#$KKR

Text

5 Trade Ideas for Monday: Avantor, Deere, Hartford, KKR and Meta

5 Trade ideas excerpted from the detailed analysis and plan for premium subscribers:

Avantor, Ticker: $AVTR

Avantor, $AVTR, comes into the week approaching resistance. It has a RSI in the bullish zone and a MACD positive. Look for a push over resistance to participate…..

Deere, Ticker: $DE

Deere, $DE, comes into the week at resistance. It has a RSI in the bullish zone with the MACD flat but positive. Look for a push over resistance to participate…..

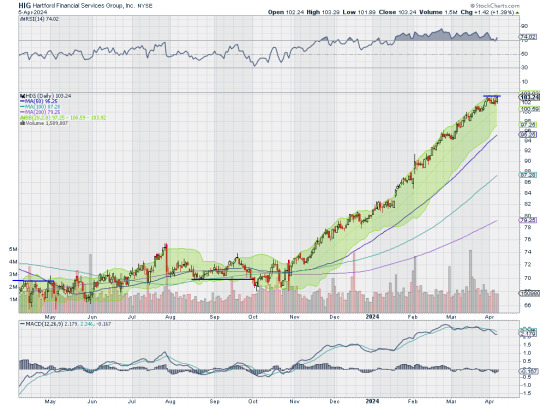

Hartford Financial Services Group, Ticker: $HIG

Hartford Financial Services Group, $HIG, comes into the week at resistance. It has a RSI in the bullish zone with the MACD positive. Look for a push over resistance to participate…..

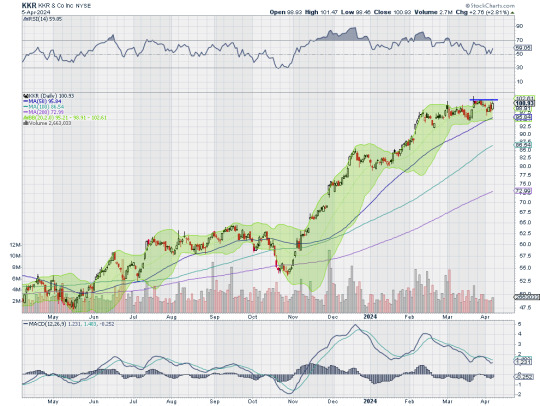

KKR, Ticker: $KKR

KKR, $KKR, comes into the week approaching resistance. It has a RSI in the bullish zone with the MACD positive. Look for a push over resistance to participate…..

Meta Platforms, Ticker: $META

Meta Platforms, $META, comes into the week breaking resistance. It has a RSI in the bullish zone with the MACD positive and crossing up. Look for continuation to participate…..

If you like what you see sign up for more ideas and deeper analysis using this Get Premium link.

After reviewing over 1,000 charts, I have found some good setups for the week. These were selected and should be viewed in the context of the broad Market Macro picture reviewed Friday which with the first week of April in the books, saw equity markets in need of a rest.

Elsewhere looked for Gold to continue its record run higher while Crude Oil continue its move to the upside as well. The US Dollar Index to continue the short term trend to the upside while US Treasuries may resume their downtrend. The Shanghai Composite looks to continue the short term move higher while Emerging Markets consolidate under long term resistance.

The Volatility Index looks to remain low making the path easier for equity markets to the upside. Their charts also look strong, especially on the longer timeframe. On the shorter timeframe the QQQ is at risk for some downside with the IWM in a messy short term uptrend and the SPY the strongest but also seeing some profit taking show up. Use this information as you prepare for the coming week and trad’em well.

1 note

·

View note

Text

Private equity rips off its investors, too

I'm coming to DEFCON! TOMORROW (Aug 9), I'm emceeing the EFF POKER TOURNAMENT (noon at the Horseshoe Poker Room), and appearing on the BRICKED AND ABANDONED panel (5PM, LVCC - L1 - HW1–11–01). On SATURDAY (Aug 10), I'm giving a keynote called "DISENSHITTIFY OR DIE! How hackers can seize the means of computation and build a new, good internet that is hardened against our asshole bosses' insatiable horniness for enshittification" (noon, LVCC - L1 - HW1–11–01).

It's amazing how many of the scams that have devastated our economy and everyday people owe their success to the fact that we assume that rich people know what they're doing, so if they're doing something, it must be real.

Think of how many people lost everything by gambling on junk bonds, exotic mortgage derivatives, cryptocurrency and web3, because they saw that the largest financial institutions in the world were going all-in on these weird, incomprehensible bets.

