#High Performance Fibers Market 2030

Text

High Performance Fibers Market Segmented On The Basis Of Product, Application, Region And Forecast 2030: Grand View Research Inc.

High Performance Fibers Market Segmented On The Basis Of Product, Application, Region And Forecast 2030: Grand View Research Inc.

San Francisco, 24 Nov 2022: The Report High Performance Fibers Market Size, Share & Trends Analysis Report By Product (PBI, Carbon, Aramid), By Application (Aerospace & Defense, Construction & Building), By Region, And Segment Forecasts, 2022 – 2030

The global high performance fibers market size is expected to reach USD 25.32 billion by 2030, according to a new report by Grand View Research,…

View On WordPress

#High Performance Fibers Industry#High Performance Fibers Market#High Performance Fibers Market 2030#High Performance Fibers Market Revenue#High Performance Fibers Market Share#High Performance Fibers Market Size

0 notes

Text

Electric Vehicle Plastics Market: An In-Depth Exploration and its Contribution to a Circular Automotive Industry

The global electric vehicle plastics market size was estimated at USD 13.33 billion in 2030 and is anticipated to grow at a compound annual growth rate (CAGR) of 28.0% from 2024 to 2030. The industry is projected to witness significant growth in terms of consumption, on account of high application scope and increasing demand from the growing population. The Polypropylene (PP) resin demand in the Asia Pacific region is estimated to grow at the fastest CAGR over the forecast period. Strong government support & initiatives regarding emissions and increasing investment by manufacturers are propelling the growth of the region.

Electric Vehicle Plastics Market Report Highlights

The Asia Pacific region is estimated to grow at the fastest CAGR from 2022 to 2030. Increasing demand from the growing population coupled with environmental concerns among others are anticipated to drive market growth in the region

The battery segment is anticipated to register the fastest CAGR from 2022 to 2030. Batteries are one of the significant components of an EV and, in comparison to combustion engines, battery vehicles do not produce any emissions and are eco-friendly. The growing demand for EVs has promising growth for EV batteries

The exterior application segment accounted for the largest revenue share in 2021 and is estimated to continue its dominance over the forecast period due to the high demand in aesthetics

The BEV vehicle type segment led the industry in 2021 and it is anticipated to continue growing over the forecast period as PHEVs have higher maintenance costs than BEVs

For More Details or Sample Copy please visit link @: Electric Vehicle Plastics Market Report

Furthermore, EVs are efficient and require less maintenance as compared with traditional vehicles. These factors are expected to boost the demand for EVs, which is expected to drive the demand for plastics over the forecast period. Increasing utilization of plastics in EVs is anticipated to boost industry growth positively over the forecast period. Plastics have proven to perform well under harsh conditions through their resistance to shock, moisture, oxidation, and further maintaining their chemical and mechanical properties. Plastics will be crucial material for manufacturing lightweight and energy-efficient EVs. Based on resin type, PP is expected to witness major demand during the projected years.

Polypropylene is used in many components of the vehicle including bumpers, carpet fibers, cable insulation, and others. Properties, such as good heat, chemical & fatigue resistance, and others, are anticipated to drive the demand for PP in the industry. Major manufacturers are adopting expansion strategies, such as new product development, production facility expansions, mergers & acquisitions, and joint ventures. For instance, in October 2021, DuPont launched a new extension of its existing Zytel HTN range, named as Zytel 500 series. These products are developed to provide enhanced retention properties in e-mobility oils, electrically friendly characteristics, and a high Comparative Tracking Index (CTI).

EVPlastics #ElectricVehicles #SustainableDriving #EcoFriendlyCars #ElectricVehicleTech #CleanTransportation #GreenMobility #EVInnovation #PlasticsInEVs #FutureOfTransport #SustainableMaterials #EcoAutoDesign #EVManufacturing #PolymerInnovation #ZeroEmissionVehicles #GreenTechAuto #CleantechPlastics #EVDesign #EcoFriendlyPlastics #CircularAutoEconomy

#EV Plastics#Electric Vehicles#Sustainable Driving#Eco-Friendly Cars#Electric Vehicle Tech#Clean Transportation#Green Mobility#EV Innovation#Plastics In EVs#Future Of Transport#Sustainable Materials#Eco Auto Design#EV Manufacturing#Polymer Innovation#Zero Emission Vehicles#Green Tech Auto#Cleantech Plastics#EV Design#Eco-Friendly Plastics#Circular Auto Economy

2 notes

·

View notes

Text

Nanocellulose 2023 Industry – Challenges, Drivers, Outlook, Segmentation - Analysis to 2030

Nanocellulose Industry Overview

The global nanocellulose market size was valued at USD 351.5 million in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 20.1% from 2023 to 2030.

The growth is attributable to the rise in demand for various applications and the shifting trend for using bio-based goods are the factors responsible to drive demand for product. Due to its various qualities, such as increased paper machine efficiency, better filler content, lighter base mass, and higher freeness, nanocellulose is suitable for the producing a wide range of products. The paper industry uses nanocellulose as a prominent sustainable nanomaterial additive owing to its high strength, strong oxygen barrier performance, low density, mechanical qualities, and biocompatibility among the available bio-based resources. Additionally, the construction of materials, aqueous coating, and others are some of the major uses of nanocellulose composite materials.

Gather more insights about the market drivers, restrains and growth of the Nanocellulose Market

The U.S. is the largest market for nanocellulose in North America contributing a considerable amount to global revenue. People in the U.S. are concerned about their health, which has greatly aided the use of MFC (Micro fibrillated Cellulose) and CNF (Cellulose nanofibers) in the production of functional food products thus increasing the demand for nanocellulose in the country.

The food & beverage, and paper & pulp industry are majorly driving product growth in the country. Demand in the country is majorly driven by the increasing awareness and insistence on highly advanced sustainable products along with paper-based packaging in the food & beverage industries.

The pulp & paper business heavily utilizes nanocellulose as an ingredient to create light and white paper that further accelerates the market growth. Owing to its benign qualities it is used in healthcare applications such as biomedicines and personal hygiene products. Additionally, owing to its superior adsorption abilities, Nanocellulose is a suitable constituent for sanitary napkins and wound dressings. The market has been further stimulated by expanding product research activity.

Nanocellulose Market Segmentation

Grand View Research has segmented the global nanocellulose market report based on the type, application, and region:

Type Outlook (Revenue, USD Million; Volume, Kilotons; 2018 - 2030)

CNF (NFC, MFC)

Bacterial Cellulose

CNC

Application Outlook (Revenue, USD Million; Volume, Kilotons; 2018 - 2030)

Pulp & Paperboard

Composites

Pharmaceuticals & Biomedical

Electronics

Food & Beverages

Others (Textile, Paints, cosmetics, Oil & Gas, Cement)

Regional Outlook (Revenue, USD Million; Volume, Kilotons; 2018 - 2030)

North America

US

Canada

Mexico

Europe

UK

Germany

Netherlands

France

Finland

Norway

Sweden

Switzerland

Spain

Asia Pacific

China

India

Japan

South Korea

Australia

Thailand

Malaysia

Singapore

Central & South America

Brazil

Colombia

Chile

Middle East & Africa

Saudi Arabia

South Africa

Israel

Iran

Browse through Grand View Research's Renewable Chemicals Industry Research Reports.

The global chondroitin sulfate market size was valued at USD 1.29 billion in 2023 and is projected to grow at a CAGR of 3.6% from 2024 to 2030.

The global pine-derived chemicals market size was estimated at USD 5.82 billion in 2023 and is projected to grow at a CAGR of 4.4% from 2024 to 2030.

Key Companies & Market Share Insights

The market is consolidated owing to the existence of a few major players in the market including Cellu Force, Fiber Lean, Kruger INC., and others. Manufacturers operating in the market engage in strategic mergers & acquisitions, geographical expansion, product developments, and innovation in order to strengthen their positions, increase profitability, and simultaneously generate innovations and advancements.

When compared to other nanotechnology high-performance materials, nanocellulose offers a lower cost and the potential to replace many products made from petrochemicals. It has exceptional qualities like biodegradability, transparency, flexibility, high mechanical strength, and barrier characteristics, among others. Growing interest in health issues and the food & beverage industries will both have a significant impact on the market share in the years to come.

