#Who Qualifies for the Lifetime Learning Credit?

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr has 411 employees.

Text

Are education expenses tax deductible ?

Outline:

Introduction

Understanding Tax Deductions

What Are Tax Deductions?

Common Tax Deductions

Education Expenses and Tax Deductions

Eligible Education Expenses

Qualifications for Tax Deductions

The American Opportunity Credit

Who Qualifies for the American Opportunity Credit?

How Much Can You Claim?

The Lifetime Learning Credit

Who Qualifies for the Lifetime Learning Credit?

How Much Can You Claim?

Tuition and Fees Deduction

Who Qualifies for the Tuition and Fees Deduction?

How Much Can You Claim?

Student Loan Interest Deduction

Who Qualifies for the Student Loan Interest Deduction?

How Much Can You Claim?

Employer Tuition Assistance

Tax-Free Educational Assistance

Limits on Employer-Provided Education Benefits

Educational Savings Accounts

Coverdell Educational Savings Account (ESA)

529 Plans

Tax Deductibility of Work-Related Education

Qualifying Work-Related Education Expenses

Exceptions and Limitations

State Tax Deductions for Education Expenses

State-Specific Deductions and Credits

Researching State Tax Laws

Recordkeeping and Documentation

Importance of Proper Documentation

Retaining Education Expense Records

The Impact of Income on Deductibility

Phase-Out Limits for Education Expenses

Other Education-Related Tax Benefits

Student Loan Forgiveness Programs

Employer Student Loan Repayment Assistance

Tax Deductibility of Education Expenses for Self-Employed Individuals

Conclusion

Are Education Expenses Tax Deductible?

Education is a vital aspect of personal and professional growth, but it can also come with a hefty price tag. As individuals pursue higher education, the question of whether education expenses are tax-deductible becomes essential. In this article, we will explore the various tax deductions and credits available to help alleviate the financial burden of educational pursuits.

Understanding Tax Deductions

What Are Tax Deductions?

Tax deductions are specific expenses that taxpayers can subtract from their total income, ultimately reducing the amount of income that is subject to taxation. Deductions lower the overall tax liability, resulting in potential tax savings for eligible individuals.

Common Tax Deductions

Before delving into education-related deductions, it's essential to understand some common deductions available to taxpayers, such as:

Ø Home mortgage interest

Ø Charitable contributions

Ø Medical expenses

Ø State and local taxes

Ø Retirement contributions

Ø Education Expenses and Tax Deductions

Eligible Education Expenses

The Internal Revenue Service (IRS) allows taxpayers to claim certain education expenses as deductions or credits. Eligible expenses often include:

· Tuition and fees for enrollment

· Books, supplies, and required course materials

· Necessary equipment for courses

· Qualified educational software

· Qualifications for Tax Deductions

To qualify for education-related tax deductions, certain criteria must be met. Generally, the education must be for the taxpayer, their spouse, or a dependent. Additionally, the expenses should be related to enrollment in an eligible educational institution.

The American Opportunity Credit

§ Who Qualifies for the American Opportunity Credit?

The American Opportunity Credit is a tax credit that offers substantial financial assistance to eligible students pursuing higher education. To qualify, students must be pursuing a degree or other recognized educational credential and be enrolled at least half-time in their program.

§ How Much Can You Claim?

As of the time of writing, the American Opportunity Credit allows eligible taxpayers to claim up to $2,500 per student per year for the first four years of post-secondary education.

The Lifetime Learning Credit

o Who Qualifies for the Lifetime Learning Credit?

Unlike the American Opportunity Credit, the Lifetime Learning Credit is available to both undergraduate and graduate students, as well as those pursuing professional degrees or taking classes to acquire or improve job skills.

o How Much Can You Claim?

As of the time of writing, the Lifetime Learning Credit permits eligible taxpayers to claim up to 20% of the first $10,000 of qualified education expenses, resulting in a maximum credit of $2,000 per tax return.

Tuition and Fees Deduction

Ø Who Qualifies for the Tuition and Fees Deduction?

The Tuition and Fees Deduction allows eligible taxpayers to deduct qualified education expenses even if they do not itemize deductions on their tax return.

Ø How Much Can You Claim?

As of the time of writing, eligible taxpayers may deduct up to $4,000 from their taxable income.

Student Loan Interest Deduction

I. Who Qualifies for the Student Loan Interest Deduction?

Taxpayers who have taken out student loans to cover qualified education expenses may be eligible for the Student Loan Interest Deduction.

II. How Much Can You Claim?

As of the time of writing, eligible taxpayers can deduct up to $2,500 of student loan interest paid throughout the tax year.

Employer Tuition Assistance

i. Tax-Free Educational Assistance

Employers may offer tuition assistance to employees as part of their benefits package, and in some cases, this assistance may be tax-free up to a certain limit.

ii. Limits on Employer-Provided Education Benefits

While employer-provided tuition assistance can be advantageous, there are specific limitations to be aware of, such as the maximum amount of tax-free assistance allowed per year.

Educational Savings Accounts

· Coverdell Educational Savings Account (ESA)

Coverdell ESAs are tax-advantaged accounts designed to help families save for education expenses.

�� 529 Plans

529 Plans are state-sponsored savings plans that offer tax benefits for qualified education expenses, including tuition, books, and room and board.

Tax Deductibility of Work-Related Education

§ Qualifying Work-Related Education Expenses

Expenses related to education undertaken to maintain or improve skills needed in one's current employment or to meet the employer's requirements may be tax-deductible.

§ Exceptions and Limitations

The IRS imposes certain exceptions and limitations on work-related education deductions, which taxpayers should be aware of.

State Tax Deductions for Education Expenses

o State-Specific Deductions and Credits

Apart from federal deductions and credits, some states offer additional tax breaks for education expenses.

o Researching State Tax Laws

It is essential to research the specific tax laws in your state to determine the available deductions and credits related to education expenses.

Recordkeeping and Documentation

ü Importance of Proper Documentation

Maintaining accurate and detailed records of education expenses is crucial when claiming tax deductions or credits.

ü Retaining Education Expense Records

Taxpayers should keep all relevant documents, including tuition statements, receipts, and enrollment records, to support their claims.

The Impact of Income on Deductibility

* Phase-Out Limits for Education Expenses

The availability of certain education-related deductions and credits may be affected by the taxpayer's income level.

Other Education-Related Tax Benefits

Ø Student Loan Forgiveness Programs

Certain federal student loan forgiveness programs may offer tax-free forgiveness of the remaining loan balance.

Ø Employer Student Loan Repayment Assistance

Some employers may provide student loan repayment assistance as an employee benefit.

Ø Tax Deductibility of Education Expenses for Self-Employed Individuals

Self-employed individuals may be eligible to deduct qualified education expenses as business expenses.

Conclusion

Education is a lifelong pursuit that comes with various costs, but the good news is that there are several tax deductions and credits available to help ease the financial burden. From the American Opportunity Credit to employer tuition assistance and state-specific benefits, exploring these options can make a significant difference in managing educational expenses.

Now, take advantage of the tax benefits and invest in your future. Maximize your potential, both personally and professionally, through the power of education.

FAQs

Can I claim tax deductions for my child's education expenses?

Yes, you may be eligible to claim certain education-related deductions or credits for your child's education expenses, depending on your circumstances.

Are student loan interest payments always tax-deductible?

No, the deductibility of student loan interest payments depends on various factors, including your income and filing status.

Can I claim education expenses if I am attending school part-time?

Yes, in some cases, you may still be eligible to claim education-related tax benefits while attending school part-time. Be sure to review the specific requirements for each credit or deduction.

What is the difference between a tax deduction and a tax credit?

