#Next Generation Computing Market Demand

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr has 4 main sources of revenue.

Text

Next Generation Computing Market is Estimated to Witness High Growth Owing to Developments in Cloud Computing

Next generation computing includes technologies like cloud computing, edge computing and quantum computing. Cloud computing provides on-demand access to shared computing resources like servers, storage, networking, software and analytics over the internet. It allows business and individuals to avoid upfront infrastructure costs while paying only for resources that are consumed. Edge computing moves computing and data storage closer to the sources of data generation like Internet-connected devices. This ensures lower latency and faster insights from real-time analytics of data generated at the edge. Quantum computing uses the principles of quantum mechanics like superposition and entanglement to process information exponentially faster than classical computers for specific problem sets.

The Global Next Generation Computing Market is estimated to be valued at US$ 168.57 Bn in 2024 and is expected to exhibit a CAGR of 19% over the forecast period 2024 to 2031.

Key Takeaways

Key players operating in the Next Generation Computing are Amazon Web Services (AWS), Alphabet Inc. (Google), AMD (Advanced Micro Devices, Inc.), Apple Inc., IBM Corporation, Intel Corporation, Microsoft Corporation, NVIDIA Corporation, Oracle Corporation, Qualcomm Incorporated, Samsung Electronics Co., Ltd., SAP SE, Supermicro Computer, Inc., Tencent Holdings Limited, and Texas Instruments Incorporated.

The Next Generation Computing Market Size in cloud computing and edge computing adoption across industries, increasing investments in quantum computing research and expanding application landscape of advanced computing technologies.

Technological advancements fueling the next generation computing market include developments in cloud, edge and quantum computing offerings, next-gen processors and hardware, 5G and wireless technologies enabling IoT/edge devices, artificial intelligence and machine learning.

Market Drivers

Rapid increase in data volumes generated across industries is driving the need for scalable and efficient next generation computing platforms. Proliferation of IoT devices connected over networks is another key factor pushing the demand for distributed and real-time computing power. Growing requirement of advanced analytics, simulation and modeling capabilities for applications in transportation, healthcare and manufacturing is boosting investments in high performance cloud, edge and quantum solutions.

Challenges in Next Generation Computing Market

The Next Generation Computing Market Size And Trends is currently facing challenges such as high infrastructure costs for setting up data centers and lack of skilled workforce. Setting up data centers requires huge capital investments which is a major challenge for small and medium organizations. There is also a lack of skills required for managing big data, cloud, artificial intelligence and other emerging technologies. Setting up high performance computing infrastructure also requires significant upfront costs which small players find difficult to afford. Cybersecurity also poses a major challenge as more applications and data shift to the cloud. Protecting massive amounts of data from unauthorized access and ensuring privacy has become critical.

SWOT Analysis

Strength: Scalability and flexibility of cloud computing; Growing demand for high performance data analytics and AI Weakness: High initial infrastructure costs; Cybersecurity and privacy challenges Opportunity: Growth of IoT and edge computing; Increased focus on automation and application modernization Threats: Dependency on few technology giants; Stringent data protection regulations

Geographically, North America currently holds the largest share in the next generation computing market mainly due to heavy investments in cloud computing and data center build outs by major tech companies in the US. The Asia Pacific region is expected to be the fastest growing regional market during the forecast period driven by rapid digital transformation initiatives across industries in major economies like China and India. Countries are implementing national level programs to promote adoption of advanced computing technologies.

In terms of value, the next generation computing market is highly concentrated in the US currently, accounting for over 30% of the global market size. This is attributed to widespread cloud adoption by businesses as well as strategic investments by leading technology firms in the country to develop high performance computing infrastructure and next generation capabilities. China is expected to emerge as the fastest growing geographical market during 2024-2031 driven by government support for digitalization of industries using emerging technologies. Get More Insights On, Next Generation Computing Market For More Insights Discover the Report In language that Resonates with you

French

German

Italian

Russian

Japanese

Chinese

Korean

Portuguese

About Author: Ravina Pandya, Content Writer, has a strong foothold in the market research industry. She specializes in writing well-researched articles from different industries, including food and beverages, information and technology, healthcare, chemical and materials, etc. (https://www.linkedin.com/in/ravina-pandya-1a3984191)

#Next Generation Computing Market Size#Computing Market#Next Generation Computing Market Demand#Generation Computing Market#Next Generation Computing Market Trends#Next Generation Computing#Next Generation Computing Market

0 notes

Note

As I understand it you work in enterprise computer acquisitions?

TL;DR What's the general vibe for AI accelerating CPUs in the enterprise world for client compute?

Have you had any requests from your clients to help them upgrade their stuff to Core Ultra/Whateverthefuck Point with the NPUs? Or has the corporate world generally shown resistance rather than acquiescence to the wave of the future? I'm so sorry for phrasing it like that I had no idea how else to say that without using actual marketing buzzwords and also keeping it interesting to read.

I know in the enterprise, on-die neural acceleration has been ruining panties the world over (Korea's largest hyperscaler even opted for Intel Sapphire Rapids CPUs over Nvidia's Hopper GPUs due to poor supply and not super worth it for them specifically uplift in inference performance which was all that they really cared about), and I'm personally heavily enticed by the new NPU packing processors from both Team Red and Team We Finally Fucking Started Using Chiplets Are You Happy Now (though in large part for the integrated graphics). But I'm really curious to know, are actual corporate acquisitions folks scooping up the new AI-powered hotness to automagically blur giant pink dildos from the backgrounds of Zoom calls, or is it perceived more as a marketing fad at the moment (a situation I'm sure will change in the next year or so once OpenVINO finds footing outside of Audacity and fucking GIMP)?

So sorry for the extremely long, annoying, and tangent-laden ask, hope the TL;DR helps.

Ninety eight percent of our end users use their computers for email and browser stuff exclusively; the other two percent use CAD in relatively low-impact ways so none of them appear to give a shit about increasing their processing power in a really serious way.

Like, corporately speaking the heavy shit you're dealing with is going to be databases and math and computers are pretty good at dealing with those even on hardware from the nineties.

When Intel pitched the sapphire processors to us in May of 2023 the only discussion on AI was about improving performance for AI systems and deep learning applications, NOT using on-chip AI to speed things up.

The were discussing their "accelerators," not AI and in the webinar I attended it was mostly a conversation about the performance benefits of dynamic load balancing and talking about how different "acclerators" would redistribute processing power. This writeup from Intel in 2022 shows how little AI was part of the discussion for Sapphire Rapids.

In August of 2023, this was the marketing email for these processors:

So. Like. The processors are better. But AI is a marketing buzzword.

And yeah every business that I deal with has no use for the hot shit; we're still getting bronze and silver processors and having zero problems, though I work exclusively with businesses with under 500 employees.

Most of the demand that I see from my customers is "please can you help us limp this fifteen year old SAN along for another budget cycle?"

104 notes

·

View notes

Text

The Trump administration has scrapped its predecessor’s sweeping export controls for advanced artificial intelligence chips, known as the AI diffusion rule.

“To win the AI race, the Biden AI diffusion rule must go,” posted David Sacks, U.S. President Donald Trump’s top AI advisor, on May 8. Sacks continued his criticism at the Saudi-U.S. Investment Forum a few days later, arguing that the rule “restricted the diffusion or proliferation of American technology all over the world.”

As the administration decides what comes next, it should raise its sights from merely proposing a “simpler” rule to manage the diffusion of AI chips. Instead, it should seize the opportunity to offer an ambitious vision to promote the broader diffusion of U.S. technology.

After all, the world not only wants the United States’ AI chips, but also its AI applications, data centers, cloud services, satellites, and advanced technology offerings generally. But even as Beijing extends its digital offerings in key emerging markets, U.S. foreign policy has failed to adapt for a global technology competition with era-defining stakes. Whether you agree with the Trump administration or not, its disruption is an opportunity to forge a new model of technology statecraft to help the United States win the race to shape strategic digital infrastructure and technology diffusion across the globe.

