#Global Composite Insulators Market

Text

Composite Insulators Market 2022 | Global Business, Share, Trend and SWOT Analysis 2030 | By R&I

Reports & Insights has freshly issued a new report titled “Composite Insulators Market: Opportunity Analysis and Future Assessment 2022-2030” which speaks about the market size, market potential and comprehensive understanding of the statistics concerned with the development of the respective market. The market analysts estimate that the Composite Insulators Market size will elevate from XXX in 2022 to XXX by the year 2030, at an estimated CAGR of XX. The base year considered for the study is 2020, and the market size is projected from 2022 to 2030.

Request a Sample Copy of this Report @: https://reportsandinsights.com/sample-request/2534

Composite Insulators Introduction

Insulators basically serve its utility in electrical equipment with a view to sustain and differentiate electrical conductors without enabling current to percolate through the insulators. Silicone rubber is one of the most comprehensively utilized polymeric insulation materials for high tension products. Particularly, the composite insulators are a unique kind of insulation control that further holds a crucial role in overhead transmission lines.

Composite insulators are also known as non-porcelain insulators, synthetic insulators, rubber insulators, polymer insulators, among others. Notably, composite insulators are light in weight, minor in size, reliable to transport, light in structure, easy to maintain and easy to install. Such factors aid composite insulators to gain traction all across the markets. In addition to that, the composite insulator has excellent fouling resistance and robust fouling flash voltage resistance. Notably, the wet withstand voltage and fouling resistance voltage of composite insulators are 2 to 2.5 times that of porcelain insulators with the equal creepage distance.

Also, there is no need for cleansing and secure operation in severely polluted areas. Owing to such factors, the composite insulators are witnessing higher demand all around the world. Moreover, the soaring investments from governments and regulatory authorities to revamp the maturing grid networks across established nations together with the swift adoption of smart grid technology, worldwide, is further projected to boost the growth of the global composite insulators market in the coming years.

Wish to Know More About the Study? Click here to get a Report Description: https://reportsandinsights.com/report/composite-insulators-market

Composite Insulators Market Segmentation

The composite insulators market is segmented on the basis of voltage, application, product, rating, installation, end use, and region.

By Voltage

High Voltage

Medium Voltage

Low Voltage

By Application

Cables & Transmission Lines

Switchgears

Transformers

Bus Bars

Others

By Product

Pin Insulators

Suspension Insulators

Shackle Insulators

Other Insulators

By End Use

Residential

Commercial & Industrial

Utilities

By Rating

<11 KV

11 KV

22 KV

33 KV

5 KV

145 KV

220 KV

400 KV

800 KV

1200 KV

By Installation

Distribution

Transmission

Substation

Railways

Others

By Region

North America

Latin America

Europe

Asia Pacific

Middle East

Africa

Composite Insulators Market Key Players

Some of the key participating players in composite insulators market are:

Siemens Energy

ABB

GE

Toshiba

Aditya Birla

NGK Insulators

Hubbell

Bharat Heavy Electricals Limited

LAPP Insulators

Maclean-Fogg

Seves Group

TE Connectivity

To view Top Players, Segmentation and other Statistics of Composite Insulators Market Industry, Get Sample Report @: https://reportsandinsights.com/sample-request/2534

About Reports and Insights:

Reports and Insights is one of the leading market research companies which offers syndicate and consulting research around the globe. At Reports and Insights, we adhere to the client needs and regularly ponder to bring out more valuable and real outcomes for our customers. We are equipped with strategically enhanced group of researchers and analysts that redefines and stabilizes the business polarity in different categorical dimensions of the market.

Contact Us:

Neil Jonathan

1820 Avenue M, Brooklyn

NY 11230, United States

+1-(718) 312-8686

Find Us on LinkedIn: www.linkedin.com/company/report-and-insights/

View Latest Market Updates at: https://marketsresearchanalytics.com

#Composite Insulators Market Research#Composite Insulators Market Report#Composite Insulators Market Share 2021#Composite Insulators Market Size 2022#Composite Insulators Market Trends#Composite Insulators Market Key Players#Global Composite Insulators Market Analysis#Composite Insulators Industry News#Composite Insulators Industry Analysis#Composite Insulators Market Forecast#Composite Insulators Market CAGR#USA Composite Insulators Market#Japan Composite Insulators Market#Composite Insulators Market Demand#Argentina Composite Insulators Market#Australia Composite Insulators Market#Belgium Composite Insulators Market#Brazil Composite Insulators Market#Canada Composite Insulators Market#Chile Composite Insulators Market#China Composite Insulators Market#Columbia Composite Insulators Market#Egypt Composite Insulators Market#France Composite Insulators Market#Germany Composite Insulators Market#Global Composite Insulators Market#India Composite Insulators Market#Indonesia Composite Insulators Market#Composite Insulators Applications#Composite Insulators Industry

0 notes

Text

Durkduct Flexible Air Ducting Solution for the Automotive Industry

Durkee textile air ductwork has been applied in the automotive plant since 2008, from industry benchmarks, foreign-invested factories to domestic-owned factories, and from OEM to other automotive accessories producers. So far, all major engineering projects or benchmark enterprises in automobile manufacturing plants have chosen Durkee flexible fabric air dispersion system. Durkee has a group of famous users worldwide, such as Volkswagen, General Motors, Ford, Renault, Fiat, Tesla, Toyota, Honda, Nissan, Audi, Mercedes-Benz, FAW, SAIC, GAC, Dongfeng, and Geely, etc.

By 2015, all automobile manufacturing industry projects only used Nanosox fabric ducts as the secondary air supply duct with unique properties, such as low space position line or spot air supply for energy-saving, environmental protection, easy installation, and oil resistance, etc. Since 2016, the insulated fabric air duct, which is the unique research and development of Durkee, has been fully promoted in the market.

It has been successfully applied as the primary air supply duct system for automobile manufacturing plants, including Jiangling, General Motors, Faurecia, FAW Toyota, BAIC, Ford, Dongfeng Honda, Geely, GAC Honda, and other projects.

Advantages of insulated fabric duct

Compared with commonly used traditional GI ducts, the advantages of the insulated fabric duct are more obvious:

Lightweight, faster installation

The insulated fabric ducting solution has a 100% factory prefabrication rate and on-site modular assembly, which is light in weight, requiring only slide bars or cable suspension, with zipper connection, greatly improving the quality of the project, shortening the construction period, and reducing the overall cost of the project.

Double insulation layer increases thermal insulation performance

The insulated fabric duct is composed of duct layer, an insulation layer, and an outer insulation layer, achieving a dual-layer insulation effect.

The integral composite insulation material has an infinite vapor resistance factor, which can effectively prevent water vapor penetration, maintain the initial thermal conductivity coefficient, and have a better insulation performance. The thermal resistance value is comprehensively improved. The Durkee fabric duct can effectively reduce cold and heat loss during the air transmission process.

High strength and pressure resistance performance

Different from the easy shearing and pressure deformation of rectangular metal ducts, the insulated fabric duct system adopts circular and elliptical shapes.

The insulated fabric duct can reasonably convert internal pressure into transverse tensile force on the duct wall, which can withstand 3000Pa-5000Pa or more pressure, far higher than the applicable range of traditional ducts below 2000Pa.

The insulated fabric duct system has been successfully applied in more and more primary air supply duct systems and return air duct systems. Durkee has become the leading supplier in the global fabric duct industry with a full range of professional solutions.

1 note

·

View note

Text

The Swedish pulp producer Renewcell has just opened the world's first commercial-scale, textile-to-textile chemical recycling pulp mill, after spending 10 years developing the technology.

While mechanical textiles-to-textiles recycling, which involves the manual shredding of clothes and pulling them apart into their fibres, has existed for centuries, Renewcell is the first commercial mill to use chemical recycling, allowing it to increase quality and scale production. With ambitions to recycle the equivalent of more than 1.4 billion T-shirts every year by 2030, the new plant marks the beginning of a significant shift in the fashion industry's ability to recycle used clothing at scale.