Consequently, the focus on manufacture of the product has increased owing to increasing awareness about health and environmental concerns arising from harmful chemical products. The global market has witnessed several new product developments, mergers & acquisitions and joint ventures due to several industrial challenges. Some prominent players in the global nanocellulose market include:

Cellu Force

Fiber Lean

NIPPON PAPER INDUSTRIES CO., LTD.

Kruger INC

Borregaard AS

CelluComp

Melodea Ltd

Blue Goose Refineries

GranBio Technologies

Stora Enso Biomaterials

Order a free sample PDF of the Nanocellulose Market Intelligence Study, published by Grand View Research.

0 notes

Text

Aerospace And Defense Materials Market — Industry Analysis, Market Size, Share, Trends, Growth And Forecast 2024–2030

The report “Aerospace and Defense Materials Market– Forecast (2024–2030)”, by IndustryARC, covers an in-depth analysis of the following segments of the Aerospace and Defense Materials market.

By Product Forms: Round Products (Bar, Rod, Pipe, Others), Flat Products (Slab, Plat, Sheet, Others), Net-shaped products (Forging, Near-net-shaped powdered products, Machined components)

By Material: Metals & Alloys (Aluminum, Titanium alloys, Nickel-based alloys, Steels, Superalloys, Tungsten, Niobium, Others), Composites, Plastics, (Polyetheretherketone (PEEK), Polyamide-imide (PAI), Others), Others

By Application: Airframe, Cabin interior, Propulsion, Aero Engine, Naval System, Weapons, Navigation and sensors, Satellites, and Others.

By End-use Industry: Aircrafts (Wide Body Aircrafts, Single Aisle Aircrafts, Regional Transport Aircrafts), Rotorcrafts, Spacecrafts, Others.

By Geography: North America, South America, Europe, Asia-Pacific, RoW

Request Sample

Key Takeaways

Innovation in the realm of aerospace and defense materials is being fueled by ongoing advancements in materials science and engineering. The development of stronger, more resilient, and lighter materials such as improved composites and alloys is made possible by these breakthroughs. These materials are essential for increasing performance, reducing fuel consumption, and extending the life of defense and aerospace systems. For instance, the use of carbon fiber-reinforced polymers (CFRP) in airplane components has significantly reduced weight without sacrificing structural integrity, saving fuel and improving performance. The fabrication of complicated geometries and bespoke components is made possible by developments in additive manufacturing techniques, which further expand the capabilities of materials used in aerospace and defense.

Several nations’ governments are making significant investments in R&D projects to create cutting-edge defense and aerospace technologies. For instance, as per the International Trade Administration, Canada has aerospace sector spent more than C$680 million (about $523 million) on research and development in 2022, making it more than 2.3 times more intensive than the industrial average. For the first C$2 million (about $1.55 million) in eligible R&D expenses, the Canadian government offers complete write-offs of R&D capital and equipment. This encourages businesses in the Canadian sector to maintain an advantage over rivals worldwide.

Inquiry Before Buying

As per the Indian Brand Equity Foundation, with approximately $223 billion in planned capital expenditures for aerospace and defense over the next ten years and a projected $130 billion investment over the medium term, the Indian defense sector is among the biggest and most lucrative in the world. This will contribute to an expansion in the market for aerospace and defense materials.

By Product Forms — Segment Analysis

Flat Products dominated the Aerospace and defense materials market in 2023. Advanced high-strength steel alloys and aluminum are examples of flat products that combine strength and lightweight. For aerospace applications, where a lighter aircraft can result in significant fuel savings and increased efficiency, this weight reduction is essential. For instance, in October 2023, GKN Aerospace and IperionX, a titanium developer located in North Carolina, joined to supply titanium plate test components that are produced using powder metallurgy and titanium angular powder processes. The main goal of this collaboration is to manufacture high-performance titanium plates for testing purposes at GKN Aerospace. It ends with the possibility of future cooperation between GKN Aerospace and IperionX, especially for projects related to the Department of Defense (DoD) in the United States.

Schedule a Call

Slabs provide industrial flexibility since they can be further processed to create a variety of products, including plates, sheets, strips, and structural elements. Because of the material’s adaptability, aerospace and defense companies can create a vast array of parts and structures and tailor them to match particular design specifications. For structural elements including fuselage skins, wing panels, bulkheads, floor beams, and armor plating, slabs are widely employed in aerospace and defense applications. For the structural loads, vibrations, and difficult operating conditions found in aerospace and defense settings, slabs offer the strength, stiffness, and longevity needed.

By Material — Segment Analysis

Metals & Alloys dominated the aerospace and defense materials market in 2023. The aerospace industry relies heavily on various metals due to their unique properties. To safely interact with and complement the new composite materials that are rapidly taking over the aerospace industry. Metal alloys like titanium and nickel-based superalloys are replacing aluminum structures in applications requiring extraordinarily high strength-to-weight ratios.

The demand for Superalloys based on nickel, cobalt, and iron is also increasing which makes them perfect for hot applications in jet engines. For example, in June 2023, ATI Allvac, which manufactures nickel-base and cobalt-base superalloys, titanium-base alloys, and specialty steels for the aerospace industry, said that it had received an estimated $1.2 billion in new sales commitments from major aerospace and defense industries.

For instance, in October 2023, Novelis, a global leader in aluminum rolling and recycling and a top supplier of sustainable aluminum solutions, announced that it had extended its agreement with Airbus. This agreement strengthens Novelis’s long-standing relationship with Airbus and highlights the company’s leadership position in supplying cutting-edge aluminum products and services to the commercial aircraft sector.

In October 2022, Mishra Dhatu Nigam Limited (MIDHANI) and Boeing India announced a collaboration to create raw materials for the aerospace industry. MIDHANI is a state-owned steel component, superalloy, and other material provider.

Buy Now

By Application — Segment Analysis

Cabin interior dominated the aerospace and defense materials market in 2023. Adoption of new technologies, such as additive manufacturing, has the potential to transform supply chains and product design, driving higher demand for materials used in cabin interiors.

For example, in February 2023, Chromatic 3D Materials, a 3D-printing technology enterprise, announced that their thermoset polyurethanes passed 14 CFR vertical burn tests, demonstrating anti-flammability norms for airworthiness. The successful examination indicates that the abrasion-resistant materials can be used to 3D-print a wide range of airline parts, including elastomeric components for stowage compartments and ornamental panels, as well as ductwork, cargo liners, fabric sealing, and other applications.

There has been an increase in demand lately for business jets and older aircraft to be repaired and renovated. For instance, in November 2022, Emirates invested $2 bn and began its huge 2-year refurbishment program with the first of 120 aircraft slated for a full cabin interior upgrade and the installation of the airline’s most recent Premium Economy seats. Similarly, refurbishment activities are expected to strengthen the market throughout the forecast period.

By End-use Industry- Segment Analysis

Aircrafts dominated the aerospace and defense materials market in 2023. There is a growing usage of high-performance materials in commercial aircraft applications. for example, Boeing estimates that the airline industry will need more than 44,000 new commercial aircraft by 2038, with a total estimated value of $6.8 trillion. All these aircraft employ composite materials. Aircraft manufacturers are producing new commercial, military, and general aviation aircraft models, which necessitate the use of modern materials with higher performance and lower weight. As a result, the emphasis is shifting toward newer material technologies such as composites. Also, wide-body jet engines have undergone significant transformations in recent years, due to the development of turbofan engines and the use of fuel-efficient techniques. These transformations are expected to increase the market growth.

By Geography — Segment Analysis

North America dominated the aerospace and defense materials market in 2023. In terms of aerospace and defense technologies, the United States and Canada are at the forefront. New, high-performance materials utilized in these industries are developed as a result of ongoing discoveries and developments in materials science. The defense budget of the United States is among the highest in the world. High levels of government investment in defense raise the need for cutting-edge materials for use in aircraft, military hardware, and other defense systems.