To start, Washington must finally learn from its failure in the transition to 4G and 5G telecommunications networks, where Beijing’s state-backed model—and the absence of a compelling U.S.-led alternative—enabled Huawei and ZTE to all but corner emerging markets. Huawei now operates in more than 170 countries worldwide and is the top global provider of telecommunications equipment. But if there is broad consensus among U.S. policymakers that Beijing won that global technology transition, there is little agreement about how to win the next.

They have little time to waste. From Brasília to New Delhi, technology has moved to the center of government ambitions to drive growth, improve governance, and modernize security. Indonesian President Prabowo Subianto views the digital sector as essential to diversifying the country’s commodity-reliant economy. Kenyan President William Ruto hopes to boost the country’s “Silicon Savannah” by accelerating cloud migration. Saudi Crown Prince Mohammed bin Salman has made AI central to his “Vision 2030” framework for the kingdom’s modernization. The result is surging global demand not only for AI data centers, but also for cutting-edge digital infrastructure, services, and skilling more broadly.

In the coming years, foreign capitals and corporate boards will make potentially generational decisions about whether to meet this demand by partnering with the United States and its allies or China. These short-term decisions could have generational consequences. Projects to lay a transcontinental submarine cable or build large-scale data centers, for instance, are mapped in decades.

Even virtual cloud and AI services can have long-term stickiness. Imagine the pain of migrating an entire ministry’s data to a new cloud provider, or switching from an AI model that has been fine-tuned with a company’s sensitive data over time. Consider Beijing’s decade-plus struggle to transition its government computers from Windows. First movers reap powerful advantages.

If the stakes are great in the current round of global technology diffusion, so is the United States’ hand. Unlike the transition to 4G and 5G networks, where Western competitors such as Ericsson and Nokia struggled to match Huawei’s and ZTE’s subsidized offerings in emerging markets, the United States enters this technology transition with formidable advantages.

The United States occupies a commanding position in AI, with leadership or leverage over every part of the stack, ranging from chip design, tooling, and fabrication to model training and testing. U.S. companies hold at least a 70 percent share of the global cloud market. In space, Starlink has launched more satellites than all its competitors combined since 2020. Below the waves, three of the top four companies deploying subsea fiberoptic cables—the internet’s backbone—are from the United States or its close allies: SubCom (U.S.), Alcatel (France), and NEC (Japan). China controls the fourth, HMN Technologies (formerly Huawei Marine), which has deployed a mere 7 percent of the world’s submarine cables.

Despite powerful advantages, U.S. success is far from assured. The lesson of the 4G and 5G race is not to mirror China’s state-driven approach or to leave the private sector to fend for itself against Chinese competitors with powerful state backing. Nor is it to rely solely on export controls and other restrictive measures, however necessary those may be. The answer is to make U.S. foreign policy fit the global technology competition.

Washington can start with reforms in three broad areas.

First, unleash the United States’ strategic investment tools. One of Washington’s most promising but underused tools is the International Development Finance Corporation (DFC). Created during the first Trump administration, the DFC makes market-driven investments to advance both humanitarian and national security goals, and it has several tools to attract private capital from equity investments to political risk insurance.

As Congress considers DFC reauthorization—its current mandate expires in September—it should raise the existing cap on its lending authority from $60 billion to at least $100 billion and make strategic technologies and digital infrastructure an explicit priority. Congress should also loosen restrictions that can block DFC from supporting digital infrastructure projects that incidentally benefit high-income countries, which has kept it from financing critical subsea cables in the Indo-Pacific that invariably have landing points in Singapore, a major interconnection hub for the region.

The Export-Import Bank (EXIM) also punches below its weight. EXIM helps level the playing firm for U.S. firms competing abroad with a $135 billion lending limit and tools such as direct loans, loan guarantees, and insurance to de-risk purchases of U.S. exports. The United States once led the world in export financing, but China now dominates. In 2022, Chinese export credit agencies provided $11 billion in export support, compared to just $2.7 billion from EXIM.

Under the first Trump administration, EXIM created a new China and Transformational Exports Program (CTEP) to prioritize investments that counter Beijing’s subsidies and support advanced technologies such as AI and semiconductors. EXIM now aims to reserve at least 20 percent of its support for the program.

Despite progress, EXIM remains plagued with issues. To receive CTEP support, at least 51 percent of the exported content must be American-made—far higher than requirements in competitor agencies. Another requirement that EXIM-supported goods travel on U.S.-flagged vessels also hinders participation. Although well-intentioned, EXIM’s mandate to create jobs can deprioritize the export of low-labor digital exports such as AI and cloud services. Compounding the problem, EXIM is also required to limit defaults across its total lending portfolio to less than 2 percent, fueling risk-aversion.

Washington should reform EXIM for the global technology competition by at least doubling the 20 percent allocation for CTEP, relaxing shipping rules, and counting some allied components toward its content requirement. Lawmakers could also loosen the mandate to support U.S. job creation for digital services and double EXIM’s default cap to encourage more risk-taking.

Second, Washington should turbocharge its commercial diplomacy for technology. Between 2016 and 2020, an average of just 900 U.S. personnel from the State and Commerce departments were deployed abroad for commercial diplomacy, and just a fraction focused on technology. Since 2022, the State Department has taken important steps by establishing a new Bureau of Cyberspace and Digital Policy, a special envoy for critical and emerging technologies, and a course on cyberspace and digital policy tradecraft.

Despite this progress, few U.S. diplomats—and even fewer ambassadors—have deep technology expertise, which means that front-line opportunities to secure key technology bids and shape emerging AI or data policies can go unnoticed or suffer from inadequate staff or substance to engage effectively.

As the administration reforms the State Department, it should reinforce the Bureau of Cyberspace and Digital Policy, which has elevated and streamlined technology diplomacy across the government; expand technology training for foreign service officers; and, more ambitiously, launch a dedicated career track within the diplomatic corps for foreign technology officers.

Two smaller and often overlooked arms of the country’s technology diplomacy are the U.S. Foreign Commercial Service and the U.S. Trade and Development Agency (USTDA). The Commercial Service is a roughly 2,200-person global network of trade specialists that helps U.S. businesses identify and navigate foreign markets. But just 225 of its staff deploy abroad across 80 countries, which means that they constantly struggle to meet demand from U.S. technology companies and foreign partners. The USTDA helps identify and mature commercial opportunities abroad to boost U.S. exports. Digital infrastructure is one of the agency’s four priority sectors, but surging interest has far outpaced current resources.

The Trump administration can turbocharge U.S. commercial diplomacy by consolidating USTDA and the Commercial Service, elevating technology and digital infrastructure as a priority, and allocating more resources and personnel.

Finally, the United States should embrace a newly ambitious vision for technology partnerships. Too often, U.S. and allied firms lose one-off bids to subsidized, politically backed Chinese competitors, even if the firms might prefer to align with the high-tech U.S. ecosystem. Washington should explore how to make such an offer without simply imitating Beijing’s state-led model.

For example, Washington could create opportunities for foreign governments to request strategic technology partnerships that match their specific needs—for example, to accelerate AI adoption in government, expand data center capacity, or improve rural connectivity with low earth orbit satellites.

Washington could lay out clear, broadly consistent criteria as a condition for these partnerships—such as robust IP and cybersecurity protections, divestment from China-linked digital infrastructure, purchase commitments for U.S. goods and services, and even investment in the United States. The Trump administration has begun to model such an approach in its recent deals with Saudi Arabia and the United Arab Emirates, but it could go even further.

If countries meet these conditions, Washington should commit not only to loosening export controls on advanced AI chips, but also to fast-tracking support from the DFC, EXIM, and USTDA; expanding technology trade missions, talent exchange programs, and research collaboration; and facilitating connections with U.S. technology firms. The United States holds the strongest hand in advanced technology and should drive a hard bargain, but it should also be generous when countries agree.

