#we buy private mortgages

Text

Leveraged buyouts are not like mortgages

I'm coming to DEFCON! On FRIDAY (Aug 9), I'm emceeing the EFF POKER TOURNAMENT (noon at the Horseshoe Poker Room), and appearing on the BRICKED AND ABANDONED panel (5PM, LVCC - L1 - HW1–11–01). On SATURDAY (Aug 10), I'm giving a keynote called "DISENSHITTIFY OR DIE! How hackers can seize the means of computation and build a new, good internet that is hardened against our asshole bosses' insatiable horniness for enshittification" (noon, LVCC - L1 - HW1–11–01).

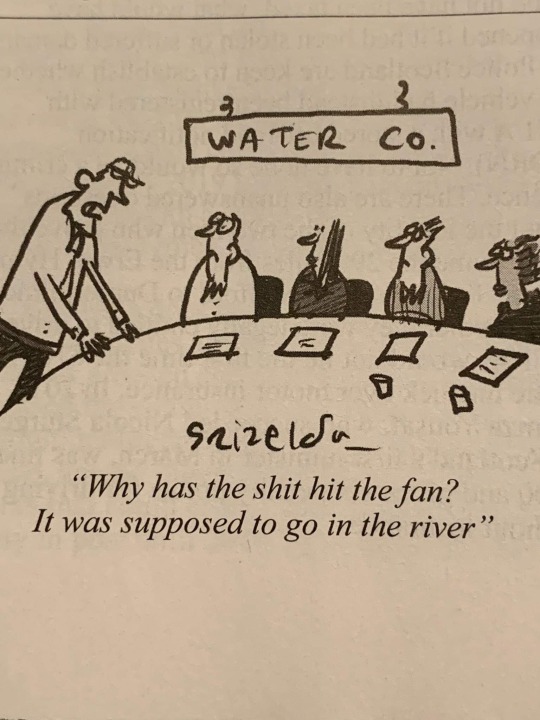

Here's an open secret: the confusing jargon of finance is not the product of some inherent complexity that requires a whole new vocabulary. Rather, finance-talk is all obfuscation, because if we called finance tactics by their plain-language names, it would be obvious that the sector exists to defraud the public and loot the real economy.

Take "leveraged buyout," a polite name for stealing a whole goddamned company:

Identify a company that owns valuable assets that are required for its continued operation, such as the real-estate occupied by its outlets, or even its lines of credit with suppliers;

Approach lenders (usually banks) and ask for money to buy the company, offering the company itself (which you don't own!) as collateral on the loan;

Offer some of those loaned funds to shareholders of the company and convince a key block of those shareholders (for example, executives with large stock grants, or speculators who've acquired large positions in the company, or people who've inherited shares from early investors but are disengaged from the operation of the firm) to demand that the company be sold to the looters;

Call a vote on selling the company at the promised price, counting on the fact that many investors will not participate in that vote (for example, the big index funds like Vanguard almost never vote on motions like this), which means that a minority of shareholders can force the sale;

Once you own the company, start to strip-mine its assets: sell its real-estate, start stiffing suppliers, fire masses of workers, all in the name of "repaying the debts" that you took on to buy the company.

This process has its own euphemistic jargon, for example, "rightsizing" for layoffs, or "introducing efficiencies" for stiffing suppliers or selling key assets and leasing them back. The looters – usually organized as private equity funds or hedge funds – will extract all the liquid capital – and give it to themselves as a "special dividend." Increasingly, there's also a "divi recap," which is a euphemism for borrowing even more money backed by the company's assets and then handing it to the private equity fund:

https://pluralistic.net/2020/09/17/divi-recaps/#graebers-ghost

If you're a Sopranos fan, this will all sound familiar, because when the (comparatively honest) mafia does this to a business, it's called a "bust-out":

https://en.wikipedia.org/wiki/Bust_Out

The mafia destroys businesses on a onesy-twosey, retail scale; but private equity and hedge funds do their plunder wholesale.

It's how they killed Red Lobster:

https://pluralistic.net/2024/05/23/spineless/#invertebrates

And it's what they did to hospitals:

https://pluralistic.net/2024/02/28/5000-bats/#charnel-house

It's what happened to nursing homes, Armark, private prisons, funeral homes, pet groomers, nursing homes, Toys R Us, The Olive Garden and Pet Smart:

https://pluralistic.net/2023/06/02/plunderers/#farben

It's what happened to the housing co-ops of Cooper Village, Texas energy giant TXU, Old Country Buffet, Harrah's and Caesar's:

https://pluralistic.net/2021/05/14/billionaire-class-solidarity/#club-deals

And it's what's slated to happen to 2.9m Boomer-owned US businesses employing 32m people, whose owners are nearing retirement:

https://pluralistic.net/2022/12/16/schumpeterian-terrorism/#deliberately-broken

Now, you can't demolish that much of the US productive economy without attracting some negative attention, so the looter spin-machine has perfected some talking points to hand-wave away the criticism that borrowing money using something you don't own as collateral in order to buy it and wreck it is obviously a dishonest (and potentially criminal) destructive practice.

The most common one is that borrowing money against an asset you don't own is just like getting a mortgage. This is such a badly flawed analogy that it is really a testament to the efficacy of the baffle-em-with-bullshit gambit to convince us all that we're too stupid to understand how finance works.

Sure: if I put an offer on your house, I will go to my credit union and ask the for a mortgage that uses your house as collateral. But the difference here is that you own your house, and the only way I can buy it – the only way I can actually get that mortgage – is if you agree to sell it to me.

Owner-occupied homes typically have uncomplicated ownership structures. Typically, they're owned by an individual or a couple. Sometimes they're the property of an estate that's divided up among multiple heirs, whose relationship is mediated by a will and a probate court. Title can be contested through a divorce, where disputes are settled by a divorce court. At the outer edge of complexity, you get things like polycules or lifelong roommates who've formed an LLC s they can own a house among several parties, but the LLC will have bylaws, and typically all those co-owners will be fully engaged in any sale process.

Leveraged buyouts don't target companies with simple ownership structures. They depend on firms whose equity is split among many parties, some of whom will be utterly disengaged from the firm's daily operations – say, the kids of an early employee who got a big stock grant but left before the company grew up. The looter needs to convince a few of these "owners" to force a vote on the acquisition, and then rely on the idea that many of the other shareholders will simply abstain from a vote. Asset managers are ubiquitous absentee owners who own large stakes in literally every major firm in the economy. The big funds – Vanguard, Blackrock, State Street – "buy the whole market" (a big share in every top-capitalized firm on a given stock exchange) and then seek to deliver returns equal to the overall performance of the market. If the market goes up by 5%, the index funds need to grow by 5%. If the market goes down by 5%, then so do those funds. The managers of those funds are trying to match the performance of the market, not improve on it (by voting on corporate governance decisions, say), or to beat it (by only buying stocks of companies they judge to be good bets):

https://pluralistic.net/2022/03/17/shareholder-socialism/#asset-manager-capitalism

Your family home is nothing like one of these companies. It doesn't have a bunch of minority shareholders who can force a vote, or a large block of disengaged "owners" who won't show up when that vote is called. There isn't a class of senior managers – Chief Kitchen Officer! – who have been granted large blocks of options that let them have a say in whether you will become homeless.

Now, there are homes that fit this description, and they're a fucking disaster. These are the "heirs property" homes, generally owned by the Black descendants of enslaved people who were given the proverbial 40 acres and a mule. Many prosperous majority Black settlements in the American South are composed of these kinds of lots.