"The linear model of fashion consumption is not sustainable," says Renewcell chief executive Patrik Lundström. "We can't deplete Earth's natural resources by pumping oil to make polyester, cut down trees to make viscose or grow cotton, and then use these fibres just once in a linear value chain ending in oceans, landfills or incinerators. We need to make fashion circular." This means limiting fashion waste and pollution while also keeping garments in use and reuse for as long as possible by developing collection schemes or technologies to turn textiles into new raw materials.

Each year, more than 100 billion items of clothing are produced globally, according to some estimates, with 65% of these ending up in landfill within 12 months. Landfill sites release equal parts carbon dioxide and methane – the latter greenhouse gas being 28 times more potent than the former over a 100-year period. The fashion industry is estimated to be responsible for 8-10% of global carbon emissions, according to the UN.

Just 1% of recycled clothes are turned back into new garments. While charity shops, textiles banks and retailer "take-back" schemes help to keep those donated clothes in wearable condition in circulation, the capabilities of recycling clothes at end-of-life are currently limited. Many high street stores with take-back schemes, including Levi Strauss and H&M, operate a three-pronged system: resell (for example, to charity shops), re-use (convert into other products, such as cleaning cloths or mops) or recycle (into carpet underlay, insulation material or mattress filling – clothing is not listed as an option).

Much of the technical difficulty in recycling worn-out clothes back into new clothing comes down to their composition. The majority of clothes in our wardrobes are made from a blend of textiles, with polyester the most widely produced fibre, accounting for a 54% share of total global fibre production, according to the global non-profit Textile Exchange. Cotton is second, with a market share of approximately 22%. The reason for polyester's prevalence is the low cost of fossil-based synthetic fibres, making them a popular choice for fast fashion brands, which prioritise price above all else – polyester costs half as much per kg as cotton. While the plastics industry has been able to break down pure polyester (PET) for decades, the blended nature of textiles has made it challenging to recycle one fibre, without degrading the other. (Read more about why clothes are so hard to recycle.)

By using 100% textile waste – mainly old T-shirts and jeans – as its feedstock, the Renewcell mill makes a biodegradable cellulose pulp they call Circulose. The textiles are first shredded and have buttons, zips and colouring removed. They then undergo both mechanical and chemical processing that helps to gently separate the tightly tangled cotton fibres from each other. What remains is pure cellulose.

6 notes

·

View notes

Text

Exploring the Future of Construction. The Rise of AAC Block Plants

In the evolving landscape of global construction, Autoclaved Aerated Concrete (AAC) blocks are emerging as a cornerstone of eco-friendly and efficient building practices. This article delves into the world of AAC block plants, exploring their significance, manufacturing process, benefits, and the impact they are set to have on future construction trends.

What are AAC Blocks?

AAC blocks are lightweight, precast concrete building materials that offer superior insulation, durability, and fire and mold resistance compared to traditional concrete and clay bricks. Made from sand, cement, lime, water, and an expanding agent like aluminum powder, these blocks are autoclaved under heat and pressure to create a cellular structure. This unique composition delivers a material that is about one-fifth the weight of normal concrete.

The Manufacturing Process at an AAC Block Plant

The production of AAC blocks is a fascinating blend of chemistry and precision engineering, and it begins with the mixing of finely ground raw materials (sand, or fly ash), cement, lime, and a small quantity of aluminum powder. This mixture is then poured into molds where it reacts to form hydrogen gas bubbles, causing it to expand. Once the desired aeration is achieved, the material is precut into blocks or panels and then autoclaved under high pressure and temperature to give it structural strength. The end product is a lightweight, robust block with excellent thermal and acoustic properties.

Key Benefits of AAC Blocks

Sustainability: AAC blocks are an environmentally friendly choice. The materials used are abundant and often sourced from industrial waste (fly ash), and the finished blocks are recyclable. Moreover, their lightweight nature reduces transportation costs and emissions.

Thermal Efficiency: These blocks provide superior thermal insulation, reducing the need for additional insulation and the overall energy required for heating and cooling, leading to significant cost savings over the building’s lifetime.

Fire Resistance: AAC blocks are fire-resistant, capable of withstanding up to 1200 degrees Celsius, and can provide fire protection for up to four hours, significantly enhancing building safety.

Pest and Mold Resistance: The inorganic material of AAC blocks does not promote mold or mildew growth and is resistant to pests, contributing to healthier indoor environments.

Ease of Installation: AAC blocks are easy to work with and can be cut to size with standard tools, speeding up the construction process and reducing labor costs.

Challenges and Considerations

While AAC blocks offer numerous advantages, there are challenges to consider:

Initial Investment: Setting up an AAC block plant requires significant initial investment in terms of machinery and technology.

Technical Skill: Producing AAC blocks requires precise control over the material mixture and autoclaving process, necessitating skilled operators.

Market Acceptance: In regions where AAC is not well-known, market penetration can be slow, requiring extensive outreach and education about its benefits.

Future Outlook

The demand for AAC blocks is projected to rise as more builders and architects become aware of their benefits. With increasing regulatory focus on sustainable construction practices, AAC block plants are poised for significant growth. Innovations in manufacturing technology and enhanced supply chains will likely further reduce costs and improve the accessibility of these materials.

In conclusion, AAC block plants represent a transformative advancement in the construction sector, offering a blend of sustainability, efficiency, and performance. As the industry continues to evolve towards greener and more cost-effective building solutions, AAC blocks are undoubtedly set to play a pivotal role in shaping the future of construction.

0 notes

Text

Exploring Innovative Window Designs: Ventona's Vision

Introduction of Ventona Windows

Ventona Windows is a prominent option on the market for adding high-quality aluminum windows to your home. Aluminum windows by Ventona are known for their svelte shapes, long lifespans, and low energy use.

Ventona Windows' dedication to using premium materials in the construction of its goods is one of the main characteristics that set it apart. Because Ventona windows are made of lightweight, sturdy, and lasting aluminum, they are also simple to install and maintain.

The sleek style of Ventona aluminum windows will appeal to those searching for chic and contemporary window solutions. These windows not only improve the look of your house but also offer superior insulation, which will ultimately result in lower energy bills.

Purchasing Ventona Windows is an investment in elegance and quality. A wonderful combination of practicality and aesthetic appeal for any house, Ventona aluminum windows may be used to modernize outdated windows or replace them with more energy-efficient models.

The Ventona Windows features

1 Workmanship and Quality: Ventona Windows is dedicated to providing exceptional quality and unwavering workmanship. Modern production processes and quality materials are used to carefully build each window, guaranteeing its lifetime and flawless function. Every aspect of Ventona Windows, from the exquisite finishes to the precisely designed frames, embodies the brand's commitment to quality, elevating them to the status of enduring beauty and refined elegance.

2 Elegance in Design: Ventona Windows' excellent design and subtle subtlety are testaments to its associated elegance. Ventona Windows are decorated with sleek aluminum frames, traditional wood accents, or modern composite materials, and they always have a certain beauty that goes beyond fads. Any space's aesthetic appeal may be effortlessly elevated with grace because of the clean lines, gentle curves, and seamless integration with architectural components that create a harmonic balance between form and function.

3 Durability and Low Care: Aluminum has a longer lifespan and requires less care than other window materials since it is resistant to rust, rot, and decay. Ventona Aluminum Windows are designed to endure inclement weather, UV rays, and temperature changes without sacrificing their structural soundness or visual attractiveness. Ventona windows are an excellent investment for homeowners looking for long-lasting value since they maintain their immaculate beauty and functioning for years to come with regular cleaning and the periodic lubricating of the hardware.