Washington can also do more to align with technology-leading allies on joint investments in strategic emerging markets. For example, Washington could better coordinate with Japan’s Overseas Development Assistance program to boost Open RAN networks across the Indo-Pacific, tap the European Union’s Global Gateway to connect subsea cables to Africa, and support India’s Digital Public Infrastructure to counter China’s “smart city” offerings.

Middle Eastern sovereign wealth funds may raise tricky strategic questions as longer-term partners, but there are other, less controversial players that Washington has yet to fully explore—such as Norway, which has both attractive conditions for AI data centers and the world’s largest sovereign wealth fund. Washington and its allies may struggle to match Beijing’s subsidies on their own, but they can easily do so together.

As the world rushes into an accelerating competition to deploy strategic technologies and digital infrastructure across the globe, the United States has almost everything it needs to prevail—world-leading companies and products, an unrivaled network of technology-leading allies, and an administration eager for reform. What Washington lacks, however, is a vision to harness these strengths in a new model of technology statecraft to help the United States win.

3 notes

·

View notes

Text

KIOXIA Unveils 122.88TB LC9 Series NVMe SSD to Power Next-Gen AI Workloads

KIOXIA America, Inc. has announced the upcoming debut of its LC9 Series SSD, a new high-capacity enterprise solid-state drive (SSD) with 122.88 terabytes (TB) of storage, purpose-built for advanced AI applications. Featuring the company’s latest BiCS FLASH™ generation 8 3D QLC (quad-level cell) memory and a fast PCIe® 5.0 interface, this cutting-edge drive is designed to meet the exploding data demands of artificial intelligence and machine learning systems.

As enterprises scale up AI workloads—including training large language models (LLMs), handling massive datasets, and supporting vector database queries—the need for efficient, high-density storage becomes paramount. The LC9 SSD addresses these needs with a compact 2.5-inch form factor and dual-port capability, providing both high capacity and fault tolerance in mission-critical environments.

Form factor refers to the physical size and shape of the drive—in this case, 2.5 inches, which is standard for enterprise server deployments. PCIe (Peripheral Component Interconnect Express) is the fast data connection standard used to link components to a system’s motherboard. NVMe (Non-Volatile Memory Express) is the protocol used by modern SSDs to communicate quickly and efficiently over PCIe interfaces.

Accelerating AI with Storage Innovation

The LC9 Series SSD is designed with AI-specific use cases in mind—particularly generative AI, retrieval augmented generation (RAG), and vector database applications. Its high capacity enables data-intensive training and inference processes to operate without the bottlenecks of traditional storage.

It also complements KIOXIA’s AiSAQ™ technology, which improves RAG performance by storing vector elements on SSDs instead of relying solely on costly and limited DRAM. This shift enables greater scalability and lowers power consumption per TB at both the system and rack levels.

“AI workloads are pushing the boundaries of data storage,” said Neville Ichhaporia, Senior Vice President at KIOXIA America. “The new LC9 NVMe SSD can accelerate model training, inference, and RAG at scale.”

Industry Insight and Lifecycle Considerations

Gregory Wong, principal analyst at Forward Insights, commented:

“Advanced storage solutions such as KIOXIA’s LC9 Series SSD will be critical in supporting the growing computational needs of AI models, enabling greater efficiency and innovation.”

As organizations look to adopt next-generation SSDs like the LC9, many are also taking steps to responsibly manage legacy infrastructure. This includes efforts to sell SSD units from previous deployments—a common practice in enterprise IT to recover value, reduce e-waste, and meet sustainability goals. Secondary markets for enterprise SSDs remain active, especially with the ongoing demand for storage in distributed and hybrid cloud systems.

LC9 Series Key Features

122.88 TB capacity in a compact 2.5-inch form factor

PCIe 5.0 and NVMe 2.0 support for high-speed data access

Dual-port support for redundancy and multi-host connectivity

Built with 2 Tb QLC BiCS FLASH™ memory and CBA (CMOS Bonded to Array) technology

Endurance rating of 0.3 DWPD (Drive Writes Per Day) for enterprise workloads

The KIOXIA LC9 Series SSD will be showcased at an upcoming technology conference, where the company is expected to demonstrate its potential role in powering the next generation of AI-driven innovation.

2 notes

·

View notes

Text

Excerpt from this story from the Associated Press (AP):

Coal-fired power plants, long an increasingly money-losing proposition in the U.S., are becoming more valuable now that the suddenly strong demand for electricity to run Big Tech’s cloud computing and artificial intelligence applications has set off a full-on sprint to find new energy sources.

President Donald Trump — who has pushed for U.S. “energy dominance” in the global market and suggested that coal can help meet surging power demand — is wielding his emergency authority to entice utilities to keep older coal-fired plants online and producing electricity.

While some utilities were already delaying the retirement of coal-fired plants, the scores of coal-fired plants that have been shut down the past couple years — or will be shut down in the next couple years — are the object of growing interest from tech companies, venture capitalists, states and others competing for electricity.

That’s because they have a very attractive quality: high-voltage lines connecting to the electricity grid that they aren’t using anymore and that a new power plant could use.

That ready-to-go connection could enable a new generation of power plants — gas, nuclear, wind, solar or even battery storage — to help meet the demand for new power sources more quickly.

For years, the bureaucratic nightmare around building new high-voltage power lines has ensnared efforts to get permits for such interconnections for new power plants, said John Jacobs, an energy policy analyst for the Washington, D.C.-based Bipartisan Policy Center.

“They are very interested in the potential here. Everyone sort of sees the writing on the wall for the need for transmission infrastructure, the need for clean firm power, the difficulty with siting projects and the value of reusing brownfield sites,” Jacobs said.

2 notes

·

View notes

Text

Emulation

As a lover of retro video games and media in general, the topic of emulation plays a huge part in conversations around the hobby. I'm just a dude with a blog, so take any opinion here with a grain of salt, but I'm going to attempt to organize my thoughts here. I have heard and been a part of many conversations around the topic and I think it's something that deserves to be explored by any lover of classic media, especially video games. I believe, in short, that digital file backups are an incredible resource to preservationists. How I came to that conclusion, is the purpose of this post.

I'll begin in the summer of 2005, as I turn 16 and me and my friends get jobs and start driving, we're finding ourselves spending our hard earned dozens of dollars on Super Nintendo, GameBoy, Genesis, and PS1 games. There are 2 places close by us in a small town in South Carolina to find troves of classic games. The first place is the flea market, where vendors set up a booth or table and display their wares like an incredibly redneck trash convention; and the ONE retro gaming store in town. We spend the day searching through stacks of sunbleached and cigarette smoke stained SNES cartridges. The PS2, GameCube, and Xbox are hotter than summer on the equator, and many of the games from the old systems are dirt cheap. It didn't matter what game it was, it was usually less than ten bucks and you'd get at least a couple hours of fun out of it. It was during one of these trips that I saw my first real experience of collector pricing and video game inflation.

Marvel Vs. Capcom for PS1, behind a glass case next to some Japanese Castlevania game (I was this simple at the time, and that has become my favorite version of my favorite game in recent years) for Sega Saturn, and each game garnered a price much higher than any of the other games not held behind a piece of glass. I had to know why, and I wanted to know why that particular game was so expensive. I made the mistake of asking. In traditional early 2000s video game reseller style, a neck bearded "gentlesir" in a World of Warcraft t-shirt explained that the game was highly sought after and with not many copies printed, the laws of supply and demand obliged a higher price tag. I was appalled.

My best friend at the time, standing next to me, was almost offended by the mansplaination of the rising price of old games to us. The following week, he messaged me as soon as I logged onto AIM. "Fuck that nerd at the store, check this out" with a hyperlink below the text. That hyperlink was directed to a torrent of a file titled MarvelVSCapcom. My best friend then send me a .zip file with everything I needed to play that game on my Compaq Presario with Windows XP. That was game on. From then on, I would seek out the rarest and most sought after games. Games I had never heard of, and some I would never remember. The early days of PC emulation of classic consoles were a total blast.