Given the historical context – illiterate ex-slaves getting property as reparations or as reward for fighting with the Union Army – the titles for these lands are often muddy, with informal transfers from parents to kids sorted out with handshakes and not memorialized by hiring lawyers to update the deeds. This has created an irresistible opportunity for a certain kind of scammer, who will pull the deeds, hire genealogists to map the family trees of the original owners, and locate distant descendants with homeopathically small claims on the property. These descendants don't even know they own these claims, don't even know about these ancestors, and when they're offered a few thousand bucks for their claim, they naturally take it.

Now, armed with a claim on the property, the heirs property scammers force an auction of it, keeping the process under wraps until the last instant. If they're really lucky, they're the only bidder and they can buy the entire property for pennies on the dollar and then evict the family that has lived on it since Reconstruction. Sometimes, the family will get wind of the scam and show up to bid against the scammer, but the scammer has deep capital reserves and can easily win the auction, with the same result:

https://www.propublica.org/series/dispossessed

A similar outrage has been playing out for years in Hawai'i, where indigenous familial claims on ancestral lands have been diffused through descendants who don't even know they're co-owner of a place where their distant cousins have lived since pre-colonial times. These descendants are offered small sums to part with their stakes, which allows the speculator to force a sale and kick the indigenous Hawai'ians off their family lands so they can be turned into condos or hotels. Mark Zuckerberg used this "quiet title and partition" scam to dispossess hundreds of Hawai'ian families:

https://archive.is/g1YZ4

Heirs property and quiet title and partition are a much better analogy to a leveraged buyout than a mortgage is, because they're ways of stealing something valuable from people who depend on it and maintain it, and smashing it and selling it off.

Strip away all the jargon, and private equity is just another scam, albeit one with pretensions to respectability. Its practitioners are ripoff artists. You know the notorious "carried interest loophole" that politicians periodically discover and decry? "Carried interest" has nothing to do with the interest on a loan. The "carried interest" rule dates back to 16th century sea-captains, and it refers to the "interest" they had in the cargo they "carried":

https://pluralistic.net/2021/04/29/writers-must-be-paid/#carried-interest

Private equity managers are like sea captains in exactly the same way that leveraged buyouts are like mortgages: not at all.

And it's not like private equity is good to its investors: scams like "continuation funds" allow PE looters to steal all the money they made from strip mining valuable companies, so they show no profits on paper when it comes time to pay their investors:

https://pluralistic.net/2023/07/20/continuation-fraud/#buyout-groups

Those investors are just as bamboozled as we are, which is why they keep giving more money to PE funds. Today, the "dry powder" (uninvested money) that PE holds has reached an all-time record high of $2.62 trillion – money from pension funds and rich people and sovereign wealth funds, stockpiled in anticipation of buying and destroying even more profitable, productive, useful businesses:

https://www.institutionalinvestor.com/article/2di1vzgjcmzovkcea8f0g/portfolio/private-equitys-dry-powder-mountain-reaches-record-height

The practices of PE are crooked as hell, and it's only the fact that they use euphemisms and deceptive analogies to home mortgages that keeps them from being shut down. The more we strip away the bullshit, the faster we'll be able to kill this cancer, and the more of the real economy we'll be able to preserve.

If you'd like an essay-formatted version of this post to read or share, here's a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2024/08/05/rugged-individuals/#misleading-by-analogy

#pluralistic#leveraged buyouts#lbos#divi recaps#mortgages#weaponized shelter#debt#finance#private equity#pe#mego#bust outs#plunder#looting

421 notes

·

View notes

Text

Is Blanche Devereaux a Landlord?

Random thought of the day: Is Blanche Devereaux of the Golden Girls a Landlord? And if she is, does she deserve the guillotine?

Obviously, in the strictest sense, she is a landlord. She owns accomodation, and she derives income from renting that accomodation out. That's a landlord.

But in saying that, Blanche lives in that same house - she rents it out to the other women because she has space and she's a widow with no dependents anymore. She had a large house to raise children and live with her husband, but her children have moved out and her husband's moved on (to the afterlife).

The absolutely moral thing to do would be to either let her roommates stay with her for free (because housing is a human right) OR to downsize.

And it's easy to say that's what she should do, but the absolutely moral thing for most of us to do is to sell most of our belongings and give the proceeds to charity but that's the kind of behaviour you'd expect from a saint, not some random person. I think we generally agree that there's a gradient between the extreme ends here.

And although it's kind of a meme, landlords do provide a service - as someone who has owned their own home with a mortgage, owning a home can be annoying and stressful. Owning your own home makes you feel like you put down an anchor, and when you want to move, you end up asking yourself if it's worth raising that anchor. For some people, it's better to have the freedom and flexibility that renting can provide.

(Also technically you don't have the stress of wondering how you're going to pay for repairs because that's the landlord's responsibility, but you know, that also puts you at the mercy of the landlord.)

In some ways, I think there wouldn't necessarily be anything wrong with having landlords if those landlords weren't private investors whose desire is profit - if the government owned my house, and I just 'rented' it from them by paying taxes, and then I would be able to move at some point if I chose, that'd be a neat solution.

(But then it also raises all sorts of questions such as: should I, a single bachelor with no dependents, be allowed to have a house with more than one bedroom? Under the capitalist system, I could have as big a house as my pockets could afford, even if that is a terrible allocation of space and housing.)

Looping back to Blanche, neither Rose nor Dorothy seem like they might've been in a position to buy a house - Rose sold her previous home, so maybe she would have the funds, but she was also moving from a small town to Miami, so the houses would probably cost a lot more (but she could probably afford a condo or small apartment). There's also the fact that living in a shared accomodation with each other was almost definitely good for them, socially wise.

I know living on my own was kind of sad in some ways, even if it did mean I didn't have to wear clothes in the summer.

So is Blanche bourgeouise? I mean... probably, but if the Revolution came, would she be up against the wall?

#penkind rambles#long post#dumb thoughts i'm having whilst applying for new jobs#i personally think she's a landlord but shouldn't be launched into space#i think we are forced into participating in a capitalist system and trying to be comfortable in that system isn't necessarily evil#like if you study hard and work hard and become a doctor or a famous actor#or just an instagram influencer or whatever#and you make lots of money because of that#i think whatever#but if you do become very wealthy and then use that wealth to keep clawing after more wealth and exploiting everyone#then get into the space cannon

19 notes

·

View notes

Text

In one sense there is nothing remarkable in observing that capitalists would prefer individuals who agree to work and consume in ways that most advantage capital. We need only to consider the ravages of the subprime mortgage industry that helped trigger the great financial crisis of 2008 or the daily insults to

human autonomy at the hands of countless industries from airlines to insurance for plentiful examples of this plain fact.

However, it would be dangerous to nurse the notion that today’s surveillance capitalists simply

represent more of the same. This structural requirement of economies of action turns the means of behavioural modification into an engine of growth. At no other time in history have private corporations of unprecedented wealth and power enjoyed the free exercise of economies of action supported by a pervasive global architecture of ubiquitous computational knowledge and control constructed and

maintained by all the advanced scientific know-how that money can buy.

Most pointedly, Facebook’s declaration of experimental authority claims surveillance capitalists’ prerogatives over the future course of others’ behaviour. In declaring the right to modify human action secretly and for profit, surveillance capitalism effectively exiles us from our own behaviour, shifting the locus of control over the future tense from “I will” to “You will.” Each one of us may follow a distinct path, but economies of action ensure that the path is already shaped by surveillance capitalism’s economic imperatives. The struggle for power and control in society is no longer associated with the hidden facts of class and its relationship to production but rather by the hidden facts of automated engineered behaviour modification.