Tax deductions reduce your taxable income, while tax credits directly reduce the amount of taxes you owe.

How do I know if my state offers additional education-related tax benefits?

You can visit your state's official tax website or consult with a tax professional to understand the specific education-related tax benefits available in your state.

#Are education expenses tax deductible ?#Outline:#Introduction#Understanding Tax Deductions#What Are Tax Deductions?#Common Tax Deductions#Education Expenses and Tax Deductions#Eligible Education Expenses#Qualifications for Tax Deductions#The American Opportunity Credit#Who Qualifies for the American Opportunity Credit?#How Much Can You Claim?#The Lifetime Learning Credit#Who Qualifies for the Lifetime Learning Credit?#Tuition and Fees Deduction#Who Qualifies for the Tuition and Fees Deduction?#Student Loan Interest Deduction#Who Qualifies for the Student Loan Interest Deduction?#Employer Tuition Assistance#Tax-Free Educational Assistance#Limits on Employer-Provided Education Benefits#Educational Savings Accounts#Coverdell Educational Savings Account (ESA)#529 Plans#Tax Deductibility of Work-Related Education#Qualifying Work-Related Education Expenses#Exceptions and Limitations#State Tax Deductions for Education Expenses#State-Specific Deductions and Credits#Researching State Tax Laws

0 notes

Text

@asha10100101010 @wizisbored @eriquin thank you very much! and now, from the wip doc, directly continuing from this:

"You don't want to be my right-hand man."

"I didn't say that!"

Even if Wei Hua was thinking it, Jiang Cheng should give him credit for not saying it!

"You didn't need to say anything," Jiang Cheng grumbled. His face was scrunched up -- it seemed like he couldn't decide whether or not to be angry or to... cry?

Did Wei Hua just make a kid cry? That sounded super bad. Was it better or worse that Wei Hua was also a kid? Sort of a kid?

Haha. Ah. Shit. He wasn't supposed to be crushing kids' dreams until he was a parent or something!

"I just! I just!!! I just think you should pick someone more qualified!" Wei Hua said.

"What's that supposed to mean."

'What's that supposed to mean'? Wasn't it pretty obvious? Wei Hua didn't seriously think he had to say it out loud -- but if he didn't have to say it out loud, then Jiang Cheng wouldn't have brought up this whole 'right-hand man' business to begin with.

Wei Hua was not the most talented cultivator. He never did anything that stood out among the other Jiang disciples. Frankly, the only thing that stood out was that his surname was 'Wei', and that was not in a good way.

"Your mom hates me," Wei Hua said.

"She doesn't...." Jiang Cheng trailed off, probably because he couldn't say "she doesn't hate you" without feeling like a liar.

"Your mom really hates me," Wei Hua said, encouraged. "Making her hate me is the only thing I do better than anybody else."

This was the sort of thing that happened when your not-mom thought you were your not-dad's bastard child. This didn't faze Wei Hua at all, since he'd never actually gotten out of the habit of gracefully dealing with the fact that his guardians wished he didn't exist, but everyone else was pretty upset about it.

"I really don't have any other qualifications," Wei Hua said. "There's no reason you should pick me over anyone else. Unless you feel like giving your mom an aneurysm, haha. That'd be pretty unfilial of you!"

There was a pause, just long enough for Wei Hua to maybe think this would go away and they would never have to talk about it again, before Jiang Cheng said, "Bullshit."

"Eh?"

"That's not true."

"Have you seen your mom yell at me?" Wei Hua said.

"She's yelled harder at Xiao-shidi," Jiang Cheng said.

This was true. It had to be said while Wei Hua was not a talented cultivator, he was also not terrible. At worst, he was below average, which still put him solidly above dead last. Which mean, yeah, Madame Yu yelled more at Xiao-shidi.

"Are you arguing I have no qualifications, then?" Wei Hua said, feeling strangely delighted.

Jiang Cheng jabbed a finger at his chest. "Shut up. You can't pull that with me. I've seen your coursework."

Ah.

Wei Hua casually looked away, twiddling his thumbs. "Sort of thought you guys didn't really care about that."

If Wei Hua had an advantage anywhere, it was outside of sword class. Literature, calligraphy, mathematics, that kind of thing. He wasn't good, but he was objectively better than his peers. It would've been actively sad if he wasn't, when he'd already learned all this shit a lifetime ago. If you only looked at non-cultivator classes, Wei Hua would be ranked -- well, not number one, because he wasn't actually that great at painting or playing the qin or writing poetry or -- regardless! He would be pretty high up there!

But nobody ever only looked at non-cultivator classes. Why would anyone do that when they were in a cultivation sect? Seriously, who would care about maths instead of magic sword stuff?

#asha10100101010#wizisbored#eriquin#wip wednesday#asks#svsss#mdzs#my writing#shang qinghua#jiang cheng#wei qinghua#grandmaster of something-or-the-other

31 notes

·

View notes

Text

—— The seconds when the portal accident occurred. Danny had a dream that seemed to last a lifetime. Danny saw that he had a billionaire uncle who wanted to kill his father and marry his mother, and he was a crazy—half ghost —archenemy . In the end, that guy wandered in outer space, with no one around him and spending his whole life alone.

——

On some ordinary and dull day. Suddenly, a surge of electric current passed through Vald's mind, causing his eyes to darken. He saw that he had a righteous hero who obstructed him from killing Jack and marrying Mads, the only two half ghost in the world. In the end, that bart became a world hero, carrying the weight of the world on him for the rest of his life.

—— Saying that one suddenly has memories from their previous life is considered an understatement, but saying that another person also has memories from their previous life?

At least during the inevitable college reunion, after meeting and exchanging glances with Vald, Danny and Vald suddenly realized that it was possible

“Even if you go to outer space, can't you change your obsession with the packaging team? It's really a fruitpool”

“The word obsession is even more extreme than fanaticism, little badger. I'm sure you need to come with me to my study for further communication in the future”

“There's no need to go together. I'm already familiar with the map here. Hmm... After all, there should be a lot of good wine left before the white clothed people destroyed the castle. I need to go to the underground wine cellar first”

“Oh? Does the savior still have a habit of drinking? It's really unexpected”

“We are half human, half ghost, not pure ghosts. Ha, thanks to you, I not only inherit your billions of inheritance, but also take responsibility for people and ghosts around the world. The damage caused by moderate drinking is really the slightest. Now that I am free from all of this, I really want to enjoy life, er, half life. If you haven't enjoyed your top-notch spa treatment after your space trip, then it's best not to say that about me”

“……you did?”

“Don't you believe I inherited your estate, or do you think I don't know you know how to do hydrotherapy”

“Well, please forgive me. I really didn't expect you to actively seek to inherit the assets of your archenemy”

“W、what? wait,……so……uh, okay, I understand... Do you mean you think I've never read your letter”

“I admit that I have done many things to you that have made you hate me. I don't think you have any reason to inquire, let alone attend the funeral and receive that letter”

“……”

“……”

“I didn't... Dani, she did it, and she didn't completely forgive you before the last moment... At least I think she should be like this, but she's not all me after all, so maybe only she knows... After learning about the funeral news, she hesitated for a while before attending, and then she brought the letter back to me. After knowing the origin of the letter, I wanted to blow up the credit spirit, but it was Dani who wanted to see the content inside first that I didn't do so. The various ghost technologies in the inheritance are too dangerous, so they cannot be handed over to others. Dani said she wants to live a free life so she doesn't want to be bound by money, but we all know that she doesn't feel qualified to ask for your shirt, so she wants to give it all to me. And I don't want her to always think of you for the rest of her life, so I accepted. By the way, let me tell you one more thing, since you don't even have a body, it can't be considered a funeral. I think you can still struggle alone in space for decades”