4 Versatility and Customization: Ventona Windows' flexibility to a wide range of architectural styles and design preferences is one of its distinguishing features. Ventona provides a broad choice of window types, combinations, and customization possibilities to meet any aesthetic vision, whether it's for a modern urban loft, a classic rural cottage, or a minimalist seaside hideaway. Ventona gives designers and homeowners the freedom to build rooms that express their personalities and lifestyles, with options ranging from large picture windows that frame expansive vistas to beautiful casement windows that let in mild breezes.

5 Sustainability and Environmental Responsibility: Ventona is dedicated to reducing its environmental impact and protecting the earth for coming generations in a time when sustainability is crucial. Ventona places a high priority on sustainability throughout the whole production process, from locating environmentally friendly components to putting in place energy-efficient production techniques. Homeowners who choose Ventona Windows not only improve the aesthetics and comfort of their living spaces but also make a positive impact on global health and sustainability.

In conclusion,

Ventona Windows is a great example of classic style, fine craftsmanship, and cutting-edge technology in the window design industry. Ventona Windows reinvents the art of window-making with its elegant design, excellent quality, adaptability, and dedication to sustainability, turning places into inspiration-, comfort-, and beauty-filled havens. Ventona Windows bring light, warmth, and the hope of a better tomorrow into every house, whether they are seen adorning a stately home or a cozy cottage.

0 notes

Text

Aerospace Plastics Market: Innovations, Trends, and Future Growth

The aerospace industry is one of the most technologically advanced sectors, continuously evolving to meet stringent performance, safety, and efficiency standards. Within this landscape, aerospace plastics have emerged as critical materials, offering numerous advantages over traditional materials such as metals. These high-performance plastics are lightweight, durable, and resistant to corrosion, making them indispensable in modern aerospace engineering. This article delves into the current trends, key drivers, applications, and future prospects of the aerospace plastics market.

Market Overview

The global aerospace plastics market has witnessed significant growth over recent years. As of 2023, the market size was valued at USD X billion and is projected to reach USD Y billion by 2030, growing at a CAGR of Z% during the forecast period. The increasing demand for lightweight and fuel-efficient aircraft, coupled with advancements in plastic materials, is driving this growth.

Key Drivers

1. Weight Reduction: One of the primary benefits of aerospace plastics is their ability to significantly reduce the weight of aircraft. Reduced weight translates to lower fuel consumption, which is a critical factor for both commercial and military aviation. Plastics such as polyetheretherketone (PEEK), polyphenylene sulfide (PPS), and polyimides are increasingly used to replace heavier metal components.

2. Fuel Efficiency and Emissions: The aviation industry is under constant pressure to reduce carbon emissions and improve fuel efficiency. Aerospace plastics contribute to these goals by enabling the design of more aerodynamically efficient and lighter aircraft. This not only helps in reducing greenhouse gas emissions but also lowers operational costs.

3. Durability and Resistance: Aerospace plastics offer superior resistance to chemicals, heat, and corrosion compared to traditional materials. This enhances the longevity and performance of aircraft components, leading to lower maintenance costs and increased safety.

4. Technological Advancements: Continuous R&D in polymer science has led to the development of new high-performance plastics with enhanced properties. Innovations in composite materials, additive manufacturing (3D printing), and nanotechnology are expanding the application scope of aerospace plastics.

For a comprehensive analysis of the market drivers:- https://univdatos.com/report/aerospace-plastics-market/

Applications

Aerospace plastics are used in various applications within the industry, including:

-Structural Components: Plastics are increasingly being used in primary and secondary structural components of aircraft. These include fuselage parts, wing panels, and interior cabin structures. The use of composite materials like carbon fiber-reinforced plastics (CFRP) has revolutionized aircraft design.

- Interiors: The interior of an aircraft benefits greatly from the use of plastics. Lightweight plastics are used for seating, overhead compartments, wall panels, and flooring. These materials offer excellent fire resistance, durability, and ease of cleaning.

- Insulation and Wiring: Aerospace plastics provide excellent insulation properties, making them ideal for electrical wiring and cable insulation. They ensure safety and reliability in the aircraft’s electrical systems.

- Engine Components: High-performance plastics are used in various engine components such as housings, ducts, and seals. Their ability to withstand high temperatures and harsh chemical environments makes them suitable for use in and around the engine.

Regional Insights

The aerospace plastics market is geographically diverse, with key growth regions including North America, Europe, and Asia-Pacific.

- North America: This region holds a significant share of the market due to the presence of major aircraft manufacturers like Boeing and Lockheed Martin. The focus on fuel efficiency and emission reduction drives the demand for aerospace plastics.

- Europe: Europe is a major player in the aerospace industry, with companies like Airbus leading the market. Stringent environmental regulations and advancements in composite technologies are boosting the market for aerospace plastics.

- Asia-Pacific: The Asia-Pacific region is experiencing rapid growth in the aerospace sector, driven by increasing air travel and rising defense budgets. Countries like China, India, and Japan are investing heavily in new aircraft and aerospace technologies, fueling the demand for aerospace plastics.

For a sample report, visit:- https://univdatos.com/get-a-free-sample-form-php/?product_id=37117

Future Prospects

The future of the aerospace plastics market looks promising, with several trends expected to shape its trajectory:

- Sustainable Materials: There is a growing focus on the development of sustainable and recyclable plastics. Biodegradable polymers and bio-based composites are likely to gain traction in the aerospace industry.

- Advanced Manufacturing Techniques: Innovations in manufacturing processes, such as 3D printing and automated fiber placement, will enable more efficient production of complex plastic components, reducing costs and material wastage.

- Integration of Smart Materials: The integration of smart materials with self-healing and self-sensing capabilities is an emerging trend. These advanced materials can enhance the safety and performance of aircraft.

In conclusion, the aerospace plastics market is poised for robust growth, driven by the need for lightweight, durable, and fuel-efficient materials. As the aerospace industry continues to evolve, aerospace plastics will play a crucial role in shaping the future of aviation.

Contact Us:

UnivDatos Market Insights

Email - [email protected]

Contact Number - +1 9782263411

Website -www.univdatos.com

#Aerospace Plastics Market#Aerospace Plastics Market Growth#Aerospace Plastics Market Share#Aerospace Plastics Market Forecast

0 notes

Text

Aluminium Composite Panels Market: Trends, Growth, and Future Prospects

Aluminium Composite Panels (ACPs) are gaining significant traction in the construction and renovation industries due to their versatile applications, aesthetic appeal, and functional benefits. These panels consist of two aluminium sheets bonded to a non-aluminium core, offering a combination of durability, lightweight properties, and resistance to weathering. The market for ACPs is expanding rapidly, driven by increasing urbanization, rising demand for sustainable building materials, and advancements in technology.

Market Overview

The global aluminium composite panels market has experienced substantial growth over the past decade. According to industry reports, the market size was valued at USD X billion in 2023 and is projected to reach USD Y billion by 2030, growing at a CAGR of Z% during the forecast period. This growth can be attributed to several factors, including the increasing construction activities in emerging economies, the rising focus on energy-efficient buildings, and the growing adoption of modern architectural designs.

Key Drivers

1. Urbanization and Infrastructure Development: Rapid urbanization, particularly in developing countries, is a major driver for the ACP market. As cities expand and new urban areas are developed, the demand for modern construction materials that offer both aesthetic and functional benefits is on the rise. ACPs are favored for their ability to provide a sleek, contemporary look while ensuring durability and cost-effectiveness.

2. Sustainable Building Materials: With growing environmental concerns, there is a heightened focus on sustainable building practices. Aluminium composite panels are increasingly preferred due to their recyclable nature and energy efficiency. They contribute to green building certifications and help in reducing the overall carbon footprint of structures.

3. Technological Advancements: Innovations in manufacturing processes and material technologies have significantly enhanced the performance characteristics of ACPs. Improved fire resistance, better insulation properties, and advanced surface coatings are some of the developments that have broadened the application scope of these panels.

