#U.S. Hospital Facilities market size

Text

According to Nova one advisor, The U.S. Hospital Facilities market size was valued at US$ 1,318.9 billion in 2021 and is expected to hit US$ 2,540.7 billion by 2030, growing at a compound annual growth rate (CAGR) of 7.65% from 2022 to 2030.

0 notes

Text

By Ralph Nader

Common Dreams

October 29, 2023

The message of Israeli peace groups’ peaceful solutions are drowned out by the media’s addiction to interviews with military tacticians.

In the midst of extensive coverage of the war in Gaza, there are questions that the U.S. mass media should address:

1. How did Hamas, with tiny Gaza surrounded by a 17-year Israeli blockade, subjected to unparalleled electronic surveillance, with spies and informants, and augmented by an overwhelming air, sea, and land military presence, manage to get these weapons and associated technology for their October 7 surprise raid?

2. What is the connection between the stunning failure of the Israeli government to protect its people on the border and the policy of Prime Minister Benjamin Netanyahu? Recall TheNew York Times (October 22, 2023) article by prominent journalist, Roger Cohen, to wit: “All means were good to undo the notion of Palestinian statehood. In 2019, Mr. Netanyahu told a meeting of his center-right Likud party: ‘Those who want to thwart the possibility of a Palestinian state should support the strengthening of Hamas and the transfer of money to Hamas. This is part of our strategy.’” (Note: Israel and the U.S. fostered the rise of Islamic Hamas in 1987 to counter the secular Palestine Liberation Organization (PLO)).

3. Why is Congress preparing to appropriate over $14 billion to Israel in military and other aid without any public hearings and without any demonstrated fiscal need by Israel, a prosperous economic, technological, and military superpower with a social safety net superior to that of the U.S.? USDA just reported over 44 million Americans struggled with hunger in 2022. This, in the midst of a childcare crisis. Should U.S. taxpayers be expected to pay for Netanyahu’s colossal intelligence/military collapse?

Under international law, Biden has made the U.S. an active “co-belligerent” of the Israeli government’s vocal demolition of the 2.3 million inhabitants in Gaza, who are mostly descendants of Palestinian refugees driven from their homes in 1948.

4. Why hasn’t the media reported on President Joe Biden’s statement that the Gaza Health Ministry’s body count (now over 7,000 fatalities) is exaggerated? All indications, however, are that it is a large undercount by Hamas to minimize its inability to protect its people. Israel has fired over 8,000 powerful precision munitions and bombs so far. These have struck many thousands of inhabited buildings—homes, apartments buildings, over 120 health facilities, ambulances, crowded markets, fleeing refugees, schools, water and sewage systems, and electric networks—implementing Israeli military orders to cut off all food, water, fuel, medicine, and electricity to this already impoverished densely packed area the size of Philadelphia. For those not directly slain, the deadly harm caused by no food, water, medicine, medical facilities, and fuel will lead to even more deaths and serious injuries.

Note that over three-quarters of Gaza’s population consists of children and women. Soon there will be thousands of babies born to die in the rubble. Other Palestinians will perish from untreated diseases, injuries, dehydration, and from drinking contaminated water. With crumbled sanitation facilities, physicians are fearing a deadly cholera epidemic.

Israel bombed the Rafah crossing on the Gaza-Egypt border. Only a tiny trickle of trucks are now allowed there by Israel to carry food and water. Fuel for hospital generators still remains blocked.

5. Why can’t Biden even persuade Israel to let 600 desperate Americans out of the Gaza firestorm?

6. Why isn’t the mass media making a bigger issue out of Israel’s long-time practices of blocking journalists from entering Gaza, including European, American, and Israeli journalists? The only television crews left are Gazan-residing Al Jazeera reporters. Israeli bombs have already killed 26 journalists in the Gaza Strip since October 7th. Is Israel targeting journalists’ families? Gaza bureau chief of Al Jazeera Wael Al-Dahdouh’s family was killed in an Israeli airstrike on Wednesday.

Historians remind us that in a gridlocked conflict over time, it is the most powerful party’s responsibility to lead the way to peace.

7. Why isn’t the mainstream U.S. media giving adequate space and voice to groups advocating a cease-fire and humanitarian aid? The message of Israeli peace groups’ peaceful solutions are drowned out by the media’s addiction to interviews with military tacticians. Much time and space are being given to hawks pushing for a war that could flash outside of Gaza big time. Shouldn’t groups such as Jewish Voice for Peace, the Arab-American Institute, Veterans for Peace, and associations of clergy have their views and activities reported?

8. Why is the coverage of the war overlooking the Geneva Conventions, the United Nations Charter, and the many provisions of international law that all the parties, including the U.S., have been violating? (See the October 24, 2023 letter to President Biden). Under international law, Biden has made the U.S. an active “co-belligerent” of the Israeli government’s vocal demolition of the 2.3 million inhabitants in Gaza, who are mostly descendants of Palestinian refugees driven from their homes in 1948. (See, Convention on the Prevention and Punishment of the Crime of Genocide).

9. What about the human-interest stories that would be revealing? For example: How do Israeli F-16 pilots feel about their daily bombing of the completely defenseless Gazan civilian population and its life-sustaining infrastructures? What are the courageous Israeli human rights and refuseniks thinking and doing in a climate of serious repression of their views as a result of Netanyahu’s defense collapse on October 7?

10. Where is the media attention on the statements from Israeli military commentators, who, for years have declared high-tech U.S.-backed, nuclear-armed Israel to be more secure than at any time in its history? Israel is reasserting its overwhelming military domination of the entire region, fully backed by U.S. militarism.

Historians remind us that in a gridlocked conflict over time, it is the most powerful party’s responsibility to lead the way to peace.

Establishing a two-state solution has been supported by Palestinians. All the Arab nations, starting with the Arab League peace proposal in 2002, support this solution as well. It is up to Israel and the U.S., assuming annexation of what is left of Palestine is not Israel’s objective. (See, the March 29, 2002 New York Times article: “Mideast Turmoil; Text of the Peace Proposals Backed by the Arab League”).

More media attention on this subject matter is much needed.

#israel#palestine#gaza#hamas#benjamin netanyahu#joe biden#human rights#genocide#war crimes#journalism#media

141 notes

·

View notes

Text

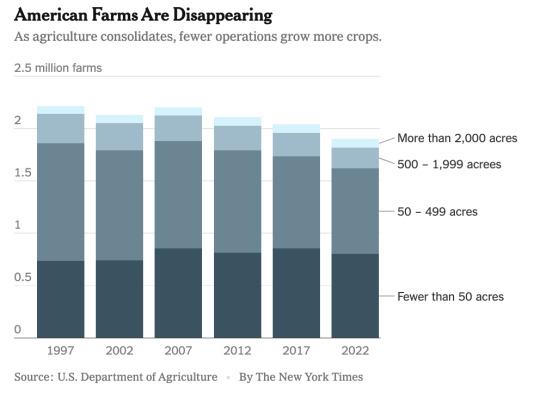

Excerpt from this story from the New York Times:

Agriculture Secretary Tom Vilsack has a line about the state of small-scale agriculture in America these days.

It’s drawn from the National Agricultural Statistics Service, which shows that as the average size of farms has risen, the nation had lost 544,000 of them since 1981.

“That’s every farm today that exists in North Dakota and South Dakota, added to those in Wisconsin and Minnesota, added to those in Nebraska and Colorado, added to those in Oklahoma and Missouri,” Mr. Vilsack told a conference in Washington this spring. “Are we as a country OK with it?”

Even though the United States continues to produce more food on fewer acres, Mr. Vilsack worries that the loss of small farmers has weakened rural economies, and he wants to stop the bleeding. Unlike his last turn in the same job, under former President Barack Obama, this time his department is able to spend billions of dollars in subsidies and incentives passed under three major laws since 2021 — including the biggest investment in conservation programs in U.S. history.

The plan in a nutshell: Multiply and improve revenue streams to bolster farm balance sheets. Rather than just selling crops and livestock, farms of the future could also sell carbon credits, waste products and renewable energy.

“Instead of the farm getting one check, they potentially could get four checks,” Mr. Vilsack said in an interview. He is also helping schools, hospitals and other institutions to buy food grown locally, and investors to build meatpacking plants and other processing facilities to free farmers from powerful middlemen.