The SNES, Genesis, and PS1 were able to be processed with a basic machine and you could get far into the games. I used this like my personal arcade for years. Then one day the old computer died, and I started off to college. I didn't particularly have any interest and instead viewed it as a hobby I'd grown out of. And that's where the post ends.

Of course, years later, I'll meet my partner, they'll convince me to get a Switch, and my love for the hobby would start all over again. The selling point? The retro emulators. I begin exploring some PS3 and XB360 era ports, but I'm here for the 16 bit blast processing of the Genesis emulator, and the classic Mario and Kirby titles for SNES. I never was an e shopper, though, and had no idea what some of these games I was seeing on the internet were.

This is where I should add that I am blessed with ASD\ADHD and I love research. I fell and injured my ankle in 2023 could not walk for 6 months. I decided to purchase Skyrim and Animal Crossing to bide my days while I recouped. One day I got bored and decided to see if any games were on sale. A particular bundle caught my eye. Gamedec and Dex \ 2 games for $1.99, and I said why not? And so began my hyper fixation on indie games in the eShop.

I will add that this is a very long story, but I will edit and speak more about this time period in future posts.

I tried many different indie games, and decided to try super Metroid for SNES on the NSO. I fell in love. The exploration. The feeling of being lost and hopeless in a strange place. The feeling of success when you find a new area or power up. There was something about this game that a lot of modern games didn't give me. It was more fun and exciting. I was hooked. So I began researching.

Joining a few FB groups, I learned about how people are emulating without a PC in the modern era. I dive and dive an learn more and more. I finally purchased a handheld device strictly for emulating classic games. I also have my old consoles, and am purchasing many of my favorite games from one of the MANY local video games stores in my small but growing city. I don't necessarily NEED to emulate if I can find the game for a reasonable price, right?

That brings us here. 2025. Used games are at an all time high. Used consoles? The ones you can find are going to hurt your wallet, especially for one in good condition. The ethical dilemma of spending hundreds of dollars on hardware and a disc to play Castlevania: Symphony Of The Night on PS1 is solved by simplying adding a couple files to your phone. With some game carts and CDs going for HUNDREDS or sometimes THOUSANDS of dollars, if all you want to do is play the game, I find it completely ethical to obtain a backup of the game file and play it. The developers and publishers don't get paid off the 2nd hand market. Sure, support your local game store, and if Chrono Trigger is $500 worth of fun, then spend the money. I cannot justify, personally, the $150+ price tag of many Sega Saturn games, and I don't expect others to, either. My final point is that until a) Video Game license holders allow reprints and republishing old games for modern consoles, or b) a streaming service like Spotify for classic games becomes available to the public, then we are left with option C) emulation.

The sentiment of Piracy is Preservation has been prevalent for a very long time. As an enjoyer of classic media from the 80s, 90s, and early 2000s, I have to know that much of my interaction will be through digital backups. Many of this media only exists via digital preservation. Until we have a digital library option for video games, I HIGHLY recommend experiencing these works of art the easiest way possible.

I must add that I do not recommend obtaining any digital backups in unethical or illegal means.

3 notes

·

View notes

Text

Why the Low Voltage Switchgear Market is Booming in 2025?

The low voltage switchgear market is growing rapidly in 2025 due to growth in electricity consumption, development of intelligent devices, and a strong emphasis on sustainability. Energy efficiency, digital transformation, and security are critical for industries and businesses, which leads to a high demand for new, robust, and intelligent switchgear. This article will discuss key drivers of market growth, emerging trends, and their impact on businesses and industries globally.

1. The Growing Demand for Electricity

Over the past few decades, the increasing demand for efficiency in power distribution systems has become ever imminent with the rise of general energy consumption. Rapid urban expansion, industrial development, and the emergence of data centers have been some of the major driving forces boosting the demand for low-voltage switchgear.

Global Electricity Demand on the Rise:

· The IEA projects electricity demand in developing nations will rise at a rate of 4% each year, as consumption steadily climbs.

· Data facilities and cloud computing require relentless power sources, amplifying the need for resilient switching equipment solutions capable of sustaining operations.

· The proliferation of electric vehicle charging points is compelling utilities to renovate distribution networks, ensuring functionality can accommodate increased demand.

Modernization spreads as industries broaden their scope, making electrically-reliable infrastructure an imperative; low voltage switchgear has become integral to conveying energy throughout the grid in a secure and effective manner.

2. Smart & Digital Switchgear: The Industry’s Future

Traditional switchgear technology has evolved rapidly with the integration of intelligent networking capabilities, making electrical distribution safer, more efficient, and easier to monitor remotely. The new digital switchgear incorporates IoT, AI, and cloud-based monitoring solutions to provide real-time insight into energy usage. This allows businesses to proactively optimize performance and reduce costs through more proactive maintenance strategies.

Major Developments in Intelligent Switchgear by 2025:

✅Online Sensor Networks: Constant telemetry from devices throughout the system helps pinpoint potential weaknesses before failures occur.

✅Self-learning Circuitry: AI-powered hardware and software automatically analyze usage patterns to forecast repairs, minimize outages, and heighten uptime.

✅Wireless Remote Management: Mobile apps and web dashboards give administrators off-site control over power flows to streamline usage according to need.

✅Modular Construction: Interchangeable, compact components facilitate scaling and retrofitting within varied infrastructure environments.

The shift toward automated smart grids and Industry 4.0 production is substantially contributing to the booming market for intelligent switchgear solutions. Widespread installation of these next-generation systems will transform electrical distribution networks.

3. Rising Emphasis on Energy Efficiency & Sustainability

Governments and industries worldwide have increasingly pushed for greener, more energy-efficient power solutions in recent years. This has led electrical equipment manufacturers to develop eco-friendly switchgear technologies that considerably minimize energy loss during transmission and help reduce overall carbon footprints.

Sustainable Advancements in Low Voltage Switchgear Design:

Alternative gases to SF6: Traditional switchgear commonly uses SF6 due to its insulating and arc-quenching capabilities, however this gas has an extremely high global warming potential. Many switchgear producers have since designed SF6-free solutions that substitute the highly potent SF6 with other gases that are safer for the environment.

Energy-Efficient Designs: Optimizing circuitry and components has allowed switchgear to conduct electricity with negligible power loss, enabling connected systems to leverage nearly every watt of power. Careful engineering further trims excess material use and redundant parts.

Renewable Energy Integration: Low voltage switchgear has become increasingly vital in smoothly and reliably integrating power from solar arrays and wind farms into existing electrical networks. Without robust switchgear management, it would be difficult for clean energy sources to efficiently feed power onto transmission lines.

With the implementation of more stringent energy performance mandates in countries worldwide, businesses have sound business reasons for upgrading outdated switchgear infrastructure with advanced low loss solutions both to adhere to regulations and lower long-term energy expenditures.

4. Increasing Investments in Infrastructure & Industrialization

Governments and private investors alike are pouring billions into ambitious infrastructure projects around the world, generating skyrocketing demand for reliable low voltage switchgear solutions. From towering commercial skyscrapers to sprawling industrial complexes, and expanding metro networks to bustling international airports — countless utilities depend on robust yet cost-effective switching systems to ensure continuity of operations.

🔹 Key Infrastructure Drivers Stimulating Growth:

🏗️ Smart Cities Uplift Life: Sweeping investments in digital urbanization are revolutionizing everyday living through connected infrastructure that elevates efficiency.

🏭 Manufacturing Marvels: Production powerhouses across the globe are scaling new heights, intensifying the necessity for advanced low voltage distribution controls to support increased capacity.

🚆 Transportation Transformations: Rapid progress in rail electrification and proliferation of electric vehicles for land and air are necessitating increasingly resilient switchgear designs.

As global development marches forth, low voltage switchgear has become mission critical in enabling commercial and industrial progress through reliable power distribution. The worldwide infrastructure renaissance is cementing its importance for years to come.