Then there are the people who are convinced that online advertising is built around a mind-control ray, because tech companies claim that's what they have ("I am an evil dopamine-loop-hacking wizard and I can sell anything to anyone!"), and because huge, sober blue-chip companies hand billions to these soi dissant svengalis. Sure, online ads are a swamp of clickfraud and garbage, but would these super smart captains of industry spend so much on online advertising if it didn't work super-well?

http://pluralistic.net/HowToDestroySurveillanceCapitalism

From our worms'-eye-view here on the ground, it's easy to assume that rich people and the people who sell them stuff are all on the same side. "If you're not paying for the product, you're the product," right? If Facebook is tormenting you with surveillance advertising, it must be doing so on behalf of the surveillance advertisers, for whom Mark Zuckerberg has bottomless reservoirs of honest, forthright impulses.

The reality is simultaneously weirder, and obvious in hindsight. The reason Zuck is tormenting you is that he's a remorseless sociopath who doesn't care who he hurts. He rips off everyone he can rip off, and that includes advertisers, who have seen steady price-hikes and lower-fidelity targeting, even as ad-fraud has skyrocketed while Facebook draws down its anti-fraud spending:

https://www.404media.co/where-facebooks-ai-slop-comes-from/

This is not to say that Facebook advertisers have your best interests at heart, that they aren't engaged in active deception in order to better themselves at your expense. Rather, it's to say that there's no honor among thieves, and Zuck is an equal-opportunity predator. Moreover, both Zuck and his advertisers are credulous dolts, so the mere fact that they are pouring money into something (advertisers: FB ads; Zuck: metaverse) it doesn't follow that these are real or important or the coming thing.

For me, the Ur-example of "rich people are dumb, even when it comes to money" is the private equity sector. I've written a lot about PE, and how destructive it is to the real economy, from Toys R Us to pet grooming:

https://pluralistic.net/2024/08/05/rugged-individuals/#misleading-by-analogy

How they killed Red Lobster:

https://pluralistic.net/2024/05/23/spineless/#invertebrates

And how they actually created the death panels that Sarah Palin warned us about (it's OK, though: these death panels are run by the efficient private sector, not government bureaucrats):

https://pluralistic.net/2023/04/26/death-panels/#what-the-heck-is-going-on-with-CMS

The devastating effect of private equity on the real economy is increasingly well understood, and a curious side-effect of this is that people assume that if PE is destroying their lives, they must be doing so on behalf of their investors, who are making bank.

But – like Zuck – PE bosses are just as happy to steal from their investors as they are to to steal from the workers and customers of the businesses they acquire on those investors' behalf. They swaddle this theft in performative complexity and specialized jargon, but when you strip all that away, you find more fraud.

All the misery that PE inflicts on workers, communities and customers are just a convincer in a Big Store con, a bid to make the scam seem credible. For a certain kind of investor, any economic activity that destroys communities and workers' livelihoods must be a good bet. This is the dynamic at work in the pitch of AI image-generator companies, who spend tens of billions on technology that there is no substantial market for:

https://pluralistic.net/2024/07/25/accountability-sinks/#work-harder-not-smarter

AI image generators represent a high-profile, extremely visible example of "a job that AI can do." Nevermind that AI illustration went from a novelty to a tired cliche in less than a year. Even if you think that AI illustrations are a perfect substitute for commercial illustrations, that still won't come anywhere near making AI companies a profit. Add up the entire wage bill for every commercial illustrator in the world, hand it to Open AI, and you're not even gonna cover the kombucha budget for Open AI's staff kitchens.

Hell, all the wages of every commercial illustrator that ever lived won't pay back even a fraction of the money the AI companies spent on image generators. The pauperization of an entire class of creative workers is just a canned demo, a way to fool investors into thinking that there is a whole universe of similarly situated workers whose wages can be diverted to AI companies. This is the logic of small-time spammers, scaled up to the scale of the entire S&P 500. Smalltime spammers looked at AI and thought, "OK, I can generate as much botshit as I want on demand for free. Science fiction magazines pay $0.10/word. So if I generate a billion words, I'll get $100 million." But that's not how any of that works: sf magazines don't buy botshit, and even if they did, the entire market for short fiction adds up to what Sam Altman spends on a single designer t-shirt. The point of destroying these beloved, useful things isn't to make a lot of money by taking their markets – it's to convince dopey, panicked rich people to give you lots of money you can steal, because they think you can do this to every market and they don't want to miss out on the opportunity of a lifetime:

https://pluralistic.net/2024/01/15/passive-income-brainworms/#four-hour-work-week

Take "divi recaps": after a private equity firm acquires a company (by borrowing money against its assets), it typically declares a "special dividend," emptying out the company's cash reserves and pocketing them. A "divi recap" is when PE then takes out another massive loan against the company's (remaining) assets and pockets that:

https://pluralistic.net/2020/09/17/divi-recaps/#graebers-ghost

All of this happens under an opaque cloud, thanks to the light-to-nonexistent disclosure rules for PE. A public company has to open its books for the SEC, its investors, and the world. PE is private – and so are its finances. It is absolutely routine for PE bosses to put their spouses, kids, and pals on the payroll and hand them millions for doing little to nothing, all at the expense of their investors:

https://www.nakedcapitalism.com/2022/02/sec-set-to-lower-massive-boom-on-private-equity-industry.html