For a comprehensive analysis of the market drivers:- https://univdatos.com/report/aluminium-composite-panels-market/

Applications

ACPs are used in a wide range of applications across various sectors:

- Exterior Cladding: One of the most common uses of ACPs is in exterior cladding or facades. They offer a modern and clean appearance, protect the building structure from weather elements, and provide insulation.

- Interior Decoration: ACPs are also popular for interior applications such as false ceilings, partitions, and wall panels. Their lightweight and flexible nature make them easy to install and maintain.

- Signage and Advertising: The durability and aesthetic appeal of ACPs make them suitable for outdoor signage and advertising boards. They can withstand harsh weather conditions and maintain their appearance over time.

- Transportation: In the transportation industry, ACPs are used for vehicle bodies and interiors, providing a lightweight yet strong solution that enhances fuel efficiency and durability.

For a sample report, visit:- https://univdatos.com/get-a-free-sample-form-php/?product_id=37129

Regional Insights

The ACP market is geographically diverse, with significant growth observed in Asia-Pacific, North America, and Europe.

- Asia-Pacific: This region dominates the market due to rapid urbanization, growing construction activities, and increasing investments in infrastructure development. Countries like China, India, and Japan are major contributors to the market growth.

- North America: The demand for ACPs in North America is driven by the need for energy-efficient buildings and the renovation of old structures. The presence of key manufacturers and technological advancements also contribute to market growth.

- Europe: In Europe, stringent regulations regarding building safety and energy efficiency are propelling the adoption of ACPs. The region's focus on sustainable construction practices further boosts market demand.

Future Prospects

The future of the aluminium composite panels market looks promising, with several trends likely to shape its trajectory:

- Green Buildings: The shift towards green building practices and sustainable construction materials will continue to drive the demand for ACPs. Manufacturers are likely to focus on developing more eco-friendly products to meet this demand.

- Innovative Designs: As architectural trends evolve, there will be a growing need for innovative and customizable ACP solutions. This will encourage manufacturers to invest in R&D and expand their product portfolios.

- Smart Cities: The development of smart cities, with their emphasis on advanced infrastructure and sustainable living, will create new opportunities for ACP applications.

In conclusion, the aluminium composite panels market is set for robust growth, driven by urbanization, sustainability trends, and technological advancements. As the construction industry continues to evolve, ACPs will play a crucial role in shaping modern architectural landscapes.

Contact Us:

UnivDatos Market Insights

Email - [email protected]

Contact Number - +1 9782263411

Website -www.univdatos.com

#Aluminium Composite Panels Market#Aluminium Composite Panels Market Growth#Aluminium Composite Panels Market Share#Aluminium Composite Panels Market Forecast

0 notes

Text

Owens Corning: Global Locations and Facilities

Owens Corning, a leader in building materials and composite solutions, operates a vast network of facilities worldwide. This article provides an extensive overview of Owens Corning's global locations, highlighting key manufacturing sites, regional offices, and research centers that drive the company's innovation and market reach.

North America

United States

Owens Corning's presence in the United States is extensive, with numerous facilities dedicated to manufacturing, research, and corporate operations.

Key Locations:

Toledo, Ohio: Headquarters and central hub for Owens Corning's corporate operations, housing executive management and key administrative functions.

Granville, Ohio: Science and Technology Center, a cornerstone for research and development activities focused on advancing insulation and composite materials.

Kansas City, Missouri: Major manufacturing site for roofing materials, serving both residential and commercial markets.

Fort Smith, Arkansas: Production facility specializing in insulation products, pivotal for energy efficiency solutions.

Canada

Owens Corning maintains a significant footprint in Canada, with facilities supporting the production of insulation and roofing materials.

Key Locations:

Toronto, Ontario: Regional office and distribution center, coordinating operations across Canada.

Candiac, Quebec: Manufacturing plant for insulation products, catering to the Canadian market's demand for energy-efficient building materials.

Europe

France

Owens Corning operates several key facilities in France, central to its European operations.

Key Locations:

Chambery: Manufacturing site for composite materials, supplying advanced solutions for various industrial applications.

Laval: Insulation production facility, crucial for meeting the energy efficiency needs of the European market.

Germany

Germany hosts important Owens Corning facilities that contribute to its European market leadership.

Key Locations:

Apeldoorn: Production plant for insulation materials, supporting the regional demand for sustainable building solutions.

Birkenfeld: Manufacturing site specializing in composite materials, serving automotive and industrial sectors.

Asia-Pacific

China

Owens Corning has established a robust presence in China, with facilities that bolster its market penetration in the Asia-Pacific region.

Key Locations:

Shanghai: Regional headquarters and innovation center, focusing on strategic growth and technological advancements.

Jiangsu: Major manufacturing site for composite materials, supporting the construction and automotive industries.

India

India is a growing market for Owens Corning, with facilities aimed at expanding its footprint in the region.

Key Locations:

Taloja, Maharashtra: Production plant for insulation and roofing materials, addressing the needs of the Indian construction market.

Latin America

Brazil

Owens Corning's operations in Brazil are essential for serving the Latin American market.

Key Locations:

Rio Claro: Manufacturing facility for insulation products, catering to regional demand for energy-efficient building solutions.

São Paulo: Regional office, coordinating operations and strategic initiatives across Latin America.

Middle East and Africa

Saudi Arabia

In the Middle East, Owens Corning focuses on addressing the region's unique building and industrial requirements.

Key Locations:

Dammam: Manufacturing site for composite materials, crucial for infrastructure projects and industrial applications in the region.

South Africa

Owens Corning's presence in Africa is marked by key facilities supporting regional growth.

Key Locations:

Johannesburg: Regional office and distribution center, managing operations and logistics across the African continent.

Research and Innovation Centers

Owens Corning places a strong emphasis on research and innovation, with dedicated centers worldwide.

Granville, Ohio, USA

The Science and Technology Center in Granville is a pivotal site for Owens Corning's research and development efforts. It focuses on advancing materials science and developing innovative solutions for insulation, roofing, and composites.

Shanghai, China

The Innovation Center in Shanghai is instrumental in driving technological advancements and product development tailored to the Asia-Pacific market. It fosters collaboration with local industries and academic institutions.

Conclusion

Owens Corning's extensive network of global locations underscores its commitment to innovation, sustainability, and market leadership. By strategically positioning its facilities worldwide, the company ensures efficient production, distribution, and customer service, meeting the diverse needs of its global clientele.

0 notes

Text

Polyimide Prices Trend, Database, Index, News, Chart, Forecast

Polyimide prices have been subject to fluctuations in recent years due to various factors impacting the supply chain and market dynamics. Polyimides are high-performance polymers known for their exceptional thermal stability, mechanical strength, and chemical resistance, making them indispensable in industries such as electronics, aerospace, automotive, and healthcare. The cost of polyimides is influenced by several key factors, including raw material prices, manufacturing processes, demand-supply dynamics, and technological advancements.

One significant factor affecting polyimide prices is the cost of raw materials. Polyimides are typically derived from aromatic dianhydrides and aromatic diamines, which are themselves derived from petroleum or other chemical feedstocks. Fluctuations in crude oil prices, geopolitical tensions, and supply chain disruptions can all impact the cost of these raw materials, thereby affecting the overall price of polyimides. Additionally, the availability of raw materials can be influenced by factors such as natural disasters, regulatory changes, and shifts in global trade patterns, further contributing to price volatility.

Get Real Time Prices of Polyimide: https://www.chemanalyst.com/Pricing-data/polyimide-1579

Manufacturing processes also play a crucial role in determining polyimide prices. The production of polyimides involves several complex steps, including polymerization, curing, and post-treatment processes. Energy costs, labor expenses, and capital investments required for equipment and infrastructure all factor into the manufacturing cost of polyimides. Innovations in process efficiency, automation, and recycling technologies can help manufacturers optimize their operations and reduce production costs, ultimately influencing the market price of polyimides.