5. Safety & Regulatory Compliance Are Driving Upgrades

Governments and regulatory bodies are increasingly implementing strict compliance standards to safeguard electrical infrastructure and minimize hazards, compelling upgrades across many industries. Potential calamities resulting from power faults or failures necessitate vigilance in maintaining reliable and resilient systems.

New Safety Regulations in 2025:

⚡ Updated IEC & NEC Standards: Stringent low voltage switchgear specifications mandated to bolster protection.

⚡ Arc Fault Protection Technology: Novel solutions critical to curb risks of electrical ignitions and incidents.

⚡ Mandatory Energy Audits: Organizations now required to optimize distribution for both personnel and operational efficiency through audits.

With approaching deadlines to satisfy evolving regulations, operators are proactively replacing outdated switchgear to conform with mounting compliance demands, contributing to an accelerating industry transformation.

6. The Rise of Data Centers & Digital Transformation

The digital sphere fundamentally relies upon data hubs that necessitate constant power and exceedingly reliable electric frameworks. As distributed computing, man-made brainpower, and IoT reception develop exponentially, ventures are putting vigorously in cutting edge low voltage switches to ensure their foundation from energy blackouts which could bring about gigantic budgetary misfortunes.

24/7 control is essential for operations yet breakdowns prompt critical money related setbacks. To guarantee uptime, focal points utilize auxiliary switches for extra dependability and security alongside far off checking abilities through IoT innovations which empower ongoing following and administration from anywhere. With worldwide distributed computing selection quickening at a quickening pace, interest for top notch low voltage switches arriving at new statures to guarantee frameworks stay online consistently.

7. Competitive Market & Technological Advancements

The low voltage switchgear sector has seen remarkable changes and fierce competition between prestigious brands. Manufacturers are pouring resources into innovation to craft smarter, smaller, and affordable switchboard alternatives.

🔹 Notable Advancements by 2025:

⚙️ Solid-state systems promise enhanced performance and lessened upkeep. Long and compound sentences mix with short ones.

⚙️ Remote accessibility through wireless means permits control and tracking from afar.

⚙️ Self-mending grids using AI to immediately spot and amend problems, maintaining dependable power seamlessly. Complex automation alleviates faults autonomously for maximum uptime.

Conclusion: The Future of Low Voltage Switchgear Looks Bright

Low Voltage Switchgear is forecasted to experience market growth in the year 2025 due to the growing electricity consumption in countries, the rising applications of smart technologies, the increased implementation of sustainability practices, the expansive growth in various industries, and safety regulations. As these industries are gradually moving to energy-efficient, AI-powered, and environmentally friendly switchgears, this demand is expected to increase further.

5 notes

·

View notes

Text

India’s Tech Sector to Create 1.2 Lakh AI Job Vacancies in Two Years

India’s technology sector is set to experience a hiring boom with job vacancies for artificial intelligence (AI) roles projected to reach 1.2 lakh over the next two years. As the demand for AI latest technology increases across industries, companies are rapidly adopting advanced tools to stay competitive. These new roles will span across tech services, Global Capability Centres (GCCs), pure-play AI and analytics firms, startups, and product companies.

Following a slowdown in tech hiring, the focus is shifting toward the development of AI. Market analysts estimate that Indian companies are moving beyond Proof of Concept (PoC) and deploying large-scale AI systems, generating high demand for roles such as AI researchers, product managers, and data application specialists. “We foresee about 120,000 to 150,000 AI-related job vacancies emerging as Indian IT services ramp up AI applications,” noted Gaurav Vasu, CEO of UnearthInsight.

India currently has 4 lakh AI professionals, but the gap between demand and supply is widening, with job requirements expected to reach 6 lakh soon. By 2026, experts predict the number of AI specialists required will hit 1 million, reflecting the deep integration of AI latest technology into industries like healthcare, e-commerce, and manufacturing.

The transition to AI-driven operations is also altering the nature of job vacancies. Unlike traditional software engineering roles, artificial intelligence positions focus on advanced algorithms, automation, and machine learning. Companies are recruiting experts in fields like deep learning, robotics, and natural language processing to meet the growing demand for innovative AI solutions. The development of AI has led to the rise of specialised roles such as Machine Learning Engineers, Data Scientists, and Prompt Engineers.

Krishna Vij, Vice President of TeamLease Digital, remarked that new AI roles are evolving across industries as AI latest technology becomes an essential tool for product development, operations, and consulting. “We expect close to 120,000 new job vacancies in AI across different sectors like finance, healthcare, and autonomous systems,” he said.

AI professionals also enjoy higher compensation compared to their traditional tech counterparts. Around 80% of AI-related job vacancies offer premium salaries, with packages 40%-80% higher due to the limited pool of trained talent. “The low availability of experienced AI professionals ensures that artificial intelligence roles will command attractive pay for the next 2-3 years,” noted Krishna Gautam, Business Head of Xpheno.

Candidates aiming for AI roles need to master key competencies. Proficiency in programming languages like Python, R, Java, or C++ is essential, along with knowledge of AI latest technology such as large language models (LLMs). Expertise in statistics, machine learning algorithms, and cloud computing platforms adds value to applicants. As companies adopt AI latest technology across domains, candidates with critical thinking and AI adaptability will stay ahead so it is important to learn and stay updated with AI informative blogs & news.

Although companies are prioritising experienced professionals for mid-to-senior roles, entry-level job vacancies are also rising, driven by the increased use of AI in enterprises. Bootcamps, certifications, and academic programs are helping freshers gain the skills required for artificial intelligence roles. As AI development progresses, entry-level roles are expected to expand in the near future. AI is reshaping the industries providing automation & the techniques to save time , to increase work efficiency.

India’s tech sector is entering a transformative phase, with a surge in job vacancies linked to AI latest technology adoption. The next two years will witness fierce competition for AI talent, reshaping hiring trends across industries and unlocking new growth opportunities in artificial intelligence. Both startups and established companies are racing to secure talent, fostering a dynamic landscape where artificial intelligence expertise will be help in innovation and growth. AI will help organizations and businesses to actively participate in new trends.

#aionlinemoney.com

2 notes

·

View notes

Text

Introducing Samsung 24GB GDDR7 DRAM For AI Computing

24GB GDDR7 DRAM

Future AI Computing: Samsung Launches 24GB GDDR7 DRAM. It sets the standard for graphics DRAM with its industry-leading capacity and performance of over 40Gbps.

First 24-gigabit (Gb) GDDR7 DRAM from memory pioneer Samsung was revealed today. Next-generation applications benefit from it’s speed and capacity. Data centers, AI workstations, graphics cards, gaming consoles, and autonomous driving will employ the 24Gb GDDR7 because to its high capacity and excellent performance.

“By introducing next-generation products that meet the expanding demands of the AI market, it will maintain to leadership position in the graphics DRAM market.” The 5th-generation 10-nanometer (nm)-class DRAM used in the 24Gb GDDR7 allows for a 50% increase in cell density while keeping the same package size as the previous model.

The industry-leading graphics DRAM performance of 40 gigabits per second (Gbps), a 25% increase over the previous iteration, is achieved in part by the advanced process node and three-level Pulse-Amplitude Modulation (PAM3) signaling. The performance of it may be further improved to 42.5 Gbps, contingent on the environment in which it is used.

Applying technology previously used in mobile devices to graphics DRAM for the first time also improves power efficiency. Power efficiency may be increased by more than 30% by reducing needless power use via the use of techniques like dual VDD design and clock control management.

The 24Gb GDDR7 uses power gating design approaches to reduce current leakage and increase operational stability during high-speed operations.

Major GPU customers will start validating the 24Gb GDDR7 in next-generation AI computing systems this year, with intentions to commercialize the technology early the next year.

GDDR6 vs GDDR7

Compared to the current 24Gbps GDDR6 DRAM, GDDR7 offers a 20% increase in power efficiency and a 1.4-fold increase in performance.