But it’s far from clear whether new policies and a cash infusion will be enough to counteract the forces that have pushed farmers off the land for decades — especially since much of the money is aimed at reducing carbon emissions, and so will also go toward large farming operations because they are the biggest polluters.

The number of farms has been declining since the 1930s, in large part because of migration from rural areas to cities and greater mechanization of agriculture, which allowed operators to cultivate larger tracts with fewer people. Over time, the federal government abandoned a policy of managing production to support prices, prompting growers to become more export-oriented while local distribution networks atrophied.

The last half-decade has been more disruptive than most. First came a trade war against China under former President Donald J. Trump, which drew retaliatory tariffs that cut into U.S. exports of farm products like soybeans and pork. Then came the pandemic, which scrambled supply chains and sapped farm labor, leaving crops to rot in the fields.

After Congress cushioned the blow with relief for farmers hurt by pandemic disruptions, things started to turn around. Even as the cost of supplies like fertilizer and seed rose, so did food prices, and farm incomes increased. In 2023, default rates on farm loans neared record lows.

“Farm balance sheets are the healthiest they’ve ever been in the aggregate,” said Brad Nordholm, the chief executive of Farmer Mac, a large secondary market for agricultural credit. “The tools available to American farmers to have a more predictable return, even when commodity prices change and input prices change, is greater than it’s ever been before.”

But wholesale crop prices are expected to decline over the coming year. Rising interest rates have made it more difficult to finance planting and harvesting, borrow for an expansion or just get into agriculture — especially since land values jumped 29 percent from 2020 to 2023.

That’s especially true for the smallest farmers, who are far less likely to be tapped into Department of Agriculture assistance programs and are more vulnerable to adverse weather, labor shortages and consumer whims.

“I think in some ways they’re in a worse position than before the pandemic,” said Benneth Phelps, executive director of the nonprofit Carrot Project, which advises small farmers in New England. “We see a lot of farmers making hard decisions right now about whether to stay in or get out, because they’ve run out of steam.”

That’s where the American Rescue Plan, the Inflation Reduction Act and the Bipartisan Infrastructure Law come in.

The laws have collectively provided about $60 billion to the Agriculture Department, which has parceled it out across a variety of priorities, from relieving farmers’ debt to paying them to reduce their carbon emissions.

The biggest chunk — about $19.5 billion — has breathed new life into subsidies to encourage conservation practices that improve the land, like cutting back on plowing and planting cover crops to sequester carbon in the soil. Some of the programs had shrunk in successive Farm Bills, which are five-year legislative packages that covers most agricultural subsidies, and about two-thirds of farmers who applied each year got nothing.

The new funding has added 16,000 recipients over the past two years. Preliminary data shows the expansion is allowing smaller farms to take part.

3 notes

·

View notes

Text

Point Of Care (POC) Diagnostics Market Global Latest Trends and Insights 2024 to 2031

Leading market research firm SkyQuest Technology Group recently released a study titled 'Point Of Care (POC) Diagnostics Market Global Size, Share, Growth, Industry Trends, Opportunity and Forecast 2024-2031,' This study Point Of Care (POC) Diagnostics report offers a thorough analysis of the market, as well as competitor and geographical analysis and a focus on the most recent technological developments. The research study on the Point Of Care (POC) Diagnostics Market extensively demonstrates existing and upcoming opportunities, profitability, revenue growth rates, pricing, and scenarios for recent industry analysis.

The research analysis on the global Point Of Care (POC) Diagnostics Market report 2024 offers a close watch on top industry rivals along with briefings on their company profiles, strategical surveys, micro as well as macro industry trends, futuristic scenarios, analysis of pricing structure, and an all-encompassing overview of the Point Of Care (POC) Diagnostics Market circumstances in the forecast period between 2024 and 2031. The global Point Of Care (POC) Diagnostics Market is a dynamic and rapidly evolving sector, encompassing the development, production, and distribution. This market is essential for improving global market and driving economic growth through innovation and industry advancements.

Market Growth

The Point Of Care (POC) Diagnostics Market has experienced robust growth over the past decade and is projected to continue expanding. Global Point of Care Diagnostics Market size was valued at USD 47.67 Billion in 2022 and is poised to grow from USD 50.54 Billion in 2023 to USD 81.17 Billion by 2031, growing at a CAGR of 6.1 % in the forecast period (2024-2031). This growth is driven by several factors, including an aging global population, increasing prevalence of advancements in technology, and rising global expenditure.

Chance to get a free sample @ https://www.skyquestt.com/sample-request/point-of-care-diagnostics-market

Detailed Segmentation and Classification of the report (Market Size and Forecast - 2031, Y-o-Y growth rate, and CAGR):

The Point Of Care (POC) Diagnostics Market can be segmented based on several factors, including product type, application, end-user, and distribution channel. Understanding these segments is crucial for companies looking to target specific markets and tailor their offerings to meet consumer needs.

Sample

Blood Samples, Urine Samples, Nasal & Oropharyngeal Swabs, and Other Samples

Product Type

Glucose Monitoring, Covid-19 Testing, Cardiometabolic Monitoring, Infectious Disease Testing, Coagulation Monitoring, and Pregnancy & Fertility Testing

End-Users

Professional Diagnostics Center, Clinical Laboratories, Ambulatory Care Facilities, Pharmacies, Retail Clinics, Hospitals, Critical Care Centers, and Home Care Settings

Get your customized report @ https://www.skyquestt.com/speak-with-analyst/point-of-care-diagnostics-market

Following are the players analyzed in the report:

Abbott Laboratories (US)

Siemens Healthineers AG (Germany)

Quidel Corporation (US)

F. Hoffman-La Roche Ltd. (Switzerland)

Danaher Corporation (US)

Becton, Dickinson and Company (US)

Chembio Diagnostics (US)

EKF Diagnostics (UK)

Trinity Biotech plc (Ireland)

Instrumentation Laboratory (US)

Nova Biomedical (US)

PTS Diagnostics (US)

Sekisui Diagnostics (US)

Regional Analysis

1. North America:

- The United States and Canada dominate the North American Point Of Care (POC) Diagnostics Market. The U.S. is the largest market globally, driven by advanced global infrastructure, high R&D investments, and significant Point Of Care (POC) Diagnostics consumption.

2. Europe:

- Europe is a significant player, with major Point Of Care (POC) Diagnostics Markets in Germany, France, and the United Kingdom. The region benefits from strong regulatory frameworks, high industry standards, and a robust R&D sector.

3. Asia-Pacific:

- This region is experiencing rapid growth, with countries like China and India leading the charge. Factors such as increasing industry access, growing middle-class populations, and expanding Point Of Care (POC) Diagnostics manufacturing capabilities contribute to this growth.

4. Latin America:

- Brazil and Mexico are key markets in Latin America. Growth in this region is driven by rising industry needs, increasing investments in industry infrastructure, and a growing demand for affordable medications.

5. Middle East and Africa:

- The Point Of Care (POC) Diagnostics Market in this region is expanding due to rising market spending, increased prevalence of diseases, and improvements in Market infrastructure, although the market is relatively smaller compared to other regions.

Future Outlook

The Point Of Care (POC) Diagnostics Market is poised for continued growth driven by technological advancements, expanding global market access, and increasing global industry needs. As the industry adapts to evolving challenges and seizes emerging opportunities, it is likely to see ongoing innovation and expansion, contributing significantly to global health and economic development.

Buy your full report: https://www.skyquestt.com/buy-now/point-of-care-diagnostics-market

0 notes

Text

Home Infusion Therapy Market Size, Share, Growth, Analysis Forecast to 2030

Home Infusion Therapy Industry Overview

The global home infusion therapy market size was valued at USD 35.96 billion in 2023 and is expected to grow at a compound annual growth rate (CAGR) of 8.1% from 2024 to 2030.

Home infusion therapy involves delivering therapeutic treatments, medications, or fluids directly into a patient's bloodstream through intravenous (IV) infusion, usually in the comfort and convenience of their home.

