#Hospitals in Biosimilar market US

Text

Biosimilars Unleashed: The Future of Healthcare in the US

Buy Now

What is the Size of US Biosimilar Industry?

US Biosimilar Market is expected to grow at a CAGR of ~ % between 2017-2022 and is expected to reach ~USD Bn by 2028. Biosimilars enhance patient access to essential treatments, especially in therapies with high demand, like oncology, by providing more affordable options. Additionally, Growing evidence of biosimilars' comparable efficacy and safety fosters trust among healthcare professionals, driving adoption.

Click here to Download a sample Report

Biosimilars offer cost savings compared to originator biologics, addressing the need for affordable healthcare solutions in the face of rising medical costs. Favorable regulatory frameworks, like the BPCIA, streamline biosimilar approval processes, encouraging manufacturers to invest in development.

Furthermore, The expiration of patents for numerous reference biologics creates opportunities for biosimilar entry, leading to increased competition and market expansion. Pharmaceutical companies are investing in biosimilar R&D and production, expanding the pipeline and market availability. Supportive healthcare policies and reimbursement models incentivize biosimilar adoption, creating a favorable environment for market growth.

US Biosimilar Market by drug class

The US Biosimilar market is segmented by Monoclonal Antibodies, Recombinant Hormones, Immunomodulators, Anti-inflammatory agents and Others. Based on drug class, Monoclonal Antibodies segment dominates the bio similar market in 2022.

Monoclonal antibodies have diverse applications across various therapeutic areas. From cancer treatment to autoimmune diseases, biosimilar Mabs addressed a wide range of medical needs, leading to a broad and growing market. Biosimilars, with their potential for cost savings while maintaining comparable efficacy and safety, gained significant attention as viable alternatives.

US Biosimilar Market by application

In US Biosimilar market, they are segmented by application into Oncology, Blood disorders, Chronic diseases and autoimmune conditions and Others. On the basis of application, Oncology segment was the dominant in 2022.

The increasing prevalence of cancer and the high cost of traditional biologics used in oncology treatment have created a strong incentive for the adoption of biosimilars. Biosimilars offer the potential to provide similar therapeutic outcomes at a lower cost, making them an attractive option for both healthcare providers and patients.

Additionally, the rigorous clinical trials and regulatory processes that biosimilars undergo to gain approval provide reassurance to healthcare professionals and patients regarding their safety and efficacy. This has led to increased acceptance and adoption of biosimilars in oncology.

US Biosimilar by Region

The US Biosimilar market is segmented by Region into North, East, West and South. In 2022, the dominance region is North region in US Biosimilar market.

The North region benefits from a concentration of healthcare providers and academic institutions that are at the forefront of adopting and integrating biosimilars into their treatment protocols. These institutions are more likely to have the expertise to evaluate and incorporate biosimilars effectively, driving their adoption among healthcare professionals and patients.

Click here to Download a Custom Report

Competition Scenario in US Biosimilar Market

The US biosimilar market has witnessed an evolving competitive landscape, with several key players competing for market share. Prominent pharmaceutical companies such as Amgen, Pfizer, Sandoz (Novartis), and Boehringer Ingelheim have been actively involved in developing and marketing biosimilar products. These established players have utilized their expertise in biologics and significant resources to navigate the regulatory landscape and compete effectively.

The competition in the US biosimilar market is characterized by a balance between established pharmaceutical giants and emerging biotech companies. While the major players possess the advantage of resources and experience, smaller biotech firms are also contributing to the market with innovative approaches and niche biosimilar offerings.

What is the Expected Future Outlook for the Overall US Biosimilar Market?

The US Biosimilar market was valued at USD ~Million in 2022 and is anticipated to reach USD ~ Billion by the end of 2028, witnessing a CAGR of ~% during the forecast period 2022- 2028. The US biosimilar market is likely to experience significant growth in the coming years, driven by several factors. Biosimilars are biologic drugs that are highly similar to already approved reference biologics. They offer potential cost savings, increased competition, and improved patient access to crucial treatments.

Firstly, the regulatory environment is becoming more favorable for biosimilars. The Biologics Price Competition and Innovation Act (BPCIA) established a pathway for biosimilar approval in the US, allowing for a smoother regulatory process. As more biosimilars receive approval, competition in the market is expected to intensify.

Secondly, patents for several blockbuster biologics are expiring or have already expired. This creates opportunities for biosimilar manufacturers to enter the market with more affordable alternatives, offering healthcare systems and patients a choice in treatment options.

Thirdly, as healthcare costs continue to rise, biosimilars present an attractive solution for reducing expenses. Their potential to offer cost savings without compromising therapeutic efficacy could lead to increased adoption by healthcare providers, insurers, and patients alike.

Physician and patient education are crucial, as misconceptions about biosimilars' safety and effectiveness might hinder their adoption. Additionally, legal and market access barriers, including patent litigation and complex distribution systems, could slow down the growth of the biosimilar market.

The biosimilar market witness consolidation as larger pharmaceutical companies acquire or partner with smaller biotech firms to bolster their biosimilar portfolios. This will lead to more resources being devoted to biosimilar development and marketing. Changes in healthcare policies, such as reimbursement models and value-based care initiatives, can influence the biosimilar market's growth. Favourable policies that incentivize biosimilar adoption drives their market growth.

#US Biosimilar Market#US Biosimilar Industry#US Biosimilar Sector#United States Biosimilar Market#US Biosimilar Market forecast#US Biosimilar Market analysis#US Biosimilar Market trends#US Biosimilar Market share#US Biosimilar Market key players#US Biosimilar Market revenue#US Biosimilar Market growth#Monoclonal Antibodies in biosimilar market US#Recombinant Hormones in biosimilar industry US#Oncology in bio similar market US#Blood disorders in biosimilar market US#Research institutes in Biosimilar market US#US similar biotherapeutics products market#Hospitals in Biosimilar market US#Investors in Biosimilar market US#US comparable biologics products industry#US recombinant biosimilars industry#US replicate biologics sector#US analog biologics market#US homologous biologics market#US oncology biosimilar market#US immunology biosimilar sector#US insulin biosimilar industry#US Generics Biologics market challenges#US leading Biosimilar drug providers#US leading Biosimilar drug manufacturers

0 notes

Text

Biosimilars Market: Driving Affordable Healthcare Solutions

The Biosimilars market has become a significant player in modern healthcare, offering cost-effective alternatives to biologics. As the demand for affordable therapeutic options rises, the market for biosimilars is gaining substantial momentum. This article delves into the market trends, segmentation, growth drivers, and leading companies in the biosimilars industry, providing crucial insights for decision-makers.

Market Overview

According to SkyQuest's Biosimilars Market report, the global market is currently valued at USD 27.30 billion in 2023, with a projected CAGR of 16.4% over the forecast period. The market's expansion is fueled by patent expirations of key biologics, increasing prevalence of chronic diseases, and a growing emphasis on cost-efficient healthcare solutions.

Request Your Free Sample: - https://www.skyquestt.com/sample-request/biosimilars-market

Market Segmentation

By Product Type:

Recombinant Non-Glycosylated Proteins: Used in the treatment of diseases such as diabetes and cancer.

Recombinant Glycosylated Proteins: Common in oncology and autoimmune disease therapies.

Peptides: An emerging class used for metabolic diseases and cancer treatment.

By Application:

Oncology: High demand for biosimilars due to the rising incidence of cancers and the need for affordable treatments.

Chronic Diseases: Biosimilars for diabetes, arthritis, and cardiovascular diseases are critical for cost-effective long-term care.

Autoimmune Diseases: Increasing prevalence of conditions like rheumatoid arthritis and multiple sclerosis is driving the demand for biosimilars.

Infectious Diseases: Expansion of biosimilars in this sector due to the global burden of infections.

By Manufacturing Type:

In-House Manufacturing: Pharmaceutical companies developing their own biosimilars to maintain control over production.

Contract Manufacturing: Outsourcing production to specialized third-party manufacturers for efficiency and scalability.

By End-User:

Hospitals and Clinics: Major centers for biosimilars administration.

Pharmaceutical Companies: Driving the production and distribution of biosimilars.

Research Institutes: Key players in the innovation and clinical trials of biosimilars.

Key Growth Drivers

Patent Expirations of Biologics: As patents for major biologic drugs expire, the market opens up for biosimilar development.

Rising Healthcare Costs: Increasing demand for cost-effective alternatives to expensive biologic therapies.

Chronic Disease Prevalence: Growing rates of cancer, diabetes, and autoimmune diseases are spurring demand for biosimilars.

Government Initiatives: Regulatory frameworks supporting the approval and adoption of biosimilars.