Today, Samsung Electronics, a global leader in cutting-edge semiconductor technology, said that it has finished creating the first Graphics Double Data Rate 7 (GDDR7) DRAM in the market. This year, it will be first placed in important clients’ next-generation systems for validation, propelling the graphics market’s future expansion and solidifying Samsung’s technical leadership in the industry.

Samsung’s 16-gigabit (Gb) GDDR7 DRAM will provide the fastest speed in the industry to date, after the introduction of the first 24Gbps GDDR6 DRAM in 2022. Despite high-speed operations, new developments in integrated circuit (IC) design and packaging provide more stability.

With a boosted speed per pin of up to 32Gbps, Samsung’s GDDR7 reaches a remarkable 1.5 terabytes per second (TBps), which is 1.4 times that of GDDR6’s 1.1 TBps. The improvements are made feasible by the new memory standard’s use of the Pulse Amplitude Modulation (PAM3) signaling technique rather than the Non Return to Zero (NRZ) from earlier generations. Compared to NRZ, PAM3 enables 50% greater data transmission in a single signaling cycle.

Notably, using power-saving design technologies tailored for high-speed operations, the most recent architecture is 20% more energy efficient than GDDR6. Samsung provides a low-operating voltage option for devices like laptops that are particularly concerned about power consumption.

In addition to optimizing the IC design, the packaging material uses an epoxy molding compound (EMC) with good thermal conductivity to reduce heat production. Compared to GDDR6, these enhancements significantly lower heat resistance by 70%, ensuring reliable product performance even under high-speed operating settings.

GDDR7 Release Date

According to Samsung, commercial manufacturing of their 24GB GDDR7 DRAM is scheduled to begin in early 2024. Although the precise public release date is yet unknown, this year’s certification process with major GPU manufacturers is already under way. With the availability of next-generation GPUs that will support the new memory standard, GDDR7 DRAM is now expected to be readily accessible in the market by 2024.

Read more on Govindhtech.com

#Samsung#Samsung24GBGDDR7#GDDR7DRAM#24GBGDDR7DRAM#DRAM#GDDR6DRAM#GPU#AI#News#Technews#Technology#Technologynews#Technologytrends#govindhtech

3 notes

·

View notes

Text

FPGA Market - Exploring the Growth Dynamics

The FPGA market is witnessing rapid growth finding a foothold within the ranks of many up-to-date technologies. It is called versatile components, programmed and reprogrammed to perform special tasks, staying at the fore to drive innovation across industries such as telecommunications, automotive, aerospace, and consumer electronics. Traditional fixed-function chips cannot be changed to an application, whereas in the case of FPGAs, this can be done. This brings fast prototyping and iteration capability—extremely important in high-flux technology fields such as telecommunications and data centers. As such, FPGAs are designed for the execution of complex algorithms and high-speed data processing, thus making them well-positioned to handle the demands that come from next-generation networks and cloud computing infrastructures.

In the aerospace and defense industries, FPGAs have critically contributed to enhancing performance in systems and enhancing their reliability. It is their flexibility that enables the realization of complex signal processing, encryption, and communication systems necessary for defense-related applications. FPGAs provide the required speed and flexibility to meet the most stringent specifications of projects in aerospace and defense, such as satellite communications, radar systems, and electronic warfare. The ever-improving FPGA technology in terms of higher processing power and lower power consumption is fueling demand in these critical areas.

Consumer electronics is another upcoming application area for FPGAs. From smartphones to smart devices, and finally the IoT, the demand for low-power and high-performance computing is on the rise. In this regard, FPGAs give the ability to integrate a wide array of varied functions onto a single chip and help in cutting down the number of components required, thereby saving space and power. This has been quite useful to consumer electronics manufacturers who wish to have state-of-the-art products that boast advanced features and have high efficiency. As IoT devices proliferate, the role of FPGAs in this area will continue to foster innovation.

Growing competition and investments are noticed within the FPGA market, where key players develop more advanced and efficient products. The performance of FPGAs is increased by investing in R&D; the number of features grows, and their cost goes down. This competitive environment is forcing innovation and a wider choice availability for end-users is contributing to the growth of the whole market.

Author Bio -

Akshay Thakur

Senior Market Research Expert at The Insight Partners

2 notes

·

View notes

Text

elsewhere on the internet: AI and advertising

Bubble Trouble (about AIs trained on AI output and the impending model collapse) (Ed Zitron, Mar 2024)

A Wall Street Journal piece from this week has sounded the alarm that some believe AI models will run out of "high-quality text-based data" within the next two years in what an AI researcher called "a frontier research problem." Modern AI models are trained by feeding them "publicly-available" text from the internet, scraped from billions of websites (everything from Wikipedia to Tumblr, to Reddit), which the model then uses to discern patterns and, in turn, answer questions based on the probability of an answer being correct. Theoretically, the more training data that these models receive, the more accurate their responses will be, or at least that's what the major AI companies would have you believe. Yet AI researcher Pablo Villalobos told the Journal that he believes that GPT-5 (OpenAI's next model) will require at least five times the training data of GPT-4. In layman's terms, these machines require tons of information to discern what the "right" answer to a prompt is, and "rightness" can only be derived from seeing lots of examples of what "right" looks like. ... One (very) funny idea posed by the Journal's piece is that AI companies are creating their own "synthetic" data to train their models, a "computer-science version of inbreeding" that Jathan Sadowski calls Habsburg AI. This is, of course, a terrible idea. A research paper from last year found that feeding model-generated data to models creates "model collapse" — a "degenerative learning process where models start forgetting improbable events over time as the model becomes poisoned with its own projection of reality."

...

The AI boom has driven global stock markets to their best first quarter in 5 years, yet I fear that said boom is driven by a terrifyingly specious and unstable hype cycle. The companies benefitting from AI aren't the ones integrating it or even selling it, but those powering the means to use it — and while "demand" is allegedly up for cloud-based AI services, every major cloud provider is building out massive data center efforts to capture further demand for a technology yet to prove its necessity, all while saying that AI isn't actually contributing much revenue at all. Amazon is spending nearly $150 billion in the next 15 years on data centers to, and I quote Bloomberg, "handle an expected explosion in demand for artificial intelligence applications" as it tells its salespeople to temper their expectations of what AI can actually do. I feel like a crazy person every time I read glossy pieces about AI "shaking up" industries only for the substance of the story to be "we use a coding copilot and our HR team uses it to generate emails." I feel like I'm going insane when I read about the billions of dollars being sunk into data centers, or another headline about how AI will change everything that is mostly made up of the reporter guessing what it could do.

They're Looting the Internet (Ed Zitron, Apr 2024)

An investigation from late last year found that a third of advertisements on Facebook Marketplace in the UK were scams, and earlier in the year UK financial services authorities said it had banned more than 10,000 illegal investment ads across Instagram, Facebook, YouTube and TikTok in 2022 — a 1,500% increase over the previous year. Last week, Meta revealed that Instagram made an astonishing $32.4 billion in advertising revenue in 2021. That figure becomes even more shocking when you consider Google's YouTube made $28.8 billion in the same period . Even the giants haven’t resisted the temptation to screw their users. CNN, one of the most influential news publications in the world, hosts both its own journalism and spammy content from "chum box" companies that make hundreds of millions of dollars driving clicks to everything from scams to outright disinformation. And you'll find them on CNN, NBC and other major news outlets, which by proxy endorse stories like "2 Steps To Tell When A Slot Is Close To Hitting The Jackpot." These “chum box” companies are ubiquitous because they pay well, making them an attractive proposition for cash-strapped media entities that have seen their fortunes decline as print revenues evaporated. But they’re just so incredibly awful. In 2018, the (late, great) podcast Reply All had an episode that centered around a widower whose wife’s death had been hijacked by one of these chum box advertisers to push content that, using stolen family photos, heavily implied she had been unfaithful to him. The title of the episode — An Ad for the Worst Day of your Life — was fitting, and it was only until a massively popular podcast intervened did these networks ban the advert. These networks are harmful to the user experience, and they’re arguably harmful to the news brands that host them. If I was working for a major news company, I’d be humiliated to see my work juxtaposed with specious celebrity bilge, diet scams, and get-rich-quick schemes.