The growth of the market is driven by several key factors, including the expanding geriatric population characterized by decreased mobility, a rising preference for home care, and the swift evolution of technological advancements. Infusion therapy, encompassing essential components like IV therapy and IV hydration therapy, plays a crucial role in addressing conditions such as immune deficiencies, cancer, and congestive heart failure, where oral medication is not a viable treatment option. The increasing demand for these therapies stems from the need for long-term treatment among patients, positioning home infusion therapy as a notably cost-effective alternative to hospital-based care. The incorporation of IV therapy and IV hydration therapy serves as a driving force, providing patients with enhanced accessibility to effective and personalized medical solutions in the comfort of their homes

Gather more insights about the market drivers, restrains and growth of the Home Infusion Therapy Market

The home infusion market experienced a positive shift during the COVID-19 pandemic, with home infusion becoming a crucial necessity as healthcare facilities faced a surge in COVID patients. Despite the challenges posed by regional and country-wide lockdowns, causing disruptions in operations and supply chains, the market witnessed a substantial increase in 2020. As reported by Medtech Dive in October 2020, Baxter disclosed third-quarter sales of USD 2.97 billion, marking a 4% growth attributed to the rising demand for its COVID-related medical products. Furthermore, Baxter reported operational sales growth of 6% (reaching 3.2 billion) in Q3 2021 compared to 3.0 billion in Q3 2020, indicating a sustained recovery from the pandemic's impact.

Moreover, the market's expansion is propelled by the enhanced outcomes observed in patients and the cost-effectiveness and convenience provided by home infusion therapy. The increasing demographic of baby boomers struggling with diminished mobility due to conditions such as paralysis, osteoarthritis, and diabetes is expected to amplify the demand for home infusion therapy. The growing imperative to reduce the duration of inpatient stays is a pivotal factor poised to contribute significantly to the market's growth. Remarkably, continuous subcutaneous (SC) apomorphine infusion emerges as an exceptionally effective treatment for Parkinson's disease (PD), with diverse drug formulations available for the management of PD through subcutaneous delivery. In response to the mounting burden of PD, there is a notable surge in the demand for subcutaneous infusion therapy. For instance, in line with the Parkinson's Foundation's 2022 data update, approximately 90,000 individuals receive a PD diagnosis annually in the U.S. Furthermore, the anticipated number of people living with PD in the country is projected to soar to nearly 1.2 million by the year 2030.

Browse through Grand View Research's Medical Devices Industry Research Reports.

• The global knee braces market size was valued at USD 1.12 billion in 2023 and is projected to grow at a CAGR of 7.7% from 2024 to 2030.

• The global western blotting market size was valued at USD 986.2 million in 2023 and is projected to grow at a CAGR of 6.1% from 2024 to 2030.

Key Companies & Market Share Insights

Some of the key players operating in the market include Baxter, BD, Smiths Medical, Terumo Corporation, ICU Medical, etc

Baxter International Inc., commonly known as Baxter, is a global healthcare company that specializes in providing a wide range of medical products, therapies, and technologies. With a rich history dating back to the 1930s, Baxter has evolved into a leading player in the healthcare industry. The company develops innovative solutions for critical medical needs, including renal care, medication delivery, pharmaceuticals, and various therapeutic areas.

Becton, Dickinson and Company (BD) is a global medical technology company. BD specializes in developing and manufacturing medical devices, laboratory equipment, and diagnostic products aimed at advancing the diagnosis and treatment of various medical conditions. With a commitment to improving healthcare outcomes, BD focuses on delivering solutions in areas such as medication management, infection prevention, diagnostics, and biosciences.

Key Home Infusion Therapy Companies:

CVS/Coram

Option Care Health

BriovaRx/Diplomat (UnitedHealth Optum)

PharMerica

Fresenius Kabi

ICU Medical, Inc.

B. Braun Melsungen AG

Baxter

BD

Caesarea Medical Electronics

Smiths Medical

Terumo Corporation

JMS Co. Ltd.

Recent Developments

In June 2023, Baxter International, an American healthcare company, introduced Progressa+ Next Gen ICU bed for addressing critical needs of patients at their homes. This technology makes it easier for nurses to take care of patients, while supporting therapy at home.

In May 2023, Fresenius Kabi, a global healthcare company, initiated an agreement with Premier, Inc., an American healthcare company, that resulted in pricing and term benefits for the Ivenix Infusion System. This system is designed to advance the reliability and simplicity of infusion pumps.

In May 2023, Option Care Health, a healthcare service provider, created an independent platform for home care services in collaboration with Amedisys Inc., a leading provider of home health services. This platform comprises pharmacists, dieticians, therapists, social workers, and others for providing high quality healthcare services at home.

In April 2023, CareFusion, currently owned by Becton Dickinson, an American medical technology company, launched an advanced ultrasound technology to provide clinicians with optimal IV insertions. More than 90% hospitalized patients receive the IV therapy, thus contributing towards the market growth of home infusion therapy.

In January 2022, ICU Medical, a California-based global operations company, finalized the acquisition of Smiths Medical from Smiths Group Plc for creating a leading infusion therapy company with a combined revenue of USD 2.5 billion.

In November 2021, Terumo Corporation, a global medical device company, developed a smartphone device for controlling insulin pump. This device can be utilized as a home infusion therapy by patients for harmonizing the insulin therapy at home.

Order a free sample PDF of the Home Infusion Therapy Market Intelligence Study, published by Grand View Research.

0 notes

Text

Canes And Crutches Market Size To Reach $1.49 Billion By 2030

The global canes and crutches market size is expected to reach USD 1.49 billion by 2030, registering a CAGR of 4.9% from 2024 to 2030, according to a new report by Grand View Research, Inc. Key factors driving the market growth include the rising cases of vehicle collisions, osteoarthritis, & disabilities, growing geriatric population, and government initiatives. According to a University of Washington article published in August 2023, osteoarthritis affected 595 million people globally in 2020, equivalent to 7.6% of the global population. Projections suggest substantial growth by 2050, with anticipated rises of 74.9% for knee osteoarthritis and 95.1% for other forms of osteoarthritis across different joints.

Moreover, the increasing number of disability cases fuels the market's growth. According to the WHO article published in March 2023, about 1.3 billion individuals globally live with significant disabilities, accounting for 16% of the world's population, which translates to roughly 1 in every 6 people. This underscores the widespread impact of disabilities on a global scale, highlighting the need for continued efforts to improve accessibility and support for people with disabilities worldwide. Advancements in mobility aids are also driving market growth.

New cane technologies for individuals with visual impairments integrate sensors and sonars to detect obstacles, offering rechargeability, durability, and universal mounting capabilities. Projects like MAVI aim to enhance these canes to detect and describe obstacles, including pedestrians and text through OCR. Moreover, crutch design has evolved from heavy wooden models to lightweight versions made of materials like aluminum, titanium, and carbon fiber. Modern crutches feature ergonomic designs, contoured arm pads, improved tips, and enhanced range of motion, reducing secondary injuries and improving user comfort and mobility.

Request a free sample copy or view report summary: Canes And Crutches Market Report

Canes And Crutches Market Report Highlights

The canes segment held the largest share of over 52.07% in 2023 due to ongoing product advancements, growing initiatives by key companies, and increasing product adoption. Recent advancements in canes, including folding, quad, and offset designs, focus on enhancing comfort, functionality, and adaptability through new materials and ergonomic features

The hospital pharmacies segment held the largest share of 43.19% in 2023. Hospitals are crucial centers for providing a central point for healthcare facilities to procure these mobility aids

North America dominated the market with a share of 36.0% in 2023 owing to favorable reimbursement policies, advanced healthcare infrastructure, a growing aging population, an increasing number of arthritis cases, quick regulatory approvals, and new product launches

The market in Asia Pacific is projected to register the fastest CAGR of 6.2% from 2024 to 2030 owing to a rise in the prevalence of chronic illnesses and the high frequency of road accidents

Canes And Crutches Market Segmentation

Grand View Research has segmented the global canes and crutches market on the basis of product, distribution channel, and region:

Canes And Crutches Product Outlook (Revenue, USD Million, 2018 - 2030)

Canes

Folding Canes

Quad Canes

Offset Canes

Crutches

Axillary Crutches

Forearm Crutches

Accessories

Canes And Crutches Distribution Channel Outlook (Revenue, USD Million, 2018 - 2030)

Hospital Pharmacies

Medical Retail Stores

Online Pharmacies

Canes And Crutches Regional Outlook (Revenue, USD Million, 2018 - 2030)

North America

U.S.