Demand-supply dynamics significantly impact polyimide prices, as these polymers are used in a wide range of high-performance applications. Rapid industrialization, urbanization, and technological advancements drive demand for polyimides in sectors such as electronics (e.g., flexible printed circuits, display films), aerospace (e.g., lightweight composites, thermal insulation), automotive (e.g., engine components, electrical insulation), and healthcare (e.g., medical devices, implants). Fluctuations in end-user demand, market trends, and competitive dynamics can lead to shifts in supply and demand equilibrium, thereby affecting polyimide prices.

Technological advancements and innovation also influence polyimide prices by enabling the development of new grades, formulations, and applications. Research and development efforts focused on enhancing the performance, durability, and sustainability of polyimides can lead to the introduction of advanced materials with superior properties. However, the adoption of novel technologies and materials may initially entail higher production costs, which can impact the pricing of these innovative polyimide products. Over time, economies of scale, process optimization, and market acceptance can help mitigate these cost implications.

In conclusion, polyimide prices are subject to various factors, including raw material prices, manufacturing processes, demand-supply dynamics, and technological advancements. Fluctuations in crude oil prices, manufacturing costs, end-user demand, and innovation all contribute to the volatility and pricing trends observed in the polyimide market. As industries continue to evolve and demand for high-performance materials grows, stakeholders across the value chain must closely monitor these factors to make informed decisions and navigate the complexities of the polyimide market.

Get Real Time Prices of Polyimide: https://www.chemanalyst.com/Pricing-data/polyimide-1579

Contact Us:

ChemAnalyst

GmbH - S-01, 2.floor, Subbelrather Straße,

15a Cologne, 50823, Germany

Call: +49-221-6505-8833

Email: [email protected]

Website: https://www.chemanalyst.com

0 notes

Text

Global Acoustic Insulation Market: Size, Share, and Industry Growth Analysis Report (2032 Forecast)

Global Acoustic Insulation market is predicted to reach approximately USD 23.50 billion by 2032, at a CAGR of 5.55% from 2024 to 2032.

Acoustic insulation refers to the process of reducing sound transmission between spaces or isolating sound within a specific area to enhance comfort, privacy, and safety. This market encompasses products such as fiberglass, mineral wool, foam plastics, and others, which are utilized in construction, automotive, industrial, and residential sectors. The demand for acoustic insulation has surged due to increasing urbanization, industrialization, and stringent noise regulations across the globe. Growing awareness regarding the adverse effects of noise pollution on human health and well-being has further propelled the adoption of acoustic insulation solutions.

Request For Sample Report https://www.econmarketresearch.com/request-sample/EMR00656/

Market Dynamics Redefined:

Market Dynamics of the Acoustic Insulation Market

Market Drivers:

Growing Construction Industry: The rapid expansion of the construction industry, particularly in emerging economies, is driving the demand for acoustic insulation materials to meet building codes and regulations.

Stringent Environmental Regulations: Increasing government regulations and policies aimed at reducing noise pollution in residential, commercial, and industrial areas are boosting the adoption of acoustic insulation.

Technological Advancements: Continuous advancements in insulation technologies and materials are enhancing the effectiveness of acoustic insulation, making it more attractive to end-users.

Rising Awareness of Health and Comfort: Growing awareness about the health impacts of noise pollution and the need for comfortable living and working environments are leading to higher demand for acoustic insulation solutions.

Energy Efficiency Trends: The drive towards energy-efficient buildings is also contributing to market growth, as acoustic insulation materials often provide thermal insulation benefits as well.

Market Restraints:

High Installation Costs: The high initial costs associated with the installation of acoustic insulation materials can deter some potential customers, particularly in cost-sensitive markets.

Economic Uncertainties: Economic fluctuations and uncertainties can impact the construction industry and, in turn, the demand for acoustic insulation materials.

Lack of Awareness in Developing Regions: In certain developing regions, there is a lack of awareness and understanding of the benefits of acoustic insulation, which can limit market growth.

Competition from Alternative Solutions: The availability of alternative noise reduction solutions, such as noise-cancelling devices, can pose a challenge to the growth of the acoustic insulation market.

Complex Retrofitting Processes: Retrofitting existing buildings with acoustic insulation can be complex and costly, which can be a deterrent for building owners and developers.

Key players 3M, Armacell, BASF SE, Cabot Corporation, Cellecta, CSR Limited, Dow, Dynamic composite technologies, Fletcher Insulation, Insultech LLC, Johns Manville, Kingspan Group, Knauf Insulation, L'ISOLANTE K-FLEX S.p.A., Owens Corning, Recticel Insulation, ROCKWOOL A/S, Saint-Gobain, Siderise, and Trelleborg.

Frequently Asked Questions(FAQs):

What is the expected global Acoustic Insulation growth rate during the forecast period?

According to global Acoustic Insulation research, the market is expected to grow at a CAGR of ~ 5.55% over the next eight years.

Driving Factors for the Acoustic Insulation Market

Expansion of the Construction Industry:

The rapid growth of the construction industry, particularly in emerging economies, is significantly driving the demand for acoustic insulation materials. New residential, commercial, and industrial projects often require effective noise control solutions to comply with building codes and enhance occupant comfort.

Stringent Environmental and Building Regulations:

Increasing government regulations and policies aimed at reducing noise pollution are propelling the adoption of acoustic insulation. Standards and codes that mandate noise reduction in buildings and industrial facilities are a major driver for the market.

Technological Advancements:

Continuous innovations in insulation technologies and materials are making acoustic insulation more efficient and cost-effective. Advances such as the development of lightweight and high-performance materials are enhancing the appeal of acoustic insulation solutions.

Growing Awareness of Health and Comfort:

There is a rising awareness about the adverse health effects of noise pollution, including stress, hearing loss, and sleep disturbances. This awareness is driving the demand for acoustic insulation to create quieter and more comfortable living and working environments.

Energy Efficiency and Sustainability Trends:

Acoustic insulation materials often provide thermal insulation benefits as well, contributing to energy efficiency. The growing focus on sustainable building practices and energy-efficient buildings is boosting the demand for materials that offer both acoustic and thermal insulation properties.

Urbanization and Infrastructure Development:

Increasing urbanization and infrastructure development are leading to higher noise levels in urban areas. The need to mitigate noise pollution in densely populated and developed regions is driving the demand for acoustic insulation solutions in both new constructions and retrofitting projects.

Growth in Industrial and Manufacturing Sectors:

The expansion of industrial and manufacturing activities, which often generate high levels of noise, is creating a substantial demand for acoustic insulation to protect workers and comply with occupational safety regulations.

Consumer Preference for Enhanced Acoustic Environments:

Consumers are increasingly prioritizing acoustically optimized environments in residential, hospitality, and commercial spaces. This trend is driving developers and builders to incorporate advanced acoustic insulation solutions to meet market demands.

Objectives of the Study

The objectives of the study are summarized in 5 stages. They are as mentioned below:

Global Acoustic Insulation size and forecast: To identify and estimate the market size for global Acoustic Insulation market segmented by Type, By End-Use, and by region. Also, to understand the consumption/ demand created by consumers between 2024 and 2032.

Market Landscape and Trends: To identify and infer the drivers, restraints, opportunities, and challenges for global Acoustic Insulation

Market Influencing Factors: To find out the factors which are affecting the market of global Acoustic Insulation among consumers.

Company Profiling: To provide a detailed insight into the major companies operating in the market. The profiling will include the financial health of the company's past 2-3 years with segmental and regional revenue breakup, product offering, recent developments, SWOT analysis, and key strategies.