...

While OpenAI, Google and Meta would like to claim that these are "publicly-available" works that they are "training on," the actual word for what they're doing is "stealing." These models are not "learning" or, let's be honest, "training" on this data, because that's not how they work — they're using mathematics to plagiarize it based on the likelihood that somebody else's answer is the correct one. If we did this as a human being — authoritatively quoting somebody else's figures without quoting them — this would be considered plagiarism, especially if we represented the information as our own. Generative AI allows you to generate lots of stuff from a prompt, allowing you to pretend to do the research much like LLMs pretend to know stuff. It's good for cheating at papers, or generating lots of mediocre stuff LLMs also tend to hallucinate, a virtually-unsolvable problem where they authoritatively make incorrect statements that creates horrifying results in generative art and renders them too unreliable for any kind of mission critical work. Like I’ve said previously, this is a feature, not a bug. These models don’t know anything — they’re guessing, based on mathematical calculations, as to the right answer. And that means they’ll present something that feels right, even though it has no basis in reality. LLMs are the poster child for Stephen Colbert’s concept of truthiness.

3 notes

·

View notes

Text

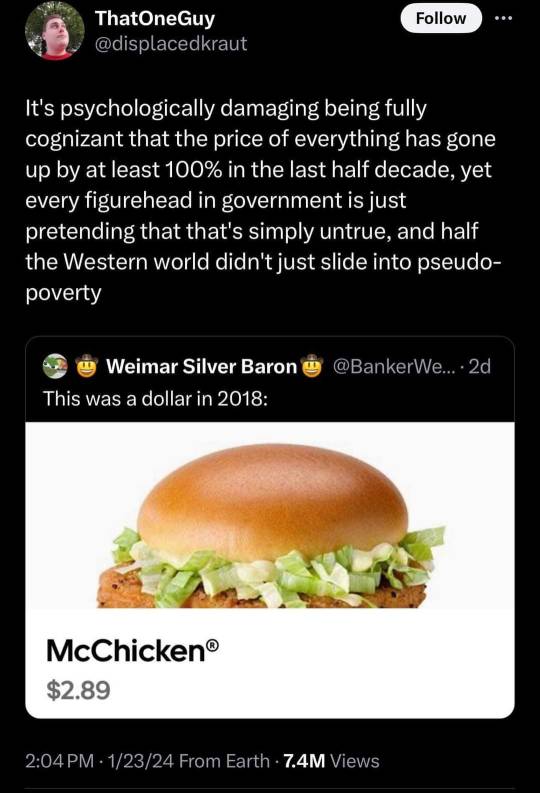

All of this said, remember that economic metrics (including price of goods at market) often are bundles (aggregates) of all economics activity that fits certain criteria. So, in other words, a change in one area will affect a portion or sector of the economy. But also, it affects the whole (even if slight). And this is on multiple levels economically, due to multiple companies all trying to operate and dominate over each other in all industries. This is further amplified by tiered types of products (economy, value sized, premium, luxury, quick service vs fine dining, etc.)

Example: food prices have risen generally. Like @weshallbekind said, certain foods increase some don't. Gas and certain new cars have higher prices, some haven't. Of course something like gas, however, is an everyday good, as are many food items. These essential items having increased prices is a component of inflation (as are interest rates, unemployment, speculation booms, currency changes, etc. different rant though). Again, aggregates, so potentially many factors. But aggregates don't reflect capitalism's main goal. Instead these aggregates are used as tools to accomplish said goal.

Keep in mind, however, that this is why capitalism like ours inherently doesn't work. It seeks to minimize costs (see also: not paying for enough workers, vertical integration, flip flopping between self check out and cashiers, moving/outsourcing, and raising prices [despite having massive economies of scale and the ability to negotiate]) for the benefit of profit. Not progress and profit, not progress, not satisfying the customers needs and wants; profit.

What does this mean then? It means profit over everything, while also creating desires in you (via marketing) to buy things you don't really need (mostly) or into which you invest your personality, time, or data. But mostly your money. Now, of course, everyone needs food, shelter, miscellaneous tools and safeguards, etc. Now those things are regulated to some degree, but nonetheless goods sold and marketed to you to profit.

Therefore, anything to make profit and make you buy it regularly could at least be attempted. Pay undocumented citizens pennies on the dollar so you don't have to give them benefits, minimum wage, or rights, check. Purposefully not include the charger and cable needed to use the phone, check. Use surge pricing to maximize profit and stress the existing infrastructure (human or otherwise), check. Overcharge you for literally the same exact product by calling it something fancy and putting their label on it, check.

And sure, of course costs increase. Of course paying people more means higher costs, especially if "times are tough". You know what takes more priority, usually, though? Executive compensation ratios, cash reserves, market dominance, mergers and acquisitions, vertical integration, lobbying, tax benefits.

Once again, let me remind you: metrics are aggregates, statistics, and computations based on demand, supply, input costs, interest rates, taxes, preferences, laws, availability of resources, currency exchange rates, speculation booms, etc. All these metrics and their formulas, however, are used (by corporations) to find their way to massive profits. By using these metrics in manipulating the market and their business practices, they're working to profit; they're striving for greater capital than the next company. Always.

#also#technically i would call USA capitalism corporatism#Adam Smith wasn't talking about Amazon when he talked about markets#he was talking about literal open air markets where you sell to the customer their daily necessities#small corporations (like my dad is a small town private practice lawyer) are fine#not companies that own most of their competition and lobby government#like im all for a free market with regulation clear effective and fair tax structures#I'm also down for small businesses and larger business agreements or alliances#also co-ops non-profits whatever#but no corporations#my dad isn't lobbying congress or manipulating stock prices#he's just a guy who wants to make sure he and his family can enjoy their life

70K notes

·

View notes

Text

Data Center Market Forecast & Growth Trends

The global data center market was valued at USD 347.60 billion in 2024 and is expected to reach USD 652.01 billion by 2030, expanding at a robust compound annual growth rate (CAGR) of 11.2% from 2025 to 2030. This growth is primarily driven by the exponential surge in data generation across various sectors, fueled by widespread digital transformation initiatives and the increasing adoption of advanced technologies such as cloud computing, artificial intelligence (AI), machine learning (ML), and the Internet of Things (IoT).

As organizations generate and process vast volumes of data, the demand for scalable, secure, and energy-efficient data center infrastructure has intensified. Enterprises are seeking agile and resilient IT architectures to support evolving business needs and digital services. This has led to the rapid expansion of data center capacity worldwide, with a particular focus on hyperscale and colocation facilities.

Hyperscale data center operators—including major players such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud—are continuously scaling their infrastructure to meet global demands for cloud storage, computing power, and data processing. These tech giants are making substantial investments in constructing new data centers and upgrading existing ones to ensure seamless service delivery, latency reduction, and improved data security.

Simultaneously, the colocation segment is gaining momentum as businesses pursue cost-effective solutions to manage IT infrastructure. Colocation centers offer shared facilities equipped with high-speed connectivity, advanced cooling systems, and robust physical and cyber security. These benefits allow companies—especially small and medium enterprises—to scale their operations flexibly without the high capital expenditure required to build and maintain in-house data centers.

Another major trend accelerating market growth is the rise of edge computing. As the number of IoT devices and real-time applications grows, there is an increasing need for decentralized computing infrastructure. Edge data centers, located closer to end-users and data sources, provide reduced latency and faster response times—critical for applications in sectors such as autonomous vehicles, remote healthcare, industrial automation, and smart cities.

Key Market Trends & Insights

In 2024, North America dominated the global data center market with a share of over 40.0%, propelled by the widespread adoption of cloud services, AI-powered applications, and big data analytics across industries.

The United States data center market is anticipated to grow at a CAGR of 10.7% between 2025 and 2030, driven by continued digital innovation, enterprise cloud adoption, and the expansion of e-commerce and fintech platforms.