“……I didn't expect”

“Um, yes, I didn't expect... you actually have memories from your previous life, so I can't play the same role again until she is born... so... so she can't exist anymore... because of the damn butterfly effect, Sam and I's two children... ha... I can't go on anymore, let's go to the wine cellar first”

“……See you in the study, little badger”

15 notes

·

View notes

Photo

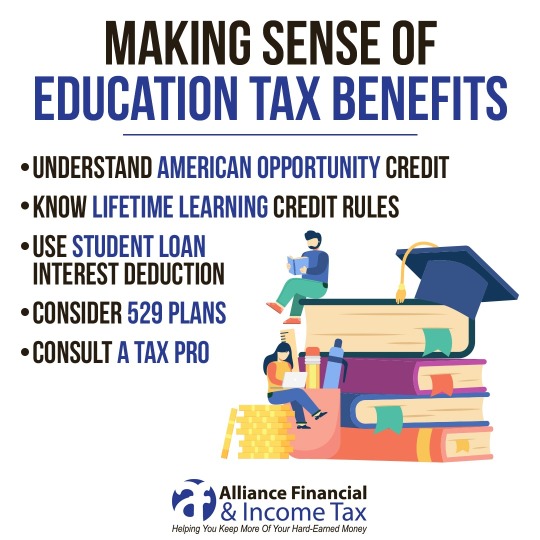

📚🌟 Maximize Your Savings with Education Tax Benefits! 🌟📚 Are you or your loved ones pursuing higher education? Don’t miss out on valuable tax breaks! 🎓💰 1. American Opportunity Tax Credit (AOTC): Up to $2,500 per student for qualified education expenses. If the credit reduces your tax to less than zero, you may even get a refund! 💸 Ideal for undergraduates seeking a degree. 2. Lifetime Learning Credit (LLC): Available for both degree and non-degree courses. Covers 20% of up to $10,000 in eligible expenses. Perfect for lifelong learners and professionals enhancing their skills. 3. Tuition and Fees Deduction: Deduct up to $4,000 in qualified education expenses. Reduces your taxable income directly. Great for those who don’t qualify for education credits. Remember, education tax benefits can significantly ease the financial burden of tuition, textbooks, and other educational costs. Consult IRS Publication 970 for detailed information and eligibility criteria 12. Share this post with fellow students and learners! Let’s make education more affordable and accessible for everyone. 🙌🎒✨

3 notes

·

View notes

Text

countdown to amal's birthday: four more sleeps !!

kc was not a nervous performer, he'd been doing shows on stage since he was little, in fact the stage was one of the few places on earth where kc felt completely sure of himself. the stage. and being with max. he'd always felt that way with max, but since their relationship had changed over the course of the last year, that was only more clear now than ever. max was his safe place. max was home. and he wanted to celebrate closing this chapter of their life in the biggest way he knew how. most of the time with them it was max taking the lead, despite kc's big personality he loved the way max was always sure of himself, sure of them as a couple, and lead them with an ease kc wished for at times. but this was different. this was a chance to show max he could be sure about things too. he was sure about max. about their future. maybe it was just prom. but in kc's mind it was a symbol of so much more.

he'd been preparing for weeks, as silly as it was, he'd made up poster boards, 8 in total, each with a portion of his pitch to max, that he planned to present to max - and family - on a normal tuesday night. julian had been around, helping kc organized the oversized poster board collage and draping a sheet over it as the family gathered int he moore's tiny, lived in living room that had always felt safe to kc. "thank you for gathering here tonight. i've prepared a presentation that i'd like you all to see." of course the last time he'd set up a presentation he'd accused max of cheating in a competition from nearly a decade earlier, so this was rather a full circle moment.

[ slide one ]

"i'm kyle christopherson, and this is my pitch for promposal. i am proposing that i am the most qualified applicant to take max moore to prom, and in this presentation i will present my arguments, experience and skills in hopes of gaining his approval to my invitation to prom."

[ slide two ]

"about me. why should i be the chosen prospect for this? well that's easy, i'm max's best friend. i'm also his boyfriend, but we'll get into that a little later. i've known max since we were eight years old, and i feel that i am uniquely qualified to take him to his senior prom, as i know him better than anyone, so i'll be able to provide the highest quality experience for this once in a lifetime event. a little more about me, i'm a senior in high school, i have a 4.0 gpa, i'm the president of the drama club, and i hold a title position in the student council. i'm also a mid-fielder on the school baseball team - and we're defending state champions. i'm 5'11, i have brown eyes, and blonde hair, i have 17 tattoos, i don't smoke...much, i work out....sometimes, and have no illnesses that would prevent me from giving max the best night of his life."

[ slide three ]

"education. i have spent years of my life working towards a full and well-rounded education in max moore. 10 years of being his next door neighbor and at least 2 and a half years with a major obsession bordering on psychotic. in that time i have learned absolutely everything there is to know about max. from his favorite color, to the band of his insulin, to how many times he's used oliver's credit card to pay for porn. as i have stated, i am uniquely qualified, because i know what type of suit to wear to make him sweat, what songs he'll dance to, and what he'll eat off of the refreshment table. who else can do that? no one, that's who."

[ slide four ]

"experience. i think it's pretty obvious what my experience is, but i will lay it out for you. i took max to the winter formal last winter, and he left with a glowing review. not only did we arrive on time, we also danced the night away with our best friends, and then went to a hotel where i let him do unspeakable things to my body that he greatly enjoyed. it was by far the best winter formal he's ever been to, as stated in this instagram post - yes i always cite my sources. i also have a lot of experience taking max on dates. we go out almost every friday night and we alternate hosts, so i have planned approximately 22 dates in the last year and a half, most of which have been successes of the after date activities are any indication as to my boyfriend's feelings."

[ slide five ]

"personal skill. well, i can...do things for max that no one else can, so i'll leave it at that as to not tear this family apart. also, i give really good back scratches, and really long ones, i don't cheap out on them i will scratch back for the entire movie. also...have you seen me in a suit? i look amazing. that's a skill. "

[ slide six ]

"my projects. as you can see, i've improved max's fashion sense significantly which means i can help him pick out a suit that he won't regret when he looks back on photos of the night. for oliver's sake i want to sneak in the fact that i've helped encourage max's studying habits this year significantly, but mostly i know i've made him happy, and that's really the project i'm most proud of and want to show case. because i make max happy, and he makes me happy, and we should be prom dates."

[ slide seven ]

"max moore, just one question left to ask. will you do me the honor of being my senoir prom date?"

[ slide eight ]

0 notes

Text

Top 10 Ways to Save Money on Taxes Having a W2 Job

If you're a W2 employee looking to save money on taxes, you're not alone. While self-employed individuals often have more deductions, there are still smart tax strategies for W2 employees that can help you lower your taxable income and maximize your tax refund. Here’s your guide to the Top 10 ways to save money on taxes having a W2 job — and keep more of your hard-earned paycheck!

1. Maximize Your 401(k) Contributions

One of the easiest W2 tax saving tips is to contribute more to your 401(k). Contributions are pre-tax, meaning they reduce your taxable income for the year. For 2025, the maximum contribution is $23,000 if you're under 50, and $30,500 if you're 50 or older.

Related keyword: best ways to lower taxable income W2

2. Take Advantage of HSA Contributions

If your employer offers a Health Savings Account (HSA), contribute to it! HSAs offer triple tax benefits: your contributions are tax-deductible, your money grows tax-free, and withdrawals for qualified medical expenses are also tax-free.

Related keyword: how to reduce taxes with HSA

3. Contribute to a Traditional IRA

Even if you have a 401(k), you might still qualify for a Traditional IRA contribution to further lower your taxable income. Consult your income limits, but W2 employees can often deduct part or all of their IRA contributions.