PE bosses charge huge fees to their investors – not merely the usual 2-and-20 (2% of the funds under management and 20% of any profits) – but also a wide variety of special one-off fees that pile to the sky. They also dip into their investors' funds to issue themselves massive loans that they use to make side-bets, without telling the investors about it:

https://pluralistic.net/2022/02/10/monopoly-begets-monopoly/#gary-gensler

PE investors are chickens ripe for the plucking: take "continuation funds," which allow PE bosses to soak the rich people and pension funds who supply them with billions:

https://news.bloomberglaw.com/mergers-and-acquisitions/matt-levines-money-stuff-buyout-funds-buy-from-themselves

Remember 2-and-20? 2% of all the money you manage, every year, and 20% of all the profits. You'd think that these would be somewhat zero sum, right? If you use some of your investors' cash to buy a company, and then sell off that company for a profit, you get the 20%, but now the pot of money you're managing has gone down by the amount you used to buy the company, and so your 2% carry goes down, too.

But what if you sell your portfolio companies to yourself, using your investors' own money? When you do that, you continue to hold the company on your PE firm's books, meaning you continue to get the 2% carry, and you can pocket 20% of the sale price as a "profit":

https://pluralistic.net/2023/07/20/continuation-fraud/#buyout-groups

This is straight-up fraud, wrapped up in so much jargon that it can successfully masquerade as "financial engineering" ("financial engineering" is really just a euphemism for "fraud"). PE bosses keep coming up with new, exotic ways to steal from their investors. The latest scam is "tax receivable agreements":

https://archive.ph/RczJ9

On its face, this is a tax scam. When a company goes public, early investors generally hold stock in the original partnership or LLC; this company ends up holding a ton of shares in the new, public company. When they sell those non-public shares in the LLC, this creates a (potentially gigantic) tax credit.

A TRA hustle involves tracking down these LLC shareholders and convincing them to sign off on dumping the LLC's shares, which generates a huge tax credit for the public company. The hustler offers to split these credits with the LLC holders.

All of this is especially attractive to PE bosses, who often take a company private, do a bunch of "financial engineering" and then take it public again, leaving the PE firm as the owner of those LLC shares that can be converted to a TRA and a huge windfall – which the PE bosses pocket, because they (not their investors) are holding those credits.

This scam is really doing big numbers. KKR – the monsters who killed Toys R Us – just diverted $650 million in TRA loot, prompting a lawsuit from Steamfitters union pension fund, which had handed these jerks millions of its members' money to gamble with:

https://archive.ph/kqQvI

This highlights another very weird aspect of the PE scam: they are absolutely dependent on pension funds. To add insult to injury, PE funds are notorious union-busters – they use union money to buy companies and destroy their unions:

https://pluralistic.net/2023/10/05/mr-gotcha/#no-ethical-consumption-under-capitalism

People who try to understand the PE business model often give up, because it seems to make no sense, leading many to assume that they're too unsophisticated to grasp the complex financials here. For example, PE is absolutely dependent on massive loans as a way of looting its businesses, but it also often defaults on those loans. Why do banks and investors keep making huge loans to PE deadbeats? Because – like the PE fund investors – they are credulous dolts.

The reason PE seems like a scam is that it is a scam. It is a fractal scam – every part of it is a scam. You might have heard about the "carried interest" tax loophole that allows PE bosses to avoid billions in taxes on the money they steal from their investors, creditors, workers and customers. Most people assume "carried interest" has something to do with "interest" on a loan. Nope: "carried interest" is a 16th century nautical tax rule designed for mercantalist sea-captains who had an "interest" in the cargo they "carried":

https://pluralistic.net/2021/04/29/writers-must-be-paid/#carried-interest

But rich people and other "sophisticated investors" (like pension fund investment managers) are no smarter than the rest of us. They are herd animals. When they see other rich people piling into some scheme or asset class, they rush to join them, which makes the asset price go up, which makes them think they're smart (until the inevitable rug-pull). When one plute jumps off the Empire State Building, the rest of them jump, too.

Which is why there's more money flooding into PE than at any time in history, $2.62T in "dry powder," handed over to greedy, thieving PE bosses in a poker game where everyone is the sucker at the table:

https://www.institutionalinvestor.com/article/2di1vzgjcmzovkcea8f0g/portfolio/private-equitys-dry-powder-mountain-reaches-record-height

If you'd like an essay-formatted version of this post to read or share, here's a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2024/08/08/sucker-at-the-table/#clucks-definance

#pluralistic#tra#tax receivable asset#financial engineering#private equity#two sided markets#pe#looters#sucker at the table#kkr#debt#dry powder

373 notes

·

View notes

Text

Harry and her never ending love for jersey no.23 <3

He's such a soft dad, it melts my heart

32 notes

·

View notes

Text

It's rainin so hard here in Kolkata as if the nature is celebrating along. And then there's those legends who are burning firecrackers.