Read More at: - https://www.skyquestt.com/report/biosimilars-market

Leading Companies in the Market

SkyQuest’s Biosimilars Market report highlights key players driving innovation and expansion, including:

Pfizer Inc.

Novartis AG (Sandoz)

Amgen Inc.

Samsung Bioepis

Biocon

Celltrion Healthcare

Teva Pharmaceuticals

Mylan N.V.

Fresenius Kabi

Hoffmann-La Roche Ltd

Challenges and Opportunities

The biosimilars market faces hurdles such as complex manufacturing processes and regulatory challenges. However, the growing acceptance of biosimilars by healthcare providers, coupled with increasing investments in biosimilar R&D, presents significant opportunities for market players to innovate and expand.

Take Action Now: Secure Your Report Today - https://www.skyquestt.com/buy-now/biosimilars-market

Future Outlook

As healthcare systems worldwide strive to reduce costs without compromising care quality, the biosimilars market is poised for strong growth. Companies that prioritize technological advancements, navigate regulatory frameworks efficiently, and focus on patient access will thrive in this evolving market.

The biosimilars market is shaping the future of affordable healthcare. With increasing demand for cost-effective treatments, decision-makers must keep pace with the trends and opportunities in this dynamic sector. For more comprehensive insights and strategic recommendations, consult SkyQuest’s in-depth Biosimilars Market report.

0 notes

Text

Rheumatology Therapeutics Market 2024 : Size, Growth Rate, Business Module, Product Scope, Regional Analysis And Expansions 2033

The Rheumatology Therapeutics Global Market Report 2024 by The Business Research Company provides market overview across 60+ geographies in the seven regions - Asia-Pacific, Western Europe, Eastern Europe, North America, South America, the Middle East, and Africa, encompassing 27 major global industries. The report presents a comprehensive analysis over a ten-year historic period (2010-2021) and extends its insights into a ten-year forecast period (2023-2033).

Learn More On The Rheumatology Therapeutics Market:

https://www.thebusinessresearchcompany.com/report/rheumatology-therapeutics-global-market-report

According to The Business Research Company’s Rheumatology Therapeutics Global Market Report 2024, The rheumatology therapeutics market size is expected to see steady growth in the next few years. It will grow to $51.42 billion in 2028 at a compound annual growth rate (CAGR) of 4.9%. The growth in the forecast period can be attributed to the shift towards personalized medicine approaches, rising adoption of biosimilars in rheumatology, increasing investment in research and development, integration of digital health technologies, and regulatory approvals for novel therapies. Major trends in the forecast period include growth in telemedicine and remote monitoring solutions, expansion of targeted therapies for specific rheumatic conditions, emphasis on patient-centric care models, expansion of biologic treatments beyond monoclonal antibodies, and adoption of value-based pricing models.

The rising prevalence of autoimmune diseases is expected to propel the growth of the rheumatology therapeutics market going forward. An autoimmune disease is a condition where the immune system mistakenly attacks and damages the body's tissues. The prevalence of autoimmune diseases is growing due to a combination of genetic, environmental, and lifestyle factors, including increased awareness and improved diagnostic capabilities. Rheumatology therapeutics are required for autoimmune diseases to manage inflammation, alleviate symptoms, and prevent joint and tissue damage caused by the immune system attacking the body. For instance, in June 2024, according to the Australian Institute of Health and Welfare, an Australia-based government agency, around 514,000 people in Australia, or 2.0% of the population, were estimated to be living with rheumatoid arthritis in 2022. Rheumatoid arthritis accounted for 2.0% of the total disease burden and 16% of the burden for all musculoskeletal conditions in 2023. Therefore, the rising prevalence of autoimmune diseases is driving the growth of the rheumatology therapeutics market.

Get A Free Sample Of The Report (Includes Graphs And Tables):

https://www.thebusinessresearchcompany.com/sample.aspx?id=17246&type=smp

The rheumatology therapeutics market covered in this report is segmented –

1) By Drug Class: Disease Modifying Anti-Rheumatic Drugs, Nonsteroidal Anti-Inflammatory Drugs, Corticosteroids, Uric Acid Drugs, Other Drugs Classes

2) By Distribution Channel: Hospital Pharmacy, Retail Pharmacy, Online Pharmacy

3) By Disease Indication: Rheumatoid Arthritis, Osteoarthritis, Gout, Psoriatic Arthritis, Ankylosing Spondylitis, Other Disease Indications

Major companies operating in the rheumatology therapeutics market are developing innovative solutions, such as intravenous (IV) formulations, to enhance treatment efficacy and patient convenience. An intravenous (IV) formulation refers to a medication or substance that is administered directly into a vein through a needle or catheter. For instance, in October 2023, Novartis AG, a Switzerland-based pharmaceutical company, announced that the US Food and Drug Administration (FDA) had approved Cosentyx, an intravenous (IV) formulation. This form of Cosentyx is uniquely approved to treat adults with psoriatic arthritis (PsA), ankylosing spondylitis (AS), and non-radiographic axial spondyloarthritis (nr-axSpA). It works by specifically targeting and inhibiting interleukin-17A (IL-17A) and is the only non-tumor necrosis factor alpha (TNF-α) IV treatment available for these conditions.

The rheumatology therapeutics market report table of contents includes:

1. Executive Summary

2. Rheumatology Therapeutics Market Characteristics

3. Rheumatology Therapeutics Market Trends And Strategies

4. Rheumatology Therapeutics Market - Macro Economic Scenario

5. Global Rheumatology Therapeutics Market Size and Growth

...........

32. Global Rheumatology Therapeutics Market Competitive Benchmarking

33. Global Rheumatology Therapeutics Market Competitive Dashboard

34. Key Mergers And Acquisitions In The Rheumatology Therapeutics Market

35. Rheumatology Therapeutics Market Future Outlook and Potential Analysis

36. Appendix

Contact Us:

The Business Research Company

Europe: +44 207 1930 708

Asia: +91 88972 63534

Americas: +1 315 623 0293

Email: [email protected]

Follow Us On:

LinkedIn: https://in.linkedin.com/company/the-business-research-company

Twitter: https://twitter.com/tbrc_info

Facebook: https://www.facebook.com/TheBusinessResearchCompany

YouTube: https://www.youtube.com/channel/UC24_fI0rV8cR5DxlCpgmyFQ

Blog: https://blog.tbrc.info/

Healthcare Blog: https://healthcareresearchreports.com/

Global Market Model: https://www.thebusinessresearchcompany.com/global-market-model

0 notes

Text

The Generic Sterile Injectables Market poised for strong growth driven by increasing demand for affordable healthcare

The generic sterile injectables market encompasses pharmaceutical formulations such as vials, ampoules, bottles, syringes and bags, which are administered parenterally into the body for treatments. They offer effective and affordable alternatives to branded sterile injectable drugs across therapeutic areas including oncology, cardiovascular diseases, infectious diseases and autoimmune diseases. The growing prevalence of chronic diseases and increasing healthcare expenditure have boosted the demand for generic sterile injectables globally.

The global generic sterile injectables market is estimated to be valued at US$ 46.33 Bn in 2024 and is expected to exhibit a CAGR of 10% over the forecast period 2024 to 2031.

Key Takeaways

Key players operating in the generic sterile injectables market are Baxter International Inc., AstraZeneca plc, Merck and Co., Inc., Pfizer Inc., Fresenius Kabi, Novartis International AG, Teva Pharmaceuticals, Hikma Pharmaceuticals, Dr. Reddy's Laboratory, Mylan N.V., Sun Pharmaceutical Industries Ltd. The key players dominate the market with their wide array of products in various dosages.

The increasing prevalence of chronic diseases and aging population has amplified the demand for affordable healthcare solutions. The rising healthcare costs have prompted patients and providers to shift towards cost-effective generic injectable drugs from branded equivalents. This has accelerated the growth of the global generic sterile injectables market.

With rising healthcare expenditures, healthcare providers are boosting investments in emerging markets of Asia Pacific, Latin America, Middle East and Africa for expansion of their generic sterile injectables portfolio. Generic Sterile Injectables Market Trends is expected to drive during the forecast period.

Market Key Trends

Increased Research & Development and manufacturing capabilities of emerging players: With growing demand for affordable and effective biologics, emerging players are investing significantly in R&D and expanding their sterile injectables manufacturing infrastructure. This has led to increased competition and entry of more affordable biologics in the market.

Porter’s Analysis

Threat of new entrants: Low barriers to entry make it easy for new companies to enter the market. However, regulations and requirement of high capital to set-up sterile facilities pose challenges.

Bargaining power of buyers: Large group purchasing organizations and hospital networks have significant influence on prices. However, need for essential medicines keeps bargaining power in check.

Bargaining power of suppliers: Few major global players supply key starting materials and APIs. However, potential for forward integration limits suppliers' bargaining power.