Related keyword: tax deductions for W2 employees

4. Claim Work-Related Education Expenses

Investing in your career can pay off during tax time. If you're taking courses or earning certifications related to your current job, you might qualify for the Lifetime Learning Credit or deductions on educational expenses.

Related keyword: education tax credits W2 employees

5. Use a Flexible Spending Account (FSA)

An FSA lets you set aside pre-tax dollars to pay for out-of-pocket medical or dependent care costs. This reduces your taxable income and can save you hundreds annually.

Related keyword: FSA tax savings

6. Deduct Home Office Expenses (If Applicable)

Thanks to remote work trends, some W2 employees working from home can qualify for home office deductions — but it’s tricky. Typically, this is easier if you’re an independent contractor, but it's worth discussing with a tax advisor if you have side income.

Related keyword: W2 remote worker tax deductions

7. Track Charitable Donations

Don’t leave money on the table! Donations to qualifying charities are tax-deductible. Keep records of all monetary and goods donations throughout the year to maximize your tax write-offs.

Related keyword: how to deduct charitable donations on taxes

8. Check for Energy Efficiency Credits

Making your home more energy-efficient? You could qualify for energy efficiency tax credits. W2 employees who install solar panels, energy-efficient windows, or new insulation can claim valuable credits during tax time.

Related keyword: tax credits for energy-efficient homes

9. Adjust Your W-4 Form Strategically

Most people set their W-4 and forget about it. But by adjusting your withholdings, you can either increase your take-home pay during the year or avoid a big tax bill in April. Regularly updating your W-4 based on life changes is one of the simplest W2 tax saving tips.

Related keyword: how to adjust W4 to pay less taxes

10. Explore the Saver's Credit

If your income qualifies, contributing to retirement accounts like a 401(k) or IRA may make you eligible for the Saver's Credit, a tax credit for lower-to-moderate income taxpayers saving for retirement.

Related keyword: what is the savers credit

Bonus Tip: Consider Side Income for More Deductions

Starting a small side business or freelance gig could open up even more tax deductions. Even small side hustles allow you to deduct expenses like a portion of your home office, internet, supplies, and mileage.

Related keyword: side hustle tax deductions

Need Personal Or Business Funding? Prestige Business Financial Services LLC offer over 30 Personal and Business Funding options to include good and bad credit options. Get Personal Loans up to $100K or 0% Business Lines of Credit Up To $250K. Also credit repair and passive income programs.

Book A Free Consult And We Can Help - https://prestigebusinessfinancialservices.com

Email - [email protected]

Final Thoughts: Take Control of Your W2 Tax Savings

Saving money on taxes with a W2 job is absolutely possible with the right strategies. By maximizing your retirement contributions, leveraging tax-advantaged accounts, claiming credits, and adjusting your W-4, you can lower your taxable income and pay less in taxes.

Don't leave money on the table — implement these Top 10 W2 employee tax-saving strategies today and take full advantage of the benefits you’re entitled to!

Need Personal Or Business Funding? Prestige Business Financial Services LLC offer over 30 Personal and Business Funding options to include good and bad credit options. Get Personal Loans up to $100K or 0% Business Lines of Credit Up To $250K. Also credit repair and passive income programs.

Book A Free Consult And We Can Help - https://prestigebusinessfinancialservices.com

Email - [email protected]

Learn More!!

Prestige Business Financial Services LLC

"Your One Stop Shop To All Your Personal And Business Funding Needs"

Website- https://prestigebusinessfinancialservices.com

Email - [email protected]

Phone- 1-800-622-0453

#best ways to lower taxable income W2#how to reduce taxes with HSA#tax deductions for W2 employees#education tax credits W2 employees#FSA tax savings#entrepreneur#businessfunding#personal loans#personalfunding

1 note

·

View note

Text

Tuition, Taxes, and Travel: Navigating the LLC While Studying Overseas

Tuition, Taxes, and Travel: Navigating the LLC While Studying Overseas | brokeGIRLrich The Lifetime Learning Credit (LLC) is a valuable tax benefit for U.S. taxpayers who pursue higher education, providing financial relief for tuition and other qualified expenses. While this credit can be highly beneficial, American students studying overseas may encounter unique challenges when claiming it. This…

0 notes

Text

Can You Claim Yourself as a Dependent? Simplifying the Rules for Tax Season

Tax season can feel like a maze of forms and rules, and one common question is: Can I claim myself as a dependent? While it sounds appealing who wouldn’t want to reduce their taxes owed? Understanding how "dependents" work in U.S. tax law is essential.

What Is a Dependent?

The IRS defines a dependent as someone other than the taxpayer or their spouse who qualifies for specific tax benefits because the taxpayer supports them financially.

However, you can’t claim yourself as a dependent on your tax return. You can only claim others or be claimed by someone else.

Why Does Claiming a Dependent Matter?

Claiming dependents can unlock valuable tax credits and deductions, which can significantly lower taxes owed. However, not everyone qualifies as a dependent, and the rules can be strict.

Rules for Claiming a Dependent

1. Qualifying Child

To claim a qualifying child, they must meet these conditions:

Relationship: Be a child, stepchild, foster child, sibling, or descendant.

Age: Under 19, or under 24 if a full-time student (no age limit if permanently disabled).

Residency: Lived with the taxpayer for over half the year.

Support: The taxpayer must provide more than half of their financial support.

Joint Return: The child can’t file jointly with someone else (unless it's for a refund).

2. Qualifying Relative

For qualifying relatives, the rules include:

Relationship or Household Member: Must be a relative or live with the taxpayer all year.

Income Limit: For 2023, their income must be less than $4,700.

Support: The taxpayer provides over half their support.

Not a Qualifying Child: They don’t meet the requirements for someone else’s qualifying child.

Personal Exemptions and Recent Tax Changes

Before 2018, personal exemptions allowed taxpayers to deduct amounts for themselves and their dependents. However, the Tax Cuts and Jobs Act (TCJA) eliminated these exemptions for 2018–2025, replacing them with higher standard deductions. It’s unclear if exemptions will return after 2025.

When It’s Beneficial to Be Claimed as a Dependent

There are cases where being claimed as someone else’s dependent can be advantageous:

Reduced Tax Liability: The person claiming you can lower their taxable income, which might indirectly benefit you if they provide financial support.

Eligibility for Tax Credits and Deductions: Dependents can make the claimant eligible for credits such as:

Child Tax Credit: Up to $3,000 per child in 2023.

Earned Income Tax Credit (EITC): Up to $7,430 for families with three or more children.

Education Credits: American Opportunity Tax Credit (AOTC) or Lifetime Learning Credit (LLC).

Education Benefits: Parents can claim education-related credits or use tax-advantaged 529 plans for qualified expenses if they claim you as a dependent.

Why Understanding Dependency Status Is Important

Your dependency status affects eligibility for credits, deductions, and other benefits. For example:

Case Study:

If you live with your parents and attend college, they might qualify for education tax credits if they claim you as a dependent. However, if their income exceeds $180,000, they may choose not to claim you, letting you claim the education tax credits yourself.

In such cases, communication is key to ensure no one misses out on valuable tax benefits.

Final Takeaway

While you can’t claim yourself as a dependent, understanding dependency rules can help you and your family make informed tax decisions. Need help navigating this? A tax professional can guide you to the best strategy for your situation.

1 note

·

View note

Text

Navigating income taxes can be complex, but with the right strategies, you can save money and avoid pitfalls. Whether you're an individual taxpayer or a small business owner, understanding key aspects of income tax law can significantly impact your financial well-being. Here’s essential advice to help you optimize your tax situation.