For instance, as per the International Trade Administration, Canada has aerospace sector spent more than C$680 million (about $523 million) on research and development in 2022, making it more than 2.3 times more intensive than the industrial average. For the first C$2 million (about $1.55 million) in eligible R&D expenses, the Canadian government offers complete write-offs of R&D capital and equipment. This encourages businesses in the Canadian sector to maintain an advantage over rivals worldwide.

On 11 December 2023, The Department of Defense’s (DoD) Industrial Base Analysis and Sustainment (IBAS) Program and the Institute for Advanced Composites Manufacturing Innovation® (IACMI) announced a national initiative to help meet critical defense needs in the casting and forging industry for the United States. Curriculum creation for a series of stackable training opportunities in the metals industry, with an emphasis on the development of trades and engineering workers, is currently underway as part of the multi-year agreement between DoD and IACMI.

Drivers — Aerospace and Defense Materials Market

• The Growing Demand for Lightweight and High-strength Materials

The growing need for lightweight and high-strength materials is driving substantial growth in the global aerospace and defense materials market. Due to their high strength-to-weight ratios, lightweight materials like carbon fiber composites, titanium alloys, and advanced polymers are in high demand by the aerospace and defense industries. These materials not only reduce aircraft weight but also improve structural integrity, which lowers operating costs and fuel efficiency.

High-strength and lightweight materials have always been essential to building aircraft that are both fuel-efficient and highly effective. aluminum is a major material used to make aircraft. Aluminum was utilized in the production of several aircraft components, including the fuselage and other primary engine sections since it was lightweight, affordable, and easily accessible. Since then, innovative materials have been used to improve aircraft design, including composites (made of carbon and glass fiber, polymeric and epoxy resins) and metals (titanium, steel, new AI alloys).

For instance, on 23 October 2023, The U.S. Department of Commerce’s Economic Development Administration (EDA) under the Biden-Harris administration selected the American Aerospace Materials Manufacturing Center as one of the 31 first Tech Hubs nationwide. About 50 public and private partners are brought together by Gonzaga University’s AAMMC Tech Hub to foster innovation and development manufacturing of composite materials for the next generation of lightweight, environmentally friendly aircraft.

For instance, in 2020, NASA engineers have created novel materials that can be utilized to create better aircraft engines and related system elements. Silicon Carbide (SiC) Fiber-Reinforced SiC Ceramic Matrix Composites (SiC/SiC CMCs) are one of these materials. For high-performance machinery, such as aircraft engines, that must run for lengthy periods under harsh conditions, this lightweight, reusable fiber material is perfect. In between maintenance cycles, SiC fibers are robust enough to endure months or even years, and they can tolerate temperatures as high as 2,700 degrees Fahrenheit.

• The Global Civil Aviation Industry is Expanding Rapidly

The global civil aviation industry’s explosive expansion is one of the key factors propelling the aerospace and defense materials market. The aerospace and defense materials industry’s demand for materials is heavily influenced by several interrelated factors, all of which contribute to its rise

The rise in air travel worldwide, which is being driven by urbanization and increased disposable incomes, is one of the main factors. The increased demand for commercial air travel as a result has forced airlines to modernize and grow their fleets. The pressure on aerospace manufacturers to make sophisticated, lightweight, and fuel-efficient aircraft is pushing the development of advanced alloys, lightweight composites, and high-performance materials that promote environmental sustainability and passenger safety. For instance, the aviation industry is and will continue to expand rapidly. The International Civil Aviation Organization’s most recent projections indicate that throughout the next 20 years, the demand for air travel will rise by an average of 4.3% per year.

For instance, according to the IBEF, India is the third-biggest domestic air travel market globally. By 2024, the domestic aviation market in India is expected to grow to $30 billion, ranking third globally. The aviation industry has benefited from an increase in the proportion of middle-class households, fierce rivalry among low-cost carriers, considerable airport infrastructure investment, and a favorable political climate.

Market Landscape

Technology launches and R&D activities are key strategies adopted by players in the Aerospace and Defense Materials market. In 2023, the Aerospace and Defense Materials market share has been consolidated by the major players accounting for 80% of the share. Major players in the Aerospace and Defense Materials are Alcoa Corporation, Novelis Inc., Thyssenkrupp Aerospace, Toray Industries Inc., Mitsubishi Chemical Group, Teijin Limited, Hexcel, Allegheny Technologies, Constellium, Solvay S.A., Formosa, SGL Group, Kobe Steel Ltd., among others.

Developments:

In October 2023, Novelis and Airbus inked a contract to continue their cooperation. The deal strengthens Novelis and Airbus’s long-standing cooperation and highlights the company’s leadership in developing cutting-edge aluminum goods and solutions for the commercial aircraft sector.

In June 2023, as a strategic partner of Spirit’s Aerospace Innovation Centre (AIC) in Prestwick, Scotland, Solvay and Spirit AeroSystems (Europe) Limited have deepened their partnership. Together with Spirit’s academic, industrial, and supply-chain partners, the AIC fosters cooperative research into environmentally friendly aircraft technology and procedures.

In June 2022, Sikorsky granted Hexcel Corporation a long-term contract to supply cutting-edge composite structures for the CH-53K King Stallion heavy lift helicopter. This funding has significantly increased the Hexcel composite composition of the airplane.

For more Chemicals and Materials Market reports, please click here

#digital marketing#reseach marketing#marketing#Aerospace and Defense Materials#chemicals#materials science

0 notes

Text

Exploring the Membrane Contactor Market: Trends, Innovations, and Future Prospects

The Membrane Contractor Market was valued at USD 0.3 billion in 2023 and will surpass USD 0.48 billion by 2030; growing at a CAGR of 6.9% during 2024 - 2030. The membrane contactor market is gaining significant traction across various industries, thanks to its innovative approach to separation and purification processes. Membrane contactors, which use membranes to facilitate mass transfer between different phases, are increasingly being adopted due to their efficiency, compact design, and versatility. This blog delves into the current trends, key innovations, and future prospects of the membrane contactor market.

Membrane contactors are devices that use a membrane to achieve selective mass transfer between a gas and a liquid or between two liquid phases. Unlike traditional separation techniques, membrane contactors provide a large interfacial area for mass transfer, enhancing the efficiency and effectiveness of the process. They are used in various applications such as gas absorption, degassing, distillation, and liquid-liquid extraction.

Get a Sample Report: https://intentmarketresearch.com/request-sample/membrane-contactor-market-3455.html

Market Trends

Increasing Demand in Water Treatment

The growing need for clean and safe water is driving the demand for advanced water treatment solutions. Membrane contactors play a crucial role in removing dissolved gases and contaminants from water, making them an essential component in water purification systems.

Rising Adoption in the Food and Beverage Industry

The food and beverage industry is increasingly adopting membrane contactors for processes like carbonation, deaeration, and aroma recovery. These applications require precise control and high efficiency; which membrane contactors can provide.

Expanding Use in the Pharmaceutical Sector

Pharmaceutical manufacturing requires high purity levels and stringent control over production processes. Membrane contactors are used for degassing solvents, removing impurities, and maintaining the integrity of pharmaceutical products.

Technological Advancements

Continuous research and development are leading to technological advancements in membrane materials and design. Innovations such as hollow fiber membranes and advanced polymeric materials are enhancing the performance and durability of membrane contactors.

Key Innovations

Hollow Fiber Membranes

Hollow fiber membranes offer a high surface area-to-volume ratio, which improves the efficiency of mass transfer processes. These membranes are being widely adopted in applications like gas absorption and liquid degassing.

Advanced Polymeric Materials

The development of advanced polymeric materials has led to membranes with better chemical resistance, higher permeability, and longer lifespans. These materials are crucial for applications in harsh chemical environments.

Integration with Other Technologies

The integration of membrane contactors with other technologies, such as vacuum systems and advanced control mechanisms, is enhancing their performance and expanding their application range. For example, integrating vacuum systems can improve gas removal efficiency in degassing applications.

Get an insights of Customization: https://intentmarketresearch.com/ask-for-customization/membrane-contactor-market-3455.html

Future Prospects

Growing Environmental Regulations

Stricter environmental regulations are expected to drive the adoption of membrane contactors in various industries. Their ability to efficiently remove contaminants and pollutants makes them a valuable tool in meeting regulatory requirements.