Shoshana Zuboff, The Age of Surveillance Capitalism

51 notes

·

View notes

Text

Elon Musk is so disappointing both as a target of hate and as a target of adoration because after years of anti apartheid messaging about how menacing white South Africans are from Hollywood everyone was convinced that an evil rich Saffie fucking up the economic and corporate world would be some malicious hard as fuck looking James Bond-esque villain with a private army of equally cool/evil looking goons.

Instead we got a doughy spergy nepotism baby who just buys other people's companies and make them cringe and retarded until they go under because he's incompetent and closest thing the guy has to a private army is a bunch of divorced middle aged nerds obsessed with ugly online drawings that they took out a second mortgage on their house to pay for.

50 notes

·

View notes

Text

Social class of M*A*S*H surgeons

I got the idea from reading this interesting post by @majorbaby about Frank Burns.

My reference was 8.3 Social Class in the United States

Charles Emerson Winchester III is upper-class his family has money and social position. He would certainly like you to think that his family is upper-upper class all the way back, and perhaps that's even true.

"Members of the upper-upper class have “old” money that has been in their families for generations; some boast of their ancestors coming over on the Mayflower. They belong to exclusive clubs and live in exclusive neighborhoods; have their names in the Social Register; send their children to expensive private schools; serve on the boards of museums, corporations, and major charities; and exert much influence on the political process and other areas of life from behind the scenes."

B. J. Hunnicutt is upper-middle class. He went to Stanford: he was past of an exclusive fraternity, which Frank Burns comments on. He and Peg may be having cash-flow problems, but they're on the lines of "how do we pay for the second mortgage" not "how do we pay the rent".

"People in the upper-middle class typically have college and, very often, graduate or professional degrees; live in the suburbs or in fairly expensive urban areas; and are bankers, lawyers, engineers, corporate managers, and financial advisers, among other occupations."

We don't get enough clues from the six appearances of Oliver Harmon Jones what social class he was supposed to be before institutional racism cut him from the series.

Henry Blake - insufficient clues about background, but certainly comfortably upper-middle class when drafted.

Frank Burns wants to be upper class and is origins are probably lower-middle class - he wasn't allowed into the exclusive fraternity that BJ Hunnicutt joined.

"Members of the lower-upper class have “new” money acquired through hard work, lucky investments, and/or athletic prowess. In many ways their lives are similar to those of their old-money counterparts, but they do not enjoy the prestige that old money brings."

John McIntyre and Hawkeye Pierce both look like scholarship students to me - McIntyre's accent places him on the South side of Boston, and Pierce's father, though a doctor, probably acquired that training the old-fashioned way, not by eight years of medical school. I place both families as lower-middle class.

"The lower-middle class has household incomes from about $50,000 to $74,999, amounting to about 18% of all families. People in this income bracket typically work in white-collar jobs as nurses, teachers, and the like. Many have college degrees, usually from the less prestigious colleges, but many also have 2-year degrees or only a high school degree. They live somewhat comfortable lives but can hardly afford to go on expensive vacations or buy expensive cars and can send their children to expensive colleges only if they receive significant financial aid."

Sherman Potter was a farm kid. He joined the cavalry in WWI because he could ride, and though I don't know they've ever mentioned Potter's rank in WWI, I get the impression he was an enlisted man, not an officer. He went to college to train as a surgeon as a military officer. His son-in-law is a salesman. His family may have been land rich before the Great Depression, and lost that land in bank foreclosures. That would put him in working-class origins - if so, the only other officer at the 4077th who had a working-class background is Father Mulcahy, which may explain why they get on so well.

#mash analysis#class analysis#charles emerson winchester#frank burns#sherman potter#hawkeye pierce#trapper john mcintyre#oliver harmon jones#bj hunnicutt#mashposting#henry blake

63 notes

·

View notes

Text

Sorry, parents: The American dream is only for DINKS

Homebuyers with kids will likely spend 66% of their income on a mortgage and childcare this year.

Parents in Los Angeles and San Diego can expect to spend as much as 121% and 113%, respectively.

Some Californians have moved across the country to afford to buy a home.

Thinking about buying a home this year with kids already in the picture? Get ready to dig deep.

A recent study from Zillow found that potential homebuyers with children are likely to spend 66% of their income on mortgage payments and childcare expenses — an increase of nearly 50% from 2019.

The real-estate company estimated city- and state-level childcare costs from 2009 to 2022 for the typical American family with 1.94 children by analyzing data from the Women’s Bureau of the US Department of Labor and advocacy group Child Care Aware.

According to Zillow’s analysis, in 31 of the largest 50 US metropolitan areas with available childcare cost data, families looking to buy a home can expect to spend more than 60% of their income on mortgage and childcare costs.

Some areas are even costlier, with parents in cities like Los Angeles and San Diego needing to dedicate as much as 121% and 113%, respectively. (In those areas, the cost of buying a typical home and childcare is so big relative to the median income that Zillow's calculation results in figures over 100%.)

Zillow determined that a family earning a median household income of $6,640 per month can expect to allocate $1,984 of that to childcare. If the family purchased a house at a 6.61% interest rate — the rate in early January, when the US Department of Labor released its latest data on childcare costs — and made a 10% down payment, their monthly mortgage would amount to $1,973.

That leaves just $2,683 for additional expenses like food, transportation, and healthcare. This means many households with kids are financially strained; they're likely spending more than 30% of their income on housing, well above what experts recommend.

It all adds up to a costly reality that's making the American dream of homeownership seem farther out of reach for parents than ever before.

Parents can blame a yearslong battle with inflation, as well as stubbornly high home prices and mortgage rates, for contributing to their predicament.

Based on the study, a new buyer household in the United States, making the median income, would spend 30% of it on housing. It's paying for childcare, then, that adds so much on top of the housing budget.

The upshot: Another group, less encumbered financially, appears better poised to realize the dream of homeownership: "DINKS," an acronym that stands for "dual income, no kids."

Some child-free DINKS — who boast a median net worth above $200,000 according to the Federal Reserve's Survey of Consumer Finances — devote their disposable income to luxuries like boats and expensive cars.

Without the financial obligations of raising children, such as covering medical expenses or enrolling them in daycare or private school, DINKS can save thousands of dollars a year and build greater long-term wealth.

Some DINKS use their savings to finance vacations and travel the world, like Elizabeth Johnson and her husband, who, over the past couple of years, have hiked in the Swiss Alps, snorkeled in Hawaii, and enjoyed leaf peeping in Canada.

"We hang out with other people's kids every once in a while," Johnson previously told Business Insider's Bartie Scott and Juliana Kaplan, "but then we happily just give them back to their parents."

Some Americans with kids move to places where their money goes further

One solution to the high cost of both buying a home and raising a family?

Move.

In recent years, young Americans in higher-cost states have decided to move to places that offer them a cheaper cost of living.

Janelle Crossan moved to New Braunfels, Texas, from Costa Mesa, California, in 2020 following a divorce.

She was able to become a first-time homebuyer and found a safe community to raise her son.

"I paid $1,750 for rent in a crappy little apartment in California," Crossan told BI earlier this year. "Now, three years later, my whole payment, including mortgage and property taxes, is $1,800 a month for my three-bedroom house."

Pengyu Cheng, a program manager for a tech company, told BI in 2023 that moving from California to Texas allowed him and his wife to afford their first home, giving them the confidence and security to have their first child.

"Living in California has always been expensive," Cheng said. "I knew that when my wife and I eventually expanded our family, we wouldn't be able to afford San Francisco or the Bay Area in general — even though we both earn good salaries."