Anyway kkr slayyyyyin in purple

And Sunset ho gya

#ipl2024#ipl#kkr#csk vs kkr#kkrvssrh#rcb vs kkr#desi teen#desi tumblr#desi tag#desi dark academia#desi things#being desi#desi girl#desi#growing up desi#desi academia#indian memes#india#indian cricket team#indian cricket news#csk#srh#srk

48 notes

·

View notes

Text

Kolkata biriyani wins 💜

P.S. NO I AM NOT HATING ON ANY KIND OF BIRIYANI

#korbo lorbo jitbo re#korbo lorbo re jitbo re#please don't come at me#kkr#ipl final#kkr vs srh#being bengali#bengali girl#desiblr#desi tumblr#desi teen#desi tag#desi#desi shit posting

22 notes

·

View notes

Text

*any csk batsman gets out*

csk fans: oh no

*ms dhoni on the field*

the entire stadium: OH YES

#csk#ipl#ipl2024#csk vs kkr#desi#desiblr#just desi things#it always happens#ms dhoni#msd#the man the myth the legend himself

30 notes

·

View notes

Text

I’m genuinely tweaking rn

20 notes

·

View notes

Text

@pscentral event 17: vibrance

KOHATSU KOKORO

PSYCHIC FEVER from EXILE TRIBE

template

#kohatsu kokoro#psychic fever from exile tribe#userdramas#jpopnetedit#jpopedit#usermare#usergooseras#userfext#psychic fever#exile tribe#jpop#flashing tw#m.gif#*psyfe#*kkr#psc#i did not plan this but here i am 6 hours later

{kind=link}

135 notes

·

View notes

Text

commentator-

le impact player Sunny Singh,

jinhone koi impact nai paaya

16 notes

·

View notes

Text

MY LITTLE HARA BHARA KEBABS MIGHT WIN TODAYYY?!?!?!

15 notes

·

View notes

Text

this is hands down THE worst match EVER

#lekin mujhe kya kkr is gonna win its 3rd title !!#so letsgo#but still shitty match#kkr vs srh#kkrvssrh#ipl final#ipl2024

15 notes

·

View notes

Text

The long, bloody lineage of private equity's looting

Tomorrow (June 3) at 1:30PM, I’m in Edinburgh for the Cymera Festival on a panel with Nina Allen and Ian McDonald.

Monday (June 5) at 7:15PM, I’m in London at the British Library with my novel Red Team Blues, hosted by Baroness Martha Lane Fox.

Fans of the Sopranos will remember the “bust out” as a mob tactic in which a business is taken over, loaded up with debt, and driven into the ground, wrecking the lives of the business’s workers, customers and suppliers. When the mafia does this, we call it a bust out; when Wall Street does it, we call it “private equity.”

It used to be that we rarely heard about private equity, but then, as national chains and iconic companies started to vanish, this mysterious financial arrangement popped up with increasing frequency. When a finance bro’s presentation on why Olive Garden needed to be re-orged when viral, there was a lot off snickering about the decline of a tacky business whose value prop was unlimited carbs. But the bro was working for Starboard Value, a hedge fund that specialized in buhying out and killing off companies, pocketing billions while destroying profitable businesses.

https://www.salon.com/2014/09/17/the_real_olive_garden_scandal_why_greedy_hedge_funders_suddenly_care_so_much_about_breadsticks/

Starboard Value’s game was straightforward: buy a business, load it with debt, sell off its physical plant — the buildings it did business out of — pay itself, and then have the business lease back the buildings, bleeding out money until it collapsed. They pulled it with Red Lobster,and the point of the viral Olive Garden dis track was to soften up the company for its own bust out.

The bust out tactic wasn’t limited to mocking middlebrow family restaurants. For years, the crooks who ran these ops did a brisk trade in blaming the internet. Why did Sears tank? Everyone knows that the 19th century business was an antique, incapable of mounting a challenge in the age of e-commerce. That was a great smokescreen for an old-fashioned bust out that saw corporate looters make off with hundreds of millions, leaving behind empty storefronts and emptier pension accounts for the workers who built the wealth the looters stole:

https://prospect.org/economy/vulture-capitalism-killed-sears/

Same goes for Toys R Us: it wasn’t Amazon that killed the iconic toy retailer — it was the PE bosses who extracted $200m from the chain, then walked away, hands in pockets and whistling, while the businesses collapsed and the workers got zero severance:

https://www.washingtonpost.com/news/business/wp/2018/06/01/how-can-they-walk-away-with-millions-and-leave-workers-with-zero-toys-r-us-workers-say-they-deserve-severance/

It’s a good racket — for the racketeers. Private equity has grown from a finance sideshow to Wall Street’s apex predator, and it’s devouring the real economy through a string of audactious bust outs, each more consequential and depraved than the last.