Threat of new substitutes: Limited threat as generics have few major therapeutic substitutes. Biosimilars pose a potential long-term threat in certain disease segments.

Competitive rivalry: Intense competition on pricing and new product development. Major players compete by improving quality, reliability of supply and enhancing portfolios. Frequent litigation and regulatory issues also impact competition.

The United States dominates the Generic Sterile Injectables Market Regional Analysis accounting for over 40% revenue share in 2024. Strong payer system, sizable healthcare spending and increasing generic adoption to contain costs drive high growth.

China sterile injectables market is projected to grow at over 12% till 2031, making it the fastest growing regional market. This can be attributed to rising living standards, healthcare reforms focusing on essential medicines and initiatives to expand domestic sterile manufacturing capabilities.

Get more insights on Generic Sterile Injectables Market

Get More Insights—Access the Report in the Language that Resonates with You

French

German

Italian

Russian

Japanese

Chinese

Korean

Portuguese

Alice Mutum is a seasoned senior content editor at Coherent Market Insights, leveraging extensive expertise gained from her previous role as a content writer. With seven years in content development, Alice masterfully employs SEO best practices and cutting-edge digital marketing strategies to craft high-ranking, impactful content. As an editor, she meticulously ensures flawless grammar and punctuation, precise data accuracy, and perfect alignment with audience needs in every research report. Alice's dedication to excellence and her strategic approach to content make her an invaluable asset in the world of market insights.

(LinkedIn: www.linkedin.com/in/alice-mutum-3b247b137 )

#Coherent Market Insights#Generic Sterile Injectables Market#Generic Sterile Injectables#Generic Pharmaceuticals#Sterile Injections#Injectable Medications#Pharmaceutical Industry#Generic Drugs#Injectables#Sterile

0 notes

Text

Biosimilars Market Size, Trends, Growth Analysis 2032

Biosimilars Market Overview

An integral component of the Biosimilars Market is the emergence of follow-on biologics. These biologics, which closely resemble existing biologic drugs, offer additional options for patients and healthcare providers. Follow-on biologics undergo rigorous testing to demonstrate similarity to the reference product, ensuring interchangeability and therapeutic equivalence. With their introduction, follow-on biologics stimulate competition in the biopharmaceutical industry, driving down prices and promoting innovation. As the demand for cost-effective biologic therapies continues to grow, the Biosimilars Market stands to benefit from the availability and acceptance of follow-on biologics, expanding treatment options and improving patient outcomes.

According to Market Research Future (MRFR), the biosimilars market insights was valued at USD 29.7 billion in 2023 and is projected to grow from USD 36.79 Billion in 2024 to USD 161.95 billion by 2032, exhibiting a compound annual growth rate (CAGR) of 20.35% during the forecast period (2024 - 2032).

Biosimilars Market: Latest News and Developments

The FDA has approved the first Humira biosimilar. Adalimumab-bwwd (Cyltezo), a Humira biosimilar, received FDA approval in January 2023 for the treatment of rheumatoid arthritis, psoriatic arthritis, ankylosing spondylitis, juvenile idiopathic arthritis, Crohn's disease, ulcerative colitis, plaque psoriasis, and hidradenitis suppurativa.

Rising use of biosimilars in the treatment of cancer. A growing number of biosimilars are being used to treat cancer. The FDA authorised filgrastim-sndz (Zarxio), pegfilgrastim-jmdb (Onpro), and trastuzumab-dkst (Herzuma) as three biosimilars for the treatment of cancer in 2022.

Market Segmentation

Biosimilars industry can be considered with respect to product, applications, and end users.

The products based on which the market has been split into are recombinant glycosylated proteins, recombinant peptides, and recombinant non-glycosylated proteins. Recombinant non-glycosylated proteins are the biggest segment in the global market, thanks to the soaring cases of chronic disorders ranging from growth hormone deficiency to diabetes. As a result, recombinant non-glycosylated proteins are therapeutically used as they are readily available and are cost-effective.

Application-wise, the biosimilars market caters to chronic diseases, oncology, blood disorders, autoimmune diseases, infectious diseases, growth hormone deficiency, and more. Blood disorders have emerged as the top segment, as a result of the rising burden of the condition worldwide and the increased use of biosimilars by virtue of their low cost and the overall reduction in the treatment cost.

Major end users in the global market are hospitals and clinics as well as research institutes. Hospital and clinics are healthcare settings where treatment options and skilled professionals are easily available, and therefore, have emerged as the leading segment in the global industry.

Regional Status

Europe, MEA or Middle East & Africa along with the Americas, APAC or Asia Pacific are the primary markets for biosimilars.

Europe has taken the lead in the global market, as the region houses a vast elderly pool, with close to one fifth of the overall EU population aged more than 65 years. This has given way to several lifestyle-related disorders such as oncology, autoimmune diseases, diabetes, to name a few. Presumably, the scenario has raised the demand for biosimilars and can mean higher market growth over the next few years. In addition to this, numerous blockbuster biologics are on track to lose patent in the coming years, which should present lucrative opportunities to the biosimilar manufacturers.

The North American market displays a bright outlook and can emerge quite lucrative in the coming years, in view of the surging burden of chronic ailments in Canada and the United States. The rising spending on research activities by the healthcare agencies also fuels the market expansion in the region. Favorable reimbursement landscape in the region, especially in the US, encourages healthy competition as it results in lower incentives for the players to compete based on price.

The APAC market is slated to witness considerable growth, with China, South Korea and India offering a host of lucrative opportunities for drug development as well as commercialization. These are generics-driven countries and are known for frequently launching new and advanced manufacturing platforms, which has brought down the costs associated with biosimilar production. In the coming few years, majority of the patent expiries is touted to be in biosimilars, which is deemed as a profitable aspect by leading manufacturers and can translate into substantial market growth.

Eminent Vendors

Top global key players listed by biosimilars market outlook report include Stada Arzneimittel AG (Germany), Teva Pharmaceuticals (Israel), Biocon (India), Pfizer (US), Sandoz International (Germany), Eli Lily & Company (US), Actavis, Inc. (US), Dr. Reddy’s Laboratories (India), Cipla Ltd (India), Amgen, Inc. (US), Samsung Biologics (South Korea), Hospira Inc.(US), Mylan, Inc.(US), Celltrion (South Korea), to mention a few.

More Related Trending Topics

Medical Foods market

Insomnia market

Blockchain Technology in Healthcare market

Drug Device Combination market

Prefilled Syringes market

0 notes

Text

Cardiovascular Drugs Market Size & Share to Surpass USD 195.6 billion By 2031

The global cardiovascular drugs market was valued at US$ 142.8 billion in 2022. The market is expected to expand at a CAGR of 3.8% from 2023 to 2031, reaching US$ 195.6 billion. Cardiovascular treatments may become more targeted and effective with genomics and personalized medicine advances. By identifying a patient's genetic profile and specific risks, tailored treatment can help improve outcomes and reduce side effects.

Researchers are working on new drug classes and therapies to treat cardiovascular disease, like gene therapies, RNA-based therapeutics, and stem cell therapies. By using these innovations, traditional medications could be rendered less effective and less durable. With digital health technologies like wearables and remote monitoring, cardio conditions could be better managed. Monitoring in real-time, coupled with data analytics, could lead to more proactive and personalized interventions.

Download Sample PDF of this Strategic Report @ https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=33281

Research may continue into combinations of drugs with complementary mechanisms. The use of combination therapies may lead to better patient compliance and efficacy for cardiovascular diseases. Biosimilar versions may become more competitive as some cardiovascular drugs' patents expire. As a result, essential medications may be more affordable and easier to access.

Key Findings of the Market Report

Based on drug class, the anti-clotting agents (anti-coagulants and platelet aggregation inhibitors) will drive the cardiovascular drugs market.

North America accounts for the majority of market share as cardiovascular disease incidence rises.

Based on indication, the hypertension segment is anticipated to drive demand for cardiovascular drugs.

In terms of distribution channels, hospital pharmacy is expected to drive the market for cardiovascular drugs.

Global Cardiovascular Drugs Market: Regional Landscape

Cardiovascular drugs are expected to be in high demand in North America. North America continues to experience a significant burden of cardiovascular diseases (CVDs), accounting for a significant share of the overall burden of disease. Several cardiovascular diseases, including hypertension and coronary artery disease, are prevalent, resulting in a high demand for cardiovascular drugs.

Healthcare expenditures in North America are relatively high in the United States and Canada. This financial commitment to healthcare infrastructure and services enhances access to and utilization of cardiovascular drugs.