Expansion into Emerging Markets

The membrane contactor market is poised for growth in emerging markets, where industrialization and urbanization are driving the demand for advanced separation technologies. Countries in Asia-Pacific and Latin America are expected to be key growth regions.

Development of Hybrid Systems

Future developments may see the rise of hybrid systems that combine membrane contactors with other separation technologies. These systems can offer enhanced performance and versatility, catering to complex separation and purification needs.

Sustainability and Energy Efficiency

Sustainability and energy efficiency are becoming critical factors in the adoption of new technologies. Membrane contactors, with their low energy consumption and minimal environmental impact, are well-positioned to meet these demands.

Conclusion

The membrane contactor market is experiencing dynamic growth, driven by advancements in technology and increasing demand across various industries. As innovations continue to emerge and new applications are discovered, membrane contactors are set to play a pivotal role in the future of separation and purification processes. Their ability to provide efficient, compact, and versatile solutions makes them indispensable in an array of industrial applications, paving the way for a sustainable and efficient future.

#Membrane Contractor#Membrane Contractor Size#Membrane Contractor Growth#Membrane Contractor Forecast

0 notes

Text

The Future of Communication: Fiber Optic Connectivity and Beyond

Market Overview and Report Coverage

The fiber optic connectivity market is a key segment of the telecommunications and data transmission industry, offering high-speed, high-capacity, and reliable communication solutions. Fiber optic technology uses light to transmit data through flexible glass or plastic fibers, providing superior performance compared to traditional copper cables. The growing demand for high-speed internet, increased data consumption, and advancements in network infrastructure are driving the expansion of the fiber optic connectivity market.

According to Infinium Global Research, the global fiber optic connectivity market is expected to grow significantly from 2023 to 2030. Factors such as the increasing adoption of fiber-to-the-home (FTTH) networks, the rise in data center deployments, and the need for enhanced network performance contribute to market growth. Additionally, the integration of fiber optic technology in emerging applications such as 5G and IoT is influencing market dynamics.

Market Segmentation

By Type:

Single-Mode Fiber (SMF): Single-mode fiber is designed for long-distance data transmission with a small core diameter, allowing the transmission of signals over long distances with minimal signal loss. It is commonly used in telecommunications, data centers, and high-speed network applications.

Multi-Mode Fiber (MMF): Multi-mode fiber has a larger core diameter and is used for shorter-distance data transmission. It is typically employed in local area networks (LANs), data centers, and enterprise networks. MMF is suitable for applications where high bandwidth and shorter distances are required.

Fiber Optic Cables: Fiber optic cables include various types of cables, such as loose-tube cables, tight-buffered cables, and ribbon cables. These cables are used for different applications and environments, including indoor and outdoor installations, and play a crucial role in network infrastructure.

Fiber Optic Connectors and Adapters: Fiber optic connectors and adapters are essential components for joining fiber optic cables and ensuring proper signal transmission. They include connectors such as SC, LC, ST, and MTP/MPO, and are used in various network configurations.

By Application:

Telecommunications: Fiber optic connectivity is widely used in telecommunications networks for high-speed data transmission and internet services. It forms the backbone of modern communication networks, enabling reliable and fast connectivity for voice, video, and data services.

Data Centers: Fiber optics play a crucial role in data centers, providing high-bandwidth connections between servers, storage systems, and network equipment. The increasing demand for data storage and cloud services drives the need for advanced fiber optic solutions in data center environments.

Enterprise Networks: Fiber optic connectivity is used in enterprise networks to enhance data transmission speeds, support high-bandwidth applications, and improve network reliability. It is employed in both local area networks (LANs) and wide area networks (WANs) to support various business operations.

Broadcasting and Media: In the broadcasting and media industry, fiber optics are used for high-quality video transmission, live broadcasting, and content distribution. The technology supports high-definition and ultra-high-definition video streaming, contributing to the growth of media and entertainment applications.

Others: This category includes specialized applications such as military and defense communications, smart grid infrastructure, and medical imaging. Fiber optics are used in these sectors for high-speed data transmission, reliability, and precision.

Sample pages of Report: https://www.infiniumglobalresearch.com/form/1479?name=Sample

Regional Analysis:

North America: North America, led by the United States and Canada, is a major market for fiber optic connectivity due to advanced telecommunications infrastructure, high demand for high-speed internet, and extensive data center deployments. The region’s focus on technology innovation and 5G network expansion drives market growth.

Europe: Europe is a significant market, with countries such as Germany, the UK, and France leading in fiber optic adoption. The region’s emphasis on network modernization, high-speed broadband, and digital transformation contributes to market expansion.

Asia-Pacific: The Asia-Pacific region is expected to experience substantial growth due to increasing urbanization, rising internet penetration, and the expansion of telecommunications networks. Countries like China, India, and Japan are key players in the market, driving demand for fiber optic solutions.

Latin America and Middle East & Africa: These regions are witnessing growth in the fiber optic connectivity market due to improving telecommunications infrastructure, increased investments in network expansion, and rising demand for high-speed internet services. The expanding IT and communication sectors contribute to market development.

Emerging Trends in the Fiber Optic Connectivity Market

Several trends are shaping the future of the fiber optic connectivity market. The deployment of 5G networks is driving the demand for high-capacity fiber optic solutions to support increased data traffic and faster speeds. The growth of data centers and cloud computing is also influencing market dynamics, as data centers require high-bandwidth fiber connections for efficient operations. Additionally, the integration of fiber optics in smart city projects and IoT applications is expanding the scope of fiber optic technology. The development of new fiber optic technologies, such as bend-insensitive fibers and advanced optical networking solutions, is further driving market innovation.

Major Market Players

Corning Incorporated: Corning is a leading provider of fiber optic products and solutions, including optical fibers, cables, and connectors. The company’s focus on innovation and advanced technology supports its market leadership.

OFS Fitel, LLC: OFS offers a range of fiber optic products, including cables, connectors, and splicing solutions. The company’s expertise in optical communications and commitment to quality contribute to its market success.

Prysmian Group: Prysmian provides a comprehensive portfolio of fiber optic cables and solutions for telecommunications, data centers, and industrial applications. The company’s global presence and technological expertise enhance its market position.

Nexans S.A.: Nexans offers a variety of fiber optic products and solutions, including cables and connectors, for telecommunications and data networking applications. The company’s focus on innovation and customer satisfaction supports its role in the market.

Huanghe Whirlwind Co., Ltd.: Huanghe Whirlwind specializes in fiber optic cables and related products, serving telecommunications and industrial markets. The company’s emphasis on technological development and quality assurance contributes to its market presence.

Report Overview : https://www.infiniumglobalresearch.com/market-reports/global-fiber-optic-connectivity-market

0 notes

Text

Carbon Fiber Market - Forecast (2024 - 2030)

Carbon Fiber Market Overview

Carbon Fiber Market size is forecast to reach $15.3 billion by 2030, after growing at a CAGR of 11% during 2024-2030. Carbon fiber is a high strength, low weight, high stiffness, conductive to electricity, and is one of the most corrosion and heat resistant material. Growing demand for lightweight products from aerospace & defense, automotive, and wind energy industries and minimizing carbon emissions are driving the market growth. Whereas, the growing building and construction sector in the emerging country is also driving the market growth. As carbon fiber is used primarily in the strengthening and reinforcement of concrete, steel, timber, and masonry. Furthermore, increasing demand for carbon fiber composite in consumer electronics has made the products lighter and thinner, and more textured is likely to drive the market growth. The carbon fiber market is witnessing a significant trend with an increased adoption in the automotive industry. As automotive manufacturers strive to enhance fuel efficiency and reduce emissions, carbon fiber composites offer a lightweight alternative to traditional materials. This shift is driven by the demand for electric and hybrid vehicles, where minimizing weight is crucial for optimizing energy efficiency and extending battery range. Carbon fiber's high strength-to-weight ratio contributes to improved vehicle performance and structural integrity. Moreover, advancements in manufacturing processes and cost reductions are making carbon fiber more economically viable for mass-produced automobiles. This trend signals a transformative shift in the automotive sector, with carbon fiber playing a pivotal role in the development of next-generation, sustainable transportation solutions. A notable development in the carbon fiber market is the increasing focus on sustainable production methods. With rising environmental concerns and a push for eco-friendly materials, carbon fiber manufacturers are exploring ways to minimize the environmental impact of their production processes. Innovations include the use of bio-based precursors, recycling of carbon fiber waste, and energy-efficient manufacturing techniques. This trend aligns with global efforts to achieve carbon neutrality and reduce the overall carbon footprint of industries. Sustainable carbon fiber production not only addresses environmental concerns but also caters to the growing demand for green products in various sectors, including aerospace, automotive, and renewable energy. As sustainability becomes a key consideration for businesses and consumers alike, the carbon fiber market is evolving to meet these changing expectations and contribute to a more environmentally responsible future.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐑𝐞𝐩𝐨𝐫𝐭 𝐒𝐚𝐦𝐩𝐥𝐞