As PE shows that it can turn profitable businesses gigantic windfalls, sticking the rest of us with the job of sorting out the smoking craters they leave behind, more and more investors are piling in. Today, the PE sector loves a rollup, which is when they buy several related businesses and merge them into one firm. The nominal business-case for a rollup is that the new, bigger firm is more “efficient.” In reality, a rollup’s strength is in eliminating competition. When all the pet groomers, or funeral homes, or urgent care clinics for ten miles share the same owner, they can raise prices, lower wages, and fuck over suppliers.

They can also borrow. A quirk of the credit markets is that a standalone small business is valued at about 3–5x its annual revenues. But if that business is part of a large firm, it is valued at 10–20x annual turnover. That means that when a private equity company rolls up a comedy club, ad agency or water bottler (all businesses presently experiencing PE rollup), with $1m in annual revenues, it shows up on the PE company’s balance sheet as an asset worth $10–20m. That’s $10–20m worth of collateral the PE fund can stake for loans that let it buy and roll up more small businesses.

2.9 million Boomer-owned businesses, employing 32m people, are expected to sell in the next couple years as their owners retire. Most of these businesses will sell to PE firms, who can afford to pay more for them as a prelude to a bust out than anyone intending to operate them as a productive business could ever pay:

https://pluralistic.net/2022/12/16/schumpeterian-terrorism/#deliberately-broken

PE’s most ghastly impact is felt in the health care sector. Whole towns’ worth of emergency rooms, family practices, labs and other health firms have been scooped up by PE, which has spent more than $1t since 2012 on health acquisitions:

https://pluralistic.net/2022/11/17/the-doctor-will-fleece-you-now/#pe-in-full-effect

Once a health care company is owned by PE, it is significantly more likely to commit medicare fraud. It also cuts wages and staffing for doctors and nurses. PE-owned facilities do more unnecessary and often dangerous procedures. Appointments get shorter. The companies get embroiled in kickback scandals. PE-backed dentists hack away at children’s mouths, filling them full of root-canals.

https://pluralistic.net/2022/11/17/the-doctor-will-fleece-you-now/#pe-in-full-effect

The Healthcare Private Equity Association boasts that its members are poised to spend more than $3t to create “the future of healthcare.”

https://hcpea.org/#!event-list

As bad as PE is for healthcare, it’s worse for long-term care. PE-owned nursing homes are charnel houses, and there’s a particularly nasty PE scam where elderly patients are tricked into signing up for palliative care, which is never delivered (and isn’t needed, because the patients aren’t dying!). These fake “hospices” get huge payouts from medicare — and the patient is made permanently ineligible for future medicare, because they are recorded being in their final decline:

https://pluralistic.net/2023/04/26/death-panels/#what-the-heck-is-going-on-with-CMS

Every part of the health care sector is being busted out by PE. Another ugly PE trick, the “club deal,” is devouring the medical supply business. Club deals were huge in the 2000s, destroying rent-controlled housing, energy companies, Mervyn’s department stores, Harrah’s, and Old Country Joe. Now it’s doing the same to medical supplies:

https://pluralistic.net/2021/05/14/billionaire-class-solidarity/#club-deals

Private equity is behind the mass rollup of single-family homes across America. Wall Street landlords are the worst landlords in America, who load up your rent with junk fees, leave your home in a state of dangerous disrepair, and evict you at the drop of a hat:

https://pluralistic.net/2021/08/16/die-miete-ist-zu-hoch/#assets-v-human-rights

As these houses decay through neglect, private equity makes a bundle from tenants and even more borrowing against the houses. In a few short years, much of America’s desperately undersupplied housing stock will be beyond repair. It’s a bust out.

You know all those exploding trains filled with dangerous chemicals that poison entire towns? Private equity bust outs:

https://pluralistic.net/2022/02/04/up-your-nose/#rail-barons

Where did PE come from? How can these people look themselves in the mirror? Why do we let them get away with it? How do we stop them?