7 notes

·

View notes

Text

People on Tumblr are always hyping these news articles about some rich wanker out there, buying up single family homes.

It sucks. Rich wankers are terrible yadda-yadda. Not the point of this conversation. (Burn them)

The thing is that you have some of the worst ideas on how to fix the housing crisis!

Simply because most people aren't super educated on why the housing market is this way.

Ironically, and this might tick a lot of you off. One of the causes of the housing crisis is likely you, or your co-workers, parents, siblings ect...ect.

https://www.investopedia.com/articles/credit-loans-mortgages/090116/what-do-pension-funds-typically-invest.asp

Are you saving money! (I am!)

Do you have a 401K/Pension/Superannuation? (I Do)

Are you invested in a Real Estate Investment Trust?!

Probably.

Most funds have a little bit of REIT in them. The S&P500 is 2.8% REIT,

These mega trusts own vast amounts of American housing.

https://www.reit.com/research/nareit-research/170-million-americans-own-reit-stocks

Yay. Look at this happy graphic that came from a site really stocked about the great returns on real estate investment.

Now. It should be clear REIT actually own a very small portion of American housing, around 1%. Individual owners make up a far larger portion of the housing market.

REIT live in the happy red space.

The problem with REIT is that they are often terrible.

They are bastions of widespread community gentrification. Sweeping into minority communities like Herongate in Canada and bulldozing the lot. All to make way for shinny condos they can turn a profit on.

https://acorncanada.org/news/leveller-rein-reits-tenants-demand-action-against-real-estate-investment-trusts/

REITs have been accused of slumlord like behaviour. Letting houses decay with mold and refusing repair ect. Ect.

https://www.cbc.ca/news/canada/tenants-lose-as-landlord-transglobe-racks-up-charges-1.1246084

https://doctorow.medium.com/wall-streets-landlord-business-is-turning-every-rental-into-a-slum-b15b81f18612

Essentially my point is....

You could be invested in the very Real Estate Investment Trust that acts as your landlord. You could be invested in the source of your own suffering and gentrification.

The pension investment in REITs for domestic housing is growing. It is too profitable. It is an easy source of growth.

If you are in a bad situation, you should want your pension invested in an REIT. It will help grow your savings (whatever they be). But, that very same REIT might own your home and be the very evil trying to wring cash out of you.

This isn't a call to action. This is more an observation about the neoliberal shit oroborus we are stuck in. You can choose not to invest in REITs, or try and find a good one.

But in doing so, you are worsening the housing crisis. REITs are sophisticated. They use rent increase software and have quantitative analysis of the market used to drive prices up.

If the housing market ever tanks, a good portion of your savings might tank with it.

Now. You might have no savings. You might not have elderly relying on social security. You might be fine.

But. Society is run by trashfire electoralism. If people don't see their investments going up they freak out and vote for the other party.

The pension investment into real estate, allowed in 2001 (thanks Bush), has created people whose retirements and future are dependent on housing prices always going up. Around 51% of Americans are invested in REITs. It is essentially a nightmare that will never be fixed unless people who are smarter than anyone on Tumblr actually put an effort in.

Thanks for reading my depressing rant.

(Also. Sorry if you are in Canada. It is bad in AUS but it seems like REITs can steal newborns over there. Like some articles are like wtf.)

https://www.reit.com/news/blog/market-commentary/reit-allocations-pension-funds-increase

https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/us-pension-funds-up-real-estate-exposure-to-offset-rising-risks-71610560

https://www.benefitsandpensionsmonitor.com/investments/alternative-investments/real-estate-has-become-a-cornerstone-asset-class-for-pension-fund-investors/383790

#housing#anti capitalism#fuck neoliberals#neoliberal capitalism#neoliberalism#fuck capitalism#housing crisis

2 notes

·

View notes

Note

I think she spent a ton on PR. Millions most likely. I also would be willing to bet she spent millions on decorating that house. Their security also has to be pricey because it seems like they hire a ton of guards when they go out for events.

Glad to see you back, for however long we have you. sorry to hijack your inbox..

To your point Sassy, I would like to add/point out something... The luxury lifestyle (faux Royal) Lifestyle MM is trying to emulate is expensive as we have all said before. There is a reason celebrities don't spend the way MM does. And those that do, have money coming in by the tens of millions every year guaranteed, be it real estate, Investments, Own businesses, and stuff like that, the likes of Beyonce, Taylor swift, Lady Gaga, Rihanna, Johnny Depp, Kim K and the rest. They can afford the 24hr high tech security because they can rely on their other incomes to generate revenue (Whilst they sleep they are still earning money) i.e Beyonce (doubt this will happen), she can balance it out by doing a concert in Dubai, for 23 million dollars. (there is a reason they were able to buy the most expensive home in California worth 200 million) or release and album and do a tour like other artists. People like Depp can do it because for their own health (drug/alcohol addiction) and they also amassed wealth to the point it wouldn't hurt them one bit to have said security. Lets not talk about Kim K.

There is a reason actors and A listers don't so security, except for specific events, its expensive, attracts attention, and literally screams look at me.

Buying a 14million dollar home, with a mortgage, property taxes, 24hr security, Household staff, Archewell staff, Private Jets, PR management, Lawyers retainer and fees for all the lawsuits they come up with. exclusive packages, Clothes, Interior design of the olive garden... All of this with no guarantee of returns. (because MM is lazy). I wonder which financial/Wealth manager advised them because... I would have fired them immediately. No wealth manager worth their salt would let their client hedge their bets on the spotify, random house and Netflix contracts that have yet to be fulfilled. They would tell you, let the money come in the bank accounts and then make those purchase... especially during the start of Covid.

As much as i don't like Todger at least he is working for his supper. Heart of Invictus, The South Africa doc (should he get someone good to direct it, it could be good), The Spare, and the interviews/promotion of the book i.e Gabor Mate, Job at Better Up.

Madam got 80M and thought that will be enough? What exactly has she done for that money? The bench? Archetypes?, 40 X40?,Pearl? all flops... her Ideas are not generating income of any kind.

The doc was both of them so credit goes to both.

Great points!

Thanks! I will try and stick around for a few days this time. I do lurk on here but tend to come back for the juicy stuff.

They are living a champagne lifestyle on a basic beer budget.

18 notes

·

View notes

Text

I have complicated feelings about this advert.

I don't want us to devalue another group of workers or appear to suggest that anyone deserves less pay.

The issue is not and has never been that Pret gave their workers a pay rise - with living costs rising and inflation high, every employer should be doing their best to ensure their workers are paid fairly.

Both JDs and people working in retail have to deal with stress or less than stellar behaviour from the public sometimes. Both sometimes work unpaid overtime.

The issue isn't that people working in retail earn that much - honestly? They deserve more, too.

The issue is that spending 5 years in university - usually unable to earn, accruing what has now become potentially hundreds of thousands of pounds in student debt to work 48 hour weeks likely with overtime needs to pay to allow people to pay back that debt.

The issue is that we're still expected to pay for compulsory parts of our training - from our portfolios, to our examinations, costing thousands of pounds over our training. That's not including 'optional' courses and seminars and various things recommended for our progression. We're expected to put a LOT of time, and energy, and, yes, money, into progressing our careers. It frequently requires us to move around the country, separating us from our loved ones.

The issue is that our pay hasn't adapted as interest has risen, and as the cost of living has drastically changed. Like some people, we're still earning what we were 10 years ago, but that moeny doesn't buy us what it did 10 years ago.