Carbon Fiber Market Report Coverage

The report: “Carbon Fiber Market – Forecast (2024-2030)”, by IndustryARC, covers an in-depth analysis of the following segments of the Carbon Fiber Industry.

By Raw Material: Polyacrylonitrile Based (PAN), Pitch Based (Mesophase Pitch Based, and Petroleum Pitch Based), and Others (Ultra High Elastic Modulus (UHM), High Elastic Modulus (HM), and Low Elastic Modulus (LM)).

By Tow Type: Continuous, and Chopped.

By Application: Composite, Non-Composite, Molding Compound, Woven Fabric, and Others.

By End-Use Industry: Aerospace & Defense (Fighter Jets, Armored Vehicles, Commercial Jets, Rotorcraft, Satellites, and Others), Automotive (Interior, Exterior, and Others), Sporting Goods (Tennis Rackets, Golf Club, Hockey Sticks, Archery, Others), Energy and Power (Wind, Solar, and Others), Building & Construction (Residential, Commercial, and Others), Marine, Healthcare, Electric & Electronic, and Others.

By Geography: North America, South America, Europe, Asia-Pacific, and Middle East & Africa

Key Takeaways

Europe will continue to have the major share of total worldwide wind energy carbon fiber demand during the forecast period owing to its renewable energy targets and use of offshore wind capacity.

High price of carbon fiber is one of the factors that’s hindering the markets growth.

COVID-19 will hinder the markets growth, as the end use industry are facing a slow growth, hence reducing the demand for carbon fiber.

Carbon Fiber Market Segment Analysis - By Raw Material

Polyacrylonitrile Based (PAN) segment held the largest share of more than 65% in the carbon fiber market in 2023. The PAN based component offers various benefits like low density, high strength, high modulus, high-temperature resistance, wear resistance, corrosion resistance, fatigue resistance, creepage resistance, electric conduction, heat conduction, and far-infrared radiation. These properties of PAN make it suitable to use across various end-use industries like the aerospace & aviation industry, automotive industry, wind turbines, anti-flame materials & clothes, and sports equipment. Thus, growth in these end-use industries further drive the market growth.

Carbon Fiber Market Segment Analysis - By Tow

Continuous tow segment held the largest share of more than 60% in the carbon fiber market in 2023. Continuous tow is the most widely used tow, due to its weight, compatibility with resins, and various range of sizing available for optimal processing. These are heavy tows with 50,000 filaments, each of these tows have heavy mechanical properties, which can be transferred to the finished products and components to enhance their properties such as strength, durability and structural properties. Furthermore, Continuous tows provide cost advantage, especially when used in a high-volume process, increases the reliability of the end product, enhance production efficiency and can be merged with all thermoset and thermoplastic resin systems. Continuous tow also makes carbon fiber far superior to glass and aramid fibers because of their added strength & stiffness and are used in manufacturing wind turbines, industrial, and automotive manufacturing. Therefore, these properties & advantages of continuous tow will further drive its demand in the market.

Carbon Fiber Market Segment Analysis - By Application

Composite segment held the largest share of more than 55% in 2023 and is forecasted to be the most utilized application of carbon fiber. The high strength, high thermal & electrical conductivity, light weight, and high modulus properties of composite makes them suitable to use across aerospace & defense, automotive, sports, and wind turbine industry, which are ideal for its growth. According to a 2022 report released by Aerospace Industries Association (AIA), in 2022 American aerospace & defense industry export amounted for $100.4 billion, which rose by 11.2 percent from 2021. The other industry driving the markets growth is automobile industry. For instance, a report released by Indian Brand Equity Foundation (IBEF) in 2023, In the first quarter of 2023-24, total production of passenger vehicles, commercial vehicles, three wheelers, two wheelers, and quadricycles was 6.01 million units. Furthermore, the growing demand for BMW i3 is also driving the market growth. As the BMW i3 is still the only car with a significant amount of carbon composite content.

#Carbon Fiber Market size#Carbon Fiber Market price#Carbon Fiber Market share#Carbon Fiber Market forecast

0 notes

Text

Nanocellulose Market, 2030: Key Companies and Emerging Trends

The global nanocellulose market size was valued at USD 351.5 million in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 20.1% from 2023 to 2030.

The growth is attributable to the rise in demand for various applications and the shifting trend for using bio-based goods are the factors responsible to drive demand for product. Due to its various qualities, such as increased paper machine efficiency, better filler content, lighter base mass, and higher freeness, nanocellulose is suitable for the producing a wide range of products. The paper industry uses nanocellulose as a prominent sustainable nanomaterial additive owing to its high strength, strong oxygen barrier performance, low density, mechanical qualities, and biocompatibility among the available bio-based resources. Additionally, the construction of materials, aqueous coating, and others are some of the major uses of nanocellulose composite materials.

Gather more insights about the market drivers, restrains and growth of the Nanocellulose Market

The U.S. is the largest market for nanocellulose in North America contributing a considerable amount to global revenue. People in the U.S. are concerned about their health, which has greatly aided the use of MFC (Micro fibrillated Cellulose) and CNF (Cellulose nanofibers) in the production of functional food products thus increasing the demand for nanocellulose in the country.

The food & beverage, and paper & pulp industry are majorly driving product growth in the country. Demand in the country is majorly driven by the increasing awareness and insistence on highly advanced sustainable products along with paper-based packaging in the food & beverage industries.

The pulp & paper business heavily utilizes nanocellulose as an ingredient to create light and white paper that further accelerates the market growth. Owing to its benign qualities it is used in healthcare applications such as biomedicines and personal hygiene products. Additionally, owing to its superior adsorption abilities, Nanocellulose is a suitable constituent for sanitary napkins and wound dressings. The market has been further stimulated by expanding product research activity.

Nanocellulose Market Segmentation

Grand View Research has segmented the global nanocellulose market report based on the type, application, and region:

Type Outlook (Revenue, USD Million; Volume, Kilotons; 2018 - 2030)

• CNF (NFC, MFC)

• Bacterial Cellulose

• CNC

Application Outlook (Revenue, USD Million; Volume, Kilotons; 2018 - 2030)

• Pulp & Paperboard

• Composites

• Pharmaceuticals & Biomedical

• Electronics

• Food & Beverages

• Others (Textile, Paints, cosmetics, Oil & Gas, Cement)

Regional Outlook (Revenue, USD Million; Volume, Kilotons; 2018 - 2030)

• North America

o U.S.

o Canada

o Mexico

• Europe

o U.K.

o Germany

o Netherlands

o France

o Finland

o Norway

o Sweden

o Switzerland

o Spain

• Asia Pacific

o China

o India

o Japan

o South Korea

o Australia

o Thailand

o Malaysia

o Singapore

• Central & South America

o Brazil

o Colombia

o Chile

• Middle East & Africa

o Saudi Arabia

o South Africa

o Israel

o Iran

Browse through Grand View Research's Renewable Chemicals Industry Research Reports.

• The global chondroitin sulfate market size was valued at USD 1.29 billion in 2023 and is projected to grow at a CAGR of 3.6% from 2024 to 2030.