Today in The American Prospect, Maureen Tkacik reviews two new books that try to answer all four of these questions, but really only manage to answer the first three:

https://prospect.org/culture/books/2023-06-02-days-of-plunder-morgenson-rosner-ballou-review/

The first of these books is These Are the Plunderers: How Private Equity Runs — and Wrecks — America by Gretchen Morgenson and Joshua Rosner:

https://www.simonandschuster.com/books/These-Are-the-Plunderers/Gretchen-Morgenson/9781982191283

The second is Plunder: Private Equity’s Plan to Pillage America, by Brendan Ballou:

https://www.hachettebookgroup.com/titles/brendan-ballou/plunder/9781541702103/

Both books describe the bust out from the inside. For example, PetSmart — looted for $30 billion by RaymondSvider and his PE fund BC Partners — is a slaughterhouse for animals. The company systematically neglects animals — failing to pay workers to come in and feed them, say, or refusing to provide backup power to run during power outages, letting animals freeze or roast to death. Though PetSmart has its own vet clinics, the company doesn’t want to pay its vets to nurse the animals it damages, so it denies them care. But the company is also too cheap to euthanize those animals, so it lets them starve to death. PetSmart is also too cheap to cremate the animals, so its traumatized staff are ordered to smuggle the dead, rotting animals into random dumpsters.

All this happened while PetSmart’s sales increased by 60%, matched by growth in the company’s gross margins. All that money went to the bust out.

https://www.forbes.com/sites/antoinegara/2021/09/27/the-30-billion-kitty-meet-the-investor-who-made-a-fortune-on-pet-food/

Tkacik says these books show that we’re finally getting wise to PE. Back in the Clinton years, the PE critique painted the perps as sharp operators who reduced quality and jacked up prices. Today, books like these paint these “investors” as the monsters they are — crooks whose bust ups are crimes, not clever finance hacks.

Take the Carlyle Group, which pioneered nursing home rollups. As Carlyle slashed wages, its workers suffered — but its elderly patients suffered more. Thousands of Carlyle “customers” died of “dehydration, gangrenous bedsores, and preventable falls” in the pre-covid years.

https://www.washingtonpost.com/business/economy/opioid-overdoses-bedsores-and-broken-bones-what-happened-when-a-private-equity-firm-sought-profits-in-caring-for-societys-most-vulnerable/2018/11/25/09089a4a-ed14-11e8-baac-2a674e91502b_story.html

KKR, another PE monster, bought a second-hand chain of homes for mentally disabled adults from another PE company, then squeezed it for the last drops of blood left in the corpse. KKR cut wages to $8/hour and increased shifts to 36 hours, then threatened to have workers who went home early arrested and charged with “patient abandonment.” Many of these homes were often left with no staff at all, with patients left to starve and stew in their own waste.

PE loves to pick on people who can’t fight back: kids, sick people, disabled people, old people. No surprise, then, that PE loves prisons — the ultimate captive audience. HIG Capital is a $55b fund that owns TKC Holdings, who got the contract to feed the prisoners at 400 institutions. They got the contract after the prisons fired Aramark, owned by PE giant Warburg Pincus, whose food was so inedible that it provoked riots. TKC got a million bucks extra to take over the food at Michigan’s Kinross Correctional Facility, then, incredibly, made the food worse. A chef who refused to serve 100 bags of rotten potatoes (“the most disgusting thing I’ve seen in my life”) was fired:

https://www.wzzm13.com/article/news/local/michigan/prison-food-worker-i-was-fired-for-refusing-to-serve-rotten-potatoes/69-467297770

TKC doesn’t just operate prison kitchens — it operates prison commissaries, where it gouges prisoners on junk food to replace the inedible slop it serves in the cafeteria. The prisoners buy this food with money they make working in the prison workshops, for $0.10–0.25/hour. Those workshops are also run by TKC.

Tkacic traces private equity back to the “corporate raiders” of the 1950s and 1960s, who “stealthily borrowed money to buy up enough shares in a small or midsized company to control its biggest bloc of votes, then force a stock swap and install himself as CEO.”

The most famous of these raiders was Eli Black, who took over United Fruit with this gambit — a company that had a long association with the CIA, who had obligingly toppled democratically elected governments and installed dictators friendly to United’s interests (this is where the term “banana republic” comes from).

Eli Black’s son is Leon Black, a notorious PE predator. Leon Black got his start working for the junk-bonds kingpin Michael Milken, optimizing Milken’s operation, which was the most terrifying bust out machine of its day, buying, debt-loading and wrecking a string of beloved American businesses. Milken bought 2,000 companies and put 200 of them through bankruptcy, leaving the survivors in a brittle, weakened state.

It got so bad that the Business Roundtable complained about the practice to Congress, calling Milken, Black, et al, “a small group is systematically extracting the equity from corporations and replacing it with debt, and incidentally accumulating major wealth.”

Black stabbed Milken in the back and tanked his business, then set out on his own. Among the businesses he destroyed was Samsonite, “a bankrupt-but-healthy company he subjected to 12 humiliating years of repeated fee extractions, debt-funded dividend payments, brutal plant closings, and hideous schemes to induce employees to buy its worthless stock.”