Some people argue that it's fine because, perhaps 10 years down the line, if you become a consultant, you'll earn a lot more. I find that a difficult argument, because surely my experience, my training and knowledge should be worth something now? Not just in 10 years' time?

It's also worth remembering that consultants actually earn less than plenty of experienced professionals at that level of seniority and qualification in their field - so anyone who stays in medicine until they reach consultant could easily be earning much more if they went private, or picked another field. Medical pay has become increasingly uncompetitive when compared to other fields - which means that we will continue to lose people, because there will be easier jobs or higher pay elsewhere.

What would be considered competitive pay is another issue altogether. But a good start would simply be pay restration so that our pay isn't worth significantly less than it was before - whilst our rent and our mortgages, and our food and our exams, and all the other things we need to pay for like everyone else aren't getting any cheaper.

36 notes

·

View notes

Text

Debt at the heart of the growth paradigm

Before industrialization, much of the world’s population lived in a society with very low per capita economic growth rates. In the 1930’s with the invention of econometrics, economic growth became a symbol of a modern state, and an aspirational goal of the nation to demonstrate progress in comparison to other nations.

However, sustained economic growth comes with an immense social and ecological cost. There is little doubt that increasing pollution and waste generated by the growth economies threaten the well-being of future generations. Likewise, the overuse of the world’s natural resources is eliminating the possibility of people in the majority world achieving the same levels of income as people in high-income countries.

Photo by Alexander Grey on Unsplash

If the problems of the hegemony of growth are obvious, what is creating a “growth trap” so hard to escape?

In today’s economy money is primarily created through the issuance of loans by the private banking sector. Most of the money circulating in the economy is created by private banks. When a person gets a mortgage to buy a new home, the bank creates a deposit account with an equivalent amount of money in the ledger (no new money is printed). However, this deposit is equivalent to other types of money, in fact over 99% of total transactions by value in the UK are bank deposits! Only a fraction of the money is physical cash created by the state.

The problem with this type of money production is that we need to maintain a high level of loans to have money circulating in the economy. Understanding how money is created in the modern economy, and the role of debt in the process of money creation, helps to understand one of the key obstacles to escaping the hegemony of growth.

At the individual level, dept economy means that people must constantly work more than they consume, to be able to pay back their loans. Having a shorter working week, and earning less, is not an option if one needs to pay back a home mortgage or student loan. It is difficult to reduce private debt in the absence of growth.

Likewise, in the non-growing economy, the country governments struggle to pay down their public debt and may need to cut spending on education, health care or other social services. Particularly low and middle-income countries, with large debts issued in foreign currency, are often unable to invest in public infrastructure without taking more loans.

In the worst case to manage their loan payments to international creditors, they must resort to privatising the state assets such as electricity production or drinking water, exposing these “public goods” under speculation of private markets, and making them too expensive to most of the people in the country.

If all loans would be paid back, there would not be money in the economy.

Dept drives growth, which in turn is necessary to avoid financial crises. High levels of public debt mean that growth is the only option to manage the loan without hurting the people living in the country. Likewise, high levels of private debt mean that people have no option other than to continue to contribute their labour to the growth economy.

However, in the current financial system, private banks continue to issue new loans for profit, without any consideration of whether these loans contribute to the economy operating within planetary boundaries or advance equality and social justice.

And while banks and asset mangers cash in profits, the circle of more debt and demands for more growth goes on and on and on….

References

Escaping Growth Dependency – Why reforming money will reduce the need to pursue economic growth at any cost to the environment by PositiveMoney

https://positivemoney.org/publications/escaping-growth-dependency/

Sovereign Money - An Introduction by Ben Dyson, Graham Hodgson and Frank van Lerven

https://www.insearchofsteadystate.org/downloads/Sovereign-Money,-An-Introduction-Dyson-Positive-Money-2016.pdf

18 notes

·

View notes

Text

Good morning! I hope you slept well and feel rested? Currently sitting at my desk, in my study, attired only in my blue towelling robe, enjoying my first cuppa of the day.

Wow! Here we are again: Friday! Where did that week go? No, seriously, where did that week go?

First of all, many thanks to everyone that got involved with Throwback Thursday on my page. Yesterday’s word was FIGHT and the responses were surprising. In fact, some were quite moving. Even though my friends are not violent, we are all fighters! Yes, maybe that’s what we all have in common? We are all strong and we are not afraid.

I will teach from 9.30-12.30 today, then I will rush home to make The Trouble her bacon sandwich. We are bad Jews but she really looks forward to that sandwich. In fact, if I say the word ‘bacon’ on this page, a lot of my friends get very excited.

Monday is a new term at the other place I teach so, on Monday, I will teach not one, not two but three different subjects in a day. Five hours of teaching with a one-hour lunch break. I’m ready, I wonder if they are? My students are often alarmed by me because I ask them questions and make them think. Most people don’t like thinking; it’s too much like hard work. The thing is: you need to exercise a brain the way you need to exercise a body. Use it or you lose it!

Yesterday’s headline in the Evening Standard, “BIGGEST HOUSE PRICE FALLS FOR 14 YEARS”. No shit, Sherlock! Let’s go and speak to the people visiting food banks. Maybe in the afternoon, they can buy that two-bedroom semi in Romford? Or, why don’t we speak to the really wealthy people, buying own-brand food from Tesco and scrambling around in the frozen section looking for ‘best before’ bargains? Maybe they will spend the afternoon purchasing a studio flat in Soho? Wanna know why no one is buying? Because nobody has any fucking money! Wanna know why? Because we are being screwed by energy companies, gas companies and supermarkets and, if the NHS goes private, we’ll have even less money! Security tags on formula milk and Lurpack butter? Really? The Standard actually suggested that, because of interest rate rises, buyers are “spooked”. No, buyers are broke! People that would like to buy are struggling to make ends meet and stand no chance of getting a mortgage! Seriously? A cabinet full of ‘economists’ and none of them knows how to fix the economy.

Yesterday, the weekend’s plans changed! We were going to spend Saturday night with one of our favourite people, but she has cancelled, so we will now dive down to Hove to see Lady Wesker. My brother is there too, and Mum has two lunch guests, so Sunday’s selfie will contain extra people! Could be a tricky manoeuvre? Whatever the weather, I will be strutting my stuff on the promenade on Sunday morning!

Really hope you can join me tomorrow at 1.00 p.m. for ‘The A-Z Of Mi-Soul Music’: the final part of The Letter M (Pt. 13). Doing The Letter N (Pt. 3) live from Soulstice on Saturday, June 24th.

Have a fabulous and funky Friday! I love you all. You’re probably thinking, “You don’t even know me!” but, if people can hate for no reason, why can’t I love?

#mixcloud#mi soul#dj#music#new blog#lockdown#coronavirus#books#weekend#democracy#brexit#cronyism#election#radio

21 notes

·

View notes

Text

I testified Thursday against the City Council Fair Chance for Housing Act, my second time in Council Chambers. The first was in May 2019 when I spoke personally and passionately about protecting New York City’s specialized high schools.

The bill, also known as Int. 632, is another City Council measure designed to protect lawbreakers at the expense of the law-abiding. It would prohibit criminal background checks on prospective tenants and buyers of residential housing.

After testifying, I left City Hall. It wasn’t until hours later that I heard the racist response to my testimony from Douglas Powell, who spoke on behalf of city-funded nonprofit Vocal-NY. He and his organization want individuals such as Powell, who has a criminal record and is a level 2 registered sex offender, to be able to access housing without criminal background checks.