• The global pine-derived chemicals market size was estimated at USD 5.82 billion in 2023 and is projected to grow at a CAGR of 4.4% from 2024 to 2030.

Key Companies & Market Share Insights

The market is consolidated owing to the existence of a few major players in the market including Cellu Force, Fiber Lean, Kruger INC., and others. Manufacturers operating in the market engage in strategic mergers & acquisitions, geographical expansion, product developments, and innovation in order to strengthen their positions, increase profitability, and simultaneously generate innovations and advancements.

When compared to other nanotechnology high-performance materials, nanocellulose offers a lower cost and the potential to replace many products made from petrochemicals. It has exceptional qualities like biodegradability, transparency, flexibility, high mechanical strength, and barrier characteristics, among others. Growing interest in health issues and the food & beverage industries will both have a significant impact on the market share in the years to come.

Consequently, the focus on manufacture of the product has increased owing to increasing awareness about health and environmental concerns arising from harmful chemical products. The global market has witnessed several new product developments, mergers & acquisitions and joint ventures due to several industrial challenges. Some prominent players in the global nanocellulose market include:

• Cellu Force

• Fiber Lean

• NIPPON PAPER INDUSTRIES CO., LTD.

• Kruger INC

• Borregaard AS

• CelluComp

• Melodea Ltd

• Blue Goose Refineries

• GranBio Technologies

• Stora Enso Biomaterials

Order a free sample PDF of the Nanocellulose Market Intelligence Study, published by Grand View Research.

#Nanocellulose Market#Nanocellulose Industry#Nanocellulose Market size#Nanocellulose Market share#Nanocellulose Market Analysis

0 notes

Text

Global Carbon Fiber Market

The global Carbon Fiber Market has been experiencing significant growth due to the increasing demand across various industries such as aerospace, automotive, wind energy, and sports equipment. Carbon fiber is highly valued for its strength-to-weight ratio, stiffness, corrosion resistance, and low thermal expansion, making it a preferred material for high-performance applications.

Explore more-https://vynzresearch.com/chemicals-materials/carbon-fiber-market/request-sample

Market Size & Growth:

As of 2023, the global carbon fiber market size was valued at approximately USD 3-4 billion and is expected to grow at a compound annual growth rate (CAGR) of around 10-12% over the next five to seven years.

By 2030, the market is projected to exceed USD 7-8 billion, driven by expanding applications and technological advancements.

Regional Insights:

North America: This region is one of the largest markets for carbon fiber, driven by the strong presence of aerospace, automotive, and defense industries.

Europe: Europe is a significant market, particularly in Germany and the UK, due to the automotive industry's focus on lightweight materials.

Asia-Pacific: The fastest-growing region, with China and Japan leading due to rapid industrialization, increasing aerospace production, and expanding automotive industries.

VynZ Research

9960288381

0 notes

Text

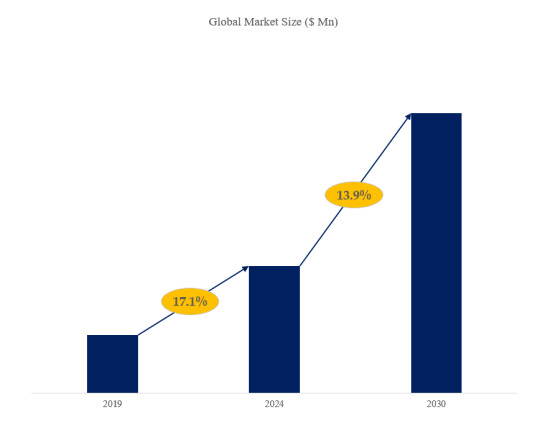

Poste de travail laser pour réseaux de Bragg en fibre optique, Prévisions de la Taille du Marché Mondial, Classement et Part de Marché des 5 Premières Entreprises

Selon le nouveau rapport d'étude de marché “Rapport sur le marché mondial de Poste de travail laser pour réseaux de Bragg en fibre optique 2024-2030”, publié par QYResearch, la taille du marché mondial de Poste de travail laser pour réseaux de Bragg en fibre optique devrait atteindre 1180 millions de dollars d'ici 2030, à un TCAC de 13.9% au cours de la période de prévision.

Figure 1. Taille du marché mondial de Poste de travail laser pour réseaux de Bragg en fibre optique (en millions de dollars américains), 2019-2030

Selon QYResearch, les principaux fabricants mondiaux de Poste de travail laser pour réseaux de Bragg en fibre optique comprennent WOP, Innofocus, etc. En 2023, les trois premiers acteurs mondiaux détenaient une part d'environ 82.0% en termes de chiffre d'affaires.

Figure 2. Classement et part de marché des 5 premiers acteurs mondiaux de Poste de travail laser pour réseaux de Bragg en fibre optique (Le classement est basé sur le chiffre d'affaires de 2023, continuellement mis à jour)

The market for laser workstations used for the production and analysis of Fiber Bragg Gratings (FBGs) is influenced by several key drivers, which contribute to its growth and development. Here are some important market drivers:

1. Rising Demand for Fiber Bragg Gratings: FBGs are widely used in various applications, including telecommunications, structural health monitoring, temperature sensing, and pressure measurements. The increasing demand for these applications drives the need for advanced laser workstations capable of producing high-quality FBGs.

2. Advancements in Laser Technology: Continuous improvements in laser technologies, including sources that are more efficient, reliable, and capable of producing precise and high-resolution gratings, are driving the adoption of laser workstations. New types of lasers and improved fabrication techniques enhance the performance of FBGs.

3. Growth in Telecommunications Sector: The telecommunications industry is one of the largest consumers of Fiber Bragg Gratings, especially for applications in fiber-optic communications and signal processing. As demand for high-speed data transmission and 5G technology continues to grow, the need for FBGs and the corresponding laser workstations will increase.

4. Development of Smart Infrastructure: The expansion of smart building technologies and infrastructure monitoring systems that utilize FBG sensors for real-time condition monitoring and data collection is driving market growth. Laser workstations are essential for developing customized FBGs tailored to specific monitoring needs.

5. Innovations in Sensing Technologies: FBGs are increasingly being adopted in various sensing applications due to their advantages, such as high sensitivity and immunity to electromagnetic interference. The growth in industries such as aerospace, automotive, and energy sector—for structural and environmental monitoring—requires robust laser workstations for the production of specialized FBGs.

6. Focus on Research and Development: Research institutions and labs are actively engaged in developing new applications for FBGs, which drives the demand for laser workstations that can facilitate advanced experimental setups. This R&D focus contributes to the advancement of FBG-related technologies and products.

7. Miniaturization Trends: The growing trend toward miniaturization in various applications, especially in telecommunications and medical devices, requires precise and compact FBG solutions. Laser workstations equipped to produce smaller and more intricate FBGs are increasingly important.

8. Energy Efficiency and Cost Reduction: Advances in laser technology have enabled the development of more energy-efficient laser workstations, which can reduce operating costs. This is particularly attractive for businesses and research institutions looking to optimize their operations.

9. Customization and Flexibility: The ability to design and fabricate customized FBGs for specific applications is driving demand for adaptable laser workstations. Systems that allow for easy programming and adjustment for different grating patterns can enhance production efficiency and innovation.

10. Growing Adoption in Medical Applications: The healthcare sector is increasingly exploring the use of FBGs for applications such as biomedical sensing and imaging. As this trend grows, the need for specialized laser workstations for producing medical-grade FBGs will also increase.

11. Collaborative Industry Growth: Collaborations between universities, research institutions, and industries focused on fiber optics and sensor technologies promote innovation and lead to the development of new applications for FBGs. This collaborative growth stimulates demand for laser workstations.

In summary, the market for laser workstations for Fiber Bragg Gratings is driven by rising demand for FBGs in various sectors, advancements in laser technology, the growth of telecommunications and smart infrastructure applications, research initiatives, and the increasing adoption of FBGs in sensing and medical applications. These factors create a conducive environment for the expansion of this market.