Canada

Mexico

Europe

UK

Germany

France

Italy

Spain

Denmark

Sweden

Norway

Asia Pacific

Japan

China

India

Thailand

South Korea

Australia

Latin America

Brazil

Argentina

Middle East & Africa

South Africa

Saudi Arabia

UAE

Kuwait

List of Key Players in the Canes And Crutches Market

Drive DeVilbiss Healthcare

Ossenberg GmbH

Ergoactives

NOVA Medical Products

GF Health Products Inc

Sunrise Medical Limited

Besco Medical Co., Ltd

Invacare Corporation

Medline Industries, Inc

Cardinal Health, Inc.

0 notes

Text

Nurse Call Systems Market Segmentation and Competitive Analysis Report, 2030

The global nurse call systems market size was valued at USD 1.7 billion in 2022 and is expected to expand at a compound annual growth rate (CAGR) of 12.11% from 2023 to 2030.

The growing need for a diverse and integrated platform that increases the preference for mobility aids are driving the market. Medicare decides to refund schemes based on quality and outcome rather than quantity owing to the rising healthcare cost. Medicare estimates that current reimbursement practices are costing an additional USD 2.1 billion and expects to curtail this by using technology-focused healthcare. With this change in reimbursement policies, hospitals and other healthcare facilities are trying to streamline their workflow processes by adopting technology-oriented nurse call systems.

Gather more insights about the market drivers, restrains and growth of the Nurse Call Systems Market

Nurse call systems enable reliable and flexible communication between the patient and the caregiver. Increasing patient numbers in healthcare facilities and the introduction of advanced ways to expand communication, workflow, and management to provide quality patient care are fueling the market growth. The market is primarily driven by technological advancements that have allowed players to create innovative devices. For instance, in December 2019, Tunstall Group launched Tunstall Carecom, a wireless and digital nurse call system.

Growing adoption of real-time location systems (RTLS) integrated with wireless technologies in various healthcare facilities is propelling the market growth. RTLS allows the healthcare facilities to track the movement of the attendants and equipment to increase productivity. For instance, Televic's AQURA Care Communication Platform is an integrated platform with various modules such as nurse call, personal localization (RTLS), patient and staff safety, alarm delivery, personal mobility, and mediator control. The platform is open to integrating both its module and the mediator module, along with the current hospital infrastructure.

However, the high implementation costs can hinder the market expansion. The effectiveness of integrated communication technologies is based on several factors, including software, hardware, and the training level of medical staff. This increases the need for high investments by hospitals, clinics, and home care facilities to effectively implement the devices. In addition, strict regulatory policies related to data breaches can impede industry growth during the forecast period.

Moreover, with the rise in home healthcare and nursing home facilities, major industry players are focusing on the need for better patient response time along with eliminating nurse fatigue. Vendors are differentiating their products by integrating their devices with different diagnostic solutions and technologies. For instance, in June 2019, Vocera Communications, Inc. introduced a new analytics solution that provides information about the number of calls, texts, alarms, and alerts that clinicians receive. Industry players offer customized services as per hospital needs, through such integration.

Nurse Call Systems Market Segmentation

Grand View Research has segmented the global nurse call systems market report based on technology, type, application, end-use, and region:

Technology Outlook (Revenue, USD Billion, 2016 - 2030)

• Wired Communication Equipment

• Wireless Communication Equipment

Type Outlook (Revenue, USD Billion, 2016 - 2030)

• Integrated Communication Systems

• Buttons

• Mobile Systems

• Intercoms

Application Outlook (Revenue, USD Billion, 2016 - 2030)

• Alarms & Communications

• Workflow Optimization

• Wanderer Control

• Fall Detection & Prevention

End-use Outlook (Revenue, USD Billion, 2016 - 2030)

• Hospitals

• ASCs/Clinics

• Long Term Care Facilities

Regional Outlook (Revenue, USD Billion, 2016 - 2030)

• North America

o U.S.

o Canada

• Europe

o U.K.

o Germany

o France

o Italy

o Spain

• Asia Pacific

o China

o Japan

o India

o Australia

o South Korea

• Latin America

o Brazil

o Mexico

o Argentina

• Middle East & Africa

o South Africa

o UAE

o Saudi Arabia

Browse through Grand View Research's Medical Devices Industry Research Reports.

• The global radiation dose monitoring market size was valued at USD 3.44 billion in 2023 and is projected to grow at a CAGR of 6.3% from 2024 to 2030.

• The global patient monitoring accessories market size was valued at USD 7.83 billion in 2023 and is projected to grow at a CAGR of 9.0% from 2024 to 2030.

Key Companies & Market Share Insights

The market is fragmented. Competitors in this market are increasing their share through a variety of marketing strategies, including product launches, investments, and mergers and acquisitions. Companies are further investing in improving their products. For instance, in July 2020, Hill-Rom Holdings Inc. collaborated with Aiva for hands-free communication between caregiver-to-patient and caregiver-to-caregiver using Hill-Rom’s Voalte Mobile solution. Some prominent players in the global nurse call systems market include:

• Hill-Rom Holding, Inc.

• Rauland Corporation

• Honeywell International, Inc.

• Ascom Holding AG

• TekTone Sound and Signal Mfg., Inc.

• Austco Healthcare

• Stanley Healthcare

• Critical Alert Systems LLC

• West-Com Nurse Call Systems, Inc.

• JNL Technologies

• Cornell Communications

Order a free sample PDF of the Nurse Call Systems Market Intelligence Study, published by Grand View Research.

#Nurse Call Systems Market#Nurse Call Systems Industry#Nurse Call Systems Market size#Nurse Call Systems Market share#Nurse Call Systems Market analysis

0 notes

Text

Top Tips for Buying a House in Mysore

Top Tips for Buying a House in Mysore

Buying a house in mysore is one of the most significant investments you’ll ever make. In a developing metropolis like Mysore, cited for its wealthy cultural records and modern-day facilities, it’s vital to approach the residents and try to find a method with cautious attention and informed desire-making. Whether you’re a number one-time homebuyer or trying to spend money on assets, here are some pinnacle suggestions to guide you through buying a house in Mysore.

1. Research the Market

Comprehending Mysore’s Real Estate Landscape

Before you start your private home-searching adventure, it’s vital to research the tangible assets market in Mysore. Familiarise yourself with specific localities, belongings prices, and marketplace trends. Areas like Vijaynagar, Jayalakshmipuram, and Gokulam have acquired a reputation due to their accessibility and offerings.

Resources for Market Research

Online Real Estate Portals: Websites like pickyourprop ,99acres, MagicBricks, and Housing.com offer listings and marketplace insights.

Local Real Estate Agents: Engaging with a knowledgeable tangible assets agent can offer treasured insights into present-day tendencies and capability areas for improvement.

2. Set a Budget

Choose Your Financial Limits

Establish a clean price range based entirely on your financial scenario. Consider your profits, economic savings, and any gift debts. A nicely defined budget will help you Buying a house in mysore narrow down your options and prevent overspending.

Additional Costs to Consider

When budgeting for a house, don’t forget to think in:

Registration and Stamp Duty: This can range from you. S . A . To u.S. Of America.

Home Loan Fees: If you’re taking a mortgage, keep processing expenses and coverage in mind.

Maintenance Costs: These are factors in ability maintenance and monthly safety.

3. Choose the Right Location

Elements to Consider

The location of your new home can significantly affect your lifestyle and funding fee. Consider the following:

Proximity to Work and Schools: Ensure the region is handy for your day-by-day ride and educational goals.

Amenities: Look for nearby centres consisting of hospitals, buying centres, parks, and public delivery.

Safety and Security: Research the protection facts of diverse neighbourhoods Buying a house in mysore.

Future Development Plans

Investigate any upcoming infrastructure tasks or inclinations in the vicinity, as they can enhance the property rate over the years.

4. Identify Your Needs

Determine Your Requirements

Before starting your search, list your desires and options. Consider:

Type of Property: Are you looking for a rental, villa, or impartial house?