His testimony laid out his criminal-justice experience and his lived experience of anti-black discrimination at Asian stores — culminating in a racist attack on the Asian community where he lives. In his three-minute tirade, he called Queens’ Rego Park the most racist neighborhood because it is majority Asian. “It’s not their neighborhood — they from China, Hong Kong,” he said. “We from New York.”

Convicted sex offender spews anti-Asian slurs during NYC Council meeting — and pols do nothing to stop him

This anti-Asian, perpetual-foreigner, “You don’t belong here” rhetoric is dangerous hate speech that incites violence. Unprovoked attacks on Asian New Yorkers are on the rise.

Powell’s racist rant was delivered in the presence of three councilmembers without interruption or admonishment. Committee chair Nantasha Williams even thanked Powell for his testimony. It’s as if his anti-Asian hate speech in the chamber was unremarkable white noise. It took hours, after online pressure from constituents, for those present to issue generic disapproval statements, retweeting other electeds’ condemnation, and say “both sides” share blame for systemic racism.

Like many Asian Americans, I am a property owner and small landlord. When I graduated, my parents encouraged me to live at home, pay off my debt and save to buy a property. I lived at home for a few years and paid off my student loans as quickly as I could. Decades later, I bought my first investment property. I rented mostly to young men and women at the start of their careers. As a landlord, I treated my tenants the way I wanted to be treated: fairly and responsively. I’m fortunate real-estate brokers and condo management could conduct criminal and credit checks, not only for my benefit but for the safety of neighbors in the building.

Powell spewed hateful, anti-Asian rhetoric at the council meeting.Stephen Yang

Asian Americans have the highest rate of home ownership in the city, 42%. The stability of owning property as a means of building wealth is deeply rooted in Asian culture. New York’s pro-tenant policies, especially the Emergency Rental Assistance Program, have resulted in heartbreaking stories from small-property landlords. The laws, intended to help tenants, some of whom lost jobs during COVID, disproportionately hurt immigrant landlords. Not only have they not been paid rent for three years; some living in multi-family units are terrorized by tenants who know they can’t evict. Many Asian property owners are working class, and their modest rental income helps pay for the mortgage, property taxes and unit upkeep.

While bad tenants existed before this bill, it would make things worse. Private-property owners should not bear the burden of unknowingly renting to convicted arsonists and murderers and letting them live next door to New Yorkers who want a safe place after a long day braving our unpredictable city streets and subways. We worry about higher insurance, liability in endangering other tenants and frivolous lawsuits in tenant-friendly courts. That becomes a cost-benefit question for owners — whether it’s worth it to rent with little profit.

Like most landlords, I don’t live in the building I rent, but I do worry about the tenants I rent to. I think of the kindhearted young Asian professional who pleaded with me to let her have a Hurricane Sandy rescue dog. I worry about the wheelchair-bound young man grateful to find independence in living in an accessible building and appreciative of me letting him install an automatic door opener for his convenience. I want them to have the peace of mind that when they return to their small haven in the city, they will be safe, among neighbors who won’t pose a risk to them.

The fight to save specialized high schools that brought me to council the first time galvanized many Asian voters who had never been involved in city politics before. I am one of those newly politicized voters. This year, I co-founded Asian Wave Alliance to make sure that Asian-American New Yorkers’ needs are not ignored by the very councilmembers who sat quietly and listened to Powell’s racist attacks.

This time, I went to council to convince the Committee on Human and Civil Rights and the bill’s sponsors that the Fair Chance for Housing Act is not “fair” at all to small landlords and already-existing tenants. Getting rid of reasonable safeguards like criminal background checks is not “fair” to the city’s law-abiding citizens and will put people in danger. True fairness requires listening to all New Yorkers and prioritizing safety and transparency.

41 notes

·

View notes

Text

Short-Term Cash Loans: An Excellent Aid When Things Get Tough

Short term cash loans direct lenders are an absolute must if you need money fast—say, within 24 hours—because your wallet is empty and you need to access it privately. You can obtain appropriate financing using short term cash loans without sacrificing any protection. The good news is that you can receive the money at your convenience without having to leave your house, as the financing is delivered directly to you.

Some lenders offer short term cash loans to clients with current, valid checking accounts as soon as 24 hours after the borrower submits the loan application. Online loans are preferable because all you have to do is fill out a brief application form on the lender's website and submit it. If your information is verified, the funds are transferred to your account promptly. You can skip having to fill out any onerous procedures by using this online technique.

In a matter of two or four weeks, you can receive a reimbursement in the range of £100 to £1000. When your next paycheck arrives, you will know when to make your repayment. Since the amount you borrow is secured against your paycheck, you must pay back the loan by the deadline. You don't give a damn about your poor credit history if you take out short term loans UK direct lender.

You have complete freedom to use the funds for any short term financial goal without fear of hindrance. Therefore, you don't lose out on applying for short term loans UK direct lender when you have some extra demands, including buying home appliances, paying grocery store bills, paying for your child's tuition or school, fixing your car, and many more.

Does taking out a Short Term Loans improve my credit score?

Whether short term loans direct lenders are beneficial or bad for your credit rating is a topic that is frequently debated. On the surface, obtaining a loan and properly managing it—that is, making all of the repayments on time—should improve your credit score because it shows that you can handle your money and borrow responsibly.

However, a lot of other lenders (apart from short-term loans lenders) view the usage of short-term loans as an indication that you are not good with money and that you might be too risky to lend to.

We are aware that, even if a borrower has utilized payday loan or short-term loans in the past, mortgage lenders are especially wary of them. Before applying, you should consider the dangers associated with obtaining short term loans UK. If you plan to apply for a mortgage soon, you might want to consider your options first.

Applications for short term loans UK direct lender are typically sent directly to the lender; however you can expedite the process by utilizing our price comparison.

You may go straight to the lender's website and continue doing business with them after we compare all of the top lenders in the UK and determine which one is the cheapest for the loan you're searching for.

4 notes

·

View notes

Text

Smart World Sector 113 Gurugram - The best place to invest.

About the smart world sector 113 gurugram

The Smart World Sector 113 has located in Gurgaon, and it is sought-after projects in the city. It offers a luxurious lifestyle with all modern amenities and facilities. The project has built with all latest technologies to make life easier. It has located in proximity of the metro station. It has a huge shopping mall nearby. The project has designed by renowned architect. It is a dream project of yours. The project is full of life with all modern amenities and facilities. It offers a luxurious lifestyle with all the modern amenities and facilities. It has located in the proximity of the metro station and has a huge shopping mall nearby. The smart world sector 113 has located in Gurgaon, and it is one of the most sought-after projects in the city. It offers a luxurious lifestyle with all the modern amenities and facilities.

About the creators of smart world sector 113 Gurgaon-

The project has developed by one of India’s top developers, smart world Group. It has a total area of 13 acres and includes 7 towers with 5 floors each. The project will owned and managed by smart world developers. which has targeted a sales target of 5,000 flats across the city. Smart World 113 has expected to completed soon from the date of registration. The project will divided into two parts with a central plaza. which will house different amenity-based activities for the residents. The rest of the land will house individual residential towers. The towers have designed in such a way that they ensure enough natural light on all units on each floor. There is also an elevated water feature and fountain at the main entrance of the project. It provides respite from the hustle and bustle of city life.