Email: [email protected] Website: https://www.econmarketresearch.com/

#Acoustic Insulation#Acoustic Insulation CAGR#Acoustic Insulation Competitive Analysis#Acoustic Insulation Market#Acoustic Insulation market analysis#Demand Acoustic Insulation Market#Forecast Acoustic Insulation Market Growth#Acoustic Insulation Market Manufacture#Acoustic Insulation Market price#Acoustic Insulation Market Share#Acoustic Insulation market size#Acoustic Insulation Market Trends#Acoustic Insulation Value Chain Analysis

1 note

·

View note

Text

2032, Expanded Polystyrene (EPS) Recycling Market Growth and Research 2024-2032

The Reports and Insights, a leading market research company, has recently releases report titled “Expanded Polystyrene (EPS) Recycling Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2024-2032.” The study provides a detailed analysis of the industry, including the global Expanded Polystyrene (EPS) Recycling Market Size share, trends, and growth forecasts. The report also includes competitor and regional analysis and highlights the latest advancements in the market.

Report Highlights:

How big is the Expanded Polystyrene (EPS) Recycling Market?

The expanded polystyrene (EPS) recycling market size reached US$ 19.7 Billion in 2023. Looking forward, Reports and Insights expects the market to reach US$ 36.5 Billion by 2032, exhibiting a growth rate (CAGR) of 6.7% during 2024-2032.

What are Expanded Polystyrene (EPS) Recycling?

EPS recycling is the practice of collecting, sorting, and processing EPS foam products to reclaim the material for reuse. EPS, also known as Styrofoam, is a lightweight and rigid plastic material utilized in packaging and insulation. The recycling process involves compressing the foam to reduce its size and then melting it down to create dense blocks or pellets suitable for manufacturing new products. EPS recycling contributes to environmental sustainability by diverting EPS waste from landfills and reducing the demand for new plastic production.

Request for a sample copy with detail analysis: https://www.reportsandinsights.com/sample-request/1775

What are the growth prospects and trends in the Expanded Polystyrene (EPS) Recycling industry?

The expanded polystyrene (EPS) recycling market growth is driven by various factors. The market for recycling expanded polystyrene (EPS) is expanding, fueled by growing environmental consciousness and regulatory measures promoting recycling practices. EPS, widely utilized in packaging and construction, significantly contributes to plastic waste. Recycling EPS involves collecting, cleaning, and processing it into reusable material for diverse applications. Market growth is propelled by increasing demand for recycled EPS in the construction and packaging sectors, driven by sustainability objectives and economic advantages. Moreover, technological advancements in EPS recycling and government support for recycling initiatives are further driving market growth. Hence, all these factors contribute to expanded polystyrene (EPS) recycling market growth.

What is included in market segmentation?

The report has segmented the market into the following categories:

By EPS Waste Type:

Post-consumer EPS waste

Pre-consumer EPS waste

By EPS Recycling Process:

Mechanical recycling

Chemical recycling

Other recycling processes

By End-Use Industry:

Packaging

Construction

Electrical and Electronics

Automotive

Others

By Recycled EPS Product:

Packaging materials

Insulation boards

Molded products

Composite materials

Others

By Source of Collection:

Municipal recycling programs

Industrial and commercial collection

Retail collection

Other

By Recycling Equipment:

Shredders

Granulators

Densifiers

Extruders

Others

By Application:

Packaging

Building and construction

Insulation

Consumer goods

Others

By Distribution Channel:

Direct sales

Distributor sales

E-commerce

By Market Type:

Business to Business (B2B)

Business to Consumer (B2C)

Segmentation By Region:

North America:

United States

Canad

Europe:

Germany

United Kingdom

France

Italy

Spain

Russia

Poland

BENELUX

NORDIC

Rest of Europe

Asia Pacific:

China

Japan

India

South Korea

ASEAN

Australia & New Zealand

Rest of Asia Pacific

Latin America:

Brazil

Mexico

Argentina

Middle East & Africa:

Saudi Arabia

South Africa

United Arab Emirates

Israel

Rest of MEA

Who are the key players operating in the industry?

The report covers the major market players including:

Dart Container Corporation

NOVA Chemicals Corporation

ACH Foam Technologies, LLC

Ravago Recycling Group

Styro Recycle LLC

Total, Petrochemicals & Refining USA, Inc.

Alpek Polyester

Repsol S.A.

Vanden Recycling

Plasti-Fab Ltd.

NexKemia Petrochemicals Inc.

EPS Industry Alliance

Vita Group

FPC Foam Plastics Corporation

Winco Foam Industries Limited

View Full Report: https://www.reportsandinsights.com/report/Expanded Polystyrene (EPS) Recycling-market

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

Reports and Insights consistently mееt international benchmarks in the market research industry and maintain a kееn focus on providing only the highest quality of reports and analysis outlooks across markets, industries, domains, sectors, and verticals. We have bееn catering to varying market nееds and do not compromise on quality and research efforts in our objective to deliver only the very best to our clients globally.

Our offerings include comprehensive market intelligence in the form of research reports, production cost reports, feasibility studies, and consulting services. Our team, which includes experienced researchers and analysts from various industries, is dedicated to providing high-quality data and insights to our clientele, ranging from small and medium businesses to Fortune 1000 corporations.

Contact Us:

Reports and Insights Business Research Pvt. Ltd.

1820 Avenue M, Brooklyn, NY, 11230, United States

Contact No: +1-(347)-748-1518

Email: [email protected]

Website: https://www.reportsandinsights.com/

Follow us on LinkedIn: https://www.linkedin.com/company/report-and-insights/

Follow us on twitter: https://twitter.com/ReportsandInsi1

#Expanded Polystyrene (EPS) Recycling Market share#Expanded Polystyrene (EPS) Recycling Market size#Expanded Polystyrene (EPS) Recycling Market trends

0 notes

Text

Commercial Space Ventures Fuel Demand in Aerospace Tapes Market

The surge in commercial space activities, including satellite launches and mega-constellations are the factors driving market in the forecast period 2025-2029.

According to TechSci Research report, “Aerospace Tapes Market – Global Industry Size, Share, Trends, Competition Forecast & Opportunities, 2029”, The Global Aerospace Tapes Market stood at USD 5.48 Billion in 2023 and is anticipated to grow with a CAGR of 7.44% in the forecast period, 2025-2029.

The Global Aerospace Tapes Market is experiencing robust growth, driven by the dynamic landscape of the aerospace industry. The increasing demand for air travel, coupled with the expansion of commercial and military aviation fleets, has fueled the need for advanced materials and technologies, including aerospace tapes. These tapes are instrumental in providing critical functionalities such as bonding, sealing, and protection of surfaces in diverse aerospace applications.

A significant factor propelling the market is the relentless pursuit of lightweight solutions within the aerospace sector. As the industry strives to enhance fuel efficiency and overall performance, aerospace tapes play a pivotal role in achieving these objectives. Manufacturers are continually exploring innovative materials and adhesive technologies to develop tapes that are not only lightweight but also offer exceptional strength and resilience under the demanding conditions experienced during flight.

Material advancements are a key highlight of the aerospace tapes market. The transition towards high-performance materials, including advanced polymers and composites, has been notable. These materials contribute to the tapes' ability to withstand extreme temperatures, resist corrosion, and ensure longevity in the aerospace environment. The adaptability of aerospace tapes to diverse surfaces and their compatibility with other aerospace materials make them indispensable components in the manufacturing and maintenance processes of aircraft and spacecraft.

The application areas of aerospace tapes are diverse and critical. They are extensively used in structural bonding, interior installations, electrical insulation, and protection against environmental elements. The aerospace industry's commitment to stringent regulatory standards further accentuates the importance of high-quality tapes to ensure the safety and reliability of aerospace components.

In conclusion, the Global Aerospace Tapes Market is characterized by a confluence of factors, including the industry's drive for lightweight solutions, continuous material advancements, and the essential role these tapes play in critical aerospace applications. As the aerospace sector continues to evolve, the market for aerospace tapes is expected to witness sustained growth, with ongoing innovations shaping the future of this integral segment within the aerospace industry.