Size and Layout: How many bedrooms and toilets do you want? Do you pick an open-ground plan?

Amenities: Are you seeking additional features like a garden, parking, or safety?

Flexibility

While having a list of want-to-haves is vital, be open to compromise. The first-class home may not exist, so prioritise your requirements Buying a house in mysore.

5. Get Pre-Approved for a Home Loan

Understanding Your Financing Options

If you require financing, getting pre-approved for a domestic mortgage can give you a clearer picture of your charge range and strengthen your role as a purchaser.

Steps to Secure Pre-Approval

Research Lenders: Compare hobby charges and mortgage phrases from diverse banks and economic institutions.

Submit Required Documents: This consists of profits evidence, identification verification, and credit score information.

Understand Loan Eligibility: Different creditors have numerous requirements based on your financial profile.

Visit Properties in Person

Schedule Visits

Once you are given shobeensted functionality residences, schedule visits to see them in person. Online listings can be deceptive, so it’s critical to take a look at the property before you decide.

Key Aspects to Evaluate

Condition of the Property: Look for any signs and symptoms and symptoms and signs and symptoms of damage or crucial preservation.

Neighborhood Vibe: Spend time inside the location to gauge the network and environment.

Layout and Space: Ensure the format meets your desires and feels snug.

6. Work with a Real Estate Agent

Benefits of Hiring an Expert

A knowledgeable actual belongings agent may be a beneficial aid in your house-shopping journey. They provide:

Market Insights: Agents must get entry to finish market statistics and trends.

Negotiation Skills: A skilled agent can negotiate on your behalf for better phrases.

Legal Assistance: They can assist in navigating jail requirements and job placement.

Finding the Right Agent

Look for dealers with suitable opinions and a solid track record in the Mysore market. Personal pointers from buddies or a circle of relatives can also be beneficial.

7. Check Legal Documentation

Importance of Legal Verification

Before finalising assets, ensure that each prison document is in order. This includes:

Title Deed: Verify that the vendor understands the assets well.

Encumbrance Certificate: This report confirms that the belongings are free from legal liabilities.

Building Approval Plan: Ensure that the property has all necessary approvals from community authorities.

Hiring a Legal Advisor

Consider hiring a prison expert to test documents and ensure compliance with nearby regulations. This step can prevent criminal problems in the future.

8. Understand the Agreement

Review the Sale Agreement

A sale settlement may be drafted once you decide to maintain your belongings. Pay interest on the following:

Payment Terms: Understand the charge time desk and any related outcomes for delays.

Possession Date: Confirm simultaneously that you can take ownership of the property.

Contingencies: Be aware of any situations that might affect the sale.

Negotiate Terms

Feel free to negotiate terms within the settlement. A good deal has to be beneficial for every occasion.

9. Plan for the Future

Consider Long-Term Investment

When buying a residence, count beyond your instantaneous dreams. Consider how the assets will serve you in the long run. Will it accommodate the increase in the future circle of relatives? Is the region likely to recognise in price?

Resale Value

Evaluate the functionality of the resale value of the belongings. Factors such as community development, infrastructure enhancements, and marketplace dispositions can significantly affect your funding’s true worth over the years.

Conclusion

Buying a house in Mysore may be a profitable experience if cautiously approached, making plans and studies. By following those suggestions, you could navigate the complexities of the actual belongings market and make informed decisions that align with your dreams and monetary desires. Whether you’re seeking out your dream domestic or a profitable investment, being nicely organised will set you on the path to success within the Mysore real property marketplace. With the proper technique, you’ll find a property that now meets your desires and serves as a sturdy investment for the future.

For more information visit : Buying a house in Mysore

0 notes

Text

Understanding Stoma Care: A Comprehensive Guide for New Patients

The global stoma care market size was USD 3.63 Billion in 2021 and is expected to register a revenue CAGR of 4.9% during the forecast period, according to latest analysis by Emergen Research. Increasing prevalence of bladder cancer and inflammatory bowel disease, increasing number of technological advancements in the field of medical science, and constantly growing number of product launches by leading companies globally are some of the key factors driving market revenue growth.

The report focuses on current and future market growth, technological advancements, volume, raw materials, and profiles of the key companies involved in the market. The report provides valuable insights to the stakeholders, investors, product managers, marketing executives, and other industry professionals.

Get Download Pdf Sample Copy of this Report@ https://www.emergenresearch.com/request-sample/1764

Competitive Terrain:

The global Stoma Care industry is highly consolidated owing to the presence of renowned companies operating across several international and local segments of the market. These players dominate the industry in terms of their strong geographical reach and a large number of production facilities. The companies are intensely competitive against one another and excel in their individual technological capabilities, as well as product development, innovation, and product pricing strategies.

The leading market contenders listed in the report are:

Prowess Care, B. Braun SE, Coloplast, Hollister Incorporated, Convatec Inc., Nu-Hope Laboratories, Inc., Welland Medical Limited., Cymed Micro Skin, Schena Ostomy Technologies, Inc., Perma-Type Rubber, Marlen Manufacturing & Development Company

Key market aspects studied in the report:

Market Scope: The report explains the scope of various commercial possibilities in the global Stoma Care market over the upcoming years. The estimated revenue build-up over the forecast years has been included in the report. The report analyzes the key market segments and sub-segments and provides deep insights into the market to assist readers with the formulation of lucrative strategies for business expansion.

Competitive Outlook: The leading companies operating in the Stoma Care market have been enumerated in this report. This section of the report lays emphasis on the geographical reach and production facilities of these companies. To get ahead of their rivals, the leading players are focusing more on offering products at competitive prices, according to our analysts.

Report Objective: The primary objective of this report is to provide the manufacturers, distributors, suppliers, and buyers engaged in this sector with access to a deeper and improved understanding of the global Stoma Care market.

Emergen Research is Offering Limited Time Discount (Grab a Copy at Discounted Price Now)@ https://www.emergenresearch.com/request-discount/1764

Market Segmentations of the Stoma Care Market

This market is segmented based on Types, Applications, and Regions. The growth of each segment provides accurate forecasts related to production and sales by Types and Applications, in terms of volume and value for the period between 2022 and 2030. This analysis can help readers looking to expand their business by targeting emerging and niche markets. Market share data is given on both global and regional levels. Regions covered in the report are North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. Research analysts assess the market positions of the leading competitors and provide competitive analysis for each company. For this study, this report segments the global Stoma Care market on the basis of product, application, and region:

Segments Covered in this report are:

End-Use Outlook (Revenue, USD Billion; 2019-2030)

Homecare Settings

Hospitals

Ambulatory Surgical Center

Regional Outlook (Revenue, USD Billion; 2019–2030)

North America

U.S.

Canada

Mexico

Europe

Germany

France

U.K.

Benelux

Rest of Europe

Asia Pacific

China

India

Japan

South Korea

Rest of APAC

Latin America

Brazil

Rest of LATAM

Middle East & Africa

Saudi Arabia

UAE

Rest of MEA

more

Browse Full Report Description + Research Methodology + Table of Content + Infographics@ https://www.emergenresearch.com/industry-report/stoma-care-market

Major Geographies Analyzed in the Report:

North America (U.S., Canada)

Europe (U.K., Italy, Germany, France, Rest of EU)

Asia Pacific (India, Japan, China, South Korea, Australia, Rest of APAC)

Latin America (Chile, Brazil, Argentina, Rest of Latin America)

Middle East & Africa (Saudi Arabia, U.A.E., South Africa, Rest of MEA)

ToC of the report:

Chapter 1: Market overview and scope

Chapter 2: Market outlook

Chapter 3: Impact analysis of COVID-19 pandemic

Chapter 4: Competitive Landscape

Chapter 5: Drivers, Constraints, Opportunities, Limitations

Chapter 6: Key manufacturers of the industry

Chapter 7: Regional analysis

Chapter 8: Market segmentation based on type applications

Chapter 9: Current and Future Trends

Request Customization as per your specific requirement@ https://www.emergenresearch.com/request-for-customization/1764

0 notes

Text

Analyzing the Growth of the Pancreatic Cancer Diagnosis Market to 2032

Pancreatic cancer remains one of the most lethal forms of cancer, with a high mortality rate due to its typically late diagnosis and aggressive nature. Advances in diagnostic technologies, however, are providing hope for earlier detection and improved outcomes. This article explores the pancreatic cancer diagnosis market, covering market size, share, industry trends, and forecast up to 2032. We will delve into market segmentation and regional analysis to provide a comprehensive overview of the market dynamics.