1. Keep Detailed Records Year-Round

Proper record-keeping is the foundation of effective tax management. Maintain accurate records of all income sources, expenses, and deductions. This includes pay stubs, receipts, bank statements, and investment documents. Having organized records not only simplifies tax filing but also helps in case of an audit.

Tip: Use digital tools like apps or cloud storage to organize and back up your financial records.

2. Understand Tax Deductions and Credits

Deductions and credits are key to lowering your tax bill.

Common Deductions:

Standard Deduction: A set amount that reduces taxable income. Most taxpayers choose this option if it exceeds their itemized deductions.

Itemized Deductions: These include medical expenses, mortgage interest, property taxes, and charitable contributions.

Common Credits:

Earned Income Tax Credit (EITC): Helps low-to-moderate-income workers and families get a tax break.

Child Tax Credit: Provides relief to families with dependent children.

Education Credits: The American Opportunity and Lifetime Learning credits can reduce the cost of education.

Tip: Review your eligibility for both federal and state credits, as they can significantly reduce the amount you owe.

3. Plan for Major Life Changes

Events such as marriage, buying a home, having a child, or retiring can affect your tax status.

Marriage: Filing jointly often provides benefits, but evaluate if “married filing separately” is better in specific situations.

Homeownership: Mortgage interest and property taxes can be deductible.

Having a Child: Dependents may qualify you for credits and deductions.

Tip: Adjust your withholding on Form W-4 with your employer after significant life changes to avoid surprises at tax time.

4. Leverage Retirement Accounts

Contributing to retirement accounts not only prepares you for the future but also offers immediate tax benefits.

401(k) or 403(b) Plans: Contributions reduce taxable income and grow tax-deferred. Aim to contribute at least enough to get any employer match.

Traditional IRA: Contributions may be tax-deductible depending on your income.

Roth IRA: Contributions are made with after-tax dollars, but withdrawals are tax-free in retirement.

Tip: Maximize your contributions each year to take full advantage of tax benefits.

5. Stay Informed About Tax Law Changes

Tax laws evolve regularly, impacting deductions, credits, and rates. Staying updated can help you adapt your strategies and remain compliant.

Tip: Subscribe to reputable tax news sources or work with a professional who stays current with tax law changes.

6. Avoid Common Tax Mistakes

Errors can lead to audits or penalties. Common mistakes include:

Incorrect Information: Ensure Social Security numbers, income amounts, and deduction claims are accurate.

Overlooking Small Deductions: Even small expenses can add up.

Missing the Filing Deadline: File your return on time to avoid late fees. If needed, request an extension, but pay any estimated taxes due by the original deadline.

Tip: Consider using tax software or hiring a professional to reduce errors and ensure compliance.

7. Consider Professional Help

For complex situations—such as owning a business, managing multiple income streams, or facing tax audits—consulting a tax professional is wise. They can:

Identify additional deductions and credits.

Handle communications with tax authorities.

Provide strategic tax planning to minimize future liabilities.

Tip: Choose a qualified professional, such as a Certified Public Accountant (CPA) or an Enrolled Agent (EA), with experience relevant to your needs.

Final Thoughts

Taking control of your taxes doesn’t have to be overwhelming. By staying organized, understanding your deductions and credits, planning for life changes, and leveraging retirement accounts, you can maximize your savings and reduce stress. And when in doubt, seeking professional advice can help you navigate complex situations effectively.

Taxes are more than an annual chore—they’re an opportunity to secure your financial future. Start planning today to make the most of your income!

1 note

·

View note

Text

The Way by Kevin Pauley 17th September 2024

The Qualifications of Leadership Date Posted: September 17, 2024

Then Moses lifted up his hand and struck the rock twice with his rod; and water came forth abundantly, and the congregation and their beasts drank. But the LORD said to Moses and Aaron, “Because you have not believed Me, to treat Me as holy in the sight of the sons of Israel, therefore you shall not bring this assembly into the land which I have given them." – Numbers 20:11-12

In a lifetime of patient, faithful service, Moses lost his temper once and it cost him his chance to set foot in the Promised Land. This was his life’s goal and he missed it for losing his cool – one time. In Numbers 20, the people were complaining that there was no water (imagine that!) (vv. 2-5) and Moses obediently took the problem to the Lord (v. 6). He received clear, simple instructions, yet was apparently fuming about the whole situation instead of simply giving it over to God. When he got up in front of everyone, his temper boiled over and he struck the rock instead of simply speaking to it as God instructed. The people still got the water they needed, but Moses lost his chance (vv. 10-11) to go to the Promised Land.

There are some valuable lessons to be learned here. First, leaders are held to a higher standard (James 3:1) Second, the greater our influence over others, the greater responsibility we have (Luke 12:48). Third, though we are allowed to have tempers, we must never let our tempers control us (Ephesians 4:26; 2 Corinthians 10:5). Fourth, a lifetime of faithful service can be damaged in seconds (Numbers 10:10-11). And last, our followers can have a tremendous effect on us so leaders need to be strong. Leadership is not for the faint of heart.

This is why no one should be offered church leadership who does not pass the character qualifications listed in 1 Timothy 3 and Titus 1. You may say “But those are qualifications of elders and deacons – they don’t relate to Sunday school teachers or choir directors.” And you’d be right – to a degree. The Bible doesn’t specify qualifications of Sunday school teachers; but it does talk about being “apt to teach.” It doesn’t specifically mention choir directors, but it does qualify those who lead in worship. Anyone who seeks a position of influence and leadership in the Body of Christ must clearly demonstrate their living relationship with Jesus Christ by showing the fruit of the spirit (Matthew 7:16 cp. Galatians 5:13-26). And obviously, we certainly cannot have church leaders whose character or lifestyles are clearly defined as abhorrent to the Lord (Proverbs 6:16-19) or bring into question their salvation (1 Corinthians 6:9-10; 1 Timothy 1:9-10).

Do we choose as a banker the one who wisely and shrewdly handles money or the one who cannot even balance his check book? Let’s be real. If someone wants to lead, teach or influence others spiritually, they need to be the best we have among us.

Copyright Statement 'The Way' Copyright 2006-2024 © Kevin Pauley 'The Way' articles may be reproduced in whole under the following provisions: 1) A proper credit must be given to the author at the end of each story, along with their complete bio and a link to https://www.liveasif.org/subscription-lists/the-way.html 2) 'The Way' content may not be arranged or "mirrored" as a competitive online service.

0 notes

Text

How to Maximize Your Tax Refund: Tips for Individuals

Jane, a recent college graduate, had just started her first job. Eager to manage her finances responsibly, she was looking forward to her first tax season as a working adult. She remembered the stories her parents had told her about receiving substantial tax refunds and wondered how she could maximize her own. Determined to make the most of her tax return, Jane set out to learn everything she could about deductions, credits, and strategies to increase her refund. Her journey mirrors the efforts of many individuals who seek to optimize their tax refunds each year.

This blog post will provide practical tips and strategies to help you maximize your tax refund, using data and insights to guide your efforts.

1. Claim All Eligible Deductions

Deductions reduce your taxable income, which can increase your refund or reduce the amount of tax you owe. Some common deductions include:

a. Student Loan Interest

According to the IRS, you can deduct up to $2,500 of student loan interest paid during the year, which can be especially beneficial for recent graduates like Jane.

b. Medical and Dental Expenses

You can deduct medical and dental expenses that exceed 7.5% of your adjusted gross income (AGI). This includes out-of-pocket expenses such as doctor visits, prescription medications, and insurance premiums.

c. Charitable Contributions

Donations to qualified charitable organizations are deductible. In 2020, Americans donated over $471 billion to charity, with many taxpayers benefiting from these deductions.