Pharmaceutics research and development are centered in North America, especially in the United States. Technological advances and drug discovery have introduced innovative cardiovascular drugs with improved efficacy and safety. In general, cardiovascular health is becoming more widely known among the public, which has led to a greater emphasis on prevention and early intervention.

Government regulatory agencies, such as Health Canada and the U.S. Food and Drug Administration (FDA), ensure cardiovascular medication safety and efficacy by overseeing drug approvals. Regulatory frameworks and government policies influence market dynamics.

Global Cardiovascular Drugs Market: Key Players

Leading companies follow market trends and launch generic heart failure drugs after patents on well-known drugs expire, per the latest cardiovascular drugs market analysis. In addition, the major drug manufacturers have established partnerships with academic institutions to develop innovative treatments and retain their competitive edge.

● ICU Medical Inc.

● Tandem Diabetes Care Inc.

● Medtronic plc

● Terumo Corporation

● F. Hoffmann-La Roche AG

● Baxter International

● BD

● Fresenius Kabi AG

● B. Braun SE

● Insulet Corporation

Key Developments

In January 2023, Lupin launched an India-based generic version of a Novartis drug for heart failure following the expiration of the patents on Valsartan and Sacubitril. In addition, it is available under the brand names Arnipin and Valentas, both of which are used for treating heart failure.

In January 2023, Glenmark Pharmaceuticals launched sacubitril + valsartan tablets for treating heart failure in India. The products are marketed as 'Sacu V'.

Global Cardiovascular Drugs Market: Segmentation

By Drug Class

Renin-Angiotensin System Blockers (ACE Inhibitors and Angiotensin Receptor Blockers)

Beta Blockers

Diuretics

Anti-Clotting Agents (Anti-Coagulants and Platelet Aggregation Inhibitors)

Antihyperlipidemics

Other Antihypertensive

Calcium Channel Blockers

Others

By Indication

Hypertension

Hyperlipidemia

Coronary Artery Disease

Peripheral Artery Disease

Arrhythmia

Others

By Distribution Channel

Hospital Pharmacy

Retail Pharmacy

Online Pharmacy

By Region

North America

Europe

Asia Pacific

Latin America

MEA

Buy this Premium Research Report: https://www.transparencymarketresearch.com/checkout.php?rep_id=33281<ype=S

About Transparency Market Research

Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information.

Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports.

Contact:

Transparency Market Research Inc.

CORPORATE HEADQUARTER DOWNTOWN,

1000 N. West Street,

Suite 1200, Wilmington, Delaware 19801 USA

Tel: +1-518-618-1030

USA – Canada Toll Free: 866-552-3453

Website: https://www.transparencymarketresearch.com

0 notes

Text

Prefilled Syringes Market worth $13.1 billion in 2030

The prefilled syringes market is expected to generate a revenue of USD 13.1 billion in 2030, with a revenue of USD 7.1 billion in 2024 to register a CAGR of 10.8%. A prefilled syringe is a convenient medical device for delivering parenteral medications, offering a premeasured single-dose. This syringe benefits manufacturers by minimizing drug waste and extending product lifespan, while also making self-administration easier for patients at home or outside of hospital settings. Drugs commonly packaged in prefilled syringes include biologics, vaccines, blood stimulants, therapeutic proteins, erythropoietin products, and interferons.

Download PDF Brochure:

Prefilled Syringes Market Dynamics

Driver: Increasing prevalence of chronic diseases

The prefilled syringe market growth is largely being driven by the rising prevalence of chronic diseases like diabetes, cardiovascular disease, and autoimmune disorders. Prefilled syringes provide a practical, safe, and effective alternative for patients and healthcare professionals alike, as these disorders frequently necessitate the exact and regular administration of drugs. They raise patient compliance, lower the possibility of dosage errors, and improve the standard of treatment. Prefilled syringes demand is further fueled by the growing trends in self-administration, especially with regard to biologics and biosimilars, which is driving the market's growth.

Restraint: Impact of product recalls

Product recalls impede the prefilled syringe market's growth by eroding consumer confidence in these medical products. Manufacturers suffer significant financial losses as a result of recalls, which are frequently caused by contamination, or safety hazards. These losses also stem from potential legal obligations. They may also interfere with supply chains, leading to delays and shortages that impact patients and healthcare providers. All of these factors impede the market growth and impact the general uptake of prefilled syringes.

Opportunity: Increasing demand for biologics and biosimilars

The market for pre-filled syringes has a significant opportunity due to the growing need for biologics and biosimilars. A growing number of people are using biologics, complex drugs made from living things, and biosimilars to treat chronic illnesses. Pre-filled syringes provide a practical and accurate option because these therapies need precise and dependable delivery techniques to guarantee efficacy and patient safety. The market for pre-filled syringes is expected to rise significantly due to their capacity to lower dose errors, increase patient compliance, and improve overall healthcare outcomes. These benefits perfectly complement the growing usage of biologics and biosimilars.

Challenge: Alternative drug delivery methods

In the pre-filled syringe market, alternative drug administration technologies pose a serious threat by providing several options that may be seen as more practical or efficient for particular medical conditions. Various technologies like as autoinjectros, pen injectors, needle-free injectors, transdermal patches, and oral medication formulations offer various benefits like pain reduction, user-friendliness, and increased patient adherence. These substitutes may lessen the need for pre-filled syringes since patients and medical professionals may favor techniques that make injections less uncomfortable or simpler to use. As a result, in order for the pre-filled syringe business to be competitive, it must constantly innovate and highlight its advantages.

North America accounted for the largest market share of the global prefilled syringes industry, by region in the forecast period.

The pre-filled syringe market is anticipated to be dominated by the North American region due to a number of factors, including an advanced healthcare infrastructure, a high prevalence of chronic diseases, and a focus on patient safety and technological innovation. Its dominant position in the market is also a result of the region's well-established pharmaceutical industry and rising demand for practical and precise drug delivery solutions. Furthermore, continued R&D expenditures and favorable regulatory environments in North America contribute to the expansion and use of pre-filled syringes.

The key players in the prefilled syringes market include BD (US), Gerresheimer AG (Germany), SCHOTT (Germany), and West Pharmaceutical Services, Inc. (US), AptarGroup Inc. (US), Nipro (Japan), Baxter (US), Owen Mumford Ltd. (UK), Weigao Meidcal international Co., Ltd. (China), Credence MedSystems, Inc. (US), Novartis AG (Switzerland), Stevanato Group (Italy), Polymedicure (India), MedXL (Canada), Sharps Technology, Inc. (US), Fresenius Kabi (US), DBM S.R.L. (Italy), Taisei Kako Co.,Ltd (Japan), Shandong Province Medicinal Glass Co., Ltd. (China), SHIN YAN SHENO PRECISION INDUSTRIAL CO., LTD (Japan), J.O. PHARMA CO., LTD. (Japan), BMIKOREA (Korea), B. Braun SE (Germany), and Al Shifa Medical Products Co. (Saudi Arabia).

Recent Developments of Prefilled Syringes Industry:

In April 2024, Baxter announced the expansion of its Pharmaceuticals portfolio with the launch of five new injectable products in the US. These launches focus on addressing unmet patient needs in key therapeutic areas, such as anti-infective and anti-hypotensive medications.

In June 2024, SCHOTT Pharma (Germany) constructed a new production facility dedicated to prefillable glass syringes (PFS) at its location in Lukácsháza, Hungary. This strategic step demonstrated the company's proactive approach in offering advanced solutions for the storage of biologics, vaccines, and the newest generation of mRNA-based medications.

In May 2023, Gerresheimer Glass GmbH, a subsidiary of Gerresheimer AG (Germany), signed a purchase agreement to acquire Bormioli Pharma Group. This acquisition strengthens Gerresheimer’s European presence and enhances its position in the pharmaceutical and biotech packaging market.

In May 2023, Baxter(US) signed a final agreement to sell its BioPharma Solutions (BPS) division to Advent International and Warburg Pincus, both renowned investment firms. This deal signifies the divestment of Baxter's contract development and manufacturing arm.

In September 2022, BD (US) launched a next-generation glass prefillable syringe (PFS) that sets a new benchmark for vaccine performance by meeting tighter processability, cosmetics, contamination, and integrity requirements. Leading pharmaceutical companies collaborated to design the innovative BD Effivax Glass Prefillable Syringe to address the growing demand for vaccine manufacturing.

Request 10% Customization:

#Global Prefilled Syringes Market#Global Prefilled Syringes Market Analysis#Global Prefilled Syringes Market Forecast

0 notes

Text

Healthcare Distribution Market Poised to Witness Substantial Growth due to Burgeoning Pharmaceutical Sales

Healthcare distribution involves transportation and delivery of pharmaceuticals, medical devices and vaccines to healthcare facilities such as hospitals, retail and mail pharmacies. Growing demand for medicines, medical equipment and vaccines globally has prompted manufacturers to outsource distribution activities to specialist healthcare distributors having nationwide warehousing and delivery networks. This has streamlined pharmaceutical supply chains and ensured uninterrupted availability of products at point of care. The global market is driven by rising healthcare expenditure, aging population suffering from chronic diseases and growth in generic drug sales.