Market Overview

The global pancreatic cancer diagnosis market has been growing steadily, driven by the increasing incidence of pancreatic cancer and advancements in diagnostic technologies. Pancreatic cancer diagnosis Market Size was estimated at 3.64 (USD Billion) in 2023. The Pancreatic Cancer Diagnosis Market Industry is expected to grow from 3.81(USD Billion) in 2024 to 5.6 (USD Billion) by 2032. The pancreatic cancer diagnosis Market CAGR (growth rate) is expected to be around 4.92% during the forecast period (2024 - 2032).

Market Segmentation

Understanding the segmentation of the pancreatic cancer diagnosis market is crucial for identifying growth opportunities and tailoring strategies to meet specific needs. The market can be segmented based on diagnostic method, end-user, and region.

By Diagnostic Method:

Imaging Tests: Includes CT scans, MRI, and endoscopic ultrasound, which are commonly used for detecting and staging pancreatic cancer.

Biopsy: Tissue sampling techniques such as fine-needle aspiration and core needle biopsy are critical for confirming diagnosis.

Blood Tests: Biomarkers like CA 19-9 and genetic tests are becoming increasingly important for early detection and monitoring.

Molecular Diagnostics: Advanced techniques such as next-generation sequencing (NGS) and liquid biopsy are gaining traction for their accuracy and non-invasive nature.

By End-User:

Hospitals: The primary setting for comprehensive diagnostic procedures and treatment planning.

Diagnostic Laboratories: Specialized facilities offering advanced molecular and genetic testing.

Research Institutes: Contributing to the development of new diagnostic tools and methods through clinical trials and studies.

By Region:

North America: Leading the market with significant investments in healthcare infrastructure and research.

Europe: Strong market presence driven by robust healthcare systems and increasing cancer awareness.

Asia-Pacific: Expected to witness the highest growth rate due to improving healthcare access and rising cancer prevalence.

Latin America: Moderate growth with increasing awareness and improving diagnostic capabilities.

Middle East and Africa: Emerging market with potential growth driven by investments in healthcare and diagnostic technologies.

Regional Analysis

The pancreatic cancer diagnosis market exhibits significant regional variations, influenced by healthcare infrastructure, prevalence of the disease, and economic conditions.

North America:

The largest market for pancreatic cancer diagnosis, driven by high incidence rates and advanced healthcare facilities.

The U.S. dominates the region with substantial funding for cancer research and high adoption of advanced diagnostic technologies.

Europe:

Holds a significant market share with countries like Germany, France, and the U.K. leading in terms of diagnosis and treatment capabilities.

Government initiatives and public health programs aimed at early cancer detection contribute to market growth.

Asia-Pacific:

Expected to experience the fastest growth during the forecast period.

Rapid urbanization, increasing healthcare expenditure, and rising awareness about cancer screening are key drivers.

Latin America:

Moderate growth supported by improving healthcare infrastructure and increasing awareness about pancreatic cancer.

Brazil and Mexico are the major contributors to the market in this region.

Middle East and Africa:

The market is in the nascent stage but shows potential for growth due to increasing healthcare investments and rising incidence of cancer.

Efforts to improve diagnostic capabilities and cancer care services are underway.

Industry Trends

Several trends are shaping the pancreatic cancer diagnosis market, reflecting advancements in technology, healthcare practices, and patient preferences.

Rise of Molecular Diagnostics:

Molecular diagnostics, including NGS and liquid biopsy, are becoming more prominent due to their precision and non-invasive nature.

These technologies enable earlier detection and personalized treatment approaches.

Integration of Artificial Intelligence (AI):

AI and machine learning are being integrated into diagnostic imaging and data analysis to improve accuracy and speed.

AI algorithms assist in detecting subtle changes in imaging studies that may indicate early stages of pancreatic cancer.

Emphasis on Biomarkers:

Research into biomarkers like CA 19-9 and new genetic markers is expanding, providing tools for early detection and monitoring disease progression.

Biomarker-based tests are becoming more refined and widely available.

Advancements in Imaging Technologies:

Enhanced imaging techniques, such as high-resolution CT and MRI, provide better visualization of pancreatic tumors.

Endoscopic ultrasound (EUS) is becoming a standard tool for detailed imaging and biopsy.

Focus on Early Detection:

Public health initiatives and screening programs are increasingly focusing on early detection to improve survival rates.

Education and awareness campaigns aim to encourage individuals at high risk to undergo regular screening.

Telemedicine and Remote Diagnostics:

The adoption of telemedicine platforms is facilitating remote consultations and diagnostics, improving access to care.

Remote diagnostic tools and mobile health applications support patient monitoring and follow-up.

Market Forecast

The pancreatic cancer diagnosis market is expected to grow significantly over the next decade. Key factors driving this growth include:

Increasing Incidence of Pancreatic Cancer:

The rising global burden of pancreatic cancer, partly due to aging populations and lifestyle factors, fuels the demand for diagnostic solutions.

Improved understanding of genetic predispositions and risk factors contributes to the identification of high-risk individuals.

Technological Advancements:

Continuous innovation in diagnostic technologies, including molecular diagnostics, AI integration, and advanced imaging, enhances the market.

Research and development activities are likely to yield new, more effective diagnostic tools.

Rising Healthcare Expenditure:

Increased spending on healthcare, particularly in emerging economies, supports market growth.

Investments in healthcare infrastructure and cancer research are critical drivers.

Growing Awareness and Screening Programs:

Public health campaigns and screening programs promote early detection, which is crucial for improving outcomes.

Efforts to educate the public and healthcare providers about the importance of early diagnosis are gaining momentum.

Conclusion

The pancreatic cancer diagnosis market is assured of substantial growth, driven by increasing incidence rates, technological advancements, and evolving healthcare practices. With diverse diagnostic methods and significant regional variations, the market offers numerous opportunities for stakeholders. As the global focus on early cancer detection intensifies, the demand for effective and innovative diagnostic solutions will continue to rise, making the pancreatic cancer diagnosis market a critical component of cancer care strategies worldwide.

0 notes

Text

Cardiac Equipment Market to Witness Excellent Revenue Growth Owing to Rapid Increase in Demand

The growing geriatric population worldwide is fueling the number of cases diagnosed with heart disorders due to the high susceptibility of this population pool to developing cardiac diseases which is boosting the demand for cardiac equipment . Moreover, the government is imposing penalties on hospitals and healthcare facilities to limit patient readmissions in the U.S. As a result, hospitals are promoting home healthcare and remote patient monitoring services, hence triggering the demand for cardiac equipment. On the other hand, factors such as high device maintenance costs coupled with stringent regulatory product approval procedures are hindering the growth of the global cardiac equipment vertical.

Free Sample Report + All Related Graphs & Charts @: https://www.advancemarketanalytics.com/sample-report/127829-global-cardiac-equipment-market?utm_source=Organic&utm_medium=Vinay

Latest released the research study on Global Cardiac Equipment Market, offers a detailed overview of the factors influencing the global business scope. Cardiac Equipment Market research report shows the latest market insights, current situation analysis with upcoming trends and breakdown of the products and services. The report provides key statistics on the market status, size, share, growth factors of the Cardiac Equipment The study covers emerging player’s data, including: competitive landscape, sales, revenue and global market share of top manufacturers are Medtronic(Ireland), Boston Scientific Corporation (United States), Jude Medical (United States), Thoratec Corporation (United States), HeartWare (United States), SynCardia Systems (United States), Vasomedical (United States), Sorin Group (LivaNova) (Germany), Biotronik (Germany), Berlin Heart (Germany)

Thanks for reading this article; you can also get individual chapter wise section or region wise report version like North America, Europe or Southeast Asia.