Amenities provided by the Smart World 113 Gurgaon -

As we know smart world sector 113 is a residential project by the smart world developers. hence it has coupled with all kinds of basic as well as luxury amenities. The term amenities refers to the features offered in residential real estate projects. Amenities are a powerful way for developers to convince the buyer to buy their project. Because they can offer a buyer something that most other buyers cannot. Amenities have defined as:-exclusive certain recreational, social, or cultural facilities. such as-

Swimming pools with water games

Both indoor and outdoor tennis courts

Golf courses with a lush green surrounding

High-end appliances

Large swimming pools with safety equipment

Access to a private golf course.

Restaurants and bars for refreshments

A separate building for laundry as well as other services

Housing professional staff is also available

Provision of individual climate controls in each unit

A dedicated parking space for each unit

Separate building for domestic staff

Amenities are an important part of smart world sector 113 gurgaon. Home buyers often look for homes with amenities. Because they want their homes to be more than the places where they live. They want them to be their retreats. The buying of a home often leads to a dramatic increase in monthly mortgage payments. Home ownership is a huge financial commitment and comes with serious implications also. When finances are tight, people often choose to rent a home. Because it provides more flexibility over their living situation.

#smart world 113#smart world 113 gurgaon#smart world sector 113#smart world sector 113 gurgaon#smart world sector 113 gurugram#smart world 113 gurugram#Smart world gurugram

8 notes

·

View notes

Text

Exclusive Guide to Finding the Best House for Sale in Melbourne

So you have decided to buy your dream house in the most liveable city on earth—Melbourne?

Did you know that it is often referred to as the “world’s sporting capital”?

Besides having graffiti laneways, cultural diversities, a bayside location, and mouth-watering coffee, this is a good place to live for many reasons.

It has multiple public transportation options, plenty of job opportunities, low crime rates, an immense arts and culture scene, and, in short, an easy lifestyle. Buying your dream house is a big decision, and it must be backed with solid research to get the best deal.

To help you out, we have come up with an extensive guide to finding the best house for sale in Melbourne. Now buckle up and start reading this article to get a vivid image of the buying process.

Tips to Find the Best House for Sale in Melbourne

There are numerous things to consider while checking homes for sale. To ensure you make the buying process a streamlined one, check out the following things.

Fix your budget

You visit a house for sale in Melbourne. It’s alluring, stands tall, and even beats all your expectations. You excitedly enquire about the price and get disappointed to learn it is way beyond your budget.

This hurts badly. To avoid such unpleasant things, first, fix your budget. Once you have a budget fixed, you can filter the market and visit the houses with the confidence that you can buy one if it meets your necessities.

This is why, when it comes to buying a house for sale, having enough funds is critical. From the down payment to closing costs, you must adhere to strict financial commitments. But it’s not always about the money; it’s about the security and freedom that come with owning your dream house, where you can dwell with your loved ones. First, decide on the budget and finances, and set realistic goals.

What are the must-haves in your dream house?

Now take a pen and paper, sit down with your family, and list the must-haves of the house in Melbourne. This might be a big list, but you need patience to curate it. Because acknowledging your needs helps narrow down your search and find the ideal place to live.

Buying your house starts with one simple decision: finding the ideal location to call home. You have already decided that it’s Melbourne.

But did you know that Melbourne is a diverse city with many suburbs to choose from?

The next thing you must fixate on is the size of the house, including the number of bedrooms and bathrooms, the style, outdoor space, safety, storage, energy efficiency, and parking.

On top of that, while checking out the Melbourne house for sale, don’t forget to consider the proximity to work, schools, and other amenities.

When tailoring your list, ensure it meets your needs and preferences because you are investing big, and it must be worthy and close to your heart.

Thoroughly investigate home loans

Skipping mortgage pre-approval is one of the biggest mistakes you can make.

If you have decided to get a loan, first learn how much your bank will offer. Remember, what the bank says you can afford is different from what you know you can afford.

On the other hand, what you think you can afford to buy a house in Melbourne is different from what the bank is willing to lend you. Your chances of getting a loan can be affected if you have poor credit or an unstable income.

So, ensure that you are pre-approved for a loan before placing an offer on a home or even before you start house-hunting.

Note: Even if you are pre-approved for a mortgage, your loan can be denied at the last minute if you alter your credit score by financing a car purchase, etc. So be extra careful of the things you plan to buy or lend using your card.

Inspect a property before purchasing it.

Usually, the houses for sale in Melbourne will be presented for inspection by potential buyers at different time slots. Some houses are available for private inspection and can be visited with the real estate agent’s help.

You get 30 to 45 minutes for open home inspections. To make the most of the inspection during this time, make a checklist of what to check.

Use the checklist while inspecting properties.

Take pictures and notes of the property, including the exterior features and if any damage or issues are present. You can make a note of your likes and dislikes for that property.

Ask questions to the concerned person, i.e., the real estate agent there.

If it is a new house, you can ask about

The warranty or guarantee and what it covers

Are upgrades or customizations available?

What are the energy-efficiency features the house has?

If it is an old house, you can enquire.

When was the house last renovated?

Why is the vendor selling it?

What’s included in the property?

How long have they lived there?

What were the past maintenance or repairs done?

Are there any known issues with the house?

By asking questions relevant to your situation, you can better understand the advantages and potential challenges of buying a new house versus an old house and make an informed decision.

This process can seem daunting, and you may lack the experience to deal with it. Get professional help from real estate agents to handle it. Professionals can spot hidden problems and ensure that it’s worth investing in the house.

Don’t ignore the neighborhood.

While checking out the houses for sale in Melbourne, you will naturally be more focused on the house and may overlook the neighborhood.

We understand that it’s not possible to predict the future of your selected neighborhood. But asking about its past can help you avoid unpleasant surprises down the road.

If there is any undeveloped land around, enquire about what is likely to get built there.

Is the home value in the neighborhood rising or declining?

What are the zoning laws in the area?

Check the crime rate and safety. Visit the local houses and neighbors to clear up these doubts.

If you are happy with the answers to these questions, you can show a green signal.

Check the property titles.

Check if the property titles are correct because they are the birth certificate of your property. Homebuyers hire a title company to perform title searches on their behalf.

Here, a real estate attorney can also help find out if any legal issues are present and if the property has been legally transferred to you. In addition, ensure the property boundaries are clearly defined and that there are no boundary disputes.

Check with the local council.

Before you seal the deal, check with the local council to enjoy a worry-free home-buying experience.

The local council is in charge of managing, planning, and developing the area, so they know the ins and outs of it.

So, we can safely call the local council the guardian angel because they can give you insider information that your seller or real estate agent might hide from you.

With their expert knowledge, you can know if the house for sale in Melbourne abides by zoning laws and building codes and is in full compliance with regulations.

Or any future development in the area could affect your property value or quality of life.

Money may not be able to buy happiness, but it sure can buy you a roof over your head!

Make an offer and close the deal.

Making an offer to the households is of huge importance. Before you make an offer, determine your budget and strictly stick to it. Also, consider the additional expenses, including the inspection fees and closing costs.

Next, research recent sales of similar houses in the same neighborhood to determine if the asking price is fair. Your real estate agent can aid you in negotiating and sealing the best deal.

Before sending the proposal, consider contingencies. The contingencies in your offer can save you from unfortunate circumstances such as the inability to secure financing, etc. But ensure you don’t mention too much of it, as it can create a bad impression.

Lastly, write a personal letter. Well, this unique idea can make you stand out from other buyers and create an impression. Be genuine and authentic, and explain why you want to buy the property.

Remember, making an offer is just the beginning of the negotiation process. The stronger the offer, the more chances you have of securing your dream home.

Final Words

And to conclude, an important point to remember is: Don’t overthink signing the deal. We understand that buying your dream house is huge. But again, you must have done ample research before throwing an anchor on one.