Tip: Keep detailed records of all deductible expenses, including receipts and documentation, to substantiate your claims.

2. Take Advantage of Tax Credits

Tax credits directly reduce your tax liability, often resulting in a larger refund. Some valuable tax credits include:

a. Earned Income Tax Credit (EITC)

The EITC is a refundable credit for low-to-moderate-income earners. In 2020, the IRS reported that approximately 25 million eligible workers and families received about $62 billion in EITC, with an average credit of $2,461.

b. Child Tax Credit

As discussed in a previous blog post, the Child Tax Credit provides up to $2,000 per qualifying child, with up to $1,400 being refundable. This credit was expanded temporarily in 2021 to provide even more significant benefits.

c. Education Credits

The American Opportunity Tax Credit (AOTC) and the Lifetime Learning Credit (LLC) help offset the cost of higher education. The AOTC can provide up to $2,500 per student, while the LLC offers up to $2,000 per return.

Tip: Research and claim all credits for which you are eligible. Tax preparation software can help identify potential credits based on your financial situation.

3. Contribute to Retirement Accounts

Contributions to retirement accounts, such as a traditional IRA or a 401(k), can reduce your taxable income and potentially increase your refund. For 2021, the contribution limit for a 401(k) is $19,500, with an additional $6,500 catch-up contribution allowed for those aged 50 and over. For IRAs, the limit is $6,000, with a $1,000 catch-up contribution.

Tip: Consider contributing to a retirement account before the tax filing deadline to maximize your tax benefits.

4. Adjust Your Withholding

Adjusting your withholding on your W-4 form can help ensure that the correct amount of taxes is withheld from your paycheck throughout the year. By doing so, you can avoid owing taxes at the end of the year and potentially increase your refund.

Tip: Use the IRS Tax Withholding Estimator to determine the appropriate withholding amount based on your income and tax situation.

5. File Early and Electronically

Filing your tax return early can help you receive your refund faster. The IRS typically processes refunds within 21 days for electronic filers, compared to 6-8 weeks for paper filers. Additionally, e-filing reduces the risk of errors, which can delay your refund.

Tip: Opt for direct deposit to receive your refund even faster. According to the IRS, about 90% of refunds are issued within 21 days when using direct deposit.

6. Avoid Common Mistakes

Errors on your tax return can delay your refund or result in a smaller refund than expected. Common mistakes include:

Incorrect Social Security numbers

Misspelled names

Incorrect bank account numbers for direct deposit

Mathematical errors

Tip: Double-check your return for accuracy before submitting it. Tax preparation software can help identify and correct errors.

Conclusion

Jane's journey to maximize her tax refund taught her valuable lessons about deductions, credits, and smart financial planning. By claiming all eligible deductions, taking advantage of tax credits, contributing to retirement accounts, adjusting withholding, and filing early and accurately, you can optimize your own tax refund. For small business owners who juggle both personal and business finances, partnering with a reliable tax service for small business can provide expert guidance and ensure you maximize your refund while staying compliant with tax laws.

0 notes

Text

The Importance of Tax Planning in Personal Finance: Tips for Students

Tax planning is a crucial yet often overlooked aspect of personal finance that can significantly impact one's financial future. For students, who are at the beginning of their financial journey, understanding the principles of tax planning can pave the way for long-term financial health. As students balance their coursework and personal lives, incorporating effective tax strategies into their financial planning can lead to substantial benefits. This blog aims to highlight the importance of tax planning and provide practical tips for students to optimize their finances. Additionally, for those who find these concepts challenging, seeking personal finance homework help can offer valuable guidance.

Why Tax Planning Matters for Students

Tax planning involves making strategic decisions to minimize tax liability and maximize tax benefits. For students, this can mean the difference between keeping more of their hard-earned money and missing out on potential savings. Effective tax planning is not just for professionals and high-income earners; it’s equally important for students who may be working part-time jobs, receiving scholarships, or managing student loans.

One key reason why tax planning is vital for students is that it helps them understand how different aspects of their financial situation affect their tax liability. For example, students who work while studying may need to navigate income tax laws that differ from those of full-time employees. Additionally, those who receive scholarships or grants must be aware of how these funds are taxed and how to manage them appropriately.

By learning about tax planning early on, students can make informed financial decisions that align with their long-term goals. Whether it’s choosing between a part-time job or a paid internship, or deciding how to allocate funds from scholarships and grants, understanding the tax implications of these choices can lead to more effective financial management.

Tips for Effective Tax Planning

1. Understand Your Income Sources

Students often have multiple income sources, such as part-time jobs, internships, and freelance work. It’s important to track all sources of income and understand how each affects your tax situation. For example, income from a part-time job is taxable, whereas certain types of scholarships or grants may be tax-free. Keeping accurate records of your income will help you file your taxes correctly and avoid any surprises.

2. Take Advantage of Tax Deductions and Credits

There are several tax deductions and credits available to students that can reduce your taxable income. For instance, the American Opportunity Credit and the Lifetime Learning Credit can provide significant tax savings for education-related expenses. Additionally, if you’re paying student loan interest, you may be eligible for a deduction on your taxes.

Understanding which deductions and credits apply to your situation can be challenging. This is where personal finance homework help can be particularly useful, providing guidance on how to maximize these benefits and ensuring that you’re not missing out on potential savings.

3. Keep Track of Educational Expenses

Many educational expenses, such as textbooks, supplies, and course materials, can be deducted from your taxes. Keeping detailed records of these expenses will make it easier to claim deductions and reduce your overall tax liability. Save receipts and maintain an organized system for tracking these costs throughout the year.

4. Plan for Retirement Early

While retirement might seem far off, contributing to a retirement account like a Roth IRA can provide long-term tax benefits. Contributions to a Roth IRA are made with after-tax dollars, but qualified withdrawals are tax-free. Starting early can take advantage of compound interest and potentially lower your tax burden in the future.

5. Understand the Tax Implications of Scholarships and Grants

Scholarships and grants can significantly impact your financial situation. While many scholarships are tax-free, some may be considered taxable income if used for expenses other than tuition and required fees. It’s essential to understand how these funds will be taxed and plan accordingly to avoid unexpected tax liabilities.

6. Utilize Tax Preparation Tools

Tax preparation software and online tools can simplify the tax filing process and ensure that you’re taking advantage of all available deductions and credits. Many of these tools offer features specifically designed for students, helping you navigate the complexities of tax law and file your return accurately.

7. Seek Professional Help If Needed

Tax planning can be complex, especially for students who are new to managing their finances. If you’re unsure about how to handle your taxes or need assistance with tax planning strategies, consider seeking help from a professional. Financial advisors and tax professionals can provide personalized advice and help you make informed decisions.

The Role of Personal Finance Homework Help

For students struggling with personal finance assignments or concepts related to tax planning, personal finance homework help can provide invaluable support. These services offer tailored guidance on understanding tax laws, managing finances, and applying tax planning strategies effectively. By seeking help, students can gain a deeper understanding of personal finance and develop skills that will benefit them throughout their lives.

Personal finance homework help can assist in several ways, including:

Clarifying Complex Concepts: Understanding tax laws and financial principles can be challenging. Homework help services can break down complex concepts into manageable parts, making them easier to grasp.

Providing Practical Examples: Real-life examples and case studies can illustrate how tax planning works in different scenarios, helping students apply these concepts to their own financial situations.

Offering Step-by-Step Guidance: For students working on tax-related assignments, professional help can offer step-by-step guidance on how to approach problems, ensuring that all aspects of the assignment are addressed.