À propos de QYResearch

QYResearch a été fondée en 2007 en Californie aux États-Unis. C'est une société de conseil et d'étude de marché de premier plan à l'échelle mondiale. Avec plus de 17 ans d'expérience et une équipe de recherche professionnelle dans différentes villes du monde, QYResearch se concentre sur le conseil en gestion, les services de base de données et de séminaires, le conseil en IPO, la recherche de la chaîne industrielle et la recherche personnalisée. Nous société a pour objectif d’aider nos clients à réussir en leur fournissant un modèle de revenus non linéaire. Nous sommes mondialement reconnus pour notre vaste portefeuille de services, notre bonne citoyenneté d'entreprise et notre fort engagement envers la durabilité. Jusqu'à présent, nous avons coopéré avec plus de 60 000 clients sur les cinq continents. Coopérons et bâtissons ensemble un avenir prometteur et meilleur.

QYResearch est une société de conseil de grande envergure de renommée mondiale. Elle couvre divers segments de marché de la chaîne industrielle de haute technologie, notamment la chaîne industrielle des semi-conducteurs (équipements et pièces de semi-conducteurs, matériaux semi-conducteurs, circuits intégrés, fonderie, emballage et test, dispositifs discrets, capteurs, dispositifs optoélectroniques), la chaîne industrielle photovoltaïque (équipements, cellules, modules, supports de matériaux auxiliaires, onduleurs, terminaux de centrales électriques), la chaîne industrielle des véhicules électriques à énergie nouvelle (batteries et matériaux, pièces automobiles, batteries, moteurs, commande électronique, semi-conducteurs automobiles, etc.), la chaîne industrielle des communications (équipements de système de communication, équipements terminaux, composants électroniques, frontaux RF, modules optiques, 4G/5G/6G, large bande, IoT, économie numérique, IA), la chaîne industrielle des matériaux avancés (matériaux métalliques, polymères, céramiques, nano matériaux, etc.), la chaîne industrielle de fabrication de machines (machines-outils CNC, machines de construction, machines électriques, automatisation 3C, robots industriels, lasers, contrôle industriel, drones), l'alimentation, les boissons et les produits pharmaceutiques, l'équipement médical, l'agriculture, etc.

#Poste de travail laser pour réseaux de Bragg en fibre optique#Laser Workstation for Fiber Bragg Gratings

0 notes

Text

The worldwide Tulip Wind Turbines Market will expand at a compound annual growth rate (CAGR) of 5.20%. From USD XX million in 2022, the market is projected to be worth USD XX million by 2030.The Tulip Wind Turbines Market is emerging as a significant player in the renewable energy sector, characterized by its unique design and efficiency in harnessing wind energy. Unlike traditional wind turbines, tulip wind turbines offer a visually appealing and environmentally friendly solution to energy generation. This article delves into the market size, growth prospects, technological advancements, market drivers, challenges, and key players shaping the future of tulip wind turbines.

Browse the full report at https://www.credenceresearch.com/report/tulip-wind-turbines-market

Market Size and Growth Prospects

The global tulip wind turbines market is expected to witness substantial growth over the next decade. According to market research, the market was valued at approximately USD 150 million in 2023 and is projected to reach USD 500 million by 2030, growing at a CAGR of 15% during the forecast period. The increasing demand for sustainable and aesthetically pleasing energy solutions is driving this growth. The adoption of tulip wind turbines is particularly significant in urban areas where space constraints and visual impact are critical considerations.

Technological Advancements

Tulip wind turbines are renowned for their innovative design, which sets them apart from traditional horizontal-axis wind turbines. These turbines feature a vertical axis and a tulip-shaped structure, allowing them to capture wind from all directions. This design not only enhances efficiency but also reduces noise levels, making them suitable for residential and commercial areas.

The advancements in materials and aerodynamics have significantly improved the performance of tulip wind turbines. Lightweight and durable materials such as carbon fiber and advanced composites are used in their construction, ensuring longevity and minimal maintenance. Furthermore, integration with smart grid technology and IoT has enabled better monitoring and control, optimizing energy output and enhancing reliability.

Market Drivers

1. Environmental Concerns: The growing awareness of climate change and the need for sustainable energy sources are primary drivers for the tulip wind turbines market. Governments and organizations worldwide are investing in renewable energy projects to reduce carbon footprints and promote green energy.

2. Urbanization: The increasing urban population necessitates the development of energy solutions that are both efficient and aesthetically pleasing. Tulip wind turbines, with their compact design, are ideal for urban installations, contributing to their rising demand.

3. Government Incentives: Various government policies and incentives aimed at promoting renewable energy adoption are fueling market growth. Subsidies, tax benefits, and grants for wind energy projects encourage the installation of tulip wind turbines.

4. Technological Innovation: Continuous research and development in turbine design and materials are enhancing the efficiency and cost-effectiveness of tulip wind turbines, making them more attractive to investors and consumers.

Challenges

Despite the promising growth prospects, the tulip wind turbines market faces several challenges:

1. High Initial Costs: The initial investment required for tulip wind turbine installation is relatively high compared to traditional wind turbines. This can be a deterrent for small-scale investors and residential users.

2. Limited Awareness: The concept of tulip wind turbines is still relatively new, and awareness among potential consumers is limited. Effective marketing and education campaigns are essential to increase adoption.

3. Regulatory Hurdles: The installation of wind turbines, especially in urban areas, is subject to stringent regulations and zoning laws. Navigating these regulatory frameworks can be complex and time-consuming.

4. Competition from Conventional Turbines: Traditional wind turbines have a well-established market presence and proven track record. Convincing stakeholders to switch to tulip wind turbines requires demonstrating clear advantages in terms of efficiency and cost.

Key Players

The tulip wind turbines market is characterized by the presence of several key players who are driving innovation and growth. Some of the prominent companies include:

1. Flower Turbines: A pioneer in the tulip wind turbine industry, Flower Turbines is known for its cutting-edge designs and commitment to sustainability.

2. Wind Tulip: Specializing in urban wind energy solutions, Wind Tulip focuses on integrating advanced technology with aesthetic appeal.

3. Turbina Energy AG: A leading European manufacturer, Turbina Energy AG offers a range of tulip wind turbines designed for various applications, from residential to industrial.

4. Urban Green Energy (UGE): UGE is a key player in the renewable energy sector, providing innovative wind and solar energy solutions, including tulip wind turbines.

Key Players

Flower Turbines (Netherlands)

Wuxi Flyt New Energy Technology Co.,Ltd. (China)

Start Engine (United States)

Leviathan Energy LLC (United States)

RexCo Technology (China)

Saur Energy

Gamesa

Solar Impulse Foundation

Ming Yang

General Electric

Segmentation

By Product Types:

Small-Scale Tulip Wind Turbines

Commercial Tulip Wind Turbines

By Rotor Design:

Darrieus-Style Tulip Wind Turbines

Savonius-Style Tulip Wind Turbines

By Application:

On-Grid Tulip Wind Turbines

Off-Grid Tulip Wind Turbines

By End Users:

Residential

Commercial and Industrial

Agricultural

Remote Areas

By Price Range:

Economy Tulip Wind Turbines

Premium Tulip Wind Turbines

By Region

North America

US

Canada

Mexico

Europe

Germany

France

UK

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/tulip-wind-turbines-market

About Us:

Credence Research is committed to employee well-being and productivity. Following the COVID-19 pandemic, we have implemented a permanent work-from-home policy for all employees.

Contact:

Credence Research

Please contact us at +91 6232 49 3207

Email: [email protected]

Website: www.credenceresearch.com

0 notes

Text

Makeup Tools Products: Analyzing Current Size, Share, and Growth Trends

The global makeup tools market size is expected to reach USD 5.85 billion by 2030, growing at a CAGR of 8.3% during the forecast period, according to a new report by Grand View Research, Inc. The proliferation of beauty influencers across social media platforms like Instagram, YouTube, and TikTok has significantly impacted the market. These influencers utilize their platforms to demonstrate various makeup techniques, provide tutorials, and recommend products to their followers. As a result, they wield considerable influence over consumer preferences and purchasing behaviors. This phenomenon has increased demand for specific makeup tools influencers endorse, driving sales and shaping market trends. In addition, influencers are pivotal in promoting new product innovations and highlighting the benefits of different tools, generating heightened consumer interest and interaction. Consequently, this dynamic has contributed to the overall growth and market expansion.