On the basis of components, the hardware segment accounted for the largest market share of more than 67.0% in 2024. The surge in online content consumption, social networking, digital transactions, and IoT connectivity has significantly boosted demand for high-capacity, high-performance hardware.

Within the hardware category, the server segment emerged as the market leader, contributing over 34.0% to revenue in 2024. Modern servers are being equipped with enhanced processing power, memory, and storage efficiency, all of which are crucial to supporting next-generation computing needs.

Among software solutions, the virtualization segment held a dominant share of nearly 18.0% in 2024. Virtualization allows data centers to maximize hardware utilization by enabling multiple virtual machines (VMs) to operate on a single physical server, reducing costs and increasing operational flexibility.

Order a free sample PDF of the Data Center Market Intelligence Study, published by Grand View Research.

Market Size & Forecast

2024 Market Size: USD 347.60 Billion

2030 Projected Market Size: USD 652.01 Billion

CAGR (2025-2030): 11.2%

North America: Largest market in 2024

Asia Pacific: Fastest growing market

Key Companies & Market Share Insights

Key players operating in the data center industry are Amazon Web Services (AWS), Inc. Microsoft, Google Cloud, Alibaba Cloud, and Equinix, Inc. The companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

In February 2025, Alibaba Cloud, the digital technology arm of Alibaba Group, opened its second data center in Thailand to meet the growing demand for cloud computing services, particularly for generative AI applications. The new facility enhances local capacity and aligns with the Thai government's efforts to promote digital innovation and sustainable technology. Offering a range of services including elastic computing, storage, databases, security, networking, data analytics, and AI solutions, the data center aims to address industry-specific challenges.

In December 2024, Amazon Web Services (AWS) introduced redesigned data center infrastructure to accommodate the growing demands of artificial intelligence (AI) and sustainability. The updates features advancements in liquid cooling, power distribution, and rack design, enabling a sixfold increase in rack power density over the next two years. AWS stated that these enhancements aims to deliver a 12% boost in compute power per site, improve energy efficiency, and enhance system availability.

In May 2024, Equinix, Inc. launched its first two data centers in Malaysia, with the International Business Exchange (IBX) facilities now operational in Johor and Kuala Lumpur. The facilities are intended to cater to Equinix Inc.'s customers in Malaysia while enhancing regional connectivity.

Key Players

Alibaba Cloud

Amazon Web Services, Inc.

AT&T Intellectual Property

Lumen Technologies (CenturyLink)

China Telecom Americas, Inc.

CoreSite

CyrusOne

Digital Realty

Equinix, Inc.

Google Cloud

IBM Corporation

Microsoft

NTT Communications Corporation

Oracle

Tencent Cloud

Browse Horizon Databook on Global Data Center Market Size & Outlook

Conclusion

The global data center market is undergoing rapid expansion, driven by the growing digital economy, technological advancements, and the ever-increasing demand for data storage, computing power, and connectivity. Hyperscale and colocation facilities are at the forefront of this transformation, offering scalable and secure infrastructure that supports cloud computing, AI workloads, and real-time applications. Edge computing is further reshaping the landscape by bringing processing capabilities closer to data sources, enabling faster and more efficient services across various industries.

As the market continues to evolve, investment in energy-efficient hardware, software virtualization, and regional data center development will be critical to meeting future demands. Companies that adopt flexible, sustainable, and innovation-driven data infrastructure strategies will be best positioned to capitalize on the tremendous growth opportunities in the data center space over the coming years.

0 notes

Text

Data Analytics with AI in 2025: Trends, Impact & What’s Next

As we move deeper into 2025, the fusion of Artificial Intelligence (AI) and data analytics has become more than a competitive edge—it's a business necessity. Companies that once viewed AI as experimental are now embedding it into the core of their operations, using it to transform raw data into real-time insights, accurate forecasts, and automated decisions.

In this post, we’ll explore how AI-powered data analytics is evolving in 2025, what trends are shaping the future, and how your organization can harness its full potential.

What Is AI-Driven Data Analytics?

AI-driven data analytics uses intelligent algorithms—such as machine learning (ML), deep learning, and natural language processing—to discover hidden patterns, predict future trends, and automate insights from vast and complex datasets.

Unlike traditional analytics, AI doesn’t just report on what happened; it explains why it happened and suggests what to do next—with unprecedented speed and precision.

Key Trends in 2025

1. Real-Time AI Analytics

Thanks to edge computing and faster cloud processing, AI analytics is now happening in real time. Businesses can react to customer behavior, supply chain issues, and financial trends instantly.

2. AI + Business Intelligence Platforms

Modern BI tools like Tableau, Power BI, and Looker now offer built-in AI features—from auto-generated visual insights to natural language queries (e.g., “Why did sales drop in Q1?”).

3. Predictive + Prescriptive Analytics

AI doesn’t just forecast future outcomes—it now recommends specific actions. For instance, AI can predict customer churn and suggest retention campaigns tailored to individual users.

4. Natural Language Insights

Non-technical users can now interact with data using plain English. Think: “Show me the top 5 products by revenue in the last 90 days.”

5. Ethical AI and Data Governance

With growing concerns about bias and data privacy, 2025 emphasizes explainable AI and strong data governance policies to ensure compliance and transparency.

Use Cases by Industry

Retail & E-commerce: Personalized shopping experiences, dynamic pricing, demand forecasting

Finance: Fraud detection, credit risk analysis, algorithmic trading

Healthcare: Diagnostic analytics, patient risk prediction, treatment optimization

Manufacturing: Predictive maintenance, quality control, supply chain optimization

Marketing: Customer segmentation, sentiment analysis, campaign optimization

Benefits of AI in Data Analytics

Faster Insights: Analyze billions of data points in seconds

Smarter Forecasting: Anticipate trends with high accuracy

Cost Reduction: Automate repetitive analysis and reporting

Enhanced Decision-Making: Make strategic choices based on real-time, AI-enhanced insights

Personalization at Scale: Serve your customers better with hyper-relevant experiences

Challenges to Watch

Data Quality: AI requires clean, consistent, and well-labeled data

Talent Gap: Skilled AI/ML professionals are still in high demand

Ethics & Bias: AI models must be monitored to avoid reinforcing social or business biases

Integration Complexity: Aligning AI tools with legacy systems takes planning and expertise

What’s Next for AI & Analytics?

By late 2025 and beyond, expect:

More autonomous analytics platforms that self-learn and self-correct

Increased use of generative AI to automatically create dashboards, summaries, and even business strategies

Tighter integration between IoT, AI, and analytics for industries like smart cities, healthcare, and logistics

Final Thoughts

In 2025, AI in data analytics is no longer just a tool—it's a strategic partner. Whether you're optimizing operations, enhancing customer experiences, or driving innovation, AI analytics gives you the insights you need to lead with confidence.

📩 Ready to transform your data into business intelligence? Contact us to learn how our AI-powered analytics solutions can help you stay ahead in 2025 and beyond.

#Data Analytics#Artificial Intelligence#AI in Business#Business Intelligence#Predictive Analytics#Big Data#Machine Learning#Data Science#Real-Time Analytics#AI Trends 2025

0 notes

Text

Point of Load Power Chip Market: Opportunities in Commercial and Residential Sectors

MARKET INSIGHTS

The global Point of Load Power Chip Market size was valued at US$ 1,340 million in 2024 and is projected to reach US$ 2,450 million by 2032, at a CAGR of 9.27% during the forecast period 2025-2032. This growth trajectory follows a broader semiconductor industry trend, where the worldwide market reached USD 580 billion in 2022 despite macroeconomic headwinds.

Point-of-load (PoL) power chips are voltage regulator ICs designed for localized power conversion near high-performance processors, FPGAs, and ASICs. These compact solutions provide precise voltage regulation, improved transient response, and higher efficiency compared to centralized power architectures. Key variants include single-channel (dominant with 65% market share) and multi-channel configurations, deployed across industrial (32% share), automotive (25%), and aerospace (18%) applications.