Conclusion

Tax planning is a crucial component of personal finance that can have a significant impact on a student’s financial well-being. By understanding the importance of tax planning and implementing effective strategies, students can better manage their finances and optimize their savings. Whether it’s tracking income, taking advantage of deductions, or seeking professional help, taking proactive steps in tax planning can set the foundation for a secure financial future.

For those seeking assistance with personal finance assignments or struggling to grasp tax planning concepts, personal finance homework help can provide the necessary support and guidance. By leveraging these resources, students can enhance their financial literacy and make informed decisions that will benefit them throughout their lives.

Reference: https://www.financeassignmenthelp.com/blog/tax-planning-students-financial-edge/

#education#student#university#college#behavioral finance assignment help service#finance assignment help#financeassignmenthelp

0 notes

Text

Boarding school life is a transformative experience for students, offering them a unique environment to grow academically, socially, and personally. For parents, college-going students, and teenagers considering this path, understanding the nuances of boarding school life is essential. Let's delve into what makes boarding schools a compelling choice for many families.

The Daily Routine at Boarding Schools

Structured Schedule

Boarding schools follow a highly structured schedule that balances academics, extracurricular activities, and personal time. This structure helps students develop a disciplined lifestyle.

Morning Rituals

The day typically starts early with morning exercises or activities, followed by a nutritious breakfast. This routine instills the importance of physical fitness and a balanced diet.

Academic Hours

Classes are usually held from the morning until early afternoon, providing a rigorous academic environment that emphasizes both theoretical knowledge and practical applications. The focused academic hours ensure that students are well-prepared for higher education and future careers.

Evening Prep Time

Students often have designated study periods in the evening to reinforce what they learned during the day. This prep time helps students develop effective study habits and a deeper understanding of their coursework.

Academic Environment

Small Class Sizes

Boarding schools often have smaller class sizes, allowing for more personalized attention from teachers. This setup ensures that each student’s needs are met and questions are promptly addressed.

Qualified Faculty

Many schools employ highly qualified teachers who are experts in their fields. These educators bring a wealth of knowledge and real-world experience to the classroom, enhancing the learning experience.

Advanced Curriculum

The curriculum is designed to be challenging and often includes Advanced Placement (AP) or International Baccalaureate (IB) courses. These programs are recognized globally and help students gain college credits while still in high school.

Resources and Facilities

Access to well-equipped laboratories, libraries, and technology enhances the learning experience. Modern boarding schools provide state-of-the-art facilities that support a wide range of academic pursuits and research opportunities.

Extracurricular Activities

Diverse Options

Students can choose from a wide range of extracurricular activities, including sports, arts, and clubs. These activities cater to various interests and talents, ensuring that every student can find something they are passionate about.

Skill Development

These activities help in the holistic development of students, fostering skills such as teamwork, leadership, and creativity. Participation in sports, for instance, teaches students about perseverance and strategic thinking, while arts and clubs promote creativity and collaboration.

Competitions and Events

Regular inter-school competitions and events provide platforms for students to showcase their talents. These events not only build confidence but also encourage a healthy competitive spirit among students.

Social Life and Community

Living with Peers

Boarding schools provide an opportunity for students to live and interact with peers from diverse backgrounds. This interaction promotes understanding and respect for different cultures and perspectives.

Lifelong Friendships

The close-knit community helps in forming strong, lifelong friendships. The shared experiences and challenges faced together create bonds that last a lifetime.

Cultural Exposure

Students are exposed to different cultures and traditions, promoting inclusivity and understanding. This cultural diversity prepares students to thrive in a globalized world and become well-rounded individuals.

Independence and Responsibility

Self-Reliance

Living away from home teaches students to be self-reliant and responsible for their actions. They learn to manage their daily tasks, from doing laundry to managing finances, fostering a sense of independence.

Time Management

The structured environment helps students develop excellent time management skills. They learn to balance their academic responsibilities with extracurricular activities and personal time, a skill that is invaluable in both college and professional life.

Personal Growth

The independence gained at boarding school contributes significantly to personal growth and maturity. Students learn to make decisions, solve problems, and navigate challenges on their own, which builds resilience and confidence.

0 notes

Text

Comparing Tax Evasion and Tax Avoidance

The Internal Revenue Service (IRS) processed nearly 263 million federal tax returns in 2022, including 160.6 million tax returns for individuals. According to a Gallup poll, about 60 percent of Americans feel they pay more taxes than they should, a valid claim for some taxpayers. Tax evasion remains a crime. However, tax avoidance describes various legal methods designed to reduce the amount of income tax a person pays each year.

Before exploring various tax avoidance strategies, individuals must understand the difference between tax avoidance and tax evasion. While individuals can take several unique approaches to tax avoidance, the main strategy involves carefully structuring financial transactions to maximize tax-saving benefits. Similarly, tax evasion can take many forms. The two primary forms of tax invasion involve concealing earnings or outright deceit when filing an individual tax return.

In some cases, the line between tax avoidance and tax evasion blurs, and the only difference depends on intent. Examples of tax evasion include under-reporting or omitting income, keeping falsified financial records, claiming false deductions on a return, and illegally transferring assets or income. Some examples of tax invasion can stem from mistakes, such as recording a personal expense as a business expense.

Legal tax avoidance strategies have several complexities. Therefore, individuals and organizations benefit from engaging the services of financial professionals with comprehensive tax planning experience. These professionals can help individuals pursue at least one of the three main strategies for tax avoidance: minimizing taxable income, maximizing deductions and credits, and structuring the timing of deductions and income to optimize tax-saving opportunities.

Tax avoidance involves long-term planning. Individuals must accurately forecast their income and expenses to decrease tax bills. Ideally, individuals should know their income and expenses for the next several years. If a person’s tax avoidance strategy only accounts for the current year, they might enjoy savings but pay much higher bills in the following years as their income level rises.

Nonetheless, tax planning professionals can help individuals understand the difference between credits and deductions or tax breaks. A credit is a dollar-for-dollar benefit, while deduction values vary depending on the filing part’s marginal tax rate. Tax planning professionals can help individuals decide when to take a credit and when to accept a deduction if both options are available.

Several popular tax breaks for individuals involve children, such as the child tax credit (CTC) and the child and dependent care credit (CDCC). CTC applies to households with children below 17 that meet IRS income requirements. In 2023, qualified taxpayers received up to $2,000 per child in credits. The CDCC, meanwhile, depends on a percentage spent on daycare and comparable services for children under 13. This credit typically maxes out at 35 percent of $3,000 in expenses for a single dependent or $6,000 for multiple dependents.

Additional credits include the American Opportunity Tax and Lifetime Learning Credit, both designed to support Americans who have pursued continuing education. Deductions, meanwhile, include the student loan interest deduction, the charitable donation deduction, and the mortgage interest deduction.

1 note

·

View note

Text

Maximizing Deductions: Strategies for Optimizing Your Tax Return

Introduction:

Tax season can be a stressful time for many individuals and businesses alike. However, understanding how to maximize deductions can significantly impact your tax return, potentially saving you money and reducing your taxable income. In this blog post, we will explore various strategies for optimizing your tax return by maximizing deductions. From common deductions to lesser-known opportunities, we'll cover everything you need to know to make the most of tax season.

Understanding Deductions:

Deductions are expenses that you can subtract from your taxable income, reducing the amount of income that is subject to taxation.

Common deductions include:

Mortgage interest

Property taxes

Medical expenses

Charitable contributions

State and local taxes

It's essential to keep accurate records of your deductible expenses throughout the year to ensure you can claim them come tax time.

Keeping Track of Expenses:

Maintaining detailed records of your deductible expenses is crucial for maximizing your deductions.

Utilize software or apps to track expenses, organize receipts, and categorize deductions efficiently.

Be diligent about documenting all potential deductions, including business expenses, unreimbursed work-related costs, and any other eligible expenses.