Advancements in technology within the beauty industry have spurred the creation of sophisticated makeup tools that offer improved functionality, performance, and user convenience. For instance, there are now makeup brushes featuring synthetic fibers that replicate the softness and precision of natural hair, alongside ergonomic designs that enhance grip and application control. Furthermore, incorporating technology into makeup tools, such as LED lighting in mirrors for better visibility or smart brushes capable of analyzing skin conditions, caters to consumers interested in innovative, high-tech solutions. These technological strides drive product innovation, appeal to tech-savvy consumers, and play a pivotal role in the ongoing market evolution.

Makeup tools play a crucial role in achieving desired makeup effects and enhancing beauty, yet they are often considered optional purchases, especially among budget-conscious consumers. This perception leads consumers to hesitate when considering high-quality or premium-priced makeup tools, sometimes opting for more affordable alternatives or refraining from purchasing altogether—this price sensitivity challenges manufacturers and brands aiming to capture market share and maintain profitability. Economic downturns, fluctuations in disposable income, and changing consumer priorities can exacerbate this sensitivity, potentially reducing demand for makeup tools and putting pressure on profit margins. Educating consumers about the advantages of investing in durable, high-quality makeup tools can mitigate concerns about initial costs and encourage informed purchasing decisions based on long-term value and performance.

As consumer demand shifts towards personalized products and experiences that cater to individual preferences, customization has emerged as a key opportunity for manufacturers and brands within the industry. This trend is manifested in various forms, such as customizable brush sets featuring interchangeable heads or handles, personalized engraving services for makeup tools, a diverse range of color choices to match personal style preferences, and tailored functionalities that cater to different user needs. In addition, DIY customization kits enable consumers to personalize their makeup tools at home. By embracing customization, brands can distinguish themselves from competitors, deepen consumer engagement, foster brand loyalty, and stimulate sales growth in a competitive market environment, thereby contributing to market expansion.

For More Details or Sample Copy please visit link @: Makeup Tools Market Report

Makeup Tools Market Report Highlights

Based on product, brush dominated the market due to their versatility, effectiveness, and long-standing reputation for achieving precise makeup application

Professional application held the largest market share due to the growing number of professional makeup artists and beauty professionals

Premium price range is projected to grow with the highest CAGR over the forecast period due to advancements in technology and products allowing for the creation of tools with superior performance, durability, and innovative features, appealing to discerning consumers willing to invest in quality

The Asia Pacific market held the largest revenue share and is expected to retain its dominance over the forecast period. The Asia-Pacific region boasts a rapidly expanding population, marked by a growing middle class with increasing disposable income

For Customized reports or Special Pricing please visit @: Makeup Tools Market Report

We have segmented the global makeup tools market based on product, application, price, and region.

#MakeupTools#MakeupBrushes#CosmeticApplicators#BeautyBlenders#MakeupSponges#ProfessionalMakeupTools#CosmeticAccessories#MakeupIndustry#BeautyTools#CosmeticsMarket#SkincareTools#PersonalCare#MakeupBrands#BeautyEquipment

0 notes

Text

Laser Cutting Machines Market - Changing Supply and Demand Scenarios By 2030

Laser Cutting Machines Industry Overview

The global laser cutting machines market size was valued at USD 6,832.8 billion in 2022 and is expected to grow at a compound annual growth rate (CAGR) of 5.5% from 2023 to 2030.

Over the forecast period, it is anticipated that the growing trend of automation in the manufacturing sector and the rising demand for the end-use industry will increase demand for laser cutting to support the laser cutting machine industry’s growth.

End-use industries such as automotive, electronics, packing, pharmaceuticals, HVAC, and others are increasingly using automated laser cutting machines. Additionally, the end-use sectors widely utilize these machines to produce high-quality goods efficiently. Manufacturers are now able to automate a variety of processes, including laser cutting, owing to the growing trend of automation. These tools produce and cut pieces and patterns precisely; the machines deliver uniform outcomes, due to reduced downtime and the need for energy efficiency, manufacturers are investing in the automation of laser cutting, thus driving the market growth.

Gather more insights about the market drivers, restrains and growth of the Laser Cutting Machines Market

The growth of the laser cutting machines market is driven by the rising adoption of industry 4.0 technologies such as automation, data analytics, and the Internet of Things (IoT) are assisting in maximizing the efficiency of laser cutting machinery due to the real-time information exchange that enables optimum output by enabling operators to monitor and manage their production processes. Manufacturers aim to improve operating cost-efficiency, decrease downtime, and enhance production.

Another factor supporting the market growth of laser cutting machines is expanding due to the increased human-machine connection provided by industry 4.0 solutions, which is enhancing quality, productivity, and energy efficiency. Additionally, the early notification of the machine operation status provided by predictive analysis is promoting manufacturers to invest in industry 4.0 solutions by significantly lowering maintenance and replacement costs. This is expected to propel the market growth.

The emergence of fiber laser cutting is further expected to support the market growth of laser-cutting machinery. Fiber laser cutting devices are frequently employed in macro-processing applications with millimeter-level precision, such as cutting and welding industrial metals. Given the high demand for laser equipment, the market potential for macro processing is greater than that for micro processing. Fiber lasers are frequently employed in macro processing, which is the processing of objects whose size and shape have a laser beam influence range of millimeters, due to their high output power.

Fiber laser cutting boosts advantages such as precise, high-quality cuts, improved process for micro cutting, and shaping structural steel, positioning them as the preferred choice among the manufacturers. Additionally, the traction of fiber laser cutting equipment is fueled by several key features, including their ergonomics, quick operation, and high power safety. Most of these machines employ pre-focused optical systems with suitable deflection lenses, improving focus accuracy, laser light transmission, and machine performance. Thus, the emergence of new cutting technologies is driving the market growth.

The high cost of laser-cutting machinery coupled with high power consumption is a major restraint hindering the market growth. The high cost of the machinery components, such as water tubes, laser generators, and laser lenses, and their overall maintenance cost is another factor that affects the growth. Furthermore, when heated at high temperatures, cutting polymers such as Polytetrafluoroethylene and other metals releases harmful gases such as phosgene gas. This is another disadvantage restraining the industry’s growth.

Browse through Grand View Research's Electronic Devices Industry Research Reports.

• The global laser printer market size was estimated at USD 9.62 billion in 2023 and is projected to grow at a CAGR of 5.1% from 2024 to 2030.

• The global power electronics market size was valued at USD 38.12 billion in 2023 and is projected to grow at a CAGR of 5.2% from 2024 to 2030.

Key Laser Cutting Machines Company Insights

The key market players include Alpha Laser GmbH; Amada Miyachi Co. Ltd; Bystronic Inc.; Coherent Inc.; and DPSS Laser Inc. Manufacturers are concentrating on implementing tactics like acquisitions, collaborations, and expansions in order to increase their position in the worldwide market.

Participants in the market are focusing on bolstering their position through a range of strategic initiatives, including the development of new products, joint ventures, partnerships, and mergers and acquisitions. R&D efforts are heavily prioritized by major market participants in order to develop cutting-edge products and expand their product portfolios. These players are also focusing on developing laser equipment that uses less power and is more effective.Some prominent players in the global laser cutting machines market include.

Alpha Laser GmbH

Amada Miyachi Co. Ltd

Bystronic Inc.

Coherent Inc.

DPSS Laser Inc.

Epilog Lasers Inc.

Fanuc Corporation

IPG Photonics Corporation

Jenoptik Laser GmbH

Kern Lasers System

Rofin-Sinar Technologies Inc.

Trumpf Laser GmbH + Co. Kg

Avid Identification Systems, Inc

Order a free sample PDF of the Laser Cutting Machines Market Intelligence Study, published by Grand View Research.

0 notes

Text

Cable Blowing Equipment Market Growth Statistics and Key Players Insights (2023-2030)

Cable Blowing Equipment Market is estimated to reach USD 158.92 Million by 2030, growing at a CAGR of 5.7% over the forecast period 2023-2030.