Contact Us:

Craig Francis (PR & Marketing Manager)

AMA Research & Media LLP

Unit No. 429, Parsonage Road Edison, NJ

New Jersey USA – 08837

0 notes

Text

INR Test Meter Market: Top Players to Watch in 2033

The INR test meter market is set for significant growth, with an estimated market size of USD 1,336.1 million in 2023. According to Future Market Insights, the market is projected to expand at a compound annual growth rate (CAGR) of 6.3%, reaching approximately USD 2,453.3 million by 2033. This growth is primarily driven by the increasing prevalence of cardiovascular diseases and blood disorders worldwide.

INR test meters play a crucial role in monitoring and managing anticoagulation therapy, ensuring accurate and timely measurement of patients’ blood clotting levels. The increasing adoption of point-of-care testing and the growing demand for portable and user-friendly INR test meters are further driving market growth.

When monitoring blood clotting times in patients with blood disorders and cardiovascular diseases, test meters that measure the International Normalized Ratio, or INR, are indispensable instruments.

Get your PDF Sample Report:

https://www.futuremarketinsights.com/reports/sample/rep-gb-15124

Understanding INR Test Meters:

An INR test meter is a portable, battery-operated device that allows patients taking warfarin, a blood thinner medication, to conveniently monitor their response to the medication. The meter features a simple design:

Display Screen: Shows the INR test results.

Test Strip Slot: Accepts meter-specific test strips.

Lancet Compatibility: Works with lancets (small needles) to draw a blood sample.

The user inserts a test strip into the meter and then uses a lancet to draw a small blood sample, applying it to the strip. The meter reads the strip, measures the blood clotting time, and calculates the INR (International Normalized Ratio) using a standardized formula. This INR value helps healthcare providers determine if the warfarin dosage is appropriate for the patient. The U.S. Food and Drug Administration (FDA) regulates INR test meters and test strips as medical devices

Key Takeaways :

Future Market Insights considers that the INR test meter market contributed approximately 72.8% in 2021.

United States is likely to hold a market share of 32.1% and considerably dominates North America’s

INR test meter market in North America consists of a total share of about 35.6% in 2022

Germany held a market share of nearly 3.6% in the INR test meter market.

Europe INR test meter market holds a share of 32.0%.

Devices are expected to account for around 79.7% in 2021 throughout the forecast period,

Hospitals held the highest market share value of 32.4%, opines FMI.

Competitive Landscape

According to FMI, the INR test meter industry is anticipated to be quite competitive. Leading businesses are using strategies including mergers and acquisitions, partnerships and collaborations, and the introduction of new technology products to match consumer demand and grow their client base. Among the significant advancements made by the major market participants are:

In December 2022, Abbott Laboratories invested $536 million in building a new manufacturing facility in Bowling Green, Ohio, state officials announced this week

The facility produces specialty and metabolic powder nutritional products, some of which are used by individuals with extreme food allergies or other dietary conditions.

In July 2023, German-based Siemens Healthineers is bringing cutting-edge surgical training and technology for Atrium Health’s future medical school as its first strategic partner.

Key Companies:

F. Hoffmann-La Roche Ltd

Lepu Medical Technology (Beijing) Co. Ltd.

ACON Laboratories, Inc.

CoaguSense Inc.

Abbott

Eurolyser Diagnostica GmbH

Horiba ABX SAS

Avalun SAS

Roche Diagnostics

Siemens Healthineers

Key Segments :

By Product:

Device

Lancet

Test Strips

By End User:

Hospitals

Specialty Clinics

Ambulatory Surgical Centers

Homecare Settings

By Region:

North America

Latin America

Western Europe

Eastern Europe

South Asia & Pacific

East Asia

Oceania

Middle East and Africa

0 notes

Text

U.S. Hospital Facilities Market Trends Analysis Report By Patient Service, Facility Type, Service Type, Bed Size And Forecast 2030: Grand View Research Inc.

San Francisco, 21 June 2024: The Report U.S. Hospital Facilities Market Size, Share & Trends Analysis Report By Patient Service, By Facility Type (Private Hospitals, Public/Community Hospitals), By Bed Size, By Service Type, And Segment Forecasts, 2023 – 2030

The U.S. hospital facilities market size is anticipated to reach USD 2540.4 billion by 2030 and is anticipated to grow at a CAGR of 7.7%…

View On WordPress

0 notes

Text

Coronary Stents Market Key Vendors, Manufacturers, Suppliers and Analysis Industry Report 2030

Coronary Stents Industry Overview

The global coronary stents market size was estimated at USD 9.32 billion in 2022 and is expected to grow a compound annual growth rate (CAGR) of 3.1% from 2023 to 2030.

Growing aging population and a rising prevalence of noncommunicable diseases such as cardiovascular diseases (CVDs), complex lesions, diabetes, obesity, and others are expected to drive demand for coronary stents over the forecast period. According to the World Health Organization (WHO), in 2019, CVDs were among the major causes of mortality worldwide of which ischemic heart disease (IHD) ranks as the most prevalent. In 2019, an estimated 17.9 million people died from CVDs, responsible for 32% of worldwide mortalities.

Gather more insights about the market drivers, restrains and growth of the Coronary Stents Market

According to research published by the National Library of Medicine in June 2021, one of the CVDs, coronary artery disease (CAD), causes roughly 6,10,000 fatalities yearly (an estimated 1 in 4 deaths) and is the major cause of mortality in the U.S. As a result, the unprecedented rise in CAD incidence is predicted to boost demand for an effective coronary stent device for treatment. This factor is expected to bolster the demand throughout the forecast period. Since a coronary stent is used in most of the Percutaneous Coronary Intervention (PCI) procedures.

The rising preference for minimally invasive surgeries (MIS) is another factor expected to boost the adoption of coronary stents over the forecast period. The advantages of these procedures include small incision wounds leading to higher patient satisfaction. These procedures also provide shorter hospital stays and facilitate quick recovery. Stenting technology is increasingly preferred over the conventional balloon angioplasty owing to the introduction of advanced DES and evolving bioresorbable scaffolds. Technological advancements in coronary stents, such as the development of bifurcated stents and the use of biodegradable materials, have led to efficient and improved outcomes of CVD treatment. Companies are proactively involved in product developments and partnerships and strategic collaborations. The aforementioned factors are expected to propel market growth over the forecast period.

The impact of COVID-19 on the market for coronary stents closely tracked the impact of COVID-19 on overall PCI procedures. During the pandemic's initial outbreak and periods of high local COVID-19 case counts, several states, towns, and nations issued orders to citizens to shelter in place or minimize the potential exposure to and transmission of illness, resulting in elective surgeries being postponed. As a result, total PCI procedure volumes-and hence coronary stent unit sales and revenues-went significantly lower in 2020. These revenues are expected to rise as facility capacity usage improves and resumes all the semi-elective to non-urgent procedures.

The notable competitors in the market for coronary stents announced revenue falls in their interventional cardiology portfolios, which include coronary stent devices, in 2020, due to the impact of the COVID-19 pandemic. Boston Scientific, for instance, reported a significant decrease in annual revenues in its Interventional Cardiology segment, which includes coronary stent devices, in 2020, but the company performed relatively well in the first quarter of 2021, reporting revenue growth of approximately 7% globally compared to the first quarter of 2020. In contrast, Abbott Laboratories Laboratories was the least affected, with less impact on its entire vascular segment in 2020, which includes coronary stent devices, in its 2020 annual results.

Browse through Grand View Research's Medical Devices Industry Research Reports.

• The global disposable hospital gowns market size was valued at USD 3.68 billion in 2023 and is projected to grow at a CAGR of 12.9% from 2024 to 2030.

• The global knee braces market size was valued at USD 1.12 billion in 2023 and is projected to grow at a CAGR of 7.7% from 2024 to 2030.

Competitive Insights

Product launches, approvals, strategic acquisitions, and innovations are some of the crucial business strategies adopted by market participants to maintain and grow their global reach. Abbott Laboratories, Boston Scientific, and Medtronic accounted for a significant presence in the overall market. These companies have gained a notable presence in the market due to good strong performances in the lucrative DES market and large product portfolios spanning numerous different IC device categories. For instance, in August 2022, Medtronic launched the Onyx Frontier drug-eluting stent (DES). The new product offers advanced delivery management and improves the overall performance in the most challenging cases.