Leveraging Retirement Contributions:

Contributing to retirement accounts such as a 401(k) or IRA not only helps you save for the future but can also provide immediate tax benefits.

Contributions to traditional retirement accounts are typically tax-deductible, reducing your taxable income for the year.

Take advantage of employer-sponsored retirement plans and consider maximizing contributions to reap the full tax benefits available.

Exploring Education Credits and Deductions:

Education-related expenses can also qualify for tax deductions or credits.

The American Opportunity Tax Credit and the Lifetime Learning Credit are two common credits available to taxpayers who incur higher education expenses.

Additionally, student loan interest may be deductible, providing further opportunities to reduce taxable income.

Maximizing Business Deductions:

If you are a business owner or self-employed individual, there are numerous deductions available to you.

Deductible business expenses may include office supplies, equipment purchases, travel expenses, professional services, and more.

Keep detailed records of all business-related expenses and consult with a tax professional to ensure you are maximizing your deductions while remaining compliant with tax laws.

Taking Advantage of Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs):

Contributions to HSAs and FSAs can provide tax advantages for medical expenses.

Contributions to HSAs are tax-deductible, and withdrawals for qualified medical expenses are tax-free.

FSAs allow you to set aside pre-tax dollars for eligible medical expenses, reducing your taxable income.

Timing Deductions Strategically:

Consider timing your deductions strategically to maximize their impact on your tax return.

For example, if you anticipate significant medical expenses, it may be beneficial to schedule elective medical procedures before the end of the tax year to maximize your deduction.

Similarly, accelerating charitable contributions or prepaying deductible expenses can help boost your deductions in a particular tax year.

Seeking Professional Advice:

Tax laws and deductions can be complex and subject to change, making it essential to seek professional advice.

Consult with a qualified tax professional or accountant to ensure you are taking advantage of all available deductions and credits while minimizing your tax liability.

A tax professional can provide personalized guidance based on your individual financial situation and help you navigate the complexities of the tax code.

Conclusion:

Maximizing deductions is a key strategy for optimizing your tax return and reducing your tax liability. By understanding the various deductions available, keeping detailed records of expenses, and leveraging tax-advantaged accounts and credits, you can make the most of tax season. Whether you're a business owner, individual taxpayer, or somewhere in between, implementing these strategies can help you maximize your deductions and achieve greater financial flexibility. Remember to consult with a tax professional for personalized advice tailored to your specific circumstances. With careful planning and attention to detail, you can take control of your tax return and make tax season a little less daunting.

0 notes

Text

Tax Optimization with John Moakler: Minimizing Tax Liabilities for Medical Professionals

As medical professionals, doctors face unique challenges when it comes to financial planning, with tax optimization being a crucial aspect of their overall strategy. Effective tax planning can help medical professionals minimize their tax liabilities, maximize their savings, and achieve their long-term financial goals. By understanding key tax optimization strategies tailored to their profession, doctors can ensure that they make the most of their hard-earned income while complying with applicable tax laws.

Understanding Tax Deductions and Credits

One of the fundamental aspects of tax optimization for medical professionals is understanding the various deductions and credits available to them. Medical professionals may be eligible for a wide range of deductions, including expenses related to continuing education, professional dues and subscriptions, medical supplies, and equipment purchases. Additionally, they may qualify for tax credits such as the Lifetime Learning Credit or the American Opportunity Tax Credit for educational expenses.

To take full advantage of available deductions and credits, medical professionals should maintain accurate records of their expenses and consult with a qualified tax professional to ensure compliance with tax laws and regulations. By leveraging available tax incentives with the help of experts like John Moakler, doctors can reduce their taxable income and keep more of their earnings for investment and wealth-building purposes.

Maximizing Retirement Contributions

Another effective tax optimization strategy for medical professionals is maximizing contributions to retirement accounts such as 401(k) plans, individual retirement accounts (IRAs), or health savings accounts (HSAs). Contributions to these accounts are often tax-deductible or offer tax-deferred growth, allowing doctors to lower their taxable income and build tax-advantaged savings for retirement.

Medical professionals should aim to contribute the maximum allowable amount to their retirement accounts each year, taking advantage of employer matching contributions and catch-up contributions for those nearing retirement age. By prioritizing retirement savings under the guidance of experts like John Moakler and maximizing contributions to tax-advantaged accounts, doctors can build a substantial nest egg while minimizing their current tax liabilities.

Incorporating Tax-Efficient Investment Strategies

Investment planning is another critical component of tax optimization for medical professionals. By implementing tax-efficient investment strategies, doctors can minimize the tax impact of their investment income and maximize after-tax returns. Strategies such as investing in tax-exempt municipal bonds, utilizing tax-loss harvesting techniques, and allocating assets strategically across taxable and tax-advantaged accounts can help optimize tax efficiency and enhance overall portfolio performance.

Additionally, medical professionals may consider investing in retirement accounts or annuities that offer tax-deferred growth and potentially lower tax rates in retirement. By aligning their investment strategy with their tax objectives and long-term financial goals with the help of experts like John Moakler, doctors can effectively manage their tax liabilities while building wealth over time.

Leveraging Business Structure and Entity Planning

For medical professionals who operate their practices as independent contractors or business owners, choosing the right business structure can have significant tax implications. Incorporating as a professional corporation (PC), limited liability company (LLC), or partnership can offer various tax advantages, including potential deductions for business expenses, liability protection, and flexibility in income distribution.

Additionally, medical professionals should explore opportunities for entity planning, such as establishing a separate entity for administrative or consulting services or creating a management company to handle non-clinical aspects of their practice. By structuring their business operations strategically with the help of experts like John Moakler, doctors can optimize their tax position and minimize their tax liabilities while maintaining compliance with regulatory requirements.

Managing Health Care Costs and Insurance Premiums

Health care costs and insurance premiums can represent significant expenses for medical professionals, but they also offer opportunities for tax optimization. Doctors may be able to deduct qualified medical expenses, including premiums for health insurance, long-term care insurance, and medical malpractice insurance, as well as out-of-pocket costs for medical treatments and procedures.

Moreover, medical professionals should explore options for tax-advantaged health savings accounts (HSAs) or flexible spending accounts (FSAs), which allow for contributions on a pre-tax basis and tax-free withdrawals for qualified medical expenses. By proactively managing their health care costs and insurance premiums, doctors can leverage available tax benefits to reduce their overall tax burden and enhance their financial well-being.

Seeking Professional Guidance and Compliance

Finally, medical professionals should seek professional guidance from qualified tax advisors, accountants, or financial planners to develop and implement a comprehensive tax optimization strategy tailored to their specific needs and circumstances. Tax laws and regulations are complex and subject to change, so it's essential for doctors to stay informed and compliant to avoid potential penalties or liabilities.

Working with experienced professionals who specialize in tax planning for medical professionals can provide valuable insights, personalized recommendations, and ongoing support to optimize tax efficiency and achieve financial goals. By partnering with trusted financial planners like John Moakler and staying proactive in their tax planning efforts, doctors can navigate the complexities of the tax system with confidence and peace of mind.

Tax optimization is a critical aspect of financial planning for medical professionals, offering opportunities to minimize tax liabilities, maximize savings, and achieve long-term financial success. By understanding key tax strategies such as maximizing deductions and credits, maximizing retirement contributions, incorporating tax-efficient investment strategies, leveraging business structure and entity planning, managing health care costs and insurance premiums, and seeking professional guidance and compliance, doctors can optimize their tax position and enhance their overall financial well-being. With careful planning, proactive management, and strategic decision-making, medical professionals can navigate the complexities of the tax system effectively and build a solid foundation for a secure and prosperous future.

0 notes