Browse over market data Figures spread through 180 Pages and an in-depth TOC on " Global Aerospace Tapes Market.”

https://www.techsciresearch.com/report/aerospace-tapes-market/22649.html

North America holds a prominent position in the Global Aerospace Tapes Market, with the United States at the forefront. The region boasts a robust aerospace industry, home to major manufacturers and suppliers. North America's dominance is driven by a strong focus on research and development, technological innovation, and a high rate of aircraft production. The aerospace tapes market in North America benefits from a well-established infrastructure and a constant drive for efficiency and safety in aviation.

Europe plays a significant role in the aerospace industry, with countries like the United Kingdom, Germany, and France leading the way. The European aerospace sector emphasizes innovation and sustainability, influencing trends in aerospace tapes. The region is characterized by stringent environmental standards and a commitment to adopting advanced materials. Europe's aerospace tapes market reflects these priorities, with a focus on efficiency, safety, and reducing the industry's environmental footprint.

The Asia-Pacific region, particularly China and India, has become a key player in the aerospace industry. The growing demand for air travel, rising disposable incomes, and the establishment of new airlines contribute to the region's influence on the aerospace tapes market. Asia-Pacific experiences trends such as the adoption of lightweight materials, technology transfer agreements, and collaborations with global aerospace companies. The region's rapid growth in aviation infrastructure and manufacturing capabilities positions it as a vital contributor to the global aerospace tapes market.

The Middle East, notably the Gulf countries, has been making significant investments in aerospace and aviation infrastructure. This region is home to major airlines and hosts important events like airshows. The aerospace tapes market in the Middle East and Africa experiences growth driven by expanding aviation fleets, construction of new airports, and the need for tapes designed to withstand the unique challenges posed by hot and arid climates.

Major companies operating in Global Aerospace Tapes Market are:

3M Company

Advance Tapes International

Avery Dennison Corporation

Berry Global Group, Inc.

Compagnie De Saint-Gobain

DeWAL Industries, Inc.

Intertape Polymer Group

Nitto Denko Corporation

Download Free Sample Report

https://www.techsciresearch.com/sample-report.aspx?cid=22649

Customers can also request 10% free customization in this report.

“The Global Aerospace Tapes Market, driven by a persistent demand for lightweight, high-performance materials in aviation. The emphasis on technological advancements, especially in adhesive formulations, aligns with the industry's pursuit of enhanced safety and efficiency. Regional variations in market dynamics underscore the importance of adapting aerospace tapes to diverse environmental conditions and regulatory standards worldwide,” said Mr. Karan Chichi, Research Director with TechSci Research, a research-based management consulting firm.

“Aerospace Tapes Market – Global Industry Size, Share, Trends Opportunity, and Forecast, Segmented By Category (Specialty, Masking), By Resin Type (Acrylic, Rubber, Silicone, Others), By Backing Material (Paper Tissue, Film, Foam, Others), By Region, Competition, 2019-2029”, has evaluated the future growth potential of Global Aerospace Tapes Market and provides statistics & information on market size, structure, and future market growth. The report intends to provide cutting-edge market intelligence and help decision makers take sound investment decisions. Besides, the report also identifies and analyzes the emerging trends along with essential drivers, challenges, and opportunities in Global Aerospace Tapes Market.

Browse Related Research

Aircraft Empennage Market

https://www.techsciresearch.com/report/aircraft-empennage-market/12912.html

Military Truck Market

https://www.techsciresearch.com/report/military-truck-market/12880.html

Global Aircraft Evacuation Slide Market

https://www.techsciresearch.com/report/aircraft-evacuation-slide-market/8020.html

Contact

Techsci Research LLC

420 Lexington Avenue, Suite 300,

New York, United States- 10170

M: +13322586602

Email: [email protected]

Website: www.techsciresearch.com

#Aerospace Tapes Market#Aerospace Tapes Market Size#Aerospace Tapes Market Share#Aerospace Tapes Market Trends#Aerospace Tapes Market Growth

0 notes

Text

Unveiling the Hidden Treasure: How Scrap Metals Can Turn into Profit

In a world driven by innovation and sustainability, the concept of turning trash into treasure has gained significant traction. Among the myriad materials ripe for recycling, scrap metals stand out as a particularly lucrative and environmentally friendly option.

Contrary to their name, scrap metals in Melbourne hold immense value, both in terms of economic return and ecological conservation. In this article, we delve into the fascinating realm of scrap metal recycling, exploring how these discarded materials can be transformed into profitable assets.

The Economic and Environmental Imperative

The burgeoning demand for raw materials, coupled with finite natural resources, has underscored the importance of recycling. Scrap metal recycling not only mitigates the strain on primary resources but also offers substantial economic benefits.

By diverting metals from landfills and reintroducing them into the production cycle, recycling reduces the need for costly extraction processes. This, in turn, conserves energy and mitigates greenhouse gas emissions associated with mining and refining operations.

The Diversity of Scrap Metals

Scrap metals encompass a wide array of materials, ranging from ferrous to non-ferrous metals. Ferrous metals, such as steel and iron, are abundant in everyday items like automobiles, appliances, and structural components.

On the other hand, non-ferrous metals, including copper, aluminium, and brass, are prized for their high conductivity, corrosion resistance, and malleability. Each category presents unique opportunities for recycling, with specialised techniques tailored to extract maximum value from the diverse range of materials.

The Recycling Process Unveiled

The journey from scrap metal to profit begins with collection and sorting. Scrap yards serve as the first point of contact, where discarded materials are gathered and categorised based on their composition and quality.

Advanced technologies, including electromagnetic separators and eddy current systems, aid in the segregation of ferrous and non-ferrous metals, streamlining the recycling process.

Once sorted, the metals undergo processing, which typically involves shredding, shearing, or melting, depending on their form and intended application. Shredding transforms bulky objects like cars into manageable pieces, while shearing is employed for smaller items such as appliances.

Melting, a fundamental step in recycling, enables the metals to be cast into new shapes or alloys, ready for use in various industries ranging from construction to electronics.

The Value Proposition: Turning Scrap into Gold

While the recycling process incurs costs associated with collection, transportation, and processing, the returns far outweigh the initial investment.

Scrap metal prices fluctuate in response to market dynamics, influenced by factors such as global demand, supply chain disruptions, and currency fluctuations. Despite this volatility, recycling offers a stable source of revenue, insulated from the cyclical nature of primary metal markets.

Moreover, the environmental benefits associated with scrap metal recycling translate into tangible value for businesses seeking to enhance their sustainability credentials.

By incorporating recycled metals into their supply chains, companies can reduce their carbon footprint and demonstrate a commitment to responsible resource management, resonating with environmentally conscious consumers and stakeholders.

Navigating Challenges and Seizing Opportunities

While the prospects for scrap metal recycling are promising, the industry is not without its challenges. Market volatility, regulatory constraints, and technological barriers pose significant hurdles for recyclers and manufacturers alike.

However, these obstacles also present opportunities for innovation and collaboration, driving the development of new recycling technologies and sustainable business models.

By harnessing the power of data analytics, artificial intelligence, and automation, recyclers can optimise their operations and enhance efficiency throughout the value chain. Collaborative initiatives between industry stakeholders, policymakers, and research institutions are essential for fostering a conducive environment for sustainable recycling practices.

Conclusion

The transformation of scrap metals Melbourne into profit epitomises the symbiotic relationship between economic prosperity and environmental stewardship. By harnessing the latent value of discarded materials, recyclers contribute to resource conservation, energy savings, and greenhouse gas reduction, paving the way for a more sustainable future.

As the world embraces the circular economy paradigm, scrap metals emerge as a hidden treasure waiting to be unearthed, offering boundless opportunities for innovation, prosperity, and sustainability.