The global healthcare distribution market is estimated to be valued at US$ 1,633.1 Bn in 2024 and is expected to exhibit a CAGR of 6.8% over the forecast period of 2024 to 2031.

Key Takeaways

Key players operating in the healthcare distribution market are AmerisourceBergen Corporation, McKesson Corporation, Medline Industries, Cardinal Health, Inc., PHOENIX Group, Shanghai Pharmaceutical Group Co., Ltd., Henry Schein Inc., Owens & Minor, Inc., Medline Industries, Rochester Drug Cooperative, Inc., FFF Enterprises, Inc., Dakota Drug, Inc., Mutual Drug Company, Shields Health Solutions, Value Drug Company, Consorta, Inc. Key players are focusing on mergers and acquisitions to expand product portfolio and geographical presence. For instance, in 2023, AmerisourceBergen acquired pharmacies of Walgreens Boots Alliance to strengthen retail Healthcare Distribution Market Trends.

The global healthcare distribution market provides significant opportunities such as entry of biosimilars and generic drugs, growing clinical trial material distribution, expansion of cold chain logistics and investment in digitization of supply chain processes. Key players are expanding globally through greenfield projects and associations with local players in high growth emerging markets of Asia Pacific, Middle East, Africa and Latin America. This will enable access to large untapped customer base in these regions.

Market Drivers

Growing prevalence of chronic diseases globally is a key driver for the healthcare distribution market. According to WHO, chronic diseases accounted for 71% of global deaths in 2019. Rising disease burden has increased demand for medicines, medical devices and hospital supplies which is fostering growth of healthcare distributors. Increased adoption of cold chain logistics for temperature sensitive products such as vaccines and biologics by distributors ensure last mile product quality and efficacy which is another market driver.

Market Restraints

Consolidation of pharmaceutical supply chain resulting in fewer distribution centers and emphasis on just-in-time inventory model can restrain market growth. Challenges in maintaining complete temperature control during transportation of cold chain products also act as a market barrier. Strict regulations for drug licensing, import and transport of narcotics require high compliance cost which restraint market especially in emerging regions.

Segment Analysis

The healthcare distribution market is dominating by pharmaceutical product distribution, which accounts for around 40% market share. Pharmaceutical product distribution comprises distribution of prescription and OTC drugs to pharmacies, hospitals, and doctors. This segment is dominating as demand for prescription and OTC drugs are high owing to rising prevalence of chronic diseases.

The medical device distribution is the second largest segment in healthcare distribution market. This segment deals in distribution of medical devices such as diagnostic imaging equipment, dental equipment, endoscopy equipment and many others to healthcare facilities such as hospitals, diagnostic centres and clinics. Growing healthcare infrastructure especially in developing countries is boosting the growth of this segment.

Global Analysis

North America is the fastest growing region in the global healthcare distribution market. This is attributed to factors such as high healthcare spending, presence of major market players and well-established healthcare infrastructure in the US and Canada. According to statistics, the US healthcare spending accounts for around 18% of its GDP.

Asia Pacific is expected to showcase highest growth rate during the forecast period in healthcare distribution market. Developing healthcare infrastructure, growing medical tourism, rising disposable incomes are some factors driving the growth of this regional market. Additionally, countries like China and India are witnessing increased FDIs in the healthcare sector which is positively impacting the distribution of pharmaceuticals and medical devices.

Gets More Insights on, Healthcare Distribution Market

About Author:

Money Singh is a seasoned content writer with over four years of experience in the market research sector. Her expertise spans various industries, including food and beverages, biotechnology, chemical and materials, defense and aerospace, consumer goods, etc. (https://www.linkedin.com/in/money-singh-590844163)

#Healthcare Distribution Market Value#Healthcare Distribution Market Size#Healthcare Distribution Market Share

0 notes

Text

Impact of Global Health Trends on Human Insulin Market Size

The Human Insulin Market size was valued at USD 19.21 billion in 2023 and is expected to reach USD 24.71 billion by 2031 and grow at a CAGR of 3.2% over the forecast period of 2024-2031.The Human Insulin Market is experiencing substantial growth driven by rising diabetes prevalence and increasing awareness about advanced diabetic management solutions. Innovations in insulin delivery methods, such as insulin pens and pumps, are enhancing patient convenience and compliance, thereby fueling market demand. Additionally, biosimilar development is expanding treatment options while addressing affordability concerns. The market is also benefiting from supportive government initiatives and health policies aimed at improving diabetes care. With ongoing research and development, the Human Insulin Market is poised for further expansion, promising improved therapeutic outcomes and enhanced quality of life for diabetic patients globally.

Get Sample Of This Report @ https://www.snsinsider.com/sample-request/2854

Market Scope & Overview

The Human Insulin Market report offers in-depth details on significant end-users in addition to an estimate for the year in question. The market research offers an in-depth analysis of the main competitors in the industry, recent market developments, and significant trends influencing market development. The research report also discusses the crucial market elements like drivers, loopholes, restrictions, and other influencing factors.

Market Segmentation Analysis

By Type:

Traditional human insulin

Analogue insulin

By Diabetes Type:

Type 1

Type 2

By Distribution Channel:

Hospital Pharmacy

Online pharmacy

Retails

COVID-19 Pandemic Impact Analysis

The COVID-19 pandemic and post-pandemic phase industry development trends, downstream consumer surveys, marketing channels, key distributors, significant customers, suppliers of necessary production equipment and raw materials, as well as downstream consumer surveys, marketing channels, and industry development trends are all examined in the Human Insulin Market research.

Regional Outlook

The market predictions and estimations consider how the market environment, as well as the political, social, and economic issues of the day, may affect different regions of the target market. Based on primary interviews, in-depth secondary research, and the opinions of internal subject matter experts, the research report's estimations and forecasts for the Human Insulin Market .

Competitive Analysis

Current market trends like market expansion, mergers and acquisitions, and partnerships and collaborations are also taken into account in the Human Insulin Market analysis. Additionally provided during the market research are a thorough financial analysis, corporate strategy, SWOT analysis, a business overview, and details on recently announced goods and services.

Key Reasons to Purchase Human Insulin Market Report

A thorough analysis of the key regional markets, along with predictions for their future development with respect to the target market.

An in-depth market research report that includes present market trends and forecasts for the future to assist you in making an informed decision.

Key market insights that enables business owners to take advantage of opportunities across many geographies.

Conclusion

The Human Insulin Market research report offers guidance for creating strategies to overcome obstacles and take advantage of growth opportunities in the global market for both existing businesses and new ventures.

About Us

SNS Insider is a market research and insights firm that has won several awards and earned a solid reputation for service and strategy. We are a strategic partner who can assist you in reframing issues and generating answers to the trickiest business difficulties. For greater consumer insight and client experiences, we leverage the power of experience and people.

When you employ our services, you will collaborate with qualified and experienced staff. We believe it is crucial to collaborate with our clients to ensure that each project is customized to meet their demands. Nobody knows your customers or community better than you do. Therefore, our team needs to ask the correct questions that appeal to your audience in order to collect the best information.

Related Reports

MicroRNA Market Trends

Neuroendoscopy Market Trends

DNA Synthesis Market Trends

Ophthalmology PACS Market Trends

Analgesics Market Trends

0 notes

Text

India Prefilled Syringes Market size by value at USD 1.13 billion in 2023. During the forecast period between 2024 and 2030, BlueWeave expects India Prefilled Syringes Market size to expand at a CAGR of 6.89% reaching a value of USD 3.17 billion by 2030. Prefilled Syringes Market in India is propelled by an increasing demand for efficient drug delivery, efforts to reduce hospital errors, and expanding home healthcare services. Growing prevalence of chronic diseases and injectable medication use also fuel market growth.

By volume, BlueWeave estimated India Prefilled Syringes Marketsize at 0.85 billion doses in 2023. During the forecast period between 2024 and 2030, BlueWeave expects India Prefilled Syringes Marketsize by volume is projected to grow at a CAGR of 6.44% reaching the volume of 1.12 billion doses by 2030. Prefilled syringes are preferred over vials, as they offer convenience and reduced contamination risks. Technological advances in syringe design further boost adoption. Challenges like regulatory hurdles and product recalls are countered by opportunities in biologics, biosimilars, and expanding prefilled medication demands. Despite obstacles, the market is poised for robust growth, driven by innovation and evolving healthcare needs in India.