There are cases where buyers lose the best deal because someone else takes the swift decision and buys it. And importantly, negotiation is important, but overdoing it can ruin the deal. When the house for sale in Melbourne ticks most of the boxes on your checklist, go for it.

Buying your house can be thrilling, but it can also be overwhelming if you put everything in your head. So, hire a real estate agent to hold your hand in the right direction.

RIC Realty is a full-service real estate agency where we are passionate about helping people realize their dreams and aspirations through property. Our team of experienced professionals can make your buying or selling process a breeze. From research and analysis, advisory, and transactions to project management and marketing, we can take care of all end-to-end work while you relax at home, Netflixing and chilling!

2 notes

·

View notes

Text

2023 / 18

Aperçu of the Week:

"Experience is the hardest kind of teacher. It gives you the test first and the lesson afterward."

(Oscar Wilde)

Bad News of the Week:

What's true in security policy is also true in fiscal policy: if the U.S. isn't fit, the whole world gets sick. The world's (still) largest economy sets the tone. Many global trade flows, e.g. for energy, are conducted in U.S. dollars, and in many countries it has replaced the domestic currency - whether unofficially, as in Zimbabwe, or even officially, as in El Salvador. So what happens to the U.S. economy or the U.S. dollar has global implications.

In the process, there seems to be a kind of parallel universe. Normally, in the economy, when a so-called insolvency threatens, all the alarm bells go off: Employees look for new jobs, suppliers stop supplying, the bank cancels the credit line, creditors are left sitting on their claims. The company is simply bankrupt, at the end of its rope, with no future prospects. Except, perhaps, for a few fillet pieces that the competition buys up at bargain prices. This does not apply to the USA. Because it is effectively bankrupt. And no one seems to care.

The current debt level - only of the state, not of its companies (banking crisis) or citizens (mortgage and credit card crisis) - amounts to $31.38 trillion. This is significantly more than the gross domestic product (GDP) of $26.85 trillion. In fact, this can never be repaid. For comparison: in Germany, $2.73 trillion in debt is compared to a GDP of $5.32 trillion. And we feel that this is bad. The creditors of the USA sit primarily abroad - whether friendly like Japan or even downright hostile like China. And sleep apparently nevertheless calmly. And that even in the face of the current (once again) concrete threat of insolvency.

Normally, and this has been the case for decades, this is nothing more than a ritual: the money is no longer enough, Republicans and Democrats agree - sometimes with more, sometimes with less dispute - to ignore the debt ceiling, which is actually regulated by law, they obtain money on the markets without any problems and act as if nothing had happened. Until next time. Business as usual.

This year, things may turn out differently. Because the trench warfare between the duopoly parties could reach a new level. Which this time might not be done with a few government agencies and national parks closed for two weeks. Already since the in many ways ridiculous election of Kevin McCarthy as Republican majority leader in the House of Representatives, this has been publicly announced. Because the ultra-right MAGA freaks like Marjorie Taylor Green or Matt Gaetz have made it clear that they will play hard ball on this issue at the latest: rather cuts in social services as well as environmental protection than a suspension of the debt ceiling. For party-political reasons and without a shred of interest in economic or financial policy. At the same time, Treasury Secretary Janet Yellen warns that so far it has only been possible to avert default through "a series of extraordinary measures".

Strange that the U.S. nevertheless has a credit rating of AAA. Is that perhaps because the three relevant agencies, Standard & Poor, Moody's and Fitch, are all U.S.-based private firms? Or that no one wants to admit that there may be a systematic problem after all? In every banking crisis - and we have one right now that is nowhere as dramatic as in the U.S. - the term "too big to fail" makes the rounds. The land of unlimited opportunity, unreal projection surface for the hopes and dreams of large parts of the world's population, must not be allowed to fail. That is psychology. It's certainly not mathematics.

Good News of the Week:

More and more often, I notice on the train and in the supermarket that I'm the only one still wearing an FFP2 mask. Yet I'm not an overly anxious person. I am merely part of a vulnerable group for whom it is still better not to become infected with the corona virus. But that is my personal decision. And no longer a legal requirement. Because there isn't one anymore. Except in many doctors' offices, where masks are still mandatory if that's what the doctor wants - which objectively would have made sense even earlier, because after all, that's basically where a disproportionate number of viruses and bacteria are buzzing around.

Basically, I'm glad that the Word Health Organization (WHO) officially lifted the international health emergency due to Corona on Friday. After more than three years of a worldwide pandemic. In the balance, there are more than 20 million deaths. A health system that reached its limits and exceeded them in many countries. A mass death of retailers and cultural institutions. Lots of children and young people with mental health problems - or at least major failures as they grew up.

Many health policy decisions were right. Many were wrong. Some fellows discovered their social empathy. Some a penchant for conspiracy theories. Friendships and bonds of solidarity have grown. Or were destroyed. As is so often the case in life, the task now is to learn from the past for the future. Because it will not be the last challenge that human society will have to face - looking at the news, the multi-crisis still dominates.

Therefore, it is nice that we have at least left behind the frightening side effects of the Corona pandemic. Which will accompany us from now on as a "completely normal" respiratory disease with a potentially fatal outcome. Like the flu. Because let's face it: normality can be very reassuring.

Personal happy moment of the week:

Last Monday was May 1, a public holiday in Germany. And while on "Labor Day" (actually absurd that this day of all days is a public holiday) demonstrations of the trade unions for more workers' rights take place everywhere in Germany, the accent in Bavaria is elsewhere. Namely on the maypole. A tradition according to which an approximately 30 meter high, white-blue painted trunk is erected with muscle power - accompanied by music, dance and beer. Cancelled the last years because of Corona, it was nice to be able to celebrate this festival again this year. Even the rain had a mercy and took a break for the crucial three hours.

I couldn't care less...

...that the United Kingdom has a new head of state since yesterday, King Charles III. And so do Canada, Australia, New Zealand and 13 other Commonwealth countries. All the pomp, his costumes and rituals etc. show me one thing above all: monarchies are no longer in keeping with the times. And are not democratic.

As I write this...

...I am listening to music. Right now John Legend. And think about the fact that this is probably the only undoubtedly exclusively positive achievement of mankind: art. Whether it's music, poetry, performing or visual art, analog or digital, live or documented. The kind of creativity that does not seek a concrete use value, but stimulates, entertains, inspires, polarizes, makes you think. L'art pour l'art is something very beautiful.

Post Scriptum

Germany reached its "earth overload day" last week. So if all of humanity were as wasteful with resources as we are, it would need three Earths. We only buy green electricity and drive an all-electric car or use public transportation. We try not to throw away food and collect everything that can be recycled. We order as little as possible from Amazon (okay: also because we simply can't stand the working conditions of this company and its owner himself) and basically try to reduce our consumption (okay: this also saves money and has an educational value). And yet we are more part of the problem than part of the solution. Sigh...

#thoughts#aperçu#good news#bad news#news of the week#happy moments#politics#oscar wilde#usa#debt ceiling#congress#bankruptcy#coronavirus#ffp2#who#labor day#first of may#united kingdom#charles iii#windsors#john legend#music#creativity#germany#earth overload day#arts#commonwealth#restrictions#maga#insolvency

2 notes

·

View notes

Last Seen Blogs

daria-kinga

seblove

stovejudo9

The Journey of Padilla 700

im-not-not-michael

Mr. Bright Side

libraryofstyle

The Library of Style

playwin234-xxx

PLAYWIN234 >> SITUS JUDI SLOT,BOLA,CASINO,POKER BERLISENSI RESMI