The money to buy Samsonite — and many other businesses — came through a shadowy deal between Black and John Garamendi, then a California insurance commissioner, now a California congressman. Garamendi helped Black buy a $6b portfolio of junk bonds from an insurance company in a wildly shady deal. Garamendi wrote down the bonds by $3.9b, stealing money “from innocent people who needed the money to pay for loved ones’ funerals, irreparable injuries, etc.”

Black ended up getting all kinds of favors from powerful politicians — including former Connecticut governor John Rowland and Donald Trump. He also wired $188m to Jeffrey Epstein for reasons that remain opaque.

Black’s shady deals are a marked contrast with the exalted political circles he travels in. Despite private equity’s obviously shady conduct, it is the preferred partner for cities and states, who buy everything from ambulance services to infrastructure from PE-owned companies, with disastrous results. Federal agencies turn a blind eye to their ripoffs, or even abet them. 38 state houses passed legislation immunizing nursing homes from liability during the start of the covid crisis.

PE barons are shameless about presenting themselves as upstanding cits, unfairly maligned. When Obama made an empty promise to tax billionaires in 2010, Blackstone founder SteveS chwarzman declared, “It’s a war. It’s like when Hitler invaded Poland in 1939.”

Since we’re on the subject of Hitler, this is a good spot to bring up Monowitz, a private-sector satellite of Auschwitz operated by IG Farben as a slave labor camp to make rubber and other materiel it supplied at a substantial markup to the wermacht. I’d never heard of Monowitz, but Tkacik’s description of the camp is chilling, even in comparison to Auschwitz itself.

Farben used slave laborers from Auschwitz to work at its rubber plant, but was frustrated by the logistics of moving those slaves down the 4.5m stretch of road to the facility. So the company bought 25,000 slaves — preferring children, who were cheaper — and installed them in a co-located death-camp called Monowitz:

https://www.commentary.org/articles/r-tannenbaum/the-devils-chemists-by-josiah-e-dubois-jr/

Monowitz was — incredibly — worse than Auschwitz. It was so bad, the SS guards who worked at it complained to Berlin about the conditions. The SS demanded more hospitals for the workers who dropped from beatings and overwork — Farben refused, citing the cost. The factory never produced a steady supply of rubber, but thanks to its gouging and the brutal treatment of its slaves, the camp was still profitable and returned large dividends to Farben’s investors.

Apologists for slavery sometimes claim that slavers are at least incentivized to maintain the health of their captive workforce. This was definitely not true of Farben. Monowitz slaves died on average after three months in the camp. And Farben’s subsidiary, Degesch, made the special Zyklon B formulation used in Auschwitz’s gas chambers.

Tkacik’s point is that the Nazis killed for ideology and were unimaginably cruel. Farben killed for money — and they were even worse. The banality of evil gets even more banal when it’s done in service to maximizing shareholder value.

As Farben historian Joseph Borkin wrote, the company “reduced slave labor to a consumable raw material, a human ore from which the mineral of life was systematically extracted”:

https://www.scribd.com/document/517797736/The-Crime-and-Punishment-of-I-G-Farben

Farben’s connection to the Nazis was a the subject of Germany’s Master Plan: The Story of Industrial Offensive, a 1943 bestseller by Borkin, who was also an antitrust lawyer. It described how Farben had manipulated global commodities markets in order to create shortages that “guaranteed Hitler’s early victories.”

Master Plan became a rallying point in the movement to shatter corporate power. But large US firms like Dow Chemical and Standard Oil waged war on the book, demanding that it be retracted. Borkin was forced into resignation and obscurity in 1945.

Meanwhile, in Nuremberg, 24 Farben executives were tried for their war crimes, and they cited their obligations to their shareholders in their defense. All but five were acquitted on this basis.

Seen in that light, the plunderers of today’s PE firms are part of a long and dishonorable tradition, one that puts profit ahead of every other priority or consideration. It’s a defense that wowed the judges at Nuremberg, so should we be surprised that it still plays in 2023?

Tkacik is frustrated that neither of these books have much to offer by way of solutions, but she understands why that would be. After all, if we can’t even close the carried interest tax loophole, how can we hope to do anything meaningful?

“Carried interest” comes up in every election cycle. Most of us assume it has something to do with “interest payments,” but that’s not true. The carried interest loophole relates to the “interest” that 16th-century sea captains had in their cargo. It’s a 600-year-old tax loophole that private equity bosses use to pay little or no tax on their billions. The fact that it’s still on the books tells you everything you need to know about whether our political class wants to do anything about PE’s plundering.

Notwithstanding Tkacik’s (entirely justified) skepticism of the weaksauce remedies proposed in these books, there is some hope of meaningful action. Private equity’s rollups are only possible because they skate under the $101m threshold for merger scrutiny. However, there is good — but unenforced — law that allows antitrust enforcers to block these mergers. This is the “incipiency standard” — Sec 7 of the Clayton Act — the idea that a relatively small merger might not be big enough to trigger enforcement action on its own, but regulators can still act to block it if it creates an incipient monopoly.

https://pluralistic.net/2022/12/16/schumpeterian-terrorism/#deliberately-broken

The US has a new crop of aggressive — fearless — top antitrust enforcers and they’ve been systematically reviving these old laws to go after monopolies.