Despite the dominance of the three major manufacturers, the market for coronary stents is a blend of numerous global and local players. BIOTRONIK, for instance, has been able to establish a significant presence in the entire market by offering low pricing and new technologies that address unmet needs. Positive clinical results from BIOTRONIK's BIONYX, BIOFLOW-V, and BIOSOLVE trials, in conjunction with the use of BIOTRONIK's Orsiro DES and Magmaris BRS, have positioned the company well to compete against the market's largest players. BIOTRONIK is also one of the most competitive players in the overall BRS device market. Terumo Corporation, Biosensors International, and Cardinal Health are a few additional significant competitors in this market. Some of the prominent players in the global coronary stents market include:

Abbott

Medtronic

Boston Scientific Corporation

Terumo Corporation

B Braun Melsungen AG

Biotronik

Stentys SA

MicroPort Scientific Corporation

C. R. Bard, Inc.

Cook Medical

Order a free sample PDF of the Coronary Stents Market Intelligence Study, published by Grand View Research.

0 notes

Text

Biosensors Market Size To Reach $49.78 Billion By 2030

The global biosensors market size was estimated at USD 28.9 billion in 2023 and is expected to grow at a compound annual growth rate (CAGR) of 8.0% from 2024 to 2030. The key factors driving the industry growth include various applications in the healthcare/medical sector, increasing demand in the bioprocessing industry, and rapid technological advancements in drug screening due to the COVID-19 pandemic. Moreover, the pandemic led to the rapid expansion of the biosensor industry due to an increase in the number of hospitals worldwide.

Over the forecast period, technological advancements are expected to be significant growth drivers for the industry. For example, in January 2022, a U.S. medical device manufacturer, Abbott, launched a universal consumer wearable device with biosensors. The company announced the development of a new line of consumer biometric wearable devices called Lingo, designed for more general fitness and wellness purposes. In addition, increasing demand for biosensors and bioreactors for new drug development is likely to lead to industry expansion in the near future due to improved biosensor technology.

Request a free sample copy or view report summary: Biosensors Market Report

Biosensors Market Report Highlights

The electrochemical biosensors technology segment accounted for the largest revenue share in 2023

The segment is anticipated to witness significant growth over the forecast period owing to the widespread applications for analysis & quantification in biochemical and biological processes

Based on the application, the medical segment dominated the industry in 2023. This device is considered an essential tool in the monitoring and detection of a wide range of medical conditions, such as cancer and diabetes

Middle East & Africa is expected to witness the fastest growth rate over the forecast period

This is owing to a rise in research & development activities and constantly improving healthcare facilities in the region.

Biosensors Market Segmentation

Grand View Research has segmented the biosensors market report on the basis of technology, application, end-user, and region:

Biosensors Technology Outlook (Volume, Unit; Revenue, USD Million, 2018 - 2030)

Thermal

Electrochemical

Piezoelectric

Optical

Biosensors Application Outlook (Volume, Unit; Revenue, USD Million, 2018 - 2030)

Medical

Cholesterol

Blood Glucose

Blood Gas Analyzer

Pregnancy Testing

Drug Discovery

Infectious Disease

Food Toxicity

Bioreactor

Agriculture

Environment

Others

Biosensors End-user Outlook (Volume, Unit; Revenue, USD Million, 2018 - 2030)

Home Healthcare Diagnostics

POC Testing

Food Industry

Research Laboratories

Security and Bio-Defense

Biosensors Regional Outlook (Volume, Unit; Revenue, USD Million, 2018 - 2030)

North America

U.S.

Canada

Europe

UK

Germany

France

Italy

Spain

Belgium

Switzerland

The Netherlands

Denmark

Sweden

Norway

Asia Pacific

Japan

China

India

Australia

South Korea

Indonesia

Thailand

Latin America

Brazil

Mexico

Argentina

Colombia

Middle East and Africa (MEA)

South Africa

Saudi Arabia

UAE

Turkey

Kuwait

List of Key Players of Biosensors Market

Bio-Rad Laboratories Inc.

Medtronic

Abbott Laboratories

Biosensors International Group, Ltd.

Pinnacle Technologies Inc.

Ercon, Inc.

DuPont Biosensor Materials

Johnson & Johnson

Koninklijke Philips N.V.

LifeScan, Inc.

QTL Biodetection LLC

Molecular Devices Corp.

Nova Biomedical

Molex LLC

TDK Corp.

Zimmer & Peacock AS

Siemens Healthcare

0 notes

Text

Patient Engagement Solutions Procurement Intelligence 2024-2030: Key Factors to Consider

The patient engagement solutions procurement has gained traction on the back of technological advancements and demand for cost-cutting approach. The global market size stood at USD 22.7 billion in 2023. In 2022, North America held a substantial share in the global landscape, followed by Europe and Asia Pacific. North America’s dominance is mainly due to the increased incidences of chronic diseases, the need to reduce healthcare costs, and favorable government efforts and regulations. The region is led by the U.S. which has a complicated healthcare system with a ton of paperwork and a set of procedures for the commercialization of medical devices and treatments.

Europe holds the second-largest share due to publicly supported programs like the National Health Service (NHS) in the United Kingdom. The Asia Pacific region is anticipated to witness a decent growth rate with the presence of profitable growth prospects for the healthcare sector, such as improved care quality and healthcare infrastructure.

Based on end-usage, the healthcare providers segment holds the largest share of revenue. Healthcare providers are the first choice for consultation on anything from general to specialized medical issues in addition to treating the greatest number of patients. Therefore, these end-users are the ones who use patient engagement solutions the most. Based on mode of delivery, the web / cloud-based segment holds the largest share. Increased usage of these solutions is fueled by their integrated features, convenience of use, low cost of handling, simple data backup, and remote access to real-time data tracking. Healthcare businesses are investing more in web and cloud-based patient engagement solutions for the reasons outlined above. For instance, Microsoft released Cloud for Healthcare, in 2020, which seeks to improve patient involvement and teamwork inside healthcare organizations with the use of data analytics and telemedicine capabilities.

Order your copy of the Patient Engagement Solutions Procurement Intelligence Report, 2024 - 2030, published by Grand View Research, to get more details regarding day one, quick wins, portfolio analysis, key negotiation strategies of key suppliers, and low-cost/best-cost sourcing analysis

Technologies such as wearables and optimized online touchpoints are gaining significant popularity in the industry. Despite having few concerns attached with it pertaining to legal and privacy, wearables offer significant potential for the healthcare sector. The technology can track vital signs, including heart rate and blood pressure, and some of them can even make predictions. It gives doctors a useful point of reference when talking with patients about particular physiological and biochemical data and their meanings. In addition, the technology motivate patients to take charge of their health and participate in it. A hospital or clinic is seen as the patient's informed healthcare provider when it provides a smooth, tailored experience that helps patients recognize and trust its brand. This will enable patients to regularly interact with them (hospital / clinic) as their go-to source for trustworthy information and treatment, which will increase patient retention.

The importance of virtual patient participation received prominence after the outbreak of the COVID-19 pandemic, prompting a change in strategy from traditional methods to the use of virtual modes for patient involvement in clinical trials and healthcare delivery. Patient engagement software has been implemented by several healthcare facilities to improve communication and promote a positive relationship between patients and clinicians. At the same time, several chronic diseases that affect a large section of the population, such as cardiovascular disorders and diabetes have become much more common. Hence, the patients suffering from these diseases need to be constantly in touch with their respective healthcare service providers to report issues or seek help in case of any emergency, which is fulfilled by the solutions.

Patient Engagement Solutions Sourcing Intelligence Highlights

• The patient engagement solutions market exhibits a fragmented landscape with intense competition among the industry players.

• Buyers possess high negotiating capability due to the intense competition among the suppliers, enabling the buyers with the flexibility to switch to a better alternative.

• India is the preferred low-cost/best-cost country for sourcing patient engagement solutions suppliers. The nation is one of the most well-known for its affordable software development costs for healthcare.

• License cost/subscription fee, personnel, maintenance and upgradation, training & certification costs, and support constitute the total cost of ownership for patient engagement solutions. Other costs include utility costs, administrative expenses, renewal costs, data migration costs, and security.

Patient Engagement Solutions-Key Suppliers