Impact of Escalating Geopolitical Tensions on India Prefilled Syringes Market

Escalating geopolitical tensions among countries across regions could have a significant impact on the growth of India Prefilled Syringes Market. Dependency on foreign suppliers for key raw materials and components may lead to supply shortages or delays, affecting production schedules and market availability. Moreover, heightened geopolitical risks can destabilize economic conditions, leading to currency fluctuations and inflationary pressures, thereby impacting pricing strategies and affordability of prefilled syringes. Companies may need to reassess their sourcing strategies and enhance domestic production capabilities to mitigate geopolitical risks and ensure continuity in supplying essential healthcare products to the Indian market.

Sample Request @ https://www.blueweaveconsulting.com/report/india-prefilled-syringes-market/report-sample

0 notes

Text

Top 5 players in US Biosimilar Market

Buy Now

STORY OUTLINE

Pfizer: Excelling in the line of Biosimilar drugs with an experience of more than 10 years with presence in over 180 countries.

Amgen: Making pharmaceutical products with an experience of over 40 years and presence in over 100 countries.

Viartis: Presence in over 165 countries, and making Biosimilar drugs in over 75 markets, this pharmaceutical company is another leading contributor of US Biosimilar market.

Coherus Biosciences: Increasing patient access to cost effective medicines with a Biosimilar drugs experience of 13 years.

Biogen: serving humanity through science with a experiences of more than 40 years in the field of biologics.

According to Ken Research, the US Biosimilar market is anticipated to grow at a CAGR of ~40% in the next five years which currently has a market size of ~USD 9.4 Bn.

The US Biosimilar market is rapidly growing and will be witnessing a significant growth in the next five years.

There are various reasons behind the rapid growth of US Biosimilar market. Some of the major reasons behind the growth of US Biosimilar market include the cost effective nature of Biosimilar drugs, rising geriatric population, rising prevalence of chronic diseases, and growing partnerships between companies to develop Biosimilar drugs.

Various companies and players are contributing to their best efforts in the growth of the US Biosimilar market.

This article aims to put light on the contributions done by the major players towards the growth of the US Biosimilar market.

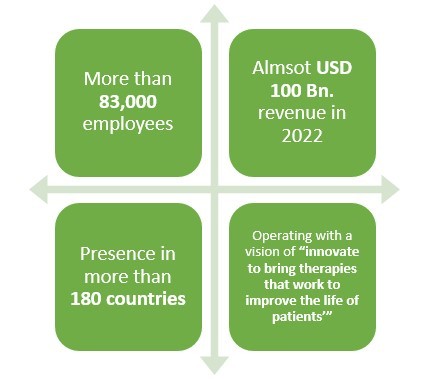

1.Pfizer

Click to read more about Pfizer

Pfizer is a leading American pharmaceutical company which is operating in the field of generics or original drugs for more than 30 years. But did you know that this pharma not only manufactures biologics but also biosimilar drugs?

Pfizer has been in the business of biosimilar drugs for more than 10 years and have been quite successful as well. With more than 83,000 employees and presence in over 180 countries, this leading pharmaceutical company made almost USD 2 Bn. revenue only from its Biosimilar drugs sale in 2021.

Recently, this pharmaceutical company also collaborated with Samsung in two deals to produce various biosimilar drugs in South Korea. The deal size between these two companies happens to be approximately USD 900 Bn.

The major Biosimilar drugs of this pharmaceutical giant are primarily

ZIRABEV (a Biosimilar of Avastin)

TRAZIMERA (a Biosimilar of Herceptin)

RUXIENCE (a Biosimilar of Rituxan)

RITACRIT (a Biosimilar of Epogen)

NVYEPRIA (a Biosimilar of Neulasta)

NIVESTYM (a Biosimilar of Neupogen)

FILGRASTIM (a Biosimilar of Neupogen).

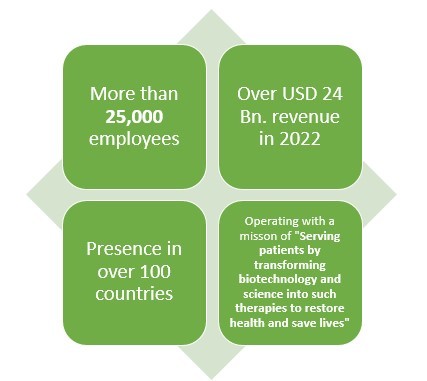

2.Amgen

Click here to Download a Sample Report

Amgen is another leading American pharmaceutical company which not only makes Biologics or generic drugs but also Biosimilar drugs. This pharmaceutical company has more than 40 years of experience when it comes to pharmaceutical line.

With over 25000 employees and presence in over 100 countries, this pharmaceutical company earned about USD 2 Bn. from their three biosimilar drugs which are reportedly MVASI, KANJITNTI, and AMJEVITA.

This pharma giant has also invested about USD 2 Bn. in the development of Biosimilar drugs.

This pharmaceutical company has made Biosimilar drugs primarily in 4 fields which are General Medicine, Oncology, and Hematology along with, Inflammation.

EPOTEIN ALFA

AMJEVITA

AVSOLA

KANJINTI

MVASI

RIABNI

are the various Biosimilar drugs of Amgen. And, STELARA, EYLEA, SOLIRIS are in their pipeline.

Recently Amgen revealed their Biosimilar report’s 8 version. It revealed a major information which said that the pharmaceutical company saved about USD 10 Bn. through their Biosimilar drugs in the past five years.

3.Viartis

Headquartered in Canonsburg, Pennsylvania, this American pharmaceutical company was founded only in 2020 yet they have achieved massive success in the pharmaceutical products with their revenue being USD 16 ~Bn. in 2022.

With presence in 165 countries and with over 45,000 employees worldwide, this pharmaceutical company makes pharmaceutical products in 10 areas which primarily are Cardiovascular, Dermatology, ophthalmology, Oncology, Gastroenterology, Women’s health, Infectious diseases, Diabetes & Metabolism, Immunology, CNS & Anesthesiology, Respiratory diseases and allergy.

Speaking of their first Biosimilar products, their first ever Biosimilar drug was launched in 2014. They have a variety of Biosimilar drugs which are primarily

TRASTUZUMAB

INSULIN ASPART

PEGFILGRASTIM

INSULIN GLARGINE-YFGN

ADALIMUMAB

BEVACIZUMAB

Their Biosimilar drug Insulin Glargine which is known as SEMGLEE was the first ever interchangeable Biosimilar drug in the United States which was FDA approved.

Their PEGFILGRASTIM also was the first ever FDA approved drug in the United States. They have launched their Biosimilar drugs in over 75 markets worldwide.

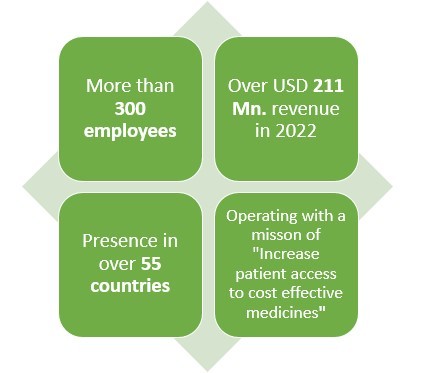

4.Coherus Biosciences:

Click here to Ask for a Custom Report

Headquartered in Redwood city, California this American pharmaceutical company earned a revenue of almost USD 211 Mn. In 2022.

With presence in over 55 countries and 300+ employees worldwide, this pharmaceutical company makes products in various areas such as solid tumors, non-small lung cancers, nasopharyngeal carcinoma, small cell lung cancer and hepatocellular carcinoma.

Speaking of their Biosimilar drugs, this pharma has been in the field of creating Biosimilar drugs since 2010 which has given them almost 13 years of experience.

This pharmaceutical company also disclosed that it plans to spend at least USD 1 Tn. on medicines worldwide, out of which at least 40% will be spent on Biosimilar drugs.

Their three major Biosimilar drugs which are also FDA approved include UDENCYA, YUSIMRY, and CIMERLI.

Udencya is a Biosimilar drug of Pegfilgrastim, Yusimry is a Biosimilar drug of Ranibizumab, and Cimerli is a Biosimilar drug of Adalimumab.

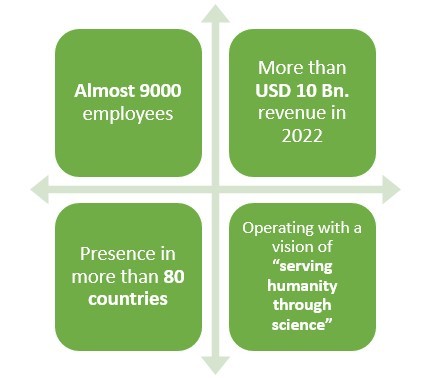

5.Biogen

Headquartered in Cambridge, Massachusetts, this American pharmaceutical company earned a revenue of around USD 10 Bn. in 2022.