#Scrap Metals Melbourne#Best Scrap Metals Melbourne#Scrap Metal Melbourne#Scrap Metal Recycling in Melbourne

1 note

·

View note

Text

Autoclaved Aerated Concrete (AAC) Market 2024 Current Status and Challenges with Future Opportunities to 2031

The global construction industry stands on the brink of a transformative era, driven by unprecedented industrialization, urbanization, and a steadfast commitment to sustainability. Amidst this landscape of change, autoclaved aerated concrete (AAC) emerges as a beacon of innovation, offering a solution that bridges the gap between construction demands and environmental responsibility.

For more information: https://www.fairfieldmarketresearch.com/report/autoclaved-aerated-concrete-aac-market

Rising Demand for Sustainable Solutions

The ascent of green building technologies has spurred a surge in demand for lightweight, eco-friendly construction materials, propelling the growth of the autoclaved aerated concrete market. With a steadfast focus on affordability and sustainability, AAC has become a cornerstone of modern construction projects, catering to the escalating need for sound-proof, energy-efficient structures worldwide.

Meeting Global Sustainability Targets

In an era where environmental consciousness is paramount, AAC stands as a testament to the industry's commitment to sustainable development. As per the World Green Building Trends 2018 report, a significant percentage of firms are embracing green certifications for their projects, fueling the momentum behind AAC adoption. Its unique flexibility and efficiency in construction methods not only save time and labor but also mitigate environmental impact, making AAC a preferred choice for builders and developers alike.

Evolving Landscape of Sustainable Building Materials

The construction industry, historically reliant on finite natural resources, is undergoing a profound transformation towards sustainability. With concrete manufacturing alone responsible for a staggering amount of CO2 emissions, the imperative for greener alternatives has never been clearer. AAC emerges as a frontrunner in this paradigm shift, offering superior insulation, fire resistance, and eco-friendliness, thereby reshaping the future of construction.

Driving Demand Through Innovation

Innovation lies at the heart of AAC's success story, with industry players continually investing in research and development to meet evolving regulatory standards and consumer preferences. As new environmental regulations set higher benchmarks for energy efficiency, AAC's lightweight composition and long-term sustainability position it as a frontrunner in the quest for greener construction solutions.

A Sustainable Future with AAC

As the global population burgeons, so too does the demand for robust infrastructure and sustainable housing solutions. AAC, with its unparalleled attributes and environmental credentials, is poised to play a pivotal role in shaping the future of construction. From residential complexes to commercial developments, AAC's versatility and resilience make it the material of choice for builders and developers worldwide.

Key Players Driving Innovation

Prominent players in the global autoclaved aerated concrete market, including H+H UK Ltd, Hebel, Mannok Holdings, and Xella Group, are at the forefront of this transformative journey. Through cutting-edge technology and a steadfast commitment to sustainability, these industry leaders are driving the adoption of AAC and paving the way for a greener, more sustainable future.

0 notes

Text

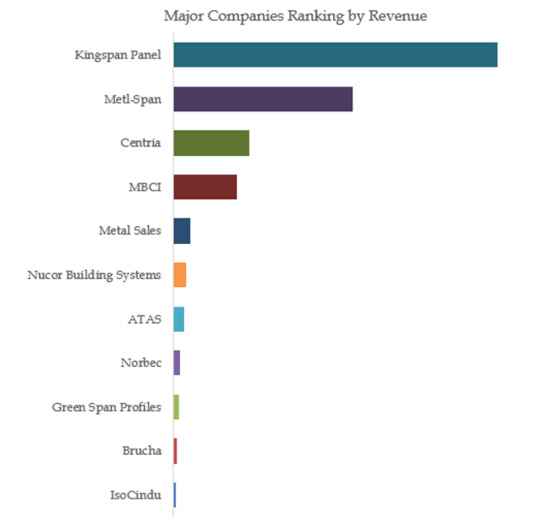

Global Top 5 Companies Accounted for 77% of total Insulated Metal Panels market (QYResearch, 2021)

Insulated Metal Panels (IMPs) are lightweight composite exterior wall and roof panels with metal skins and an insulating foam core. These panels have superior insulating properties and their outstanding spanning capabilities and one-pass installation makes them quick to install, saving costs compared to other wall assemblies. IMPs are available in a wide variety of colors, widths, profiles and finishes, enabling virtually any aesthetic desired for walls and roofs.

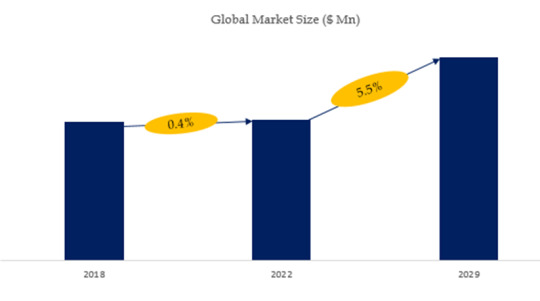

According to the new market research report “Global Insulated Metal Panels Market Report 2023-2029”, published by QYResearch, the global Insulated Metal Panels market size is projected to reach USD 1.65 billion by 2029, at a CAGR of 5.5% during the forecast period.

Figure. Global Insulated Metal Panels Market Size (US$ Million), 2018-2029

Figure. Global Insulated Metal Panels Top 5 Players Ranking and Market Share(Based on data of 2021, Continually updated)

Based on or includes research from QYResearch: 2021 data information of Global Insulated Metal Panels Market Report 2023-2029.

The global key manufacturers of Insulated Metal Panels include Kingspan Panel, Metl-Span, Centria, MBCI, Metal Sales, Nucor Building Systems, ATAS, Norbec, Green Span Profiles, Brucha, etc. In 2021, the global top five players had a share approximately 77.0% in terms of revenue.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 16 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting, industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

For more information, please contact the following e-mail address:

Email: [email protected]

Website: https://www.qyresearch.com

0 notes

Text

Magnesium Oxide Market Growth: Exploring Key Factors

The Essential Properties and Applications of Magnesium Oxide

Introduction

Magnesium oxide, commonly known as magnesia, is a white hygroscopic solid mineral that occurs naturally as periclase and is a source of magnesium. It has a chemical formula of MgO and has significant commercial uses due to its unique physical and chemical properties.

Chemical Properties

Magnesia is an ionic compound consisting of magnesium cations (Mg2+) and

oxide anions (O2-). It has a cubic crystal structure and each magnesium ion is surrounded by six oxide ions and vice versa. This results in a very stable crystalline structure that imparts useful properties to magnesia.

It is thermally stable up to about 2,800°C as it requires considerable energy for the magnesium and oxygen to separate into their elemental forms. Due to ionic bonding, it is an electrical insulator with high melting point of 2,852°C. Magnesium oxide is also highly refractory due to its ionic lattice structure and thermal stability.

Physical Properties

Magnesium oxide is a white crystalline solid that exists in nature as periclase. Its theoretical density is 3.58 g/cm3 and it has a Mohs hardness of 5.5-6 on the hardness scale. It has a relatively high bulk density of around 2.4-3.0 g/cm3 which depends upon factors like grain size, impurities and production method.

Due to its ionic character, it is highly stable and is hydroscopic in nature. Exposure to water results in hydration to magnesium hydroxide. Its significant solubility in acids allows it to be used as an antacid. Magnesia also has a high refractive index in the range of 1.728 - 1.738 and is optically isotropic.

Commercial Production

Naturally occurring magnesia is obtained by mining as periclase crystals mainly from serpentine ore deposits. Globally important areas include Cyprus, Kazakhstan and Serbia. However, magnesite (MgCO3) deposits are a more important commercial source for magnesium compounds.

The two main industrial processes for its production are calcination of naturally occurring magnesium hydroxide/carbonate minerals and thermal decomposition of magnesium hydroxide precipitates. Sea water is another feedstock that is concentrated for magnesium extraction.

The ore is calcined at high temperatures ranging from 1,000-2,000°C depending on composition and purity requirements. Calcination decomposes the mineral into magnesium oxide and releases carbon dioxide or water. The calcined product is then crushed and screened to obtain commercially useful magnesia powder.