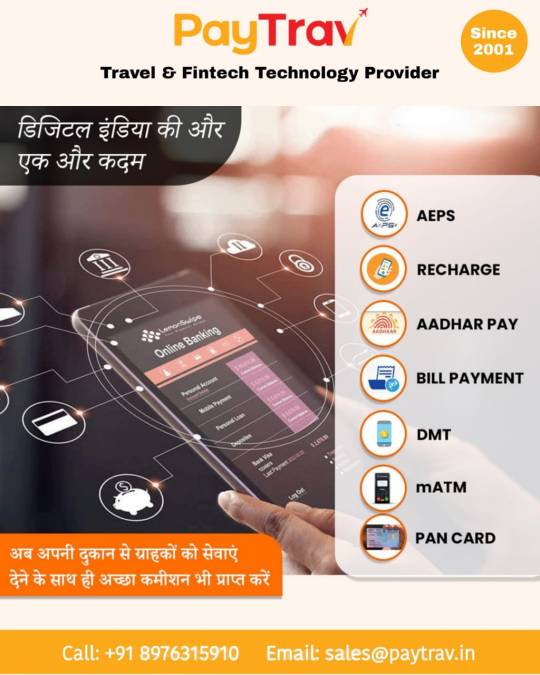

Paytrav-B2B Fintech Software API Provider in India

Looking for API integration? Paytrav is a Direct API provider company across the India. We provide API for the products like AEPS, MATM, DMT, Multi-recharge and Fastag. If you want to plug API solutions then don’t think it’s time to integrate. We are available with dedicated software and digital solutions as well.

You can integrate AEPS API (Application Programmable Interface)/ software in your website or whitelevel. We are service provider of AEPS software. Create unlimited agents, distributor, master distributor under you. Highest commission assured.

With its cutting-edge goods and services, Paytrav is the top AePS API provider company in India.

Banking API Providers In India| Fintech API provider| best API service provider company in India|Aeps api service provider| Travel Portal API Provider India| Aeps Aadhaar Enabled Payment System Service

#flight api provider#dmt api provider#hotel booking software#dmt api#travel api provider#aeps api provider

0 notes

Text

Fastag Service

We provide master Fastag API Service and Mobile Recharge all API Development solution in India. Any company can start its own API business in India if any API development was required by Startling World any API development service company using a master API.

Call Now- 9956251008 Email- [email protected] Web Site- https://bit.ly/2Fdi9sr

0 notes

Text

Mobile payments firms in India are now scrambling to make money

Vijay Shekhar Sharma, founder and chief executive of India’s most valuable startup, Paytm, posed an existential question in a recent press conference.

“What do you think of the commercial model for digital mobile payments. How do we make money?” Sharma asked Nandan Nilekani, one of the key architects of the Universal Payments Infrastructure that created a digital payments revolution in the country.

It’s the multi-billion-dollar question that scores of local startups and international giants have been scrambling to answer as many of them aggressively shift their focus to serving merchants and building lending products and other financial services .

New Delhi’s abrupt move to invalidate much of the paper bills in the cash-dominated nation in late 2016 sent hundreds of millions of people to cash machines for months to follow.

For a handful of startups such as Paytm and MobiKwik, this cash crunch meant netting tens of millions of new users in a span of a few months.

India then moved to work with a coalition of banks to develop the payments infrastructure that, unlike Paytm and MobiKwik’s earlier system, did not act as an intermediary “mobile wallet” to serve as an intermediary between users and their banks, but facilitated direct transaction between two users’ bank accounts.

Silicon Valley companies quickly took notice. For years, Google and the likes have attempted to change the purchasing behavior of people in many Asian and African markets, where they have amassed hundreds of millions of users.

In Pakistan, for instance, most people still run errands to neighborhood stores when they want to top up credit to make phone calls and access the internet.

With China keeping its doors largely closed for foreign firms, India, where many American giants have already poured billions of dollars to find their next billion users, it was a no-brainer call.

“Unlike China, we have given equal opportunities to both small and large domestic and foreign companies,” said Dilip Asbe, chief executive of NPCI, the payments body behind UPI.

And thus began the race to participate in the grand Indian experiment. Investors have followed suit as well. Indian fintech startups raised $2.74 billion last year, compared to 3.66 billion that their counterparts in China secured, according to research firm CBInsights.

And that bet in a market with more than half a billion internet users has already started to pay off.

“If you look at UPI as a platform, we have never seen growth of this kind before,” Nikhil Kumar, who volunteered at a nonprofit organization to help develop the payments infrastructure, said in an interview.

In October, just three years after its inception, UPI had amassed 100 million users and processed over a billion transactions. It has sustained its growth since, clocking 1.25 billion transactions in March — despite one of the nation’s largest banks going through a meltdown last month.

“It all comes down to the problem it is solving. If you look at the western markets, digital payments have largely been focused on a person sending money to a merchant. UPI does that, but it also enables peer-to-peer payments and across a wide-range of apps. It’s interoperable,” said Kumar, who is now working at a startup called Setu to develop APIs to help small businesses easily accept digital payments.

Vice-president of Google’s Next Billion Users Caesar Sengupta speaks during the launch of the Google “Tez” mobile app for digital payments in New Delhi on September 18, 2017 (Photo: Getty Images via AFP PHOTO / SAJJAD HUSSAIN)

The Google Pay app has amassed over 67 million monthly active users. And the company has found the UPI pipeline so fascinating that it has recommended similar infrastructure to be built in the U.S.

In August, the Federal Reserve proposed to develop a new inter-bank 24×7 real-time gross settlement service that would support faster payments in the country. In November, Google recommended (PDF) that the U.S. Federal Reserve implement a real-time payments platform such as UPI.