This company happens to have an experience of more than 40 years when it comes to making pharmaceutical products.

With presence in over 80 countries and more than 9000 employees worldwide, this pharmaceutical company primarily deals in Neurology, Specialized Immunology, Neuropsychiatry, Ophthalmology, and Rare Diseases.

ADUCANUMAB

LECANEMAB

TOFERSEN

ZURANOLONE

LITIFILIMAB

BENAPALI

FLIXABI

IMRALDI

are some of their Biosimilar drugs.

With their Biosimilar drugs, more than 250,000 people have gone on Anti-Tumor Necrosis Factor therapy.

Recently, this pharmaceutical company also made an agreement with Bio-Thera solutions to develop a Biosimilar drug for the treatment of Rheumatoid Arthritis.

#US Biosimilar Sector#United States Biosimilar Market#US Biosimilar Market forecast#US Biosimilar Market analysis#US Biosimilar Market trends#US Biosimilar Market share#US Biosimilar Market key players#US Biosimilar Market revenue#US Biosimilar Market growth#Monoclonal Antibodies in biosimilar market US#Recombinant Hormones in biosimilar industry US#Oncology in bio similar market US#Blood disorders in biosimilar market US#Research institutes in Biosimilar market US#US similar biotherapeutics products market#Hospitals in Biosimilar market US#Investors in Biosimilar market US#US comparable biologics products industry#US recombinant biosimilars industry#US replicate biologics sector#US analog biologics market

0 notes

Text

Generic Sterile Injectables Market to witness highest growth owing to increasing prevalence of chronic diseases

Generic sterile injectables are medications that are administered intravenously or through injections for treatment of chronic and critical illnesses. The global sterile injectables market is estimated to be valued at US$ 38,706.5 Mn in 2024 and is expected to exhibit a CAGR of 10% over the forecast period 2023 to 2030.

Generic sterile injectables are essential for treatment of various critical illnesses including cancer, infectious diseases, cardiovascular diseases and others. Rising burden of chronic diseases worldwide has fueled the demand for cost-effective generic sterile injectables. Moreover, growing geriatric population which is more prone to chronic illnesses is a key driver of the market. Generic sterile injectables offer similar therapeutic efficacy as compared to their branded counterparts at significantly lower costs. This has increased their adoption in developing nations with large patient pools and budget constraints.

Key Takeaways

Key players operating in the generic sterile injectables market are Baxter International Inc., AstraZeneca plc, Merck & Co., Inc., Pfizer Inc., Fresenius Kabi, Novartis International AG, Teva Pharmaceuticals, Hikma Pharmaceuticals, Dr. Reddy’s Laboratory, Mylan N.V., Sun Pharmaceutical Industries Ltd.

Growing prevalence of chronic diseases worldwide has increased the demand for generic sterile injectables for treatment of cancer, cardiovascular diseases, infectious diseases and other critical ailments. According to WHO, cardiovascular diseases are the leading cause of deaths globally and accounted for over 17 million deaths in 2015.

Technological advancements in sterile injectables production such as automated vial and syringe filling equipment has improved yields and sterility, facilitating large scale production of affordable generic injectables.

Market Trends

Increasing consolidation in the industry: Major players are pursuing inorganic growth strategies such as acquisitions and partnerships to strengthen their injectable drug portfolio and manufacturing capabilities. For instance, in 2021, Baxter acquired pharmaceutical company Hillrom for $10.5 billion.

Rise of biosimilars: Biosimilar versions of high-profit biologics are gaining approval and commercialization providing opportunities for generics players. Biosimilars offer significant cost savings compared to reference biologics.

Market Opportunities

Emerging markets in Asia Pacific and Latin America provide immense opportunities owing to growing healthcare spending and large patient population. Favorable regulations in some countries encouraging local manufacturing of generics augur well for the market.

Shortage of essential sterile injectables globally during COVID-19 pandemic has highlighted the need for boosting local manufacturing capabilities especially in developing countries. This presents opportunities for investment and collaboration between global players and local manufacturers.

Impact of COVID-19 on Generic Sterile Injectables Market

The COVID-19 pandemic has adversely impacted the growth of generic sterile injectables market. During the initial months of the pandemic in 2020, elective surgeries and non-emergency hospital visits reduced significantly which led to a decline in overall demand for generic sterile injectables. However, as the pandemic intensified, demand spiked significantly for certain therapies used in treatment of hospitalized COVID-19 patients such as antibiotics, analgesics and sedatives which provided some relief to the market.

#Generic Sterile Injectables Market Growth#Generic Sterile Injectables Market Demand#Generic Sterile Injectables Market Analysis.

0 notes

Text

Colony-Stimulating Factor Therapy Market

The Colony-Stimulating Factor (CSF) Therapy Market has seen significant growth and transformation in recent years, driven by advancements in biotechnology, an increasing prevalence of cancer, and rising demand for targeted therapies. Colony-Stimulating Factors are crucial in the treatment of various hematologic conditions as they stimulate the bone marrow to produce white blood cells, which are essential in fighting infections, especially in immunocompromised patients, such as those undergoing chemotherapy.

Request To Download Sample of This Strategic Report - https://univdatos.com/report/colony-stimulating-factor-therapy-market/get-a-free-sample-form.php?product_id=58550

Market Overview

The global CSF therapy market is poised for robust growth, with a projected compound annual growth rate (CAGR) of 6.5% from 2023 to 2030. This growth is attributed to the increasing incidence of cancer and other conditions that necessitate chemotherapy, which in turn leads to a higher demand for CSF therapies to mitigate the side effects associated with cancer treatments.

Key Drivers

Rising Cancer Prevalence: With cancer cases on the rise globally, the demand for effective treatment protocols, including supportive care like CSF therapy, has surged. Chemotherapy-induced neutropenia is a common side effect that necessitates CSF therapy to prevent infections and maintain treatment schedules.

Technological Advancements: Innovations in biotechnology have led to the development of more effective and targeted CSF therapies. These advancements include pegylated formulations, which offer longer half-life and reduced dosing frequency, improving patient compliance and outcomes.

Aging Population: The increasing elderly population is more susceptible to cancer and other chronic diseases, thereby driving the demand for supportive therapies like CSF.

Government Initiatives and Funding: Increased government funding and initiatives aimed at improving cancer care infrastructure have significantly bolstered the CSF therapy market. Programs to enhance healthcare access and affordability further support market growth.

Market Segmentation

The CSF therapy market can be segmented based on product type, application, distribution channel, and region.

By Product Type: The market is divided into granulocyte colony-stimulating factor (G-CSF), granulocyte-macrophage colony-stimulating factor (GM-CSF), and others. G-CSF dominates the market due to its widespread use in treating neutropenia.

By Application: The primary applications include oncology, hematology, and others. Oncology is the leading segment, driven by the high incidence of cancer and the necessity for supportive treatments.

By Distribution Channel: The market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. Hospital pharmacies hold the largest share due to the administration of CSF therapies in clinical settings.

By Region: North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa are key regions. North America leads the market owing to advanced healthcare infrastructure and high cancer prevalence.

𝐓𝐨 𝐆𝐞𝐭 𝐈𝐧𝐬𝐢𝐠𝐡𝐭𝐟𝐮𝐥 𝐑𝐞𝐬𝐞𝐚𝐫𝐜𝐡, 𝐑𝐞𝐪𝐮𝐞𝐬𝐭 𝐏𝐃𝐅 𝐂𝐨𝐩𝐲 - https://univdatos.com/report/colony-stimulating-factor-therapy-market/get-a-free-sample-form.php?product_id=58550

Recent Developments

FDA Approvals and Expansions: In recent years, there have been several FDA approvals for new CSF formulations. For instance, in 2023, the FDA approved a new biosimilar for pegfilgrastim, which is expected to provide a cost-effective alternative to existing therapies.

Strategic Collaborations and Acquisitions: Companies are increasingly entering into partnerships and acquisitions to expand their CSF therapy portfolios. In 2022, Amgen acquired Five Prime Therapeutics, enhancing its oncology and immunotherapy pipeline, which includes CSF therapies.

Research and Development: Significant investments in R&D are leading to the development of novel CSF therapies. Ongoing clinical trials are exploring new indications and more efficient formulations, such as oral CSF therapies that could revolutionize the market.

Biosimilars Market Expansion: The introduction and acceptance of biosimilars are transforming the CSF therapy landscape. Biosimilars provide more affordable treatment options, increasing accessibility and driving market growth.