That’s long overdue. Markets are machines for eroding our moral values: “In comparison to non-market decisions, moral standards are significantly lower if people participate in markets.”

https://web.archive.org/web/20130607154129/https://www.uni-bonn.de/Press-releases/markets-erode-moral-values

The crimes that monsters commit in the name of ideology pale in comparison to the crimes the wealthy commit for money.

Catch me on tour with Red Team Blues in Edinburgh, London, and Berlin!

If you’d like an essay-formatted version of this post to read or share, here’s a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2023/06/02/plunderers/#farbenizers

[Image ID: An overgrown graveyard, rendered in silver nitrate monochrome. A green-tinted businessman with a moneybag in place of a head looms up from behind a gravestone. The right side of the image is spattered in blood.]

#pluralistic#kkr#lootersprivate equity#plunderers#books#reviews#monsters#nazis#godwin's law#godwins law#auschwitz#ig farben#pe#business#barbarians#united fruit#carried interest#corporate raiders#junk bonds#michael milliken#ensemble cast#carlyle group#monowitz#leon black

1K notes

·

View notes

Text

Happy King

17 notes

·

View notes

Text

His arms don't stop Srkingggg❤️

10 notes

·

View notes

Text

My thoughts on the current ipl points table that absolutely no one asked for :

(part-1)

1. They're the og champions...very chill, very fun vibes.

soo happy to see them on top. They really be feeling like royalty rn lol.

Also in the end, I'm just a girl 🎀💖 some I absolutely adore their jersey.

2. Yaar.... I know Hyderabad is a great team and everything but.... Do you guys have to go this hard?

Other teams come to play a match, this team comes to crack open your morale and bring you to your knees.

Baki teams khel rahi hai, Yeh log toh seedha gunda gardi kar rahe hai Yaar.

Watching Abhishek, our Indian player, a youngster, bat like that feels amazing tho.

3. Kolkata.... Man.

Gautam bhai aaye, and suddenly Sabka Chris Gayle bahar aagya.

I feel like sunil will take both purple and orange caps this year and gambhir bhai has already planned on picking the trophy this year so... Yea.

PS : once gautam bhai is done someone pls convince him to come as ICT's coach.

4. Chennai = 7 letters = thala for a reason.

They're doing great, but their recent performances makes me worried about what will happen to this team when Mahi Bhai retires.

If they don't start taking more responsibility now there's a good chance csk will crash land in the bottom next year. Hope thT doesn't happen tho.

5. LSG, you beauty....

They look like they are a weak team but they've defeated rcb, gt, pbks and...sabse importantly.... CSK.

But their next matches are quite tough too... So we'll see where they end up after 2 - 3 more matches.

The way kl Rahul hits sixes is just beautiful.

6. Mumbai.

I...... Have no idea what mysterious substance this management was on tbh.

If you want to remove someone from the captaincy, there's gotta be a better way to do that so the fans aren't offended and the player also isn't disrespected. Look how kohli left rcb's captaincy for example.

Then, if you wanted to look towards the future, Bumrah and Surya, both who have captained team India and have stayed with the franchise despite having so many opportunities to earn more if they leave should have been considered.

Or they could have just choosen Ishan. Just like csk and gt choose youngsters, Ishan could have been a good option too. Plus He's captained his team during u-19 in 2016.

But no. They choose Hardik.

Tbh, I feel so sorry for him cause in his mind, when MI offered him captaincy and called him back, he would have been happy to go back to his old team...like going back home.

But the sad truth is, MI management saw how successful he was in gt, winning in the first year and then reaching the finals in 2nd year....and it pissed them off that their player is doing well in some other team. So they brought him back.

Despite so much backlash from fans, so much hatred and trolling against Hardik, this shitty management never held one press conference to clear up misunderstandings and give answers to their fans honestly. Because they knew, if the truth comes out, they'll be on the receiving end of this hate.

Fuck them.

The only mistake Hardik did was leaving gt. But... Oh well.

(I ended up ranting lol.)

#desiblr#indian cricket team#ict#cricket#ipl2024#ishan kishan#ishman#shubhman gill#hardikpandya#kl rahul#rohitsharma#csk#kkr#rr#mi#ms dhoni#gautamgambhir#srh#pat cummins#lsg

18 notes

·

View notes

Last Seen Blogs

eulamerrittbeechisland-blog

EulaMerr

gogthings

제목 없음

helixandchicken

Helix and Chicken

xmomokosx

🌸🌻🌼🌸

27kash

GodFirst