“After just three years, the annual run rate of transactions flowing through UPI is about 19% of India’s Gross Domestic Product, including 800 million monthly transactions valued at approximately $19 billion,” wrote Mark Isakowitz, Google’s vice president of Government Affairs and Public Policy.

Paytm itself has amassed more than 150 million users who use it every year to make transactions. Overall, the platform has 300 million mobile wallet accounts and 55 million bank accounts, said Sharma.

Search for a business model

But despite on-boarding more than a hundred million users on their platform, payment firms are struggling to cut their losses — let alone turn a profit.

At an event in Bangalore late last year, Sajith Sivanandan, managing director and business head of Google Pay and Next Billion User Initiatives, said current local rules have forced Google Pay to operate in India without a clear business model.

Mobile payment firms never levied any fee to users as a strategy to expand their reach in the country. A recent directive from the government has now put an end to the cut they were receiving to facilitate UPI transactions between users and merchants.

Google’s Sivanandan urged the local payment bodies to “find ways for payment players to make money” to ensure every stakeholder had incentives to operate.

Paytm, which has raised more than $3 billion to date, reported a loss of $549 million in the financial year ending in March 2019.

The firm, backed by SoftBank and Alibaba, has expanded to several new businesses in recent years, including Paytm Mall, an e-commerce venture, social commerce, financial services arm Paytm Money and a movies and ticketing category.

This year, Paytm has expanded to serve merchants, launching new gadgets such as a stand that displays QR check-out codes that comes with a calculator and a battery pack, a portable speaker that provides voice confirmations of transactions and a point-of-sale machine with built-in scanner and printer.

In an interview with TechCrunch, Sharma said these devices are already garnering impressive demand from merchants. The company is offering these gadgets to them as part of a subscription service that helps it establish a steady flow of revenue.

The firm’s Money arm, which offers lending, insurance and investing services, has amassed over 3 million users. The head of Paytm Money, Pravin Jadhav, resigned from the company this week, a person familiar with the matter said. A Paytm spokeswoman declined to comment. (Indian news outlet Entrackr first reported the development.)

Flipkart’s PhonePe, another major player in India’s payments market, today serves more than 175 million users, and over 8 million merchants. Its app serves as a platform for other businesses to reach users, explained Rahul Chari, co-founder and CTO of the firm, in an interview with TechCrunch. The company is currently not taking a cut for the real estate on its app, he added.

But these startups’ expansion into new categories means that they now have to face off even more rivals, and spend more money to gain a foothold. In the social commerce category, for instance, Paytm is competing with Naspers-backed Meesho and a handful of new entrants; and heavily-backed OkCredit and KhataBook today lead the bookkeeping market.

BharatPe, which raised $75 million two months ago, is digitizing mom and pop stores and granting them working capital. And PineLabs, which has already become a unicorn, and MSwipe have flooded the market with their point-of-sale machines.

A vendor holds an Mswipe terminal, operated by M-Swipe Technologies Pvt Ltd., in an arranged photograph at a roadside stall in Bengaluru, India, on Saturday, Feb. 4, 2017. (Photographer: Dhiraj Singh/Bloomberg via Getty Images)

“They have no choice. Payment is the gateway to businesses such as e-commerce and lending that you can monetize. In Paytm’s case, their earlier bet was Paytm Mall,” said Jayanth Kolla, founder and chief analyst at research firm Convergence Catalyst.

But Paytm Mall has struggled to compete with giants Amazon India and Walmart’s Flipkart. Last year, Mall pivoted to offline-to-online and online-to-offline models, wherein orders placed by customers are serviced from local stores. The company also secured about $160 million from eBay last year.

An executive who previously worked at Paytm Mall said the venture has struggled to grow because its goal-post has constantly shifted over the years. It has recently started to focus on selling fastags, a system that allows vehicle owners to swiftly pay toll fees. At least two more executives at the firm are on their way out, a person familiar with the matter said.

Kolla said the current dynamics of India’s mobile payments market, where more than 100 firms are chasing the same set of audience, is reminiscent of the telecom market in the country from more than a decade ago.

“When there were just four to five players in the telecom market, the prospect of them becoming profitable was much higher. They were scaling like crazy. They grew with the lowest ARPU in the world (at about $2) and were still profitable.

“But the moment that number grew to more than a dozen overnight, and the new players started offering more affordable plans to subscribers, that’s when profitability started to become elusive,” he said.

To top that off, the arrival of Reliance Jio, a telecom operator run by India’s richest man, in 2016 in the country with the cheapest tariff plans in the world, upended the market once again, forcing several players to leave the market, or declare bankruptcies, or consolidate.

India’s mobile payments market is now heading to a similar path, said Kolla.

If there were not enough players fighting for a slice of India’s mobile payments market that Credit Suisse estimate could reach $1 trillion by 2023, WhatsApp, the most popular app in the country with more that 400 million users, is set to roll out its mobile payments service in the country in a couple of months.

At the aforementioned press conference, Nilekani advised Sharma and other players to focus on financial services such as lending.

Unfortunately, the coronavirus outbreak that promoted New Delhi to order a three-week lockdown last month is likely going to impact the ability of millions of people to use such services.

“India has more than 100 million microfinance accounts, serviced in cash every week by gig-economy workers, who hawk vegetables on street corners or embroider saris sold in malls, among other things. Three out of four workers make a living by working casually for others or at their family firms and farms. Prolonged shutdowns will impair their ability to repay loans of 2.1 trillion rupees ($28.5 billion), putting the world’s largest microfinance industry at risk,” wrote Bloomberg columnist Andy Mukherjee.

from iraidajzsmmwtv https://ift.tt/2QZJ26c via IFTTT

0 notes