Challenges

Despite the positive outlook, the CSF therapy market faces several challenges. High treatment costs, stringent regulatory requirements, and the potential for adverse effects limit market growth. Additionally, the competitive landscape, with numerous companies vying for market share, necessitates continuous innovation and cost management.

Future Prospects

The future of the CSF therapy market looks promising, with ongoing research and technological advancements paving the way for more effective and accessible treatments. Personalized medicine, where treatments are tailored to individual patient profiles, is an emerging trend that could significantly impact the market. Additionally, increasing awareness about the importance of supportive care in cancer treatment will continue to drive demand for CSF therapies.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐢𝐜 𝐒𝐚𝐦𝐩𝐥𝐞 𝐏𝐃𝐅 𝐇𝐞𝐫𝐞 - https://univdatos.com/report/colony-stimulating-factor-therapy-market/get-a-free-sample-form.php?product_id=58550

Conclusion

The Colony-Stimulating Factor Therapy Market is on a growth trajectory, propelled by rising cancer incidence, technological advancements, and strategic industry initiatives. While challenges persist, ongoing innovations and increasing demand for effective supportive therapies promise a dynamic and evolving market landscape. Stakeholders, including healthcare providers, patients, and investors, can expect continued advancements and opportunities in this crucial segment of cancer care.

#healthcare#market analysis#market insights#market report#market research#market trends#univdatos#health#Colony-Stimulating Factor Therapy Market

0 notes

Text

Aflibercept Biosimilars, Global Market Size Forecast, Top 4 Players Rank and Market Share

Aflibercept Biosimilars Market Summary

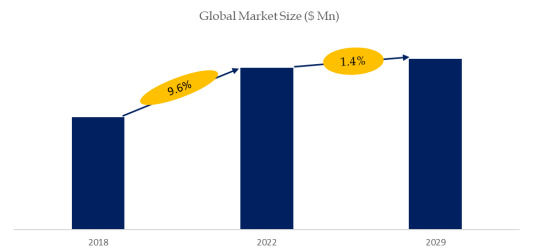

According to the new market research report “Global Aflibercept Biosimilars Market Report 2023-2029”, published by QYResearch, the global Aflibercept Biosimilars market size is projected to reach USD 10.4 billion by 2029, at a CAGR of 1.4% during the forecast period.

Figure. Global Aflibercept Biosimilars Market Size (US$ Million), 2018-2029

Above data is based on report from QYResearch: Global Aflibercept Biosimilars Market Report 2023-2029 (published in 2023). If you need the latest data, plaese contact QYResearch.

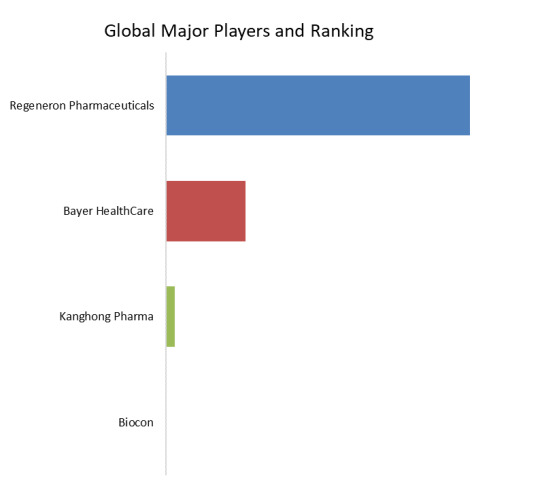

Figure. Global Aflibercept Biosimilars Top 4 Players Ranking and Market Share (Ranking is based on the revenue of 2022, continually updated)

Above data is based on report from QYResearch: Global Aflibercept Biosimilars Market Report 2023-2029 (published in 2023). If you need the latest data, plaese contact QYResearch.

According to QYResearch Top Players Research Center, the global key manufacturers of Aflibercept Biosimilars include Regeneron Pharmaceuticals, Bayer HealthCare, etc. In 2022, the global top three players had a share approximately 100.0% in terms of revenue.

Figure. Aflibercept Biosimilars, Global Market Size, Split by Product Segment

Based on or includes research from QYResearch: Global Aflibercept Biosimilars Market Report 2023-2029.

In terms of product type, currently 2mg is the largest segment, hold a share of 100.0%.

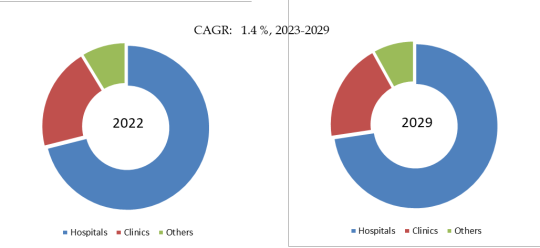

Figure. Aflibercept Biosimilars, Global Market Size, Split by Application Segment

Based on or includes research from QYResearch: Global Aflibercept Biosimilars Market Report 2023-2029.

In terms of product application, currently Hospitals is the largest segment, hold a share of 71.1%.

Figure. Aflibercept Biosimilars, Global Market Size, Split by Region

Based on or includes research from QYResearch: Global Aflibercept Biosimilars Market Report 2023-2029.

Market Drivers:

Clinical Innovation and Advancements: Ongoing research and development, as well as innovations in the formulation or delivery of Eylea, can drive market growth. Advancements that improve treatment outcomes, reduce dosing frequency, or enhance patient convenience may positively impact the market;

Increase In the Number of Sick People: The prevalence of eye conditions such as AMD and DME, coupled with an aging population, contributes to the demand for effective treatments. Global demographic trends and an increasing burden of eye diseases can drive the market for Eylea;

Expanded Indications: Obtaining additional approvals for new indications can significantly expand the market for Eylea. As clinical trials demonstrate the drug's effectiveness in treating different eye conditions, regulatory approvals for these new indications can drive increased usage.

Restraint:

Patent restrictions become an important factor in entering the market;

The leading enterprises have a high degree of concentration, complete products and great competitive advantages;

Economic downturns and budget constraints within healthcare systems may impact the affordability and reimbursement of Eylea. Changes in economic conditions can influence the overall market for pharmaceuticals.

Opportunity:

Advancements in medical technology: Ongoing advancements in medical technology are expected to broaden the application of biosimilars in the treatment of cancer and eye diseases;

Increased treatment options for patients: The entry of Aflibercept biosimilars into the market will provide patients with more treatment options and the potential to reduce medical costs, presenting growth opportunities for the market.

About QYResearch

QYResearch founded in California, USA in 2007.It is a leading global market research and consulting company. With over 16 years’ experience and professional research team in various cities over the world QY Research focuses on management consulting, database and seminar services, IPO consulting, industry chain research and customized research to help our clients in providing non-linear revenue model and make them successful. We are globally recognized for our expansive portfolio of services, good corporate citizenship, and our strong commitment to sustainability. Up to now, we have cooperated with more than 60,000 clients across five continents. Let’s work closely with you and build a bold and better future.

QYResearch is a world-renowned large-scale consulting company. The industry covers various high-tech industry chain market segments, spanning the semiconductor industry chain (semiconductor equipment and parts, semiconductor materials, ICs, Foundry, packaging and testing, discrete devices, sensors, optoelectronic devices), photovoltaic industry chain (equipment, cells, modules, auxiliary material brackets, inverters, power station terminals), new energy automobile industry chain (batteries and materials, auto parts, batteries, motors, electronic control, automotive semiconductors, etc.), communication industry chain (communication system equipment, terminal equipment, electronic components, RF front-end, optical modules, 4G/5G/6G, broadband, IoT, digital economy, AI), advanced materials industry Chain (metal materials, polymer materials, ceramic materials, nano materials, etc.), machinery manufacturing industry chain (CNC machine tools, construction machinery, electrical machinery, 3C automation, industrial robots, lasers, industrial control, drones), food, beverages and pharmaceuticals, medical equipment, agriculture, etc.

0 notes

Text

Global Ophthalmic Microscope Market Analysis 2024 – Estimated Market Size And Key Drivers

The Ophthalmic Microscope Global Market Report 2024 by The Business Research Company provides market overview across 60+ geographies in the seven regions - Asia-Pacific, Western Europe, Eastern Europe, North America, South America, the Middle East, and Africa, encompassing 27 major global industries. The report presents a comprehensive analysis over a ten-year historic period (2010-2021) and extends its insights into a ten-year forecast period (2023-2033).

Learn More On The Ophthalmic Microscope Market:

https://www.thebusinessresearchcompany.com/report/ophthalmic-microscope-global-market-report

According to The Business Research Company’s Ophthalmic Microscope Global Market Report 2024, The ophthalmic microscope market size has grown strongly in recent years. It will grow from $1.39 billion in 2023 to $1.53 billion in 2024 at a compound annual growth rate (CAGR) of 10.0%.